Embed Size (px)

Citation preview

1

Tax Evasion through Trade Intermediation: Evidence from Chinese Exporters

Xuepeng Liu†

Kennesaw State University

Huimin Shi†† Renmin University of China

Michael Ferrantinoξ

The World Bank

December 20, 2014

Abstract

Many production firms use intermediary trading firms to export indirectly. This paper

investigates the tax evasion motive through indirect trade, using Chinese export data at

transaction level. We provide strong evidence that, under the partial export VAT rebate

policy of China, production firms can effectively evade value-added taxes (VAT) by

under-reporting their selling prices to domestic intermediary trading firms, especially when

they sell differentiated products. The benefit of such an evasion can be as high as 17% of the

under-reported value. This tax evasion motive is estimated to have an economically

comparable and often larger effect on trade intermediation compared to factors examined in

other studies for Chinese exporters. Even for a moderate level of under-reporting, the revenue

loss is close to one billion U.S. dollars. We also find that such under-reporting behavior

through domestic intermediaries may be associated with cross-border evasion through

under-reporting export values to foreign partners. In addition, our result indicates that the

evasion motive is stronger for larger transactions.

Acknowledgement: We thank Carlos Ramirez, Mark Rider and the participants at the International and Development Economics Workshop at the Federal Reserve Atlanta,the North America Chinese Economists Society Meetings at Purdue University,and China Meeting of Econometric Society at Xiamen University for comments and suggestions. † Xuepeng Liu, Associate Professor of Economics, Department of Economics & Finance, Coles College of Business, Kennesaw State University (email: [email protected]). †† Huimin Shi (corresponding author), Assistant Professor of Economics, School of Economics, Renmin University of China (email: [email protected]). ξ Michael Ferrantino, Lead Economist, International Trade Department, the World Bank (email: [email protected]). Disclaimer: The findings, interpretations, and conclusions expressed in this paper are entirely those of the authors. They do not necessarily represent the views of the International Bank for Reconstruction and Development/World Bank and its affiliated organizations, or those of the Executive Directors of the World Bank or the governments they represent.

2

1. Introduction

Production firms can export directly by themselves or rely on intermediary trading

firms to export for them (indirect exports).1 Intermediary trading firms play an important role

in international trade. In the U.S., wholesale and retail firms account for about 11 percent and

24 percent of exports and imports respectively (Bernard et al., 2010). In the early 1980s, three

hundred Japanese trading firms (sogo shosha) handled 80 percent of Japanese trade (Rossman

1984). According to the data from China Customs, indirect exports in China accounted for 38

percent of the shipments and 21 percent of the value in the year of 2005. Despite the

extensive studies at firm level in the recent trade literature, the role of trading firms has not

been fully explored. This paper investigates the tax evasion motive behind indirect exports in

China, stemming from the partial export value-added tax (VAT) rebate policy.

In countries that adopt a destination-based VAT, including China, the VAT should be

collected on domestic transactions, but not on exports. The VAT on the value added at the

final stage before exporting should be exempted, and the previously paid input VAT should

be fully refunded in principle so that exporters can regain their initial competitiveness. Unlike

the full rebate policy in the EU and elsewhere, China has a partial rebate system with rebate

rates less than or at most equal to collection rates. The unrebated part of the VAT becomes

effectively an export tax,2 which is calculated based on the export prices for direct exporters

(production firms) but domestic purchasing prices for indirect exporters (trading firms).

To evade such an export tax, exporters have an incentive to under-report either their

export prices or domestic purchasing prices. 3 Direct exporters (production firms) may

directly evade the effective VAT by under-reporting its FOB price as long as they can find

foreign partners to collude in order to recover the loss due to under-reporting. Indirect

exporters (trading firms) may have an incentive to under-report their domestic purchasing

price to evade VAT; they also have an incentive to under-report export prices to minimize

purchasing-selling price differentials, which is used by the government to detect tax evasion.

Although foreign partners are also needed to recover the under-reported values, trading firms 1 Our focus is on the case where a production firm sells its products to an intermediary trading firm, with the trading firm taking charge of the tax rebate. Alternately, the intermediary’s main role may be to help a production firm to find buyers, while the production firm is still in charge of the tax rebate itself. We analyze the former case because we do not observe the latter case directly. 2 Feldstein and Krugman (1990) show that a destination-based VAT system should provide exporters full rebates and an incomplete rebate is equivalent to an export tax. 3 Ferrantino, Liu and Wang (2012) provide empirical evidence for how production firms may have incentive to under-report their export values in the case of direct exports, while the current paper investigates the evasion through indirect exporting. The evasion behaviors discussed in these papers are different from another popular type of VAT evasion by firms within a VAT-adopting country in which they over-report their input VAT using fake invoices to obtain more input VAT credits and hence reduce their VAT liabilities.

3

are more skilled to do so because they are normally larger, more politically connected, and

more familiar with foreign markets than production firms. As a result, it is relatively easier

for trading companies to under-report prices than production firms. This paper explores how

firms evade such an export tax through indirect exports.

The above discussion suggests a positive correlation between export tax rates (i.e., the

nonrefundable part of VAT) and probability of indirect exporting, which is measured by the

share of indirect exports in our product level analysis. That is, the higher the implicit export

tax, the more likely it is that exporting will be done through an intermediary. We test this

hypothesis using China Customs export data at the transaction level for the year 2005, which

is the first year after the full liberalization of trading rights under China’s WTO

commitments.4 This correlation is empirically robust, especially for differentiated products

whose values are easier to under-report than homogenous products, and is also stronger for

the exports of state-owned enterprises (SOEs), which are more politically connected with the

government than private or foreign firms.

As mentioned above, although the VAT rebate to a trading firm is not based on its

final export price, it may also have an incentive to under-report exporting prices to minimize

the chance of being caught. This is because the purchasing and selling price differential is

used by Chinese tax authorities to detect evasion behaviors. Such a view is supported by a

product-country level analysis. This implies that the tax evasion through domestic trading

firms may be associated with cross border evasion in the case of indirect exports. Therefore,

both types of evasion should be reflected in the under-reported export values and the data

reporting discrepancies between China and importing countries. The current paper provides a

complete explanation for the export price under-reporting by both direct and indirect

exporters, which in turn helps to explain why China reported exports are significantly smaller

than the corresponding imports reported by partner countries such as the U.S. The

fast-growing trade of China, especially its exports and large trade surplus, has drawn

increasing attention. Investigating the incentives behind the under-reporting of China’s

exports not only provide policy makers a clearer picture of China’s trade but also help

authorities to detect and curb evasion behaviors.

Although the scope of VAT evasion is usually considered to be small because this tax

4 We choose to use the data for year 2005 for the following reasons. First, before 2005, the export and import right was under the examination and approval system. Production firms would have to choose indirect exports if they did not have export right, which is unrelated to tax evasion. Second, two other related papers on Chinese intermediary firms, Ahn, Khandelwal, and Wei (2011) and Tang and Zhang (2012), also use the data of 2005. To facilitate the comparison with their work, we follow them by choosing the same year.

4

is imposed at every stage of production and it is difficult for all of the involved firms to

collude, our results suggest that the partial rebate policy can motivate firms to evade VAT.

We show how firms respond to tax incentives by choosing to export either directly or

indirectly through intermediaries. Anecdotal evidence shows that some production firms

export indirectly through trading companies or establish seemingly separate but actually

related trading companies simply to facilitate tax evasion. Such kinds of related transactions

are usually difficult to observe and to identify. The methodology in this paper provides

evidence that is consistent with such kinds of evasion behaviors. In fact, there are explicit

provisions in China for production companies to own and control trading intermediaries

(Ministry of Foreign Trade, 1999).5

Our estimate implies that, even for a moderate level of under-reporting (understating

the true value by one third), the revenue loss is close to one billion U.S. dollars, a sizable

amount. This is also how much tax revenue the government can potentially obtain in the

absence of such evasion. The evasion comes with a real cost over and beyond the tax revenue

loss. For instance, the evasion has implications for the ability of the Chinese government to

use variable VAT rebates as a policy instrument with various aims: promote high-technology

sectors, reduce energy/pollution/resource-intensive products, promote phasing out of obsolete

capital, reduce trade frictions, etc. It may be questioned a priori whether a single policy

instrument can bear the weight of being addressed to so many objectives simultaneously. Our

results imply that the effectiveness of variable VAT rebate rates as a policy instrument can be

undermined by widespread evasion of the VAT on the part of exporting firms. The policy

implications of this paper go beyond the specific context of tax evasion through trading firms

in China. In general, this paper shows that rational firms, motivated by certain benefits, may

change their export modes and organizational forms, which is otherwise unnecessary. Such

kind of unproductive behaviors come with significant social costs to governments and market

participants, especially in developing countries or countries in transition, like China.

The rest of the paper is organized as follows. We review the literature in Section 2. In

Section 3, we introduce the policy background of China’s export tax rebate and the tax

evasion mechanism. Section 4 discusses the empirical strategy and data. Section 5 presents

the empirical results. Robustness checks are provided in Section 6. And Section 7 concludes.

5 See Circular [2004] No. 14: “The Act of Foreign Trade Business Registration”. Before July 1, 2004, there are restrictions on establishing an intermediary trading firm by a production firm. After that date, China opened the export and import rights to both production firms and pure trading firms. Under this rule, production firms can establish the intermediary firm legally.

5

2. Literature review

Our paper is related to the recent literature on tax evasion in international trade and

trade intermediation. Tax evasion has been studied extensively in the public finance

literature.6 The review of the literature in the current paper focuses on tax evasion in

international trade. One thread of the existing papers in this area follows the approach

suggested by Fisman and Wei (2004), identifying the evasion behaviors based on a

correlation between tax or tariff rate and trade data reporting discrepancy (see also Javorcik

and Narciso, 2008; Mishra, Subramanian, and Topalova, 2008; and Ferrantino, Liu, and

Wang, 2008, among others). Another thread of related papers studies the transfer pricing

behaviors of multinational firms and how countries’ tax rates affect firms’ intra-firm trade

prices and trade flows (see, e.g., Swenson, 2001; Clausing, 2003 and 2006; Bernard, Jensen,

and Schott, 2006).

