Embed Size (px)

Citation preview

Taxation RoI

Revision 3

Topic: Payroll & BIK

Ciarán Armstrong

12th May 2020

PAYE system – methods of calculation

Methods of calculating tax under PAYE

1. Cumulative basis (a) no changes in monthly figures (b) changes in monthly figures

2. Emergency basis (a) with PPS supplied (b) no PPS

3. Week 1/ Month 1

PRSI is always calculated on a week 1 basis.

Calculate AX & AL PRSI credit on weekly amounts.

To determine PRSI class for monthly salaries: * 12/52

If total PRSI is required, use combined Employee & Employer figure.

In exam questions USC can usually be calculated on a week 1/month 1 and is more time effective.

PAYE is calculated on all taxable Schedule E less allowable Pension Contributions.

USC & PRSI: Pension Contributions are not deductible, and calculations are based on total Schedule E.

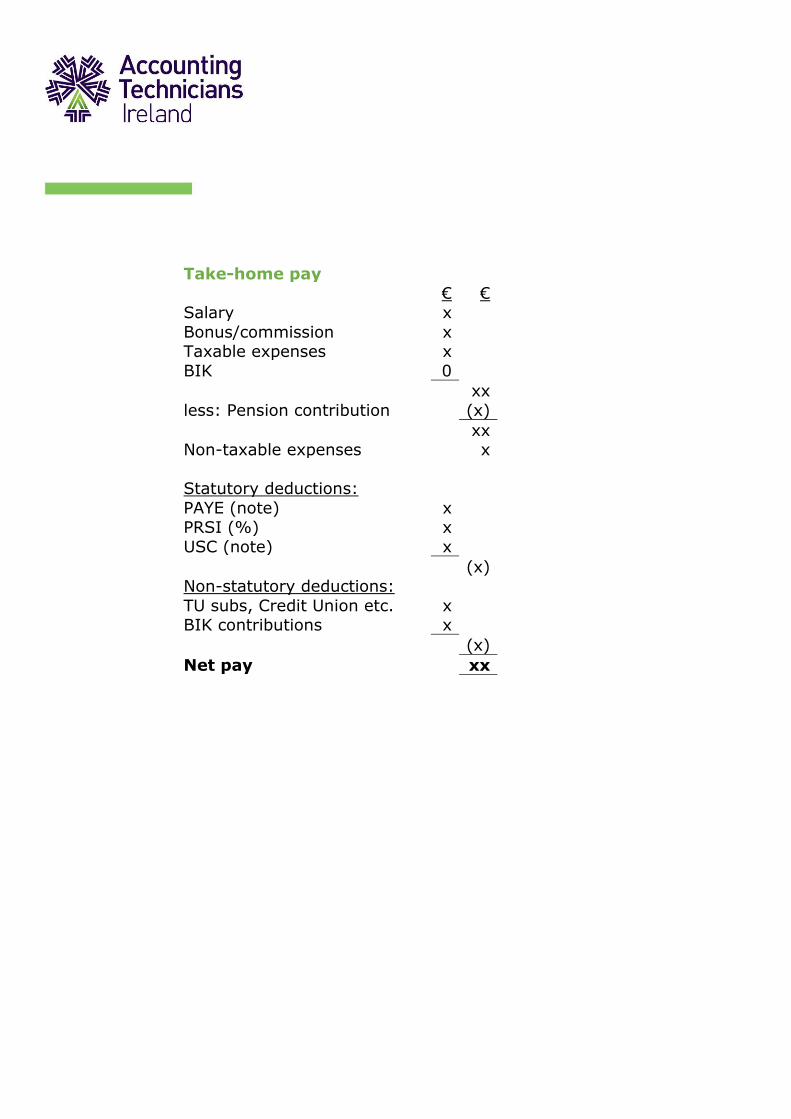

Take-home pay

€ € Salary x

Bonus/commission x Taxable expenses x

BIK 0

xx

less: Pension contribution (x)

xx Non-taxable expenses x

Statutory deductions:

PAYE (note) x PRSI (%) x

USC (note) x

(x) Non-statutory deductions:

