Embed Size (px)

Citation preview

The Bermuda LegalGuide 2009

IN ASSOCIATION WITH

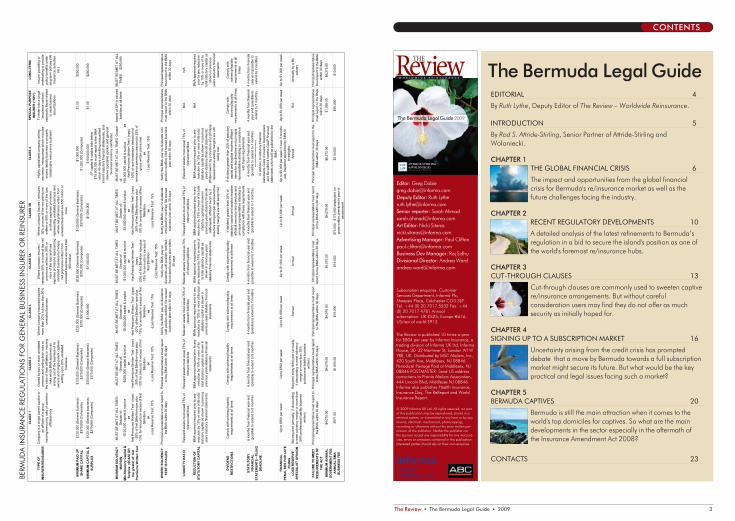

CONTENTS

The Review • The Bermuda Legal Guide • 2009 3

EDITORIAL 4

By Ruth Lythe, Deputy Editor of The Review – Worldwide Reinsurance.

INTRODUCTION 5

By Rod S. Attride-Stirling, Senior Partner of Attride-Stirling andWoloniecki.

CHAPTER 1THE GLOBAL FINANCIAL CRISIS 6

The impact and opportunities from the global financialcrisis for Bermuda's re/insurance market as well as thefuture challenges facing the industry.

CHAPTER 2RECENT REGULATORY DEVELOPMENTS 10

A detailed analysis of the latest refinements to Bermuda’sregulation in a bid to secure the island's position as one ofthe world's foremost re/insurance hubs.

CHAPTER 3CUT-THROUGH CLAUSES 13

Cut-through clauses are commonly used to sweeten captivere/insurance arrangements. But without carefulconsideration users may find they do not offer as muchsecurity as initially hoped for.

CHAPTER 4SIGNING UP TO A SUBSCRIPTION MARKET 16

Uncertainty arising from the credit crisis has prompteddebate that a move by Bermuda towards a full subscriptionmarket might secure its future. But what would be the keypractical and legal issues facing such a market?

CHAPTER 5BERMUDA CAPTIVES 20

Bermuda is still the main attraction when it comes to theworld's top domiciles for captives. So what are the maindevelopments in the sector especially in the aftermath ofthe Insurance Amendment Act 2008?

CONTACTS 23

The Bermuda LegalGuide 2009

The Bermuda Legal Guide

Subscription enquiries: CustomerServices Department, Informa Plc,Sheepen Place, Colchester CO3 3LP.Tel: +44 (0) 20 7017 5532 Fax: +44(0) 20 7017 4781 Annual subscription: UK £525; Europe !616,US/rest of world $913.

Editor: Greg [email protected] Editor: Ruth [email protected] reporter: Sarah [email protected] Editor: Nicki [email protected] Manager: Paul Clifton [email protected] Dev Manager: Raj SidhuDivisional Director: Andrea [email protected]

© 2009 Informa UK Ltd. All rights reserved; no partof this publication may be reproduced, stored in aretrieval system, or transmitted in any form or by anymeans, electrical, mechanical, photocopying,recording or otherwise without the prior written per-mission of the publisher. Neither the publisher northe sponsor accept any responsibility for any inaccura-cies, errors or omissions contained in this publication.Interested parties should rely on their own enquiries.

The Review is published 10 times a yearfor $804 per year by Informa Insurance, atrading division of Informa UK Ltd, InformaHouse, 30–32 Mortimer St, London W1W7RE, UK. Distributed by MSC Mailers, Inc,420 South Ave, Middlesex, NJ 08846.Periodical Postage Paid at Middlesex, NJ08846 POSTMASTER: Send US addresscorrections to Pronto Mailers Association,444 Lincoln Blvd, Middlesex NJ 08846.Informa also publishes Health Insurance,Insurance Day, The ReReport and WorldInsurance Report.

BERM

UD

A IN

SURA

NC

E RE

GU

LATI

ON

S FO

R G

ENER

AL B

USI

NES

S IN

SURE

R O

R RE

INSU

RER

INTRODUCTION

The Review • The Bermuda Legal Guide • 2009 5

In recent months the economic crisis has transformed assets into liabilities and reducedsome of the world’s most famous financial institutions to rubble. But through all the dramaof collapses, stock market dives and the bailout of AIG, the Bermuda market has held firm.From the middle of the Atlantic, the island has even increased its influence as a powerhouse

for global re/insurance markets and lost none of its allure as a domicile for captives.Such strength in the depths of what is possibly the biggest financial storm ever to hit the

world economy is no happy accident.As this guide shows, Bermuda has made every effort to stay ahead of the game, constantly

honing a regulatory regime that aims to be both facilitive yet responsible.And past months have been marked by further refinements from the Bermuda Monetary

Authority, which are set out in Chapter 2.Most notably the Insurance Amendment Act 2008 has placed Bermuda firmly at the

forefront of a risk-based approach to regulation.The island is continuing to develop this concept, which will help it to cement its position as a

platform of choice for insurance carriers in the US and Europe.But while Bermuda’s re/insurers have for the most part, survived the adverse effects of the

economic crisis, the future holds its fair share of challenges.The global downturn has left a cruel legacy on balance sheets in the form of impoverished

investment returns, which have only been compounded by a liquidity drought.In addition, regulation, whether targeted at offshore jurisdictions or the looming

implementation of Solvency II in Europe has created yet more bridges for the market to cross.Nonetheless innovation has always been the watchword of the Bermuda market from 9/11

to Hurricane Ike.In recent months many of the island’s re/insurers have again managed to turn times of

crisis into opportunity. And if history is anything to go by this is bound to continue.I would like to thank Attride-Stirling & Woloniecki for their contribution to the sixth Bermuda

legal guide. As their fascinating exploration of the key issues that make and shape the island’sre/insurance market powerfully shows, a strong legal framework will help withstand anystorm.

Ruth LytheDeputy EditorThe Review – Worldwide Reinsurance

EDITORIAL

4 The Review • The Bermuda Legal Guide • 2009

2009 is off to an interesting start in Bermuda. While the outside world descends intoeconomic chaos, the number of new captives formed in the first quarter in Bermuda is up, incomparison to the number for 2008. And interest in captives is rising. In addition, people

are already speaking of the ‘Class of 2009,’ with reference to companies such as Torus,Ironshore, Argo and Canopius. While not all are wholly new entities, they have expandedaggressively either in terms of scaling up their personnel drastically or in providing additionalcapital and capacity in various areas. At a time when companies around the world were havingdifficulties and contracting, these Bermudians were expanding with zeal.

