Embed Size (px)

Citation preview

/ --

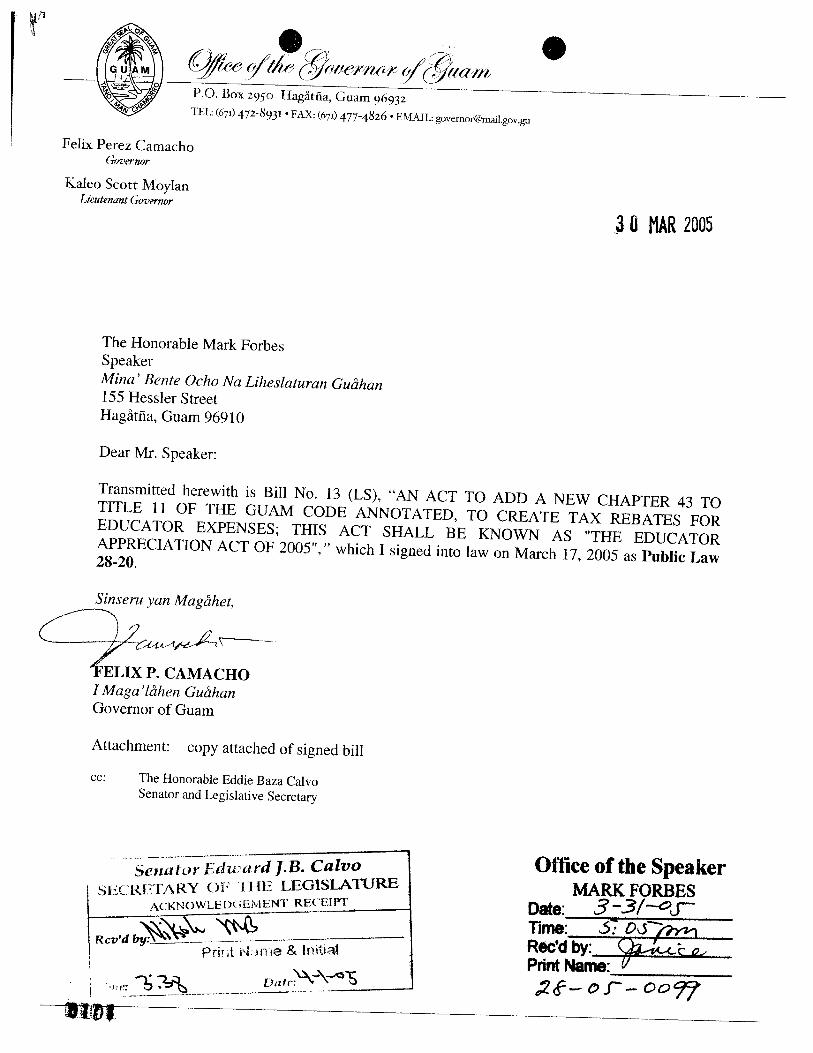

P.O. Box 2950 HagPatha, Guam 96932 TEL: (671) 472-8931 FAX: (671) 477-4826 E W L : [email protected]

I Felix Perez Carnacho Gmwnor

Kaleo Scott Moylan L i m m t G o v m

The Honorable Mark Forbes Speaker Mina' Bente Ocho Na Liheslaturan GuHhan 155 Hessler Street Hagitfia, Guam 969 10

Dear Mr. Speaker:

Transmitted herewith is Bill No. 13 (LS), "AN ACT TO ADD A NEW CHAPTER 43 TO TITLE 11 OF THE GUAM CODE ANNOTATED, TO CREATE TAX REBATES FOR EDUCATOR EXPENSES; THIS ACT SHALL BE KNOWN AS "THE EDUCATOR APPRECIATION ACT OF 2005"," which I signed into law on March 17. 2005 as Public Law 28-20.

Sinseru yan MagHhet,

qLu&-..- I Maga'liihen Guiihan Governor of Guam

Attachment: copy attached of signed bill

cc: The Honorable Eddie Baza Calvo Senator and Legislative Secretary

Office of the Speaker MARK FORBES

Date: 3-3IeL T i m S f z ~ ~ Rec'd &:_ Print Na;meiG

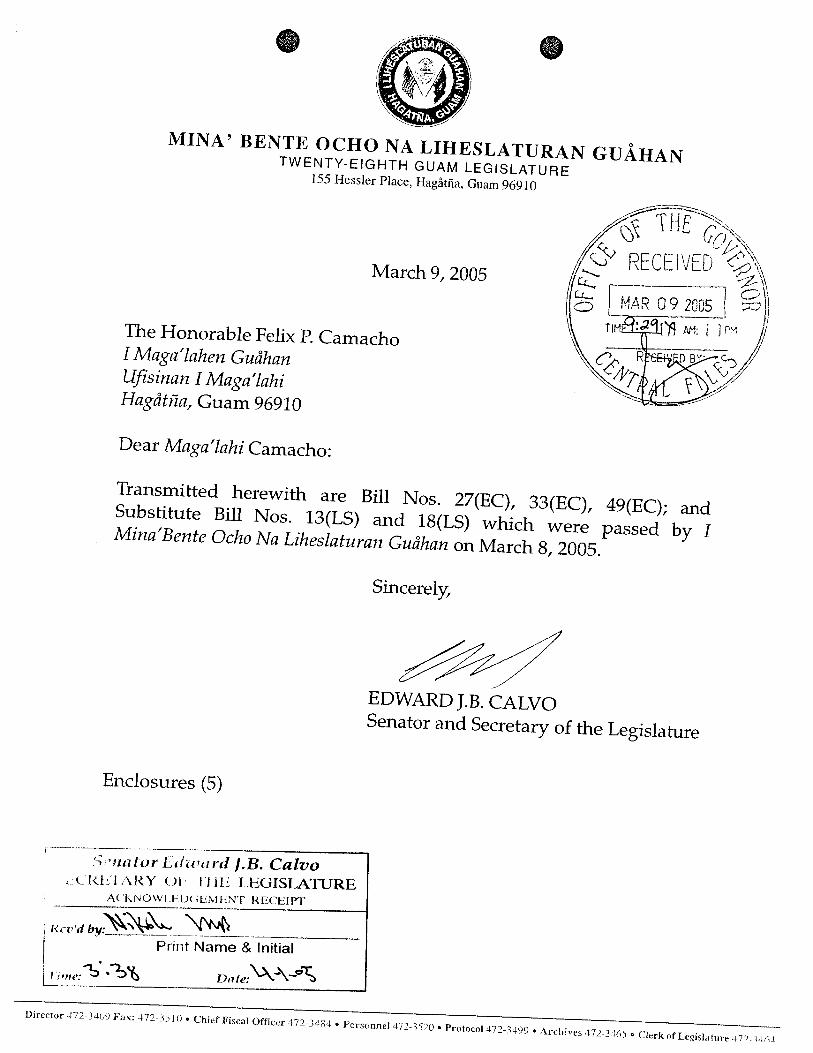

MINA? BENTE OCHO NA LIHESLATURAN GUAHAN TWENTY-EIGHTH GUAM LEGISLATURE

155 Hessler Place, HagAtiia, Guam 96910

March 9,2005

The Honorable Felix P. Camacho I Maga'lahen Gudkan Ufsinan I Maga'laki Hagdttia, Guam 96910

Dear Maga'lahi Camacho:

Transmitted herewith are Bill Nos. 27(EC), 33(EC), 49(EC); and Substitute Bill Nos. 13(LS) and 18(LS) which were passed by I Mina'Bente Ocho Na Likeslaturan Guihan on March 8,2005.

Sincerely,

EDWARD J.B. CALVO Senator and Secretary of the Legislature

Enclosures (5)

6 4 d ? t l a f ~ r t t X z 4 t ~ r t . t - E J.B. Calvo ,_c lcl; 1 i'\i<Y c )k+ 1 1 12: LEGISLATURE

A< k N O W l d t U C ~ L , M k N ' T RECEIPT

FiaL- w / licv'd by: I I Print Name & Initial I

Director 472-3409 Far: 172-35 l i i Chief Fiscal Officer 472-348" Personnel 472-3520 Protocol 172-3499 Archives 472-3465 * Clerk DfLegiS13~1,re 47 ?.?'1*1

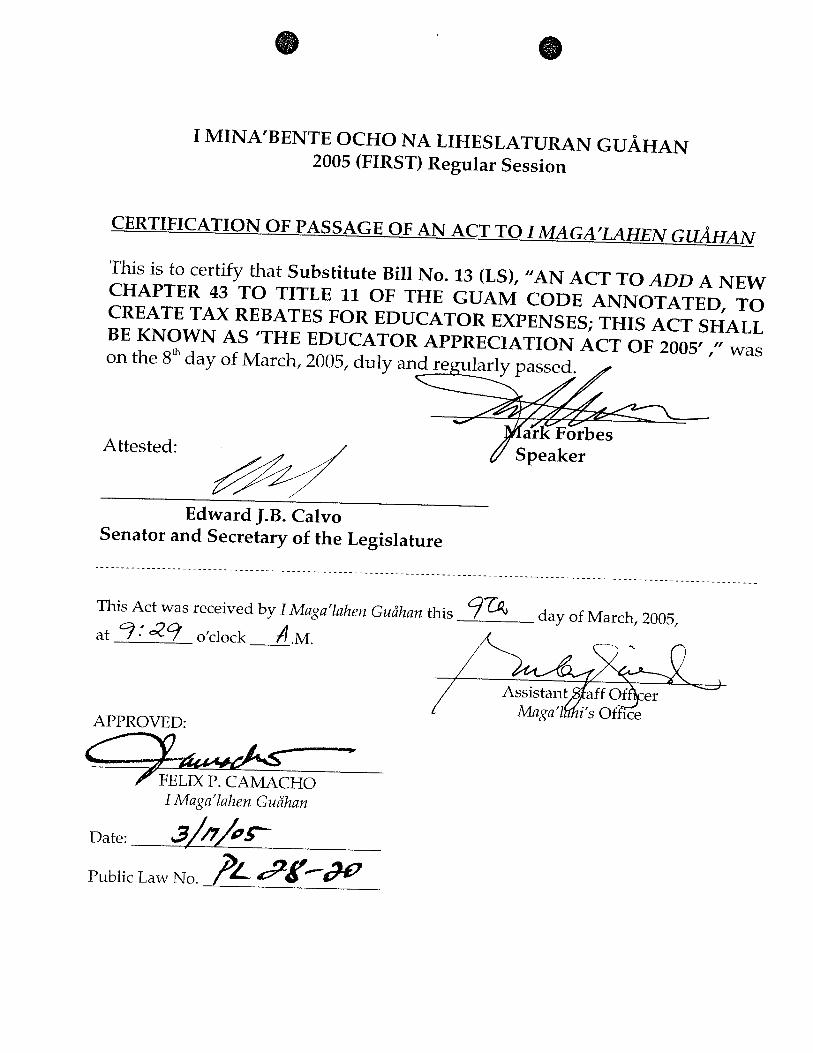

I MINA'BENTE OCHO NA LIHESLATURAN GUAHAN 2005 (FIRST) Regular Session

CERTIFICATION OF PASSAGE OF AN ACT TO IMAGA'LAHEN GU&-XAN

Th~s is to certify that Substitute Bill No. 13 (LS), "AN ACT TO ADD A NEW CHAPTER 43 TO TITLE 11 OF THE GUAM CODE ANNOTATED, TO CREATE TAX REBATES FOR EDUCATOR EXPENSES; THIS ACT SHALL BE KNOWN AS 'THE EDUCATOR APPRECIATION ACT OF 2005' ," was on the 8" day of March, 2005, duly

,/ Speaker

Edward J.B. Calvo Senator and Secretary of the Legislature

This Act was received by 1 Maga'lahen Guihan this day of March, 2005,

at 7: 29 o'clock A.M. 1 -

APPROVED:

/'FELIX P. CAMACHO I Maga'lahen Gudhan

Date: 3//r/ps"

Public Law No. ?L ~ g f l a '

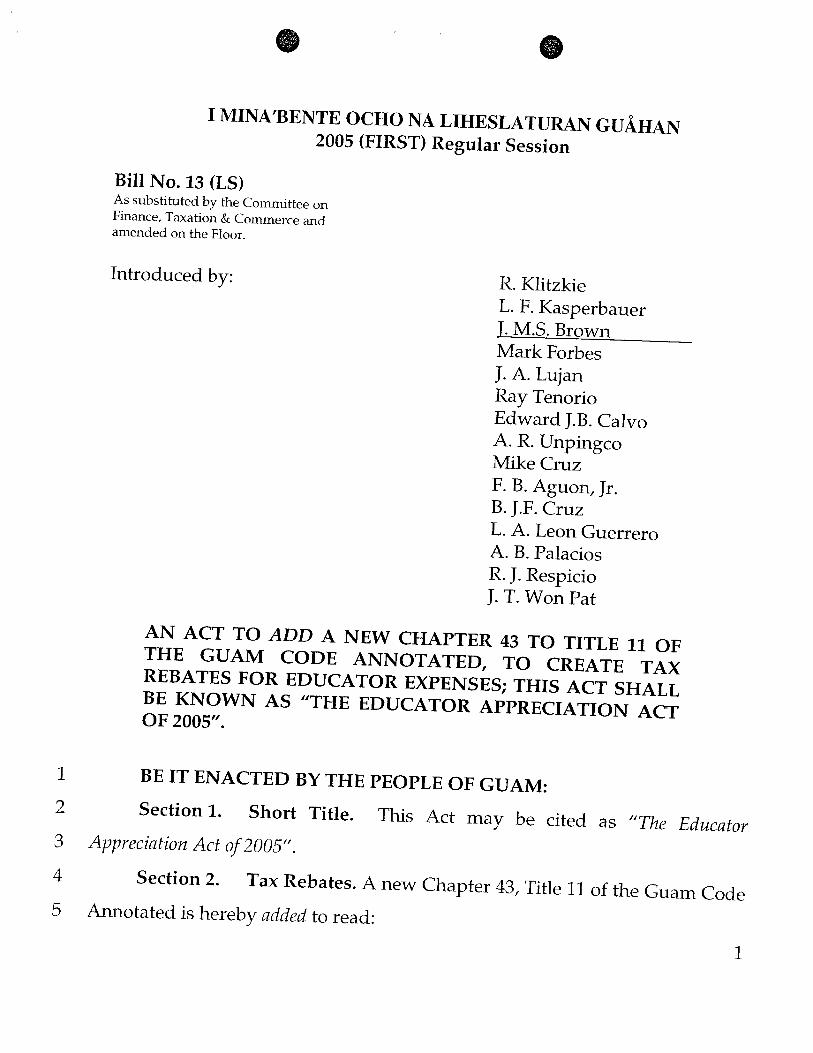

I MINA'BENTE OCHO NA LIHESLATURAN GUAHAN 2005 (FIRST) Regular Session

Bill No. 13 (LS) As substituted by the Committee on Finance, Taxation & Commerce and amended on the Floor.

Introduced by: R. Klitzkie L. F. Kasperbauer J. M.S. Brown Mark Forbes J. A. Lujan Ray Tenorio Edward J.B. Calvo A. R. Unpingco Wke Cruz F. B. Aguon, Jr. B. J.F. Cruz L. A. Leon Guerrero A. B. Palacios R. J. Respicio J. T. Won Pat

AN ACT TO ADD A NEW CHAPTER 43 TO TITLE 11 OF THE GUAM CODE ANNOTATED, TO CREATE TAX REBATES FOR EDUCATOR EXPENSES; THIS ACT SHALL BE KNOWN AS "THE EDUCATOR APPRECIATION ACT OF 2005".

1 BE IT ENACTED BY THE PEOPLE OF GUAM:

2 Section 1. Short Title. This Act may be cited as "The Educator

3 Appreciation Act of2005".

4 Section 2. Tax Rebates. A new Chapter 43, Title 11 of the Guam Code

5 Annotated is hereby added to read: 1

"CHAPTER 43.

The Educator Appreciation Act

TAX REBATES FOR EDUCATOR EXPENSES

54301. Statement of Legislative Purpose.

54302. Definitions.

54303. Tax Rebate for Educator Expenses.

54304. Procedure to Claim Rebated Taxes.

54305. Rebate Fund.

54306. Implementation by Tax Commissioner.

54307. Sunset Provision.

54308. Construction.

$4301. Statement of Legislative Purpose. Teachers traditionally

spend their own money on various supplies (e.g. bulletin board

materials, books, pencils, crayons and markers). Although these

expenses are deductible as unreirnbursed business expenses on a

teacher's income tax return, election of the standard deduction meant

that most teachers bore the entire cost of these generous expenditures.

The United States Congress recognized the plight of teachers and

effective tax year 2002 allowed a deduction of Two Hundred-Fifty

Dollars ($250.00) from the adjusted gross income (see line 23, Internal

Revenue Service ('IRS') Form 1040 for 2004) thereby allowing all

teachers and other educators to deduct qualified expenses even if the

educator did not itemize deductions.

While the Two Hundred-Fifty Dollars ($250.00) tax deduction may

be sufficient for teachers in some areas, it is woefully inadequate for

many teachers teaching in the Guam Public School System. Because of

several years of chronic under-funding, public school educators have,

for several years, responded to the needs of their students by spending

their own money on what are denominated qualifed expenses in this Act.

Furthermore, educators in Guam's private schools are faced with the

same conditions, thereby finding it necessary to spend their own private

funds to provide supplies and materials cited as qualifed expenses in this

Act. Given the state of Guam's economy it is almost a certainty that

educators will continue to attempt to meet the needs of their students by

spending their own money. This Act allows educators to claim a tax

rebate to recover u p to Five Hundred Dollars ($500.00) of personal

expenditures over and above the Two Hundred-Fifty Dollar ($250.00)

deduction allowed by the Internal Revenue Code ('IRC').

This Act adopts much of the operative language of §62 of the

Internal Revenue Code ('IRC') thereby making the various instructions,

pamphlets and other papers issued by the Internal Revenue Service

('IRS') available for the interpretation of this Act, e.g. expenses

deductible at line 23 of Internal Revenue Service ('IRS') Form 1040 are

subject to rebate under this Act to the extent they exceed the Two

Hundred-Fifty Dollar ($250.00) deduction.

GEDA Qualifying Certificates have been issued to businesses,

allowing them tax rebates for nearly forty (40) years and have fostered

much economic development. This Act extends the functional

equivalent of the Qualifying Certificate (the Educator's Qualzfijing

Certlficafe or 'EQC') and tax rebate, on a much smaller scale, to teachers.

Wlule this rebate is insufficient to make up for the economic hardship

suffered by teachers, it is one way for this community to show its

appreciation to its educators.

54302. Definitions. The definitions set forth herein shall govern

the construction and interpretation of this Chapter;

(a) 'Eligible educator' means a kindergarten through grade 12 in

the Guam Public School System and in Guam's private

schools:

1) Teacher;

2) Instructor;

3) Counselor;

4) Principal; or

5) Aide.

(b) 'Qualifed expenses' means unreimbursed expenses exceeding

Two Hundred-Flfty Dollars ($250.00), less any unreimbursed

employee expenses upon which a deduction from adjusted

gross income is based that an elipble educator paid or

incurred for books, supplies, computer equipment

(including related software and services), other equipment,

and supplementary materials that the educator used in his

or her classroom. For courses in health or physical

education, expenses for supplies are qualified expenses only

if they are related to athletics.

(c) 'Educator's Qualihing Certificate (EQC)' means the declaration

of an eligible educator, made pursuant to 6 GCA $4308, of the

qualified expenses he or she incurred during a tax year.

54303. Tax Rebate for Educator Expenses. A rebate in an

amount equal to the qualified expenses incurred, but not to exceed Five

Hundred Dollars ($500.00) of personal income tax paid by resident

individual taxpayers, who are eligible educators, to the government of

Guam is hereby established and declared.

54304. Procedure to Claim Rebated Taxes. When a tax return is

accompanied by an EQC(s), the amount of tax due prior to the rebate

shall be deposited with the government of Guam at the time of filing the

income tax return. Alternatively, if no payment is due at the time the

tax return is filed, the Tax Commissioner of Guam shall credit the

amount of the EQC to the Rebate Fund from taxes paid by the taxpayer.

Absent a finding by the Tax Commissioner that the rebate is not

payable, the rebate shall be withdrawn from the deposit and returned to

the taxpayer(s) within one hundred and eighty (180) days of the deposit

without interest.

54305. Rebate Fund. Deposits made pursuant to 54304 shall be

covered over and deposited into the fund created by 12 GCA s58138.

94306. Implementation by Tax Commissioner. The Tax

Commissioner of Guam shall, no later than ninety (90) days after the

effective date hereof, develop necessary procedures to implement this

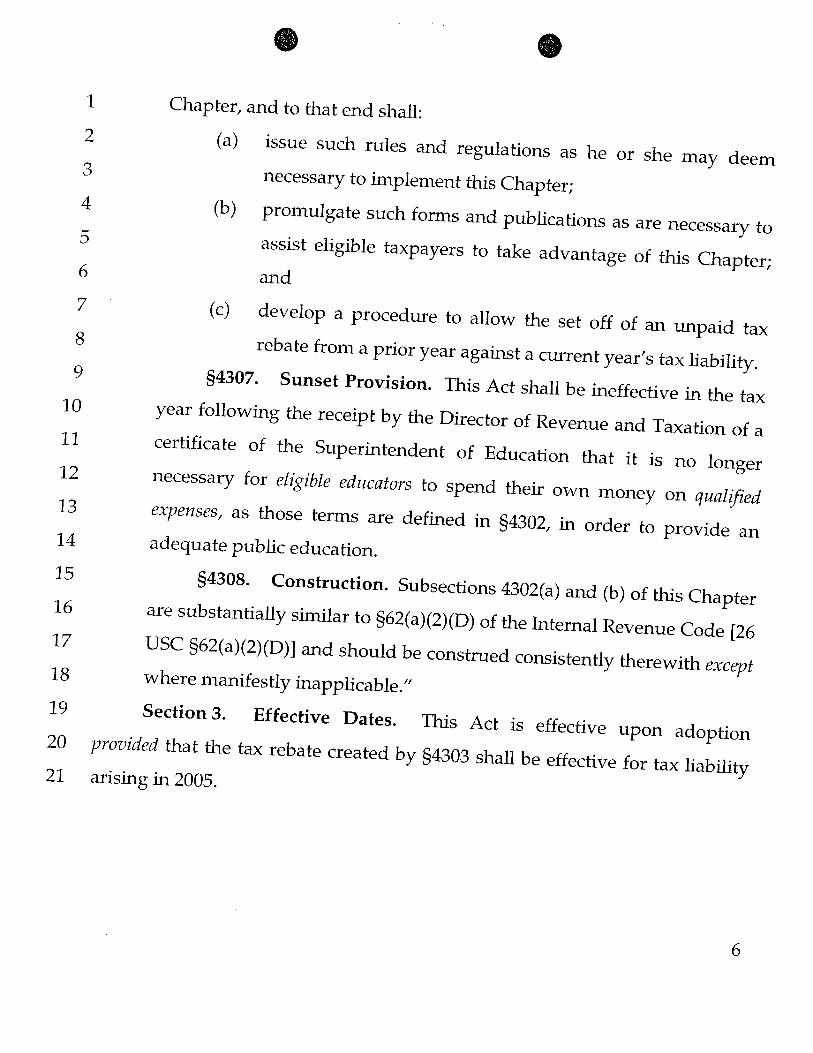

Chapter, and to that end shall:

(a) issue such rules and regulations as he or she may deem

necessary to implement this Chapter;

(b) promulgate such forms and publications as are necessary to

assist eligible taxpayers to take advantage of this Chapter;

and

(c) develop a procedure to allow the set off of an unpaid tax

rebate from a prior year against a current year's tax liability.