The current paper, however, proposes a completely different approach to identify

another evasion behavior, based on a correlation between unrefunded export VAT and tax

benefit to indirect exports compared to direct exports. To the best knowledge of ours, the

only existing paper investigating explicitly the role of trade intermediation in tax evasion is

Fisman, Moustakerski and Wei (2008), who find evidence that Hong Kong intermediaries

that re-export Chinese products help to facilitate tariff evasion, and the incentive to evade

tariffs increases with tariff rates. In their paper, the middlemen are trade intermediaries in

Hong Kong, helping foreign exporters (either production or trading firms) to evade Chinese

tariffs. Different from their paper, we study how trading companies may help domestic

production firms to evade value added taxes through arm-length transactions or disguised

intra-firm transfers. We add new evidence to the growing empirical literature on tax evasion

in international trade. The practice of using middlemen for purposes of tax avoidance (legal)

or tax evasion (illegal) and under-reporting trade values appears to exist throughout the world.

Thus, we believe that our findings are of more general relevance as well.

Much of the literature on trade intermediation focuses on the legitimate roles of

intermediaries or middlemen in trade, such as guaranteeing product quality, matching sellers

with buyers, liquidity provision, and contract enforcement. As Spulber (1996) puts it,

“Intermediaries, by setting prices, purchasing and sales decisions, managing inventories,

supplying information and coordinating transactions, provide the underlying microstructure

of most markets.” More recently, Feenstra and Hanson (2004) show that intermediary firms

6 See, e.g., Slemrod and Yitzhaki (2000) for a review of the literature on income tax evasion.

6

mitigate adverse selection by acting as guarantees of quality. Rauch and Watson (2004)

model the emergence of trade intermediaries as an outcome of search frictions and network in

international trade. Bernard et al. (2010) find a greater penetration of U.S. intermediate

exports into smaller markets and a larger dominance of wholesalers in agriculture-related

trade. Antras and Costinot (2011) study the welfare impact of trade liberalization in the form

of a reduction in search frictions with the help of intermediaries. Felbermayr and Jung (2011)

examine the effects of hold-up in trade intermediation in destination countries, emphasizing

the relationship specificity of the products. In addition, several recent papers find a positive

correlation between intermediated trade and various proxies for fixed trade costs (see, e.g.,

Bernard, Grazzi, and Tomasi, 2011; and Akerman, 2013).

Unlike previous papers, we investigate the tax evasion incentive behind trade

intermediation in China’s exports. To our best knowledge, our paper is the first in the

literature that investigates the dark side of firms’ choice of their export modes. It is closely

related to Ahn, Khandelwal, and Wei (2011) and Tang and Zhang (2012), both of which also

study trade intermediation in China’s exports, but have very different focuses from ours. Ahn,

Khandelwal, and Wei (2011) build a model in which firms with different productivity levels

endogenously select to export directly, indirectly, or do not export at all. In their model, the

most productive firms export directly; the firms with intermediate levels of productivity

export indirectly; and the rest of firms do not export. They also provide empirical evidence

that the intermediaries play a more important role in the markets that are more difficult to

penetrate. Tang and Zhang (2012) study the roles of the intermediaries in quality

differentiation and signaling. They test the story of quality verification by establishing a

model with heterogeneity in productivity. They distinguish horizontal differentiation, which

is the elasticity of substitution of consumers’ preference, from vertical differentiation, which

is the quality difference. Under the assumption that firms cannot write contracts ex ante to

specify the division of surplus between producer and intermediary, the investment by

intermediaries to investigate quality will be too low from the perspective of producers.

Because such under-investment is especially detrimental to high quality products, we should

expect to see a negative correlation between indirect exporting and vertical differentiation.

For product more horizontally differentiated (less substitutable), quality concern is less

important; so their model predicts a positive correlation between the prevalence of trade

intermediation and cross product horizontal differentiation, which is consistent with Feenstra

and Hanson (2004).

Finally, our paper is also related to a growing literature on China’s export VAT rebates.

7

Besides the several already mentioned papers on tax evasion, several other existing papers

study the effect of China’s export tax rebates on exports, e.g., Chao, Chou, and Yu (2001),

Chao, Yu, and Yu (2006), Chien, Mai, and Yu (2006), and Chandra and Long (2013),

Gourdon, Monjon, and Poncet (2014). These papers find a positive relationship between

rebate rates and exports, as what the policy was intended to do. Our paper is different from

these papers as we study how VAT rebates affect the modes of exports (direct or indirect),

instead of the level of exports.

3. Policy background and tax evasion mechanism

3.1. Export VAT rebate policies in China

Our findings exploit a feature of the Chinese VAT system. The VAT rebate rates for

exports in China vary across products and over time, unlike the case of a pure

destination-based VAT (e.g. that of the European Union). Since this feature of the system,

giving rise to a de facto variable export tax, is central to our results, some background on the

institutional framework is warranted.

Export tax rebates are a common practice in international trade. To avoid double

taxation, tax authorities usually return to exporters the indirect taxes (e.g., VAT) firms have

already paid in the production and distribution process. This practice is permitted under the

GATT/WTO, as long as the tax rebate rates are no higher than the actual collection rates. For

a long time, China has applied different taxes to domestic sales and foreign trade: domestic

sales are subject to VAT; exports are VAT-free (i.e., no VAT on the value added at the final

stage before exporting) and are usually eligible for rebates of previously paid input VAT;

imports sometimes are exempt from duties. As documented by Cui (2003), China

implemented the export tax rebate policy in 1985 and established the “full refund” principle

in 1988. After a major tax reform in 1994, the old industrial and commercial standard tax

(gong shang tong yi shui) was replaced with a new VAT system. In principle, the VAT paid

on previous paid inputs of exported products is supposed to be fully rebated. At first, tax

rebates increased dramatically with the surge in exports, but only for a brief time. Because

VAT refunds had been treated as a budgeted expenditure rather than as entitlements, the

central government, facing a budget shortfall, was forced to reduce the rebate rates twice in

1995 and 1996.7 To counter the negative impact of the 1997 Asian financial crisis and to

7 The central government was responsible for all the VAT rebates during 2000-2003. In 2004, the central government set the amount of tax rebates in 2003 as the benchmark; within the benchmark, the central

8

promote exports, China increased the export tax rebates for various products nine times from

1998 to 1999. In recent years, China has adjusted the rebate rates frequently, especially since

2004.8 Variations in the rebate have been employed for multiple policy objectives; for

example as an industrial policy (e.g. to encourage high-tech sectors or discourage polluting

sectors) or to manage trade frictions (address foreign calls for appreciation of the yuan9 or

frequent anti-dumping investigations affecting Chinese exports). This use of the varying VAT

rebate causes China’s VAT to depart from a pure destination-based system. It also gives rise

to the variation in the tax rate we are able to exploit.

Since 2002, the most common method of export tax rebate for direct exporters or

production firms is called “Exemption, Credit, and Refund (ECR)”.10 “Exemption” means

that export sales are exempt from output VAT. “Credit” means that input VAT on raw

materials and supplies used for production can be credited against the output VAT on

domestic sales. “Refund” means that the excess amount of input VAT over the output VAT

will be rebated until a threshold, usually export value times rebate rate, is met. For

intermediary trading firms, the method is called “Exemption and Refund”: exemption means

the same thing as in the case of ECR, and refund refers to the rebate of previously paid VAT

on domestic purchases. Another difference between direct and indirect exports, which is

critical to our analysis, is that the rebate to a direct exporter is based on its export FOB price,

while the rebate to a trading firm is based on its domestic purchasing price.11

The rebate policies also differ across customs regimes.12 China has two major types of

customs regimes: normal trade and processing trade. Normal trade refers to imports intended

for domestic markets and exports using mainly local inputs. Processing trade refers to the

business activity of importing all or part of the inputs from abroad duty-free, and then

exporting the finished products after processing or assembly. It includes processing with

government is still responsible for all the rebates; beyond the benchmark, local governments share 25% of the rebate burden, which was adjusted to 7.5% in 2005. 8 See Circular [2003] No. 222: “Notice of Adjusting Export Tax Rebate Rates,” issued jointly by the Ministry of Finance and the State Administration of Taxation in October 2003. 9 See the following link for an interview with Chinese economist Lin, Yifu (former Chief Economist of the World Bank). http://english.people.com.cn/200310/05/eng20031005_125408.shtml. He said explicitly that abolishing or cutting tax rebates to Chinese exporters would help relieve the pressure for appreciation of Yuan. 10 For a more detailed description of this method, see Circular [2002] No. 7: “Notice of Further Implementing the ‘Exemption, Credit and Refund’ System of Export Tax Rebates,” issued jointly by the Ministry of Finance and the State Administration of Taxation in October 2002. 11 Because a trading firm does not pay VAT on its mark-up or value-added (if any), domestic purchasing price rather than export price is used to calculate rebate. 12 See Circular [1994] No. 31: “Notice of Printing and Distributing the Methods of Tax Refund (Exemption) for Exported Goods,” issued by the State Administration of Taxation in 1994. It is still in force according to the official Chinese central government website: http://www.gov.cn/gongbao/content/2011/content_1825138.htm

9

supplied materials and processing with imported materials.13 Firms under normal trade

regime need to pay VAT on inputs purchased in China or imported abroad, and are qualified

for rebates when exporting their final products. Processing firms can import inputs duty-free;

they will not get tax rebate on imported inputs since they do not pay the taxes in the first

place. For the inputs purchased domestically within China, the rebate policies are different

for different types of processing firms. Similar to exporters under the normal trade regime,

processing firms with imported materials, after completing their export process in China, can

obtain at least partial rebates according to the ECR method. By contrast, the “no collection

and no refund” VAT policy applies to processing trade with supplied materials; this means

that no output VAT is collected and they are not qualified for input VAT rebates either.14

This implies that export VAT evasion is less relevant to processing firms with supplied

materials. For this reason, we leave out this type of processing trade and many other minor

types of regimes out of our data used for the subsequent empirical analysis, and keep only

normal trade regime and processing trade with imported materials, to which the ECR rebate

method applies.