TU subs, Credit Union etc. x BIK contributions x

(x)

Net pay xx

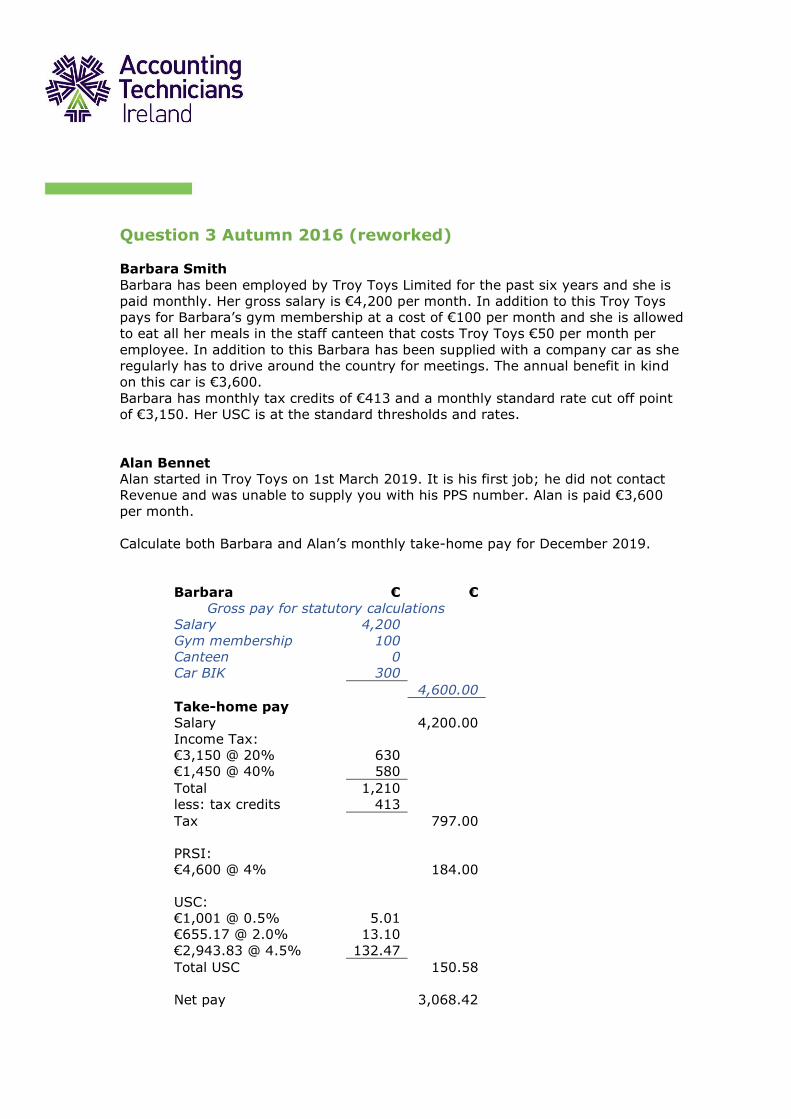

Question 3 Autumn 2016 (reworked)

Barbara Smith

Barbara has been employed by Troy Toys Limited for the past six years and she is

paid monthly. Her gross salary is €4,200 per month. In addition to this Troy Toys

pays for Barbara’s gym membership at a cost of €100 per month and she is allowed

to eat all her meals in the staff canteen that costs Troy Toys €50 per month per

employee. In addition to this Barbara has been supplied with a company car as she

regularly has to drive around the country for meetings. The annual benefit in kind

on this car is €3,600.

Barbara has monthly tax credits of €413 and a monthly standard rate cut off point

of €3,150. Her USC is at the standard thresholds and rates.

Alan Bennet

Alan started in Troy Toys on 1st March 2019. It is his first job; he did not contact

Revenue and was unable to supply you with his PPS number. Alan is paid €3,600

per month.

Calculate both Barbara and Alan’s monthly take-home pay for December 2019.

