Embed Size (px)

Citation preview

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 1/42

1 | P a g e

Marketing Strategy

For

GROUP NO. 9

DEBRAJ NASKER B10077

INDERJEET SINGH B10081

NAYAN GOSWAMI B10091

PINAKI MAJUMDER B10095

SOUVIK HALDER B10112

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 2/42

2 | P a g e

Contents

Introduction ................................ ................................ ................................ .......................... 4

A. Objectives: ................................ ................................ ................................ ................ 6

a. Corpor ate Objectives: ................................ ................................ ................................ . 6

b. Mark eting Objectives: ................................ ................................ ................................ 6

B. Situation Analysis ................................ ................................ ................................ ..... 8

a. The Product8

................................ ................................ ................................ .............. 8

b. Competitor s:................................ ................................ ................................ ............... 9

c. Analysis of Dir ect-To-Home Mark et in India ................................ ........................... 11

D. Categor y Factor s ................................ ................................ ................................ ...... 16

e. Environmental Factor s ................................ ................................ ............................. 18

C. Company and Competitor Analysis ................................ ................................ ....... 23

a. Product Featur e Matrix9 ................................ ................................ ........................ 23

b. Str ategies ................................ ................................ ................................ .............. 23

c. Mark eting Mix................................ ................................ ................................ ...... 24

d. Profits ................................ ................................ ................................ ................... 26

e. Value chain................................ ................................ ................................ ........... 26

f . Diff er ential Advantage for each company ................................ ............................. 27

g. Expected futur e str ategies ................................ ................................ ..................... 28

D. Customer Analysis................................ ................................ ................................ .. 29

a. Segmentation Str ategy ................................ ................................ .............................. 29

1. Demogr aphic Factor s: ................................ ................................ ........................... 29

2. Geogr aphic Factor s: ................................ ................................ .............................. 29

3. Lif estyle: ................................ ................................ ................................ .............. 29

b. Consumer Behaviour ................................ ................................ ................................ 30

c. Tar geting ................................ ................................ ................................ .................. 31

d. Positioning ................................ ................................ ................................ ............... 32

E. Assumptions in Planning Process ................................ ................................ .............. 34

a. Mark et Potential ................................ ................................ ................................ ....... 34

b. For ecast Assumptions................................ ................................ ............................... 34

F. Strategy ................................ ................................ ................................ ...................... 35

a. Cor e Str ategy ................................ ................................ ................................ ........... 35

b. Customer Tar gets ................................ ................................ ................................ ..... 35

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 3/42

3 | P a g e

c. Product/Service Featur es ................................ ................................ .......................... 35

G. Strategy-Marketing Communications Programmes ................................ ............. 37

a. Integr ated Mark eting Communications Progr ammes ................................ ............. 37

b. Pricing Str ategy ................................ ................................ ................................ .... 39

c. Channel Str ategy................................ ................................ ................................ ... 39

d. Customer Management Str ategy ................................ ................................ ........... 40

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 4/42

4 | P a g e

Introduction Television industr y in India took birth with the launch of Doordar shan in 1959

1. Back then,

television was r egarded as a luxur y item which only a f ew people could afford. In 1992 cable

industr y came into existence which went down as the biggest r evolution in the histor y of

Indian Entertainment Industr y.

Cable TV changed the way the aver age Indian watched TV. Suddenly the entertainment

starved part of the population got mor e options as a huge inf lux of for eign and new domestic

channels f looded the mark et. However this tr emendous growth saw continuous tariff hik es in

cable TV which didn¶t go down too well with the middle-income mass mark et of consumer s.

People cr aved for better quality pictur e and wanted to watch r egional language channels

which they pr ef err ed. Hence ther e was a vocif erous demand and willingness to pay for

quality and what one desir ed.

The stage was perf ectly set for the introduction of satellite TV ± Dir ect to Home (DTH)

broadcasting. Location and accessibility to the cable line didn¶t matter anymor e in DTH

scenario. DTH Digital TV system r eceives signals dir ectly from satellite through the dish,

decodes it with the Set-Top Box and then sends stunningly clear pictur e and sound to TV.

Better addr essability, quality of service and incr eased number of channels ensur ed that this

technology was her e to stay.

Tata Sk y is a DTH satellite television provider in

India, using MPEG-2 digital compr ession technology, tr ansmitting using INSAT 4A at 83.0°.

Tata sk y was incorpor ated in 2004; Tata Sk y is a Joint Ventur e between the TATA Group

and STAR 2. Tata Sk y DTH endeavour s to off er Indian viewer s a wor ld-class television

viewing experience through its satellite television service. Vikr am Kaushik is pr esent CEO of

Tata Sk y Ltd.

1. http://india.gov.in/knowindia/television.php

2. http://en.wikipedia.or g/wiki/Tata_Sk y

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 5/42

5 | P a g e

The SKY br and, owned by the UK -based British Sk y

Broadcasting Group, brings to Tata Sk y the r eputation of mor e than 20 year s experience of

satellite broadcasting. SKY is well known for the innovative products and services launched

by BSk y, such as DTH broadcasting in 1989, digital satellite broadcasting in 1998, inter active

television services in 1999 and the SKY+ per sonal video r ecorder in 20013. Tata Sk y Ltd is

the Fir st Indian DTH provider to be awarded the ISO 27001:2005 accr editation, the ultimate

benchmark for information security4.

In October 2008, Tata Sk y announced launching of DVR service Tata Sky+ which allowed

90 hour s of r ecording in a MPEG-4 compatible Set Top Box. Tata Sk y was selected as a

SUPER BRAND for the year 2009-2010 by an independent and voluntar y council of experts

known as Super br ands Council. It is the only Indian DTH to have won this distinction 2.

3. http://www.tatask y.com/corpor ate-info.html

4. http://en.wikipedia.or g/wiki/Tata_Sk y

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 6/42

6 | P a g e

A. Objectives:

a. Corpor ate Objectives:

i. To be the leading Dir ect-to-Home (DTH) service provider in India,

off ering DVD quality pictur e and CD quality sound along with new age

inter active services.

ii. To be the leading round-the-clock air-time provider, cr eating customer

value.

iii. To establish the company as the cr eator of entertainment and edutainment

products and services. Through these services, the company intends to

become an integr al part of the global mark et. As a corpor ation, company

want to be profitable, productive, cr eative, tr end setting and financially

rugged with car e and concern for all stak e holder s.

b. Mark eting Objectives:i. Volumes & Profits

5: Company wants to double its customer base by 2012.

Curr ently it has 45 lak h of the total 2 cror e DTH customer s in India, which

is also pr edicted to r each 4 cror e by 2012. Also in India ther e ar e

approximately 13 cror e TV sets of which only 2 cror e is cater ed by the

DTH service. Ther e is a huge potential to tap this r eserve. In terms of

profit, Company r eached br eak-even after 4 year s of its start-up. Now it

aims to double its profits ever y year .

ii. Image: The Company wants to project itself as an ³Edutainment´ service6

r ather than just an entertainment service provider . For this it has launched

inter active services lik e Active English, Active WizK ids and other s. Nowit plans to expand this initiative and grow on this front.

iii. Aver age Revenue Per User (ARPU) 7: The company intends to gain value

mark et shar e and incr ease its ARPU when compar ed to other DTH

provider s through quality value added service and customer service.

Comparing with Dish TV who is having ARPU of 135 Rs, Tata Sk y

curr ently has an ARPU of 270 Rs which it intends to incr ease to 300 Rs.

Internationally, the ARPUs ar e quite high when compar ed with India. This

indicates that ther e is a potential upside in the ARPUs.

5. Article on News Center, 10 th March 2010

6. Excerpts of interview with Mr . Vikr am Mehta (Chief Mark eting Officer, Tata Sk y) published in Business

Line, 7th Januar y 20107.

7. http://business.r ediff .com/r eport/2010/apr/06/tata-sk y-str ategy-to-attr act-mor e-customer s.htm

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 7/42

7 | P a g e

iv. Customer Retention: Company believes that its long term sustainability

and viability depends on how long the customer r emains loyal to the

company. Company believes that by tar geting customer s who go for the

cheapest product, it is putting itself at a risk as these customer s can churn-

out any time.

v. Customer Delight: By providing services lik e movies on demand, ActiveMall, Active Dar shan, Active Cooking, company wants to provide extr a

value added service at a pr emium cost. Company has curr ently 3 call

center s catering to the diff er ent r egional needs and it plans to expand on

this initiative. It is also looking to improve distribution channel and tr ack

customer services efficiently.Company is tar geting 30% savings by cost

cutting measur es through vendor and dealer s channels improvement.

vi. Technology Upgr adation: The company tar gets to shift all of it existing

customer s to the latest technology (Tatask y+) at the ear liest. Curr ently

only 10% of the customer s have shifted 7. It also plans to provide HD

services in all channels, curr ently is has started with ³Discover y´ and ³

National Geogr aphic´.

vii. Regional and r emote ar ea: Curr ently mor e than 50% of the volume ar e

from outside top 50 cities in India7

and it wants to capitalize on the

beginning. Also it is tar geting r emote ar eas lik e Siachen, Burma, Indo-Pak

border .

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 8/42

8 | P a g e

B. Situation Analysis

a. The Product8

i. Tata Sk y launches itself as a DTH services r equiring a Dish, A set top box

and network access card per television. Later variant lik e Community dish

for entir e building wer e launched. Recently Tata Sk y Plus with Per sonal

Video Recording technology has been launched. Latest entr ants ar e the

HD channels of Discover y and NGC.

ii. Enjoy over 190 Channels and services in DVD quality pictur e and CD

quality sound.

iii. Various pack ages ar e provided for the customer to choose from. These

include:

1. Super-Hit pack (67 channels)

2. Super-Value pack (102 channels)

3. Super-Saver pack (127 channels)

4. South-Starter pack (76 channels) 5. South-Value pack (99 channels)

6. South-Saver pack (110 channels)

7. South-Jumbo pack (143 channels)

8. http://www.tatask y.com/

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 9/42

9 | P a g e

iv. Various services provided by TATA Sk y include:

1. Active English: Enhance your English conver sation skills.

2. Active Mall: Save time and money, shop on your TV !

3. Active Showcase: Your private multiplex at home

4. Active Cooking: Get your f avourite r ecipes when you want

5. Active Stories: Enjoy your stor y book on television 6. Active Starnews: Go dir ectly to your f avourite news section

7. Active WizK ids: Mak e your child a genius

8. Active Learning: Tak e Daily quizzes covering Math, GK and

science on your Television.

9. Active Games: Inter active games for all ages

10. Active Dar shan: Get 24x7 dar shan of the following temples: Shirdi

Sai Baba, Mumbai¶s SiddhiVinayak, ISKCON and Kashi

Vishwanath.