54307. Sunset Provision. This Act shall be ineffective in the tax

year following the receipt by the Director of Revenue and Taxation of a

certificate of the Superintendent of Education that it is no longer

necessary for eligible educators to spend their own money on qualifiPd

expenses, as those terms are defined in 94302, in order to provide an

adequate public education.

94308. Construction. Subsections 4302(a) and (b) of this Chapter

are substantially similar to §62(a)(2)(D) of the Internal Revenue Code (26

USC §62(a)(2)(D)] and should be construed consistently therewith except

where manifestly inapplicable."

Section 3. Effective Dates. This Act is effective upon adoption

provided that the tax rebate created by 94303 shall be effective for tax liability

arising in 2005.

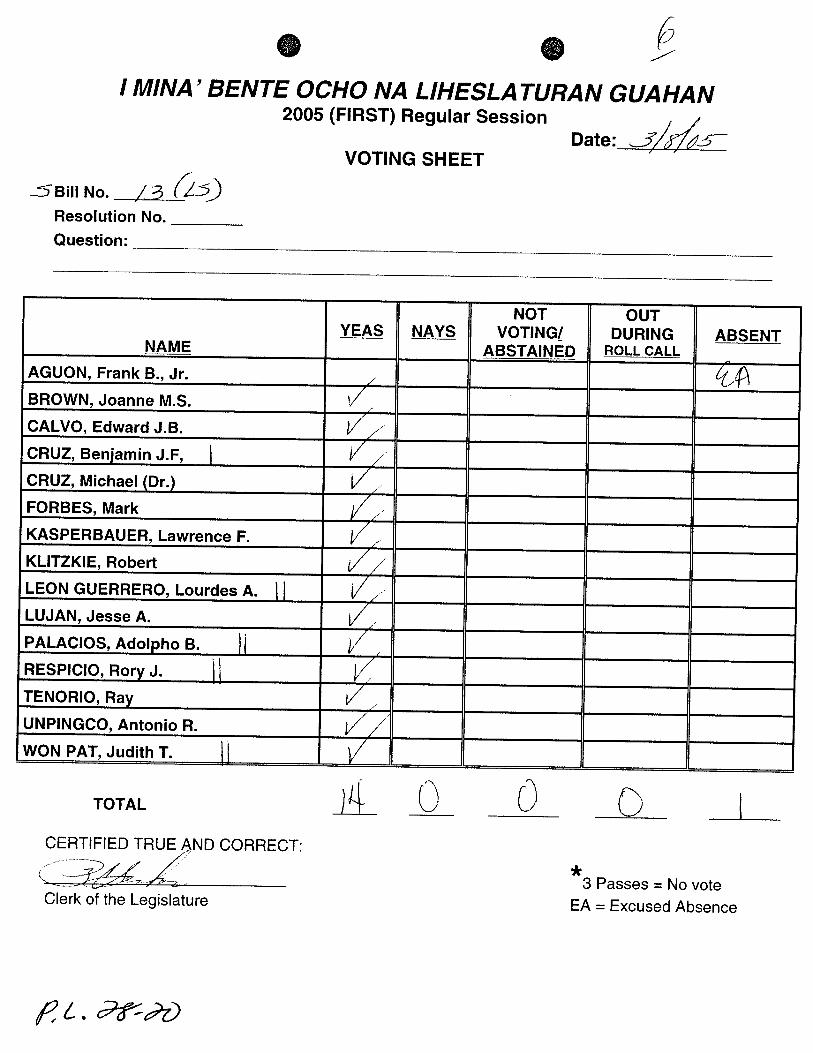

/ M/NA' BENT€ OCHO NA L/HESLATURAN GUAHAN 2005 (FIRST) Regular Session

VOTING SHEET Date: </&5

Resolution No. Question:

TOTAL

CERTIFIED TRUE AND CORRECT: * 3 Passes = No vote

EA = Excused Absence Clerk of the Legislature

4 ' 1 . , .

. . MINA'BENTE O C H O N A L I I I E S I 3 A ' T U R ~ 1 N G U X H A N . r 5 ~ i ~ ~ ' ~ ' ~ - ~ ~ ~ ; ~ ~ ~ ~ ~ c;'cin~ LLG rsl.,%+rr; ~ t : ;

S e n a t o r Edward J . B . Ca'tvo S E C R E T A K Y O F T H E L I E G I S L A ' ~ U R E

Chairman COMMIITEE ON FINXiWCE, 'I'iPX4TiON & COMMERCE

OFFICE OF FINANCE IWD BUIIGEI'

E-Mail ar!drcss: ~ J ~ ~ ~ p r c ~ ~ \ l ! \ o ~ i m I ~ ~ ) t ,i!.<i.i&.js~ T ~ ~ ~ X X X : (071) 475-@&1~

155 Hcslci Street IingStiia. C;uam y691o Farsimilc: (6-1) l-;,-tWhs - - - -- - -- . . -. . - A ~ . . .

" --- - C''t -- 3

Thc f i t )norable Mark Forbes Speahcr ,\,liritr L; '~~r t rc ' Ocizo ita I,iltc.~lurrirarr (;uB170tz 155 Hebler Place i-lripitna. Guam 069 I 0

fIt.;fi~ I I C ~ C I I ' , Mr. Spcakcr:

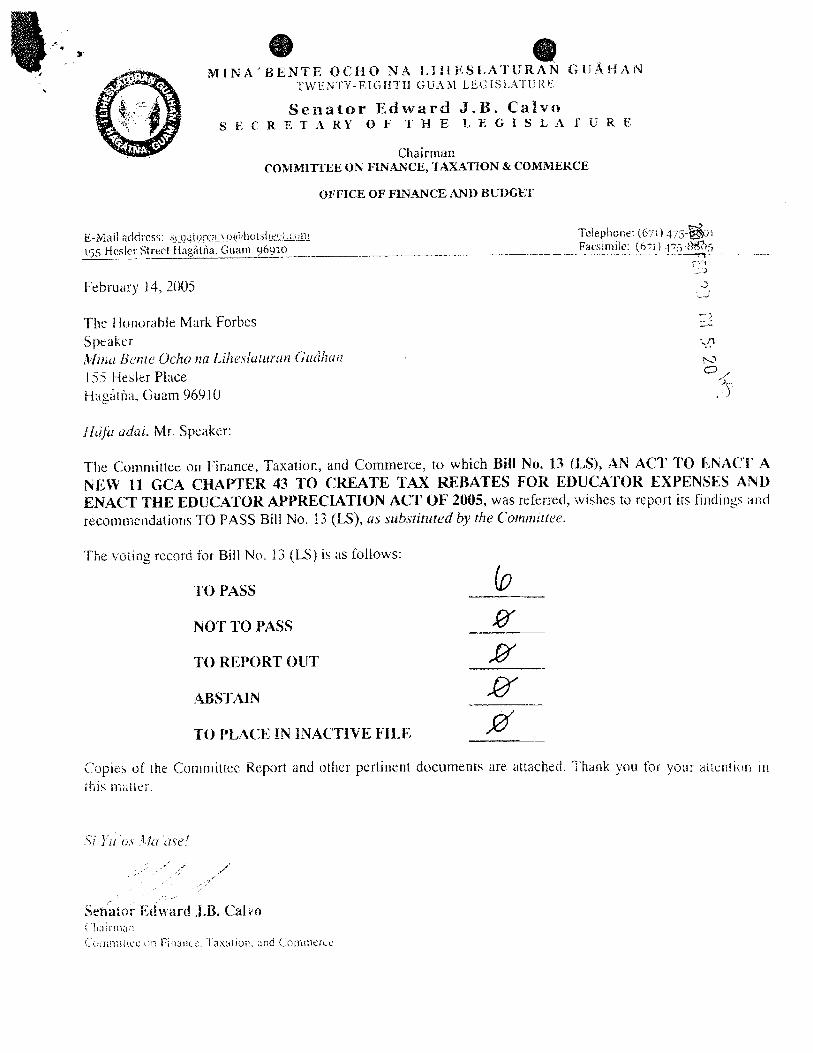

The Comntittee on Finance, Taxation, and Commerce, to which Bill No. 13 fLS). A-1V ACT TO KfiAC'I' A MW 11 GCA CHAPTER 43 TO CREATE TAX REBATES FOR EDUCATC)K EXPENSES AND ENACT THE EDUCATOR APPRECIATION ACT OF 2005. was referred, wishes to report its filldirlgs and recoxnrncndations TO PASS Bill No. 13 (LS), as sub.stinrted by f!zf C'otnmirfeu.

'T'hc voting rccord for Bill No. 12 (i,S) i~ as follows:

TO PASS

NOT 1'0 PASS

TO REPORT OUT

ABSTAIN -

TO I'EACE IN INACTIVE FILE ,@'

Copies of the Committee Report and other pertinent documents are attached. 'i'hank you fc?r yotlr zt:e~itic-)n 111

diis niailer.

MINA'BESTE O C H O NL4 LIE4ESLATURAM G I J A H A N I b l k Y T Y - E I G H T H GUXA; LEGISLATURE

S e a a t o r Edward J . B . Ca lvo S k , C R E T A K Y O F ; T H E I J E @ I S L , A T l ! K E

Chairtn,in &'OMblITiTEE ON I:lNN4NCE. 'I'AUTION & CUM RI EKCE

February 14. 2005

Tc?: C'ornruiitee Directors

kldn;. Chairma;:. Cc,mmi\ier. on Financc, Taxaiion. and Cornmercz

Sub~cut: Committee report 011 Bill 13 (LS) as. sub.\rlturcd by the Cornmitter MI Fiizutico, 7usurion, unli ( ( ~ ~ ~ ~ i ~ i c ~ . ~ <

This mrmurani lur it; accompanied by thc following:

1 . Contrnittcc voting shcet 3 -. I'u biic Hearing sign-in sheet 1 . 7 . Nctticc n?' Public Fiearirlg 4. Trstimtinics subtnitfed

I ' 1 c . i ~ iakr. ihc appropriate ~iciion Oil !he attached voting L. sheel. Your attcntjorr aiid coopct-ation it1 this matter is c r t d t i y appreciartd. Sl~oulti [ h e x be any questions regarding this matter, plcasc feel free to alntact my olfiice at 4?5-$SO I .

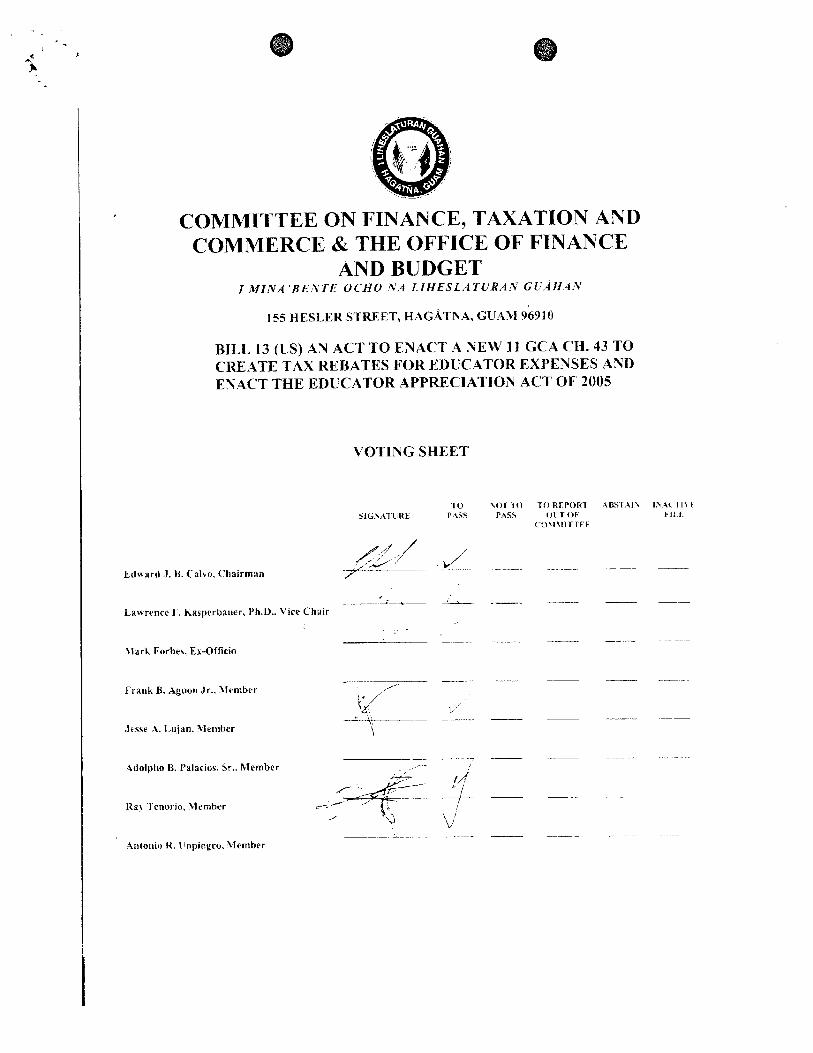

COMMITTEE ON FINANCE, TAXATION AND COMMERCE & THE OFFICE OF FINANCE

AND BUDGET I M I N A 'BEIVTE OCEIO NA L I H E S L A T U R . 4 3 GU.4H/1:V

155 HESLER STREET, H A G . & T ~ A , GUAM 96910

BILL 13 (LS) AN ACT TO ENACT A NEW 1 1 GCA CH. 43 TO CREATE TAX REBATES FOR EDLTATOR EXPENSES .AND ENIQCT THE EDUCATOR APPRECIATION ACT OF 2005

VOTING SHEET

TO \OTTO TO RCPORT ABST.Ai\ 1h.AC.l I \ k SlC;.\ATL:HE 1'455 P4SS O I T O F hILC

CDi1MJTTFF

Edwsrtl J . H. Calvo. Chairman

- - - Laurence F. Kaspcrbauer, Ph.21.. Vice Chair

Fra~ ih B. Aguon Jr.. l iember

Jrsse 1. Lujan. 3lember

-- - -- - idulpho B. Palac~os, Sr,. klembcr .- -

-L-

l- 14 ' 1 7- - - - Rat lcnorro, \Iemher

, G \ I

i/

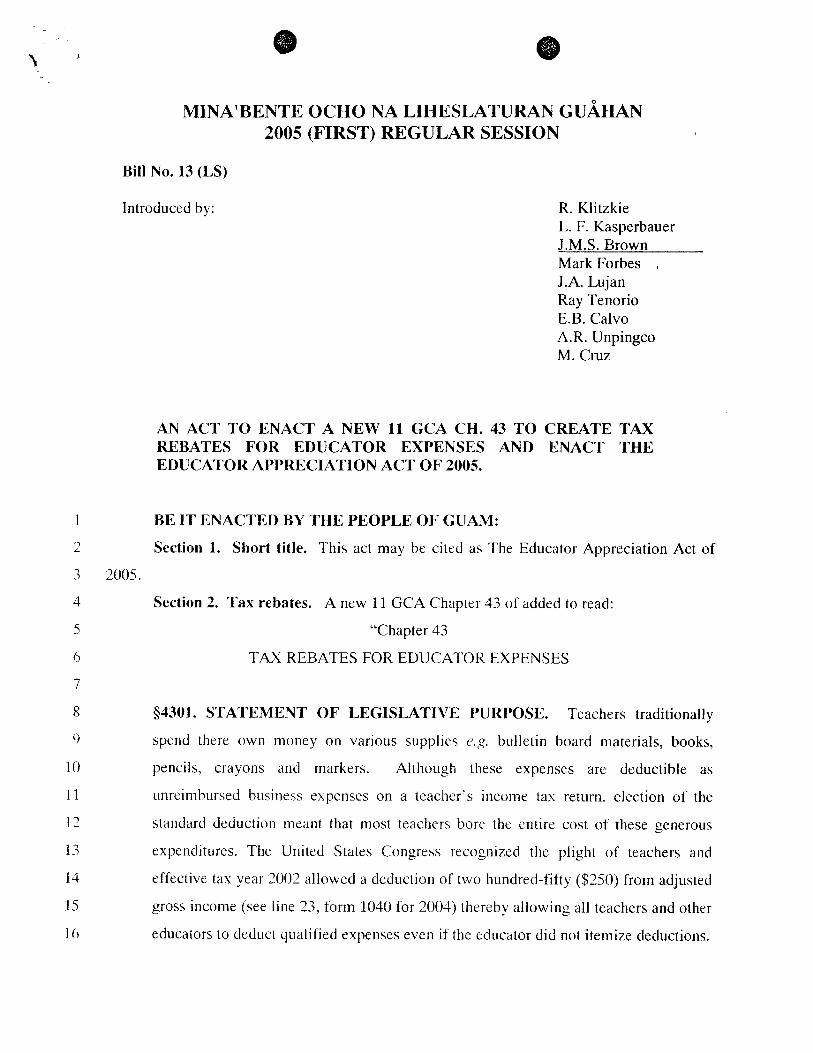

MINA'BENTE OCHO NA LIHESLATURAN GUAHAN 2005 (FIRST) REGULAR SESSION

Bill No. 13 (LS)

Introduced by: R. Klitzkie L. F. Kasperbauer J.M.S. Brown Mark Forbes , J.A. Lujan Ray Tenorio E.B. Calvo A.R. Unpingco M. Cruz

AN ACT TO ENACT A NEW 11 GCA CH. 43 TO CREATE TAX REBATES FOR EDUCATOR EXPENSES AND ENACT THE EDUCATOR APPRECIATION ACT OF 2005.

BE IT ENACTED BY THE PEOPLE OF GUAM:

Section 1. Short title. This act may be cited as The Educator Appreciation Act of

2005.

Section 2. Tax rebates. A new 11 GCA Chapter 43 of added to read:

"Chapter 43

TAX REBATES FOR EDUCATOR EXPENSES

$4301. STATEMENT OF LEGISLATIVE PURPOSE. Teachers traditionally

spend there own money on various supplies e.g. bulletin board materials, books,

pencils, crayons and markers. Although these expenses are deductible as

unreimbursed business expenses on a teacl~er's irlcome tax return, election of the

standard deduction meant that most teachers bore the entire cost of these generous

expenditures. The United States Congress recognized the plight of teachers and

effective tax year 2002 allowed a deduction of two hundred-fifty ($250) from adjusted

gross income (see line 23, form 1030 for 2004) thereby allowing all teachers and other

16 educators to deduct qualified expenses even if the educator did not itemize deductions.

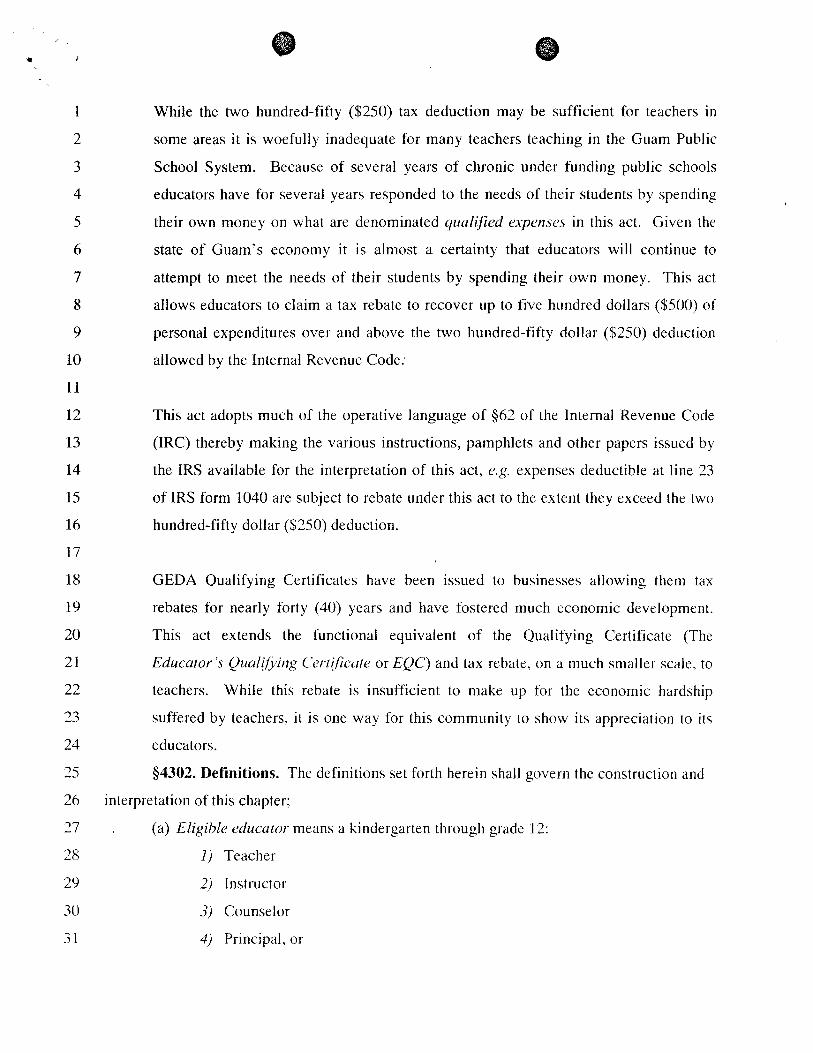

1 While the two hundred-fifty ($250) tax deduction may be sufficient for teachers in

2 some areas it is woefully inadequate for many teachers teaching in the Guam Public

3 School System. Because of several years of chronic under funding public schools

4 educators have for several years responded to the needs of their students by spending

5 their own money on what are denominated quulified experzses in this act. Given the

6 state of Guam's economy it is almost a certainty that educators will contiilue to

7 attempt to meet the needs of their students by spending their own money. This act

8 allows educators to claim a tax rebate to recover up to five hundred dollars ($500) of

9 personal expenditures over and above the two hundred-fifty dollar ($250) deduction

10 allowed by the Internal Revenue Code:

11

12 This act adopts much of the operative language of $62 of the Internal Revenue Code

13 (IRC) thereby making the various instructions, pamphlets and other papers issued by

14 the IRS available for the interpretation of this act, e.g. expenses deductible at line 23

15 of IRS form 1040 are subject to rebate under this act to the extent they exceed the two

16 hundred-fifty dollar ($250) deduction.

