Embed Size (px)

Citation preview

1

Term Research Project: Nike, Inc.

Shawn Rembecky

Montclair State University

Fundamentals of Accounting ACCT 204-21

Professor Patricia Villano, CPA

June 23, 2015

2

Table of Contents

Nike, Inc. Summary and Recommendation Letter………………………………….….…………….. 3

Introduction ..................................................................................................................... 4

Financial Statements ..................................................................................................... 6

Statement of Cash Flows .............................................................................................. 6

Income Statement ......................................................................................................... 8

Income Statement Horizontal Analysis ..................................................................... 8

Income Statement Vertical Analysis .......................................................................... 9

Balance Sheet ............................................................................................................. 12

Balance Sheet Horizontal Analysis ......................................................................... 12

Balance Sheet Vertical Analysis ............................................................................. 13

Financial Ratio Analysis .............................................................................................. 16

Liquidity ....................................................................................................................... 16

Solvency ..................................................................................................................... 17

Profitability .................................................................................................................. 18

Industry and Competitor Analysis .............................................................................. 20

Conclusion .................................................................................................................... 22

Appendix: Full Set of Nike, Inc. Financial Statements ............................................. 23

3

TO: Professor Patricia Villano, CPA

FROM: Shawn Rembecky

DATE: June 23, 2015

SUBJECT: Nike, Inc. Summary and Recommendation Letter

Over the last three decades, Nike, Inc. has established itself in America as the

unquestioned leader of the Textile - Apparel Footwear & Accessories industry. Nike’s

growing domestic success propelled the company to become an instantly recognized

brand internationally, competing with the likes of Adidas. Even with new competitors

nipping at their heels, Nike’s power and influence within the industry continues to grow.

Findings

The year 2014 saw continued solid performance by Nike across the board, as

evidenced by the company’s strong financial statements. An overview of Nike’s Income

Statement revealed Nike has experienced steady increases in revenue and net income

every year since 2012. Nike’s Statement of Cash Flows also showed the company is

paying significant dividends to its investors, a finding that was also supported by

fantastic Financial Ratios that measured Nike’s profitability.

Recommendations

Upon exploring the possibility of investing in Nike based on the company’s trends over

the last three years, it is highly recommended to Just Do It. Buy Nike stock. The

company’s financials reveal Nike has discovered a winning formula and plans to stick

with its bread and butter over the coming years: investing considerable capital into

developing their products and strategically pursuing athletic sponsorships.

4

Introduction

Bill Bowerman, a track and field coach, and Phil Knight, a middle-distance runner

who was enrolled in the University of Oregon, teamed up to found Nike in 1964. The

company was originally named Blue Ribbon Sports and operated as a distributor for the

Japanese shoemaker Onitsuka Tiger, which later became ASICS. The company

officially became Nike, Inc. in 1971 when Nike's first employee, Jeff Johnson, had the

idea to adopt the name from the Greek goddess of victory. Interestingly, the iconic Nike

swoosh was designed by Portland State University student Carolyn Davidson for just

$35. Quite the bargain. As compensation for her contribution to the company, Nike

awarded her stock many years later that is worth over $640,000 today.

A pivotal moment in the company’s history came in 1984 when Nike signed then-

rookie Michael Jordan to an endorsement deal and shortly after released his first

signature shoe, the Air Jordan. Originally, the NBA banned players from wearing the Air

Jordan, which drew a remarkable amount of publicity. In a crucial business decision to

continue promoting the shoe, Nike agreed to pay all of Jordan’s fines handed down by

the NBA. The decision proved to be the right one: as Jordan’s popularity and success

soared, Nike benefitted wonderfully from the partnership and quickly saw the value in

establishing athlete partnerships.Despite not playing professionally since 2003, Jordan

still reportedly earns $60 million annually in royalties from Nike, making him the athlete

with, by far, the biggest Nike endorsement deal in the history of the company. The year

2003 also marked the first time in the company’s celebrated history that international

sales exceeded domestic sales, pointing to a clear shift within the industry as Nike

continued to develop into a truly global brand.

5

Today, Nike is headquartered in Beaverton, Oregon, and prides itself on being

the “largest and most successful brand of shoes, sports equipment, clothing, controlling

more than 60% of the market, and becoming a pop culture icon.” Within the United

States, Nike has identified Under Armour as an up and coming competitor. Globally,

Nike has identified Adidas as their biggest competitor, another storied company with

deep roots in athletics. Not known for their nature to be complacent within the Textile -

Apparel Footwear and Accessories industry, Nike has always made it a point to stay

ahead of their competition by continuously pushing new products into the market. Nike

products have stretched beyond running shoes to apparel, to sports equipment, to

eyewear, and even to fitness tracking technology products such as the Nike+

SportWatch GPS, Nike+ Fuelband, and Nike+ Sportbrand, which have all been recently

introduced since the turn of the decade.

Nike also continues to thrive on corporate sponsorships ranging across American

sports including football and basketball, and international sports such as soccer, golf,

handball, and cricket. Identifying key star athletes and sponsoring entire professional or

college teams have contributed to building Nike’s brand and acquiring a greater

domestic and international market share of the industry. Within the Textile - Apparel

Footwear & Accessories industry, Nike has established themselves as a leader and

innovator that does not show any signs of letting up any time soon.