11. Zeetos r ewards: Earn through fun on TV

v. Par ental Control

vi. Search and Scan Banner : Find out what¶s palying on other channels

without changing the channel you ar e watching

vii. Guide (including Hindi Display) with 4 day listing of all progr ams with

r eminder f acility

viii. Customer Service- 24 x 7 help. Support in 11 languages.

b. Competitor s:

i. Dish TV: Mark et leader amongst private player s

ii. Sun Dir ect: Price warrior, Strong Br and equity in south.

iii. Airtel: Pr esence of a strong telcom infr astructur e

iv. Big TV: Strong br and image and superior telcom infr astructur e

v. Videocon DTH: riding on its str ength in television manuf acturing and

distribution. Company wants to integr ate set top box with television.

vi. Doordar shan: National pr esence (90% r each), fr ee service.

vii. Local cable oper ator s: In mark et for close to 20 year s and have high

mark et penetr ation.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 10/42

10 | P a g e

SWOT ANALYSIS OF TATA SKY

Strengths:

y Ability to use the br and TATA for br and imaging.

y Superior quality hardwar e and machiner y used (Newscorp¶s DTH arm Sk y).

y High pictur e and sound quality and superior customer service provided.

y Ability to provide service even during power-cuts through gener ator s as opposed to

tr aditional cable lines.

y Against the pr evailing ³One size fit all´ str ategy. Customised services for ever y

customer .

y An established player in the mark et helps for the visibility of the product.

y Inroads into the rur al mark et through r etailing avenues, working with Godr ej Adhaar,

ITC's e-choupal, Tata Chemicals and Rallis initiatives.

Weakness:

y Is not ver y financially healthy.

y High oper ating expenses hence br eak-even point seems a f ar cr y.

y Higher service char ges and installation char ges compar ed to cable T.V or other DTH

provider s.

y Small distribution network limited to the ur ban; hassled by distribution issues.

Opportunities:

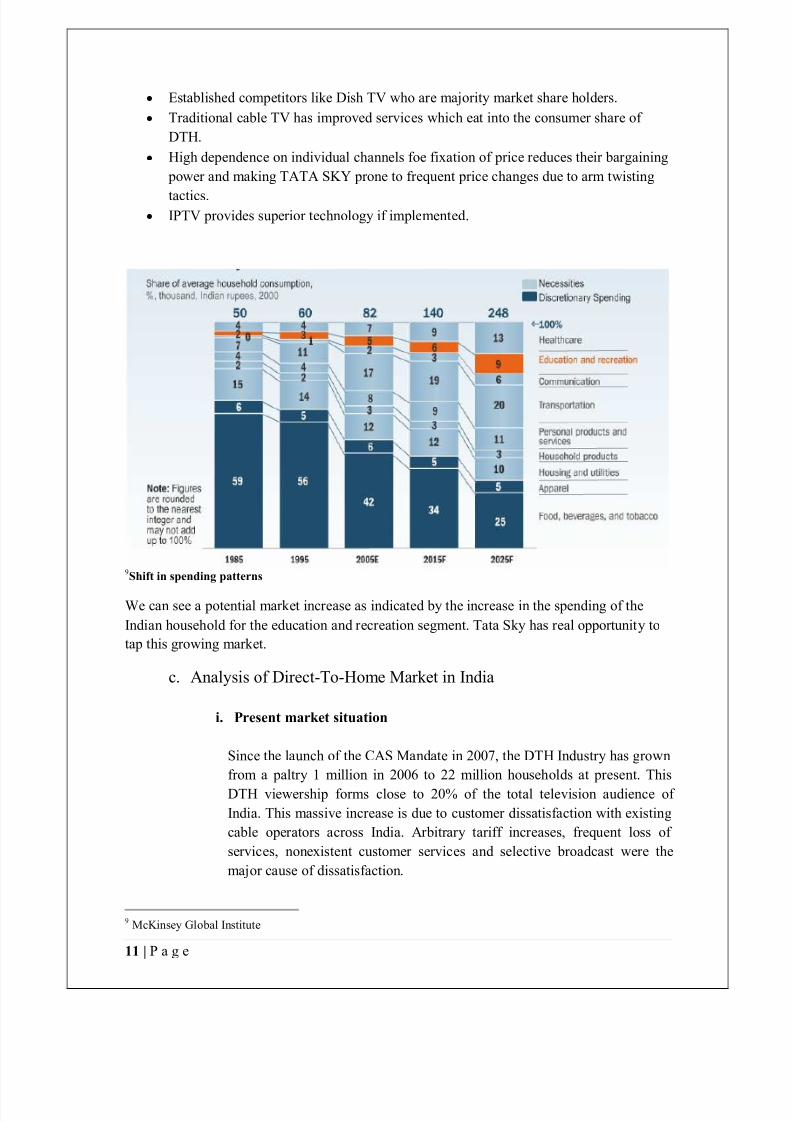

y The shar e of the wallet of Indians have been incr easingly moving towards education

and entertainment(see illustr ation)as a consolidated function which TATA SKYcan

ver y aptly fulfil.

y Higher disposable income with the Indian population.

y R ur al mark et has huge potential.

y Growing demand for customised television viewer ship.

y HDTV services provide an opportunity with the Commonwealth Games and Wor ld

Cup around the corner . y Implementation of CAS has incr eased the need for DTH services lik e TATA SKY.

Threats:

y Online live str eaming ± Off er s superior services and at much lower costs (eff ectively

almost fr ee).

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 11/42

11 | P a g e

y Established competitor s lik e Dish TV who ar e majority mark et shar e holder s.

y Tr aditional cable TV has improved services which eat into the consumer shar e of

DTH.

y High dependence on individual channels foe fixation of price r educes their bar gaining

power and making TATA SKY prone to fr equent price changes due to arm twisting

tactics. y IPTV provides superior technology if implemented.

9Shift in spending patterns

We can see a potential mark et incr ease as indicated by the incr ease in the spending of the

Indian household for the education and r ecr eation segment. Tata Sk y has r eal opportunity to

tap this growing mark et.

c. Analysis of Dir ect-To-Home Mark et in India

i. Present market situation

Since the launch of the CAS Mandate in 2007, the DTH Industr y has grown

from a paltr y 1 million in 2006 to 22 million households at pr esent. This

DTH viewer ship forms close to 20% of the total television audience of

India. This massive incr ease is due to customer dissatisf action with existing

cable oper ator s across India. Ar bitr ar y tariff incr eases, fr equent loss of

services, nonexistent customer services and selective broadcast wer e the

major cause of dissatisf action.

9 McK insey Global Institute

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 12/42

12 | P a g e

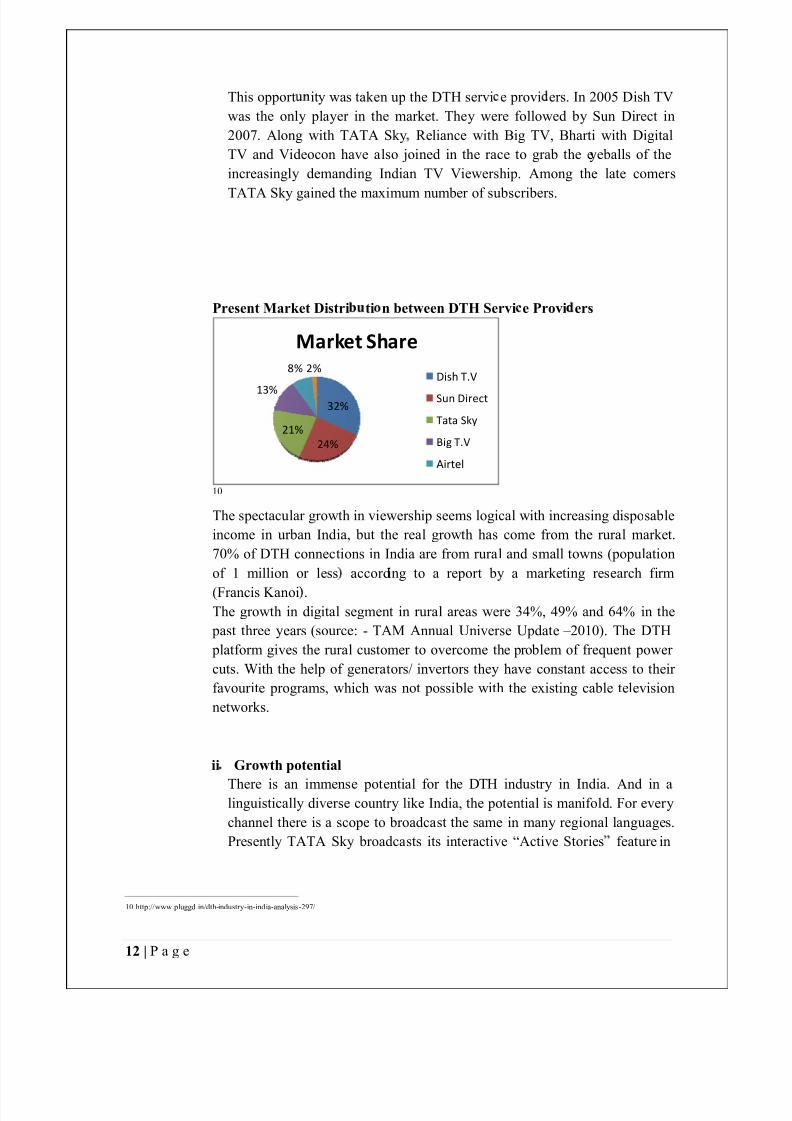

This oppor t ity was taken up the DTH servi e provi er s. In 2005 Dish TV

was the only player in the market. They were followed by Sun Direct in

2007. Along with TATA Sk y R eliance with Big TV, Bhar ti with Digital

TV and Videocon have also joined in the race to grab the eyeballs of the

increasingly demanding Indian TV Viewer ship. Among the late comer s

TATA Sk y gained the maximum number of subscr iber s.

Present Market Distri ti n between DTH Servi e Provi ers

10

The spectacular growth in viewer ship seems logical with increasing disposable

income in urban India, but the real growth has come from the rural market.

70% of DTH connections in India are from rural and small towns (population

of 1 million or less according to a repor t by a marketing research f irm

(Francis Kanoi .

The growth in digital segment in rural areas were 34%, 49% and 64% in the

past three year s (source: - TAM Annual Univer se Update ±2010). The DTH

platform gives the rural customer to overcome the problem of frequent power

cuts. With the help of generator s/ inver tor s they have constant access to their

favour ite programs, which was not possible with the existing cable television

network s.

ii Growth potential

There is an immense potential for the DTH industr y in India. And in alinguistically diver se countr y like India, the potential is manifold. For ever y

channel there is a scope to broadcast the same in many regional languages.

