Embed Size (px)

Citation preview

Taxation of Foreign Trusts and Related TopicsBy: Edward D. Brown, Esq.

Engel & Reiman pc

Copyright 2011Engel & Reiman pcAll rights reserved

• What is (and what is not) a Foreign Trust?

– Offshore vs. Foreign• For Income Tax Purposes• Offshore does not mean

foreign necessarily– A foreign trust with any US

beneficiaries created by a US person is a grantor trust

• Therefore, all trust income is taxable directly to the grantor/settlor

• Some may be of the misimpression that a grantor trust with a US grantor must be a domestic trust Copyright 2011

Engel & Reiman pcAll rights reserved

A Misperception

• A misperception with foreign trusts is that some advisors think that if a trust has a FEIN, that fact alone makes the trust domestic.

– When a Taxpayer ID# is applied for with respect to a trust, even though the SS-4 application for that trust shows a foreign address and an obviously foreign name for the trustee, the IRS issues the FEIN with a letter that says: here it is and we look forward to your Form 1041 next year.

• What a trap. By the time the 1041 would be due, the 3520-A is already a month late.

• What is a Foreign Trust?

– Code Section 7701(a)(31) defines a foreign trust

– Court and Control Tests –Code Section 7701(a)(30)

Copyright 2011Engel & Reiman pcAll rights reserved

Is the Trust

“Domestic”?

Court Test: Any US court is able to exercise primary supervision over the administration of the trust

*Concurrent jurisdiction OK

http://www.engelreiman.com

Is the Trust

“Domestic”?

Control Test: A US person must have the authority to control all substantial decisions of the trust

http://www.engelreiman.com

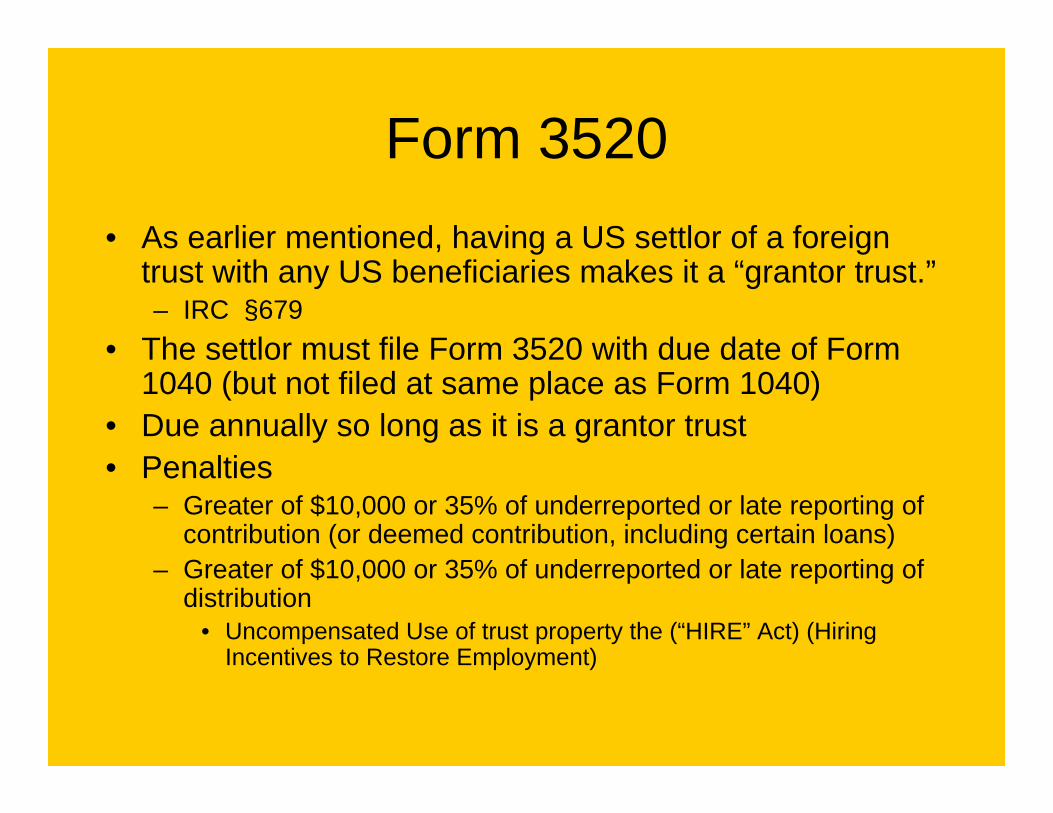

Form 3520• As earlier mentioned, having a US settlor of a foreign

trust with any US beneficiaries makes it a “grantor trust.”– IRC §679

• The settlor must file Form 3520 with due date of Form 1040 (but not filed at same place as Form 1040)

• Due annually so long as it is a grantor trust• Penalties

– Greater of $10,000 or 35% of underreported or late reporting of contribution (or deemed contribution, including certain loans)

– Greater of $10,000 or 35% of underreported or late reporting of distribution

• Uncompensated Use of trust property the (“HIRE” Act) (Hiring Incentives to Restore Employment)

