Embed Size (px)

Citation preview

presented by:John Burns | CEO

949-870-1210

F E B R U A R Y 2 4 t h 2 0 1 7

Teachers Retirement

System of TexasHousing Overview

& Strategies

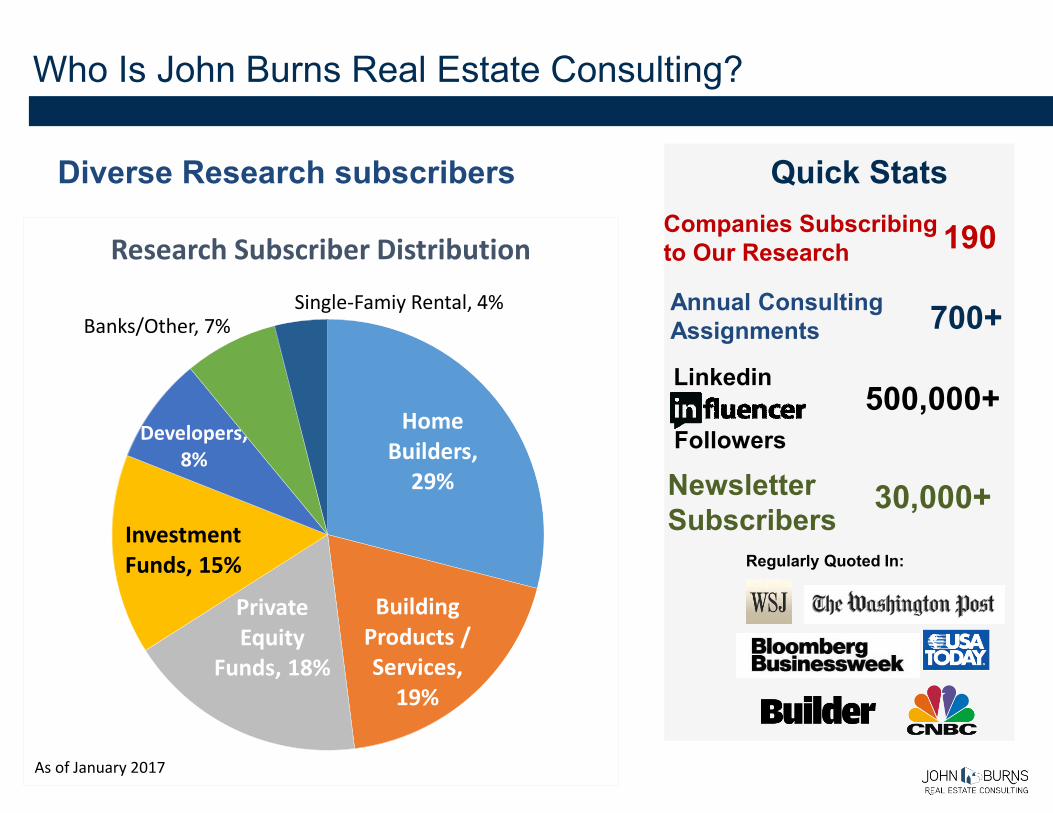

Who Is John Burns Real Estate Consulting?

Quick Stats

30,000+

500,000+Linkedin

NewsletterSubscribers

Regularly Quoted In:

Companies Subscribing to Our Research

Diverse Research subscribers

Home Builders,

29%

Building Products / Services,

19%

Private Equity

Funds, 18%

Investment Funds, 15%

Developers, 8%

Banks/Other, 7%Single-Famiy Rental, 4%

Research Subscriber Distribution

As of January 2017

700+

190

Annual Consulting Assignments

Followers

Our Nationwide Team of Housing Experts in 17 Locations

Jody Kahn(603) [email protected]

Dean Wehrli(916) [email protected]

NORTHERN CALIFORNIA

TEXAS

FLORIDA

SOUTHEAST

NORTHEAST

Lesley Deutch(561) [email protected]

David Kalosis(770) [email protected]

Jody Kahn(603) [email protected]

SOUTHERN CALIFORNIAORANGE COUNTY

Don Walker(858) [email protected]

Pete Reeb(858) [email protected]

Ken Perlman(858) [email protected]

Chris Porter

Mollie Carmichael(949) [email protected]

Chris Porter(949) [email protected]

Todd Tomalak(920) [email protected]

MIDWEST

Steve Dutra(949) [email protected]

Nicole Murray(949) [email protected]

Rick Palacios, Jr.(949) [email protected]

John Burns(949) [email protected]

SOUTHERN CALIFORNIASAN DIEGO

Lisa Marquis Jackson(214) [email protected]

SOUTHWEST

Steve Burch(248) 797-4469

David Jarvis(713) [email protected]

Dan Fulton(703) [email protected]

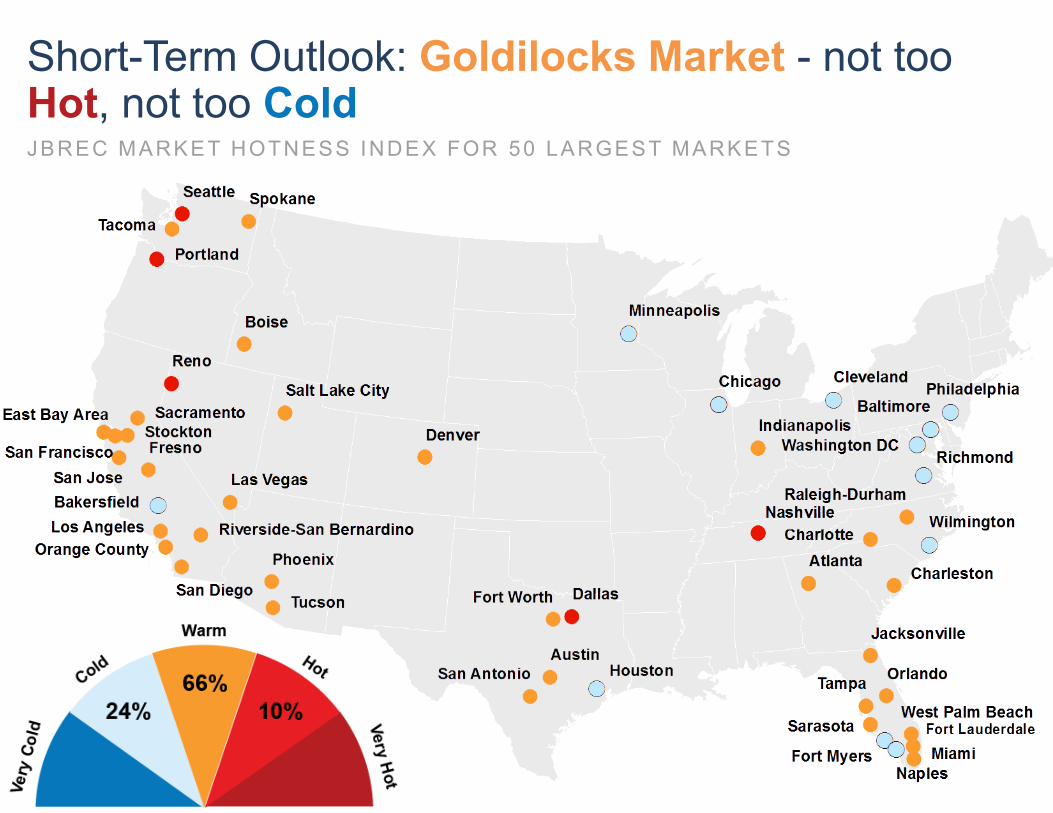

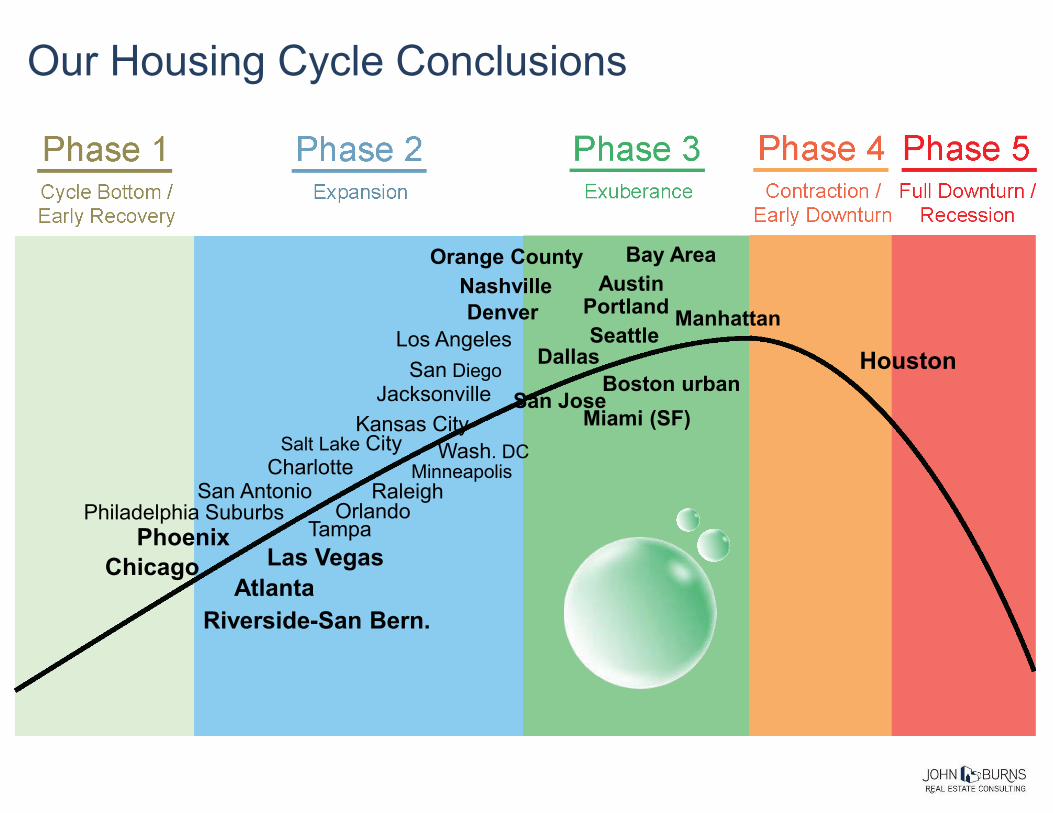

Short-Term Outlook: Goldilocks Market - not too Hot, not too ColdJBREC MARKET HOTNESS INDEX FOR 50 LARGEST MARKETS

