Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

Tax Reform: Impact on REITs, Real Estate Businesses and Investors Pass-Through Business and Interest Deductions, Cost Recovery, Carried Interest, Sale of Partnership Interests, and More

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, FEBRUARY 27, 2018

Presenting a live 90-minute webinar with interactive Q&A

Steven R. Meier, Partner, Seyfarth Shaw, Chicago

John P. Napoli, Partner, Seyfarth Shaw, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-871-8924 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Seyfarth Shaw LLP “Seyfarth Shaw” refers to Seyfarth Shaw LLP (an Illinois limited liability partnership).

Tax Reform: Impact on REITs, Real Estate Businesses, and Investors

John Napoli and Steven Meier

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential

Agenda

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential

01 Background: Timing of tax law changes

02 Overview: What has changed/stayed the same

03 Pass-through business deduction

04 REIT dividends

05 Business interest deduction

06 Cost recovery

6

Agenda

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential

07 Like-kind exchanges

08 Carried interest holding period requirements

09 Sales of partnership interests by foreign partners

10 State and local tax deduction

11 Section 179 expensing

12 Historic preservation and rehabilitation tax credits

7

Agenda

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential

• How we’ll proceed:

• After a little background and an overview, we’ll cover

the major provisions that impact real estate and REITs

• We’ll discuss the provisions, work through an example

or two, discuss the implications of the provision for real

estate and REITs, and then point out some issues that

will require Treasury/IRS guidance

• We will answer questions at the end

8

Background: Timing of tax law changes

• November 2: House introduces “Tax Cuts & Jobs Act” (the

“Act”)

• November 3: House releases Chairman’s Mark of the Act

• November 9:

• House Ways and Means Committee approves of the Act

• Senate releases Chairman’s Mark of the Act

• November 16:

• House passes the Act

• Senate Finance Committee approves of the Act

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 10

Background: Timing of tax law changes

• November 28: Senate Budget Committee approves of the

Act

• December 2: Senate passes the Act

• December 15: Conferees appointed

• December 19: Senate passes modified Act

• December 20: House passes modified Act

• December 22: President Trump signs the Act into law

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 11

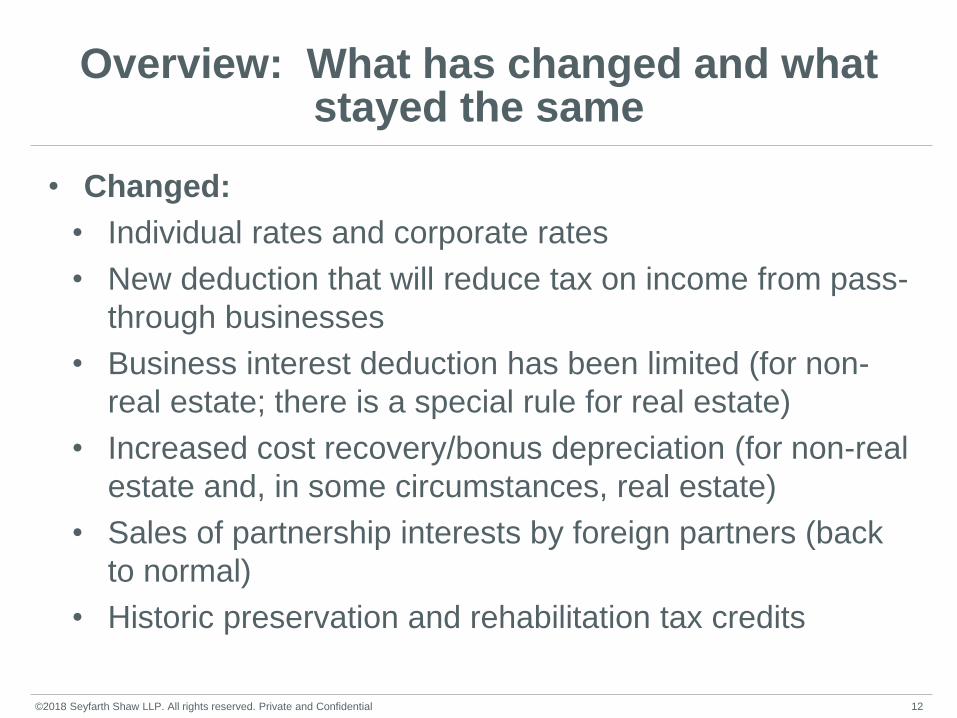

Overview: What has changed and what stayed the same

• Changed:

• Individual rates and corporate rates

• New deduction that will reduce tax on income from pass-

through businesses

• Business interest deduction has been limited (for non-

real estate; there is a special rule for real estate)

