Embed Size (px)

Citation preview

The 2021 Reilly Report

Letter From the President . . . . . . . . . . . . . . . . .

Tales of Working Remotely . . . . . . . . . . . . . . . . .

Home Workspaces . . . . . . . . . . . . . . . . . . . .

Volunteer Day at the San Diego Food Bank . . . . . . . . .

Meet Our Corporate Retirement Services Team . . . . . . .

Meet Our Investment Committee . . . . . . . . . . . . . .

2020 Year in Review and 2021 Outlook . . . . . . . .

Barron’s in Education Partnership . . . . . . . . . . . . .

Furry and Feathered Friends . . . . . . . . . . . . . . . .

Staff Volunteer Spotlight . . . . . . . . . . . . . . . . .

A Virtual Tour of Our Newport Beach Office . . . . . . . . .

San Diego Office Expansion . . . . . . . . . . . . . . . .

Congratulations to Sonja Larimore, J.D., IACCP®, AIF® . . . . .

New Hires . . . . . . . . . . . . . . . . . . . . . . . .

New Arrival . . . . . . . . . . . . . . . . . . . . . . . .

Christmas Party Cooking Class . . . . . . . . . . . . . . .

Key Numbers for 2021 . . . . . . . . . . . . . . . . . .

Lisa Goodman’s Grandmother Is 100! . . . . . . . . . . .

3

4–5

6–7

8–9

10–11

12–15

16–28

29

30–31

32–33

34–35

36–37

38–39

40–42

43

44–45

46–47

48

The 2021 Reilly Report

In January 2020, I was thrilled about the San Diego office’s pending expansion to the second floor and looking forward to the additional growth opportunities that stood before us. I had no idea what was waiting for us—and the world—a couple of months down the road.

March brought the coronavirus market downturn, which saw the fastest fall in global stock markets in financial history. It was then that we also had to close our offices and send our employees to work from home. However, we were more prepared than many.

We were fortunate to have had many of the technological solutions needed to work from home in place long before the pandemic struck. We remain so grateful to our employees and IT team, who made the transition to working from home as smooth as it could have been. I never expected the transition to be seamless, and I appreciate our employees for being so understanding as we worked through the kinks together.

I’m also very grateful to you, our clients, for understanding that we are living in trying times; your patience and flexibility have made our transitions that much easier. While working from home isn’t always ideal, throughout the entire pandemic we have remained able to take care of you and your needs without fail—an accomplishment I’m proud of.

In the aftermath of the coronavirus market downturn, some advisors chose to lay low. We at RFA took the opposite approach, stepping up our communication to make sure you stayed well informed about the actions we were taking to upgrade your portfolios. It’s an amazing testament to your strength, willpower, and confidence in RFA that you did not let fear determine your actions but rather stayed the course. Now, less than a year later, you have already seen your determination pay off.

Since March 2020, RFA has closed, reopened, and repeated the process. And despite several close calls with COVID-19, we were lucky to have all but two employees, who have now made full recoveries, avoid the virus. Just like the stock market, things here, too, have gone up and down. Through it all, I have remained full of gratitude for our wonderful clients, staff, and support teams as well as RFA’s ability to continue serving you in the best possible manner.

I know I, for one, am certainly hopeful for a prosperous and less eventful 2021. I am very much anticipating the widespread use of proven COVID-19 vaccines and our communities fully opening back up. I am looking forward to the days when all RFA staff can return to their desks and once again engage in the holiday celebrations and team building events we so enjoy hosting (as well as the daily interactions that make our workplace so special). And I of course cannot wait until we can once again welcome you into our offices with fresh-baked chocolate chip cookies and a hot cup of coffee.

It is my wish to be able to see many of you in person in 2021.

Warm regards,

Frank ReillyPresident and Co-Founder

3

Tales of Working RemotelyAll RFA team members found themselves working from home for a portion of 2020, often sharing their space with spouses or children. These are some of their stories.

“When the first stay-at-home order was announced, my adult children decided to move back in with me. Everyone was working from home simultaneously, and the house felt like a shared workspace venue. Whenever I would try to use the restroom, I would find someone else waiting ahead of me and had to join the line.”

- Taher Ali, Head Research Analyst/Portfolio Manager

“For me, one positive thing to come out of the stay-at-home orders was a reduced commute time.”

- Curtis West, Senior Wealth Advisor

“My wife and I were both working from home, and I quickly learned that she prefers to make all her calls on speaker phone.”

- Andrew Ferrette, Senior Wealth Advisor

“While working from home, my wife and I started taking morning walks around the neighborhood before we began work for the day. We have continued this tradition even though I am now back in the office.”

- Dean Peabody, Managing Director – Trading

4

“My favorite part about working from home was comfortable attire for the whole family—RFA T-shirts and cozy socks! Here’s my daughter, Evelyn, modeling the look.”

- Gabrielle Reilly, Senior Wealth Advisor

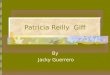

“I use a virtual background when on Zoom meetings, and during one particular meeting Frank had noticed me periodically touching my shoulder. Near the end of the meeting, I touched my shoulder again and produced a brightly colored bird, as if by magic—and Frank did a double take. My bird had been completely obscured to everyone in the meeting up until that point.”

- Jennifer Arganbright, Marketing Manager

“My most memorable experience working from home was shooting the RFA Weekly Market Update using my iPhone 7, with my daughter acting as camerawoman, and then emailing the video to the editor.”

-Tom Weary, Chief Investment Officer

“When our office first transitioned to working from home, our daughter was just turning five months old. In many ways, working from home was an incredible blessing; my wife and I saw our daughter roll over, crawl, stand, and take her first steps—something we may not have been able to experience in a “normal year.” That said, I may owe a few clients an apology if you heard her crying in the background during one of our meetings!”

- Bradley Johnston, Senior Wealth Advisor

“I had to get special headphones in order to be able to take phone calls from home, because my wife and I were working 15 feet from each other in a one-bedroom apartment and constantly talking over one another.”

- Jason Brothers, Securities Trader

“Working from home while having five- and seven-year-old boys at home in a virtual learning environment comes with many challenges. However, one instance I never expected to happen occurred during an all-staff meeting. We were at a rather serious moment in the meeting when my office door suddenly burst open, and in marched two young lads clad only in their Spider-Man and Star Wars underwear, respectively. There was no hiding it; regardless of where I moved my head, the duo would not be blocked. The mood in the meeting lightened, and many burst into laughter. While my cheeks reddened, I was glad the team could finally understand exactly what my days were filled with. Lesson learned: lock the office door!”

- Christina Dodge, Chief Operating Officer

5

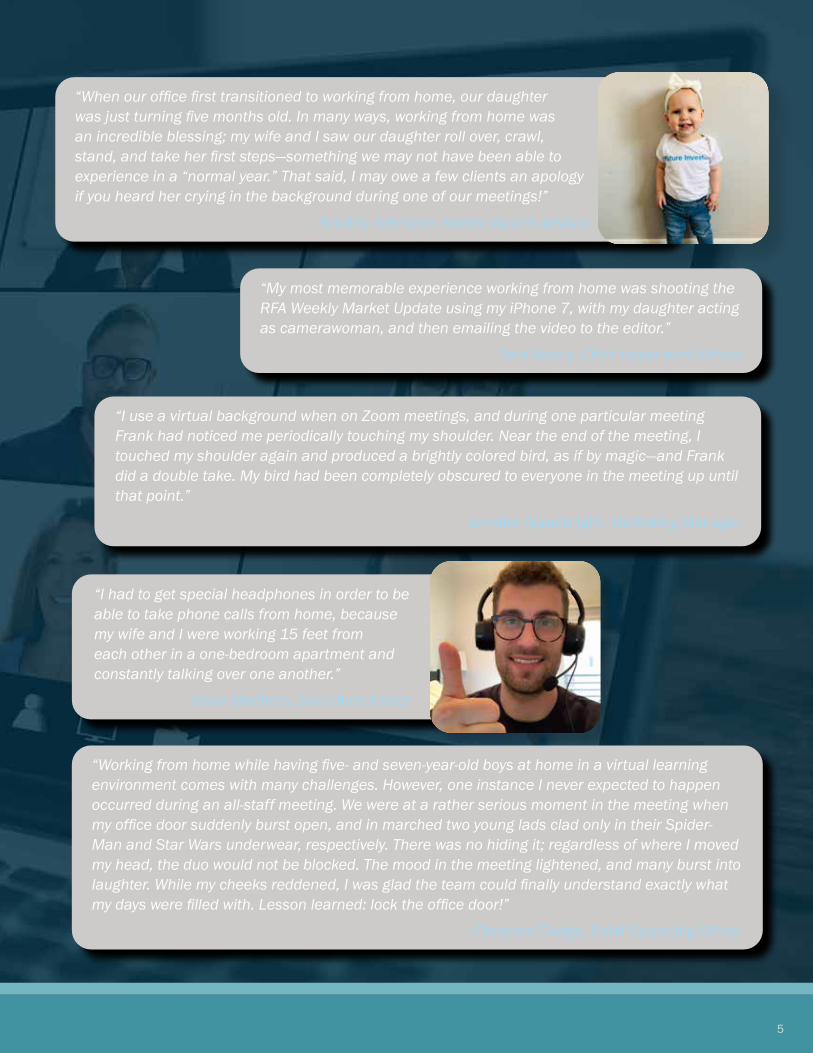

When the RFA team was working from home last year, many had to make do with unconventional workspaces (at least until the proper equipment arrived). Here’s a peek at some of the workspaces people set up in their homes.