3.2. Tax evasion through indirect exports and main hypotheses

Because we do not observe the domestic purchasing price when a trading firm buys

products from a producer in the customs data, we cannot test our hypothesis based on the

price differential. Instead, we identify the evasion behaviors by examining the correlation

between export tax rates and the probability of indirect exports. In the following, we explain

the benefits and costs of this type of evasion and propose the testable hypotheses.

We assume that a production firm A can directly export a certain amount of goods at an

FOB value of X; 푡 is the VAT rate; and 푟 is the VAT tax rebate rate. Under the ECR

method, the total amount of tax burden firm A bears for this transaction is 푋(푡 − 푟).15

Instead of exporting directly, production firm A may sell the same shipment to firm B,

an intermediary trading firm, at the value of Y (VAT included). The amount of VAT firm B

pays to A should be 푡 ∗ 푌/(1 + 푡), which is included in B’s purchasing value of Y. We

13 The major difference between them is that local firms in processing with supplied materials are pure processors without obtaining the ownership of the supplied materials or final goods. In comparison, local firms in processing with imported materials obtain the ownership of the imported materials and are responsible for exporting the finished goods. 14 Another VAT method in China is “Refund After Collection”: collect the VAT first on exports and refund later. This method, rarely used after 2002, is less relevant to our analysis which covers year 2005. 15 The exact formula for VAT liabilities is more complicated when a firm also sells in China, but here we consider only the part relevant to exports. See Ferrantino, Liu, and Wang (2008), and Liu (2013) for additional discussion on China’s export VAT rebate calculation.

10

denote the net of VAT domestic purchasing price as 푋 = 푌/(1 + 푡). The trading firm B does

not pay VAT when exporting, and can get a VAT rebate calculated as 푋 × 푟.16 Therefore,

the total amount of export tax burden on this transaction is 푋 × (푡 − 푟).

To evade taxes, firms may under-report X or 푋. In the case of indirect exporting of the

products produced by firm A through a trading firm B, we also use X to denote the export

value firm A would otherwise report under the hypothetical scenario of direct exporting,

which can be different from trading firm B’s export FOB price Xind, where the subscript ind

denotes indirect exporting. A direct exporter (production firm) may under-report X for tax

evasion purpose if it has a foreign partner to collude to recover later the losses due to export

price under-reporting.17 A trading firm, when under-reporting its domestic purchasing price,

may also under-report export value Xi to reduce the purchasing and selling price differential

as discussed later.

Although both 푋 and X may be understated, we believe that 푋 is generally more

likely to be under-reported than X for two reasons. First, it is arguably easier for firms to

under-report 푋 domestically than under-reporting the export price X, for which firms need to

find foreign partners to collude. Second, trading companies are usually larger and more

familiar with foreign markets than production firms, so they are more likely to under-report

export prices than direct exporters, which in turns helps to explain why trading firms are also

more likely to under-report their domestic purchasing price 푋 without worrying too much

about the purchasing and selling price differentials. In other words, firms are less likely to

under-report export price X when exporting directly, but are more likely to under-report the

domestic purchasing price 푋 (and export price Xind) when exporting indirectly. Hence, 푋 in

general is expected to be smaller than X, the export value a firm would report when exporting

directly.18

Taking the export tax burden in both cases together, we can write the joint tax benefit to

16 The rebates for trading firms are based on their purchasing price Y or 푋, rather than their exporting price. See Circular [1994] 31: “Notice on the Issuance of the Methods of Export Tax Refund (Exemption),” issued by the State Administration of Taxation in 1994; and Circular [2004] 64: “Notice on the Issues of the Managing Export Tax Refund (Exemption),” issued by the State Administration of Taxation in 2004. 17 As an illustrative example, the foreign partner (importer) may agree to remit a fraction of the true purchasing price directly to the exporter, causing an understatement for tax purposes, and place the rest in an offshore account for the benefit of the exporter. The balance in the offshore account can either be repatriated in a second, possibly concealed, transaction or used for such expenses as foreign education of the exporter’s children. Another example is transfer pricing, a tax evasion scheme to shift income from high tax locations to low tax locations through manipulating trading prices within a multinational firm. 18 For a trading firm, its export selling price can be larger than its domestic purchasing price for legitimate (e.g., markup, and/or compensation for packaging and labeling services, and/or the provision of quality guarantee) or illegitimate reasons (e.g., tax evasion). The latter is what we consider in this paper.

11

firms A and B from indirect exporting as follows (compared to the hypothetical case of direct

exporting by firm A).

퐵푒푛푒푓푖푡 = 푋(푡 − 푟) − 푋(푡 − 푟) = (푋 − 푋)(푡 − 푟) (1)

If X is larger than 푋 for reasons discussed earlier, the benefit will be positive as long as

t > r. When 푡 = 푟, 퐵푒푛푒푓푖푡 = 0. In other words, exporting through intermediary trading

firm brings no benefit when export tax rate (t-r) is zero. This benefit is always non-negative

because r is no higher than t. If we express 푋 = 푢푋 as a proportion of X, where 0 ≤ 푢 ≤ 1

measuring the ratio of the reported value to the true value (lower u means a larger degree of

under-reporting), we can rewrite Equation (1) as follows:

퐵푒푛푒푓푖푡 = (1 − 푢)(푡 − 푟)푋 (2)

Tax evasion not only can bring benefits to firms, but also can incur penalty when they

get caught. The more taxes a firm evade, usually the heavier the penalty will be. The

Criminal Law of China19 has a specific article on the crime of defrauding national export tax

rebates and tax evasion (Article 204): “those evading a large amount of export VAT rebates

through false-reporting exports or other fraudulent means will be subject to up to five years

of imprisonment or criminal detention and a fine of one to five times of the defrauded tax

amount; those defrauding a huge amount of tax or belonging to other serious circumstances

will be subject to five to ten years of imprisonment and a fine of one to five times of the

defrauded tax amount; those defrauding an especially huge amount of tax or belonging to

other especially serious circumstances will be subject to at least ten years of term

imprisonment or life imprisonment, and a fine of one to five times of the amount defrauded

or confiscation of property.” In addition, the State Administration of Taxation issued a

circular on some general rules of tax evaluation in March 2005.20 In January 2007, the State

Administration of Taxation issued another circular specifically about the evaluation of tax

rebates.21 There are five categories of indicators for the intermediary trading firms: export

price, export growth rate, domestic flow of export products, customs office, and unclaimed

tax rebate. Under the export price category, two of indicators the government considers are

purchasing price differential (PPD) and purchasing and selling price differential (PSD),

among others.

19 The new criminal law of 1997, vis-à-vis the old law of 1979, was distributed on March 14, 1997, and came into force from October 1, 1999. So the new law applies to our sample year 2005. 20 See Circular [2005] No. 43, “The Notice on Issuance of the ‘The Administrative Measures of Tax Assessment (Trial)”, the State Administration of Taxation of China in 2005. 21 See Circular [2007] No. 4, “The Notice on Strengthening the Assessment of Export Tax Rebates (Exemption)”, the State Administration of Taxation of China.

12

PPD = 100%*(Purchasing Price - Average Purchasing Price)/Average Purchasing Price

PSD = 100%*(Export Price - Purchasing Price)/Purchasing Price

Here the average price, used as a reference price level, means the average of all the

prices within a particular industry. The larger are these price differentials or the extent of

under-reporting, the more likely a tax evading firm will be caught. The purchasing price is 푋

as in Equation (2), while the export price and average purchasing price can be reasonably

considered a proxy for 푋, the “true” value.22 The above laws and rules suggest that the

penalty is proportional to (푋 − 푋) or (1 − 푢)푋. Therefore, we can write the net benefit of tax

evasion through intermediaries as follows:

∆= (1 − 푢)(푡 − 푟)푋 − 푏(1 − 푢)푋 = (1 − 푢)(푡 − 푟 − 푏)푋 (3) where b is a penalty parameter, which can vary with firm or product characteristics.23 A

couple of notes on b are in order here. First, some of the supervision rules actually came into

force after 2005, the year covered by our analysis. This is not necessarily a problem because

b captures not just the above-mentioned government supervision. Even before this particular

policy came into force, other factors could still influence the cost (e.g., the above-mentioned

Criminal Law) or at least the perceived cost of evasion. For example, if a firm consider it

unsafe to under-report the price of homogenous goods such as wheat or rice, it will be less

likely to do so even without an explicit supervision policy in place. Second, there are

certainly other benefits or costs firms would consider when they decide to export directly or

indirectly. For example, one important factor behind exporting directly is to save the fixed

cost of direct exporting. Here, we choose to simplify away all of the other benefits or costs

resulting from choosing direct or indirect export modes. This simplification is not a problem

because the other benefits or costs are unlikely related to export tax.

If we ignore all of other benefits or costs related to indirect exports, the probability of a

firm choosing to export indirectly can be written as follows:

푃푟표푏(푖푛푑푖푟푒푐푡 푒푥푝표푟푡) = 푃푟표푏(∆> 0) = 푃[(푡 − 푟) > 푏] (4) In our empirical analysis, the probability of indirect export is captured by a continuous

measure of the share of indirect exports in total exports for each product. For a given b, the

larger (푡 − 푟) is, the stronger is the motive of exporting through trading firm. Hence, we have

22 The comparison between a firm’s price with the average industrial level price is a useful indicator. Alternatively, the differential between a trading firm’s own purchasing and selling prices may also be used, but it can be rendered ineffective if the firm under-reports both of its purchasing and selling (export) prices. 23 b measures the expected level of punishment, determined by the probability of a firm being caught and the level of punishment once it gets caught. Because we cannot distinguish the two from each other in our empirical analysis, we simply take b as the expected level of punishment. For a rational exporter, b should be between 0 and 1.