2009 becomes more and more interesting. The mergers and acquisitions season has started inearnest. The current dust-up over which suitor will carry away the fair IPC Re has created a greatdeal of interest in and outside Bermuda. And market observers believe that this is a sign of thingsto come. It has always been the case that Bermuda would see new companies set up in ‘waves’following natural and man-made disasters (hurricanes, September 11, etc) and then within a shortperiod of years there would follow a series of mergers and acquisitions. The financial crisis slowedthis natural cycle, but recent events show that one cannot stop progress. So watch this ‘space’.

The market appears to be hardening, however the extent of this remains to be seen. But ahardening market bodes well for the Bermuda Market.

The offshore world has received some harsh media attention, with some accusing ‘off-shore’ ofbeing entirely responsible for the economic problems in the West. But all of this ignores the realityor realities. The sub-prime problem was very much an onshore problem. And the issues of invest-ment in and the collapse of the banking industry in Iceland have absolutely nothing to do with theso-called off-shore world.

As to the ‘tax-haven label’, Bermuda has for a number of years been aggressively pursuing theexecution of Tax Information Exchange Agreements (TIEAs) and has now completed 15 TIEAs, andis pursuing more, noting that 12 is the number which the Organisation for Economic Cooperationand Development (OECD) plucked out of the sky as being the number it identified with not being aTax Haven. Bermuda hopes to come off the OECD ‘grey list’ as a result of this and moreimportantly the fact that Bermuda not only executes TIEAs but also enforces them.

When the attempts to find a scape-goat for the current world financial crisis have faded, theuniverse will return to business as usual. In Bermuda this means trying to find new ways tomanage risks, control risks, insure risks and to manage capital. This is what we have always doneand will continue to do. Bermuda companies paid approximately 27% of the $57bn in losesarising in the devastating hurricanes of 2005 (Katrina et al). This highlights the very positivecontributions which the Bermuda market makes to the US and the world economies, acontribution which will continue in the years to come.

Rod S. Attride-StirlingSenior PartnerAttride-Stirling & Woloniecki

Riding the waveStrength in the storm

THE FINANCIAL CRISIS CHAPTER 1

The Review • The Bermuda Legal Guide • 2009 76 The Review • The Bermuda Legal Guide • 2009

A DIFFERING PICTUREBermuda continues to providethe lion’s share of propertyand casualty capacity to theUS market but pricing varieswidely across the differentclasses of re/insurancebusiness.

On the propertyreinsurance side the softmarket has finally ended withrates in ‘peak zones’, (ieCalifornian Quake and USWindstorm) increasing by 20-30%. In property insuranceprices are increasing in directcorrelation to the likelihoodof cat exposure (especially forFortune 1000 companies)with increases of 20% to even60% reported as‘verticalisation’ of the markettakes hold.

The story is not so good forthe casualty reinsurancemarket where Bermuda istaking a very cautiousunderwriting approach andawaiting an upturn in thecasualty insurance market.Except for financialinstitutions D&O insurance,which has seen sharp pricingincreases of 20-30% inresponse to the sub-primesecuritizations andMadoff/Stanford fraudlitigation in the US, elsewherein the casualty insurance classBermuda is seeing ratescontinue to decline, or remainstagnant. Rates remain lowapparently as a result of lesscustomer demand, as well asthe introduction of four newercompetitors – Ironshore,Torus, Canopius and Argo Re– to the market.

The causes of the current global economic crisis are well documented. In theUS we have seen the predictable burst of the sub-prime mortgages bubbleand the catastrophic effect it has had on the securities market and the

finance industry as a whole. The sheer magnitude of the toxic Collaterised Debt Obligations (CDOs) and

Credit Default Swaps (CDSs) proliferating the financial markets led to the wellpublicised failures of those most prestigious institutions of Lehman Brothers andBear Stearns, as well as the US government bailout of AIG. In turn, CEOs ofleading re/insurance companies such as AIG, Swiss Re and XL resigned.

Just when things looked like they could not get any worse, the scarcity ofcapital caused by the credit crunch exposed numerous large scale frauds, mostnotably the Madoff scandal – said to be the largest Ponzi Scheme in historycausing approximately US$50-60bn of losses.

But how has the economic crisis impacted the Bermuda re/insurance marketand what lies in store in the future?

Rough watersThe whirlwind of the financial crisis has hit Bermuda

from all angles but the island’s re/insurance industry remains ready to fight another day, says Peter Dunlop

LURE OF LLOYD’SA significant number ofinsureds are reported to havesought alternative security tothat previous provided byAIG, although AIG remainthe primary insurer on manycasualty insurance programs.Meanwhile, Bermuda-ownedLloyd’s syndicates are allreporting strong surges inQ1, 2009 premium income,although that it is no doubtdue to the beneficial effectsof a stronger dollar in thecurrency exchange process ofUK premium income beingtranslated into US dollars.

Overall, the Bermudare/insurance market istherefore withstanding theadverse effects of theeconomic crisis better thanthe financial markets. This isnotwithstanding thatcustomers buying personallines coverage have less cashtoday. Even commercialinsureds, such as hotel chainsand factories, are strugglingto find the same capital theypossessed some 12 months

Under today’s capital constraints,

Bermuda is taking allprecautions to ensure

that underwritingdecisions are the correctones. To that end, thereis far greater scrutiny of

counterparty credit risk

ago. Certainly, the morevolatile peak zone propertycat re/insurance market hashardened, along withfinancial institutions directorsand officers (D&O) insurance,which is a welcomedevelopment in Bermuda.Across all classes there is areal focus on riskmanagement and a return toprudent core underwriting.Under today’s capitalconstraints, Bermuda istaking all precautions toensure that underwritingdecisions are the correctones. To that end, there is fargreater scrutiny ofcounterparty credit risk.Whereas in the pastconsideration was givenmainly to a counterparty’simmediate finances, todaysees reinsurance actuariesconsidering future financialindicators, including stockperformance, bond yieldsand CDS pricing in theirassessments of scenarios thatmay lead to a loss of surplusin future.

IMPOVERISHEDINVESTMENTSThe cautious underwritingapproach employed today isexplained by the fact thatalmost all Bermudianre/insurers have sustainedsignificant investment losses,although not as grave as theirEuropean counterparts.Bermuda’s re/insurers arecurrently seeking to repositiontheir investments out of highrisk funds/asset classes andinto more solid, conservative

THE FINANCIAL CRISIS

of internal reinsurancearrangements, deducting taxon the way through. Many ofBermuda’s re/insurers do notcede more than 10% ofpremiums from onshore butdo provide valuablereinsurance capacity ataffordable rates, thuskeeping US domesticinsurance rates lower.Finally, unlike many otheroffshore and tax-secretive

jurisdictions listed by theOECD, Bermuda signed upto the OECD in 2000 andhas for some time beenpoised to pass the requirednumber of appropriate TIEAsrequired.