Special thanks go to Senior Wealth Advisor Bradley Johnston for modeling RFA’s strict work-from-home dress code.

6

Home Workspaces

7

8

With all that’s going on in the world today, families are experiencing food insecurity more than ever before. Knowing this, we wanted to do what we could to give back.

We began by organizing an RFA volunteer day at the San Diego Food Bank (after checking to make sure that adequate safety protocols were in place). Then, after coming to better understand just how much families across San Diego county were struggling, we decided that we could do more.

At RFA, we don’t just talk the talk—we walk the walk. That’s why in 2020 we opted to make a significant cash donation to the San Diego Food Bank. Through this singular donation, we were able to provide 180,000 meals to families in need.

Here are some photos from RFA’s volunteer day at the San Diego Food Bank, where firm employees worked together to bag 8,300 lbs. of produce and sort 1,600 lbs. of rice.

Volunteer Day at theSan Diego Food Bank

9

10

What CRS Does for Plan Sponsors

For sponsors (companies) just starting to offer a retirement plan, CRS can craft an intelligent plan from scratch. And for those sponsors in search of ways to better the plan they currently operate, CRS aims to reduce fees dramatically while adding more efficient investments and additional services for all employees. Beyond this, the CRS team helps the sponsor on an ongoing basis in two key ways: by acting as an extension of the sponsor’s human resources department, eliminating most of the work associated with the company retirement plan, and by acting as fiduciary, thus limiting sponsor liability.

What CRS Does for Plan Participants

CRS currently serves more than 6,000 participants, which is no small feat considering the tremendous amount of support and resources it provides. In addition to contacting each plan participant at least once per year to check in, CRS also provides education to plan participants through onsite lunches (when possible) or Zoom presentations, hosts one-on-one meetings with current and prospective plan participants, and delivers a quarterly investment newsletter penned by RFA CIO Tom Weary, CFA®.

Most importantly, CRS offers personalized financial planning to employees at no cost while providing them with access to professionally managed portfolios and institutionally priced mutual funds.

In our last Reilly Report, we talked about how RFA’s Corporate Retirement Services (CRS) team came to be. This year we would like to delve deeper, sharing a bit more detail about what the team does and the employees who form it.

The main goals of RFA’s CRS division are to design and implement efficient retirement plans and provide services that have historically not been offered. Read on to learn how the CRS team works to help sponsors and participants alike.

Meet Our CorporateRetirement Services Team

11

Damian DufourCRPS®, CPFA

Director – Retirement Services

Scott MartineauVice President

Plan Management

Jackson MillerCRPS, AIF®

Retirement Plan Specialist II

Christian ReillyParticipant Specialist I

Here are just some of the CRS team’s many success stories:

• A plan participant had asked us to review the cost of an investment product outside of her company’s retirement plan; upon review, we found that the fees were much higher than the industry average. At the participant’s request, we were able to help transfer her funds into a significantly lower cost solution, saving her substantial money through reduced fees.

• We had one plan sponsor where only 120 out of their 400 employees were contributing to the plan; after turning on an auto-enrollment feature, we were able to increase participation to 300 of 400 employees.

• Some plans have a significant amount of employee assets sitting in cash, meaning they are typically earning less than 1%. Time and again we have helped reduce those cash positions to get more employees into higher growth allocations and increase their probability of success in retirement.

• One plan sponsor came to us paying annual fees of $112,000, which we were able to reduce to only $37,000 while also raising the quality of the portfolio.

If you know a plan sponsor who may be able to benefit from RFA’s corporate retirement services, we would be happy to provide them with a free analysis of their current plan to assess how we can be of service.

At Reilly Financial Advisors, we believe that no one person is truly able to successfully manage your money. Just as governments thrive on a checks and balances system, so do successful investment managers. That’s why we rely on the expertise of our Investment Committee, a team of tenured professionals who meet regularly to develop ideas, analyze portfolio holdings, and discuss the impact that economic trends, both stateside and global, will have on our portfolios. Each team member’s diverse understanding allows us a unique opportunity to formulate strategies that enhance our portfolios. Additionally, our international experience—including living, working, and having offices abroad—allows us global macroeconomic insight on how world events may impact portfolio positions. This combined knowledge provides the groundwork for the portfolios we create to help our clients navigate a path to successful retirement.

If you haven’t done so already, we invite you to learn more about the team that makes up RFA’s Investment Committee.

Meet Our Investment Committee

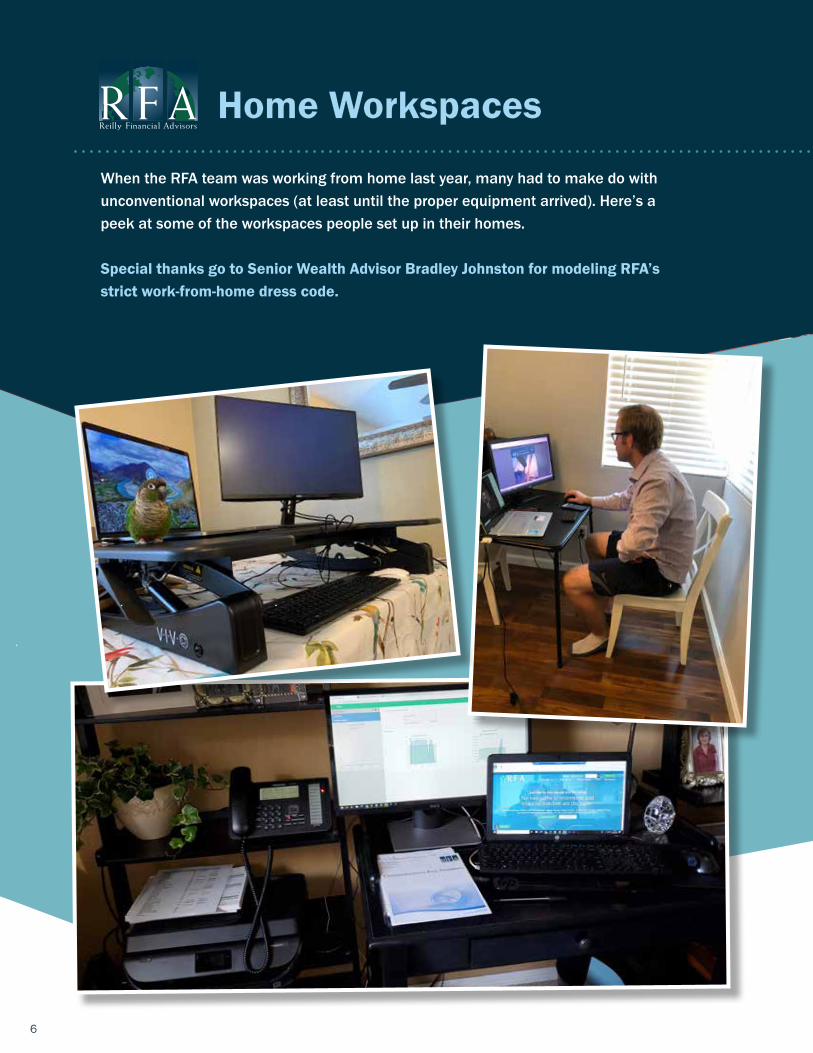

Tom Weary, CFA®

Chief Investment Officer

As Reilly Financial Advisors’ Chief Investment Officer, Tom is co-chair of the Investment Committee and leads the Research Department in building and managing all client portfolios in adherence to the firm’s rigorous investment discipline. Tom’s broad experience, varied background, and unique perspective on investing have all helped him to excel in this role.

With more than three decades of investment experience, through several market cycles, Tom has experience managing portfolios for mutual funds, pension plans, insurance

company reserves, and high-net-worth families.

Tom graduated from Harvard University with an honors degree in Philosophy and attained the Chartered Financial Analyst® designation in 1993.

In 1996, Tom was recruited by a large insurance provider to lead their Equity Department, where he led a spin-out of Investment Operations into a stand-alone institutional investment management firm. There, Tom oversaw a team of 12 analysts and portfolio managers as well as $3.4 billion in stocks.

Tom then spent most of the next decade building a small advisory firm focused on high-quality large cap stocks that combined traditional financial analysis and a proprietary qualitative assessment tool that examined corporate culture.

