Embed Size (px)

Citation preview

Tax Services Provided to Audit Clients:PCAOB view and the report of the IFAC

Tax Services Review Group

Tax Services Provided to Audit Clients:PCAOB view and the report of the IFAC

Tax Services Review Group

IFAC SMP Permanent Task ForceMarch 8, 2005

Prague

IFAC SMP Permanent Task ForceMarch 8, 2005

Prague

presented bypresented byDr. Helmut Klaas, IDW, Dr. Helmut Klaas, IDW,

GermanyGermany

2

StructureStructure

I. Background of the topic

II. The PCAOB rulemaking docket dated December 14, 2004

III. Reaction of the accounting profession

IV. Main critical areas of the PCAOB rulemaking docket

V. Possible impact on legislations outside the US

VI. IFAC‘s Tax Services Review Group‘s report on tax services and the accounting profession

VII. Conclusions and recommendations

I. Background of the topic

II. The PCAOB rulemaking docket dated December 14, 2004

III. Reaction of the accounting profession

IV. Main critical areas of the PCAOB rulemaking docket

V. Possible impact on legislations outside the US

VI. IFAC‘s Tax Services Review Group‘s report on tax services and the accounting profession

VII. Conclusions and recommendations

3

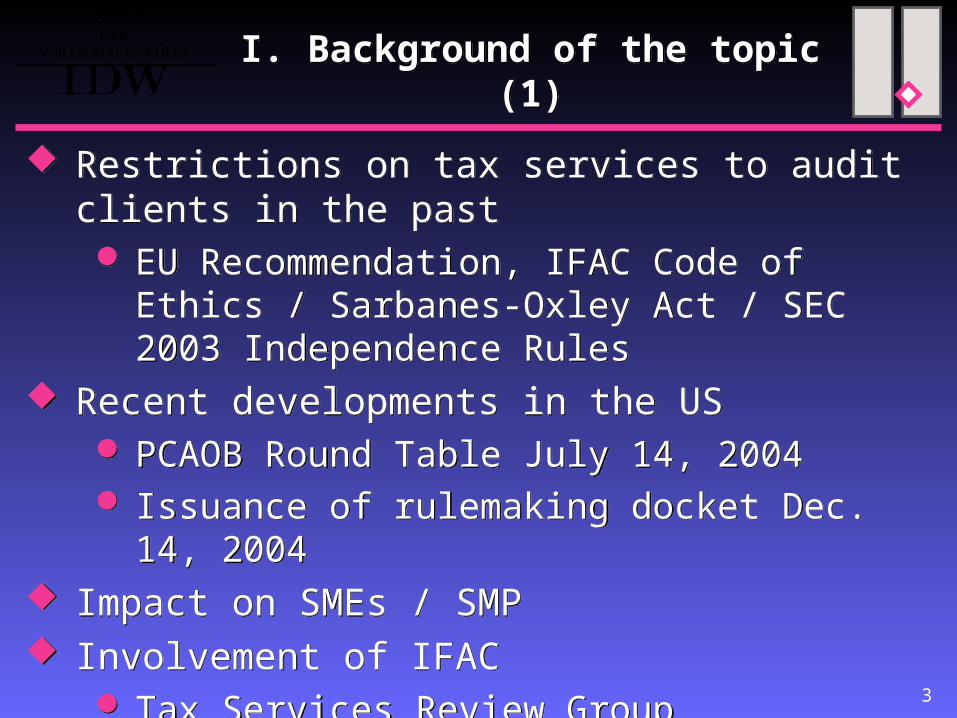

I. Background of the topic (1)I. Background of the topic (1)

Restrictions on tax services to audit clients in the past EU Recommendation, IFAC Code of Ethics /

Sarbanes-Oxley Act / SEC 2003 Independence Rules

Recent developments in the US PCAOB Round Table July 14, 2004 Issuance of rulemaking docket Dec. 14, 2004

Impact on SMEs / SMP Involvement of IFAC

Tax Services Review Group

Restrictions on tax services to audit clients in the past EU Recommendation, IFAC Code of Ethics /

