Embed Size (px)

Citation preview

See important disclosures at the end of this report Powered by EFATM

Platform 1

Reinitiating Coverage, 15 September 2015

Tiger Airways (TGR SP) Buy (Maintained) Transport - Aviation Target Price: SGD0.32

Market Cap: USD485m Price: SGD0.28

Ready (Again) For Take Off

Macro

3.00

Risks

3.00

Growth

1.00

Value

3.00

64

68

73

77

82

86

91

95

100

104

0.20

0.22

0.24

0.26

0.28

0.30

0.32

0.34

0.36

0.38

Tiger Airways (TGR SP)Price Close Relative to Straits Times Index (RHS)

20

40

60

80

100

120

Sep

-14

No

v-1

4

Jan-1

5

Mar-

15

May-1

5

Jul-15

Vo

l m

Source: Bloomberg

Avg Turnover (SGD/USD) 1.15m/0.83m

Cons. Upside (%) 7.1

Upside (%) 16.94

52-wk Price low/high (SGD) 0.22 - 0.36

Free float (%) 44

Share outstanding (m) 2,499

Shareholders (%)

Singapore Airlines 55.8

Vanguard Group 0.5

Check Kian Low 0.3

Share Performance (%)

YTD 1m 3m 6m 12m

Absolute 3.8 (5.2) (8.3) (11.3) (19.1)

Relative 18.0 2.1 5.6 2.8 (5.4)

Shekhar Jaiswal +65 6232 3894

Forecasts and Valuations Mar-14 Mar-15 Mar-16F Mar-17F Mar-18F

Total turnover (SGDm) 746 677 728 749 803

Reported net profit (SGDm) (223) (264) 22 55 65

Recurring net profit (SGDm) (223) (264) 22 55 65

Recurring net profit growth (%) 391.2 18.5 na 153.0 18.2

Recurring EPS (SGD) (0.25) (0.15) 0.01 0.02 0.03

Recurring P/E (x) na na 31.6 12.5 10.6

P/B (x) 0.97 3.19 2.74 2.25 1.85

P/CF (x) na 16.7 10.2 6.2 5.3

EV/EBITDA (x) na na 7.83 4.55 3.27

Return on average equity (%) (93.4) (107.0) 9.3 19.8 19.3

Net debt to equity (%) 67.6 net cash net cash net cash net cash

Our vs consensus EPS (adjusted) (%) (45.5) (11.8) 0.2

Source: Company data, RHB

We resume coverage on Tigerair with a BUY and SGD0.32TP (17% upside), well supported by earnings recovery after four years of losses. After ridding off loss-making overseas operations, rationalising fleet size and booking significant one-time losses in the past two years, it is ready to book SGD22m in FY16 earnings, aided by higher yields on capacity discipline, better load factor and lower jet fuel costs.

The worst may be behind us. Tiger Airways (Tigerair) reported losses

for four years, driven by the poor performance of its overseas affiliates. However, it has now withdrawn from all loss-making overseas ventures and has sold or sub-leased surplus aircraft that were returned to the group by the overseas affiliates to ensure that Tigerair’s core Singapore operations become profitable.

Recovery aided by yield improvement and lower fuel costs. Aided by

the capacity discipline installed by the airline after the removal of surplus aircraft, Tigerair should witness an increase in yield and load factor over the next two years. As the group has hedged 40% of its fuel needs for the next 15 months at USD87/barrel (bbl), net fuel price paid by the airline is likely to be higher than spot prices. However, Tigerair would still benefit from YoY decline in fuel costs, which account for 40% of total operating costs.

Benefits of being Singapore Airlines’ (SIA) (SIA SP, NR) baby. We

believe that SIA becoming Tigerair’s largest shareholder and parent is one of the key elements for its turnaround and future sustainable growth. The airline would not only benefit from its parent’s scale and network connectivity (as well as those of its affiliates), but also gains on cost and operational efficiencies by building a deeper cooperation with Scoot Pte Ltd, SIA’s budget medium- to long-haul carrier.

Valuation. Our SGD0.32 TP is based on 6x 2016F EV/EBITDA, slightly

below peer average multiple. Our TP implies 2.8x 2016F P/BV, ie just below Tigerair’s historical mean since listing. Based on adjusted EBITDAR, the implied 6.9x 2016F EV/EBITDAR is a slight premium to peers.

Key risks to our rating: i) downturn in air travel demand from

macroeconomic events, ii) a slowdown in Singapore’s economic growth, iii) rise in jet fuel prices, iv) weakness in the SGD, and v) equity raising in case of losses.

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 2

A Quick Glance

Key financials Valuation and TP basis

FYE (Mar) FY15 FY16F FY17F FY18F

Revenue SGDm 677 728 749 803

Revenue growth % -9% 7% 3% 7%

EBITDAR SGDm 66 152 192 213

EBITDAR margin % 10% 21% 26% 27%

Net profit SGDm (264) 22 55 65

Net profit margin % -39% 3% 7% 8%

EPS SGD (0.15) 0.01 0.02 0.03

EPS growth % nm nm 153% 18%

BVPS SGD 0.09 0.10 0.12 0.15

Operating cash flow SGDm 28 67 110 130

Free cash flow SGDm (13) 49 90 110

Our SGD0.32 TP for Tigerair is based on 6x 2016F EV/EBITDA and implies 2.8x 2016F P/BV, which is just below its historical mean since listing. Our TP implies a target 2016F EV/EBITDAR multiple of 6.9x, which, although is at slight premium to its peers, is well supported by the recovery in Tigerair’s earnings and expansion in its EBITDAR margins to 21% in FY16F (Mar) and 26% in FY17F from 10% in FY15.

P/BV chart

Title:

Source:

Please fill in the values above to have them entered in your report

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

P/BV Avg. P/BV=2.9 -1 std=2.2 +1 std=3.7

Key assumptions

FY15 FY16F FY17F FY18F

No. of passengers 000 5,140 5,246 5,235 5,471

Load factor % 82% 84% 85% 85%

Fare per pax SGD 102 106 110 113

ASK m km 11,834 11,967 11,968 12,692

RPK SGD cents 6.8 6.9 7.0 7.1

CASK SGD cents 6.0 5.7 5.7 5.7

Jet fuel price SGD/bbl 127.6 94.0 89.2 99.3

USDSGD x 1.29 1.40 1.43 1.39

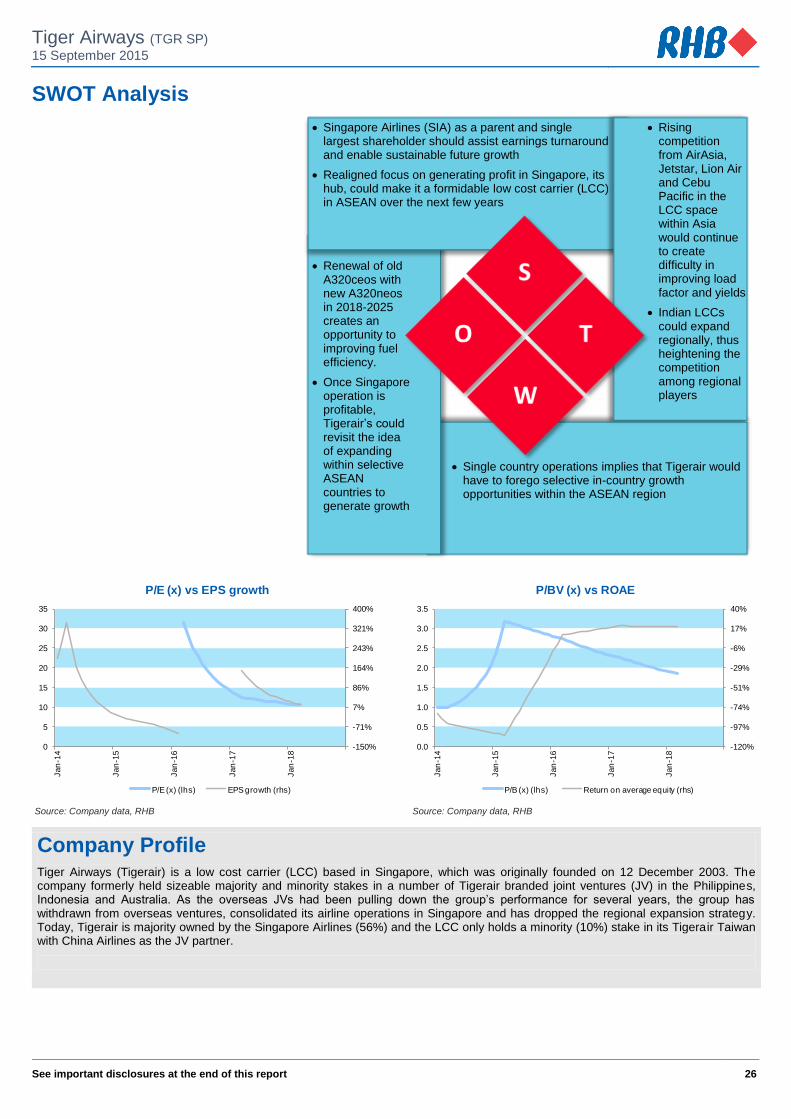

Company description Upside risks Downside risks

Tigerair is a low cost carrier (LCC) based in Singapore, which was originally founded in Dec 2003. The company formerly held stakes in a number of Tigerair branded joint-

ventures (JVs) in the Philippines, Indonesia and Australia. Today, Tigerair is majority owned by the Singapore Airlines (56%) and the LCC only holds a minority (10%) stake in its Tigerair Taiwan JV with China Airlines (2610 TT, NR).

These are: i) better-than-estimated yields, ii) a decline in jet fuel prices, iii) more-than-estimated declines in operational and asset costs, iv) a rapid appreciation of the SGD vs. the USD, and iv) consolidation of LCCs around the region, leading to a less competitive environment.