Before joining Reilly Financial Advisors, Tom was the Chief Investment Officer of a family office unit of a large trust company.

Dan Seiver, Ph.D.Chief Economist

Dan earned his bachelor’s degree, master’s degree, and Ph.D.—all in economics—from Yale University. As Reilly Financial Advisors’ Chief Economist and a member of the firm’s Investment Committee, he enhances the firm’s global macroeconomic approach and outlook, ensuring that all portfolios are managed within context of the global economy.

Dan has published his research in The Journal of Wealth Management and is a member of the Economics faculty at Cal Poly, San Luis Obispo, where he has taught Introductory Economics, Money and Banking, and Intermediate Macroeconomic Theory.

From 2005 to 2013, Dan was on the Finance faculty at San Diego State University (SDSU), where he taught International Business Finance, Investments, Personal Finance, and Managerial Economics. While at SDSU, Dan received the Finance Teaching Award in 2007 and the International Business Teaching Award in 2011.

Prior to that, from 1978 to 2005, Dan was a Professor of Economics at Miami University (Ohio), where he taught ten different courses in economics and had more than 20 refereed publications in professional journals.

Dan has coauthored an MIT Press book on regional economic policy and a Probus/McGraw-Hill book on investment strategy. Additionally, he was a consultant to the Center for Naval Analyses and an investment adviser to the Population Association of America for many years.

13

Frank Reilly, MIBACo-Founder and President

As co-chair of Reilly Financial Advisors’ Investment Committee, Frank remains squarely focused on reducing risk within the firm’s variety of portfolios.

As the President of Reilly Financial Advisors, Frank oversees all aspects for the firm, including day-to-day operations, strategic alliances, and joint ventures. He also works to develop new services and represents the firm internationally.

Frank’s immersion in international business has served as the foundation for the firm’s global approach. Prior to co-founding Reilly Financial Advisors, Frank worked in multiple roles at a large San Diego-based investment advisory firm. There, he researched and negotiated several international alliance contracts with multiple countries and was an integral member of the team that began an international institutional money management firm that still exists today. Frank has attended investment and economic symposiums internationally and traveled for business to Europe, Africa, the Middle East, India, and the Far East, including 16 around-the-world and 20 intercontinental trips.

Frank holds a bachelor’s degree and a master’s degree in international business from United States International University and has earned the FINRA Series 4, 7, 24, 63, and 65 licenses.

Frank’s professional and personal experiences traveling and conducting business around the world, combined with his advanced education in international business, have shaped his real-world perspective, guide firm reactions to world events, and help him to position portfolios to the benefit of the firm’s clients.

Don ReillyCo-Founder and Chairman Emeritus

Don Reilly began his career in residential real estate in the late 1960s. Shortly thereafter, he joined a well-known real estate firm. There, he rose through the ranks to become the youngest President of Regional Franchisees the company had ever had. After branching out and transitioning from residential real estate to investment properties, Don became the Managing Director of 30+ partnerships, specializing in both real estate and land trustees in California, Arizona, and Texas.

When clients Don had acquired began asking for more than just real estate in the 1980s, Don founded his own broker-dealer in order to begin offering a wider slate of investments. In 1990, Don joined a large San Diego-based advisory firm, where he quickly became a member of the elite Chairman’s Club (which he remained a member of for all nine years of his employ).

Don co-founded Reilly Financial Advisors in 1999 after deciding that becoming independent was the only way to give truly unbiased advice, provide truly great client service, and fully embrace the fiduciary standard. He wanted to do things his way, which, among many other things, meant no packaged funds and dealing in individual stocks and bonds.

Today, Don has more than 40 years of experience providing comprehensive financial solutions and investment management advice to a broad base of international clients. In his role as chief mentor to the Investment Committee, Don is proud to ensure that every investment decision the committee makes is made with the best interests of all clients in mind.

Don has earned the FINRA Series 1, 3, 7, 24, 26, 39, 63, and 65 licenses.

14

Jason BrothersSecurities Trader

In his role as a Securities Trader, Jason works closely with the Managing Director of Trading to implement the firm’s investment strategies by purchasing and selling securities and rebalancing client portfolios.

Jason received his bachelor’s degree in business economics from the University of California, Irvine, and his dual master’s degree in business administration and finance from the University of San Diego. He has also passed the CFA Level 1 exam.

Dean PeabodyManaging Director of Trading

Dean oversees the operational aspects of the firm’s portfolio management software as well as day-to-day transactional procedures, working hand-in-hand with RFA custodians. Additionally, Dean works closely with the rest of Reilly Financial Advisors’ Investment Committee on stock selection, retention, and purchasing to ensure that client portfolios adhere to the firm’s 20-point inspection process and investment philosophy. He is also a sitting member of the Executive Committee.

Dean joined the Reilly family business in 1994 and has earned the FINRA Series 7 and 63 licenses.

Taher AliHead Research Analyst/Portfolio Manager

In his role as Head Research Analyst/Portfolio Manager, and as an acting member of the Investment Committee, Taher is responsible for the execution of Reilly Financial Advisors’ proprietary investment discipline and daily monitoring of the firm’s portfolio holdings.

Taher’s industry experience spans nearly 25 years. Prior to joining Reilly Financial Advisors, he worked for 15 years as an analyst and portfolio manager for the investment division of the Saudi French Bank. Taher attended California State Polytechnic University, Pomona.

How the Pandemic Affected Our Investment CommitteeWith markets as fluid as they were in mid-March, when the pandemic first locked down the country, our Investment Committee began meeting every day, working to make changes that would enhance the long-term performance of client portfolios and allow clients to leave the bull market with stronger, higher-quality portfolios of great companies than they owned coming in to it. In recent months, the Investment Committee has gone back to its regular schedule, holding meetings via Zoom.

15

2020 Year in Review and 2021 Outlook

The 2021 Reilly Report

17

2020 Year in Review and 2021 Outlook

2020 Review2020 was a year like no other, both for financial markets and the economy. The stock market started the year in what turned out to be the last days of the longest bull market in history. The end was sudden, as a fierce but brief bear market drove stocks down sharply. By May, a brand new and powerful bull market had begun, and it lasted right through the end of a truly dramatic year. The economy also peaked early in the year, then fell into a very deep recession, and finally began a recovery that, unlike stocks, was losing steam by the end of the year.

The simple explanation for the economic and financial turmoil was COVID-19. But the full cast of characters in this drama includes the Federal Reserve (Fed), Congress, the president, and a worldwide scientific effort to uncover

the virus’s tricks of replication and transmission and thus find a “magic bullet” vaccine to conquer the pandemic. Reviewing the roles of the major players and each one’s detailed effects on the economy and financial markets will help us to outline the shape of things to come in 2021.

The Fed, which during the Great Recession learned the importance of coming at a crisis hard and fast, began reducing short-term interest rates in March as the economy and stock market each began a free fall. By the end of March, the Fed funds rate was effectively zero (Fig. 1), and the Fed intensified its unconventional monetary policy, buying trillions of dollars of long-term government securities as well as municipal and corporate bonds (Fig. 2). In addition, the Fed provided the liquidity necessary to keep all financial markets functioning.

The required reserve ratio was also reduced to zero, freeing up even more funds for bank lending. In addition, the CARES Act created new lending programs to channel

The Economy

Dr. Dan Seiver, Ph.D.Chief Economist

Fed Funds RateFig. 1

Federal Reserve Total Assets

18

2020 Year in Review and 2021 Outlook

credit lifelines to smaller businesses. Although the Fed’s main concern was to keep the recession from turning into a full-blown depression, it also had the side effect of stopping the stock market decline in its tracks and fueling a new bull market, as stock traders love easy money. By the end of the year, the Federal Open Market Committee was still promising to keep the “pedal to the metal,” as the economic recovery was stalling out at levels well below the peak at the start of the year.

Some credit must also go to Congress and the president, as expansionary fiscal policy was hurriedly enacted to put spendable funds directly in the hands of most Americans—especially the millions of newly unemployed (Fig. 3). These extra trillions, which Uncle Sam could borrow at near-zero interest rates, cushioned the blow of the virus-induced economic shutdown and prevented the economic collapse from feeding on itself in a vicious circle. Sure enough, a truly horrendous decline in second quarter GDP was followed by a massive recovery in the third quarter (Fig. 4). However, the cessation of some of the provisions of the CARES Act and a resurgence of the virus later in the year began to weaken the economy once again as lockdown orders began spreading across the U.S.

While the economy and stock market were on a roller-coaster ride, the scientific community moved steadily forward, fully decoding the SARS-CoV-2 virus and pinning down the key modes of replication (the spike protein) and transmission (aerosols, especially indoors). By the end of the year, even though infections in most countries, including the U.S., had reached new highs (Fig. 5), two highly efficacious vaccines were in the early stages of distribution in many countries. Never before had the worldwide scientific community achieved so much in such a short period of time, and even more vaccines in the research and testing pipeline remain likely to be approved early in 2021.

