Embed Size (px)

Citation preview

1Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Thailand’s Competitiveness:Where Does the Country Stand?

Professor Michael E. PorterInstitute for Strategy and Competitiveness

Harvard Business School

Bangkok, Thailand13 July 2005

This presentation draws on ideas from Professor Porter’s articles and books, in particular, The Competitive Advantage of Nations (The Free Press, 1990), “The Microeconomic Foundations of Economic Development,” in The Global Competitiveness Report 2004, (World Economic Forum, 2004), “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition (Harvard Business School Press, 1998), and the Clusters of Innovation Initiative (www.compete.org), a joint effort of the Council on Competitiveness, Monitor Group, and Professor Porter. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording, or otherwise - without the permission of Michael E. Porter.Additional information may be found at the website of the Institute for Strategy and Competitiveness, www.isc.hbs.edu

2Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

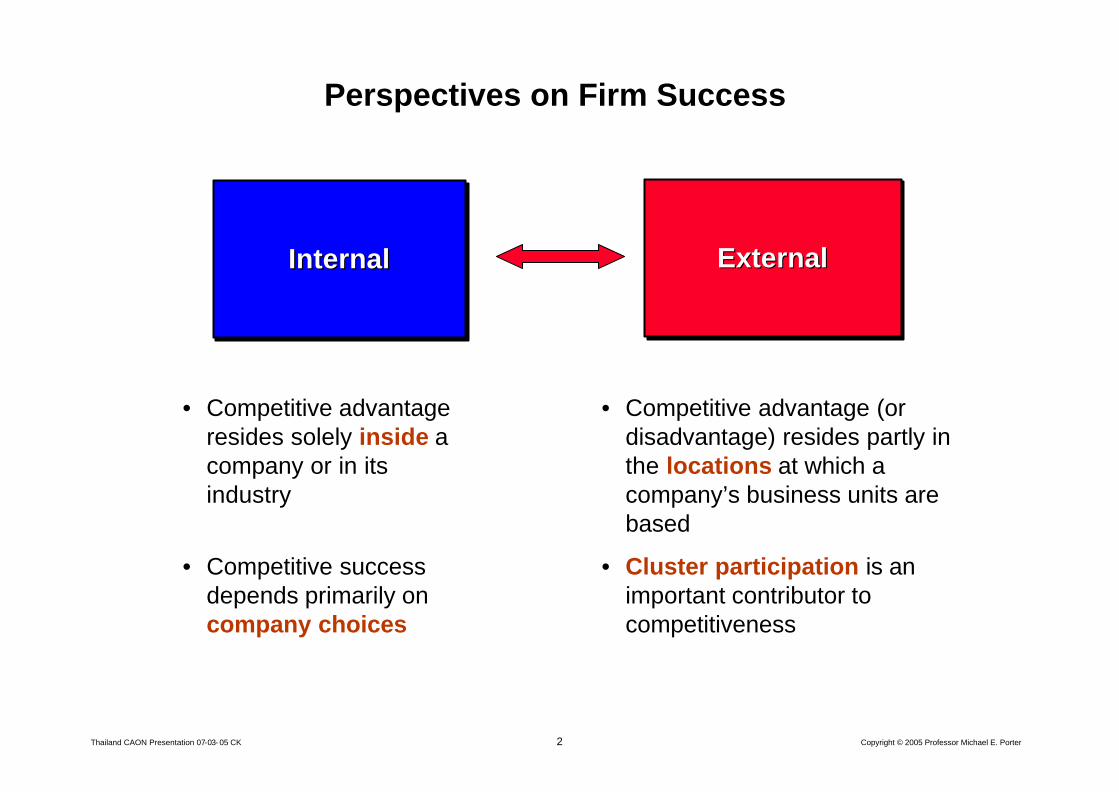

Perspectives on Firm Success

InternalInternalInternal ExternalExternalExternal

• Competitive advantage resides solely inside a company or in its industry

• Competitive success depends primarily on company choices

• Competitive advantage (or disadvantage) resides partly in the locations at which a company’s business units are based

• Cluster participation is an important contributor to competitiveness

3Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

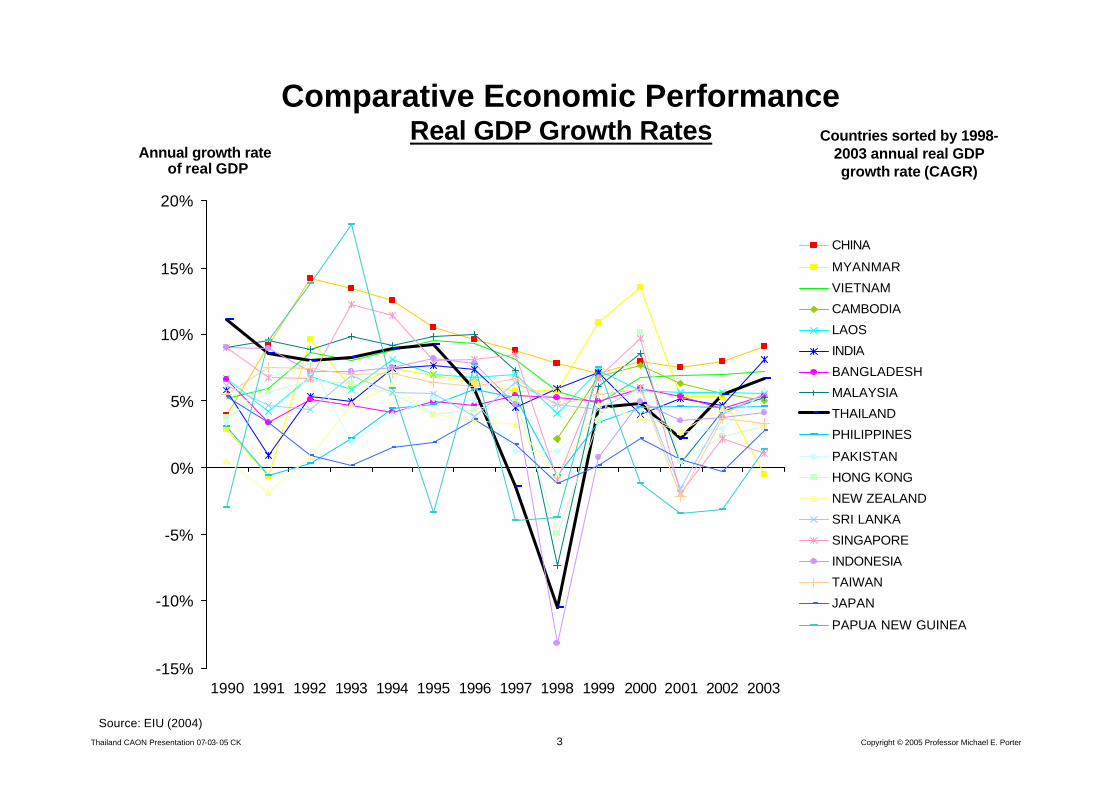

Comparative Economic PerformanceReal GDP Growth Rates

-15%

-10%

-5%

0%

5%

10%

15%

20%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

CHINA

MYANMAR

VIETNAM

CAMBODIA

LAOS

INDIA

BANGLADESH

MALAYSIA

THAILAND

PHILIPPINES

PAKISTAN

HONG KONG

NEW ZEALAND

SRI LANKA

SINGAPORE

INDONESIA

TAIWAN

JAPAN

PAPUA NEW GUINEA

Source: EIU (2004)

Countries sorted by 1998-2003 annual real GDP growth rate (CAGR)

Annual growth rateof real GDP

4Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

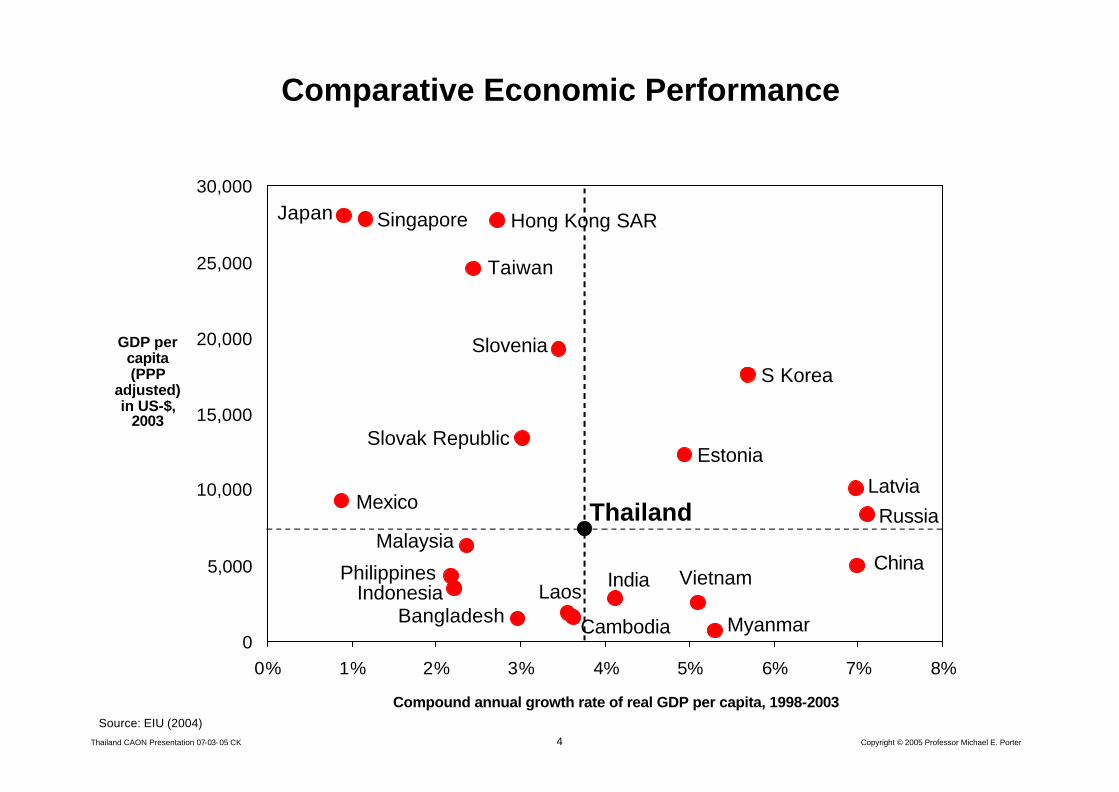

0

5,000

10,000

15,000

20,000

25,000

30,000

0% 1% 2% 3% 4% 5% 6% 7% 8%

Comparative Economic Performance

Compound annual growth rate of real GDP per capita, 1998-2003

GDP per capita (PPP

adjusted) in US-$,

2003

Source: EIU (2004)

Vietnam

Japan

Thailand

S Korea

Indonesia

Malaysia

LaosPhilippines

Taiwan

Bangladesh

China

Hong Kong SAR

India

Myanmar

Singapore

Cambodia

Estonia

Latvia

Slovenia

Slovak Republic

RussiaMexico

5Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Thailand’s Competitiveness

• The Thai economy had to deal with a number of serious crises(Asian crisis, SARS, 2004 Tsunami) in the last decade

• Despite these challenges, prosperity has improved at a solid rate since 1999

• The 2004 drop in the Global Competitiveness Report ranking is a reminder, however, that further improvements are not automatic

• Thailand needs to continue the upgrading processes to deliver rising competitiveness

• A key task for the country is the improving ability to move fromstrategic ambition to sustainable action

6Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

• Competitiveness is determined by the productivity (value per unit of input) with which a nation, region, or cluster uses its human, capital, and natural resources. Productivity sets a nation’s or region’s standard of living (wages, returns on capital, returns on natural resources)

– Productivity depends both on the value of products and services (e.g. uniqueness, quality) as well as the efficiency with which they are produced.

– It is not what industries a nation or region competes in that matters for prosperity, buthow firms compete in those industries

– Productivity in a nation or region is a reflection of what both domestic and foreign firms choose to do in that location. The location of ownership is secondary for national prosperity.

– The productivity of “local” industries is of fundamental importance to competitiveness, not just that of traded industries

– Devaluation and revaluation do not make a country more or less “competitive”

• Nations or regions compete in offering the most productive environment for business

• The public and private sectors should play different but interrelated roles in creating a productive economy

What is Competitiveness?

7Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

0%

1%

2%

3%

4%

5%

6%

0% 5% 10% 15% 20% 25% 30% 35%

USA

Germany SwedenCanada

Japan

Italy

South Korea

Israel

NL

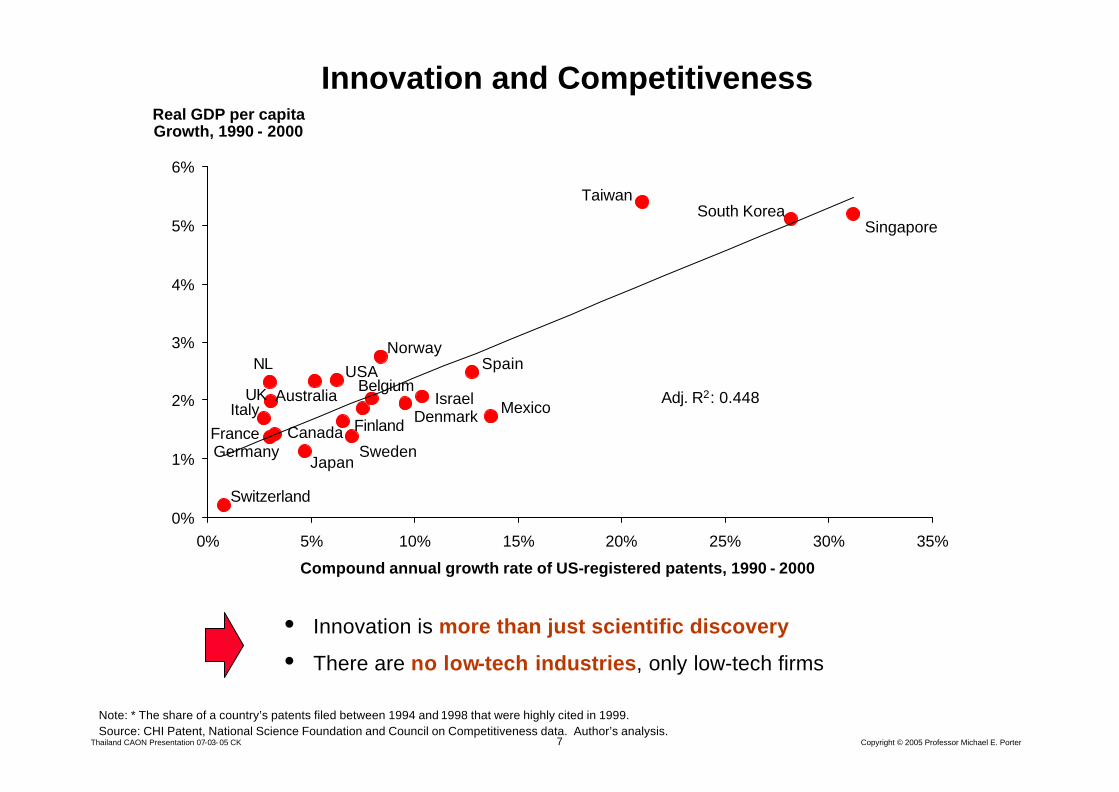

Innovation and Competitiveness

Switzerland

Singapore

Norway

Finland Denmark

Real GDP per capita Growth, 1990 - 2000

Source: CHI Patent, National Science Foundation and Council on Competitiveness data. Author’s analysis.Note: * The share of a country’s patents filed between 1994 and 1998 that were highly cited in 1999.

Mexico

Spain

Taiwan

Compound annual growth rate of US-registered patents, 1990 - 2000

AustraliaBelgium

France

UK Adj. R2: 0.448

• Innovation is more than just scientific discovery

• There are no low-tech industries, only low-tech firms

8Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Microeconomic FoundationsMicroeconomic Foundations

The Quality of the Microeconomic

BusinessEnvironment

The Quality of the The Quality of the MicroeconomicMicroeconomic

BusinessBusinessEnvironmentEnvironment

The Sophisticationof Company

Operations andStrategy

The SophisticationThe Sophisticationof Companyof Company

Operations andOperations andStrategyStrategy

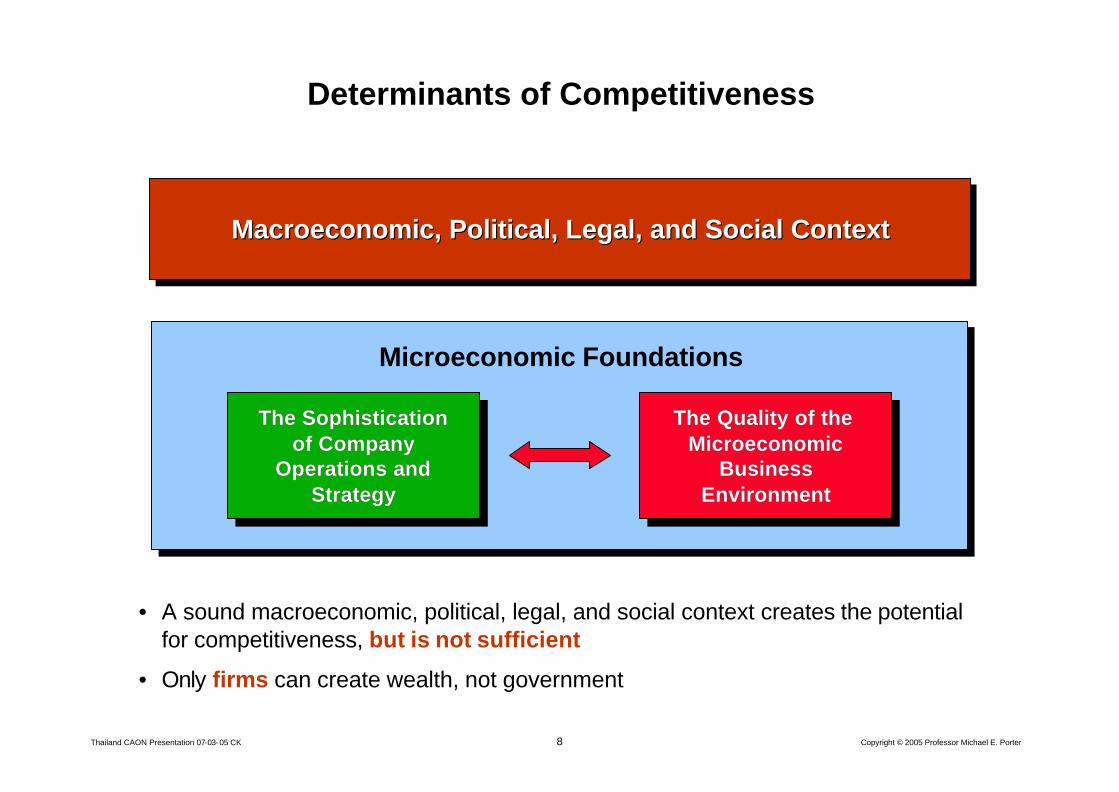

Determinants of Competitiveness

Macroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social Context

• A sound macroeconomic, political, legal, and social context creates the potential for competitiveness, but is not sufficient

