Embed Size (px)

Citation preview

Tax implication on

Salary Income

Presented by:Presented by:Presented by:Presented by:

Sachin Gujar Sachin Gujar Sachin Gujar Sachin Gujar

Chartered AccountantChartered AccountantChartered AccountantChartered Accountant

Sachin Gujar, C.A 2

“Salary” Salary is a periodical payment for Services rendered by an

employee to an employer. However under sec.17(1) of the Income

Tax Act, following items are also included :

1. Wages

2. Any annuity or pension

3. Any Gratuity

4. Any Fees, commission, perquisites or profits in lieu of or in addition to any salary or wages.

5. Any advance for Salary.

6. Any payment received by an employee while in service in respect of any period of leave not availed of by him. ( i.e. leave encashment)

Sachin Gujar, C.A 3

Other items included under Salary

� Dearness Allowance :

It is an additional payment over & above the basic Salary for meting the high cost of living.

� Bonus :

It is a payment made under a service agreement between the employer & employee, which may be in the form of Diwali Bonus, Performance Bonus etc.

� Commission / Incentive :

If an employee is appointed on a fixed monthly salary plus commission as a percentage of revenue or sales then the said commission shall also be included in his Salary.

Sachin Gujar, C.A 4

Exemptions under Sec.10(14)

Nature of Allowance Extent to which Exempt

1. Conveyance Allowance

Rs.800/- per month

2. Children Education Allowance

Rs.100/- per month per child upto max. of 2 children

3. Allowance to meet

the hostel expenditure of the child

Rs.300/- per month per child upto max. of 2 children

Sachin Gujar, C.A 5

Exemption towards reimbursement of

Medical expenses

The reimbursement by employer of actual expenditure incurred by an

employee for Medical treatment of himself or any of his family

members is exempt subject to a maximum ceiling of Rs.15000/-p.a.

“Family” in relation to an employee means :

� The Spouse and children of the employee

� Parents, brothers and sisters of the employee who are wholly or mainly dependent on him

Sachin Gujar, C.A 6

Exemption towards House rent

Allowance

An employee is entitled to claim the exemption towards

HRA U/s.10(13A) when all the following conditions are fulfilled:

1. The allowance from the employer must be specific to meet expenditure on payment of rent.

2. The residential accommodation occupied by the employee is not owned by him.

3. The actual payment of rent should exceed 10% of his salary.

Sachin Gujar, C.A 7

If all these conditions are satisfied then HRA is exempt subject to least of the following:

� Actual HRA received

� Rent paid in excess of 10% of Salary

� 40% of Salary

For the purpose of this section Salary means Basic + D.A

Exemption towards House rent

Allowance (contd...)

Sachin Gujar, C.A 8

Rs.(p.a) Rs.(p.a) Rs.(p.a) Annual salary 1,44,000

House rent allowance received 86,400

Less: Exemption u/s. 10(13A)read with Rule2A:

(a)House rent allowance recd... 86,400

Rs.

(b)Actual rent paid 93,600

Less: 10% of Salary 14,400 79,200

(c) 40% of salary 57,600

Least of (a), (b) & (c) is exempt 57,600 28,800

Salary income subject to deduction... 1,72,800

Let us see an example for HRA

Sachin Gujar, C.A 9

Exemption towards Leave Travel

concession Leave travel concession / allowance received by an employee for

himself and his family in connection with his proceeding on leave to

any place in India is exempt U/s.10(5) subject to the following

conditions framed under Rule 2B:

� Where the journey is performed by Air an amount not exceeding the economy air fare of the National carrier and where the journey is performed by Rail or any other mode of transport an amount not exceeding the First Class A.C rail fare by the shortest route to the place of destination.

� The said exemption is available in respect of two journeys performed in a block of 4 calendar years.

� It is important to understand that the LTA is exempted only towards the expenses incurred for the mode of transport and excluding hotel, food, entertainment expenses etc.

Sachin Gujar, C.A 10

Deductions available from Deductions available from Deductions available from Deductions available from

Salary (Way to save your TAX )Salary (Way to save your TAX )Salary (Way to save your TAX )Salary (Way to save your TAX )

After computing the net salary as mentioned in the previous provisions an individual is entitled to claim deductions under various other sections of the Income Tax Act, which are mentioned here under:

1. Deduction U/s.80C:

Amount invested in specified savings like Life Insurance Premium, PF, PPF, NSC, ELSS Mutual Fund & Housing Loan principal repayment.