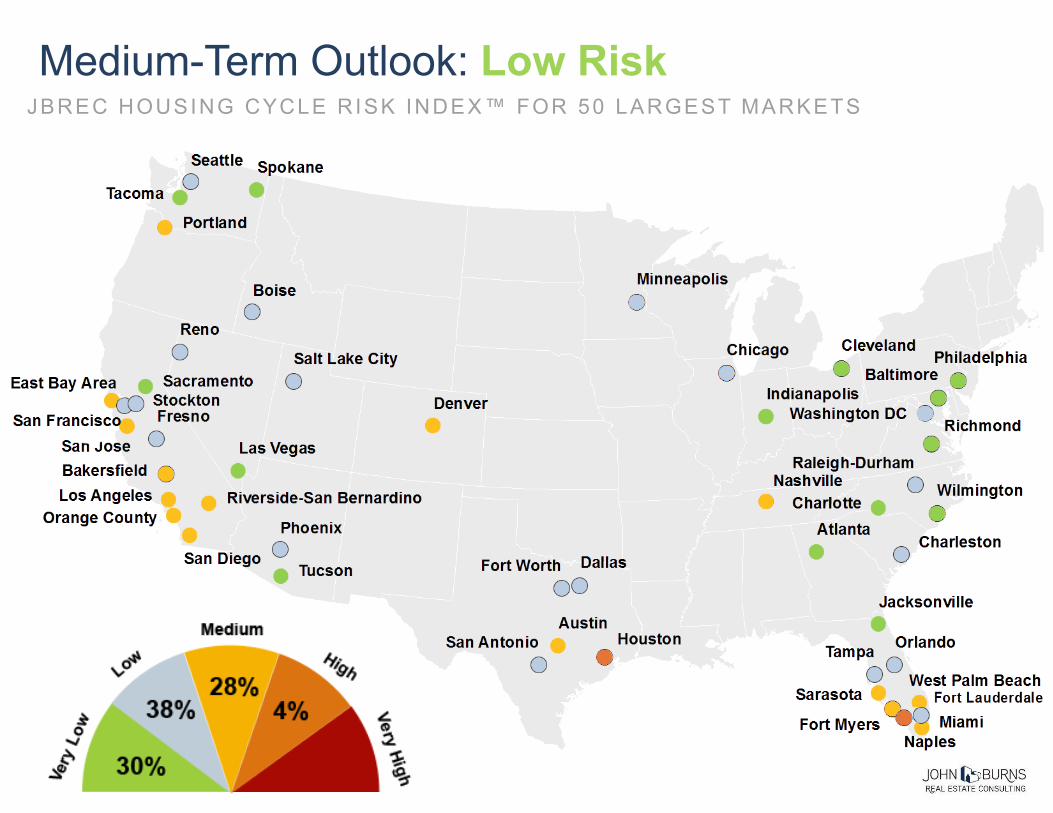

Medium-Term Outlook: Low RiskJBREC HOUSING CYCLE RISK INDEX™ FOR 50 LARGEST MARKETS

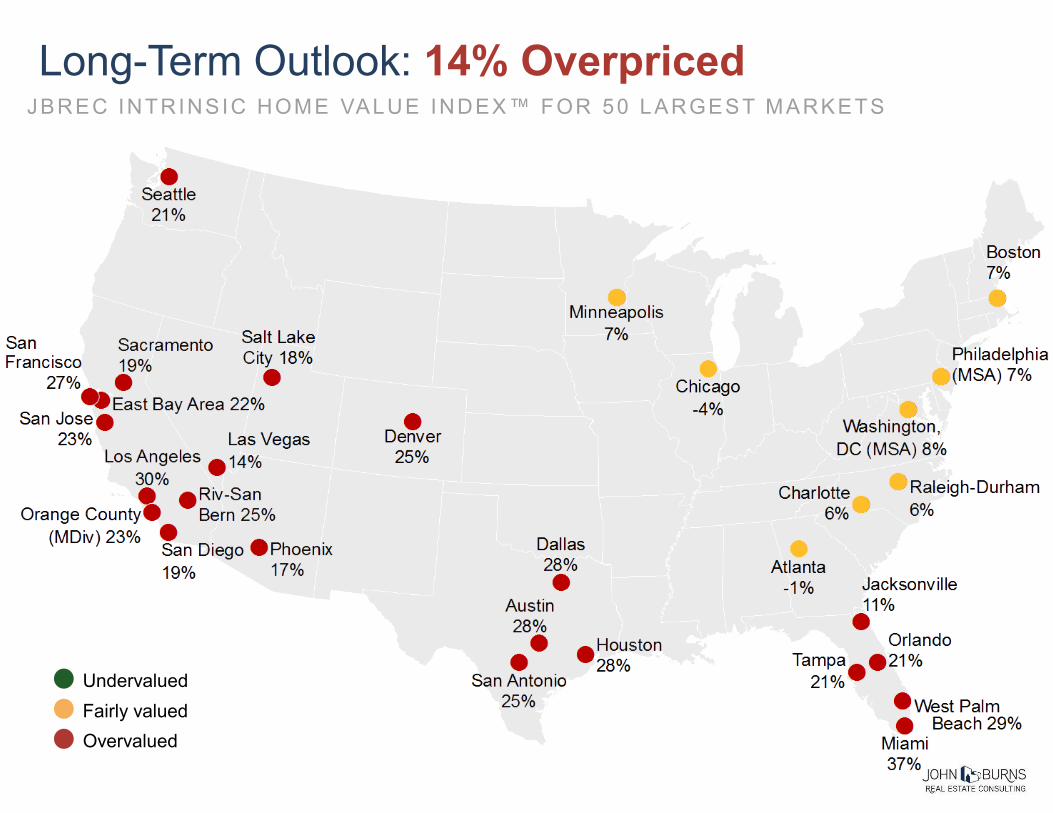

Long-Term Outlook: 14% OverpricedJBREC INTRINSIC HOME VALUE INDEX™ FOR 50 LARGEST MARKETS

Overvalued

UndervaluedFairly valued

Houston

Orange County

Los Angeles

Riverside-San Bern.

Chicago

Dallas

Austin

Orlando

Las Vegas

Wash. DC

Tampa

Nashville

Phoenix

Atlanta

CharlotteRaleighSan Antonio

Bay Area

DenverSeattle

Philadelphia Suburbs

Minneapolis

ManhattanPortland

Miami (SF)Boston urbanSan Diego

Jacksonville

Salt Lake City

Our Housing Cycle Conclusions

San JoseKansas City

Demographic

Clarity

for Business

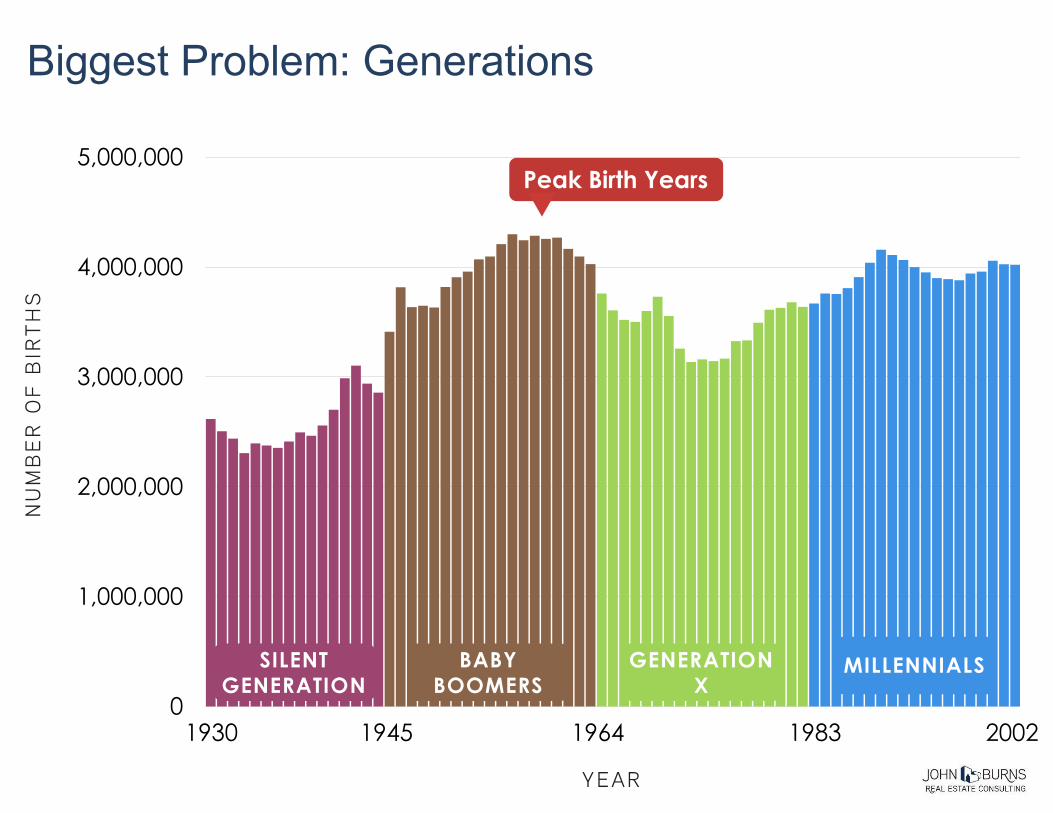

Demographics drive the economy with household formation and home buying

1. Group the Generations into Decade Born

2. Filter through the 4-5-6 Rule

2025347 million (+8%)

INFLUENCERS

LIFE

STAGES

New Framework for Demographic Clarity

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

NU

MB

ER

OF

BIR

TH

S

YEAR

Peak Birth Years

1930 1945 1964 1983 2002

SILENT

GENERATION

BABY

BOOMERS

GENERATION

XMILLENNIALS

Biggest Problem: Generations

32 year old

Working Father

16 year old

High School Junior

1984 2002M I L L E N N I A L S

What do these two have in common?

