Embed Size (px)

Citation preview

The Better-for-you Business Case:

How Is the Supermarket Sector

Shaping Up?

www.obesity-solutions.org

Hank Cardello

Senior Fellow & Director

Obesity Solutions Initiative

June 9, 2015

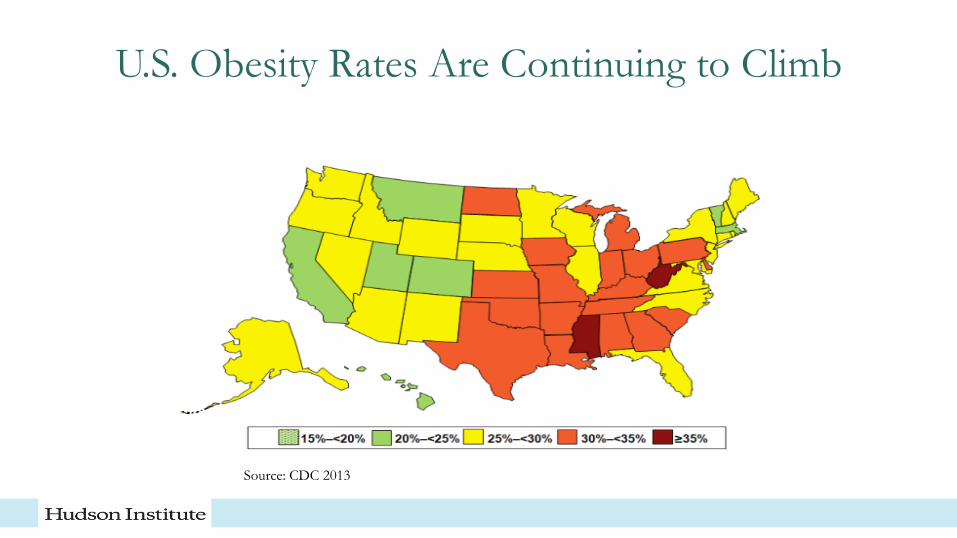

U.S. Obesity Rates Are Continuing to Climb

Source: CDC 2013

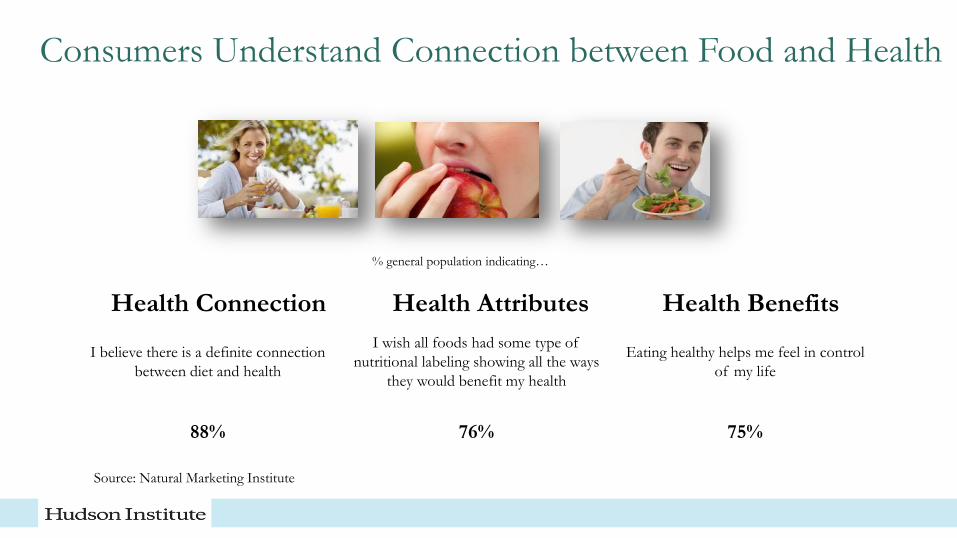

Consumers Understand Connection between Food and Health

I believe there is a definite connection

between diet and health

I wish all foods had some type of

nutritional labeling showing all the ways

they would benefit my health

Eating healthy helps me feel in control

of my life

88% 76% 75%

% general population indicating…

Health Connection Health Attributes Health Benefits

Source: Natural Marketing Institute

Our Approach:

Is There a Business Case for Selling More

Better-for-you/Lower-Calorie Products?

4

Studies Show That Better-for-you/Lower-Calorie

Foods Are Key Growth Drivers

5

Supermarket study funded by

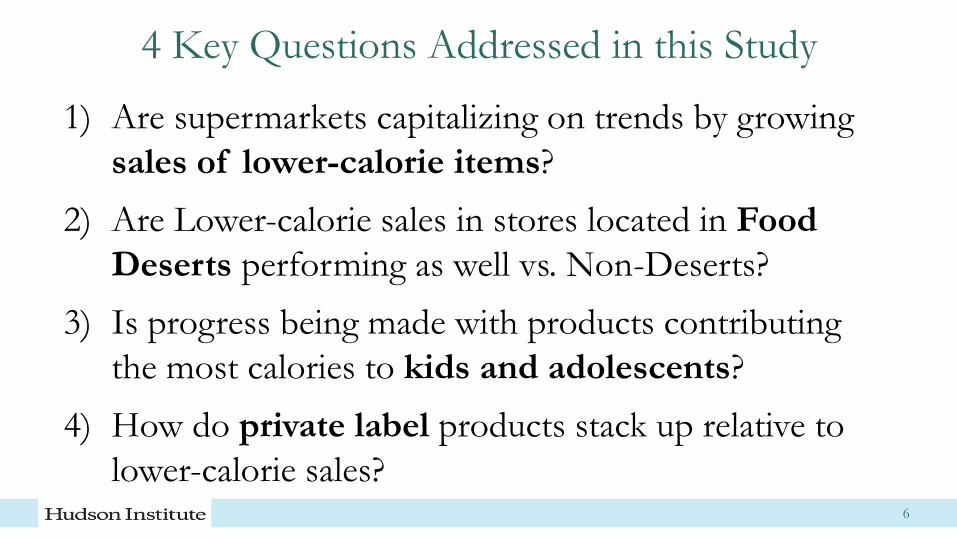

4 Key Questions Addressed in this Study

1) Are supermarkets capitalizing on trends by growing

sales of lower-calorie items?

2) Are Lower-calorie sales in stores located in Food

Deserts performing as well vs. Non-Deserts?

3) Is progress being made with products contributing

the most calories to kids and adolescents?

4) How do private label products stack up relative to

lower-calorie sales? 6

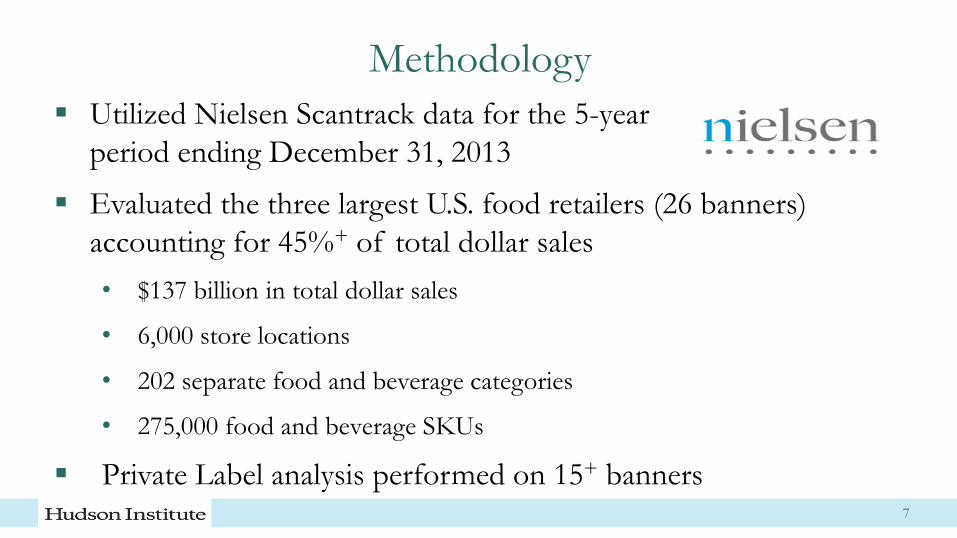

Methodology

Utilized Nielsen Scantrack data for the 5-year

period ending December 31, 2013

Evaluated the three largest U.S. food retailers (26 banners)