Barbara € €

Gross pay for statutory calculations

Salary 4,200

Gym membership 100

Canteen 0

Car BIK 300

4,600.00

Take-home pay

Salary 4,200.00

Income Tax:

€3,150 @ 20% 630

€1,450 @ 40% 580

Total 1,210

less: tax credits 413

Tax 797.00

PRSI:

€4,600 @ 4% 184.00

USC:

€1,001 @ 0.5% 5.01

€655.17 @ 2.0% 13.10

€2,943.83 @ 4.5% 132.47

Total USC 150.58

Net pay 3,068.42

Payroll question: Glynis

Glynis has been employed by Lugalla Ltd. for a number of years. Details of her

monthly salary and deductions for each of the months January to October 2019 are

as follows:

€

Salary 3.600

Pension contribution 180

Savings club deduction 400

3.020

The RPN details used for payroll calculation in months 1 to 10 showed a monthly

tax credit of €356 and a monthly standard rate cut off point of €3,150 for Glynis.

For month 11 Glynis received a pay increase and her revised salary and deductions

are:

€

Salary 3.780

Pension contribution 190

Savings club refund 4.000

7.590

In addition to the pay increase from the 1st November 2019, Glynis was given a

company car and the annual benefit in kind has been calculated at €5,040.

An RPN was received in time for the calculation of the wages for month 11 of the

2019 tax year showing revised monthly tax credits of €396 and a monthly standard

rate cut off point of €3,250

Calculate Glynis’s take-home pay for month 11, assuming standard USC

rates and thresholds apply.

Glynis: take home pay October 2019

€ €

Salary 3,780.00

Less pension contribution 190.00

BIK -

3,590.00

Statutory deductions:

PAYE (note 2) (42.00)

PRSI {(€3,780+€420) *4%} 168.00

USC (note 3) 132.58

258.58

3,331.42

Savings club refund 4,000.00

7,331.42

Note 1: pay to end of October:

€ 1 mth 10 mths

Salary 3,600 36,000

Pension 180 1,800

Taxable 3,420 34,200

3.150 @ 20% 630

270 @ 40% 108

3,420 738

Tax credits 356

382 3,820

Note 2: PAYE

€ Mth 11

Salary 3,780

Pension (190)

BIK (€5,040/12) 420

Taxable 4,010

p/e October 34,200

cumulative 38,210

Revised SRCOP (€32250*11) 35,750

@20% 7,150

@40% (€2,460) 984

Total tax 8,134

Revised tax credits (€396*11) 4,356

Cumulative tax 3,778

Tax paid 3,820

Tax this month (42)

Note 3: USC

€ €

@ 0.5% 1,001.00 5.01

@ 2.0% 655.17 13.10

@ 4.5% (4,200.00 – 1,656.17) 114.47

132.58

Payroll question types Cumulative basis - no monthly changes

Simon is paid an annual salary of €48,000. He makes a monthly contribution to

the pension scheme of €1,000 through payroll. He has the use of a company car

for the year and the monthly benefit in kind is €600. He is single and has a

monthly standard rate cut-off of €2,879.17 and monthly tax credits of €275.

Calculate Simon’s net pay for January 2019.

Solution: Simon € €

Gross salary 4,000.00

BIK 600.00

4,600.00

Less: pension contributions (1,000.00)

3,600.00

(1) PAYE 3,600.00

€2,879.17 @ 20% 575.83

€720.83 @ 40% 288.77

864.16

Less: tax credits 275.00

589.16

(2) PRSI €4,600 @ 4% 184.00

(3) USC

€1,001@ 0.5% 5.00

€655.17 @ 2% 13.10

€2,943.83 @ 4.5% 132.47

150.57

Take-home pay:

Salary (excl. BIK) 4,000.00

Pension contributions (1,000.00)

3,000.00

PAYE (1) 589.16

PRSI (2) 184.00

USC (3) 150.57

923.73

Net pay 2,076.27

Cumulative basis - monthly changes

See Glynis example

Emergency basis – no PPS

Alan started in AF2 on 1st March 2019. This was his first job, no RPN has been

received from Revenue and Alan was unable to supply his PPS number. Alan is paid

€3,600 per month.

All of Alan’s salary of €3,600.00 will be taxed at 40% for PAYE and 8% for USC.