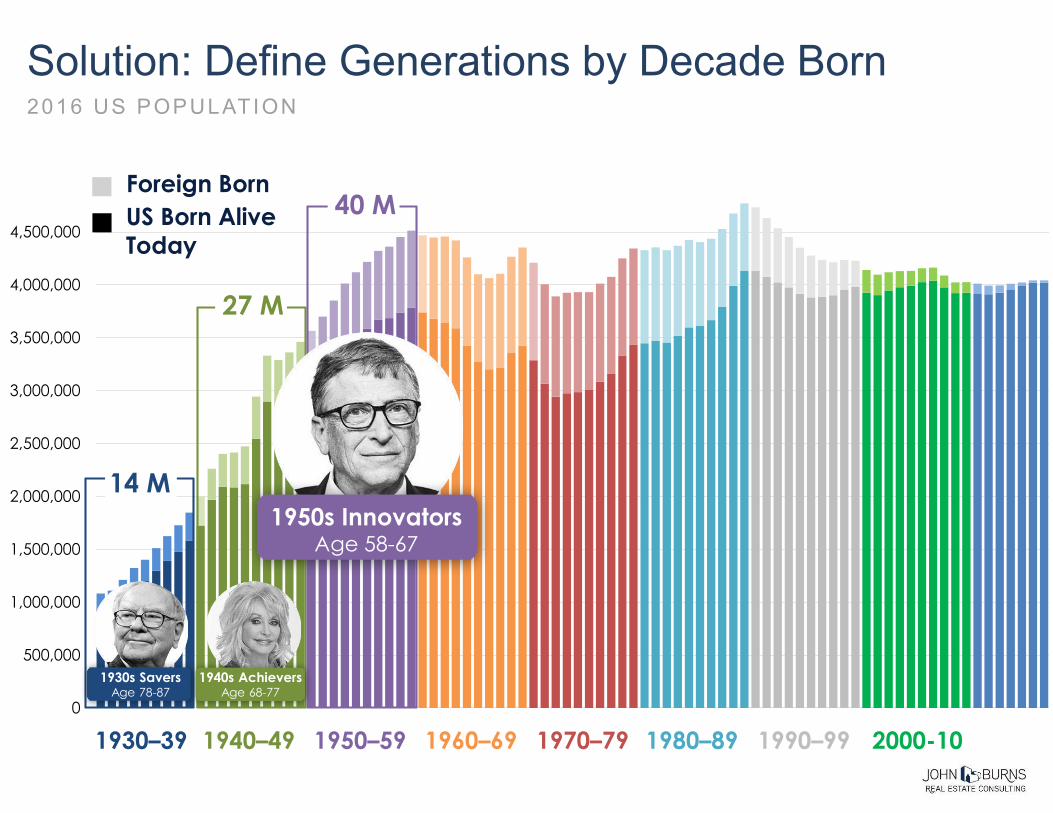

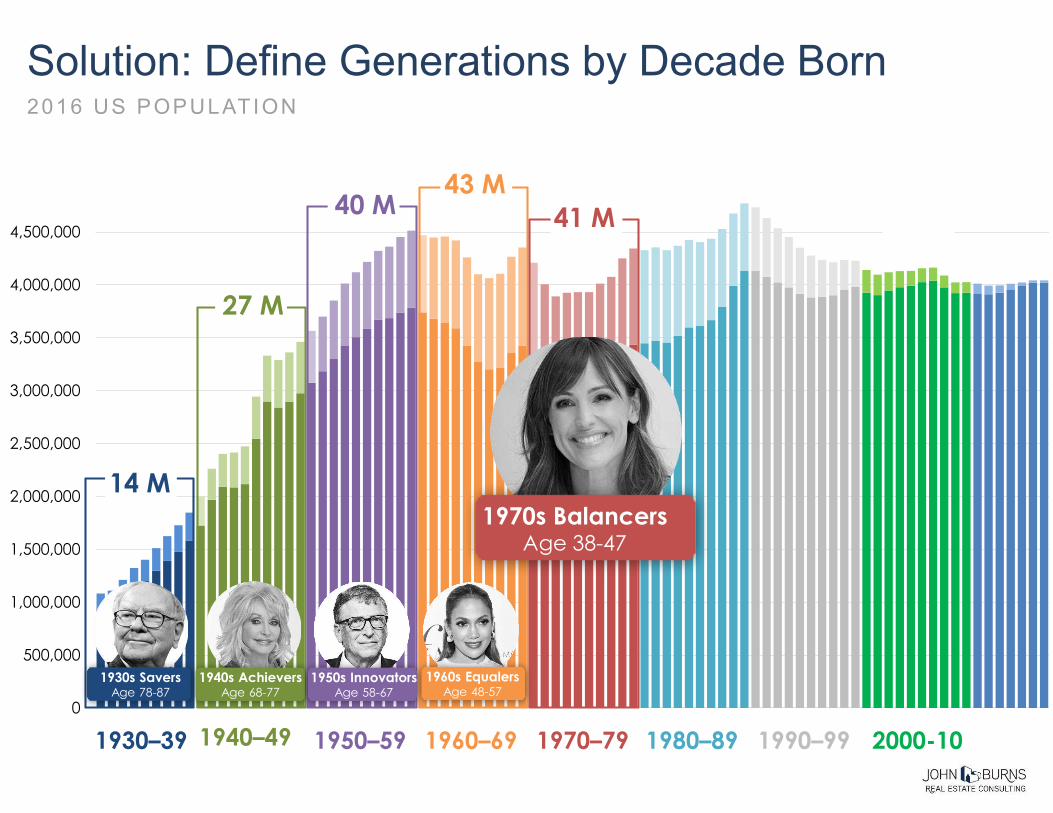

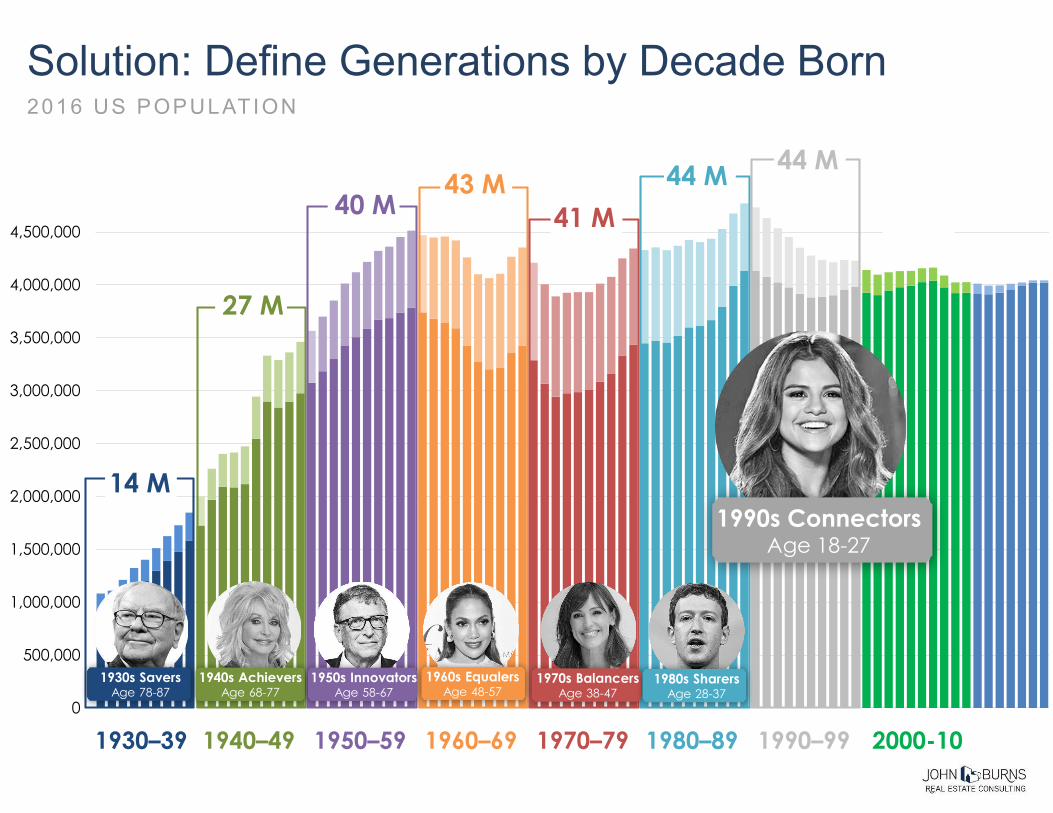

Solution: Define Generations by Decade Born2016 US POPULATION

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000US Born Alive

Today

Foreign Born

27 M

40 M

1930s SaversAge 78-87

1940s AchieversAge 68-77

14 M

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

1950s InnovatorsAge 58-67

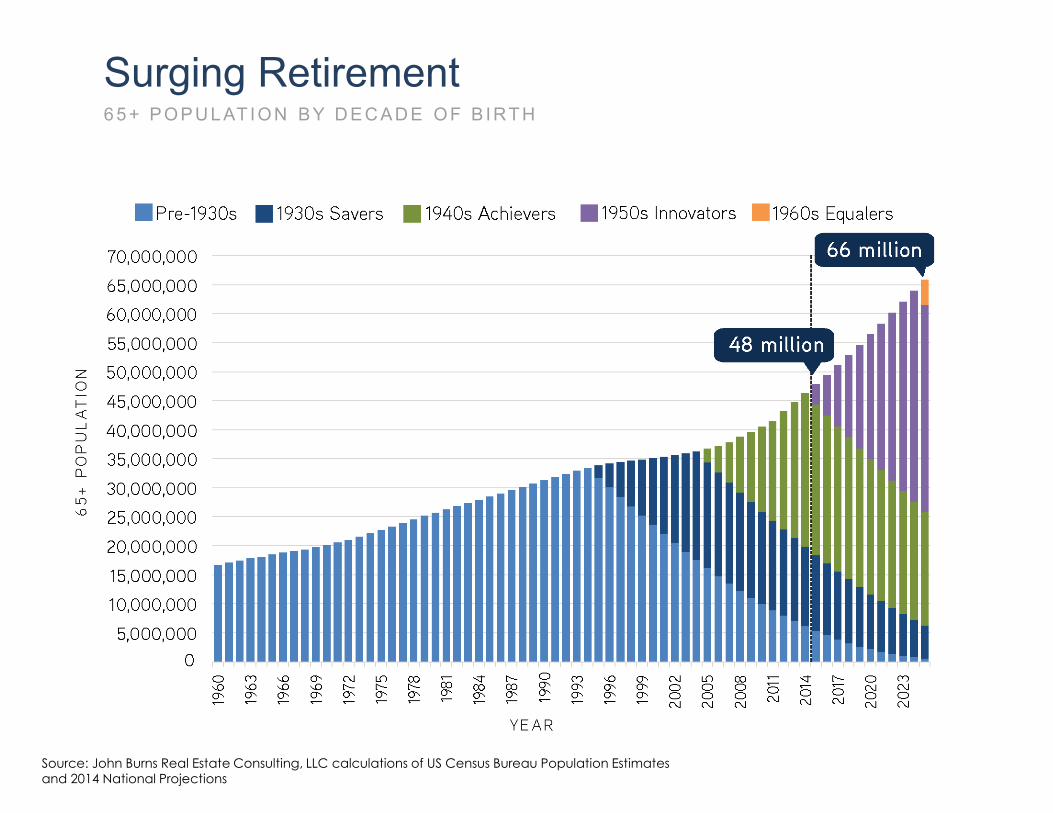

Surging Retirement6 5 + PO PU L AT IO N BY D EC AD E O F B IRT H

Source: John Burns Real Estate Consulting, LLC calculations of US Census Bureau Population Estimates

