Embed Size (px)

Citation preview

This presentation draws on ideas from Professor Porter’s books and articles, in particular, Competitive Strategy (The Free Press, 1980); Competitive

Advantage (The Free Press, 1985); “What is Strategy?” (Harvard Business Review, Nov/Dec 1996); and On Competition (Harvard Business Review,

2008). No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means—electronic, mechanical,

photocopying, recording, or otherwise—without the permission of Michael E. Porter. Additional information may be found at the website of the Institute for

Strategy and Competitiveness, www.isc.hbs.edu.

Strategy and Competition

Professor Michael E. Porter

Harvard Business School

BSP International Conference

Pont Fer, Phoenix, Mauritius

April 2nd, 2014

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 2

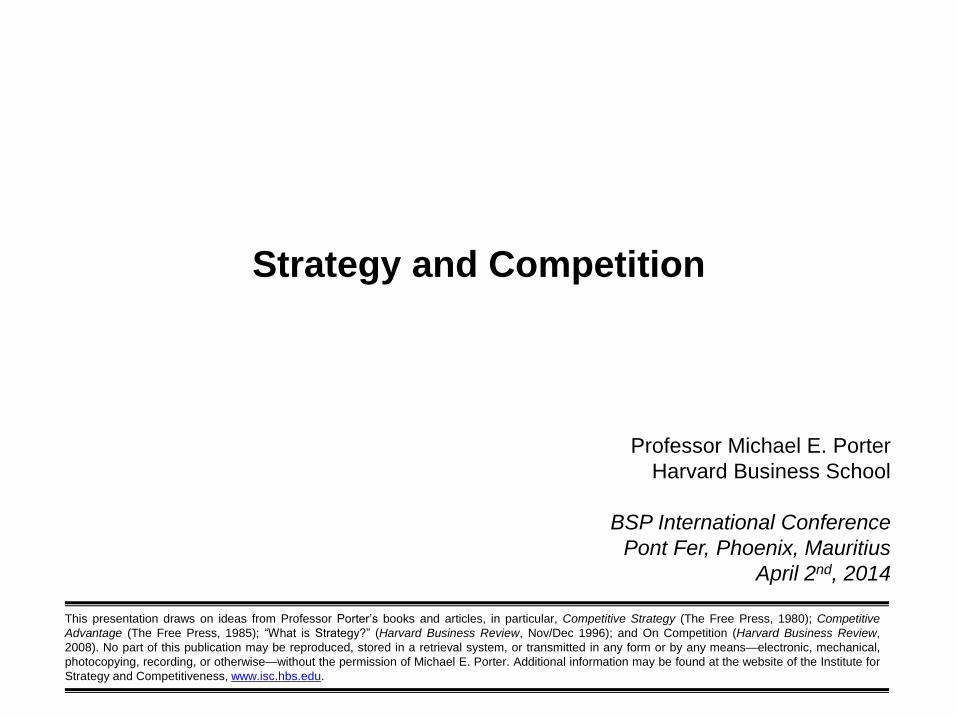

Thinking Strategically

COMPETING

TO BE THE BEST

COMPETING

TO BE UNIQUE

The worst error in strategy is to compete

with rivals on the same dimensions

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 3

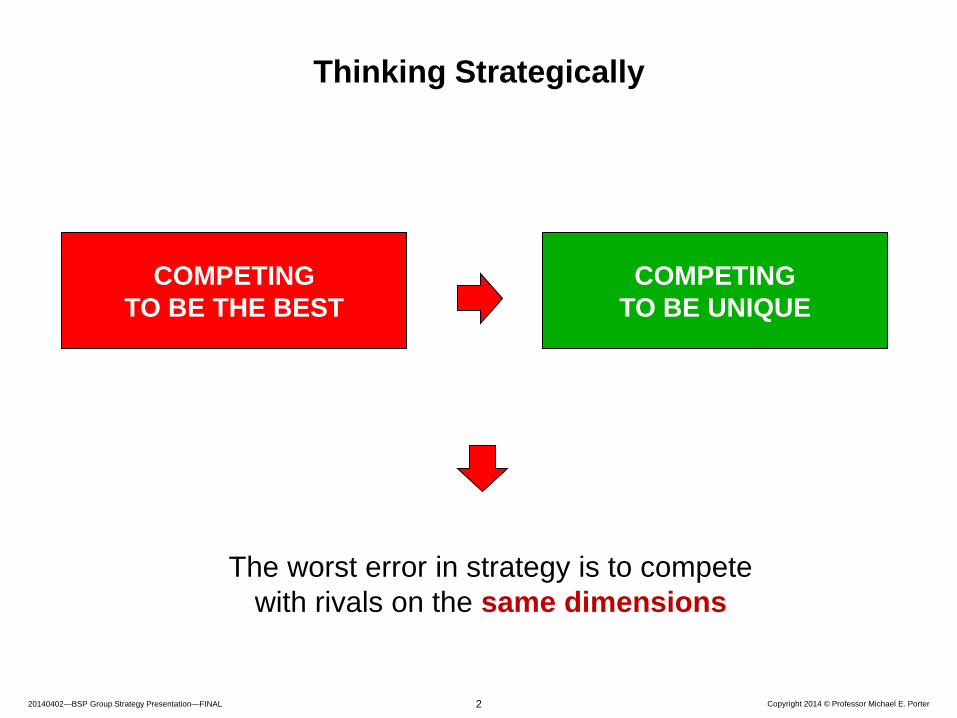

What Do We Mean by a Strategy?

• Strategy is different than aspirations

– “Our strategy is to be #1 or #2…”

– “Our strategy is to grow…”

– “Our strategy is to provide superior returns to our shareholders…”

• Strategy is more than a particular action

– “Our strategy is to merge…”

– “… internationalize…”

– “… consolidate the industry…”

– “…double our R&D budget…”

• Strategy is not the same as vision / values

– “Our strategy is to serve our customers and communities meeting the highest standards

of integrity…”

• Strategy defines the company’s distinctive approach to competing

and the competitive advantages on which it will be based

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 4

Setting the Right Financial Goals

• Strategic thinking starts with setting proper financial goals for the company

• The fundamental goal of a company is superior long-term return on

investment

• Growth is good only if superiority in ROIC is achieved and sustained

– ROIC threshold

• Setting unrealistic profitability or growth targets can undermine strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 5