PRSI will be deducted as normal.

Emergency basis with PPS number

Paul started with AFZ straight from college on 1 January 2019 and this is his first

job. No RPN has been received from Revenue. He gave AFZ his PPS number on

commencement of his employment. He is paid €4,200 per month.

January: Alan will be given a COP of €2,942 and tax credits of €0. USC will all be at

8% and PRSI as normal.

February: as for no PPS, all PAYE at 40%.

Week 1/ Month 1 basis

John is paid a salary of €57,600 per year. He makes a monthly contribution to the

company pension scheme of €400. He uses a company car for the full year and the

annual benefit in kind for the car is €6,000. You have the following details for

John:

Monthly SRCOP €2,816.67

Monthly Tax Credits €275.00

Normal USC rates apply

Month 1 basis applies

Calculate John’s take home pay for March 2019.

Other question types

Self-employed USC and PRSI

Sally is a self-employed crafter. She has Case I tax adjusted profits of €125,000 in

2016. She paid €12,000 into a Revenue Approved Pension scheme in 2016. Sally

is 45 years old.

Question 5 May 2019

Jane is self-employed and has Case I tax adjusted profits of €300,000. She made a

retirement annuity contribution of €30,000 which qualifies for tax relief in 2018.

Calculate the total PRSI and Universal Social charge payable by Jane for the 2018

tax year. (4 Marks)

Retirement annuity is not deductible for PRSI & USC, Jane’s liability will be

calculated on €300,000

€ €

PRSI: (class S1)

€300,000 @ 4% 12,000.00

USC: (@ 2019 rates)

€12,012 @ 0.5% 60.06

€7,862 @ 2% 157.24

€50,170 @ 4.5% 2,257.65

€29,956 @ 8% 2,396.48

€200,000 @ 11% 22,000.00

26,871.43

Taxation of Benefits: Q4 May 2016

Kevin has been employed by AB Solutions Ltd for the last ten years and he is paid

on a monthly basis. For the month of July 2015, he earned €4,250 gross. In

addition to his salary Kevin has been provided with a number of benefits as follows:

A bicycle for cycling to and from work each day. This costs AB Solutions Ltd €800

when they purchased it for Kevin in April 2015.

Subsidised canteen meals which are provided to all employees. Kevin estimates this

saves him €120 per month on food.

Kevin is employed in the engineering department and AB Solutions Ltd paid his

annual subscription to Engineers Ireland Ltd amounting to €1,200.

Gym membership of €65 per month.

The month 1 basis applies. Kevin has a monthly SRCOP of €3,150 and a monthly

tax credit of €275. His USC monthly cut off point is €1,001.