• Increased cost recovery/bonus depreciation (for non-real

estate and, in some circumstances, real estate)

• Sales of partnership interests by foreign partners (back

to normal)

• Historic preservation and rehabilitation tax credits

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 12

Overview: What has changed and what stayed the same

• Did not change:

• Business interest deduction (for real estate)

• Cost recovery/bonus depreciation (for real estate)

• 1031s survived! (for the most part)

• Most of the rules related to carried interests

• SALT deduction (for businesses)

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 13

Pass-through business deduction

• New Code Section 199A: 20% tax deduction for individuals for

“qualified business income” from “pass-through businesses”

• This deduction is scheduled to expire after 2025

• Pass-through businesses include domestic:

• Sole proprietorships

• Partnerships

• S corporations

• LLCs taxed as partnerships, S corporations, disregarded entities,

trusts, etc.

• REITs

• Publicly traded partnerships

• Cooperatives

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 14

Pass-through business deduction

• Qualified business income does not include:

• Income (received by taxpayers with income above $315,000 if filing

a joint return or $157,500 otherwise) from a “specified service trade

or business”

– Health, law, accounting, actuarial science, performing arts,

consulting, athletics, financial services, brokerage services,

investing or investment management, trading, or dealing in

securities, partnership interests, or commodities, or any trade or

business where the principal asset of such trade or business is

the reputation or skill of one or more of its employees or owners

• Section 707(c) guaranteed payments for services

• Amounts paid that are treated as reasonable compensation paid to

a taxpayer

• Amounts paid or incurred for services by a partnership to a partner

who is acting other than in his or her capacity as a partner

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 15

Pass-through business deduction

• Deduction amount limitation:

– “Wage limitation” and “basis limitation”

– For taxpayers with incomes above certain thresholds

($315,000 joint return or $157,500 otherwise), the 20%

deduction is limited to the greater of:

50% of the W-2 wages paid by the business, or

25% of the W-2 wages paid by the business, plus

2.5% of the unadjusted basis, immediately after

acquisition, of depreciable property (which includes

structures, but not land)

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 16

Pass-through business deduction

• Deduction amount limitation:

– Real estate businesses need to look carefully at the

wage and basis limitations to be sure that they will

receive the full 20% deduction

The “plus 2.5% of the unadjusted basis, immediately

after acquisition, of depreciable property” is very

significant for real estate businesses

- For most real estate businesses the 2.5% will be

sufficient to allow the full 20% deduction

- If not, the business may need to consider

restructuring to shift around W-2 employees

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 17

Pass-through business deduction

• Example 1:

– Jim, an individual, is the sole owner of Jim’s Business, LLC

– In 2018, Jim receives $1,000,000 from Jim’s Business, LLC

– In 2018, Jim’s Business, LLC paid $100,000 in W-2 wages and

has $5,000,000 unadjusted basis in depreciable property

– Jim’s maximum deduction, before considering the limitations,

would be $200,000 (20% of 1,000,000)

– BUT: Jim’s limitation (the greater of 50% of W-2 wages or 25% of

W-2 wages + 2.5% of basis in depreciable property) is:

$150,000

- 50% of $100,000 = $50,000

- 25% of $100,000 + 2.5% of $5,000,000 = $25,000 + $125,000

= $150,000

– Jim can only deduct $150,000, the rest is taxed at individual rates

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 18

Pass-through business deduction

• Example 2:

– Same as Example 1, except Jim’s Business, LLC paid

$100,000 in W-2 wages and has $7,500,000 unadjusted

basis in depreciable property in 2018

– Jim’s maximum deduction, before considering the

limitations, would still be $200,000.

– Jim’s limitation is:

$212,500

- 50% of $100,000 = $50,000

- 25% of $100,000 + 2.5% of $7,500,000 = $25,000 +

$187,500 = $212,500

– Jim can deduct the full $200,000, the rest is taxed at

individual rates

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 19

Pass-through business deduction

• Example 3:

– Same as Example 1, except Jim’s Business, LLC is a pure

real estate business (non-S corporation) with no

employees, and so no W-2 wages, but has $10,000,000

unadjusted basis in depreciable property in 2018

– Jim’s maximum deduction, before considering the limitations,

would still be $200,000

– Jim’s limitation is:

$250,000

- 50% of $0 = $0

- 25% of $0 + 2.5% of $10,000,000 = $0 + $250,000 =

$250,000

– Jim can deduct the full $200,000, the rest is taxed at

individual rates ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 20

Pass-through business deduction

• Example 4:

– Same as Example 1, except Jim’s Business, LLC is a

“specified service trade or business” (here, say a

consulting business)