17

18 GEDA Qualifying Certificates have been issued to businesses allowing the~n tax

19 rebates for nearly forty (40) years and have fostered much economic development.

20 This act extends the functional equivalent of the Qualifying Certificate (The

2 1 Educulor 's Qzwlfying C'crtificule or EQC) and tax rebate, on a much smaller scale, to

22 teachers. While this rebate is insufficient to make up for the economic hardship

23 suffered by teachers, i t is one way for this community to show its appreciation to its

24 educators.

25 $4302. Definitions. The definitions set forth herein shall govern the construction and

26 interpretation of this chapter;

27 , (a) Eligible educator- means a kindergarten through grade 12:

28 I ) Teacher

29 2) Instructor

30 3) Counselor

3 1 4) Principal, or

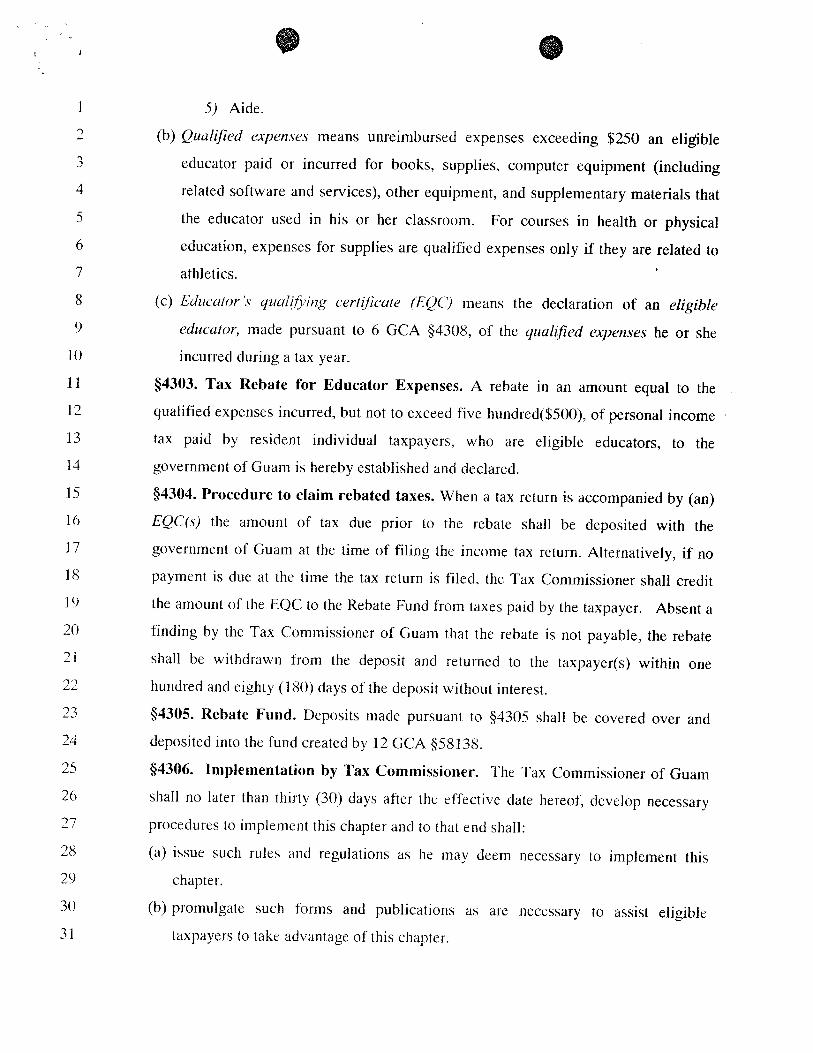

5) Aide.

(b) Quulified expetzses means unreimbursed expenses exceeding $250 an eli&ble

educator paid or incurred for books, supplies, computer equipment (including

related software and services), other equipment, and supplementary materials that

the educator used in his or her classroom. For courses in health or physical

education, expenses for supplies are qualified expenses only if they are related to 1

athletics.

(c) Edzica/or.'.r yzrulifiirzg certificate (EQC) means the declaration of an eligible

educatoi; made pursuant to 6 GCA 54308, of the quulified expenses he or she

incurred during a tax year.

$4303. Tax Rebate for Educator Expenses. A rebate in an amount equal to the

qualified expenses incurred, but not to exceed five hundred($500), of personal income a

tax paid by resident individual taxpayers, who are eligible educators, to the

government of Guam is hereby established and declared.

$4304. Procedure to claim rebated taxes. When a tax return is accompanied by (an)

EQC(s) the amount of tax due prior to the rebate shall be deposited with the

government of Guam at the time of filing the income tax return. Alternatively, if no

payment is due at the time the tax return is filed, the Tax Commissioner shall credit

the amount of the EQC to the Rebate Fund from taxes paid by the taxpayer. Absent a

finding by the Tax Commissioner of Guam that the rebate is not payable, the rebate

shall be withdrawn from the deposit and returned to the taxpayer(s) within one

hundred and eighty (180) days of the deposit without interest.

$4305. Rebate Fund. Deposits made pursuant to $4305 shall be covered over and

deposited into the fund created by 12 GCA $58138.

$4306. Implementation by Tax Commissioner. The Tax Commissioner of Guam

shall no later than thirty (30) days after the effective date hereof, develop necessary

procedures to implement this chapter and to that end shall:

(a) issue such rules and regulations as he may deem necessary to implement this

chapter.

(b) promulgate such forms and publications as are necessary to assist eligible

taxpayers to take advantage of this chapter.

(c) develop a procedure to allow the set off of an unpaid tax rebate from a prior year

against a current year's tax liability.

$4307. Sunset Provision. This act shall be ineffective in the tax year following the

receipt by the Director of Revenue and Taxation of the certificate of the

Superintendent of Education that it is no longer necessary for eligible educators to

spend there own money on quulified expenses, as those terms are defined in $4302, in

order to provide an adequate public education.

$4308. Construction. Subsections 4302(a) and (b) of this chapter are substantially

similar to §62(a)(2)(D) of the Internal Revenue Code [26 USC §62(a)(2)(D)] and

should be construed consistently therewith except where manifestly inapplicable.

$43409. Effective dates. This act is effective upon adoption provided that the tax

rebate created by $4303 shall be effective for tax liability arising in 2005."

MINA'BENTE OCHO NA LIHESLATURAN GU- 2005 (FIRST) Regular Session

Bill No. 13 (LS)

Introduced by: As Substituted by the Committee on

Finance, Taxation & Commercc

R. Klitzkie L. F. Kasperbauer J.M.S. Brown, C

Mark Forbes J.A. Lujan Ray Tenorio E.B. Calvo A.R. Unpingco M. Cruz

AN ACT TO ENACT A NEW 11 GCA CH. 43 TO CREATE TAX REBATES FOR EDUCATOR EXPENSES AND ENACT THE EDUCATOR APPRECIATION ACT OF 2005.

BE IT ENACTED BY THE PEOPLE OF GUAM:

Section 1. Short Title. This act may be cited as "The Educator

Appreciation Act of 2005".

Section 2. Tax rebates. A new 11 GCA Chapter 43 ef added to read:

The Eclucator Appreciation Act TAX REBATES FOR EDUCATOR EXPENSES

$4301. STATEMENT OF LEGISLATIVE PURPOSE. Teachers

traditionally spend there own money on various supplies (Le.g. bulletin board

31 materials, books, pencils, crayons and markers). Although these expenses are

deductible as unreiinbursed business expenses on a teacher's income tax return,

election of the standard deduction meant that most teachers bore the entire cost

of these generous expenditures. The United States Congress recognized the

plight of teachers and effective tax year 2002, allowed a deduction of two

hundred-fifty dollars ($250) from the adjusted gross income (see line 23, IRS Form 1040 for 2004) thereby allowing all teachers and other educators to deduct

qualified expenses even if the educator did not itemize deductions.

While the two hundred-fifty dollar ($250) tax deduction may be sufficient

for teachers in some areas, it is woefully inadequate for many teachers teaching

in the Guam Public School System. Because of several years of chronic&

under funding public schools, educators have for several years responded to the

needs of their students by spending their own money on what are denominated

qualified expenses in this act. Given the state of Guam's economy, it is almost a

certainty that educators will continue to attempt to meet the needs of their

students by spending their own money. This act allows educators to claim a tax

rebate to recover up to five hundred dollars ($500) of personal expenditures over

and above the two hundred-fifty dollar ($250) deduction allowed by the Internal

Revenue Code.

This act adopts much of the operative language of $62 of the Internal

Revenue Code (IRC) thereby making the various instructions, pamphlets and

other papers issued by the IRS available for the interpretation of this act, e.g.

expenses deductible at line 23 of IRS form 1040 are subject to rebate under this

act to the extent they exceed the two hundred-fifty dollar ($250) deduction.

GEDA Qualifying Certificates have been issued to businesses allowing

them tax rebates for nearly forty (40) years and have fostered much economic

development. This act extends the functional equivalent of the Qualifying

Certificate (The educator.'^ Quallfiing Cert~ficate or EQC) and tax rebate, on a

much smaller scale, to teachers. While this rebate is insufficient to make up for

the economic hardship suffered by teachers, it is one way for this community to

show its appreciation to its educators.

$4302. Definitions. The definitions set forth herein shall govern the

construction and interpretation of this chapter;

(a) Eligible educator means a kindergarten through grade 12:

I ) Teacher

2) Instructor

3) Counselor

4) Principal, or

5) Aide.

(b)Qualfied expenses means unreimbursed expenses exceeding two

hundred fifty dollars [$250) less any unreimbursed employee expenses

upon which a deduction from adjusted g;ross income is based that an

eligible educator paid or incurred for books, supplies, computer

equipment (including related software and services), other equipment,

and supplementary materials that the educator used in his or her

classroom. For courses in health or physical education, expenses for

supplies are qualified expenses only if they are related to athletics.

(c) Edzrcator's qualzfiing ceutzficate (EQC) means the declaration of an

eligible educator, made pursuant to 6 GCA $4308, of the qualified

expenses he or she incurred during a tax year.

$4303. Tax Rebate for Educator Expenses. A rebate in an amount equal

to the qualified expenses incurred, b u ~ not to exceed five hundred dollars ($500),

of personal income tax paid by resident individual taxpayers, who are eligible

educators, to the government of Guam is hereby established and declared.

$4304. Procedure to claim rebated taxes. When a tax return is

accompanied by (an) EQC(s) the amount of tax due prior to the rebate shall be

deposited with the government of Guam at the time of filing the income tax

return. Alternatively, if no payment is due at the time the tax return is filed, the

Tax Commissioner shall credit the amount of the EQC to the Rebate Fund from

taxes paid by the taxpayer. Absent a finding by the Tax Commissioner of

Guam that the rebate is not payable, the rebate shall be withdrawn from the

deposit and returned to the taxpayer(s) within one hundred and eighty (180) days

of the deposit without interest.

$4305. Rebate Fund. Deposits made pursuant to $4305 shall be covered

over and deposited into the fund created by 12 GCA $58138.

$4306. Implementation by Tax Commissioner. The Tax

Commissioner of Guam shall no later than thirty (30) days after the effective

date hereof, develop necessary procedures to implement this chapter and to that

end shall:

(a)Issue such rules and regulations as he may deem necessary to

implement this chapter.

(b)promulgate such forms and publications as are necessary to assist

eligible taxpayers to take advantage of this chapter.

(c) develop a procedure to allow the set off of an unpaid tax rebate from a

prior year against a current year's tax liability.

$4307. Sunset Provision. This act shall be ineffective in the tax year

following the receipt by the Director of Revenue and Taxation of the certificate

of the Superintendent of Education that it is no longer necessary for eligible

educators to spend there own money on quulijied expenses, as those terms are

defined in $4302, in order to provide an adequate public education.

$4308. Construction. Subsections 4302(a) and (b) of this chapter are

substantially similar to §62(a)(2)(D) of the Internal Revenue Code 126 USC

§62(a)(2)(D)] and should be construed consistently therewith except where

manifestly inapplicable.

$43409. Effective dates. This act is effective upon adoption provided

that the tax rebate created by $4303 shall be effective for tax liability arising in

2005.

Waiver on Fiscal Note

i n accordsiice with $9105 of Title 2 GCA, 1 hereby certify that prompt

committee action on Bill Number 13 (LS) is necessary for the proper conduct

of legislative business. Therefore, 1 am waiving the requirement Cor a fiscal

note on Bill Number 13 (LS).

Edward J.B. Calvo Chairman Cornrnitlee on Finance, Taxatiorl and Commerce

I I. OVERVIEW

The Committee on Finance, Taxation and Commerce and the Office of Finance and Budget held a public hearing on Tuesday, January 25, 2005 at 930 AM at the Guam Legislature public hearing room in Hagatna, Guam. Notice of public hearing was disseminated throughout all local media via fax (see attached).

Senators present were: Senator Eddie Calvo, Chairman Vice Speaker Joanne Brown Speaker Mark Forbes Senator Robert Klitzkie Senator Larry Kasperbauer Senator Lou Leon Guerrero Senator Jesse Lujan Senator Adolpho Palacios Senator Antonio Unpingco Senator Judith Won Pat

11. SUMMARY OF TESTIMONY

The following bill was heard at the public hearing in which oral and/or written testimony were provided:

BILL 13 (LS) AN ACT TO ENACT A NEW 11 GCA CH. 43 TO CREATE TAX REBATES FOR EDUCATOR EXPENSES AND ENACT THE EDUCATOR APPRECIATlON ACT OF 2005.

Senator Robert Klitzkie's Remarks:

Senator Klitzkie described Bill 13 as a display of gratitude towards teachers working in local schools. He referenced the Internal Revenue Code provision of a $250 deduction for educators, but stated that a $250 deduction is inadequate for Guam teachers. He explained the need to supplement the deduction with a $500 rebate to compensate teachers for spending their own money on school supplies. Klitzkie explained Bill 13 as having a "salutary purpose of reimbursing teachers 'some' of the money out their own pockets."

Oral testimony only for Bill 13 public hearing was provided by the following individuals:

1. Senator Antonio Unpingco, Spouse of a Teacher & Local Resident

Senator Antonio Unpingco presented oral testimony in favor of Bill 13. As a husband of a local teacher, he has witnessed the use of personal funds to purchase supplies for the classroom. He quoted expenditures of up to $4,000 for school supplies by his wife. He commented that Bill 13 is "good as a matter of appreciation."

I

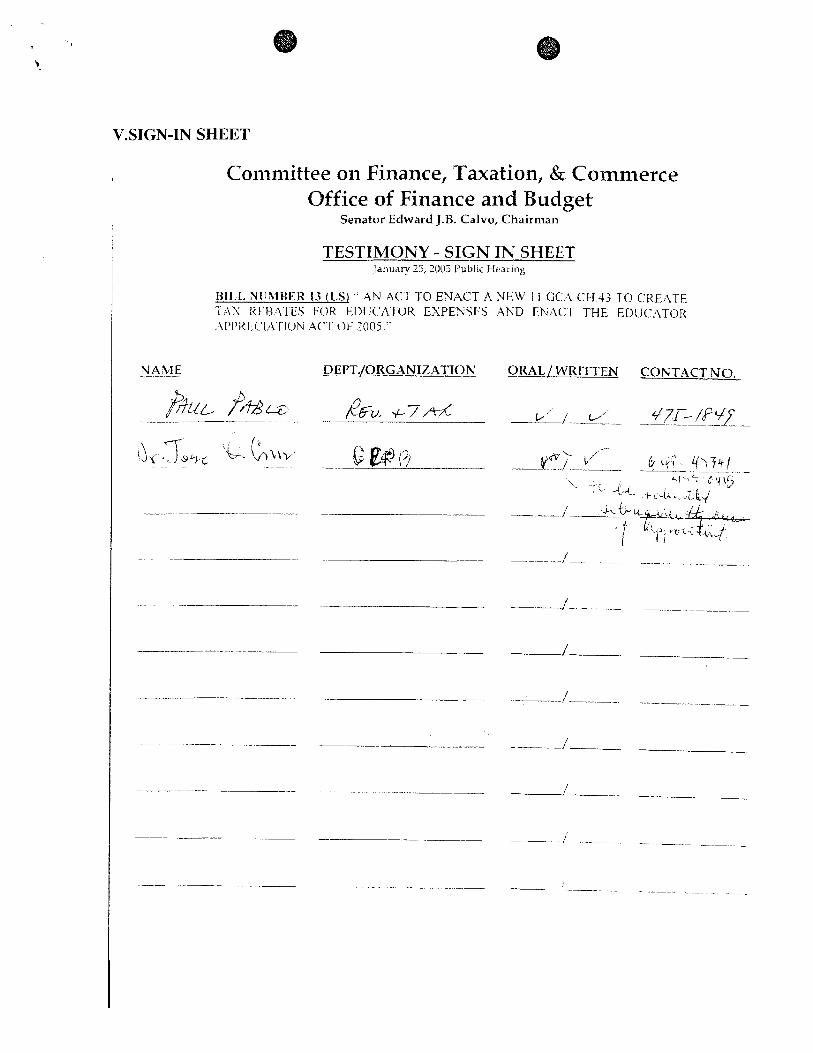

2. Paul Pablo, Tax Enforcement Administrator, Dept. of Revenue and Taxation

Mr. Pablo presented oral testimony in opposition of Bill 13. He expressed his understanding of the need to compensate teachers, but voiced reservations on the opportunity for "double benefits" presented by Bill 13. He referenced the Schedule A form that can be filed with a 1040, allowing educators to itemize unreimbursed employee expenses when the expenses exceed 2% of adjusted gross income. Pablo stated that this is "not the right time to '

do i t with the state of rev and tax."

Written testimony only for Bill 13 public hearing was provided by the following individual:

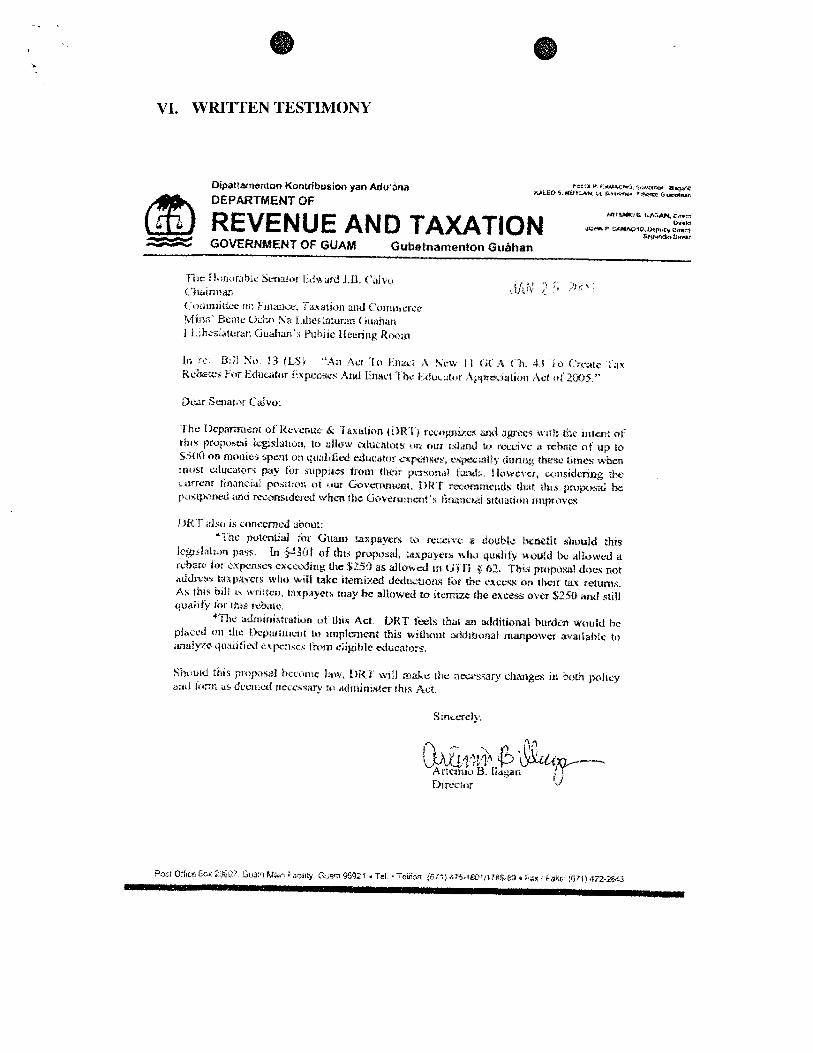

1. Artemio B. Ilagan, Director, Department of Revenue and Taxation

Mr. Ilagan submitted written testimony in opposition of Bill 13. He reported that the Department of Revenue and Taxation (DRT) agrees with the intent of the bill, but recommends postponement due to the financial status of the government. He stated concerns on the double benefit educators may receive if they deduct unreimbursed employee expenses and clainl the rebate. Ilagan also said that additional manpower is needed to analyze qualified expenses. He said the DRT will work with the law in the event Bill 13 is enacted.

111. FINDINGS AND RECOMMENDATION

Chronic under-funding of public schools has led to an increase in teacher spending on school supplies over the years. Classrooms have been left unequipped with books, pencils, crayons, paper, glue. scissors. and erasers. The only way for educators to address the problem is to spend their own money to ensure their classrooms are properly equipped.

In 2002 the United States Congress recognized the necessity for teachers to spend there own money on their jobs and implemented a two-hundred-fifty ($250) deduction from income for educators. The enactment of Bill 13 would allow teachers to receive an additional rebate of $500 for expenses over and above the $250 deduction. While the $250 deduction may be adequate for teachers in some areas, the current state of the Department of Education (DOE) shows that this amount will not suffice for public school teachers on Guam.

Bill 13 addresses this issue and attempts to compensate local teachers by supplementing the $250 amount with a rebate of $500. The requirement for an Educator's Qualifying Certificate (EQC) is outlined to ensure only eligible educators are rebated qualified expenses, as defined in $4302. The bill "piggy backs" on the $250 provision already enacted in the Internal Revenue Service Code (IRC), in particular, $62. Replicating materials used by the IRS would provide ease of administration for DRT in granting the $500 rebate to local teachers.

Additionally, the bill creates a sunset provision in $4307 to discontinue the increased benefit after the Superintendent of DOE certifies to the Director of Revenue and Taxation that teachers no longer need to spend their own money to provide an adequate education. The goal is to reimburse some of the money to educators through the, rebate until our government can afford to provide adequate resources to our students.

Public testimony on Bill 13 was very supportive of the need to compensate educators, though some individuals presented concerns for the opportunity of a "double benefit." Line 23 (educator expenses) on form 1040 allows educators to take advantage of the $250 deduction. In addition, line 20 on the Schedule A form provides the option for itemizing unreimbursed employee expenses not already covered, which exceed 2% of the amount on line 37 of the 1040. The simultaneous use of the Schedule A itemized deductions and the $500 rebate presented by Bill 13 could result in a "double benefit" for educators.