6

Financial Statements

Statement of Cash Flows

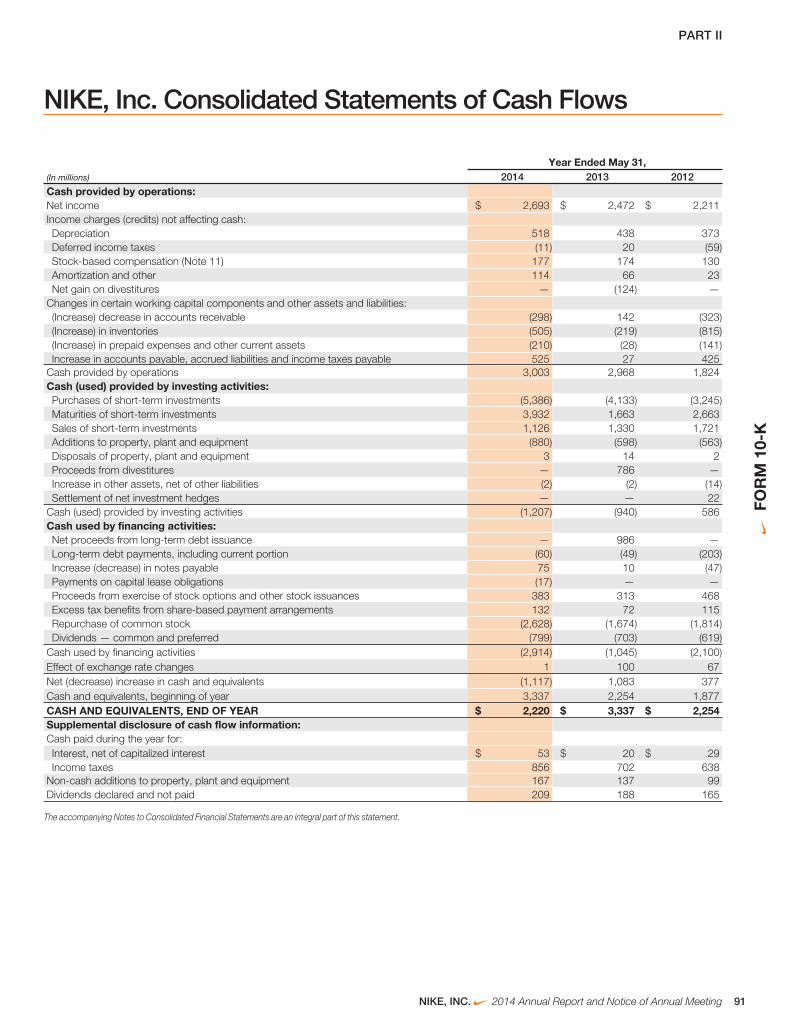

Nike’s Statement of Cash Flows is very telling of the company’s activities over

the last three years. Reviewing Nike’s operating activities, we see the company has

generated approximately $3 billion in cash from operating activities, which indicates that

Nike’s cash receipts from customers ($4 billion) exceeded their cash payments to

suppliers ($1 billion) in 2014. Glancing over Nike’s 2012 ($1.8 billion) and 2013 ($2.9

billion) numbers, we see that Nike has steadily increased its cash from operating

activities over the last three years, which tells us Nike is profitable and operating

efficiently. Aside from Net Income ($2.6 billion), the bulk of Nike’s cash inflows appear to

come from depreciation ($518 million) and accounts payable ($525 million). Observing

that depreciation has steadily increased over the years would suggest Nike is acquiring

more new assets faster than existing assets are reaching the end of their lifecycles. This

is promising considering Nike is capable of generating large gains. Increased accounts

payable from the previous year simply suggests Nike owes dues that it may be

expected to pay as early as 2015.

Examining Nike’s investing activities since 2012, we see Nike has gradually

spent more cash in its investments, accumulating $1.2 billion in 2014. The greatest cash

outflows came with Nike’s increase in purchases of short-term investments ($5.3 billion)

and additions to property, plant, and equipment ($880 million). We also see a noticeable

spike in cash inflows from maturities of short-term investments ($3.9 billion) in 2014,

signaling Nike has been wise with its short-term investments and is enjoying immediate

results from its successful decisions.

7

Lastly, we look at Nike’s financing activities, totaling $2.9 billion for 2014. Among

Nike’s financing activities from last year, two notable activities are Nike’s repurchasing

of common stock ($2.6 billion) and payment of dividends ($799 million). Foremost,

paying dividends is a positive sign for investors. More importantly, Nike has recorded

paying ever-increasing dividends over the last three years, which is very encouraging.

Nike’s decision to repurchase stock also helps investors because repurchasing stock

typically helps increase the value of stock. However, Nike’s repurchase of stock in 2014

far surpassed previous years ($1.6 billion in 2013, $1.8 billion in 2012), which

contributed to Nike’s expensive financing activities final balance.

Despite an increase in cash from operating activities, Nike’s steep cash outflows

from investing and financing activities resulted in its lowest end-of-year cash and

equivalents balance over the last three years. While this may sound daunting on the

surface, Nike actually received $986 million in net proceeds from long-term debt

insurance in 2013, something Nike did not receive in either 2014 or 2012. Removing this

one activity places Nike’s 2014 total right in the ballpark of its cash and equivalents

balances from recent years.

8

Financial Statements

Income Statement

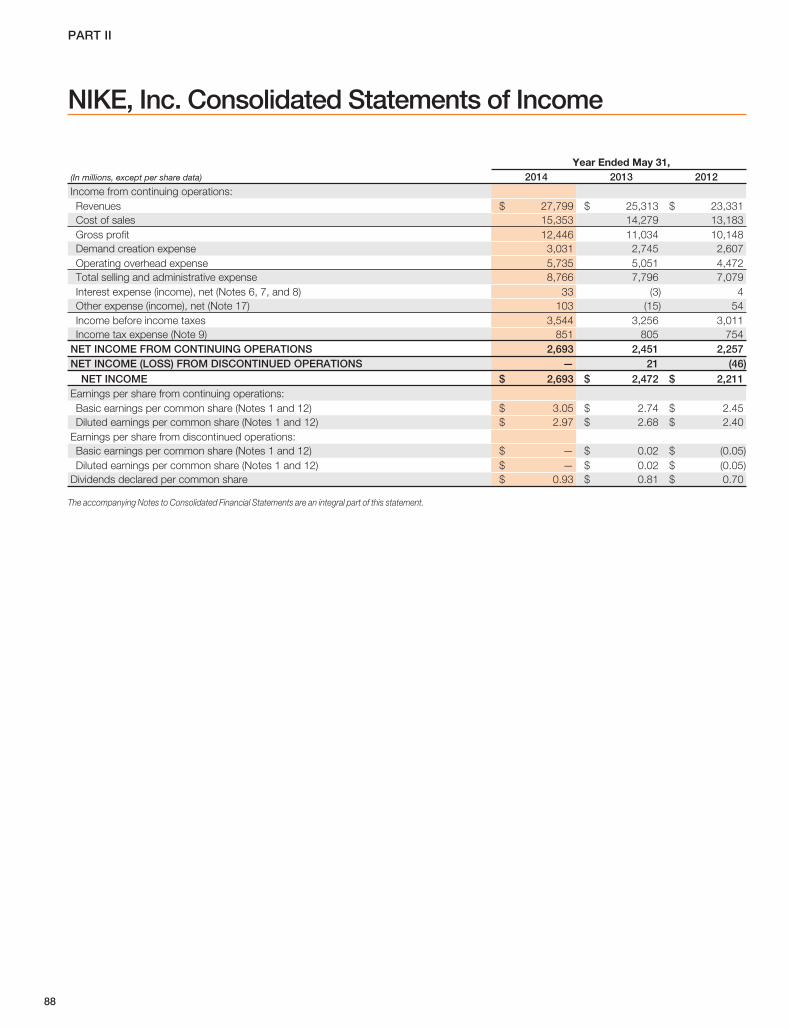

Nike’s 2014 Income Statement stands rather impressively. The company has

experienced increases in revenue and net income every year since 2012. In the

process, Nike managed to increase revenues while keeping cost of sales down,

resulting in a higher gross profit than the last two years. Of course, as more money

comes into the company, more money must go out to ensure the company continues to

run smoothly. As a result, Nike also experienced increased spending across all

expenses from previous years. These increases were necessary, yet it is important for

Nike to be mindful of their steadily growing expenses moving forward.