• Only firms can create wealth, not government

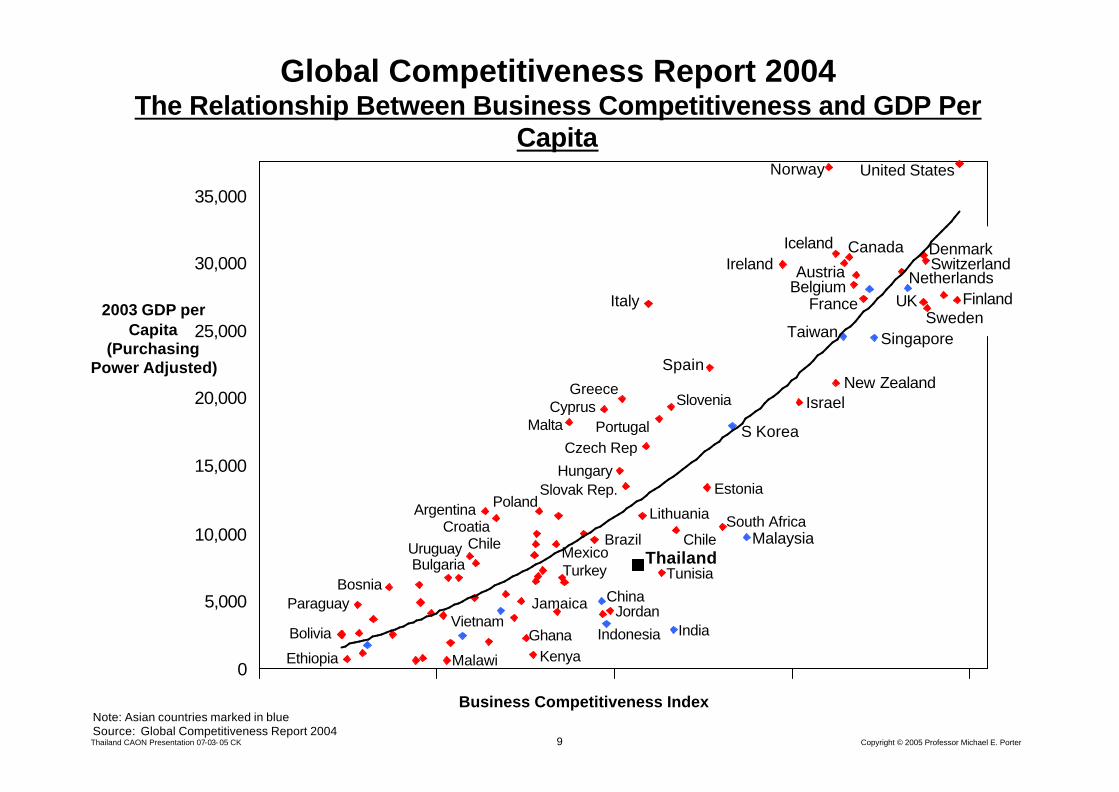

9Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Global Competitiveness Report 2004The Relationship Between Business Competitiveness and GDP Per

CapitaUnited States

Switzerland

UK

Denmark

Singapore

New Zealand

Taiwan

Norway

IcelandIreland

GreeceIsrael

Italy

S Korea

Hungary

India

Netherlands

Spain

Czech RepPortugal

Business Competitiveness Index

2003 GDP per Capita

(Purchasing Power Adjusted)

Brazil Malaysia

China

Chile

VietnamJordan

Uruguay

ArgentinaSouth Africa

Note: Asian countries marked in blueSource: Global Competitiveness Report 2004

Estonia

Indonesia

Sweden

Malta

Kenya

Austria

Paraguay

Croatia

Slovak Rep.

Tunisia

PolandLithuania

Bulgaria

Canada

France FinlandBelgium

Cyprus Slovenia

Chile

Ghana

Ethiopia

Bolivia

Malawi

TurkeyMexico

JamaicaBosnia

Thailand

10Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

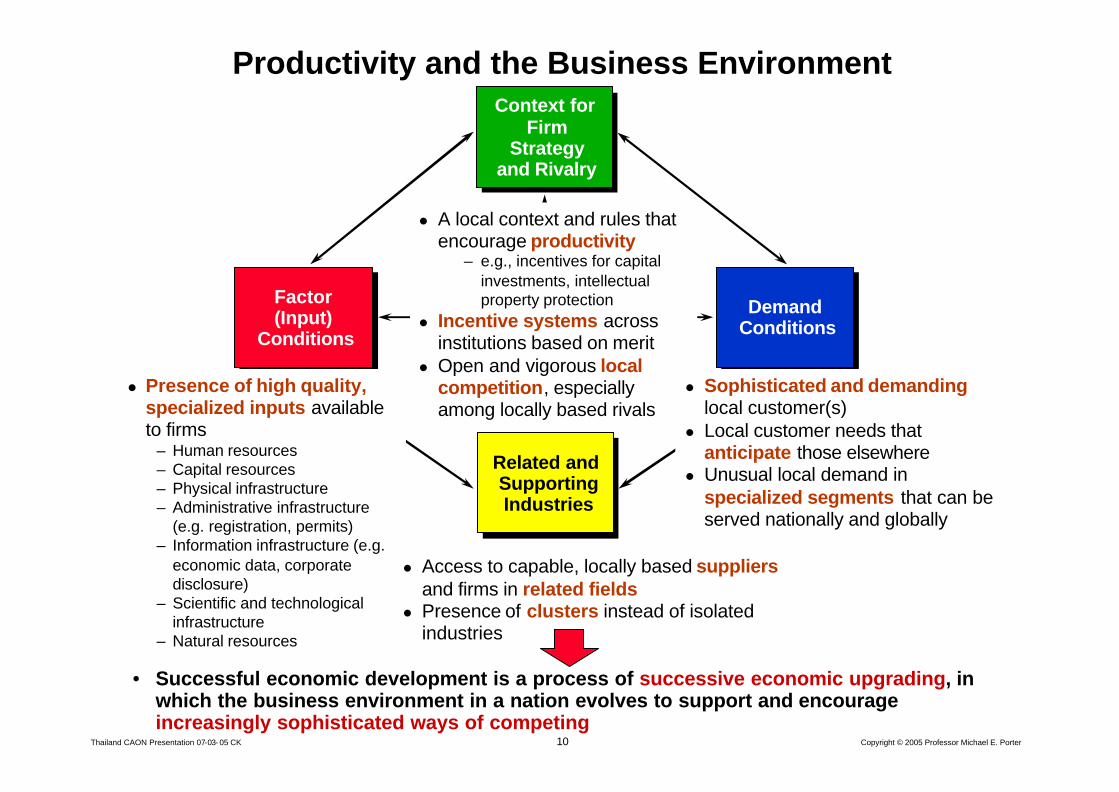

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

l Presence of high quality, specialized inputs available to firms

– Human resources– Capital resources– Physical infrastructure– Administrative infrastructure

(e.g. registration, permits)– Information infrastructure (e.g.

economic data, corporate disclosure)

– Scientific and technological infrastructure

– Natural resources

l Access to capable, locally based suppliersand firms in related fields

l Presence of clusters instead of isolated industries

l A local context and rules that encourage productivity

– e.g., incentives for capital investments, intellectual property protection

l Incentive systems across institutions based on merit

l Open and vigorous local competition, especially among locally based rivals

l Sophisticated and demandinglocal customer(s)

l Local customer needs that anticipate those elsewhere

l Unusual local demand in specialized segments that can be served nationally and globally

Productivity and the Business Environment

• Successful economic development is a process of successive economic upgrading, in which the business environment in a nation evolves to support and encourage increasingly sophisticated ways of competing

11Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

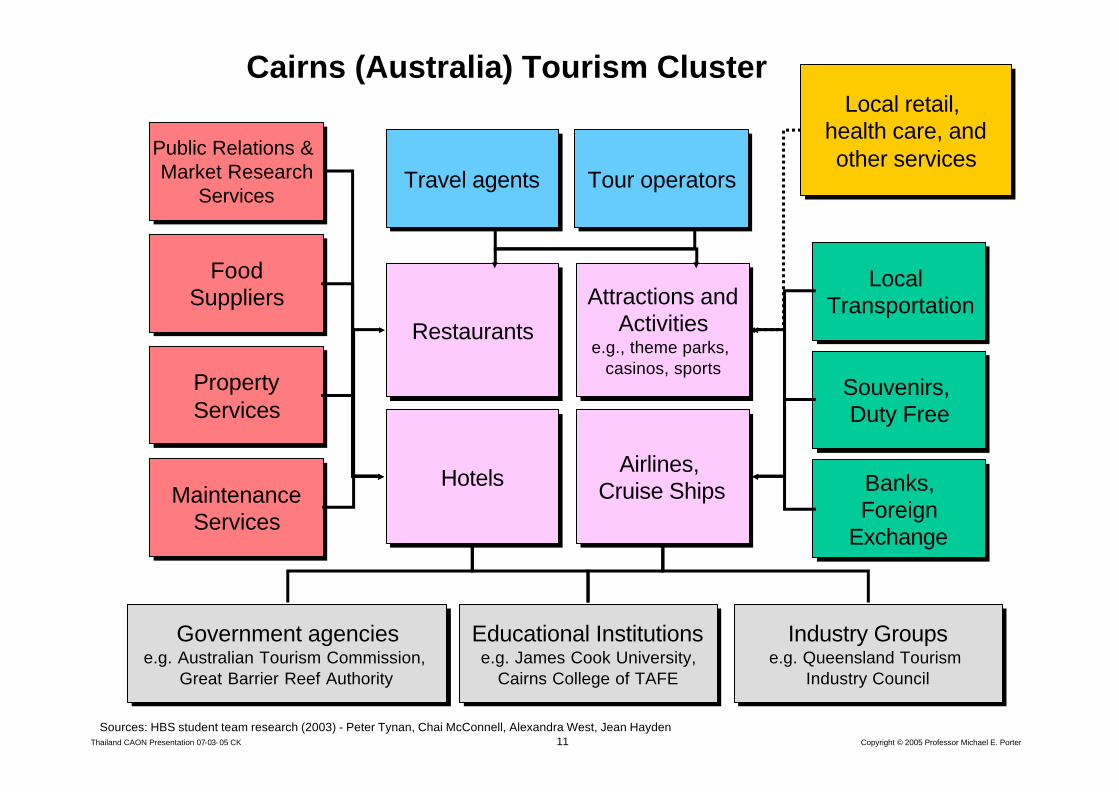

Cairns (Australia) Tourism Cluster

Sources: HBS student team research (2003) - Peter Tynan, Chai McConnell, Alexandra West, Jean Hayden

HotelsHotels

Attractions andActivities

e.g., theme parks, casinos, sports

Attractions andActivities

e.g., theme parks, casinos, sports

Airlines, Cruise Ships

Airlines, Cruise Ships

Travel agentsTravel agents Tour operatorsTour operators

RestaurantsRestaurants

PropertyServicesPropertyServices

Souvenirs, Duty Free

Souvenirs, Duty Free

Banks,Foreign

Exchange

Banks,Foreign

Exchange

Local Transportation

Local Transportation

MaintenanceServices

MaintenanceServices

Government agenciese.g. Australian Tourism Commission,

Great Barrier Reef Authority

Government agenciese.g. Australian Tourism Commission,

Great Barrier Reef Authority

Educational Institutionse.g. James Cook University,

Cairns College of TAFE

Educational Institutionse.g. James Cook University,

Cairns College of TAFE

Industry Groupse.g. Queensland Tourism

Industry Council

Industry Groupse.g. Queensland Tourism

Industry Council

FoodSuppliers

FoodSuppliers

Public Relations & Market Research

Services

Public Relations & Market Research

Services

Local retail, health care, andother services

Local retail, health care, andother services

12Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

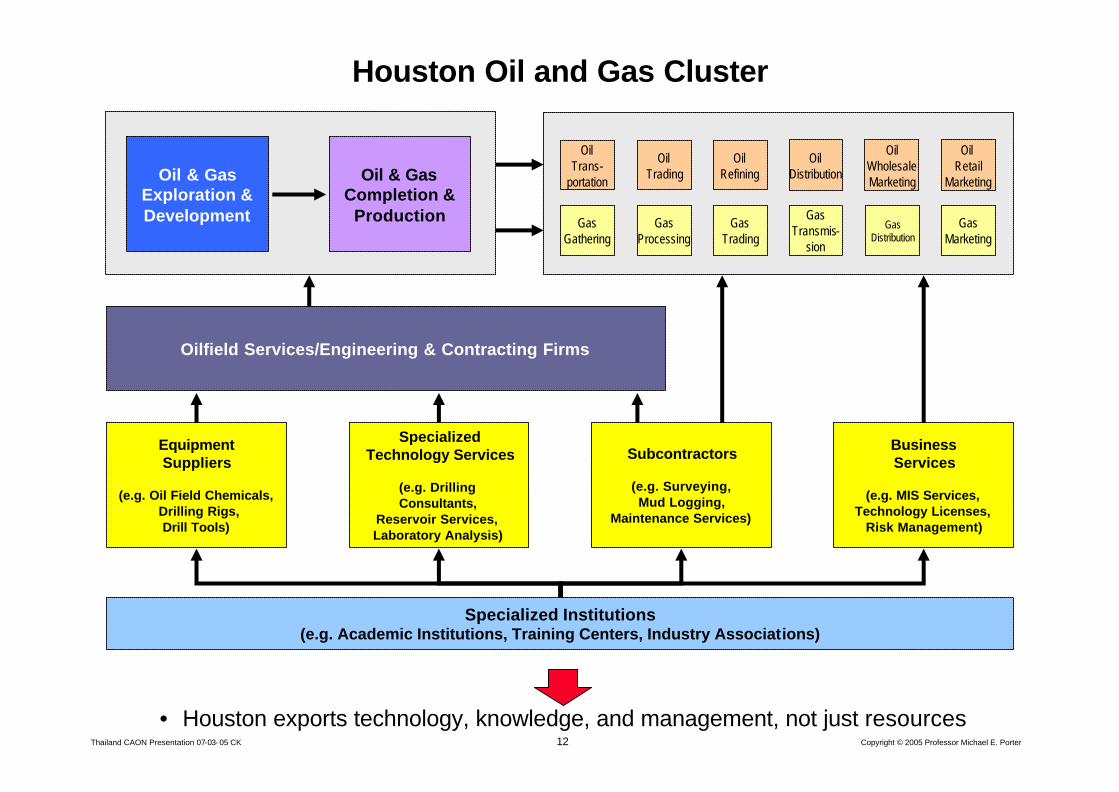

Houston Oil and Gas Cluster

• Houston exports technology, knowledge, and management, not just resources

Equipment Suppliers

(e.g. Oil Field Chemicals,Drilling Rigs, Drill Tools)

GasProcessing

GasTrading

GasTransmis-

sion

GasDistribution

GasMarketing

Oil & Gas Completion &

Production

Oil & GasExploration & Development

Oilfield Services/Engineering & Contracting Firms

OilRefining

OilDistribution

OilWholesaleMarketing

Oil Retail

Marketing

SpecializedTechnology Services

(e.g. Drilling Consultants,

Reservoir Services, Laboratory Analysis)

Subcontractors

(e.g. Surveying,Mud Logging,

Maintenance Services)

BusinessServices

(e.g. MIS Services,Technology Licenses,

Risk Management)

OilTrading

OilTrans-

portation

GasGathering

Specialized Institutions (e.g. Academic Institutions, Training Centers, Industry Associations)

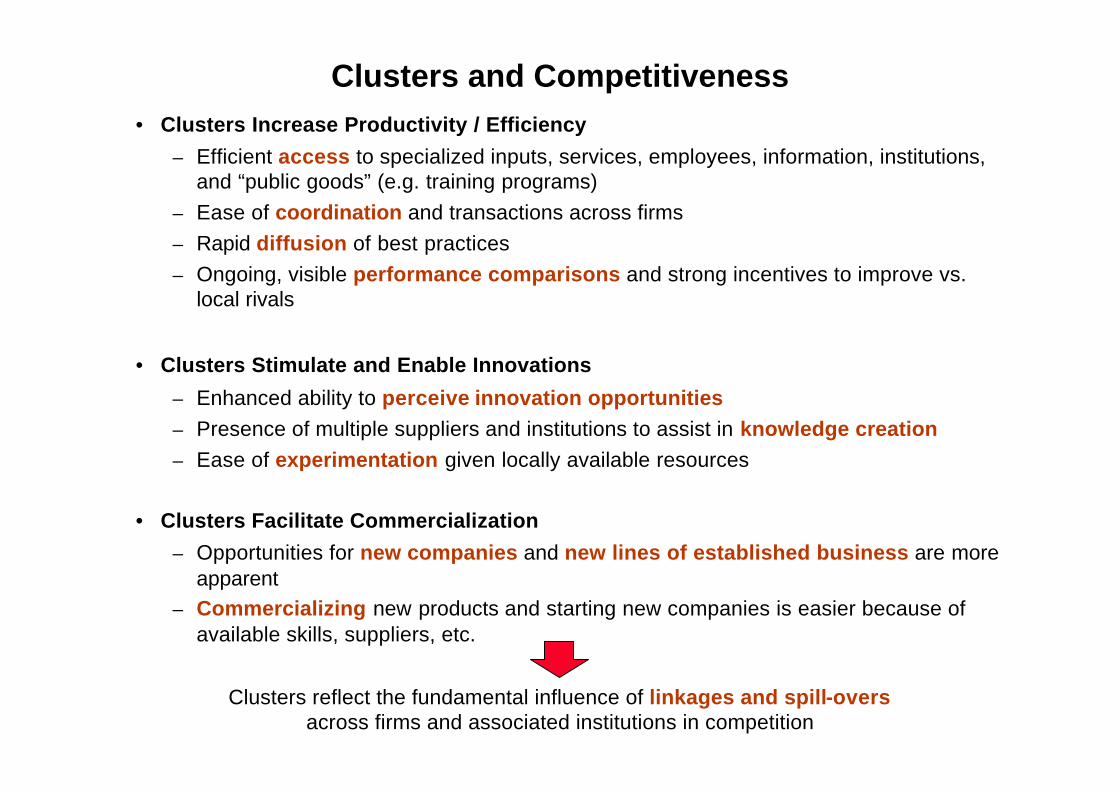

Clusters and Competitiveness• Clusters Increase Productivity / Efficiency

– Efficient access to specialized inputs, services, employees, information, institutions, and “public goods” (e.g. training programs)

– Ease of coordination and transactions across firms– Rapid diffusion of best practices– Ongoing, visible performance comparisons and strong incentives to improve vs.

local rivals

• Clusters Stimulate and Enable Innovations

– Enhanced ability to perceive innovation opportunities– Presence of multiple suppliers and institutions to assist in knowledge creation– Ease of experimentation given locally available resources

• Clusters Facilitate Commercialization

– Opportunities for new companies and new lines of established business are more apparent

– Commercializing new products and starting new companies is easier because of available skills, suppliers, etc.