These are: i) a downturn in regional air travel demand from macroeconomic or geopolitical events, ii) a slowdown in Singapore’s economic growth, iii) a rise in jet fuel prices, iv) continuing weakness in the SGD, and v) capital raising in case of continued losses from operations.

Sensitivity analysis Comparison with consensus

FY16F FY16 FY17 FY17

FYE (Mar) EBITDA profit EBITDA profit

1% increase in passengers booked 7% 22% 6% 12%

1% increase in load factor 8% 26% 7% 14%

1% increase in fare per pax 5% 18% 5% 9%

1% increase in jet fuel price -1% -4% -1% -2%

RHB Consensus

FY16 (Mar) estimate estimate

Revenue SGDm 728 688

EBITDA SGDm 73 85

Net profit SGDm 22 36

Relative comps

P/E P/BV EV/EBITDA Net debt/equity

Dec-15 Dec-16 Dec-15 Dec-16 Dec-15 Dec-16 Dec-15 Dec-16

AirAsia 5.3 4.0 0.62 0.56 6.2 6.3 199% 203%

Asia Aviation 12.3 15.5 1.05 1.01 6.8 8.6 14% 25%

Nok Air 10.6 5.5 1.13 0.97 na 0.6 -80% -84%

Tigerair** - 14.6 2.84 2.35 11.1 5.1 -36% -60%

Note: Tigerair numbers are for four quarters ending December. Prices are as at 14 Sep 2015. More detailed comparisons are provided in Figure 4.

Source: Bloomberg, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 3

Table of Contents

A Quick Glance ............................................................................................... 2

Investment Thesis – Valuation And Risks ...................................................... 4

Investment thesis ........................................................................................ 4

Valuation and price target ........................................................................... 4

What’s the worst case scenario? ................................................................ 6

Risks to our rating and price target............................................................. 6

Got Rid Of Bleeding Overseas Ventures And Excess Aircraft ....................... 7

Struggling affiliates meant overcapacity in a mature Singapore market .... 7

Tigerair has withdrawn from all overseas loss making operations… ......... 7

…and has reduced its fleet size to a more realistic number ...................... 8

Yield Recovery And Lower Unit Cost To Help Improve Profits .................... 10

Route rationalisation and terminations has reduced capacity .................. 10

Improvement in yields and load factor already visible .............................. 11

Low fuel prices and a decline in high fuel price hedge to keep costs low 12

To Benefit From Its Growing Relationship With SIA .................................... 13

Leveraging on Scoot’s complementary network ....................................... 13

Co-operation with Scoot is not limited to network .................................... 13

It is not all about Scoot, getting help from KrisFlyer too ........................... 13

Witnessing a Financial Turnaround .............................................................. 14

Witnessing a turnaround, growth to sustain for at least two years ........... 14

Re-capitalised balance sheet with a strong shareholder .......................... 15

Costs to increase if SGD continues to weaken against the USD ............. 16

Rise in jet fuel prices could also throw Tigerair off its recovery track ....... 16

Revised aggressive depreciation policy to help keep the fleet young ...... 16

A Quick Comparison With Regional LCCs ................................................... 17

Company Background .................................................................................. 17

Appendix 1 - Tigerair’s Route Map ............................................................... 19

Appendix 2 - Tigerair’s Flight Departures From Singapore .......................... 20

Appendix 3 – History Of (Failed) Overseas Expansions .............................. 21

Overseas expansions gone sour .............................................................. 21

Overseas ventures that never took off ..................................................... 23

Regional partnerships that were later cancelled ...................................... 23

Financial Exhibits .......................................................................................... 24

Financial Exhibits .......................................................................................... 25

SWOT Analysis ............................................................................................ 26

Recommendation Chart ................................................................................ 27

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 4

Investment Thesis – Valuation And Risks

Investment thesis

We believe that Tigerair’s worst years are now in the past and the airline is moving towards strong earnings recovery. We expect the group to report its first full-year profit of SGD22m in FY16 after four consecutive years of losses. The recovery would be driven by a reduction in seat capacity and network rationalisation initiatives undertaken over the last two years.

Tigerair has withdrawn, closed or sold all of its loss-making overseas operations. It has also reduced its fleet size by either selling or sub-leasing aircraft. Most one-time charges related to: i) sales of associates at a loss, ii) sales of aircraft at a loss, iii) sub-lease of aircraft at lower rental rates, iv) increased provisions related to the adoption of an aggressive depreciation policy, and v) higher maintenance costs for leased aircraft have already been booked in last two years. With capacity discipline in place, load factor and yield improvements have started to depict a more visible recovery trend, which makes us believe that there is limited downside risk.

Leveraging on Tigerair’s relationship with SIA and its affiliates, especially Scoot, the latter’s medium- to long-haul budget carrier, would enable the airline to further optimise its network and reduce operating costs. We believe that Tigerair could emerge as one of the stronger LCCs within the ASEAN region over the next 2-3 years, well supported by parent SIA, which is also now its single-largest shareholder.

Valuation and price target

Our SGD0.32 TP for Tigerair is based 6x 2016F EV/EBITDA multiple, which is slightly below the average multiple for its peers. Our TP implies 2.8x 2016F P/BV, which is just below the stock’s historical mean since listing. Our TP implies a target 2016F EV/EBITDAR multiple of 6.9x, which, although at a slight premium to its peers, we believe is well supported by a recovery in Tigerair’s earnings and expansion in its EBITDAR margins to 21% in FY16 and 26% in FY17 from 10% in FY15.

Figure 1: Target price derivation

EV/EBITDA based valuation

Rolling

Quarter ended Mar-16 Jun-16 Sep-16 Dec-16 quarters

EBITDA SGDm 32.5 23.1 18.5 31.5 105.6

Target EV/EBITDA multiple x 6.0

Target EV SGDm 633.7

Estimated net debt SGDm (171.2)

Equity value SGDm 805.0

Year-end (basic) shares o/s m 2,497.5

Year-end price target SGD 0.32

Source: RHB

Figure 2: Implied P/BV valuation Figure 3: Implied P/E valuation

P/BV based valuation

Financial year ended Dec-16

BPS (basic) SGD 0.11

Target P/BV multiple x 2.8

Target price SGD 0.32

PE based valuation

Financial year ended Dec-16

EPS (basic) SGD 0.02

Target PE multiple x 15.0

Target price SGD 0.32

Source: RHB Source: RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 5

Figure 4: Relative comparisons

BBG Price M Cap Last FY ROE N.Margin

Company name ticker (LCY) (USD m) FY0 FY0 FY1 FY2 FY0 FY1 FY2 FY0 FY1 FY2 FY1 FY1

ASEAN low cost carriers

Cebu Air CEB PM 88.35 1,145 Dec-14 62.7 7.5 6.7 9.7 6.0 6.0 2.49 1.98 1.62 27.5% 12.7%

AirAsia AIRA MK 1.23 794 Dec-14 12.5 5.3 4.0 9.2 6.2 6.3 0.75 0.62 0.56 18.4% 15.5%

Asia Aviation AAV TB 4.42 595 Dec-14 108.3 12.3 15.5 25.3 6.8 8.6 1.12 1.05 1.01 8.8% 5.8%

AirAsia X AAX MK 0.19 183 Dec-14 - - - - 39.2 9.3 0.65 1.00 1.05 -40.5% -10.3%

Nok Airlines Co Ltd NOK TB 7.30 127 Dec-14 - 10.6 5.5 - - 0.6 1.24 1.13 0.97 11.2% 3.1%

Weighted average 2,844 57.7 8.1 7.8 13.2 8.4 6.6 1.54 1.31 1.13 19.8% 11.6%

Global low cost carriers

Southwest Airlines LUV US 38.54 25,412 Dec-14 23.4 11.1 10.4 7.9 5.1 4.9 3.84 2.99 2.49 31.6% 11.9%

Ryanair RYA ID 13.60 20,844 Mar-15 21.7 15.4 13.4 12.3 9.4 8.2 4.64 3.89 3.07 27.5% 19.3%

EasyJet EZJ LN 1,774.00 10,886 Sep-14 15.5 13.0 11.9 9.5 8.0 7.4 3.24 2.78 2.51 23.5% 11.6%

JetBlue Airways JBLU US 25.68 8,084 Dec-14 18.9 13.7 12.0 11.0 6.0 5.3 3.15 2.68 2.18 22.6% 10.1%

WestJet WJA CN 24.07 2,277 Dec-14 10.8 8.0 8.0 4.1 3.5 3.4 1.73 1.55 1.33 19.2% 9.3%

Air Arabia AIRARABI DB 1.40 1,779 Dec-14 11.7 10.8 9.5 10.0 8.3 7.3 1.29 1.24 1.18 12.1% 15.9%

GOL Airways GOLL4 BZ 4.30 386 Dec-14 - - - 7.0 10.1 7.2 - - - 119.9% -13.4%

Weighted average 69,668 20.4 12.9 11.6 9.7 7.0 6.4 3.77 3.10 2.56 27.6% 13.9%

Tigerair** TGR SP 0.28 488 Mar-15 - - 14.6 - 11.1 5.1 2.04 2.84 2.35 20.6% 7.1%

P/E EV/EBITDA P/BV

Note: Tigerair numbers are for four quarters ending December. Prices are as at 14 Sep 2015.

Source: Bloomberg, RHB

Figure 5: Tigerair - 1-year forward (unadjusted) EV/EBITDAR Figure 6: Tigerair - 1-year forward P/BV

Title:

Source:

Please fill in the values above to have them entered in your report

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

EV/ EBITDAR Avg. EV/ EBITDAR=9.1

-1 std=4.6 +1 std=13.6

Title:

Source:

Please fill in the values above to have them entered in your report

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

P/BV Avg. P/BV=2.9 -1 std=2.2 +1 std=3.7

Source: Bloomberg, company data, RHB Source: Bloomberg, company data, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 6

What’s the worst case scenario?

