Embed Size (px)

Citation preview

Thai Oil Public Company Limited

Q4 & 2016 Opportunity Day Presentation

2 Mar 2017

Time : 1.00 - 2.00 PM

Venue : Stock Exchange of Thailand

-2-

Disclaimer

The information contained in this presentation is intended solely for your

personal reference. Please do not circulate this material. If you are not an

intended recipient, you must not read, disclose, copy, retain, distribute or take

any action in reliance upon it.

Some statements made in this material are forward-looking with relevant

assumptions, which are subject to uncertainties, which may cause the actual

result/performance to be materially deviated from any future

result/performance implied by such forward-looking statements. Please note

that the company and management/staff are not capable to control and

guarantee if these forward-looking statements will be accurately materialized,

they are subject to various risks and uncertainties.

-3-

VISIONA LEADING FULLY INTEGRATED REFINING & PETROCHEMICAL

COMPANY IN ASIA PACIFIC

MISSION

• To be in top quartile on performance and return on investment

• To create a high-performance organization that promotes

teamwork, innovation and trust for sustainability

• To emphasis good Corporate Governance and commit to Corporate

Social Responsibility

VALUES

Corporate Vision, Mission and Values

Professionalism

Ownership & Commitment

Social Responsibility Integrity Teamwork & CollaborationInitiative

Vision Focus

Excellent Striving

-4-

Corporate Governance

Corporate Governance PolicyThe board of directors, management and all staff shall

commit to moral principles, equitable treatment to all

stakeholders and perform their duties for the company’s interest

with dedication, integrity, and transparency.

Anti-Corruption PolicyThe Board, the management, and employees must not

corrupt or accept corruption of all forms in any circumstances,

covering the business of the Company in every country and in

every relevant agency. The Company defines guidelines,

operating measures, and roles and duties of responsible persons,

as well as regularly monitoring and reviewing the

implementation of the anti-corruption policy in compliance with

changes in businesses, rules, regulations, and relevant laws.

Roles and Responsibilities

for Stakeholders

• Truthfully report company’s

situation and future trends to all

stakeholders equally on a timely

manner.

• Shall not exploit the confidential

information for the benefit of

related parties or personal gains.

• Shall not disclose any confidential

information to external parties.

Whistle-Blowing Channels

Should you discover any

ethical wrongdoing that is

not compliance to CG

policies or any activity that

could harm the Company’s

interest, please inform:

Chairman of the Board or

Chairman of the CG Committee or

Chairman of the Audit Committee or

CEO/President or Company Secretary

Thai Oil Public Company Limited

555/1 Energy Complex Building A

11F, Vibhavadi Rangsit Road,

Chatuchak, Bangkok 10900

http://www.thaioilgroup.com

+66-0-2797-2999 ext. 7440-7442

+66-0-2797-2973

-5-

Our Achievement in Sustainable Development

The World Most Sustainable Oil & Gas Refining and Marketing Company(from 28 invited companies in oil & gas refining and marketing industry)

60 industries3,420 companies invited2,473 companies assessed**cover companies outside DJSI invitation

For 4 consecutive years

For consecutive years 4

-6-

Presentation Agenda

2016 KEY HIGHLIGHTS

Q4 & 2016 PERFORMANCE ANALYSIS

1H-17 & 2017 MARKET OUTLOOK

TOP GROUP OVERVIEW

-7-

Thai Oil Group Business Structure

IRPC 20.0%

• 5 Oil & Chemical TankersCapacity : 52,350 DWT

• Crude Tankers: 3VLCCsCapacity: 881,050 DWT

• 14 crew & utility boats (120 DWT each)

• 2 Large vessels for crude, feedstock & product storage and transportation servicesCapacity: 200,000 DWT

• Ship management services

9.2 %

Principal power plant of PTTTotal Equity Capacity 1,922 MW of electricity 1,582 tons/hour of steam 2,080 Cu.m./hour of Industrial water 12,000 RT of Chilled water

PTT Group 80.0%

100.0% 100.0% 74.0% 100.0%

Thaioil (TOP)Thai Lube Base

(TLB)Thaioil Power

(TP)

Global Power Synergy Public Company Limited

Thaioil Energy Services(TES)

Thaioil Marine(TM)

Capacity : 275,000 barrels/day Small Power Producer

Program3-on-1 Combined CycleElectricity 118 MWSteam 216 tons/hour

PTT 26.0%

Proceeds the business on various professional of management services

PTT 22.6%

Thaioil 8.9%

TP 20.8%

100.0%

Thappline (THAP)

Multi-product PipelineCapacity:26,000 m.lts/y

20.0%

PTT 40.4%

Others 50.4%

Lube Base Oil Capacity :Base Oil 267,015 tons/annumBitumen350,000 tons/annumTDAE67,520 tons/annum

Thaioil SolventThrough TOP Solvent (TS)

100.0%

100.0%

Thaioil Ethanol(TET)

Solvent manufacturerCapacity : 141,000tons/annum

Thai Paraxylene(TPX)

100.0%80.5%

Solvent distribute in Thailand

Sak Chaisidhi (SAKC)

Top Solvent Vietnam

Solvent distribute in Vietnam

PTT ICT Solutions(PTT ICT)

Sapthip (SAP)

Cassava Based EthanolCapacity : 200,000 lts/day

50.0%

Ubon Bio Ethanol (UBE)21.3%

Cassava/Molasses Based PlantCapacity : 400,000 lts/day

PTT Energy Solutions(PTTES)

Provides engineering technique consulting services

20.0%PTT 40.0%

PTTGC 20.0%

BCP 21.3%Others 57.4%

PTTGC 22.7%

Aromatics Capacity:Paraxylene 527,000 tons/annumMixed Xylene52,000 tons/annumBenzene 259,000 tons/annumTotal 838,000 tons/annum

LABIX Company Limited (LABIX)

LAB producer and distributorCapacity: 120 KTA COD: 2016

Mitsui 25.0%75.0% TOP SPP

2 Small Power Producers Total capacity: 239 MWSteam capacity 498 T/HCOD 2016

100.0%

Sells Electricity/Steam to Group

47% 28% 14% 11%RefineryAromaticsLube BaseOthers

Net Profit Contribution

(Avg. from 2006 – 2016)

-8-

Key Milestones: 55 Years, A Long Track Record of Success

2007• Increased refining capacity to 275 kbd

2008• The first refinery in Thailand with diesel

production to comply with the sulfur content requirements of Euro IV

• Capacity expansion of Thai Paraxylene with total aromatics capacity of 900,000 tons p.a.

• Invested in Solvents business in Thailand and Vietnam

1993• We expanded our refining capacity to 190 kbd

1994 – 1997• Increased total refining capacity to 220 kbd• Initial investment in Thai Paraxylene (“TPX”) and

Thai Lube Base (“TLB”)• IPT became the first IPP to enter into a PPA with

EGAT2 with 700 MW capacity ; separately, Thaioil Power (“TP”) constructed the power generation plant under the SPP with 118 MW capacity

1961 – 1997 Capacity expansion and initial stage of

business diversification

2004 – 2011Listing, expansion and

diversification

TodayA leading integrated refining and

petrochemical group in Asia Pacific

• 275 kbd refinery ( approximately 22% of Thailand’s total refining capacity)

• Nelson index 9.81

• Diversified business through 13 subsidiaries

• The 3rd largest listed companyby revenue in Thailand

1961 – 1964

2004

1961• Incorporated

1964• Commenced

operation with distillation capacity of 35 kbd

• Simple refinery with Nelson complexity Index ~ 41

1970• Refining capacity

expanded to 65 kbpd

1989• Increased refining

capacity to 90 kbpd

2004• IPO and listed on the SET • Acquired remaining shares in

Thai Paraxylene and Thai Lube Base which became our wholly-owned subsidiaries

2007 -2008

2010

2011

1993-19971970-1989

2013-2014• Established LABIX• Invested in power biz via

GPSC & TOP SPP• Completed Emission

Improvement, HVU-2 Debottlenecking & CDU-3 Preheat Train project

2015-2016• 2016 Revenue 274,739 MB • 2016 Net profit 21,222 MB • Completed Projects: LABIX

& TOP SPP

2011• Manufactured diesel and

ULG in compliance with the sulfur and BZ aromatics content requirements of the Euro IV

• Acquired 1st VLCC

2010• Established

Thaioil Ethanol • Production

expansion of TDAE by 50,000 tons per annum

Note 1. Based on our internal estimates using the methodology of the Nelson Complexity Index 2. The Electricity Generating Authority of Thailand (“EGAT”) is the national grid

-9-

TOP Group Synergy & Strategic Role in PTT Group Value Chain

NATURAL GAS

CRUDE IMPORT

Mixed-Xylene

Solvent

Toluene

Pentane

Hexane

SOLVENTS

TP & TOP SPP provides electricity and steam to Thai Oil group and sells its remaining power to the national grid

AROMATICS & LAB

Lube Base Oil

Bitumen

TDAE

Slack Wax

ExtractLUBE BASE

REFINERY LPG

Fuel Oil

Diesel

Gasoline

Jet/Kero

PLATFORMATE

LONG RESIDUE

REFINED PETROLEUM

POWER

Diversifying to a broad

range of downstream

products to enjoy higher

profit margins and

reduce earnings

volatility

Thai Oil’s Businesses

The majority of refined petroleum products are sold domestically to PTT

PTT is our principal domestic customer for our lube base products

Upstream Intermediate Downstream

Paraxylene

Benzene

Mixed-Xylene

Toluene

LAB

-10-

2016 KEY HIGHLIGHTS

-11-

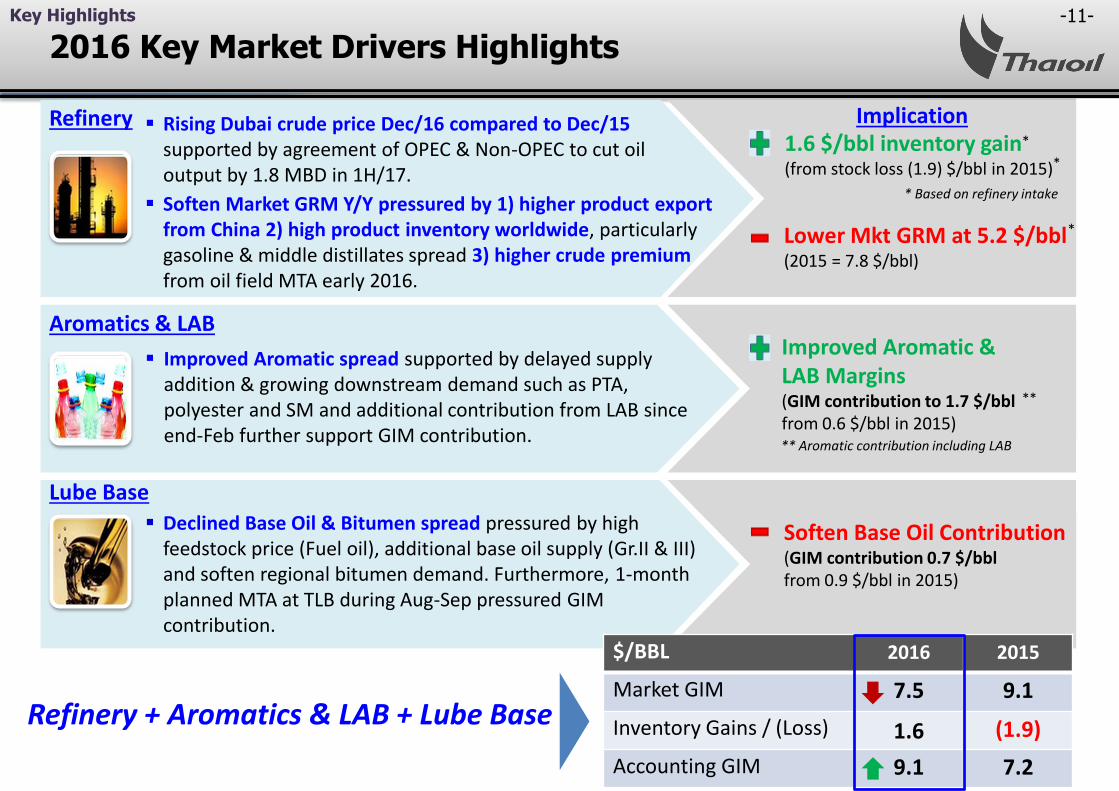

2016 Key Market Drivers Highlights

Improved Aromatic & LAB Margins(GIM contribution to 1.7 $/bbl from 0.6 $/bbl in 2015)

Implication1.6 $/bbl inventory gain(from stock loss (1.9) $/bbl in 2015)

Lower Mkt GRM at 5.2 $/bbl (2015 = 7.8 $/bbl)

Refinery

Aromatics & LAB

Lube Base

Soften Base Oil Contribution(GIM contribution 0.7 $/bbl from 0.9 $/bbl in 2015)

Refinery + Aromatics & LAB + Lube Base

$/BBL 2016 2015

Market GIM 7.5 9.1

Inventory Gains / (Loss) 1.6 (1.9)

Accounting GIM 9.1 7.2

Rising Dubai crude price Dec/16 compared to Dec/15 supported by agreement of OPEC & Non-OPEC to cut oil output by 1.8 MBD in 1H/17.

Soften Market GRM Y/Y pressured by 1) higher product export from China 2) high product inventory worldwide, particularly gasoline & middle distillates spread 3) higher crude premium from oil field MTA early 2016.

Declined Base Oil & Bitumen spread pressured by high feedstock price (Fuel oil), additional base oil supply (Gr.II & III) and soften regional bitumen demand. Furthermore, 1-month planned MTA at TLB during Aug-Sep pressured GIM contribution.