Clusters reflect the fundamental influence of linkages and spill-oversacross firms and associated institutions in competition

14Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

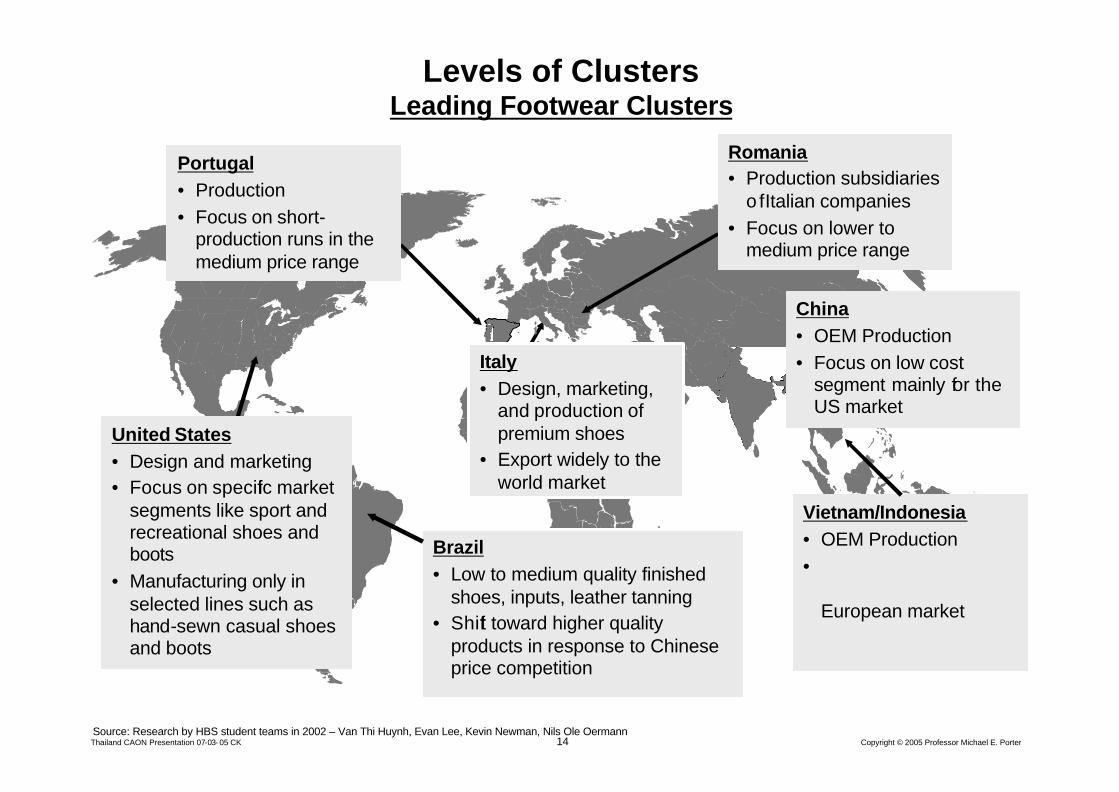

Levels of ClustersLeading Footwear Clusters

Vietnam/Indonesia• OEM Production •

European market

China• OEM Production• Focus on low cost

segment mainly for the US market

Portugal• Production • Focus on short-

production runs in the medium price range

Romania• Production subsidiaries

o f Italian companies• Focus on lower to

medium price range

United States• Design and marketing • Focus on specific market

segments like sport and recreational shoes and boots

• Manufacturing only in selected lines such as hand-sewn casual shoes and boots

Source: Research by HBS student teams in 2002 – Van Thi Huynh, Evan Lee, Kevin Newman, Nils Ole Oermann

Italy• Design, marketing,

and production of premium shoes

• Export widely to the world market

Brazil• Low to medium quality finished

shoes, inputs, leather tanning• Shift toward higher quality

products in response to Chinese price competition

15Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

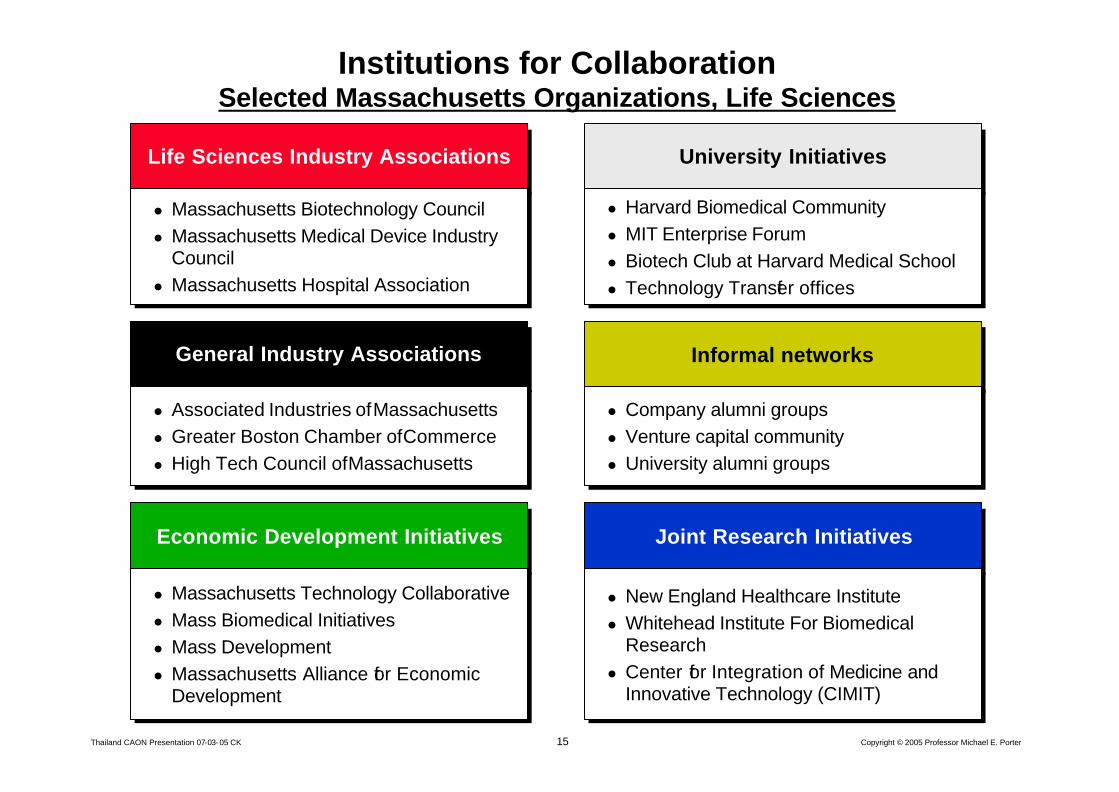

Institutions for CollaborationSelected Massachusetts Organizations, Life Sciences

Economic Development InitiativesEconomic Development Initiatives

l Massachusetts Technology Collaborativel Mass Biomedical Initiativesl Mass Developmentl Massachusetts Alliance for Economic

Development

l Massachusetts Technology Collaborativel Mass Biomedical Initiativesl Mass Developmentl Massachusetts Alliance for Economic

Development

Life Sciences Industry AssociationsLife Sciences Industry Associations

l Massachusetts Biotechnology Councill Massachusetts Medical Device Industry

Councill Massachusetts Hospital Association

l Massachusetts Biotechnology Councill Massachusetts Medical Device Industry

Councill Massachusetts Hospital Association

General Industry AssociationsGeneral Industry Associations

l Associated Industries of Massachusettsl Greater Boston Chamber of Commercel High Tech Council of Massachusetts

l Associated Industries of Massachusettsl Greater Boston Chamber of Commercel High Tech Council of Massachusetts

University InitiativesUniversity Initiatives

l Harvard Biomedical Communityl MIT Enterprise Foruml Biotech Club at Harvard Medical Schooll Technology Transfer offices

l Harvard Biomedical Communityl MIT Enterprise Foruml Biotech Club at Harvard Medical Schooll Technology Transfer offices

Informal networksInformal networks

l Company alumni groupsl Venture capital communityl University alumni groups

l Company alumni groupsl Venture capital communityl University alumni groups

Joint Research InitiativesJoint Research Initiatives

l New England Healthcare Institutel Whitehead Institute For Biomedical

Researchl Center for Integration of Medicine and

Innovative Technology (CIMIT)

l New England Healthcare Institutel Whitehead Institute For Biomedical

Researchl Center for Integration of Medicine and

Innovative Technology (CIMIT)

16Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

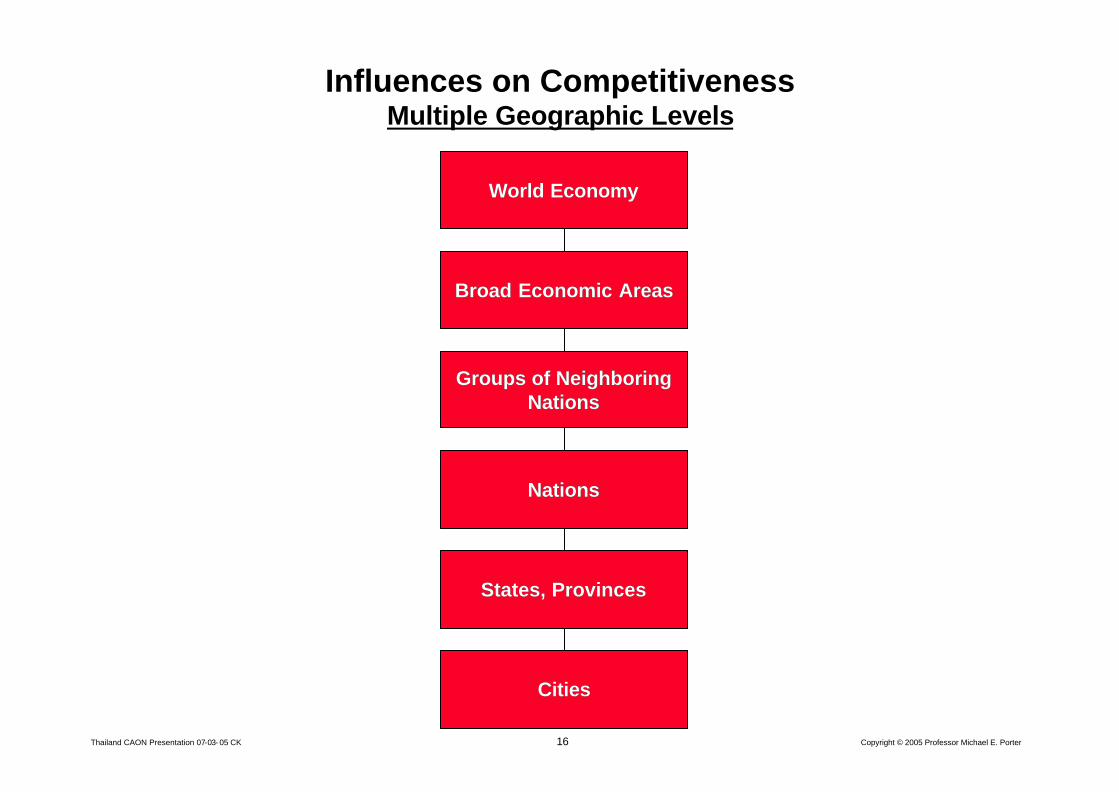

Influences on CompetitivenessMultiple Geographic Levels

Broad Economic AreasBroad Economic Areas

Groups of Neighboring Groups of Neighboring NationsNations

States, ProvincesStates, Provinces

CitiesCities

NationsNations

World EconomyWorld Economy

17Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

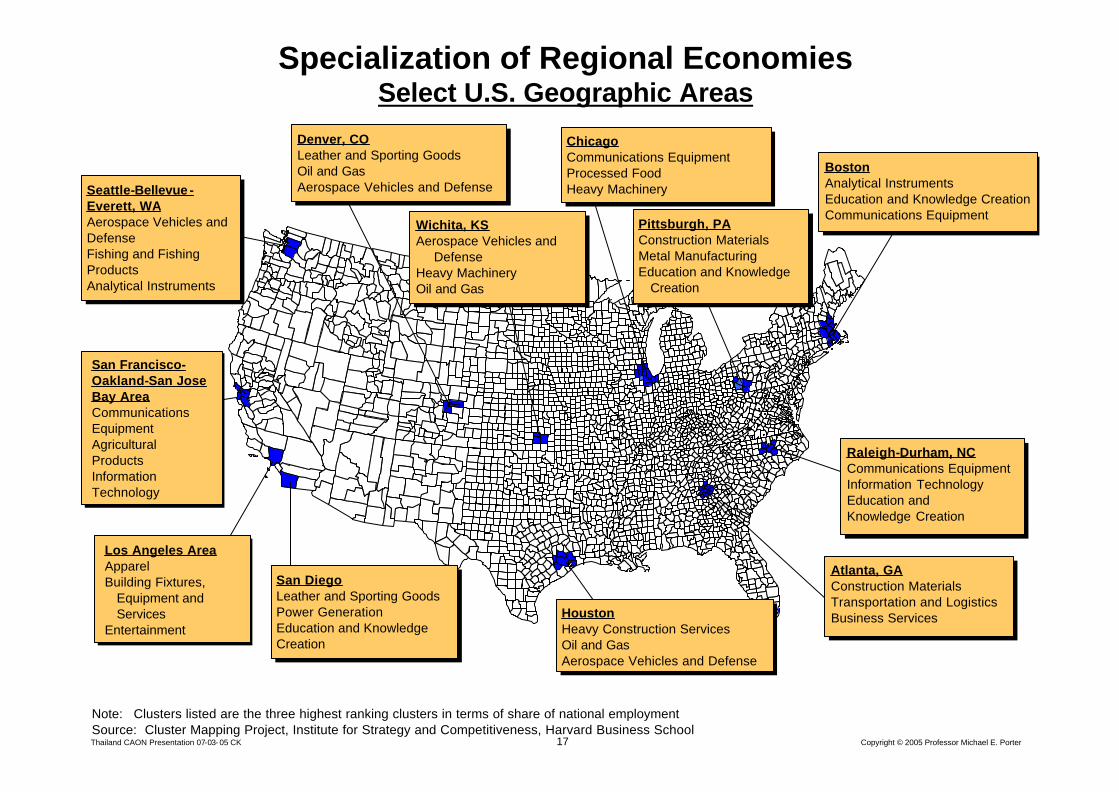

Specialization of Regional EconomiesSelect U.S. Geographic Areas

BostonAnalytical InstrumentsEducation and Knowledge CreationCommunications Equipment

BostonAnalytical InstrumentsEducation and Knowledge CreationCommunications Equipment

Los Angeles AreaApparelBuilding Fixtures,

Equipment and Services

Entertainment

Los Angeles AreaApparelBuilding Fixtures,

Equipment and Services

Entertainment

ChicagoCommunications EquipmentProcessed FoodHeavy Machinery

ChicagoCommunications EquipmentProcessed FoodHeavy Machinery

Denver, COLeather and Sporting GoodsOil and GasAerospace Vehicles and Defense

Denver, COLeather and Sporting GoodsOil and GasAerospace Vehicles and Defense

San DiegoLeather and Sporting GoodsPower GenerationEducation and Knowledge Creation

San DiegoLeather and Sporting GoodsPower GenerationEducation and Knowledge Creation

San Francisco-Oakland-San Jose Bay AreaCommunications EquipmentAgricultural ProductsInformation Technology

San Francisco-Oakland-San Jose Bay AreaCommunications EquipmentAgricultural ProductsInformation Technology

Seattle-Bellevue -Everett, WAAerospace Vehicles and DefenseFishing and Fishing ProductsAnalytical Instruments

Seattle-Bellevue -Everett, WAAerospace Vehicles and DefenseFishing and Fishing ProductsAnalytical Instruments

HoustonHeavy Construction ServicesOil and GasAerospace Vehicles and Defense

HoustonHeavy Construction ServicesOil and GasAerospace Vehicles and Defense

Pittsburgh, PAConstruction MaterialsMetal ManufacturingEducation and Knowledge

Creation

Pittsburgh, PAConstruction MaterialsMetal ManufacturingEducation and Knowledge

Creation

Atlanta, GAConstruction MaterialsTransportation and LogisticsBusiness Services

Atlanta, GAConstruction MaterialsTransportation and LogisticsBusiness Services

Raleigh-Durham, NCCommunications EquipmentInformation TechnologyEducation andKnowledge Creation

Raleigh-Durham, NCCommunications EquipmentInformation TechnologyEducation andKnowledge Creation

Wichita, KSAerospace Vehicles and

DefenseHeavy MachineryOil and Gas

Wichita, KSAerospace Vehicles and

DefenseHeavy MachineryOil and Gas

Note: Clusters listed are the three highest ranking clusters in terms of share of national employmentSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

18Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

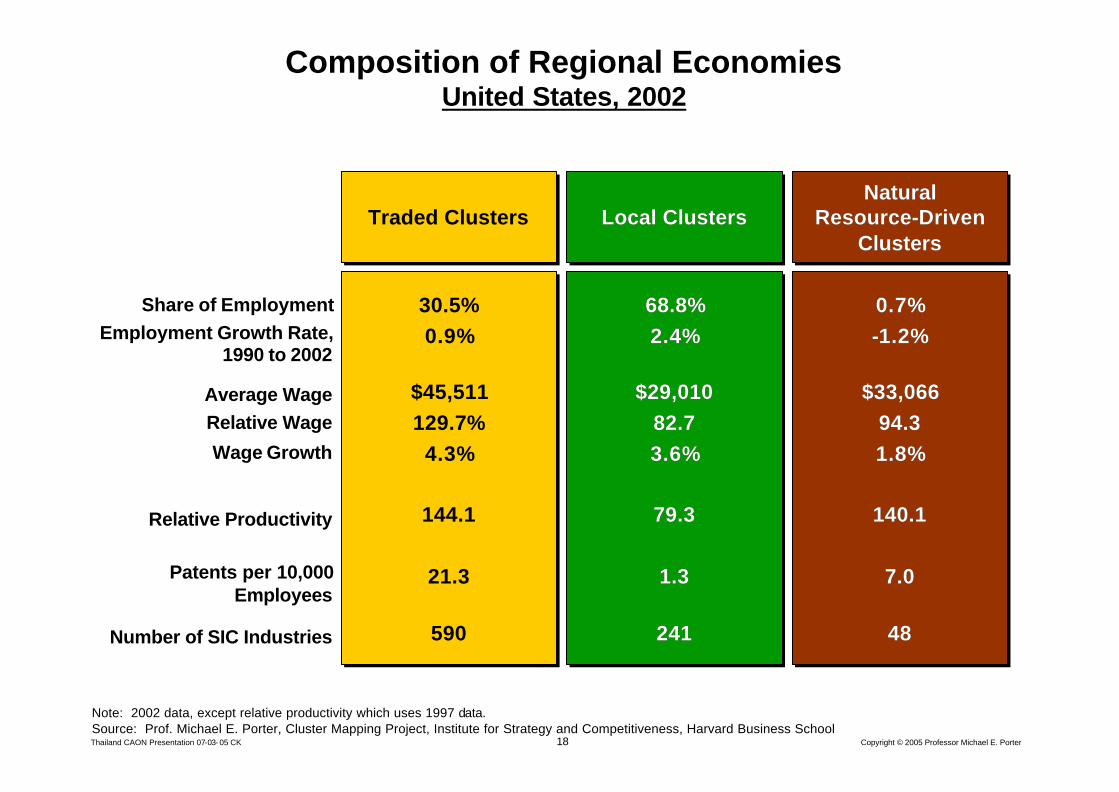

Traded ClustersTraded Clusters

30.5%0.9%

$45,511129.7%

4.3%

144.1

21.3

590

30.5%0.9%

$45,511129.7%

4.3%

144.1

21.3

590

Local ClustersLocal ClustersLocal Clusters

68.8%2.4%

$29,01082.73.6%

79.3

1.3

241

68.8%68.8%2.4%2.4%

$29,010$29,01082.782.73.6%3.6%

79.379.3

1.31.3

241241

NaturalResource-Driven

Clusters

NaturalNaturalResourceResource--Driven Driven

ClustersClusters

0.7%-1.2%

$33,06694.31.8%

140.1

7.0

48

0.7%0.7%--1.2%1.2%

$33,066$33,06694.394.31.8%1.8%

140.1140.1

7.07.0

4848

Share of EmploymentEmployment Growth Rate,

1990 to 2002

Average WageRelative Wage

Wage Growth

Relative Productivity

Patents per 10,000 Employees

Number of SIC Industries

Note: 2002 data, except relative productivity which uses 1997 data.Source: Prof. Michael E. Porter, Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Composition of Regional EconomiesUnited States, 2002

19Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

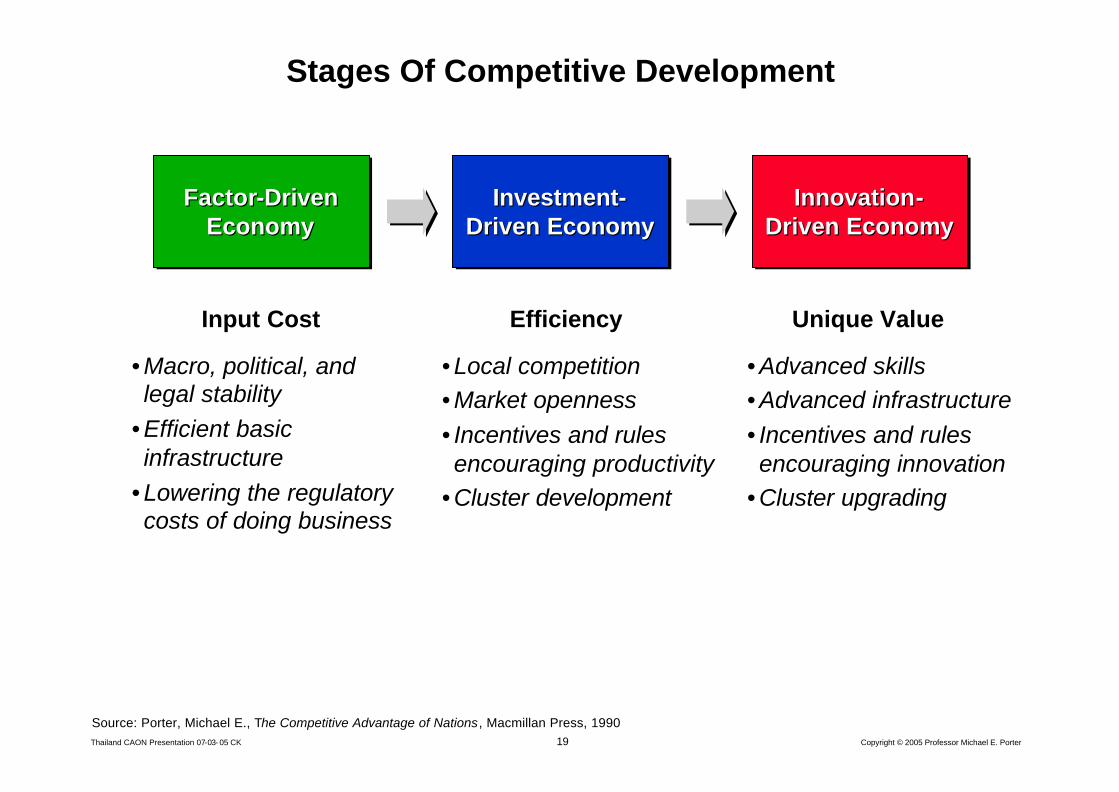

Stages Of Competitive Development

Factor-Driven Economy

FactorFactor--Driven Driven EconomyEconomy

Investment-Driven Economy

InvestmentInvestment--Driven EconomyDriven Economy

Innovation-Driven Economy

InnovationInnovation--Driven EconomyDriven Economy

Source: Porter, Michael E., The Competitive Advantage of Nations, Macmillan Press, 1990

Input Cost Efficiency Unique Value

• Macro, political, and legal stability

• Efficient basic infrastructure

• Lowering the regulatory costs of doing business

• Local competition• Market openness• Incentives and rulesencouraging productivity

• Cluster development

• Advanced skills• Advanced infrastructure• Incentives and rulesencouraging innovation

• Cluster upgrading

20Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

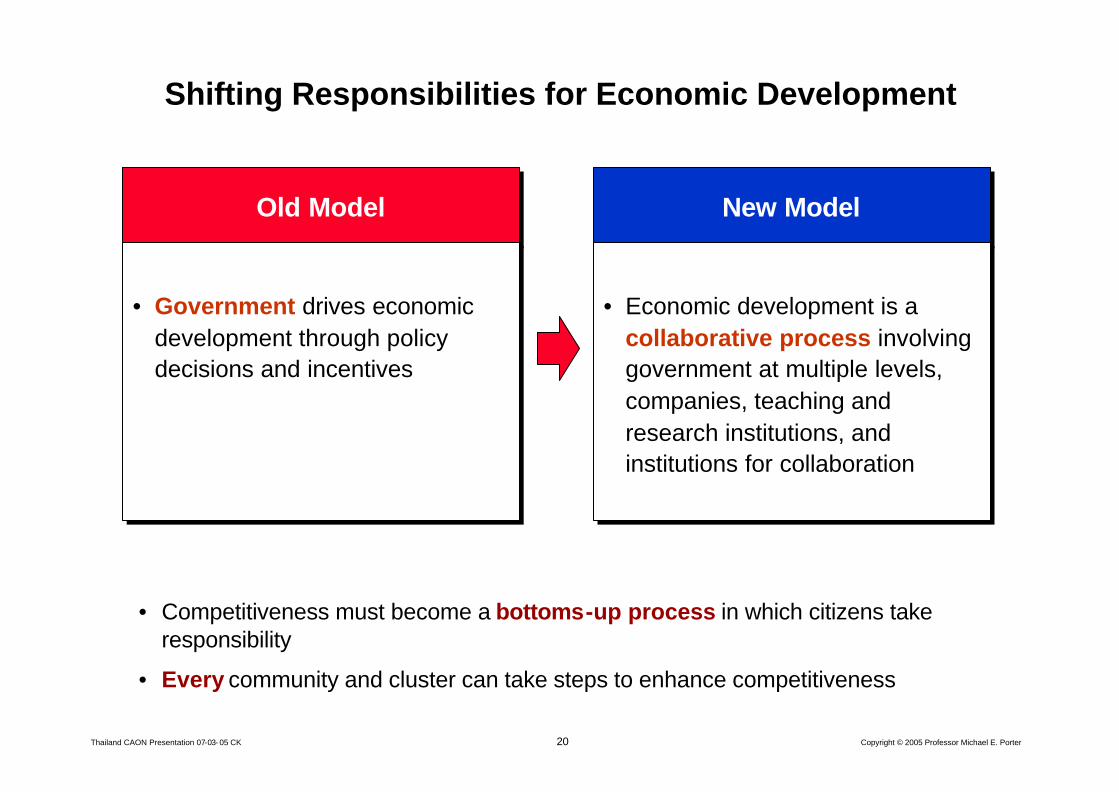

Shifting Responsibilities for Economic Development

Old ModelOld Model

• Government drives economic development through policy decisions and incentives

• Government drives economic development through policy decisions and incentives

New ModelNew Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Competitiveness must become a bottoms-up process in which citizens take responsibility

• Every community and cluster can take steps to enhance competitiveness

21Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Assessing Thailand’s CompetitivenessResults

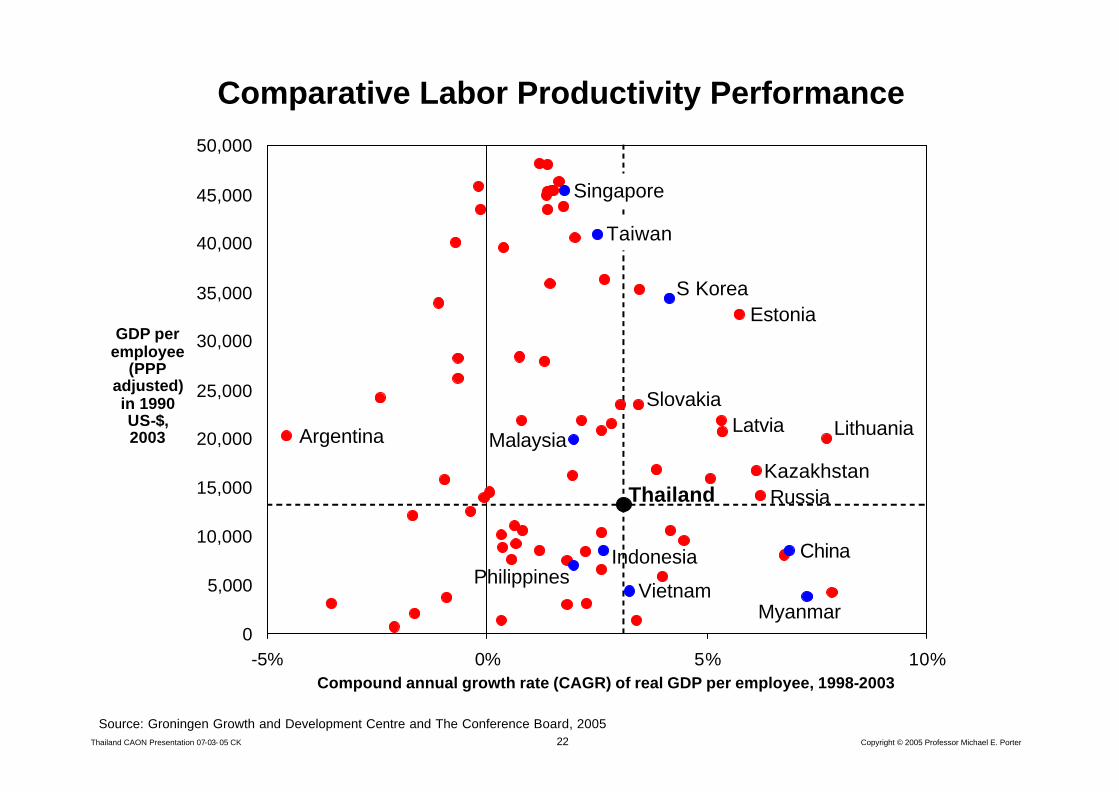

• Labor productivity remains relatively low but has been growing at a steady rate in recent years

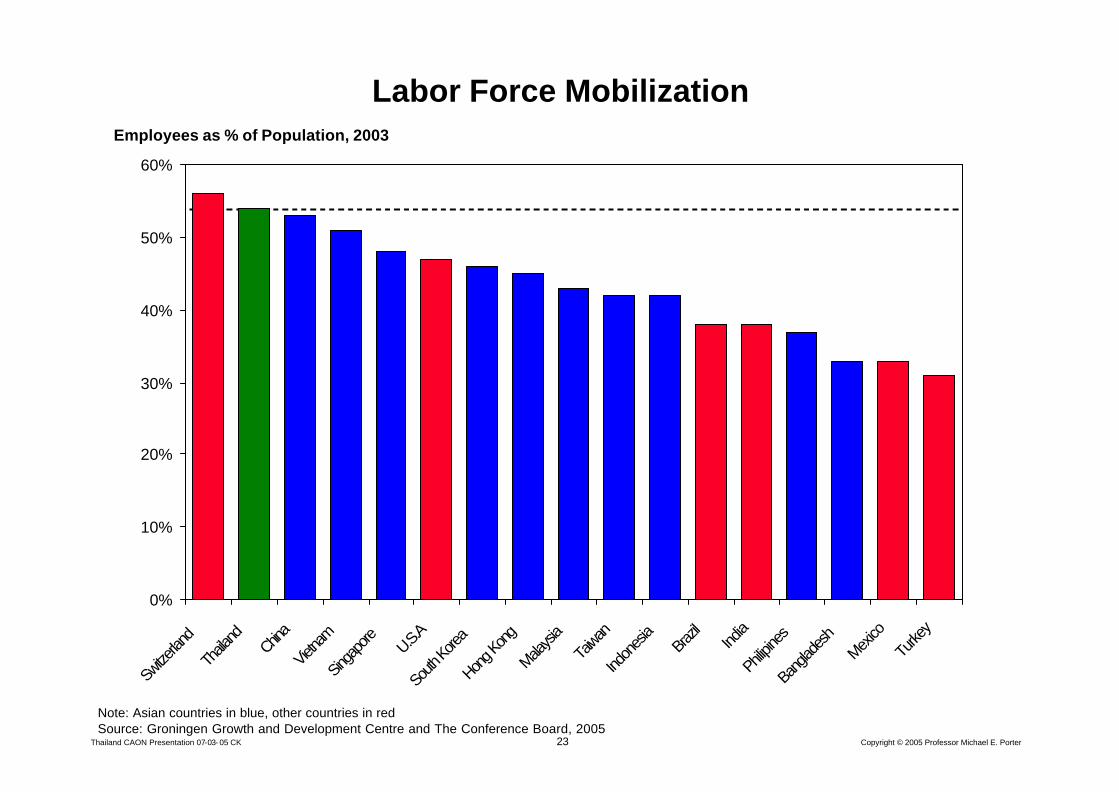

• Labor force mobilization is high

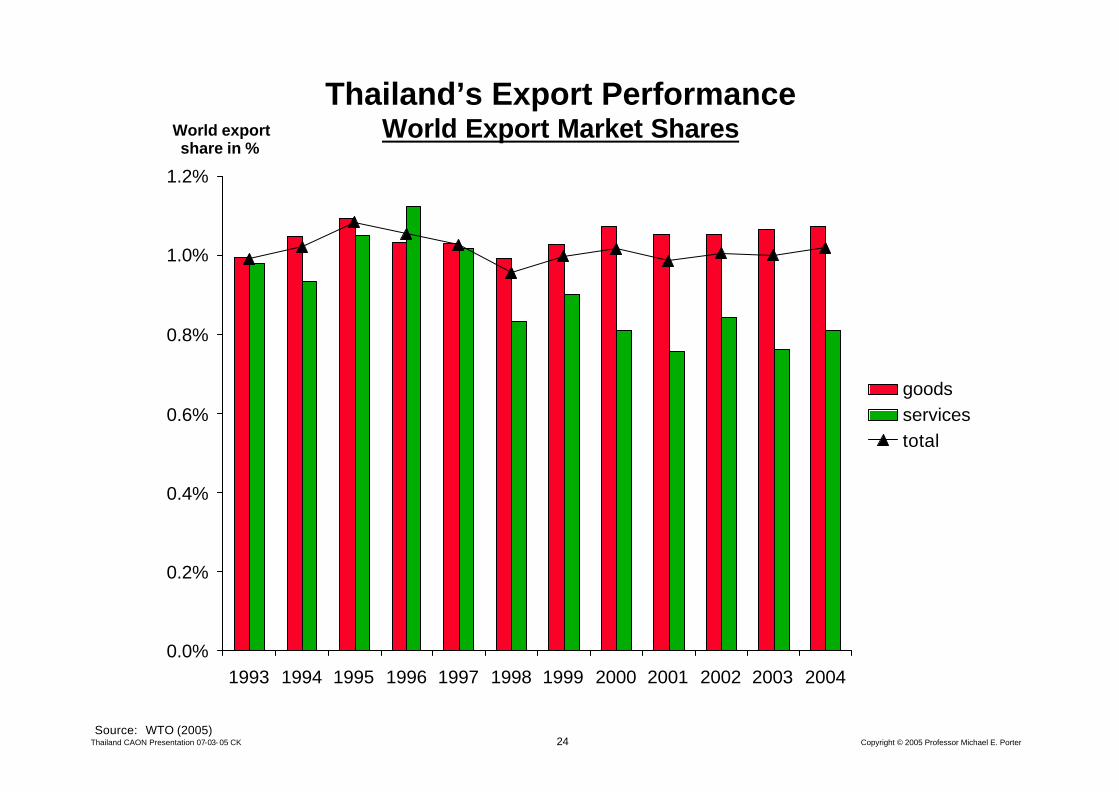

• Thailand’s overall world export market share has been stable over time– Services (especially tourism) have not regained their position from the

mid 1990s

• Moderate level of FDI; behind leading peers in the region

• Weak on patenting

22Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Taiwan

Singapore

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

-5% 0% 5% 10%

Comparative Labor Productivity Performance

Compound annual growth rate (CAGR) of real GDP per employee, 1998-2003

GDP per employee

(PPP adjusted) in 1990 US-$, 2003

Source: Groningen Growth and Development Centre and The Conference Board, 2005

Thailand

Latvia LithuaniaArgentina

China

MyanmarVietnam

PhilippinesIndonesia

KazakhstanRussia

S Korea

Slovakia

Malaysia

Estonia

23Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Labor Force Mobilization

0%

10%

20%

30%

40%

50%

60%

Switze

rland

Thaila

ndChin

a

Vietna

m

Singa

pore

U.S.A

South

Korea

Hong K

ong

Malaysi

aTa

iwan

Indon

esia

Brazil

India

Philipin

es

Bang

lades

hMex

icoTu

rkey

Employees as % of Population, 2003

Note: Asian countries in blue, other countries in red Source: Groningen Growth and Development Centre and The Conference Board, 2005

24Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Thailand’s Export PerformanceWorld Export Market Shares

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

goodsservicestotal

Source: WTO (2005)

World export share in %

25Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

0%

10%

20%

30%

40%

50%

60%

70%

80%

0% 10% 20% 30% 40% 50% 60%

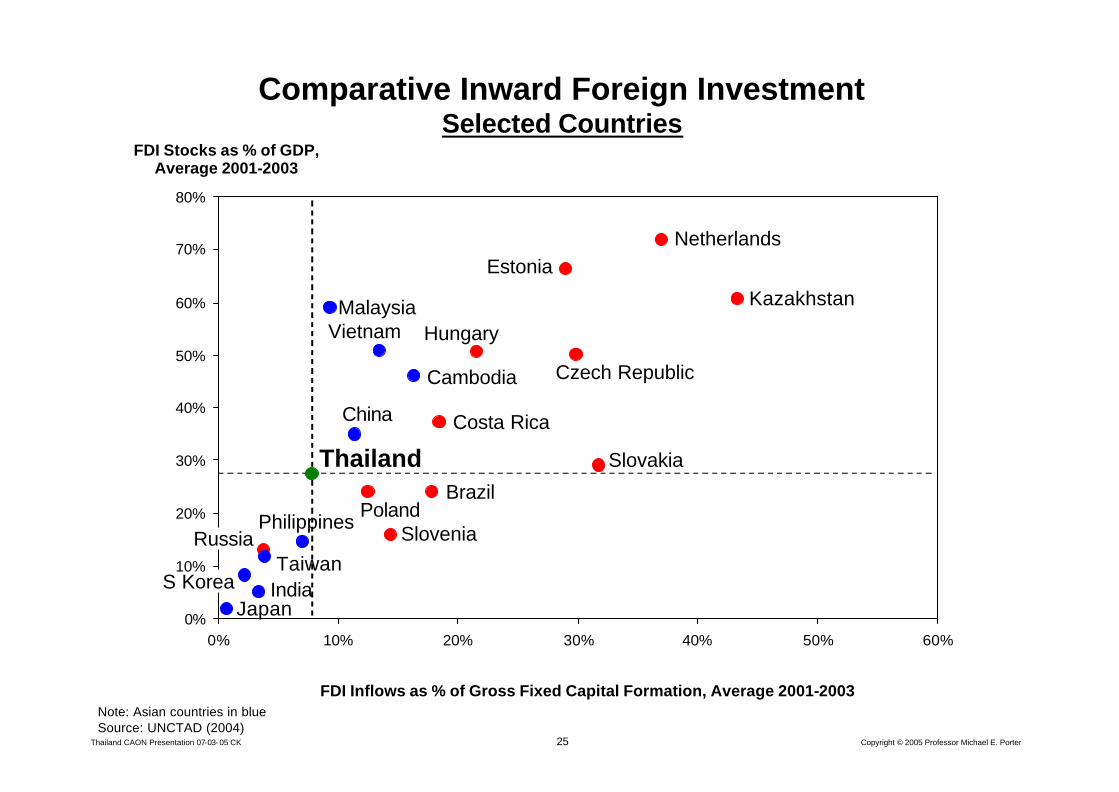

Comparative Inward Foreign InvestmentSelected Countries

FDI Stocks as % of GDP, Average 2001-2003

FDI Inflows as % of Gross Fixed Capital Formation, Average 2001-2003Note: Asian countries in blueSource: UNCTAD (2004)

Vietnam

Japan

Netherlands

Brazil

Costa Rica

Kazakhstan

Cambodia

China

India

Malaysia

Philippines

Taiwan

Thailand

Czech Republic

Estonia

Hungary

Poland

S Korea

Russia

Slovakia

Slovenia

26Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

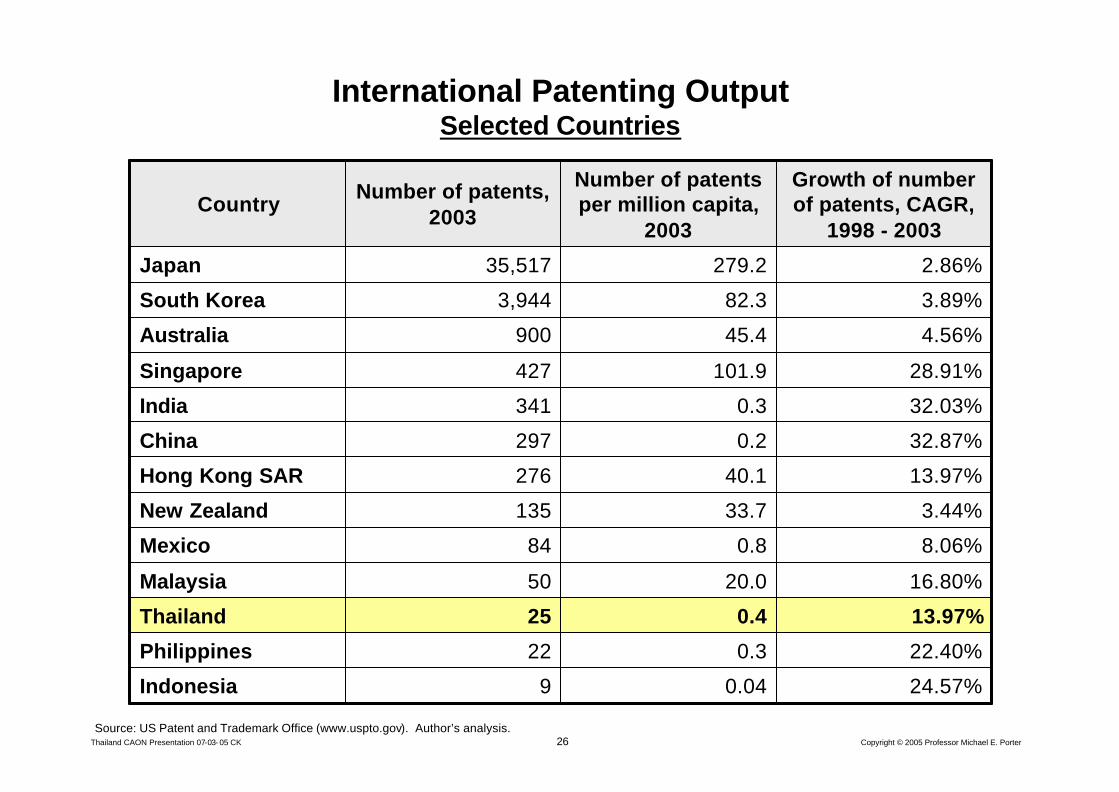

International Patenting OutputSelected Countries

24.57%0.049Indonesia

22.40%0.322Philippines

13.97%0.425Thailand

16.80%20.050Malaysia

8.06%0.884Mexico

3.44%33.7135New Zealand

13.97%40.1276Hong Kong SAR

32.87%0.2297China

32.03%0.3341India

28.91%101.9427Singapore

4.56%45.4900Australia

3.89%82.33,944South Korea

2.86%279.235,517Japan

Growth of number of patents, CAGR,

1998 - 2003

Number of patents per million capita,

2003

Number of patents, 2003

Country

Source: US Patent and Trademark Office (www.uspto.gov). Author’s analysis.

27Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

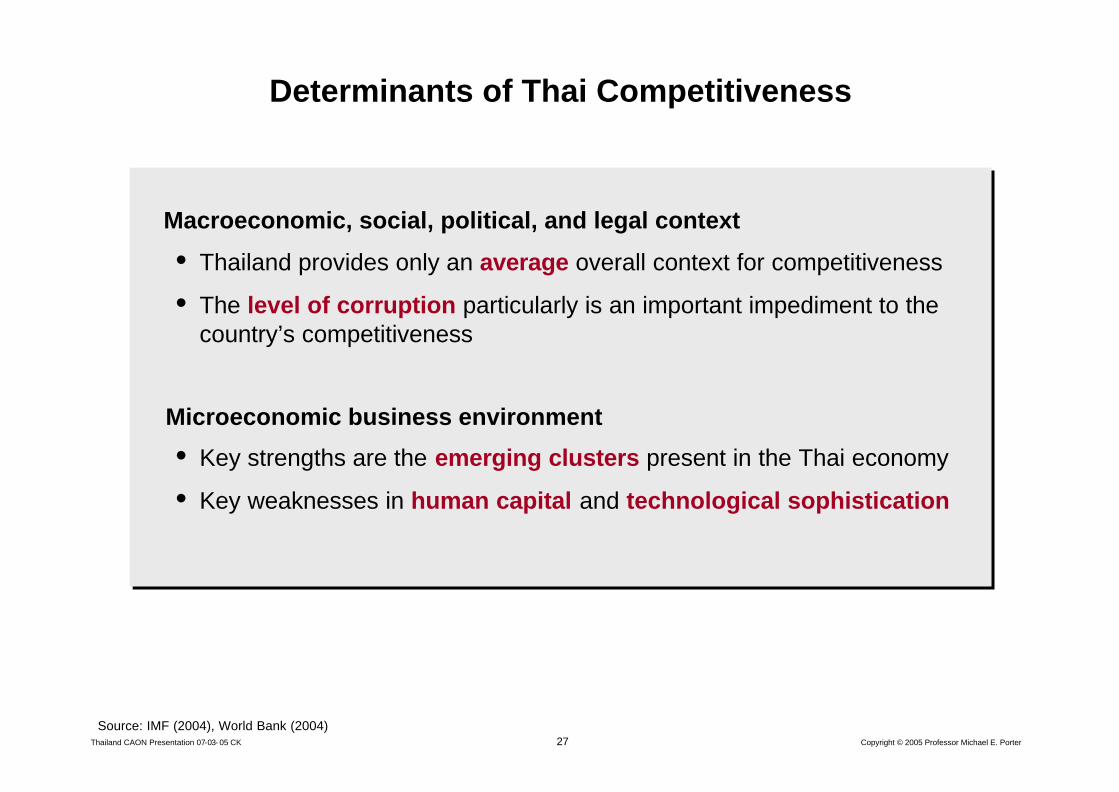

Determinants of Thai Competitiveness

Macroeconomic, social, political, and legal context

• Thailand provides only an average overall context for competitiveness

• The level of corruption particularly is an important impediment to the country’s competitiveness

Microeconomic business environment

• Key strengths are the emerging clusters present in the Thai economy

• Key weaknesses in human capital and technological sophistication

Macroeconomic, social, political, and legal context

• Thailand provides only an average overall context for competitiveness

• The level of corruption particularly is an important impediment to the country’s competitiveness

Microeconomic business environment

• Key strengths are the emerging clusters present in the Thai economy

• Key weaknesses in human capital and technological sophistication

Source: IMF (2004), World Bank (2004)

28Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

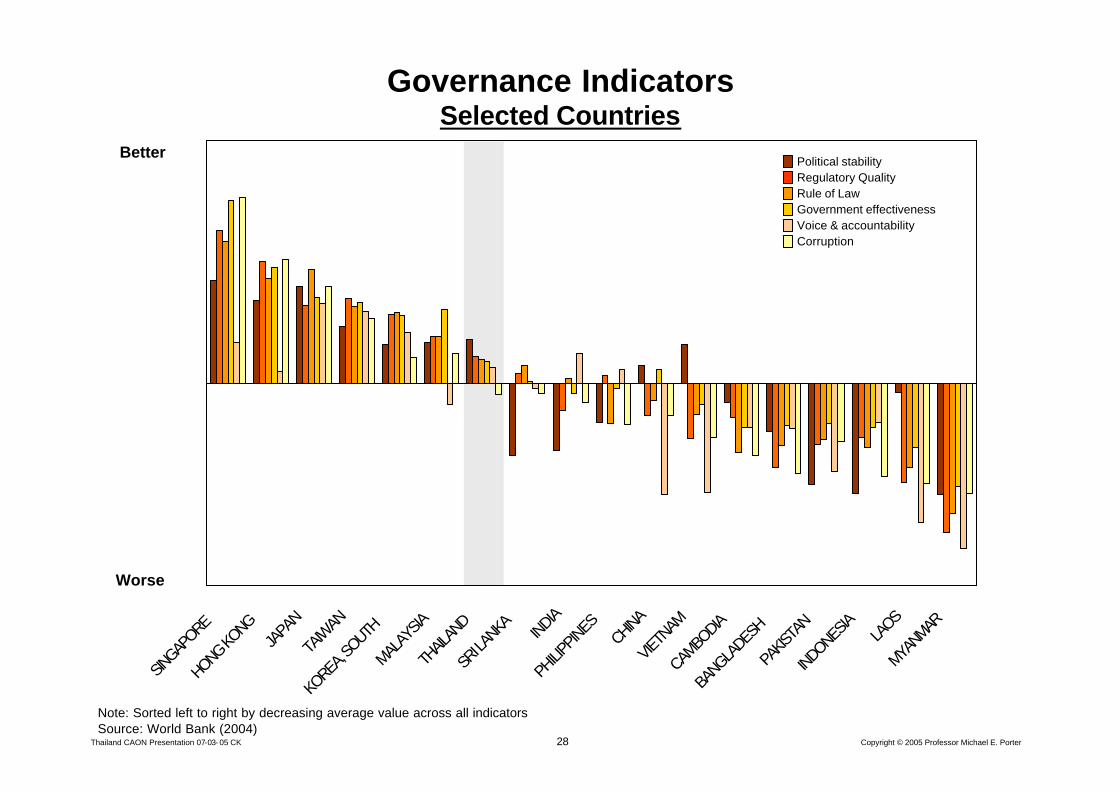

Governance IndicatorsSelected Countries

SINGAP

ORE

HONG KONG

JAPA

N

TAIW

AN

KOREA

, SOUTH

MALAY

SIA

THAIL

AND

SRI LA

NKA INDIA

PHILIP

PINES

CHINA

VIETN

AM

CAMBO

DIA

BANGLA

DESH

PAKIS

TAN

INDONESIA

LAOS

MYANM

AR

Note: Sorted left to right by decreasing average value across all indicatorsSource: World Bank (2004)

Better

Worse

Corruption

Regulatory QualityRule of LawGovernment effectivenessVoice & accountability

Political stability

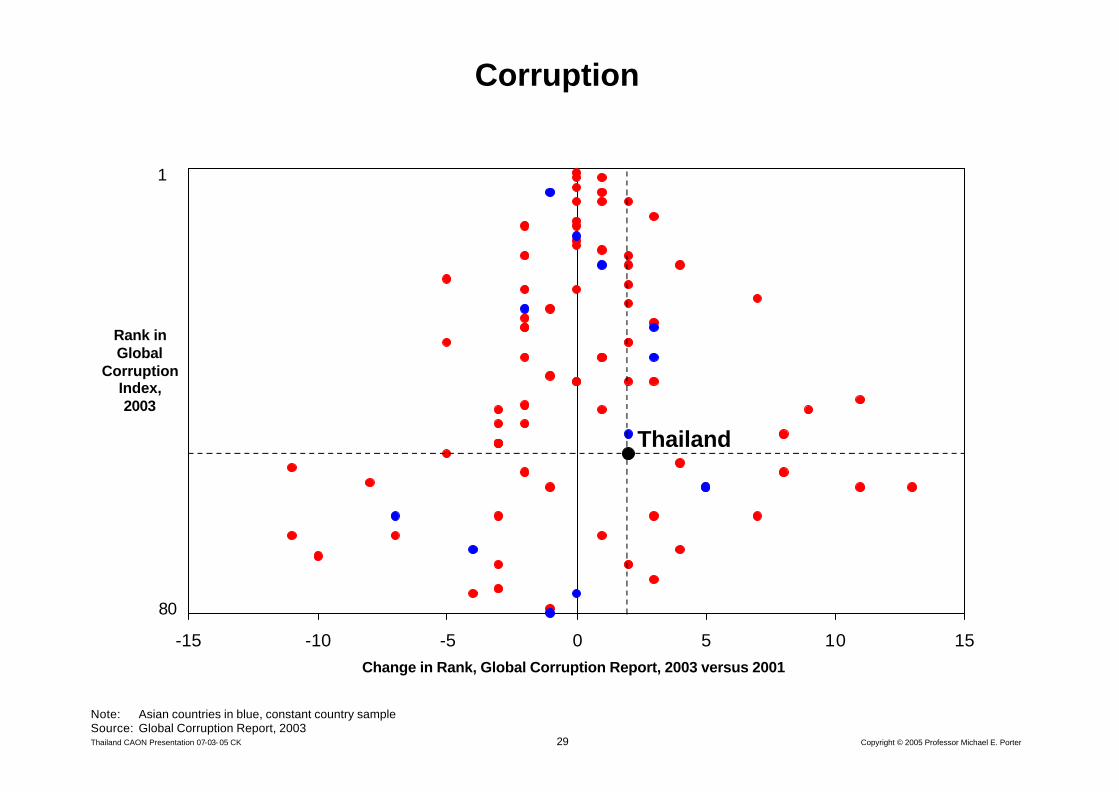

29Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

-15 -10 -5 0 5 10 15

Corruption

Thailand

Note: Asian countries in blue, constant country sampleSource: Global Corruption Report, 2003

Change in Rank, Global Corruption Report, 2003 versus 2001

Rank in Global

CorruptionIndex,2003

80

1

30Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Business Competitiveness Index Rankings, 2004