Sarbanes-Oxley Act / SEC 2003 Independence Rules

Recent developments in the US PCAOB Round Table July 14, 2004 Issuance of rulemaking docket Dec. 14, 2004

Impact on SMEs / SMP Involvement of IFAC

Tax Services Review Group

4

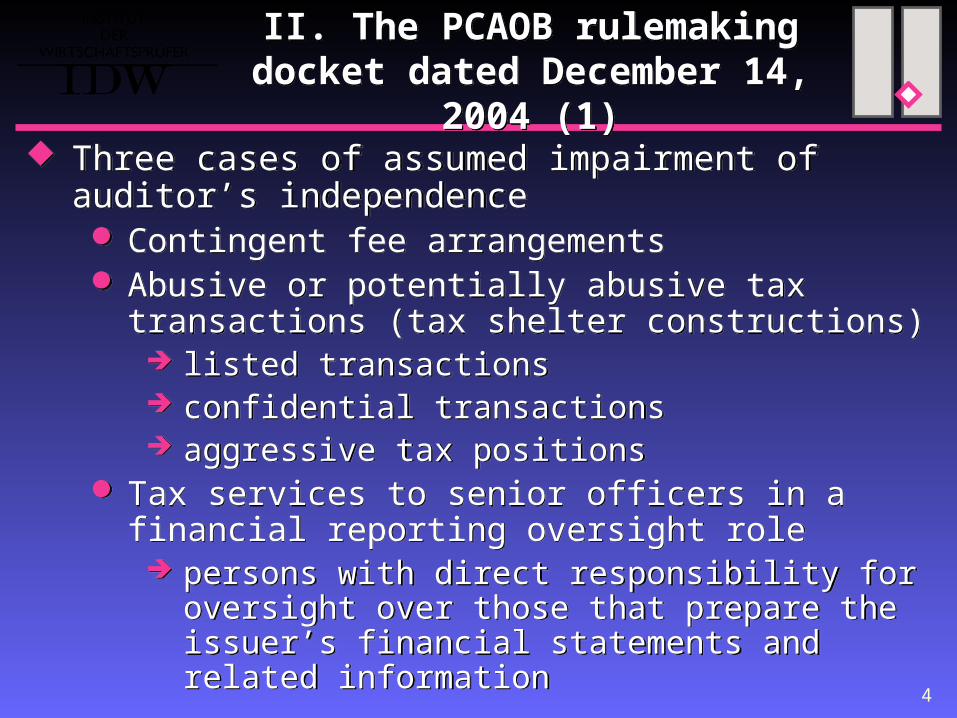

II. The PCAOB rulemaking docket dated December 14, 2004 (1)

II. The PCAOB rulemaking docket dated December 14, 2004 (1)

Three cases of assumed impairment of auditor’s independence Contingent fee arrangements Abusive or potentially abusive tax transactions

(tax shelter constructions) listed transactions confidential transactions aggressive tax positions

Tax services to senior officers in a financial reporting oversight role persons with direct responsibility for oversight

over those that prepare the issuer’s financial statements and related information

Three cases of assumed impairment of auditor’s independence Contingent fee arrangements Abusive or potentially abusive tax transactions

(tax shelter constructions) listed transactions confidential transactions aggressive tax positions

Tax services to senior officers in a financial reporting oversight role persons with direct responsibility for oversight

over those that prepare the issuer’s financial statements and related information