– Jim received $1,000,000 in 2018, so his income

exceeds the threshold ($315,000 if filing a joint return

or $157,500 otherwise) and the “specified service

trade or business” provision applies to him

– Jim’s income from Jim’s Business, LLC is not

“qualifying business income”

– Jim cannot deduct any of the $1,000,000 he received

from Jim’s Business, LLC, everything is taxed at

individual rates ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 21

REIT dividends

• REITs are considered a pass-through business for

purposes of this deduction

• As a result, REIT most dividends qualify for the deduction

• REIT qualified and capital gains dividends do not qualify

for the deduction

• REIT dividends are not subject to the wage and basis

limitations

• Effective maximum U.S. federal income tax rate on

qualified REIT dividends is 29.6% (plus additional 3.8%

Medicare tax on dividends)

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 22

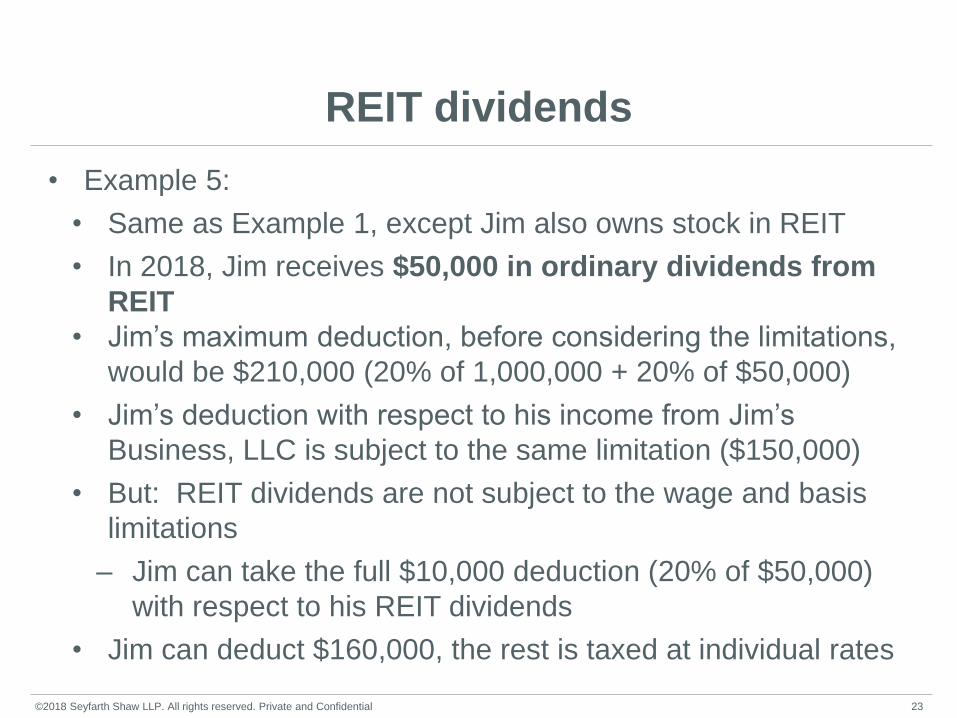

REIT dividends

• Example 5:

• Same as Example 1, except Jim also owns stock in REIT

• In 2018, Jim receives $50,000 in ordinary dividends from

REIT

• Jim’s maximum deduction, before considering the limitations,

would be $210,000 (20% of 1,000,000 + 20% of $50,000)

• Jim’s deduction with respect to his income from Jim’s

Business, LLC is subject to the same limitation ($150,000)

• But: REIT dividends are not subject to the wage and basis

limitations

– Jim can take the full $10,000 deduction (20% of $50,000)

with respect to his REIT dividends

• Jim can deduct $160,000, the rest is taxed at individual rates

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 23

Implications: Pass-through business deduction & REIT Dividends

• The combination of the new deduction and the reduction of the

maximum individual tax bracket from 39.6% to 37% will result in

significant tax savings for real estate investors

• The carve out for “specified service trade or business” may mean

that service professionals should consider whether it makes sense

to run their business through a personal service corporation

• For REITs, the reduced corporate tax rate (now 21%) reduces, but

does not eliminate, the benefit to choosing REIT rather than

corporate form

• The Act reduces the favorable rate differential between qualified

REIT dividends and C corporation dividends from 8.4% to 7.2%

• However, C corporation tax rate does not expire, but the pass-

through deduction will expire, unless extended, after 2025

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 24

Issues: Pass-through business deduction & REIT Dividends

• Combination of qualified and nonqualified businesses

• What if a partnership has two different businesses, one qualified

and the other nonqualified? Do you need to bifurcate? On what

basis do you bifurcate? How do you bifurcate employees/assets?

• Consulting

• What if consulting is an ancillary part of the business? Does it taint

the qualifying business? How significant must it be before it taints?