LOOMING REGULATIONThe shadow of the EU’sSolvency II regulatory regimeof risk-based capitalmanagement requirementsand intra-European‘passporting’ looms large,imposing a requirement onthe Bermuda market toobtain mutual recognition

from foreign regulators.Many (European) doubtershave suggested that Bermudais a ‘light touch’ regulatoryjurisdiction which is unlikelyto be able to implementsufficient solvencyrequirements required to gainEuropean equivalence. Infact, the Bermuda MonetaryAuthority (BMA) is aresponsible but facilitativeregulator, which provides nodomicile for the rogue traderor tax cheat. The BMA hasmade great progresspreparing for Solvency II. ItsCEO Matthew Elderfield hasstated that the aim is forClass 4 and possibly evenClass 3B and 3A insurers tobe compliant by 2011, whichis some way ahead of manyEuropean regulators that aimto fully implement Solvency IIby 2013 or beyond.

STEERING A COURSEBermuda faces toughchallenges in underwritingand investment, as well aspowerful external politicaland regulatory pressure.Regardless of the down cyclewe are in or what this year’shurricane season has in store,what can be said withcertainty is that the Bermudamarket has navigated rougheconomic waters before. Asthe economic pendulumswings again the market willrespond through soundunderwriting judgment and aproper, responsible level ofregulation to steer a coursetowards continued financialsuccess. ®

CHAPTER 1

The Review • The Bermuda Legal Guide • 2009 9

THE FINANCIAL CRISISCHAPTER 1

8 The Review • The Bermuda Legal Guide • 2009

secretive jurisdictions andclose ‘tax loopholes’,exploited by US re/insurersand Bermudian affiliates.

US Congressman RichardNeal’s previouslyunsupported bill, HR6969,which sought tocounterbalance the perceivedcompetitive disadvantage toUS re/insurers writing USbusiness, has resurfaced.Senator Carl Levin’sproposed Stop Tax HavenAbuse Act has spawned asubcommittee charged withinvestigating tax fraudcommitted by US companies.The diplomatic Organisationfor Economic Co-operationand Development (OECD)has ‘named and shamed’, byproducing ‘white’, ‘grey’ and‘black’ lists all of thosejurisdictions that have, orhave not, signed a requisitenumber of Tax Informationand Exchange Agreements(TIEAs).

While these actions havebeen reported in somewhatalarmist terms, the likelyimpact on Bermuda isminimal. Bermuda is not a‘tax haven’ and as are/insurance market hasprovided approximately 40%coverage to the CaliforniaEarthquake Authority, nearly70% to Florida insurers andaround 65% to the TexasWindstorm InsuranceAssociation. The real targetsare those few US re/insurersthat write very large volumesof premium business in theUS and cede those premiumsto Bermuda affiliates by way

classes. Investment returnstoday therefore remainimpoverished, with littlechance of a meaningfulincrease in future despite therecent rally of the stockmarkets. Those lowinvestment returns have themost punishing impact onlong tail business which couldpreviously rely upon returns of5 to 7% year on year until a

claim became payable.In terms of writing new

business in 2009, liquidityhas dried up, the cost ofcapital has increased to aprecarious level andretrocession capacity haseither become prohibitivelyexpensive or has contracted.Reinsurance capacityprovided in the past by thecapital markets in the form of

sidecars, cat bonds and ILWshas shrunk in line with thecrash in investment andliquidity formerly available toinvestment funds, hedgefunds and banks.

MORE M&AWhat this means for theBermuda market is thatreserve releases fromprevious years have, orinevitably shortly will, cease.In the present economicclimate it is almost impossiblefor many Bermudianre/insurers to ‘reload’ capitalin the same way as theyhistorically have donefollowing major hurricanes orother disasters.

It is unlikely that there areviable start-up companieswaiting in the wings toreplace the collapsedre/insurers of the future, asthey so successfully did in2001 and 2005. Today,Bermudian re/insurers aretherefore committed toreducing loss ratios andunderwriting for a profit. Nolonger can the investmentside of the businesscounterbalance underwritinglosses and the presentbusiness reality maynecessitate consolidation ofmore Bermuda re/insurers.

NOT A ‘TAX HAVEN’It will not have escapedanyone’s attention thatPresident Obama, supportedby the major Europeanpolitical leaders, has followedthrough on his promise totarget offshore and tax-

Without doubt, thecost and lack ofcapital availability intoday’s economicclimate,compounded by theMadoff scandal, hashad a devastatingimpact on the multi-billion dollar hedgefunds industry inBermuda. Fundshave been hitconsistently withredemption requestsin the last 12months, causingfunds to suspend netasset valuecalculations orredemptionsaltogether. Manyfunds are now inliquidation orteetering on thebrink of insolvency.A significant numberwere alsoparticipating asMadoff feederfunds. Investors inthose funds areangry and looking

for someone toblame. Fundmanagers,administrators andauditors are in thefiring line. It remainsto be seen howgreat an impact theMadoff scandal willhave on D&O, E&Oor any other lines ofbusiness but somecommentators havesuggested that awide spread of$760m to $3.8bn inMadoff-relatedclaims will beasserted.

Without doubt,more subprime-related securitiesclaims have beencommenced in theUS in the last 12months than theentire period of theSavings and Loandebacle. How thosewill translate intosuccessful D&O andE&O claims remainsto be seen butclaims on financialguaranteecompanies such asSCA, CIFG andChannel Re appearto have beensuccessfullycontained.

The real questionBermuda is askingitself is what thisseason’s hurricaneseason has in store.Depending on theanswer to thatquestion there maybe goodopportunities for therun-off market.

HARD TIMES FOR HEDGE FUNDS

Bermuda is not a ‘taxhaven’ and as a

re/insurance market hasprovided approximately

40% coverage to theCalifornia Earthquake

Authority, nearly 70% toFlorida insurers and

around 65% to the TexasWindstorm Insurance

Association

REGULATION

The Amendment Act alsopermits the BermudaMonetary Authority (BMA) tomake orders that setprudential standards forenhanced capitalrequirements and gives theBMA the power to requirecapital add-ons.

Additionally, it reclassifiedBermuda’s Class 3 insurersinto three classes, 3, 3A and3B. The new legislation furtherpermits the establishment of a‘special purpose insurer’ toconduct ‘special purposeinsurance’.

The Amendment Actrequires Class 4 reinsurers toprepare and file with the BMAadditional financial state-ments prepared in accor-dance with GAAP or IFRSwhich must be audited. TheBMA shall publish such state-ments in the manner it consid-ers appropriate to bring themto the attention of the public.The filing and publication ofthese financial statements willprovide greater transparencyin relation to the financials ofClass 4 companies. Class 4reinsurers are alreadyrequired to file with the BMAstatutory financial statementsprepared in accordance withthe requirements of Bermu-da’s Insurance Act 1978 andits related regulations.