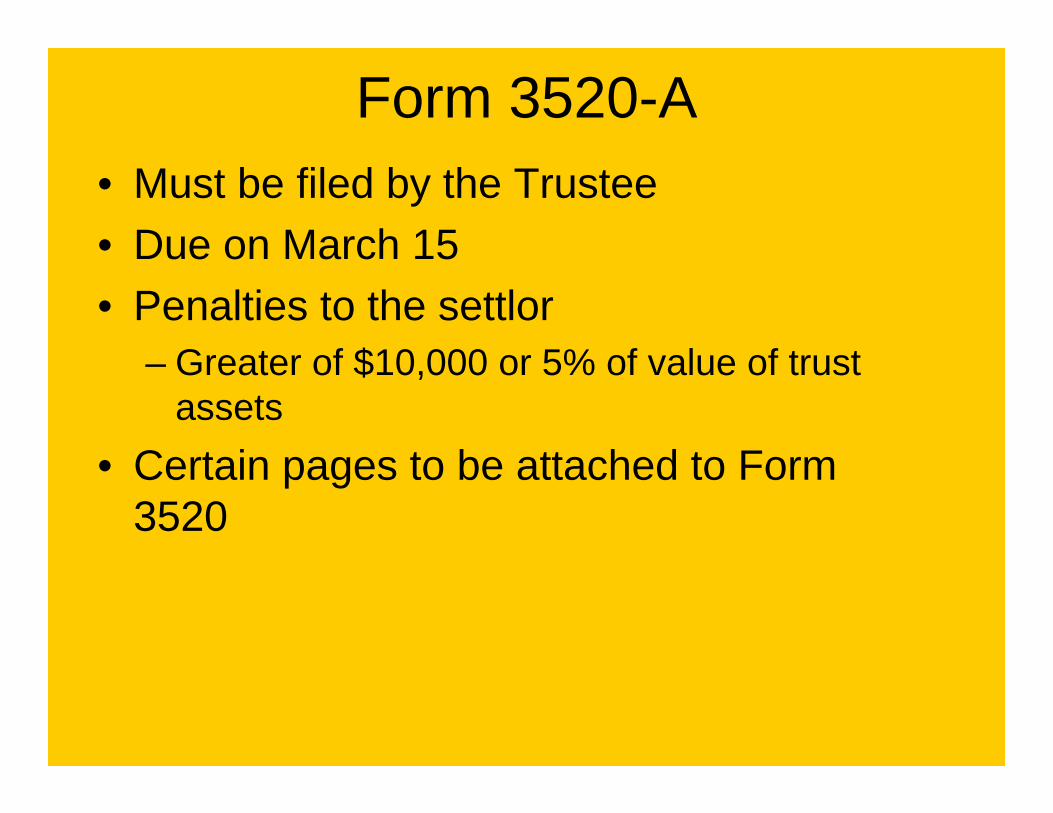

Form 3520-A• Must be filed by the Trustee• Due on March 15• Penalties to the settlor

– Greater of $10,000 or 5% of value of trust assets

• Certain pages to be attached to Form 3520

• Appointment of US Agent recommended– So IRS has someone to accept service of

process, etc.

• Not required, but if no US agent appointed in writing, more voluminous filing requirement

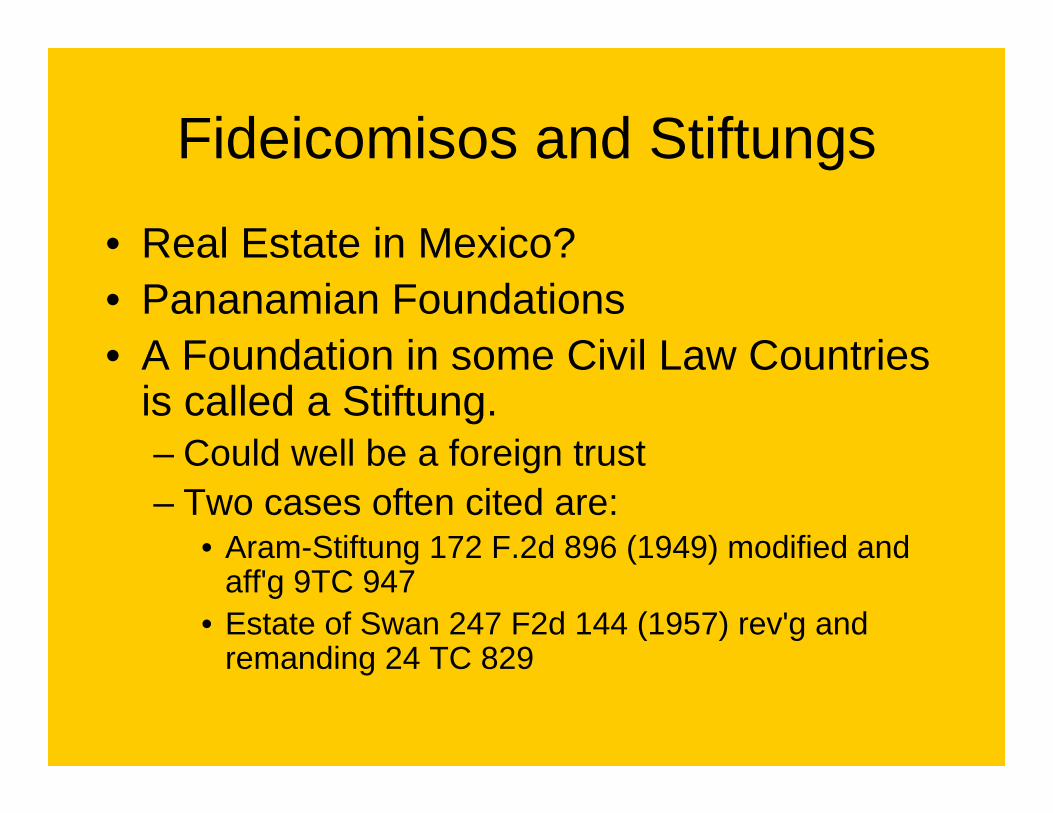

Fideicomisos and Stiftungs

• Real Estate in Mexico?• Pananamian Foundations• A Foundation in some Civil Law Countries

is called a Stiftung.– Could well be a foreign trust– Two cases often cited are:

• Aram-Stiftung 172 F.2d 896 (1949) modified and aff'g 9TC 947

• Estate of Swan 247 F2d 144 (1957) rev'g and remanding 24 TC 829

History Lesson

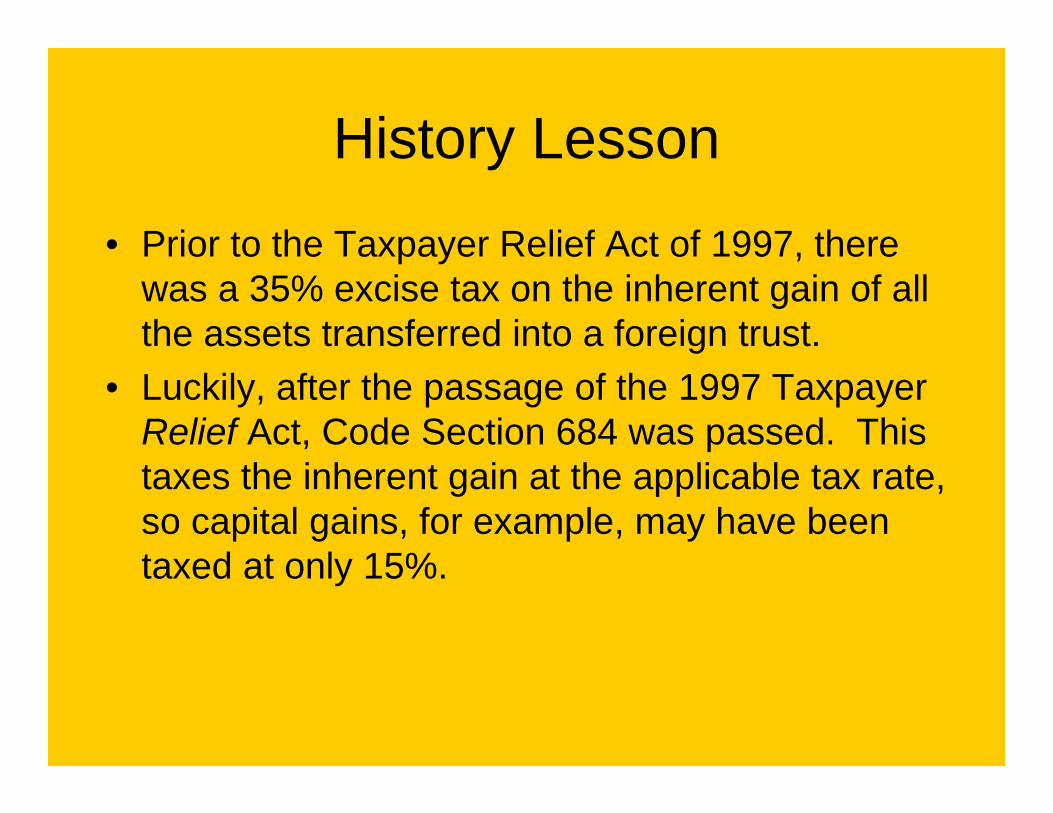

• Prior to the Taxpayer Relief Act of 1997, there was a 35% excise tax on the inherent gain of all the assets transferred into a foreign trust.

• Luckily, after the passage of the 1997 Taxpayer Relief Act, Code Section 684 was passed. This taxes the inherent gain at the applicable tax rate, so capital gains, for example, may have been taxed at only 15%.

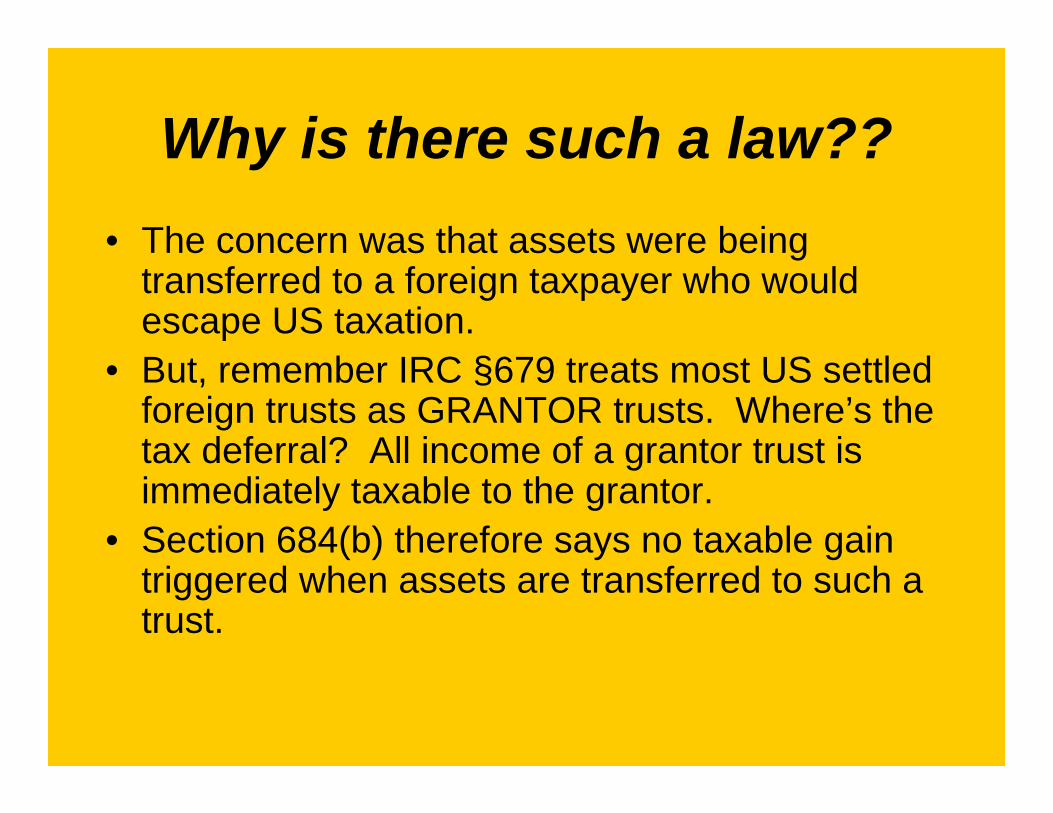

Why is there such a law??• The concern was that assets were being

transferred to a foreign taxpayer who would escape US taxation.

• But, remember IRC §679 treats most US settled foreign trusts as GRANTOR trusts. Where’s the tax deferral? All income of a grantor trust is immediately taxable to the grantor.

• Section 684(b) therefore says no taxable gain triggered when assets are transferred to such a trust.

So, can we just ignore §684 now??

• Well, what happens if the grantor dies. If the trust is then foreign, you have a foreign trust that can no longer be a grantor trust.

• §684 was a bit unclear as to whether a §684 tax was then triggered.

• Final Regulations in 2001 provided that so long as the trust assets were subject to Code §1014(a) (the basis step up rules), no tax is triggered.

• Most trusts of the asset protection variety are included in the grantor’s taxable estate.– But consider whether it is a completed gift trust

So, is that the end of the story on §684??

• Not really. Some assets included in the grantor’s estate may be IRD. This includes items that were taxable income to the grantor, but because of the timing of his death, the income is not recognized until post death.

• For example, accrued interest while alive, paid after death; dividends declared while alive, paid after death.

Last year, 2010, there was one other item to think about.

• Assets other than IRD might also not get a step up in basis since we were in the year of the “carryover basis” rules (if so elected). Therefore, if a client died last year with a foreign trust, there could be additional §684 taxes (if carryover basis elected).

Is the foreign trust taxed after the grantor’s death.

• If no US trade or business or US source income, no US tax

Children’s visions of a perpetual tax free source of income

• Quickly squelched

• Any distributions will be taxable to the children when they receive the funds. See Form 4970. Not only that, but they also will have to pay a non-deductible interest charge for the privilege of gaining tax deferral while the income remained in the trust.

• If that isn’t enough to burst their bubble, any capital gains that occurred in prior years will be treated as ordinary income in the year distributed.

Withholding Taxes

• See Outline for details (pages 9 – 12)• In general:

– US person pays US income to foreign person– Beginning in 2013, certain non-compliant

foreign entities will be subject to a 30% withholding on US income payable to them.

• Even portfolio interest income, which would otherwise be exempt from US taxation.

Form 709

• Even if an “incomplete gift”???

http://www.engelreiman.com

-Foreign Account?