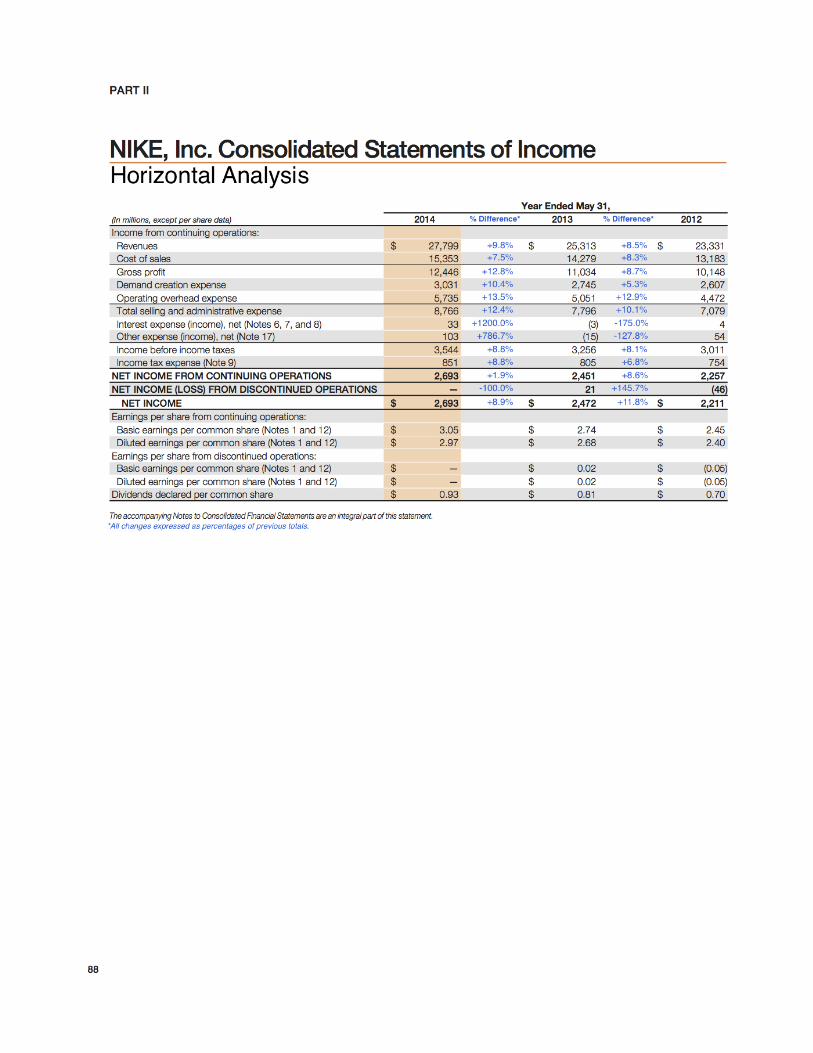

Income Statement Horizontal Analysis

Performing a Horizontal Analysis on Nike’s 2014 Income Statement is indicative

of Nike’s continued growth over the last few years. Right off the bat, we see that

although Nike’s revenue (+9.8%) and cost of Sales (+7.5%) have both increased since

2013, Nike’s revenue experienced greater growth, resulting in a noticeable spike in

gross profit (+12.8%). It is also encouraging to see Nike is willing to increase its demand

creation expense (advertising and promotion expenses, including costs of endorsement

contracts) by +5.3% in 2013 and an additional +10.4% in 2014. These increases show

Nike is sticking with its commitment to creative marketing, one of its tried-and-true

business strategies that it executes to near perfection and sets Nike apart from its

competitors. We also see total selling and administrative expenses increased from 2012

to 2013 (+10.1%) and again from 2013 to 2014 (+12.4%), in large part due to the

aforementioned demand creation expense. While Nike’s net income increased each

9

year over the last three years, the company experienced its greatest rise from 2012 to

2013 (+11.8%) and another significant boost from 2013 to 2014 (+8.9%).

Income Statement Vertical Analysis

A Vertical Analysis of Nike’s 2014 Income Statement tells a slightly different story

about Nike’s numbers and sheds an interesting light on the company’s financial

responsibility. Comparing numbers from the last three years, Nike has remained

relatively consistent with its allocation of resources. Cost of sales have hovered around

55%-56% of sales, while gross profit has hovered around 43%-44% of sales. The same

holds true for Nike’s demand creation expense (10%-11%), operating overhead

expense (19%-20%), total selling and administrative Expense (30%-31%), and even net

income (9%). Nike’s consistency is indicative of the company’s structure. This Vertical

Analysis perfectly illustrates that Nike is not a company to make questionable or

unpredictable decisions with their resources, which is yet another promising sign for

potential investors.

Trends over the last three years indicate Nike is doing a better job of keeping

cost of sales down and maximizing its gross profit. We also see that, although Nike is

spending more on demand creation expense, it is still in proportion to being a

percentage of sales as it was in previous years. Likewise, Nike’s net income has also

steadily increased in total dollar amount, but still only accounts for just fewer than 10%

of total sales. It would appear as though Nike is not taking a larger piece of the pie, but

rather the entire pie itself is simply growing in size.