and 2014 National Projections

1930s

I N N O V A T O R S

1950s

40 Million Aged 57-66

1930s

I N N O V A T O R S

1950s

40 Million Aged 57-66

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

27 M

40 M43 M

1930s SaversAge 78-87

1940s AchieversAge 68-77

1950s InnovatorsAge 58-67

14 M

1960s EqualersAge 48-57

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

Step 1: Define Generations by Decade Born2016 US POPULATION

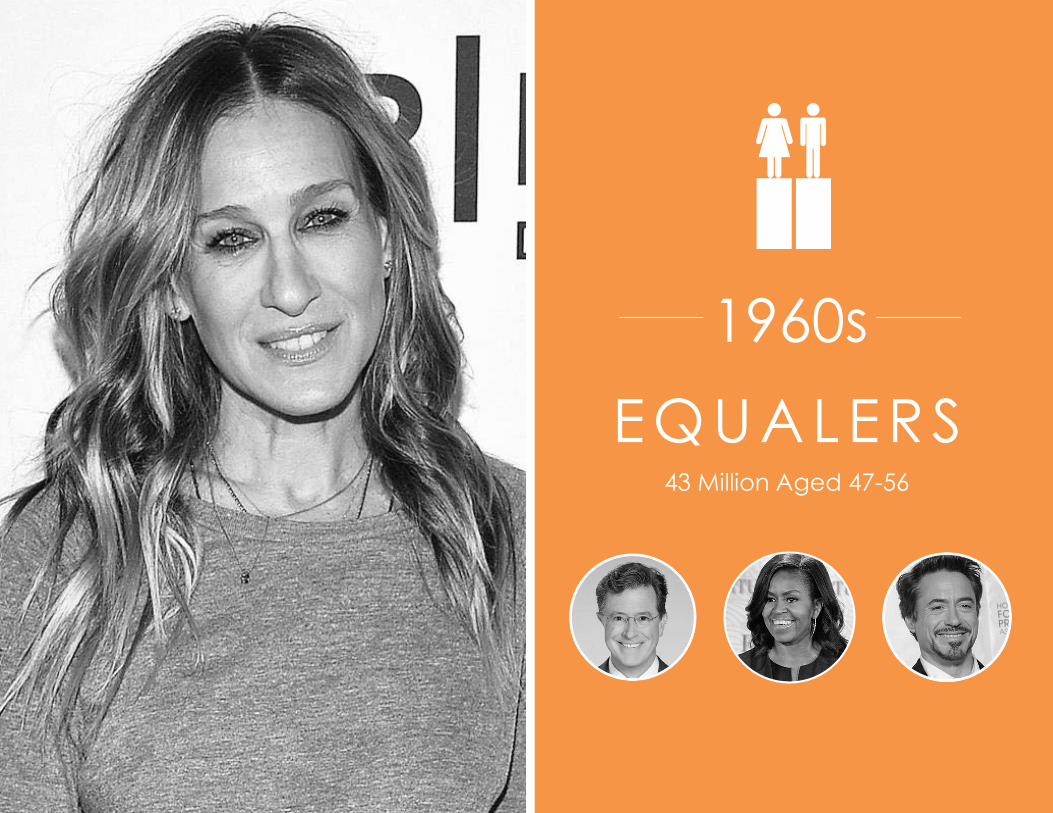

EQUALERS

1960s

43 Million Aged 47-56

EQUALERS

1960s

43 Million Aged 47-56

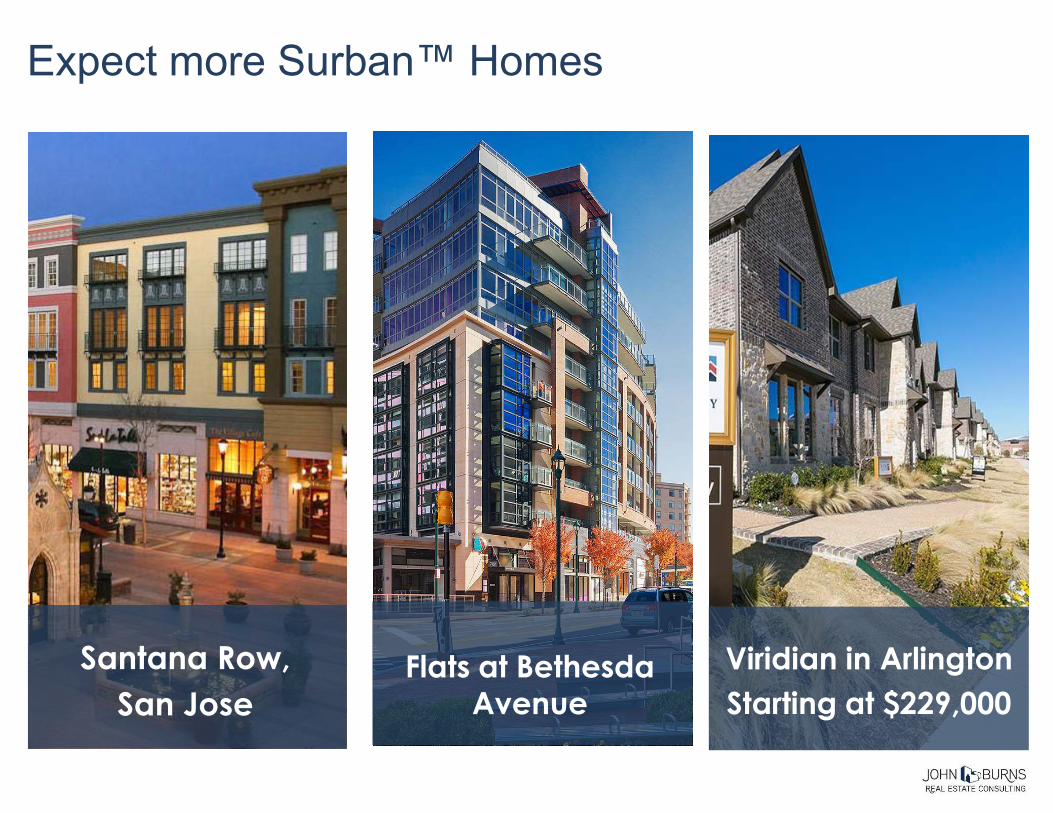

Expect more Surban™ Homes

Santana Row,

San Jose

Viridian in Arlington

Starting at $229,000Flats at Bethesda

Avenue

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

27 M

40 M43 M

41 M

1930s SaversAge 78-87

1940s AchieversAge 68-77

1950s InnovatorsAge 58-67

14 M

1970s BalancersAge 38-47

1960s EqualersAge 48-57

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

Solution: Define Generations by Decade Born2016 US POPULATION

Source: John Burns Real Estate Consulting, LLC calculations of Bureau of Labor Statistics data; color-coded