5

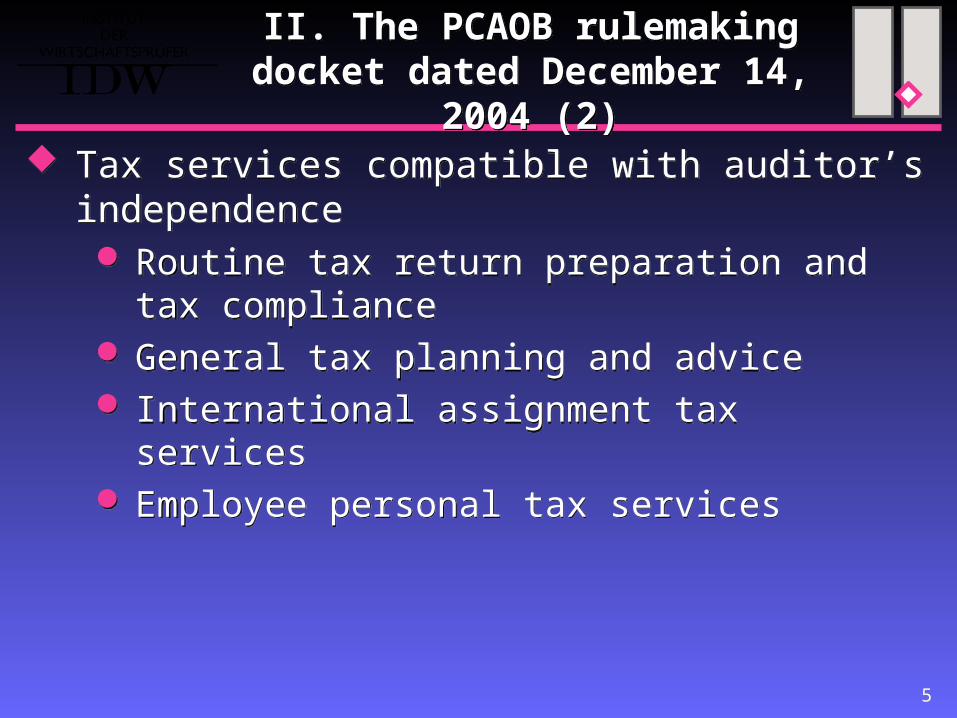

II. The PCAOB rulemaking docket dated December 14, 2004 (2)

II. The PCAOB rulemaking docket dated December 14, 2004 (2)

Tax services compatible with auditor’s independence Routine tax return preparation and tax compliance General tax planning and advice International assignment tax services Employee personal tax services

Tax services compatible with auditor’s independence Routine tax return preparation and tax compliance General tax planning and advice International assignment tax services Employee personal tax services