-Form TD F 90-22.1

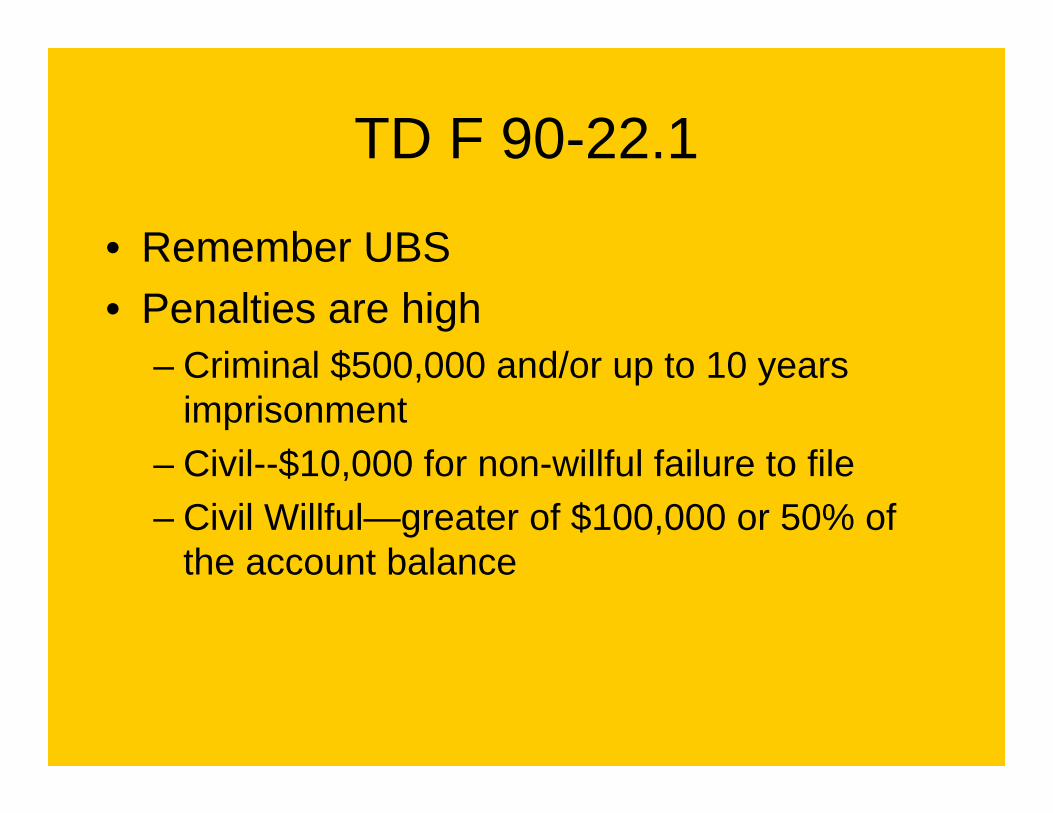

TD F 90-22.1

• Remember UBS• Penalties are high

– Criminal $500,000 and/or up to 10 years imprisonment

– Civil--$10,000 for non-willful failure to file– Civil Willful—greater of $100,000 or 50% of

the account balance

TD F 90-22.1Who Must File?

• Financial Interest; or

• Signature Authority

• Form 1040 Schedule B– Deemed intentional omission?

• Anyone else?

More of the “F” Word FormTD F 90-22.1

• TD F 90-22.1 (better known as the F-B-A-R)• What is a ‘willful” failure to file?

– Careless disregard not enough– Willful blindness per public access to IRM

provisions• “a conscious effort to avoid learning about the FBAR

reporting and record–keeping requirements.”

More of that four-letter word (FBAR) Form

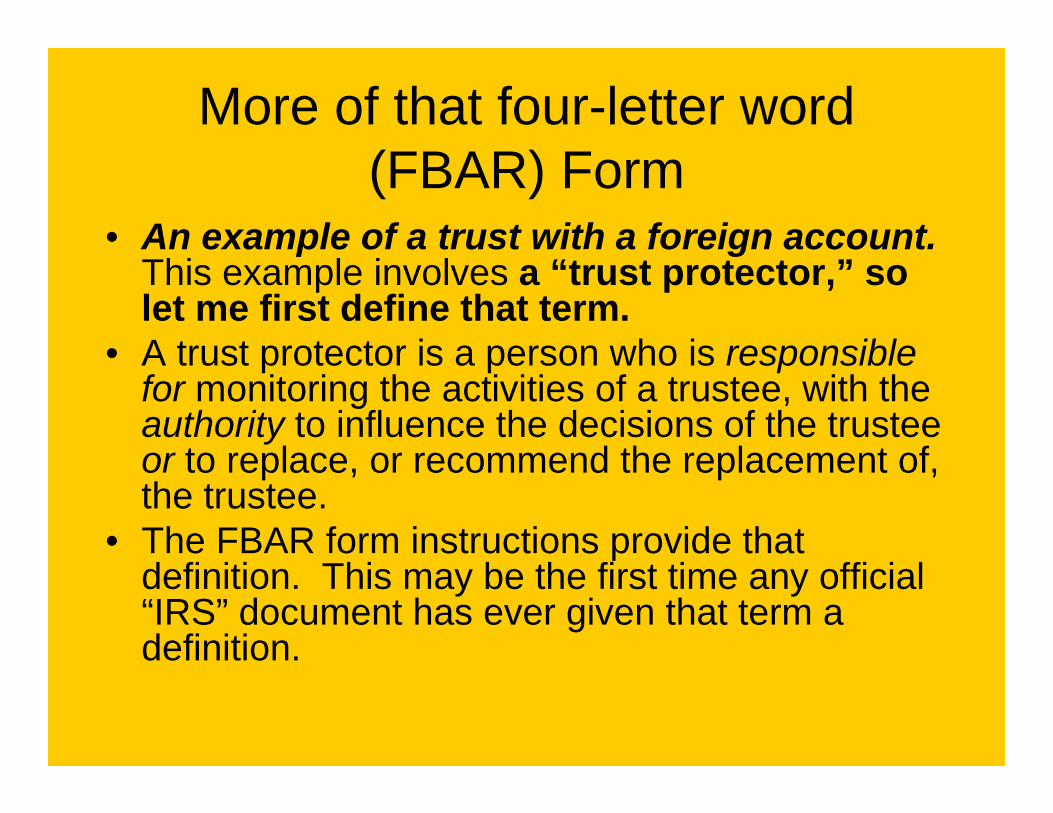

• An example of a trust with a foreign account. This example involves a “trust protector,” so let me first define that term.

• A trust protector is a person who is responsible for monitoring the activities of a trustee, with the authority to influence the decisions of the trustee or to replace, or recommend the replacement of, the trustee.

• The FBAR form instructions provide that definition. This may be the first time any official “IRS” document has ever given that term a definition.