accounting for 45%+ of total dollar sales

• $137 billion in total dollar sales

• 6,000 store locations

• 202 separate food and beverage categories

• 275,000 food and beverage SKUs

Private Label analysis performed on 15+ banners 7

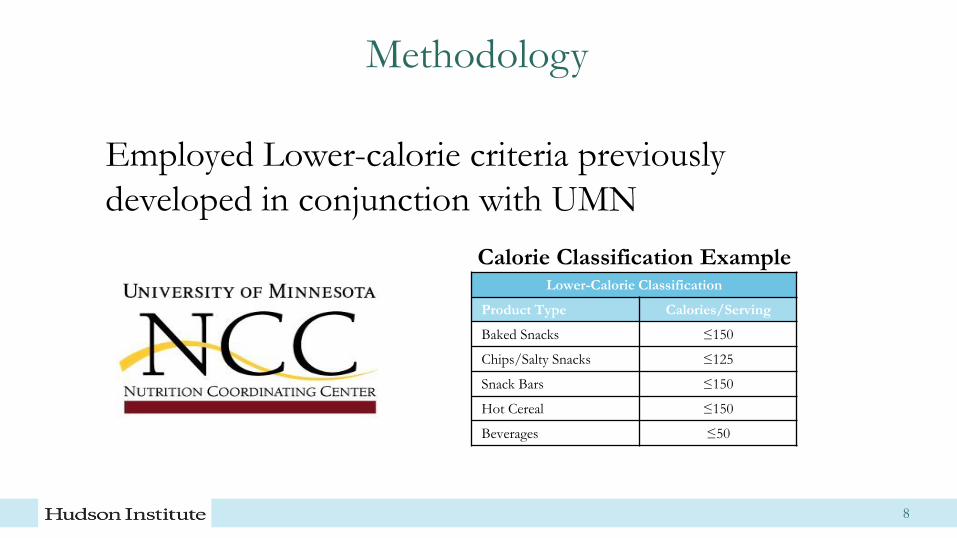

Methodology

Lower-Calorie Classification

Product Type Calories/Serving

Baked Snacks ≤150

Chips/Salty Snacks ≤125

Snack Bars ≤150

Hot Cereal ≤150

Beverages ≤50

Calorie Classification Example

8

Employed Lower-calorie criteria previously

developed in conjunction with UMN

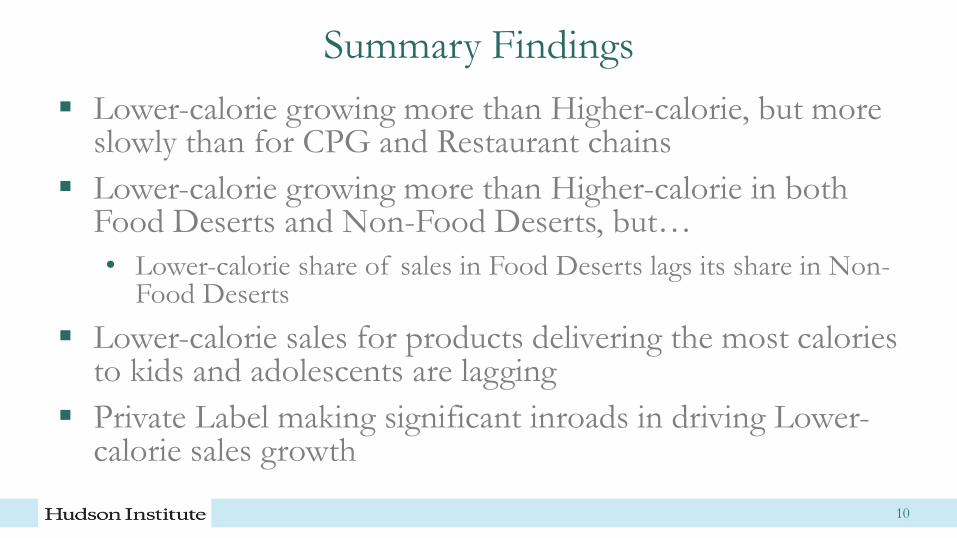

Summary Findings

Summary Findings

Lower-calorie growing more than Higher-calorie, but more slowly than for CPG and Restaurant chains

Lower-calorie growing more than Higher-calorie in both Food Deserts and Non-Food Deserts, but…

• Lower-calorie share of sales in Food Deserts lags its share in Non-Food Deserts

Lower-calorie sales for products delivering the most calories to kids and adolescents are lagging

