Embed Size (px)

Citation preview

Telecommunications Sector Presentation

By Brad Moore

Sector Overview

The Telecommunications Services Sector contains companies that provide communications services primarily through a fixed-‐line, cellular, wireless, high bandwidth and/or fiber optic cable network.

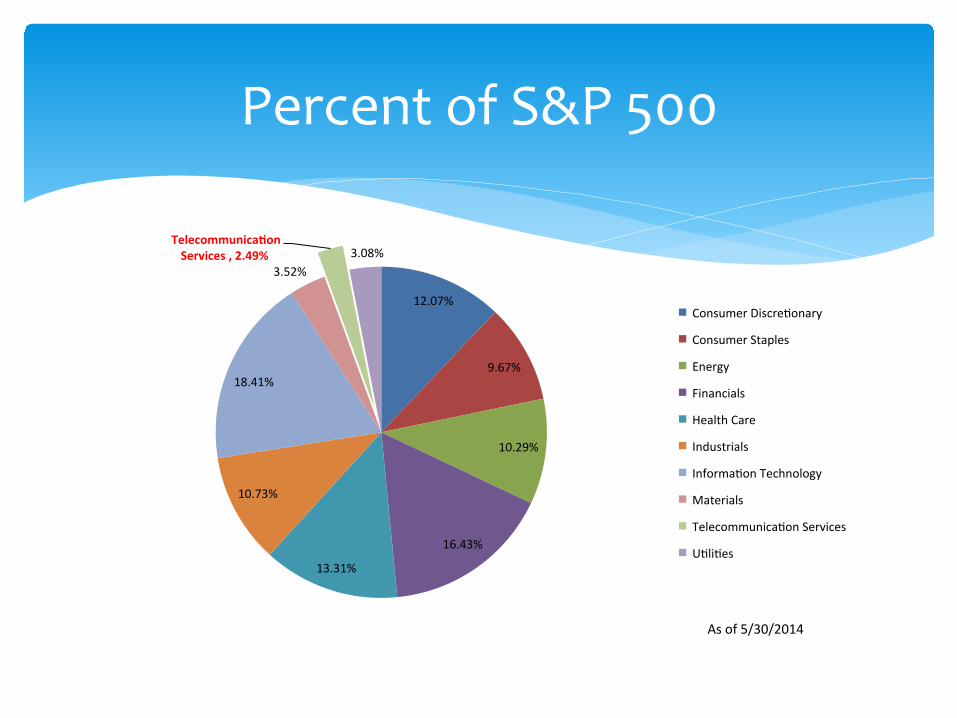

Percent of S&P 500

12.07%

9.67%

10.29%

16.43%

13.31%

10.73%

18.41%

3.52%

Telecommunica+on Services , 2.49% 3.08%

Consumer Discre9onary

Consumer Staples

Energy

Financials

Health Care

Industrials

Informa9on Technology

Materials

Telecommunica9on Services

U9li9es

As of 5/30/2014

• Diversified Telecommunication Services • “Wireline” services • Use broadband or fiber optic cable to transmit data