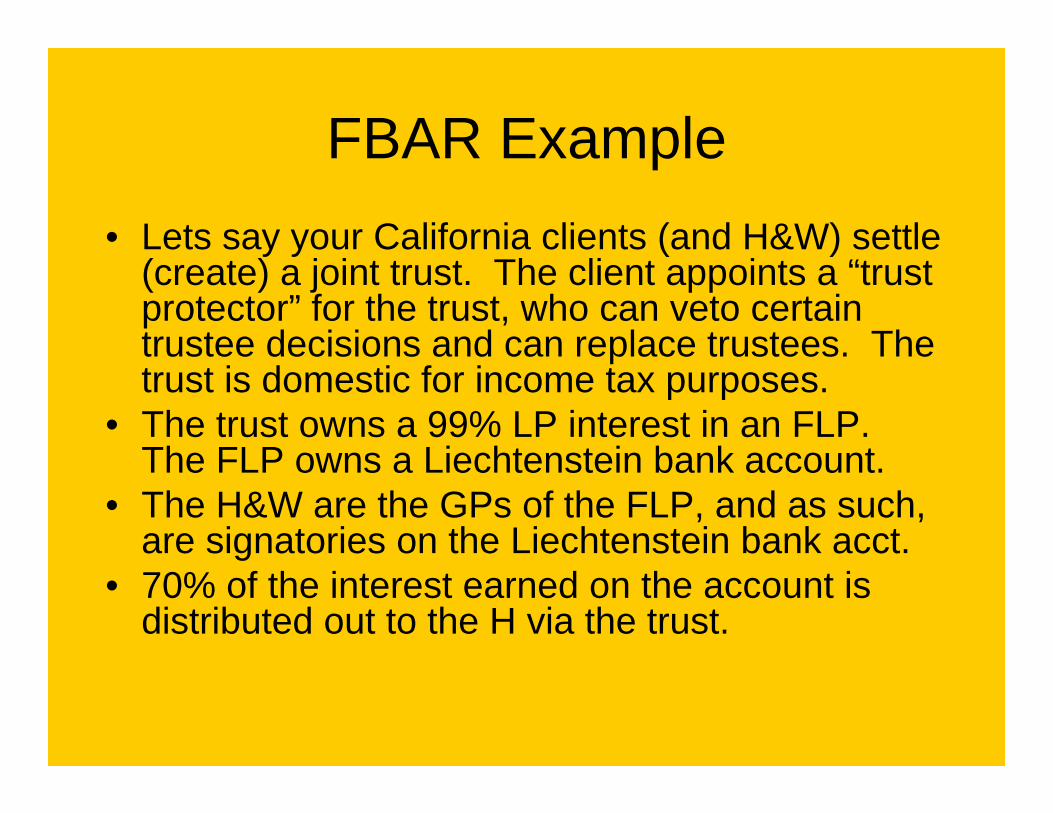

FBAR Example• Lets say your California clients (and H&W) settle

(create) a joint trust. The client appoints a “trust protector” for the trust, who can veto certain trustee decisions and can replace trustees. The trust is domestic for income tax purposes.

• The trust owns a 99% LP interest in an FLP. The FLP owns a Liechtenstein bank account.

• The H&W are the GPs of the FLP, and as such, are signatories on the Liechtenstein bank acct.

• 70% of the interest earned on the account is distributed out to the H via the trust.

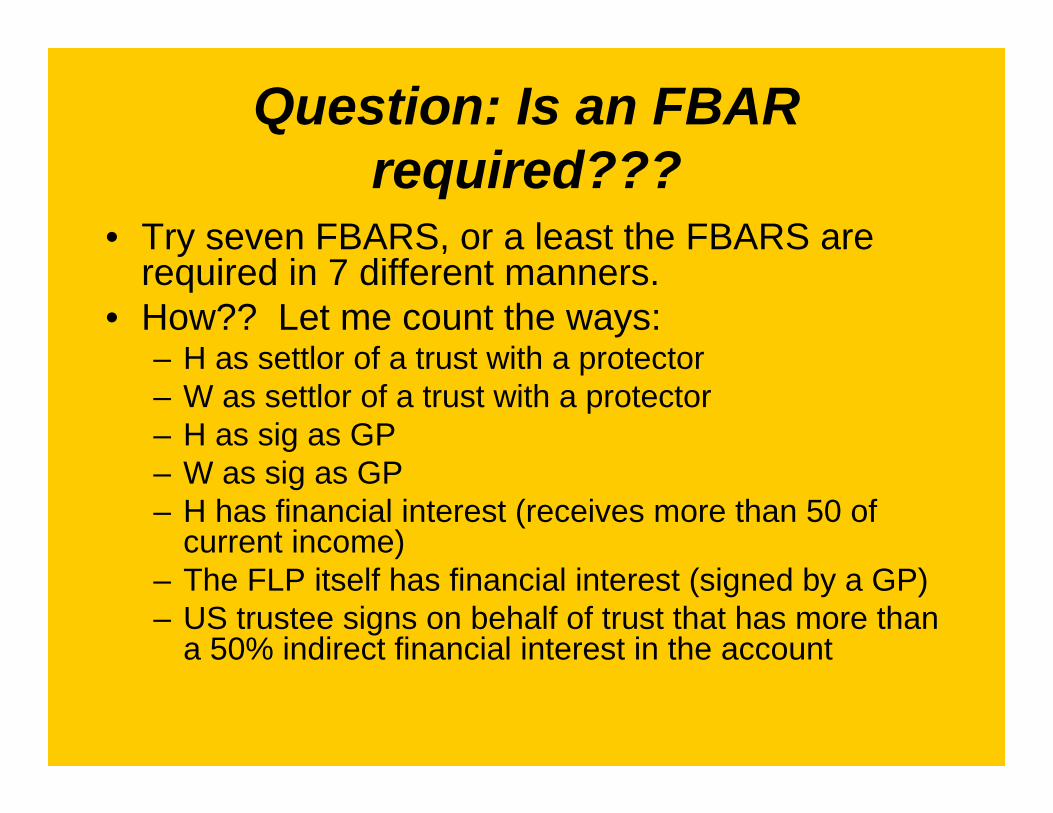

Question: Is an FBAR required???

• Try seven FBARS, or a least the FBARS are required in 7 different manners.