The pandemic was truly worldwide, sparing no nation or continent. At the end of 2020, as a powerful new wave of the virus spread around the world, even Antarctica reported its first infections. The few exceptions to this pattern were noteworthy: China, where the virus started, executed draconian lockdowns that stopped the viral spread and allowed economic activity to resume while most of the world was still losing the battle with the highly contagious pathogen. For China, this meant that economic growth could resume in the second quarter of the year,

Fig. 2

19

2020 Year in Review and 2021 Outlook

Unemployment RateFig. 3

Real Gross Domestic Product (GDP)Fig. 4

Source: FRED®, Federal Reserve Bank of St. Louis

20

2020 Year in Review and 2021 Outlook

when most of the world was mired in recession. Chinese stocks also rallied sooner than those of the rest of the world, although the Shanghai Composite gained no ground after early July as U.S.-Chinese economic and political tensions rose steadily. These tensions may not be reduced by the Biden administration, which may have concluded that a cold war with China, centering on technology and human rights, is inevitable.

Taiwan was another pandemic exception: the island nation of 24 million has recorded a total of 776 cases and seven deaths. Near-universal masking, distancing, testing, and contact tracing were the keys. As a result, Taiwan’s economy should grow 2.2% for the year while most of the world’s economies will show substantial declines. This growth rate may even exceed mainland China’s, which is forecasted to grow at 2% for 2020. Not surprisingly, Taiwan’s stock market rallied 65% from its early March low to an all-time high in December.

Japan’s economy was already in recession when the virus arrived, and a collapse in exports will mean two

straight years of economic decline for a country that has had stagnant growth for decades. The good news is that Japan’s economic growth for fiscal 2021 (starting in March) is projected to be 3.5%–4%, which would be the highest since the collapse of its real estate and stock market bubble in 1990. The Japanese government has continued to press on the fiscal accelerator even though Japan’s debt-to-GDP ratio is by far the highest among rich countries. Japan’s expansionary monetary policy has kept short-term rates below zero for years, while the Japanese 10-year bond in December yielded almost exactly zero in spite of Japan’s fiscal imbalance. Japanese stock traders love easy money as much as American stock traders; in 2020, the Nikkei 225 index rose more than 60% from its March low, reaching its highest level in 30 years in December.

Europe was another story. The virus repeatedly devastated much of the continent, with most governments adopting more and more draconian policies to stem the late-year new wave of infections. The British may have suffered the most, with a new mutation apparently leading to an

COVID-19 Confirmed CasesFig. 5

21

2020 Year in Review and 2021 Outlook

even more potent transmission of the virus. Under a new Tier 4 lockdown policy in effect for much of the country in December, all nonessential businesses had to close, and people could not meet with others indoors unless they lived with them or were part of their support bubble. These policies were forecasted to cause a double-dip recession in Britain that may only be ended by the wide distribution of vaccines. British stocks ended the year down almost 15% from their early 2020 peak, although a last-minute breakthrough in Brexit negotiations may prevent even greater economic and financial weakness in 2021.

The picture was similar in the rest of Europe. Even the Swedes, who appeared to have a superior model for dealing with the virus, saw explosive growth in cases since November. The French responded to a fall surge in cases with another national lockdown in November. A continued surge in cases in Germany led the government to impose a full lockdown in December. The European economy’s recovery will thus be weaker, in spite of extremely easy money and expansionary fiscal policy. European stocks, as measured by the STOXX Europe 600 index, reflected this tug-of-war between economic weakness and easy money. Although major European stocks were up 40% from their March low by the end of the year, they still remained about 10% below their early-2020 highs. As in the U.S., Europeans continued to await the widespread distribution of vaccines in 2021, which will be key to the resumption of economic growth.

2021 OutlookFour key factors will again determine the path of the economy and stock market in 2021 and beyond: monetary policy, fiscal policy, the virus, and the scientific assault on this deadly pathogen.

The outlook for monetary policy is the clearest: the Fed has repeatedly stated that it will keep short-term rates near zero for many months and continue to buy vast

quantities of other securities to keep other interest rates very low. The Fed has specifically asked Congress and the president for additional help, as the synergy of expansionary monetary and fiscal policy provides an even more powerful impetus to a recovering economy. The expiration of some lending and assistance programs in late 2020, which was accompanied by a significant slowdown in economic activity, underlines the importance of this cooperative effort for 2021.

Unfortunately, the outlook for fiscal policy is much less clear. At the end of 2020, President Trump vetoed a major defense bill and threatened a veto of a $900 billion new spending bill that was a hard-fought bipartisan compromise among House Democrats, Senate Republicans, and the incoming Biden administration. The spending bill was ultimately passed, and Congress overrode President Trump’s military veto. As of this writing, Congress was still considering larger stimulus payments and two early January runoff elections in Georgia were set to determine control of an evenly divided Senate in 2021. Murkier still is the prospect for further bipartisan cooperation on any of Biden’s key initiatives that Republicans might be willing to support, such as a trillion-dollar down payment on long-overdue repairs to our crumbling infrastructure of roads, highways, bridges, ports, airports, and Internet connectivity. As an example, U.S. broadband Internet speed ranks eleventh in the world, below Hungary and Romania.

The first months of 2021 will be grim ones in the battle against the coronavirus. Americans traveling and gathering for the Christmas season could drive a new and even greater wave of infections, hospitalizations, and deaths before vaccines can be widely distributed. Many hospitals are reaching, or passing, limits on beds and facilities, which will mean even less availability for severe non-COVID illnesses. The necessity for further lockdowns, combined with the absence of new fiscal initiatives, could push the U.S. economy back into recession in the first quarter. But the second and subsequent quarters should

22

2020 Year in Review and 2021 Outlook

be much stronger as the mass of vaccines begins to spread immunity widely enough to break the back of virus transmission.

While the recovery should gain strength in 2021, it will not be evenly spread across industries or regions, nor will it return the U.S. to the pre-virus status quo. The economic evidence from 2020’s collapse and recovery is instructive: while the goods portion of the economy more than fully recovered in the third quarter of the year, the services portion, which includes many sectors that require face-to-face interactions, fell faster and recovered much more slowly (Fig. 6).

This K-shape pattern could persist through 2021, reflecting long-term underlying changes in the economy that economists call hysteresis. In simple terms, this means that some economic sectors, such as brick-and-mortar retail, travel and leisure, medicine, and even the market for office space, may be permanently downsized

as more and more activity and work moves online. Regions and cities that concentrate on technology, science, and goods production may grow faster than areas and industries more reliant on activities like travel and tourism.

Also benefitting are sectors that are interest-rate sensitive, like housing (which recovered dramatically in 2020, with housing starts strong (Fig. 7) and home prices soaring in supply-constrained parts of the country). Record-low mortgage interest rates fueled a rising tide of refinances, new home purchases, and remodelings, which then stimulated all housing-related sectors of the economy. On the other hand, the banking sector continues to lag, as ultra-low interest rates and rising loan losses impact profitability.

Depending on how much cooperation can be achieved among President-elect Biden, House Democrats, and Senate Republicans, the U.S. could also take some

Personal Consumption ExpendituresFig. 6

Goods Services

23

2020 Year in Review and 2021 Outlook

Monthly Housing StartsFig. 7

tentative steps toward the mitigation of climate change. The transition away from fossil fuels could pick up speed in 2021, even if economists’ favorite tool, a revenue-neutral carbon tax, is a political non-starter. It may also become politically feasible to restrengthen trading relationships with our allies in North America, Europe, and Asia. An expansion of trade and reduction of trade barriers will benefit all nations.

The overall economic outlook for the U.S. can then be characterized as a few months of stormy weather followed by clearing skies as the virus retreats, with the sun shining more brightly in some areas than others.

The past year was truly one for the history books, with record numbers of wildfires in the West, named hurricanes in the East, protests in the streets globally, and voters in the November U.S. elections. All that in a year when a global pandemic has infected more than 80 million people, killing nearly 2 million so far, even as governments around the world imposed draconian measures to halt the spread of the

coronavirus, shutting the global economy almost overnight and causing stock markets everywhere to plummet.