ENHANCED POWERSThe Amendment Act permitsthe BMA to prescribe by orderprudential standards inrelation to enhanced capitalrequirements and capital andsolvency returns, which must

be complied with byregistered insurers. Suchstandards may imposedifferent requirements to becomplied with by differentclasses of insurers. Thisprovides the primarylegislative basis for theadoption of the BermudaCapital SolvencyRequirements (BSCR) whichare more attuned to thespecific risk profile of thecarrier than previously. Theadoption of BSCR is part ofthe BMA Roadmap towardsSolvency II Equivalence, newlyemerging European Union

insurance standards. The BMA may make

adjustments to an insurer’senhanced capitalrequirement and availablestatutory capital and surplus.The BMA can only make suchadjustments in certainprescribed circumstances.These relate to the BMAconcluding that the riskprofile of the insurer deviatessignificantly from certainunderlying assumptions. Anyadjustments so made wouldonly have effect 90 daysfollowing notification to theinsurer.

CLASS 3 CHANGESPrior to the Amendment ActBermuda’s Class 3 insurerscomprised a miscellaneousclass categorised by notbeing licensed as Class 1(single or group ownedcaptives), Class 2 (multi-owner captives and/orcaptives writing up to 20%unrelated risk) or Class 4(writing property catastrophereinsurance or excess liabilitybusiness).

Class 3 insurers covered awide spectrum ranging fromessentially captive-typeentities with a level ofunrelated risk that exceeded20% through to commercialreinsurers that wrote onlyunrelated risk. Consistentwith Bermuda’s risk-basedapproach towards regulation,it was felt appropriate toreclassify the sector morecomprehensively to recognisethe different types of Class 3insurer (see page 12).

Notwithstanding theseprovisions, the AmendmentAct provides that the BMAmay register an insurer in anyparticular class, even if thecompany may not qualify tobe registered in such class, ifthe BMA deems suchregistration appropriate.

The Amendment Actincluded transitionalprovisions in relation to Class3 insurers. It required insurerswho so qualify to makeapplication to the BMA to bereclassified as Class 3A or, asthe case may be, Class 3Binsurers before December 312008. Failure to do so

CHAPTER 2

The Review • The Bermuda Legal Guide • 2009 1110 The Review • The Bermuda Legal Guide • 2009

Rightly or wrongly, the global financial crisis isswinging the pendulum towards increasedregulation in the financial sector on a global basis.

In times of change such as the one evolving before us,Bermuda has consistently sought and found newopportunities to provide responsible yet facilitative marketdriven solutions at the pace required by modern business.

In the insurance sector, regulation in Europe is movingfrom a rules-based approach to a risk-based approach toregulation. The good news is that Bermuda has been atthe forefront of the risk-based approach to regulation,and as we will see, with the Insurance Amendment Act2008 (Amendment Act) and its related regulations,Bermuda continues to develop and refine this concept andprime Bermuda as a platform of choice for insurancecarriers in the US and Europe in these times of change.The Amendment Act introduced several importantchanges to the regulation of insurance business inBermuda. It introduced new requirements on Bermuda’shighly-capitalised property catastrophe and excess of lossClass 4 carriers to prepare, in addition to statutoryfinancial statements, audited financial statementsprepared in accordance with GAAP or IFRS standards.

Aheadofthe curveBermuda has always managed to adapt and lead when it comes to regulatorydevelopments. In today’s economic climate this is a quality needed more than ever, say Neil Horner and Federico Candiolo

Consistent withBermuda’s risk-based

approach towardsregulation, it was felt

appropriate to reclassifythe sector more

comprehensively torecognise the differenttypes of Class 3 insurer

The Review • The Bermuda Legal Guide • 2009 13

enabled the BMA to canceltheir registration.

SPECIAL PURPOSE INSURERSThe Amendment Act legisla-tively creates the concept of aspecial purpose insurer (SPI)with the following features:

• A SPI will only bepermitted to write ‘specialpurpose business’ which is

defined by the AmendmentAct as ‘insurance businessunder which an insurer fullyfunds its liabilities to thepersons insured through adebt issuance where therepayment rights of theproviders of such debt aresubordinated to the rights ofthe person insured or someother financing mechanism

approved by the BMA orthrough cash or timedeposits’.• The minimum paid-upshare capital will be US$1.• An SPI must maintainsufficient assets to meet itsinsurance obligations giventhe size, business mix,complexity and risk-profile ofthe SPI.• The SPI will be restrictedfrom entering into any otherbusiness agreements exceptthose which are related to itsspecial purpose.

The Amendment Actdescribes what factors shouldbe considered by the BMAwhen it comes to registering abody as an SPI. The BMAshould have regard towhether the insurer is solelyinsuring or reinsuring one ormore risks or group of riskswith one or morepolicyholders and thesophistication of thepolicyholders or thesophistication of the parties toa debt issuance or otherfunding mechanism.

KEY TO SUCCESSThese new provisions willenhance Bermuda’s ability tooffer innovative transformertype structures.

Bermuda is committed toprovide a responsible yetdynamic environment forinsurers and reinsurers toconduct insurance business.Risk-based regulatorysupervision is core to thecontinued success of theBermuda insuranceproposition. ®

REGULATIONCHAPTER 2

12 The Review • The Bermuda Legal Guide • 2009

Bermuda’s Class 3insurers have nowbeen reclassified intoClass 3, Class 3A andClass 3B.

Class 3 insurersnow include insurerswhose percentage ofunrelated businessrepresents more than20% but less than50% of unrelatedbusiness (on a netpremium basis).Existing Class 3segregated accountscompanies will beallowed to remain asClass 3 insurers atthis time. Likewise,fully collateralisedsidecars will not berequired to re-register as Class 3Aor Class 3B.

Class 3A is thecategory which isexpected to apply tothe majority of exist-ing Class 3 insurersand will includethose insurers whosepercentage of unre-lated business which

exceeds or is expect-ed to exceed 50% ofnet premium writtenand/or net loss andloss expense provi-sions, and where theunrelated businesspremium does not,or is not projected toexceed US$50m.

Class 3B includesinsurers whosepercentage ofunrelated businessexceeds or isprojected to exceed,50% of net premiumwritten and/or netloss and loss expenseprovisions andwhere the unrelatedbusiness premiumdoes exceed or isprojected to exceedUS$50m.

Class 3B insurerswill be subjected torestrictions onpayment ofdividends. Theserestrictions include,making paymentsexceeding 25% of aClass 3B insurer’s

total statutory capitaland surplus, unlesscertain declarationsare filed with theBMA.

It should be notedin this context that‘loss and lossexpense provisions’means the amountcalculated in relationto a body corporateby the application ofthe principles set outin the InsuranceAccountsRegulations 1980 (asamended by theInsurance AccountsAmendmentRegulations 2008)for the calculation ofthose amounts inrelation to an insurer,and ‘unrelatedbusiness’ refers tothe insurancebusiness consistingof insuring risks ofpersons who are notshareholders in, oraffiliates of, theinsurer.

CLASS 3 – THE NEW RULES A dangerous illusion?