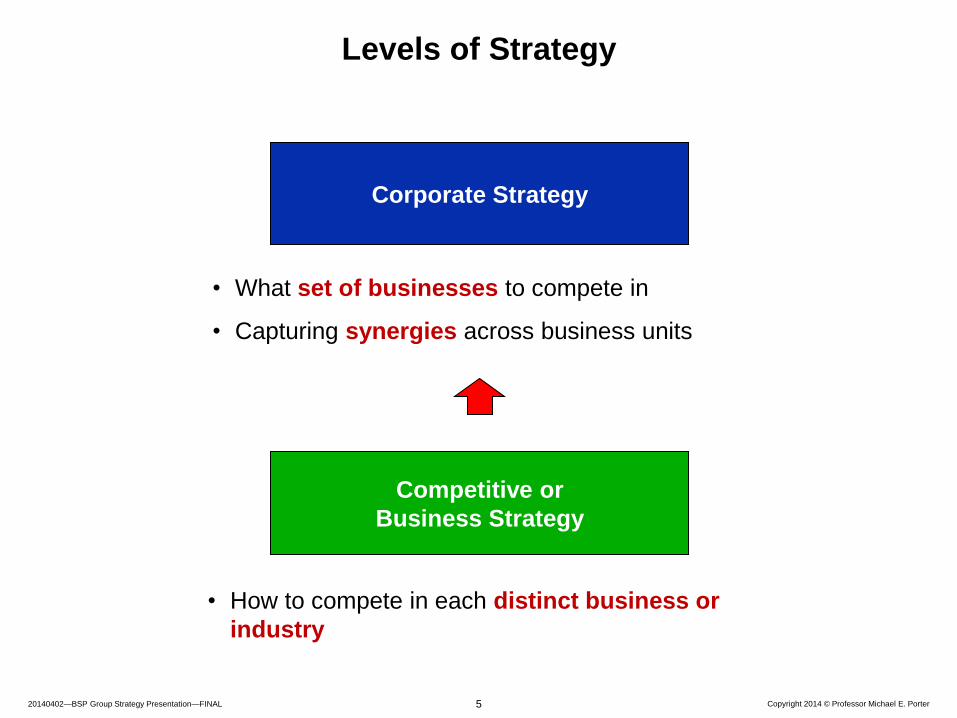

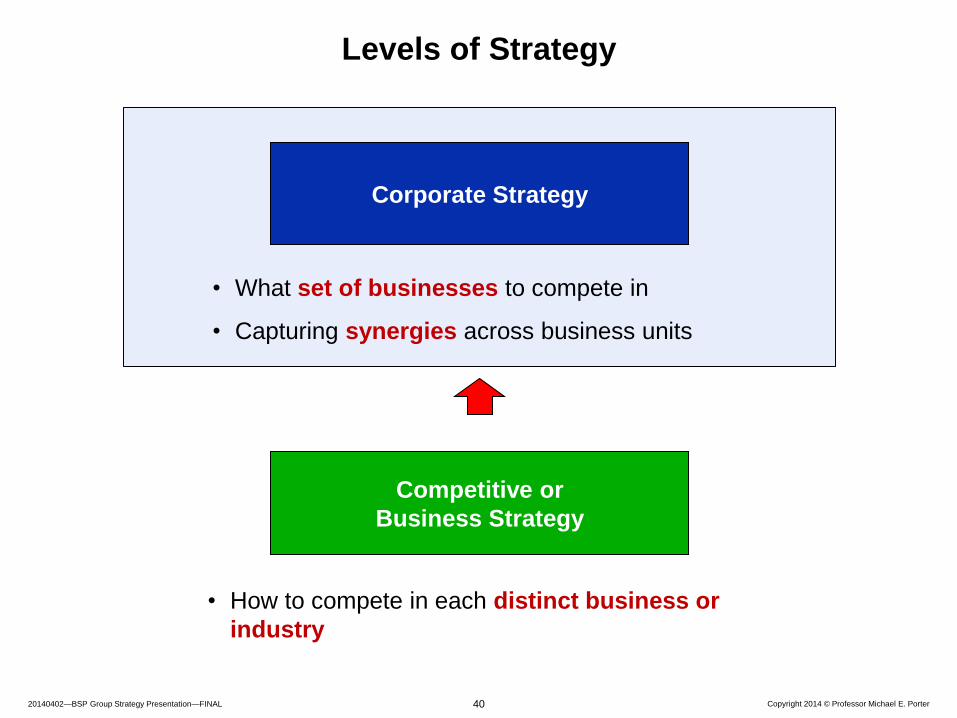

• What set of businesses to compete in

• Capturing synergies across business units

Levels of Strategy

• How to compete in each distinct business or

industry

Corporate Strategy

Competitive or

Business Strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 6

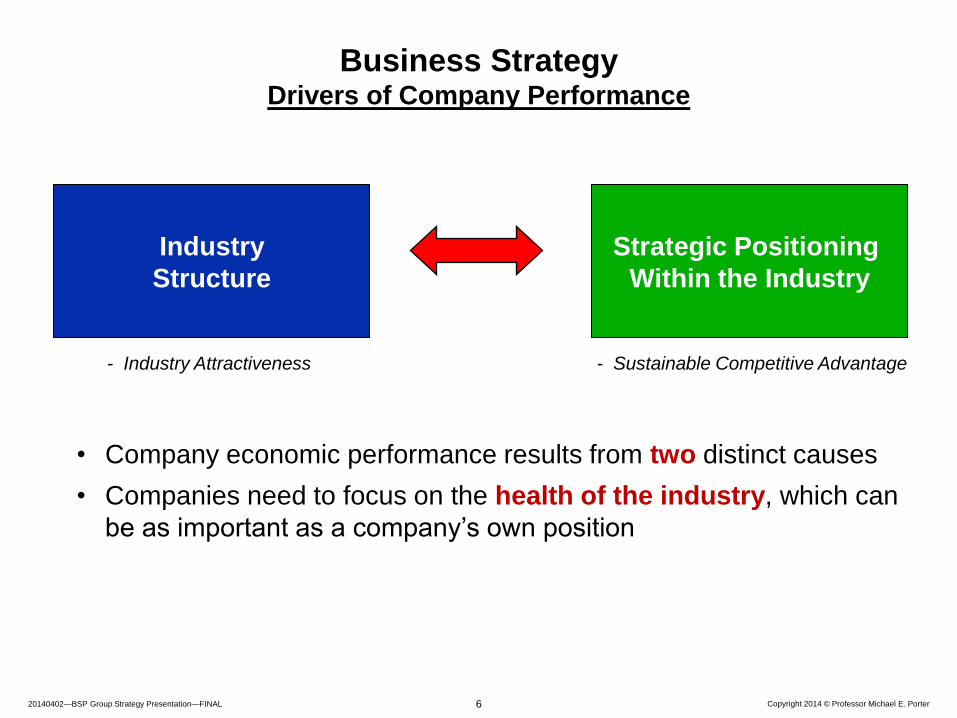

• Company economic performance results from two distinct causes

• Companies need to focus on the health of the industry, which can

be as important as a company’s own position

Industry

Structure

Strategic Positioning

Within the Industry

- Industry Attractiveness - Sustainable Competitive Advantage

Business Strategy Drivers of Company Performance

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 7

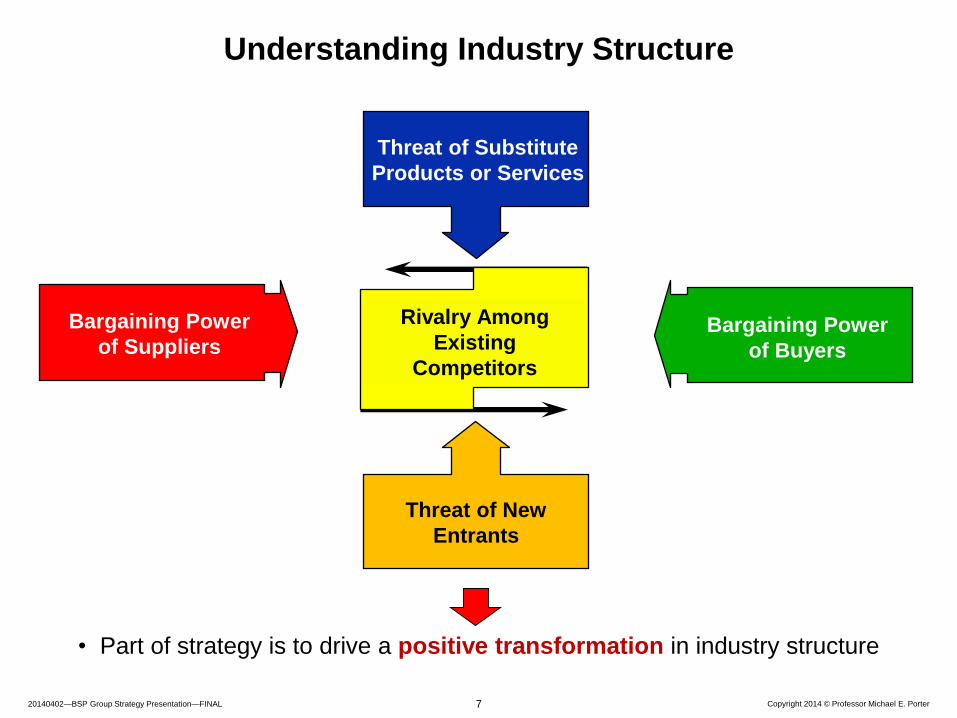

• Part of strategy is to drive a positive transformation in industry structure

Threat of Substitute

Products or Services

Threat of New

Entrants

Rivalry Among

Existing

Competitors

Bargaining Power

of Suppliers Bargaining Power

of Buyers

Understanding Industry Structure

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 8

• Part of strategy is to drive a positive transformation in industry structure

Threat of Substitute

Products or Services

Threat of New

Entrants

Rivalry Among

Existing

Competitors

Bargaining Power

of Suppliers Bargaining Power

of Buyers

Understanding Industry Structure

• Channels

• End users

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 9

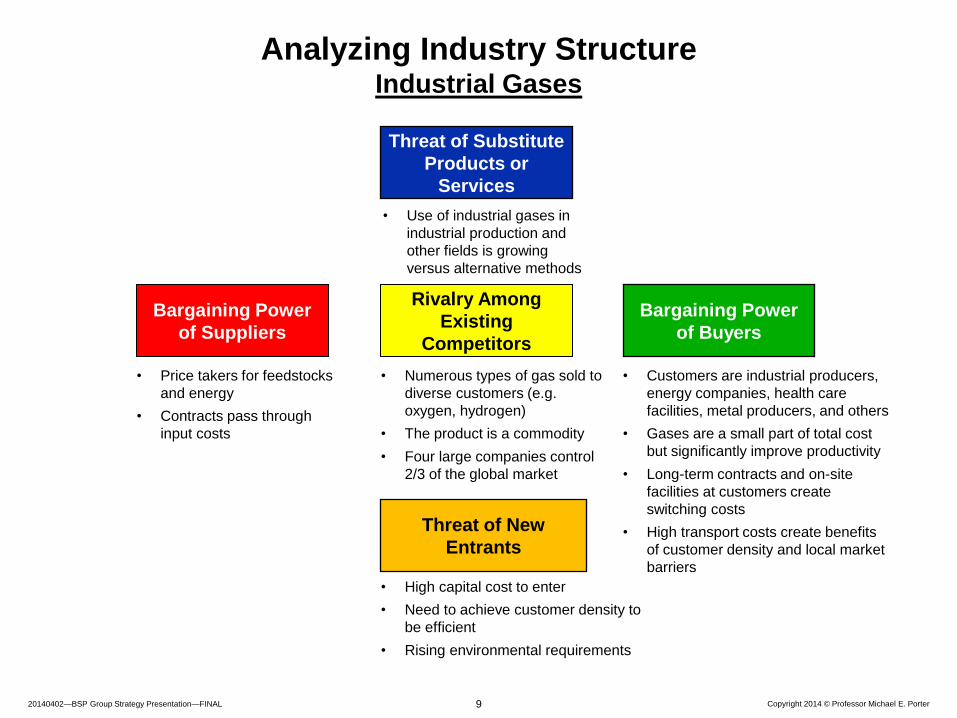

• Price takers for feedstocks

and energy

• Contracts pass through

input costs

Bargaining Power

of Suppliers

Rivalry Among

Existing

Competitors

Bargaining Power

of Buyers

Threat of New

Entrants

Threat of Substitute

Products or

Services

• High capital cost to enter

• Need to achieve customer density to

be efficient

• Rising environmental requirements

• Numerous types of gas sold to

diverse customers (e.g.

oxygen, hydrogen)

• The product is a commodity

• Four large companies control

2/3 of the global market

• Customers are industrial producers,

energy companies, health care

facilities, metal producers, and others

• Gases are a small part of total cost

but significantly improve productivity

• Long-term contracts and on-site

facilities at customers create

switching costs

• High transport costs create benefits

of customer density and local market

barriers

• Use of industrial gases in

industrial production and

other fields is growing

versus alternative methods

Analyzing Industry Structure Industrial Gases

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 10

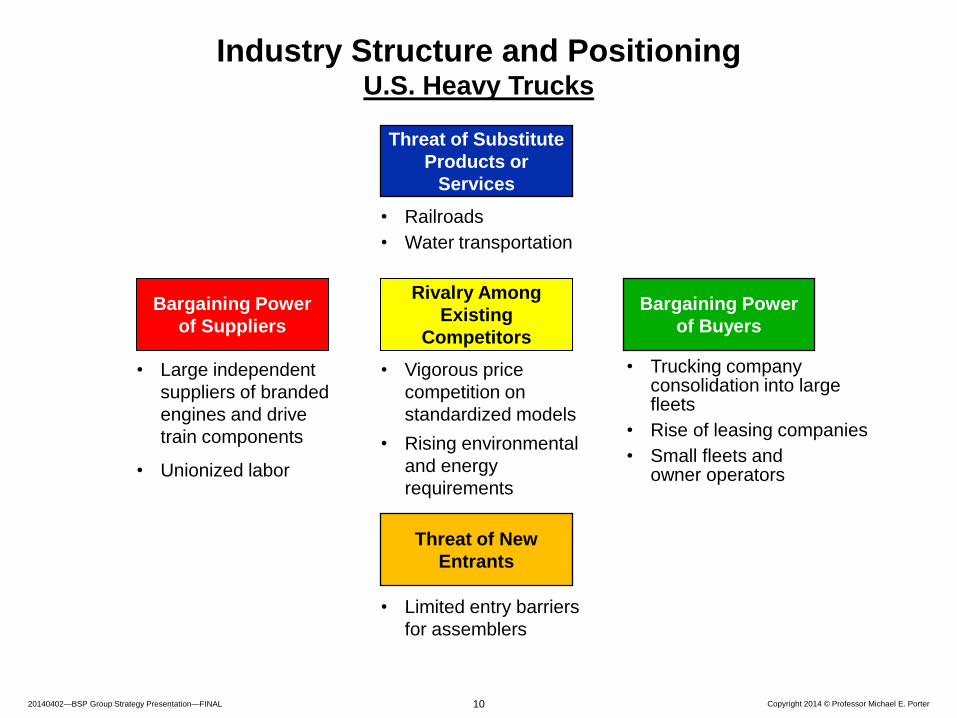

• Large independent

suppliers of branded

engines and drive

train components

• Unionized labor

Bargaining Power

of Suppliers

Rivalry Among

Existing

Competitors

Bargaining Power

of Buyers

Threat of New

Entrants

Threat of Substitute

Products or

Services

• Limited entry barriers

for assemblers

• Vigorous price

competition on

standardized models

• Rising environmental

and energy

requirements

• Trucking company consolidation into large fleets

• Rise of leasing companies

• Small fleets and owner operators

• Railroads

• Water transportation

Industry Structure and Positioning U.S. Heavy Trucks

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 11

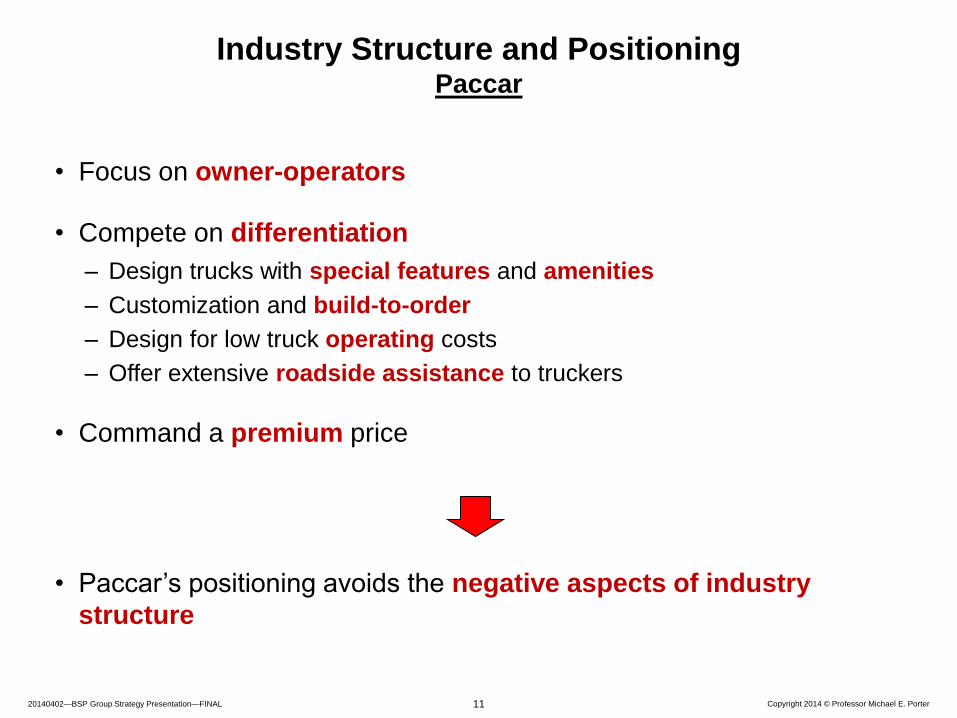

Industry Structure and Positioning Paccar

• Focus on owner-operators

• Compete on differentiation

– Design trucks with special features and amenities

– Customization and build-to-order

– Design for low truck operating costs

– Offer extensive roadside assistance to truckers

• Command a premium price

• Paccar’s positioning avoids the negative aspects of industry

structure

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 12

Machinery, ingredient, and

package suppliers

• Ties packaging material

sales to sale of machines

Bargaining Power

of Suppliers

Rivalry Among

Existing

Competitors

Bargaining Power

of Buyers

Threat of New

Entrants

Threat of Substitute

Products or

Services

New entrants to aseptic packaging

• Provides extensive assistance and

financing to bring new packers into

aseptic

Food packaging companies

• Provides standard products and

technical assistance and

support to level the playing field

among its customers

Consumer and food-away-from-home

food companies

• Invests in educating, and supporting

food companies to shift to aseptic

packaging and working with Tetra Pak

customers

Other package types and

packaging technologies

(refrigerated, retort cans/ bottles)