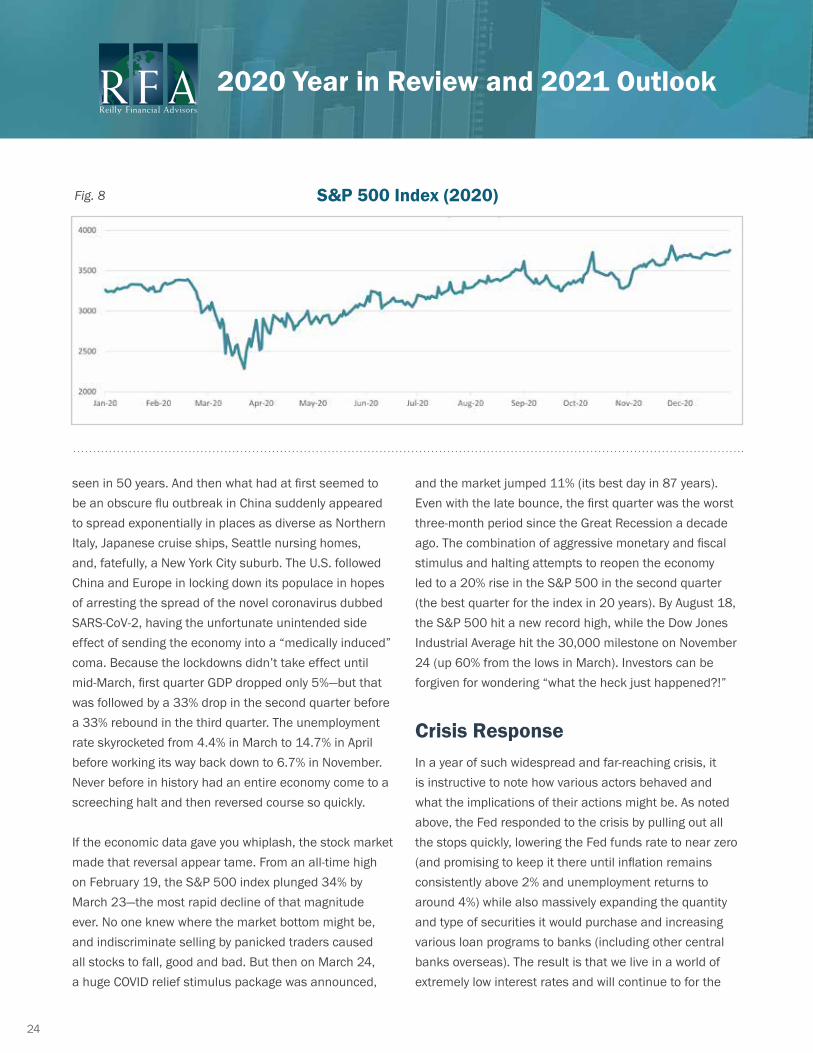

Figure 8 illustrates the maxim that “the market takes the elevator down and the escalator back up,” as stocks fell off a cliff before climbing back to reach new record highs recently. The economy and financial markets were so extremely tumultuous in 2020 that it is difficult to comprehend the violence of the reversals we experienced. As 2020 began, we were enjoying an economic expansion of record length with unemployment reaching lows not

Tom Weary, CFA®

Chief Investment Officer

Financial Markets

24

2020 Year in Review and 2021 Outlook

S&P 500 Index (2020)Fig. 8

seen in 50 years. And then what had at first seemed to be an obscure flu outbreak in China suddenly appeared to spread exponentially in places as diverse as Northern Italy, Japanese cruise ships, Seattle nursing homes, and, fatefully, a New York City suburb. The U.S. followed China and Europe in locking down its populace in hopes of arresting the spread of the novel coronavirus dubbed SARS-CoV-2, having the unfortunate unintended side effect of sending the economy into a “medically induced” coma. Because the lockdowns didn’t take effect until mid-March, first quarter GDP dropped only 5%—but that was followed by a 33% drop in the second quarter before a 33% rebound in the third quarter. The unemployment rate skyrocketed from 4.4% in March to 14.7% in April before working its way back down to 6.7% in November. Never before in history had an entire economy come to a screeching halt and then reversed course so quickly.

If the economic data gave you whiplash, the stock market made that reversal appear tame. From an all-time high on February 19, the S&P 500 index plunged 34% by March 23—the most rapid decline of that magnitude ever. No one knew where the market bottom might be, and indiscriminate selling by panicked traders caused all stocks to fall, good and bad. But then on March 24, a huge COVID relief stimulus package was announced,

and the market jumped 11% (its best day in 87 years). Even with the late bounce, the first quarter was the worst three-month period since the Great Recession a decade ago. The combination of aggressive monetary and fiscal stimulus and halting attempts to reopen the economy led to a 20% rise in the S&P 500 in the second quarter (the best quarter for the index in 20 years). By August 18, the S&P 500 hit a new record high, while the Dow Jones Industrial Average hit the 30,000 milestone on November 24 (up 60% from the lows in March). Investors can be forgiven for wondering “what the heck just happened?!”

Crisis ResponseIn a year of such widespread and far-reaching crisis, it is instructive to note how various actors behaved and what the implications of their actions might be. As noted above, the Fed responded to the crisis by pulling out all the stops quickly, lowering the Fed funds rate to near zero (and promising to keep it there until inflation remains consistently above 2% and unemployment returns to around 4%) while also massively expanding the quantity and type of securities it would purchase and increasing various loan programs to banks (including other central banks overseas). The result is that we live in a world of extremely low interest rates and will continue to for the

25

2020 Year in Review and 2021 Outlook

foreseeable future, presenting a challenge to fixed-income investors.

At the same time, Congress responded by passing a $2 trillion coronavirus relief package aimed at getting money quickly into the hands of consumers thrown out of work through no fault of their own, preventing bankruptcies and evictions while sustaining some level of consumer spending. Resulting from this relief package are deficits and debt levels unseen outside of wartime, thus raising the likelihood that taxes will have to rise at some point.

Investors responded to all this monetary and fiscal stimulus, while also looking through the current crisis to the post-pandemic recovery ahead, by rushing back into stocks, driving most benchmarks to new record highs. The results are high valuations and the corollary that future returns must necessarily be lower.

Consumers responded by retrenching, not only out of fear brought on by the sudden recession but also out of necessity, as the lockdown prevented spending in many discretionary areas such as travel, entertainment, restaurant dining, and even getting a haircut. The result is that there is a tremendous amount of pent-up demand in the economy (as long as the lockdowns don’t drag on so long that consumers’ savings and earnings power are permanently impacted).

Corporations also responded to the crisis by retrenching, figuring out ways to continue operating with fewer employees, less real estate, and little or no corporate travel. The result is increased productivity and profitability that is likely to continue even after the pandemic has passed.

Voters responded by delivering divided government, as both houses of Congress ended up with smaller majorities. The political division in the country rests on an even narrower knife edge. The result is likely to be very benign policy alterations during the next administration,

as neither party appears to have a mandate to make significant changes. For example, a major change in the federal tax system seems highly unlikely.

RFA clients responded by remaining steadfast in pursuing their long-term goals, tuning out the noise of market pundits during the cataclysm and thus enjoying the market’s rebound, as surprisingly sudden as it was. Kudos to you all!

Major DivergencesThe economic crisis brought on by the pandemic unleashed or reinforced a number of prominent divergences. The divergence between the growing success of online retailers and the struggles of brick-and-mortar stores accelerated as most of us were stuck at home and stores were forced to close, at least temporarily. Existing online retailers such as Amazon became even more dominant, while those such as Nike who were able to pivot quickly to digital sales thrived and will exit the pandemic even stronger than they entered it. A number of retailers without a strong online presence will not survive the pandemic.

Because many service jobs by definition require face-to-face interaction, whereas manufacturing jobs often can be conducted while physically distancing from other workers, a big divergence appeared between the performance of a weak recovery in the services sector and a robust recovery in the manufacturing sector.

Residential real estate boomed as low interest rates encouraged families seeking more space for working and schooling from home to buy larger homes away from city centers, even as they faced inventories constrained by COVID-19 restrictions. On the other hand, commercial real estate struggled (as retail and office properties were suddenly vacant for months on end). As consumer and worker behavior adapts to changes brought on by the pandemic, the longer-term threat is that this behavior

26

2020 Year in Review and 2021 Outlook

becomes ingrained and much of the property becomes surplus.

Another divergence that emerged was the ability of higher-income, knowledge-based employees to work from home whereas lower-income service workers either lost their jobs or were exposed to the coronavirus. Many knowledge workers suffered little or no loss of income during lockdowns, whereas service workers lost their incomes while often having little in the way of savings. The issue of income inequality became even more glaring thanks to the pandemic.

Perhaps the most notable divergence was between the stocks of companies that seemed to benefit from the lockdowns (in particular, Apple, Amazon, Microsoft, Google, and Facebook) and everyone else. By the end of October, just before the announcement of a successful vaccine trial, these five stocks had gained an average of 38.6% in 2020 versus a loss of 4.8% for the other 495 stocks in the S&P 500. So dominant are these five companies that they have grown to represent 25% of the index.

Deflationary ShocksThe rise of these megacap tech titans exemplifies one of the four major economic shocks the world has experienced thus far in the 21st century—the rise of the digital economy. While we think of the late 1990s as the period of an explosion in information technology investing, it wasn’t really until the new millennium that we witnessed tech become central to our lives. Just think about the rapid spread of Amazon’s offerings from merely books and CDs, how the iPhone has changed our lives since its introduction in 2007, and the central role social media has come to play.