based on the year a generation turns 20

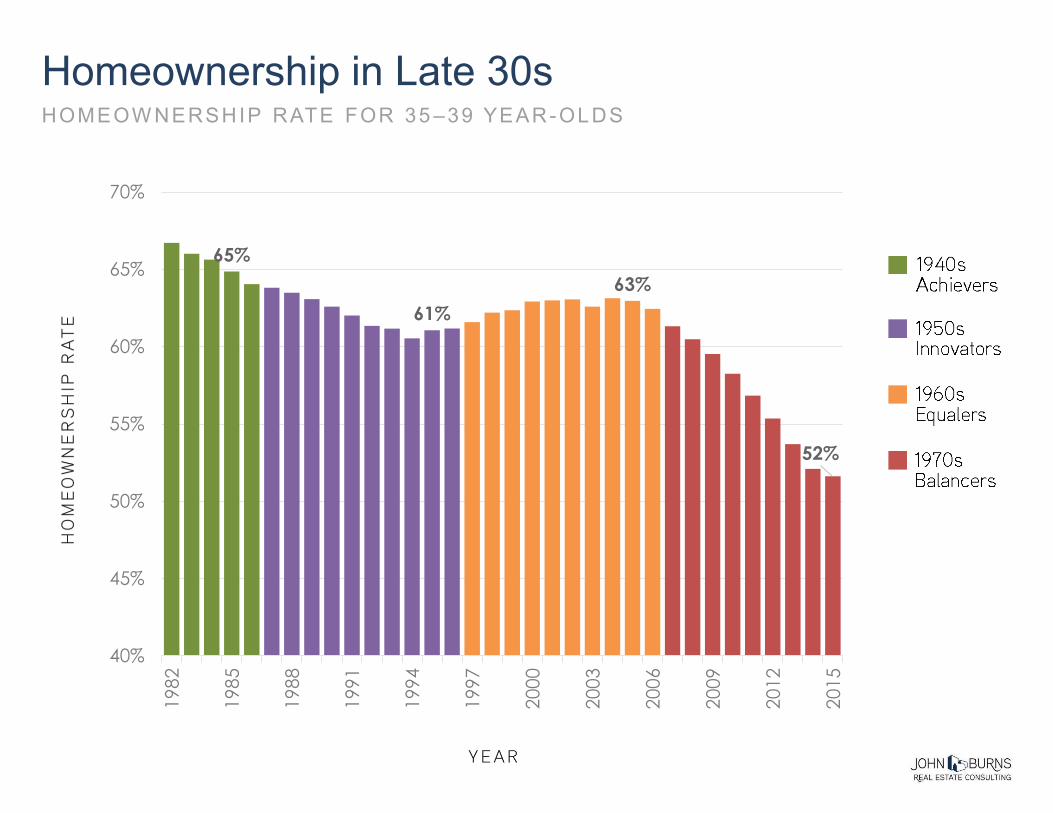

37%

Fewer WorkingFEMALE LABOR FORCE PARTICIPATION RATE, AGES 20 –64

44%

23%

29%

More Stay-at-Home MomsSHARE OF MOMS WHO STAY AT HOME FULL T IME

65%

61%

63%

52%

40%

45%

50%

55%

60%

65%

70%1

98

2

198

5

198

8

199

1

199

4

199

7

200

0

200

3

200

6

200

9

201

2

201

5

Homeownership in Late 30sHOMEOW NERSHIP RATE FOR 35 –39 YEAR-OLDS

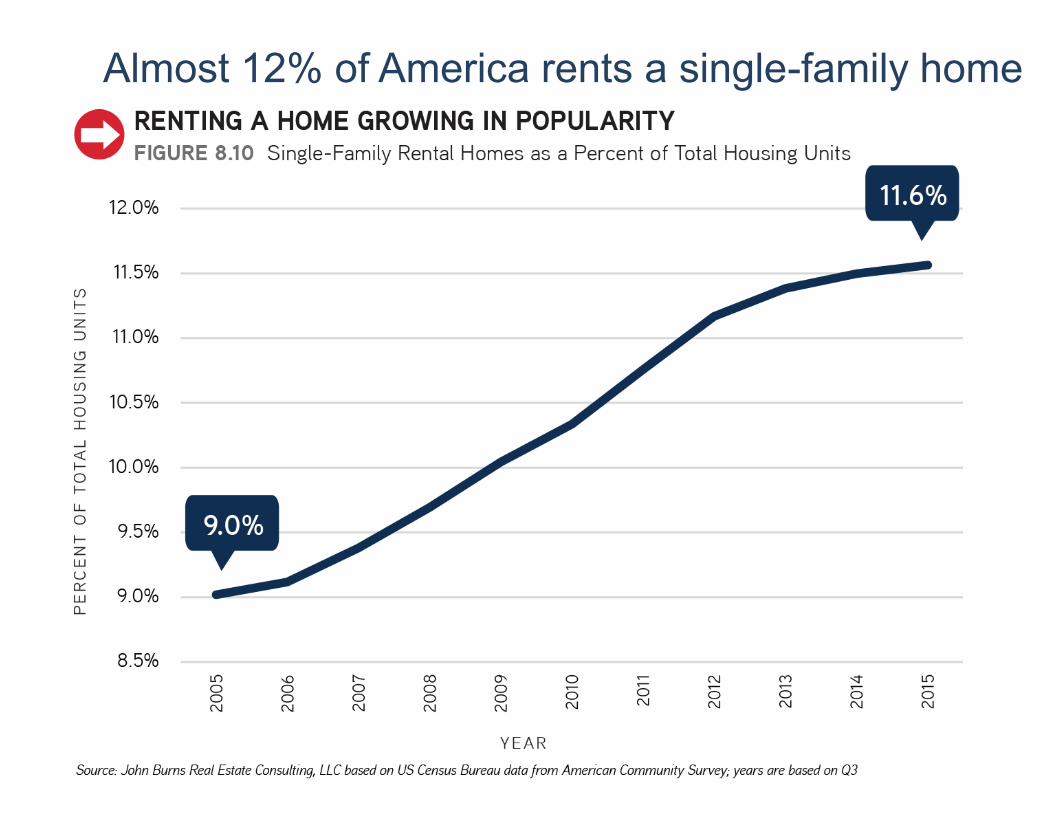

Almost 12% of America rents a single-family home

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

27 M

40 M43 M

41 M

44 M

1930s SaversAge 78-87

1970s BalancersAge 38-47

1940s AchieversAge 68-77

1950s InnovatorsAge 58-67

14 M

1980s SharersAge 28-37

1960s EqualersAge 48-57

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

Solution: Define Generations by Decade Born2016 US POPULATION

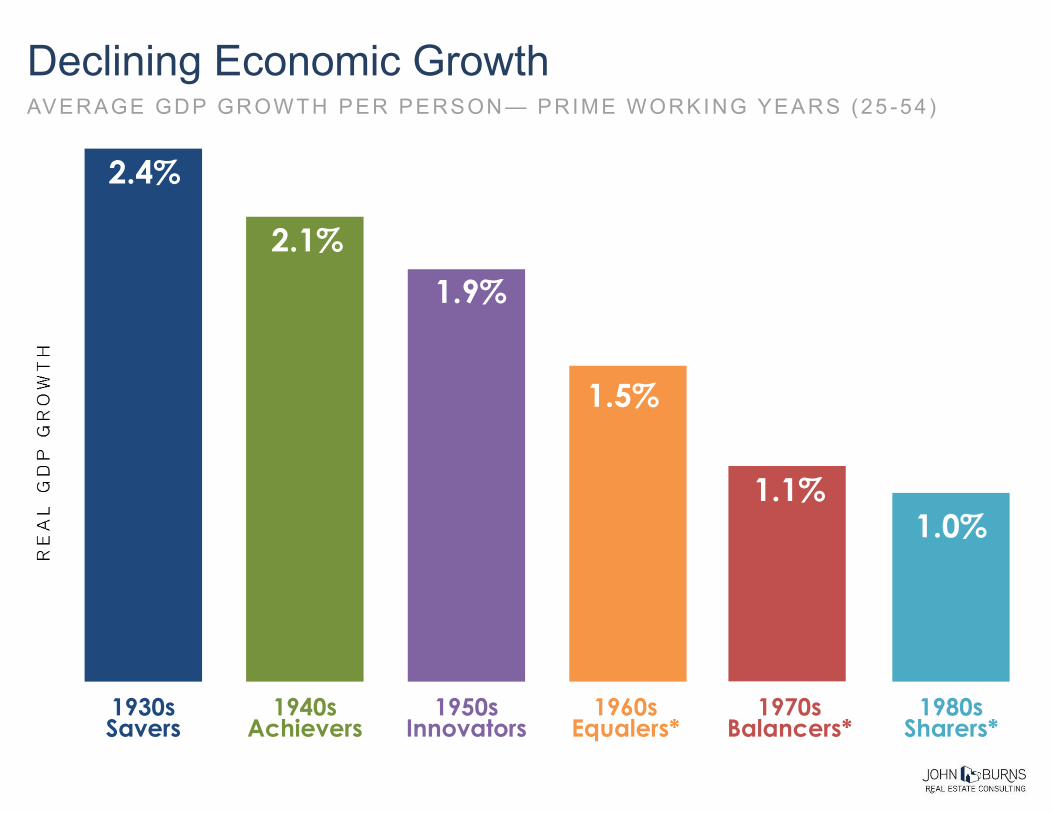

2.4%

2.1%

1.9%

1.5%

1.1%1.0%

1930sSavers

1940sAchievers

1950sInnovators

1960sEqualers*

1970sBalancers*

1980sSharers*

Declining Economic GrowthAVERAGE GDP GROWTH PER PERSON — PRIME WORKING YEARS (25 -54)

SHARERS

1980s

44 Million Aged 27-36

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

27 M

40 M43 M

41 M

44 M44 M

1930s SaversAge 78-87

1970s BalancersAge 38-47

1980s SharersAge 28-37

1940s AchieversAge 68-77

1990s ConnectorsAge 18-27

1950s InnovatorsAge 58-67

14 M

1960s EqualersAge 48-57

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

Solution: Define Generations by Decade Born2016 US POPULATION

Urban and suburban will capture a high share of growthSHARE OF HOUSEHOLD GROW TH BY DECADE