123456789

10111213141516171819202122232425

123456789

10111213141516171819202122232425

RankRank Country

United StatesFinland

GermanySweden

SwitzerlandUnited Kingdom

DenmarkJapan

NetherlandsSingapore

Hong Kong SARFrance

AustraliaBelgiumCanadaAustriaTaiwan

New ZealandIcelandNorwayIsraelIreland

MalaysiaS Korea

South Africa

26272829303132333435363738394041424344454647484950

26272829303132333435363738394041424344454647484950

RankRank Country

SpainEstoniaChileIndia

SloveniaTunisiaPortugal

ItalyCzech Republic

LithuaniaThailand

BrazilSlovak Republic

GreeceHungaryJordan

IndonesiaCyprus

MoroccoChina

Costa RicaLatviaMalta

NamibiaTurkey

31Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

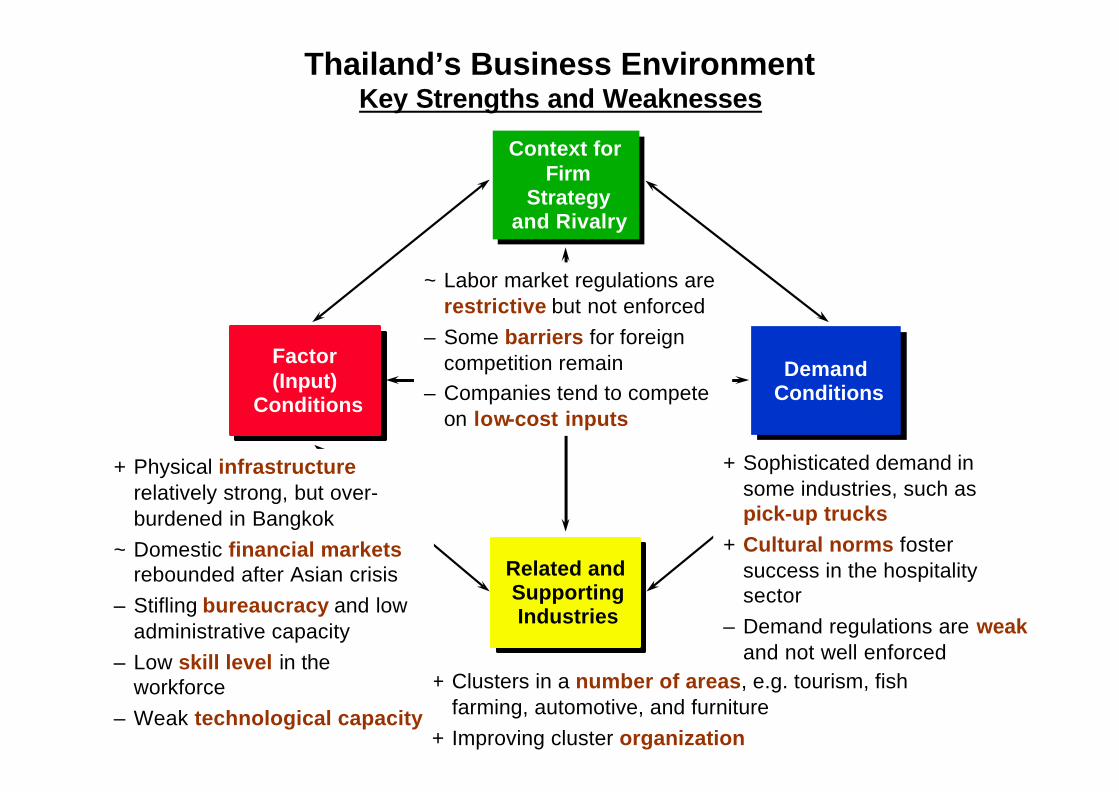

+ Clusters in a number of areas, e.g. tourism, fish farming, automotive, and furniture

+ Improving cluster organization

Thailand’s Business EnvironmentKey Strengths and Weaknesses

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

+ Physical infrastructurerelatively strong, but over-burdened in Bangkok

~ Domestic financial markets rebounded after Asian crisis

– Stifling bureaucracy and low administrative capacity

– Low skill level in the workforce

– Weak technological capacity

+ Sophisticated demand in some industries, such as pick-up trucks

+ Cultural norms foster success in the hospitality sector

– Demand regulations are weakand not well enforced

~ Labor market regulations are restrictive but not enforced

– Some barriers for foreign competition remain

– Companies tend to compete on low-cost inputs

32Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

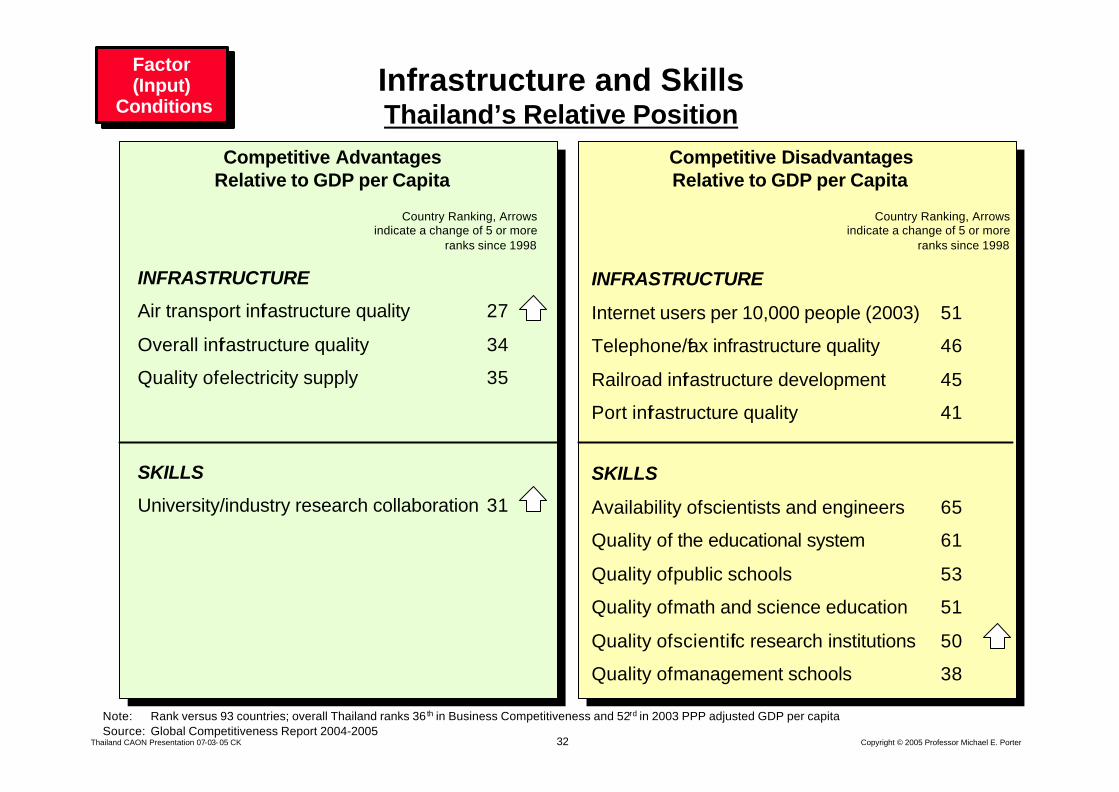

Infrastructure and SkillsThailand’s Relative Position

Factor(Input)

Conditions

Factor(Input)

Conditions

INFRASTRUCTURE

Air transport infrastructure quality 27

Overall infrastructure quality 34

Quality of electricity supply 35

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

INFRASTRUCTURE

Internet users per 10,000 people (2003) 51

Telephone/fax infrastructure quality 46

Railroad infrastructure development 45

Port infrastructure quality 41

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

SKILLS

University/industry research collaboration 31

SKILLS

Availability of scientists and engineers 65

Quality of the educational system 61

Quality of public schools 53

Quality of math and science education 51

Quality of scientific research institutions 50

Quality of management schools 38

33Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

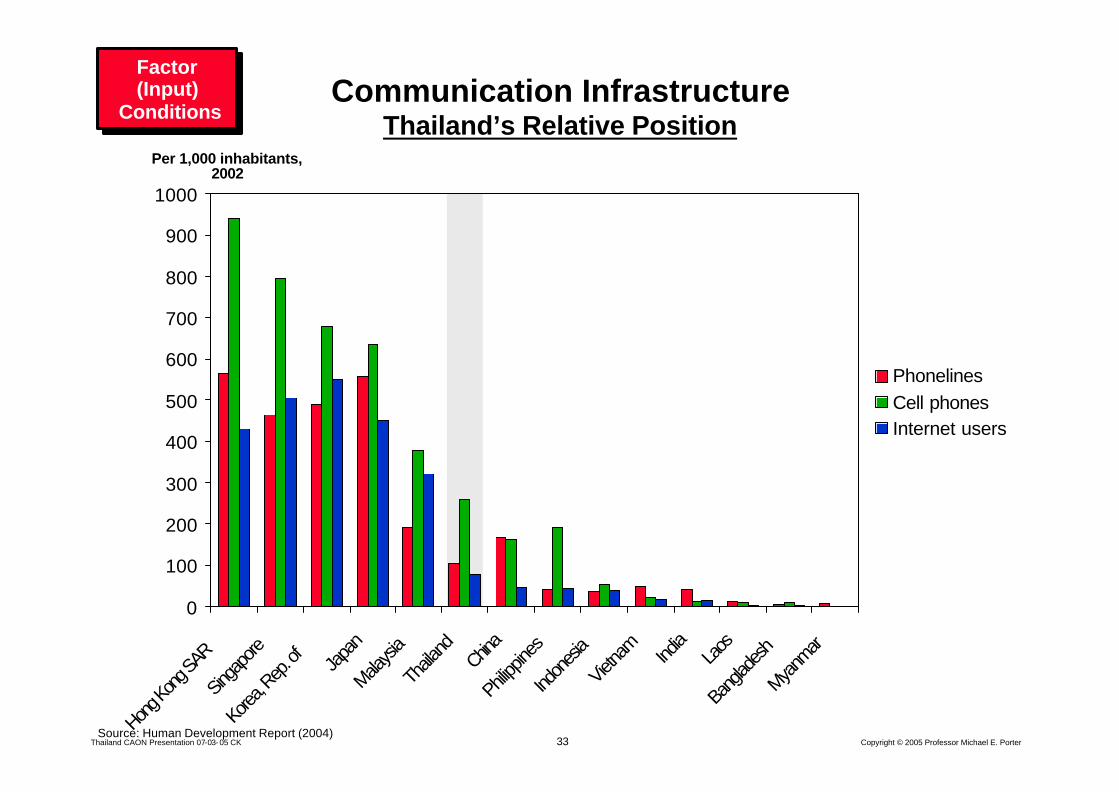

Communication InfrastructureThailand’s Relative Position

0

100

200

300

400

500

600

700

800

900

1000

Hong K

ong S

AR

Singa

pore

Korea

, Rep

. of Japa

n

Malaysi

a

Thaila

ndChin

a

Philipp

ines

Indon

esia

Vietna

mInd

iaLa

os

Bang

lades

h

Myanm

ar

PhonelinesCell phonesInternet users

Per 1,000 inhabitants, 2002

Source: Human Development Report (2004)

Factor(Input)

Conditions

Factor(Input)

Conditions

34Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

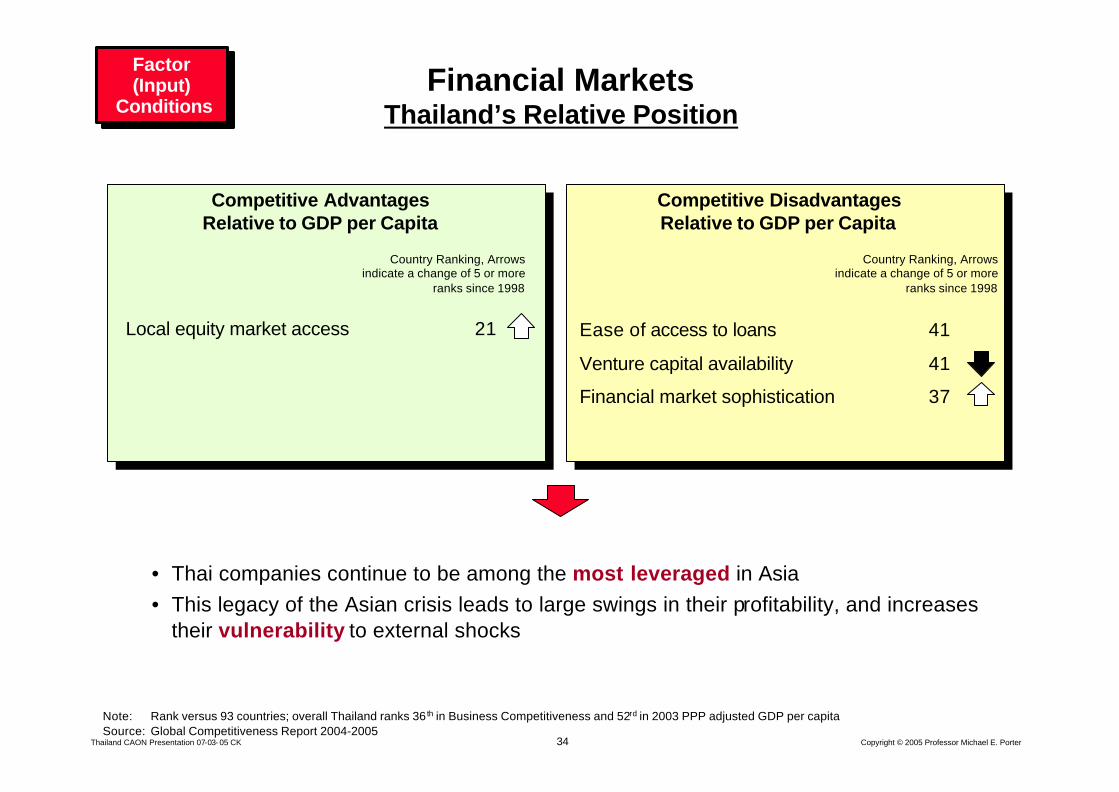

Financial MarketsThailand’s Relative Position

Factor(Input)

Conditions

Factor(Input)

Conditions

Local equity market access 21

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

Ease of access to loans 41

Venture capital availability 41

Financial market sophistication 37

• Thai companies continue to be among the most leveraged in Asia• This legacy of the Asian crisis leads to large swings in their profitability, and increases

their vulnerability to external shocks

35Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

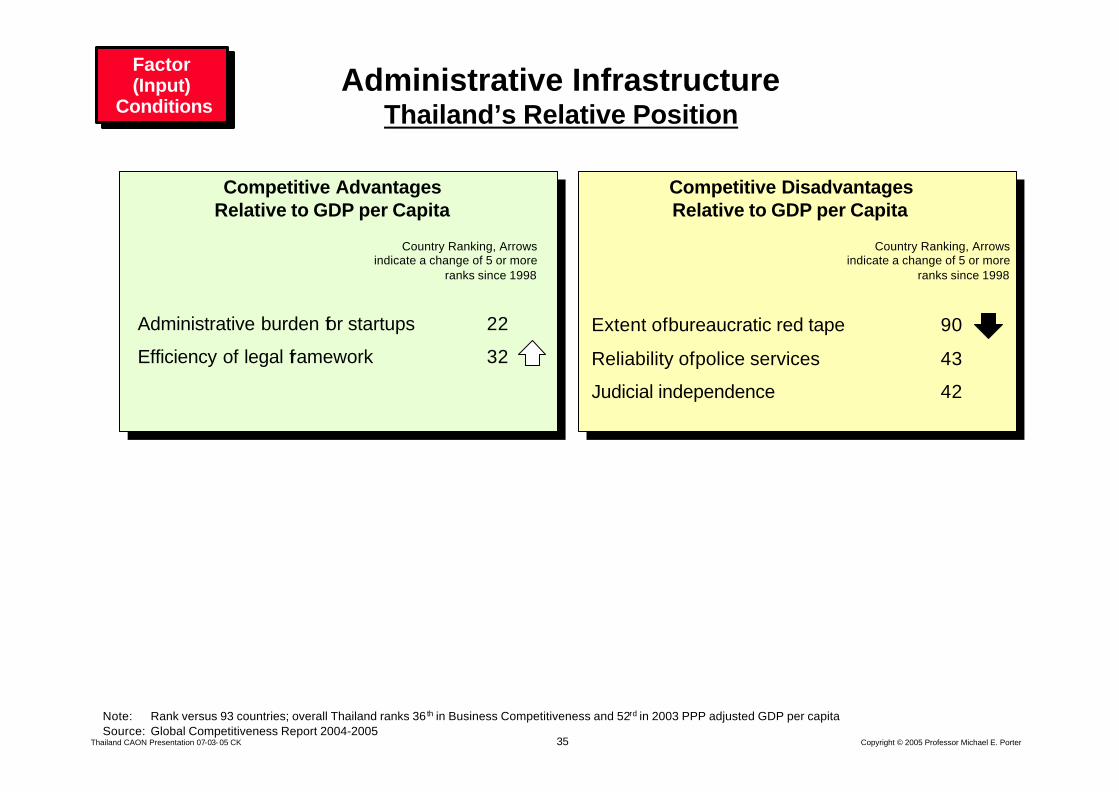

Administrative InfrastructureThailand’s Relative Position

Factor(Input)

Conditions

Factor(Input)

Conditions

Administrative burden for startups 22

Efficiency of legal framework 32

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Extent of bureaucratic red tape 90

Reliability of police services 43

Judicial independence 42

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

36Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

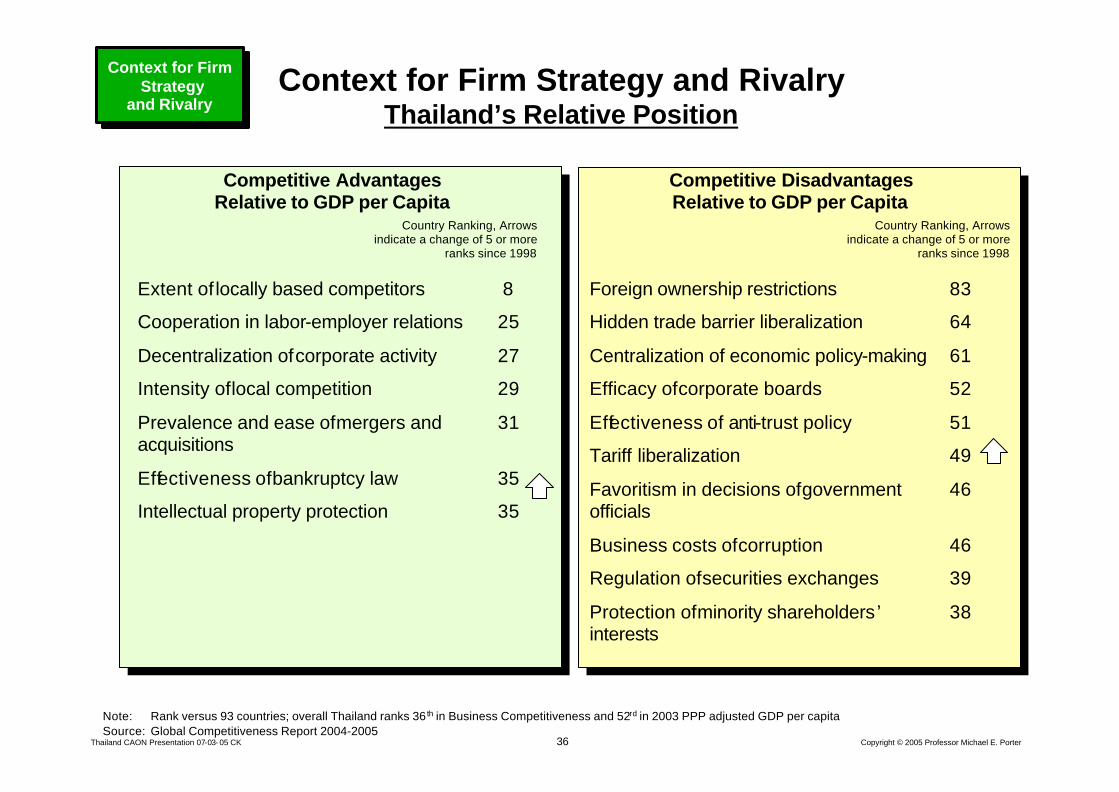

Context for Firm Strategy and RivalryThailand’s Relative Position

Extent of locally based competitors 8

Cooperation in labor-employer relations 25

Decentralization of corporate activity 27

Intensity of local competition 29

Prevalence and ease of mergers and 31 acquisitions

Effectiveness of bankruptcy law 35

Intellectual property protection 35

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Context for Firm Strategy

and Rivalry

Context for Firm Strategy

and Rivalry

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Foreign ownership restrictions 83