Presently TATA Sk y broadcasts its interactive ³Active Stor ies feature in

10

http://www.pluggd.in/dth-industr y-in-india-analysis-297/

32%

24%

21%

13%

8% 2%

Market Share

Dish T.V

Sun Direct

Tata Sky

Big T.V

Airtel

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 13/42

13 | P a g e

six diff er ent languages- English, Hindi, Tamil, Telugu, Bengali and

Mar athi.

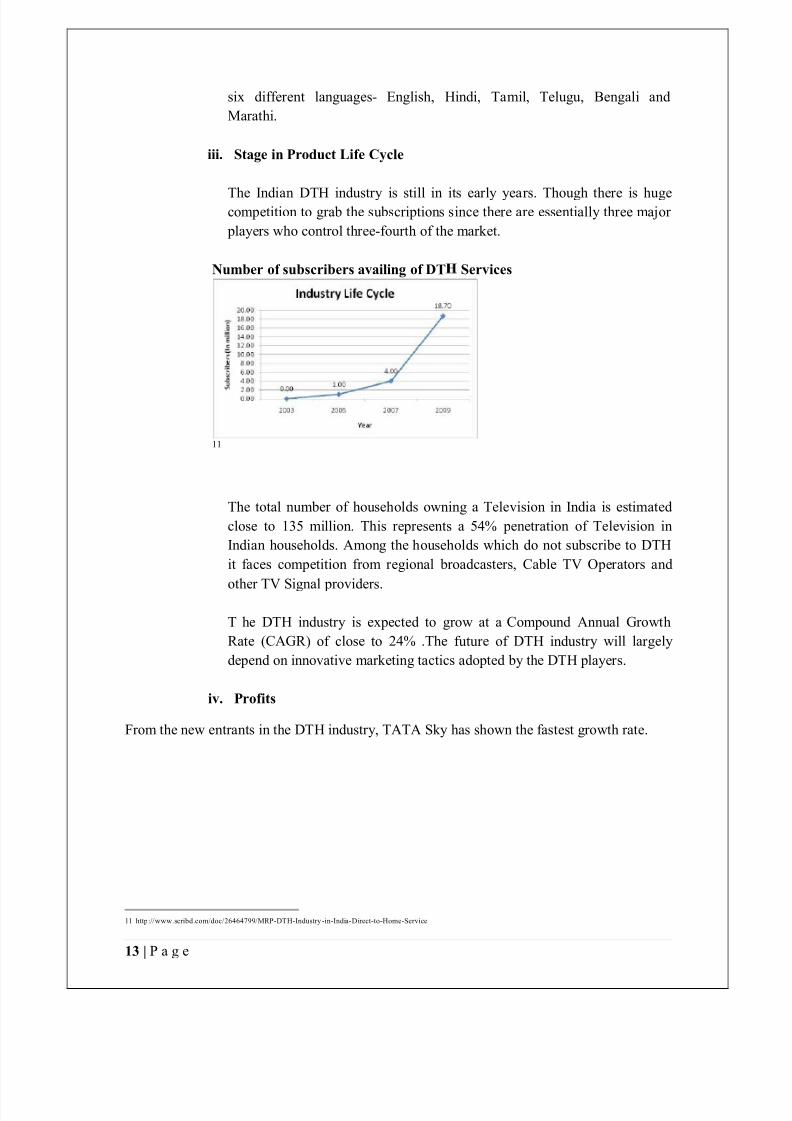

iii. Stage in Product Life Cycle

The Indian DTH industr y is still in its ear ly year s. Though ther e is hugecompetition to gr ab the subscriptions since ther e ar e essentially thr ee major

player s who control thr ee-fourth of the mark et.

Number of subscribers availing of DT Services

11

The total number of households owning a Television in India is estimated

close to 135 million. This r epr esents a 54% penetr ation of Television in

Indian households. Among the households which do not subscribe to DTH

it f aces competition from r egional broadcaster s, Cable TV Oper ator s and

other TV Signal provider s.

T he DTH industr y is expected to grow at a Compound Annual Growth

Rate (CAGR ) of close to 24% .The futur e of DTH industr y will lar gely

depend on innovative mark eting tactics adopted by the DTH player s.

iv. Profits

From the new entr ants in the DTH industr y, TATA Sk y has shown the f astest growth r ate.

11 http://www.scribd.com/doc/26464799/MRP-DTH-Industr y -in-India-Dir ect-to-Home-Service

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 14/42

14 | P a g e

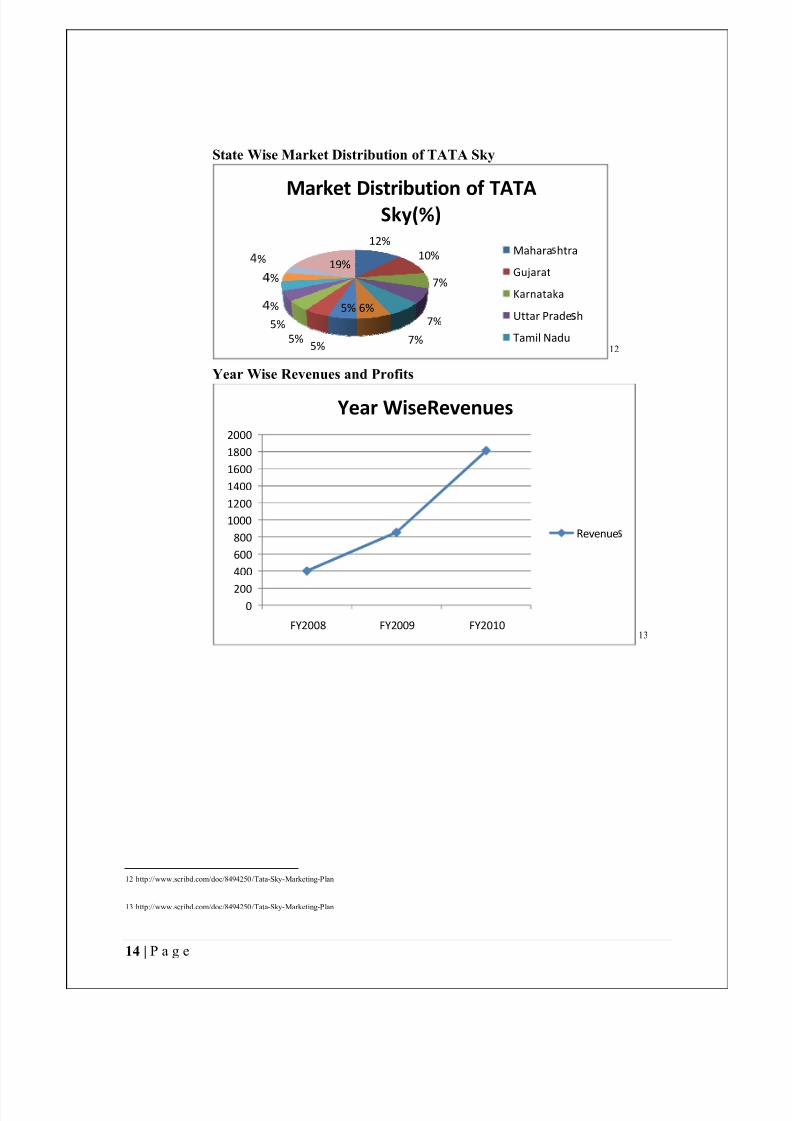

State Wise Market Distribution of TATA Sky

12

Year Wise Revenues and Prof its

13

12 http://www.scr ibd.com/doc/8494250/Tata-Sk y-Marketing-Plan

13

http://www.scr ibd.com/doc/8494250/Tata-Sk y-Marketing-Plan

12%

10%

7%

7%

7%

6%5%

5%5%

5%

%

¡ %

%19%

Market Distribution of TATASky(%)

Mahara¢ htra

Gujarat

Karnataka

Uttar Prade ¢ h

Tamil Nadu

0200

400

600

800

1000

1200

1400

1600

1800

2000

FY2008 FY2009 FY2010

Year WiseRevenues

Revenue¢

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 15/42

15 | P a g e

14

14

http://www.scribd.com/doc/8494250/Tata-Sk y-Mark eting-Plan

-600

-580

-560

-540

-520

-500

-480

-460

-440

F£

2008 F£

2009 F£

2010

Year i e P

Profit after tax

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 16/42

16 | P a g e

d. Categor y Factor s

The categor y f actor s inf luencing the mark et conditions of TATA SKY can be succinctly

described by the Porter¶s Five Forces Model Analysis:

y Threats of new entrants: The thr eats from new entr ants can be analysed from the

per spective of the following:

o Proper distribution network : A DTH subscriber in order to be successful

needs a proper distribution network, lik e those of Airtel Digital TV or TATA

SKY. Such a distribution network tak es time to matur e so an immediate thr eat

from a new entr ant is low.

o License and regulation issues: TRAI r egulates the player s of the DTH

industr y and hence entr y into the sector is highly monitor ed. Besides the

pricing Consumer Pr emise Equipment (CPE) lik e the set-top boxes and the

positioning of tr ansponder s is patented. Hence this too mak es the thr eat from

new entr ants low. o Established players: The existence of established player s in the mark et lik e

TATA SKY, Airtel Digital TV, etc cr eates high entr y barrier s for new

entr ants.

y Bargaining power of buyers: The pr esence of seven established br ands in the

mark et in the form of Airtel Digital TV, Big TV, Dish TV, Sun Dir ect, etc provides

the consumer s with a lot of options. Hence competition in the sector leads to ther e

being a high bar gaining power of the buyer s. So product diff er entiation achieves a lot

of importance.