Source: John Burns Real Estate Consulting, LLC based on US Census Bureau data

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

27 M

40 M43 M

41 M

44 M44 M

41 M

1930s SaversAge 78-87

1970s BalancersAge 38-47

1980s SharersAge 28-37

1990s ConnectorsAge 18-27

1940s AchieversAge 68-77

1950s InnovatorsAge 58-67

14 M

1960s EqualersAge 48-57

2000s GlobalsAge 8-17

1930–39 1940–49 1950–59 1960–69 1970–79 1980–89 1990–99 2000-10

Solution: Define Generations by Decade Born2016 US POPULATION

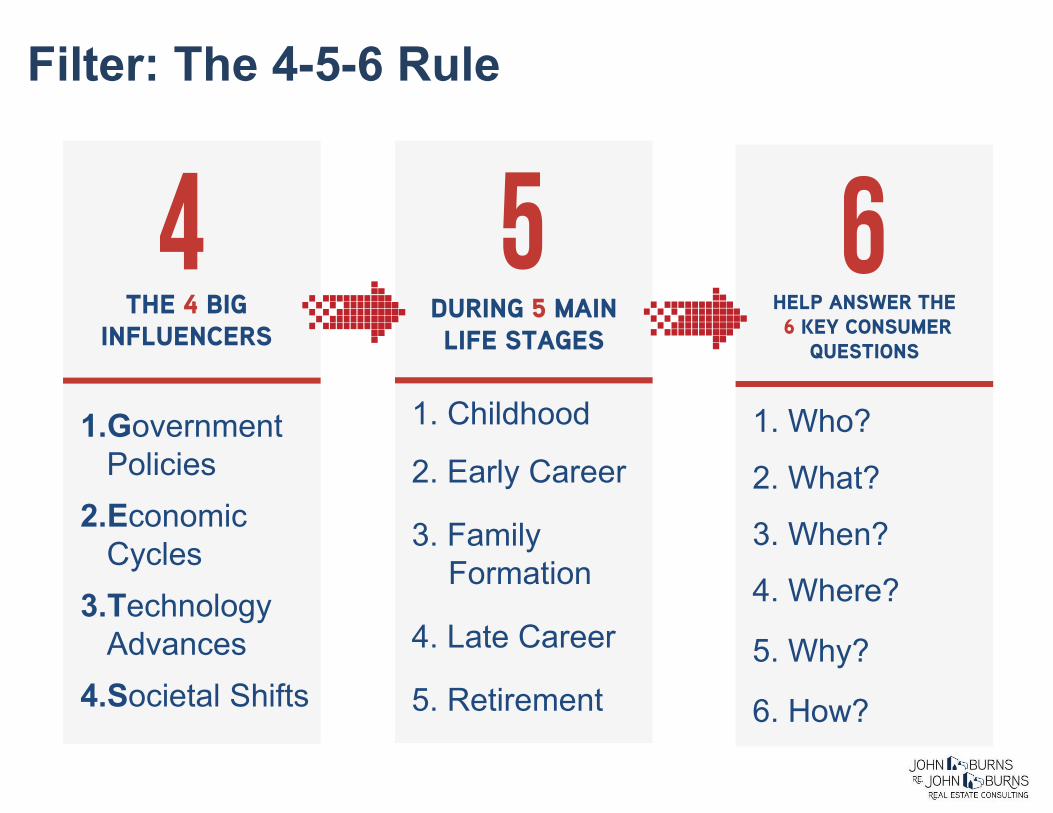

THE 4 BIG

INFLUENCERS

1.Government Policies

2.Economic Cycles

3.Technology Advances

4.Societal Shifts

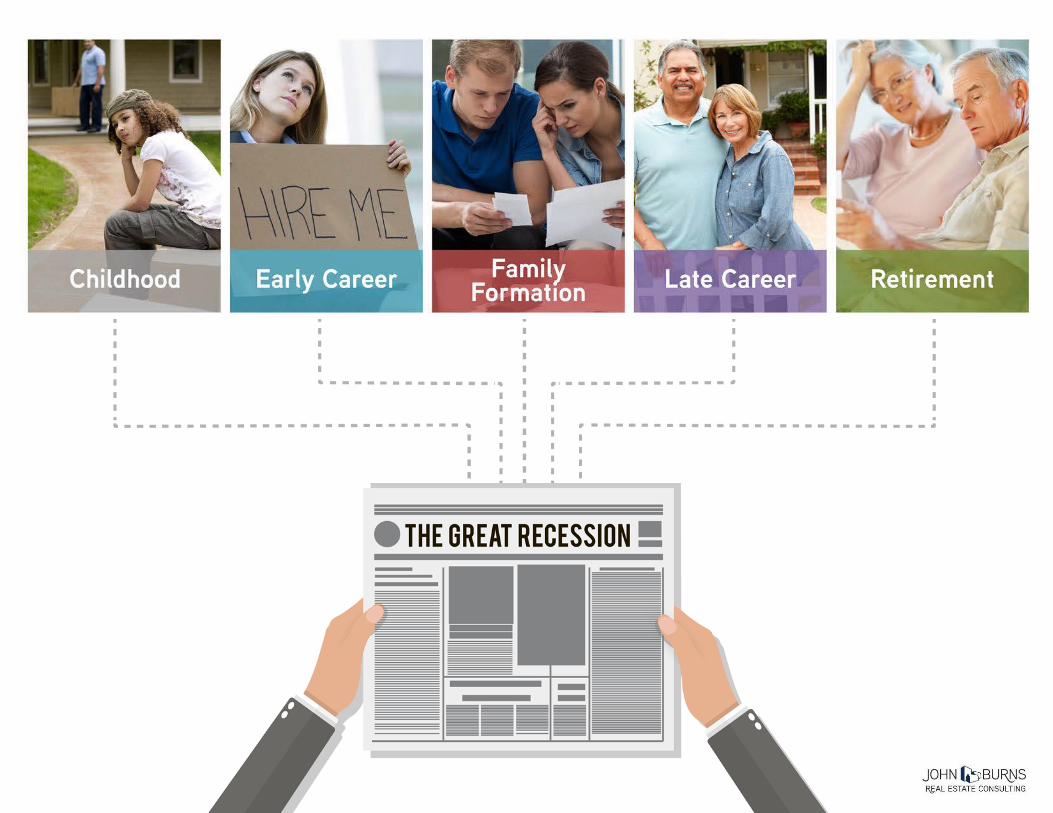

DURING 5 MAIN

LIFE STAGES

1. Childhood

2. Early Career

3. Family Formation

4. Late Career

5. Retirement

Filter: The 4-5-6 Rule

HELP ANSWER THE

6 KEY CONSUMER

QUESTIONS

1. Who?

2. What?

3. When?

4. Where?

5. Why?

6. How?

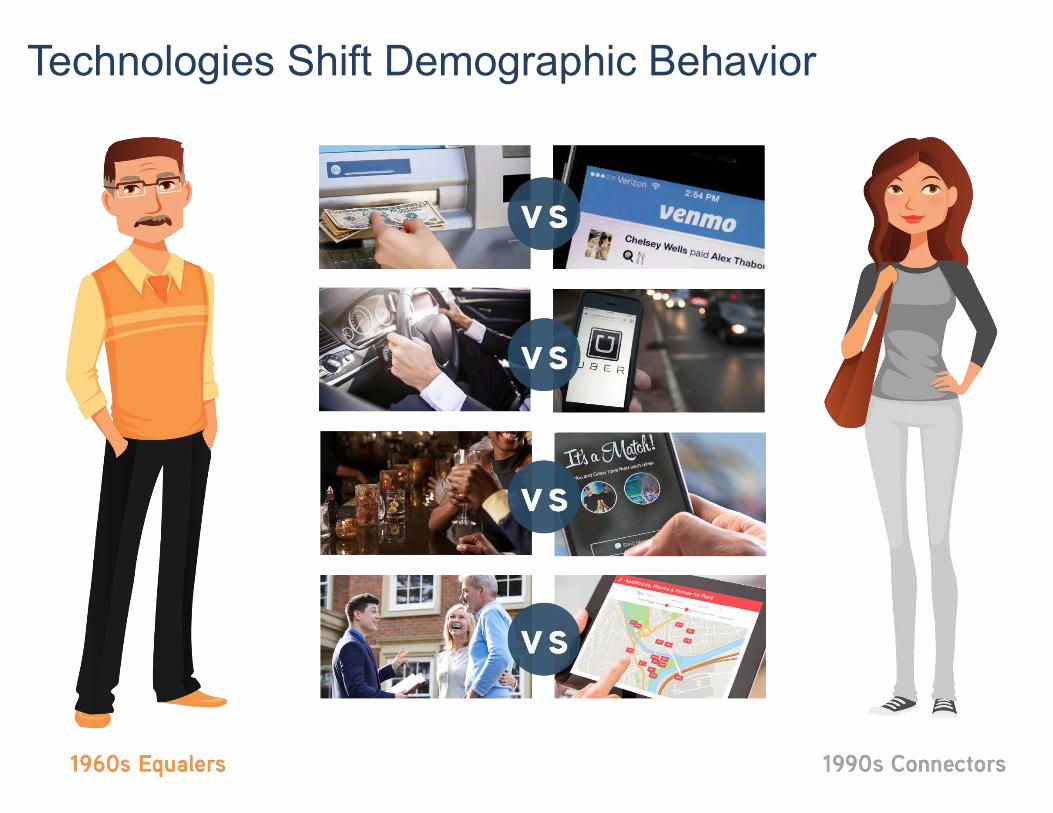

Technologies Shift Demographic Behavior

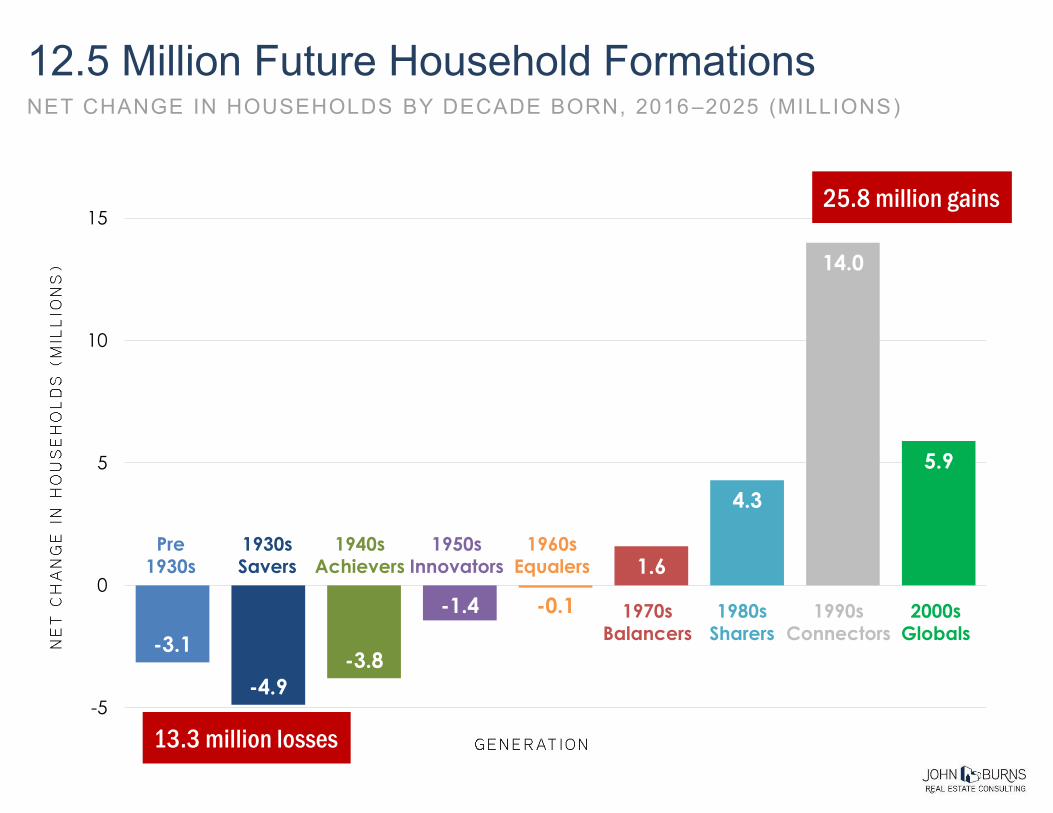

Each generation from 1950 on should form 23-24 million households.ESTIMATED 2016 HOUSEHOLDS BY DECADE BORN