Cut-through clauses are oftenused in conjunction with

Bermudian captive re/insur-ance arrangements. For example,

a US insured is obliged under itslocal laws to interpose a local

insurer to front much of itsinsurance business needs

before its Bermudian captivecan assume the business. Thefronting commission will be a

welcome sweetener but thefronting company will there-

after be exposed to the insuredand the credit risk of the insured’scaptive – which is the front’s rein-

surer in respect of this frontedbusiness.To comfort the fronting

company that the captive willremain capitalised by the parentinsured with sufficient monies to

‘reimburse’ the fronting company,a cut-through clause can be incor-porated into the contract of retro-

cession – the aim being to give thefront, which has no privity in the retro-

cessional contract, the right to claimmonies from the retrocessionaire

under that contract in certain pre-scribed circumstances.

Cut-through clauses, commonly used to sweeten captive re/insurance

arrangements, may not offer the A-grade security hoped for

when put to the test, warn Alex Jenkins and Kehinde George

CUT-THROUGH CLAUSES

namely, sections 36A to 36G.If it were shown that the cut-through clause was agreed toby the captive for no consider-ation at all or at an underval-ue to the value ofretrocessional contract andthat the dominant purpose ofthe cut-through clause was toput the proceeds of the retro-cessional policies beyond thereach of an entity or class ofentities which is making ormay at some time make aclaim against the captive, cer-tain creditors could apply tohave the transaction set aside.This is relatively new legisla-tion in Bermuda which has notyet been tested before theBermuda Courts and as suchits precise application to sucha scenario may be open touncertainty.

However, even if theretrocession’s governing lawpermits the enforcement of acut-through clause, eg, wheresuch a clause allows a cut-through in the event of latepayment by the captive to thefront, the clause may becomeineffective in the event of theBermudian captive’sinsolvency. The point has alsonot been tested in theBermuda Courts - nor havethe following workingsolutions which are predictedto avoid insolvency relatedproblems (see section listingalternatives to cut-throughclauses on previous page).

CAPTIVES INSOLVENCY ANDCUT-THROUGH CLAUSESSection 237 of the BermudianCompanies Act 1981 will ren-

der a payment made under acut-through clause void if,firstly, at the date that the cap-tive agreed to the cut-throughclause it was unable to pay itsdebts as they became duefrom its own money; and secondly, where the cut-through was made with a viewof giving the fronting compa-ny a preference over othercreditors of the captive. If bothfactors are present and thecaptive bought the retroces-sion within six months beforethe commencement of its

winding up (ie, the date ofpresentation of a winding-uppetition or date of the passingof a resolution by its membersthat it be wound up voluntari-ly), the cut-through clausewould be likely deemed afraudulent preference of itscreditors and invalid.

Enforcement of the cut-through clause in the captive’sliquidation would probably becontrary to public policy. TheBermuda Court would likelyconsider the English House ofLords judgment in BritishEagle International Airlines vCompagnie International AirFrance [1975] to be highlypersuasive. That case heldthat it was open to the courts

to refuse to give effect toprovisions of a contract whichachieved a distribution of aninsolvent’s property which rancounter to insolvencylegislation.

MERELY ILLUSORY?The attraction of frontingbusiness includes the risk ofthere being only illusory rein-surance arrangements inplace for such exposures.Where a front has no com-mercial relationship with theinsured parent company,there is a risk of credit unwor-thiness and even, as has beenseen in the US Courts recently(see the facts of the case ofFencourt Reinsurance Co. vITT Industries, No.04-4786,2008 US Dist. LEXIS 47724(E.D. Pa. June 20, 2008)), thepossibility that the reinsuringcaptive will be divested andsold under-capitalised fromthe parent company group toa new and perhaps unwittingparent which is reluctant topay for the incumbent liabili-ties. The serious and oftenoverlooked problems associ-ated with the validity andenforceability of cut-throughclauses, emphasise theimportance of considering thecredit risk of the fronted pro-gramme as a whole. Tradi-tional cut-through clauseswhich are used to sweeten thedeal may be merely illusoryrather than A-grade security.As such, there are advanta-geous routes around suchproblems but careful thoughtshould be given to theirimplementation. ®

CHAPTER 3

The Review • The Bermuda Legal Guide • 2009 15

Usually, one of the prescribedtriggers entitling the front toclaim reimbursement forclaims liabilities it has paid tothe parent insured or becomesliable for, is the insolvency ofthe reinsuring captive. Howev-er, that does not mean theclause, if legally effective atinception of the policy) willcontinue to ‘work’ after thecaptive becomes insolvent. Theenforceability of a cut-throughclause allowing the front to‘reach-around’ the local cap-tive is a matter of the substan-tive contract law governing theretrocessional policy as well asBermudian insolvency law gov-erning the winding-up of thecaptive. These are eachaddressed in turn.

QUESTIONABLE VALIDITY While the UK has enactedlegislation permitting theenforcement of contracts bythird parties to receive abenefit under them if draftedappropriately, Bermuda hasno such statutory assistance. Ifthe retrocession (whichcontains the cut-throughclause) were governed byBermudian law and not, say,English law, the cut-throughclause would very likely beunenforceable due to anabsence of common lawprivity of contract – the frontnot being a named party tothe retrocession contract.

Equally, payment of moniesunder a cut-through arrange-ment might also fail for beinga disposition of property underthe provisions of Bermuda’sConveyancing Act 1983,

CUT-THROUGH CLAUSESCHAPTER 3

ALTERNATIVES TO CUT-THROUGH CLAUSES

14 The Review • The Bermuda Legal Guide • 2009

Traditional cut-throughclauses which are used

to sweeten the deal maybe merely illusory rather

than A-grade security

A security interest

It should be possibleto side step suchproblems if thefronting company isgiven a securityinterest over thecaptive’s rights toretrocessional claimsmonies. Provided thatthe securityagreement does notitself fall foul of theinvalidity provisionsreferred to herein, thefront should be ableto rely upon thecaptive’s rights as asecured creditor asagainst the liquidatorof the captive.A trust structureThe captive coulddeclare a trust, withinthe wording of theretrocessionalcontract, overprospectiveretrocessionalcollections to hold anysuch monies on trustfor the front, whichwould be thebeneficiary of thetrust. However, thecaptive would not beable to claim theretrocessional policyas a reinsurance asset– it would be an assetof the trust.Retrocessional monieswould be trustmonies. This mayhave regulatoryconcerns relating tothe captive’s solvencymargins.

ConditionalassignmentmechanismThe assignmentwould need to becarefully drafted toavoid a challenge toits validity that as atransfer of thecaptive’s future rights(a future chose inaction) toretrocessional policyclaims monies it is an‘agreement to assign’and not anassignment of knownrights to ascertainedmonies – the captivecannot legally assignthat which he doesnot already have.Under principles ofequity, a ‘future’assignment would beheld enforceable andbinding providedvaluableconsideration wasgiven by the front – a requirement thatcould be satisfied ifthe assignmentdocument was signedas a deed.

A segregatedaccounts companyIf a Bermudiancaptive which is asegregated accountscompany goes intoliquidation, ‘theliquidator shall ensurethat the assets linkedto one segregatedaccount are notapplied to theliabilities linked toany other segregatedaccount or to thegeneral account’(section 25(1) ofSAC).