In considering the testimony, the committee finds that to address the potential of a "double benefit" an additional element is needed in the definitional section of Bill 13. Therefore, the committee recommends that subsection (b) of $4302 be amended to read:

$4302. Definitions. The definitions set forth herein shall govern the construction and interpretation of this chapter;

(b) Quulifird expenses means unreimbursed expenses exceeding $250 less any unreimbursed employee expenses upon which a deduction from adiusted gross income is based that an eligible educator paid or incurred for books, supplies, computer equipment (including related software and services), other equipment, and supplementary materials that the educator used in his or her classroom. For courses in health or physical education. expenses for supplies are qualified expenses only if they are related to athletics.

The committee recommends that a substitute bill be prepared incorporating the findings and recommendations of the committee. The substitute bill is submitted herewith.

Accordingly, the Committee on Finance, Taxation and Commerce and the Office of Finance and Budget does hereby submit it's findings and recommendations to I Mirw ' Belzle

Ocho Nu Lilzesluturan Guatzurz TO PASS BILL 13 (LS) AN ACT TO ENACTA NEW I 1 GCA CH. 43 TO CREATE TAX REBATES FOR EDUCATOR EXPENSES AND ENACT THE ED UCA TOR A PPRECIA TION ACT OF 2005.

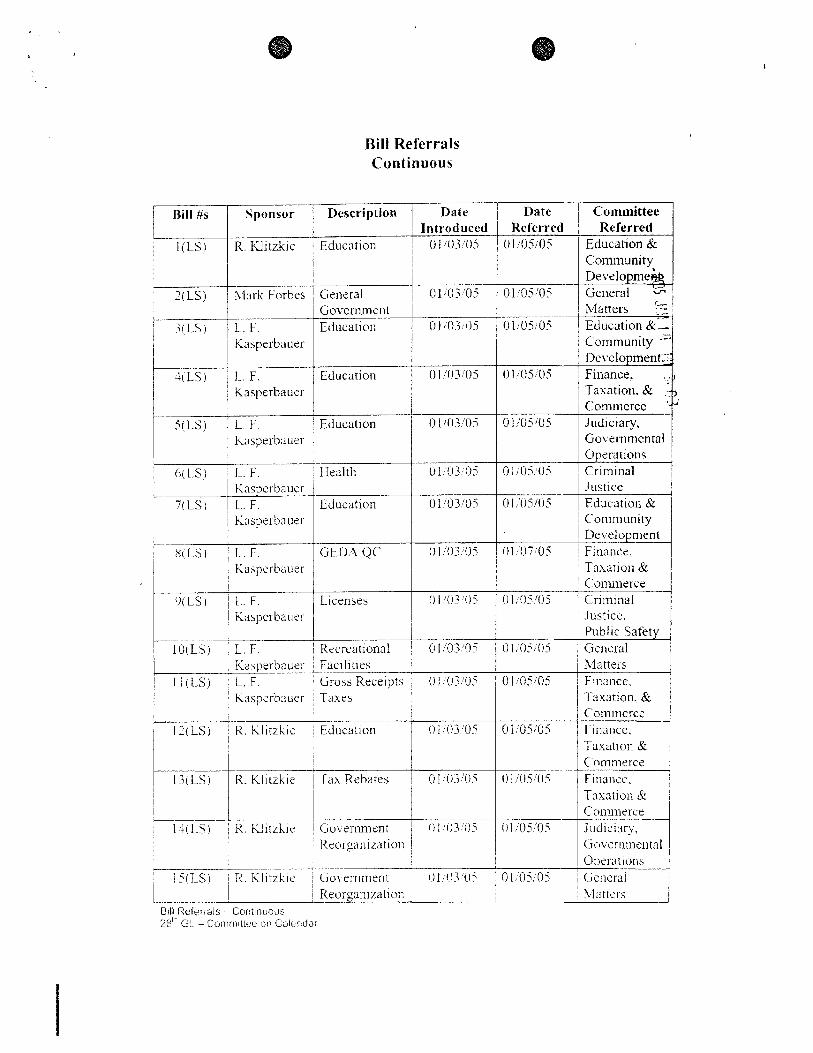

Bill Referrals Continuous

Date Introduced

0 I '0.3 05

4iLSi / I. F. Education i 0 1 iO305 j Knsperbauer

j I

5lLS) L t I Education Kd\per Lxuer

I

0 1 :U3 05

; S!LSi

I

iiasprrbatier Fac~lities I I(LS) L. F. : Gross Receipts 0 I ;O?.'OS

(j 1 .'03;05

0 1 '03.'0-5

i b(LS) / L . F . : I-iealth i 1 Knspcrbaucr

9(LS) 1 L . F . ! Kiisperbaurr

L . F .

Kasperbauer

Committee

C:ommunity

kducation I 7(LS)

Licenses

I I

0 1 '05 '0 5 1 General 's

L. F. Kasperbauel-

GEDA QC

0 l !03 ' 0 5

/ Matters i?: 01,05 O i 1 Education &,;

0 I i03 'rli

I7( LS)

I Community "1

I

Education R. Kli:zl\ie

a Dcvclopment:" 0 1 ,05105 Finance.

O I '03A3.i

I Operations 0 1 ;05,!05 I Crtrninal 1 I

--, '-"

; Taxation. &

Bill Referrals - Contimioiis 28" GL - Coinni~ttee on Crjlendar

0 1 '0545

Jitsticz 0 I ,'05!05 Education 6r

Community

Finance. 1 Taxanon & i C:ollmerct:

0 1 .'05.'05 C'riminai .I~sticc. Public Safety

0 ' 0 0 : Cier~cral / Matters

01.:05:'05 / Flriancc.

C'omrncrcc Judlcrary, Go1 ernmcntal

0 1,'05:05

01/()5:0i

- 01 i()5:[)5

1 ' 5 : C;cilcral I \ I ~ ~ ~ ~ I - s i

1-asation: & Comrnercc Finance. Taxation BL Commerce Finnnsc. Taxation & Cnilxnercr J~~dici;try- (io~:cniin~11tal ,

'

Operations - ,

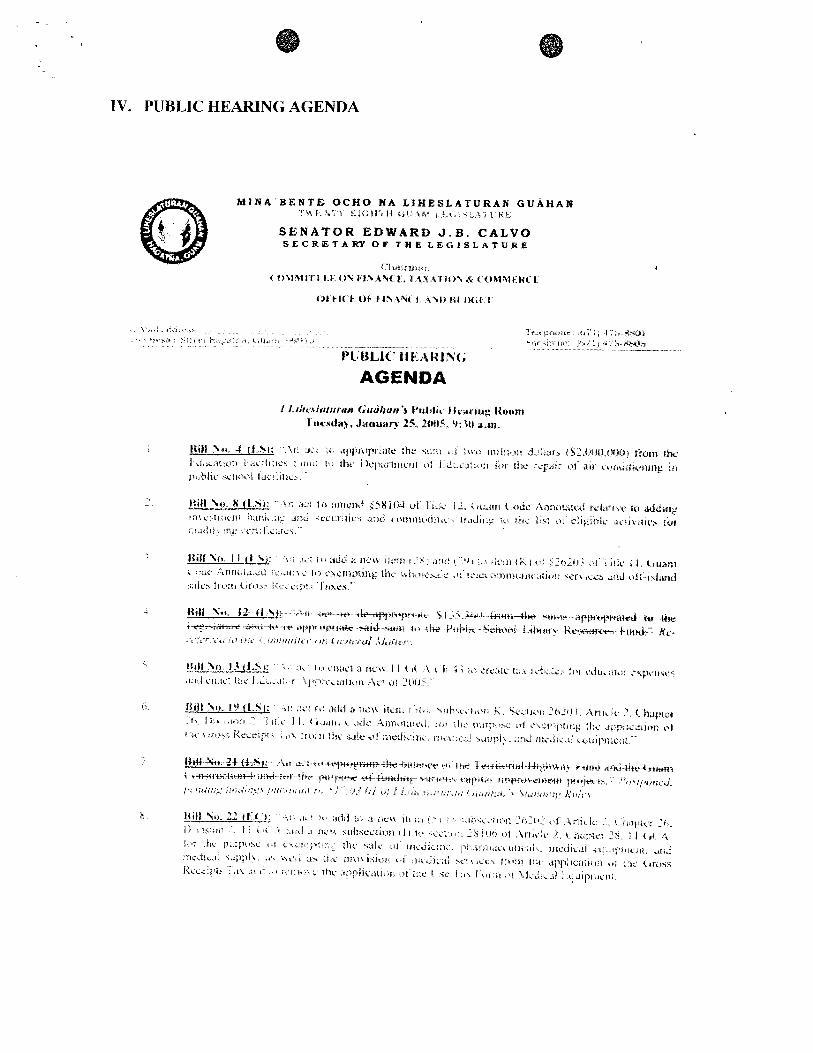

IV. PUBLIC HEARING NOTICE

IV. PUBLIC HEAFUNG AGENDA

M l H A B E H T E OCHQ N A L l H E S L A T U R A P i C p U A H A l ' \ \ I ' 3 - i : 3 < x l i ' k I b L \ k $ L!,( . - % > i + k

S E N A T O R EDWARD J.B. CALVO S E C R E T A R Y O F T f l E L E G I S L A T I I R B

1:i 4&! r1i.t*.

i t+U%tfi f I ). O\ I ,BX,i%i K , ' B A \ 4 1 1 . 1 > \ h < C)%lbl#&1Cl

'L',,.$ . g;,lt..,.:- " . - -.- 1t;t (;:irrnc ; d l ; : , .I':,: E.St)P 7.-. : i r st.: ..I:, . I /Il'<,+:: l,. t i l j * i i : l ' ^ 1 1 f 1 1 , I ...- , .. . . - .. . .. - - - - . ? < $ ( %l2.,ll!.' I t * , , : J ,'h-8%F&bJ . .

Pl~lJLIC: 13 EAKlil'C;

AGENDA

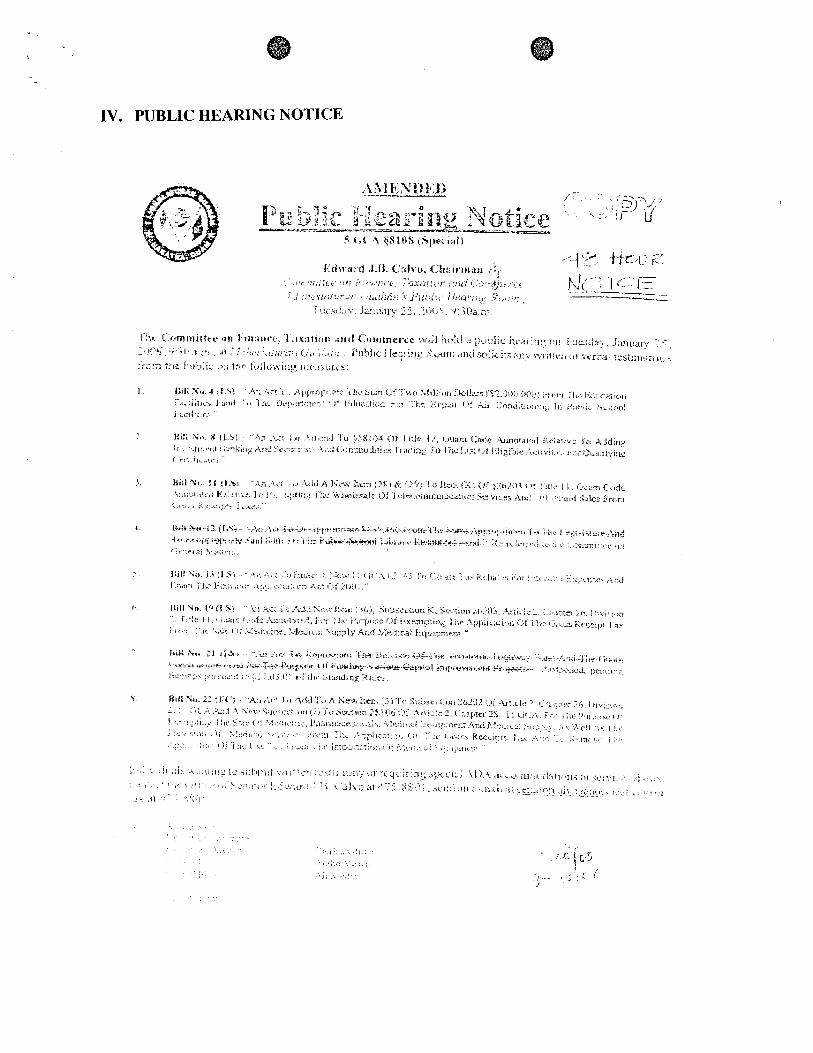

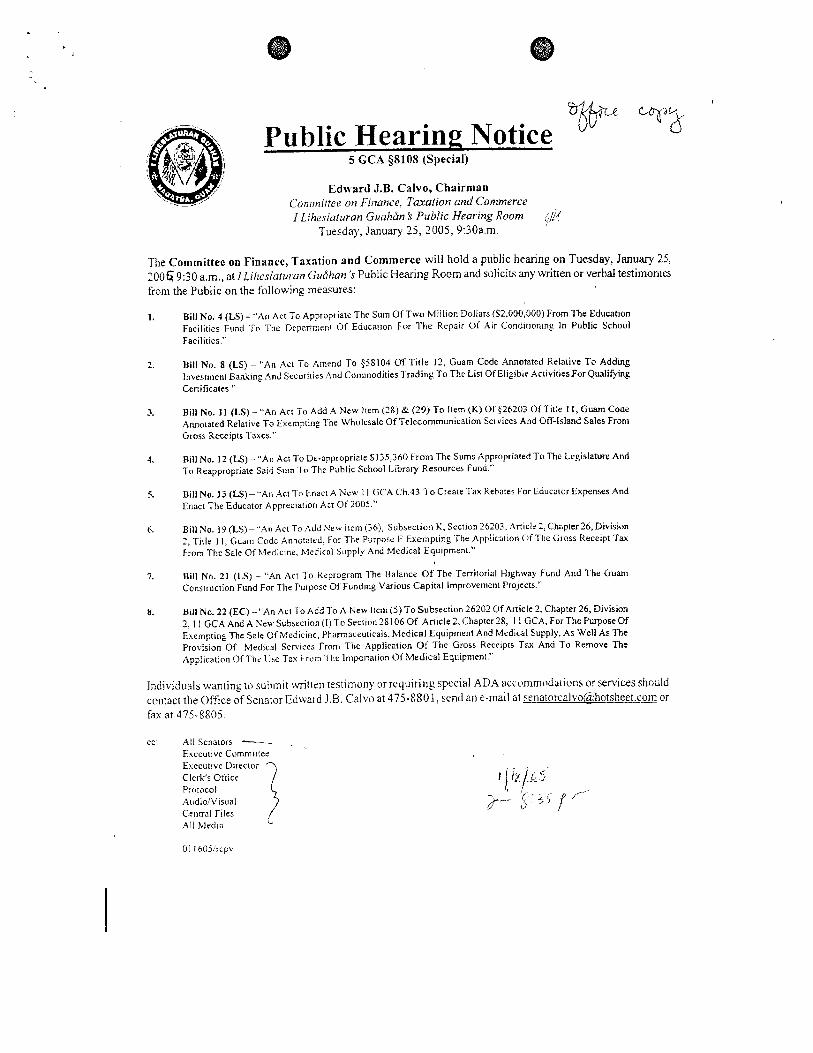

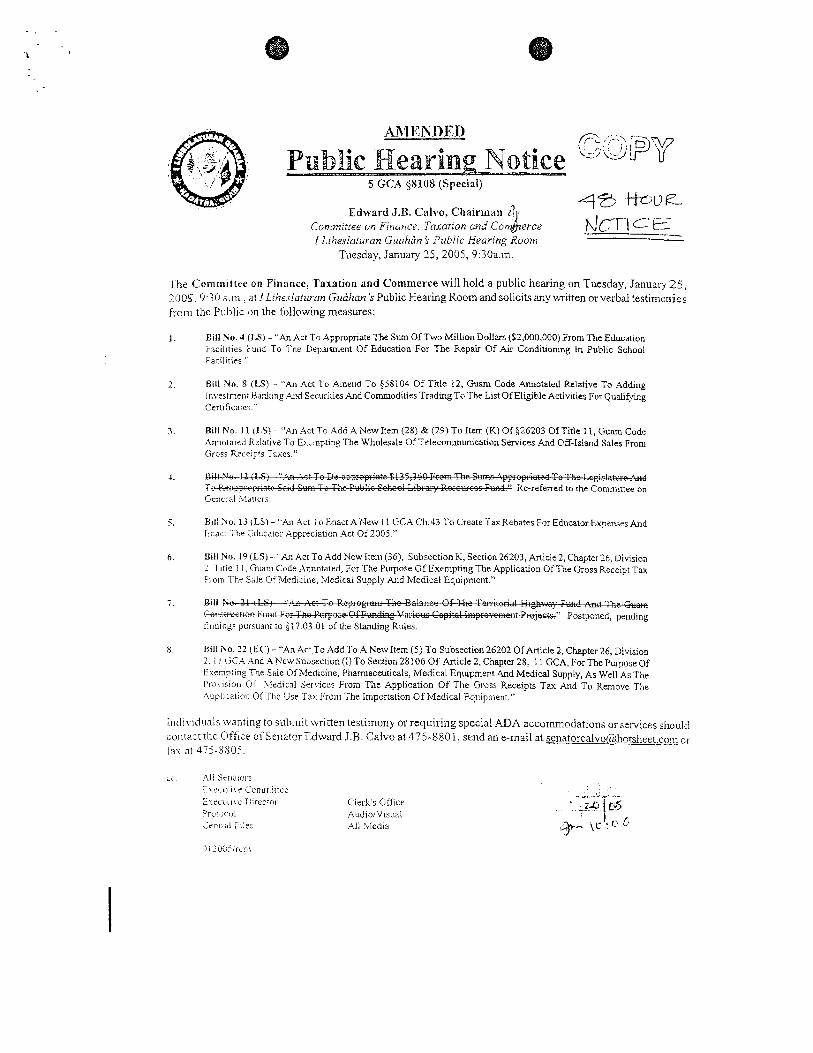

Public Hearing: Notice 5 GCA $8108 (Special)

Edward J.B. Calvo, Chairman Coniruirree on Finance, Taxation and Commerce I Liherlnturan Guahdnk Public Hearing Room {/id

Tuesday, J a n u q 25,2005,9:30a.m.

The Committee on Finance, Taxation and Commerce will hold a public hearing on Tuesday, January 25. 2006 9:30 a.m., at ILiheslaturon Gudllan 's Public Hearing Room and solicits any written or verbal testimonies from the Public on the following measures:

1. Bill No. 4 (LS) - "An Act To Appropriate The Sum Of Two Miilion Dollars (%2.000,000) From The Education Facilities Fund To The Drpartn~ent Of Education For The Repair Of Air Conditioillng In Public School Facilities."

2. Bill No. 8 (LS) - "An Act To Amend To $58104 Of Title 12, Guam Code Annotated Relative To Adding Investment Bak ing And Securities And Colnmodities Trading To Tile List Of Eligible ActivitiesFor Qualifying Ccnificatcs."

3. Bill No. 1 l (LS) -"An Act To Add A New lrem (28) & (29) To kern (K) Of 526203 Of Title 11, Guam Code Annotated Relative To Exempting The Wholesale Of Telecommunication Services And Off-Island Sales From Gross Receipts Taxcs."

1. Bill No. 12 (LS) -"An Act To De-appropriate $135,360 From The Sums Appropriated To The Legislature And To Reappropriatc Said Sum To The Public School Library Resources Fund."

5. Bill No. 13 (LS) - '.An Act To Enact A New 1 1 GCA Ch.43 TO Create Tax Rebates For Educator Expenses And Enact The Educator Appreciat~on Act Of 2005."

6. Bill No. 19 (LS)-'.An Act To AddNeit ltem (36). Subsection K , Section 26203.Anicle 2, Chapter26,Division 2, Title I I, Guam Code Annotated. For The Purpose F Exempting The Application Of The Gross Receipt Tax From The Sale Of Medicine. hledicnl Supply And Medical Equtpment."

7. Bill No. 21 (LS) - '.An Act To Reprogram The Balance Of The Terrirorial Highway Fund And The Guam Construction Fund For The Purpose Of Fund~ng Various Cap~tal Improvement Projects."

8. Bill No. 22 (EC) -'.An Act To Add To A New ltem (5) To Subsection 26202 Of Aniclc 2. Chapter 26, Division 2,11 GCA And A Kew Subsection (1) To Section 28106 Of Article 2, Chapter 28, I 1 GCA, For The Purpose Of Evenipting Thc Sale Of Medicme, Pharmaceuticals, Medical Equipment And Medical Supply, As Well As The Provision Of Medical Sew~ces From The Application Of The Gross Recelpts Tax And To Remove The Application Of The Use Tau From The Importation Of Med~cal Equipment."

Individuals wanting to submit written restirnony or requiring special ADA accommodations or services should contact the Office of Senator Edtvard J.B. Calvo at 475-8801, send an e-mail at senatorcalvo6?hotsheet.cgj or fax at 475-8805.

cc. All Scnarors ----. ;

Esecui~ve Comrnitiee Executive Director Clerk's Office Protxol Audio;\'csual Central Files ,411 Media

1 I

Public Hearing Notice 1 GC.4pBlW Pp-0

~d" rd1 .a ma- coarm"" n >-<. TmolrmdCo,--ir 1 luuI.,'r.cn w t ?.we nrsrsne R R :*

- ' A Cnnm 18r. oo ),i.a.. Tssmnvs sndC.nrrtrr~ n l l r.- i ro- I: Lr.8 7 ..> T r q 1 , . ~ 2 < , r -5 ' ! r c . r : I l . L , ' w . r . j L C h u , h n l i < r k r q r - ~ l % ~ L . " , rin-Z,.-.--

m.n *r r.,r.r m . r e ( n l r - n g m & . r e ,

, Public Hearing Notice 5 CCA i a l ~ (sporl)

~ ~ . . r d la c.hh r ~ . = Ccnmulw on F i n a r t . r . a ~ d C w m r : c r ILlh3lm.m L w M " + PLbh H H H H 1 1 ,I

Public hear in^ Notice d GCA &SIC8 (Swdrll

mrsd J a UI,-, cb.bn.. -. Cnmvrrr m ii-. Tmmm l m d C w m w n

iirn.o,wmr-k>mbzr .Vau<m P a m ilrr

j mir. z~clsi--*r.~r~r~+pe n c i a r r r u n r r a - - - r ~ ~ ~ pa- ~ ) . ~ ~ , m - + . r v p . e n r - r.--~- -w-L-

1 Public Hearing Xotice s cc* (elm tsp-1,

&dx.rdJn. Gh* Cb.h.n C~'"rnl~< O n 6 i r o r n . T - . , ~ n r d C m u r u 1 L : h r i l ~ o n ~ I KUKU h , m , A m .h-

; @ Public Hearing Notice 5 6 r A 68108 (9pmd)

i ... ., ' Edr0.d JS. C&o, 0 n r l u . l l

cmn;nrr so i ~ w x r rm- mi co-m L . . " i r t i R Fj(

~iudi:, z, 1 ~ s . ~ )ram.