• Doing business with a “specified service trade or business”

• If a business provides permissible services on an arm’s length basis

to a “specified service trade or business”, does the business qualify

for the 20% deductions?

• “Skill and reputation” as a “principle asset”

• What does this mean?

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 25

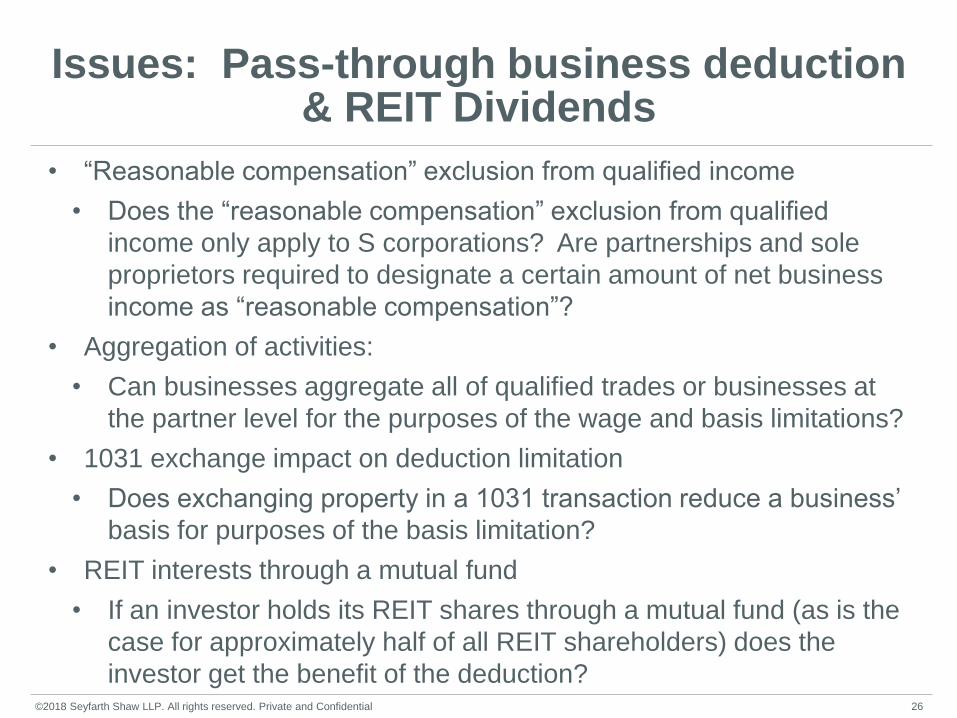

Issues: Pass-through business deduction & REIT Dividends

• “Reasonable compensation” exclusion from qualified income

• Does the “reasonable compensation” exclusion from qualified

income only apply to S corporations? Are partnerships and sole

proprietors required to designate a certain amount of net business

income as “reasonable compensation”?

• Aggregation of activities:

• Can businesses aggregate all of qualified trades or businesses at

the partner level for the purposes of the wage and basis limitations?

• 1031 exchange impact on deduction limitation

• Does exchanging property in a 1031 transaction reduce a business’

basis for purposes of the basis limitation?

• REIT interests through a mutual fund

• If an investor holds its REIT shares through a mutual fund (as is the

case for approximately half of all REIT shareholders) does the

investor get the benefit of the deduction? ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 26

Business interest deduction

• Business interest deduction (Generally):

• “Business interest” = any interest paid or accrued on

indebtedness properly allocable to a trade or business,

excluding “investment interest”

• New Code Section 163(j): for most taxpayers, the Act

disallows the deductibility of business interest to the

extent that net interest expense exceeds 30% of

EBITDA (2018 through 2022) or EBIT (beginning in

2022)

– EBITDA = taxpayer’s earnings before interest, taxes,

depreciation and amortization

– EBIT = taxpayer’s earnings before interest and taxes

– EBITDA is the bigger number ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 27