Improved Aromatic spread supported by delayed supply addition & growing downstream demand such as PTA, polyester and SM and additional contribution from LAB since end-Feb further support GIM contribution.

Key Highlights

*

*

* Based on refinery intake

*

**

** Aromatic contribution including LAB

-12-

3,292 4,078

12,55918,972

3,629

2,624

(532)

3,510

6,138

(6,945)(93)

242

1,041 1,338

274

(2,028) (2,145)

(3,808)

Net Operating Profit (before tax) Profitability Improvement

Stock G/(L) (before tax) Reversal of NRV/(NRV) (before tax)

Others

67%15%

6%9%

3%

2016 Key Achievements

Key Achievements 2016

Key Highlights

TOP Group Net Profit

Maintain high reliable production Unit : million THB (MB)

i.e. FX G/(L), Hedging G/(L), tax expense etc.

Operational Excellence 2016 2015

Refinery 108 % 108 %

Aromatic 81 % 81 %

Base Oil 81 % 86 %

21,222 MB

Q4/16

5,802 MB

Q3/16

2,941 MB

2016

12,181 MB

2015

Thailand Energy Awards 2016 (The Outstanding Award in Energy Conservation for a controlled plant)

Best IR by Senior Management & Best IR in Energy Sector from IR Magazine South East Asia 2016 & Best IR from SET Award 2016

The World Most Sustainable Oil & Gas Refining & Marketing Company for 4th

consecutive years (Jan/17)

Successfully COD: LAB in Q1/16 SPP (2 blocks) in Q2/16

Capture high local & Indochina sales of petroleum products

2016 2015

Local 87 % 80 %

Indochina 9 % 9 %

Other exports 4 % 11 %Growth

Sustainability& Awards

65%5%

17%

8%5%

2016 2015

* 1-month planned MTA

*

-13-

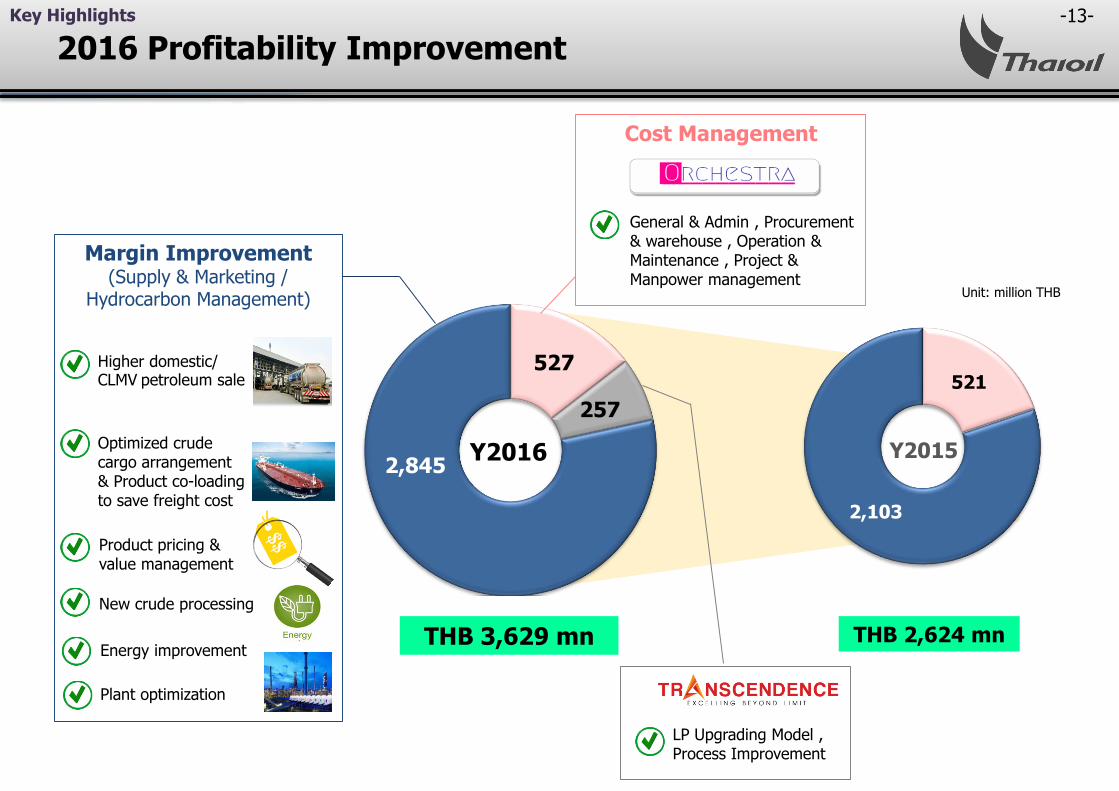

521

2,103

Y2016 Y2015

THB 3,629 mn THB 2,624 mn

Unit: million THB

527

257

2,845

Margin Improvement (Supply & Marketing /

Hydrocarbon Management)

Higher domestic/ CLMV petroleum sale

Product pricing & value management

Optimized crude cargo arrangement & Product co-loading to save freight cost

New crude processing

Energy improvement

Plant optimization

Cost Management

General & Admin , Procurement & warehouse , Operation & Maintenance , Project & Manpower management

LP Upgrading Model , Process Improvement

2016 Profitability ImprovementKey Highlights

-14-

Annual DPS (Baht/share)

1.80 3.50 3.50 4.50 2.75 2.55 2.00 3.30 2.70 2.30 1.16 2.70 4.50

Dividend Payout 25% 40% 45% 48% n.a. 43% 45% 45% 45% 50% n.a. 45% 43%

Dividend Yield* 4.0% 5.6% 5.6% 6.2% 5.2% 7.1% 4.0% 4.7% 4.2% 3.6% 2.3% 5.0% 6.7%

7.82

9.19

8.13

9.40

0.11

5.91

4.39

7.28

6.04

4.57

-2.03

5.97

10.40

FY/04 FY/05 FY/06 FY/07 FY/08 FY/09 FY/10 FY/11 FY/12 FY/13 FY/14 FY/15 FY/16

Avg TOP price 44.7 63.0 62.7 72.7 53.3 35.9 49.9 69.8 65.1 64.6 50.4 53.5 66.7

1.501.75 1.75

1.050.60

1.300.50 0.80 0.56 0.90

1.50

2.00

2.75

1.00 1.50

1.40

2.00

2.20 1.50 0.60

1.80

3.00

1.80

3.50

Dividend Policy : Not less than 25% of consolidated net profit after deducting reserves, subject to cash flow and investment plan

Unit : THB/Share EPSR

1H dividend

* Based on average TOP share price in each year

2H dividend

Year Dividend

2016 Dividend Payment

R Based on restated financial statement (year 2013 – 2014)

**

** Dividend payout before restated = 45%

***

*** Subject to AGM Approval on Apr 7,2017

Key Highlights

-15-

Q4 & 2016 PERFORMANCE ANALYSIS

-16-

TOP’s Domestic Sale vs Industry**Sales breakdown by customers

Refinery: Ongoing High Utilization Rate & Domestic Sales Portion

** Source: Department of Energy Business, Ministry of Energy

85%85% 87% 89% 87%

86%80%

71%

15% 15% 13%11% 13% 14% 20% 29%

Q4/16

TOP IndustryThailand

TOP IndustryThailand

FY/15

TOP IndustryThailand

Q3/16

ExportQ3/16 Q4/16 FY/16 FY/15

TOP Ind. TOP Ind. TOP Ind. TOP Ind.

CLMV 9% 5% 8% 6% 9% 5% 9% 8%

Others 6% 10% 5% 5% 4% 9% 11% 21%

Domestic

Export

FY/16

TOP IndustryThailand

39%

12%6%

1%

29%

9%4%

DomesticJobbers

Q4/16

Sales

Breakdown

Export 13%

39%

12%6%

1%

29%

9%4%

DomesticJobbers

FY/16

Sales

Breakdown

Export 13%

TOP/ Domestic Refinery Utilization Rate

94% 95% 94% 95%

91%88% 89%

95% 94%91%

106%107%107%110%

107%109%

107%110%

108%108%

70%

90%

110%

Q1/15 Q2 Q3 Q4 Q1/16 Q2 Q3 Q4 2015 2016

Industry utilization rate TOP utilization rate

Unit: % Utilization Rate

0

200

400

600

800

Mogas Jet/Kero Diesel Total Demand

2015 2016

3.1%

9.8%

5.4%

KBD

6.8%

Domestic Oil Demand

*

* exclude Fuel Oil & LPG demand

Refining

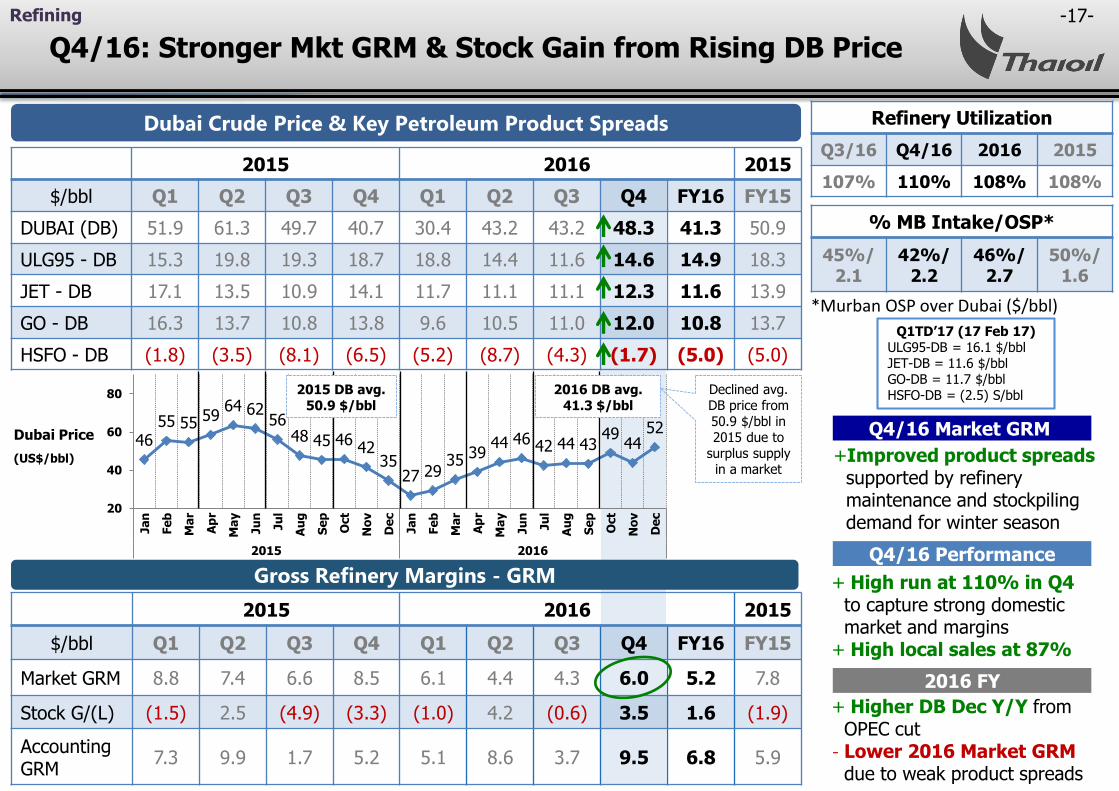

-17-

2015 2016 2015

$/bbl Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

DUBAI (DB) 51.9 61.3 49.7 40.7 30.4 43.2 43.2 48.3 41.3 50.9

ULG95 - DB 15.3 19.8 19.3 18.7 18.8 14.4 11.6 14.6 14.9 18.3

JET - DB 17.1 13.5 10.9 14.1 11.7 11.1 11.1 12.3 11.6 13.9

GO - DB 16.3 13.7 10.8 13.8 9.6 10.5 11.0 12.0 10.8 13.7

HSFO - DB (1.8) (3.5) (8.1) (6.5) (5.2) (8.7) (4.3) (1.7) (5.0) (5.0)

2015 2016 2015

$/bbl Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

Market GRM 8.8 7.4 6.6 8.5 6.1 4.4 4.3 6.0 5.2 7.8

Stock G/(L) (1.5) 2.5 (4.9) (3.3) (1.0) 4.2 (0.6) 3.5 1.6 (1.9)

AccountingGRM

7.3 9.9 1.7 5.2 5.1 8.6 3.7 9.5 6.8 5.9

4655 55 59

64 6256

48 45 4642

3527 29

35 3944 46 42 44 43

4944

52

20

40

60

80

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oct

No

v

De

c

2015 2016

Refining

Dubai Crude Price & Key Petroleum Product Spreads Refinery Utilization

Q3/16 Q4/16 2016 2015

107% 110% 108% 108%

Gross Refinery Margins - GRM

+Improved product spreads supported by refinery maintenance and stockpiling demand for winter season

Dubai Price

(US$/bbl)

Q4/16 Market GRM

Q4/16 Performance

*Murban OSP over Dubai ($/bbl)

Q1TD’17 (17 Feb 17) ULG95-DB = 16.1 $/bblJET-DB = 11.6 $/bblGO-DB = 11.7 $/bblHSFO-DB = (2.5) S/bbl