Private Label making significant inroads in driving Lower-calorie sales growth

10

Key Findings

Overall Store & Dollar Sales Findings

12

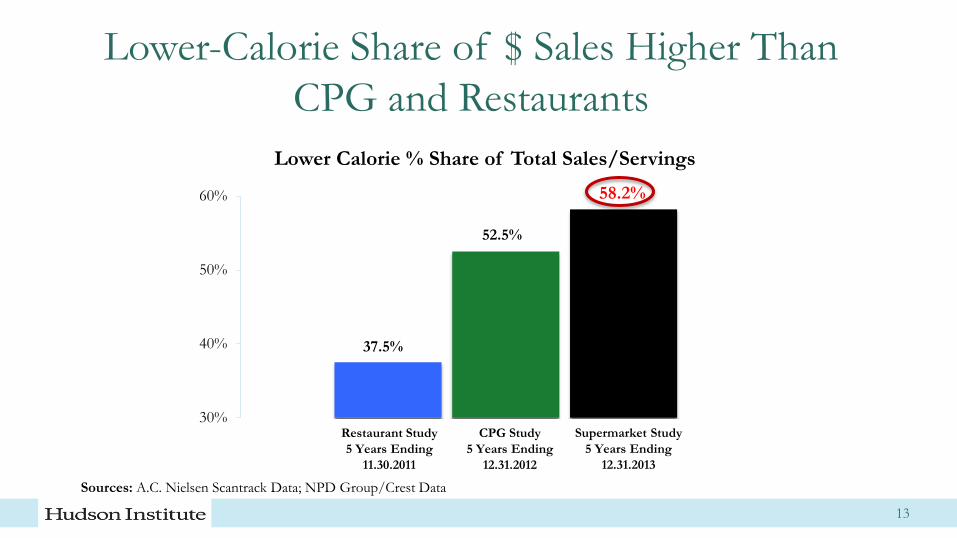

Lower-Calorie Share of $ Sales Higher Than

CPG and Restaurants

100%

13

58.2%

58.2%

37.5%

52.5%

58.2%

30%

40%

50%

60%

Lower Calorie % Share of Total Sales/Servings

Restaurant Study

5 Years Ending

11.30.2011

CPG Study

5 Years Ending

12.31.2012

Supermarket Study

5 Years Ending

12.31.2013

Sources: A.C. Nielsen Scantrack Data; NPD Group/Crest Data

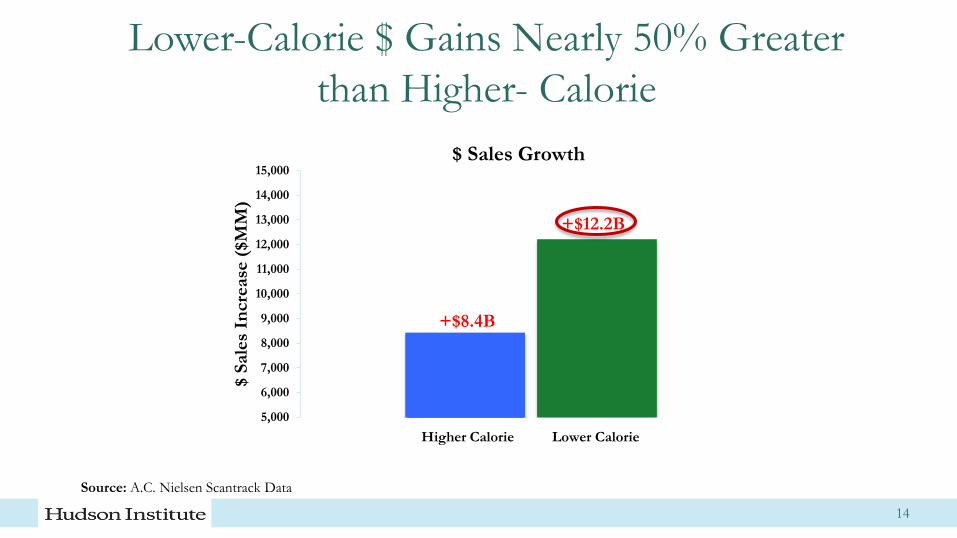

Lower-Calorie $ Gains Nearly 50% Greater

than Higher- Calorie

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

$ S

ale

s In

cre

ase

($M

M)

Higher Calorie

14

$ Sales Growth

Lower Calorie

+$8.4B

+$12.2B

Source: A.C. Nielsen Scantrack Data

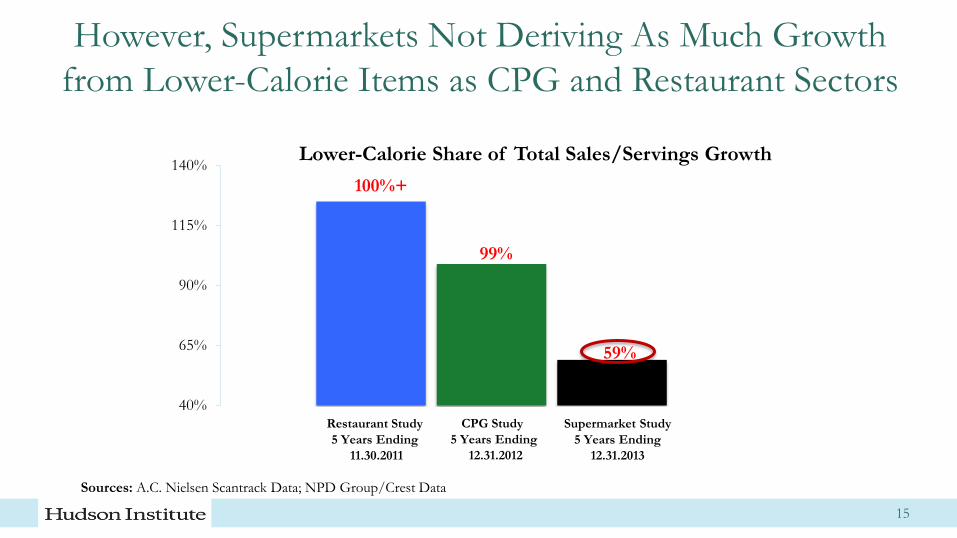

However, Supermarkets Not Deriving As Much Growth

from Lower-Calorie Items as CPG and Restaurant Sectors

100%

15

58.2%

58.2% 40%

65%

90%

115%

140%Lower-Calorie Share of Total Sales/Servings Growth

Restaurant Study

5 Years Ending

11.30.2011

CPG Study

5 Years Ending

12.31.2012

Supermarket Study

5 Years Ending

12.31.2013

Sources: A.C. Nielsen Scantrack Data; NPD Group/Crest Data

100%+

99%

59%

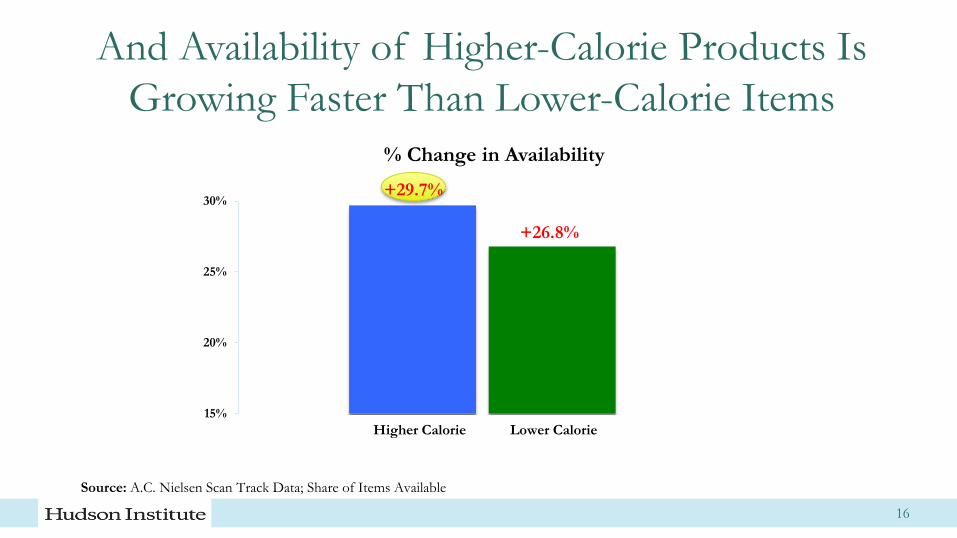

And Availability of Higher-Calorie Products Is

Growing Faster Than Lower-Calorie Items

100%

16

58.2%

58.2% 15%

20%

25%

30%

Higher Calorie Lower Calorie

+29.7%

+26.8%

% Change in Availability

Source: A.C. Nielsen Scan Track Data; Share of Items Available

Food Desert Assessment

17

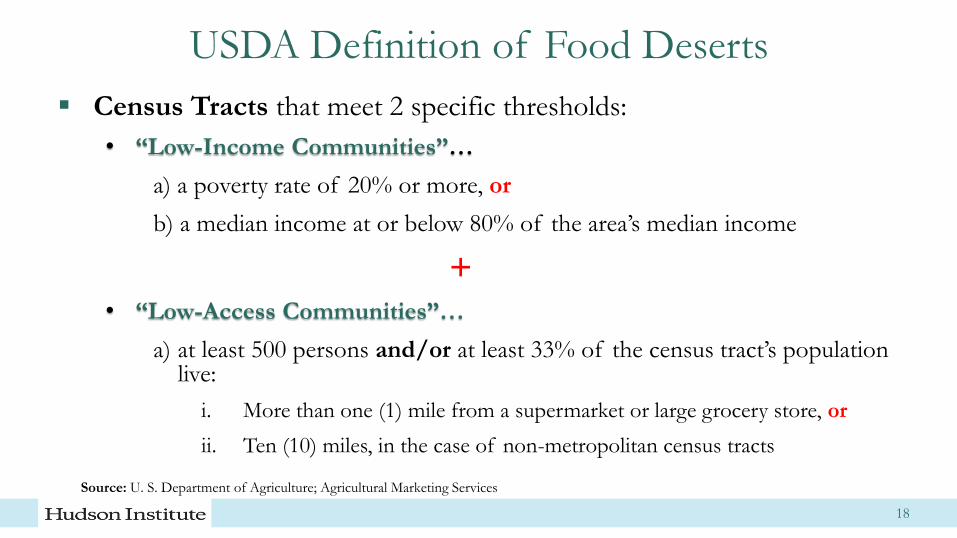

USDA Definition of Food Deserts

Census Tracts that meet 2 specific thresholds:

• “Low-Income Communities”…

a) a poverty rate of 20% or more, or

b) a median income at or below 80% of the area’s median income

+

• “Low-Access Communities”…

a) at least 500 persons and/or at least 33% of the census tract’s population live:

i. More than one (1) mile from a supermarket or large grocery store, or

ii. Ten (10) miles, in the case of non-metropolitan census tracts

18

Source: U. S. Department of Agriculture; Agricultural Marketing Services

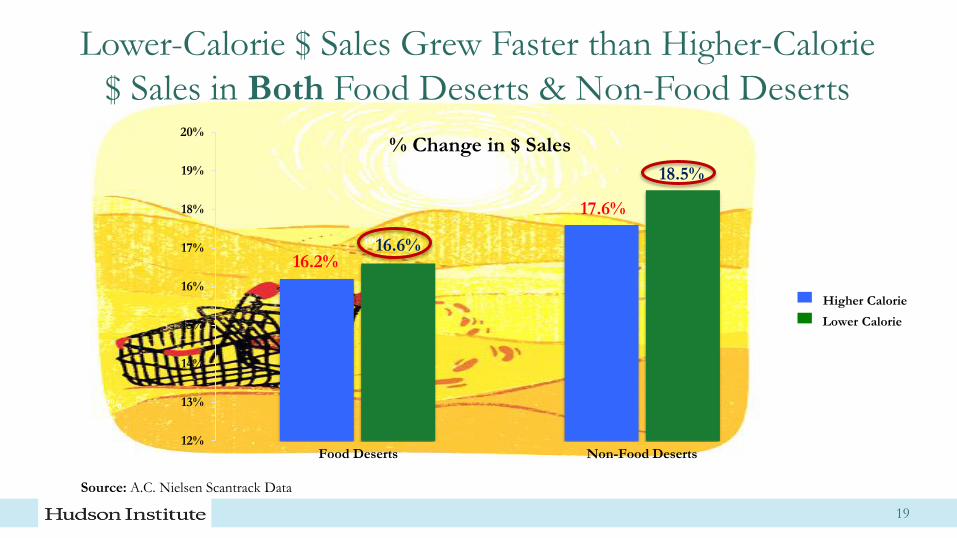

Lower-Calorie $ Sales Grew Faster than Higher-Calorie

$ Sales in Both Food Deserts & Non-Food Deserts

100%

19

58.2%

58.2%

16.2%

17.6%

16.6%

18.5%

12%

13%

14%

15%

16%

17%

18%

19%

20%

Food Deserts Non-Food Deserts

Source: A.C. Nielsen Scantrack Data

% Change in $ Sales

Higher Calorie

Lower Calorie

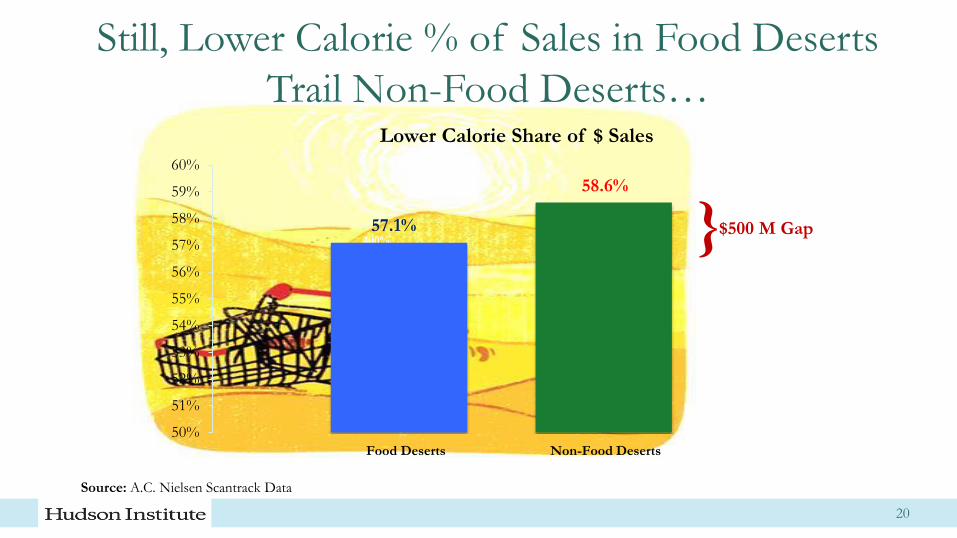

Still, Lower Calorie % of Sales in Food Deserts

Trail Non-Food Deserts…

100%

20

58.2%

58.2%

57.1%

58.6%

50%

51%

52%

53%

54%

55%

56%

57%

58%

59%

60%

Lower Calorie Share of $ Sales

}

Food Deserts Non-Food Deserts

Source: A.C. Nielsen Scantrack Data

$500 M Gap

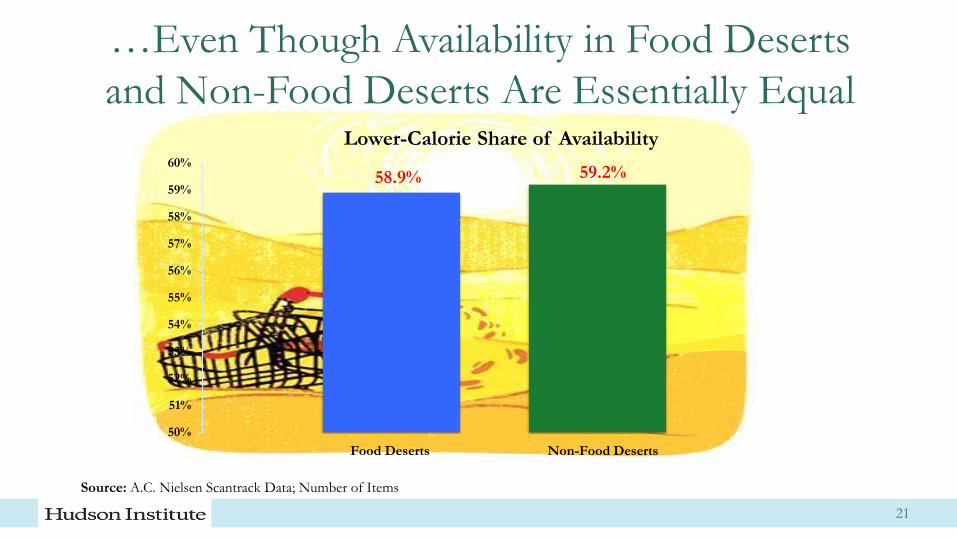

…Even Though Availability in Food Deserts

and Non-Food Deserts Are Essentially Equal

100%

21

58.2%

58.2%

58.9% 59.2%

50%

51%

52%

53%

54%

55%

56%

57%

58%

59%

60%

Lower-Calorie Share of Availability

Food Deserts Non-Food Deserts

Source: A.C. Nielsen Scantrack Data; Number of Items

Foods Contributing The Most Calories to Children

22

Foods That Are Top Calorie Contributors to Children Grain desserts: cookies, donuts, pies, muffins, cake, cobblers, toaster pastries, frosting and

granola bars

Beverages: juices (except adult varieties), carbonated soft drinks (CSDs), powdered soft drinks

(PSDs), sports drinks and sweetened/vitamin waters

Pasta: macaroni & cheese

Pizza (excludes French Bread, premium/super premium and reduced calorie)

Milk (excludes buttermilk)

White Bread

23

Sources: Reedy, J. et al, “Dietary Sources of Energy, Solid Fats, and Added Sugars Among Children and Adolescents in the United

States,” Journal of the American Dietetic Association, 2010;110:1477-1484; Popkin, B. analysis, University of North Carolina at Chapel Hill.