• Aggressively advocates aseptic

packaging versus other forms

• Big focus on sustainability

Shaping Industry Structure Tetra Pak in Aseptic Food Packaging

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 13

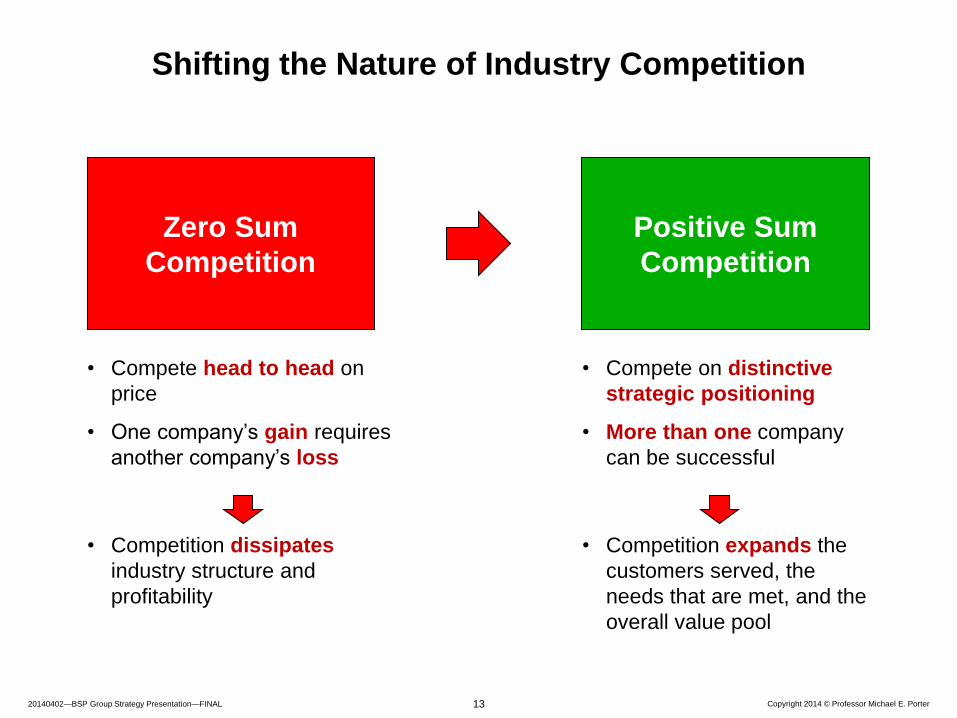

Shifting the Nature of Industry Competition

Zero Sum

Competition

Positive Sum

Competition

• Compete head to head on

price

• One company’s gain requires

another company’s loss

• Competition dissipates

industry structure and

profitability

• Compete on distinctive

strategic positioning

• More than one company

can be successful

• Competition expands the

customers served, the

needs that are met, and the

overall value pool

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 14

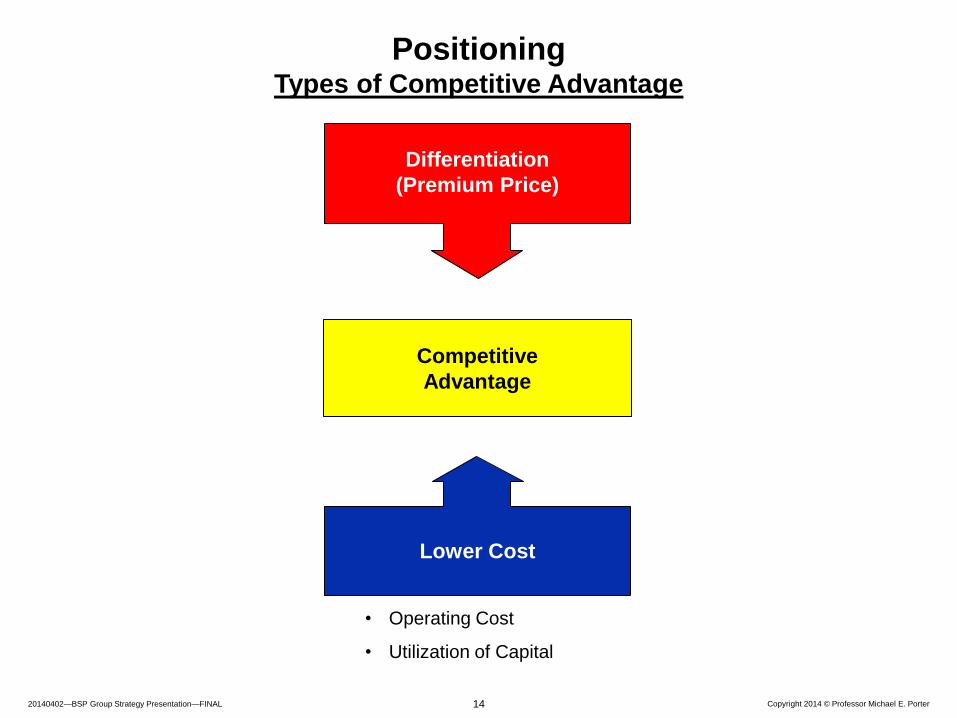

Positioning Types of Competitive Advantage

Differentiation

(Premium Price)

Lower Cost

Competitive

Advantage

• Operating Cost

• Utilization of Capital

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 15

• The value chain is the activities involved in delivering value to customers

• Strategy is reflected in the set of choices about how activities are configured and linked together

Sources of Competitive Advantage

The Value Chain

Support

Activities

Marketing

& Sales

(e.g., Sales

Force,

Promotion,

Advertising,

Proposal

Writing,

Website)

Inbound

Logistics

(e.g., Customer

Access, Data

Collection,

Incoming

Material

Storage,

Service)

Operations

(e.g., Branch

Operations,

Assembly,

Component

Fabrication)

Outbound

Logistics

(e.g., Order

Processing,

Warehousing,

Report

Preparation)

After-Sales

Service

(e.g., Installation,

Customer

Support,

Complaint

Resolution,

Repair)

M

a

r

g

i

n

Primary Activities

Firm Infrastructure (e.g., Financing, Planning, Investor Relations)

Procurement (e.g., Services, Machines, Advertising, Data)

Technology Development (e.g., Product Design, Process Design, Market Research)

Human Resource Management (e.g., Recruiting, Training, Compensation System)

Value

What

buyers are

willing to

pay

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 16

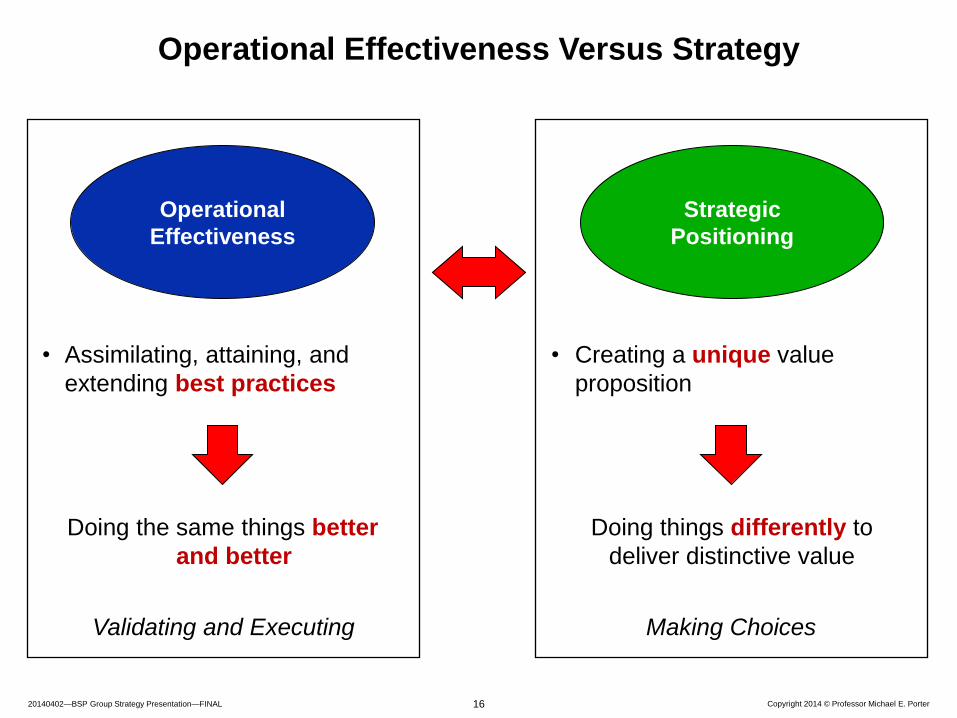

• Creating a unique value

proposition

• Assimilating, attaining, and

extending best practices

Operational

Effectiveness

Operational Effectiveness Versus Strategy

Doing the same things better

and better

Doing things differently to

deliver distinctive value

Validating and Executing Making Choices

Strategic

Positioning

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 17

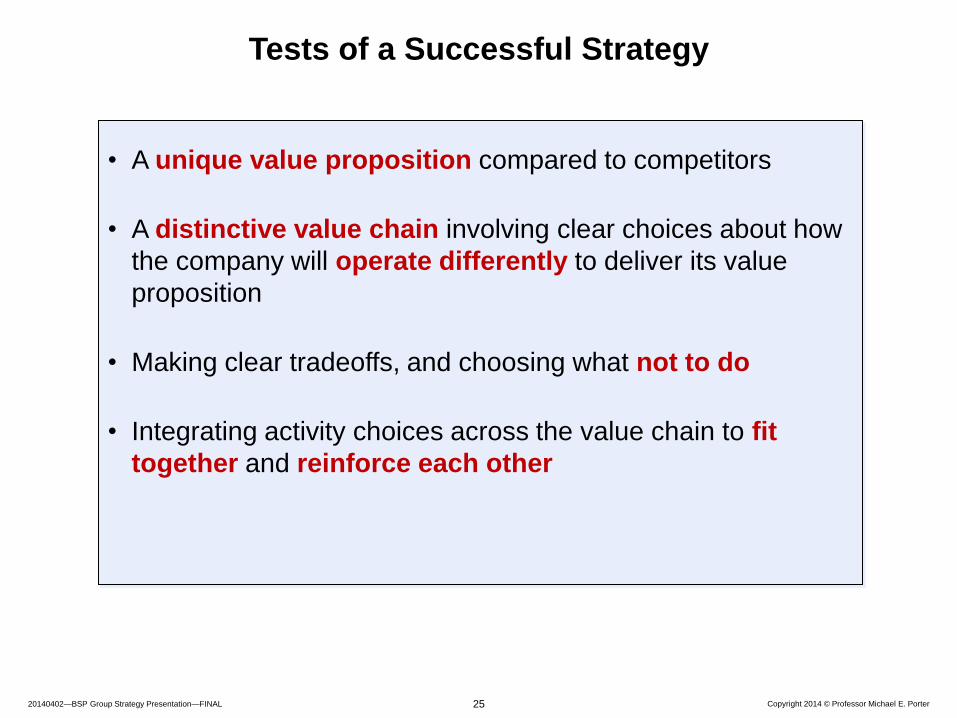

Tests of a Successful Strategy

• A unique value proposition compared to competitors

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 18

Defining the Value Proposition

What Relative

Price?

What

Customers? Which Needs?

• What end users?

• What channels?

• Which products?