In practical termsthe captive’sretrocessional policies wouldreinsure a specificsegregated accountof the captive ie adesignated single cell– for example oneentitled ‘Cell #053’.Cell #053 would benamed as theretrocedant. The same cell would have in turn reinsuredthe front.

The claimsmonies, which areultimately destinedfor the front would beinsulated/firewalled(within Cell #053)from the captive’sliquidation – thusmaking the use of acut-through clause, atrust arrangement or an assignment of retrocessional claims moniesunnecessary.

SUBSCRIPTION MARKET

If Bermuda moved to becomea pure subscription market orif a Lloyd’s satellite franchisecame to Bermuda – as hasalso been mooted, certainpractical market and legaldifficulties may arise many ofwhich have been addressedby the London Courts. Despite these efforts, majorloose-ends persist. Theseissues affect the lifetime of arisk, from initial presentation,to claims notification andsubsequent dispute resolution.

BROKERS’ RESPONSIBILITIESA number of legal authoritiesindicate that brokers owe aduty of care to their clientassureds not to place businesswith known/potentially weaksecurity. There are obviousbenefits to a broker spreadingthe potential of an insolvencyrisk of one or moresubscribing underwriters.

OVERSUBSCRIPTION BENEFITSThe English case of TheZephyr [1984] 1 All E.R. 35recognised the marketadvantages of seeking oversubscription: (i) it enablesa broker to show his businessto more underwriters; (ii) largelines encourage other largelines and to reach a 100%written line sooner; and (iii)if an assured wishes toincrease the sum insured orexceed its estimated grosswritten premium income tothe treaty, then the broker’sburden may be helped if theslip was initially oversubscribed.

SIGNING DOWN Market practice in Londonpermits the broker tounilaterally reduce each linepro rata if subscriptionsexceed 100%. This is thepractice of ‘signing down’which was recognised in theAppeal decision of the FenniaPatria, [1983] 2 Lloyd’s Rep.287, per Kerr L.J. The casealso heard that ‘signingdown’ can be prevented if anunderwriter states as muchnext to his signature.

SIGNING UPImagine the followingscenario: underwriter ‘U1’writes a 100% line. It issigned down to 50% asunderwriter ‘U2’ laterscratches a 100% line too.The presentation then‘closes’. If U2 latersuccessfully avoids itsparticipation, will U1’s 50%signed down line revert backto its original 100%?

The opportunity for‘signing up’ is arguable on acommon sense analysis, if

one considers that therescission would be effectiveab initio, in other words, U2avoids the policy as if it hadnever written its 100% line(subsequent to U1’s).

However, the Courts havegone some way to recognisewhat is a staggered processtoward a crystallisation‘closing’, by the broker, ofoversubscribed lines down toa fixed signed down line sothat ‘...each line written on aslip gives rise to a bindingcontract pro tanto betweenthe underwriter and theinsured or reinsured for whomthe broker is acting when hepresents the slip. Theunderwriter is therefore boundby this line, subject only to thecontingency that it may fall tobe written down on 'closing' tosome extent if the slip turnsout to have been over-subscribed.’ (per Kerr LJ inFennia Patria.)

There is no direct authorityon ‘signing-up’. The writer isaware of one serious attemptat a signing-up argumentunder English law but whichlost in arbitration and also onappeal to the London Court,the award and judgment arenot publicly available.

MORE RESPONSIBILITYUsually, the client of thebroker is the re/assured.However, the workings of asubscription market mayextend a broker’s duty of carebeyond its client to include itsunderwriting market. Oversubscription can beunpopular with underwriters

CHAPTER 4

The Review • The Bermuda Legal Guide • 2009 1716 The Review • The Bermuda Legal Guide • 2009

Bermuda’s re/insurers are in strong form but credit crisis uncertainty has sparked debatethat a full subscription market might make theirfuture even more secure, says Alex Jenkins

Subscribingto change

If Bermuda moved tobecome a pure

subscription market orif a Lloyd’s satellitefranchise came to

Bermuda – as has alsobeen mooted, certainpractical market and

legal difficulties may arise

Subscription underwriting, where the risk being written is taken in various proportions by a number of re/insurers, is nothing new

in Bermuda. Underwriting practices describedinfamously by Thomas J. in Sphere Drake v EIU, SCB et al [2003] EWHC 1636 showed Bermudianmanaging general underwriters(MGUs) regularly co-subscribing to retrocessional business withnumerous 50-100% lines on a given contract – but that was arguably participation in the Londonmarket and not Bermuda per se. A mix of non andpure subscription underwriting exists here, thoughtraditionally, Bermudian carriers are known to write100% lines of the whole tower or of a single layeralbeit a narrower layer than might be co-written in London.

since it may cause them tohave less of a desirable riskthan they would like. Moreunpopular still can be theconverse, where a brokergave a ‘signing indication’ toan underwriter of the likelyeventual level of signingdown, only not to go on andachieve that anticipatedresult. There the underwriter,who did not sign his line ‘tostand’, is left with a larger linethan he desired or hisunderwriting guidelinespermit.

In The Zephyr it was notedthat underwriters were notable to evade liability to theirassured for the balancebetween the actual signeddown line and the signeddown line envisaged by thebroker – had the signingindication been achieved.

The brokers, however, wereheld liable for the balancedue to their apparentnegligence for failing toexercise reasonable care touse best endeavours toachieve the signingindication. Also, the broker’sliability arose for breach ofcontract as the signingindication had constituted anoffer by the broker to takereasonable care – a failure todo so meant a breach of the‘collateral’ contract betweenbroker and underwriter.

LEADER’S OBLIGATIONS If there is more than oneunderwriter, there will almostcertainly be a leader - often,but not always, theunderwriter writing the largest

line. The leading underwriterclause in a contract isdesigned to allow the brokerto return only to the leader(s)to have certain mattersagreed, thereby binding thefollowers as well. Theseclauses/general underwritingagreements (which haveevolved with London Marketassociation direction) areusually silent or unclear as tothe nature of the relationshipbetween ‘follower’ and ‘lead’– and therefore theobligations (if any) owed inperforming the leader’sdelegated authority to agreeor vary terms and settleclaims.

Whether the lead owes thefollowing market duties ofcare to avoid negligence as atort or as a contracted agentof the following market, is notclear. The answer to whichmay be significant to thefollowing market for claimsagainst the leader whenmeasuring loss/damages ortime bar expiry. Regrettably,there is no clear answer atpresent.

CLAIMS NOTIFICATIONS It is not unusual for a delay inthe presentation of claims bythe broker to the followingmarket. In practice thefollowing market tends not totake any point even where thecontract is strict onnotification. In the recent caseof HLB Kidsons v Lloyd’sUnderwriters Subscribing toLloyd’s Policy No621/PKID00101 [2007]EWHC 1951, the broker

delayed notifying thefollowing market by threemonths when the policyrequired notice ‘as soon aspracticable’. Whilst the Courtrecognised expert evidencethat it takes time fornotification of a claim to bemade, the kind of delaytolerated ‘…would normallybe measured in weeks or atmost ‘some months’.’

