Embed Size (px)

Citation preview

TAB

LE O

F C

ON

TEN

TS

Table of

Contents

Introduction 4

Jordan A Regional Gateway 6

Stable And Growing Economy 10

Competitive And Educated Workforce 16

Commitment To Investors’ Success 22

Reliable Infrastructure 28

Quality Of Life 34

TURN TO TURN TO JORDAN

In driving its growth, Jordan relied on harnessing its immense human capital. Boasting the most successful education system in the region, Jordan has excelled on many different levels. Today, Jordan has the highest literacy and female education rates in the region, the largest number of engineers relative to the population in the world, and is home to the largest number of doctors and nurses relative to the population than any other country in the region.

Jordan continues to leverage its demographic blessings, with 70% of the population under the age of 30. Jordan’s youth are well-educated and motivated with training in both industry and services. Jordan also possesses a high number of technical, highly skilled, and ICT proficient personnel.

Jordan's investment friendly environment is further supported by a modern, well-developed infrastructure and telecommunications network. The country’s three airports provide ready access to many international destinations, while the sea port in Aqaba provides a key access point for transit and international trade.

Special economic and development zones established in key locations across the country offer a wide range of economic incentives to investors including specialized business clusters, reliable infrastructure, highly advantageous tax structures, and proximity to resources and markets.

Capitalizing on its highly qualified graduate pool, Jordan has seen the emergence of several knowledge and skills centered industries such as ICT, Outsourcing, Pharmaceuticals, Healthcare, Clean Tech and Light Manufacturing.

Jordan is home to some of the most renowned cultural and archeological sites, and is blessed with security and stability, as well as year-round pleasant weather leading to a moderate and highly desirable quality of life.

Jordan

Capitalizing on its robust and liberal economy, its stability and security, its immense human capital, and its high quality of life, coupled with the ongoing economic liberalization process, Jordan is well positioned as a regional investment gateway.

Decades of sound macroeconomic management and sustained structural reforms, including legislative, regulatory, and judicial reforms, have positioned Jordan as a magnet for capital and a robust platform for business profitability. Prudent fiscal and monetary policies have enabled healthy and sustained economic growth, reduced external debt as a percentage of output by more than half, while inflation has been kept at low levels. Coupled with open and liberal market policies, Jordan has positioned itself as an ideal base for export-led growth to regional and international markets. Jordan's unique trade and framework agreements offer investors access to a core market of 320 million consumers and a global market of over one billion consumers.

«For foreign companies that enter emerging markets, there are valuable connections to: in-country markets and regional trading networks; to a competitive workforce; to important knowledge about regional cultures and customers. Such businesses find significant trade and investment opportunities - especially in economies like Jordan's, which are on a path of modernization and growth ... and which are regional gateways ... in our case, to the 300-million people of the Arab World.»

His Majesty King Abdullah II

TUR

N T

O JO

RD

AN

4 5

TURN TO

JOR

DA

N A

REG

ION

AL

GA

TEW

AY

Jordan is strategically situated at the convergence of the three continents of Europe, Asia, and Africa. It is therefore an ideal gateway for the MENA region and beyond.

The country also boasts high political and economic stability. The current system of the Government is parliamentary with a hereditary monarchy. Since 1989, Jordan’s rulers maintained regular parliamentary elections for a house of assembly and have made significant efforts to ferment political liberalization. Members sit for four year terms, with the next election scheduled for November 2010. An appointed senate is also in place, with members chosen by the King to sit for four-year terms.

Jordan enjoys a Mediterranean climate and four seasons of temperate weather; in fact, Amman is considered to be the coldest Arab capital, with an average temperature of 23.2 oC due to its location on a mountainous range that is 1,029 meters above sea level.

Capitalizing on its strategic position, Jordan has adopted a policy of building global partnerships and institutional relationships that would allow for free trade and global market access. As a result of these open and liberal policies, the Kingdom today offers investors access to over one billion consumers in strategic regional and international markets.

Jordan secured an Association Agreement with the European Union, gained membership to the World Trade Organization in record time, and was the first Arab country to sign a free trade agreement with the United States. Moreover, and as a signatory to the Greater Arab Free Trade Agreement, Jordan has preferential access to most Arab markets including GCC countries. Jordan also signed the Qualifying Industrial Zones Agreement (QIZs), with the U.S., which allow products developed in special designated areas access to the U.S. market, free of quotas and tariffs.