13

the following hypothesis:

HYPOTHESIS 1 The probability of exporting indirectly should be higher in industries

facing larger unrebated export VAT rates (i.e., t-r).

Equation (3) also suggests that a production firm is more likely to choose to export

indirectly when b (the degree of penalty) is lower. For example, the probability of evasion

through indirect exporting would be higher when they are unlikely to be caught or unlikely to

be heavily penalized (b is small). In addition, a marginal increase in (t-r) will be more likely

to make a difference in determining firms’ choice of export modes when b is low. On the

contrary, when b is high, the condition in Equation (4) will be less likely to hold and a small

increase in (t-r) may not change firms’ choices of export modes. Hence we have another

hypothesis as follows:

HYPOTHESIS 2 The tax evasion motive through indirect exports should be higher

when the firms are less likely to be penalized for such behaviors, ceteris paribus.

We previously mention that the benefit in Equations (1) and (2) should be non-negative.

The same is true for the net benefit in Equation (3). If (푡 − 푟) > b, then the net benefit is

positive and a production firm will choose to export indirectly to evade taxes. If (푡 − 푟) ≤ 푏,

then the net benefit will be censored at zero (not negative) because the production firm will

not export indirectly for tax evasion purpose. Therefore, we can just consider the case when

(푡 − 푟) > 푏, and the production firm exports indirectly for tax evasion purpose. When the

benefit is bounded below by zero, a larger transaction value (X) can only increase the benefit

from the evasion through intermediaries. Moreover, if we also consider the fixed cost of

evasion, a production firm will export indirectly only if the net tax benefit (∆) as in Equation

(3) exceeds the fixed cost, ceteris paribus. Because the net benefit increases with X, we have

the following hypothesis, which can be tested using transaction level data rather than HS8

product level data.

HYPOTHESIS 3 The tax evasion motive through indirect exports should be higher for

larger transactions (larger X).

14

4. Empirical strategy and data

4.1. Empirical strategy

We aim to examine empirically how export VAT taxes affect indirect exports. The

dependent variable is the indirect export share, measured in both conservative and liberal

versions as defined later in Section 4.2. For explanatory variables, we have the data on export

VAT tax rates (t-r), the shares of exports by firm ownership types, and trade regimes (normal

or processing trade). As control variables, we include prc_sh (share of exports under

processing trade with imported materials), taking share of exports under normal trade as the

omitted variable; we also include collpriv_sh (share of exports by collective and private firms)

and for_sh (share of exports by foreign firms), with the share of exports by SOEs as the

omitted variable. The share of processing trade can also help to control for the value-added

content of a product as processing trade with imported materials is usually associated with

lower share of domestic value added contents. For simplicity, all of the other minor types of

trade regimes and ownership types are left out of our data.

Because China applies the same VAT rebate rate on a product exported to all of the

destination countries, we are able to test the tax evasion hypothesis using data at product level

without importing countries’ information. Our benchmark regressions will be carried out at

the HS 8-digit product level (HS8) at test the first two hypotheses, using the following

specification:

iii eZrtshindirect γ)(_ 10 (5)

where the subscript i denotes the Harmonized System (HS, version 2002) 8-digit product24; Z

is a vector of control variables including trade regime and firm ownership type variables,

measures of product differentiation, etc.; γ is the coefficient vector for Z; and ei is the error

term.

To test the second hypothesis, we examine how the tax evasion motive varies with

product and firm characteristics. Similar to Javorcik and Narciso (2008) and Mishra,

Subramanian, and Topalova (2008), we argue that evasion through price under-reporting

might be easier for differentiated products than homogenous products whose prices are often

standard. Rauch (1999) defines homogeneous goods as products whose price is set on

organized exchanges, defines reference priced goods as those not traded on organized

24 The Harmonized System, as agreed by the World Customs Organization, is standardized at the 6-digit level (HS6). HS8 here refers to the local tariff-line implementation of the HS by China Customs, which differentiates products and duties at a finer level.

15

exchanges but possessing a benchmark price, and defines the goods whose price is not set on

organized exchanges and which lack a reference price because of their intrinsic features as

differentiated products. We would expect to find stronger support for the evasion hypothesis

from differentiated products, while weaker evidence from referenced and especially

homogenous products. We will run regressions for different subsamples grouped based on the

level of product differentiation or include interaction terms between export tax rate and the

trade regime and firm ownership type variables.25

4.2. Customs trade data

The shipment level trade data of China are released by the China Customs Office. It is

organized monthly based on the shipment documents that firms submit to the corresponding

customs offices. In our paper, we use only the information of destination/source country, HS

8-digit product codes, firm IDs, firm names, trade regimes, ownership types, and the values

of the shipments. As a commitment made under the WTO, the Chinese government fully

opened export and import rights to all firms since the mid of 2004.26 Under the new system,

all firms can export regardless of their sales, ownership types, and ages. For this reason, we

use only 2005 data in our analysis, not the data before 2005.

In the data, China Customs does not directly distinguish the production firms from the

intermediary trading firms, but firms’ Chinese names include the words like “Jinchukou”,

“Jingmao”, “Maoyi”, “Waimao”, “Kemao”, “Waijing”, and “Gong Mao”. Ahn, Khandelwal,

and Wei (2011) classify all of them except “Gongmao” as trading firms, while Tang and

Zhang (2012) include also “Gongmao”.27 Following them, we also use these keywords to

identify trading firms and create two measures: a conservative measure as in Ahn, Khandelwal,

and Wei (2011); and a liberal measure as in Tang and Zhang (2012). In 2005, the share of

indirect exports among total exports in China is about 20% based on the conservative

definition of indirect exports (21%, based on the liberal definition). Because the average size

of shipments tends to be smaller for indirect exports than that for direct exports, the 25 The different findings from homogenous and differentiated products can also help to invalidate alternative interpretations other than tax evasion. For instance, in a standard Melitz-type model, higher export tax rates would reduce profits from direct exporting, making indirect exporting relatively more profitable. In terms of Ahn, Khandelwal, and Wei (2011), this means that the cutoff productivity level for direct exporting increases, and thus indirect export share also increases. Although our empirical findings of a positive correlation between unrebated VAT rates and indirect exports share are also consistent with the productivity sorting mechanism, this mechanism cannot explain the stronger support from differentiated products. 26 See Circular [2003] 1019 , “Forwarding the Notice of Adjusting the Export and Import Eligibility Criteria and Approval Procedures by Ministry of Finance” issued by the State Administration of Taxation of China in 2003. The registration method started from July 1, 2004. 27 Gongmao firms, also involved in the design and production of their products, are not pure intermediary trading companies.

16

corresponding shares are larger in terms of the number of shipments: 37% and 38% based on

the conservative and liberal measures of trading firms respectively. In sum, indirect exports

constitute a large percentage of Chinese exports in 2005.

There are sixteen types of trade regimes in the trade data from China Customs, but we

consider only normal trade and processing trade with imported materials.28 We leave out the

processing trade with supplied materials for reasons discussed in Section 3.1 and all of the

other thirteen trade regimes when calculating the shares by trade regimes. 29 This is

acceptable because the export values under most of the other regimes are very small, and we

have limited information on the policies applied to these trade regimes. Eventually, we only

have two types of trade regimes in the product-level analysis: normal trade and processing

trade with imported materials whose shares sum to one for each HS 8-digit product.

In total, there are seven firm types in the 2005 data, including three types of domestic

firms (state-owned enterprises, collective firms, and private firms), three types of foreign

firms (equity joint ventures, contractual joint ventures, and wholly foreign-owned enterprises)

and a category for all of the other types. To simplify the analysis, we combine collective with

private firms, and combine the three foreign firm types together, but leave out all the other

types when calculating the shares of exports by SOEs, collective and private firms, and

foreign firms (soe_sh, collpriv_sh, and for_share). The three shares sum to one.

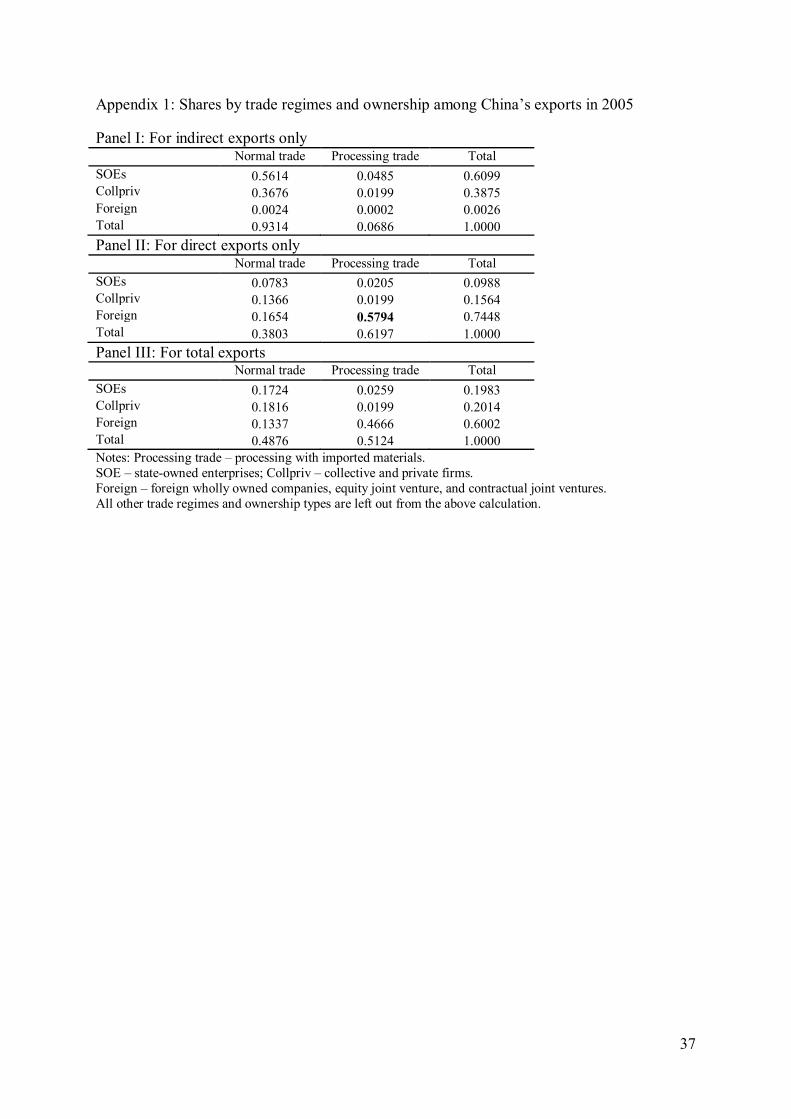

Appendix 1 provides a cross-tabulation of China’s exports in 2005 by trade regimes and

ownership types for indirect, direct, and total exports respectively. Panel I shows that Chinese

indirect exports are dominated by normal exporters, whose share accounts for 93% of the

total indirect exports in 2005. In terms of the firm ownership, indirect exporters are almost

completely domestic firms (61% for SOEs and 39% for collective and private firms), with

foreign firms accounting for a negligible share (0.26%). By comparison, Panel II shows that

the direct exports are dominated by foreign firms and processing trade. These facts help to

explain the empirical results reported later. For total exports, Panel III suggests that normal

trade and processing trade are overall equally important, and foreign firms play a larger role

than domestic firms in China’s 2005 exports.