• Wireless Telecommunication Services • Provide cellular or wireless services

Industries

Companies

Market Cap by Company

Company Market Cap

AT&T Inc 184,686,934,030

CenturyLink Inc 21,771,564,850

Fron9er Communica9ons Corp 5,787,377,130

Verizon Communica9ons Inc 206,891,404,360

Windstream Holdings Inc 5,703,758,280

Total 424,841,038,650

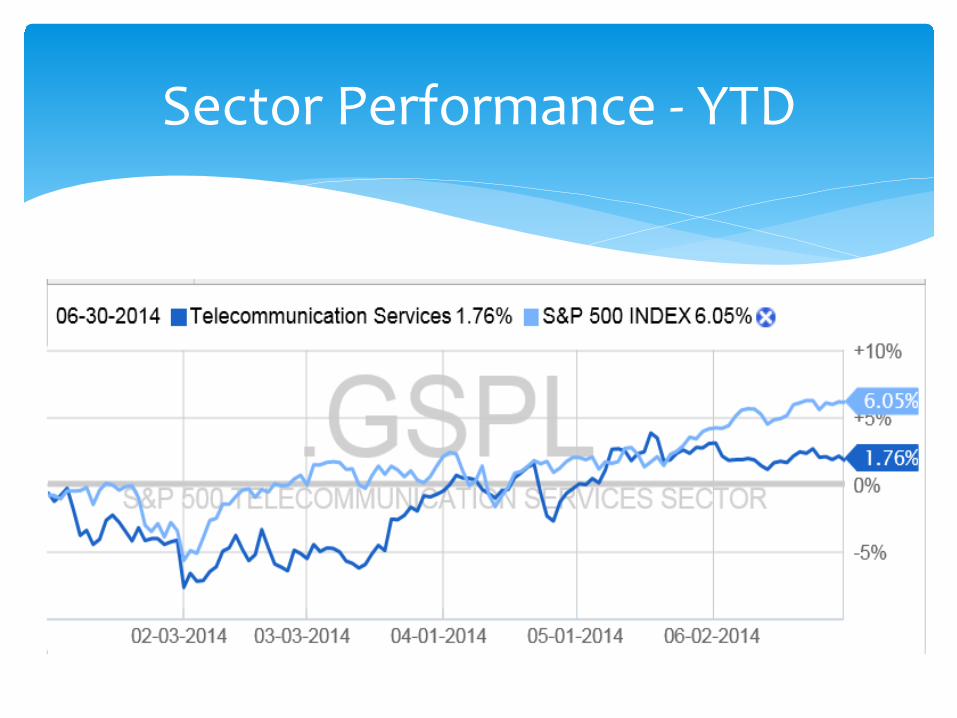

Sector Performance -‐ YTD

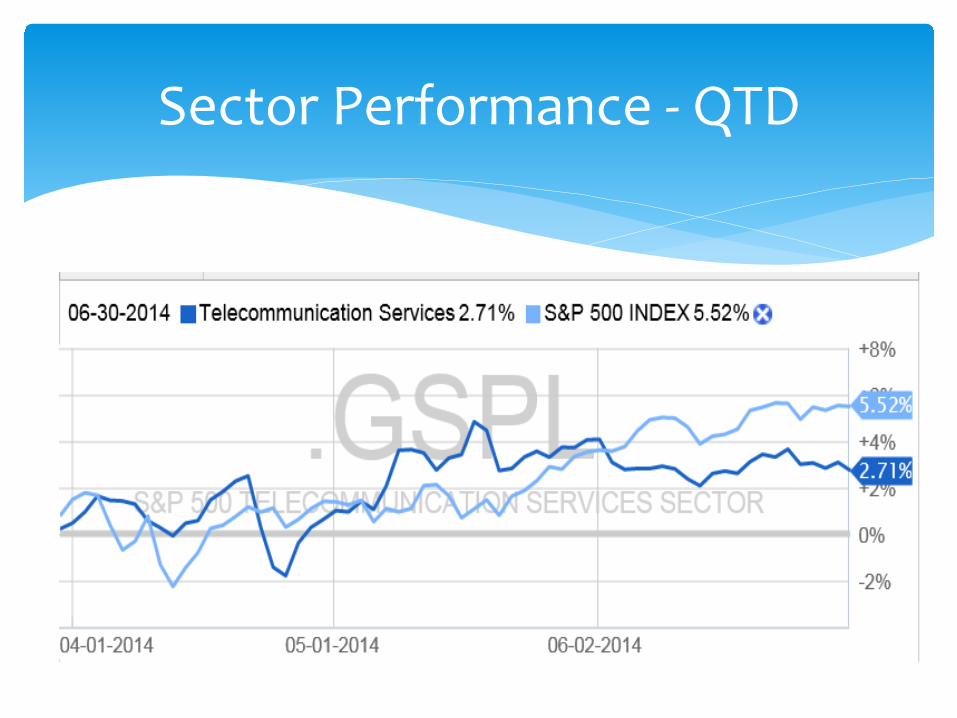

Sector Performance -‐ QTD

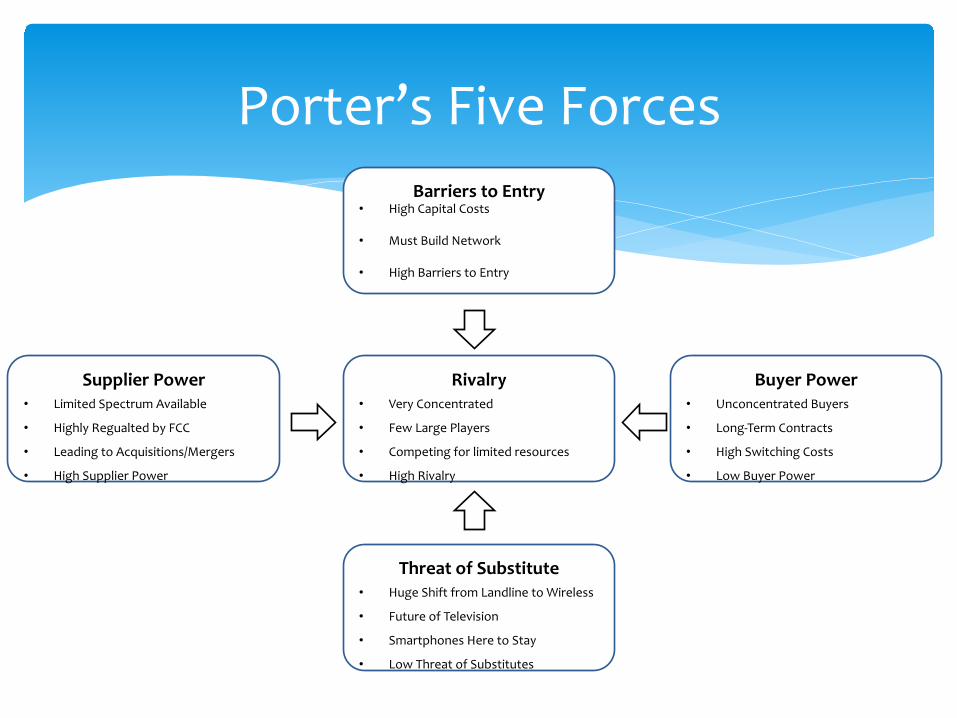

Rivalry • Very Concentrated

• Few Large Players

• Competing for limited resources