6

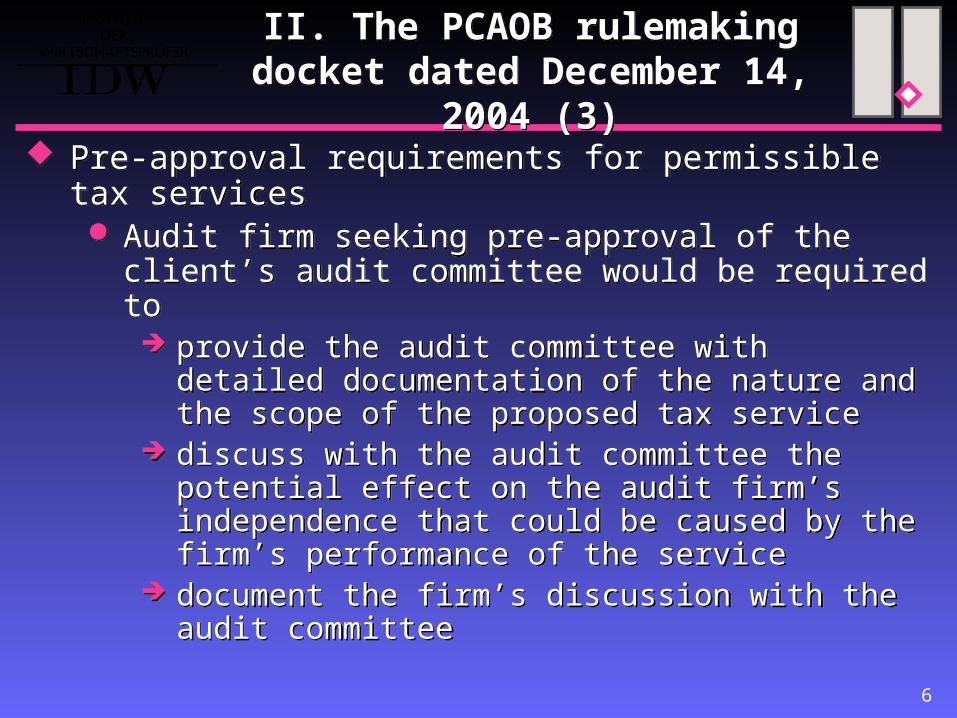

II. The PCAOB rulemaking docket dated December 14, 2004 (3)

II. The PCAOB rulemaking docket dated December 14, 2004 (3)

Pre-approval requirements for permissible tax services Audit firm seeking pre-approval of the client’s

audit committee would be required to provide the audit committee with detailed

documentation of the nature and the scope of the proposed tax service

discuss with the audit committee the potential effect on the audit firm’s independence that could be caused by the firm’s performance of the service

document the firm’s discussion with the audit committee

Pre-approval requirements for permissible tax services Audit firm seeking pre-approval of the client’s

audit committee would be required to provide the audit committee with detailed

documentation of the nature and the scope of the proposed tax service

discuss with the audit committee the potential effect on the audit firm’s independence that could be caused by the firm’s performance of the service

document the firm’s discussion with the audit committee

7

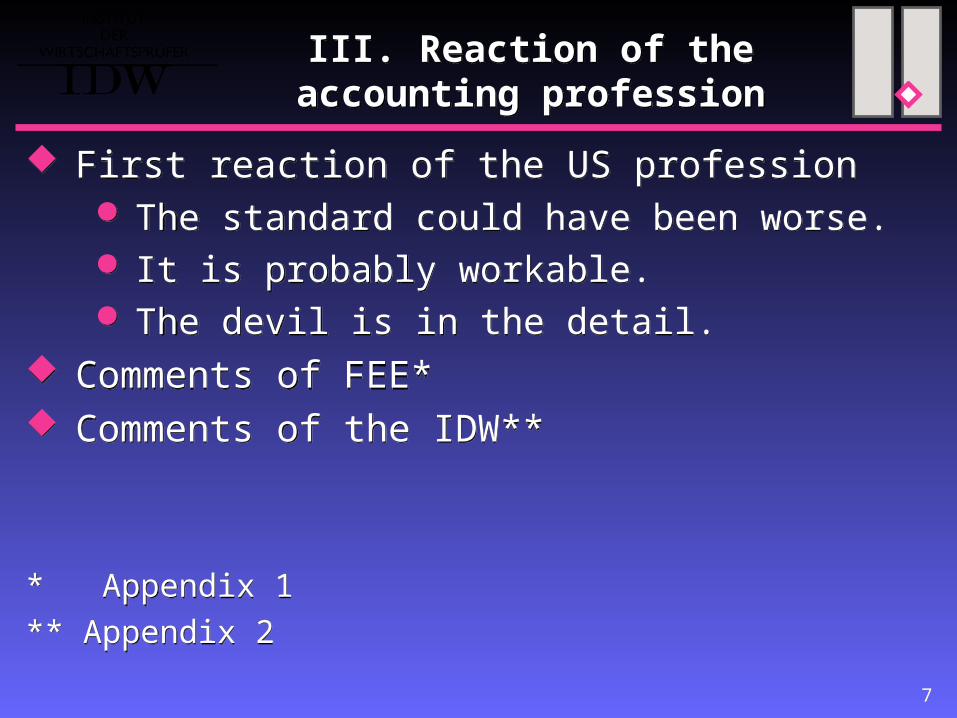

III. Reaction of the accounting profession

III. Reaction of the accounting profession

First reaction of the US profession The standard could have been worse. It is probably workable. The devil is in the detail.

Comments of FEE* Comments of the IDW**

* Appendix 1

** Appendix 2

First reaction of the US profession The standard could have been worse. It is probably workable. The devil is in the detail.