Besides, the switching cost of user s from one subscriber to another is not ver y high asit includes only a change in a subscription. DTH player s have been tr ying to r educe

this by ensuring that their set-top boxes ar e back ward compatible.

y Bargaining power of suppliers: The DTH supplier s lik e TATA SKY depend on

thr ee major types of supplies ± CPE (Customer Pr emise Equipment) lik e set-top

boxes, tr ansponder s and content. As ther e is an issue of back ward compatibility of

set-top boxes, thus the services ar e at the mercy of the set-top box supplier s. The

tr ansponder s ar e supplied by ISRO and the absence of proper r egulation in the pricing

of bandwidths; the player s ar e at the mercy of the supplier s.

y Pressure from substitutes: The thr eat to the DTH sector is thr ee-fold:

o I/P TV: They provide a lucr ative option for the buyer as they come with fr ee

set-top boxes and promise HD quality pictur es. Besides they also have the

added advantage of off ering Internet services along with the television

services.

o Tr aditional terr estrial cable TV: The mark et penetr ation of DTH player s have

still been slow because people have been showing a lot of inertia while

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 17/42

17 | P a g e

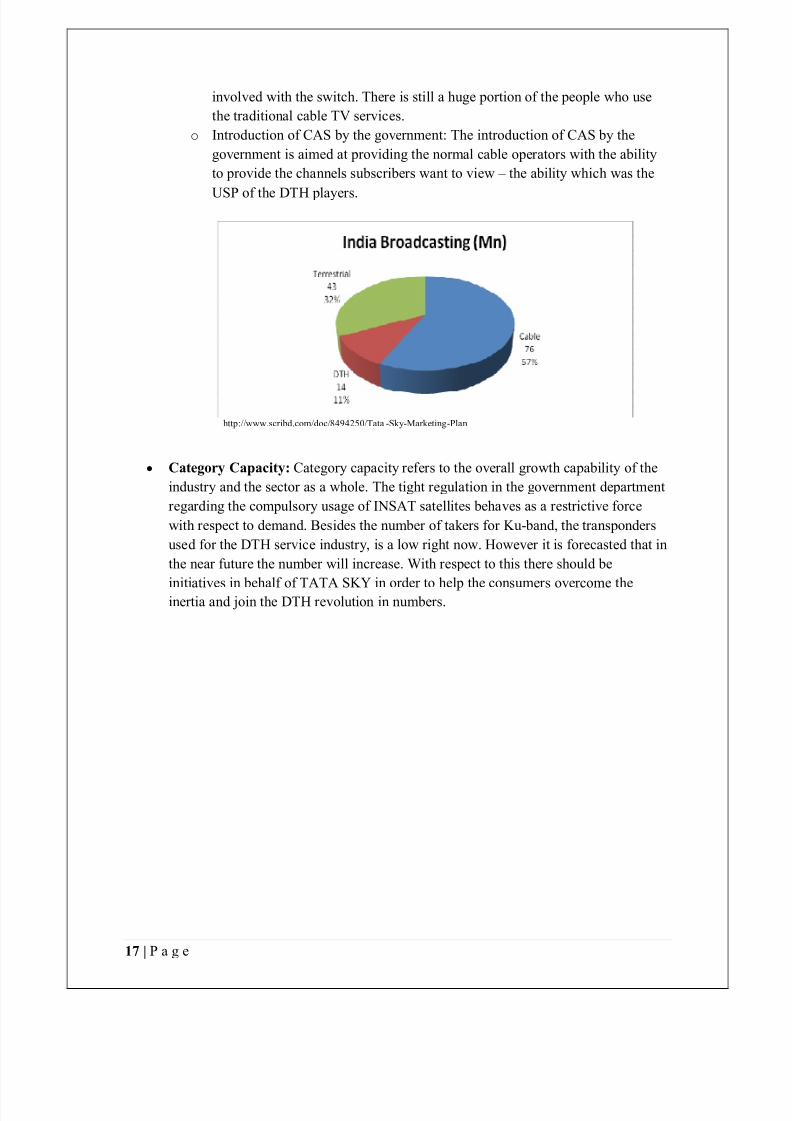

involved with the switch. Ther e is still a huge portion of the people who use

the tr aditional cable TV services.

o Introduction of CAS by the government: The introduction of CAS by the

government is aimed at providing the normal cable oper ator s with the ability

to provide the channels subscriber s want to view ± the ability which was the

USP of the DTH player s.

http://www.scribd.com/doc/8494250/Tata -Sk y-Mark eting-Plan

y Category Capacity: Categor y capacity r ef er s to the over all growth capability of the

industr y and the sector as a whole. The tight r egulation in the government department

r egarding the compulsor y usage of INSAT satellites behaves as a r estrictive force

with r espect to demand. Besides the number of tak er s for K u-band, the tr ansponder s

used for the DTH service industr y, is a low right now. However it is for ecasted that in

the near futur e the number will incr ease. With r espect to this ther e should be

initiatives in behalf of TATA SKY in order to help the consumer s overcome theinertia and join the DTH r evolution in number s.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 18/42

18 | P a g e

e. Environmental Factor s

The external mark et environmental conditions in which TATA Sk y oper ates can be described

under the following heads.

y Political

y Economic

y Social

y Technological

These ar e not the only heads under which all the f actor s can be categorized. In case of a

highly r egulated industr y wher e the f actor s such as FDI and Entr y/Exit conditions ar e

defined, a separ ate head for Legal is also consider ed.

The above combination of f actor categories is known as PEST or r earr anged as STEP. With

addition of other heads as Legal and Environment, it is also known PESTEL.

We shall closely look at each of the f actor s that inf luence TATA Sk y as well as the DTH

industr y as a whole.

i. POLITICAL

y POLITICAL OPPOSITION

In ear ly 1997 Star TV was set to launch its DTH Service, Indian Sk y

Broadcasting (ISkyB). But the Centr al Government banned the K u-

Band equipments that wer e to be used in the DTH service. Eventually

due to political decisions the launch was suspended.

Finally after long deliber ations in 2000, r egulation for DTH services

wer e formulated. But this doesn¶t mean that the service provider s ar e

content with the pr esent situation. Ther e ar e ongoing discussions to

incr ease the FDI limit from the pr esent 49 % and 20% for Broadcasting

and Cable companies to the proposed 74%.

The implications of the incr ease in FDI limits ar e manifold. Incr ease in

availability of funds would help the DTH service provider s to r each

profitable oper ations. Quality of Infr astructur e and Skill would

incr ease.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 19/42

19 | P a g e

y CONTENT REGULATION

The progr ammes being broadcasted ar e r egulated by the Information

and Broadcasting Ministr y. As the service provider they also come

under their purview. Also the DTH service provider s ar e not allowed to

beam exclusive content. The same set of channels means that ther e is

no diff er entiation in the content, and the services ar e the only things

that diff er .

y COALITION GOVER NMENTS

The curr ent Indian scenario is that one of Coalition Politics. The

Government at the centr e is a mix of r egional and a one or two major

national parties. Coalition also means that the stability is suspect to the

common inter ests of the coalition. Each Government comes with its

own set of rules and r egulations. This instability to r egulations, Tariff

laws cr eate an unf avour able situation for business.

y POLITICAL CONNECTION

Most of the six DTH player s in India have connections with people in

the upper echelons in political circles. Some even have holdings

through r elatives. This sometimes gives an unf air advantage and a high

entr y barrier for new player s.

ECONOMIC

Factor s such as Inf lation, Growth Rate, Banking Inter est Rate, For eign Exchange Rate,

Budget allowances have a cumulative eff ect on the DTH player s.

y IMPACT OF ECONOMIC POLICIES

As most of the equipment for the setup, such as the Set Top Boxes

(STB) ar e imported. Exchange r ates ther efor e play a big role her e.

Inf lation often dictates the amount of money left with the customer to

spend on something as non-essential as DTH. In times of high

inf lation, the industr y will experience less number of new subscriber s.

With high GDP r ates and FDI allowances the industr y will be aff ected

positively.

Import duty on STBs was r emoved from Budget 2008-09. Such liber al

decisions will help the industr y to grow r apidly.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 20/42

20 | P a g e

y HIGHER DISPOSABLE INCOME

With incr ease in the discr etionar y spending of the ever growing Indian

Middle-Class, ther e ar e mor e demands from the service provider s. The

ease of switching always k eeps the provider s on their toes to k eep their base intact.

SOCIAL

Factor s such as Social and Cultur al aspir ations, buying and consumption behaviour aff ect the

business for DTH player s and ar e categorized as Social.

y ASPIRATIONS

The growing middle class and their aspir ations to r each the next social

str ata in terms of income and status ar e becoming ver y important. This

can be seen by some of the special services provided by the player s.

TATA Sk y r ecently came up with a service called Active English,

which cater s to the categor y which eager to learn English. Also the

easy availability of aff luent lif estyle in forms of broadcasted channel

gives them easy access.

y VER NACULAR vs NATIONAL CHANNELS

The number of channels being broadcast in India is 423, including

English and Hindi. The rur al DTH customer is the big consumer of

these r egional channels.

y

PEER PRESSURE

As DTH is slowly tr ansforming from a luxur y to necessity, its absence

is becoming mor e and mor e conspicuous. Driven by the need to

maintain a standing, a part of the population become DTH consumer s.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 21/42

21 | P a g e

TECHNOLOGICAL

y BANDWIDTH- RESTR ICTED USAGE

According to ISRO, the provider of satellite services to the DTH

industr y, the industr y is wasting spectrum on the K u Band, and have

advices pooling of r esources. With the incr ease in the number of

channels, the DTH player s have been asking for mor e and mor e

bandwidth. Some player s have converted to MPEG-4 from MPEG-2,

but the cost associated r estricts other player s from doing the same.

y ADVANCEMENTS

To diff er entiate their service and cr eate mor e value for the customer s

the player s ar e banking on visible technological advancements.

Services lik e Mobile and Internet Progr am Recording is an attempt to

conver ge customer experiences. TATA Sk y, SUN Dir ect have

launched High Definition (HD) broadcast channel and other s ar e

expected to follow soon. Videocon have introduced DVD player s and

TVs with integr ated DTH STBs.

LEGAL

The legal r equir ements to get in the DTH industr y have been in place since 2000. As a whole

ther e has not been too much displeasur e in the role of TRAI as the r egulator in the DTH

industr y. But the long gestation period, experienced by all player s to r each profit has caused

sever al voices to rise for mor e r eformation.

y CHANNELS ON A-LA-CARTE BASIS

According to a r ecent order from TRAI, DTH subscriber s will have the

chance to pick a list of channels as they wish, but pay only 150

minimum. The DTH oper ator s have estimated that this will incr ease

their earnings.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 22/42

22 | P a g e

y TAXATION ISSUES

Tax burdens ar e a popular ar ea of complaints. With a cumulative

taxation of over 40%, it is one of the most heavily taxed sector s in the

countr y.

y License Tax ± 10% of Gross Revenue

y Service Tax ± 12.36% of subscription and r ental income from STBs

y VAT ± 12.5% provision of STB to the consumer

y Entertainment Tax ± 10-12% (varies in States)

Deliber ations ar e ongoing for r educing the License Tax to 6%. A

uniform Goods and Services Tax (GST) from April 2011 would

somewhat lessen the burden.