CUSTODIANS OF RECORDS– A COMMON LAW DUTY?Brokers have in the pastassumed the service role ascustodian of placing, claimsand premium accountingfiles for their subscriptionmarkets. Again, this raisesquestions of practicality. The London Market has thesedays established standardterms of business withbrokers which the Bermudianmarket might well choose toadopt. Absent such marketagreements, the common lawposition would guide asfollows:

The English decision ofEquitas Ltd & Anor. v HoraceHolman & Company Ltd.[2007] EWHC 903, suggestsa broker owes a duty to itsclient re/assured to:

(i) take reasonable care tomaintain proper andadequate records to allowclient re/assureds

(ii) to ascertain ‘the truestate of their account’; and

(iii) ‘preserve and beconstantly ready with correctaccounts of all its dealingsand transactions on behalf ofeach [client]’; and

SUBSCRIPTION MARKETCHAPTER 4

18 The Review • The Bermuda Legal Guide • 2009

SUBSCRIPTION MARKET

(iv) provide its clientre/assured with records in sofar as they relate totransactions done as its agent.Where records were keptmixed with records relating toother principals, the brokerwas responsible to provide therecords in such a way that theclient reassured could extractthe relevant from theirrelevant.

REVIEWING PLACEMENT DOCUMENTSIn Goshawk v Tyser [2006]EWCA Civ54 the Court ofAppeal considered that a termis to be implied intore/insurance policies thatplacing and claimsdocuments (held by thebroker, as agent of theassured) previously shown tounderwriters, together withpremium accountingdocuments necessary to theoperation of the contract,should be available tounderwriters in case of‘reasonable necessity’.

Reinsurance treaties whichcontain inspections of booksand records clauses (or whichare implied at law) includelegally recognised constraintsas to the volume of thedocuments are to be madeavailable for inspection. Suchconstraints can be overcomewhere co-subscribingreinsurers work together toeach inspect portions of thecedant’s book of businesspiecemeal.

Insistence by a cedant oneach inspecting reinsurersigning confidentiality

agreements, so as to preventcopies of inspecteddocuments being sharedamongst co-subscribingreinsurers, may or may notbe accepted/challenged asan unlawful variation of thebooks and records clause.

DISPUTESA reassured seekingrecoveries from a number ofco-subscribing reinsurers ona single layer will need theBermudian Court’spermission to consolidateeach (largely identical) set ofproceedings if time andmoney is to be saved. Wherethe risk’s wording contains anarbitration clause, unless allthe parties agree, eacharbitration will need to bepursued discretely (without aprecedent being establishedor an issue estoppel createdafter each set of proceedingsis concluded). Such amultiplication in effort may bea powerful incentive to forcea re/assured to compromise.

An efficiency saving of thesubscription market is that thefollowing market can partlybase its decision to co-subscribe on the basis that afair presentation has beenmade to the lead underwriterand so rely on the leader’sunderwriting judgement –that way, the broker short-circuit making a fullpresentation to eachfollowing underwriter.

The law is unclear as towhether a followingunderwriter can avoid apolicy for the same reasons

which the leader has. Recentcase law, however, suggeststhat it is itself a material non-disclosure to the followingmarket, by the re/assured,that the broker failed to makea fair presentation of the riskto the leader. The Court inScottish Coal Company Ltd &Ors v Royal and Sun AllianceInsurance Plc & Ors [2008]EWHC 880 indicated thatbefore a Court will permit thefollowing market to avoid,evidence of materiality andthe inducement of thefollowing market to write therisk is required, ie, therebeing no presumption of anentitlement to avoid in favourof the following market. Thisis arguably tacit judicialapproval of such a groundfor rescission.

IN LONDON’S FOOTSTEPS?Hamilton’s ‘HM11’ postcodeis similar in size to London’s‘EC3’, which may in itselfencourage the growth of aLondon-style subscriptionmarket – with brokersroutinely walking their filesbetween Bermudiana andReid streets. That does notmean Bermuda would becompelled or indeed want tofollow in London’s footstepsentirely but a cursory look athow the Courts have strivento rationalise abstruseLondon Market practicesuggests Bermuda would dowell to consider from theoutset how a modernsubscription market shouldbe characterised at a legallevel. ®

CHAPTER 4

The Review • The Bermuda Legal Guide • 2009 19

CAPTIVES

A ONE STOP SHOPBermuda continues to be theworld’s leading captivedomicile. In Profiling theBermuda Captive Market, DrMarcelo Ramella, assistantdirector of research at theBermuda Monetary Authority,provided a detailed analysisof Bermuda’s global positionin the captive insurancemarket. This shows thatBermuda’s captive marketexperienced a 28% growthbetween 2003 and 2005, withClasses 1 and 2 showing thesteepest growth, with 57%and 47% growth respectively.North American businesspredominates in Bermuda,with 74% of all Bermudacaptive risk coming from theUS in 2005. Global insurancerisks provide 14%, Europe 7%and other areas, 5%.

A key advantage ofestablishing a captive inBermuda is the access suchincorporation provides to thehighly developed Bermudareinsurance market. Bermudaprovides a ‘one-stop shop’, ascaptives have both excellentreinsurance andretrocessional support.Bermuda’s leading position inthe captive market is furtherenhanced by its facilitative butresponsible regulation.

The introduction of modernpublic segregated accountslegislation with theSegregated AccountsCompanies Act 2000 hasprovided sophisticated celltechnology, giving thosesmaller captives that cannotafford to establish a stand-

alone insurance company amore cost-effective option toparticipate in a segregatedaccount structure, at leastuntil their programmepremium volume reachesmore sustainable level.Bermuda pioneered theconcept of separate accountcompanies with Private Actlegislation but has introducedpublic cell legislation.

Bermuda also has a highlydeveloped infrastructure ofinsurance experts and serviceproviders including lawyers,

accountants and managers,which altogether serve tomaintain the jurisdiction’sstrong market position.

THE BERMUDA APPROACH Bermuda has always had a‘risk-based’ approachtowards the regulation of itsre/insurers, as regulatorsrecognise that a one-size-fits-all approach is not sensibleand that insurers will need to

adapt different corporategovernance needs dependingon the nature, complexity andrisk profile of its particularorganisation.