The infusion of capital from SIA has helped strengthen Tigerair’s balance sheet. However, assuming the airline continues to report losses from its core operations in Singapore and with no fresh capital-raising undertaken, the LCC’s share price could fall to SGD0.13, which is our worst case estimate of its current book value.

Figure 7: Tigerair’s worst case book value estimate

RNAV assessment

Last

reported

Aircraft at market selling price SGDm 9.0 36.0 324.0 Assuming 20% discount to market selling price

Pre-payment, receivables & aircraft deposits (1QFY16) SGDm 159.0

Payables (1QFY16) SGDm (84.8)

Sales in advance (1QFY16) SGDm (67.7)

Net cash/(net debt) (1QFY16) SGDm 2.2

Total SGDm 332.7

Shares outstanding (1QFY16) m 2,497.5

Per share value SGD 0.13

Source: Company data, RHB

Risks to our rating and price target

Key downside risks include: i) a downturn in regional air travel demand from

macroeconomic or geopolitical events, ii) a slowdown in Singapore’s economic growth, iii) a rise in jet fuel prices, iv) continuing weakness in the SGD, and v) capital raising in case of continued losses from operations.

Key upside risks include: i) better-than-estimated yields, ii) a decline in jet fuel

prices, iii) more-than-estimated declines in operational and asset costs, iv) a rapid appreciation of the SGD vs. the USD, and v) consolidation of LCCs around the region, leading to a less-competitive environment.

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 7

Got Rid Of Bleeding Overseas Ventures And Excess Aircraft

Struggling affiliates meant overcapacity in a mature Singapore market

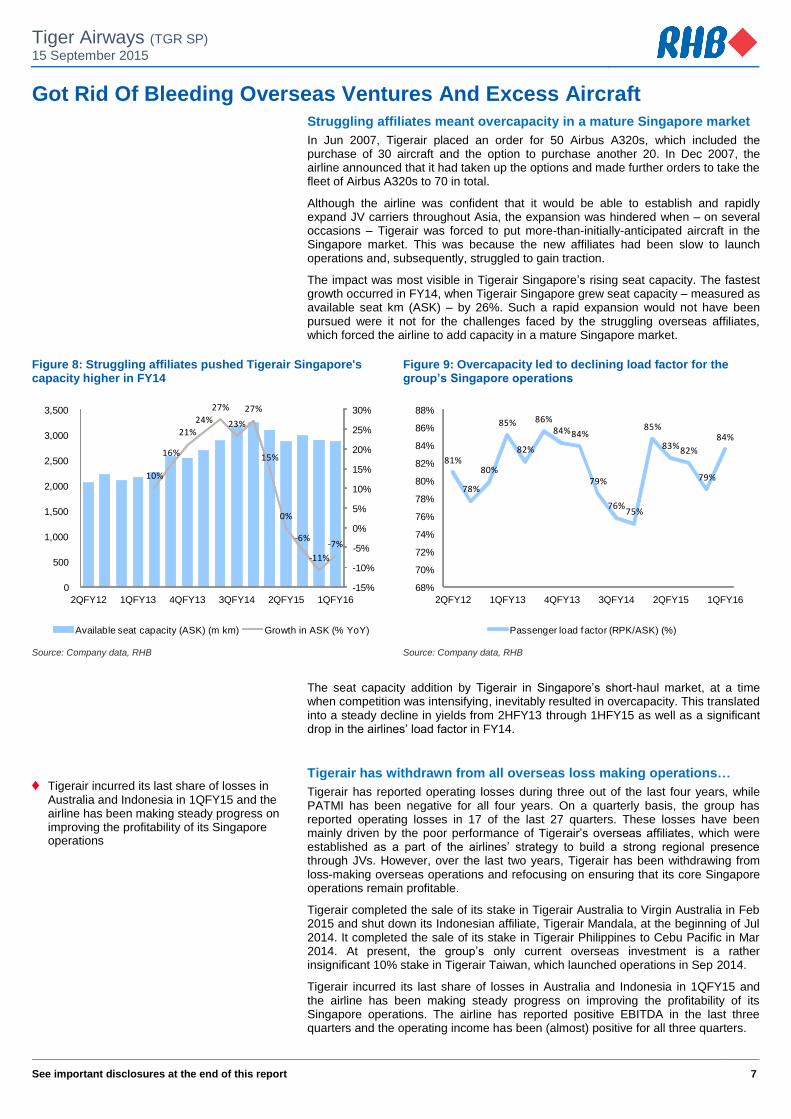

In Jun 2007, Tigerair placed an order for 50 Airbus A320s, which included the purchase of 30 aircraft and the option to purchase another 20. In Dec 2007, the airline announced that it had taken up the options and made further orders to take the fleet of Airbus A320s to 70 in total.

Although the airline was confident that it would be able to establish and rapidly expand JV carriers throughout Asia, the expansion was hindered when – on several occasions – Tigerair was forced to put more-than-initially-anticipated aircraft in the Singapore market. This was because the new affiliates had been slow to launch operations and, subsequently, struggled to gain traction.

The impact was most visible in Tigerair Singapore’s rising seat capacity. The fastest growth occurred in FY14, when Tigerair Singapore grew seat capacity – measured as available seat km (ASK) – by 26%. Such a rapid expansion would not have been pursued were it not for the challenges faced by the struggling overseas affiliates, which forced the airline to add capacity in a mature Singapore market.

Figure 8: Struggling affiliates pushed Tigerair Singapore's capacity higher in FY14

Figure 9: Overcapacity led to declining load factor for the group’s Singapore operations

Title:

Source:

Please fill in the values above to have them entered in your report

10%

16%

21%

24%

27%

23%

27%

15%

0%

-6%

-11%

-7%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2QFY12 1QFY13 4QFY13 3QFY14 2QFY15 1QFY16

Available seat capacity (ASK) (m km) Growth in ASK (% YoY)

Title:

Source:

Please fill in the values above to have them entered in your report81%

78%

80%

85%

82%

86%84%84%

79%

76%75%

85%

83%82%

79%

84%

68%

70%

72%

74%

76%

78%

80%

82%

84%

86%

88%

2QFY12 1QFY13 4QFY13 3QFY14 2QFY15 1QFY16

Passenger load factor (RPK/ASK) (%)

Source: Company data, RHB Source: Company data, RHB

The seat capacity addition by Tigerair in Singapore’s short-haul market, at a time when competition was intensifying, inevitably resulted in overcapacity. This translated into a steady decline in yields from 2HFY13 through 1HFY15 as well as a significant drop in the airlines’ load factor in FY14.

Tigerair has withdrawn from all overseas loss making operations…

Tigerair has reported operating losses during three out of the last four years, while PATMI has been negative for all four years. On a quarterly basis, the group has reported operating losses in 17 of the last 27 quarters. These losses have been mainly driven by the poor performance of Tigerair’s overseas affiliates, which were established as a part of the airlines’ strategy to build a strong regional presence through JVs. However, over the last two years, Tigerair has been withdrawing from loss-making overseas operations and refocusing on ensuring that its core Singapore operations remain profitable.

Tigerair completed the sale of its stake in Tigerair Australia to Virgin Australia in Feb 2015 and shut down its Indonesian affiliate, Tigerair Mandala, at the beginning of Jul 2014. It completed the sale of its stake in Tigerair Philippines to Cebu Pacific in Mar 2014. At present, the group’s only current overseas investment is a rather insignificant 10% stake in Tigerair Taiwan, which launched operations in Sep 2014.

Tigerair incurred its last share of losses in Australia and Indonesia in 1QFY15 and the airline has been making steady progress on improving the profitability of its Singapore operations. The airline has reported positive EBITDA in the last three quarters and the operating income has been (almost) positive for all three quarters.

Tigerair incurred its last share of losses in Australia and Indonesia in 1QFY15 and the airline has been making steady progress on improving the profitability of its Singapore operations

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 8

We believe the sale and closure of Tigerair’s affiliates in Australia, Indonesia and the Philippines should improve the group’s outlook over the medium to long term. For a detailed discussion on Tigerair’s failed or abandoned overseas ventures, please look at Appendix 2.

…and has reduced its fleet size to a more realistic number

Subsequent to the overseas venture exits, Tigerair was left with a significant number of surplus aircraft that the Singapore operation could not absorb. In order to manage excess capacity, the airline proactively addressed its surplus aircraft issue through sub-lease arrangements, novation of aircraft leases and the disposal of aircraft.

Tigerair’s FY15 results were impacted by several one-off charges related to fleet adjustments, which became necessary as the group had to take back 14 aircraft that had earlier been operating in Indonesia and the Philippines. While Tigerair had sold its stake in Tigerair Philippines at the end of FY14, the group’s five aircraft that had been operating in the market were only returned to Tigerair in early FY15.

As the Singapore operations could not absorb the surplus aircrafts, Tigerair had to ground several A320s in FY15 while it tried to remarket the surplus aircraft. The group managed to forge a sub-lease agreement with Indigo, an Indian LCC, for 12 A320s, 10 of which were delivered in 2HFY15. The last two were delivered in the early part of FY16. However, because the market for used aircraft is weak, Tigerair had to sub-lease the aircraft at a lower rate and incurred a loss of around SGD110m in the transaction.

Tigerair has already sub-leased or placed three aircraft with Tigerair Australia, which is now owned and operated by Virgin Australia. In addition, the airline managed to sub-lease or place two A320s with Tigerair Taiwan by end-1QFY15. The rental rates for aircraft sub-leased to Tigerair Taiwan and Tigerair Australia are on a “back-to-back” basis, with the head leases entered into between the airline and third party lessors, whereby the sub-lease period matched the head lease duration.

Tigerair also cancelled the order for nine A320ceo (current engine option) aircraft, which were originally slated for delivery in FY15 and FY16. The cancellations were part of a deal with Airbus (AIR FP, NR) that was forged in Mar 2014, which included the placement of new orders for 37 A320neo (new engine option) aircraft plus an option to buy an additional 13 of this variant.