Q4/16: Stronger Mkt GRM & Stock Gain from Rising DB Price

2015 DB avg. 50.9 $/bbl

2016 DB avg. 41.3 $/bbl

Declined avg. DB price from 50.9 $/bbl in 2015 due to

surplus supply in a market

% MB Intake/OSP*

45%/2.1

42%/2.2

46%/2.7

50%/1.6

2016 FY

+ High run at 110% in Q4 to capture strong domestic market and margins

+ High local sales at 87%

+ Higher DB Dec Y/Y from OPEC cut

- Lower 2016 Market GRM due to weak product spreads

-18-

2015 2016 2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

Aromatic P2F -$/ton 11 76 54 93 98 99 109 95 100 63

Aromatic P2F -$/bbl 1.4 9.9 7.1 12.2 12.8 13.0 14.3 12.4 13.1 8.2

GIM contribution** (0.4) 0.8 0.5 1.3 1.4 1.7 1.9 1.5 1.7 0.6

Remark: TOL –ULG95 Q3/16 = 99 $/ton, Q4/16 = 103 $/ton, 2016 = 115 $/ton

290 251

224 277

238 224

266 235 235

270 295 299 290

360 347 339

292 314

377 345

303 266

296 278

120

56

119

184

66 94

164

70

25 59

125 119

121 167

180 177

130 108

193 187 143

100

191

264

-30

120

270

420

2015 2016 2015

$/ton Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

PX*-ULG95 255 246 233 288 332 315 341 280 317 256

BZ*-ULG95 98 115 74 101 156 138 174 185 163 97

- Pressured Aromatics marginmainly from declined PX spread as startup of new PX plant from Reliance Industries No.4 phase 1 (0.8 MTA) but partially offset by better BZ spread as less supply from China & Japan due to environmental & earthquake incident respectively

Aromatics/LAB

Aromatics Spreads and Margins

Aromatic’s Sales (excluding byproduct) & Product-To-Feed Margin (P2F)

Aromatics Production

Q3/16 Q4/16 2016 2015

80% 82% 81% 81%

(Unit : KTon)

(US$/Ton)

PX-ULG95

BZ-ULG95

Q4/16 Market GRM

+ Higher Aromatic run at 82% & maintain high LAB run at 104%

103 108 126 106 104 113 108 110

48 4451

42 43 4435 545

3221 20

17 11 8TL

BZ

PX

** including LAB contribution since 25 Feb 2016

Q1TD’17 (17 Feb 17) PX-ULG95 = 302 $/tonBZ-ULG95 = 380 $/ton

Q4/16: Fallen Margins Mainly Pressured by Lower PX spread

435

17657

442

18559

* PX price = CFP Taiwan, BZ price = FOB Korea

Q4/16 Performance

2016 FY

+ Higher P2F due to less supply addition

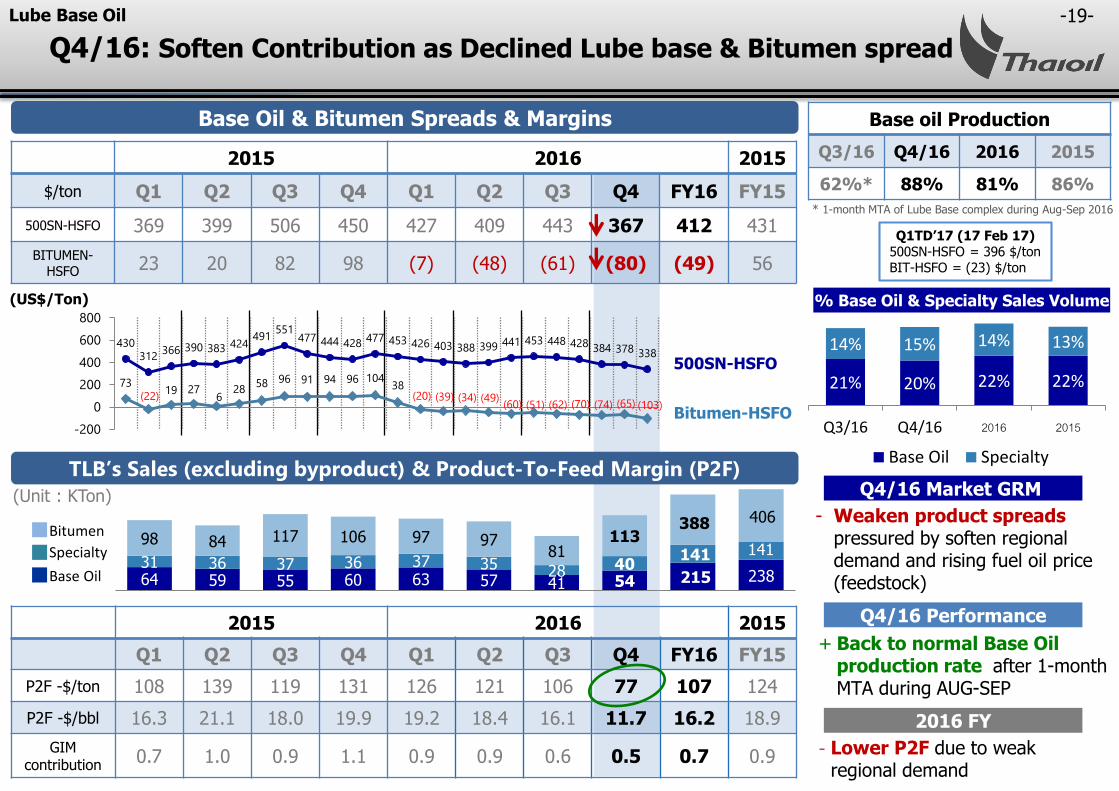

-19-

2015 2016 2015

$/ton Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

500SN-HSFO 369 399 506 450 427 409 443 367 412 431

BITUMEN-HSFO 23 20 82 98 (7) (48) (61) (80) (49) 56

430312

366 390 383 424491

551477 444 428

477 453 426 403 388 399 441 453 448 428 384 378 338

73 (22)

19 27 6

28 58 96 91 94 96 104

38 (20) (39) (34) (49)

(60) (51) (62) (70) (74) (65) (103)

-200

0

200

400

600

800

2015 2016 2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 FY16 FY15

P2F -$/ton 108 139 119 131 126 121 106 77 107 124

P2F -$/bbl 16.3 21.1 18.0 19.9 19.2 18.4 16.1 11.7 16.2 18.9

GIM contribution

0.7 1.0 0.9 1.1 0.9 0.9 0.6 0.5 0.7 0.9

Lube Base Oil

64 59 55 60 63 57 41 5431 36 37 36 37 35 28 40

98 84 117 106 97 9781

113

Base Oil & Bitumen Spreads & Margins

TLB’s Sales (excluding byproduct) & Product-To-Feed Margin (P2F)

Base oil Production

Q3/16 Q4/16 2016 2015

62%* 88% 81% 86%

500SN-HSFO

Bitumen-HSFO

(Unit : KTon)

(US$/Ton)

Q4/16 Performance

Bitumen

Specialty

Base Oil

+ Back to normal Base Oil production rate after 1-month MTA during AUG-SEP

21% 20% 22% 22%

14% 15% 14% 13%

Q3/16 Q4/16 2016 2015

Base Oil Specialty

% Base Oil & Specialty Sales Volume

Q1TD’17 (17 Feb 17) 500SN-HSFO = 396 $/tonBIT-HSFO = (23) $/ton

Lower Base Oil Sales Volume

215

141

388

238

141

406

Q4/16: Soften Contribution as Declined Lube base & Bitumen spread

Q4/16 Market GRM

- Weaken product spreads pressured by soften regional demand and rising fuel oil price (feedstock)

* 1-month MTA of Lube Base complex during Aug-Sep 2016

2016 FY

- Lower P2F due to weak regional demand

-20-

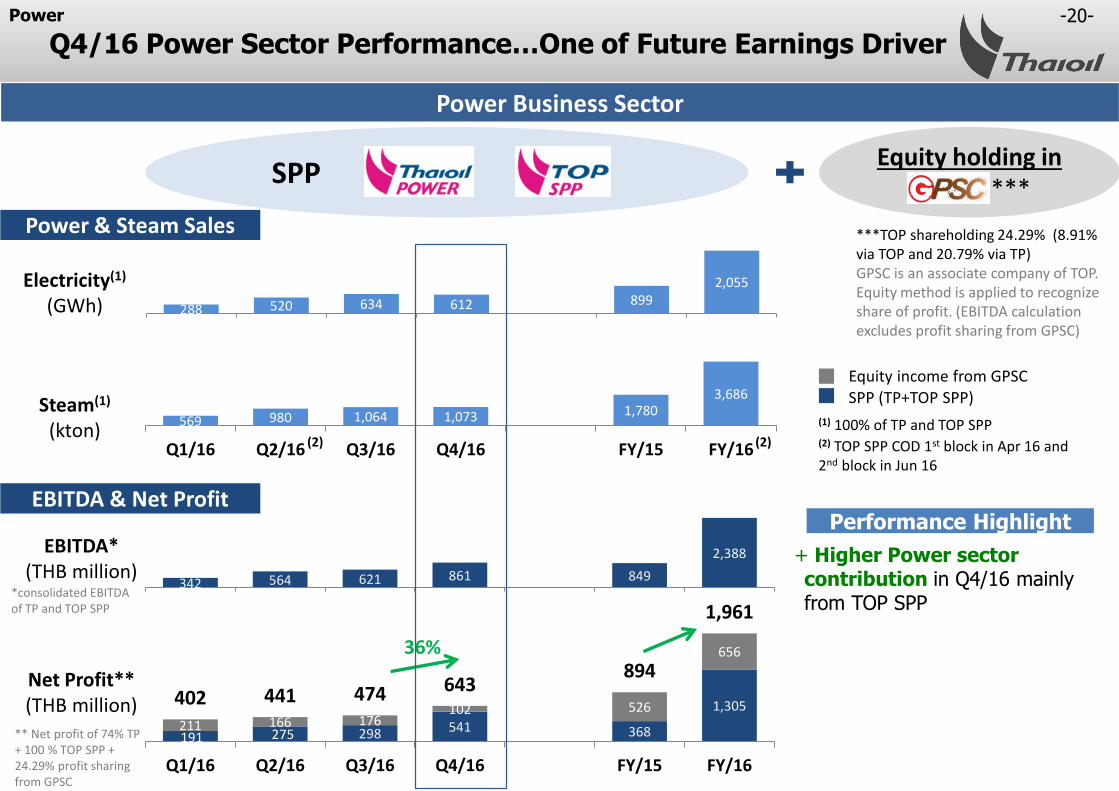

288 520 634 612 8992,055

Q1/16 Q2/16 Q3/16 Q4/16 FY/15 FY/16

Equity holding inGPSC ****

SPP

Q4/16 Power Sector Performance…One of Future Earnings Driver

342 564 621 861 849

2,388

Q1/16 Q2/16 Q3/16 Q4/16 FY/15 FY/16

191 275 298 541 368

1,305

211 166 176102 526

656

402 441 474 643894

1,961

Q1/16 Q2/16 Q3/16 Q4/16 FY/15 FY/16

*consolidated EBITDA of TP and TOP SPP

** Net profit of 74% TP + 100 % TOP SPP + 24.29% profit sharing from GPSC

+ Higher Power sector contribution in Q4/16 mainly from TOP SPP

36%

Power Business Sector

Power & Steam Sales

EBITDA & Net Profit

Electricity(1)

(GWh)

Steam(1)

(kton)569 980 1,064 1,073 1,780

3,686

Q1/16 Q2/16 Q3/16 Q4/16 FY/15 FY/16

EBITDA*(THB million)

Net Profit**(THB million)

***TOP shareholding 24.29% (8.91% via TOP and 20.79% via TP)GPSC is an associate company of TOP. Equity method is applied to recognize share of profit. (EBITDA calculation excludes profit sharing from GPSC)

SPP (TP+TOP SPP)Equity income from GPSC

Power

(1) 100% of TP and TOP SPP(2) (2) (2) TOP SPP COD 1st block in Apr 16 and

2nd block in Jun 16

Performance Highlight

-21-

4.1 4.9 5.4

1.1

7.6 5.8 5.2

6.7 5.9

9.4 1.8 1.8

0.1

0.1

0.6

0.6 1.7 1.7

1.6

1.6

0.9 0.9

0.7

0.7

0.9

0.9 0.7

0.7 0.5

0.5

6.8 6.2

9.17.5 8.07.6

1.9

7.2 9.1

11.5

2013 2014 2015 2016 Q4/16

Refinery Aromatics+LAB Lube Base

4.3

5.7

7.8

5.26.0

5.1

1.2

5.96.8

9.5

2013 2014 2015 2016 Q4/16

1.4 1.5 1.3 1.4 1.80.7 0.8 0.6 0.5

0.52.1 2.3 1.9 1.9 2.3

2013 2014 2015 2016 Q4/16

Operating Cost Interest Expense

1.7 1.8 1.5 1.8 2.30.6 0.7 0.6 0.5

0.62.32.5

2.1 2.3 2.9

2013 2014 2015 2016 Q4/16

Operating Cost Interest Expense

Refinery’s Cash Cost

(Unit: US$/bbl)

Group’s Cash Cost

(Unit: US$/bbl)

(Unit: US$/bbl)

Market GIM Accounting GIM (Market GIM + Stock G/L)

Market GRM Accounting GRM (Market GRM + Stock G/L)

Gross Refining Margin

Gross Integrated Margin

(Unit: US$/bbl)

Integrated Margin & Competitive Cash Cost

Financial

*

*

*Including MTA cost in MTA period since mid Jun-late July 2014 for 46 days (TOP MTA cost in 2014 = 436 MB or 0.14 $/bbl)

*Including MTA cost in MTA period since mid Jun-late July 2014 for 46 days ( TOP group MTA cost in 2014 = 609 MB or 0.20 $/bbl)

(excl. one-time non-operating item)

(excl. one-time non-operating item)

(net)

(net)

Higher group cash cost in 2016 mainly from MTA cost in TLB ~198 MB or ~ 0.1 $/bbl