Comments of FEE* Comments of the IDW**

* Appendix 1

** Appendix 2

8

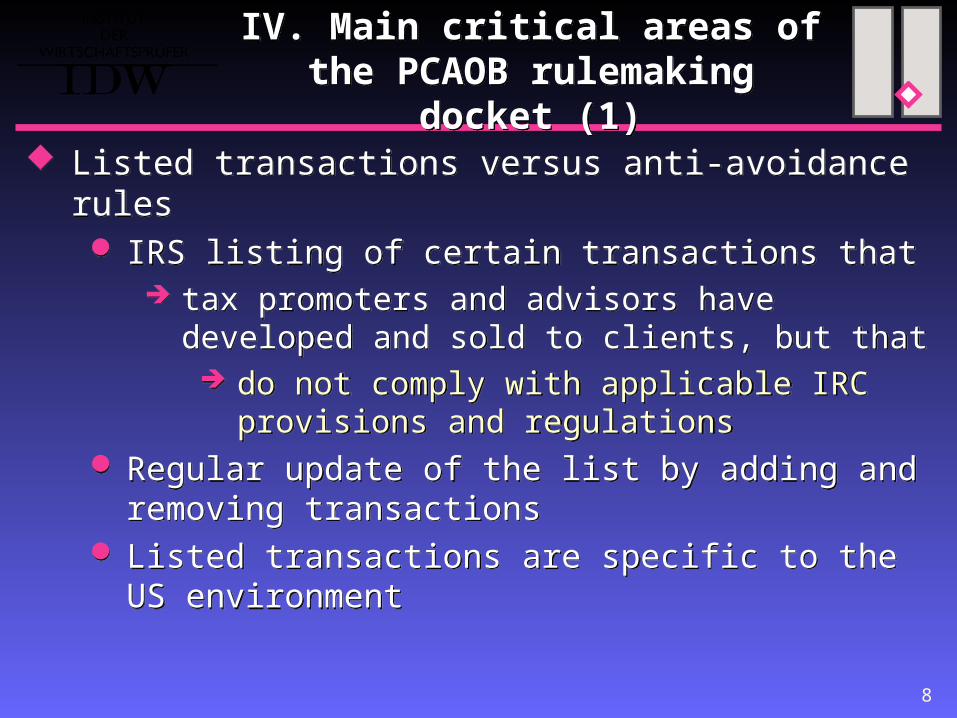

IV. Main critical areas of the PCAOB rulemaking docket (1)IV. Main critical areas of the

PCAOB rulemaking docket (1)

Listed transactions versus anti-avoidance rules IRS listing of certain transactions that

tax promoters and advisors have developed and sold to clients, but that do not comply with applicable IRC

provisions and regulations Regular update of the list by adding and removing

transactions Listed transactions are specific to the US

environment

Listed transactions versus anti-avoidance rules IRS listing of certain transactions that

tax promoters and advisors have developed and sold to clients, but that do not comply with applicable IRC

provisions and regulations Regular update of the list by adding and removing

transactions Listed transactions are specific to the US

environment

9

IV. Main critical areas of the PCAOB rulemaking docket (2)IV. Main critical areas of the

PCAOB rulemaking docket (2)

In the majority of EU Member States instead of listing application of anti-avoidance provisions, e.g. article 42 General Tax Code in Germany

Proposal of FEE restrictions on advice on US listed transactions

to be limited to US transactions and not to be extended to non-US transactions

In the majority of EU Member States instead of listing application of anti-avoidance provisions, e.g. article 42 General Tax Code in Germany

Proposal of FEE restrictions on advice on US listed transactions

to be limited to US transactions and not to be extended to non-US transactions

10

IV. Main critical areas of the PCAOB rulemaking docket (3)IV. Main critical areas of the

PCAOB rulemaking docket (3)

Criteria for aggressive tax positions Second criterion: “a significant purpose of which

is tax avoidance” to be replaced by “sole business purpose of which is tax avoidance” would be in line with the wording of the SEC’s

guidance to audit committees in its 2003 release

would reflect the main purpose of almost any tax advice: to reveal to the client the potential for tax savings