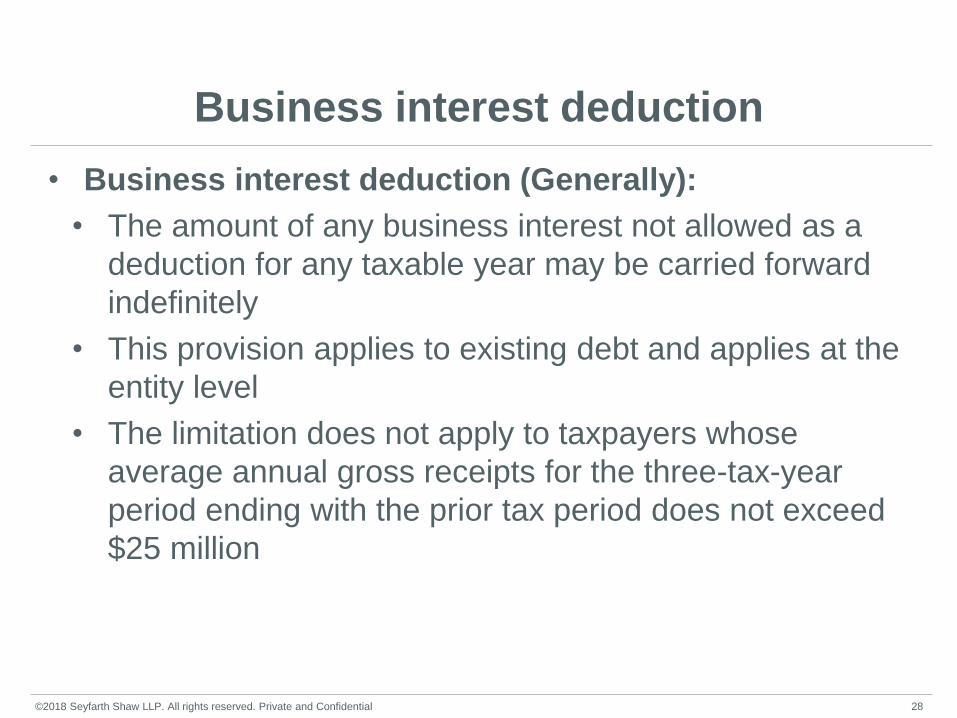

Business interest deduction

• Business interest deduction (Generally):

• The amount of any business interest not allowed as a

deduction for any taxable year may be carried forward

indefinitely

• This provision applies to existing debt and applies at the

entity level

• The limitation does not apply to taxpayers whose

average annual gross receipts for the three-tax-year

period ending with the prior tax period does not exceed

$25 million

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 28

Business interest deduction

• Business interest deduction (Real Estate):

• A real property trade or business can elect out of the

new business interest disallowance regime.

– Any business engaged in real property development,

redevelopment, construction, reconstruction,

acquisition, conversion, rental, operation,

management, leasing, or brokerage trade or business

• The real estate exception extends to

– (1) the activities of corporations and REITs, and

– (2) the operation or management of a hotel.

• The election out is irrevocable

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 29

Business interest deduction

• Business interest deduction (Partnerships):

• The limitation on the deduction is determined at the

partnership level, and any deduction available after

applying such limitation is included in the partners’

nonseparately stated taxable income or loss from the

partnership

• Any business interest that is not allowed as a deduction

to the partnership for the taxable year is not carried

forward by the partnership but, instead, is allocated to

each partner as "excess business interest" in the same

manner as nonseparately stated taxable income or loss

of the partnership

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 30

Business interest deduction

• Business interest deduction (Partnerships):

• The partner may deduct its share of the partnership’s

excess business interest in any future year, but only

against excess taxable income attributed to the partner

by such partnership

• A partner’s share of excess taxable income is

determined in the same manner as nonseparately stated

income and loss

• Any disallowed interest expense allocated to a partner

immediately reduces the unitholder’s basis in its

partnership interest, but any amounts that remain

unused upon disposition of the interest are restored to

basis immediately prior to disposition

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 31

Business interest deduction

• Example 6:

• In 2018, Jim’s Business, LLC paid $2,000,000 in net

interest expense that is properly allocable to its trade or

business to Lender

• In 2018, Jim’s Business, LLC’s earnings before interest,

taxes, depreciation and amortization is $5,000,000

• The business interest expense limitation is $1,500,000

(30% of $5,000,000)

• Jim’s Business, LLC can only deduct $1,500,000 in

business interest in 2018

• Jim’s Business, LLC can carry forward the $500,000 in

disallowed business interest indefinitely

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 32

Business interest deduction

• Example 7:

• Same as Example 6, except Jim’s Business, LLC is a

real property development business

• Jim’s Business, LLC can make an election out of the

business interest deduction

• Jim’s Business, LLC would then be able to deduct the

full $2,000,000 in net interest

• However, the election does have an impact on Jim’s

Business, LLC’s ability to take advantage of the new

cost recover provisions

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 33

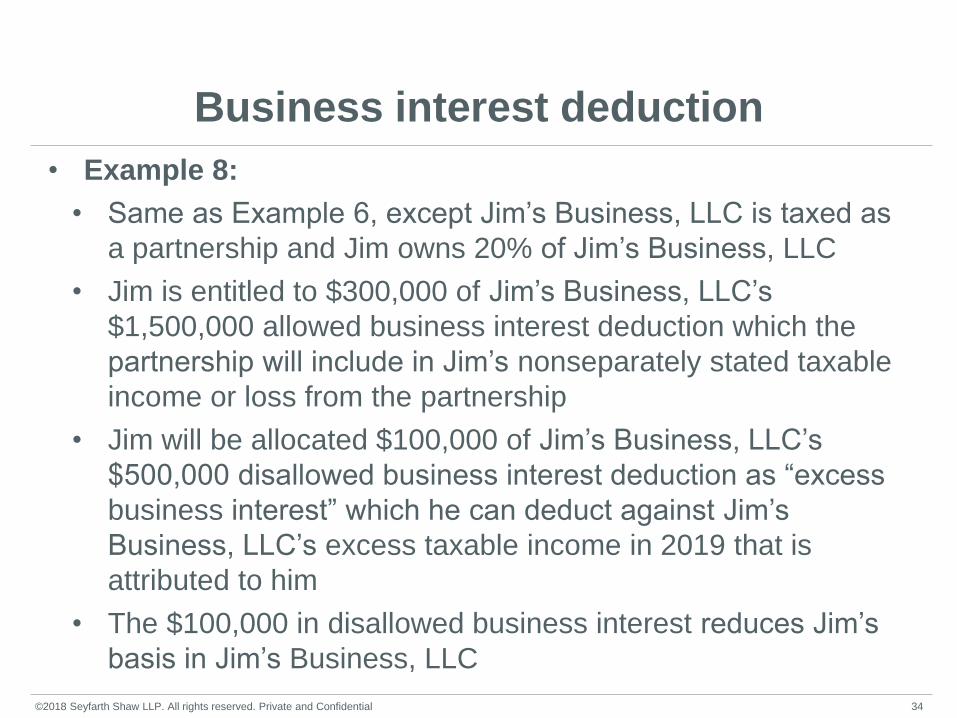

Business interest deduction

• Example 8:

• Same as Example 6, except Jim’s Business, LLC is taxed as

a partnership and Jim owns 20% of Jim’s Business, LLC

• Jim is entitled to $300,000 of Jim’s Business, LLC’s

$1,500,000 allowed business interest deduction which the

partnership will include in Jim’s nonseparately stated taxable

income or loss from the partnership

• Jim will be allocated $100,000 of Jim’s Business, LLC’s

$500,000 disallowed business interest deduction as “excess

business interest” which he can deduct against Jim’s

Business, LLC’s excess taxable income in 2019 that is

attributed to him

• The $100,000 in disallowed business interest reduces Jim’s

basis in Jim’s Business, LLC

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 34

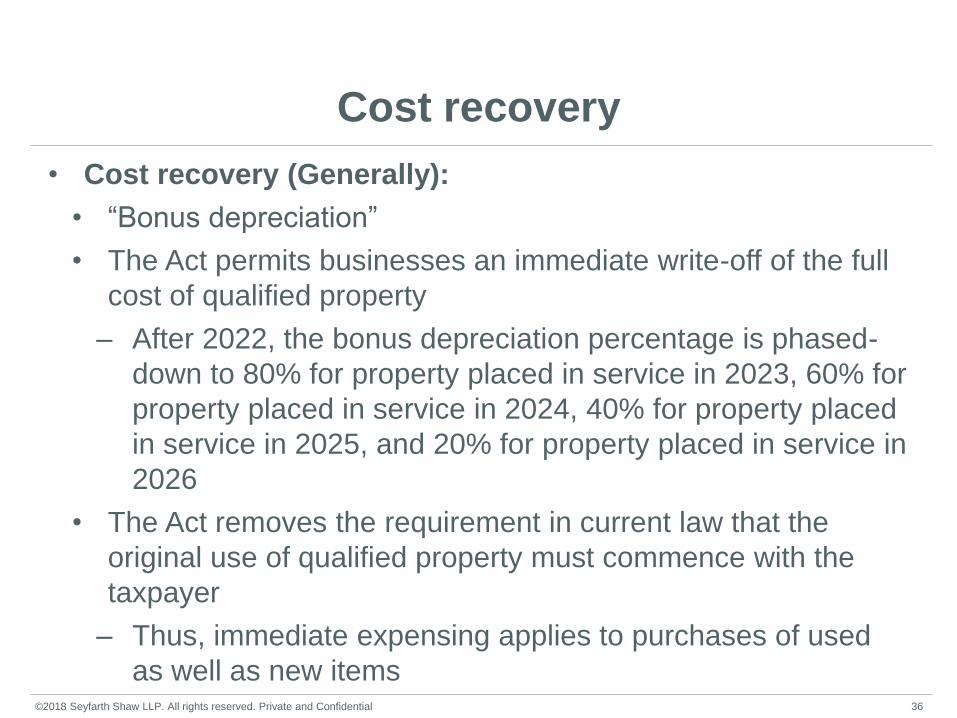

Cost recovery

• Cost recovery (Generally):