, .UI. USE'. U I . . , , I,,.. L *., ., . ID,.=- . 6 X l l i ' l * r . l 1 1 3 3 r m U - - ' I it, ,...*.-..*"in , . * 7 m . 8 0 a C . m . - > ~ . * ' c * , r l " P . V ' l .. ",,, ., ,I" ..-, .h.rc.rr,.. * ...I I & . + " M * d * L V O 1 . ..?... U>

I r .,-.. \-,,-I- I.. .+p.**L 0: k ..a. 1mG.37.3 *Y T, b7. I. ,;iL -̂ _, .. L..'..,, 'n I t . . V " I L I P o l U ~ I I " O - Y -

, ' - ~ : - > . , - . r.,, , , + i ' , . ,

-- . - . .. - - . .. ~

: L : : b = - 3 . - 7 -. - .. . -, I , . , . i - * 1 . , , . z e : . . - . . . - -. I 5 - .- --

, . . ,. . . , - - . . - . = . , I , - , . - ~ , I I: 8 = - . - . . . . - , ~- ..- - --

i - - i . . .. - ' Z - . , . - - - . - . Z C - - c 4

- - . - . , - . - ~ . . . , . - - L - r . . , = _ - . .

. . . . . . - . . . , - ,

. - . . - - , . - r r . 1 . ,.-,-I - . . . , . , - 7

- - a - . . . .'. - - . , - r .: r , . , 7 - - - 3 , - - - .. - * - . - G,,'. F : - .

Public Hearing Notice , s~.c .44alM(Sprt .I )

Fdr.rdI*B Cab- Cb-= r.-vm on Fmvn 7-un d T c m , c s

Public Hearing Notice .a* $sics (spod.0

?Award 18. C n h , Cblbm.. Cnnn*" 111 F?n-, I - ;O*~CDMUCI ~ L & M W ~ ~uo*dn t M:C enme RP .a

I [ @ Public hear in^ Notice

5 GCA L l I G 3 ( S p a 0 4

-- M w . ~ J B C.h.,, &-a

C r m o r i rn F u a q 7mmm d Clo-m I Llhr31~hr.m Lw"* % Pvhllr H**,nr A%!

@ Public Hearins Notice 5 C C A gSl-33 (Sprd4

zhuJ*aGh., Cb-Wm C d ~ a u olF- TmrhnmdGunvr r IL,hrhhrun G&"I ,"Air Ixmim .&

- - > .- , , - . ,., , . , , : 7 . * "1

--- -. - - I - - - .,;-* 7 . , - , -,- I 'lli - , ~ , - . C,.~,.. < , , - : m * I " , , , , +. :51-=-, ,.,I - .

- - - . . . .- ~ I =-:. - r - - ~~ .- I -

, : - - ' d - - - , : * 1 ,. : - - = : * , . - . b , 7 , E: / , - . 1 ;:-:7- - --

__-_ L-._ i.. -.-...A_ . __ i .A. ...

I ? : % : -. . I ' - , , ' T F - " I

* : , *-, I-: - , ,.: , i ; : - , C , i T I .- - - 3

' - . .. - - - . , 5 : :+< ; 'I, l ( - F i l - . . I ,,,\ , =+-,:re 2 , . , , * ,,., - .

. . . - . , . . . . ; . , - 'C, f 7 : f I - - . ... - * * , , - I -. ,, , > - L . - - . - . . .

-. - : - 3 - - 5 c C - - . . : I I,.,: . T - , i . . I -,-;,I - r

, - - 5 - , 7 . - - r - * , - c , + _ . , . - ,.. j -2 ~. . : , i

Public Hearing Notice 5 CCA W1W (9pcd.ll

E6r.d 1.a. C* ch.b.* rmmurr ros M, T d 0 ~ L . d cm-< IL*ul-m C d > Prb(rb( H . w y A- ;$

' S u l ~ , n . J a n q 25.1CC5. U 3 k m

J B X ~ ~ ~ ~ ~ ~ . . ~ A ~ T ~ U ~ A H ~ I I ~ ~ I L C A ) T - ~ ~ P ) W ~ ~ O I ~ * ~ ~ I , C C ~

I ~ , . ~ ~ r T , - - n * ' m - L a T ~ k - - - - ~ M - C h h M l- T u r n -

'. a n H c # l R 5 ) . . e * n T s a m . I I 1 W R a n h b A w T ~ h L ~ - A r d r ~ ~ q p . r y ~ ~ r a i ~ r ~ r a ~ t l r n U u ~ ~ ~ ~ - ~ '

5 LSI*LU/LS) 4 ~ ~ . 1 a L ~ ~ * r l l G U O * J ' ~ D C ; - ~ T U I I ~ " F - C ~ L ~ - M F,r4 mbrr&ur-ll- * n c 1 m -

Ir&rii& r- w rmvt %?om ~clm.uwor.qukLip y c u l A D A --%-or mot. ib& mnrh.:txOPTlcto'SI~m:Fh+%C J B Cdna l i S - B S O l , r m d m r - w l r ~ fZ."l;l-&BO5

' n3xmm

T ~ - , I Z t : d o c c r r - c ~ c r ~ t was c n n f I r - r n e d .

! i.-e'ccl~~,:~ed san ln I f: a n d df :?ra 1 I s t ~ e I ( 3 ~ 4 j

3 3 : : I I e I- T S I z e L e t t e r - C.

fdYsW2 @ Public Hearing Notice a cc* WIM m w

TI? 1 5 d o . r u m e r ~ t w a s c o n + I r m e d .

( r e d ~ l c e d s a m p l e a n d d e t a I l s b e l o v $ ) p ~ o u m e t - ~ t S I Z G L e t t e r - S

NDED

I

I 3 GC* BIWBpd.0

r-ya sa ah. cu- 4 ~ a n m r r a m ~ e m d &

, k: .:, , :, :. T , = . - - - . , - F 9 5 i r 9 9 " c . sj e z .,. qe',? ~ A I 5 ; r ~ e \ e i; ,..at l n c L _ ; ;::%<c L*':' . ,- , - . . h i , : . - s c I = ' 2 , - * ' %'?T,,,:i. P . = ? w e : ,r , :*rr, ,cc :- . - . I,;,, 8 ; ~ i F * i : - e r e ,. e tc w e m s i - 3 6 ' r 3 i in' q e ~ i l ? , e~ - - - T r 1 : Tern ' : % : s o u; , , r e - ,:. +,:>. :, ,.- - 2 . . r i 2 7 p. , - - - v - c r r s o C U - F , : .- , - . . ,.at I , % 2 T r a r i i ' i r

>.-. - - - - , - r F.. - I = ' A,>%: Zeta ,,e =h<. 'g l -u l l 'n .'a< i r.;. Z 6 c . K C . ,.a ? , # , j i e n a

- 1 . ~ ~ G c . I J ~ ~ I - I ~ was c o n + I r m e d . ( r - e d u c e . c l s a n i p l e a n d deta I i s ke I ow)

p c . c . u t n e r - ~ t S ! ze Letter-s

DED

@ +" ,/ P I I ~ I ~ C Hzing ~ o t i c e

S-fstmapau

I Etrud 3 B Ghr r-2

-T- - I I I d o c i - l r n e r t t w a s con+ I r r n e d .

!~-edii':;ed s a r n p l e a n d d e t a I I s b e I ow) : r r Slze Letter-S

AMENDED

I 5 G u plus pjpm,)

I Ed.rrdLP Cdr. Ch+ ' -<mF- T & & C o L

i . :*: -. - . . -: ..: ,-i-:: F T : ~ , + e r i - _ : ,-?I t~ C . ' - e r ~ r t U P . 3ez-8 . e r s ( . r a m I;: - - = - . c 2 c - -,<r z + . : . 1 - I L.=. zc I C E 6 = % v c : ~ F-. . ry..,-r I -re.- , , C T . . . - . : . I . , - e 7 s i PM: -'eie 8 - e :i. ILIETC-i -- ..,... : . . z . c ~ , ' ~ . - , T - A ~ T C ' , . ~ C T i A . -e rP l . l ' i e? 1:: i , s g . - if. , . > T ? ~ r l l C C - 3:st = , - , T i Z c : F 3 , - , : F . ' ,: ,.?A' ,,: ( Y,B : rip T-p,,.:-;

+ = : , C . Z T C < - s f h s s x 30.:a . . ,a G M . F c , - r r i - l lira 11:3 C C C b Z : i.; n z S E ~ J

/ T r 3 n s m I s s . I on R e p o r t i

TI-, I :s ! : i c s c u r r ~ e n t 'bvas co r r f I rmed. ! r -ecJc i r .ed samp I e a n d d e t a I I s tre I O W )

i ~ , ; l j z u r r : e r - ~ t Size iet t s r - S

I @, Public HZ;?~ Notice . \ I l.cn w w (s+>

zi-w I.& C'hq Lhrpm." -r m - T n a m,cArir

. . - , . i . : - 1 , ,. . - . , = . c ~ ~ ~ . - .l -c- r,. sii c7. C E ~ C : ~ I ' E : n e c e , . , s :a i ~ s i r ; . -. - , . =(.:&::;:. 5 C 5 , : , - ( 6 > > ( 2 = c i .5 . i c I l l ' , ; 3 = C n l : T r i P I : '-:ye. : e r - . . . > z , - : * , 16 - :? .. era.. ;-': F S ~ B . , . 7 ; *J< .OCT, DI- C ~ C U ~ I P ' T FC,:IIC 2 - 5 7%:. r e - , - - S : e ~ l lEl-

? > ? - - . . , + s . - c s - r . - , - T E L . Fi i - C P ~ , ,?,LC,,: ;'T ' . 4 l t l ^ ' c - - e n Y T l r -

* ' + . c : - - C C . -2s: 6 e . t r e F' . ' : F O ~ V Z S I J t / B l l . ; C - L C : n'C. ; * t 8 I l ! r . i ? ,<end

AMENDED p< ;,:::-, in t . ; j - -)y 1:

5 GC.4 58108 (Special)

Edward J.B. Calvo, Cha~ruian cl qE t-k~e-

Cornmitree on Finance, Tarviion and Combrrce ~ ' G T C E I I lheslaturan Gunhdn 's Publzc Heur~ng Room

Tuesday, January 25, 2005,9:30a.m.

]-he Committee on Finance, Taxation and Commerce will hold a public hearing on Tuesday, Janua1-y 2 j, 2005. 0:30 a.m., at ILihesiuturnn Gudhan's Public Hearing Room andsolicits any written or verbal testimonies fi.0111 the Public on the following measures:

1. Bill 5 0 . 4 (IS) - "An Act To Appropriate The Stun Of Two Million Dollars i$2,000,000) From The Education Facil~ties Fund To The Depament Of Education For The Repair Of Air Conditioning In Public School Fariliries "

2 . Rill No. 8 (LS) - "An Act To Amend To $58104 Of Title 12, Guam Code Annotated Relative To Adding Invesiment Rarkrng Asxi Securities And Commodities Trading To The List OfEligible Activities For QualifyLng Certificates."

3. Bill No. 11 (1,s) - "An Act To Add A New Item (28) & (29) To Item CK) Of $26203 Of Title 11, Gunm Code Annotared Rclative To E:.-:npting The Wholesale Of Telecommunication Services And 08-Island Sales From (.+ross Receipts Ttxes."

5 . Bill Yo. 13 (LS) - "An .Act To Ensct A New I 1 GCA Ch.43 To Create TaxRebates For Educator Expenses And l : n m 3'l.e Educatoi- Appreciat~on .4ct Of 2005."

6. Sill No. 19 (M)- "An Act To Add Hew Itern (36), Subsection K, Section 26203, Article 2, Chapter 26, Division 3. T ~ r i e 1 1, G\:am Code Annotated, For The Purpose Of Exempting The Application Of The Gross Receipt Tax FI on1 The Sale Of Medicine, Medical Supply And Medical Equipment."

7 . ali- ' . , , ..

t n d r i : ~ ~ put-suanr to $17.03.01 of the Standing Rules.

8 . R~ll So. 22 (ECj - "An Ar' To Add To A New Item (5) To Subsection 26202 OfArticle 2, Chapter 26, Division 2. i i (JCA iind .4 New Subsection (I) To Section 281 06 Of Article 2, Chapter 28: 11 GCA, For The Purpose Of Escrnp~ing The Sale Of Mcdiclne, Pharmaceuticals, Medical Equipment And Medical Supply, As Well As The Pro\iiion Of Medical Services From The Application Of The Gross Receipts Tax And To Rmove rile ,lppliialtol; Of The Use Tax From The Importation Of Medical Equipment."

Individuals xvant~ng to submit written testimony or requiring special ADA accommodations or services should contact thc Office of Senator Edward J.B. Calvo at 475-8801, send an e-mail at sei~atorcalvo@,hotsheet.c~~~~ or lir at 475-8SO;.

Clerk s Office huaio!Visual ,411 Media

TI-, c; c { ~ c u r n e t > t was c c ? t 7 f I rmsd. ( r - e c l u c e d s a r n p l e srici d e t a I I s D e I ow)

AMENDED @ Public Hearhe Notice Gapy 5 wim W l

M"d1B.c.k - * qz h E - a - m m m r a w m & & &jllCE r L l h u - ~ ~ ~ I r H r r i a i l c i l c ---2--

-.*_ - , e : ' r-' . - ? I 3FUr.5 : < r i -me,. : 1

- , ! , , : c:c = * T : . = z r 5 : .P

- - - , * -.c . TIC i_

-- - . - -- --- , > , p - - : z . : .-z2-,-=. - . . - , -. ;.M ;

_ / -- . . .-

-I b : l e l : - - = r , , - : i . ; i 1-*:i -r c : < z , > - , - . . Z D . = I 1 - 1 U c F ~ T : : ? I . 4 5 . F 1 1 + ..% :: :.a ~ r i . . - -

- . - ? , . , ,:: :*.: ,,= . , - = - , 2- = ,~ , , r,,z, re",- - * - , - + < \ . ,. , , - e < . r , L : , <

= .: ., , % - < < b'.: , - - Z . e + :: , ~ * ? ~ , r , 1 6 :>:LL,,,~'.$,? F e r : e. 1 % . - * , - - ? l & > = : e 3 .., , c e r -. - . - : c 3 , . , tC 3 ? i r C I - , ~ : ,:. = : - - 6 3 ; , T L I . I T ..,:I:I ,:I T I . + - I - - , 4.-, , : s : ;:, C F ' A: - i F- ,, ? zt,,

- _ - v . 3 .' t . l i . i 1 , 3 5 . i ; ' .5 . , < , : , , > :a ,.

. - . . .. :,, - 5 c - . .,&. . . - .. I .- P 3 1 e S ;,;PL " , 5 2 ' .

I -- -- - .. - . . . ! 1 . . ?. ' s e , 1 : 7 5 <::t,:- = - : . < - - .- . 7 m,e r ( * r - = t 1 ‘ = , - , I - . . . .. - -. - -- - 65'213s

. - -

.. - . ;I+ I ; C P T B C : - s ~ ~ , . , ; C

. 3 Ll, .:: '::-e.. 1 1-:i->=. ? . 75 , - t . 4 5 5 ' . 1 , - _i_ . -

:, - - C P 1 1 - -

, i - : ? > . -. - . - -*:- C K . c c r q - . - P I ' = 0 r r - ,.- " c r i . T e ,.;. - . . , . z , , a , , = - K : 1

- - - E l t . l i. 7 7 I,. , c : - L , , : = , : c : z : - 5 , c : t F : . zr. . - , a C ~ ~ ~ - ~ t ~ i i : , e - -;+. J C T l i . -

. , - A _ s:+: r e . * .i: T: e 1 5 7 3 - 1 c: - +,,T F ~ Q C .%. I

yl- r c C : z . . . T I ~ . m q , ~ : : . . c ? -.. , , 8 : c -

- c -> : * ::., F:. F,, ,:*,, : , ? . , . # , C - ', . .,: , 7.1 c,; , , - * r , : . & -

- , - - . t r.. --,. ,,<:>, -,<,. * , e I r , , i . . ; : , - , . ; p F , , o

C i T % l - Pt - - I > > ' , '

L c : a l I C - 7 , " 5 i;": L C C 6 1 .3mE SE l - - . F k. . . f. C - L .'-' r-.,><$:?a,e - < 2: j E r ; L T , ^ ? t C r r = : J D. -:-i. 1

TI-] I 5 c jc )corner -~ t was con+ l rrned. ! r - E ; d u c f d s s m p l e a n d d e t a I l c b e l O W )

AMENDM espy Public Hearin~ Notice 5 C C A palor (spl.D

m".dlachb..C6W. * 48 cmWd .=+ -. f- - U ~ I CE 1-m 5 hbik H- RMM ----

T ~ , l - Z5. -m. mas

I

ALa3REQ C"3Y Public Hearing Kotjce "u

i S o C A B 6 1 W ( 9 ~ 1

Bd.nd la u n a a+wme i 4E h'e

I - . ~ m r u m ~ - n d c & ~ ~ < tJmCE I L U a l - M 5 P E b ' k & a ! l a r Rmr

- - 3 , L:~,..~ ::.,. + - a ' , . I < - 1 1 T i i i F d C S r f i i l r f d . - .. -

L.:: c-, f i - :* s - 5 x 8.2 ,

--i- --- I ' 5 < j - G . Z - 2

- -- , C P 2

I - - - ,.< 7 - 5

FC 5 , . C . . : r re : : F L ' I - , C P E , ~ F G . D P ~ I F ~ ~ 3 : ~>i:~.c:: : .=: y%e <% . & 7 - ,,s .-p E; 5 , . 3 4 . <:: > ~ ? - : ('7. , , 7 -::, , F T ' K C I z r : L F P T I : : F r, D : , ~ - ,,, -,= - z I,,: : + : 5 C , " - * = e , . i :; i . iP"'c' .! 5 2 . G:.cL,,,c , ' r r-s. ,< "e,: - t 4 : 7 ; ,,, , , . ,Z,xe, 5 s * , - - - . + ' - - - - . . : a - C F . i . - I - i t , L - . r X:s: : ~ J = L , T .. . , . . e i : T , > - c + + .

I ' -,:r: = - C L . r(:ri Z . , j , , . * = > I . = 7 r . ~ < . . < i \.: , . 2 :... : . z . ,&,:%: - < :*-:,

T I ,::c c 1-4 m i? t-I t kc; .3 s c c. I? f I 1.- 171 s i j . i , - t : d u ~ e d s a m c I e sncl d s r I 1 s be I ompi.)

~ , o . c ~ - ~ r n e r ? t Size L e t t e r - 5 ;

Alamm Public Rearine Notice GDF'i"

5 CICA IJIW (spebrj

E d 4 3.8 c*s k q~ ttuL;n C-ORF- mdaawie&fu,. tJoTlCE I W l . b r r a O d c h 5 M k b h r ~ l i l i -

>*.i T l " E . . - . . & - , : 5 . 7 -?F6.,

,.::a: 1: 8- ' 4 7 5 ire

L C . ',B".* - -

. - ;:ti :T<F E 6 . C - L . 3 >.-.,. - - - . - - .. -.': ;=.I. .-k :...-PC -. t. :.-' 2

m\-I)m @=?py Public Hearing Notice "W

5 c C A t d 1 w ( S m

U~.rdJ.B.Cli.a Ch.8m.n ' 4g wR ~-~-r.-&~n(.&-~ tdmCE r b i - e a b k w n ~ h -

?*, i- 2s. 29% PI&

1 a As- -<- ' - ,rDuuv .- iw.,~.

i d r r ~ A & ' Y r t *I1 M.dA

TI-, 1 5 c i o c c r m e n t 'hias cnt-I+ I rrned.

! r - e d u ~ e t J ; ; a m p l e a n d d e t a ~ I s t= .e lov~! E o c u r r > ~ ? r ~ t S I ze L e t t e r - S

T-ri:. 0 v Public ?Jotice Lbpk'

5 CC* m1m *fipsl.l,

I cl *L - .n ' u w r O o c 7 . m &%..< F- a . _ ~ .

*'a Crm i,",

Mad-

! *!I*

::wxp.

Public Hearing Yotice 3 icl WlBi (s-i

. , , . . . T:;:' c s j s x i 5 r b i i r ~ e ~

-- , - re , , , - : - L P . -", 5 T 8 - : - 1 1 0 e

. . .- - . . .- -- - . -- , .,: - < : z , 5 ; , . - L L - : c , - - - : 2 4 2 , . , . - - ; I . , / K C :

--- -. .- .- ,.. - ..-

T j - I , .:j Q c it 171 9 t? t ',v 3 E 1: ;3 n f I r r- i i E ci .

( ; - e d ~ ~ c e d s a l n p l e al?i=l d e t a I I s b e I O W )

~ o r : ~ . ! m e n t Size i e t t s r - .5

2%@mm

Public Hearing Notice 3 ccr Wcs cswd.l,

3% c h a h 48 tfDUE -...Q-T-~C&,~ F J Q ~ C E I i L k . b ~ G M l v h , ~ I c ~ r t m n ----

7-.l-25,2W,9.lhw

- , . , - .ZL.+C I , - l l l l .i ' - 72: i 237C;. : L ' i r 8 T C 9 ^ :

-- .- - I _ -

? - L . : , = ,#<<,:* a - > n T. - # T < E ! <'+ 3 T t C r - ! ' * C G ~ ~ c o ~ - ; ~ ~ ~ : % ce: t ..% 1 . . : . . . . . . 1 , . .z! -s :; -.:? P,., C" . : 1 e c / , I , - A 2 - - 1 :t - % - :r J. 4

.--- . -. -. -~ I i i c c c : - , :-.., ::r3..z.c --

r L . F + C ~ - Z . r , ~ : - 5,: CC' I.? ~ i n c r t ,'.$ : 2 s ~ ~ 8 ~ .? T c I,? :,; %

L C z , . ~ ,:::s- $+,-, a ',r I .. - F L I +,: c . ~ I , c a = - ; : , . e - - i . . - - - I - 2 , b - r , - , : 5 r . . Z T - - . < . ,a:- C I E - = . * * h - q a = , c - , ,-,*. ..?1?r4,~ ;ena--;.:i -L:. - 5 ~ - 3 $ , a r e : ,: , ? + -

, . i. - .;:>- -c, .,:,< - F ,- r, 7 F.. = z r c e 3 ~ : t ~ : < . , r . .. .. 2 - , a - a 2 , =T,= , - .

+ = i - - - . . F n - 6 . I.::: & + c e , % F ~ I : r i r i . ~ - : % . + C; c : - , ? . >..& - . i. S F - , i

L . B ? C , T l l i l E 1 ----:5, 7 : i ':,C%4

L C . . , I C . - ,: , 4 7 - "'= - -.--

L C C : I i d ~ - i e I E - & - - C , F f. .. E. 't..~. 3 -:? c < -.. - 2 > : ssr ,-7- x =r,.~!2:: ., e . L*L :

r- - , 1 , 1 i:li7<: U~T'IGI? t was c ~ r - ~ f I r-1-fled.