Criteria for aggressive tax positions Second criterion: “a significant purpose of which

is tax avoidance” to be replaced by “sole business purpose of which is tax avoidance” would be in line with the wording of the SEC’s

guidance to audit committees in its 2003 release

would reflect the main purpose of almost any tax advice: to reveal to the client the potential for tax savings

11

IV. Main critical areas of the PCAOB rulemaking docket (4)IV. Main critical areas of the

PCAOB rulemaking docket (4)

Scope of application of the prohibition to provide tax services to senior officers Not sufficiently clear which individuals will be

affected prohibitions not to be applied to those charged

with governance of the audit client

Scope of application of the prohibition to provide tax services to senior officers Not sufficiently clear which individuals will be

affected prohibitions not to be applied to those charged

with governance of the audit client

12

IV. Main critical areas of the PCAOB rulemaking docket (5)IV. Main critical areas of the

PCAOB rulemaking docket (5)

Approach to preclude the auditor in general from providing tax services to an audit client’s management is internationally unique application of the framework approach would be

helpful

Approach to preclude the auditor in general from providing tax services to an audit client’s management is internationally unique application of the framework approach would be

helpful

13

IV. Main critical areas of the PCAOB rulemaking docket (6)IV. Main critical areas of the

PCAOB rulemaking docket (6)

The auditor’s involvement with the audit committee’s pre-approval requirements The rules

are excessively detailed and bureaucratic reduce flexibility below the level that is

necessary given the variety of services concerned

may impose disproportionate burdens on the audit firm and on audit committees to no apparent public benefit

May lead to a de facto prohibition of even legally permissible tax services to audit clients

The auditor’s involvement with the audit committee’s pre-approval requirements The rules

are excessively detailed and bureaucratic reduce flexibility below the level that is

necessary given the variety of services concerned

may impose disproportionate burdens on the audit firm and on audit committees to no apparent public benefit

May lead to a de facto prohibition of even legally permissible tax services to audit clients

14

V. Possible impact on legislation outside the US (1)

V. Possible impact on legislation outside the US (1)

Revised 8th EU-Directive In the ECOFIN version of December 7, 2004

no specific reference to the provisions of tax services to audit clients

However: ban on non-audit services provided to public

interest audit clients in case of self review or self interest threat where appropriate to safeguard the auditor’s independence

Revised 8th EU-Directive In the ECOFIN version of December 7, 2004

no specific reference to the provisions of tax services to audit clients

However: ban on non-audit services provided to public

interest audit clients in case of self review or self interest threat where appropriate to safeguard the auditor’s independence

15

V. Possible impact on legislation outside the US (2)

V. Possible impact on legislation outside the US (2)

option of the EU-Commission to adopt principles-based implementing measures concerning the cases of self-review or self-interest in which statutory audits may be carried out or not (comitology procedure)

member states’ option to set additional conditions, e.g. on the scope of activities auditors may carry out

At present discussion to find a compromise between EU Commission, ECOFIN and European Parliament

option of the EU-Commission to adopt principles-based implementing measures concerning the cases of self-review or self-interest in which statutory audits may be carried out or not (comitology procedure)

member states’ option to set additional conditions, e.g. on the scope of activities auditors may carry out

At present discussion to find a compromise between EU Commission, ECOFIN and European Parliament

16

V. Possible impact on legislation outside the US (3)

V. Possible impact on legislation outside the US (3)

Accounting Reform Act in Germany No general ban on tax services provided to audit

clients Newly inserted provision applicable to listed

companies prohibiting tax or legal services performed outside the scope of the audit function, if they – cumulatively – extend beyond the elaboration of alternatives impact the presentation of the financial position

materially impact the presentation of the financial position

directly

Accounting Reform Act in Germany No general ban on tax services provided to audit

clients Newly inserted provision applicable to listed

companies prohibiting tax or legal services performed outside the scope of the audit function, if they – cumulatively – extend beyond the elaboration of alternatives impact the presentation of the financial position

materially impact the presentation of the financial position

directly

17

V. Possible impact on legislation outside the US (4)

V. Possible impact on legislation outside the US (4)

Previously considered preclusion of the auditor from representing audit clients before tax courts was dropped