• “Bonus depreciation”

• The Act permits businesses an immediate write-off of the full

cost of qualified property

– After 2022, the bonus depreciation percentage is phased-

down to 80% for property placed in service in 2023, 60% for

property placed in service in 2024, 40% for property placed

in service in 2025, and 20% for property placed in service in

2026

• The Act removes the requirement in current law that the

original use of qualified property must commence with the

taxpayer

– Thus, immediate expensing applies to purchases of used

as well as new items ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 36

Cost recovery

• Cost recovery (Real Estate):

• Taxpayers that elect to use the business interest real estate

exception will be permitted to fully expense land improvements and

tangible, personal property used in their real property trade or

business from 2018 to 2023

• However, such taxpayers must depreciate real property using ADS

under slightly longer recovery periods: 40 years for nonresidential

property, 30 years for residential rental property, and 20 years for

qualified improvement property (interior)

• The switch to ADS applies to all nonresidential rental property,

residential rental property, and qualified improvement property, not

just property placed in service beginning in 2018

• The Act did not adopt the Senate proposal to reduce the MACRS

depreciable lives on residential and nonresidential depreciable

property

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 37

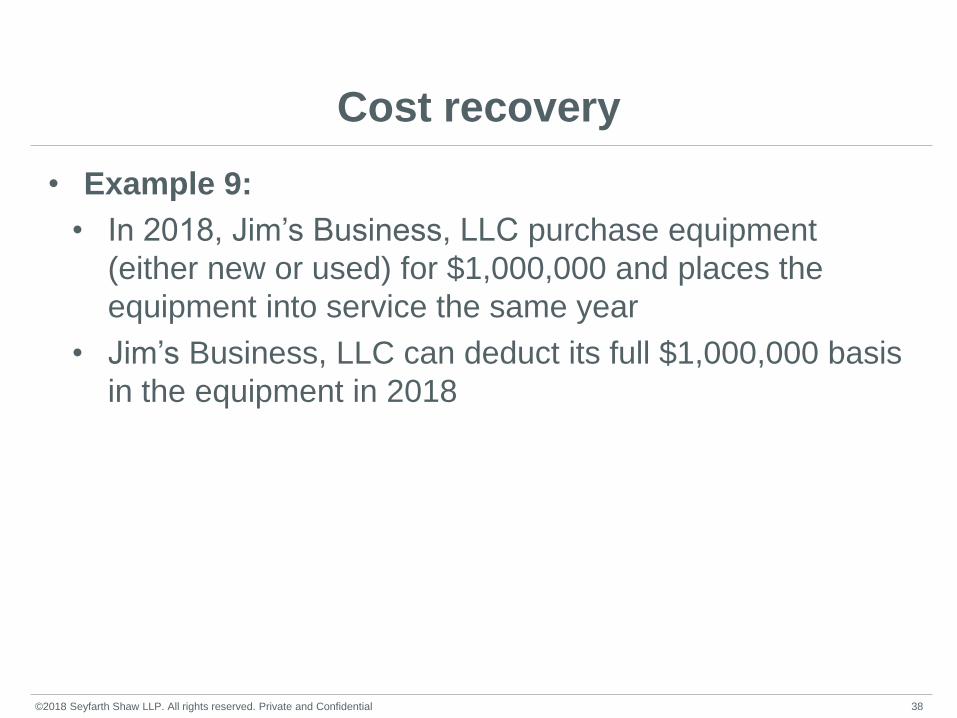

Cost recovery

• Example 9:

• In 2018, Jim’s Business, LLC purchase equipment

(either new or used) for $1,000,000 and places the

equipment into service the same year

• Jim’s Business, LLC can deduct its full $1,000,000 basis

in the equipment in 2018

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 38

Cost recovery

• Example 10:

• Same as Example 9, except Jim’s Business, LLC

elected out of the business interest deduction limitation

• Jim’s Business, LLC cannot fully expense its equipment

in 2018

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 39

Implications: Business interest deduction & cost recovery

• Real estate trades and businesses will need to decide which is

more important to their business

– Companies that rely heavily on leverage, may choose to elect

out of the business interest deduction limitation

– Companies that do not rely heavily on leverage may find that

the shorter depreciable lives of real property (and expensing

for qualified improvement property) may outweigh any

detriment from the limitation on interest deductions

– The interest limitation will be less onerous initially because

adjusted taxable income will not include deductions for

depreciation, amortization, or depletion until to 2022. This

may mean that the depreciation and expensing benefits could

justify deferring the election for exemption from the interest

limitation until 2022

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 40

Issues: Business interest deduction & cost recovery

• Debt incurred to capitalize an entity that engages in a real

property trade or business

– If a taxpayer borrows money and uses the money to capitalize

an entity that is engaged in a real property trade or business,

can that taxpayer elect out of the business interest deduction

limitation and deduct the interest?