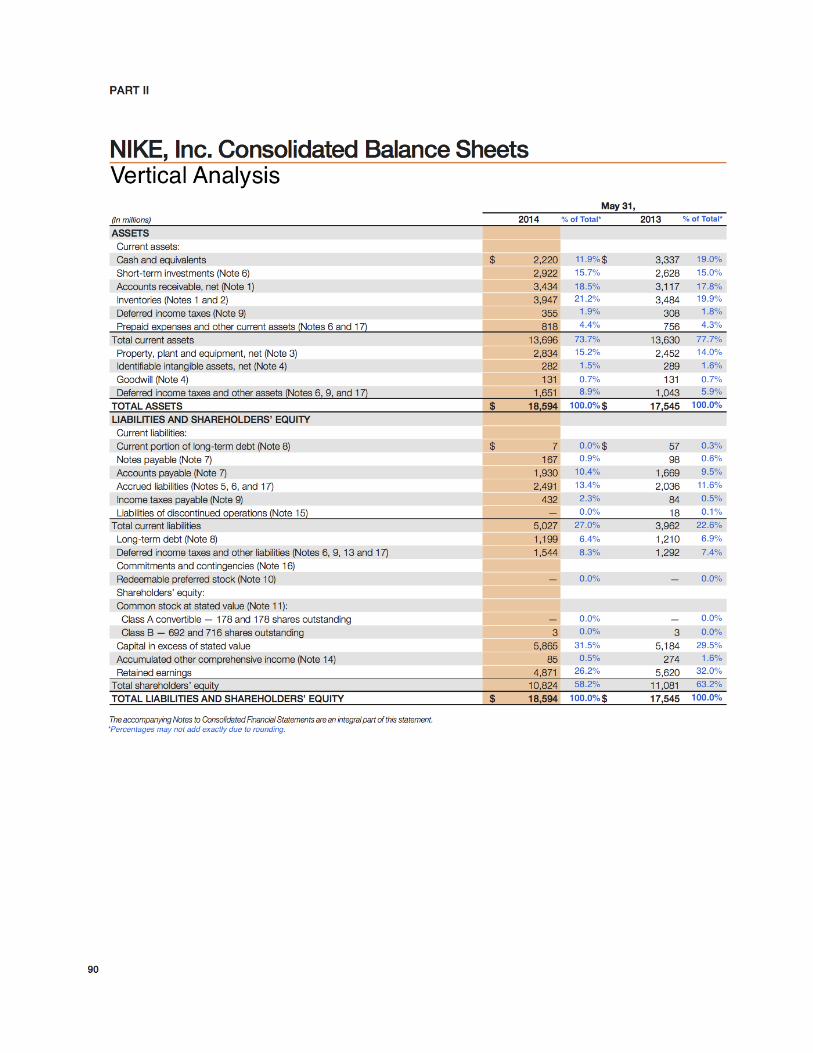

12

Financial Statements

Balance Sheet

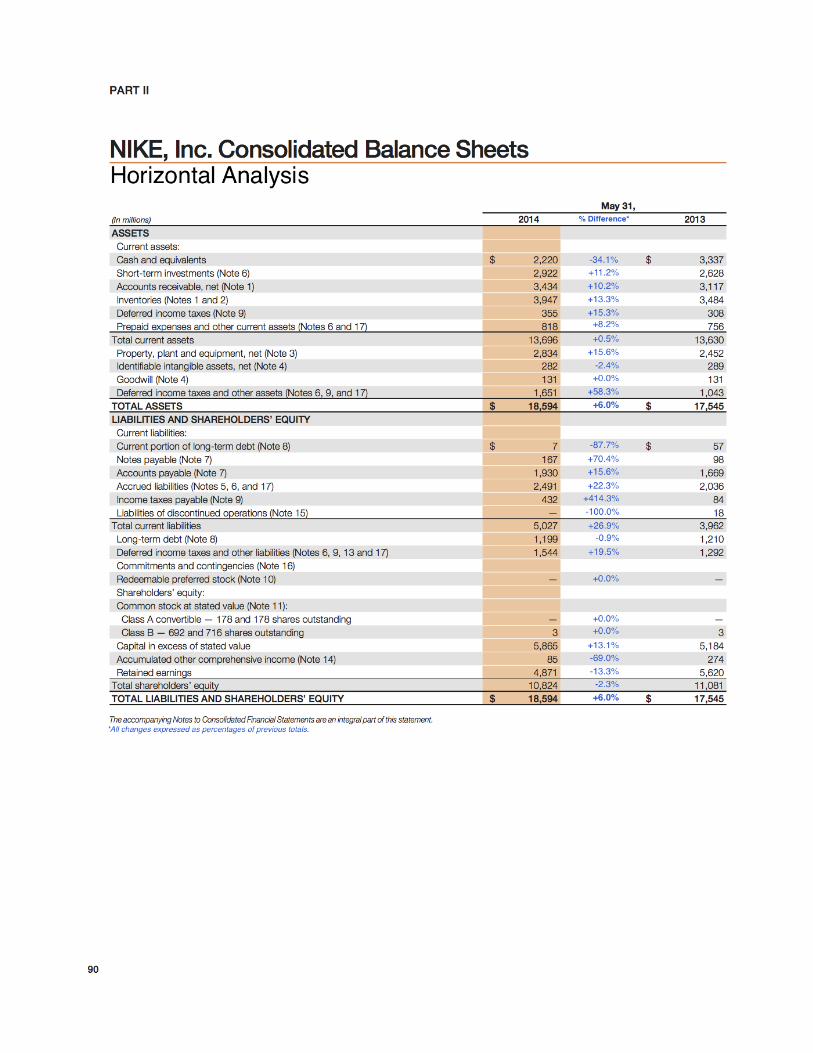

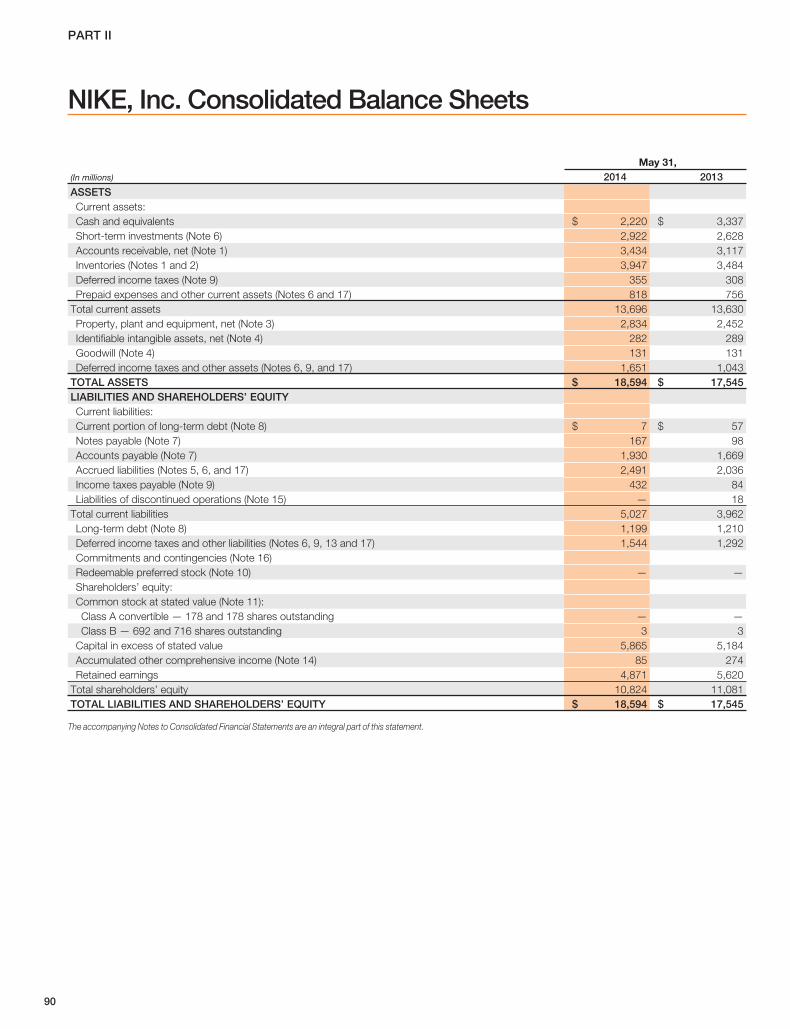

An overview of the Assets portion of the 2014 Balance Sheet reveals that,

despite experiencing a massive hit to the cash and equivalents account to the tune of

$1.117 billion, Nike still managed to grow their other assets and finish 2014 with a $66

million increase in total current assets from the previous year. It is also worth noting the

jump in property, plant, and equipment, which is likely a result of Nike spending more on

manufacturing equipment, or expanding their brick and mortar presence across the

world.