There are six ‘classes’ ofre/insurer, primarily classifiedby the type of risks insuredand ranging from a Class 1pure captive to a Class 4property catastrophereinsurer. Single-ownercaptives are established asClass 1 captives, while multi-owner captives may beestablished as Class 2captives. A Class 2 licensedinsurer may also write up to20% third party risk unrelatedto the owners of the insurancecompany or any affiliates ofthose owners or insure riskswhich arise out of thebusiness or operations of itsowners or their affiliates. TheAmendment Act hasredefined Class 3 insurers byreclassifying them into threesub-categories, 3, 3A, and3B. A captive would qualify as a Class 3 insurer if itsunrelated business is morethan 20% but less than 50%,Class 3A if its unrelatedbusiness exceeds or isexpected to exceed 50% ofnet premium written and/ornet loss and loss expenseprovisions, and where theunrelated business premiumdoes not, or is not projectedto exceed US$50m and Class3B where the captive’spercentage of unrelatedbusiness exceeds, or isprojected to exceed, 50% ofnet premium written and/ornet loss and loss expense

CHAPTER 5

The Review • The Bermuda Legal Guide • 2009 2120 The Review • The Bermuda Legal Guide • 2009

While Bermuda has evolved into a world-beating centre for property catastrophere/insurance, it has lost none of its attraction as a hub for captives, say Neil Horner and Natasha Scotland

Bermuda’sbedrock

Acaptive insurancecompany, in itspurest form, is an

insurance companyestablished as a subsidiaryof a non-insurance entityto insure the risks of itsparent entity and/or itsaffiliates. Bermuda hasbeen and continues to bethe world’s leading captiveand rent-a-captivedomicile since the captiveconcept was firstintroduced in Bermuda inthe 1960s.

ADVANTAGES OF CAPTIVESA captive can assist inavoiding commercialinsurers’ administrativeoverheads, allowing itsparent to retain incomethat would otherwise have

been lost in expenditure toa third party insuranceprovider.

Secondly, commonmarket practice withcommercial insuranceproviders is to havepremiums based on ageneral industry-widestandard as opposed toan individual company’sown risk. With a captive,premiums are fixed, basedupon the specific riskexperience of the captive’sparent and affiliates asopposed to the industry.

As a captive isincorporated to dealspecifically with the risksof its parent and affiliates,it can cater more preciselyto the specific insuranceneeds of its parent,allowing for a greater

degree of flexibility andcontrol over riskmanagement, asprograms can bespecifically designed todeal with a company’soperations.

Participation in a captive provides insula-tion against the vagariesof the commercial insur-ance market and canprovide breadth of coverage that is eitherunavailable or availableonly at excessive pricesfrom commercial insur-ers.

Finally, captives canaccess the reinsurancemarket and purchasereinsurance (wholesale)which is something thatcannot be obtained fromprimary insurers.

A key advantage ofestablishing a captive inBermuda is the access

such incorporationprovides to the highlydeveloped Bermudareinsurance market.Bermuda provides a‘one-stop shop’, ascaptives have both

excellent reinsuranceand retrocessional

support

ROD S. ATTRIDE-STIRLING, J.PSenior [email protected] Tel: 441 296 8314

BALA NADARAJAHSpecial Legal [email protected] Tel: 441 295 8104

KEHINDE A.L. GEORGEHead of [email protected] Tel: 441 296 8316

JAN W. WOLONIECKIHead of [email protected] Tel: 441 296 8315

NEIL HORNERHead of [email protected] Tel: 441 295 81460

FEDERICO [email protected] Tel: 441 294 0132

LOUISE [email protected] Tel: 441 295 1295

PETER [email protected] Tel: 441 295 5788

ALEX [email protected] Tel: 441 294 0135

VICTOR LYON, [email protected] Tel: 441 294 0134

MINA [email protected] Tel: 441 296 0356

LARRY [email protected] Tel: 441 296 8317

NATASHA [email protected] Tel: 441 294 0136

EVERARD BARCLAY [email protected] Tel: 441 295 1652

SHADE [email protected] Tel: 441 295 9159

NATHANIEL A. [email protected] Tel: 441 296 6650

SUSIE [email protected] Tel: 441 294 0134

CONTACTS

The Review • The Bermuda Legal Guide • 2009 23

provisions, and where theunrelated business premiumdoes exceed or is projected toexceed US$50m. Class 4 arethe highly capitalisedcommercial insurers whosecoverage must include excessliability business and/orproperty catastrophereinsurance business.

In accordance with the risk-based approach, Bermudaadopts a graduated scale ofregulation – Class 1 captivesare subject to the lowest levelof regulation and Class 4commercial insurers to thehighest.

A further important facet ofthe Bermuda landscape is thata Bermuda insurer must havea Bermuda-based ‘principalrepresentative’, who hascertain statutoryresponsibilities to theBermuda Monetary Authority(BMA) to ensure that theinsurer continues at all timesto meet its solvency marginand other responsibilitiesunder the Insurance Act.

THE APPLICATION PROCESSThe application to form aBermuda captive is made onprescribed forms to the BMAInsurance Division by 5pmeach Monday. The so-calledpre-incorporation form setsout, amongst other things, thecapitalisation of the proposedinsurer, the category ofinsurance business the insurerproposes to write, theproposed class the insurer willhave, the estimated financials,levels of risk retention anddetails of any proposed

reinsurance. It also sets outthe insurer’s principalrepresentative, insurancemanager, approved auditor,loss reserve specialist, this isnot required for Class 1companies. In addition, theapplication must contain abusiness plan explaining thebusiness case for theBermuda captive. Projectedpro-forma financials shouldalso be included (ideally, fora five-year period). It wouldalso be very helpful ifactuarial analysis can beincluded substantiating theproposed premium levels,adequacy of reserves, andgenerally the pro formafinancials.

Applications to form a newinsurer are heard at theweekly Friday meeting of theAssessment and LicensingCommittee (ALC). The ALC ismade up completely ofemployees from BMA.Members of the TechnicalAdvisory Group (TAG),consisting of experiencedinsurance professionals,actuaries and accountants,may be invited to meetings ofthe ALC, which will generallyhappen in the case of Class2, 3, 3A, 3B and 4applications.

The ALC/TAG may at itsweekly Friday meeting,recommend to the BMA toapprove the applicationunconditionally or subject toconditions (which may be setout in the licence), defer theapplication pendingclarification of certainmatters, or reject the

application if it considers thebusiness case simply cannotbe substantiated. Once BMAapproval has beenobtained, it is then possibleto organise the captive andapply for the insurancelicence. The captive must befully capitalised before thelicence application is made.The application will be madeby the attorneys submittingthe so-called Form 1B (whicheffectively mirrors the pre-incorporation form) togetherwith payment of theappropriate licensing fee(which is on a graduatedbasis depending on theproposed class of theinsurer). The licence willgenerally have the date ofthe licence application as theeffective date of registration,and as of the registration,the Bermuda captive will belicensed to conductinsurance business of thetype depending on itsclassification.

HIGHLY VALUEDThe captive remains thebedrock of the Bermudainsurance industry alongsideBermuda’s highly developedand capitalised propertycatastrophe reinsuranceindustry. Bermuda values itscaptive insurance clientshighly and continues toprovide an efficient, credibleand facilitative infrastructurefor the growth of the captiveindustry and themaintenance of its pre-eminent role as the world’sleading captive domicile. ®

CAPTIVESCHAPTER 5

22 The Review • The Bermuda Legal Guide • 2009

ATTRIDE-STIRLING & WOLONIECKICrawford House, 50 Cedar AvenueHamilton HM 11, Bermuda

OR

P.O. Box HM 2879, Hamilton HM LX, BermudaTel: (001) 441 295 6500, Fax: 441 295 6566E-mail: [email protected], Web: www.aswlaw.com

IN ASSOCIATION WITH