y LEVEL PLAYING FIELD

The cause of the DTH industr y in India is advocated by the DTH

Association of India (DOAI). Recently TRAI told Broadcaster s that

they can char ge DTH service provider s only 35% of the f ee that they

char ge r egular Cable TV oper ator s. Also

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 23/42

23 | P a g e

C. Company and Competitor Analysis

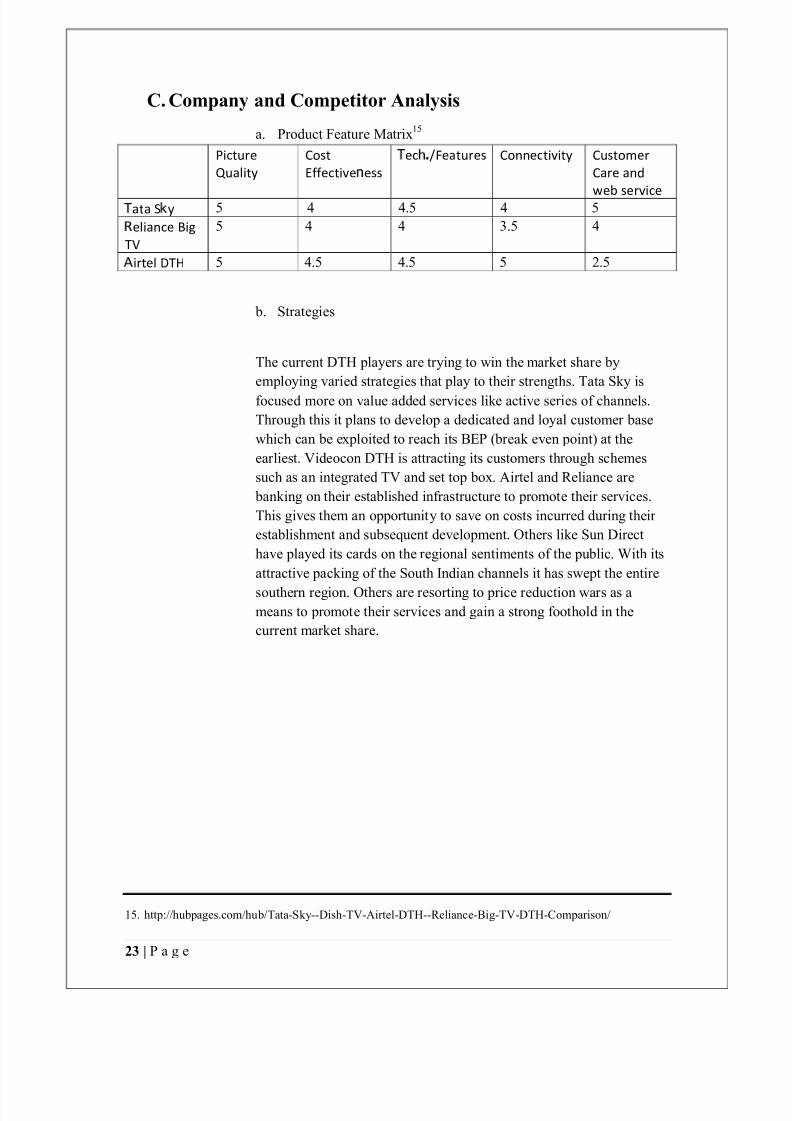

a. Product Featur e Matrix15

Picture

Q uality

Cost

Eff ective ¤ ess

¥

ec¦ §

/Features Connectivity Customer

Care and

web

service ¥

ata S ̈ y 5 4 4.5 4 5

© eliance Big

TV

5 4 4 3.5 4

irtel DTH 5 4.5 4.5 5 2.5

b. Str ategies

The curr ent DTH player s ar e tr ying to win the mark et shar e by

employing varied str ategies that play to their str engths. Tata Sk y is

focused mor e on value added services lik e active series of channels.

Through this it plans to develop a dedicated and loyal customer base

which can be exploited to r each its BEP (br eak even point) at the

ear liest. Videocon DTH is attr acting its customer s through schemes

such as an integr ated TV and set top box. Airtel and Reliance ar e

banking on their established infr astructur e to promote their services.

This gives them an opportunity to save on costs incurr ed during their

establishment and subsequent development. Other s lik e Sun Dir ect

have played its cards on the r egional sentiments of the public. With its

attr active packing of the South Indian channels it has swept the entir e

southern r egion. Other s ar e r esorting to price r eduction war s as a

means to promote their services and gain a strong foothold in the

curr ent mark et shar e.

15. http://hubpages.com/hub/Tata-Sk y--Dish-TV-Airtel-DTH--Reliance-Big-TV-DTH-Comparison/

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 24/42

24 | P a g e

c. Mark eting Mix

1. Pricing

Some player s ar e using price to attain customer s while

other s ar e r elying on value services. Comparison on thisbasis is difficult as it varies on what pack ages the DTH

provider gives. But on a whole Tata Sk y is deemed to be

expensive and Sun Dir ect to be cheapest.

2. Promotion

Most of the DTH provider s have bank ed on the Bollywood

X-f actor to promote themselves.

TATA Sk y

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 25/42

25 | P a g e

Airtel DTH

Videocon DTH

Apart from these the also tr y to tak e advantage of the sport

fr enzy nation lik e our s. Time and again special off er s ar e

announced befor e sporting events lik e FIFA Wor ld Cup,

Commonwealth Games, Delhi and may be in the 2011 ICC

Wor ld Cup. Tata Sk y plans to launch its HD pack age for

sports along with one of these events. These opportunities

provide a good launch platform for the provider s to kick

start their oper ations.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 26/42

26 | P a g e

3. Placing

The best examples of placing can be seen in Sun Dir ect.

They have concentr ated on South India and have penetr ated

the mark et by their cheap and attr active pack ages especially

for the r egional (south Indian) channels. The r est have a

pan-India pr esence wher e they ar e not able to connect to thelocal people as well as Sun Dir ect has been able to do in

south India. So the provider s concentr ate on customer

satisf action as a whole to place their product.

4. Product

The scope for product diff er entiation is not much in such a

mark et. The after sales service is one ar ea wher e the player s

can pitch in to lur e their customer s. Also much depends on

the value added f eatur e and services that sets your product

diff er ent from other s. Such as live r ecording, active series

in Tata Sk y.

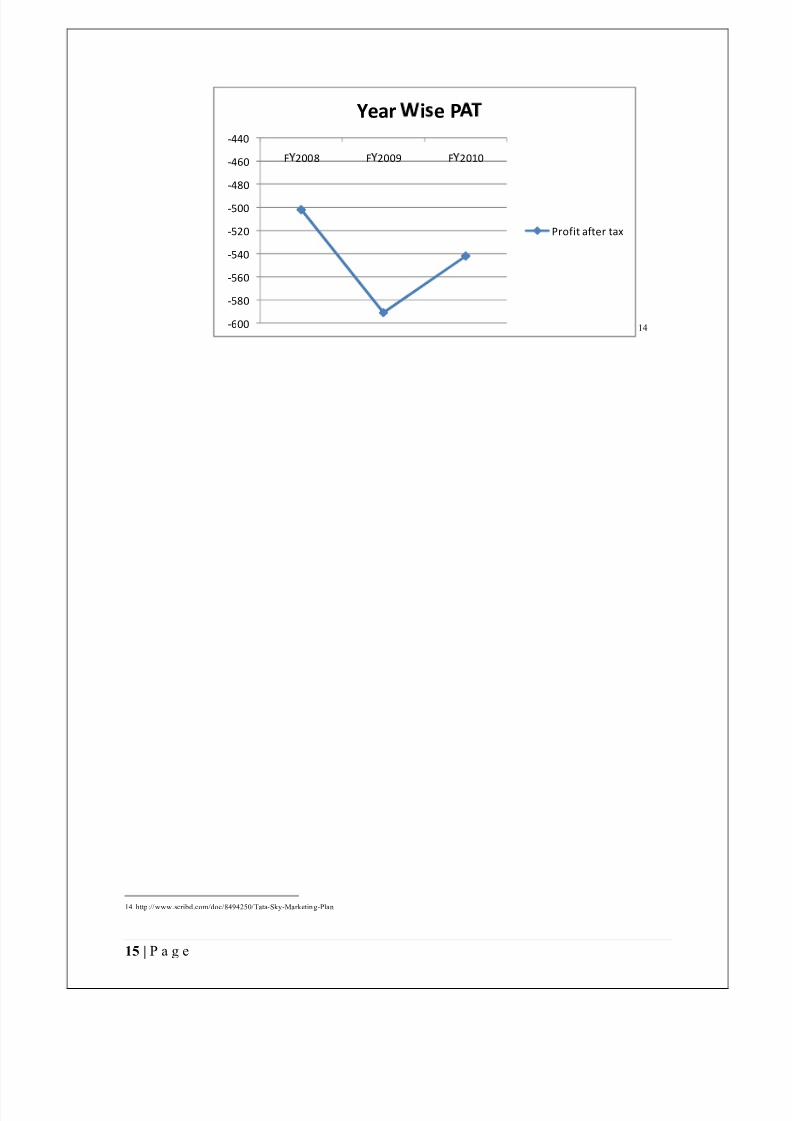

d. Profits

The DTH sector is r elatively a new field and it r equir es high capital

investment. The gestation period is also high. It tak es about 5-6

year s and about 6 million customer s befor e profits begin to show

up in the balance sheets. Most of the companies ar e running in

losses. Only Dish TV and Tata Sk y will be posting profits soon.

Consumer acquisition costs could var y between Rs 1,700 and Rs8,000 per subscriber

15. The industr y aver age is mor e lik e Rs 2,400-

4,000 per subscriber . The biggest part of this cost is the set-top-box

(STB). Hence, the focus is on how to r etain customer s so that the

BEP is r eached soon.

e. Value chain

The value chain for this service can be divided in segments lik e

Technology, content provided, deliver y (customer service), price

and post sales services.

In the technology part Tata Sk y was the 1st one to launch theconcept of r ecording live TV in India. After which r est followed

suit. Now it has also lined up the launch of HD services (NGC and

Discover y). These initiatives play a crucial role in developing a

positive f eeling about the company amongst the customer s and the

company could have a good customer base.

15 DTH industr y: A glimpse of profits at last! Vanita K ohli -Khandek ar / New Delhi November 9, 2009

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 27/42

27 | P a g e

On the content front the DTH player s don¶t have many variables to

play with as it is dictated by the channel provider s and the mark et

pr ef er ences. The content pr ef er ences diff er from place to place and

hence it has to tr ade-off at certain places.