Most of Nike’s drastic changes from the previous year appear in the Liabilities

and Stockholder’s Equity portions of the 2014 Balance Sheet. Nike’s retained earnings

fell $749 million from 2013 to 2014. That decrease in retained earnings is likely a direct

result of the substantial repurchase of common stock and heftier dividends paid out to

investors, which was previously mentioned in the analysis of Nike’s Income Statement.

The decrease in retained earnings from the previous year also represents lost capital

Nike will be without when making future business decisions.

Balance Sheet Horizontal Analysis

Conducting a Horizontal Analysis on Nike’s 2014 Balance Sheet reveals some

noteworthy findings. Nike experienced a -34.1% difference in cash and equivalents from

its 2013 total and only a +0.5% increase in total current assets over that same

timespan. Among the biggest increases in Nike’s Assets came from deferred income

taxes and other assets (+58.3%), property, plant, and equipment (+15.6%), and

inventories (+13.3%). An increase in inventories may prove troublesome if Nike finds

the task of moving older inventory too difficult. It is possible that Nike is currently

13

collecting obsolete inventory, and the company may be forced to recognize it as a loss

in the future.

Meanwhile, total current liabilities experienced a +26.9% jump and total

stockholder’s equity fell -2.3% from the previous year. Major changes to this portion of

the Balance Sheet came from income taxes payable (+414.3%), notes payable

(+70.4%), accumulated other comprehensive income (-69.0%), and current portion of

long-term debt (-87.7%). For a company of Nike’s size and wealth, experiencing such

drastic increases in accounts payable may not be as problematic as they actually seem.

It is worth noting Nike also has assets tied up in Accounts Receivable that significantly

outweigh total accounts payable. Of course, this only helps Nike if their debtors honor

their debts when Nike expects them to.

Balance Sheet Vertical Analysis

When performing a Vertical Analysis on Nike’s 2014 Balance Sheet, previous

concerns uncovered by the Horizontal Analysis no longer seem as significant. Once

again, Nike proves to be consistent with its financial allocation of resources. With the

exception of cash and equivalents, all Asset accounts as a percentage of total assets

appear to be relatively consistent with their corresponding calculated percentages from

2013. The Liabilities and Stockholder’s Equity portion of the Balance Sheet seems to tell

a similar story. Minor changes within each of the Liabilities and Stockholder’s Equity

accounts over the last two years shifted some of the weight from total stockholder’s

equity (63.2% in 2013 compared to 58.2% in 2014), onto total liabilities (22.6% in 2013

compared to 27.0% in 2014), but individual accounts as a percentage of total liabilities

and stockholder’s equity remain fairly unchanged.

16

Financial Ratio Analysis

Although reviewing Nike’s financial statements can offer great insight into the

productivity and growth of the company, conducting a Financial Ratio Analysis helps to

provide a more complete picture of Nike’s financial health. Here, we examine Nike’s

liquidity, solvency, and profitability by comparing 2014’s results against the company’s

performance in 2013. All definitions of the terms and ratios for this part of the analysis

were derived directly from our course textbook.

Liquidity

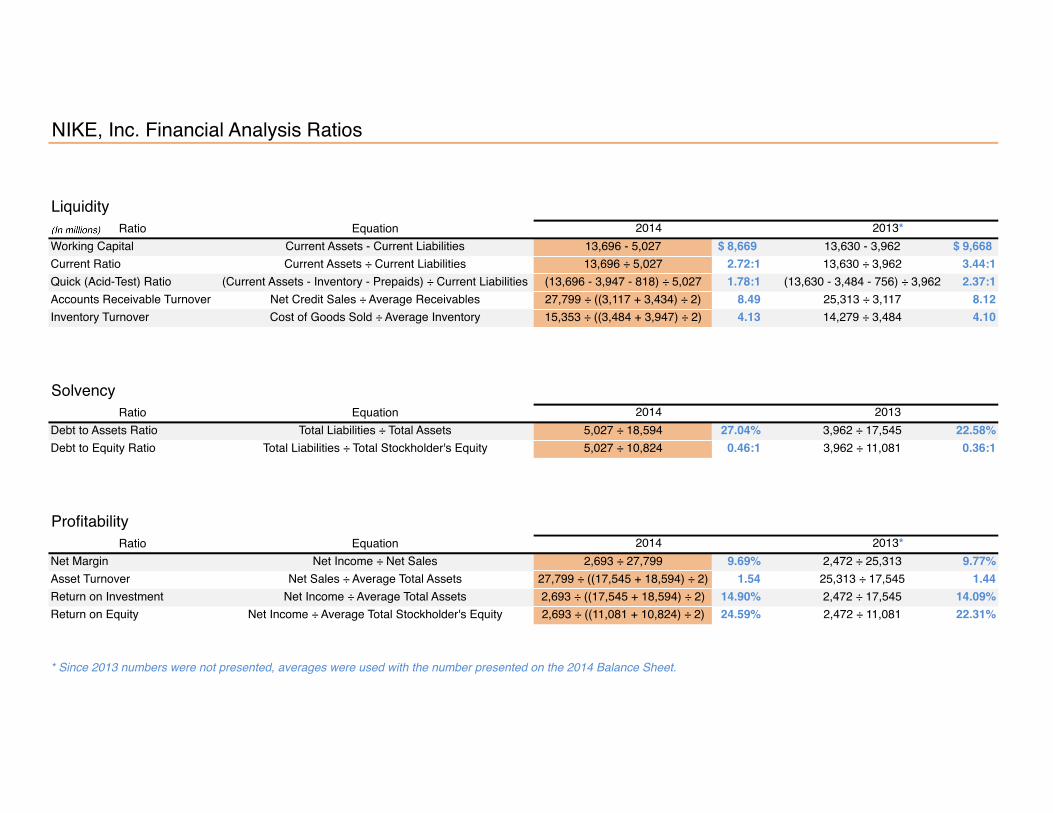

Liquidity indicates “a company’s ability to pay short-term debts.” First, we will

take a look at Nike’s working capital, which measures “the excess funds the company

will have available for operations.” In this case, Nike had a working capital of $9.6 billion

in 2013 and $8.6 billion in 2014. Alone, these numbers do not reveal much except that

Nike’s short-term debts should not exceed these totals. A more telling ratio is Nike’s

current ratio, which was 3.44:1 in 2013 and 2.72:1 in 2014. These are massively

impressive numbers, especially when considering the Dow Jones Industrial Average

was around 1.38:1. It would appear as though Nike realized its very strong working

capital position in 2013 and decided to use it to their advantage by investing more in its

factories and developing new products in 2014, resulting in a lower, but still strong,

current ratio than the year prior. Nike also recorded a strong quick ratio, which

measures “a company’s immediate debt-paying ability.” Nike’s quick ratio was 2.37:1 in

2013 and 1.78:1 in 2014. This decrease from 2013 to 2014 is driven by Nike’s decrease

in cash and equivalents and an increase in total current liabilities.