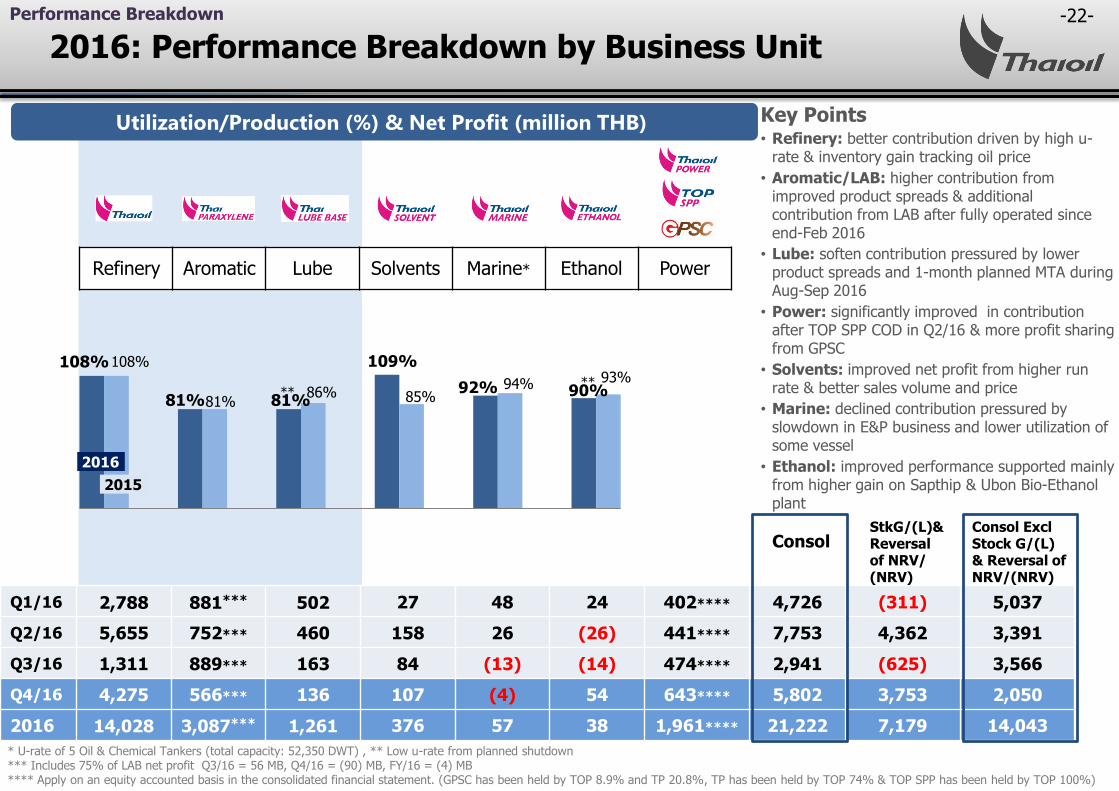

-22-

* U-rate of 5 Oil & Chemical Tankers (total capacity: 52,350 DWT) , ** Low u-rate from planned shutdown*** Includes 75% of LAB net profit Q3/16 = 56 MB, Q4/16 = (90) MB, FY/16 = (4) MB**** Apply on an equity accounted basis in the consolidated financial statement. (GPSC has been held by TOP 8.9% and TP 20.8%, TP has been held by TOP 74% & TOP SPP has been held by TOP 100%)

2016: Performance Breakdown by Business Unit

Q1/16 2,788 881*** 502 27 48 24 402**** 4,726 (311) 5,037

Q2/16 5,655 752*** 460 158 26 (26) 441**** 7,753 4,362 3,391

Q3/16 1,311 889*** 163 84 (13) (14) 474**** 2,941 (625) 3,566

Q4/16 4,275 566*** 136 107 (4) 54 643**** 5,802 3,753 2,050

2016 14,028 3,087*** 1,261 376 57 38 1,961**** 21,222 7,179 14,043

108%

81% 81%

109%

92% 90%

108%

81%86% 85%

94% 93%

2016

2015

Refinery Aromatic Lube Solvents Marine* Ethanol Power

Performance Breakdown

Consol

Utilization/Production (%) & Net Profit (million THB)

StkG/(L)&Reversal of NRV/(NRV)

Consol ExclStock G/(L)& Reversal of NRV/(NRV)

****

Key Points• Refinery: better contribution driven by high u-

rate & inventory gain tracking oil price

• Aromatic/LAB: higher contribution from improved product spreads & additional contribution from LAB after fully operated since end-Feb 2016

• Lube: soften contribution pressured by lower product spreads and 1-month planned MTA during Aug-Sep 2016

• Power: significantly improved in contribution after TOP SPP COD in Q2/16 & more profit sharing from GPSC

• Solvents: improved net profit from higher run rate & better sales volume and price

• Marine: declined contribution pressured by slowdown in E&P business and lower utilization of some vessel

• Ethanol: improved performance supported mainly from higher gain on Sapthip & Ubon Bio-Ethanol plant

-23-

THB/US$ - average 35.57 35.00 0.57

THB/US$ - ending 36.00 34.88 1.12

Effective Tax Rate (%) * 12% 13% (1%)

35.46 34.44 1.02

36.00 36.25 (0.25)

10% 11% (1%)

Stock G/(L)&Reversal of NRV/(NRV) 3,753 (625) 4,378

Net Profit/ (Loss) excl. StkG/(L) and Reversal of NRV/(NRV)

2,050 3,566 (1,516)

Sales Revenue 77,104 68,476 8,628

Hedging Gain / (Loss) (330) 206 (536)

EBITDA 10,085 5,392 4,693

EBITDA excl. Stk G/(L) & Reversal of NRV/(NRV)

6,332 6,017 315

Financial Charges (911) (879) (32)

FX G/(L) & CCS (870) 519 (1,389)

(Tax Expense)/reversal of income tax (794) (451) (343)

Net Profit / (Loss) 5,802 2,941 2,861

EPS (THB/Share) 2.84 1.44 1.40

35.99 (0.42)

36.25 (0.25)

13% (1%)

(4,166) 7,918

7,915 (5,865)

Financial

68,446 8,658

1,053 (1,383)

6,348 3,737

10,514 (4,182)

(659) (252)

318 (1,188)

(566) (228)

3,749 2,053

1.84 1.00

7,179 (5,608) 12,786

14,043 17,789 (3,746)

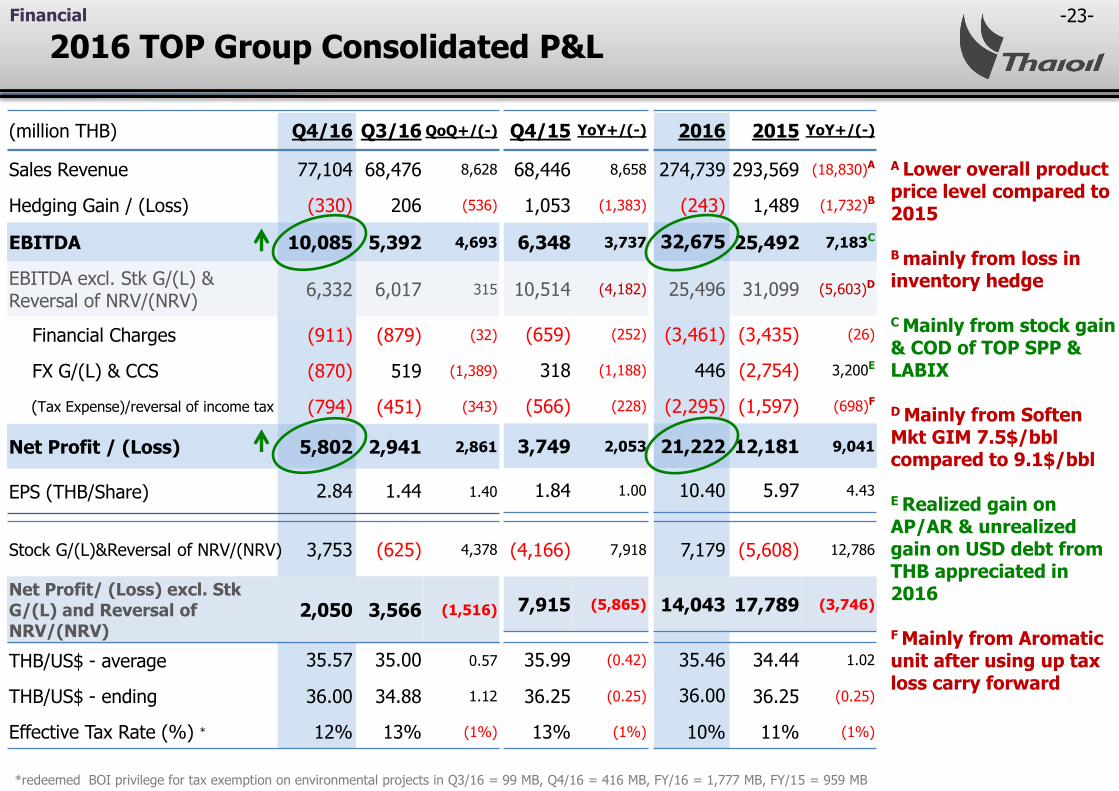

274,739 293,569 (18,830)A

(243) 1,489 (1,732)B

32,675 25,492 7,183C

25,496 31,099 (5,603)D

(3,461) (3,435) (26)

446 (2,754) 3,200E

(2,295) (1,597) (698)F

21,222 12,181 9,041

10.40 5.97 4.43

2016 TOP Group Consolidated P&L

*redeemed BOI privilege for tax exemption on environmental projects in Q3/16 = 99 MB, Q4/16 = 416 MB, FY/16 = 1,777 MB, FY/15 = 959 MB

(million THB) Q4/16 Q3/16 QoQ+/(-) Q4/15 YoY+/(-) 2016 2015 YoY+/(-)

A Lower overall product price level compared to 2015

B mainly from loss in inventory hedge

C Mainly from stock gain & COD of TOP SPP & LABIX

D Mainly from Soften Mkt GIM 7.5$/bbl compared to 9.1$/bbl

E Realized gain on AP/AR & unrealized gain on USD debt from THB appreciated in 2016

F Mainly from Aromatic unit after using up tax loss carry forward

-24--24-

Financing (9,397) (14,740)

Loans proceeding 4,0912 4,971

Loans repayment (3,051)3 (13,128)

Dividends paid (6,994) (3,194)

Interest (3,443) (3,389)

2016 2015

Operating Cash Flow 23,182 31,708

Net income & non-cash adj. 32,832 25,453

Change in working capital (9,650) 6,255

Free Cash Flow 4,830 34,238

2016 TOP Group Consolidated Cash Flow

Beginning

cash 35,764

S/T investment 17,365

53,129

+

+ =

+

2016 2015

Investments (18,352) 2,530

ST investments (12,057) 12,881

CAPEX (PP&E) & other (6,295)1 (10,351)

Ending

31,1214

29,654

60,775

Effect of FCD

(76)+Change

(4,567)

12,290*

Operating Cash Flow Investments

Financing

(Unit: Million THB) (Unit: Million THB)

Financial

1 Mainly from LABIX, TOPSPP and TOP

2 Mainly form LABIX3 Mainly form SAPTHIP, LABIX, SAKC & TM

4 Mainly form USD FCD

*non-cash transaction 233MB recorded as other payable-Proceed of purchase securities (Private fund)

-25-

Value (Million) Portion

US$ Bond & US$ Loan USD 1,191 57%

THB Bond THB 25,500 34%

THB Loan THB 7,050 9%

101,676 102,982 102,000

37,361 44,458 54,956

53,129 56,425 60,775

97,009

105,730 111,597

75,093 74,374 75,434

20,064 23,761

30,700

1.7

0.7 0.6

31-Dec-14 31-Dec-15 31-Dec-16

0.4 0.2 0.1

31-Dec-14 31-Dec-15 31-Dec-16

1) Including current portion of Long-Term Debt

Financial Ratios

Net Debt / adj. EBITDA** Net Debt / Equity

Statements of Financial Position

(Unit: million THB)

Trade Payable/ Others

LT Debt1)

Equities

CurrentAssets

Non-CurrentAssets

Cash & ST investment

217,731192,166

31 Dec 15 31 Dec 16

** Annualized EBITDA (excl stock gain/loss & Reversal of NRV/(NRV))

2016 TOP Group Strong Financial Position & Financial RatiosFinancial

ROE 13.2% 18.9% 20.3%

ROIC 12.6% 17.9% 18.8%

*

* Based on actual performance in the past 12 months

*

***Calculated by interest expense net off interest income as per FS as at 31 Dec 16

*

*

30 Sep 16

203,865

Cost of Debt

TOP Group (Net***) 3.63%

TOP Group (Gross) 4.75%

BBBStable Outlook

Baa1Stable Outlook

AA- (tha)Stable Outlook

Interest Rate Portion

Float 10%

Fixed 90%

TOP avg.debt life 10.9 Yrs

Consolidated Long-Term Debt as at 31 Dec 16 1)

75,434 million THB

(US$ 2,095 million

equivalence)

Total Long-Term Debt Net Debt

As at 31 Dec 16 (36.00 THB/US$)

15,526 million THB

(US$ 431 million equivalence)

-26-

1H-17 & 2017 MARKET OUTLOOK

• Crude Oil

• Petroleum Products

• Aromatics

• Base Oil & Bitumen

• Linear Alkyl Benzene (LAB)