• How?? Let me count the ways:– H as settlor of a trust with a protector– W as settlor of a trust with a protector– H as sig as GP– W as sig as GP– H has financial interest (receives more than 50 of

current income)– The FLP itself has financial interest (signed by a GP)– US trustee signs on behalf of trust that has more than

a 50% indirect financial interest in the account

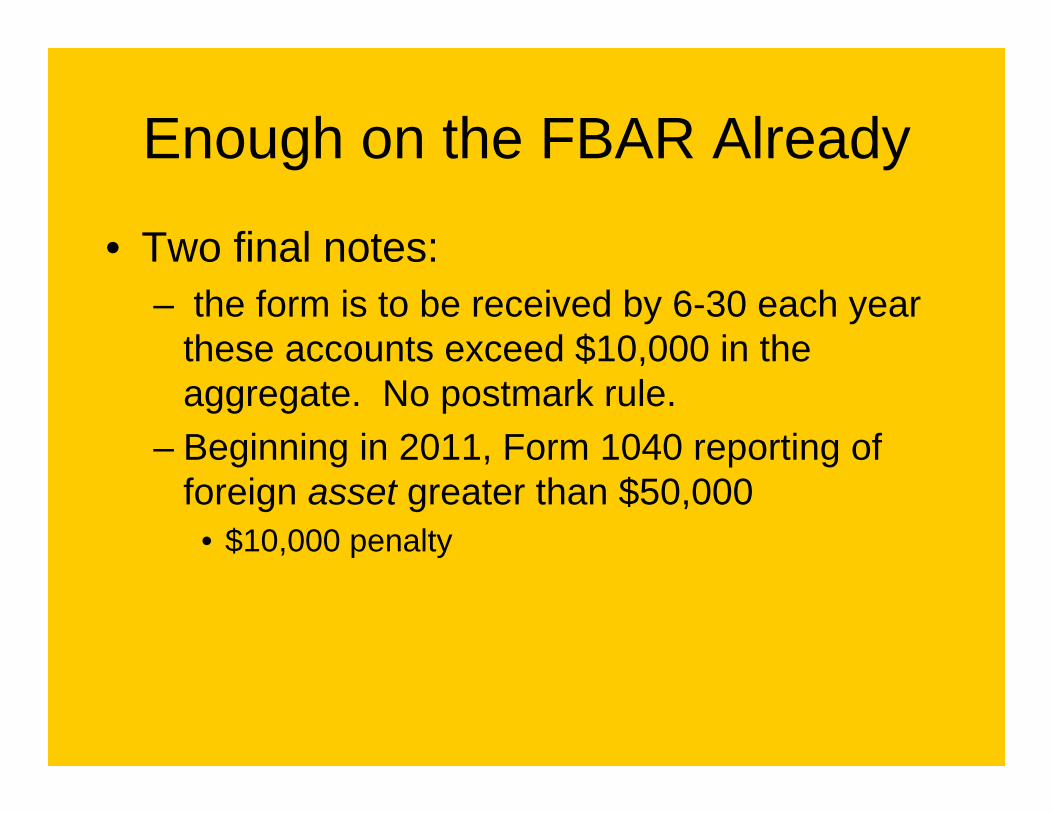

Enough on the FBAR Already

• Two final notes:– the form is to be received by 6-30 each year

these accounts exceed $10,000 in the aggregate. No postmark rule.