-3.1

-4.9

-3.8

-1.4 -0.1

1.6

4.3

14.0

5.9

-5

0

5

10

15

Pre 1930s

1930sSavers

1940sAchievers

1950sInnovators

1960sEqualers

1970sBalancers

1980sSharers

1990sConnectors

2000sGlobals

13.3 million losses

25.8 million gains

12.5 Million Future Household FormationsNET CHANGE IN HOUSEHOLDS BY DECADE BORN, 2016 –2025 (MILLIONS)

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Under Age 45

Age 45–64

Age 65+

0.01 M

0.8 M

2.5 M

-0.8 M

-0.2 M

5.4 M

4.3 M

0.5 M

Big Shift in Household CompositionHOUSEHOLD FORMATION BY AGE GROUP, 2016–2025

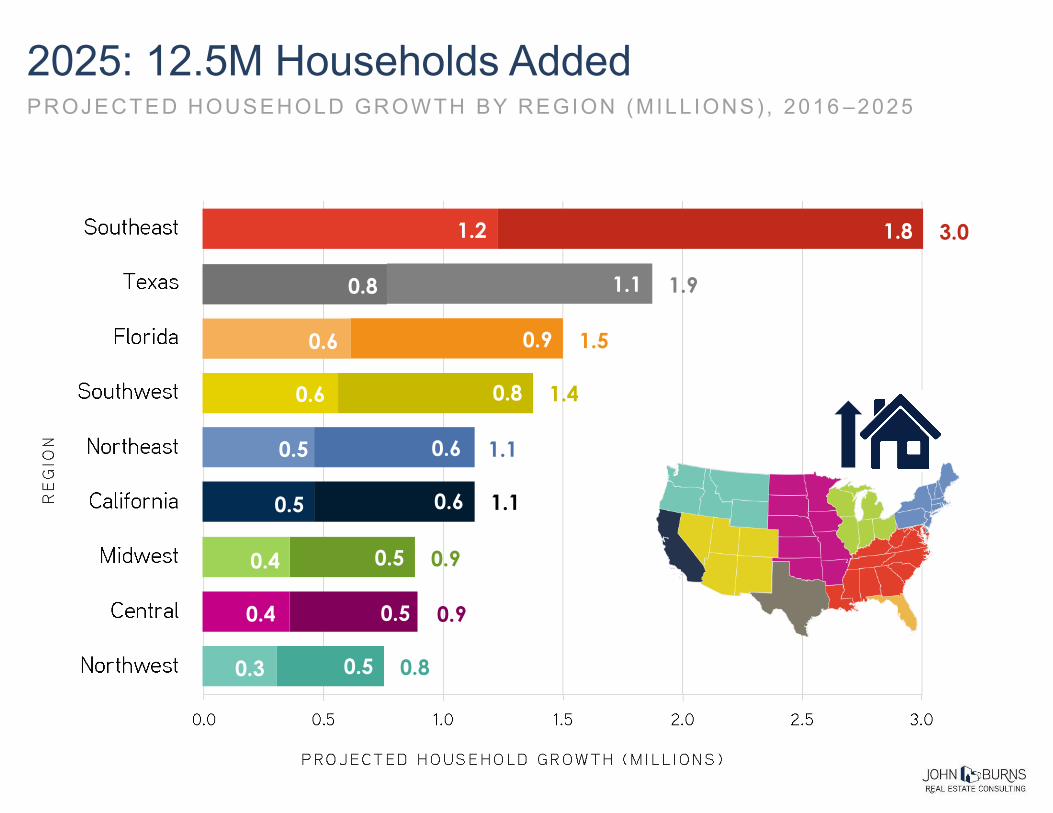

1.1

0.9

0.8

1.8

0.5

0.6

0.5

0.5

0.6

2025: 12.5M Households AddedPROJECTED HOUSEHOLD GROWTH BY REGION (MILL IONS) , 2016 –2025

Owners Renters

1.2

0.8

0.6

0.6

0.3

0.5

0.4

0.4

0.5

1.9

1.5

1.4

3.0

0.8

1.1

0.9

0.9

1.1

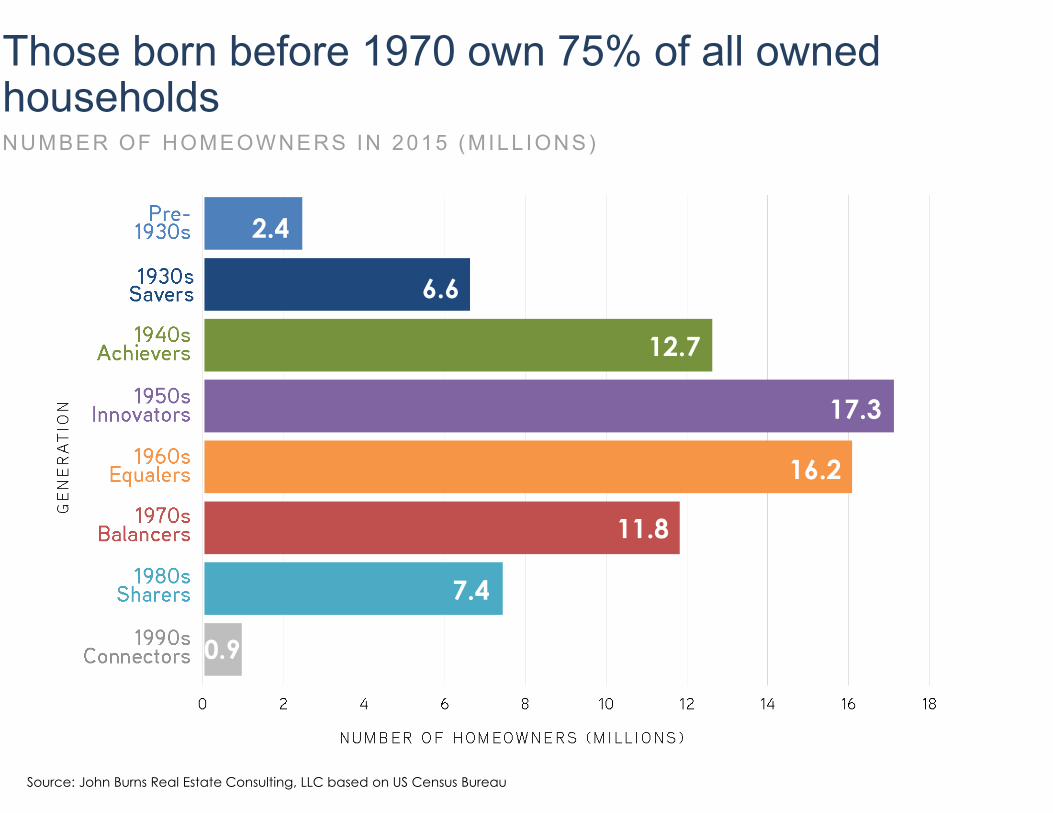

Those born before 1970 own 75% of all owned householdsNUMBER OF HOMEOWNERS IN 2015 (MILL IONS)

2.4

6.6

12.7

17.3

16.2

11.8

7.4

0.9

Source: John Burns Real Estate Consulting, LLC based on US Census Bureau

Sources: John Burns Real Estate Consulting

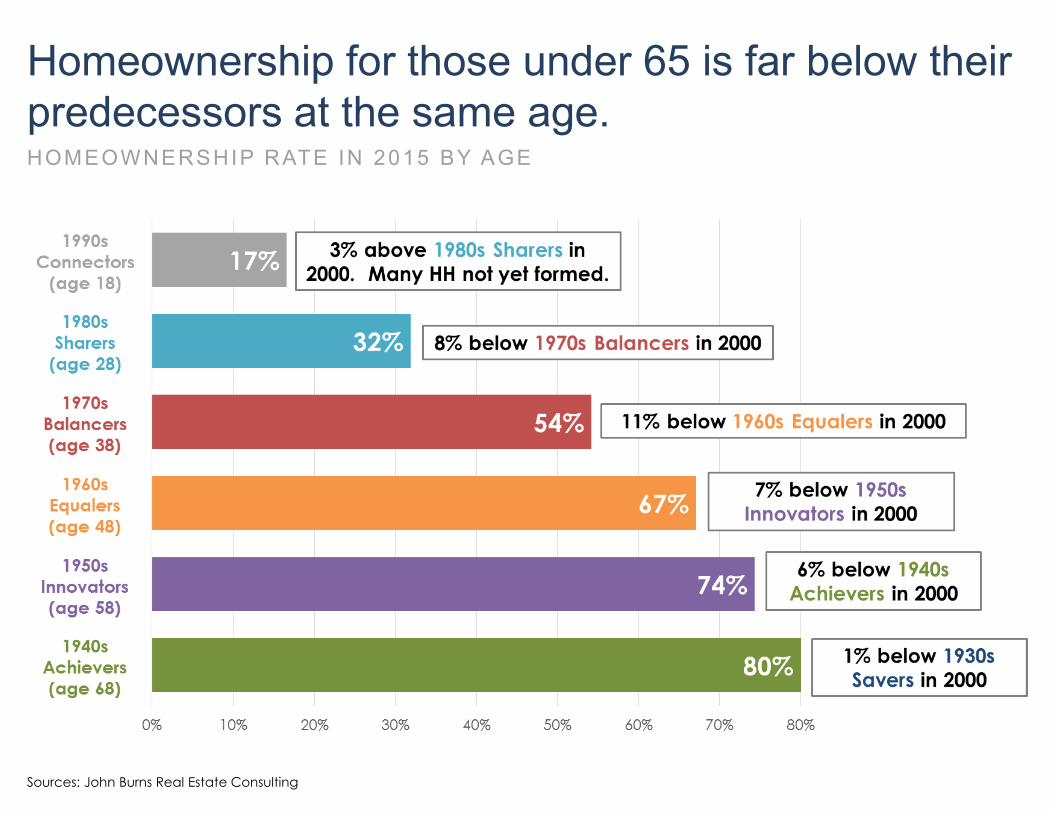

Homeownership for those under 65 is far below their predecessors at the same age.HOMEOWNERSHIP RATE IN 2015 BY AGE

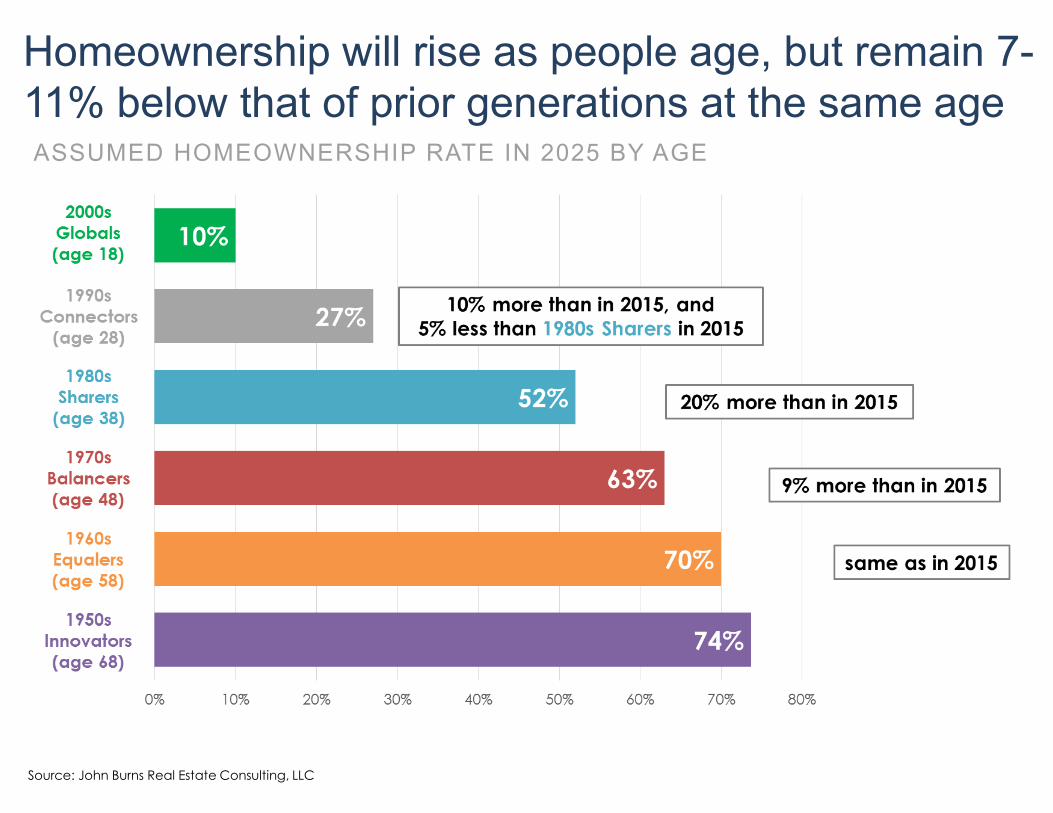

Homeownership will rise as people age, but remain 7-11% below that of prior generations at the same ageASSUMED HOMEOWNERSHIP RATE IN 2025 BY AGE