-27-

CRUDE OIL

-28-

0

20

40

60

80

Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17

$/BBL

Dubai Price Movement

•Expectation of High Compliance For Output Cut Deal

• Oil Market to Rebalance, Driven By Output Cut Deal and Growing Oil Demand

• Risks Over Rising Crude Oil Supply

China’s stock market crash

Crude Oil

Crude Oil Market: Oil Market to Rebalance in 2017

Key Highlights in 1H-17 *Q1TD’17 (as of 10 Feb): $ 53.8/BBL

OPEC failed to agree on an

output ceiling

No consensus on output freeze

1

2

BREXIT

Iran’s nuclear deal done

Canada wildfire & Nigerian outages

Iran’s nuclear sanction lifted

OPEC targeted 32.5-33.0 MBD output

OPEC agreed to cut output to 32.5 MBD

3

Non-OPEC agreed to cut output by 0.558 MBD

-29-

10.6

10.8

11.0

11.2

11.4

11.6

11.8

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17

Russia’s Crude Oil Production

1 Expectation of High Compliance For Output Cut Deal

Russia to Gradually Reduce Its Output

High Compliance From OPEC and Non-OPEC Bigger Cut Than Agreed Level From Saudi

MBD

A

C

B

1.164 1.078

0.558

0.403

0.0

0.5

1.0

1.5

2.0

Target cut Expected cut

OPEC & Non-OPEC Supply Cut

OPEC Non-OPEC

► Around 86% compliance from OPEC

and Non-OPEC members

► 93% compliance from OPEC, more

than the initial 60% compliance during

the previous cuts in 2009

0.0

0.2

0.4

0.6

0.8

Saudi Arabia Iraq UAE Kuwait

Major OPEC Production Cut

Target cut Expected cut

MBD

123%

40%59% 92%

MBD

Sources: IEA (Jan’17) and PIRA (Jan’17)

Target Cut :0.3 MBD

Jan’s Cut :0.1 MBD (33%)

Crude Oil

Sources: OPEC (Jan’17), and Reuters (Jan’17)

1.722

1.481

Sources: OPEC (Jan’17), and Reuters (Jan’17)

-30-

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

90

92

94

96

98

100

1Q-14 3Q-14 1Q-15 3Q-15 1Q-16 3Q-16 1Q-17 3Q-17

MBDMBD

Surplus (RHS) Demand (LHS) Supply (LHS)

Global Demand/Supply Balance

2017Demand: + 1.3 MBD YoYSupply: + 0.1 MBD YoY

Lower Oil Supply from Output Cut Deal

Rebalancing Oil Market, Driven By Output Cut Deal and Growing Oil Demand

Crude Oil

2

Market to Rebalance in 2017 Growing Oil Demand on Improving Economy

MBD

A

C

-2.0

-1.0

0.0

1.0

2.0

Q4-14 Q2-15 Q4-15 Q2-16 Q4-16 Q2-17 Q4-17

Oil Supply Growth (QoQ)

OPEC growth Non-OPEC growth

B

► Sharp declines in OPEC and non-OPEC

production in Q1-17

► OPEC output to gradually rise in Q3-17

to meet higher seasonal demand

Sources: IEA (Jan’17), PIRA (Jan’17), TOP’s Estimate

1.01.2

2.0

1.51.3

2013 2014 2015 2016 2017*

Global Oil Demand Growth (MBD)

Sources: IEA (Jan’17)* Forecasted global oil demand by IEA

Sources: IEA (Jan’17) and TOP’s Estimate

-31-Crude Oil

3 Risks Over Rising Crude Oil Supply

Rising Libyan Output After Being Disrupted Concerns Over Resuming Nigeria’s Oil SupplyA B

Recovering US Shale Oil on More Drilling ActivitiesC

Total U.S. Oil Production YoYMBD

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015 2016 2017

Libya’s Oil Production

Capacity : 1.6 MBD

MBD

Gov’t Target :1.25 MBD

Market view :1.00 MBD

Sources: IEA (Jan’17), Reuters, TOP’s Estimates

Sources: EIA (Jan’17) and IEA (Jan’17)

Sources: IEA (Jan’17) and PIRA (Jan’17)

Dakota Pipeline to Be Completed in Q2-17D

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jan'15 Jul'15 Jan'16 Jul'16 Jan'17 Jul'17

Alaska Gulf of Mexico Lower 48 states

US production to rise

by 0.1 MBD in 2017

Dakota Access Pipeline Map

Freight saving(over railways)

= “$5-10/BBL”

1 Railways 2

Capacity : 470 KBD

Location :Bakken – Illinois

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015 2016 2017

Nigeria’s Oil ProductionMBD

Capacity : 2.2 MBD

Gov’t Target :2.20 MBD

Market view :1.55 MBD

North Dakota (Bakken)

-32-

PETROLEUM PRODUCTS

-32-

-33-

5.8

8.57.9

6.1

8.0 7.6 7.7

5.0 5.2

6.76.2

6.9

Y2014 Q1-15 Q2-15 Q3-15 Q4-15 Y2015 Q1-16 Q2-16 Q3-16 Q4-16 Y2016 Q1TD-17*

Key Highlights in 1H-17

Singapore Cracking GRM ($/BBL)

Better Gasoline Margins on Solid Demand Growth and Low ME Supply

1

Steady Middle Distillate Cracks from Recovered Demand on Improved Economy and Cold Weather

Still-High Margins from Demand Outpacing Refinery Addition

($/BBL) Q1-16 Q2-16 Q3-16 Q4-16 2016 Q1TD-17*

ULG95-DB 18.8 14.4 11.6 14.6 14.9 16.1

JET-DB 11.7 11.1 11.1 12.3 11.6 11.6

GO-DB 9.6 10.5 11.0 12.0 10.8 11.7

HSFO-DB (5.2) (8.7) (4.3) (1.7) (5.0) (2.5)

2

Remarks: *Q1TD-17 as of 17 Feb 17

Refinery

-34-

Deficit in Q2/17 on High DemandB

Demand Continues to Outstrip Supply in 2017D

Better Gasoline Margins on Solid Demand Growth and Low ME Supply1

Refinery

Tighter Product Supplied in ME after Ruwais S/DC

Still-high Gasoline Demand from Low Oil PricesA

MBD

0.0

0.2

0.4

0.6

0.8

1.0

2015 2016 2017(1H-17)

LPG

Naphtha

Gasoline

Jet Fuel

Diesel

Fuel Oil

Ruwais’s Refinery ProductionRuwais 2 (417 KBD)

Startup in Jan’16RFCC (125 KBD) S/D after fire broke out in Jan’17

Asia Pacific Gasoline Demand

6.0

6.5

7.0

7.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

MBD

573 546532444

0

300

600

900

1200

2014 2015 2016 2017

Demand Supply

World Gasoline Demand & Supply Growth YoY

KBD

41102

Asia Pacific Gasoline Balance

-200

0

200

400

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

MBD

1H-17 : 7.0 MBD (+4% YoY)

Source : FACTs (Jan’17) Source : FACTs (Jan’17)

Source : FACTs (Oct’16) , JBC (Nov’16) and TOP’s estimateSource : Reuters (Jan’17) and FGE (Feb’17)

-35-

Steady Exports from Stricter Regulations on TeapotC Better Market in 2017 from Recovered Demand D

Steady Middle Distillate Cracks from Recovered Demand on Improved Economy and Cold Weather2

Refinery

Greater Demand due to Cold WeatherBBetter Demand from Recovered Global Economy A

10.0

11.0

12.0

13.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

MBDAsia Pacific Middle Distillate Demand U.S. Middle Distillate Demand

5.0

5.2

5.4

5.6

5.8

6.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

MBD

126

716

36

417

0

300

600

900

1200

2014 2015 2016 2017

Demand Supply

World Middle Distillate Demand & Supply Growth YoYKBD

KBD Chinese Gasoil Export

0

100

200

300

400

500

600

Jan-16 Jul-16 Jan-17

1H-17 : 11.7 MBD (+2.4% YoY) 1H-17 : 5.5 MBD (+1.9% YoY)

AVG 2016 : 318 KBD AVG 1H-17 : 317 KBD

Source : FACTs (Jan’17)

Source : FACTs (Jan’17) Source : FACTs (Oct’16) , JBC (Nov’16) and TOP’s estimate

Source : EIA (Jan’17)

90

299

-36-

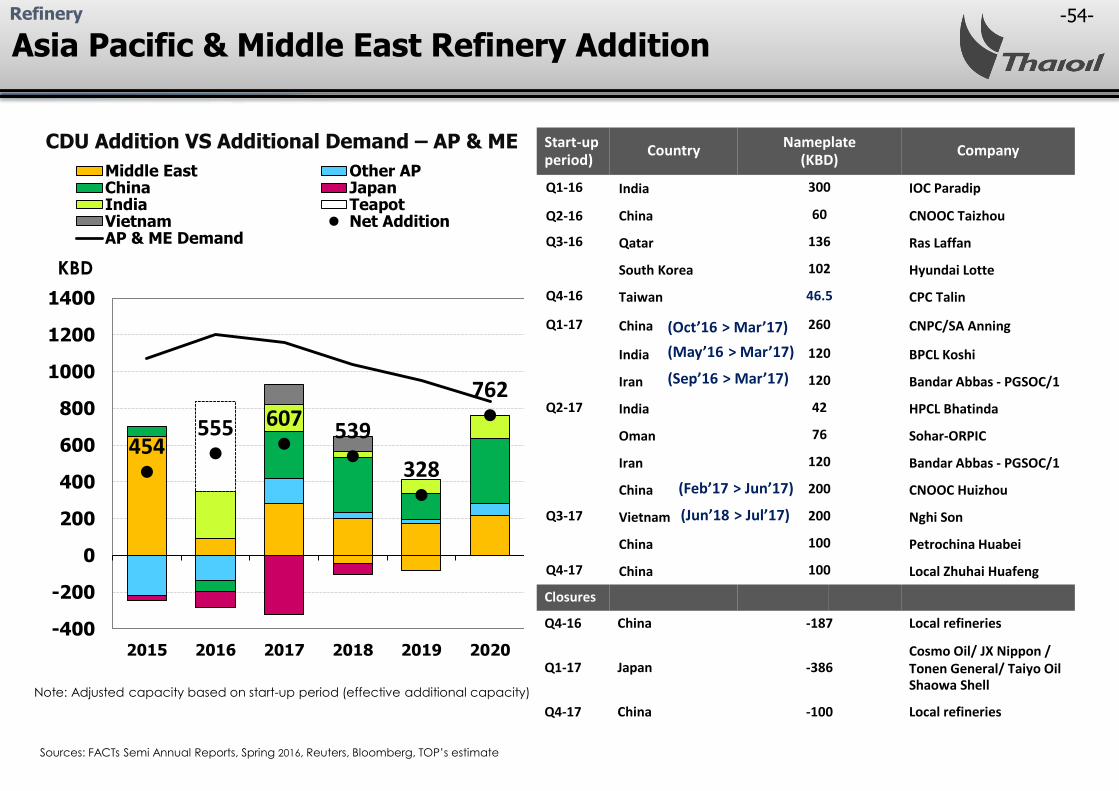

Firm Refinery Margins in 2017 as Demand Outpaces Refinery Addition

Refinery

Note: Adjusted capacity based on start-up period (effective additional capacity)

454555 607 539

328

762

-400

-200

0

200

400

600

800

1000

1200

1400

2015 2016 2017 2018 2019 2020

KBD

Middle East China Other AP

Japan India Vietnam

Teapot Net Addition AP & ME Demand

CDU Addition VS Additional Demand – AP & ME

Sources: FACTs Semi Annual Reports, Fall 2016, Reuters (Jan’17) , TOP’s estimate

Lower refinery addition in 2017 due to regulatory restrictions in Japan and delayed startup of two Chinese mega refineries

-37-

Year on YearAverage

2011-2015(B) Y 2015(B) Y 2016(B) Y 2017(C)

Mogas (A) +7.1% +13.3% +9.8% +1.3%

Jet/Kero +4.4% +9.7% +6.8% +3.7%

Diesel (A) +3.4% +4.0% +3.1% +2.4%

Total +4.4% +7.1% +5.4% +2.3%

GDP +3.4% +2.8% N/A +3.2%(D)

Domestic

Remarks: (A) Mogas and Diesel includes Ethanol and Biodiesel, respectively

(B) DOEB Statistics (Feb-17)

(C) PTT’s Estimation (Jul-16)

(D) BOT’s Estimate (BOT Monetary Report as of Dec-16)

Thailand Oil Demand Growth

Thailand Oil Demand Growth

Thailand oil demand growth at 2.3% YoY in 2017

-38-

AROMATICS

-39-

($/TON) Q1-16 Q2-16 Q3-16 Q4-16 2016 Q1TD-17*

PX-ULG95 332 315 341 280 317 302

BZ-ULG95 156 138 174 185 163 380

Key Highlights in 1H-17

Aromatics Market

Positive PX Outlook due to Strong Chinese Polyester Demand

Firm Chinese SM Demand Drives BZ Market

1

2

255 246 233

288256

332 315341

280317 302

Q1

-15

Q2

-15

Q3

-15

Q4

-15

Y2

01

5

Q1

-16

Q2

-16

Q3

-16

Q4

-16

Y2

01

6

Q1

TD

-17

*

PX CFR Taiwan-ULG95 ($/TON)

98 11574

101 97

156 138174 185

163

380

Q1

-15

Q2

-15

Q3

-15

Q4

-15

Y2

01

5

Q1

-16

Q2

-16

Q3

-16

Q4

-16

Y2

01

6

Q1

TD

-17

*

BZ FOB Korea-ULG95 ($/TON)

Firm Aromatics Market due to Strong Downstream Demand

Remarks: *Q1TD-17 as of 17 Feb 17

Aromatics

-40-

Growing Chinese PX Import Lifts MarketPolyester Demand Growth Boosts PX Market

Heavy Maintenance in Q2-17 Supports MarketNew PTA Capacity Addition Supports Market

Sources: PCI WoodMackenzie (Dec’16), IHS (Jan’17)

Positive PX Outlook due to Strong Chinese Polyester Demand

1

C

A

D

B

Aromatics

0.660.47

0.26

0.69

0.97

0.660.79

0.30

0.0

0.5

1.0

1.5

Q3-16 Q4-16 Q1-17 Q2-17

Mil TON

Asian PX and PTA Plant Maintenance

PX PTA (PX Equivalent)