• Which features?

• Which services?

• A novel value proposition can expand the market

• Finding a unique value proposition often involves a new

way of segmenting the market

• Premium? Parity?

Discount?

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 19

Strategic Positioning IKEA, Sweden

Value Proposition

• A wide line of stylish, functional and

good quality furniture and accessories

sold with limited customer service

• Very low price points

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 20

Tests of a Successful Strategy

• A unique value proposition compared to competitors

• A distinctive value chain involving clear choices about how

the company will operate differently to deliver its value

proposition

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 21

Strategic Positioning IKEA, Sweden

• Wide range of styles which are all displayed in

huge warehouse stores with large on-site

inventories

• Modular, ready-to-assemble, easy to ship

furniture designs

• In-house design of all products

• IKEA designer names attached to related

products to inform coordinated purchases

• Self-selection by the customer, with minimal

in-store service

• Extensive customer information in the form

of catalogs, mobile app, website, explanatory

ticketing, do-it-yourself videos, online planning

tools, and assembly instructions

• Self-delivery by most customers

• Suburban and urban locations with large

parking lots

• Long hours of operation

• On-site, low-cost restaurants

• Child care provided in the store

Value Proposition Distinctive Activities

• A wide line of stylish, functional and

good quality furniture and accessories

sold with limited customer service

• Very low price points

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 22

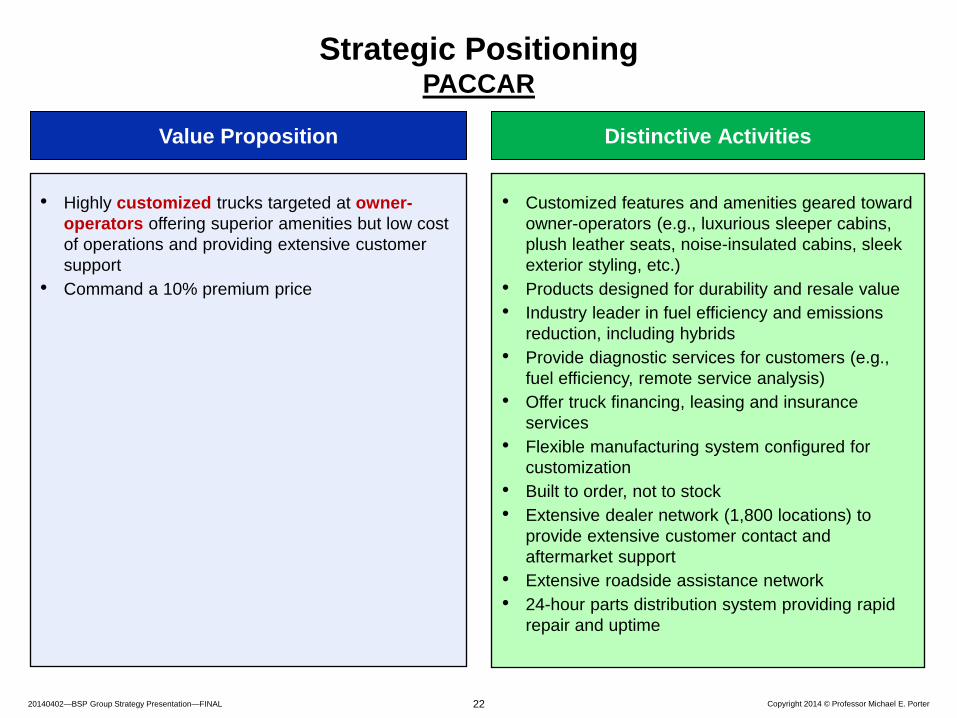

• Highly customized trucks targeted at owner-

operators offering superior amenities but low cost

of operations and providing extensive customer

support

• Command a 10% premium price

• Customized features and amenities geared toward

owner-operators (e.g., luxurious sleeper cabins,

plush leather seats, noise-insulated cabins, sleek

exterior styling, etc.)

• Products designed for durability and resale value

• Industry leader in fuel efficiency and emissions

reduction, including hybrids

• Provide diagnostic services for customers (e.g.,

fuel efficiency, remote service analysis)

• Offer truck financing, leasing and insurance

services

• Flexible manufacturing system configured for

customization

• Built to order, not to stock

• Extensive dealer network (1,800 locations) to

provide extensive customer contact and

aftermarket support

• Extensive roadside assistance network

• 24-hour parts distribution system providing rapid

repair and uptime

Value Proposition Distinctive Activities

Strategic Positioning PACCAR

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 23

Tests of a Successful Strategy

• A unique value proposition compared to competitors

• A distinctive value chain involving clear choices about how

the company will operate differently to deliver its value

proposition

• Making clear tradeoffs, and choosing what not to do

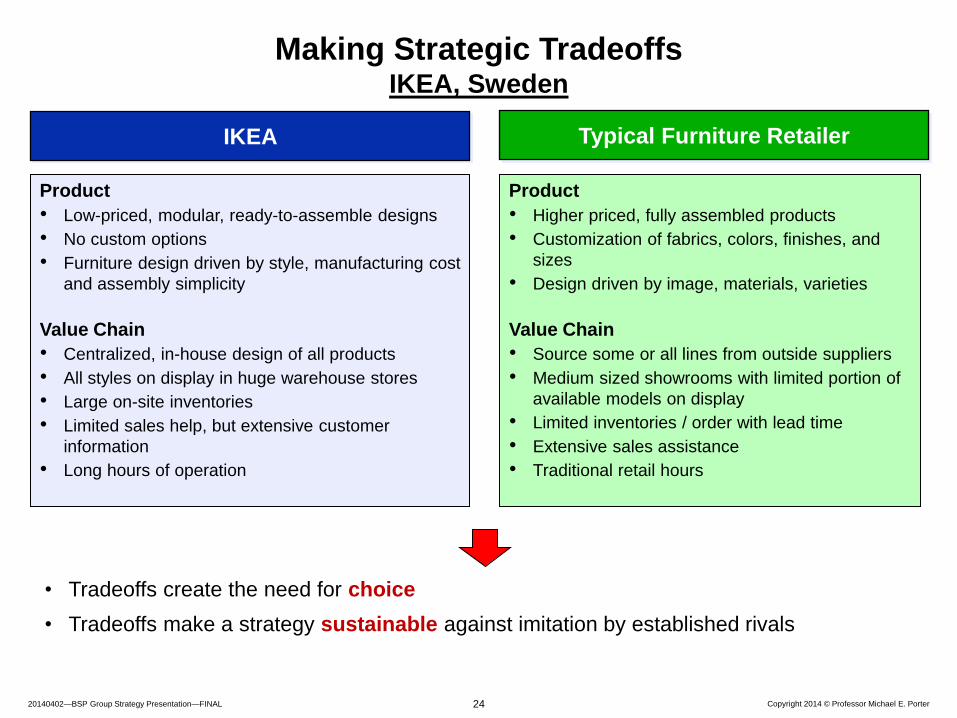

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 24

Product

• Higher priced, fully assembled products

• Customization of fabrics, colors, finishes, and

sizes

• Design driven by image, materials, varieties

Value Chain

• Source some or all lines from outside suppliers

• Medium sized showrooms with limited portion of

available models on display

• Limited inventories / order with lead time

• Extensive sales assistance

• Traditional retail hours

Making Strategic Tradeoffs IKEA, Sweden

Product

• Low-priced, modular, ready-to-assemble designs

• No custom options

• Furniture design driven by style, manufacturing cost

and assembly simplicity

Value Chain

• Centralized, in-house design of all products

• All styles on display in huge warehouse stores

• Large on-site inventories

• Limited sales help, but extensive customer

information

• Long hours of operation

IKEA Typical Furniture Retailer

• Tradeoffs create the need for choice

• Tradeoffs make a strategy sustainable against imitation by established rivals

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 25

• A unique value proposition compared to competitors

• A distinctive value chain involving clear choices about how

the company will operate differently to deliver its value

proposition

• Making clear tradeoffs, and choosing what not to do

• Integrating activity choices across the value chain to fit

together and reinforce each other

Tests of a Successful Strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 26

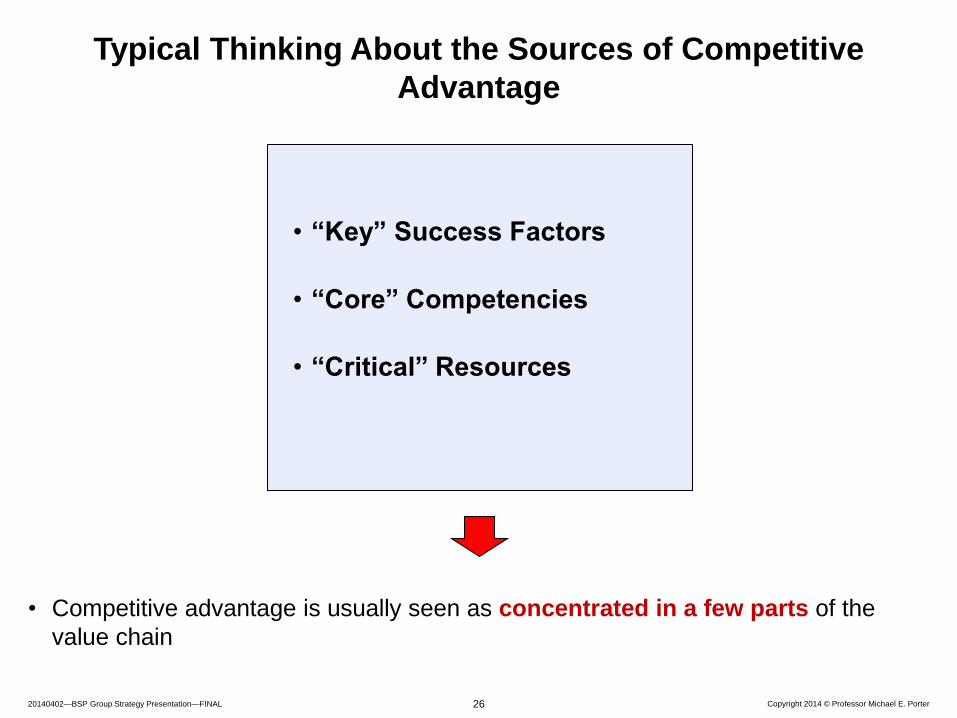

Typical Thinking About the Sources of Competitive

Advantage

• Competitive advantage is usually seen as concentrated in a few parts of the

value chain

• “Key” Success Factors

• “Core” Competencies

• “Critical” Resources

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 27

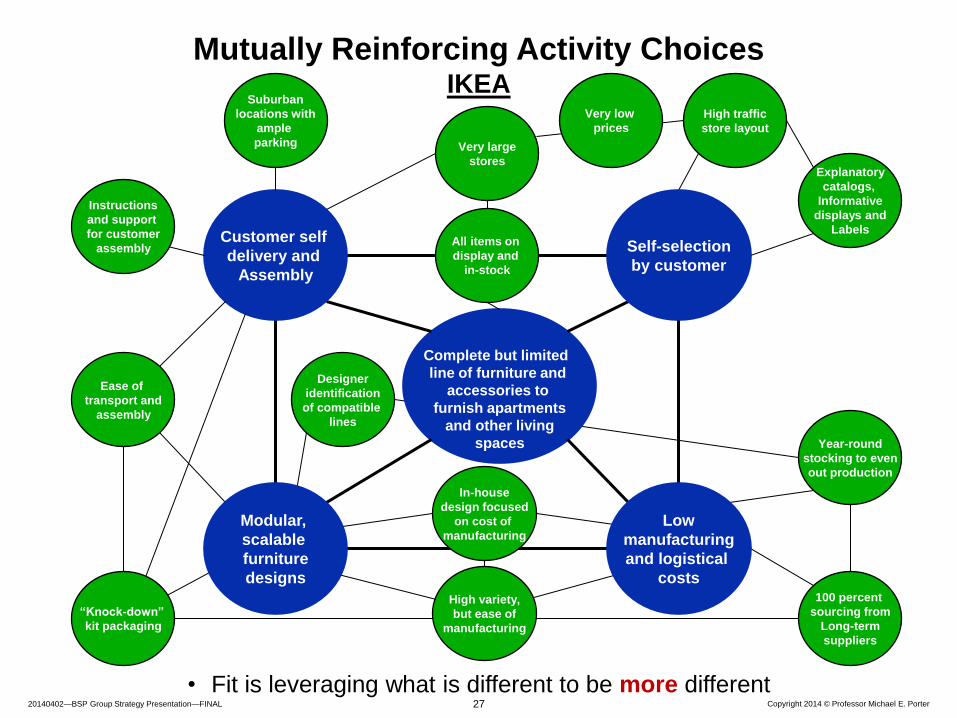

• Fit is leveraging what is different to be more different

Complete but limited

line of furniture and

accessories to

furnish apartments

and other living

spaces

Mutually Reinforcing Activity Choices IKEA

Customer self

delivery and

Assembly

Self-selection

by customer

Low

manufacturing

and logistical

costs

Modular,

scalable

furniture

designs

All items on

display and

in-stock

Very large

stores

High variety,

but ease of

manufacturing

In-house

design focused

on cost of

manufacturing

Designer

identification

of compatible

lines

Ease of

transport and

assembly

“Knock-down”

kit packaging

Instructions

and support

for customer

assembly

100 percent

sourcing from

Long-term

suppliers

Explanatory

catalogs,

Informative

displays and

Labels

Year-round

stocking to even

out production

High traffic

store layout

Suburban

locations with

ample

parking

Very low

prices

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 28

• A unique value proposition compared to competitors

• A distinctive value chain involving clear choices about how

the company will operate differently to deliver its value

proposition

• Making clear tradeoffs, and choosing what not to do

• Integrating activity choices across the value chain to fit

together and reinforce each other

• Continuity of strategic direction with continuous

improvement in realizing the unique value proposition

Tests of a Successful Strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 29