The integration of China into the world economy after it joined the World Trade Organization in 2001 offered the promise of a vast new market but also introduced

legions of low-wage workers into global supply chains. Multinationals rushed to take advantage, suppressing manufacturing wages around the world.

The Global Financial Crisis of 2008 demonstrated how interconnected national economies and financial markets had become during a period of rapid globalization. Low interest rates around the world fed a global housing bubble that popped when underwriting standards evaporated due to the unquenchable demand for mortgages to create securitized investment products. As we saw with “portfolio insurance” in 1987, “ultra-safe” collateralized mortgage obligations proved to be anything but safe.

The novel coronavirus pandemic is just the latest major economic shock of the 21st century. Unlike the others, which developed over extended periods, the Global Viral Crisis hit the world economy everywhere in the blink of an eye. The hope of policymakers is that by acting aggressively they can limit the damage and revive economies quickly once the pandemic passes.

What all these economic shocks share is that their impacts are deflationary. Overlaid on top of this are the demographics of rapidly aging populations around the world, which is also highly deflationary. Japan’s population is not only old but already shrinking, having peaked in 2009 at 128 million. And with a one-child policy for more than two generations, China’s population will age and shrink faster than Japan’s. Given this global trend, the Fed’s goal of generating sustainable inflation above 2% and attractive nominal interest rates is looking perhaps to be but a “yield of dreams.”

Decennial CrisesHaving been at this for a while, it is beginning to seem to me as if we have some form of major crisis on a recurring basis every decade. Below are a few that I have experienced during my career.

27

2020 Year in Review and 2021 Outlook

On December 31 of each year listed below (Fig. 9), we found ourselves in the midst of some major crisis that appeared pretty daunting. Yet we somehow managed to navigate our way out of each predicament. In 1980, Fed Chairman Paul Volcker broke the back of roaring inflation by raising the Fed funds rate above 20%, throwing the U.S. into a double-dip recession; but as you can see, both inflation and interest rates have fallen dramatically ever since. And the subsequent decade ended up being pretty good for stock investors, as the S&P 500 returned nearly 14% annually, on average.

Fast forward a decade to 1990 and real estate problems had morphed into a financial crisis (sound familiar?) as numerous savings and loan associations went under. The backdrop of war with Iraq also made investors jittery. And yet the decade of the 1990s proved to be even more rewarding to stock investors, with an average annual return of more than 17%.

Dot-com mania unwound in 2000, ushering in a decade of abysmal equity returns and illustrating that perhaps excessive enthusiasm and attendant extended valuations are the greatest dangers facing investors. With the decade beginning and ending in bear markets for U.S. stocks, investors were better off seeking returns almost anywhere else (e.g., international stocks, fixed income, hedge funds, and other alternative investments). Many chose to focus on real estate, which led to the next problem.

By 2010, the world was beginning to make its way out of the rubble of the Global Financial Crisis, but it didn’t feel like it at the time. The price of gold was shooting higher, and a sovereign debt and banking crisis was unfolding in Europe. Interest rates continued to fall as many countries fought to skirt outright deflation. And yet, the decade proved to be very rewarding to stalwart stock investors.

Fig. 9

Decade Crisis Core CPI 10-Year U.S. Treasury Bond Yield

S&P 500 Total Return*

1980 The Crisis of Inflation 12.2 12.43 13.99

1990 The Savingsand Loan Crisis 5.3 8.08 17.59

2000 The Dot-Com Bubble Bursting 2.6 5.12 1.36

2010 The Global Financial Crisis 0.7 3.30 13.90

2020 The Global Viral Crisis 1.6 0.93 ?

Decennial Crises

Source: Federal Reserve Economic Database, Robert Shiller*Subsequent 10-Year Compound Annual Growth Rate (CAGR)

2020 Year in Review and 2021 Outlook

OutlookWe find ourselves in the midst of yet another major crisis with many dimensions—political, economic, and public health-related—that combine to seem overwhelming. What, if anything, can we discern about what lies ahead? I think that we can make a few observations.

First, if 2020 taught us anything, it is the futility of forecasting; no one could have foreseen in 2019 what would unfold the following year. Therefore, always take what I say with a grain of salt.

Second, deflationary forces appear to be in the driver’s seat, and thus the era of low inflation and low interest rates is likely to persist for the foreseeable future.

Third, the pandemic has reinforced and accelerated trends that were already in place, such as the rise of the digital economy and the waning of globalization.

Fourth, while global trade may weaken, we have learned that some challenges, such as the pandemic and climate change, do require global cooperation.

And finally, we will survive this crisis. Yet there will be another crisis in the future—and we will survive that one, too.

The 2021 Reilly Report

Barron’s in Education Partnership A fun fact about our firm you likely won’t know is that we have hired more of our wealth management and tax advisors from the Fowler College of Business at San Diego State University (SDSU), located just a stone’s throw from our San Diego headquarters, than from any other university. We have also provided numerous internship opportunities to SDSU students interested in pursuing post-graduation careers in the financial industry.

Given all that the Fowler College of Business has done for us, we wanted to give something back. That’s why in fall 2020, Reilly Financial Advisors began a two-year partnership with the Fowler College of Business and Barron’s in Education in order to provide a digital subscription to Barron’s magazine to all Fowler staff and students.

In addition to the digital subscription, Fowler faculty members will also receive a weekly review of financial news and events, an email newsletter summarizing Barron’s headline articles and investment stories, and access to live guest lecturers and exclusive webinars through Dow Jones and Barron’s. Also through this partnership, Fowler students can connect with Barron’s corporate recruitment teams about career openings and student internship programs and will even be offered the opportunity to participate in a private tour of Dow Jones’ New York headquarters (at their own expense).

Said RFA President Frank Reilly about the partnership, “I am so excited to have the opportunity to give back to SDSU in a meaningful way. More than one-third of our staff are SDSU alumni, and we currently have employees enrolled in the graduate program at the Fowler College of Business. As a financial professional, I can’t stress the importance of financial literacy enough, and I’m happy to share my professional experience in the classroom as an SDSU guest lecturer and through ongoing volunteer work.”

29

Furry and Feathered Friends

BacardiOwner: McKenzie Reilly

OskarOwner: Brad Berman

BeansOwner: Bradley Johnston

HunterOwner: Lindsey Boyd

BrewskyOwner: Lindsey Boyd

BuddyOwner: Jennifer Arganbright

MaxOwner: Christina Dodge

Ellie McCream Puff and OchoOwner: Sonja Larimore

MiaOwner: Gabrielle Reilly

30

RFA pets are considered part of the family, so we’re excited to share this glimpse at some of the many furry and feathered friends that round out our RFA tribe.

LilaOwner: Jason Watters

CamelliaOwner: Tom Weary

OreoOwner: Tom Weary

Jameson and KillianOwner: Frank and Gina Reilly

Dill PickleOwner: Jenifer Pratt

SunnyOwner: Jenifer Pratt

Chanel and PTOwner: Lisa Goodman

LouisOwner: The Reilly Family

RileyOwner: Joshua Land

31

Jennifer Arganbright and Voices for Children

Staff Volunteer Spotlight

32

“I want you to imagine walking through the door of the courthouse, and you’re eight. . . . Imagine wondering if your mom is going to be there. And you’re kind of

mad at your mom because you know that she has been using drugs, but you also miss her because she’s your mom. And then imagine walking into that courtroom where you don’t know who the people are, everybody’s talking in code, and you know that somebody that day is going to make a decision about where you live. Imagine how terrifying that must be. And now imagine that when you walk up to the door of your courtroom you see your CASA, and your CASA has promised you that afterward you’re going to get pizza. And it’s going to be at your favorite pizza place—and your CASA knows what your favorite pizza place is. That is what you do.”

This excerpt from a heartfelt speech by San Diego Superior Court Judge Marian Gaston is what first put me on the path to becoming a court appointed special advocate, or CASA, with Voices for Children. Immediately after hearing it at my friend’s graduation from CASA training, I went home and recited as much of the speech as I could remember to my husband—who was ultimately moved to sign up as well. The work Voices for Children and its volunteers do on behalf of foster kids is especially meaningful to us, because my husband spent ages two through five in foster care himself.

Because of the confidential nature of the program, I can’t share any specifics about the children I advocate for, but I can give you an overview of the program and what it means to be a CASA.

Voices for Children serves foster children who have been removed from their homes due to neglect, abuse, or abandonment. Whereas a family court lawyer may represent 100 or more children and a social worker may juggle a caseload of more than 25, CASAs devote their attention to just one child or sibling group, closely monitoring each child’s situation. A CASA is often the only consistent adult presence in a foster child’s life who is not getting paid to oversee their welfare or spend time with them.

INTERNATIONAL DOMINICAN FOUNDATION

RFA and Its Staff Proudly Support These Organizations

33

To become a CASA, one must first make a minimum 18-month commitment to the program. Then, after successfully completing training (which, among other things, includes 35 hours of instruction and a thorough background check), the CASA will be officially appointed to a case by a juvenile court judge.