Hidden trade barrier liberalization 64

Centralization of economic policy-making 61

Efficacy of corporate boards 52

Effectiveness of anti-trust policy 51

Tariff liberalization 49

Favoritism in decisions of government 46 officials

Business costs of corruption 46

Regulation of securities exchanges 39

Protection of minority shareholders’ 38 interests

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

37Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

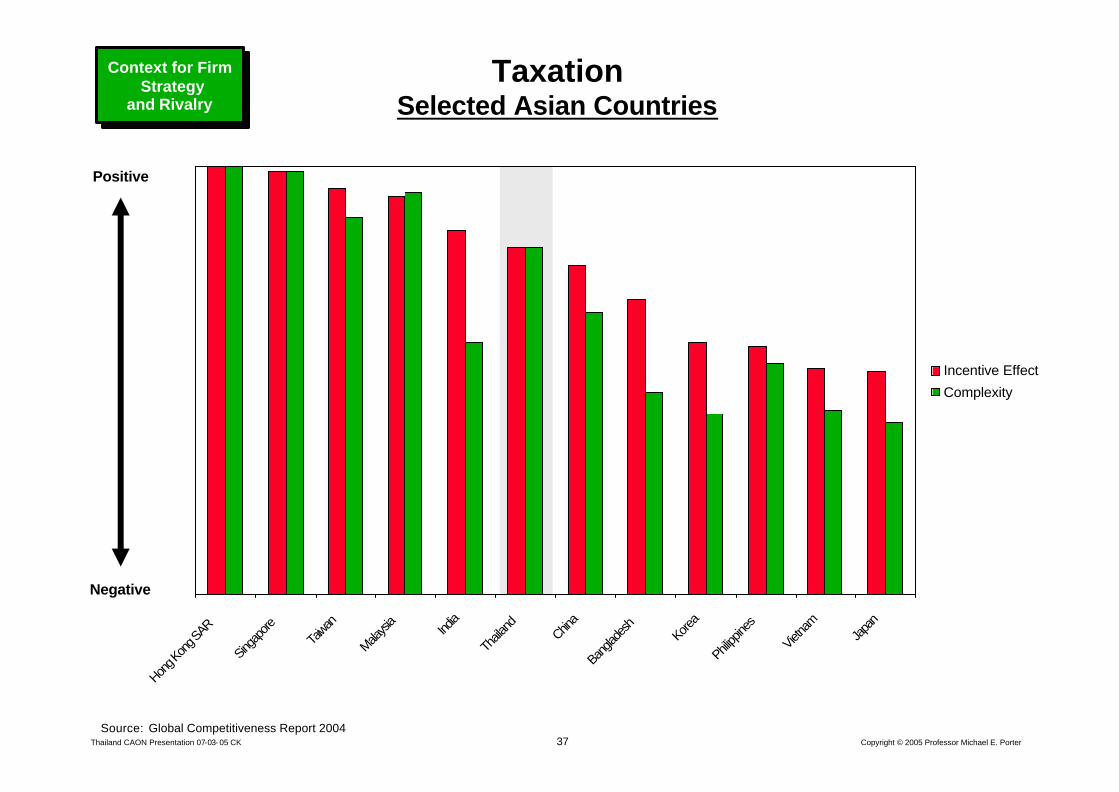

Hong K

ong S

AR

Singap

oreTa

iwan

Malaysi

aInd

ia

Thaila

ndChin

a

Bang

lades

hKore

a

Philipp

ines

Vietna

mJa

pan

Incentive Effect

Complexity

Positive

Negative

Source: Global Competitiveness Report 2004

TaxationSelected Asian Countries

Context for Firm Strategy

and Rivalry

Context for Firm Strategy

and Rivalry

38Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

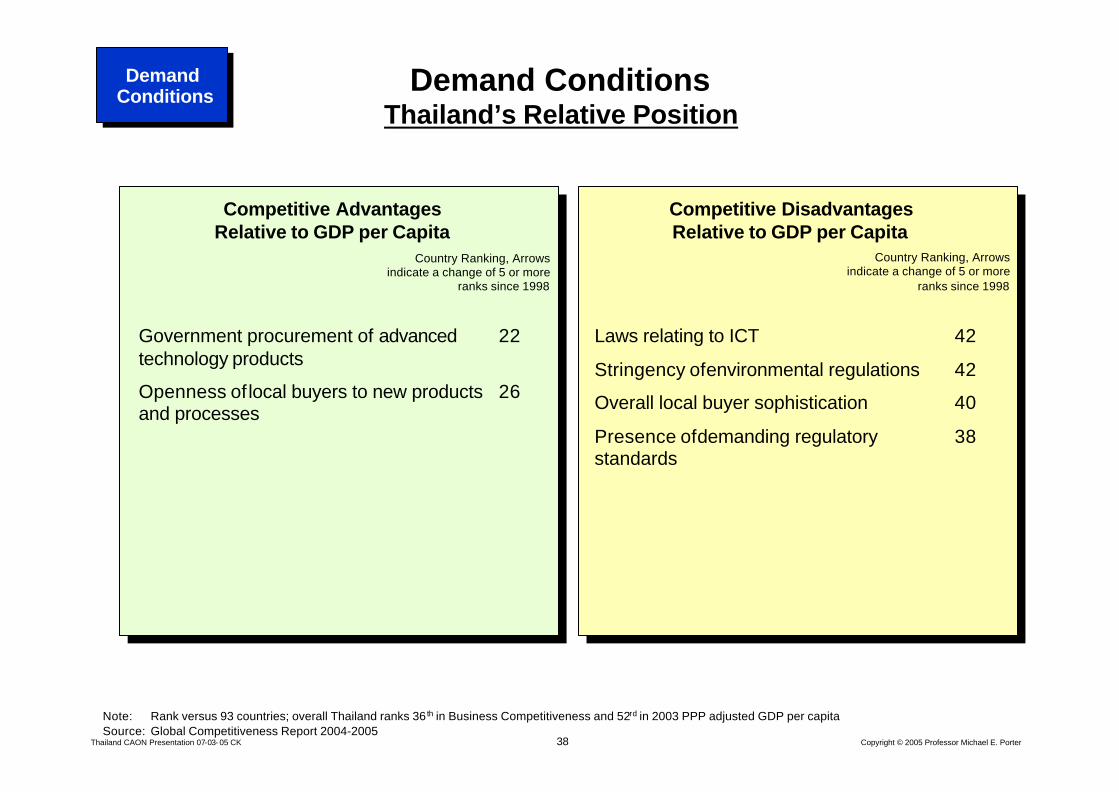

Demand ConditionsThailand’s Relative Position

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Demand ConditionsDemand

Conditions

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Government procurement of advanced 22 technology products

Openness of local buyers to new products 26 and processes

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Laws relating to ICT 42

Stringency of environmental regulations 42

Overall local buyer sophistication 40

Presence of demanding regulatory 38 standards

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

39Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

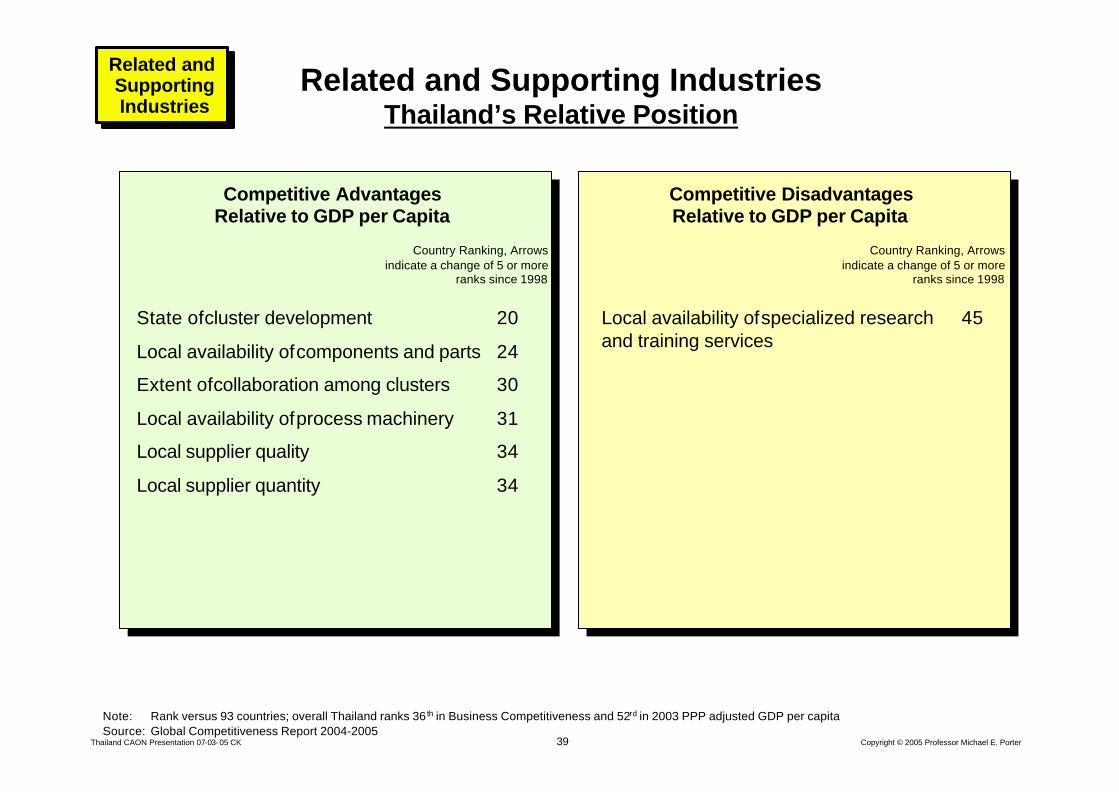

Related and Supporting IndustriesThailand’s Relative Position

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Related and Supporting Industries

Related and Supporting Industries

State of cluster development 20

Local availability of components and parts 24

Extent of collaboration among clusters 30

Local availability of process machinery 31

Local supplier quality 34

Local supplier quantity 34

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Local availability of specialized research 45 and training services

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

40Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

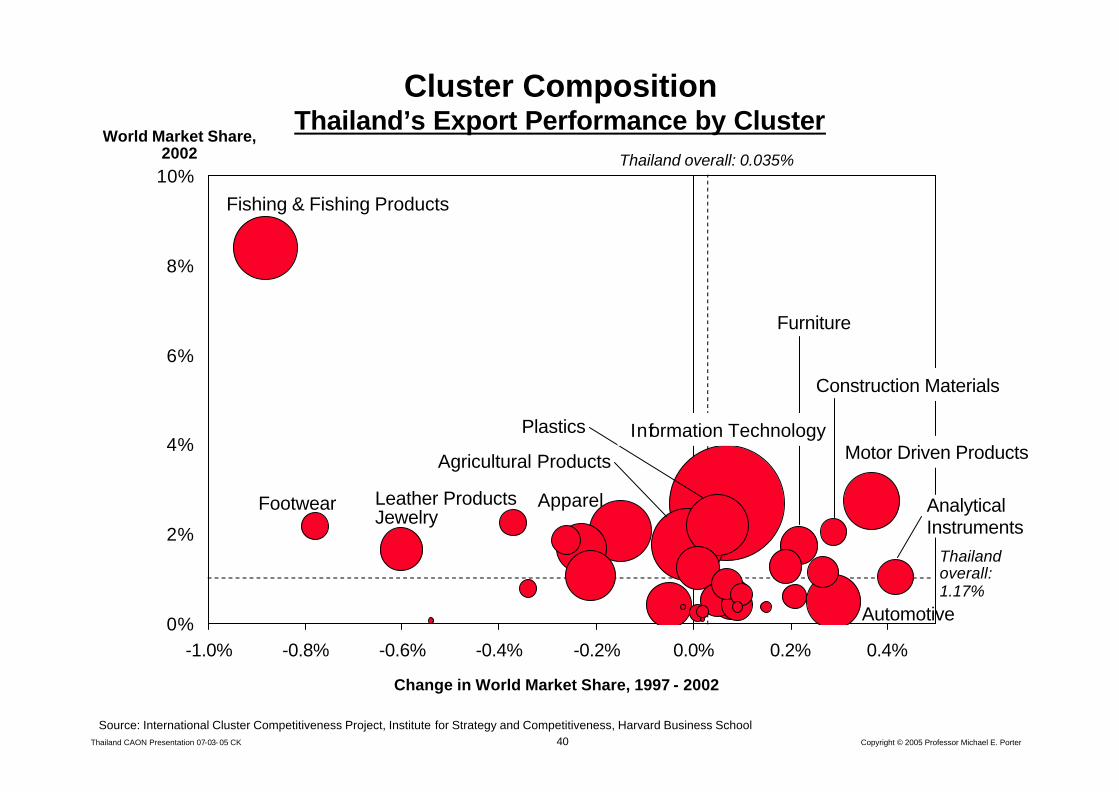

0%

2%

4%

6%

8%

10%

-1.0% -0.8% -0.6% -0.4% -0.2% 0.0% 0.2% 0.4%

Source: International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School

World Market Share, 2002

Change in World Market Share, 1997 - 2002

Cluster CompositionThailand’s Export Performance by Cluster

Thailand overall: 0.035%

Thailand overall:1.17%

Plastics

Agricultural Products Motor Driven Products

Apparel

Fishing & Fishing Products

Automotive

JewelryAnalytical Instruments

Leather ProductsFootwear

Construction Materials

Information Technology

Furniture

41Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

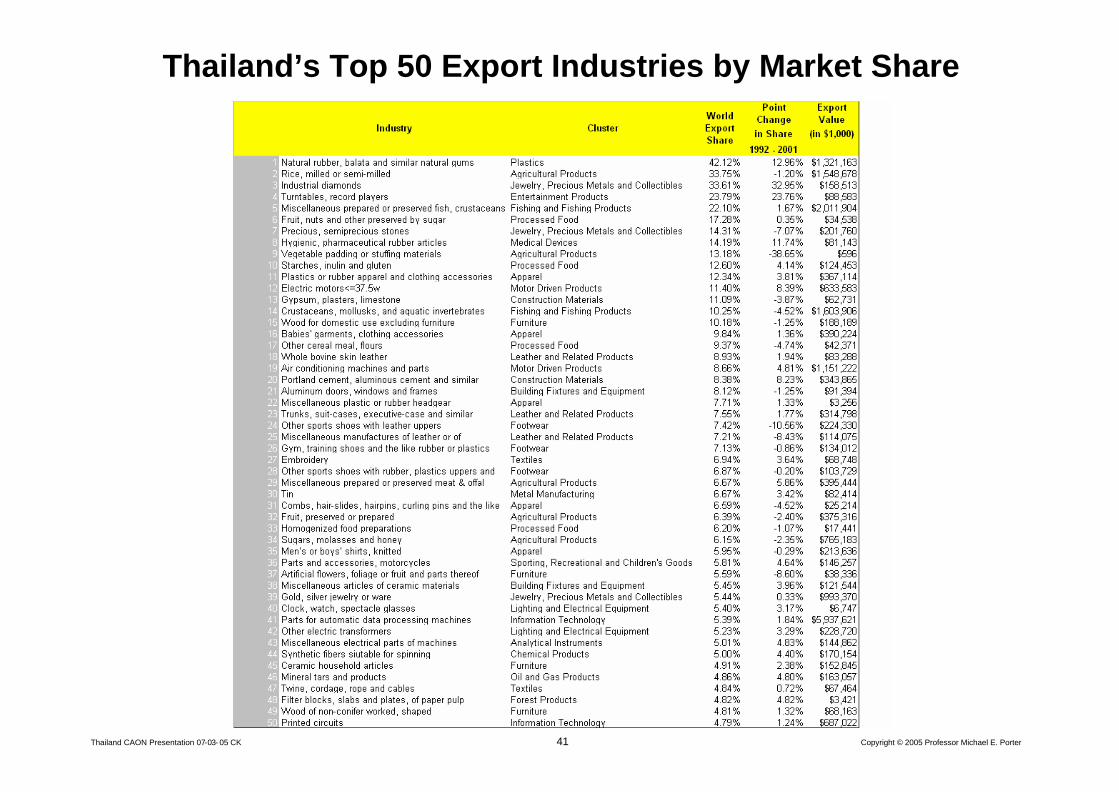

Thailand’s Top 50 Export Industries by Market Share

42Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

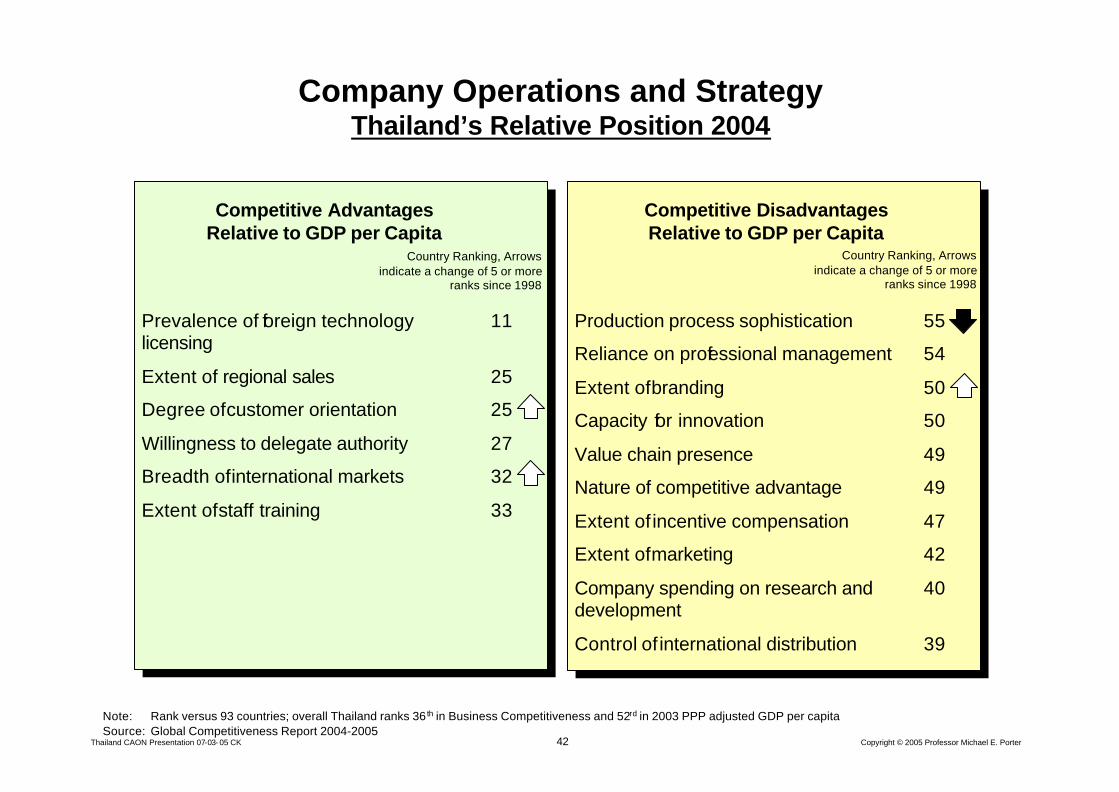

Company Operations and StrategyThailand’s Relative Position 2004

Production process sophistication 55

Reliance on professional management 54

Extent of branding 50

Capacity for innovation 50

Value chain presence 49

Nature of competitive advantage 49

Extent of incentive compensation 47

Extent of marketing 42

Company spending on research and 40 development

Control of international distribution 39

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Country Ranking, Arrows indicate a change of 5 or more

ranks since 1998

Prevalence of foreign technology 11 licensing

Extent of regional sales 25

Degree of customer orientation 25

Willingness to delegate authority 27

Breadth of international markets 32

Extent of staff training 33

Note: Rank versus 93 countries; overall Thailand ranks 36 th in Business Competitiveness and 52rd in 2003 PPP adjusted GDP per capitaSource: Global Competitiveness Report 2004-2005

43Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

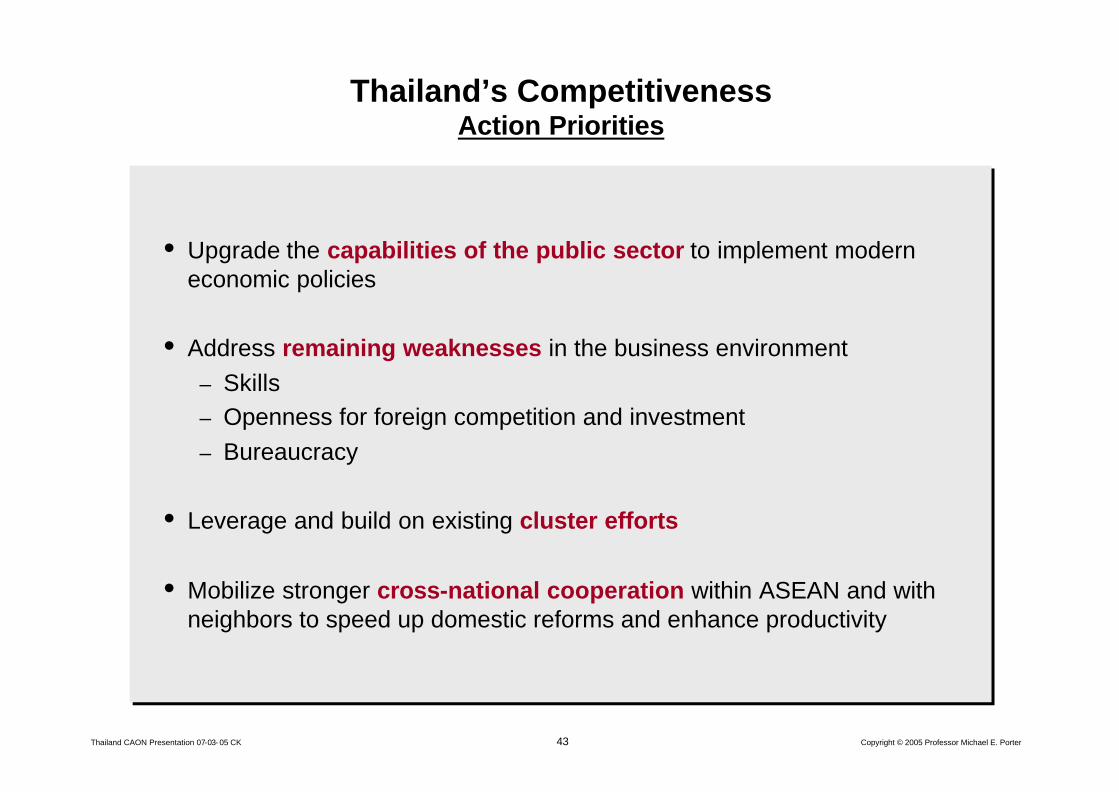

Thailand’s Competitiveness Action Priorities

• Upgrade the capabilities of the public sector to implement modern economic policies

• Address remaining weaknesses in the business environment– Skills – Openness for foreign competition and investment– Bureaucracy

• Leverage and build on existing cluster efforts

• Mobilize stronger cross-national cooperation within ASEAN and with neighbors to speed up domestic reforms and enhance productivity

• Upgrade the capabilities of the public sector to implement modern economic policies

• Address remaining weaknesses in the business environment– Skills – Openness for foreign competition and investment– Bureaucracy

• Leverage and build on existing cluster efforts

• Mobilize stronger cross-national cooperation within ASEAN and with neighbors to speed up domestic reforms and enhance productivity

44Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

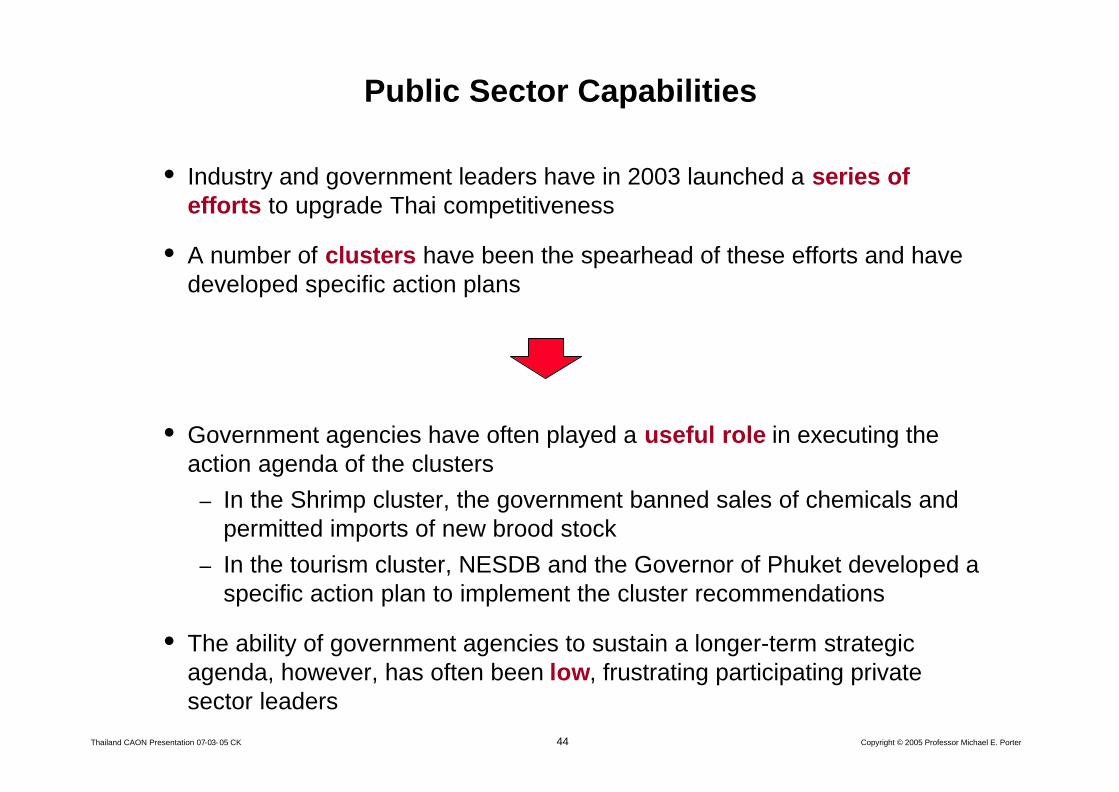

Public Sector Capabilities

• Industry and government leaders have in 2003 launched a series of efforts to upgrade Thai competitiveness

• A number of clusters have been the spearhead of these efforts and have developed specific action plans

• Government agencies have often played a useful role in executing the action agenda of the clusters

– In the Shrimp cluster, the government banned sales of chemicals and permitted imports of new brood stock

– In the tourism cluster, NESDB and the Governor of Phuket developed a specific action plan to implement the cluster recommendations

• The ability of government agencies to sustain a longer-term strategic agenda, however, has often been low, frustrating participating private sector leaders

45Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

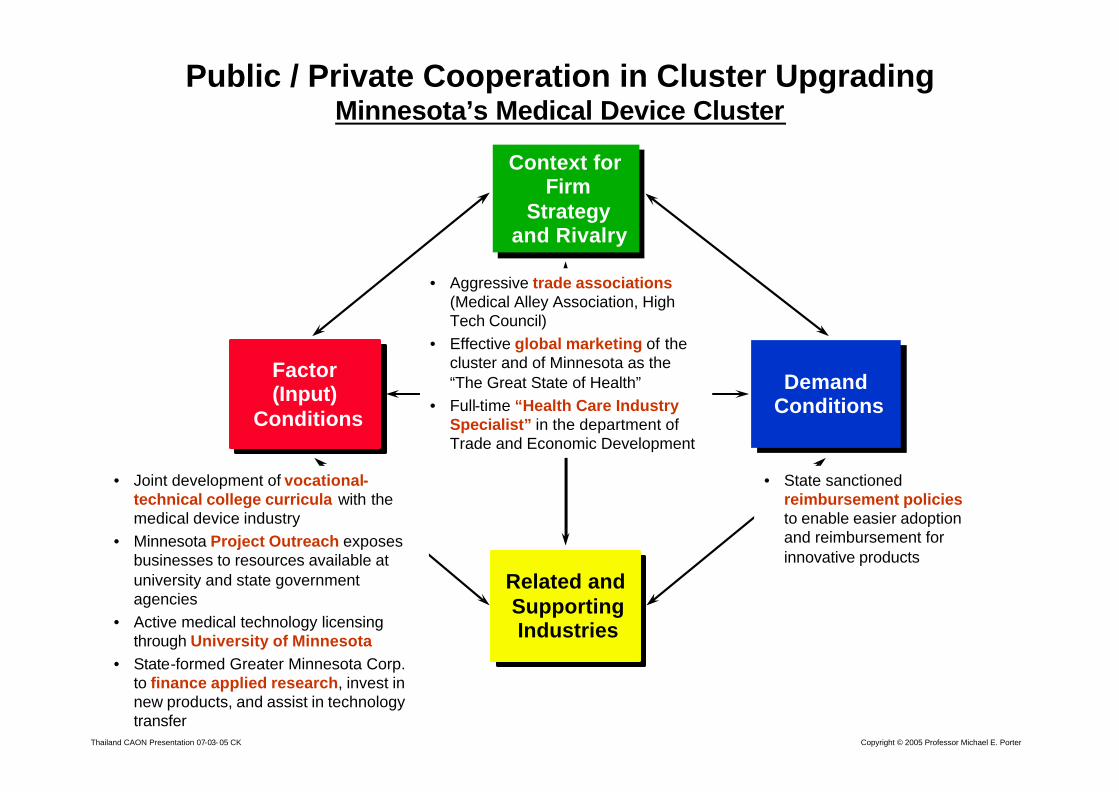

Public / Private Cooperation in Cluster UpgradingMinnesota’s Medical Device Cluster

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

Conditions

Demand ConditionsDemand

Conditions

• Joint development of vocational-technical college curricula with the medical device industry

• Minnesota Project Outreach exposes businesses to resources available at university and state government agencies

• Active medical technology licensing through University of Minnesota

• State-formed Greater Minnesota Corp. to finance applied research, invest in new products, and assist in technology transfer

• State sanctioned reimbursement policiesto enable easier adoption and reimbursement for innovative products

• Aggressive trade associations(Medical Alley Association, High Tech Council)

• Effective global marketing of the cluster and of Minnesota as the “The Great State of Health”

• Full-time “Health Care Industry Specialist” in the department of Trade and Economic Development

46Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Clusters as a Tool For Economic PolicyOverview

• A new way of thinking about an economy and organizing economic development efforts

• Better aligned with the nature of competition and sources of competitive advantage. Clusters capture important linkages in terms of technology, skills, information, marketing and customer needs that cut across firms and industries. Such linkages are fundamental to competition and, especially, to the direction and pace of innovation

• Recast the role of the private sector, government, trade associations and educational or research institutions

• Brings together firms of all sizes

• Creates a forum for constructive business-government dialog

• A means to identify common opportunities, not just common problems

• Provides guidance for both economic and social policies

47Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Appropriate Roles of Government in Cluster Development

• A successful cluster policy builds on sound overall economic policies

• Government should support the development of all clusters, not pick winners among them

• Government policy should reinforce established and emerging clustersrather than attempt to create entirely new ones

• Government can seed new clusters through attracting foreign direct investment

• Government’s role in cluster initiatives is as facilitator and participant. The most successful cluster initiatives are public-private partnerships

• Government should NOT provide subsidies, set preferential tariffs, exempt companies from competition laws, give preferential tax exemptions, etc.

48Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Role of the Private Sector in Economic Development

• A company’s competitive advantage is partly the result of the local environment

• Company membership in a cluster offers collective benefits• Private investment in “public goods” is justified

• Take an active role in upgrading the local infrastructure• Nurture local suppliers and attract new supplier investments • Work closely with local educational and research institutions to upgrade

quality and create specialized programs addressing cluster needs• Provide government with information and substantive input on

regulatory issues and constraints bearing on cluster development• Focus corporate philanthropy on enhancing the local business

environment

• An important role for trade associations– Greater influence

– Cost sharing

49Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Regions and Economic StrategyTraditional Views• Regions as free trade zones; regions as economic unions (e.g., United States, European Union)

New View• A regional strategy as a powerful tool to enhance competitiveness across countries

– Expanding internal trade and investment• Gains from internal trade and investment

AND– Upgrading company operations and strategy

• Enhancing the competitive capability o f firms• Expanding trade in non-traditional export industries

– Improving the business environment• Mutual benefits to the productivity of the business environment through policy

coordination that captures external economies and the benefits of specialization in institutions and infrastructure across borders

– Fostering cluster development• Cross-border cluster specialization and integration

– Attracting foreign investment• Enhancing interest and investment in the region by the international community

– Accelerating the economic policy process• Improving economic policy formulation and implementation at the national level

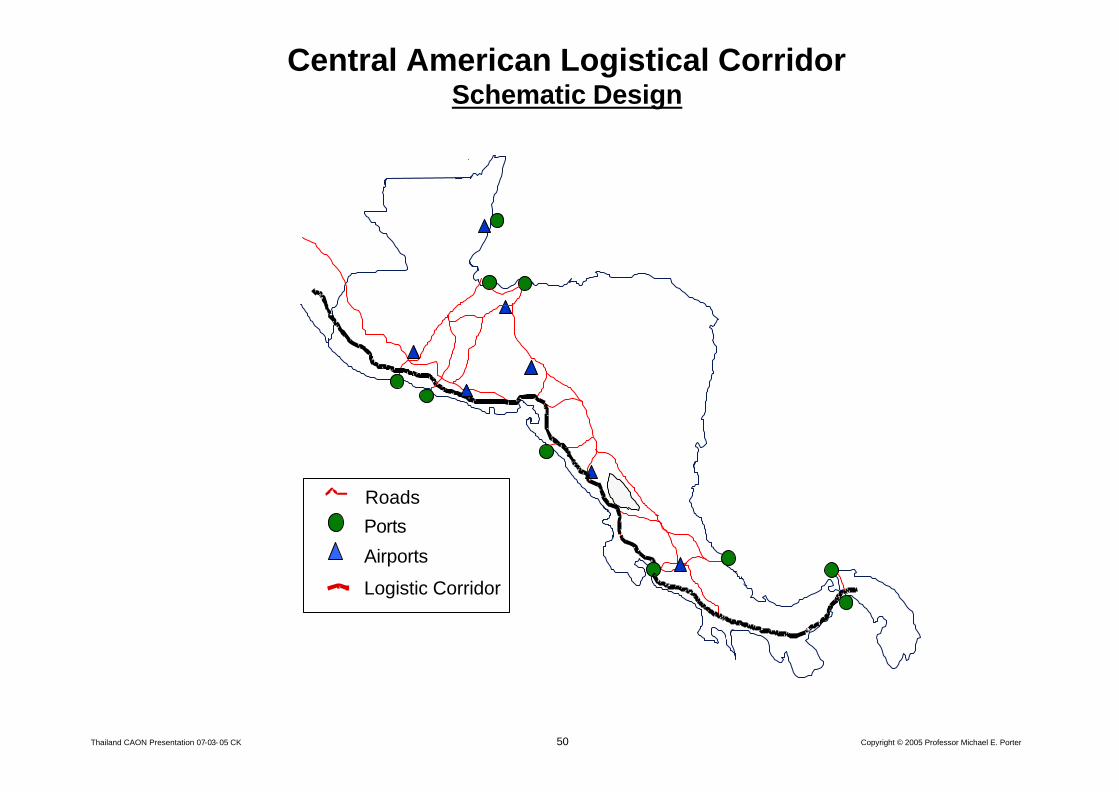

50Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Roads

Airports

Ports

Logistic Corridor

Central American Logistical CorridorSchematic Design

51Thailand CAON Presentation 07-03- 05 CK Copyright © 2005 Professor Michael E. Porter

Thailand’s Competitiveness in 2005

• Thailand has made a number of right steps towards improving the foundations of its competitiveness

• The critical barriers to overcome – in public sector reform as well as in business environment upgrading – are political, not financial

• The government, based with a majority unique in the country’s history, has the opportunity and obligation to aggressively pursue further competitiveness upgrading