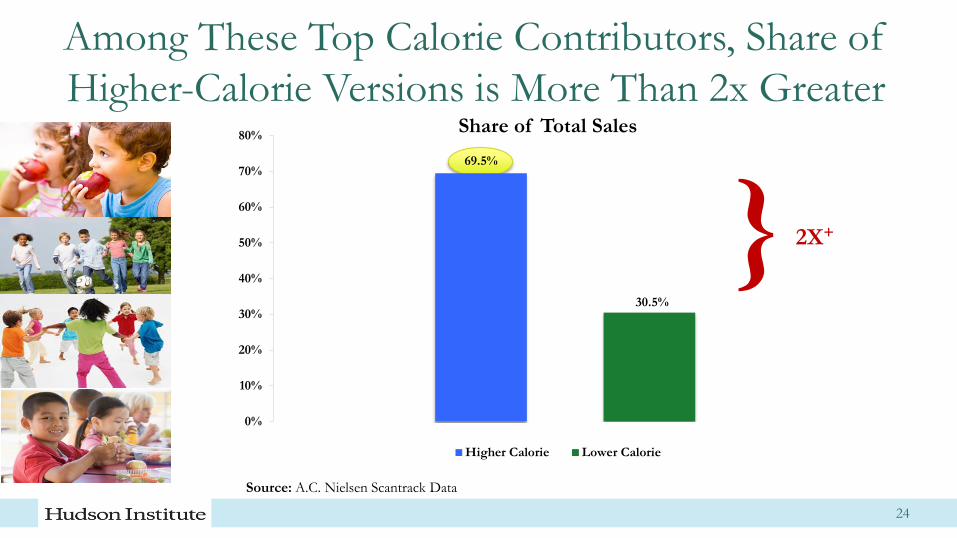

Among These Top Calorie Contributors, Share of

Higher-Calorie Versions is More Than 2x Greater

69.5%

30.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Higher Calorie Lower Calorie

Share of Total Sales

Source: A.C. Nielsen Scantrack Data

} 2X+

24

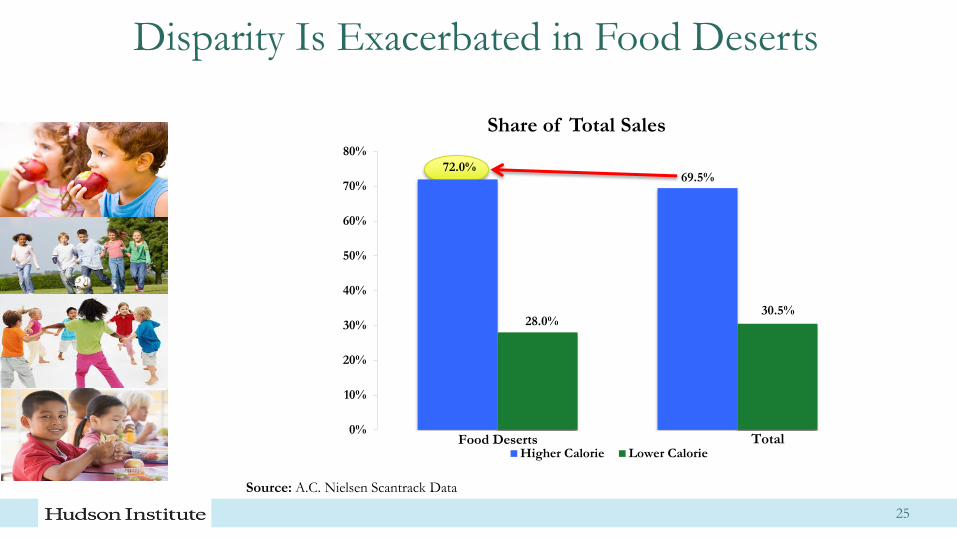

Disparity Is Exacerbated in Food Deserts

72.0% 69.5%

28.0% 30.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Higher Calorie Lower CalorieFood Deserts Total