The trade regimes of exports are strictly supervised by the Customs, and do not change

regardless of the export modes (direct or indirect exports). However, the ownership of an

28 The other 16 trade regimes are: entrepôt trade by bonded areas, international aid, donation by overseas Chinese, compensation trade, goods on consignment, border trade, equipment for processing trade, goods for foreign contracted project, goods on lease, equipment investment by foreign-invested enterprise, outward processing, barter trade, duty-free commodity, warehousing trade, equipment imported into EPZs, and others. 29 The results are very similar when only normal and processing exports are used for the dependent variables.

17

intermediary trading company can be different from the ownerships of the producers of the

exported products, so the shares by ownership types of indirect exports may not reflect

correctly the production structure of exported products in their production process. Keeping

this mind, we should be cautious when using the ownership variables and interpreting the

results. With no access to better measures, we believe that they can still provide useful

information and choose to include these ownership variables in our empirical analysis.30

4.3. VAT rebate rate and other data

The VAT rebate rates data are from the State Administration of Taxation. The data are

available at the tariff-line level. There are many rate changes in the middle of a year. If a

product has multiple rates in 2005, we use their average rates weighted by the number of days

during which each rate applies. The more detailed information at levels higher than HS

8-digit is averaged first to the HS 8-digit level. The major VAT rebate rates (r) in 2005 are 0%

(3.87%), 5% (9%), 13% (72.3%), and 17% (7%), with the shares of the HS 8-digit product

lines under each rebate rate in parentheses. The corresponding figures for statutory VAT

collection rates (t) for normal tax payers are 13% (13.3%) and 17% (84.3%). The major rates

for the tax net of rebate (t-r) are 0% (7.5%), 4% (70.5), 8% (11.1%), and 17% (3.4%). In line

with the WTO rules, the VAT rebate rates are always no higher than the collection rates.

The data used in our country-product level and transaction level analysis will be

described in Sections 5.2 and 5.3 respectively. Other variables used in the robustness checks

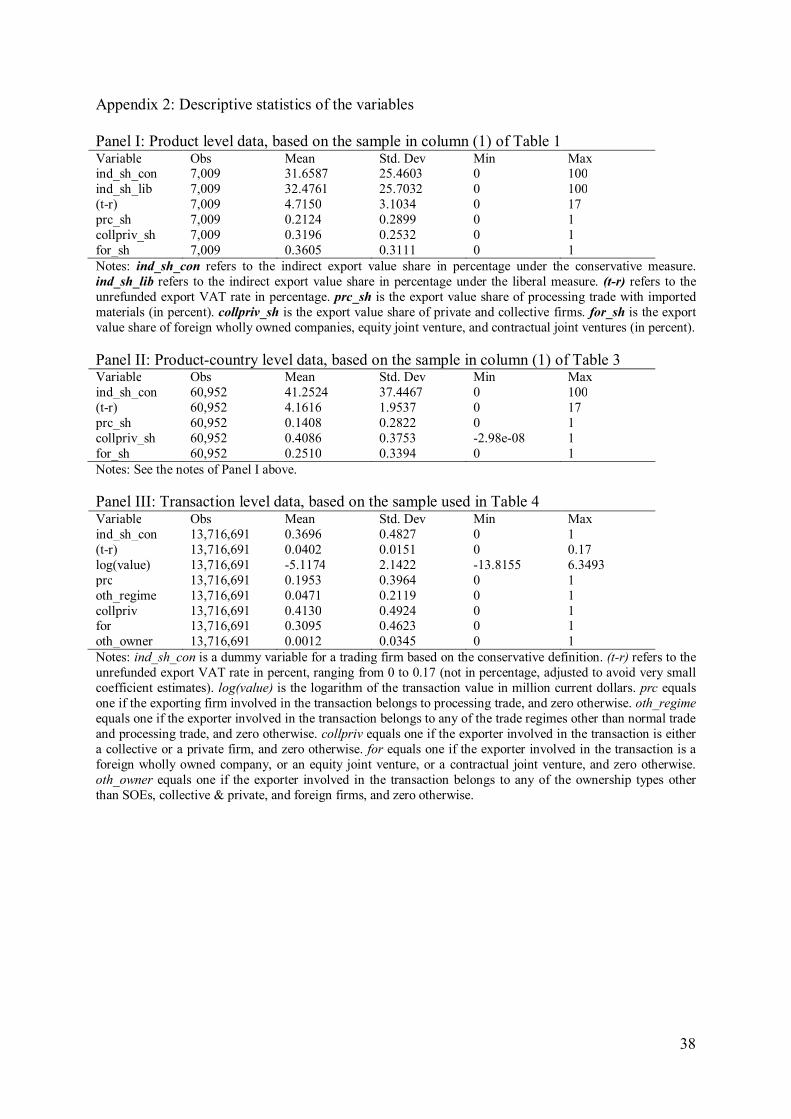

will be discussed in Section 6. Appendix 2 lists some descriptive statistics of the variables

used in the paper.

5. Empirical results

5.1. A product level analysis

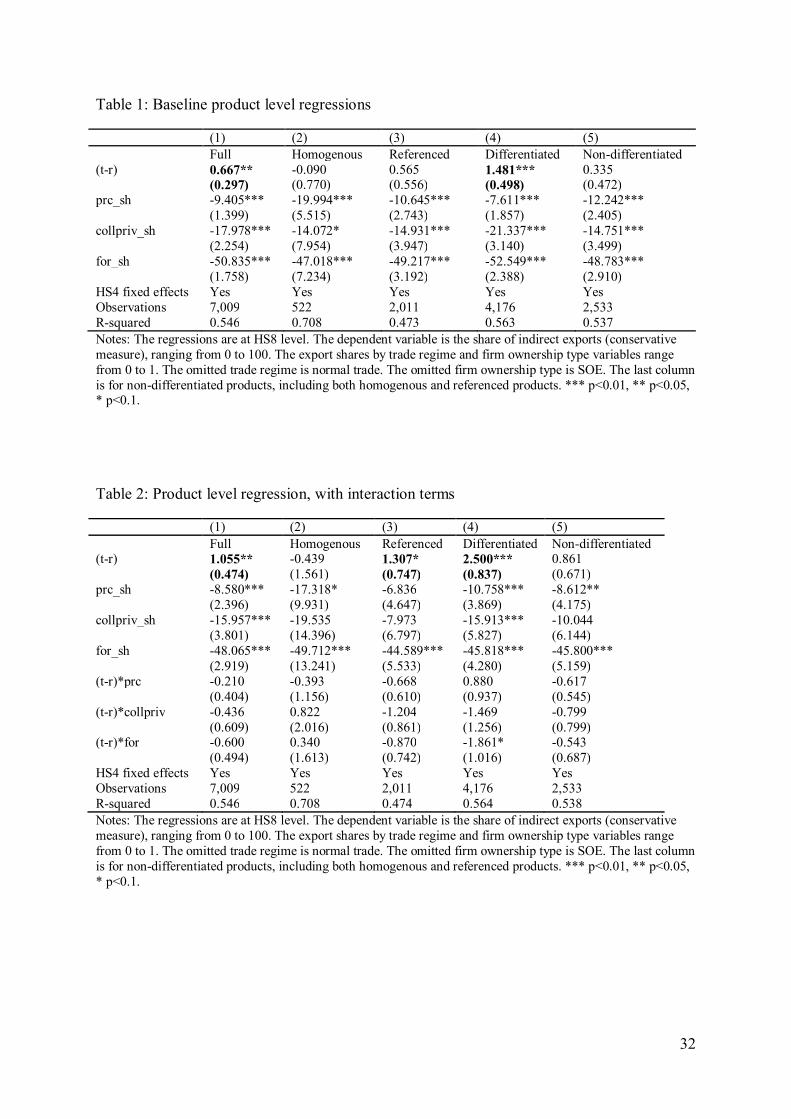

Table 1 reports the baseline regression results at the HS8 level, using the conservative

measure of indirect export share as the dependent variable. Because our key variable of

interest, (t-r), is at HS 8-digit level and we have the data only for year 2005, we cannot

30 It is tempting to calculate ownership shares based only on direct exports. Implicitly, this method assumes that the ownership structure of the products exported indirectly is the same as that of directly exported products. If this assumption is correct, then the ownership shares should not affect the indirect export shares and hence should not be included in the regressions in the first place. If the production structures are different for directly and indirectly exported products, then using the ownership based only on direct exporters will also be problematic. This is why we continue to calculate ownership shares based on total exports. Dropping these ownership variables from our regressions does not affect our main findings at all.