Previously considered preclusion of the auditor from representing audit clients before tax courts was dropped

18

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (1)

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (1)

Purpose: To cover the independence issue when tax

services are provided to audit clients To reflect the market situation

Auditor’s independence and tax services Description of the different approaches and

restrictions in IFAC Code of Ethics / 8th EU-Directive / SEC-rules / some major countries

Evaluation of tax services provided to audit clients

Purpose: To cover the independence issue when tax

services are provided to audit clients To reflect the market situation

Auditor’s independence and tax services Description of the different approaches and

restrictions in IFAC Code of Ethics / 8th EU-Directive / SEC-rules / some major countries

Evaluation of tax services provided to audit clients

19

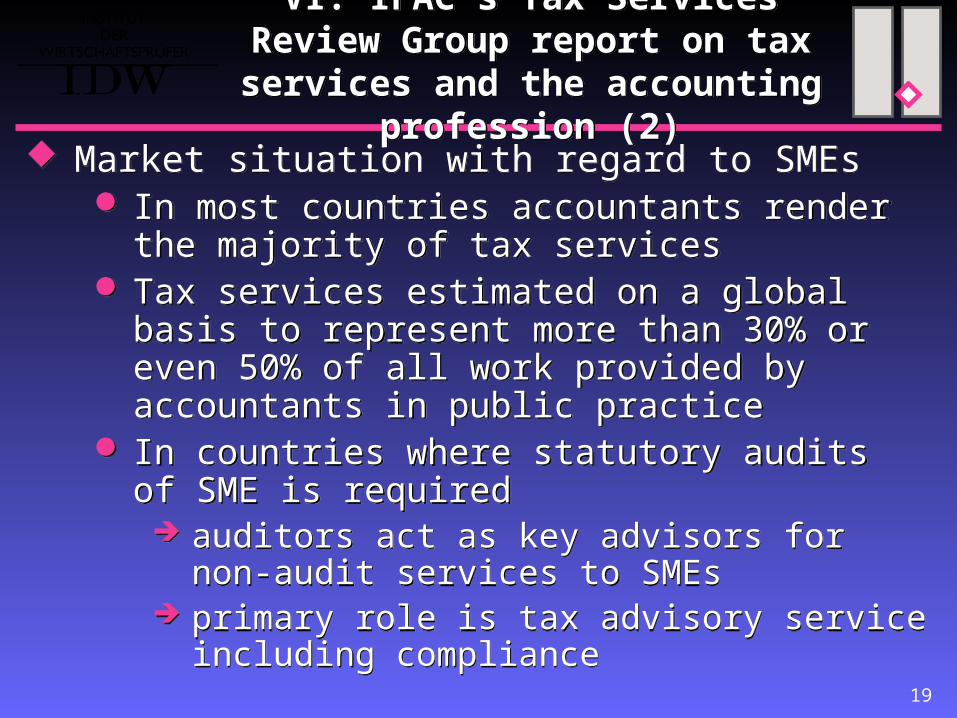

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (2)

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (2)

Market situation with regard to SMEs In most countries accountants render the majority

of tax services Tax services estimated on a global basis to

represent more than 30% or even 50% of all work provided by accountants in public practice

In countries where statutory audits of SME is required auditors act as key advisors for non-audit

services to SMEs primary role is tax advisory service including

compliance

Market situation with regard to SMEs In most countries accountants render the majority

of tax services Tax services estimated on a global basis to

represent more than 30% or even 50% of all work provided by accountants in public practice