0.23 0.07 0.20

0.56

0.06 -0.01

0.390.48

-0.5

0.0

0.5

1.0

Q3-16 Q4-16 Q1-17 Q2-17

Mil TON

AP & ME PX and PTA Capacity Addition

PX Effective Capacity Addition

PTA Effective Capacity Addition (PX Equivalent)

Two fires at NE Asia refineries in end-Jan boosted PX spot price

20.01

21.25

22.46

23.31

18

19

20

21

22

23

24

2014 2015 2016 2017

Mil TON

Chinese Polyester Production(PX Equivalent)

9.87

11.6912.29

13.18

0

2

4

6

8

10

12

14

2014 2015 2016 2017

Mil TON

Chinese PX Net Trade

-41-

Firm Chinese Import Helps Boost BZ MarketRising SM Demand in China Pushes BZ Market

Heavy Maintenance in Q2-17 Supports MarketBalanced Market due to New Downstream Plant

Source: IHS (Jan’17)

Aromatics

2 Firm Chinese SM Demand Drives BZ Market

C D

BA

0.120.18

0.32

0.48

0.240.20

0.36 0.37

0.0

0.1

0.2

0.3

0.4

0.5

Q3-16 Q4-16 Q1-17 Q2-17

Mil TON

AP & ME BZ and Downstream Capacity Addition

BZ Effective Capacity Addition

Downstream Effective Capacity Addition (BZ Equivalent)

0.63

0.43

0.18

0.480.46

0.20 0.18 0.22

0.0

0.2

0.4

0.6

0.8

1.0

Q3-16 Q4-16 Q1-17 Q2-17

Mil TON

AP BZ, SM and Phenol Plant Maintenance

BZ SM and Phenol (BZ Equivalent)

Two fires at NE Asia refineries in end-Jan boosted BZ spot price

3.89 4.084.46

4.90

0

1

2

3

4

5

6

2014 2015 2016 2017

Mil TON

Chinese SM Production(BZ Equivalent)

0.60

1.09

1.55

1.87

0.0

0.5

1.0

1.5

2.0

2014 2015 2016 2017

Mil TONChinese BZ Net Trade

-42-

BASE OIL & BITUMEN

-43-

($/TON) Q1-16 Q2-16 Q3-16 Q4-16 2016 Q1TD-17*

500SN

-HSFO427 409 443 367 412 396

Lower Global Base Oil Capacity Addition

Lower Asia Pacific Plant Maintenance

Peak Seasonal Demand in Q2’17 to Support the Market

Base Oil & Bitumen

Key Highlights in 1H-17

Global Additional Nameplate Capacity

AP Plant Maintenance (Effective Capacity)

Mil TON

Sources: Argus Jan’17 and TOP’s Estimate

Mil TON

495

369 399506

450 431 427 409 443367

412 396

Y2

01

4

Q1

-15

Q2

-15

Q3

-15

Q4

-15

Y2

01

5

Q1

-16

Q2

-16

Q3

-16

Q4

-16

Y2

01

6

Q1

TD

-17

*

Firm Base Oil Market in H1 on Lower Global Base Oil Capacity Addition amid Seasonal Demand

0.3

0.7

0.3

0.0

0.5

1.0

H1-16 H2-16 H1-17

Group 1 Group 2 Group 3 Net Capacity

0.10.6

0.3

-2.0

0.0

2.0

H1-16 H2-16 H1-17

Group 1 Group 2 Group 3 Net Capacity

2

1500SN – HSFO ($/TON)

Remarks: *Q1TD-17 as of 17 Feb 17

0.8 0.60.0

-2.0

0.0

2.0

H1-16 H2-16 H1-17

Group 1 Group 2 Group 3 Net Capacity

AP Additional Nameplate Capacity

Mil TON

2

1

3

Sources: Argus (Jan’16-Jan’17) and TOP’s Estimate

-44-Base Oil & Bitumen

($/TON) Q1-16 Q2-16 Q3-16 Q4-16 2016 Q1TD-17*

Bitumen

-HSFO(7) (48) (61) (80) (49) (23)

Firm Bitumen Market on Seasonal Demand in the Region

-32

23 20

82 98 56

-7 -48 -61 -80

-49-23

Y2

01

4

Q1

-15

Q2

-15

Q3

-15

Q4

-15

Y2

01

5

Q1

-16

Q2

-16

Q3

-16

Q4

-16

Y2

01

6

Q1

TD

-17

*

Import Volume of Major Asian Players in 2016

Expected Firm Thai Demand in 2017

Bitumen-HSFO ($/TON)

‘000 Km.

Expect Higher Import Interest during Peak Paving Season

Improved Thai Demand on Higher Infrastructure Budget and Road Maintenance Plan

Key Highlights in 1H-17

Source: Department of Highways and Maintenance Bureau (2014-Sep’16)

KTON/MONTH China

VietnamKTON/MONTH

IndiaKTON/MONTH

IndonesiaKTON/MONTH

1

2

Source: Bitumart (Oct’16)

40

41

42

43

44

45

2015 2016 2017

2.9%YoY Growth1

2

Billion Baht

0

50

100

150

200

2015 2016 2017

RuralRoadsdept.

Highwaysdept.

12%YoY Growth

0

300

600

Jan-16 May-16 Sep-16

0

100

200

Jan-16 May-16 Sep-16

0

100

200

Jan-16 May-16 Sep-16

0

100

200

Jan-16 May-16 Sep-16

Infrastructure Budget Asphalt Road Distance

Remarks: *Q1TD-17 as of 17 Feb 17

-45-

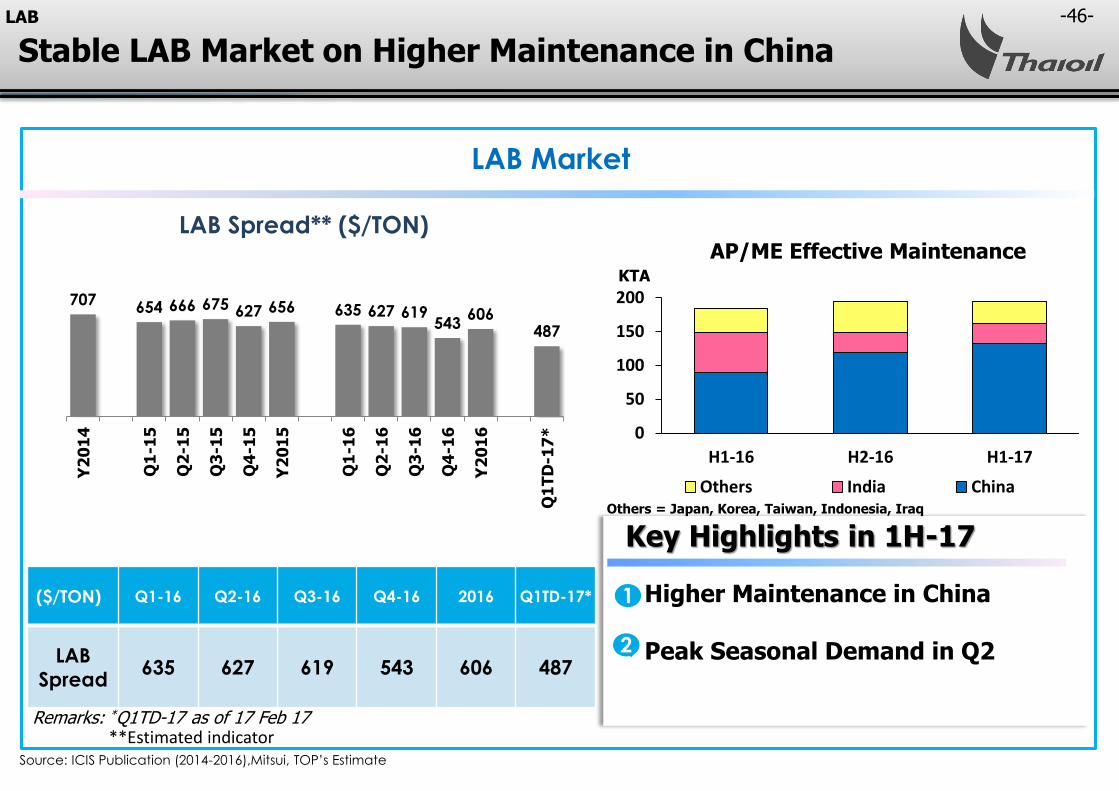

Linear Alkyl Benzene (LAB)

-46-

Key Highlights in 1H-17

Higher Maintenance in China

Peak Seasonal Demand in Q2

LAB Market

Source: ICIS Publication (2014-2016),Mitsui, TOP’s Estimate

LAB Spread** ($/TON)

1

2

($/TON) Q1-16 Q2-16 Q3-16 Q4-16 2016 Q1TD-17*

LAB

Spread635 627 619 543 606 487

707 654 666 675 627 656 635 627 619543

606487

Y2

01

4

Q1

-15

Q2

-15

Q3

-15

Q4

-15

Y2

01

5

Q1

-16

Q2

-16

Q3

-16

Q4

-16

Y2

01

6

Q1

TD

-17

*

KTA

Remarks: *Q1TD-17 as of 17 Feb 17

AP/ME Effective Maintenance

0

50

100

150

200

H1-16 H2-16 H1-17

Others* India ChinaOthers = Japan, Korea, Taiwan, Indonesia, Iraq

**Estimated indicator

LAB

Stable LAB Market on Higher Maintenance in China

-47-

CONCLUSION

-48-Conclusion

2017 Market Outlook Conclusion

Stable LAB Market on Higher Plant Maintenance in China

(vs. 2016)

Crude Oil

Refinery

Lube Base

LAB

Aromatics Firm Aromatics Market from Stronger Demand Despite Increasing New Capacity Addition

Firm Base Oil Market due to No Additional Capacity in Asia Despite Lower Regional Plant Maintenance

Firm Bitumen Market on Expectation of Improved Regional Demand

Still-High Margins from Demand Outpacing Refinery Addition

Oil Market to Rebalance in 2017, Driven by Output Cut Deal and Growing Oil Demand

-49-

Thank You

Any queries, please contact:

at email: [email protected]

Tel: 662-797-2999 / 662-797-2961

Fax: 662-797-2976

-50-

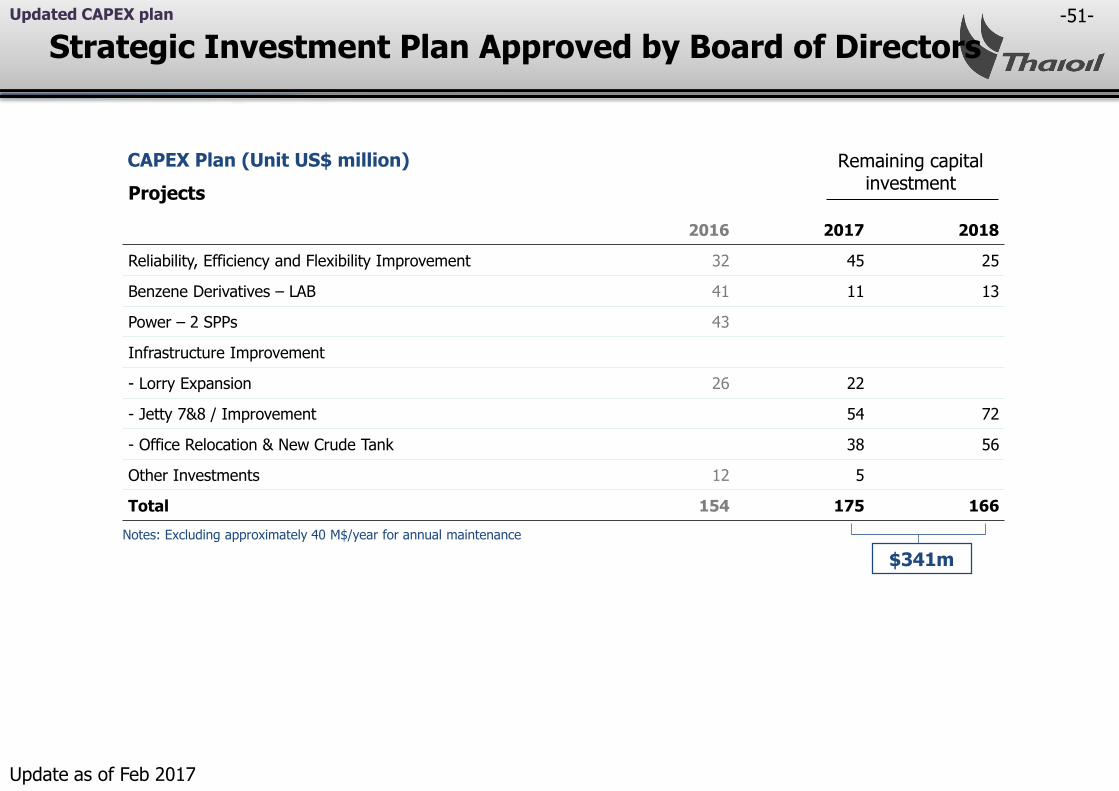

APPENDIX

• Strategic Investment Plan

• Optimized & Flexible Operations…Superior Performance

• CDU Addition VS Additional Demand – AP & ME

• World GRM / Inventories

• Thailand petroleum demand by products

-51-

Remaining capital investment

Strategic Investment Plan Approved by Board of Directors

Projects

2016 2017 2018

Reliability, Efficiency and Flexibility Improvement 32 45 25

Benzene Derivatives – LAB 41 11 13

Power – 2 SPPs 43

Infrastructure Improvement

- Lorry Expansion 26 22

- Jetty 7&8 / Improvement 54 72

- Office Relocation & New Crude Tank 38 56

Other Investments 12 5

Total 154 175 166

CAPEX Plan (Unit US$ million)

Notes: Excluding approximately 40 M$/year for annual maintenance

$341m

Updated CAPEX plan

Update as of Feb 2017

-52-

Optimized & Flexible Operations…Superior Performance

27%17%

7%17%

28%29%

28%28%

45% 54%65%

55%

Oman Dubai Murban ArabLight

Short Residue Waxy Gas/Distillates

Sources of Crude

• Flexibility in crude intake allows diversification of crude types to source cheaper crude

• Flexibility in product outputs by maximizing middle distillates (jet and diesel) by adjusting production mode to capture domestic demand and price premium

• Maximize Platformate production to capture higher margin on aromatics

• Minimize fuel oil output to avoid lower margin products

Product output

Domestic demand for

petroleum products**

**Source: Energy Policy and Planning Office, Ministry of Energy Thailand

% S = 0.78API = 39.4

% S = 1.43API = 32.0

% S = 2.52API = 31.2

Crude Assays based onTOP configuration*

Thai Oil is able to diversify its type of crude intake and product outputs to maximize demand and margin

*** Including Nigeria, Russia and others

% S = 1.97API = 32.8

*Crude yield as per assay in Spiral as of Feb 2016

79%

7%

12%

2%

5%

7%

32%

23%

16%

12%

4%

4%

42%

12%

20%

21%Far East

Local

Middle East

Q4/16

1SAUDI ARAMCO

MOPS Jet Kerosene FOB

SG

MOPS Gasoil 0.05% Sulfur

FOB SG

MOPS ULG 95 FOB SG

Others

1.LPG price = LPG CP - 20$/ton)since 2 Feb 15onwards.