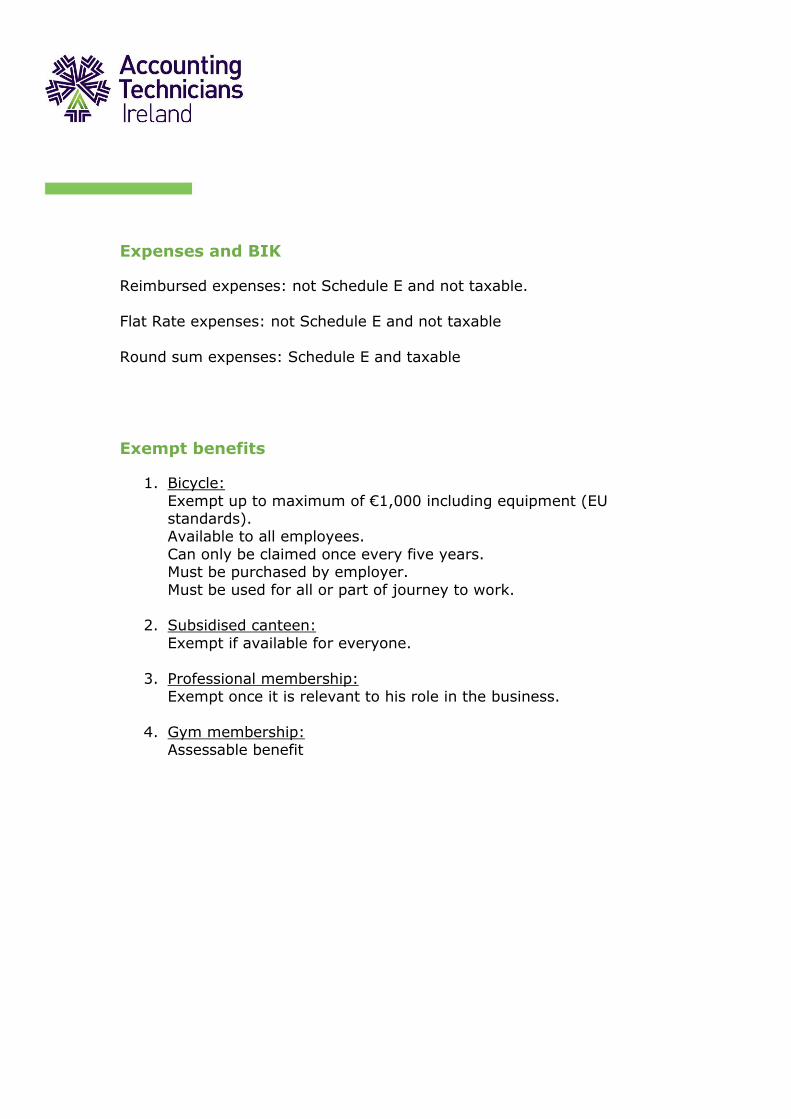

Expenses and BIK

Reimbursed expenses: not Schedule E and not taxable. Flat Rate expenses: not Schedule E and not taxable

Round sum expenses: Schedule E and taxable

Exempt benefits

1. Bicycle:

Exempt up to maximum of €1,000 including equipment (EU standards). Available to all employees.

Can only be claimed once every five years. Must be purchased by employer.

Must be used for all or part of journey to work.

2. Subsidised canteen:

Exempt if available for everyone.

3. Professional membership: Exempt once it is relevant to his role in the business.

4. Gym membership: Assessable benefit

Preferential loans:

Assume all loans are interest payment only and the capital is fully payable at the termination

of the loan unless informed otherwise.

A. Bill was given two loans by his employer in 2016

1. €100,000 towards an addition to his family home @ 2% interest

2. €20,000 to purchase a new car @ 14%

Bill: (1) €2,000 {€100,000 @ (4% - 2%)} addition to family home qualifies

` as loan for PPR.

(2) No BIK as rate charged by employer exceeds Revenue’s specified rate.

B. Amy has the following loans from her employer since 2015.

1. €20,000 @ 4% to purchase new furniture for her first home

2. €10,000 @ 13% for medical bills incurred in respect of her new baby.

3. €80,000 @ 4% towards purchase of an apartment to rent.

Amy: (1) €1,900 {€20,000 @ (13.5% - 4%)} loan for furniture does not

qualify as PPR loan.

(2) €500 {€10,000 @ (13.5% - 13%)}

(3) €7,600 {€80,000 @ (13.5% - 4%)} apartment is for rent not residence.

C. Ritchie works for a bank and has been provided with the following loans

since 2014.

1. €200,000 @ 3% towards purchase of his family home.

2. €100,000 @ 3.6% for improvements to his home.

3. €40,000 @ 3.5% to build a studio in the garden for his wife who is a

painter.

The bank’s rate for customer mortgages is 3.5%

Ritchie: Because he works for a bank the rate available to customers for

mortgages (3.5%) becomes the specified rate.

(1) €1.000 {€200,000 @ (3.5% - 3%)}

(2) No BIK, improvements count at PPR rate and the rate charged of 3.6%

exceeds the adjusted specified rate of 3.5%.

(3) €4,000 {€40,000 @ (13.5% - 3.5%)} the studio is business, not PPR.

D. John was given a loan by his employer on 1st February 2019 of €60,000 @

3.5% to purchase a holiday home. John then sold the home and repaid the

loan on 30th November 2019

John: €5,000 {€60,000 @ (13.5% - 3.5%) * 10/12} loan was for 10

months.