In countries where statutory audits of SME is required auditors act as key advisors for non-audit

services to SMEs primary role is tax advisory service including

compliance

20

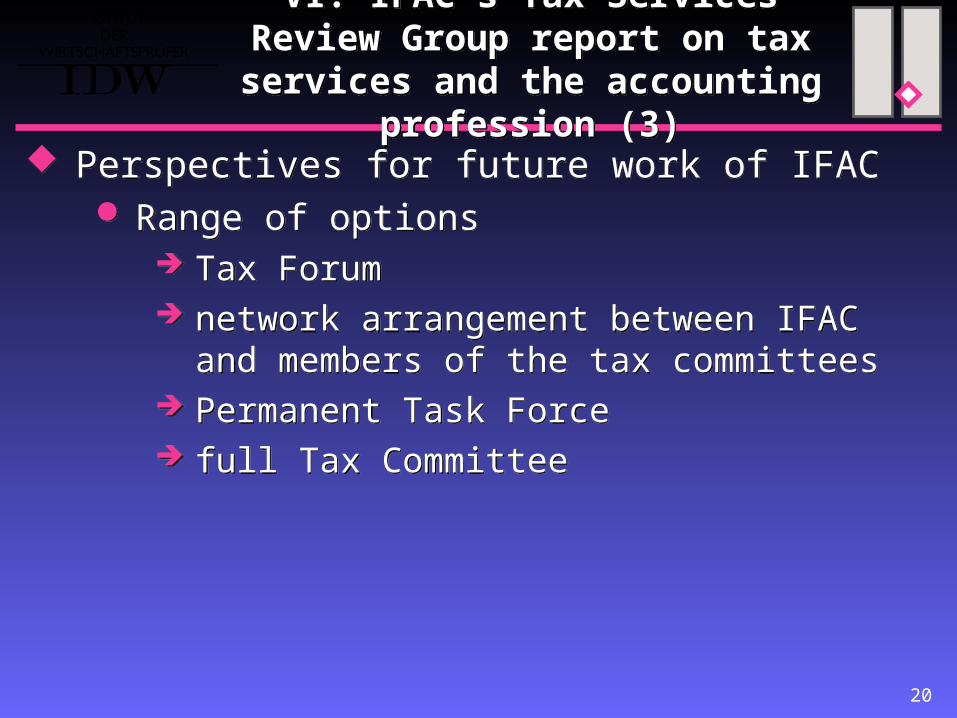

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (3)

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (3)

Perspectives for future work of IFAC Range of options

Tax Forum network arrangement between IFAC and

members of the tax committees Permanent Task Force full Tax Committee

Perspectives for future work of IFAC Range of options

Tax Forum network arrangement between IFAC and

members of the tax committees Permanent Task Force full Tax Committee

21

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (4)

VI. IFAC’s Tax Services Review Group report on tax services and

the accounting profession (4)

Recommendations to IFAC Board Invitation to other IFAC committees (Ethics and

Education) to discuss relevant points of the report, in particular whether the framework approach provides sufficient guidance

Report to external parties Decision on the way forward

Recommendations to IFAC Board Invitation to other IFAC committees (Ethics and

Education) to discuss relevant points of the report, in particular whether the framework approach provides sufficient guidance

Report to external parties Decision on the way forward

22

VII. Conclusions and Recommendations (1)VII. Conclusions and

Recommendations (1)

Extend the recommendation in the report of the Tax Services Review Group

Consider the impact on SMEs/SMPs together with IFAC SMP Permanent Task Force

Analyze final version of PCAOB docket rule to which extent it may affect the SME/SMP area indirectly

Consider preparation of a position paper on the importance of the provision of tax services to SMEs by qualified accountants

Contribute to IFAC’s future work on tax services

Extend the recommendation in the report of the Tax Services Review Group

Consider the impact on SMEs/SMPs together with IFAC SMP Permanent Task Force

Analyze final version of PCAOB docket rule to which extent it may affect the SME/SMP area indirectly

Consider preparation of a position paper on the importance of the provision of tax services to SMEs by qualified accountants

Contribute to IFAC’s future work on tax services