Strategic Continuity

• Continuity of strategy is essential to creating and sustaining competitive

advantage

– Understanding the strategy throughout the organization

– Building truly unique skills and assets related to the strategy

– Establishing a clear identity with customers, channels, and vendors

• “Reinvention” and frequent shifts in direction are costly and confuse the

customer, the industry, and the organization

• Maintain continuity in the value proposition, but continuously improve how

to realize it

• Continuity of strategy allows faster improvement

− Strategic continuity and continuous change are reinforcing

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 30

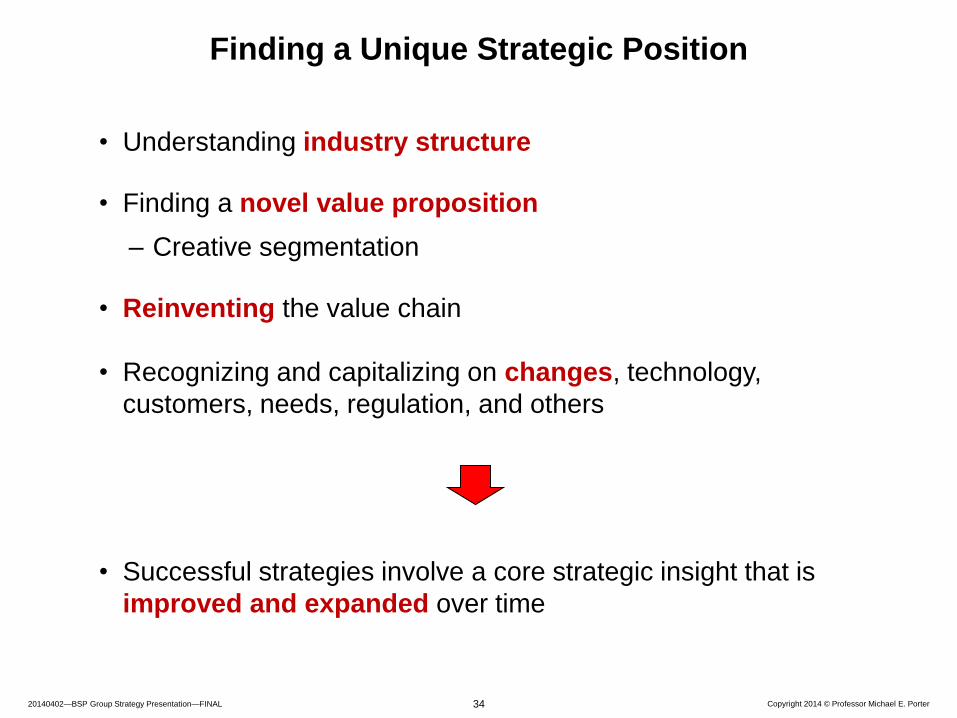

• Understanding industry structure

• Finding a novel value proposition

– Creative segmentation

Finding a Unique Strategic Position

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 31

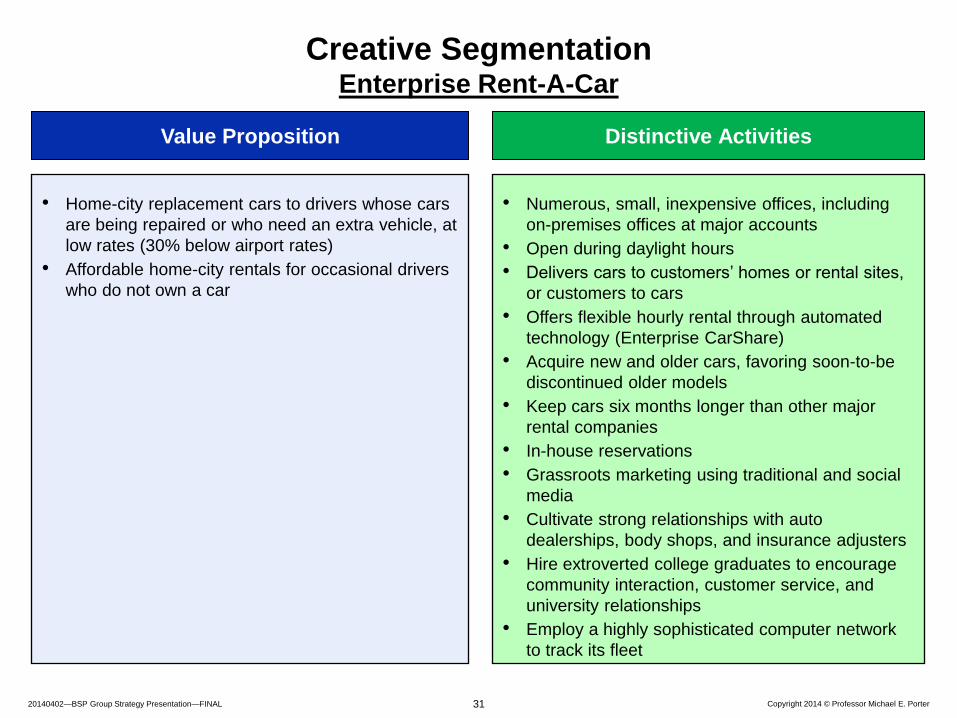

• Home-city replacement cars to drivers whose cars

are being repaired or who need an extra vehicle, at

low rates (30% below airport rates)

• Affordable home-city rentals for occasional drivers

who do not own a car

• Numerous, small, inexpensive offices, including

on-premises offices at major accounts

• Open during daylight hours

• Delivers cars to customers’ homes or rental sites,

or customers to cars

• Offers flexible hourly rental through automated

technology (Enterprise CarShare)

• Acquire new and older cars, favoring soon-to-be

discontinued older models

• Keep cars six months longer than other major

rental companies

• In-house reservations

• Grassroots marketing using traditional and social

media

• Cultivate strong relationships with auto

dealerships, body shops, and insurance adjusters

• Hire extroverted college graduates to encourage

community interaction, customer service, and

university relationships

• Employ a highly sophisticated computer network

to track its fleet

Value Proposition Distinctive Activities

Creative Segmentation Enterprise Rent-A-Car

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 32

• Understanding industry structure

• Finding a novel value proposition

– Creative segmentation

• Reinventing the value chain

Finding a Unique Strategic Position

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 33

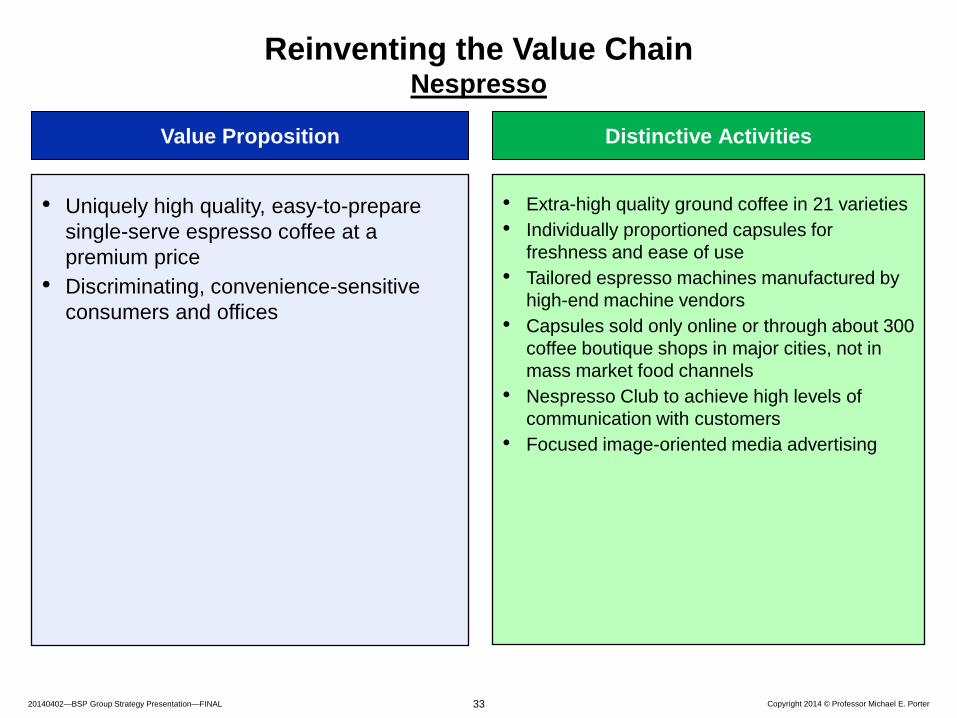

Reinventing the Value Chain Nespresso

• Uniquely high quality, easy-to-prepare

single-serve espresso coffee at a

premium price

• Discriminating, convenience-sensitive

consumers and offices

• Extra-high quality ground coffee in 21 varieties

• Individually proportioned capsules for

freshness and ease of use

• Tailored espresso machines manufactured by

high-end machine vendors

• Capsules sold only online or through about 300

coffee boutique shops in major cities, not in

mass market food channels

• Nespresso Club to achieve high levels of

communication with customers

• Focused image-oriented media advertising

Value Proposition Distinctive Activities

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 34

• Understanding industry structure

• Finding a novel value proposition

– Creative segmentation

• Reinventing the value chain

• Recognizing and capitalizing on changes, technology,

customers, needs, regulation, and others

• Successful strategies involve a core strategic insight that is

improved and expanded over time

Finding a Unique Strategic Position

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 35

Growing Strategically

1. Make the strategy even more distinctive

– Introduce new technologies, features, products or services that leverage other

distinctive activities within the value chain

– Create a social dimension to the value proposition and the value chain

2. Deepen the strategic position (rather than broaden it)

– Raise the penetration of chosen customers / needs

3. Expand geographically to tap new regions or countries using the same

positioning

– Aggressively reposition foreign acquisitions around the company’s strategy

4. Expand the market for what the company can uniquely deliver

– Find other customers and segments that value the strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 36