( I - e d u c e d s t i m p l e a n d d e t t I I s ~e 1 o w ) C , ( > c ~ - ~ m e n t Size L e t t t r r . 5

&I!mw2 I @ Public Hearing Notice alpy 5 GU )61W (5-1

I U-ad J BGh, n a b n u . q 4% m n

c-yon k-, imam&co&ra ~ W C E l i , k ~ & & i . f P r b o s k t " p I m n

T ; , ~ : +-:,*., Z : Z c C J ' 1 T O T ; , C81+1 Ci. ' - , f I I - - C J 3 ' I

- -. _ _ - - ___ . . . - . .. _ , . ]-‘...;:. , $ 5 5 i5.:TT a7e -*-

I - 1 5 : ~ ~ 2 ' 5 1 - L - - : , 5 . - . ; T = h ' 2 - i ,

L..L - - 1 . -1 -- - -.L. . -

. . - . , . - - ,>:- : . . - . . P C ' P e r + - : : P C ' C 1 % . C - k i i i C i t I.',%: Z e - . k ~e :: t , a ~ , : : .

.. - = < ,. . .: - s = ~ .! k , , r . " , , P : c = ri--. = I i . r' FC ,. T~ F : , c " * . ,,re- ,,., > : , . - .- . . . . .,, , + - i - F, . L L ; ~ s .; :nsn- 2 . - L C . 2 5 ~ 8 ~ - i , ; : C E T C .i I : t I , , 5 r -

, > - . . - & ? . +<r.z: : r t - t F 7 ; ' -CS: -. .>:r.r. . '- . ,#, : t : 8 ,-, ; T .. 6 .-, - = L '2

,= , . . - - - = * - c , h ; ~ : ~ e . 6 : F . : r i r r ~ r ~ : I : ;:.c ..5 L - i , . l - , c - za7;,

- 1 1 - 1 1.5 c l i = . c c r r n e n t ' ~ ~ 3 . 5 : c c n f I rm . - .d .

1 t- e d u c e d s a m p l e a n d d e t a i I s ~3 1 E W )

D o c u m e n T Size L e t t e r - S

AWh-DLD

Public Hearin9 Notice CQpv a cugs loa (5-) - m *. c b . h . 2 43

C - - ~ ~ ~ F - T - - C & - t\jmCE I W m r h O& 1 Prblr **,*?- -- -

T-IW ISXW u. amr r h

I --- ton "Icn

LsrhwreCluaux

1V. PUBLIC HEARING ACEWDA

N I N A S E N T E OCHO N A L I H E S L A T U R A I I G U ~ H A I I *'A~.\:Y r;8<;lEll ..,?.: , t . ~ . . , . ' , , . , I h l

S E N A T O R E D W A R D J . B . C A L V O S E C R E T A R Y O P T H E L E C I t r L A T U Y P

L'I,.<.,,,,.X, 1 onntn ' l ru ctu k 3 ~ 4 % i t . 1 .ts \ ~ c o ~ , $ r (1Rl\ l fUc i

AGENDA

.' Bill \ c s . S*>J; ",V; .c! t*, >tccr%I <Xi 1f.d k)i .I 1112 12. < # t , : & t t t ( d c ,\,17~l::\.! ICI~:I>.: o:<:;.l$

.,,.,<:.1,:,:,.1 ?*..2.:*Ig .I,;.. ,c\,c:,'!. 3x .,>l:ll;;*<,:!c% lr.,,iil* .%, 1L l!..l ..>: .- I~~?zIc :*.I\ : L \ It.+

. 8 , t l i l> ! f ; ! , . ~ ~ ? : l ,..id% '.

\'. SIGN-IN SHEET

Sign-in sheet not provided by Committee on Finance. Taxation, and Commcrce

\ I . WRITTEN TESTIMONY

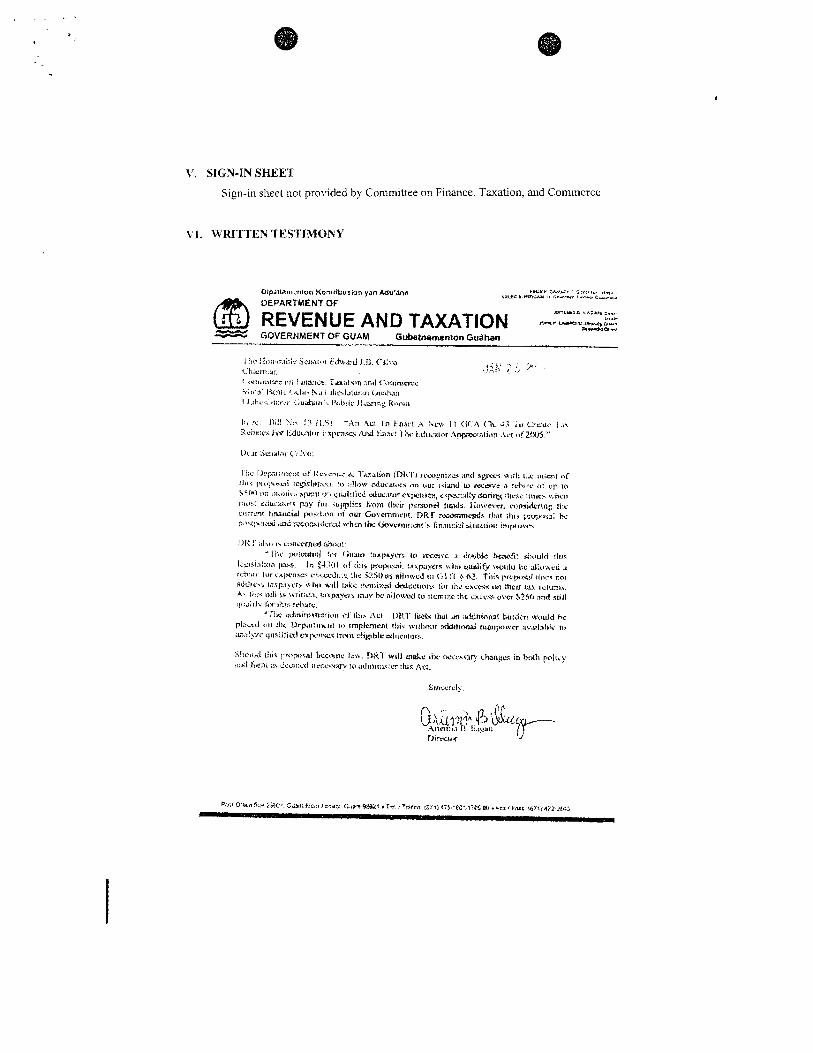

DEPARTMENT OF Mu.*,. ' ,>a* :".

0,.* REVENUE AND TAXATION -p--*m-*e- a)rrhDra

GOVERNMENT OF GUAM Gubetnamenlon Gu&tran

IY, rt 13(!l kc,. !'! f l , % i '-.A;I %il In k$kac! :\ k-,~ 1 1 < i C ' , \ Ch. 4; '#s! CKUC i . 1 ~

Rci?s:cr inr Irdih:~lor i.xlr0.w Alad Cnx: l'nc tk?ucamr . A ~ w r n t i . ~ t ~ .\n t>f201)5 "

l i:c l)i~>m:7,c;tl uf Kcrir8.i. &. l..nntr<m (i'lli 1') ~c io~ct~: . t r r .wxl fiylrrs ~ . r l : llx u t i ~ l i f $4 r l ~ ~ % ~'~tb;w-a'i :cglsln~:~..~. to ::lloaf c t l u c z l ~ ~ : ~ on uu; ;Jmd u o v z o ;cS.;i+c (r: up In

\'(*I on 5114,,1t~.. > p e l t u:, q~c.tl!licd aluc.ztor cupcnrta, cipcs-.rlly &ant% :hew :inn% nnctr i;tttac ulu~.~: ,rr\ pay f o r . u M ~ c r 1r11m lltcu pemntil hods. I lo\revcr. cttrt,klnra:: $1 t. i-urirnr trnatlck! pvi:llc%n r l t our G o ~ n m n c r ? ~ . DR'T m c a m w d s rli;sl i111.; p:vjk~ss; k p>it;+-~;cxi .d r;iinzrc&~i?I whm :tic (iaunun:cnt's lin.xl~ciui b i t u t i t ~ ~ I : I ~ X U % ~

:)I< !- ,>I\<, rr ~.r,lt'uW;* i1;Ir>u! ' 1i.z pctlcxdzul :tx GXIUII : B X ~ R ~ ~ T < to ~WCXCE z ( i ~ l l h k be,%li? dhnlki !111s

! : n 5 fr: $.lli~l <,1'rh1s pyr,wi. :a~,pa.wrs \vi~:r qualify \w:tu bc .tl:t~,.\cu .t rc!x~r< lor c.qm.%c L ? ~ ~ I I I ~ :I$: $.?st) e , a l i o ~ e d %:I ( i I I I $ 62. T 3 3 q prqxmt it)^-< not a d d ~ r \ > t,trp:l:,~.rs %clnb w l l lakc ~:eilllilzi.d & ~ C I I @ I ~ IUI ~i:c C X C ~ ~ S on mctr tm rrIu~11\. 4% I:,>* biii u :\-nrieq r~n*tpaycrb l r u y hc nll~\wyl to ilcmrzc :hc cxcqsc o v t ~ $?SO and slr l l ,,<:~;,l> (,:r Ih,:. re&.<.

":!x ~dmimm-e;ion ot'rl?i.. , \GI. 1%1' li.eir hot .m xklltiirna: hur4.n u30uld hc plniccl c i 1 1 :lit L)~~;II:II~LIII 1,) ~ m p l m c n l thir wtlh8n:t &to& ruiurp,%vcr ;ri.arlafr.. 11.

.L~. I !~ IC ;laaiifia! C X ( ~ T ~ K T 17~11 Ct&blti oducrttora.

S I r o r ~ i l IIII< ~:r,>p%.?t bcsei~c la*. !')R1 wtil m d z tic Irz.rwry c l n n j i e in bclt f~ poll,.). :cxl ftmt C~:GICIII<I I I C C W ~ t e JI~I:)I~:LC:LT : ~ I L At:.

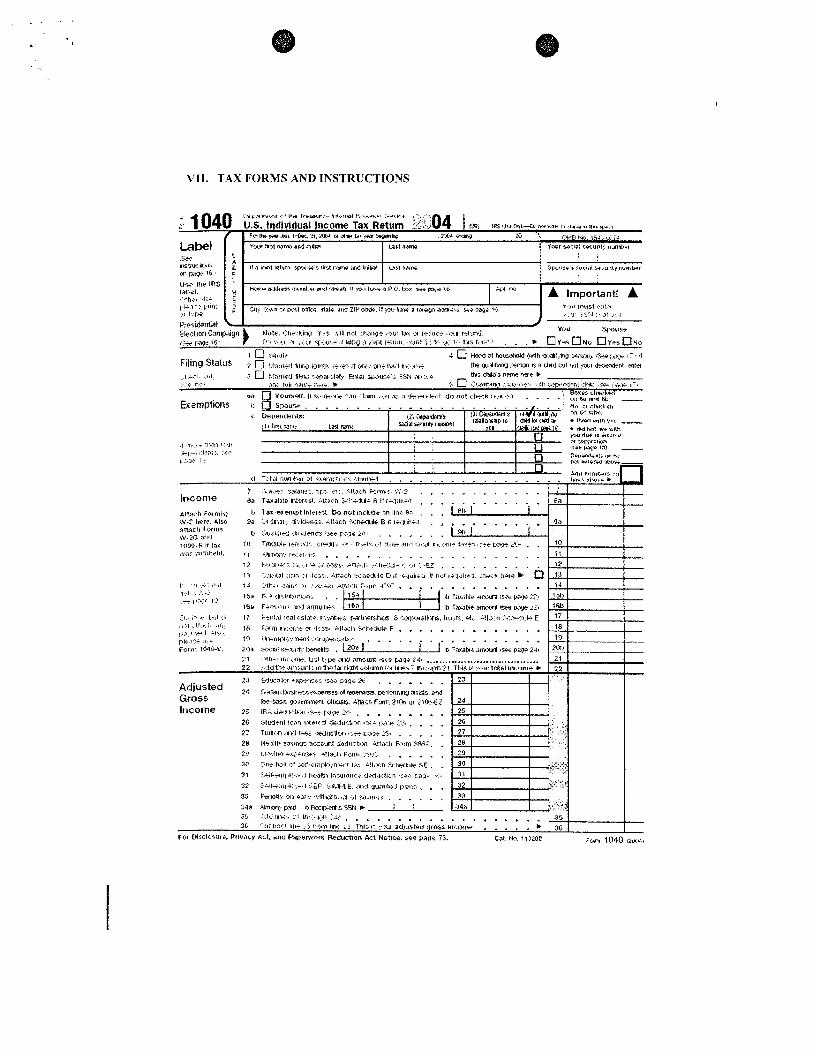

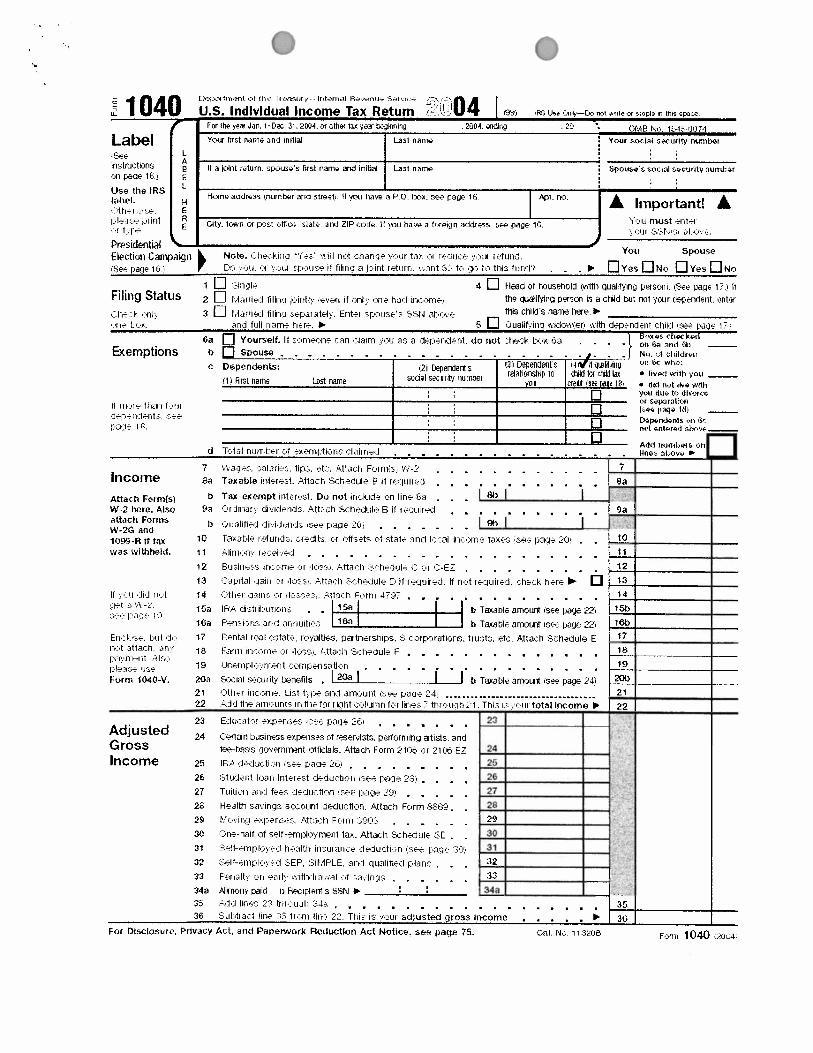

V 1 I . TAX FORMS AND INSTRUCTIONS

040 t:i.lam..,f+l . I 11- rrdYYni - L ~ . ~ , ~ I e.rr-ltr- :;:-' U.S. indlvldoal Income Tax Return <<.'!.:!04 1 m! ~ ~ ~ c , a t ~ m l i h n c + rntr CI n ~ ~ b n mr vpr:-

Fallalvahnl-W-31.2aU u J h O r w M t 9 mit4 -2 2CI ' m.43 ry;.l,d?,;q

La be1 <w ta t MOW md tn4z.d LZSI n ~ m : Your ancia! recunf: n n * w

G I i t t s n CI w.51 o t i t ~ dab I I P m . 11.p~ haw s rscyli. an;; M ~ 1 ~ ) i 16 1 -.I, !nust - fat* <.'L,, :.$I 1.5, 21-r.

Y&' .!ill n d :bang+ i.:.ur 4, ,:r IC:~ICI ,:,.I rdvrr" YOU .srW,lSa

:.v.l ,*.-.LI~- 81 bin?> a ~ : ~ I I I I IWUIII .:~nl i d I,.. .>:. t . 3 A liuli-1, . . . 0 Y- ONG 0 YPS NO

I :d-m,~ii 4 ttsd 8 t u r n wa:npl w+m, .s+e F..- ,-., n Filing Status ,,I,,,~~, ,, I:~,,,, .,, fi mi, we ,,:.::a,r t* q.h-4tte~ r ~ a 6 a a d OJI WI ,WI ec.n~ a&

,i .,,:,: :rm> I:.?,, .&l:-,,:lL;>l ,, :- k3F. I :,

. . . 4 f t a ~ h Formir) b Tax-wmpt lntr)r?t Dct nat lnslnt m line ;L, w-: Iwre. A& 9a ,~.lljdt; d;iYcnj; -.ttach 7,ctwAde 6 d l++ilh:l , . a w n fwmr . . . . . . . b 3UBililW , l i Y l m & I,%? p?3i i t s ,

$ 3 I 11.~1a1 ~7i f i :I 11.235; iina.:h :-h+:-:~t~i G 11 tt;,usci II nst I;:IUI~+,I crei* >nr, t It " .L '" i 4 3-' .k,,'? c.' ii~m J-c- . . . ,. . . . . . . . . . 1-1 .> .\ -2 ... -I, ,%>+ 19 15.2 IF2 . :b , l rP . t rL:< , , 11 lar;.Nc **lrun tsa 1w.e 22,

188 Fh%unr imd 3 n i i U n ~ ~ b T m t t e amxrt (91% kW Z2!

. . . . . . . . . . b 7?U3bl+ dm=* I*& pSX 2211

e 25 IEA &fir&:o .sit t d p ?:,, . . . . . . . . . X, S t M ~ c i l lr.+n , @ % r e :JrJw.ti:.n .-- tx rkx 23. . . . . 27 T w e c n a ~ J Ier .wmUot.;- p > . ~ i%r . . . . . 28 Hs~lnh 3aoirff~ BSZW aeOfb30.m 4t15:lx Fcrm L%??. . 29 I.i.~:in) s ~ q s r w s 411aJ-, F ~ n i l'?.,? . . . . . . 3C C.w-hln i.i WI-any+-.inwit la. L ! Ixh $zkh!le SE . . 31 Wit(mpl-:.;-~i hw!!l> liiwt?rl,:: dclutti jn ,c+i gag. i..,.

32 ;uf+iil:b ,.+J s ~ f , ; I~ IF~E ai.3 .~ts*-ili*as pnnc. . . . 35 FilwLlv 913 i ~ ; l - :.l#klnv,,si 31 5il;m.i: . . . . . . 34a H m a r ~ . p r d b k p s i t s sw c : s :.:I J 1 t e 5 i., mt :.urn >la . . . . . . . . . . . . . . . . . . . I 3G .iuruu,:+ IilE >:, ;?to> are r. Rrr, .. :.cur a@)u%tarr gross v l c m . . . . . 30 1

For mscloqure, Prlvacy Act, nlld Pananvmk Redochon Act Nonce. s?. page i5. &t ~ - i 1 1 w B :m to40 m:44

Adjusted Gross Income

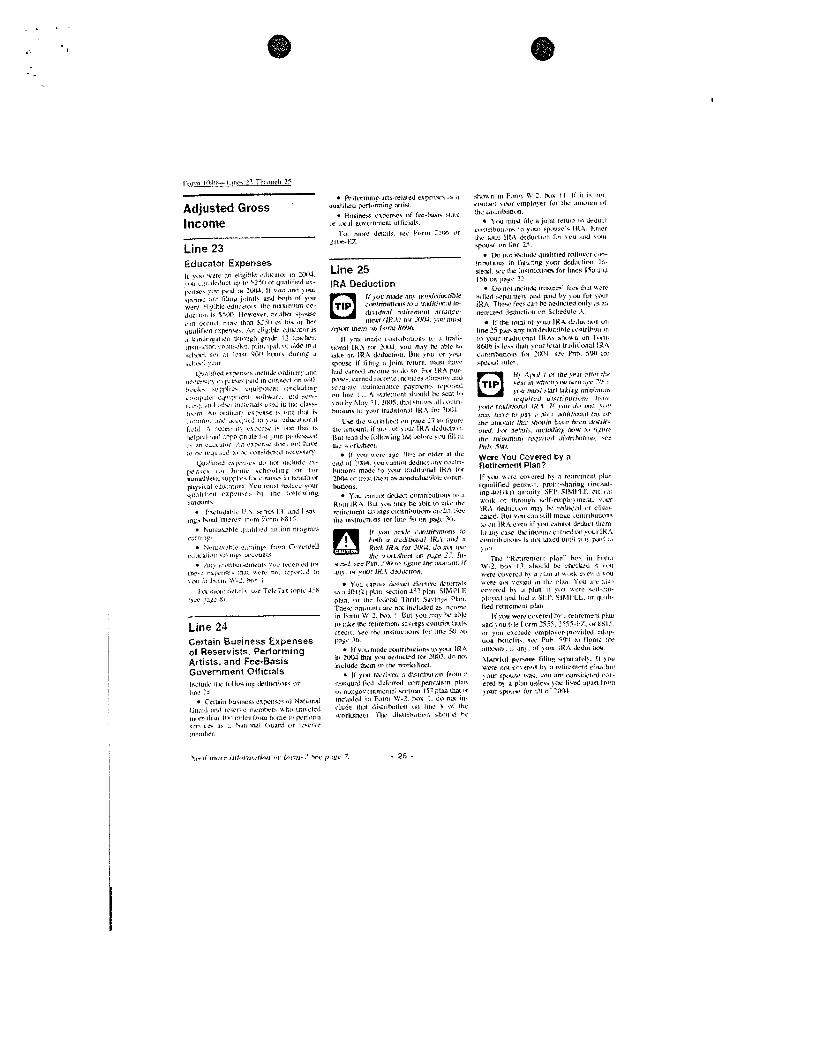

Line 23 Educator Expenses

r,xi ucrz an r,lrp&h& eJor.rlor ID ZCYU. ,,it ,2n JCY~ULT I,, Vv1 o i qwd,fid ex- lunu., !""? p c ~ J rn .'MU li ?nix .tnc !swr ,FXW .A,? l i ! tn~ jlrtoll) and h ~ t h or )cru

cli$~hC ~durelcas Ihc muxinirtm +?-

d u c l r l , IC %%(XI Hlo\rc%r,r. r r i l b x cr.p,%~W . ,n &duii nuut than S:5ll ,?I h,, or kt q~itliCk'il c y w n w ,411 dllylt& C ~ U ~ N W is ., Lin&k.lyanr+n 011vi~gI1 pr& I2 lca'h'l. ~nsinianr ~.i-.o~tsdc!r i;nris;p.~l. m sidr in .I ritnr.1 I.'! .!I Ira-I VlWi Ilcurq dilrlnc .t