Despite the cancellation of order for the new A320ceos and sub-leasing of 17 aircraft, Tigerair continued to be saddled with excess capacity. The airline announced its plan to dispose of two A320s in FY16 and incurred a one-time charge of SGD17.5m in 4QFY15 to reflect the anticipated sale of these self-owned aircraft.

Tigerair now operates 25 aircraft, which includes 23 A320s and two A319s, one of which is grounded. The carrier plans to reactivate the grounded A319 to replace the two A320s, which have been earmarked for sale in FY16.

Figure 10: Tigerair’s current fleet details Figure 11: Fleet details as estimated at end-FY16

Aircraft In fleet Firm orders Options Passengers

per aircraft

Airbus A319 2 - - 144

Airbus A320ceo 23 - - 180

Airbus A320neo - 39 11

Total 25 39 11

Aircraft In fleet Firm orders Options Passengers

per aircraft

Airbus A319 2 - - 144

Airbus A320ceo 21 - - 180

Airbus A320neo - 39 11

Total 23 39 11

Source: Company data, RHB Source: Company data, RHB

Following the fleet rationalisation exercise, Tigerair’s operating fleet declined to 24 in 1QFY16 from 27 in 1QFY15. The fleet size is to be further reduced to 23 by end-FY16 following the proposed sale of two A320s. We estimate for Tigerair’s fleet strength to remain unchanged at 23 till 2QFY18.

Long-term fleet challenges still remain though

We believe managing a fleet of 23 aircraft in a relatively mature Singapore market seems more realistic when compared to 27 aircraft that Tigerair was operating at the start of 1QFY15 when its elevated capacity levels exceeded demand. However, the airline faces long-term fleet challenges as it is now committed to 39 new A320neo aircraft for delivery from 2018.

12 aircraft were sub-leased to Indigo, an Indian LCC, at a discounted lease rate

Tigerair managed to sub-lease or place two A320s with Tigerair Taiwan by end-1QFY15

Cancelled the order for nine A320ceo aircraft, which were originally slated for delivery in FY15 and FY16

Planned delivery of 39 A320neos in 2018-2025 and return of 11 A320ceos in 2018-2019, which were sub-leased to Indigo, would lead to excess fleet capacity starting FY19

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 9

In addition, the 12 aircraft that have been placed with Indigo have been sub-leased for between 3-4 years and would be returned to Tigerair starting late FY18.

Among the 12 aircraft sub-leased to Indigo, the lease for one is expiring in 2018. Hence, only 11 aircraft are to be returned to Tigerair following the expiry of the sub-lease period. Post their return, the airline plans to induct seven aircraft into its operating fleet, while four are to be stored and progressively reintroduced to the service network within two years.

We believe Tigerair could struggle to find markets for all 39 A320neos. Singapore has limited growth opportunities and is unlikely to support more than 25 aircraft – at most 30 – from the airline.

As Tigerair does not have any plans to re-establish a portfolio of overseas affiliates, we believe the airline is likely to have limited alternatives for placing the excess A320neos. Tigerair no longer has any stakes in Tigerair Australia and Tigerair Philippines, both of which could be rebranded in FY16. Tigerair Taiwan has also indicated that it plans to source its future aircraft outside the group, which only has a 10% stake in Taiwanese carrier and, therefore, has limited influence on its fleet decisions.

Placing the excess A320neos at another SIA subsidiary is also not a possibility as SilkAir is transitioning its fleet to Boeing’s 737s from A320s. Although Vistara, SIA’s latest JV carrier in India, operates a fleet of A320s, it has already committed to acquiring 20 A320s from BOC Aviation Pte Ltd.

Unless Tigerair manages to expand operations beyond Singapore, which is not the plan at present, the airline might have to consider: i) storing excess aircraft until it manages to sub-lease them, and/or ii) the early disposal of its self-owned aircraft or early termination of lease for leased aircraft in order to gradually replace its old A320ceo fleet with new A320neos. However, either of these options would lead to elevated costs or one-time charges, which would drag earnings starting from FY19.

The Singapore market can support a maximum of 30 aircraft from Tigerair

SilkAir, the regional wing of SIA, is transitioning to an all Boeing 737 fleet, while SIA’s Indian JV has already committed to acquiring 20 A320s

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 10

Yield Recovery And Lower Unit Cost To Help Improve Profits

Route rationalisation and terminations has reduced capacity

Tigerair began slowing its expansion in FY14 and this continued into FY15. Capacity and network cuts were implemented throughout FY15, with total ASK declining 9.3% YoY to 11,812m km. The decline in ASK continued into early FY16 with ASK declining 7.2% YoY in 1QFY16.

The Centre for Asia Pacific Aviation (CAPA) reported that, in FY15, Tigerair launched four routes and axed seven as the airline rationalised its network. Although Tigerair began FY15 with 39 routes, it ended the year with 36 and connected Singapore with 13 Asian countries.

In August, the airline announced plans to commence scheduled flights to Quanzhou in China and Lucknow in India from 28 Sep 2015 and 3 Dec 2015 respectively. Based on Tigerair’s year-end operating fleet, and including these newly-announced routes, we estimate for the airline’s year-end seat capacity to be at 6,015 thousand seats, which is 5% lower than end-FY15’s 6,339 thousand seats.

Figure 12: Singapore LCC market share in May 2014 Figure 13: Singapore LCC market share in May 2015

Title:

Source:

Please fill in the values above to have them entered in your report

Tigerair, 33%

Jetstar, 21%

AirAsia, 26%

Scoot, 8%

Lion Air, 5%

Cebu Pacif ic, 4%

Others, 3%

Title:

Source:

Please fill in the values above to have them entered in your report

Tigerair, 29%

Jetstar, 25%

AirAsia, 23%

Scoot, 9%

Lion Air, 7%

Cebu Pacif ic, 5%

Others, 2%

Source: Centre for Asia Pacific Aviation (CAPA), RHB Source: CAPA, RHB

Figure 14: Load factors should gradually improve to 85%... Figure 15: ...while yield could grow at 1.2-1.5% pa over next three years

Title:

Source:

Please fill in the values above to have them entered in your report

81%

86% 86%

81%

84%

79%

82%

84%

85% 85%

74%

76%

78%

80%

82%

84%

86%

88%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Available seat capacity (m km) Passenger load factor (%)

Title:

Source:

Please fill in the values above to have them entered in your report

-0.3%

5.5%

-5.1%

9.2%

-11.2%

-2.6%

1.2% 1.5% 1.3%

-15%

-10%

-5%

0%

5%

10%

15%

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Revenue per RPK (SGD cents) Growth (YoY %)

Source: Company data, RHB Source: Company data, RHB

We expect Tigerair to maintain discipline on capacity expansion. Despite the decline in the average number of aircraft to 24 in FY16 and 23 by FY17 from 25 in FY15, we expect unit capacity as defined by ASK (available seat kilometres) to increase by 1.3% in FY16 and remain unchanged in FY17. The increase in ASK will be aided by 3% YoY improvement in average distance flown by an aircraft. Tigerair will offer

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 11

flights to new destinations in China and India in FY16. Note that in 1Q16, Tiger saw an increase in utilisation hours of 8.8% YoY (to 12.2 hours).

Strong capacity discipline should provide a lift to Tigerair’s yield (we estimate an improvement of 1.2% and 1.5% yields for FY16 and FY17 respectively), while load factor is assumed to recover to 84% in FY16 and 85% in FY17 from 82% in FY15.

Improvement in yields and load factor already visible

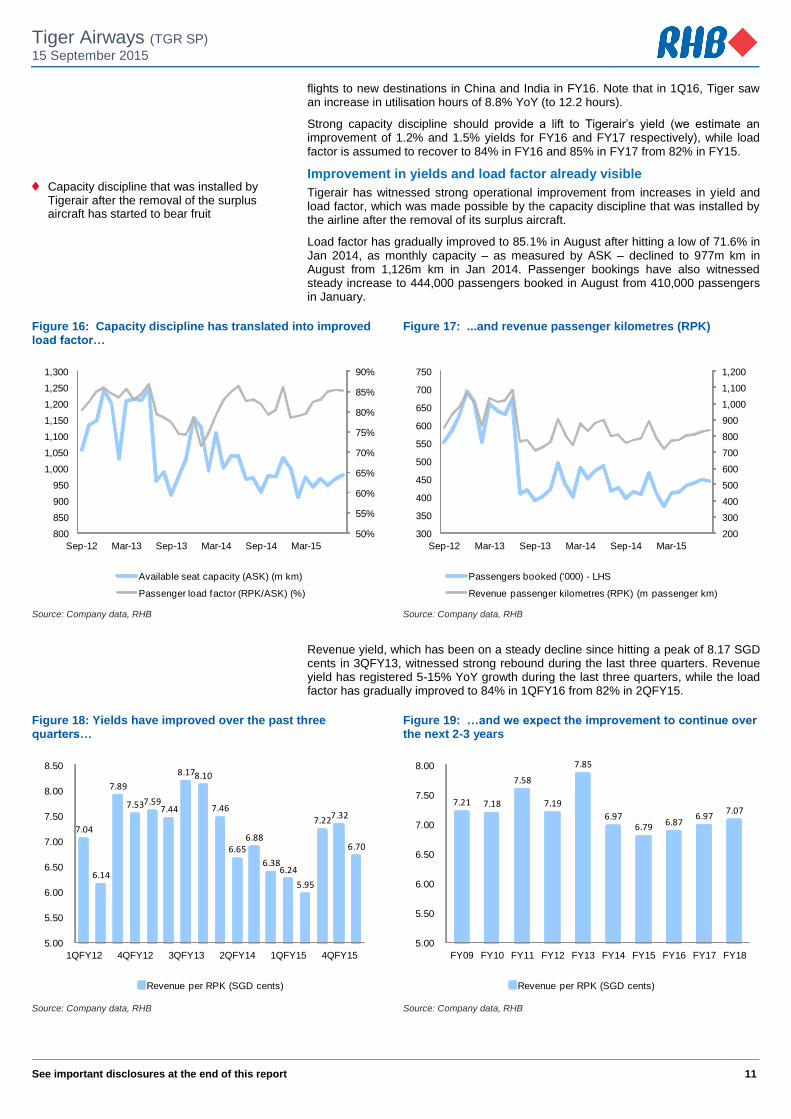

Tigerair has witnessed strong operational improvement from increases in yield and load factor, which was made possible by the capacity discipline that was installed by the airline after the removal of its surplus aircraft.