• High Rivalry

Barriers to Entry • High Capital Costs

• Must Build Network

• High Barriers to Entry

Threat of Substitute • Huge Shift from Landline to Wireless

• Future of Television

• Smartphones Here to Stay

• Low Threat of Substitutes

Supplier Power • Limited Spectrum Available

• Highly Regualted by FCC

• Leading to Acquisitions/Mergers

• High Supplier Power

Buyer Power • Unconcentrated Buyers

• Long-‐Term Contracts

• High Switching Costs

• Low Buyer Power

Porter’s Five Forces

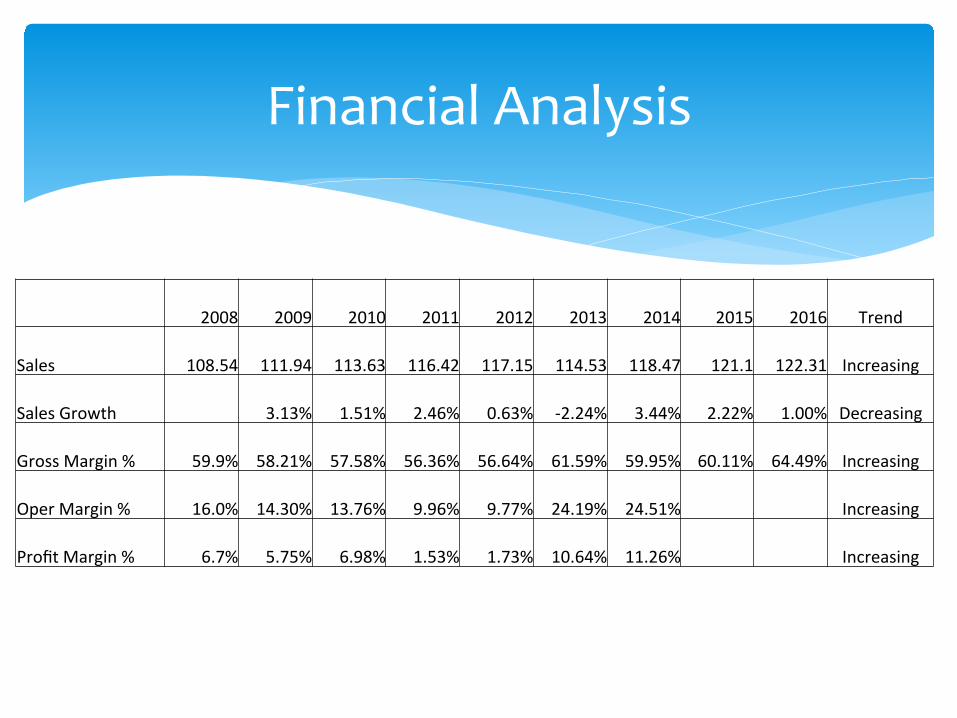

Financial Analysis