Note: Where the loan is used for employee’s PPR the BIK interest will be treated as interest

paid for the purpose of mortgage interest relief.

Medical insurance premiums

Since October 2013 tax relief on medical insurance premiums is limited to the first €1,000 of the gross premium per adult and €500 per child.

An individual purchases a policy costing €800. They are entitled to tax relief of €160 (€800*20%), meaning the net cost of the policy is €640 and the

individual pays this net amount to the insurance provider.

The insurance provider then claims the tax credit on behalf of the policyholder (even if they are not a taxpayer). This is known as Tax Relief at Source (TRS).

Premium paid by employer: As it is a payment of an employee expense by the employer a BIK will arise.

In the example above the employer must refund the TRS of €160 to Revenue (the individual is entitled to the tax relief, not the employer). The

employer has now paid the gross amount of the premium €800 (€640 to insurance provider and €160 refunded to Revenue), and therefore the

employee is liable for BIK on the full benefit of €800. The employee is now entitled to claim the tax relief directly either by

requesting it be added to his Tax Credits or including it on his Taxation Return.

Other BIK

Provision of Creche/Childcare facilities.

Provision of service or payment of expenses by employer.

Employer provided accommodation:

See exempt benefits (3.4.1 no.1)

Market rent plus costs borne by the employer

Actual rent paid by employer less employee contribution.

Sample narrative questions

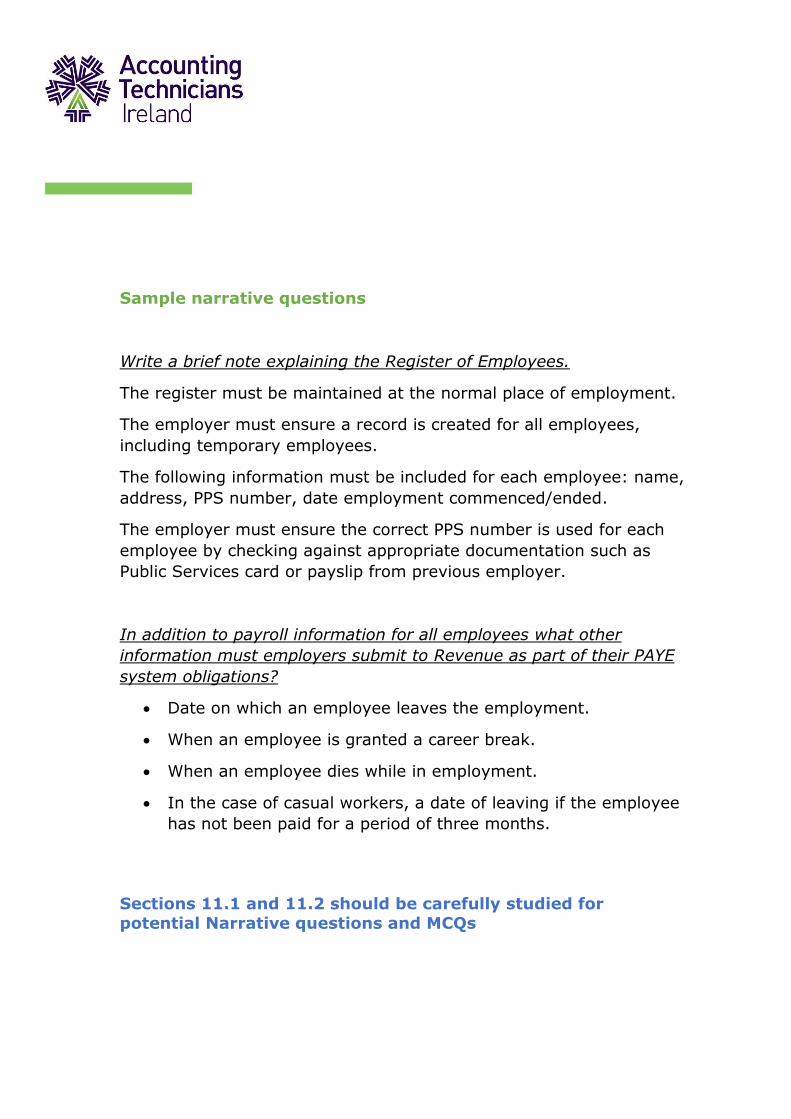

Write a brief note explaining the Register of Employees.