,~l,,k,: q.,alti,td txFnw, CIICI~~.~ , x d t n w > .~nd

,s;~bc!r, 2x)wnw\ ~ p d d in a>ntkxltiln vc'kll b , ~ ~ . i . wpplc?.. vquryawnt ~lncl lui lng .,<",f,,,l>.,. cqc;,"n,,Tl W~Il'.+.,~<. ,U)& xm- t~,.!. ,tnJ otkdr ;~i.~;cri.d. u ~ d IU ~n: c h w - r,,.w 41 ndlcnr> z ~ p v n u I< rv;r l l ~ i l I\ ,li.~iniim .,nd . I L C . ~ ~ ~ In >s,ut edwalar-n.tl (,<id ,A ".e:e5, i,! c\p.nx' 1, cvw lhdt ex

h.Ip~xI ,lid .ippr..pnak I r r o u r p r~ i fzs~ lus .I< an cr iurd<r ,'.I? c v r . n r . &\ trio! ll.t\c ~u R.~!I$~CJ at! iv ~ ~ ) n - i & x c ~ l n<ceLTcl)

Q u ~ l i l r d :.~gi-ow, ili, I!,% nhiudc i\- pr1l~r.5 i.v hc.n;e \ ~ h o t % l i n ~ or lor nonatd~dw -rupylc\ 1.r ,.~-.nrtc* ~n hr..$lll t*r phpriul cdk.acu!i Yurt !nus1 -miucc sour qt!nlslfed crpl'll'r- hj lha f~,flol\'lng :nmunls.

tuludahlc L' \ u v r x 1-F .uld l at- Ins, hlrui ~ n l - ~ e ~ l crt.ln 1 om1 ti615 . horl.,t.ihic ,p~.ll~h:J Iub!lOn pragnull r a r n l i ; p

Ui,ru.l~sh,~. : ~ r r ~ t ~ p i n m Ci,~crdcll c~r*rl,oir ..:I rr;)?. . E < C U U 3 . A:)? ~ ~ l ~ l ~ t ~ u r ~ ~ ~ i ~ n l ~ :<v ~t \c l \zd Ivr ih..: c ~ l k ~ n x , ~ , h . ~ ,xcrc ~ t , l rcp~-Itcd 1s) ,,* ;,>1.cn, *.\-2. i x x v ;

rut ~ IKW 6~!,<11, u.u TcIvTir W ~ I L 4% ,$a' ,uy< bl

Line 24 Certain Business Expenses of Reservists. Performing Artists, and Fee-Basis Government Officials

I t . r tmn~npzn?-wl r Id w(*'l:u-i ;& .I qual l l rd pcrfb+rrntnr. mi>;

H u s i n e ~ CXW"OY> of i m - h l b U.IIC cx I,K.~I ~ n \ c r n m ~ ' n i uficioh

l o r ~noae dnal1.i. h'u I.omt I ( a c,r 21w-1-z

Line 25 IRA Deduction

tLJ I1 rrlu rn.dca an! m~rdn lur ih rc cr&tiibmnlr 1'1 8 M*IAI~W;J in- rlr,~dsnl m9irenlt~rll arr~1l:r- IIEN ilK.-1) t~ -~)(i:. . ~ u j a~uu

r~p?un rhctr~ tm Ir*rlu 8416

I f !DU made ~ ~ > l l l l t h i ~ l h ~ n b R. J !I.di-

ttolwl IRA liw :<NU. you may Ix .lhlc lo w l u sn I R h &ktuctnnt. Rtu \ ~ u . or bvur s p l w I f l i l i r t ~ 3 )ornl raunt. IIIU<I have h:d r r m d ~ncat lu 119 Jhi 1;n l-cr I R A pua- p-.c\. wmud tnknltc ~ ~ x l u J ~ a l s w ~ n ? and scpiu.btc. m~intcn.lacd p y n m l z ri'i.iv1.4 *ti llnz ! 1 4 <ukm%snt ~ I~ .~ l l< l kv e n r I,, !nu hs hlj:: 1 I. 2Ws . lhal ~ h t ~ i ~ r . t l l i c o l n - hurjms I<, j01tr lraJ!lloni>l 1K,\ iari ?#XU

P*s liac ~uslrl;cwl o i l ~.qi. 17 I t3 CIyutr !It,. ~~ln,unt. ii w:. of >w: 1 K h ~I-JULIIIIII I3uc wxd ilw fo4kwinp!r% W r r c yr.u lit: 11:

*,c U<>rLst*,-r. . If !;.u uerc 1st 70b.: w ' (~ Ik r 11 the rtld .>: 1cXY. )LW c ~ n l i o l ,&dl& t an! r r~n ln - htalon.; ma* :u y~w~r l :~md~l~~~nr l IKA t c g r

Zcxu <s I~CZ: thi.n~ 3% nondeii~vt~hl.- cooln- butions

Y L ? ~ c:tnu,x AYIIAY crm~nbt~ l rnn~ 10 a ROIII tK4. But 5uu *rra: he nhlc lo 111'. the wlin*nto>l Ingr c~mlrlhotnms crcJil See thz !nuruinins Ici I& 10 on 'i,.

15b on p g r 12 . Do m r IIXIIIL~ trurl-.?' ice6 \rcro h,llcd u.placly nnd puJ hy >,u :oilr iL\. T l k w fez- wn k iiCJ,~lPd wily .B .W

;vn~rzed d d u r l h ~ n on \c l ldu lc A.

IT W I~YJ ot )rwr IKA d c l h t ~ l a x n ur~ ltrw 25 plur any I~OII~CJICII~IC tOnVilldl-,ll

I<> ) m r tr<uvnLd IRA, a i l ~ ~ v o UII I $,or; Kt46 h idzb lhvn ycoi local l rd< l l l l l~& l IR.\ ~i,nmhuuotiy lrrr ?IYU c:.i. I4ih. 5W lor .pc<ldl r,,lcc.

H * .1&$11 1 <f rhe)t.u alrer r/:r ~ ( p I s r r o r nhrrhilur arm.t.w :I*: 0 )1w rcq<rircd I ~ W I I \la1 ~I..I~!~III,<~II., uklng ~ianrrnuol tro,>r

! 'wr tm11rx~m;I I # t 11 :ou d o m ~ l . tv!' Inn$ n l t r 11, pa) ,I .W'> .aWr:k~~ul rxr r\n thc mwrmr !hu J<uIrl hate h.m d i r h o l d PLY drbsl.. mrlrrdin# hlr nx ri,?rrrr rhr mi2lm:m~ rr~llurcd d1rlrriw11,a). uc Puh SVI.

Were Y o u Covered by a Retirement Plan? t i ),xu KPTC ~x~\r.srd h) a r c l l m c n l plur rq61.>li!-wd pco%?L-n. p i f i l - ~ b n n n p ~tnciud- Ing r ~ l i h j l . sn~icr~ly. SEP SIMlbl.t. ;tc r ..I uort or lilintuph ~ ~ l ( - m l ~ p h ~ ) m i ' n ~ . vour IWA d d u c i u ~ ~ r ma) t~ mlnr'd w 2111111- naurl. no1 ytn1 i.ln %il l mnhc il ' l i l l~lttiw?n- ~o:,n IRA c v r ~ it ) iw ~ . i n n d &duc1 Ihcm lii XI,> u w Ihr iw~,laccnrnnlo! iy~xi i IR:i ,~<nlrrhuu<m, i s i loi uxcd uulll 11 la pa'! I t '

L US,

The " K n ~ m n t c l ~ l p h ~ " hr,\ 10 f.oml \V-3. ho\ 1.7. should k c h r l ' d t I \,*\I n n c i ~ ~ v c n ' d h: rtp1.10 &I unri i! 11)11 u r n oa r.t.i~cd In ill: plan I'N .\I* :I;W

cotox4 h! .I plun il ?13u uerc r.ll-;:ll- p l v y ~ d .wJ h.d a 51 1'. 51f.11'LL. cn ~ ~ J I I - lid rcmcrxn l p l m

li :wtt ucte c,ntrclt hv . tn . t ! r~~n~~nt pluu and !nu file Corm 3 .5s . li55-i:L or LSl! ,,f >,,,, <~~l " , l r . <#l,pl<,>er-~~r\ \wI<,I .1,I.>p- clcro t r fw l i l \ (I\- Pub SVi! 10 ficurz ti*.

:imxtill. 11 an), <,I yottr iKA Ldwkn

\ l a r r l ~ d p t m w l ~ Illil~~ <t~la~.>Icl!. 11 )wr u s e nn4 C L I I ~ ~ I(> i t ccurenldll 1-la, hut >our sp-w !ia-. lor, 3. r n n u k l d co, . crcJ $ A pl:in unit%. >,w l ist4 ap:tn In,!ii !nm h p u r ior :dl of l W .

SCHEDULES A&B (Form I W

7 F'+:.:,ndl p?prr i l.tieC . - . . . . . . . . ................. 8 i ? t h 1.vea L1-2 l : ,p and iunowi b..

T.3.7~ L..

ffnte. ......... - ................. - .................................. F-,-. ,I' 12 P-in: r. i~ ~qi?~:ij\r +I, j r ] Form lC*??Y Sm PH.W A,.!

htrsctlbrmol~s .................................................. Oadacltoas ................................................................

21 la l r e p r r , ~ l ~ ~ , n !+, . . . . . . . . . . . 2: 8,311~ ~ ~ p ~ ~ i ? ~ - - ~ m r - . ; t ~ n i n t &?I, .d;~-K,s~ lx,v at; LE1

t.;p -%-..I a l r ~ t n d b ................... ... ................. ................................................................

. . . 27 A,.h l l~n+. ii tlifc*.~ah iZ

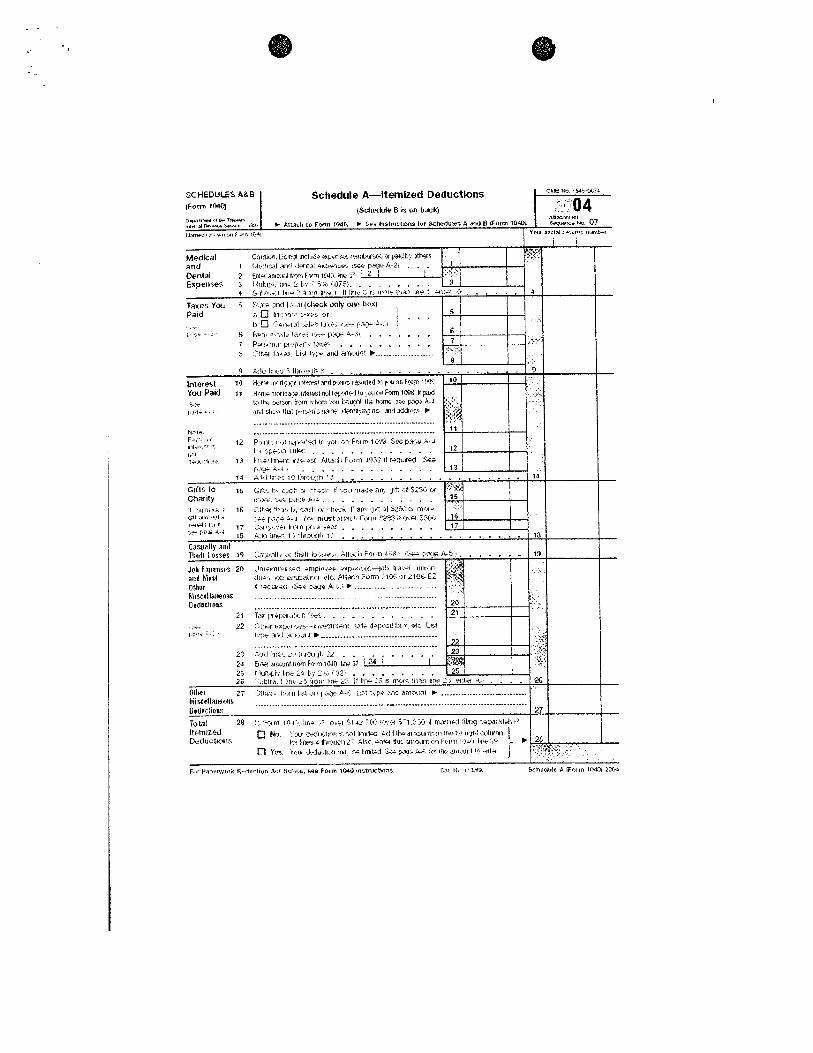

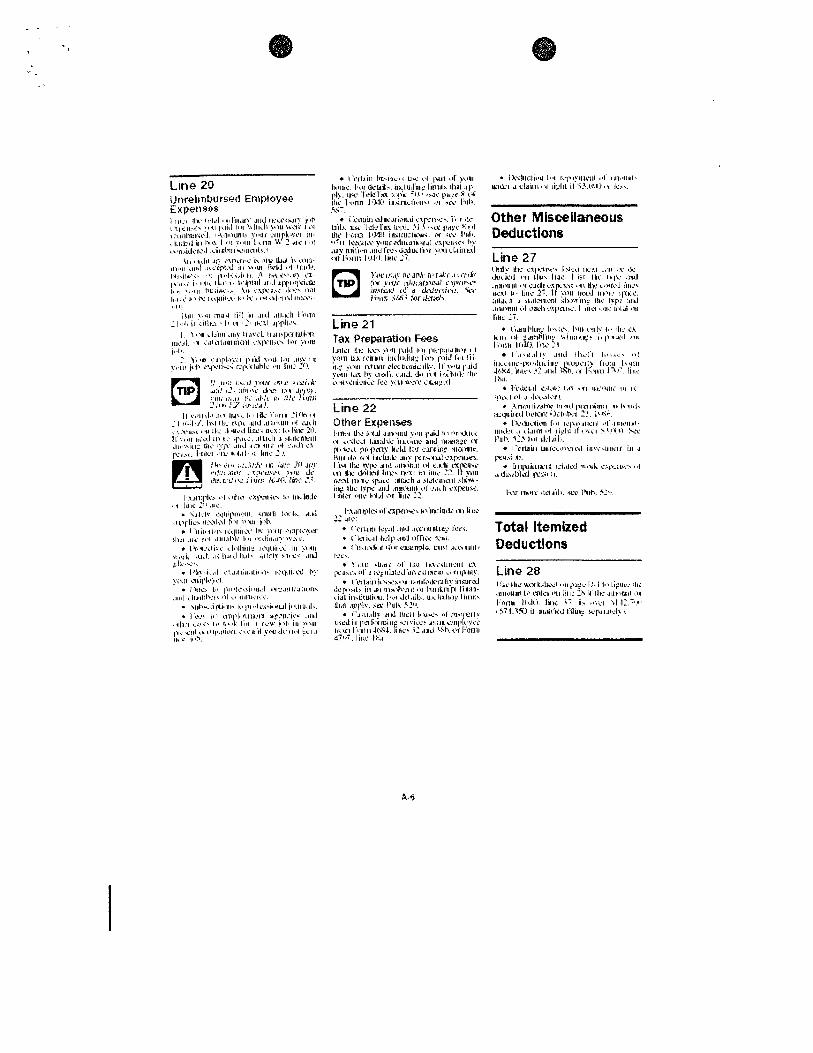

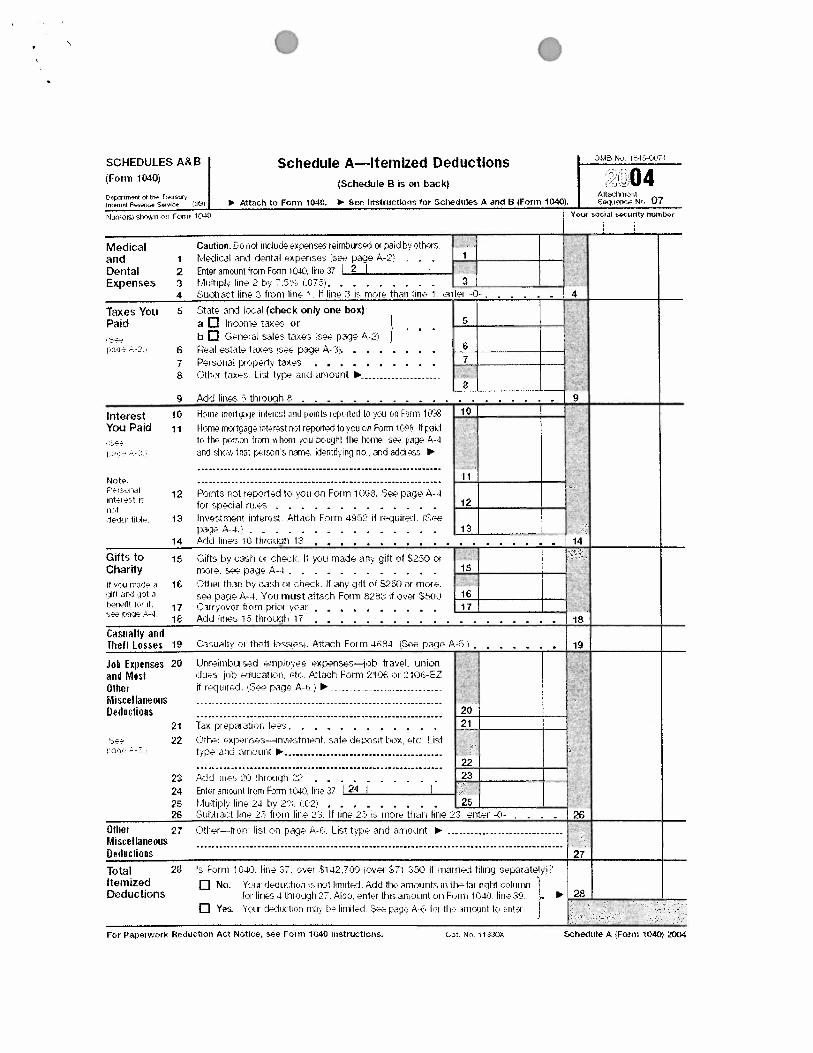

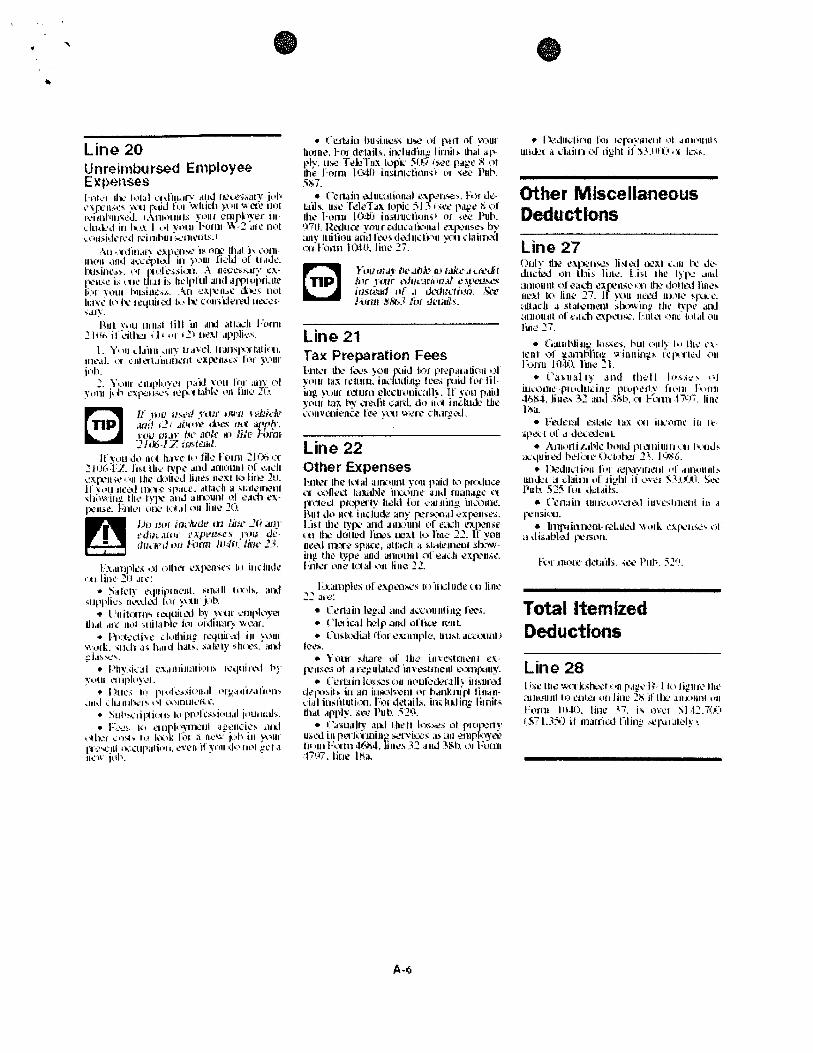

Line 20 Unreltnlxlrsed Etiiployee Expenses

Line 22 Other Expnses 1.rrli.l Ute 1b.f.d rtlt--ed )I'II p ~ i d 10, l'l'.&lii ~3 rn%Utscl f.is:tl~lc i~u.srue 2114 ts.yJge rr jr,*eil ~ > ~ p ~ u - l y kclJ It*r cJrnmp uldmr. Ihu~ 110 ,101 i l a l u ~ k j u r u ~ ~ a l csp3njn. I i k l Ihc n'lc riel .flt?HIlIl (*I r..r'll b " ~ un*r t w IIW d4i11~d II~W\ 1x31 l o ~111,. 22. 1'1 \+tw m.21 l r l r c >PAC 21I.Ch d ~ I d ~ l l l U 1 I ih;u nv; Ibc lvpc .u~d .~II~~LIII~ 3,t s:.sh CSfVUni. 1.1-1Icr VRO I.1.11 L-n l i i i l tc 21.

Other Mlsce lh l eous Deductions

Line 27 !)ldv U?: r'trcn-:% li\r;<l t vs l L.III h, ducicrl 8111 I l1i5 linc. I i\l Ib< I?(*: .rnJ .aaouclt $ , I c ~ d l L.S Irrc G tr Ub: \I+1II1d lille, ~wst r . l ~ n o 27. IF:^^^ ~lccd Iwr;.. < p r r . all.t,h r slahvncnt shn% 111g Itlr Irpr . t ~ r l .I~UI~IIIII <!I ~ 4 t h CtpcIlw. 1 61Ic.7 3 %11c htld sul rib* :7.