Jordan

A Regional Gateway Location:Situated between latitudes 29 and 33 north and longitudes 34 and 39 East

Time Zone:2 -3 hours ahead of Greenwich timing in Winter and Summer times respectively. Countries within one time zone include those in Eastern Europe and GCC countries

Total Area:89,342 km2²; Land 88,802 km2 and Water 540 km2

Elevation Extremes:Lowest point: Dead Sea - 416 m below sea levelHighest point: Jabal Umm Al Dami - 1,854 m

Weather:Summers in Jordan are moderate and dry, while winters are cool and rainy Amman Avg High oC (F): 23.2 (74)Amman Avg Low oC (F): 11.9 (53)

Natural Disasters:Jordan has a low risk for natural disasters such as earthquakes and floods Direct Flights to:New York, Chicago, Madrid, London, Dubai, Paris, Frankfurt, Cairo, Zurich, Geneva, Amsterdam, London, Hong Kong and Bangkok, among others

WORLDLOCATION MAP: JORDAN

SPRINGBOARD TO REGIONAL AND INTERNATIONAL MARKETS

TURN TO JORDAN

Section 1 6 7

JORDAN

TURN TO

JOR

DA

N A

REG

ION

AL

GA

TEW

AY

PAKISTAN in negotiation phase. (Approximate population 166 million)

MERCOSUR in negotiation phase. (Approximate population 240 million)

CANADA - Canada has signed a free trade agreement with Jordan, its first with an arab country on june 2009. The agreement is still pending ratification from the Canadian parliament. (Approximate population 33 million)

JORDAN-EU ASSOCIATION AGREEMENT came into force in 2002, the agreement aims at creating a free trade area by end of 2010. (Approximate population 500 million)

GAFTA establishment of the Arab free trade zone by january 2005. (Approximate population 322 million)

TURKEY - The Jordanian-Turkish free trade agreement (FTA) was signed between the two countries in december 2009. The agreement is in the last stage of ratification in Turkey and it will enter into force at the beginning of 2011. (Approximate population 74 million)

C O M E S A Jordan has signed an MOU as a preliminary step towards full membership, it was accepted as an observer to the comesa secretariat general in november 2006. (Approximate population 370 million)

EUROPEAN FREE TRADE ASSOCIATION entered into force in January 2002, it aims at setting up a fully operational free trade area over a period of 12 years. (Approximate population 13 million)

USA - JUSFTA has been in force since 2001. It was the first free trade agreement negotiated by the US with an Arab country, and the fourth with any country in the world. A complete free trade agreement between the two countries will be achieved by january 1, 2010. (Approximate population 300 million)

SINGAPORE signed in may 2004; the agreement aims at the gradual elimination of customs duties over a period of 10 years. (Approximate population 5 million)

AGADIR entered into force on july 6th 2006, the agreement allows for diagonal accumulation of origin amongst its member countries. (Approximate population 124 million)Jordan also signed FTAs with most arab countries including: the palestinian national authority, Algeria, Syria, Tunisia, Egypt, Sudan, UAE, Kuwait and Bahrain. Jordan also signed preferential agreements with Morocco, Lebanon and Kingdom of Saudi Arabia

TRADE LINKAGES THROUGH FREE TRADE AGREEMENTS

SIGNED TRADE AND FRAMEWORKS AGREEMENTS FREE TRADE AND FRAMEWORKS AGREEMENTS IN THE PIPELINE

TURN TO JORDAN

8 9

TURN TO

STA

BLE

AN

D G

RO

WIN

G E

CO

NO

MY

Stable And

Growing Economy

Jordan’s strategy has been to create a modern economy that is based on knowledge and successful global integration. To this end, the country adopted an aggressive, yet comprehensive and integrated approach towards development that relies on the active participation of the private sector, as well as the creation of a strong and thriving investment climate. Jordan’s commitment to attract foreign investment is also demonstrated through focusing on creating an enabling investment environment for foreign capital in all sectors.

A liberal and open economy has underpinned Jordan’s economic development. Through maintaining a stable macroeconomic environment, a liberalizing economy has allowed the private sector to drive growth and development. Over the last two decades, through prudent fiscal and monetary policy, inflation has been kept at low annual

average rates ranging between 3-5% while the currency remained stable, thus providing private sector companies with the macroeconomic environment for sound business planning.