The register must be maintained at the normal place of employment.

The employer must ensure a record is created for all employees,

including temporary employees.

The following information must be included for each employee: name,

address, PPS number, date employment commenced/ended.

The employer must ensure the correct PPS number is used for each

employee by checking against appropriate documentation such as

Public Services card or payslip from previous employer.

In addition to payroll information for all employees what other

information must employers submit to Revenue as part of their PAYE

system obligations?

• Date on which an employee leaves the employment.

• When an employee is granted a career break.

• When an employee dies while in employment.

• In the case of casual workers, a date of leaving if the employee

has not been paid for a period of three months.

Sections 11.1 and 11.2 should be carefully studied for

potential Narrative questions and MCQs

PRSI

Employer PRSI

Class A threshold for the higher rate of employer PRSI is €386

Class A Employee PRSI

The Class A employee PRSI rate is 4%.

For gross earnings between €352.01 and €424, the amount of the PRSI

charge at 4% is reduced by a tapered weekly PRSI Credit.

The maximum weekly PRSI Credit of €12.00 applies at gross weekly

earnings of €352.01.

For gross weekly earnings over €352.01, the maximum weekly PRSI Credit

of €12.00 is reduced by one-sixth of weekly earnings in excess of €352.01.

There is no PRSI Credit once gross weekly earnings exceed €424.

Calculation of PRSI credit

The calculation of the PRSI charge for Class A with gross weekly earnings between

€352.01 and €424, involves 3 separate calculations: The following example shows

how to calculate the PRSI Credit for gross weekly earnings of €377.

1. Calculate the PRSI Credit:

Maximum PRSI Credit €12.00

One-sixth of earnings in excess of €352.01

(377.00 – 352.01 = 24.99 / 6) (€ 4.17)

Reduced PRSI Credit € 7.83

2. Calculate the PRSI charge @ 4% €15.08

3. Deduct the Reduced PRSI Credit from the 4% PRSI Charge

Weekly PRSI Charge € 7.25

PRSI for self-employed

Self-employed people, other than self-employed company directors, must register

with the Revenue Commissioners for PRSI purposes. Under the self- assessment

system, PRSI is paid to the local tax office together with any other payment due.

Self-employed company directors pay their PRSI under the PAYE system.

Minimum/Flat rate Self-employed Payments:

Self-employed contributors with annual self-employed income over €5,000 pay

Class S PRSI at the rate of 4%, subject to a minimum payment of €500.

The flat rate of payment of Voluntary Contributions made by a former self-

employed contributor is €500.

USC

1. Taxpayers are always liable to USC on a single assessment basis.

2. USC is normally taxed on a cumulative basis but using wk1/mth1 will work in most situations.

3. If emergency basis use 8% rate.

4. Main exemptions:

Social welfare payments: Exempt BIK: DIRT: Rent a Room/Childcare services relief.

5. No marginal relief, once taxpayer exceeds €13,000 USC is calculated on all chargeable income.

6. Exceptions to basic rates and thresholds:

Aged ≥ 70, income ‹ €60,000:

Aged ‹ 70, income ‹ €60,000 + full medical card All income above €12,012 is taxed @ 2% rate

Self-employed exceeding €100,000 » 3% surcharge

7. DIRT is assumed to include USC liability

8. In general, all Dept. of Social Protection payments including some that are subject to Income Tax are exempt from USC.

9. There are no specific credits or reliefs allowed against USC

10.Outside of anything above, USC tends to follow Income Tax. BIK

Rent a Room relief, TaxSaver commuter tickets Statutory redundancy Covenants

Maintenance payments

Taxation exam

Avoid last-minute revision.

Time allocation, each mark = 1½minutes » full question = 30 mins.

Allow time at start and end, 10 – 15 mins.