Load factor has gradually improved to 85.1% in August after hitting a low of 71.6% in Jan 2014, as monthly capacity – as measured by ASK – declined to 977m km in August from 1,126m km in Jan 2014. Passenger bookings have also witnessed steady increase to 444,000 passengers booked in August from 410,000 passengers in January.

Figure 16: Capacity discipline has translated into improved load factor…

Figure 17: ...and revenue passenger kilometres (RPK)

Title:

Source:

Please fill in the values above to have them entered in your report

50%

55%

60%

65%

70%

75%

80%

85%

90%

800

850

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

Available seat capacity (ASK) (m km)

Passenger load factor (RPK/ASK) (%)

Title:

Source:

Please fill in the values above to have them entered in your report

200

300

400

500

600

700

800

900

1,000

1,100

1,200

300

350

400

450

500

550

600

650

700

750

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

Passengers booked ('000) - LHS

Revenue passenger kilometres (RPK) (m passenger km)

Source: Company data, RHB Source: Company data, RHB

Revenue yield, which has been on a steady decline since hitting a peak of 8.17 SGD cents in 3QFY13, witnessed strong rebound during the last three quarters. Revenue yield has registered 5-15% YoY growth during the last three quarters, while the load factor has gradually improved to 84% in 1QFY16 from 82% in 2QFY15.

Figure 18: Yields have improved over the past three quarters…

Figure 19: …and we expect the improvement to continue over the next 2-3 years

Title:

Source:

Please fill in the values above to have them entered in your report

7.04

6.14

7.89

7.53 7.59 7.44

8.17 8.10

7.46

6.65 6.88

6.38 6.24

5.95

7.22 7.32

6.70

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

1QFY12 4QFY12 3QFY13 2QFY14 1QFY15 4QFY15

Revenue per RPK (SGD cents)

Title:

Source:

Please fill in the values above to have them entered in your report7.21 7.18

7.58

7.19

7.85

6.97 6.79 6.87

6.97 7.07

5.00

5.50

6.00

6.50

7.00

7.50

8.00

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Revenue per RPK (SGD cents)

Source: Company data, RHB Source: Company data, RHB

Capacity discipline that was installed by Tigerair after the removal of the surplus aircraft has started to bear fruit

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 12

Low fuel prices and a decline in high fuel price hedge to keep costs low

In line with global crude oil prices, jet fuel price has been on a decline. Intuitively, this should be positive for the profitability of airline companies. However, most carriers globally maintain a hedging policy and Tigerair is no different. The group only started providing details of its fuel hedging policy in 4QFY15.

As at end of 1QFY16, Tigerair had hedged 40% of its jet fuel requirement for the next 15 months at USD87 per bbl. As the hedged fuel price is higher than spot prices, the carrier would have to incur losses as it unwinds/rolls forward the hedging position. However, management highlighted that the airline would continue to hedge 40-60% of its forward fuel requirements, implying that subsequent fuel hedges would be at a lower price. This should help Tigerair to maintain lower unit fuel costs as it optimises its route network and fleet. We expect total fuel cost as a percentage of reported revenue to decline to 33% in FY16 from 43% in FY15 and eventually drop to 29% in FY17.

Figure 20: Jet fuel prices have dropped and are expected to stay low for some time

Figure 21: Lower jet fuel prices should help improve operating margins

Title:

Source:

Please fill in the values above to have them entered in your report

0

20

40

60

80

100

120

140

160

1QFY09 2QFY10 3QFY11 4QFY12 1QFY14 2QFY15 3QFY16 4QFY17

Jet fuel spot (Singapore) (USD/barrel)

Jet fuel spot (Singapore) - forecast (USD/barrel)

Title:

Source:

Please fill in the values above to have them entered in your report

74 123 199 182 226 289 364 338 293 241 221 233

43%41%

53%

37% 36%

47%

42%45%

43%

33%29% 29%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

400

FY07 FY09 FY11 FY13 FY15 FY17

Fuel cost (SGDm) Fuel cost (% of revenue) (%)

Source: Bloomberg, RHB Source: Company data, RHB

We estimate spot price for jet fuel to decline 26% YoY to SGD94 per bbl in FY16. However, due to Tigerair’s high fuel price hedge, the net jet fuel price paid by the airline would decline only by 23% to SGD108 per bbl. This should translate into 18% YoY decline in fuel costs. The total fuel cost is expected to decline further by 8% in FY17, largely in line with our expectations of further declines in jet fuel prices.

Figure 22: Operating cost split for FY15 Figure 23: Subsequent jet fuel hedges at current low prices should ensure that costs remain under control

Title:

Source:

Please fill in the values above to have them entered in your report

Fuel cost, 41%

Staf f cost, 12%

Aircraf t rental, 10%

Airport & handling, 12%

Maintenance & repair, 11%

Route charges, 3%

Marketing costs, 3% D&A,

5%

Others, 4%

Title:

Source:

Please fill in the values above to have them entered in your report

143

120

135

161 156

152

128

94 89

99

106 111

157

136 133

157 154

151

141

109

101 102 106

109

80

90

100

110

120

130

140

150

160

170

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Jet fuel assumption SGD/barrel

Jet fuel price paid (net) SGD/barrel

Source: Company data, RHB Source: Bloomberg, Company data, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 13

To Benefit From Its Growing Relationship With SIA SIA becoming the largest shareholder of Tigerair is one of the key elements for a decisive turnaround and future sustainable growth for the LCC. The airline would not only benefit from the scale and network connectivity of SIA and its affiliates, but also gain on cost efficiencies by building a deeper cooperation with Scoot, the latter’s LCC for medium- and long-haul routes.

Leveraging on Scoot’s complementary network

The market for budget air travel in Asia has moved past the initial years of high growth and it is becoming increasingly crowded with the entry of new LCCs and expanding fleet size of the existing budget carriers. The abandoning of its “cub strategy” and the selling/closing down its overseas ventures imply that Tigerair is likely to struggle to expand by only providing point-to-point flights from its Singapore base. We believe partnerships would be needed to sustain growth and we see Scoot as a natural partner, since its Singapore base and complimentary medium- to long-haul network provides the greatest potential for connecting traffic.

Since the Competition Commission of Singapore granted anti-trust immunity in Aug 2014, Tigerair and Scoot have been working hard to build revenue synergies, particularly by connecting passengers to each other’s networks. Tigerair highlighted that it has witnessed many travellers connecting from Scoot’s Australia and North-East China points to Tigerair’s South-East Asia points. Without stating the financial impact of the benefits, Tigerair, in a January press release, highlighted that it had witnessed a doubling of passengers connecting between the two airlines due to co-ordinated joint promotions and the launch of new itineraries only available by combining the routes of both Tigerair and Scoot.

We believe that JV agreements on routes that both budget carriers operate, such as Hong Kong and Bangkok, would result in better performances for the two airlines as both would be able to meet the competition with their combined strength.

Co-operation with Scoot is not limited to network

In addition to connecting passengers to each other’s networks, Tigerair and Scoot are also in discussions to leverage on other synergies. Beyond coordination on promotions, distribution and networks, both airlines could also explore opportunities for deeper cooperation, including common ground handling, procurement and service centres.

As both airlines operate out of the same terminal at Singapore’s Changi Airport, we believe it makes sense for the two parties to potentially combine their facilities at the terminal. Tigerair and Scoot both use the same computer reservation system, and management highlighted that the merging of the two systems into one would result in more seamless transactions for its passengers and lead to higher cost efficiencies. We believe benefits from such cost synergies would start becoming visible from FY16 onwards.

It is not all about Scoot, getting help from KrisFlyer too

Tigerair’s integration with SIA is not only with Scoot. The LCC is also benefitting from its participation in SIA’s frequent flyer programme, KrisFlyer. Since April, members of

this programme can redeem miles for vouchers to travel on Tigerair flights.

Figure 24: Redemption of KrisFlyer miles for Tigerair vouchers

KrisFlyer miles required for redemption Value of voucher (SGD)

3,200 30

5,300 50

10,500 100

Source: SIA, RHB

While we believe that Tigerair’s relationship with SIA and its affiliates has started to make positive contributions to the LCC’s operations, management has not yet ascribe a monetary value to the benefits. Tigerair continues to explore additional opportunities for synergies with SIA in commercial, operations and other areas of business, benefits of which are likely to continue to be visible over the next few years.

SIA becoming the largest shareholder of Tigerair is one of the key elements for a decisive turnaround and future sustainable growth of the LCC

Tigerair, in a January press release, highlighted that it has witnessed a doubling of passengers connecting between itself and Scoot

Cost synergies from common ground handling, procurement, service centres and a merged single reservation system will start becoming visible from FY16

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 14

Witnessing A Financial Turnaround

Witnessing a turnaround, growth to sustain for at least two years

Tigerair’s focus on capacity discipline, either through the disposal or sub-leasing of surplus aircraft, has started to pay off. Evidence of this was visible in the last three quarters.

On a full-year basis, the airline has been reporting operating losses for the past two financial years. However, the airline reported operating income of SGD4.1m in 3QFY15, followed by a marginal operating loss of SGD2.3m in 4QFY15 and an operating income of SGD600,000 in 1QFY16. This was in sharp contrast with operating losses of SGD8.8m-24.2m during the same quarters a year ago.