18

include HS8 product fixed effects. Nevertheless, we always include HS 4-digit level fixed

effects to control for any unobserved heterogeneity at HS4 level (about 1300 products).31 In

most tables (except Table 4 on transaction level analysis), the dependent variable is the share

of indirect exports, ranging from 0 to 100; (t-r) is also measured in percentage point, ranging

from 0 to 17. But the export shares by trade regime and firm ownership type are measured in

percent, between 0 and 1. The omitted trade regime is normal trade. The omitted firm type is

SOE.

The first regression uses the full sample, while the next three regressions use the

subsamples of homogenous, referenced, and differentiated products respectively according to

the Rauch’s product classification.32 In the last column, we combine homogenous with

referenced products, and call them together non-differentiated products. The estimated

coefficient of (t-r) is positive and significant at the 5% level in the regressions using the full

sample, supporting our Hypothesis 1. For regressions based on subsamples, the coefficient of

(t-r) is positive and significant only for differentiated products, but insignificant for

homogenous and referenced products. In addition, the estimated coefficient is much larger for

differentiated products in absolute value (-1.481). The result that (t-r) is positive and

significant only for differentiated products but not for other products supports our second

hypothesis. Finally, in the last column, we combine homogenous with referenced products to

increase the number of observations and find that the coefficient of (t-r) is still highly

insignificant, suggesting that the insignificant result in Columns (2) and (3) are not simply

driven by smaller observations.

Our estimates also imply that the impact of avoidance behavior is economically

significant. The estimate reported in Column (4) implies that a one standard deviation

increase in (t-r), which is 3.1 as shown in Appendix 2 (Panel I), would lead to about a 7.76

percentage increase in the indirect export share of differentiated products; when a

differentiated product changes from zero export tax to a full 17% tax, its indirect export share

would increase by 25.5%. Even if we use the point estimate in Column (1) of Table 1 for the

full sample, one standard deviation change in (t-r) can increase indirect export share by 4.6

percentage point. The magnitude is comparable to those estimated for factors in other papers.

For example, Tang and Zhang (2012) show that one standard deviation change in various

31 We do not use HS6 fixed effects because only about 8% of the HS6 products lines have more than two HS8 lines. Including HS6 fixed effects would be too demanding because they would absorb most of the variations in (t-r). 32 We concord the original liberal measure of Rauch’s classification at 4-digit SITC level to HS 6-digit level, and then to HS 8-digit level.

19

vertical or horizontal product differentiation measures leads to about 4 to 8.5 percentage

change in indirect export share. We can also compare our estimates to the effects of some

country characteristics estimated by Ahn, Khandelwal, and Wei (2011), although it is less

comparable due to different regression design. Following their specification, we have tried

including (t-r) in logarithm; the results show that one percent change in (t-r) raises indirect

export share by about 5 percentage point (for the full sample) or 8.2 percentage point (for

differentiated goods). In their Table 6, they show that one log point or percent change in

geographic distance and market size can lead to about 2 to 3 percentage point change in

indirect export share. The effects of some other factors examined by Ahn, Khandelwal, and

Wei (2011), such as ethically Chinese population and MFN tariff rate, are even smaller. In

sum, export tax is estimated to have an economically comparable and often larger effect on

trade intermediation compared to factors examined in other studies.

We can also show the potential tax revenue loss from evasion through trade

intermediation, as a back-of-envelope calculation. Using Equation (3) and assuming away the

penalty of evasion (b) for now, the tax benefit to firms or revenue loss to government is

(1-u)*(t-r)*X, where X refers to the expected value of indirect export value for tax evasion

purpose. To estimate X, we first calculate the probability of indirect export for tax evasion

purpose as the product of the coefficient estimate for differentiated products (i.e., 1.5

percentage points increase for a percentage increase in export tax) and export tax rate, and

then multiply this probability by the total export value (direct plus indirect export) for each

differentiated product. Using Equation (3) and assuming u = 0, the estimated revenue loss for

all of the differentiated products can be as large as 2.73 billion U.S. dollars in 2005. Even for

a moderate level of under-reporting (let’s say u = 2/3, implying that the true transaction value

is under-reported by 1/3), the revenue loss is close to one billion U.S. dollars, a sizable

amount. This is also how much tax revenue the government can potentially obtain in the

absence of such an evasion.

The results in Table 1 also suggest that processing firms, already teamed up with

foreign partners, are significantly less likely to export indirectly compared to normal firms

(the default category). Collective, private, and especially foreign firms are less likely to

export indirectly as compared to state-owned firms (the omitted category). These results can

also reflect partly the entry rules of the intermediary firms imposed by the government. It was

much more difficult to establish a foreign or private trading firm than a SOE trading company

for a long time. Even after the relaxation of the entry policy in 2004, the SOE share of

intermediary trading firms remained much higher than that of the production firms for a while.

20

In addition, foreign firms usually export directly because the fixed cost of direct exporting is

low due to their close connections to foreign markets and they may be more capable of

evading taxes through other means such as transfer pricing through intra-firm transactions.

Considering that exporters belonging to different trade regimes and ownership types

may have different levels of evasion incentive, we include in the regressions on Table 2 the

interaction terms between (t-r) and the shares by trade regimes and firm ownership types. The

regressions in Table 2 are analogous to those in Table 1, except that we include these

interaction terms. These interaction terms are mostly negative but almost always insignificant

at the 10% level. Although the results suggest that processing firms and non-SOE firms seem

to be less likely to evade taxes through intermediaries than normal and SOE firms (the default

category), the evidence is weak. Because these interaction terms are mostly insignificant, we

do not include them in our baseline regressions.

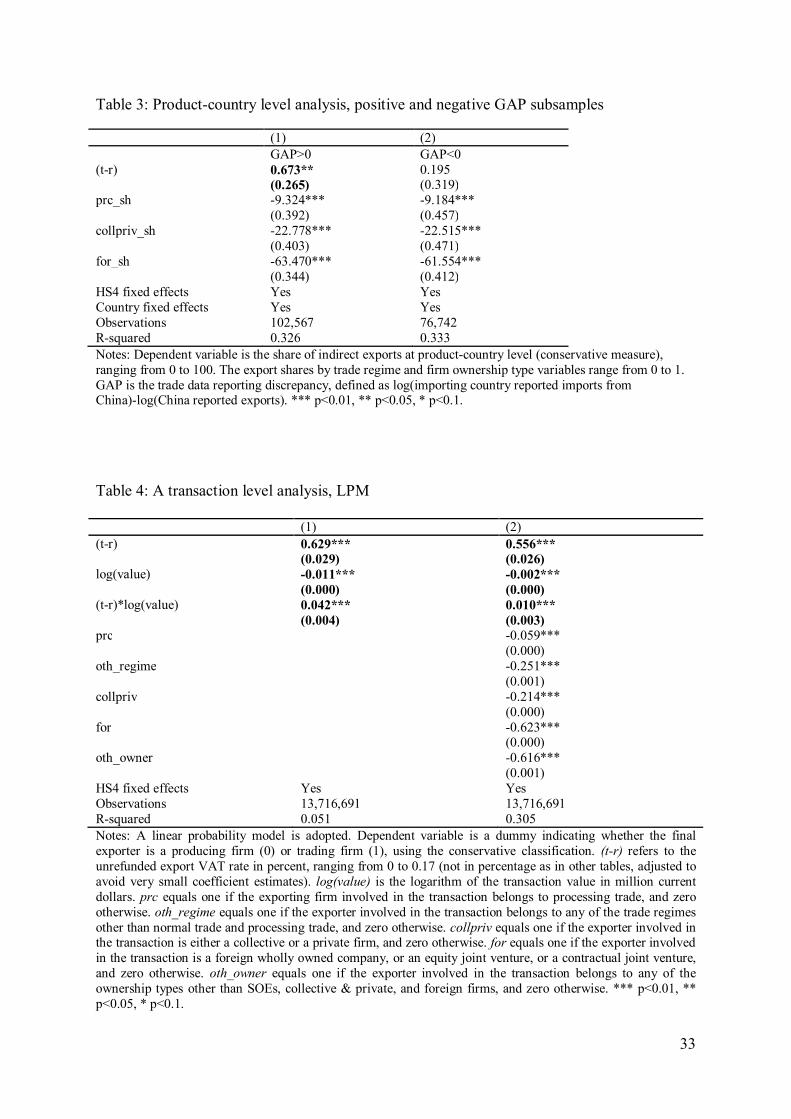

5.2. A product-country level analysis: domestic evasion and cross-border evasion

In this subsection, we instead examine whether domestic evasion and cross-border

evasion are linked to each other. As discussed above, one of the criteria Chinese tax

authorities adopt to detect evasion behaviors is based on purchasing and selling price

differential (PSD). As a result, trading companies that have purchased products from

production firms at an under-reported price (i.e., domestic evasion) will also have an

incentive to under-report export prices (i.e., cross-border evasion), to avoid large PSD and

minimize the chance of being caught.

Following the approach proposed by Fisman and Wei (2004), we calculate the

discrepancies between China reported exports to each importing countries in logarithms and

partner country reported imports from China in logarithms at HS 6-digit level for year 2005,

using the trade data from the UN COMTRADE (i.e., GAP = log(partner reported imports

from China) – log(China reported export). When export values are under-reported at Chinese

border, GAP tends to be positive. If the evasion through under-reporting domestic purchasing

price of a trading company is associated with its cross-border evasion through

under-reporting export prices, we would expect to see stronger evidence of tax evasion

through indirect exports for products whose values were under-reported at the Chinese border

(positive GAP). To test this hypothesis, we carry out a product-country level analysis.

Many characteristics of the importing countries of Chinese products, such as geographic

distance and destination market size can also affect firms’ choice of export modes. For

example, geographic distance adds to the transportation costs of exporting, so firms tend to

21

avoid exporting directly to countries far away; the probability of indirect exporting to a large

foreign market is low because it is worthwhile to invest in the fixed costs of direct exporting

when a destination market is large enough. Although these factors are interesting, they are not

the focus of this paper and have already been studied by existing papers (e.g., Bernard et al.,

2010; Ahn, Khandelwal, and Wei, 2011). Since country fixed effects will be used in our

product-country level analysis, all of these country characteristics are absorbed by the fixed

effects.