– If the debt is used to capitalize several businesses, some of

which are real property trades or businesses and others are

not, does the taxpayer need to allocate debt/interest among

the businesses?

• Corporations borrowing to invest in REITs

– If a corporation incurs debt to purchase REIT shares, can the

corporation elect out of the business interest deduction

limitation and deduct the interest? ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 41

Like-kind exchanges

• The Act permits taxpayers to continue to defer gain on real

estate like-kind exchanges.

• Improved real estate and unimproved real estate will continue

to be considered property of a like kind.

• However, the portion of any exchange that includes personal

property will no longer qualify for tax deferred treatment under

Code Section 1031

• General Implications: This is very good for real estate

because it will continue to generate interest in real estate

investments

• Not a significant change from current law

• Cost Segregation Implications

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 42

Carried interest holding period requirements

• Holders of a carried interest in certain types of

partnerships, including hedge funds, private equity funds,

and real estate, must hold the interest for 3 years in order

to receive long-term capital gain treatment.

• The 3-year holding period applies to the partnership

interest and to the assets held by the partnership

• If the holder disposes of the interest before the 3 years,

they receive short-term capital gain treatment

• Implications: this is unlikely to have a significant impact

– Most carried interest holders hold their interest for

more than 3 years anyways

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 43

Sales of partnership interests by foreign partners

• The Act added a provision that treats gain or loss from the sale of a

partnership interest by a foreign partner as effectively connected

income (“ECI”) that is taxable in the U.S. if the gain or loss from the

sale of the underlying assets held by the partnership would be treated

as ECI

• This provision statutorily reverses the Tax Court’s recent decision

in Grecian Magnesite Mining, Industrial & Shipping Co., SA vs.

Commissioner, 149 T.C. No. 3 (Jul. 13, 2017) and returns to a rule

similar to Revenue Ruling 91-32 (1991-1 C.B. 107)

• The Act also requires the purchaser of a partnership interest from a

partner to withhold 10% of the amount realized on the sale or

exchange of the partnership interest unless the transferor certifies that

the transferor is not a nonresident alien individual or a foreign

corporation

• Implication: Return to status quo; must account for new withholding

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 44

State and local tax deduction

• The Act continues to permit pass-through entities the

ability to deduct state and local taxes paid or accrued in

carrying on a trade or business or in an activity related to

the production of income

• Implication: Status quo

• However, for individuals, the property and SALT tax

deduction is limited to a combined $10,000

• Implication: This may have an impact on residential

property values in high-tax states

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 45

Section 179 expensing

• The Act increases the maximum amount that a taxpayer

may expense under Code Section 179 to $1,000,000, and

increases the phase-out threshold amount to $2,500,000

• The provision also expands the definition of Code Section

179 property to include:

• Certain depreciable tangible personal property used

predominantly to furnish lodging or in connection with

furnishing lodging, and

• Any of the following improvements to nonresidential real

property placed in service after the date the real

property was first placed in service: roofs; heating,

ventilation, and air-conditioning property; fire protection

and alarm systems; and security systems

• Implications: Helpful for smaller real estate businesses ©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 46

Historic preservation and rehabilitation tax credits

• The Act preserves the 20% tax credit for the rehabilitation

of historically certified structures, but now requires that

taxpayers claim the credit ratably over a 5-year period.

• The Act repeals the 10% credit for the rehabilitation of pre-

1936 structures

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 47

Overall Impressions

• Benign to favorable for real estate

• New pass-through deduction is helpful for bringing in new

investors

• Real estate businesses will need to choose between

avoiding the new business interest deduction limitation or

enjoying the new full and immediate bonus depreciation

• May cause a shift away from debt financing towards

equity financing

• Retention of 1031s for real property is critical

• Carried interest left largely unharmed

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 48

Questions?

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 49

Thank you

Steven R. Meier

John P. Napoli

©2018 Seyfarth Shaw LLP. All rights reserved. Private and Confidential 50

![[Najib Razali] Islamic REITS - prres.net REITs.pdfDo Islamic REITs Behave Differently from Conventional REITs? – Empirical Evidence from Malaysian REITs Sing Tien Foo National University](https://img.pdfslide.us/doc/110x75/5abe8db57f8b9a7e418d14eb/najib-razali-islamic-reits-prres-reitspdfdo-islamic-reits-behave-differently.jpg)