2008 2009 2010 2011 2012 2013 2014 2015 2016 Trend

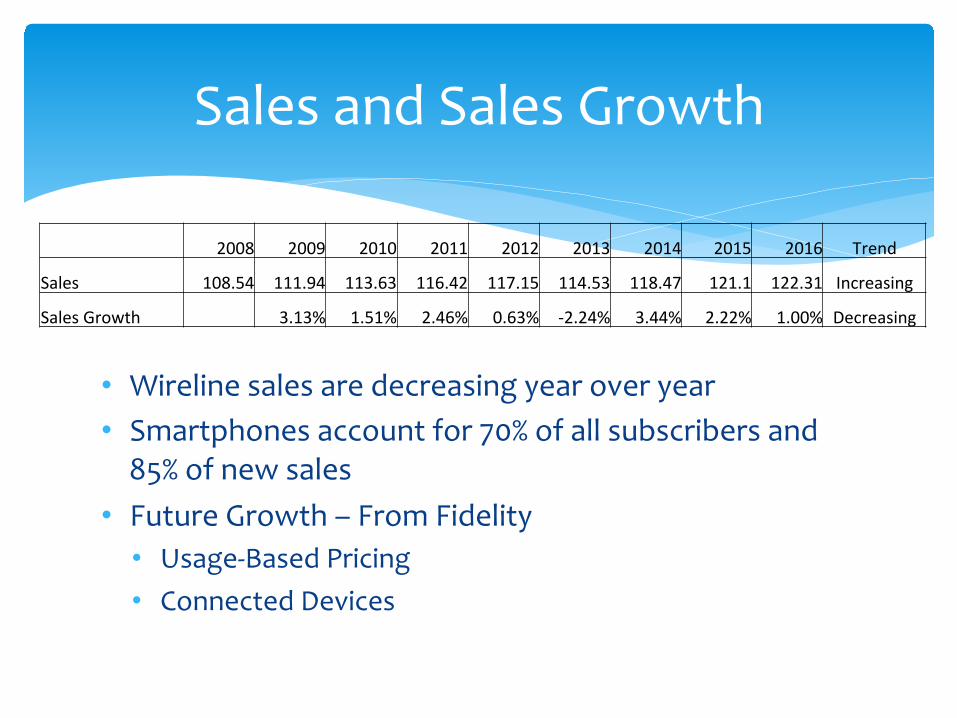

Sales 108.54 111.94 113.63 116.42 117.15 114.53 118.47 121.1 122.31 Increasing

Sales Growth 3.13% 1.51% 2.46% 0.63% -‐2.24% 3.44% 2.22% 1.00% Decreasing

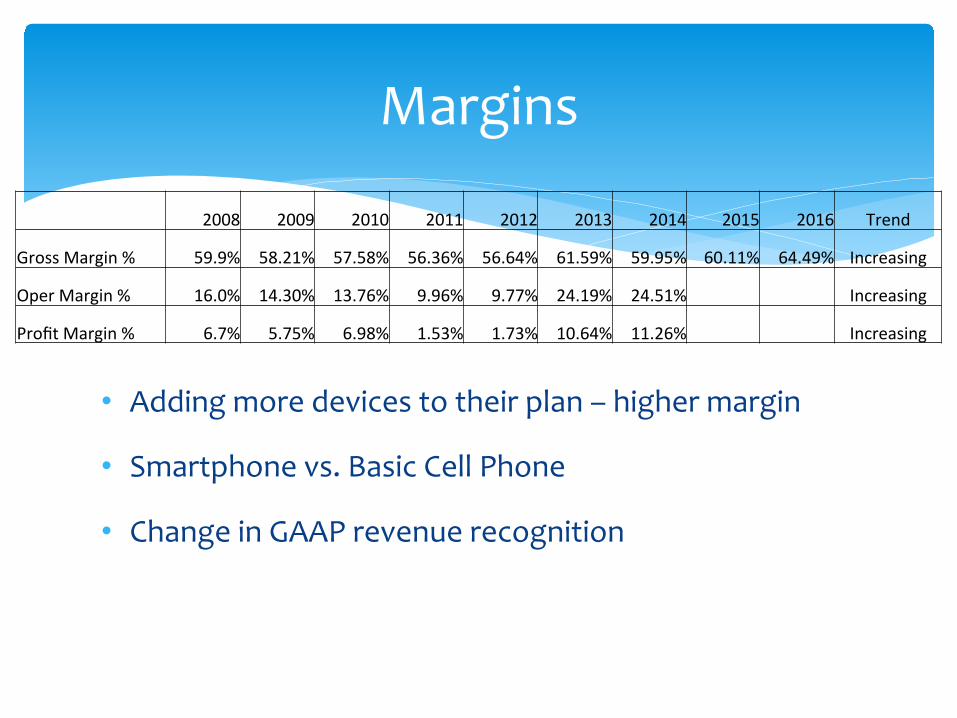

Gross Margin % 59.9% 58.21% 57.58% 56.36% 56.64% 61.59% 59.95% 60.11% 64.49% Increasing

Oper Margin % 16.0% 14.30% 13.76% 9.96% 9.77% 24.19% 24.51% Increasing

Profit Margin % 6.7% 5.75% 6.98% 1.53% 1.73% 10.64% 11.26% Increasing

• Wireline sales are decreasing year over year • Smartphones account for 70% of all subscribers and 85% of new sales

• Future Growth – From Fidelity • Usage-‐Based Pricing • Connected Devices

Sales and Sales Growth

2008 2009 2010 2011 2012 2013 2014 2015 2016 Trend

Sales 108.54 111.94 113.63 116.42 117.15 114.53 118.47 121.1 122.31 Increasing

Sales Growth 3.13% 1.51% 2.46% 0.63% -‐2.24% 3.44% 2.22% 1.00% Decreasing

• Adding more devices to their plan – higher margin

• Smartphone vs. Basic Cell Phone

• Change in GAAP revenue recognition

Margins

2008 2009 2010 2011 2012 2013 2014 2015 2016 Trend

Gross Margin % 59.9% 58.21% 57.58% 56.36% 56.64% 61.59% 59.95% 60.11% 64.49% Increasing