While we expect 2QFY16 to be a weak quarter due to seasonality, we estimate for the airline to return to full-year profitability with operating incomes of SGD31m and SGD65m in FY16 and FY17 respectively.

As most one-time charges have already been booked by the airline during the precious financial years, we expect the operating income to translate into a positive PATMI of SGD22 in FY16. FY16 could be the first profitable year for Tigerair after consecutive years of losses. Consensus estimates are even more bullish, with street expecting the carrier to report a profit of SGD36m in FY16.

Figure 25: After a series of volatile quarters, Tigerair's quarterly EBITDAR has stabilised above SGD25m

Figure 26: Tigerair should witness strong improvement in EBITDAR

Title:

Source:

Please fill in the values above to have them entered in your report

14.7 16.2

44.7

40.4

22.8

8.9

14.2

0.1

10.1

(2.0)

28.0 29.4 30.0

(10.0)

-

10.0

20.0

30.0

40.0

50.0

1QFY13 3QFY13 1QFY14 3QFY14 1QFY15 3QFY15 1QFY16

EBITDAR (SGDm)

Title:

Source:

Please fill in the values above to have them entered in your report

25.6

62.6

13.3

96.4

122.3

9.7

116.1

46.0

65.6

152.3

192.1

212.9

-

50.0

100.0

150.0

200.0

250.0

FY07 FY09 FY11 FY13 FY15 FY17

EBITDAR (SGDm)

Source: Company data, RHB Source: Company data, RHB

Figure 27: FY14 and FY15 were the years of kitchen sinking Figure 28: Tigerair should report profit in FY16 after four consecutive years of losses

Title:

Source:

Please fill in the values above to have them entered in your report(13.7)(18.3)

2.0

(15.4)

(32.8)

23.8

(118.5)

(95.5)

(65.2)

(182.4)

2.2

(18.8)

(1.7)

(200.0)

(150.0)

(100.0)

(50.0)

-

50.0

1QFY13 3QFY13 1QFY14 3QFY14 1QFY15 3QFY15 1QFY16

PATMI (clean) (SGDm)

Title:

Source:

Please fill in the values above to have them entered in your report

(14.8)

9.9

(50.8)

28.2 39.9

(98.8)

(45.4)

(223.0)

(264.2)

21.8

55.0 65.1

(300.0)

(250.0)

(200.0)

(150.0)

(100.0)

(50.0)

-

50.0

100.0

FY07 FY09 FY11 FY13 FY15 FY17

PATMI (clean) (SGDm)

Source: Company data, RHB Source: Company data, RHB

Consensus estimates are even more bullish and street expects Tigerair to report a profit of SGD36m in FY16

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 15

We expect Tigerair to sustain strong earnings growth for at least two years, before the risks related to the overcapacity issue arising from addition of new A320neos and the return of aircraft from Indigo starts impacting yields and load factor.

Re-capitalised balance sheet with a strong shareholder

Tigerair has undertaken multiple rights share issues over the past 5-6 years, raising a total of about SGD675m. The latest rights share issue was undertaken in 2014, which helped to raise SGD27m and ensured that the airline had sufficient balance sheet strength to keep looking at selected growth opportunities in terms of network expansion. As at end 1QFY16, Tigerair has a total cash balance of SGD300m and a net cash position of SGD2.2m. As the group starts reporting positive earnings from FY16 and keeps growing its EBITDA, we expect the airline to gradually grow its net cash position to SGD116m by end FY16.

Figure 29: Aided by strong turnaround in operations, we expect Tigerair's EBITDA to witness strong growth

Figure 30: Tigerair should return to a strong net cash position in the next 2-3 years

Title:

Source:

Please fill in the values above to have them entered in your report

(13.5)

8.0

(47.4)

26.6

59.9

(52.0)

41.3

(17.9)

(3.0)

72.9

108.0 119.3

(80.0)

(60.0)

(40.0)

(20.0)

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

FY07 FY09 FY11 FY13 FY15 FY17

EBITDA (SGDm)

Title:

Source:

Please fill in the values above to have them entered in your report

31 6 88 5 345 423 397 188

(3) (116)(196)(296)

-58%

-15%

-80%

3%

177%170%

200%

68%

-1%

-46%-64%

-80% -100%

-50%

0%

50%

100%

150%

200%

250%

(400.0)

(300.0)

(200.0)

(100.0)

0.0

100.0

200.0

300.0

400.0

500.0

FY07 FY09 FY11 FY13 FY15 FY17

Net debt/(cash) (SGDm) Net debt or (net cash)/equity %

Source: Company data, RHB Source: Company data, RHB

SIA’s shareholding in Tigerair was diluted to 32.7% post the LCC’s IPO in 2010. The former had earlier held a 49% stake in the latter. In 2013, SIA increased its stake in Tigerair to 40% following the acquisition of 7.3% stake from Temasek Holdings for SGD49m. In Dec 2014, SIA converted 189m of its perpetual securities, raising its stake in Tigerair to 55.8% from the aforementioned 40%, thereby becoming the single largest shareholder of Tigerair. We had earlier, in this note, highlighted the operational and commercial benefits of having SIA as the single-largest shareholder of Tigerair.

A quick history of Tigerair’s capital raising activity:

In 2011, Tigerair issued 273.2m new shares a part of a right share issue that raised gross proceeds of SGD158m. Each rights share was priced at SGD0.58, on the basis of one rights share for every two existing ordinary shares.

In 2013, the airline completed a rights issue and issued 164.2m new shares, raising SGD76m in gross proceeds. The right issue was priced at SGD0.47 for each rights share, on the basis of one rights share for every five ordinary shares.

In 2013, Tigerair also completed a non-renounceable preferential offering and issued 205.3m perpetual convertible securities for a net proceed of SGD218m. The perpetual convertible securities holders had the right to convert their securities into ordinary shares of the company. They also had the right to received ordinary distribution of 2% pa for the first five years.

In 2014, Tigerair announced a renounceable non-underwritten rights issue. Existing shareholders were given the opportunity to subscribe for 85 rights shares for every 100 existing shares at an issue price of SGD0.20. The completion of the rights issue led to an issuance of 1,147m rights shares and helped the airline to raise SGD227m.

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 16

Costs to increase if SGD continues to weaken against the USD

We estimate that at least 60% of Tigerair’s costs are denominated in USD. These include fuel, and aircraft rental and maintenance costs. However, by comparison, as the airline largely operates out of a Singapore hub, the majority of its revenue remains denominated in SGD. As the group reports its financials in the local currency, a weakening of SGD against the USD would further push up costs and could impact its earnings recovery.

Figure 31: The impact of a weaker-than-estimated SGD against the USD

FY16 FY17

USDSGD x 1.40 1.43

PATMI SGDm 21.8 55.0

Aditional 1% weakening SGD 1.41 1.44

Revised PATMI SGDm 19.0 50.6

% change % -13% -8%

Source: RHB

Although we believe our exchange rate assumptions for the SGD against the USD are already quite conservative, we estimate that an additional 1% weakening in the SGD against the greenback would lower our FY16 and FY17 earnings by 13% and 8% respectively. We think that the actual impact might be smaller than our estimate, though, as some of Tigerair’s revenue is denominated in USD while we have assumed all revenue to be denominated in SGD. In addition, the group hedges its USD exposure, but does not publically disclose the hedged price for the SGD against the greenback.

Rise in jet fuel prices could also throw Tigerair off its recovery track

We expect crude oil prices and, hence, the price of jet fuel, to stabilise at around the current levels for rest of the year and to decline further next year. Our regional oil and gas analyst expects crude oil price (Brent) to average at USD53.30/bbl for 2015, and USD50/bbl for 2016. In line with this, we estimate for jet fuel prices (after taking into account the hedge positions) for Tigerair to average at SGD94/bbl (USD67.2/bbl) in FY16 and SGD89.2/bbl (USD62.6/bbl) in FY17.

Our underlying estimation of a turnaround in Tigerair’s fortunes in FY16 is strongly rooted in oil prices remaining low. This is mainly because fuel accounts for 40% of the airline’s total cost. In addition, the group has hedged 40% of its next 15 month’s fuel requirement at USD87/bbl (estimated USD122/bbl). Hence, a sharp rebound in jet fuel prices could throw Tigerair off its strong earnings recovery track. While a 5% rise in jet fuel price from our underlying assumption would lower the airline’s FY16 and FY17 profits by 28% and 10% respectively, we would like to highlight that Tigerair would still continue to remain profitable, albeit with smaller profits. This is thanks to strong improvements in its capacity discipline and operational capabilities.

Figure 32: The impact of higher jet fuel prices

FY16 FY17

Jet fuel price SGD per barrel 94.0 89.2

PATMI SGDm 21.8 55.0

5% rise in jet fuel price 98.7 93.7

Revised PATMI SGDm 15.6 49.4

% change % -28% -10%

Source: RHB

Revised aggressive depreciation policy to help keep the fleet young

Tigerair announced that, at the end of FY15, it changed its accounting policies for the depreciation and maintenance of aircraft. The airline also made changes to the estimated residual value of its aeroplane fleet. The useful life of an owned aircraft was shortened to 15 years (from 23) while the residual value was adjusted to 10% of the original cost (from 15% previously). Tigerair also reassessed and reviewed the provisions for maintenance expenses at a leased aircraft’s return. Although the change in the accounting policies are likely to lead to higher annual costs moving forward, we believe the changes ought to ensure that the airline remains competitive against its regional peers by operating a relatively young and fuel-efficient aircraft fleet.