In Table 3, we report the results from regressions at the HS8 product-country level. The

dependent variable is the indirect export share calculated at the product-country level. The

key explanatory variable is (t-r), which still varies only across products as before because the

same rate applies to a product exported to all destination markets. The control variables

include the export shares by trade regimes and firm ownership types, calculated at the

product-country level. The first regression is based on the subsample with positive GAP,

while the second columns are for the subsample with negative or zero GAP. HS4 product and

country fixed effects are always included. As expected, (t-r) has a positive and significant

effect on indirect export share only for products with positive GAP that indicates a higher

chance of export under-reporting at Chinese border. This implies that the under-reporting

behaviors through domestic intermediaries may be associated with cross-border evasion

through under-reporting export values. The magnitude of the coefficient of (t-r) for the

positive GAP subsample is very similar to that reported in Column (1) of Table 1 for the

whole sample (0.667 vs. 0.673). The coefficients of other variables also have expected signs:

non-SOEs (especially foreign firms) and processing firms are less likely to use intermediaries

than SOEs and normal firms.

5.3. A transaction level analysis

Our third hypothesis states that the evasion motive is stronger for larger transactions. To

test it, we need to carry out a transaction level analysis. In Table 4, we report the results from

regressions at the transaction level. Here the dependent variable is a dummy indicating

whether the final exporter in a transaction is a production firm (0) or trading firm (1), based

on the conservative classification. (t-r) is still measured at HS8 product level.33 log(value) is

the logarithm of the value of an export transaction, where value is measured in current 33 Because the dependent variable is a dummy, which is on average much smaller than the indirect export share in percentage (ranging from 1 to 100), the coefficients can be much smaller than what we got from the product-level analysis. To avoid very small estimated coefficients of (t-r) and its interaction with log(value), we divide (t-r) by 100, so that it is now measured in percent, not in percentage as in our product-level analysis.

22

million U.S. dollars. Since a firm may exports multiple products at the tariff line level and

each product may be exported through multiple transactions in a year, the number of

observations at transaction level is extremely large, up to nearly 14 million in the regression.

To avoid intensive computation, we adopt a linear probability model (LPM) rather than a

logit or probit model. To prevent the variable (t-r) from being dropped, we include HS 4-digit

fixed effects rather than HS 8-digit fixed effects. We also include country fixed effects to

control for the unobserved heterogeneity at country level. In regression (1), we include only

(t-r), log(value) and their interaction term as the explanatory variables. The coefficient of (t-r)

is still positive as expected and is highly significant. The negative coefficient of log(value)

suggests that firms involving in larger transactions are less likely to use intermediaries on

average probably because the fixed costs of direct exporting becomes less important for large

transactions. More importantly, the positive coefficient of (t-r)*log(value) implies that firms

involved in larger transactions are more likely to evade taxes through indirect exports, all else

equal. This lends strong support to Hypothesis 3.

In regression (2), we also control for the trade regimes and ownership types of the

transactions. At the transaction level, these variables are simply indicators rather than shares

as in the product level analysis. In addition to the dummy for both types of processing firms

together, we also add a dummy for all other trade regimes (oth_regime), taking normal trade

as the default category. If we leave out the processing trade with supplied materials and all of

the other regimes as what we did for the product level analysis, the results do not change

much. In addition to the dummies for collective-private firms and foreign firms, we also

include a dummy for all other ownership types (oth_owner), taking SOEs as the default

category. The sign pattern of the first three variables is the same as that in regression (1), and

all of three coefficients are highly significant. Same as what is shown by the previous

product-level regression results, collective-private firms, foreign firms, processing firms are

found to be less likely to export indirectly than SOEs and exporters under normal trade.

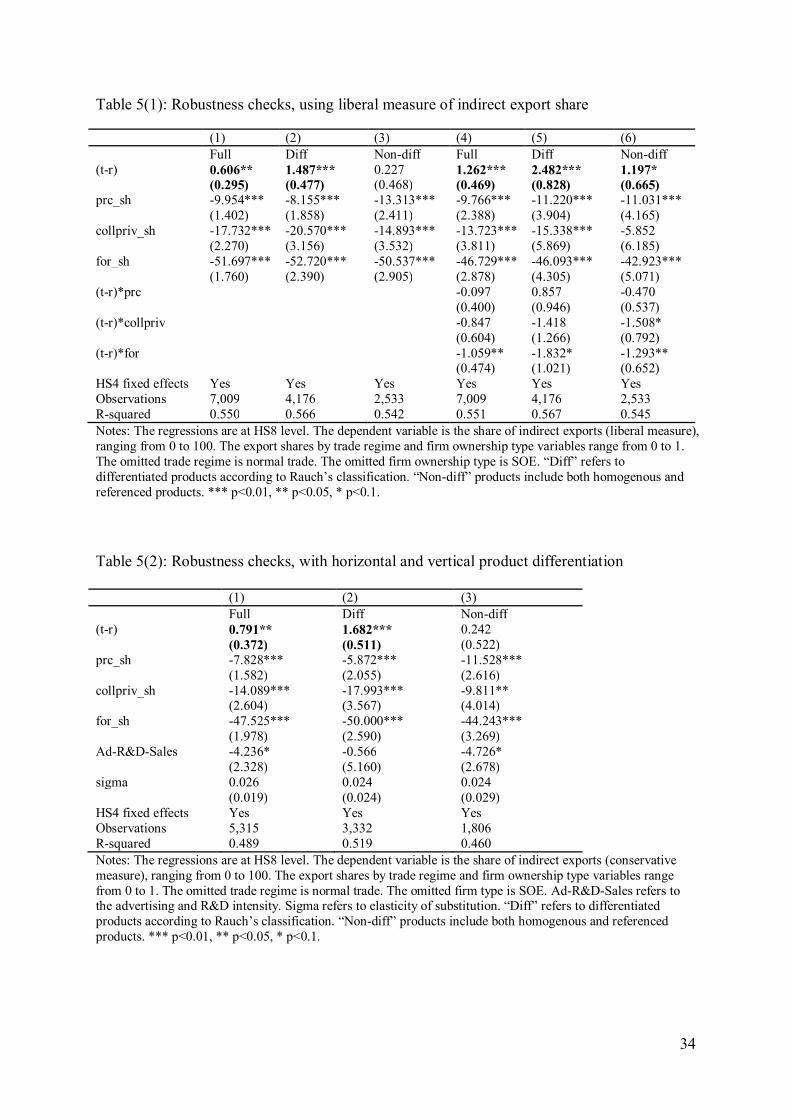

6. Robustness checks and other issues

In this section, we perform a number of robustness checks and discuss several

additional issues.

First, we always use the conservative measure of indirect export share in our previous

analysis. In Table 5(1), we check the robustness of our results to the alternative liberal

measure. The first three regressions are based on the full sample, and subsamples for

differentiated and non-differentiated (i.e., homogenous and referenced) products, respectively,

23

without including any interaction terms. The next three regressions are analogous to the first

three ones, with additional interaction terms between (t-r) and processing trade share and the

shares by ownership types. The results are very similar to the corresponding regressions using

the same specifications reported earlier, except that the interactions between (t-r) with firm

ownership shares (especially with the foreign share) are more significant. We find stronger

evidence for the evasion by SOEs probably because SOEs are more familiar with the

domestic policies and are better connected to government officials, and hence can do better

than foreign firms to take advantage of the policy loopholes in China. The results from the

previous country-product level and transaction level analyses are also robust to the alternative

liberal definition of trading firms, but are not shown in tables to save space. This is to be

expected given the small difference between the conservative and liberal definitions of

trading firms as reported in Section 4.2.

Second, we consider some additional variables that may also explain the variations in

indirect export share. As discussed in the literature, trading firms can play a role in verifying

product quality for buyers. Therefore, different product quality heterogeneity across

industries can affect the choice of exporting modes. Following Tang and Zhang (2012), we

examine both the horizontal differentiation and vertical differentiation, together with the tax

evasion motivation. For the horizontal differentiation, we use the elasticity of substitution

estimated by Broda and Weinstein (2006). For vertical differentiation, we use R&D and

advertising intensity of each industry constructed from the NBS industrial census data as in

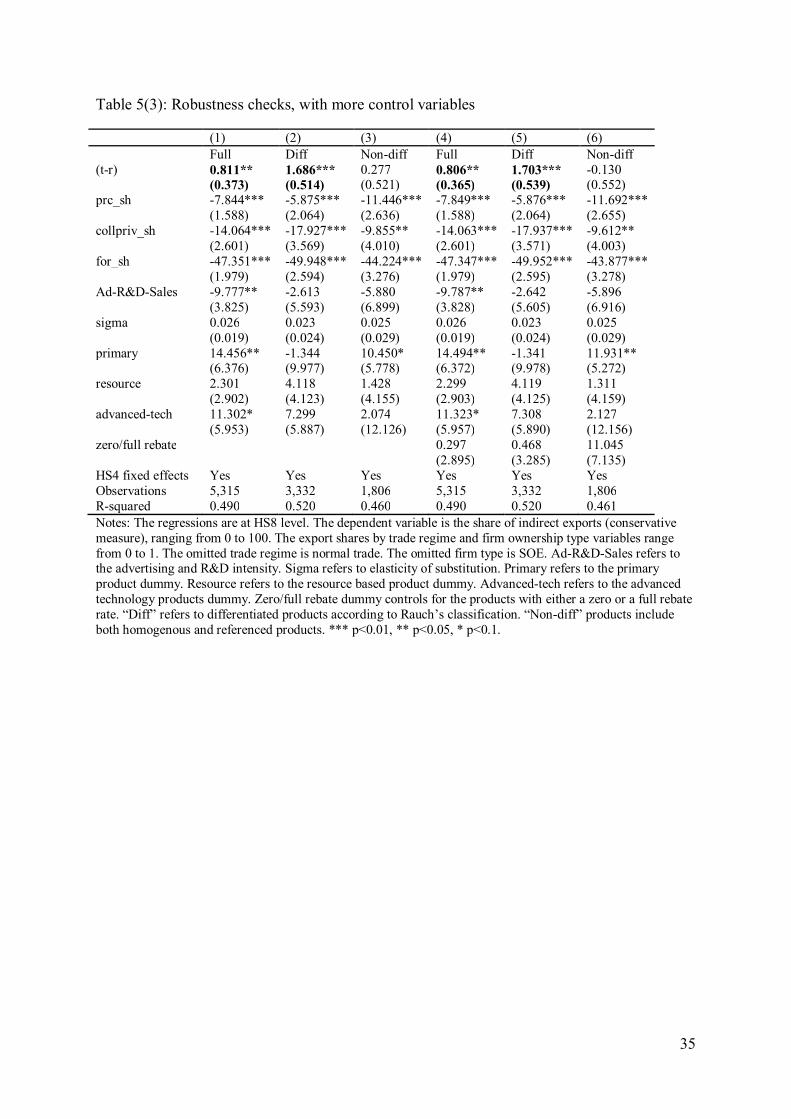

Tang and Zhang (2012).34 In Table 5(2), we add the two variables to regressions based on