25

Share of Total Sales

Source: A.C. Nielsen Scantrack Data

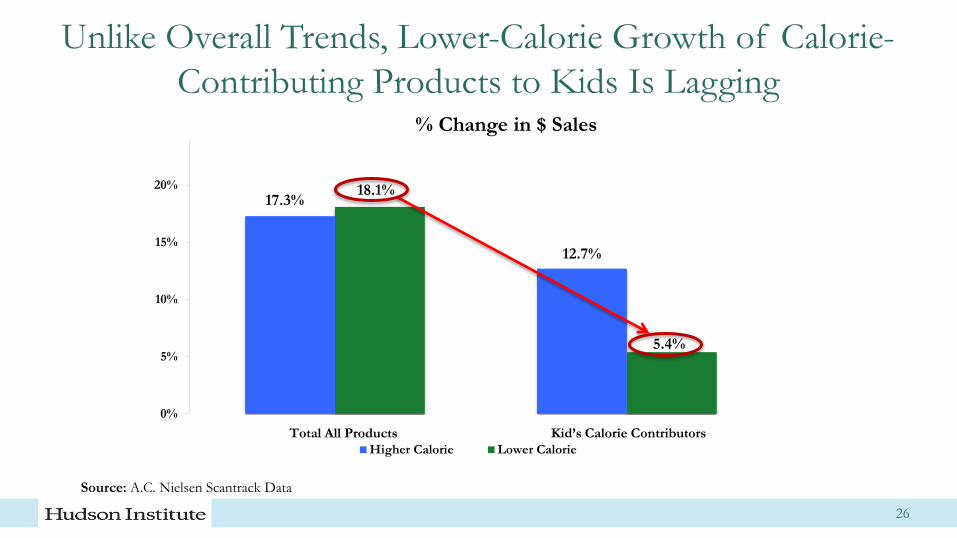

Unlike Overall Trends, Lower-Calorie Growth of Calorie-

Contributing Products to Kids Is Lagging

17.3%

12.7%

18.1%

5.4%

0%

5%

10%

15%

20%

Higher Calorie Lower Calorie

Kid’s Calorie Contributors Total All Products

26

% Change in $ Sales

Source: A.C. Nielsen Scantrack Data

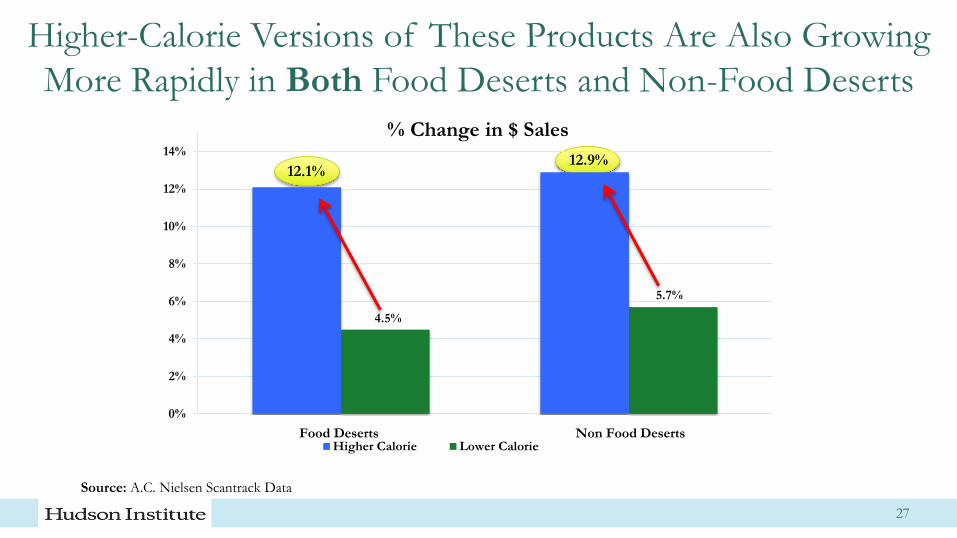

Higher-Calorie Versions of These Products Are Also Growing

More Rapidly in Both Food Deserts and Non-Food Deserts

12.1% 12.9%

4.5%

5.7%

0%

2%

4%

6%

8%

10%

12%

14%

Higher Calorie Lower CalorieNon Food Deserts Food Deserts

27

% Change in $ Sales

Source: A.C. Nielsen Scantrack Data

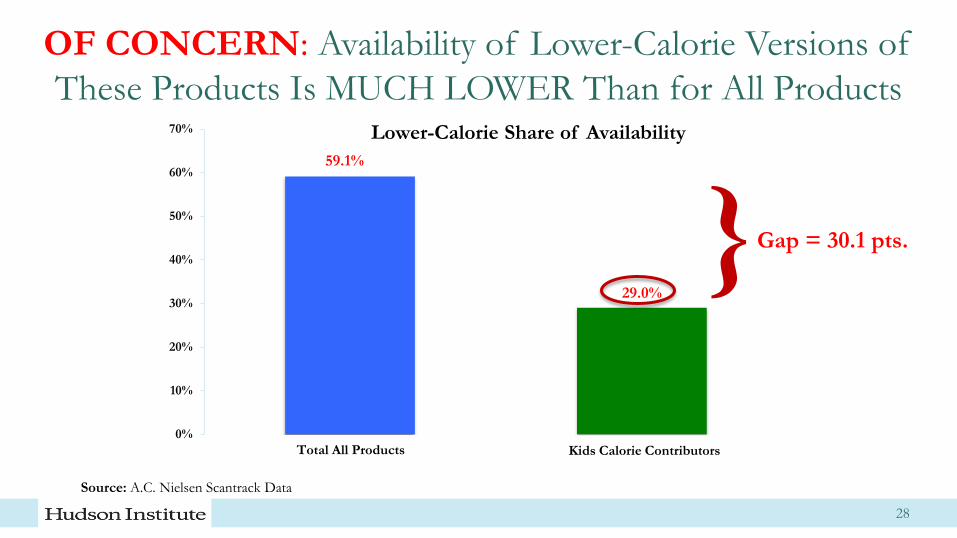

OF CONCERN: Availability of Lower-Calorie Versions of

These Products Is MUCH LOWER Than for All Products

59.1%

29.0%

0%

10%

20%

30%

40%

50%

60%

70%

Total All Products Kids Calorie Contributors

100%

28

Lower-Calorie Share of Availability

Source: A.C. Nielsen Scantrack Data

Gap = 30.1 pts. }

Private Label Analysis

29

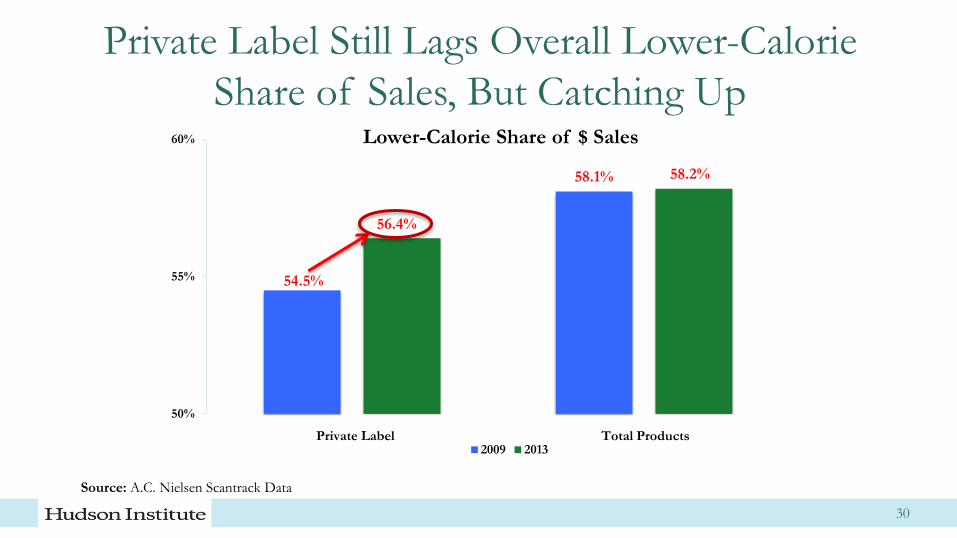

Private Label Still Lags Overall Lower-Calorie

Share of Sales, But Catching Up

54.5%

58.1%

56.4%

58.2%

50%

55%

60%

2009 2013Private Label

Lower-Calorie Share of $ Sales

30

Total Products

Source: A.C. Nielsen Scantrack Data

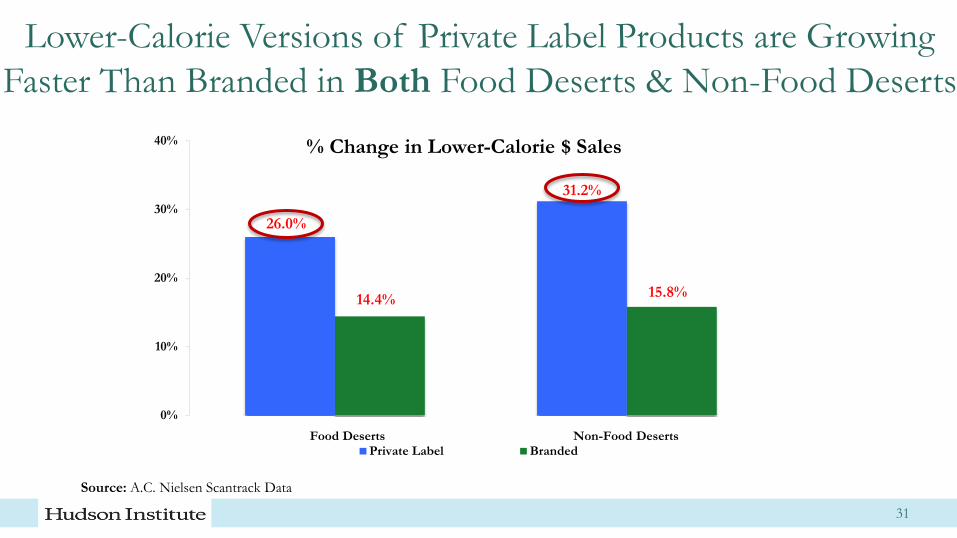

Lower-Calorie Versions of Private Label Products are Growing

Faster Than Branded in Both Food Deserts & Non-Food Deserts

26.0%

31.2%

14.4% 15.8%

0%

10%

20%

30%

40%

Private Label Branded

74.7%

Food Deserts

% Change in Lower-Calorie $ Sales

31

Source: A.C. Nielsen Scantrack Data

Non-Food Deserts

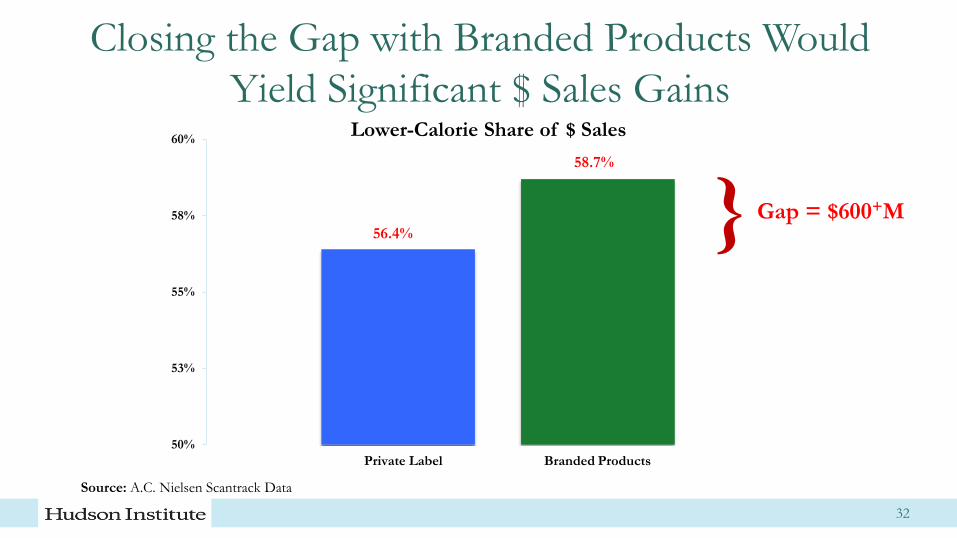

Closing the Gap with Branded Products Would

Yield Significant $ Sales Gains

56.4%

58.7%

50%

53%

55%

58%

60%

Private Label

Lower-Calorie Share of $ Sales

32

Branded Products

Source: A.C. Nielsen Scantrack Data

} Gap = $600+M

Implications

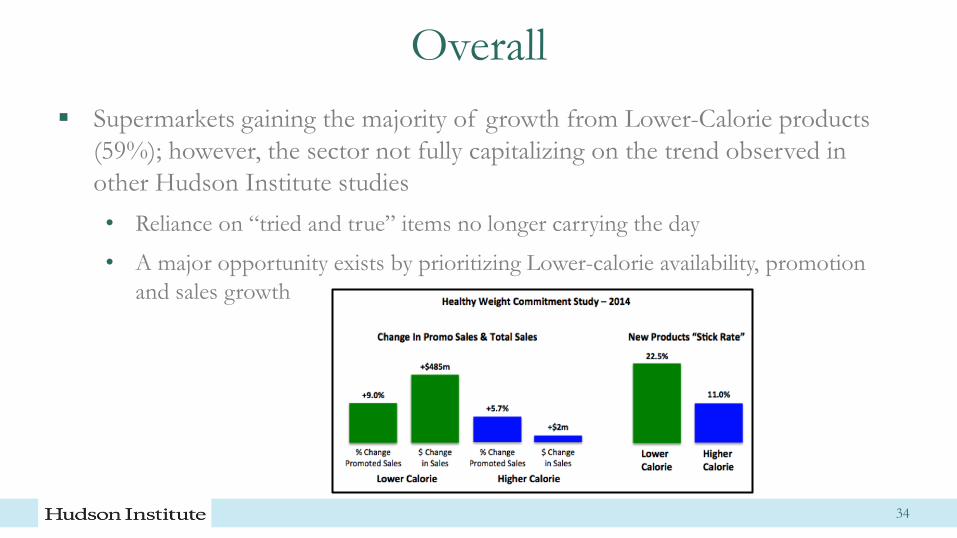

Overall

Supermarkets gaining the majority of growth from Lower-Calorie products

(59%); however, the sector not fully capitalizing on the trend observed in