17

Next, we will examine Nike’s accounts receivable turnover, which measures

“how fast accounts receivable are turned into cash.” Nike experienced an 8.12 accounts

receivable turnover in 2013 and 8.49 in 2014, signaling that Nike made faster collections

in 2014 than in the year prior, but still not as fast as the Dow Jones Industrial Average.

Nike also recorded an inventory turnover not quite as fast as the Dow Jones Industrial

Average. Inventory turnover measures “the number of times, on average, that inventory

is totally replaced during the year.” Nike recorded a 4.10 inventory turnover rate in 2013

and 4.13 rate in 2014. Such a low turnover for Nike may seem perplexing considering

Nike has positioned itself in the apparel industry. However, it is worth mentioning that

Nike is also in the industry of selling sports equipment, which would not require such a

high inventory turnover rate because equipment such as footballs, basketballs, and

baseballs are not expected to change as drastically as apparel might over the years.

Solvency

Solvency analyzes a “company’s long-term debt-paying ability and its financing

structure.” We will begin by taking a look at Nike’s debt to assets ratio, which

measures the “percentage of a company’s assets that are financed by debt.” In 2013,

Nike’s debt to assets ratio was 22.58% and reached 27.04% by 2014. When compared

to the Dow Jones Industrial Average of 42%, Nike emerges as a financially strong

company due to its diminished reliance on liabilities. Nike’s debt to equity ratio also

proves to be strong. The debt to equity ratio “compares creditor financing to owner

financing.” Nike’s debt to equity ratio in 2013 was 0.36:1 and finished at 0.46:1 for 2014.

Again, Nike’s diminished reliance on liabilities also manages to show Nike is protected

against any likelihood of bankruptcy over the long-term.

18

Profitability

Profitability represents “a company’s ability to generate earnings.” An important

measure of profitability is net margin, which “describes the percent of each sales dollar

remaining after subtracting other expenses as well as cost of goods sold.” Nike’s net

margin was 9.77% in 2013 and 9.69% in 2014. Both are respectable numbers but still

below the Dow Jones Industrial Average of 12%. Nike could boost its net margin either

by increasing selling prices or by cutting down expenses. Another useful indicator of

profitability is the asset turnover ratio, which measures “how many sales dollars were

generated for each dollar of assets invested.” In 2013, Nike recorded an asset turnover

ratio of 1.44 and a ratio of 1.54 for 2014. It is reasonable to expect that Nike would have

a lower ratio because the company operates in an industry that relies on large

investments in plant and machinery to develop its products.

Nike’s return on investment proves to be a convincing indicator of the

company’s strong performance. Return on investment is “the ratio of wealth generated

(net income) to the amount invested (average total assets) to generate the wealth.” Nike

had a 14.09% return on investment in 2013 and a 14.90% return on investment in 2014,

well above the Dow Jones Industrial Average of 9%. Typically, higher return on

investments indicates better company performance. Nike’s return on equity is equally

as impressive. Return on equity measures “the profitability of the stockholder’s

investment.” In Nike’s case, investors enjoyed a sizeable 22.31% return on equity in

2013 and a 24.59% return on equity in 2014. These generous returns were sure to

please Nike investors over the last two years.

NIKE, Inc. Financial Analysis Ratios

Ratio EquationWorking Capital Current Assets - Current Liabilities 13,696 - 5,027 8,669$ 13,630 - 3,962 9,668$ Current Ratio Current Assets ÷ Current Liabilities 13,696 ÷ 5,027 2.72:1 13,630 ÷ 3,962 3.44:1Quick (Acid-Test) Ratio (Current Assets - Inventory - Prepaids) ÷ Current Liabilities (13,696 - 3,947 - 818) ÷ 5,027 1.78:1 (13,630 - 3,484 - 756) ÷ 3,962 2.37:1Accounts Receivable Turnover Net Credit Sales ÷ Average Receivables 27,799 ÷ ((3,117 + 3,434) ÷ 2) 8.49 25,313 ÷ 3,117 8.12Inventory Turnover Cost of Goods Sold ÷ Average Inventory 15,353 ÷ ((3,484 + 3,947) ÷ 2) 4.13 14,279 ÷ 3,484 4.10

Ratio EquationDebt to Assets Ratio Total Liabilities ÷ Total Assets 5,027 ÷ 18,594 27.04% 3,962 ÷ 17,545 22.58%Debt to Equity Ratio Total Liabilities ÷ Total Stockholder's Equity 5,027 ÷ 10,824 0.46:1 3,962 ÷ 11,081 0.36:1

Ratio EquationNet Margin Net Income ÷ Net Sales 2,693 ÷ 27,799 9.69% 2,472 ÷ 25,313 9.77%Asset Turnover Net Sales ÷ Average Total Assets 27,799 ÷ ((17,545 + 18,594) ÷ 2) 1.54 25,313 ÷ 17,545 1.44Return on Investment Net Income ÷ Average Total Assets 2,693 ÷ ((17,545 + 18,594) ÷ 2) 14.90% 2,472 ÷ 17,545 14.09%Return on Equity Net Income ÷ Average Total Stockholder's Equity 2,693 ÷ ((11,081 + 10,824) ÷ 2) 24.59% 2,472 ÷ 11,081 22.31%

2014 2013*

Liquidity

Solvency

Profitability

* Since 2013 numbers were not presented, averages were used with the number presented on the 2014 Balance Sheet.

2014 2013*

2014 2013

20

Industry and Competitor Analysis

Within the Textile - Apparel Footwear & Accessories industry, Nike has not been

shy about positioning itself as a premium brand when placing thick price tags on their

products throughout the years. Very telling of Nike’s brand power is the company’s

ability to price a running shoe at $225 running shoe, when there are plenty of shoes

available for under $100, and still manage to generate a profit. How is this possible?

Although a simple answer may not suffice for such a perplexing paradox, Nike has

greatly benefitted from being a steadfast company built on reliable, but not radical,

products and marketing ingenuity. Smart, sensible, strategic movements contribute to

shape Nike’s legacy today even as the company turned 50-years old just last year.

Nike has also built its empire on successfully managed athlete, team, and league

endorsements. Among Nike’s newest deals is an agreement with the NBA to replace

Adidas as the league’s official on-court apparel provider. Even more monumental is the

fact that Nike will become the first apparel company in league history to feature its logo

on player uniforms. The eight-year deal is for the 2017-18 season and is reportedly

worth at $1 billion, giving Nike an even greater hold on the globalized sports market.