+ !;rnuhlin*. l n . ~ , ~ . I>III 3 ~11:: 1 3 . Ih,. c\ 1c1t1 *b~rmf i i~~c ~IIIIIII~~ lcl-* I~<I l~ t in l l I!-&!. rt,12 > I

I ' .~~n.r l l ! . J I I ~ lllL~l'l Ix!i..:\ 1n~i81ne-pca.~llt,i11(. vlupcrt) ir.~111 I \ *n l -lh%4, iiilcr 32 .#nf ;hb. ,A I-,xu -1'1:. 11ikr. I h l .

l~~~~,I~l.ll e.,L,k 1.4s < * I lI,:~~n,~ 1st ,< <(>L\ I r t l ,# t l c ~ ~ d ~ ~ ~ l .

r !nnmi,al~b h i w l ~xnriitsnt t x t 11 91~1.

:i2quird t l r . l ~ ~ ~ I ) i l * ~ h Y ' 5 . I*-*i.,. I v ~ h c l i t w L~,I I,,~I~III~~II .irnt>Iutt %

UII,&:I ., c1~11n td IP;III it- \ { ~ ' * I I . 5 % ~ [ 'Uh i 2 1 It51 d.'~Jil;.

r 1 LIIJUI UII~~.~~?~;:ICLI ~RVC.IIIICIII ill d

FII.,~, ST.

b n l ~ i & t ~ r ~ U ~:I.tlcd wttth C\~-IL->< 8 t l

>I di>abld ~YI:*QVI.

Total Itemized Deductions

Line 28 l i i e lhc s\ixk,Ix~l L ~I I pr;c I L. I I t 4 Li.;~tt.: llli ,UIIUIIIII t ~ ? mkh lilt< 2h 'd'tlx .IEI>.~UIII on I'OIIII ILIJII. 1i11c ??. i, ,-.\.I >lJ:,:+nt

c 5: I. 43-I ii nlkIr'a'd idin; X.~I.II.:I~ 8.

\'III. CORRESPOYDENCE

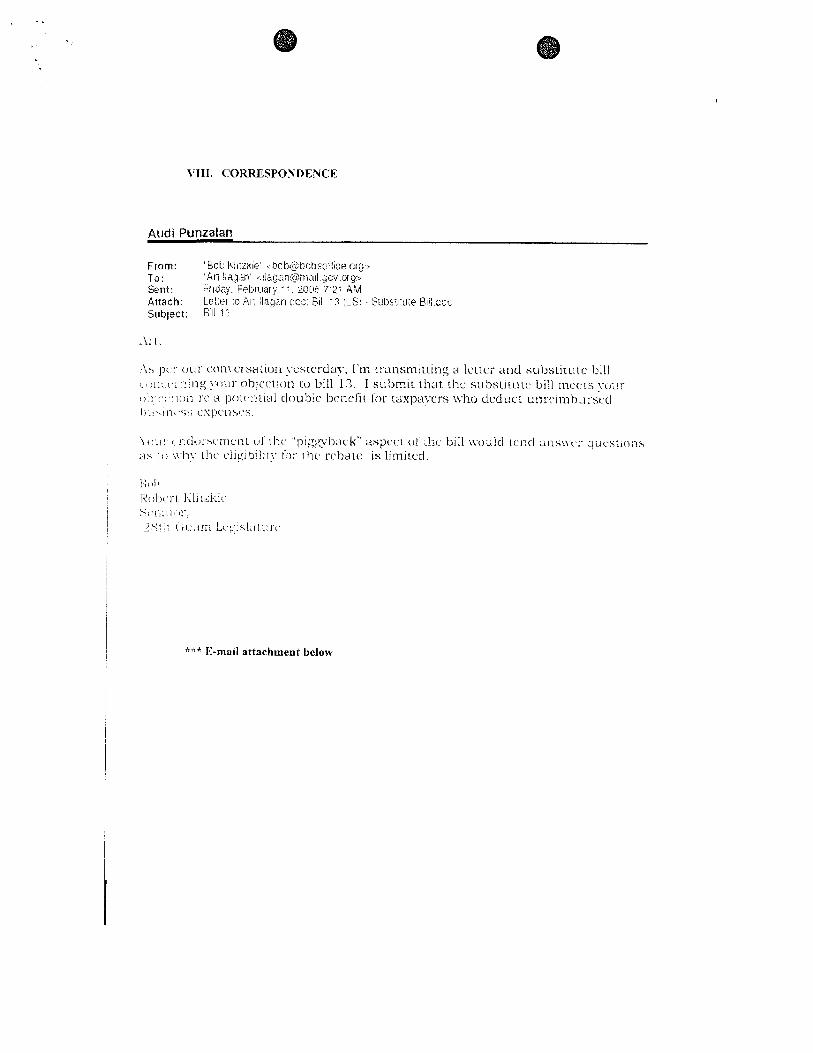

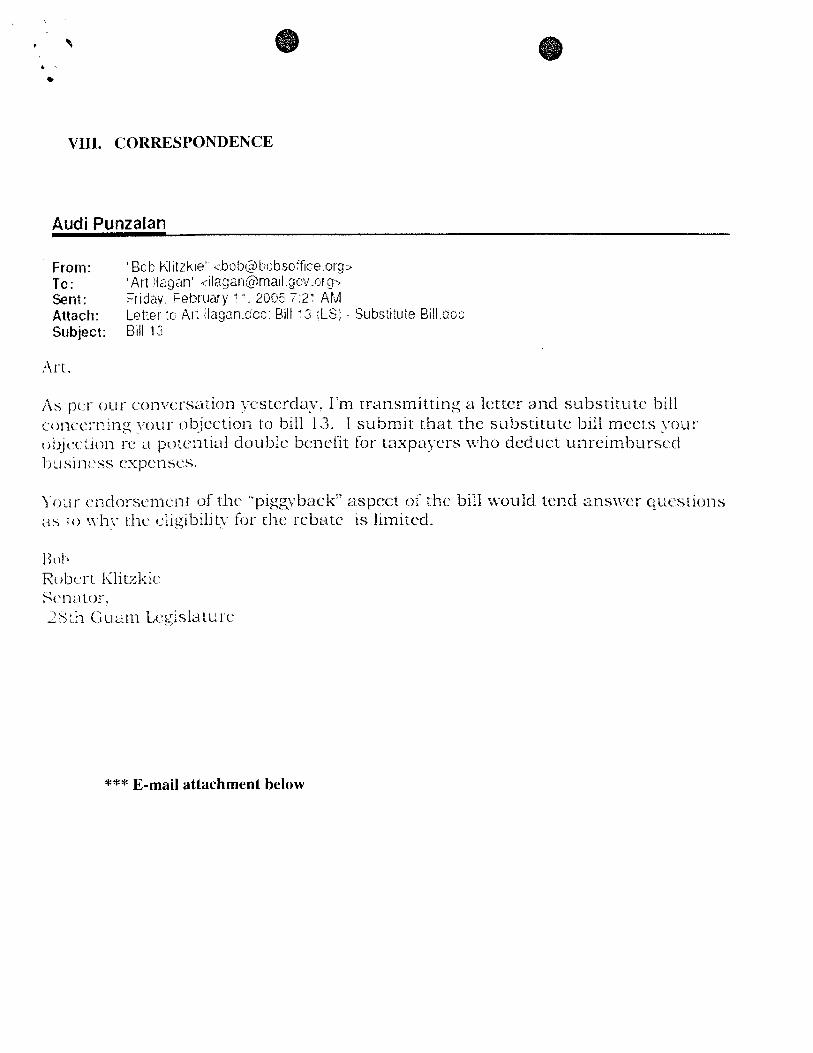

Aildi Punzaian

From: 'BPI:: Klitzk~e' ..bcb@bcbsc+fi::e.c~~~. To : 'An iiagan' ~.ri~~?i.n;:fimail .;~c'!.or g, Sent: 'r~dzj. Febriiary ' '. 213[15 7 27 AM Attach: Letrer ;o At: i lag i r~ dcc: Pill ' 3 ;LS: - Su4s:t:ir:e Eli; ccc Sublect: 6111 1:

])I.[. O L I I - c o n \ . c r s ~ t i ~ ~ ~ \.cst~'i.da>., I't71 L : . L I I I S ~ I ~ I ~ ~ ~ I I ~ >I I ~ t t c r ant1 s u l ~ s l i t ~ ; ~ ~ bill l.,,!i;:c.:-~:ing :\-our objcc~tjon to bill 13. I st~lxzit that t h ~ + sabstirutt5 biil mcc:!s y ~ ; i ~ ( : , I . ( . ~ ! i l i 1-1. ;-I [I():( :ltial doubic bc~:cfir (or taspkkycrs who dcdu~:t u11rcimba:-scd I J . ~ XI lil.?% < ~ ~ ' : l ~ ~ L > h ( ~ S ,

'\ {:.I:. I, i;cld 1;-si nlc.nL rrl ll ic. "11igg.i~,-1ck* aspcct oi ;!:c biil .i\-o;iIcl L C I : ~ uns\\i.:- c!iicstlt>ns A S : t : n-h7%- [!I(. ri~glbili~!. ios [hi' rc.bate is Limitcd.

""" E-mail attachment be lo^

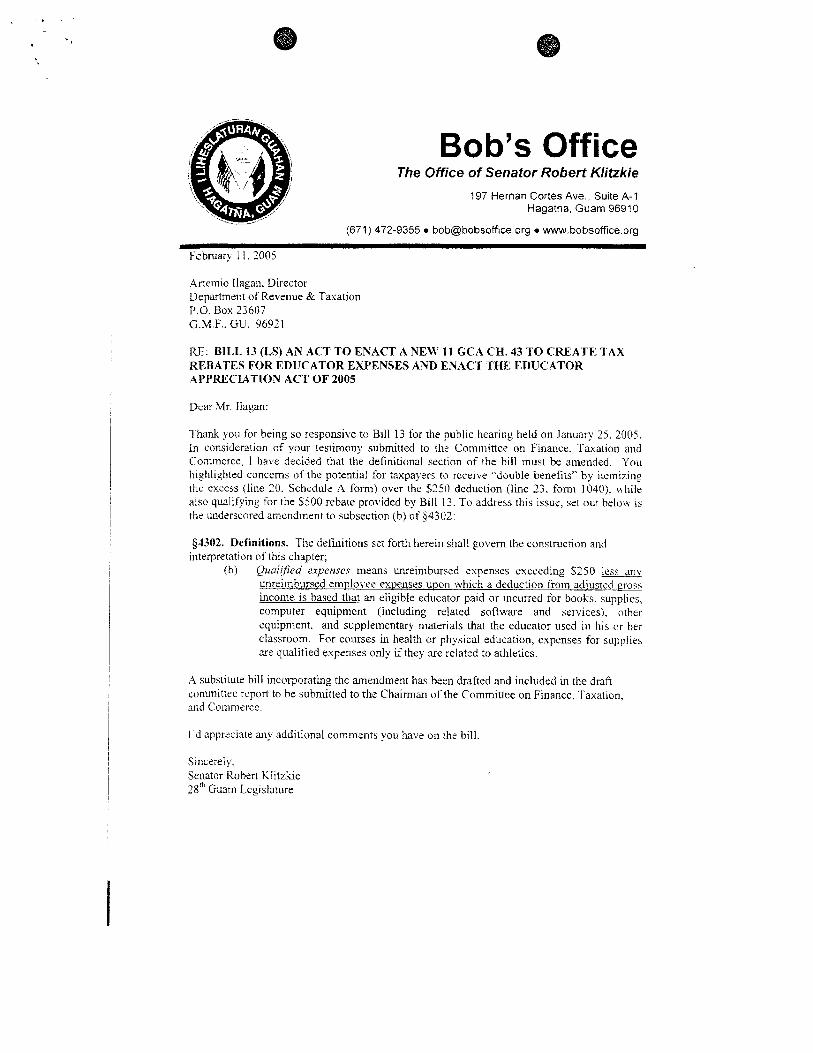

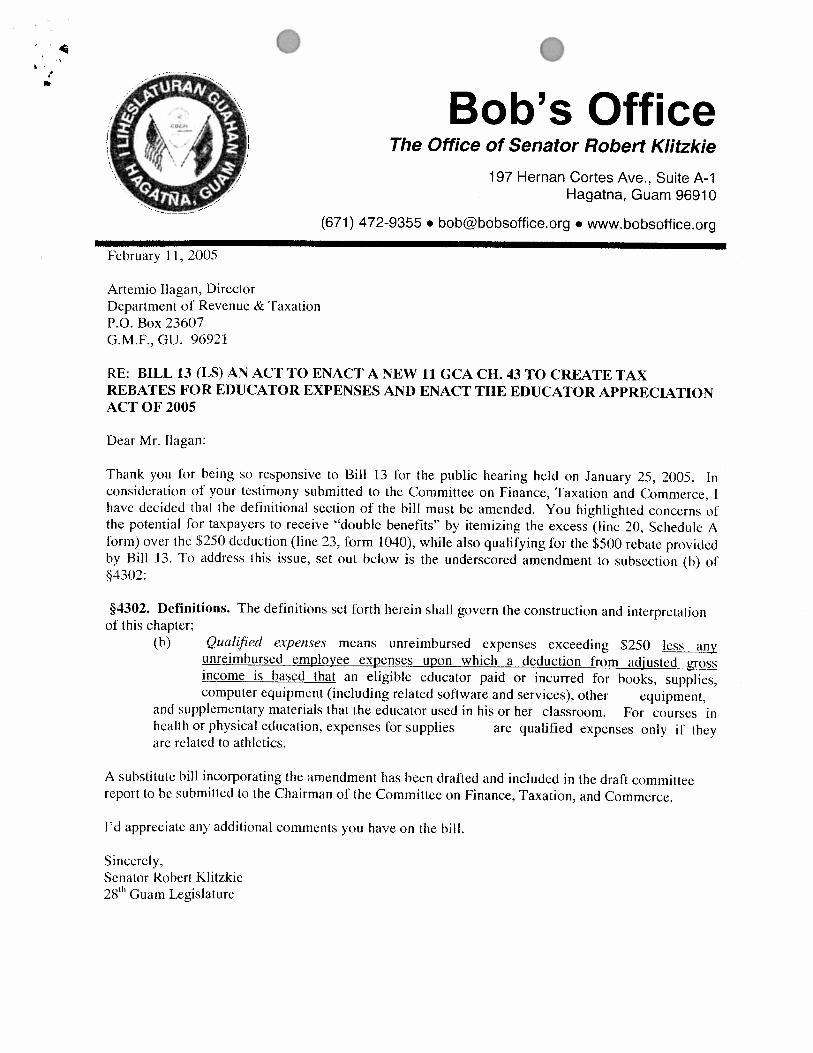

Bob's Office The Office of Senator Robert Klitzkie

197 Hernan Cortes Ave.. Suite A-1 Hagatna, Guam 96910

(671) 472-9355 [email protected] www.bobsofice.org

Arteniio Ilagru~. Director Departmeilt of Revenue & Taxation P.O. Box 23607 G.M.F.. GU. 96921

RF.. BILL 13 (LS) AN .4CT TO EKACT A NEW 1 1 GCA CH. 43 TO CREATE TAX REBATES POK EDUCATOR EXPENSES AND ENACT THE EDUCATOR APPRECIATION ACT OF 2005

Deal Mr. Ilagan:

l'ha~lli you for being so responsive to Bill 13 for the public hearins held on January 25. 2005. In consideration of your testimony submitted to the Committee on Finance. Taxation and Commerce, I have decided that the definitional section of the bill must be amended. You highlighted concerns of the potential h r taxpayers to receive "double benefirs" by itc~nizing the excess (line 20. Schedule A Soim) over the $250 deduction (line 23. fomm 1040). \\-hilt: also qualifying for the SSOO rebate provided by Bill 13. To address this issue, set out bclu\+ is the underscored amendment to subsection (h) of g.1302:

$4302. Definitions. The definitions set forth herein shall govern the constnlction and interpretation of this chapter;

(b) C)uai?fified c x p c ~ ~ . ~ c s means unreinlburscd expenses exceeding S150 less anv unreirnb~uscd cmplo~ee expenses uDon which a deduction from adiustcd gross inconle is bascd that an eligible educator paid or incurred for books. supplies, computer equupmcnt (including related software and senices), other equipment. and supplementary materials that the educator uscd in his or her classroom. For courses in health or physical education. expenses for supplies are qualified expenses only if they arc related to athletics.

'4 substitute bill incorporating the ametldment has beell drafted and included in the draft conlrnittec report to be submitted to thc Chairman ofthe Coinmittee on Financc, Taxation. and Com~ncrcc.

I'd appreciate any additional comments you h v e on the bill

Sincerely. Senator Robcr~ Klltzkie 28' Guam Lcgislature

V.SIGN-IN SHEET

Committee on Finance, Taxation, & Commerce Office of Finance and Budget

Senator Edward J.B. Calvo, Chair~linn

TESTIMONY - SIGN IN SHEET Tai~uary 2.5, 2UU5 Public Hearing

HII,L NlrhIRER 12 (L,S) " .1N ACT TO ENACT A NEW 1 1 CiC:1 CH.43 T'C) CE,\TE TAX REBI\TES p()K k,DI:'C:ATOR LXPEYSf-'S AkD EK.:AC:T THE EDIICATOR

DEP'T'JORGANIZATION ORAL / M7RiTTEN CONTACT NO.

VI. WRITTEN TESTIMONY

Dipattwurcntcm KvnUibue i~ yan Adu'ana

- GOVERNMENT OF GUAM Gubetnamenton Grtlhan

The tjcpmfiit~~~ of ~ C C C C R U C & T~dx~Lton (i3R.l f S U ~ O ~ W C S itnd 9grec~ with tke t~ttmt ~ T E tht* pr<~pi*srri ibrnuki~~un. 1u :illoi.ff trrtucaton nls utrr rslad tu r e c ~ r e ii ~ b i % ~ o'i UP to S.%Fk an muiuru spm: 1%3 c;ualified &t;wtnr cgpal+o, wj~tf33I:y &JIY ng these :trnch uRn most ed~sclatt\r\ pay to$ ~ ~ ~ p p ~ a c s trnm Qlwnr ptnnnal funds fiorvcvcr, cansrdcrrfig t1.e ium.~; fnn,lnczel p ~ f t t ~ s of F ~ U I Gtwmmcat, ISRT ~cz~063mctdx4 81141 I h t ~ g~rupc~sZt! he: p-&l.h~r.auE dncf re~~tnsrdca:da.it tvhm tixc Gc.tcnn,nw?'~ l'fnai~cr~d ~ t r t t ~ i a o ~ ~ rtrtprtlvfi

?IK f dbtr IS iit~-crncd +~~wuI. * C ~ C p d ~ l l i t a l f01 1311?~1sa Eaxpaycr% ~ C I rewive 8 do~blc h e t i t JwulS thrs

Ic;t~~~~ih~rn pass gf of this p~upuad, ~BkWyt.?t& \\I#, ~ u R J I ~ ~ aoukd h. dillcr\\'crl a rchraec tor ~'xpcrw? cxc~cdtitg 911e Q2Stf 85 dlot~ed ~n ( i f t i 4 ($2 TAW p~pusuf dim wt ,rJdrcs\ axpuwcrs wllu w~il take rw~verd drcllrcuogls tor cix excc~s an t h r u x r a u m ~ . 4, tihis brli 1 % amttm, taxpiym 1r3i?)r he alkowtd to 3tcanr;kc the excess over $2S@ am1 stti1 yual~iy f iw- tRrs rv&re

*T!lr udnrtnrdtraiiern uf this Act UR? S k l h that an !xiif~tional burdm ~ ~ t k ~ i d be pldLrtf c t ~ i :he f)cpai;ltie~~r k t ~;rnplm~eel tiis ttstl.inslt addittondl rmnpxva apiwlnbr: to m~rlyrc guair ti tzl expmicr tn3rn cilglble c&iucntt>; s.

nkouid tdtis prr?psai hcc~ttt'tc l s ~ , fliC'1' i ~ ~ i l m&c thr :mxh%ary chmg~% in both pctllcy ar~t l ilrnl; as dcctricrf nrcc9snr)l $c! itilrniniii?rr lhgs Act.

L 0 .

(See 0 , 4 ,

lnstnrctions ' If a joint raturn. sp-s's ftrst namo and lnlttal Last n a m z j Spouse's sucral m u t i t y twrnkw on $age 1G.j E , t

' . use ttle IRS I F l t ~ l . Home address [number arrj strautj. If yw liaw a P.0. Cox. see psga 16. Apt. m.

: ~ I I E A Important! A I:'lint

' Uty. town w post off lc~ state 3 r d ZIP coda. If mu h a w a lweign dbtiss. ?a page 16. \'ou must +-kt+ ,:,r t> I:+.

P r e s ~ d e n t ~ i C'hazkln~ 'Ye.?" 5.t,rll not c h a n ~ e your t a i 01 rczluce yn!a refund.

. . . ;sea paw 16 i C~G \.:*.I. '3 )~?i.n gous? if flbnn a hint rdurn. aant '92 t*:. @:, tit t l rs fund? + R y e s ONO D y e s ON^

2% Otlicl initmie. hs t bpe m 3 arnuunt cser paue 31 .................... 22 .Add tlic am'sunts ln t l i i fcu I aht 3:irll~rnn fi,I l r ~ e s - tltt<v<li h 21. This is :.~<II

24 C&sn k~s~nessexpnses of resarr.lsts, petiwnilng artists and fee-bask governmi offkiats. Attach Forin 2 l R or 2 1 0 M Z

25 IRA sjsi lubcn ~ s r i page 2ii . . . . . . . . . 26 :Studant lean intelryt ,&ductioll (see page 938 . . . .

. . . . . 27 Tuitrtm a i d fees ~ckdlh:Q?n !see p a j r , 2 9 1

23 Healm sa;:ings av-n~mt deduction. Attattach Form - . . . . . . 29 fto~in~znpel~s+s..Att3.:hFc,rm?0~?3

30 (In?-half of self-m@oyment tax. Attach S c W u l e 5E . . 31 S.-lf-r~?iployerl h+Jlth irlrularlie deducthin :r~t. (-age 313: 32 Sdf-imy:,l.:~:ed SEP. :i.II,APLE, and qudiflscl plans . . - 33 Pat,ilty (2n ?all:: ;s:itli~:l~a,;;al r+f savings . . . . . . Ma Almn:r' wid b Recdent's SSN b I I . . 35 k J i l I n s 23 Vil,:,udh 243 . . . . . . . . . . 36 lut.tract IIE 3.5 ftcnl 111-e E l . Thr:, Is you1 adjusted gross inconle . . . . .

For Disclosure. Privacy Act, and PapetWork Reduction Act Notice. sea page 75. Cat. No 1 1 3'208 F l ~ l n 10.40 i X 4 ,

1 lirngle 4 HE& of household (~4th qualifying WSWFII !See w e 17.j If Filing Status 2 Idallied f l l n ~ eintly t e ~ ~ 1 ~f ord! ane h ~ d tl-p;o~ilit @ifylflg person IS a cMd but not your dependent. entw