We think that the actual impact might be smaller than our estimate. This is because some revenue is denominated in USD and, although Tigerair hedges its greenback exposure, it does not publically disclose the hedge price

Tigerair can still generate positive EPS in FY16 if jet fuel prices increase 5% in SGD terms

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 17

A Quick Comparison With Regional LCCs

Figure 33: Available seat capacity measured (in bn km) Figure 34: Load factor comparison among ASEAN LCCs

Title:

Source:

Please fill in the values above to have them entered in your report28

33 35

37 40

41

10 13

15

18 21

23

3 4 5 6 7 7

10 13 13

12 12 12

-

5

10

15

20

25

30

35

40

45

FY12 FY13 FY14 FY15F FY16F FY17F

AirAsia Asia Aviation Nok Air Tigerair

Title:

Source:

Please fill in the values above to have them entered in your report

80%80%

79% 79%79%

80%

82%

84%

81%81%

80%

81%

84% 84% 81% 82% 83% 83%

81%

84%

79%

82%

84%

85%

74%

76%

78%

80%

82%

84%

86%

FY12 FY13 FY14 FY15F FY16F FY17F

AirAsia Asia Aviation Nok Air Tigerair

Source: Company data, RHB Source: Company data, RHB

Company Background Tigerair is a LCC based in Singapore. It was originally founded on 12 Dec 2003 by a consortium that included SIA, Indigo Partners, Irelandia Investments and Temasek Holdings. The group formerly held sizeable majority and minority stakes in a number of Tigerair branded JVs in the Philippines, Indonesia and Australia. As these overseas JVs had been pulling down Tigerair’s performance for several years, the group has withdrawn from such ventures, choosing instead to consolidate its airline operations in Singapore. It has even dropped its regional expansion strategy. Today, Tigerair is majority owned by SIA (56%) and the LCC only holds a minority (10%) stake in Tigerair Taiwan, where China Airlines is the JV partner. The stock has been listed on the Singapore Exchange since 22 Jan 2010.

Tigerair operates two narrow body aircraft types, the Airbus A319 and A320, offering single class economy seating of 144 and 180 seats respectively. As at end 1QFY16, the group operates a fleet of 25 aircraft, of which 23 A320s and one A319 are in operation while one A319 is stored, but would be put into service in the current financial year.

Figure 35: Tigerair's revenue split in FY15 Figure 36: Tigerair’s aircraft fleet details

Title:

Source:

Please fill in the values above to have them entered in your report

Passenger revenue

77%

Ancillary revenue

22%

Lease rental income

1%

Aircraft In fleet Firm orders Options Passengers

per aircraft

Airbus A319 2 - - 144

Airbus A320ceo 23 - - 180

Airbus A320neo - 39 11

Total 25 39 11

Source: Company data, RHB Source: Company data, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 18

Figure 37: Tigerair’s Top 10 shareholders Figure 38: Tigerair’s key management personnel

Shareholder name % holding

SIA 55.8%

Vanguard Group 0.5%

Low Check Kian 0.3%

Blackrock 0.3%

Teachers Advisors 0.2%

Norges Bank 0.1%

State Street 0.0%

Hsieh Fu Hua 0.0%

Charles Schwab 0.0%

Chin Sak Hin 0.0%

Name Designation Experience in industry

Lee Lik Hsin CEO Previously: SIA Cargo

president and SIA senior

vice president corporate

planning

Vanessa Lau Man Yee CFO Previously: Brightoil

Petroleum oil tanker

business CFO and NOL

group financial controller

Ho Yuen Sang COO 20 years of experience in

the aviation sector

Mui Chee Wai Director: planning Previously: vice president

talent management and

development at SIA

Tommy Ng Yew Chye Director: human resource Over 30 years of experience

Teh Yik Chuan Director: sales & marketing Nine years with SIA in a

variety of functions

David Liew Director: corporate services 43 years of working

experience Source: Bloomberg, RHB Source: Company, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 19

Appendix 1 - Tigerair’s Route Map

Figure 39: Tigerair’s current destinations (either on its own network or via partner airlines Cebu Pacific and Scoot)

Note: As at 17 Aug 2015

Source: Company, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 20

Appendix 2 - Tigerair’s Flight Departures From Singapore

Figure 40: Tigerair's flight departures from its Singapore hub

Country City Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Bangladesh Dhaka 1.0 1.0 1.0 1.0 1.0 1.0 1.0 7.0

China Guangzhou 2.0 2.0 2.0 2.0 2.0 2.0 2.0 14.0

China Guilin - - - - - 1.0 - 1.0

China Haikou - 1.0 - - - 1.0 - 2.0

China Nanning 1.0 - - - - 1.0 - 2.0

China Ningbo - 1.0 - - - 1.0 - 2.0

China Quanzhou 1.0 - - 1.0 - 1.0 - 3.0 Starting on 28 Sep 2015

China Shenzhen 1.0 1.0 1.0 - 1.0 1.0 - 5.0

China Xi An 1.0 1.0 - 1.0 1.0 1.0 - 5.0

Hong Kong Hong Kong 2.0 3.0 3.0 3.0 3.0 2.0 3.0 19.0

India Bangalore 1.0 1.0 1.0 1.0 1.0 1.0 1.0 7.0

India Chennai 2.0 1.0 2.0 2.0 2.0 1.0 1.0 11.0

India Hyderabad - 1.0 - - 1.0 1.0 1.0 4.0

India Kochi 1.0 - 1.0 - 1.0 - 1.0 4.0

India Lucknow - 1.0 - 1.0 - - 1.0 3.0 Starting on 3 Dec 2015

India Trichy 2.0 1.0 2.0 2.0 1.0 2.0 2.0 12.0

Indonesia Bali 2.0 2.0 2.0 2.0 2.0 2.0 2.0 14.0

Indonesia Jakarta 3.0 3.0 3.0 3.0 3.0 3.0 3.0 21.0

Indonesia Surabaya 1.0 - 1.0 1.0 1.0 - 1.0 5.0

Macau Macau 1.0 1.0 1.0 2.0 1.0 1.0 2.0 9.0

Malaysia Ipoh 1.0 1.0 1.0 - 1.0 - 1.0 5.0

Malaysia Kuala Lumpur 3.0 2.0 2.0 3.0 5.0 3.0 5.0 23.0

Malaysia Langkawi - 1.0 - - 1.0 - 1.0 3.0

Malaysia Penang 2.0 1.0 1.0 2.0 3.0 2.0 3.0 14.0

Maldives Male 1.0 - 1.0 - 1.0 - 1.0 4.0

Myanmar Yangon 1.0 - 1.0 - 1.0 1.0 1.0 5.0

Philippines Cebu 1.0 - - - - - - 1.0

Philippines Clark - 1.0 - 1.0 1.0 1.0 1.0 5.0

Philippines Kalibo 1.0 - 1.0 - 1.0 - 1.0 4.0

Philippines Manila 2.0 2.0 2.0 2.0 2.0 2.0 2.0 14.0

Taiwan Taipei 2.0 1.0 1.0 1.0 1.0 2.0 1.0 9.0

Thailand Bangkok 5.0 5.0 5.0 5.0 5.0 5.0 5.0 35.0

Thailand Chiang Mai - 1.0 - 1.0 - 1.0 - 3.0

Thailand Hat Yai 1.0 1.0 1.0 1.0 1.0 1.0 1.0 7.0

Thailand Krabi 1.0 1.0 1.0 1.0 1.0 1.0 1.0 7.0

Thailand Phuket 2.0 1.0 1.0 2.0 3.0 2.0 3.0 14.0

Vietnam Hanoi - 1.0 - - 1.0 1.0 1.0 4.0

Vietnam Ho Chi Minh City 3.0 2.0 2.0 2.0 4.0 3.0 4.0 20.0

48.0 42.0 40.0 43.0 53.0 48.0 53.0 327.0

Note: As at 31 Aug 2015

Source: RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 21

Appendix 3 – History Of (Failed) Overseas Expansions

Overseas expansions gone sour

Tigerair Australia. Tigerair Australia was formed as an Australian affiliate of Tigerair.

In Feb 2007, the group announced its intention to become Australia’s third full-scale domestic airline, competing with Virgin Australia and Qantas/Jetstar. Following the receipt of approval in Mar 2007, Tigerair Australia commenced operations in Nov 2007.

In 1QFY12, operations were marred by the ash cloud from Chile’s Puyehue-Cordón Caulle volcano, which disrupted Australian domestic air travel. This was followed by the 6-week suspension of Tigerair Australia’s operations by the Civil Aviation Safety Authority of Australia (CASA) between 2 Jul 2011 and 11 Aug 2011. Post removal of this suspension, Tigerair Australia reduced operations as it built up services at a measured pace. With the consolidation of operations into a single base at Tullamarine Airport (also known as Melbourne Airport), bases at Avalon Airport (one of Melbourne’s four airports) and Adelaide Airport (Adelaide) were closed.

Figure 41: Australian operations were hit badly in 2011 following a volcanic eruption in Chile and a 6-week suspension of services

Figure 42: While flight services resumed and grew following the disruptions in 2011, operations remained financially unviable

Title:

Source:

Please fill in the values above to have them entered in your report

0

50

100

150

200

250

300

350

400

450

0

50

100

150

200

250

300

350

May-11 Nov-11 May-12 Nov-12 May-13 Nov-13 May-14

Passengers booked ('000) - LHS

Revenue passenger kilometres (RPK) (m passenger km)

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

May-11 Dec-11 Jul-12 Feb-13 Sep-13 Apr-14

Available seat capacity (ASK) (m km)

Passenger load factor (RPK/ASK) (%)

Source: Company data, RHB Source: Company data, RHB

In 2012, in light of infrastructure constraints at Tullamarine Airport (and with an intention to develop its network), Tigerair Australia opened a base in Sydney. It also worked with Tullamarine Airport on airport expansion plans to cater for growth out of Melbourne.

However, the group’s Australian operations had always struggled to become financially viable. Therefore, in Jul 2013, Tigerair completed the sale of 60% of Tigerair Australia to Virgin Australia for a cash consideration of AUD35m. Accordingly, Tigerair Australia ceased to be a subsidiary of the group and became a JV instead. A gain on loss of control of subsidiary – which amounted to SGD106.1m – was recorded in the profit and loss statement on the date of divestment.