– Beginning in 2011, Form 1040 reporting of foreign asset greater than $50,000

• $10,000 penalty

http://www.engelreiman.com

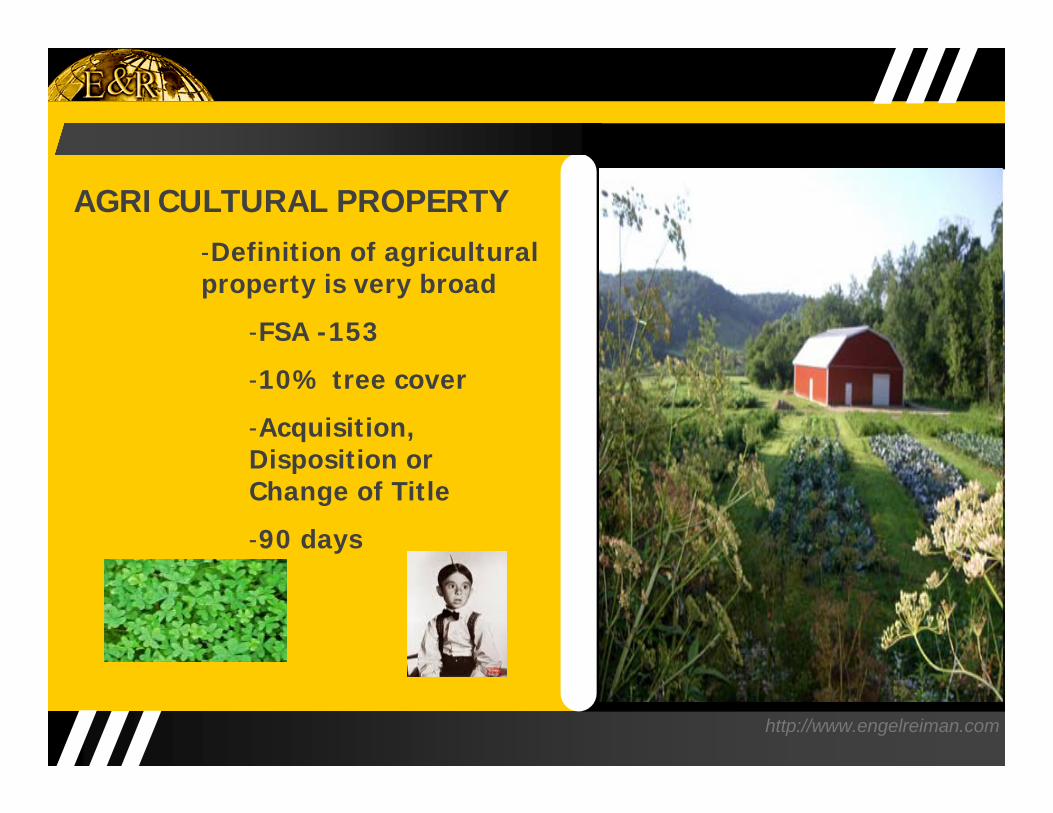

AGRICULTURAL PROPERTY -Definition of agricultural property is very broad

-FSA -153

-10% tree cover

-Acquisition, Disposition or Change of Title

-90 days

FSA-153

• Penalties can be as high as 25% of the value of the property

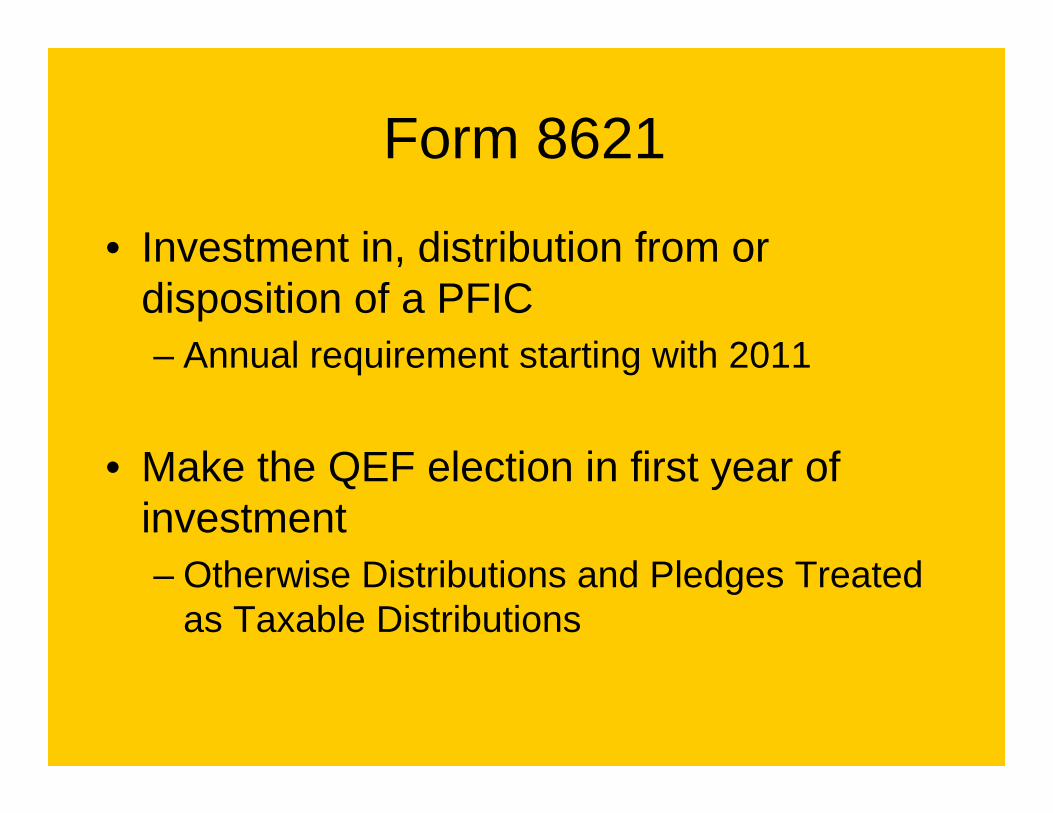

Form 8621

• Investment in, distribution from or disposition of a PFIC– Annual requirement starting with 2011

• Make the QEF election in first year of investment– Otherwise Distributions and Pledges Treated

as Taxable Distributions

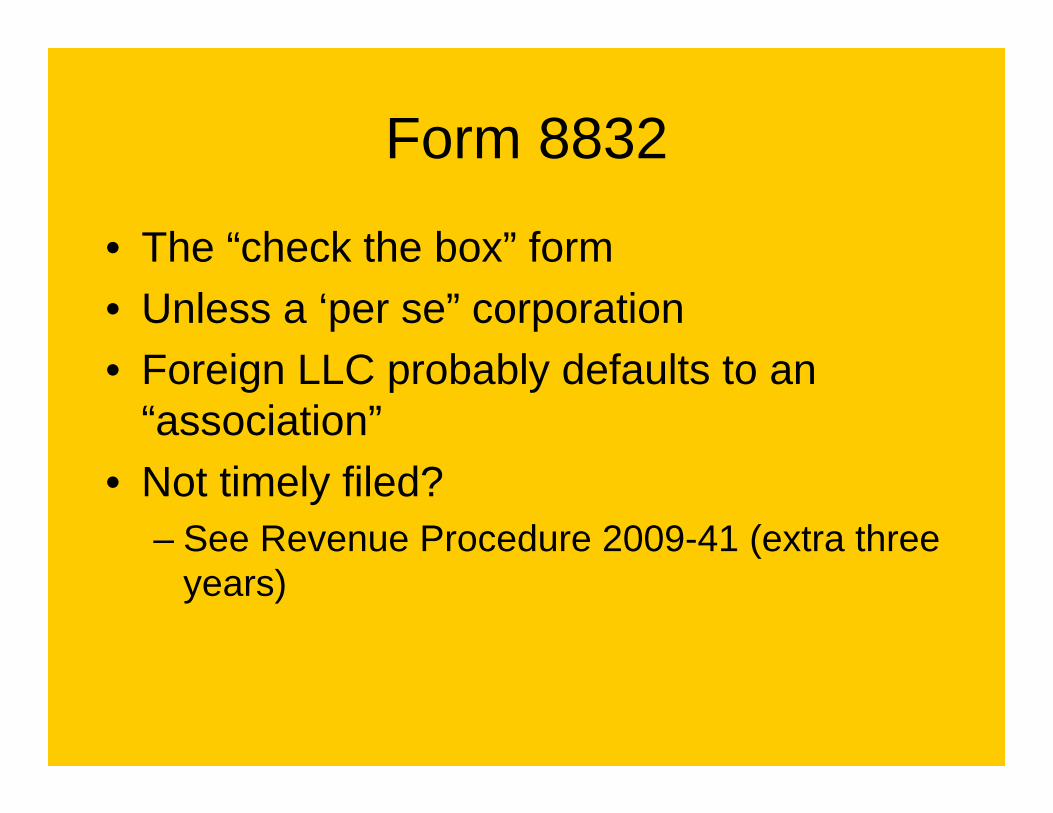

Form 8832

• The “check the box” form• Unless a ‘per se” corporation• Foreign LLC probably defaults to an

“association”• Not timely filed?

– See Revenue Procedure 2009-41 (extra three years)