CASAs meet with their case child at least once per month. They gather information from court documents, social workers’ files, and educational/medical/therapy records. They speak with their case child as well as his or her family members, school officials, and healthcare providers. They may even attend their case child’s supervised visits with biological parents or hold educational rights. CASAs then use the information they have gathered, as well as their firsthand observations, to advocate for their case child in court, at school, and in other aspects of their lives.

Above all, the role of a CASA is to consider what is in each child’s best interest and make sure that his or her needs are met. Some CASAs are even able to build and maintain positive, trusting relationships with their case children, much like mentors.

If you would like to learn more about Voices for Children or lend your support, head to www.speakupnow.org

Reilly Financial Advisors’ 2,800-square-foot Newport Beach office opened in March 2018 with just three employees. While the office was home to four members of our team for the majority of 2020, a new face will be joining them in 2021. Given the Newport Beach office’s continued success, we’re happy to announce the addition of a second Senior Wealth Advisor to their ranks. Because many of you won’t have the opportunity to visit the Newport Beach office yourselves, we thought it would be nice to provide this virtual tour.

A Virtual Tour of Our Newport Beach Office

34

35

San Diego Office ExpansionIn The 2020 Reilly Report, we gave you a sneak peek of our San Diego office’s 7,200-square-foot expansion to the second floor, just above the first-floor office.

While construction was completed in spring 2020 as expected, we have not had many visitors to the space since (given how things have been). While we look forward to the day when many of you can visit us in person and tour the office yourself, for now we would like to share this first look at our newly renovated second-floor space.

36

Under Construction

37

Big congratulations go to Sonja Larimore, J.D., IACCP®, AIF®, on finishing law school and for her promotion from Managing Director of Operations & Compliance to Chief Compliance Officer!

In 2020, Sonja received her juris doctor from San Diego’s Thomas Jefferson School of Law, graduating magnum cum laude. There, she was also Managing Editor on the Law Review Board and President of the Women’s Law Association. In fall 2019, her Note, “Child Soldiering and How the United States Can Up Its Game Against Those States That Still Continue This Practice,” was published in the Thomas Jefferson Law Review.

Read on to learn more about Sonja, her four-year journey through law school, and her new role as RFA’s Chief Compliance Officer.

What were your personal reasons for pursuing a law degree?I had wanted to be a lawyer ever since I can remember. I watch all the crime shows and all the lawyer shows on TV. It is fascinating to me how one person can be responsible for sending someone to—or keeping someone out of—jail, shaping that person’s life and the lives of their family members. When I told my family I got into law school, my grandpa said he knew that would happen since I was eight years old.

What were your professional reasons for pursuing a law degree?When I was first hired in 2004, I told RFA I was taking a year off from education before attending law school. But when the time came, I loved working at RFA and law school did not seem viable. However, my desire to attend law school remained, and I also knew that a law degree would help me to become the firm’s Chief Compliance Officer (which was my ultimate goal). Years later, I seized the opportunity when it presented itself.

As you continued along your journey, what kept you going?I really like to learn, and I learned something new every day at law school. I also like to read, so I was fine with all the reading I had to do each week. One of the good things about working full time was that I was more organized than some of the other students. Because I had limited time to study and do my homework, I had to be disciplined. I set a schedule and told myself that each Saturday and Sunday I would study until 4:00 p.m. so that I could go to a movie or watch my DVR in the evenings. Structure and organization were important.

Congratulations to Sonja Larimore, J.D., IACCP®, AIF®

3038

Can you walk us through getting your Note published?The process was long and difficult. We had one semester to write a Note for consideration of publication. On top of all other homework and studying, I had this extra research and writing that had to be completed and turned in for review. Deadlines were strict, and if they were not met, I might have been released as a provisional member. I definitely worked past 4:00 p.m. on weekends during the semester I spent researching and writing my Note, but it was worth it; I learned a lot about child soldiering and the U.S. laws pertaining to it.

Were there any setbacks along the way?I wouldn’t say there were any true setbacks, but my timing was definitely unfortunate. Due to the pandemic, my last half-semester had to be completed online, and I was unable to walk across the stage at graduation or have a graduation party.

How will your law schooling help you in your new role as RFA’s Chief Compliance Officer?Compliance, as it pertains to financial advisors, is all about following the rules put forth by the SEC. Now, when new regulations are introduced, I am better able to understand the language used in order to ensure RFA properly adheres to them. I also became a better writer, which helps when writing policies for the company as needed.

To learn more about Sonja and her role as RFA’s Chief Compliance Officer, visit www.rfadvisors.com/about

39

30

Jason Watters, MBAAlternative Investment Analyst

As RFA’s Alternative Investment Analyst, Jason oversees RFA’s non-traded portfolio allocations. He provides ongoing due diligence for currently held hedge, private equity, and private market funds and maintains open dialogue with fund managers to ensure all objectives are being met. He is also responsible for screening and analyzing new alternative funds before presenting them to the Investment Committee for consideration.

Before joining RFA, Jason worked as an Advisory & Product Consultant for a large broker-dealer. There, Jason served as the lead alternative investment consultant,

assisting in educating financial advisors on alternative products and recommending portfolio allocations.

Jason received both his bachelor’s and master’s degrees in business administration, with minors in finance and international marketing, from Alliant International University in San Diego. He holds a professional certificate in Alternative Investment Fundamentals from the CAIA Association and also holds FINRA Series 7, Series 63, and Series 65 licenses.

Jason is a native San Diegan and loves to do anything outdoors. He is a PADI-certified dive master who enjoys teaching and leading scuba diving courses in local waters and is passionate about ocean conservation. He enjoys traveling to experience new cultures whenever possible and spending time with his young daughter and large family.

Why I Do What I Do:I enjoy having the opportunity to make complex alternative products easily accessible and understandable to our clients while ensuring these products complement their long-term financial goals.

New HiresMeet the Latest Additions to Our Team

40

Andrew Ferrette, MSBA, CFP®

Senior Wealth Advisor

As a Senior Wealth Advisor, Andrew works closely with new and existing clients to develop and implement financial plans based on their individual goals. He serves as their main point of contact, resource for financial decisions, and trusted advisor. He is passionate about providing superior service, clarity, and client-focused solutions to help individuals achieve their financial goals.

Prior to joining Reilly Financial Advisors, Andrew served as a Financial Planner at a family office in San Diego. He assisted client families in developing, monitoring, and implementing comprehensive financial plans to address all existing and

future financial objectives. He has more than 10 years of experience in the financial services industry, holding various roles in client service, portfolio management, financial planning, and retirement planning.

Andrew received his bachelor’s degree in economics from Sonoma State University. While at Sonoma State, he played four years of lacrosse, serving as team president and captain. Andrew is a CERTIFIED FINANCIAL PLANNER™ professional, holds the FINRA Series 7 and Series 63 licenses, and earned his master’s degree in tax and financial planning from San Diego State University.

Andrew was born and raised in San Diego and enjoys spending time with his wife, son, friends, and family. He also loves watching sports (especially the San Diego Padres), playing golf, cooking, traveling, and being a lifelong learner.

Why I Do What I Do:During the 2008–2009 recession, I was beginning my career and saw firsthand the emotional distress individuals experienced during uncertain times. I realized that through financial guidance and education, I could help individuals gain confidence and find peace of mind within their financial lives. I am dedicated to providing personalized advice and education to help clients navigate financial decisions and reach their goals.

41

New HiresMeet the Latest Additions to Our Team

Nicole Doherty, MSA, CPATax Manager

Nicole works with RFA clients to help prepare their annual tax returns while also coordinating with the advisor team for client tax planning throughout the year.

Prior to joining Reilly Financial Advisors, Nicole worked as a tax manager at a global accounting firm, providing guidance and review on individual, corporate, and partnership income tax returns, primarily in the real estate and investment fund sectors. Embracing her love of education and development, Nicole was also actively involved in technical trainings and mentorship within the firm.

A San Diego native, Nicole has stayed close to home, studying at San Diego State University. There, she received her master’s degree in accountancy (with a taxation focus) and her bachelor’s degree in business administration (with an accounting emphasis), graduating summa cum laude. Nicole is a Certified Public Accountant and a member of both the American Institute of CPAs and the California Society of CPAs.

In her free time, Nicole is often found planning or embarking on an adventure, be it a new hiking trail or multicountry trip throughout Europe. With so much to explore, so many wonderful people to meet, and so many delicious foods to enjoy, her free time is kept happily busy.

Why I Do What I Do:I’ve always had a fondness for solving problems, as well as a general curiosity for how things work. The latter was not appreciated when I took apart the family phone; however, when I applied that curiosity to trying to understand how a tax return came together, my family was much more pleased. Over the years, I discovered that this natural curiosity, coupled with a love for helping others, was the way I could make a difference.