2. Deduction U/s.80CCC:

Contribution towards pension plans subject to a maximum payment of Rs.10000/- It may however be noted that the overall ceiling for investment U/s.80C & 80CCC is restricted to Rs.1.00 Lac p.a.

3. Deduction U/s.80D:

Medical insurance premium paid for the health of the individual and spouse or dependent parents or dependent children subject to a maximum of Rs.10000/-p.a.

Sachin Gujar, C.A 11

4. Deduction U/s.80DD:

Expenditure incurred for maintenance and medical treatment of a dependent who is a person with disability subject to deduction of Rs.50000/- p.a. or Rs.75000/-p.a. if such person has severe disability as mentioned in the provision.

5. Deduction U/s.80E:

Expenditure incurred on interest on loan (and not repayment of principal amount) taken from any financial institution for the purpose of higher education.100% of interest repayment is allowed as a deduction for 8 successive years beginning from the year in which the repayment starts.

Deductions available fromDeductions available fromDeductions available fromDeductions available from

Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…

Sachin Gujar, C.A 12

Deductions available fromDeductions available fromDeductions available fromDeductions available from

Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…Salary (Way to save your TAX ) contd…

6. Deduction U/s.80G:

Donations to approved funds, Institutions & Trusts qualify for 50% or 100% deduction as applicable, U/s.80G.

It may however be noted that the total deduction U/s.80G should not exceed 10% of gross total income.

7. Deduction U/s.80GG:

Where a individual is not entitled to HRA and who is paying rent in excess of 10% of his total income and who files a declaration in form no.10BA is eligible for deduction under this section subject to the following conditions:-

a. The Assessee does not own any other residential accommodation at the place / city where he performs his duties for employment and

b. Subject to max. of 25% of total income or Rs.2000/- per month whichever is less

Sachin Gujar, C.A 13

Deduction for Housing Loan Repayment

One of the important deduction available under the Income Tax Act is repayment of your housing loan.

� The Interest component is exempt with a upper

limit of Rs.1.50 Lacs p.a. U/s.24 � The principal component is deductible with a

upper limit of Rs.1.00 Lac p.a. (together with other specified savings) U/s.80C

Sachin Gujar, C.A 14

Income Tax Rates Individual Tax Payable for Mar’07

If the net income is upto 1 Lac p.a.

Nil

Between Rs.1.00 Lac p.a. to Rs.1.50 Lacs p.a.

10% of the amount by which the total income exceeds Rs. 1,00,000/ p.a.

Between Rs. 1,50,000/-p.a. to Rs.2,50,000/- p.a.

Rs. 5000 + 20% of the amount by which the total income exceeds Rs. 1,50,000/-p.a.

Rs.2,50,000/-p.a. and above

Rs. 25,000/- + 30% of the amount by which the total income exceeds Rs. 2,50,000/-p.a.

Surcharge

10 % of the tax payable if total income exceeds Rs. 10.00 lacs p.a.

otherwise NIL

Education Cess 2 % of Tax Payable

Sachin Gujar, C.A 15

Income Tax rates for Women Individual Tax Payable for Mar’07

If net income is upto Rs.1.35 Lac p.a.

Nil

Between Rs.1.35 Lac p.a. to Rs.1.50 Lacs p.a.

10% of the amount by which the. total income exceeds Rs. 1,35,000/-p.a.

Between Rs.1,50,000/-p.a. to Rs.2,50,000/-p.a.

Rs. 1500 + 20% of the amount by which the total income exceeds Rs. 1,50,000/-p.a.

Rs.2,50,000/-p.a. and above

Rs. 21500/- + 30% of the amount by which the total income exceeds Rs. 2,50,000/-p.a.

Surcharge

10 % of the tax payable if total income exceeds Rs. 10.00 lacs p.a. otherwise NIL