David Carter, principal of The Sports Business Group, commented, “Adidas

made it clear months ago that it was going to shift from pursuing a league-wide deal to

signing more high-profile stars to endorsement contracts.” Adidas also admitted their

deal with the NBA was not as rewarding as it was expecting. However, Nike is expecting

a different result. Today, Nike accounts for 90% of basketball shoe sales in America and

also supplies apparel for USA Basketball and many different college programs

21

throughout the country. Nike is also well known for its partnership with Michael Jordan

and is expected to leverage that partnership during its tenure of supplying the NBA.

Adidas’s decision to forgo the NBA deal reveals a telling shift in Adidas’s

strategy. They are facing pressure from a new, formidable competitor: Under Armour.

Nike is currently the largest sportswear company in America. The second largest is

Under Armour, surpassing Adidas just last year. Like Adidas, Nike has identified Under

Armour as a force within the industry, and their corporate battles have spilled onto

countless playing fields.

Earlier this month, the country watched as the Golden State Warriors, led by

2015 NBA MVP Stephen Curry, defeated arguably the greatest player in the world,

LeBron James, and the Cleveland Cavaliers to capture the NBA Finals championship.

Although the Warriors were favored to win the championship, the matchup between

Curry and James had bigger implications in the sports business world: Nike sponsors

James, and Under Armour sponsors Curry. Historically, Nike has dominated sports

sponsorships, signing larger-than-life personalities among the likes of Michael Jordan,

Tiger Woods, and Kobe Bryant. Under Armour, on the other hand, has managed to

make some big sponsorship splashes as of late, and with relatively unknown athletes,

such as Curry and Masters champion Jordan Spieth who most recently won the U.S.

Open at Chambers Bay in Washington this past Father’s Day weekend.

While Under Armour continues to nip at Nike’s heels, Nike’s hold on the industry

does not appear to be loosening any time soon. Even with James losing to Curry in the

NBA Finals, one market research firm estimates James helped to produce $340 million

in basketball shoe sales for Nike in 2014.

22

Conclusion

Reviewing Nike’s Statement of Cash Flows revealed the company’s convincing

capacity to generate cash from operating activities, and Nike’s commitment to well-

calculated cash outflows for investing activities. Nike’s Income Statement also displayed

impressive growth in net income over the last three years. Performing Vertical Analyses

on Nike’s Income Statement and Balance Sheet spoke to the company’s ability to

maintain consistency with its finances and the overall stability of Nike. Among Nike’s

strongest financial ratios were the debt to assets ratio, debt to equity ratio, return on

investment, and return on equity, which proved Nike is far from bankruptcy and able to

provide substantial returns to its investors.

In addition to these valid points, it is also necessary to consider Nike’s innovative

company culture as another reason to invest. In 2013, Fast Company named Nike as

the most innovative company of the year. Bearing in mind physical activity is once again

gaining popularity in America, this “fitness craze” opens the doors for an innovative

company, such as Nike, to develop products that fulfill consumers’ needs for new

products, like wearable fitness tracking technology and exceptional high-performance

sports apparel. In the coming years, Nike is expected to capitalize on this phenomenon

with aggressive spending and fighting to acquire a larger global share of the industry.

Considering the strength of Nike’s financials and promising outlook for the future,

it is highly recommended to buy Nike stock – but only if you have the means. Nike is

currently traded on the New York Stock Exchange and its share price is listed at over

$105. If you do not consider the high valuation of the stock to be a roadblock, choosing

to invest in Nike would be a wise decision.

PART II

NIKE, Inc. Consolidated Statements of Cash Flows

Year Ended May 31,(In millions) 2014 2013 2012Cash provided by operations:Net income $ 2,693 $ 2,472 $ 2,211Income charges (credits) not affecting cash:Depreciation 518 438 373Deferred income taxes (11) 20 (59)Stock-based compensation (Note 11) 177 174 130Amortization and other 114 66 23Net gain on divestitures — (124) —

Changes in certain working capital components and other assets and liabilities:(Increase) decrease in accounts receivable (298) 142 (323)(Increase) in inventories (505) (219) (815)(Increase) in prepaid expenses and other current assets (210) (28) (141)Increase in accounts payable, accrued liabilities and income taxes payable 525 27 425

Cash provided by operations 3,003 2,968 1,824Cash (used) provided by investing activities:Purchases of short-term investments (5,386) (4,133) (3,245)Maturities of short-term investments 3,932 1,663 2,663Sales of short-term investments 1,126 1,330 1,721Additions to property, plant and equipment (880) (598) (563)Disposals of property, plant and equipment 3 14 2Proceeds from divestitures — 786 —Increase in other assets, net of other liabilities (2) (2) (14)Settlement of net investment hedges — — 22

Cash (used) provided by investing activities (1,207) (940) 586Cash used by financing activities:Net proceeds from long-term debt issuance — 986 —Long-term debt payments, including current portion (60) (49) (203)Increase (decrease) in notes payable 75 10 (47)Payments on capital lease obligations (17) — —Proceeds from exercise of stock options and other stock issuances 383 313 468Excess tax benefits from share-based payment arrangements 132 72 115Repurchase of common stock (2,628) (1,674) (1,814)Dividends — common and preferred (799) (703) (619)

Cash used by financing activities (2,914) (1,045) (2,100)Effect of exchange rate changes 1 100 67Net (decrease) increase in cash and equivalents (1,117) 1,083 377Cash and equivalents, beginning of year 3,337 2,254 1,877CASH AND EQUIVALENTS, END OF YEAR $ 2,220 $ 3,337 $ 2,254Supplemental disclosure of cash flow information:Cash paid during the year for:Interest, net of capitalized interest $ 53 $ 20 $ 29Income taxes 856 702 638

Non-cash additions to property, plant and equipment 167 137 99Dividends declared and not paid 209 188 165

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

NIKE, INC. 2014 Annual Report and Notice of Annual Meeting 91

FOR

M10

-K

PART II

NIKE, Inc. Consolidated Statements of Income

Year Ended May 31,(In millions, except per share data) 2014 2013 2012Income from continuing operations:Revenues $ 27,799 $ 25,313 $ 23,331Cost of sales 15,353 14,279 13,183Gross profit 12,446 11,034 10,148Demand creation expense 3,031 2,745 2,607Operating overhead expense 5,735 5,051 4,472Total selling and administrative expense 8,766 7,796 7,079Interest expense (income), net (Notes 6, 7, and 8) 33 (3) 4Other expense (income), net (Note 17) 103 (15) 54Income before income taxes 3,544 3,256 3,011Income tax expense (Note 9) 851 805 754

NET INCOME FROM CONTINUING OPERATIONS 2,693 2,451 2,257NET INCOME (LOSS) FROM DISCONTINUED OPERATIONS — 21 (46)

NET INCOME $ 2,693 $ 2,472 $ 2,211Earnings per share from continuing operations:Basic earnings per common share (Notes 1 and 12) $ 3.05 $ 2.74 $ 2.45Diluted earnings per common share (Notes 1 and 12) $ 2.97 $ 2.68 $ 2.40