Oper Margin % 16.0% 14.30% 13.76% 9.96% 9.77% 24.19% 24.51% Increasing

Profit Margin % 6.7% 5.75% 6.98% 1.53% 1.73% 10.64% 11.26% Increasing

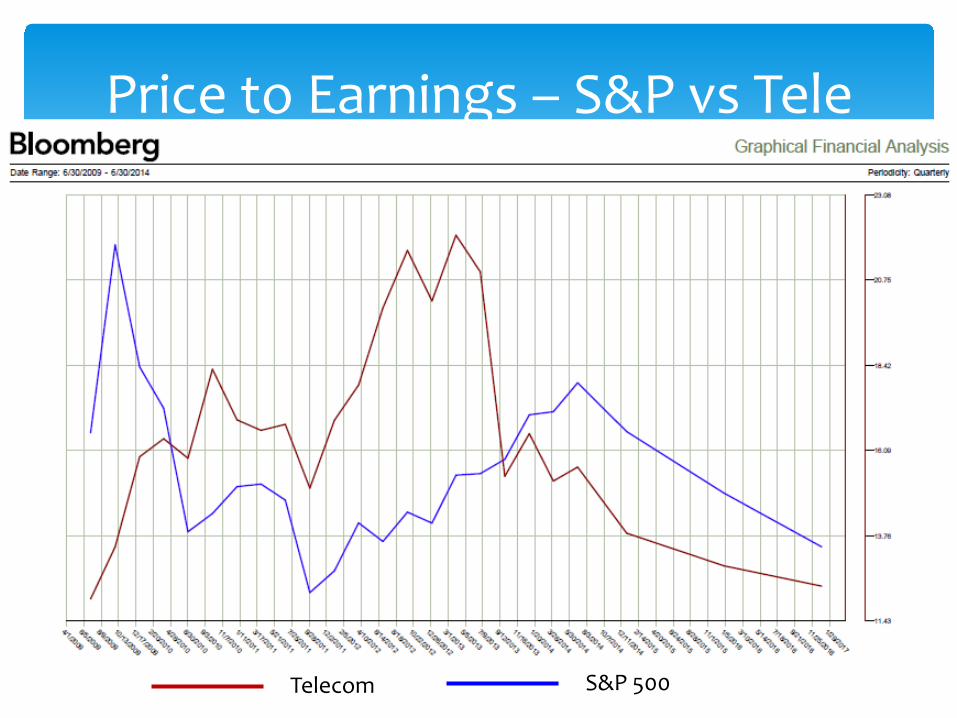

Price to Earnings – S&P vs Tele

Telecom S&P 500

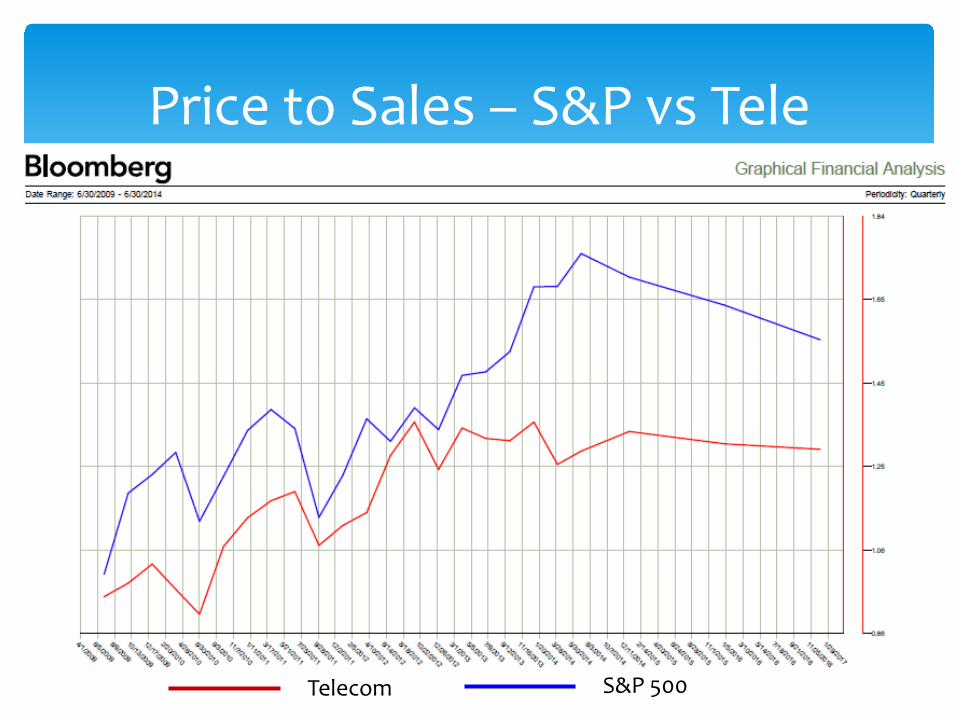

Price to Sales – S&P vs Tele

Telecom S&P 500

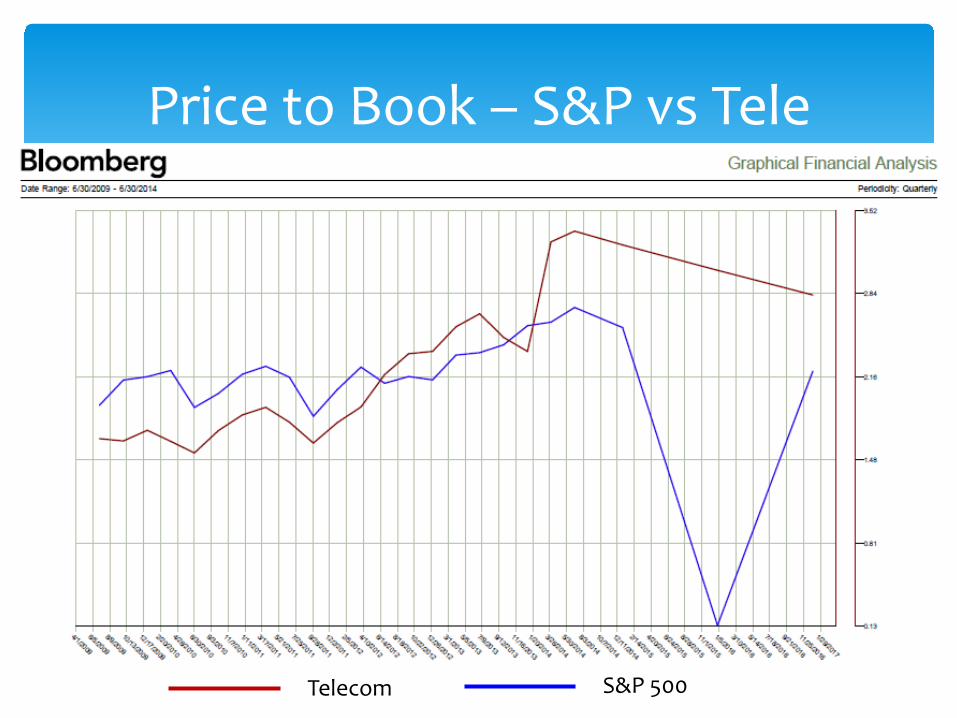

Price to Book – S&P vs Tele

Telecom S&P 500

• Difficulty using valuation methods on multi-‐industry businesses

• Example AT&T/DirecTV

• Creates riskiness of cash flows – increase in discount rate

• How realistic are synergies?

• Negative impacts of transaction

• Google acquisition of wireless start up

Affect of Mergers/Acquisitions

• Currently, overweight in Telecommunications (2.84% vs. 2.49%

of S&P)

• Should move to be underweight

• No diversification within Telecommunications (AT&T only)

• Spread investment over multiple companies that look appealing

• Be ready for a rebound in this sector

Recommendation