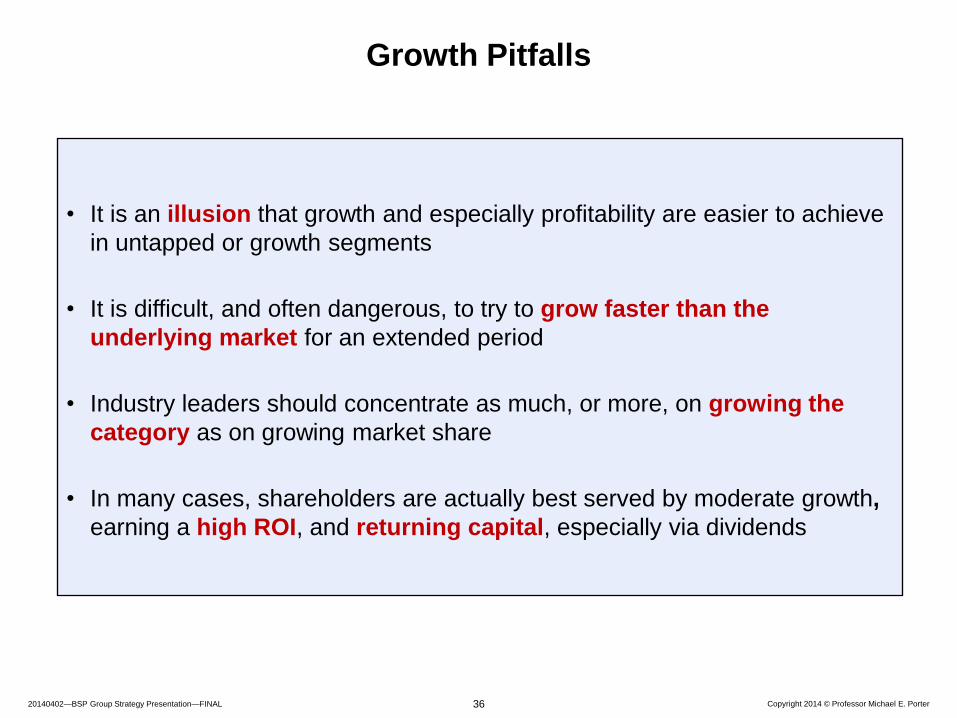

Growth Pitfalls

• It is an illusion that growth and especially profitability are easier to achieve

in untapped or growth segments

• It is difficult, and often dangerous, to try to grow faster than the

underlying market for an extended period

• Industry leaders should concentrate as much, or more, on growing the

category as on growing market share

• In many cases, shareholders are actually best served by moderate growth,

earning a high ROI, and returning capital, especially via dividends

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 37

Internationalization Strategic Principles

• Internationalize in ways that reinforce the company’s strategy

• Internationalize first in product lines or customer segments where the company

has the most unique advantages

• Prioritize markets to enter

– Similar needs and segments

– Expatriates

• Gain direct access to foreign markets as soon as practical rather than relying

solely on intermediaries

• Use alliances selectively as transitional strategies

– Ensure that alliances do not block the company’s ability to gain competitive advantage

and build its own capabilities

• Locate and integrate manufacturing and other activities from a regional

perspective

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 38

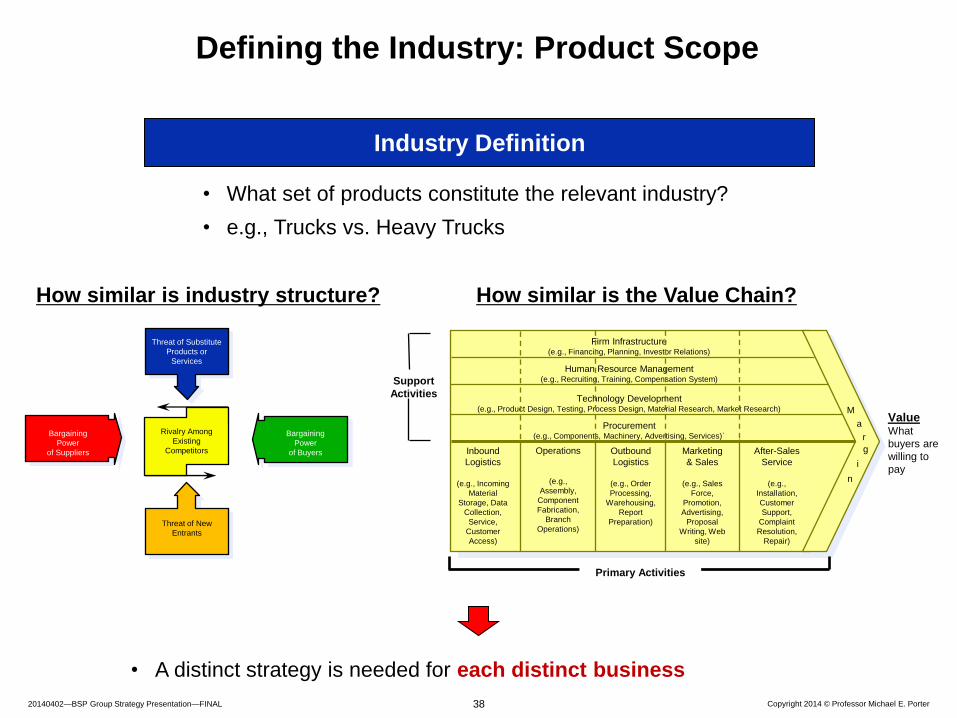

Defining the Industry: Product Scope

Support

Activities

Marketing

& Sales

(e.g., Sales

Force,

Promotion,

Advertising,

Proposal

Writing, Web

site)

Inbound

Logistics

(e.g., Incoming

Material

Storage, Data

Collection,

Service,

Customer

Access)

Operations

(e.g.,

Assembly,

Component

Fabrication,

Branch

Operations)

Outbound

Logistics

(e.g., Order

Processing,

Warehousing,

Report

Preparation)

After-Sales

Service

(e.g.,

Installation,

Customer

Support,

Complaint

Resolution,

Repair)

M

a

r

g

i

n

Primary Activities

Firm Infrastructure (e.g., Financing, Planning, Investor Relations)

Procurement (e.g., Components, Machinery, Advertising, Services)`

Technology Development (e.g., Product Design, Testing, Process Design, Material Research, Market Research)

Human Resource Management (e.g., Recruiting, Training, Compensation System)

Value What

buyers are

willing to

pay

• A distinct strategy is needed for each distinct business

Threat of Substitute

Products or

Services

Threat of New

Entrants

Rivalry Among

Existing

Competitors

Bargaining

Power

of Suppliers

Bargaining

Power

of Buyers

• What set of products constitute the relevant industry?

• e.g., Trucks vs. Heavy Trucks

Industry Definition

How similar is industry structure? How similar is the Value Chain?

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 39

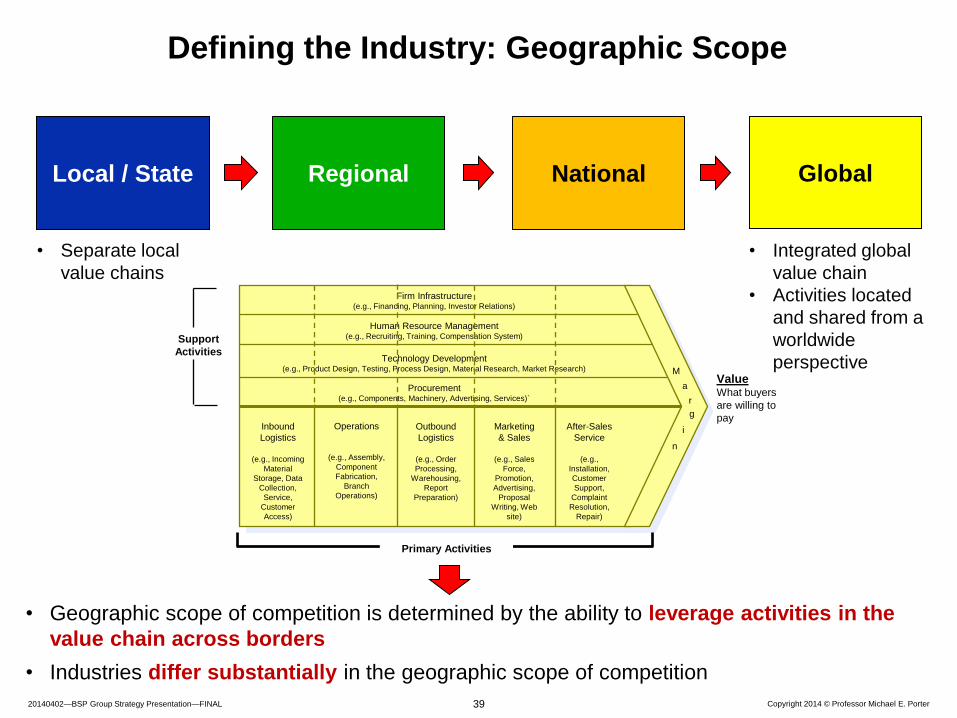

Defining the Industry: Geographic Scope

Support

Activities

Marketing

& Sales

(e.g., Sales

Force,

Promotion,

Advertising,

Proposal

Writing, Web

site)

Inbound

Logistics

(e.g., Incoming

Material

Storage, Data

Collection,

Service,

Customer

Access)

Operations

(e.g., Assembly,

Component

Fabrication,

Branch

Operations)

Outbound

Logistics

(e.g., Order

Processing,

Warehousing,

Report

Preparation)

After-Sales

Service

(e.g.,

Installation,

Customer

Support,

Complaint

Resolution,

Repair)

M

a

r

g

i

n

Primary Activities

Firm Infrastructure (e.g., Financing, Planning, Investor Relations)

Procurement (e.g., Components, Machinery, Advertising, Services)`

Technology Development (e.g., Product Design, Testing, Process Design, Material Research, Market Research)

Human Resource Management (e.g., Recruiting, Training, Compensation System)

Value What buyers

are willing to

pay

• Separate local

value chains

• Geographic scope of competition is determined by the ability to leverage activities in the