Earnings per share from discontinued operations:Basic earnings per common share (Notes 1 and 12) $ — $ 0.02 $ (0.05)Diluted earnings per common share (Notes 1 and 12) $ — $ 0.02 $ (0.05)

Dividends declared per common share $ 0.93 $ 0.81 $ 0.70

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

88

PART II

NIKE, Inc. Consolidated Balance Sheets

May 31,(In millions) 2014 2013ASSETSCurrent assets:Cash and equivalents $ 2,220 $ 3,337Short-term investments (Note 6) 2,922 2,628Accounts receivable, net (Note 1) 3,434 3,117Inventories (Notes 1 and 2) 3,947 3,484Deferred income taxes (Note 9) 355 308Prepaid expenses and other current assets (Notes 6 and 17) 818 756

Total current assets 13,696 13,630Property, plant and equipment, net (Note 3) 2,834 2,452Identifiable intangible assets, net (Note 4) 282 289Goodwill (Note 4) 131 131Deferred income taxes and other assets (Notes 6, 9, and 17) 1,651 1,043

TOTAL ASSETS $ 18,594 $ 17,545LIABILITIES AND SHAREHOLDERS’ EQUITYCurrent liabilities:Current portion of long-term debt (Note 8) $ 7 $ 57Notes payable (Note 7) 167 98Accounts payable (Note 7) 1,930 1,669Accrued liabilities (Notes 5, 6, and 17) 2,491 2,036Income taxes payable (Note 9) 432 84Liabilities of discontinued operations (Note 15) — 18

Total current liabilities 5,027 3,962Long-term debt (Note 8) 1,199 1,210Deferred income taxes and other liabilities (Notes 6, 9, 13 and 17) 1,544 1,292Commitments and contingencies (Note 16)Redeemable preferred stock (Note 10) — —Shareholders’ equity:Common stock at stated value (Note 11):Class A convertible — 178 and 178 shares outstanding — —Class B — 692 and 716 shares outstanding 3 3

Capital in excess of stated value 5,865 5,184Accumulated other comprehensive income (Note 14) 85 274Retained earnings 4,871 5,620

Total shareholders’ equity 10,824 11,081TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY $ 18,594 $ 17,545

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

90

PART II

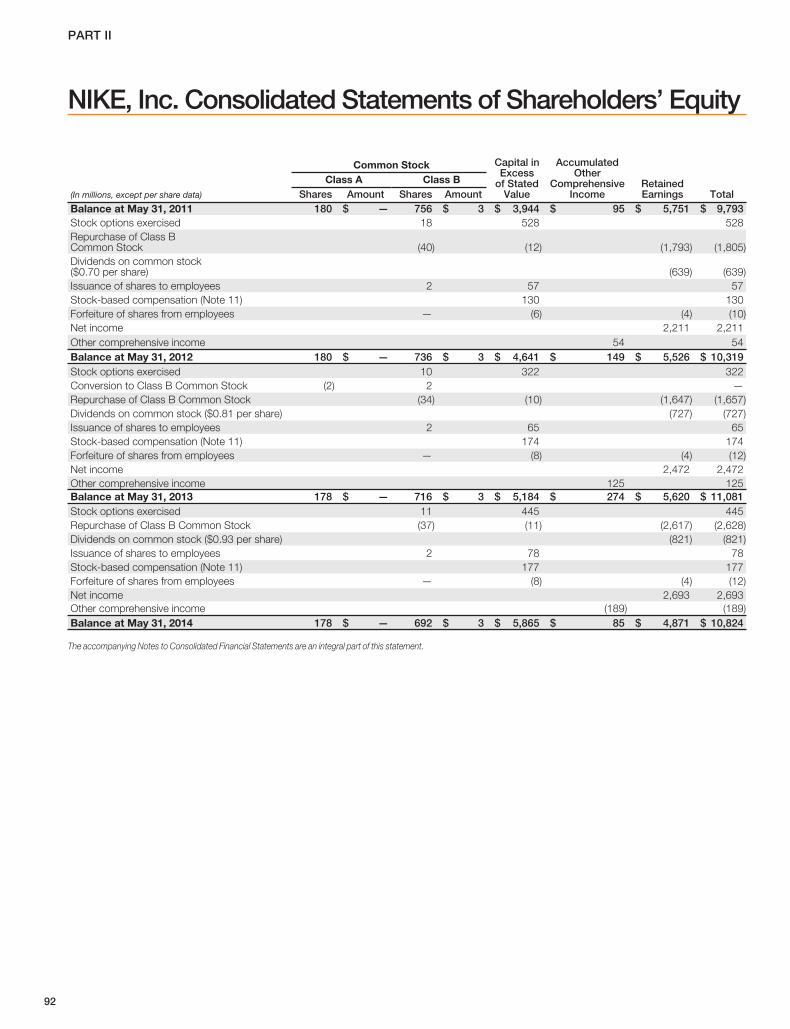

NIKE, Inc. Consolidated Statements of Shareholders’ Equity

Common Stock Capital inExcess

of StatedValue

AccumulatedOther

ComprehensiveIncome

RetainedEarnings Total

Class A Class B(In millions, except per share data) Shares Amount Shares AmountBalance at May 31, 2011 180 $ — 756 $ 3 $ 3,944 $ 95 $ 5,751 $ 9,793Stock options exercised 18 528 528Repurchase of Class BCommon Stock (40) (12) (1,793) (1,805)Dividends on common stock($0.70 per share) (639) (639)Issuance of shares to employees 2 57 57Stock-based compensation (Note 11) 130 130Forfeiture of shares from employees — (6) (4) (10)Net income 2,211 2,211Other comprehensive income 54 54Balance at May 31, 2012 180 $ — 736 $ 3 $ 4,641 $ 149 $ 5,526 $ 10,319Stock options exercised 10 322 322Conversion to Class B Common Stock (2) 2 —Repurchase of Class B Common Stock (34) (10) (1,647) (1,657)Dividends on common stock ($0.81 per share) (727) (727)Issuance of shares to employees 2 65 65Stock-based compensation (Note 11) 174 174Forfeiture of shares from employees — (8) (4) (12)Net income 2,472 2,472Other comprehensive income 125 125Balance at May 31, 2013 178 $ — 716 $ 3 $ 5,184 $ 274 $ 5,620 $ 11,081Stock options exercised 11 445 445Repurchase of Class B Common Stock (37) (11) (2,617) (2,628)Dividends on common stock ($0.93 per share) (821) (821)Issuance of shares to employees 2 78 78Stock-based compensation (Note 11) 177 177Forfeiture of shares from employees — (8) (4) (12)Net income 2,693 2,693Other comprehensive income (189) (189)Balance at May 31, 2014 178 $ — 692 $ 3 $ 5,865 $ 85 $ 4,871 $ 10,824

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

92

NIKE, INC.One Bowerman DriveBeaverton, OR 97005-6453www.nike.com