On the deliver y front all player s ar e equally strong with deliver y

promised within 24 hr s. So anyone lagging on this bench mark has

to pay heavily.

f . Diff er ential Advantage for each company

a. Ability to design new products:

As discussed ear lier in this field the product development is not

much and mor e depends on value added f eatur e, Tata sk y is the

leader as of now when it comes to value added services.

b. Ability to deliver the service:

All the player s ar e on an equal footing with online f acilities being

provided by all.

c. Ability to mark et:

Mark eting medium is usually through electronic showrooms/

r etailer s for most of the DTH companies. Mark eting is also based

on the tar geted segment lik e r egional mark ets or pan-Indiapr esence e.g. Sun Dir ect Vs the Rest.

d. Ability to finance:

This basically depends on how the br and in viewed by the public if

it has to source its money from the people. In case of Tata Sk y. The

br and of Tata gives it huge cr edibility and it also has the backing of

the SKY group of companies. For provider s lik e Big TV and Airtel

DTH, the par ent company (r eliance, bharti) itself can tak e car e of the finances.

e. Ability to manage:

The f act that many of the DTH player s have a huge par ent

company with year s of experience behind them gives them an edge

to manage their activities pr etty well.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 28/42

28 | P a g e

g. Expected futur e str ategies

With the DTH mark et set to double by 2012, all the player s will be

looking to consolidate their position and would lik e to see the

profits go gr een from r ed. For this one k ey ar ea will be the

customer r etention plans and new value added services being

provided. Price war s may also be a way to win the mark et shar e.Player s could also look to expand their foothold in rur al ar eas and

r emote ar eas of India to expand their mark et.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 29/42

29 | P a g e

D. Customer Analysis

a. Segmentation Str ategy

Mark eter s have gener ally been moving from serving lar ge mass

mark ets to specifications of smaller segments with customized mark eting progr ams. The choice in front if the mark eter s at Tata Sk y

for the segmentation wer e:

y Mass Mark et

y Mark et Segment

y Mark et Niches

y Individuals

Tata Sk y has gone in for the mark et segments categor y as it doesn¶t

want to be viewed as an ever yday product.

The gener al descriptor s used for the segmentation of the mark et as

used by the mark eting team of Tata Sk y ar e:

1. Demogr aphic Factor s:

The DTH industr y on India has been found to be f avour ably

inclined towards the middle aged working class individuals (DINK

and DIOK f amilies). The r ecording option that comes along with

the DTH provider s seems to be agr eeable with the lif estyle of the

working class.

2. Geogr aphic Factor s:

The ur ban and rur al mark ets have to be tr eated separ ately because of

the level of disposable income. DTH industr y has a distinct footprint in

the rur al mark et.

3. Lif estyle:

The customer s should be profiled based on the type of lif estyle theylead. Tata Sk y can be segmented as a lif estyle product wher ein it

becomes a symbol of a thriving lif estyle.

Besides the basic descriptor s segmentation could also have been done

on the basis of the customer¶s behaviour or r elationship with the

product.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 30/42

30 | P a g e

y Benefit based segmentation: Performance , Ver satility or Price

y User status: User vs. Non-user

y TV usage rate: Light , medium or heavy user

b. Consumer Behaviour

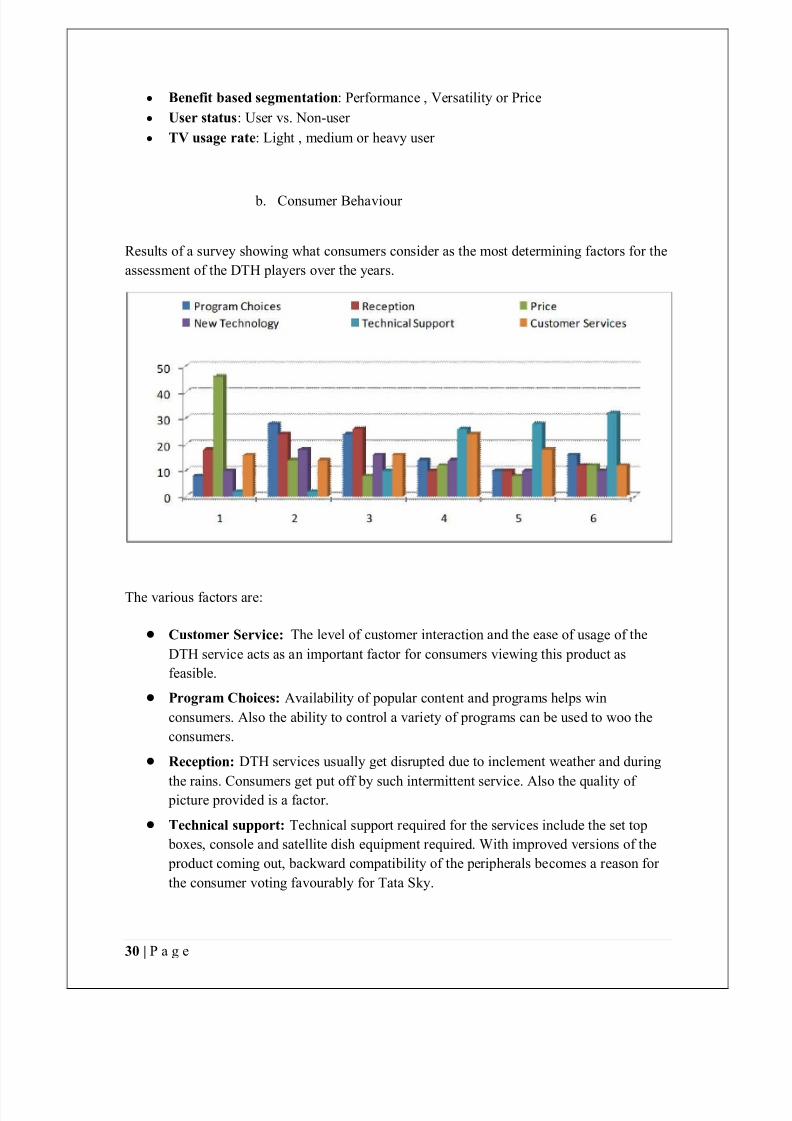

Results of a survey showing what consumer s consider as the most determining f actor s for the

assessment of the DTH player s over the year s.

The various f actor s ar e:

y Customer Service: The level of customer inter action and the ease of usage of the

DTH service acts as an important f actor for consumer s viewing this product as

f easible.

y Program Choices: Availability of popular content and progr ams helps win

consumer s. Also the ability to control a variety of progr ams can be used to woo the

consumer s.

y R eception: DTH services usually get disrupted due to inclement weather and during

the r ains. Consumer s get put off by such intermittent service. Also the quality of pictur e provided is a f actor .

y Technical support: Technical support r equir ed for the services include the set top

boxes, console and satellite dish equipment r equir ed. With improved ver sions of the

product coming out, back ward compatibility of the peripher als becomes a r eason for

the consumer voting f avour ably for Tata Sk y.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 31/42

31 | P a g e

y Price: The consumer s of the segment tar geted ar e becoming incr easingly price in-

sensitive as they want quality product and ther e emphasis is on performance than n

price. However, for the rur al mark et price still r emains an order winner .

c. Tar geting

Tata Sk y wants to go in for value based tar geting in order to incr ease its footprint

beyond the Tier-I cities and also so that it is able to br eak even quick ly. Value for money from the working class:

Tata Sk y wants to tar get the DINK and the DIOK categories in the ur ban sector

because it wants to acquir e µvalue¶ customer s so as to incr ease the ARPU (Aver ageRevenue per User). These working class f amilies also miss their TV progr ams and

thus the r ecording f eatur e and the playback f eatur e of Tata Sk y can be a hugeattr acting f actor for them. This type of tar geting happens mainly in the ur ban sector .

First time users vs. user

Consumer s can also be tar geted based on those people who can be converted from the

usage of cable TV and want to be able to dictate the content they want to view. These

people can be wooed with the promise of gr eater control over viewer ship and content

management of the progr ams viewed.

Existing user s can be categorised into those who want to go in for sustained

r elationships and those who want to µtr ade- up¶ to newer ver sions of Tata Sk y lik e

HDTV and Tata Sk y+.

TV viewer ship in India is lower than the global levels. So on demand movie and

r ecording f acility can be promoted as people usually do not spend hour s in front of the

TV. Hence they would want better control over the content they view.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 32/42

32 | P a g e

16

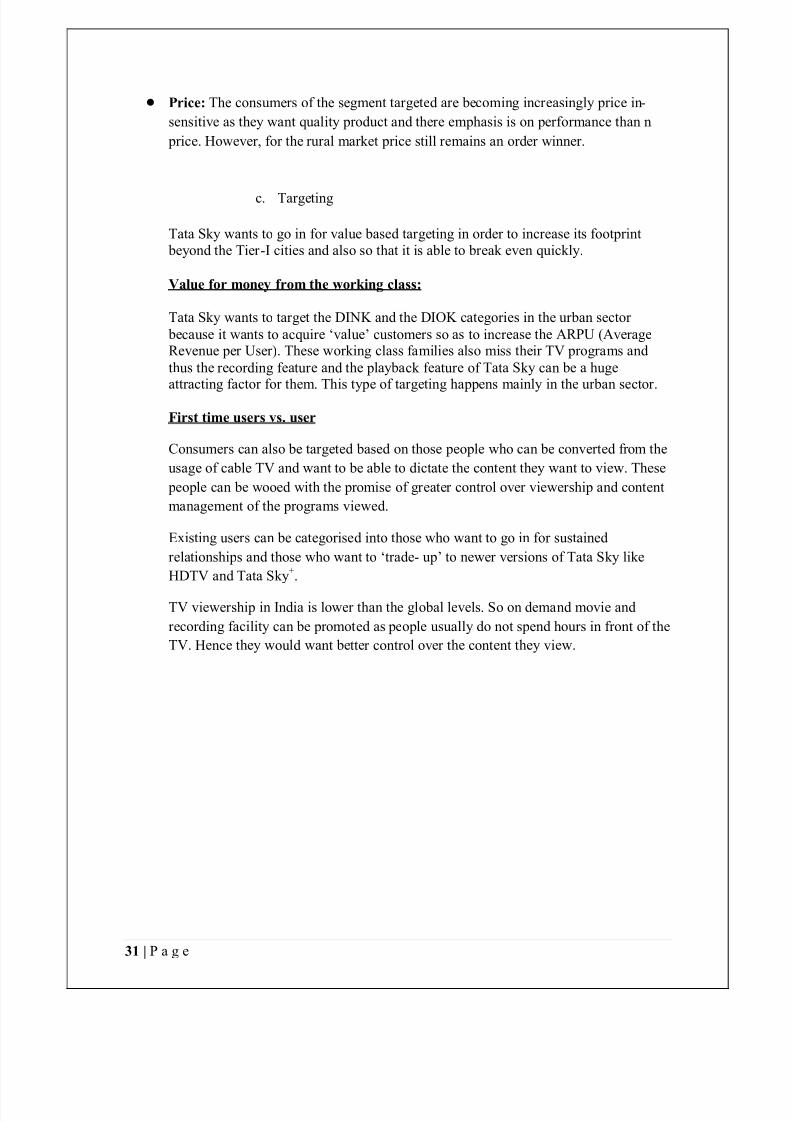

d. Positioning

Positioning of DTH services happens k eeping in mind the product portfolio of the

br and. The product is mainly pr esented as a lif estyle product and positioned as an

³Edutainment´ pack age.