value chain across borders

• Industries differ substantially in the geographic scope of competition

Regional Local / State National

• Integrated global

value chain

• Activities located

and shared from a

worldwide

perspective

Global

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 40

• What set of businesses to compete in

• Capturing synergies across business units

Levels of Strategy

• How to compete in each distinct business or

industry

Corporate Strategy

Competitive or

Business Strategy

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 41

Fundamentals of Corporate Strategy

• Overall corporate size or diversity per se does not create economic value

• Competition occurs at the level of individual businesses, where competitive

advantage resides

• Being part of a diversified company involves inevitable costs for business

units

• Shareholders can diversify directly at lower cost

• A successful corporate strategy must produce clear and significant benefits to

the competitive advantage of business units

- The central issue is how being part of the corporation adds value to each

business

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 42

Car

Dealership

Financial

Services

Sugar

Airline

Hotel

Real Estate

Services

Computer

Wholesaler

Grocery

Stores

Fast Food

Franchises

Industrial

Parts

Imports/

Distribution

Food

Processing

Tobacco

Textiles

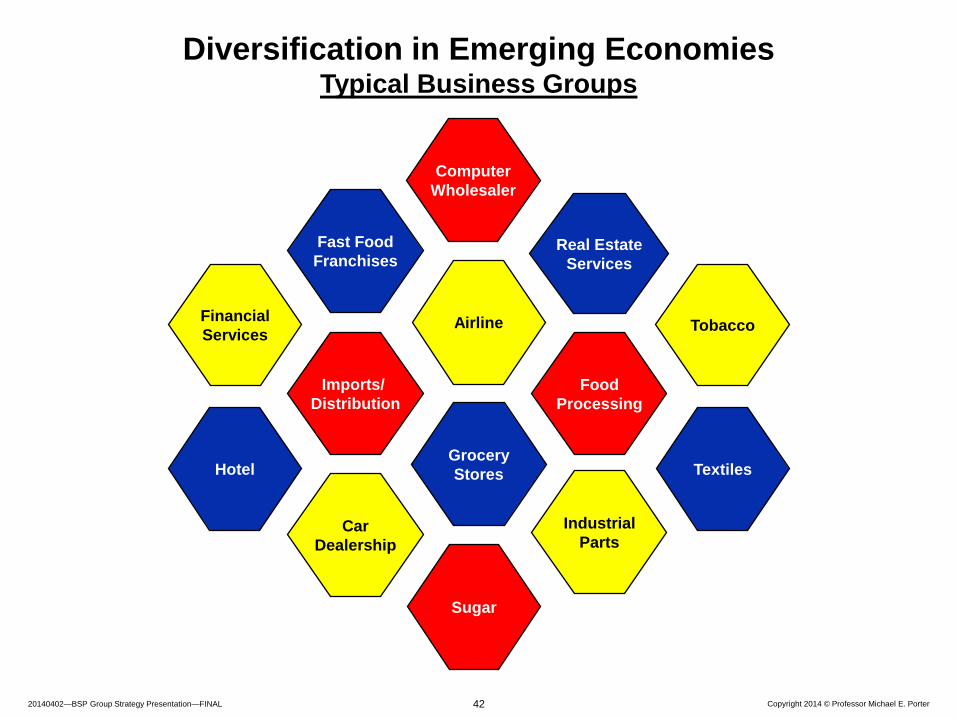

Diversification in Emerging Economies Typical Business Groups

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 43

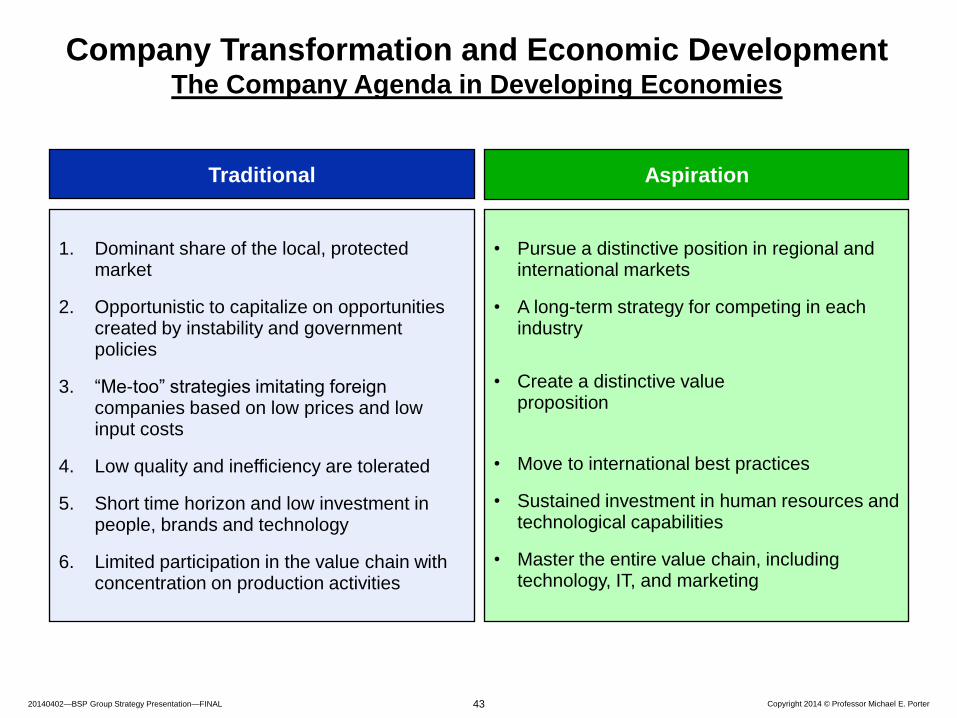

Company Transformation and Economic Development The Company Agenda in Developing Economies

1. Dominant share of the local, protected market

2. Opportunistic to capitalize on opportunities created by instability and government policies

3. “Me-too” strategies imitating foreign companies based on low prices and low input costs

4. Low quality and inefficiency are tolerated

5. Short time horizon and low investment in people, brands and technology

6. Limited participation in the value chain with concentration on production activities

• Pursue a distinctive position in regional and international markets

• A long-term strategy for competing in each industry

• Create a distinctive value proposition

• Move to international best practices

• Sustained investment in human resources and technological capabilities

• Master the entire value chain, including technology, IT, and marketing

Traditional Aspiration

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 44

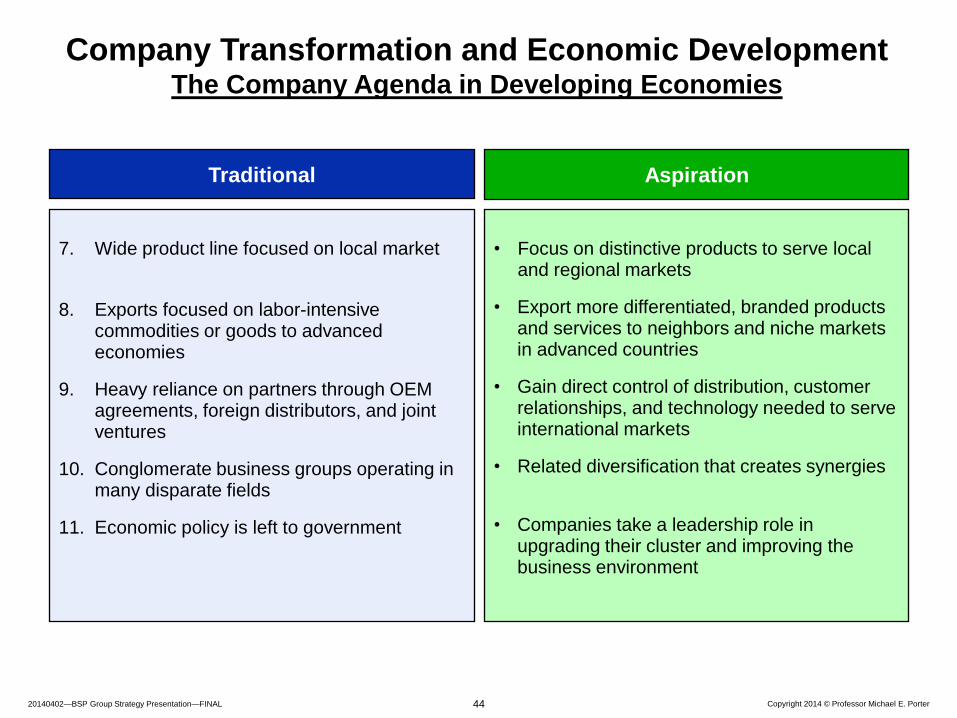

7. Wide product line focused on local market

8. Exports focused on labor-intensive commodities or goods to advanced economies

9. Heavy reliance on partners through OEM agreements, foreign distributors, and joint ventures

10. Conglomerate business groups operating in many disparate fields

11. Economic policy is left to government

• Focus on distinctive products to serve local and regional markets

• Export more differentiated, branded products and services to neighbors and niche markets in advanced countries

• Gain direct control of distribution, customer relationships, and technology needed to serve international markets

• Related diversification that creates synergies

• Companies take a leadership role in upgrading their cluster and improving the business environment

Traditional Aspiration

Company Transformation and Economic Development The Company Agenda in Developing Economies