LPG

PLATFORMATE

GASOLINE

JET

DIESEL

FUEL OIL

Q4/16

***

LONG RESIDUE

MOPS Fuel Oil 180 CST 3.5% Sulfur FOB SG

Reference Price

Crude

-53--53-

Optimized & Flexible Operations…Superior Performance

27%17%

7%17%

28%29%

28%28%

45% 54%65%

55%

Oman Dubai Murban ArabLight

Short Residue Waxy Gas/Distillates

Sources of Crude

• Flexibility in crude intake allows diversification of crude types to source cheaper crude

• Flexibility in product outputs by maximizing middle distillates (jet and diesel) by adjusting production mode to capture domestic demand and price premium

• Maximize Platformate production to capture higher margin on aromatics

• Minimize fuel oil output to avoid lower margin products

Product output

Domestic demand for

petroleum products**

**Source: Energy Policy and Planning Office, Ministry of Energy Thailand

% S = 0.78API = 39.4

% S = 1.43API = 32.0

% S = 2.52API = 31.2

Crude Assays based onTOP configuration*

Thai Oil is able to diversify its type of crude intake and product outputs to maximize demand and margin

*** Including Nigeria, Russia and others

% S = 1.97API = 32.8

*Crude yield as per assay in Spiral as of Feb 2016

79%

8%

10%

3%

4%7%

34%

22%

16%

12%

4%

6%

57%

16%

27%

28%Far East

Local

Middle East

FY/16

1SAUDI ARAMCO

MOPS Jet Kerosene FOB

SG

MOPS Gasoil 0.05% Sulfur

FOB SG

MOPS ULG 95 FOB SG

Others

1.LPG price = LPG CP - 20$/ton)since 2 Feb 15onwards.

LPG

PLATFORMATE

GASOLINE

JET

DIESEL

FUEL OIL

FY/16

***

LONG RESIDUE

MOPS Fuel Oil 180 CST 3.5% Sulfur FOB SG

Reference Price

-54-

Sources: FACTs Semi Annual Reports, Spring 2016, Reuters, Bloomberg, TOP’s estimate

CDU Addition VS Additional Demand – AP & ME Start-up period)

CountryNameplate

(KBD)Company

Q1-16 India 300 IOC Paradip

Q2-16 China 60 CNOOC Taizhou

Q3-16 Qatar 136 Ras Laffan

South Korea 102 Hyundai Lotte

Q4-16 Taiwan 46.5 CPC Talin

Q1-17 China 260 CNPC/SA Anning

India 120 BPCL Koshi

Iran 120 Bandar Abbas - PGSOC/1

Q2-17 India 42 HPCL Bhatinda

Oman 76 Sohar-ORPIC

Iran 120 Bandar Abbas - PGSOC/1

China 200 CNOOC Huizhou

Q3-17 Vietnam 200 Nghi Son

China 100 Petrochina Huabei

Q4-17 China 100 Local Zhuhai Huafeng

Closures

Q4-16 China -187 Local refineries

Q1-17 Japan -386Cosmo Oil/ JX Nippon /Tonen General/ Taiyo OilShaowa Shell

Q4-17 China -100 Local refineries

Note: Adjusted capacity based on start-up period (effective additional capacity)

(Sep’16 > Mar’17)

(May’16 > Mar’17)

(Jun’18 > Jul’17)

454555 607

539

328

762

-400

-200

0

200

400

600

800

1000

1200

1400

2015 2016 2017 2018 2019 2020

KBD

Middle East Other APChina JapanIndia TeapotVietnam Net AdditionAP & ME Demand

(Oct’16 > Mar’17)

(Feb’17 > Jun’17)

Asia Pacific & Middle East Refinery AdditionRefinery

-55-

Asian Margin Vs. US-EU margin

World GRM

12

13

14

15

16

17

18

1 5 9 13 17 21 25 29 33 37 41 45 49

U.S. Crude Refinery Input

5yr-range 20162017 avg 12-16

MBDSource : EIA

8

9

10

11

12

1 2 3 4 5 6 7 8 9 10 11 12

EU 16 Crude Refinery Input

5yr-range 20162017 avg 12-16

MBDSource : Euroil

2.5

3.0

3.5

4.0

4.5

1 5 9 13 17 21 25 29 33 37 41 45 49

Japan Crude Refinery Input

5yr-range 20162017 avg 12-16

MBDSource : METI

-10

0

10

20

30

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

$/BBL

BRENT CRACK BRENT HYDRO WTI CRACK

US and EU GRM

-8

-4

0

4

8

12

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

$/BBL

SING CRACK SING HYDRO

Singapore GRM

Total Capacity: 3.8 MBD 87.57% 67.15% 93.68%Total Capacity: 18.1 MBD Total Capacity: 15.8 MBD

-56-

250

300

350

400

450

500

550

600

1 5 9 13 17 21 25 29 33 37 41 45 49

U.S. Crude Stocks (excl. SPR)

5yr-range 2016 2017 avg 12-16

MBBLSource : EIA

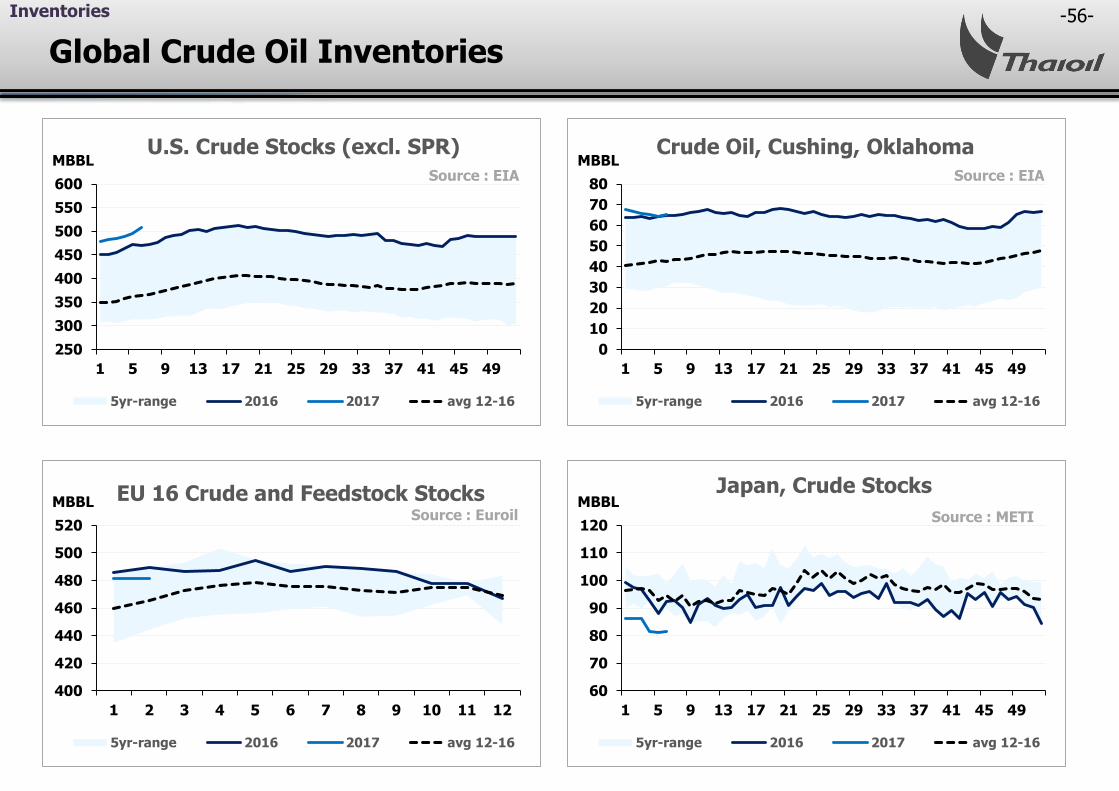

Global Crude Oil Inventories

Inventories

0

10

20

30

40

50

60

70

80

1 5 9 13 17 21 25 29 33 37 41 45 49

Crude Oil, Cushing, Oklahoma

5yr-range 2016 2017 avg 12-16

MBBLSource : EIA

60

70

80

90

100

110

120

1 5 9 13 17 21 25 29 33 37 41 45 49

Japan, Crude Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : METI

400

420

440

460

480

500

520

1 2 3 4 5 6 7 8 9 10 11 12

EU 16 Crude and Feedstock Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : Euroil

-57-

180

200

220

240

260

280

1 5 9 13 17 21 25 29 33 37 41 45 49

U.S. Gasoline Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : EIA

Global Gasoline Inventories

Inventories

0

5

10

15

20

1 5 9 13 17 21 25 29 33 37 41 45 49

Japan, Gasoline Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : METI

80

100

120

140

1 2 3 4 5 6 7 8 9 10 11 12

EU 16 Gasoline Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : Euroil

0

10

20

1 5 9 13 17 21 25 29 33 37 41 45 49

Singapore Gasoline Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : IE Singapore

-58-

80

100

120

140

160

180

1 5 9 13 17 21 25 29 33 37 41 45 49

U.S. Diesel Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : EIA

Global Middle Distillate Inventories

Inventories

30

40

50

60

70

1 5 9 13 17 21 25 29 33 37 41 45 49

Japan, Middle Distillate Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : METI

300

350

400

450

500

1 2 3 4 5 6 7 8 9 10 11 12

EU 16 Diesel Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : Euroil

0

10

20

1 5 9 13 17 21 25 29 33 37 41 45 49

Singapore Middle Distillate Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : IE Singapore

-59-

20

30

40

50

1 5 9 13 17 21 25 29 33 37 41 45 49

U.S. Residual Fuel Oil Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : EIA

Global Fuel Oil Inventories

Inventories

0

5

10

15

20

1 5 9 13 17 21 25 29 33 37 41 45 49

Japan, Residual Fuel Oil Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : METI

60

70

80

90

100

1 2 3 4 5 6 7 8 9 10 11 12

EU 16 Residual Fuel Oil Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : Euroil

0

10

20

30

40

1 5 9 13 17 21 25 29 33 37 41 45 49

Singapore Residual Fuel Oil Stocks

5yr-range 2016 2017 avg 12-16

MBBLSource : IE Singapore

-60-

China’s Refined Product Exports

China Export

0

50

100

150

200

250

300

350

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

China’s Gasoline Exports

2015 2016

KBDSource : China Custom

0

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

China’s Gasoil Exports

2015 2016

KBDSource : China Custom

0

100

200

300

400

500

600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

China’s Jet/Kero Exports

2015 2016

KBDSource : China Custom

0

50

100

150

200

250

300

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

China’s Fuel Oil Exports

2015 2016

KBDSource : China Custom

-61-

Domestic LPG Demand

LPG Demand by Sector

LPG Demand Highlight

• In 2016, LPG demand fell significantly by 8.6%YoY on account of lower usages in all sectors. Most of the decline came from petrochemical sector which its feedstock switching from LPG to Naphtha leading to drop in this sector. Furthermore, LPG demand in automobile fell harshly by 15.5%YoY, as a result of fuel switching from LPG to Mogas due to lower price of Mogas.

Outlook for 2017

• LPG demand is expected to dropped by 1.5% YoYpressured by the expectation of more fuel switching from LPG to Mogas, due to low oil price.

• Moreover, the demand from household sector is also expected to decrease from changing of customers’ behavior.

• However, the slowdown of LPG demand was expected to be limited by higher usage in industry sector as a result of persistent low level of LPG price.

Thailand LPG Demand

Remark : LPG demand includes Petrochemical and own used consumption

Source: EPPO, DOEB (As of February 2017)

Thailand petroleum demand by products

-62--62-

Domestic Gasoline/Gasohol Demand

Gasoline/Gasohol Demand by Grade

GASOLINE/Gasohol Demand Highlight

• In 2016, Mogas demand jumped sharply by 9.8%YoY to an average 28.99 ML/day. This was mainly due to lower retail prices and higher number of passenger cars since the end of the last year, as a result of avoiding new tax implementation. In fact, the gasohol portion increase significantly to 95.4% of total mogasdemand as a result of lower proportion of ULG95 from 5.2% to 4.6%, according to more attractive price gap of ULG95 and GSH E10.