Source: John Burns Real Estate Consulting, LLC

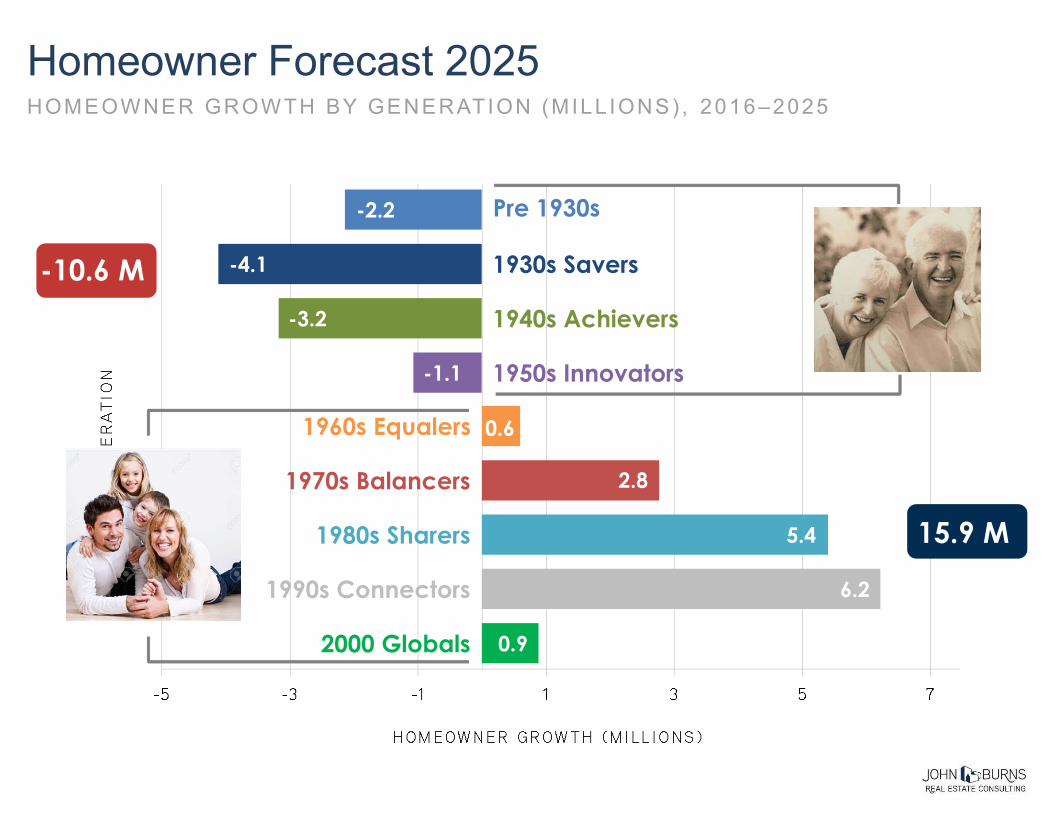

Pre 1930s

1930s Savers

1940s Achievers

1950s Innovators

1960s Equalers

1970s Balancers

1980s Sharers

1990s Connectors

2000 Globals

-2.2

-4.1

-3.2

-1.1

0.6

2.8

5.4

6.2

0.9

15.9 M

Homeowner Forecast 2025HOMEOWNER GROWTH BY GENERATION (MILL IONS) , 2016–2025

-10.6 M

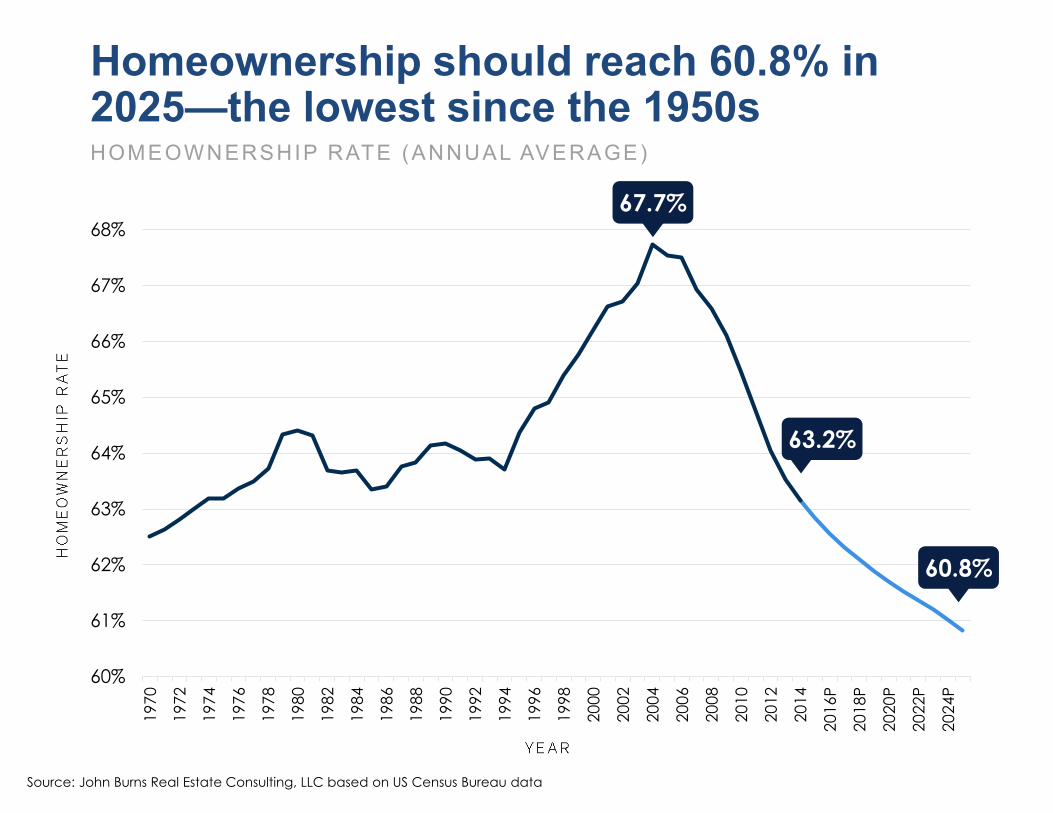

Homeownership should reach 60.8% in 2025—the lowest since the 1950sHOMEOWNERSHIP RATE (ANNUAL AVERAGE)

60%

61%

62%

63%

64%

65%

66%

67%

68%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

P

20

18

P

20

20

P

20

22

P

20

24

P

67.7%

63.2%

60.8%

Source: John Burns Real Estate Consulting, LLC based on US Census Bureau data

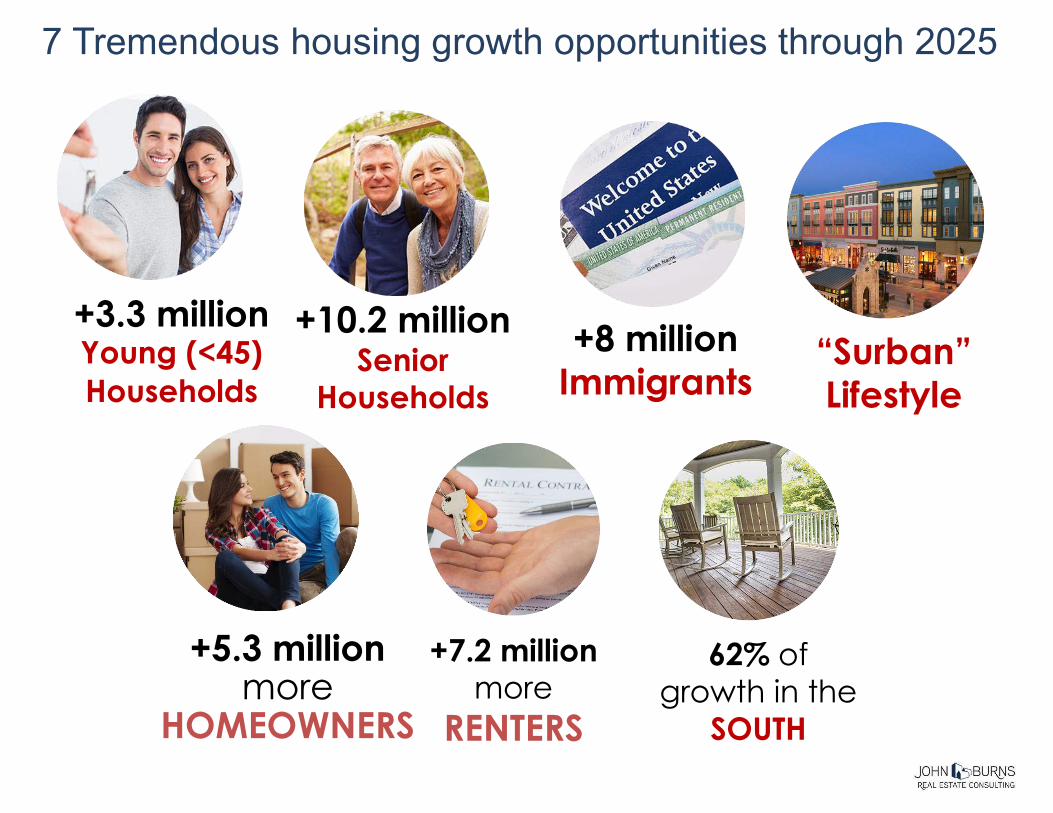

+3.3 millionYoung (<45)

Households

+8 million

Immigrants

+10.2 million Senior

Households

+5.3 millionmore

HOMEOWNERS

7 Tremendous housing growth opportunities through 2025

+7.2 millionmore

RENTERS

62% of

growth in the

SOUTH

“Surban”

Lifestyle

![Por Una Cabeza - Arr.williams-Perlman[1]](https://img.pdfslide.us/doc/110x75/545db836b0af9ff1168b4710/por-una-cabeza-arrwilliams-perlman1.jpg)