the full sample, and subsamples for differentiated and non-differentiated products

respectively. Although the number of observations is greatly reduced owing to missing data

in the two additional variables, our main finding remains robust: (t-r) is positive and

significant not only for differentiated products but also in the full sample, but not significant

for non-differentiated products. The coefficient of the measure of elasticity of substitution

(sigma) is never statistically significant at the 10% level. Advertising and R&D intensity,

when significant at the 10% level, has a negative effect on indirect export share. This is

consistent with the argument in Tang and Zhang (2012). We do not include these variables in

our baseline regressions to avoid dropping a large number of observations due to missing

data. 34 This census covers all of the SOEs and all of the other types of firms with sales above 5 million RMB. First, we calculate the ratio of advertising and R&D expenditure to sales for each firm (Ad-R&D-Sales). Then, we take the average of this ratio for each Chinese Industry Code (CIC). Finally, we concord CIC to ISIC Revision 3 and then to HS6 and HS8.

24

Third, we examine some alternative stories which can also be consistent with our results.

China has used the rebate rates frequently as an industrial policy to promote the exports of

high-tech and deep processed products and discourage the exports of pollution and resource

intensive products and primary products. To curb the exports of resource-intensive products

such as rare earths, for example, China reduced their rebate rates in 2004, leading to higher

unrefunded export VAT rates (t-r) for these products. Because these resource-based products

are also more likely to be state-owned than other products and SOEs are more likely to export

indirectly as shown previously, this may also lead to a positive correlation between indirect

export share and (t-r). Based on the classification for primary products and resource-based

products as in Lall (2000), we find that the average unrefund rates for primary products and

resource-based products in our sample are indeed higher than that of other products (7.06%

and 5.84% vs. 4%), and the average indirect export shares of primary and resource-based

products are also higher than that of other products (35% and 33% vs. 31%).35

On the contrary, high-tech products have been encouraged by Chinese government and

received relatively higher rebate rates (in other words, lower (t-r)). If high-tech products

which are usually associated with higher quality are less likely to be exported indirectly

according to Tang and Zhang (2012), this can also lead to a positive correlation between (t-r)

and the share of indirect exports. Based on China’s official classification of advanced

technology products as published on the 2005 China Statistical Yearbook on Science and

Technology36, we find that the average unrefund rate for advanced-technology products in

our sample is higher than that of other products (5.84% vs. 4.45%), but the average indirect

export share advanced-technology products is only slightly higher than that of other products

(32.5% vs. 31.6%).

Although including HS4 product fixed effects can help to alleviate the above concerns,

we also take them as problems of omitted variable bias by checking the robustness of our

previous main finding after including the dummies for primary products (Primary),

resource-based products (Resource), and advanced-technology products (Advanced-tech).

The results are reported in the first three regressions of Table 5(3), where with the three

35 These data are based on the sample used in the first regression in Table 1. The three groups of products (Primary Products, Resource-based Products, and others) are mutually exclusive, accounting for 840, 1317 and 4,852 observations respectively. 36 The original primary product and resource-based product data in Lall (2000) are in SITC 3-digit level. We concord them to HS 6-digit. The original ATP data are at 4-digit Chinese Industrial Classification (CIC). We first concord CIC to 4-digit ISIC, and then to HS 6-digit. Although we have access to other classifications of high-tech products such as those in Lall (2000) and Ferrantino et al. (2007), we choose to use China’s own official definition because that is what the rebate rates are actually based on.

25

additional dummies in addition to the product differentiation measures (Ad-R&D-Sales and

sigma). Similar to what we found earlier, the key covariate (t-r) remains positive and

significant in the regressions based on the full sample and the subsample for differentiated

goods, but insignificant for non-differentiated goods, with little change in the magnitude of

the estimated coefficients compared to the previous result table. The coefficients of these

newly added dummies suggest that primary and high-tech products are more likely to be

exported through trading firms, but they are not always significant and sometimes bear mixed

signs for the two subsamples. We conclude that omitting them from our baseline regressions

does not significantly bias our estimated coefficients.

For similar reasons as stated above, some products are subject to zero or full rebates

when the government intended to promote or discourage the exports in certain sectors. To

make sure that our results are not driven by various other unobserved policies besides the

VAT rebates, we also add to our regressions in the last three columns of Table 5(3) a dummy

indicating if a product is subject to zero or full rebate rate. This variable, however, turns out

to be insignificant. Although this variable is likely correlated with rebate rates, it may not

vary with indirect export share in a significant way. The estimated coefficients of other

variables change little, suggesting that our results are not driven by these factors.

In addition, besides the use of export rebate rate as an industrial policy, other factors

may also affect the rebate rates. For example, as described in Section 3.1, China started with

a full rebate system but changed it to a partial rebate system due to budget constraint.

Ignoring the budget issue is not a problem for us unless it is also correlated with indirect

export share. Although budget shortfall might motivate the government to tackle tax evasion

problems, there is no evidence showing that the evasion through indirect exports in particular

has already been in the radar of the government when it adjusts rebate rates. Moreover, rebate

rates may also be adjusted in response to the level or the growth rate of exports in an industry.

However, this is not a problem either as long as the level or the growth rate of exports is not

correlated with indirect export share. All of these concerns, together with those considered in

Table 5(3), are related to the endogeneity of VAT rebate rates. In our opinion, however, the

endogeneity issues do not seem to be a major concern.

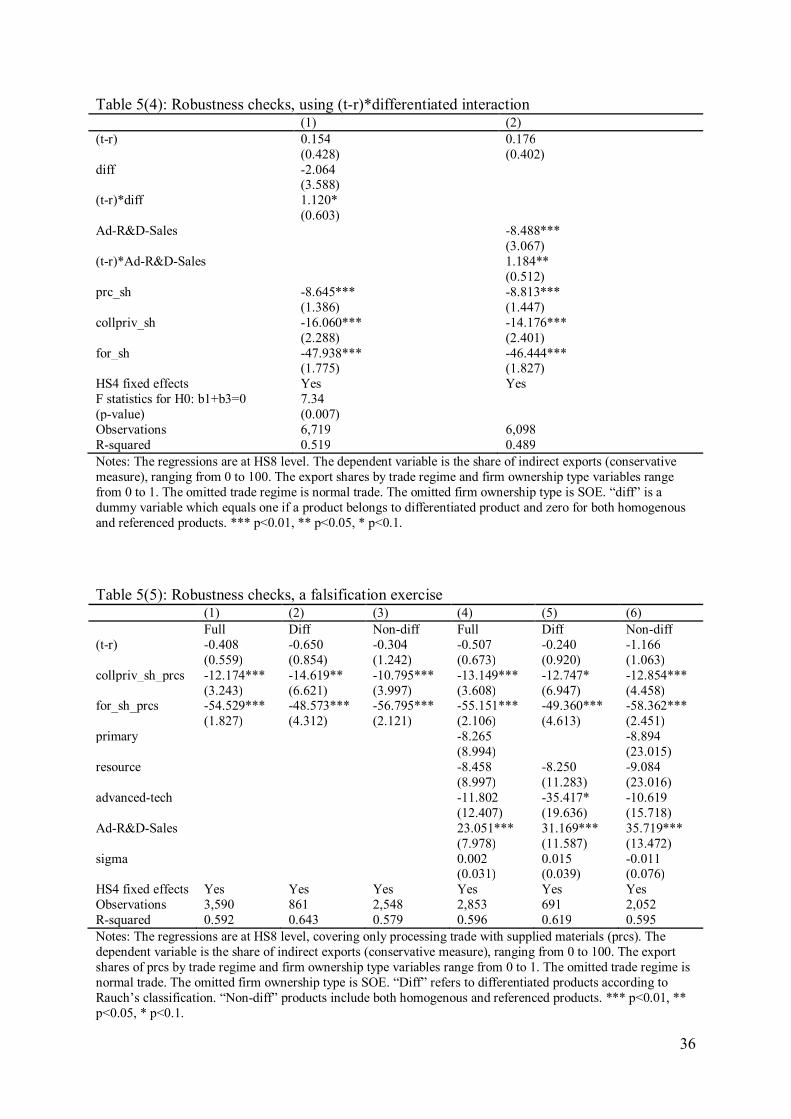

Fourth, we have so far split the full sample into differentiated and non-differentiated

products. Alternatively, we can also create a dummy variable indicating if a product belongs

to differentiated product and then interact it with export tax rate. The benefit of doing this is

that we can retain all the products in the regressions to increase the sample size. The result is

reported in the first column of Table 5(4). The result shows that (t-r) has a significant and

26

positive effect on indirect export share only for differentiated product, which is the same as

what we found earlier. For non-differentiated products, the effect is insignificant, as shown

by the coefficient of (t-r). An F-test, reported at the bottom of the table, shows that the sum of

the first and the third coefficients are significantly different from zero at the 1% level.