other Hudson Institute studies

• Reliance on “tried and true” items no longer carrying the day

• A major opportunity exists by prioritizing Lower-calorie availability, promotion

and sales growth

34

Food Deserts

Lower-calorie growth is outpacing Higher-calorie growth in both Food

Deserts and Non-Food Deserts

• Signals that consumers, regardless of where they live or shop, are increasingly

seeking out Lower-calorie alternatives and must not be ignored

• As demand is there plus have availability…must rethink promotion and

merchandising strategies to narrow Lower-calorie sales gap with non-food deserts

35

Calorie Contributors to Kids & Adolescents

Continued over-emphasis on Higher-calorie versions will face even stronger

headwinds from:

Consumers

Public health community/regulators

• Situation aggravated in Food Deserts and by Lower-calorie availability deficiencies

Suggests there is an opportunity to re-think store makeup, merchandising/

promotion practices and distribution priorities to capture huge growth

potential in BFY products for youth.

36

Private Label

Private Label is making significant strides in Lower-Calorie

• Huge sales potential if retailers bridge Gap with branded products in

Lower-calorie versions

• Opportunity exists to drive innovation in Private Label by addressing the

“headwinds” found in those products that contribute the most calories to

kids

37

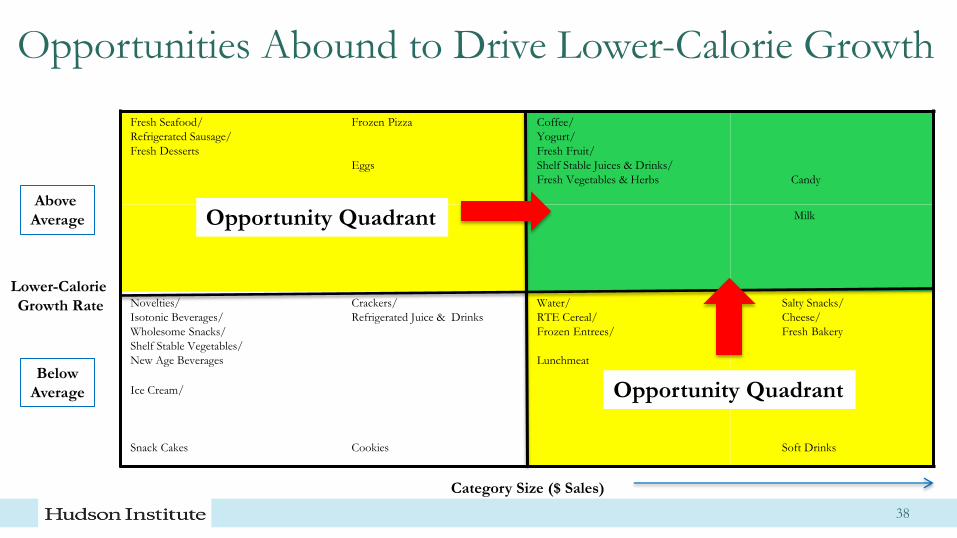

Opportunities Abound to Drive Lower-Calorie Growth

Fresh Seafood/

Refrigerated Sausage/

Fresh Desserts

Frozen Pizza

Eggs

Coffee/

Yogurt/

Fresh Fruit/

Shelf Stable Juices & Drinks/

Fresh Vegetables & Herbs

Candy

Milk

Novelties/

Isotonic Beverages/

Wholesome Snacks/

Shelf Stable Vegetables/

New Age Beverages

Crackers/

Refrigerated Juice & Drinks

Water/

RTE Cereal/

Frozen Entrees/

Lunchmeat

Salty Snacks/

Cheese/

Fresh Bakery

Ice Cream/

Snack Cakes

Cookies

Soft Drinks

Lower-Calorie

Growth Rate

Above

Average

Below

Average

Category Size ($ Sales)

Opportunity Quadrant

Opportunity Quadrant

38

39

Appendix

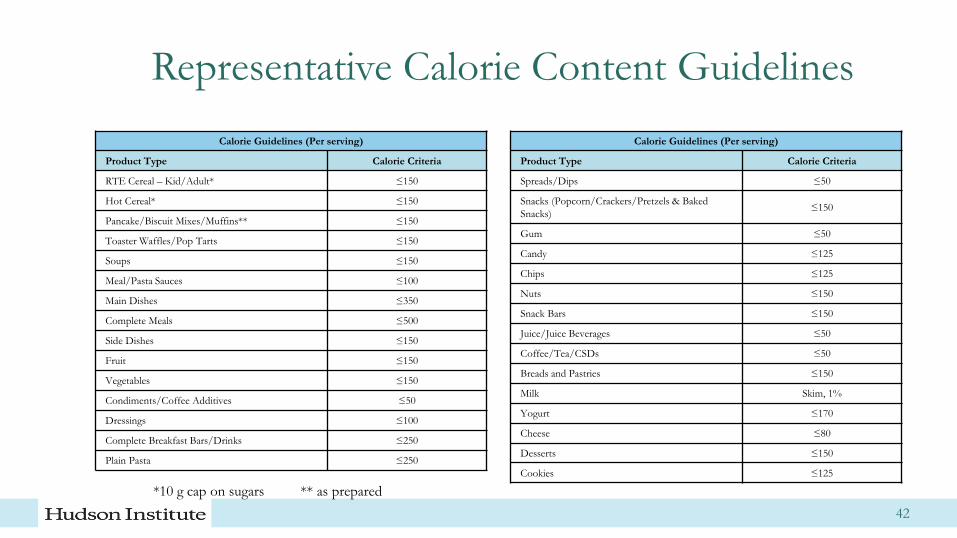

Representative Calorie Content Guidelines

Calorie Guidelines (Per serving)