• The level of domestic ethanol demand, in 2016, rose significantly by 9.5%YoY from 3.57 mml/day to 3.91 mml/day following the rising of Mogasdemand. Additionally, this was also because of higher demand in GSH-91, GSH-95, E20, and E85 which increased by 1.6%YoY, 20.5%YoY, 15.7%YoY, and 1.9%YoY, respectively, backed by increasing in the number of new E20 vehicle, E20 gas station, and wider GSH95-E20 price gap.

Outlook for 2017

• Mogas consumption is predicted to grow by 1.3% YoY supported by expectation of growing of new passengers cars from return of private consumption. However, the demand is limited by high growth level in 2016 and higher oil price.

Thailand Gasoline/Gasohol Demand

Source: DOEB (As of February 2017)

Thailand petroleum demand by products

-63--63-

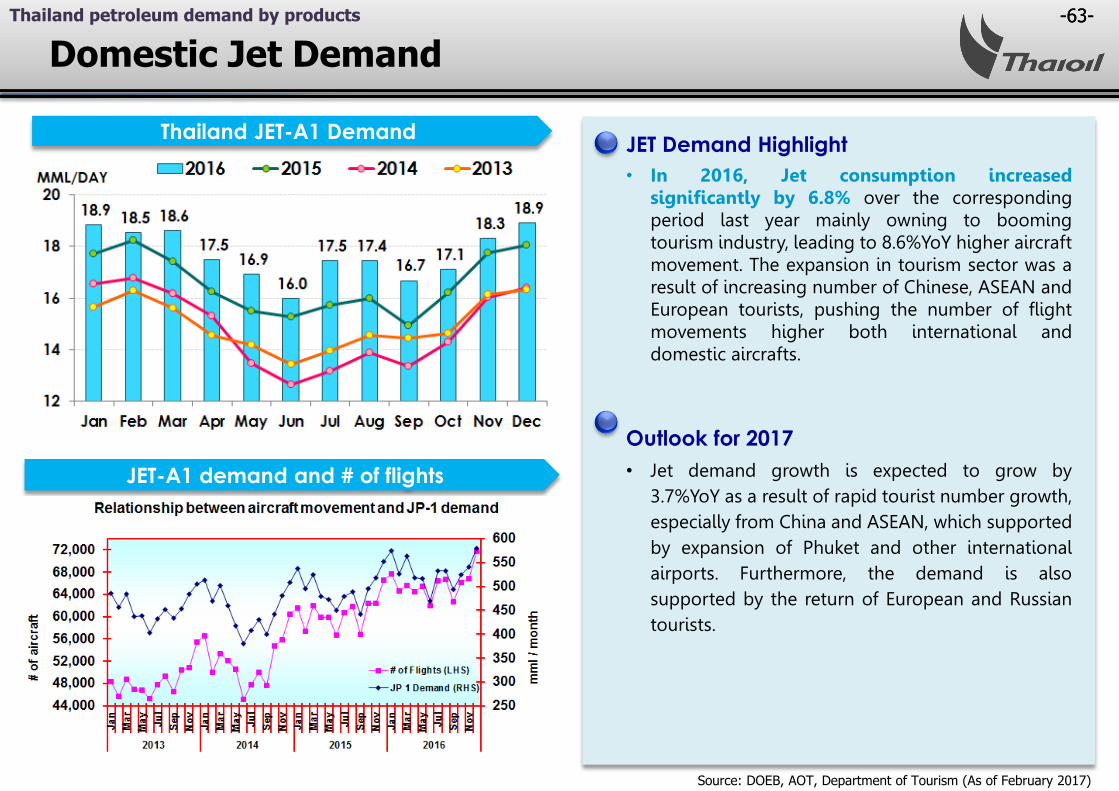

Domestic Jet Demand

JET-A1 demand and # of flights

JET Demand Highlight

• In 2016, Jet consumption increased significantly by 6.8% over the corresponding period last year mainly owning to booming tourism industry, leading to 8.6%YoY higher aircraft movement. The expansion in tourism sector was a result of increasing number of Chinese, ASEAN and European tourists, pushing the number of flight movements higher both international and domestic aircrafts.

Outlook for 2017

• Jet demand growth is expected to grow by 3.7%YoY as a result of rapid tourist number growth, especially from China and ASEAN, which supported by expansion of Phuket and other international airports. Furthermore, the demand is also supported by the return of European and Russian tourists.

Thailand JET-A1 Demand

Source: DOEB, AOT, Department of Tourism (As of February 2017)

Thailand petroleum demand by products

-64--64-

Domestic Gasoil and NGV Demand

NGV Demand

Diesel Demand Highlight

• In 2016, Diesel demand rose gradually by 3.1% YoY as relatively low retail prices boosted the consumption amidst higher number of accumulated commercial vehicles. Nevertheless, demand growth was curbed by lower level of export activity, as a result of slowdown of global economy.

Outlook for 2017

• Diesel demand in 2017 is expected to expand by 1.8% YoY supported by Thailand economic improvement.

NGV Demand Highlight

• In 2016, NGV demand declined significantly by 9.1%YoY. This was mainly because of higher NGV retail price, which had increased to hit the record high at 13.5 baht/kg in Q1/16, and lower oil prices which reduced the fuel switching from old cars.

Thailand Gasoil Demand

Source: DOEB (As of February 2017)

Thailand petroleum demand by products

-65--65-

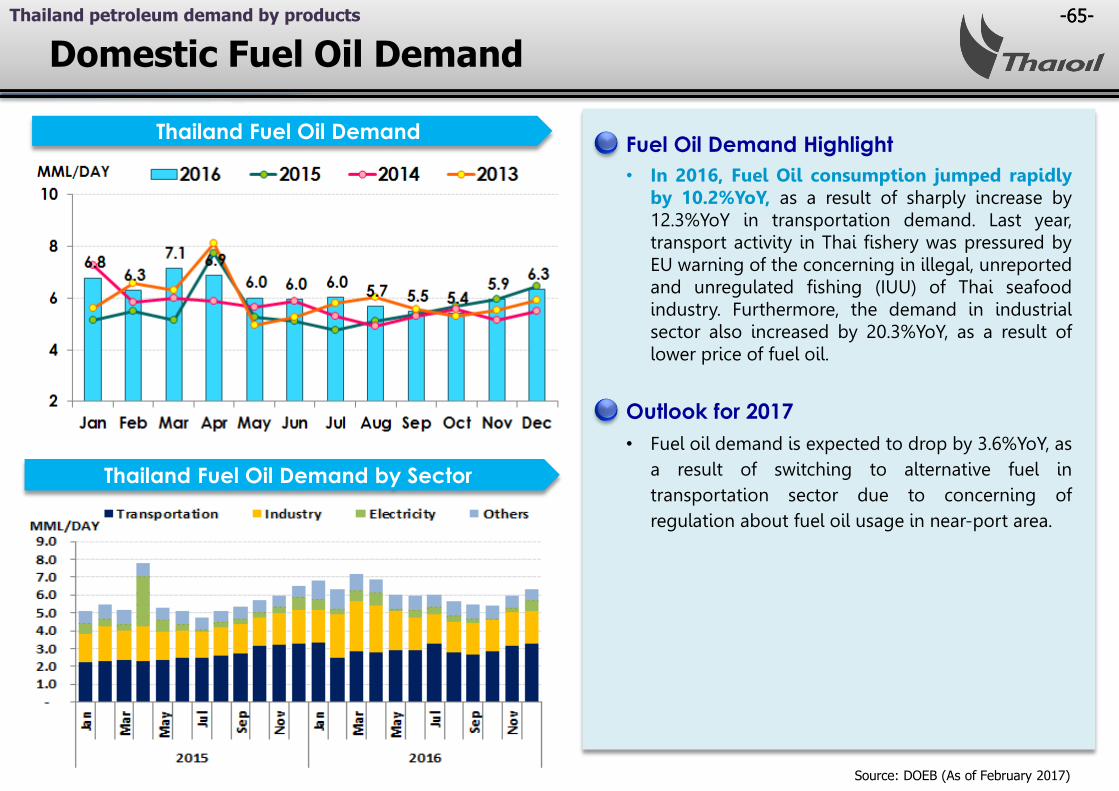

Domestic Fuel Oil Demand

Thailand Fuel Oil Demand by Sector

Fuel Oil Demand Highlight

• In 2016, Fuel Oil consumption jumped rapidly by 10.2%YoY, as a result of sharply increase by 12.3%YoY in transportation demand. Last year, transport activity in Thai fishery was pressured by EU warning of the concerning in illegal, unreported and unregulated fishing (IUU) of Thai seafood industry. Furthermore, the demand in industrial sector also increased by 20.3%YoY, as a result of lower price of fuel oil.

Outlook for 2017

• Fuel oil demand is expected to drop by 3.6%YoY, as a result of switching to alternative fuel in transportation sector due to concerning of regulation about fuel oil usage in near-port area.

Thailand Fuel Oil Demand

Source: DOEB (As of February 2017)

Thailand petroleum demand by products

-66-

Broadening Growth, Capturing Step Out ,Pursuing Sustainability

A Leading fully integrated refining andpetrochemical company in Asia Pacific

Vision

Core Strategies

Financial disciplineManpower readiness Process/System

Vision Measurement by 2021

WA

YEN

D

Enables

MEA

N

• Operational excellence(Safety, Reliability, Efficiency, Flexibility)

• Margin improvement

• Cost management

• Complete projects i.e. LABIX, TOP SPP

• Organic growth i.e. CFP

• PTT Group collaboration in Srirachaarea/ International business

• Value chain enhancement & Integrated downstream

• New business

• R&D

• Portfolio master plan

Review external environments / scenarios & stress test

Top quartile performer DJSI

(Sustainability)

Top Qrt ROIC & NP Growth

Strategy

-67-

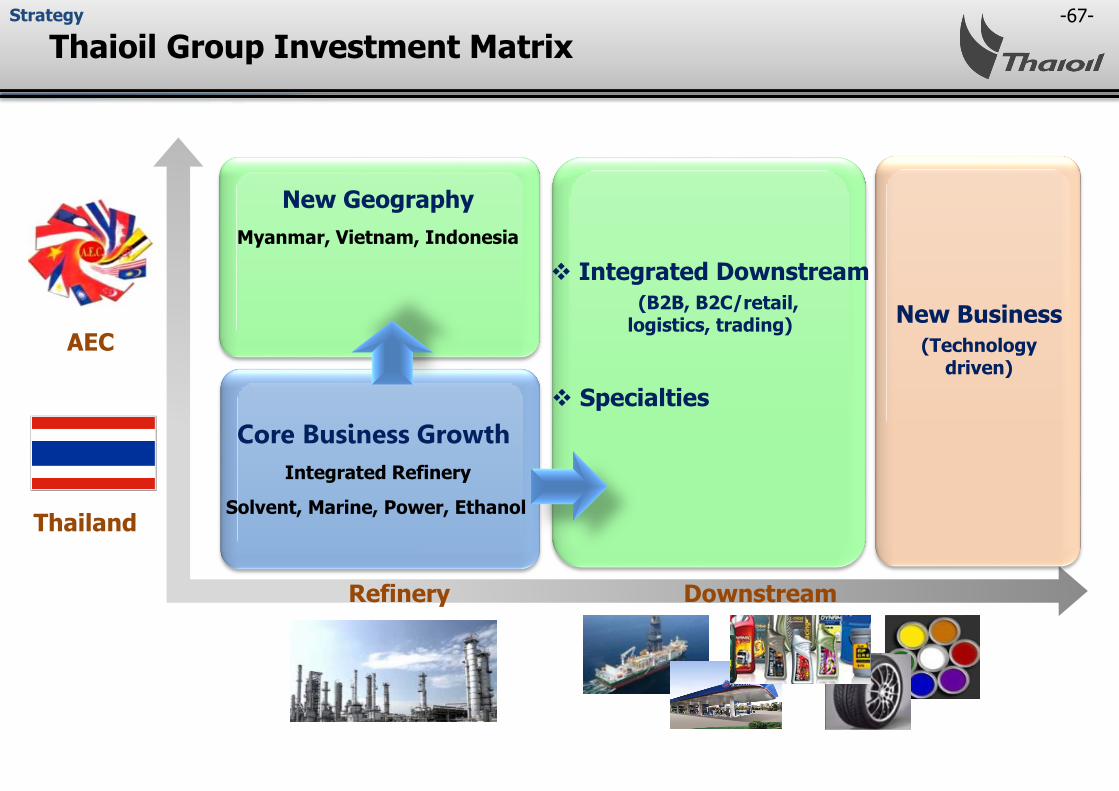

Thaioil Group Investment Matrix

Refinery Downstream

AEC

Thailand

Core Business Growth

New Geography

Myanmar, Vietnam, Indonesia

Integrated Downstream

(B2B, B2C/retail, logistics, trading)

Specialties

Integrated Refinery

New Business

(Technology driven)

Solvent, Marine, Power, Ethanol

Strategy

-68-

Study Project : Clean Fuel Project (CFP)

2015 2016 2017 2018 2019 2020 2021

BDP

FEED

EPC (Engineering Procurement Construction)

EPC Bidding

CODCFP Study Time line

Main objectives of CFP

Enhance competitive advantage of the refinery and maintain 1st quartile performer

Enhance capability to upgrade lower value product into higher value product and ability to process heavier (cheaper) crude oil

(Basic Design Package)

(Front-End Engineering and Design)

FID (Final Investment Decision)

CAPEX +/- 10%

Project Update

-69--69-

Thank You

Any queries, please contact:

at email: [email protected]

Tel: 662-797-2999 / 662-797-2961

Fax: 662-797-2976