The product has also been making inroads into the rur al mark et wher e it has been

improving its pr esence. The product is mainly positioned for the middle class so as to

also have r eturns from the customer and maximize customer equity.

16 http://micamedia.files.wordpr ess.com/2009/07/time-spent-viewing-tv.jpg%3Fw%3D408%26h%3D302

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 33/42

33 | P a g e

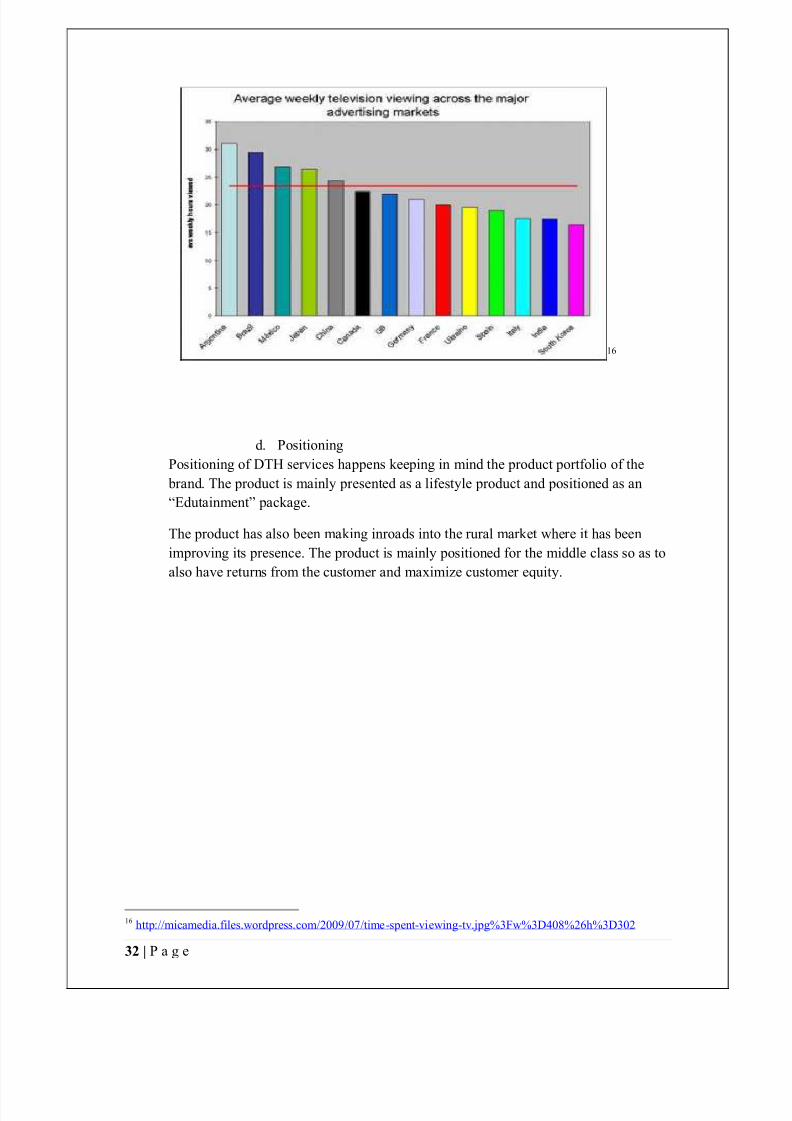

The channel partner s for Tata Sk y also help in proper positioning of the product and

add to the convenience of r eaching the product for the consumer s.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 34/42

34 | P a g e

E. Assumptions in Planning Process

a. Mark et Potential

y India will become the lar gest DTH mark et in the wor ld by 2012, overtaking theUnited States, and boast of 45 million DTH subscriber s by 2014

y R ur al TV mark et to incr ease by 3-4 million ever y year

b. For ecast Assumptions

y Monthly ARPUs of DTH player s will climb to Rs 220 by 2014

y Player s in the DTH Industr y will move out of pricing str ategy towards value addition

str ategy

y Government r egulation for expansion in the for eign countries will be r elaxed y Addition of KU bands by the government due to incr ease in demand

y VAS (value added services), HDTV (high definition television) will provide a boost

as well as the impact of up-selling to new tier s

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 35/42

35 | P a g e

F. Strategy

a. Cor e Str ategy

Our str ategy for Tata sk y is on the line of mobile phones. Mobile phone started as a basic

communication device. Due to incr ease in competition for capturing the mark et shar e, the

service provider s r esorted to price war . This dir ectly aff ected their profit mar gins. In

order to captur e mark et shar e, Player s started diff er entiating their products with added

f eatur es lik e SMS, Mp3 player, Blue Tooth etc. Similar ly for Tata sk y, we ar e planning to

go beyond the customer demand and providing them with added f eatur es.

These points ar e discussed below

b. Customer Tar gets

Tata sk y has gr eat potential in entering new mark ets lik e

a) R ur al Mark ets

R ur al television mark et is incr easing by 3-4 million per year . Only 2-3 % rur al mark et

has access to cable network .

b) Entering neighbouring countries provide license policies of those countries ar e

compatible.

c) Entering tr avel ar ea mark et by collabor ating with long distance buses etc.

d) Tie up with hotels and r estaur ants provides huge business opportunity for Tata Sk y.

c. Product/Service Featur es

y Common dish for multiple f lats in a society having multiple television sets.

y Inter active services based on stock mark ets.

y Inter active video games including multi player games (with console).

y Inter active R ur al mark et services which will give r egular updates about prices of

diff er ent commodities to f armer s.

y Use of r egional languages in the guide panel for diver se customer s.

y Enhanced compatibility with digital equipments lik e laptops for daily use.

y Extensive use of Radio r eception as one of its services.y Introduction of fr ee channel for playing of on demand songs.

y Tata Sk y can act as a conver gence provider bundling services such as f ax, voice and

internet.

Ways to improve quality services

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 36/42

36 | P a g e

Technical glitches aroused due to r ain cannot be fully r esolved. But they can be r educed

by using water proof coating on the antenna and also incr easing tr ansmission power .

While incr easing customer base is important for growth of the company, Retaining

customer should be of par amount importance to Tata sk y.

Proper customer grievances r edr essal mechanism should be adopted and issues should ber esolved at the ear liest.

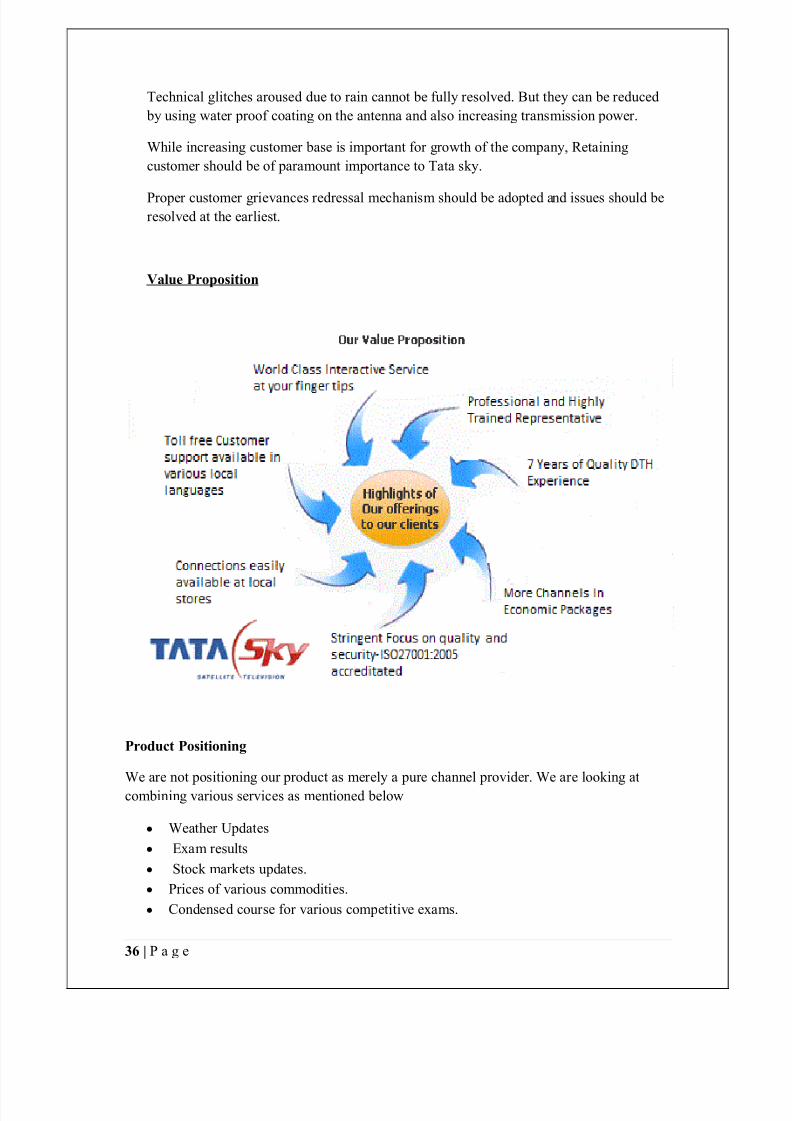

Value Proposition

Product Positioning

We ar e not positioning our product as mer ely a pur e channel provider . We ar e looking at

combining various services as mentioned below

y Weather Updates

y Exam r esults

y Stock mark ets updates.

y Prices of various commodities.

y Condensed cour se for various competitive exams.