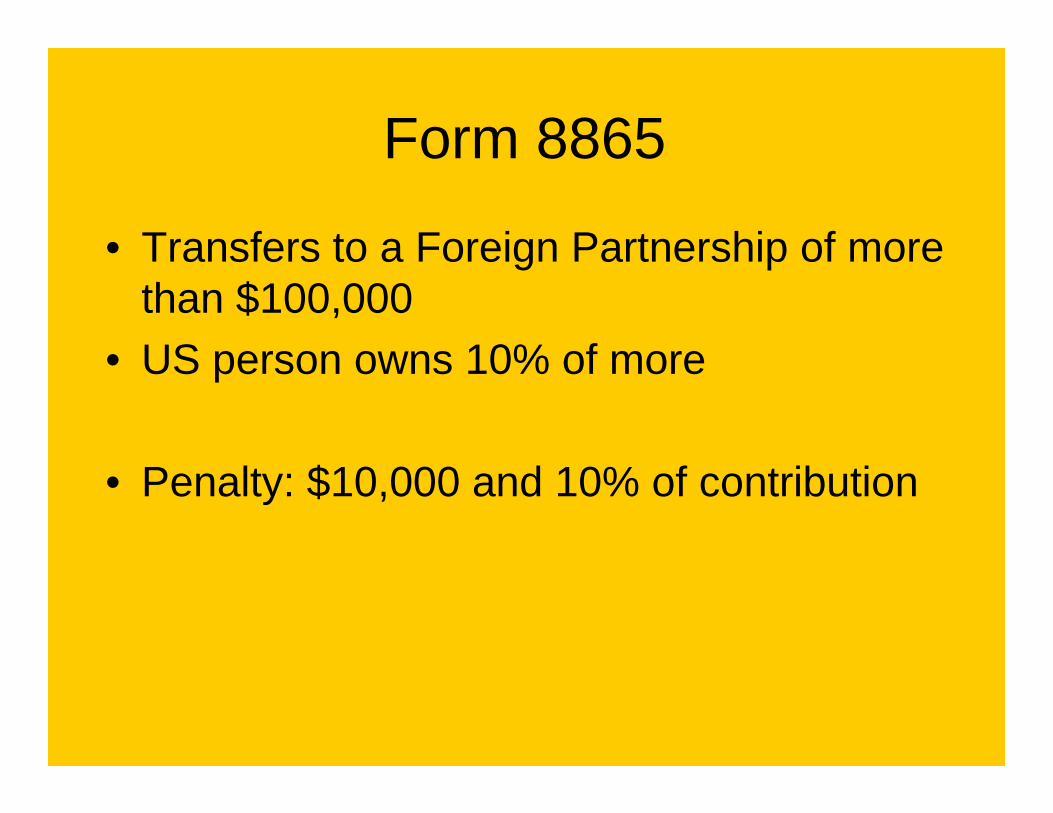

Form 8865

• Transfers to a Foreign Partnership of more than $100,000

• US person owns 10% of more

• Penalty: $10,000 and 10% of contribution

Form 8858

• Single member foreign “disregarded entity”owned by a US person– Penalty $10,000

Other Forms (Details in outline)

• Form 926-Transfers to a foreign corporation– Penalty 10% of value of transfer

• Form 5471-Shareholder, officer or director of a foreign corporation– Penalty $10,000

Forms 1042 and 1042-S (withholding forms)Forms W-9, W-8 IMY, W-8 BEN

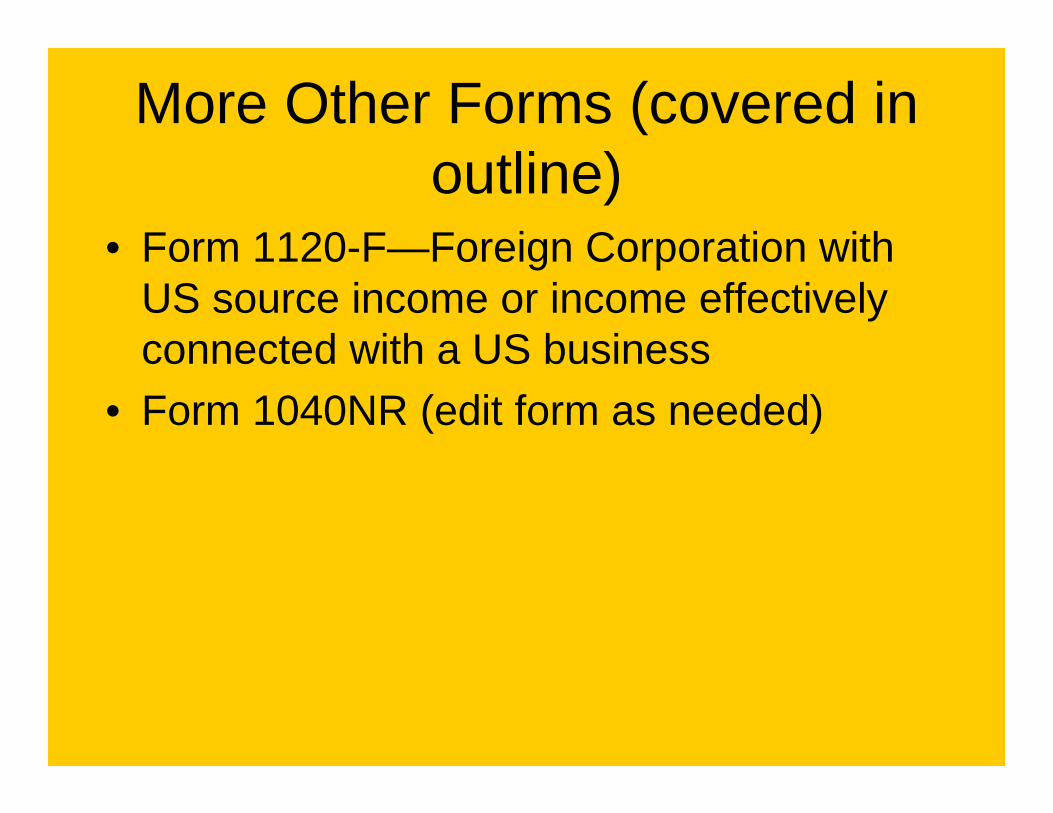

More Other Forms (covered in outline)

• Form 1120-F—Foreign Corporation with US source income or income effectively connected with a US business

• Form 1040NR (edit form as needed)

Other Honorable Mentions(see page 18 of outline)

• Form 56

• FinCen Forms 104 and 105

• Form 5472

• Form 8300

Voluntary Compliance Program (#2)

• Must complete before August 31, 2011• IRS promises no criminal charges• Available to those who did not report all

the related income

What will IRS do?• Assess back-taxes and interest• Assess accuracy and/or delinquency

penalties (IRC §6662)• 25% penalty on the highest balance

between 2003 and 2010 (in lieu of all other penalties, such as the aforementioned $10,000 and $100,000 penalties and the 75% fraud penalty [§§6651(f) and 6663], not to mention criminal prosecution)

Failed to File, But Paid All Taxes

• These taxpayers also have until August 31 to file delinquent returns (not as part of the Voluntary Compliance Program).– Penalty free

• If so, use current forms (Oct 2008)• But for 2010, FBARs still due by June 30,

2011

Advisors:* Be sure representations to Treasury are

accurate*If taxpayer decides not to comply, must advise of

potential consequences*Can not prepare any more tax returns for that

client

Need Guidance?

• IRS Hotline 1-800-800-2877, or• Email to [email protected]

• IRS website has fairly comprehensive Q&A– “2011 Offshore Voluntary Disclosure Initiative

Frequently Asked Questions and Answers”