Product Type Calorie Criteria

RTE Cereal – Kid/Adult* ≤150

Hot Cereal* ≤150

Pancake/Biscuit Mixes/Muffins** ≤150

Toaster Waffles/Pop Tarts ≤150

Soups ≤150

Meal/Pasta Sauces ≤100

Main Dishes ≤350

Complete Meals ≤500

Side Dishes ≤150

Fruit ≤150

Vegetables ≤150

Condiments/Coffee Additives ≤50

Dressings ≤100

Complete Breakfast Bars/Drinks ≤250

Plain Pasta ≤250

*10 g cap on sugars ** as prepared

Calorie Guidelines (Per serving)

Product Type Calorie Criteria

Spreads/Dips ≤50

Snacks (Popcorn/Crackers/Pretzels & Baked

Snacks) ≤150

Gum ≤50

Candy ≤125

Chips ≤125

Nuts ≤150

Snack Bars ≤150

Juice/Juice Beverages ≤50

Coffee/Tea/CSDs ≤50

Breads and Pastries ≤150

Milk Skim, 1%

Yogurt ≤170

Cheese ≤80

Desserts ≤150

Cookies ≤125

42

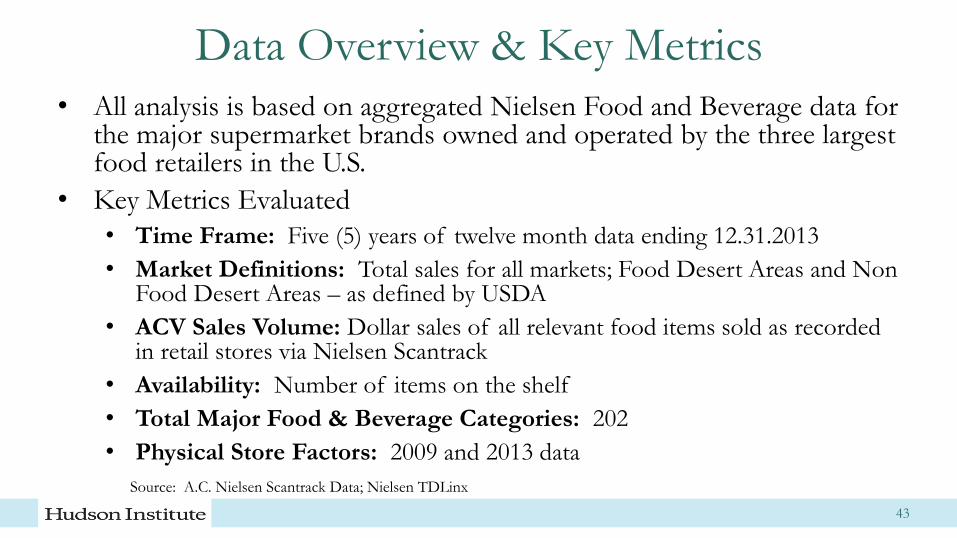

Data Overview & Key Metrics

• All analysis is based on aggregated Nielsen Food and Beverage data for the major supermarket brands owned and operated by the three largest food retailers in the U.S.

• Key Metrics Evaluated

• Time Frame: Five (5) years of twelve month data ending 12.31.2013

• Market Definitions: Total sales for all markets; Food Desert Areas and Non Food Desert Areas – as defined by USDA

• ACV Sales Volume: Dollar sales of all relevant food items sold as recorded in retail stores via Nielsen Scantrack

• Availability: Number of items on the shelf

• Total Major Food & Beverage Categories: 202

• Physical Store Factors: 2009 and 2013 data

43

Source: A.C. Nielsen Scantrack Data; Nielsen TDLinx

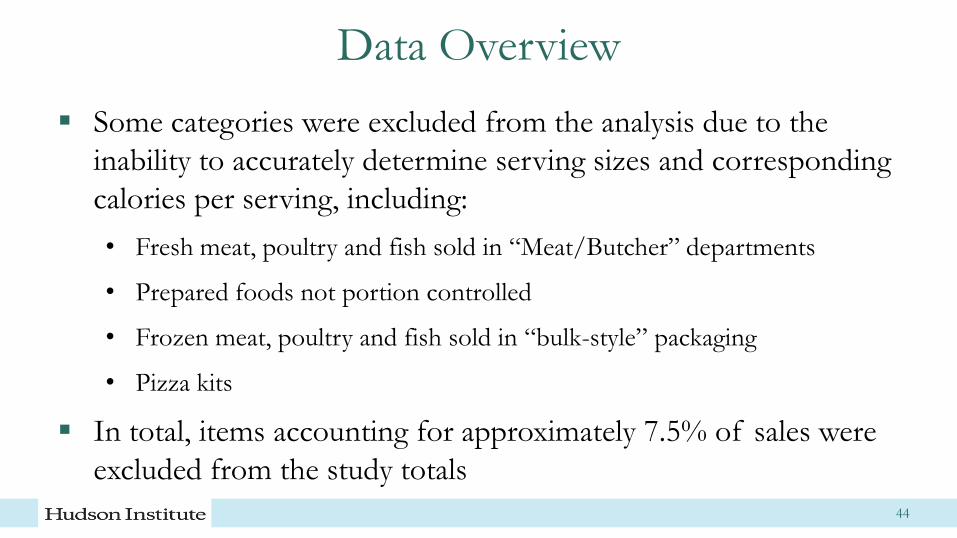

Data Overview

Some categories were excluded from the analysis due to the

inability to accurately determine serving sizes and corresponding

calories per serving, including:

• Fresh meat, poultry and fish sold in “Meat/Butcher” departments

• Prepared foods not portion controlled

• Frozen meat, poultry and fish sold in “bulk-style” packaging

• Pizza kits

In total, items accounting for approximately 7.5% of sales were

excluded from the study totals

44

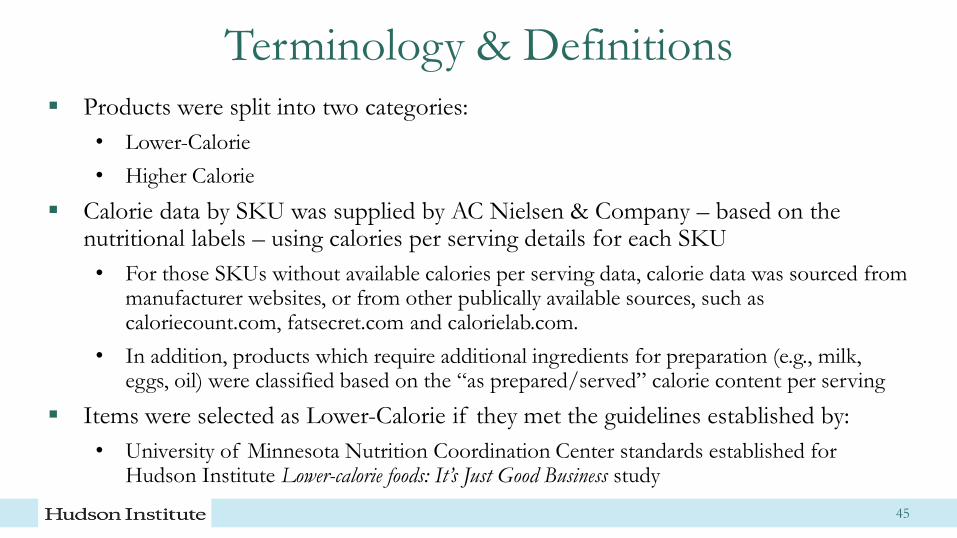

Terminology & Definitions Products were split into two categories:

• Lower-Calorie

• Higher Calorie

Calorie data by SKU was supplied by AC Nielsen & Company – based on the nutritional labels – using calories per serving details for each SKU

• For those SKUs without available calories per serving data, calorie data was sourced from manufacturer websites, or from other publically available sources, such as caloriecount.com, fatsecret.com and calorielab.com.

• In addition, products which require additional ingredients for preparation (e.g., milk, eggs, oil) were classified based on the “as prepared/served” calorie content per serving

Items were selected as Lower-Calorie if they met the guidelines established by:

• University of Minnesota Nutrition Coordination Center standards established for Hudson Institute Lower-calorie foods: It’s Just Good Business study

45