42

New HiresMeet the Latest Additions to Our Team

Josh’s Baby

Stephanie and Joshua Land

Avery Celine7 lbs., 2 oz., 20 inches

43

RFA welcomed just one baby in 2020, the daughter of Senior Wealth Advisor Joshua Land and his wife, Stephanie.

New Arrival

RFA’s annual Christmas party is an important firm tradition. When deciding how to get together in 2020, we wanted to be creative with our choice of virtual activity. On the evening of December 11, all employees and their guests gathered around Zoom to participate in a live Italian cooking class led by classic Italian-born Giacomo from A Casa Mia. On the menu was Tuscan focaccia, pasta with a rustic ragu, and cannoli with homemade ricotta cream. As you can see, while our plated results may have varied, everyone had a great time!

Christmas Party Cooking Class

44

45

Taxable Income Tax Due plus % of income*

SingleUp to $9,950 $0 + 10%

$9,951 to $40,525 $95.00 + 12%

$40,526 to $86,375 $4,664.00 + 22%

$86,376 to $164,925 $14,751.00 + 24%

$164,926 to $209,425 $33,603.00 + 32%

$209,426 to $523,600 $47,843.00 + 35%

$523,601 or more $157,804.25 + 37%

Married filing jointlyUp to $19,900 $0 + 10%

$19,901 to $81,050 $1,990.00 + 12%

$81,051 to $172,750 $9,328.00 + 22%

$172,751 to $329,850 $29,502.00 + 24%

$329,851 to $418,850 $67,206.00 + 32%

$418,851 to $628,300 $95,686.00 + 35%

$628,301 or more $168,993.50 + 37%

Married filing separatelyUp to $9,950 $0 + 10%

$9,951 to $40,525 $995.00 + 12%

$40,526 to $86,375 $4,664.00 + 22%

$86,376 to $164,925 $14,751.00 + 24%

$164,926 to $209,425 $33,603.00 + 32%

$209,426 to $314,150 $47,843.00 + 35%

$314,151 or more $84,496.75 + 37%

Head of householdUp to $14,200 $0 + 10%

$14,201 to $54,200 $1,420.00 + 12%

$54,201 to $86,350 $6,220.00 + 22%

$86,351 to $164,900 $13,293.00 + 24%

$164,901 to $209,400 $32,145.00 + 32%

$209,401 to $523,600 $46,385.00 + 35%

$523,601 or more $156,355.00 + 37%

* The percentage applies to each dollar of taxable income within the range until the next income threshold is reached.

Income Tax (2020 Tax Rate Tables)

Single $12,550

Married filing jointly $25,100

Married filing separately $12,550

Head of household $18,800

Dependent* $1,100*

Standard Deduction

Additional deduction for blind or aged (over age 65)Single or head of household $1,700

Married filing jointly orseparately $1,350

* Dependent standard deduction is the greater of $1,100 or $350 plus earned income.

Maximumexemption amount

Exemptionphaseout threshold

Single or head of household $73,600 $523,600

Married filing jointly $114,600 $1,047,200

Married filing separately $57,300 $523,600

26% rate applies to AMT income up to $199,900*28% rate applies to AMT income over $199,900*

* $99,950 if married filing separately.

Alternative Minimum Tax (AMT)

MAGI phaseout rangesSingle or head of household

Marriedfiling jointly

Lifetime Learning credit($2,000 max) $59,000 to $69,000 $119,000 to $139,000

American Opportunity credit($2,500 max) $80,000 to $90,000 $160,000 to $180,000

Education loan interest deduction ($2,500 max) $70,000 to $85,000 $140,000 to $170,000

U.S. Savings bond interest exclusion for higher education expenses

$83,200 to $98,200 $124,800 to $154,800

Education Credits and Deductions

Annual gift tax exclusion $15,000

Non-citizen spouse annual gift tax exclusion $159,000

Top gift, estate, and GST tax rate 40%

Gift tax and estate tax applicable exclusion amount $11,700,000 + DSUEA*

Generation-skipping transfer (GST) tax exemption $11,700,000**

* Basic exclusion amount plus deceased spousal unused exclusion amount (exclusion is portable).** The GST tax exemption is not portable.

Estate Planning

Key Numbers for 2021Tax reference numbers at a glance

46

Employee contribution limits to employer plans*401(k) plans, 403(b) plans, 457(b) plans, and SAR-SEPs (includes Roth contributions to these plans)

$19,500

Annual catch-up contribution (age 50+) $6,500

SIMPLE 401(k) and SIMPLE IRA plans $13,500

Annual catch-up contribution (age 50+) $3,000

IRA contribution limits**Traditional and Roth IRAs (combined) $6,000

Annual catch-up contribution (age 50+) $1,000

* Lesser of these limits or 100% of participant’s compensation.** Lesser of these limits or 100% of earned income.

MAGI phaseout limits for deductible contributions to a traditional IRA (affects taxpayers covered by an employer-sponsored retirement plan)Single or head of household $66,000 to $76,000

Married filing jointly when the spouse who makesthe contribution is covered by a workplace plan $105,000 to $125,000

Married filing jointly when the spouse who makesthe contribution is not covered by a workplace plan but the other spouse is covered

$198,000 to $208,000

Married filing separately Up to $10,000

MAGI phaseout limits to contribute to a Roth IRASingle or head of household $125,000 to $140,000

Married filing jointly $198,000 to $208,000

Married filing separately Up to $10,000

Retirement Planning

Flexible spending account (FSA) for health careMaximum salary reduction contribution $2,750

Health savings account (HSA)Annual contribution limit — individual coverage $3,600

Annual contribution limit — family coverage $7,200

Annual catch-up contribution (age 55+) $1,000

High-deductible health plan (HDHP)Minimum deductible — individual coverage $1,400

Minimum deductible — family coverage $2,800

Maximum out-of-pocket amount — individual $7,000

Maximum out-of-pocket amount — family $14,000

Health Care

Maximum taxable earningsSocial Security (OASDI only) $142,800

Medicare (HI only) No limit

Social Security/Medicare

Business purposes TBD*

Medical purposes TBD*

Charitable purposes 14¢ per mile

Moving purposes TBD*

Standard Mileage Rates

Single filer Married filing jointly Married filing separately Head of household Tax rate

Long-term capital gain & qualified dividend tax (taxable income thresholds)Up to $40,400 Up to $80,800 Up to $40,400 Up to $54,100 0%

$40,001 up to $445,850 $80,801 up to $501,600 $40,401 up to $250,800 $54,101 up to $473,750 15%

More than $445,850 More than $501,600 More than $250,800 More than $473,750 20%

Net investment income tax (MAGI thresholds)Over $200,000 Over $250,000 Over $125,000 Over $200,000 3.8%*

* The 3.8% net investment income tax (also referred to as the unearned income Medicare contribution tax) applies to the lesser of (a) net investment income or (b) modified adjusted gross income (MAGI) exceeding the above thresholds. It does not apply to municipal bond interest or qualified retirement plan/IRA withdrawals.

Investment Taxes

IMPORTANT DISCLOSURES

This information was provided by Broadridge Investor Communication Solutions, Inc. Broadridge Investor Communication Solutions, Inc., does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual’s personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

47

* In 2020, mileage rates were 57.5¢ per mile for business purposes and17¢ per mile for medical or moving purposes.

Mildred Balestra, the grandmother of RFA’s own Lisa Goodman, celebrated her 100th birthday last year! We spoke to Lisa, a VP of Wealth Management working out of RFA’s Orange County branch, to learn a little bit about Mildred’s long life.

Mildred was born on February 13, 1920, to a large immigrant family. One of nine children, Mildred has always been active, and beloved hobbies of hers over the years included traveling, going for walks, and playing golf (in fact, she’s a member of the esteemed hole-in-one club!).

In 1984, Mildred’s husband passed away from Lou Gehrig’s disease (also known as ALS). Today, Mildred lives in Jacksonville, Florida, at an assisted living facility close to her son.

Lisa is so happy to have been able to make the trip to visit Mildred for her big centennial birthday celebration not long before the country shut down due to the pandemic.

The good news is that Lisa can still speak to her grandmother on a weekly basis, thanks to the magic of Zoom and FaceTime (which Mildred is absolutely fascinated with)! In these times, it’s the little things that count.

Lisa Goodman’s Grandmother Is

100!

48

(800) [email protected]

7777 Alvarado Road, Suite 116La Mesa, CA 91942

(619) 698-7260

San Diego

(800) [email protected]

4675 MacArthur Court, Suite 545Newport Beach, CA 92660

Orange County

+1 (619) [email protected]

Visit ExpatAdvisors.com

Europe

+966 [email protected]

Fontana Gardens – Flat A312Building: 4682, Road: 2468, Block: Juffair 324

Manama, Kingdom of Bahrain

Middle East

(800) 682-3237www.rfadvisors.com