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 37/42

37 | P a g e

G. Strategy-Marketing Communi ations Programmes

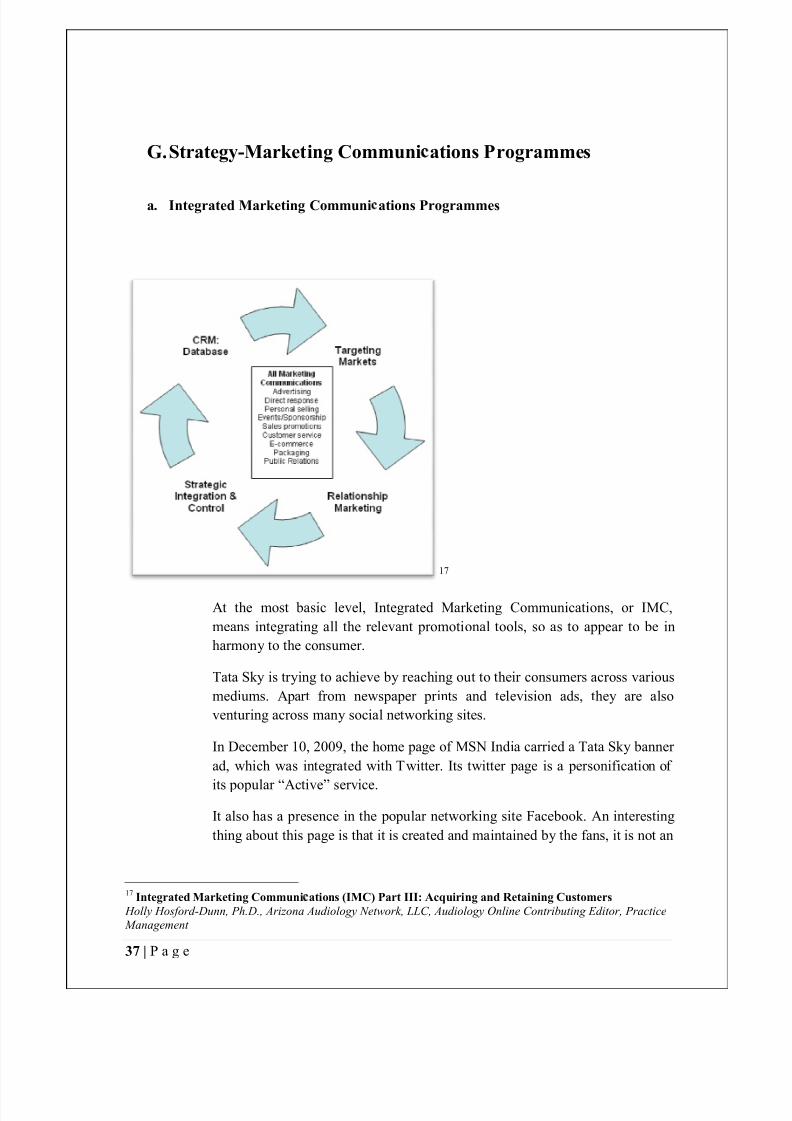

a. Integrated Marketing Communi ations Programmes

17

At the most basic level, Integrated Marketing Communications, or IMC,

means integrating all the relevant promotional tools, so as to appear to be in

harmony to the consumer .

Tata Sk y is tr ying to achieve by reaching out to their consumer s across var ious

mediums. Apar t from newspaper pr ints and television ads, they are also

ventur ing across many social network ing sites.

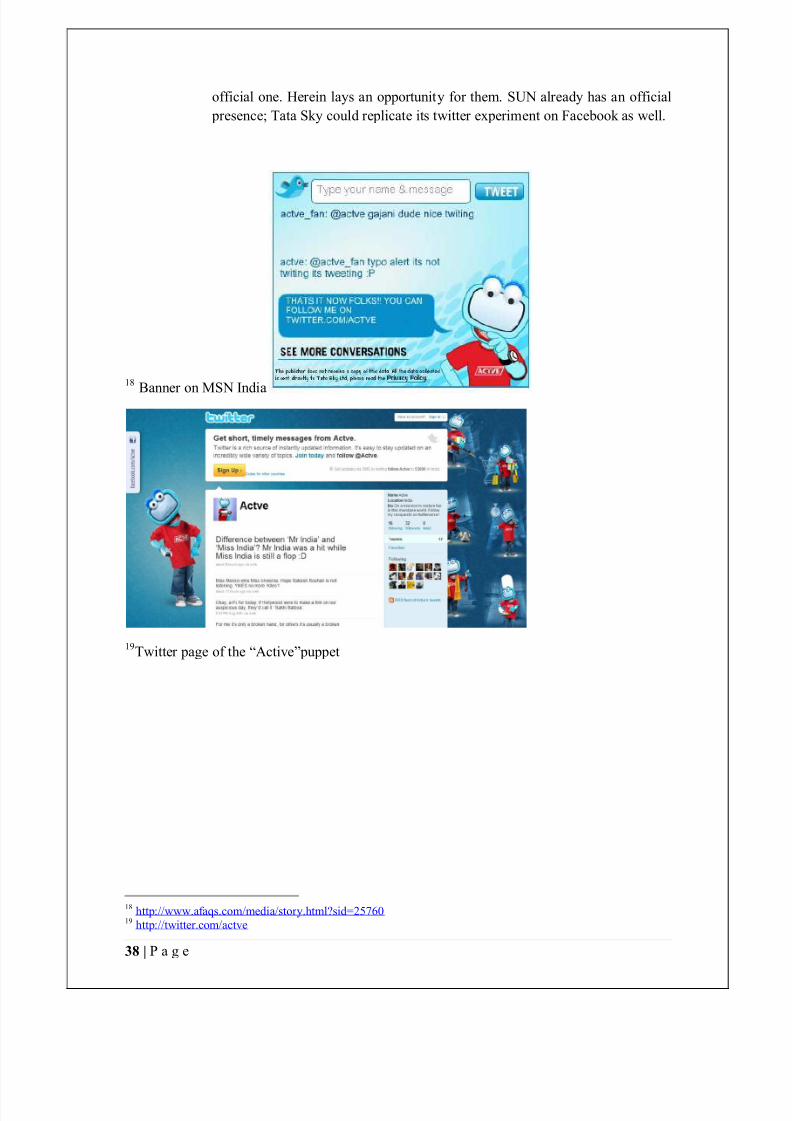

In December 10, 2009, the home page of MSN India carr ied a Tata Sk y banner

ad, which was integrated with Twitter . Its twitter page is a per sonif ication of

its popular ³Active´ service.

It also has a presence in the popular network ing site Facebook . An interesting

thing about this page is that it is created and maintained by the fans, it is not an

17

Integrated Marketing Communi ations (IMC) Part III: Acquiring and Retaining Customers

Holly Hosford-Dunn, Ph.D., Arizona Audiology Network, LLC, Audiology Online Contributing Editor, Practice

Management

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 38/42

38 | P a g e

official one. Her ein lays an opportunity for them. SUN alr eady has an official

pr esence; Tata Sk y could r eplicate its twitter experiment on Facebook as well.

18

Banner on MSN India

19Twitter page of the ³Active´puppet

18

http://www.af aqs.com/media/stor y.html?sid=25760 19 http://twitter .com/actve

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 39/42

39 | P a g e

20Facebook page cr eated by f ans

b. Pricing Strategy

With prolif er ation of the DTH mark et and the competitor s gunning to captur e the

mark et, all the DTH player s have r esorted to cutting prices in existing off erings as

well as new off erings as HD services. It has r ecently launched its HD services at a

ver y aggr essive price of Rs 259921

. Compar ed to other s (SUN-Rs 9990, Reliance- Rs

7490, and Dish TV- 5999) it is the cheapest and is expected to give rise to another

price war . But it is also expected to captur e a lot of initial mark et because of the

cheaper positioning.

Apart from aggr essive pricing some other options that Tata Sk y can consider ar e:

y Starting Post Paid services wher e the customer gets a bill at the end of thestipulated bill period instead of paying up when the balance runs out. This will

ensur e that the customer doesn¶t stop his viewing experience even for some

time.

y Off er r eward for r ef err als to customer s who bring in other s to subscribe too.

y Start special pack ages in the same line as the telecom service provider s,

depending on special holidays or f estivals.

c. Channel Strategy

Using local talent:

At pr esent TATA Sk y can be subscribed from designated showrooms and dealer s.

The local Cable TV oper ator s ar e seen as a thr eat to the DTH industr y. If these

oper ator s can be brought under fold then the existing distribution channel can be

20

http://www.f acebook .com/pages/Tata-Sk y/109676475716872 21 http://www.thehindubusinessline.com/2010/06/15/stories/2010061551112000.htm

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 40/42

40 | P a g e

r eused. As these people will be well known in the locality, a lot of f amilies will be

easy converts from cable to Tata Sk y. The distributor s can be per suaded with

f avour able terms to become Tata Sk y employees.

Using rur al structur e:

In villages, the village self-government structur e is highly r espected. The villageadministr ator s can be inf luenced to experience and further advocate the positives of

Tata sk y to the villager s.

d. Customer Management Strategy

With the number of choices incr easing daily and the ease of changing to another DTH

service provider also incr easing, focus is incr easing mor e and mor e on Customer

loyalty and r etention. The use of Customer Relationship Management (CRM) as a

str ategy for nurturing and managing a company¶s inter actions with customer s is

coming to the for efront.

Tata Sk y has selected Siebel, leader s in CRM softwar e, to support the oper ations

across the ar eas of call centr es and field service oper ator s, customer order

management and product configur ation.22

22 http://www.tatask y.com/corpor ate-info.html

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 41/42

41 | P a g e

H. R eferences 1. http://www.tatask y.com/corpor ate-info.html

4. http://en.wikipedia.or g/wiki/Tata_Sk y

5. Article on News Center, 10th

March 2010

6. Excerpts of interview with Mr . Vikr am Mehta (Chief Mark eting Officer, Tata Sk y) published

in Business Line, 7th Januar y 20107.

7. http://business.r ediff .com/r eport/2010/apr/06/tata-sk y-str ategy-to-attr act-mor e-customer s.htm

8. http://www.tatask y.com/

9 McK insey Global Institute

10 http://www.pluggd.in/dth-industr y-in-india-analysis-297/

11 http://www.scribd.com/doc/26464799/MRP-DTH-Industr y-in-India-Dir ect-to-Home-Service

12 http://www.scribd.com/doc/8494250/Tata-Sk y-Mark eting-Plan

13 http://www.scribd.com/doc/8494250/Tata-Sk y-Mark eting-Plan

14 http://www.scribd.com/doc/8494250/Tata-Sk y-Mark eting-Plan

15. http://hubpages.com/hub/Tata-Sk y--Dish-TV-Airtel-DTH--Reliance-Big-TV-DTH-Comparison/

15 DTH industr y: A glimpse of profits at last! Vanita K ohli-Khandek ar / New Delhi November 9,

2009

16 http://micamedia.files.wordpr ess.com/2009/07/time-spent-viewing-

tv.jpg%3Fw%3D408%26h%3D302

17 Integrated Marketing Communications (IMC) Part III: Acquiring and R etaining Customers

Holl Hosf ord-Dunn, Ph.D., Ar i ona Aud iol ogy N twork, LLC , Aud iol ogy Online C ont r i

uting Ed it or,

Practice Management

18 http://www.af aqs.com/media/stor y.html?sid=25760

19http://twitter .com/actve

8/7/2019 Tata_Sky_Marketing_Strategy_Report_final

http://slidepdf.com/reader/full/tataskymarketingstrategyreportfinal 42/42

20 http://www.f acebook .com/pages/Tata-Sk y/109676475716872

21 http://www.thehindubusinessline.com/2010/06/15/stories/2010061551112000.htm

21 http://www.tatask y.com/corpor ate-info.html