Education Cess 2 % of Tax Payable

Sachin Gujar, C.A 16

Illustration No.1

Tax payable by an individual having total income of Rs.2.00 lacs

On Rs.1.00 Lac p.a. NIL

On Rs.1.00 Lac p.a. to Rs.1.50 Lacs p.a. @ 10%

5000/-

On Rs.1.50 Lacs p.a. to Rs.2.00 Lacs p.a. @ 20%

10000/-

Tax Payable 15000/-

Add: Education Cess @ 2% 300/-

Net Tax Payable 15300/-

Sachin Gujar, C.A 17

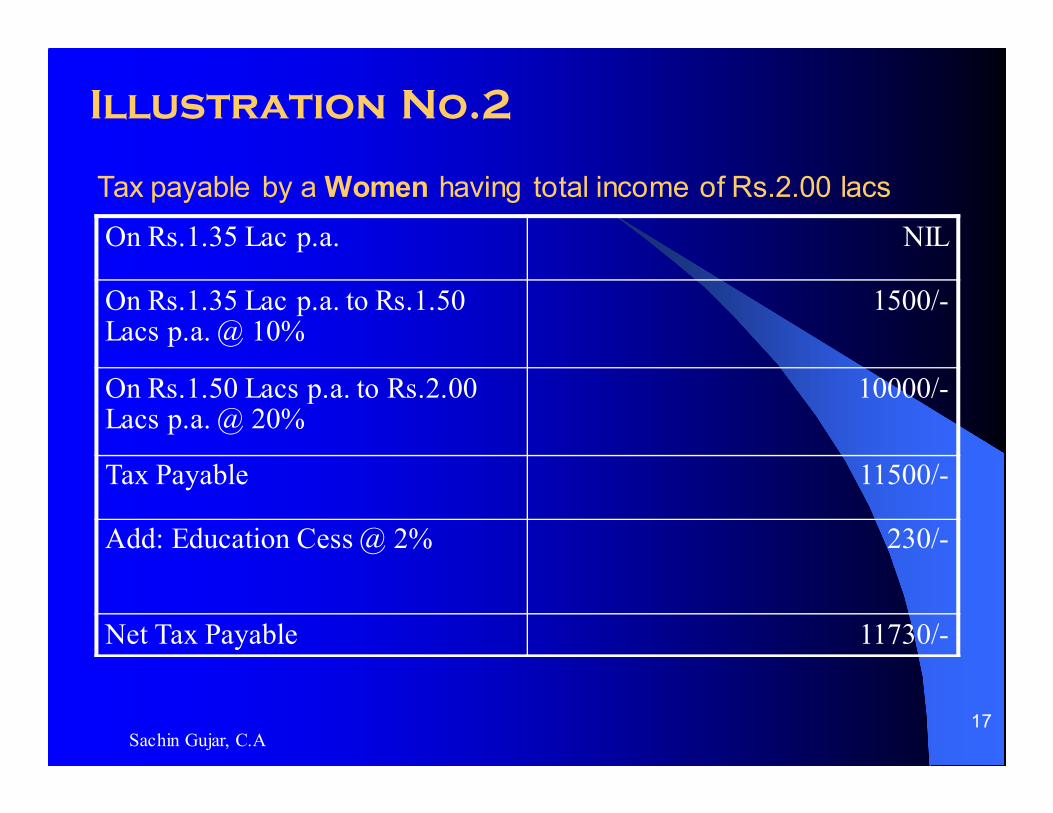

Illustration No.2

Tax payable by a Women having total income of Rs.2.00 lacs

On Rs.1.35 Lac p.a. NIL

On Rs.1.35 Lac p.a. to Rs.1.50 Lacs p.a. @ 10%

1500/-

On Rs.1.50 Lacs p.a. to Rs.2.00 Lacs p.a. @ 20%

10000/-

Tax Payable 11500/-

Add: Education Cess @ 2% 230/-

Net Tax Payable 11730/-

Sachin Gujar, C.A 18

Due Date For Filing your Tax Return

� The Due date for filing your Tax Return is 31st July

� Non Filing of your Return in time can attract Interest / Penalty

� You have to file your Tax Return in Form No.2D ( Saral ).

Sachin Gujar, C.A 19

Budget Implications for F.Y 2007-08

� Basic exemption increased from Rs.1.00 Lac p.a. to Rs.1.10 Lacs

p.a. and from Rs.1.35 Lacs p.a. to Rs.1.45 Lacs p.a. for women.

� Deduction U/s.80D for medical insurance premium increased from Rs.10000/-p.a. to Rs.15000/-p.a.

� Education cess increased from 2% to 3%.

Sachin Gujar, C.A 20

Thank You……..!!!

Sachin Gujar, C.A 21

Contact Us:

Sachin Gujar

Chartered Accountant

1040, Sadashiv Peth,

Bahar Apts,

Near Nagnath Par,

Pune – 411 030

: 020-24477990

Email : [email protected]

![Basel 3 & Implication[1]](https://img.pdfslide.us/doc/110x75/577d1e721a28ab4e1e8e9042/basel-3-implication1.jpg)