Amidst continuing difficulties in managing its Australian operations, Tigerair finally divested the balance 40% holding in Tigerair Australia to Virgin Australia in February 2015. Virgin Australia acquired the group’s 40% stake for a cash consideration of AUD1. With this, Tigerair Australia ceased to be a JV for the group. A loss on disposal of JV amounting to SGD37.1m was recorded in the profit and loss statement during the year. As a part of the deal, Virgin Australia would retain the Tigerair name and acquire the brand rights for Tigerair to operate to some international destinations from Australia. Going forward, the group continues to earn franchising income from Tigerair Australia.

Tigerair Mandala. Tigerair Mandala (formerly Mandala Airlines) was a LCC

headquartered in Jakarta, Indonesia. It was an associate company of the group. A former full-service airline, it had repositioned itself as a budget airline/LCC following a year-long grounding in 2011 caused by debt woes.

Tigerair Australia was fully sold to Virgin Australia

Tigerair Mandala’s share of losses in FY13 was SGD8m, which increased to SGD56m in FY14

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 22

Mandala resumed operations in Apr 2012 following an injection of fresh capital by Indonesia’s Saratoga Investment Corp, which took an over 51% stake in the airline. Partner Tigerair took a 33% shareholding while the 16% balance was held by previous shareholders and creditors of Mandala.

Tigerair Mandala started operations in Apr 2012, with one domestic route between its home base in Jakarta and Medan, the capital of North Sumatra. This was followed by its first international destination when it launched the Medan-Singapore route in the same month. In May 2012, Tigerair Mandala flew to Kuala Lumpur from Jakarta.

In FY13, the group recognised its SGD8m in share of losses from Tigerair Mandala. The cumulative share of losses related to this associate amounted to SGD13.3m, as Tigerair’s share of losses had exceeded its net investment in Mandala. In FY14, the share of losses from Tigerair Mandala amounted to SGD56m.

Tigerair Mandala ceased all operations in Jul 2014 as it was not be able to sustain its operations and the airline’s key shareholders decided to cease funding the carrier. Before it ceased operations, Tigerair had a 35.8% stake in Tigerair Mandala.

Figure 43: Decline in number of passengers booked and RPK was in line with reduced capacity before Tigerair Mandala ceased operations

Figure 44: Amidst rising losses, Tigerair Mandala had started to gradually reduce capacity before it ceased operations in Jul 2014

Title:

Source:

Please fill in the values above to have them entered in your report

0

50

100

150

200

250

300

0

50

100

150

200

250

Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14

Passengers booked ('000) - LHS

Revenue passenger kilometres (RPK) (m passenger km)

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

450

Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14

Available seat capacity (ASK) (m km)

Passenger load factor (RPK/ASK) (%)

Source: Company data, RHB Source: Company data, RHB

Tigerair Philippines. Tigerair Philippines (formerly known as SEAir or South East

Asian Airlines) is a LCC headquartered in Manila, the Philippines. The airline was the Filipino affiliate of Tigerair. In 2006, although a deal was announced in which Tigerair would enter a commercial and operational tie-up with SEAir from Feb 2007, the plan was put into hiatus due to the unfavourable operating environment. Tigerair and SEAir revisited the partnership plan in 2010. In FY13, the group acquired a 40% equity interest in SEAir for a consideration of USD2.5m.

Since this acquisition, Tigerair Philippines has faced hurdles that hampered its expansion plans. Slots were not available at Manila’s Ninoy Aquino International Airport. The airline was also unable to gain traction in the Philippines market with a relatively small fleet of five aircraft. As the group did not foresee Tigerair Philippines turning profitable quickly with its small scale of operation, in Jan 2014, Tigerair entered into a strategic alliance with Cebu Pacific. As part of this alliance, Tigerair Philippines was divested to the latter.

This divestment exercise was completed in Mar 2014 and the group recorded a SGD29m loss on disposal of Tigerair Philippines. In FY13, Tigerair’s share of losses from Tiger Philippines amounted to SGD19m and the amount of losses remained unchanged in FY14.

Tigerair Philippines’ share of losses in FY13 and FY14 was SGD19m each. A loss of SGD29m was recorded on disposal of operations to Cebu Pacific

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 23

Overseas ventures that never took off

Incheon Tiger. In Nov 2007, while Tigerair was looking to expand its presence in the

region under its “cub strategy”, the group announced that it would be starting a South Korea-based budget airline. Incheon Tiger was to have been a JV between Tiger Airways and Incheon Metropolitan City, with flights to destinations in Japan, China, Mongolia and the Russian Far East. The airline was to have been based in South Korea's Incheon International Airport and planned to begin services by 2009. However, the project was abandoned in Dec 2008 due to the worsening global economic situation. Regulatory problems in South Korea were also quoted as one of the reasons behind Tigerair’s decision to abandon the project.

Thai Tiger. Tigerair and Thai Airways International (Thai Airways) (THAI TB,

TRADING BUY, TP: THB15.58) had signed a memorandum of understanding in Aug 2010 with the aim of starting up a Bangkok-based LCC JV that was expected to begin operations by the first quarter of 2011. Thai Airways and Tigerair had expected to own 51% and 39% respectively of the newly-formed airline, while Ryanthai Ltd would hold the remaining 10%. The group subsequently dropped its plan to set up the JV after failing to get the necessary investment approvals from the Thai Government. As a result, in Dec 2011, Thai Airways, Tigerair and Ryanthai decided not to proceed with the incorporation of Thai Tiger.

Regional partnerships that were later cancelled

SpiceJet (India). In Dec 2013, Tigerair announced a 3-year interline agreement with

SpiceJet Ltd, India’s preferred low fare airline, which paved the way for greater connectivity between flights operated by both carriers.

Starting from 1 Jan 2014, customers travelling on SpiceJet’s domestic network from 14 Indian cities could seamlessly connect through Hyderabad’s Rajiv Gandhi International Airport onto Tigerair’s Singapore-bound flights. In the same way, starting from 31 Jan 2014, Tigerair customers from Singapore were able to get easy access to SpiceJet’s wide domestic Indian network. The 14 Indian cities were Ahmadabad, Bhopal, Mumbai, Kolkata, Coimbatore, Delhi, Goa, Indore, Mangalore, Madurai, Pune, Rajahmundry, Tirupati and Visakhapatnam.

However, in less than a year of operations, Tigerair terminated this interline agreement in January. The tie-up with SpiceJet had ended earlier than expected, mainly because the group could not achieve the revenue target that it was seeking from the agreement.

Budget airline projects in South Korea and Thailand that never took off

A 3-year interline agreement with SpiceJet, an Indian LCC, was cancelled with a year as revenue targets were not met

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 24

Financial Exhibits

Profit & Loss (SGDm) Mar-14 Mar-15 Mar-16F Mar-17F Mar-18F

Total turnover 746 677 728 749 803

Gross profit 746 677 728 749 803

Gen & admin expenses - - (8) (7) (8)

Selling expenses (31) (24) (23) (22) (28)

Other operating costs (768) (693) (666) (655) (692)

Operating profit (52) (40) 31 65 75

Operating EBITDA (18) (3) 73 108 119

Depreciation of fixed assets (33) (37) (42) (43) (45)

Amortisation of intangible assets (1) (0) (0) - -

Operating EBIT (52) (40) 31 65 75

Net income from investments (95) (35) - - -

Other recurring income (80) (192) - - -

Interest income 6 2 1 2 2

Interest expense (11) (8) (10) (10) (10)

Pre-tax profit (232) (273) 23 57 67

Taxation 9 8 (1) (2) (2)

Profit after tax & minorities (223) (264) 22 55 65

Reported net profit (223) (264) 22 55 65

Recurring net profit (223) (264) 22 55 65

Source: Company data, RHB

Cash flow (SGDm) Mar-14 Mar-15 Mar-16F Mar-17F Mar-18F

Operating profit (52) (40) 31 65 75

Depreciation & amortisation 34 37 42 43 45

Change in working capital (100) 14 (7) 2 11

Other operating cash flow 27 16 0 - 0

Operating cash flow (91) 28 67 110 130

Interest received 6 2 1 2 2

Tax paid (0) (1) (1) (2) (2)

Cash flow from operations (86) 29 67 110 130

Capex (365) (41) (17) (20) (20)

Other investing cash flow 378 (12) 72 - -

Cash flow from investing activities 13 (53) 55 (20) (20)

Proceeds from issue of shares 292 223 (0) - -

Increase in debt (154) (53) (9) - -

Other financing cash flow (10) (7) (9) (10) (10)

Cash flow from financing activities 127 163 (19) (10) (10)

Cash at beginning of period 117 172 310 413 494

Total cash generated 54 139 103 80 100

Forex effects (0) 0 0 - 0

Implied cash at end of period 172 310 413 494 594

Source: Company data, RHB

Tiger Airways (TGR SP)

15 September 2015

See important disclosures at the end of this report 25

Financial Exhibits

Balance Sheet (SGDm) Mar-14 Mar-15 Mar-16F Mar-17F Mar-18F

Total cash and equivalents 172 310 413 494 594

Accounts receivable 115 30 27 28 29

Other current assets 22 103 28 28 28

Total current assets 309 443 468 549 651

Tangible fixed assets 570 454 428 405 380

Intangible assets 0 0 0 0 0

Total other assets 107 125 120 120 120

Total non-current assets 676 579 548 525 500

Total assets 986 1,022 1,016 1,074 1,151

Short-term debt 53 84 - - -

Accounts payable 158 116 114 116 128

Other current liabilities 112 141 117 117 117

Total current liabilities 324 340 230 233 245

Total long-term debt 307 223 298 298 298

Other liabilities 76 244 238 238 238

Total non-current liabilities 383 467 536 536 536

Total liabilities 707 807 766 769 780

Share capital 703 931 931 931 931

Retained earnings reserve (424) (715) (681) (625) (560)