Expect a nasty surprise somewhere in the paper – it’ll only be a few

marks

Start: Read all questions

o Decide order

o Start with easiest to answer eg TAP (low hanging fruit)

o Underline/highlight

Theory question(s)

o Read carefully

o Allocate time

o Explain or define

o Any amounts?

o Use sentences

o Leave spaces

o TRM?

MCQs: Answer all/tick only one answer

All questions

o Attempt 5

o Good layout

o Space

o TRM

End: review if possible, especially MCQ & TAP

Questions for Zoom Webinar

Q1 Calculate the total PRSI liability for each of the following in the pay period quoted and specify the PRSI class applicable. Monthly pay infers a

calendar month.

I. Weekly pay €300

II. Monthly pay €1,540

III. Monthly pay €2,080

IV. Weekly pay €400

Q2 Edna Noonan joined the company on 1 December 2019 and received a monthly salary of €1,560 for December. At 31 December you had not received an RPN notification and Edna has failed to provide you with a PPS

number. This is Edna’s first employment.

Calculate all statutory amounts payable to Revenue in respect of Edna for 2019.

Q3 Joanne was provided with a company car on 1 September 2019. The cost of the car was €30,000 and Joanne agreed to directly purchase €80 of

petrol each month to cover private travel. During the period to 31 December 2019 she travelled 16,200k, 25% of which was agreed as private

motoring.

Calculate Joanne’s BIK for 2019

Payroll Questions Question 1 You have been asked to calculate the take home pay of the following two

employees of SW Ltd.

Alison Cross

Alison commenced employment with the company on Monday 16th December 2019

(week 51 of the tax year). Details from her previous employment shows the

following:

Date of leaving 18 November 2019

Week number 46

Gross pay €36,000

Tax deducted €5,208

Weekly cut-off point €630

Weekly tax credit €60

Details of her pay from SW Ltd. are:

Week 51 Week 52

Gross pay 820 340

Alison did not receive any income between 18 November and 19 December, an RPN

notification received by SW Ltd on 18 December showed the same tax credits and

srcop as above.

Barry Parker

Barry is a director of the company. Details regarding his income and deductions are

as follows:

Salary: €83,200 per annum paid weekly.

Payment for business expense based on receipts supplied (week 52) - €550

Allowance to cover purchase of drinks for staff at Christmas party (week 51) -

€500. The company pays all expenses through the payroll system

In addition to the above Barry has an interest free loan from the company since 1st

January 2011 amounting to €18,000. The money was used by Barry to finance the

purchase of a new boat.

Barry’s weekly tax credit is €100, and his weekly cut off point is €800. Tax is

calculated on cumulative basis and after week 50 tax paid to date was €19,400.

PRSI Class S applies to Barry.

Requirement

Calculate both Alison’s and Barry’s take-home pay for weeks 51 & 52.

You should calculate USC on a week1/month1 basis for the weeks involved.

Question 2

You have been asked to manage the payroll of SWIS Ltd (Employer registration no.

1357924J). Details regarding two of the employees are as follows.

Kevin Press PPS no. 1236549R

Kevin commenced employment with SWIS Ltd on 16th December 2019 (week 51 of

the tax year).

RPN supplied by Revenue shows the following details:

Date of leaving 15 Nov 2019

Week number 46

Gross pay €36,000

Tax deducted €4,919

Total PRSI €5,310

Employee PRSI €1,440

Weekly tax cut-off point €630.77

Weekly tax credit €63.46

USC deducted €1,099.97

USC was deducted by his previous employer using the standard thresholds

Both PAYE and USC were deducted on a cumulative basis.

The RPN from Revenue indicated that week1/month1 basis applies.

Details of Kevin’s pay and deductions for weeks 51 and 52 are as follows:

Week 51 Week 52

Week 51 € €

Gross pay 340 520

Contribution to pension scheme 40 40

Contribution to Christmas party 50

Davina Hirst

Davina has been employed by SWIS Ltd for many years. She is paid €340 gross per

week and contributes €20 per week to an approved pension scheme. Her annual

tax credits for 2019 are €3,300 and her annual standard rate cut-off point is

€33,800.

Requirement:

Calculate net take home pay for weeks 51 and 52 for Kevin & Davina.