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 45

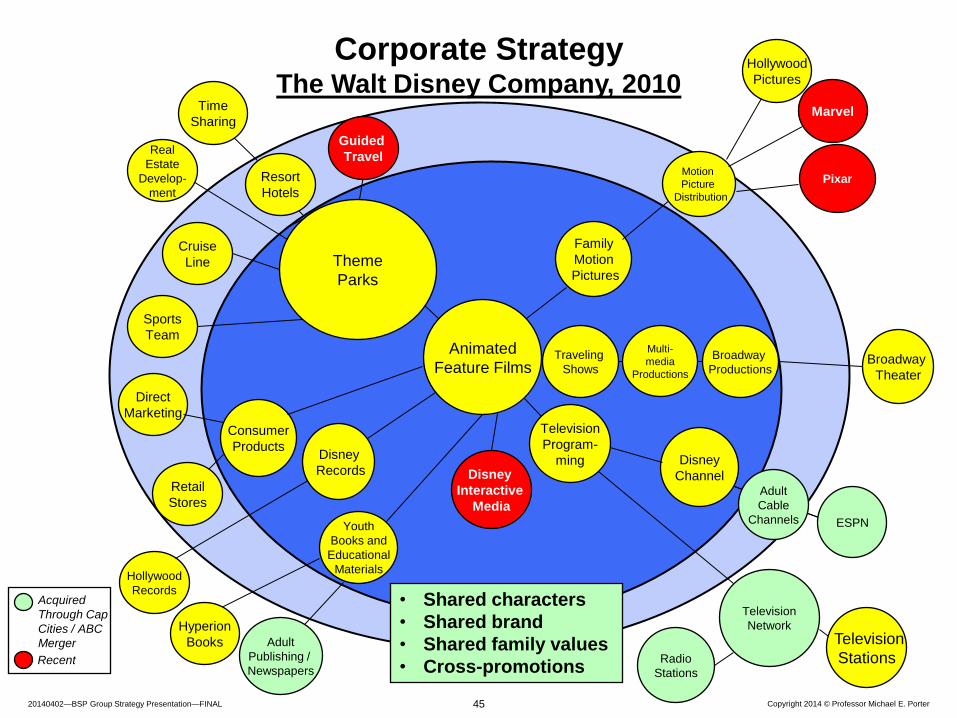

Direct

Marketing

Cruise

Line

Corporate Strategy The Walt Disney Company, 2010

Disney

Channel

Family

Motion

Pictures

Consumer

Products

Sports

Team Multi-

media

Productions

Broadway

Productions

Acquired

Through Cap

Cities / ABC

Merger

Traveling

Shows

Youth

Books and

Educational

Materials

• Shared characters

• Shared brand

• Shared family values

• Cross-promotions

Marvel

Hollywood

Pictures

Real

Estate

Develop-

ment

Time

Sharing

Television

Stations

Broadway

Theater

Television

Network

Hollywood

Records

Motion

Picture

Distribution

Disney

Records

Retail

Stores

Animated

Feature Films

Television

Program-

ming

Theme

Parks

Pixar

Guided

Travel

Disney

Interactive

Media

Recent

ESPN

Adult

Cable

Channels

Radio

Stations

Adult

Publishing /

Newspapers

Hyperion

Books

Resort

Hotels

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 46

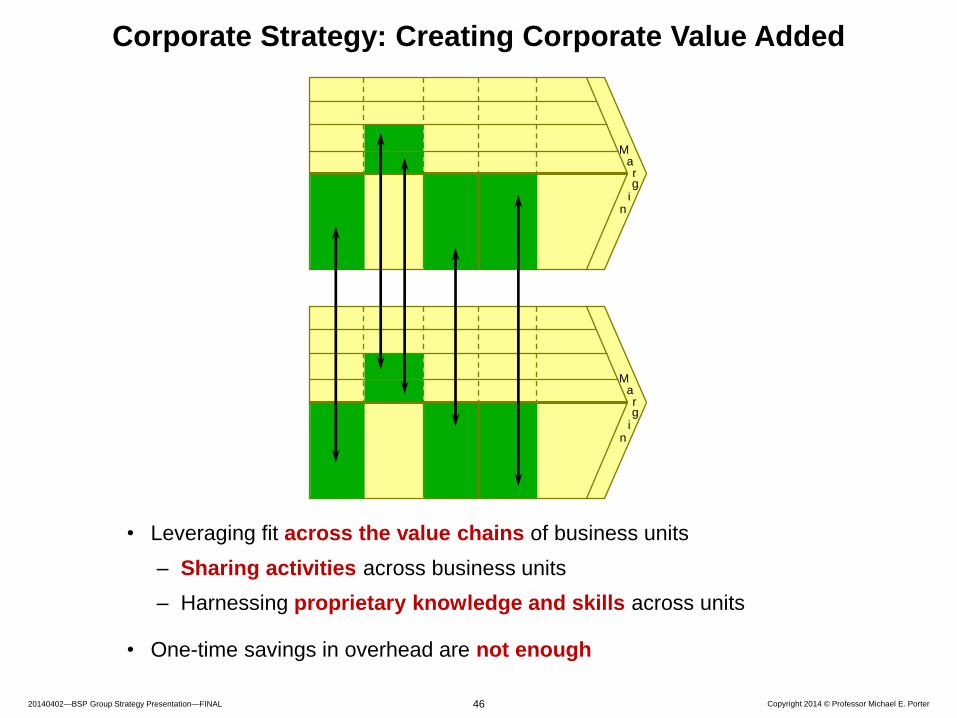

• Leveraging fit across the value chains of business units

– Sharing activities across business units

– Harnessing proprietary knowledge and skills across units

• One-time savings in overhead are not enough

M a r g

i n

M a r g

i n

Corporate Strategy: Creating Corporate Value Added

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 47

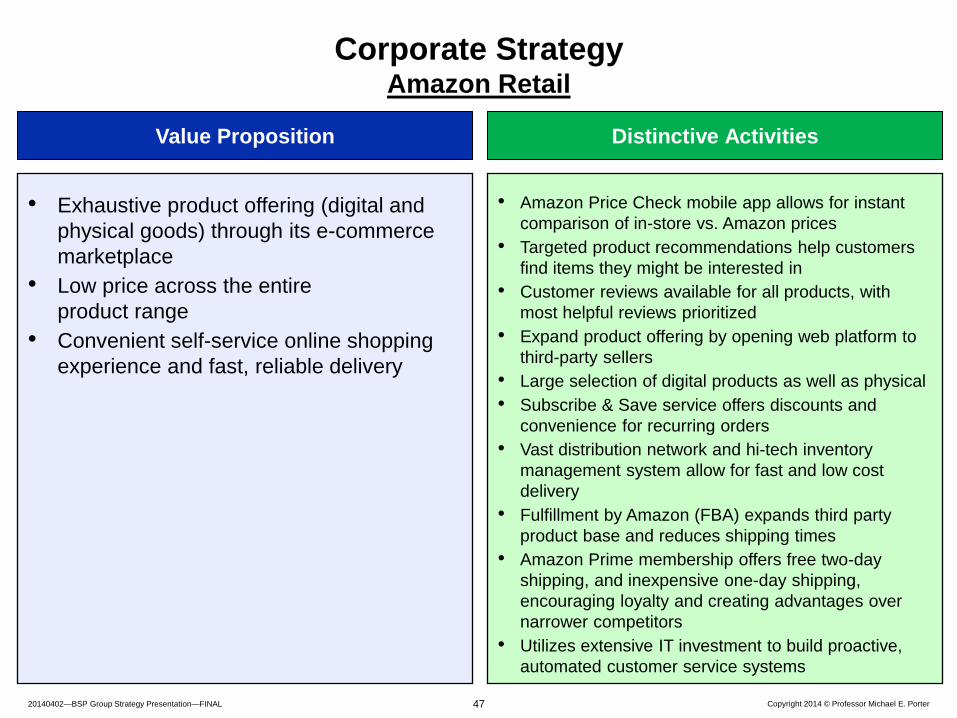

Corporate Strategy Amazon Retail

• Amazon Price Check mobile app allows for instant

comparison of in-store vs. Amazon prices

• Targeted product recommendations help customers

find items they might be interested in

• Customer reviews available for all products, with

most helpful reviews prioritized

• Expand product offering by opening web platform to

third-party sellers

• Large selection of digital products as well as physical

• Subscribe & Save service offers discounts and

convenience for recurring orders

• Vast distribution network and hi-tech inventory

management system allow for fast and low cost

delivery

• Fulfillment by Amazon (FBA) expands third party

product base and reduces shipping times

• Amazon Prime membership offers free two-day

shipping, and inexpensive one-day shipping,

encouraging loyalty and creating advantages over

narrower competitors

• Utilizes extensive IT investment to build proactive,

automated customer service systems

Value Proposition Distinctive Activities

• Exhaustive product offering (digital and

physical goods) through its e-commerce

marketplace

• Low price across the entire

product range

• Convenient self-service online shopping

experience and fast, reliable delivery

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 48

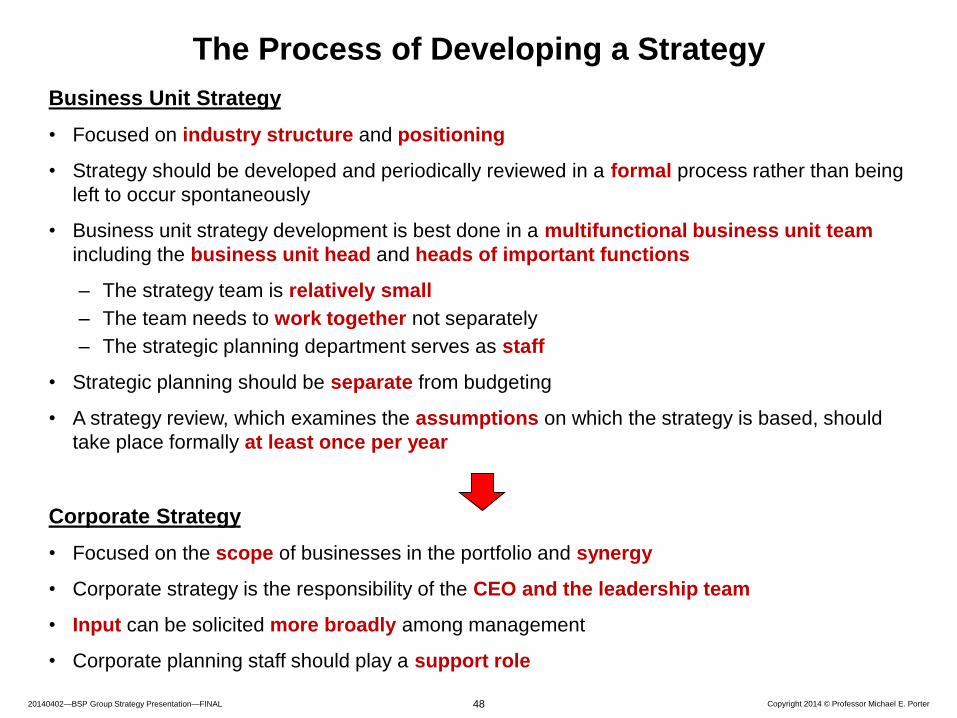

The Process of Developing a Strategy

Business Unit Strategy

• Focused on industry structure and positioning

• Strategy should be developed and periodically reviewed in a formal process rather than being

left to occur spontaneously

• Business unit strategy development is best done in a multifunctional business unit team

including the business unit head and heads of important functions

– The strategy team is relatively small

– The team needs to work together not separately

– The strategic planning department serves as staff

• Strategic planning should be separate from budgeting

• A strategy review, which examines the assumptions on which the strategy is based, should

take place formally at least once per year

Corporate Strategy

• Focused on the scope of businesses in the portfolio and synergy

• Corporate strategy is the responsibility of the CEO and the leadership team

• Input can be solicited more broadly among management

• Corporate planning staff should play a support role

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 49

Communicating Strategy

• Strategy involves everyone in an organization, not just senior management

• The basic strategy and value proposition must also be communicated to customers,

channels, suppliers, and financial markets

– What about confidentiality?

• The benefits of strategy are greatest when it is communicated widely in the organization

• Communicating strategy requires a simple and vivid way of describing the essence of the

company’s unique position

– Symbols of the strategy are invaluable tools

– Repetition

• Leaders should not assume that subordinates understand the strategy, or that they agree

with it

– Help each organizational unit translate the strategy into implications for its own mandate

• Individuals who do not ultimately accept the strategy cannot have an ongoing role in the

company

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 50

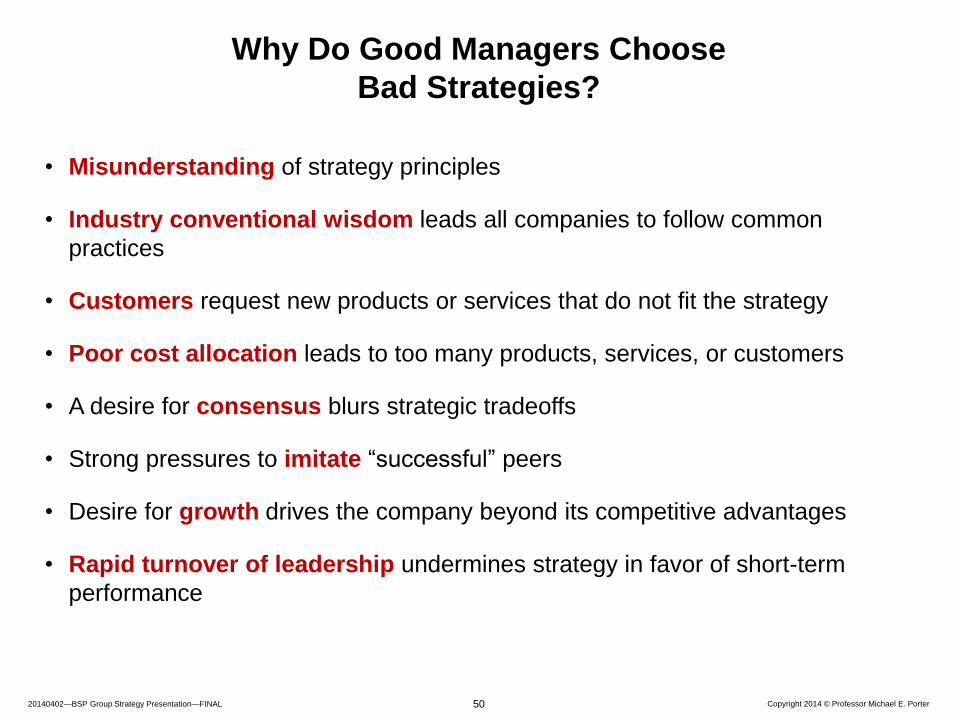

Why Do Good Managers Choose

Bad Strategies?

• Misunderstanding of strategy principles

• Industry conventional wisdom leads all companies to follow common

practices

• Customers request new products or services that do not fit the strategy

• Poor cost allocation leads to too many products, services, or customers

• A desire for consensus blurs strategic tradeoffs

• Strong pressures to imitate “successful” peers

• Desire for growth drives the company beyond its competitive advantages

• Rapid turnover of leadership undermines strategy in favor of short-term

performance

20140402—BSP Group Strategy Presentation—FINAL Copyright 2014 © Professor Michael E. Porter 51

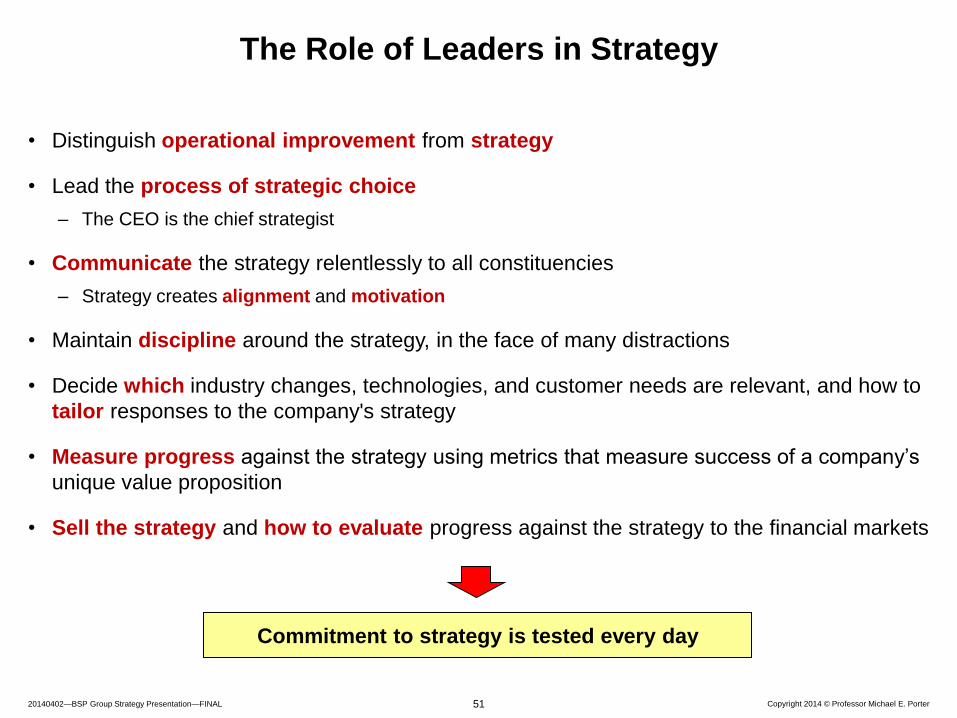

The Role of Leaders in Strategy

• Distinguish operational improvement from strategy

• Lead the process of strategic choice

– The CEO is the chief strategist

• Communicate the strategy relentlessly to all constituencies

– Strategy creates alignment and motivation

• Maintain discipline around the strategy, in the face of many distractions

• Decide which industry changes, technologies, and customer needs are relevant, and how to

tailor responses to the company's strategy

• Measure progress against the strategy using metrics that measure success of a company’s

unique value proposition

• Sell the strategy and how to evaluate progress against the strategy to the financial markets

Commitment to strategy is tested every day