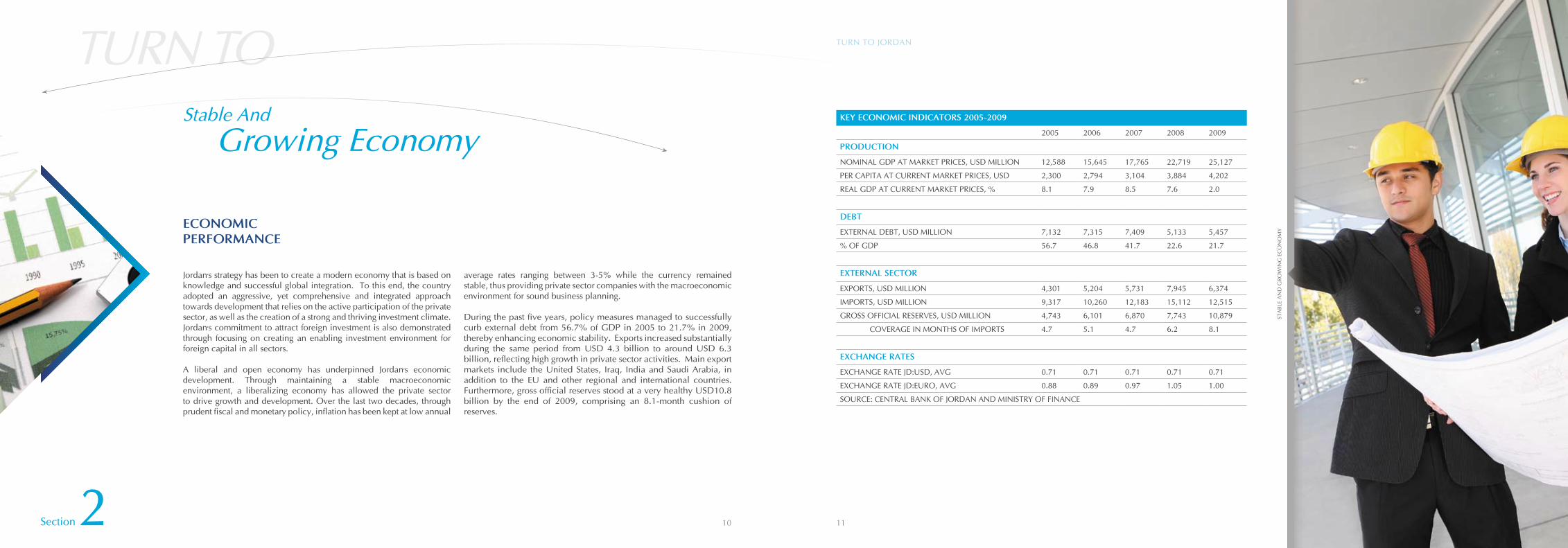

During the past five years, policy measures managed to successfully curb external debt from 56.7% of GDP in 2005 to 21.7% in 2009, thereby enhancing economic stability. Exports increased substantially during the same period from USD 4.3 billion to around USD 6.3 billion, reflecting high growth in private sector activities. Main export markets include the United States, Iraq, India and Saudi Arabia, in addition to the EU and other regional and international countries. Furthermore, gross official reserves stood at a very healthy USD10.8 billion by the end of 2009, comprising an 8.1-month cushion of reserves.

ECONOMIC PERFORMANCE

TURN TO JORDAN

10 11Section 2

KEY ECONOMIC INDICATORS 2005-2009

2005 2006 2007 2008 2009

PRODUCTION

NOMINAL GDP AT MARKET PRICES, USD MILLION 12,588 15,645 17,765 22,719 25,127

PER CAPITA AT CURRENT MARKET PRICES, USD 2,300 2,794 3,104 3,884 4,202

REAL GDP AT CURRENT MARKET PRICES, % 8.1 7.9 8.5 7.6 2.0

DEBT

EXTERNAL DEBT, USD MILLION 7,132 7,315 7,409 5,133 5,457

% OF GDP 56.7 46.8 41.7 22.6 21.7

EXTERNAL SECTOR

EXPORTS, USD MILLION 4,301 5,204 5,731 7,945 6,374

IMPORTS, USD MILLION 9,317 10,260 12,183 15,112 12,515

GROSS OFFICIAL RESERVES, USD MILLION 4,743 6,101 6,870 7,743 10,879

COVERAGE IN MONTHS OF IMPORTS 4.7 5.1 4.7 6.2 8.1

EXCHANGE RATES

EXCHANGE RATE JD:USD, AVG 0.71 0.71 0.71 0.71 0.71

EXCHANGE RATE JD:EURO, AVG 0.88 0.89 0.97 1.05 1.00

SOURCE: CENTRAL BANK OF JORDAN AND MINISTRY OF FINANCE

TURN TOCOMPETITIVE ATTRIBUTES

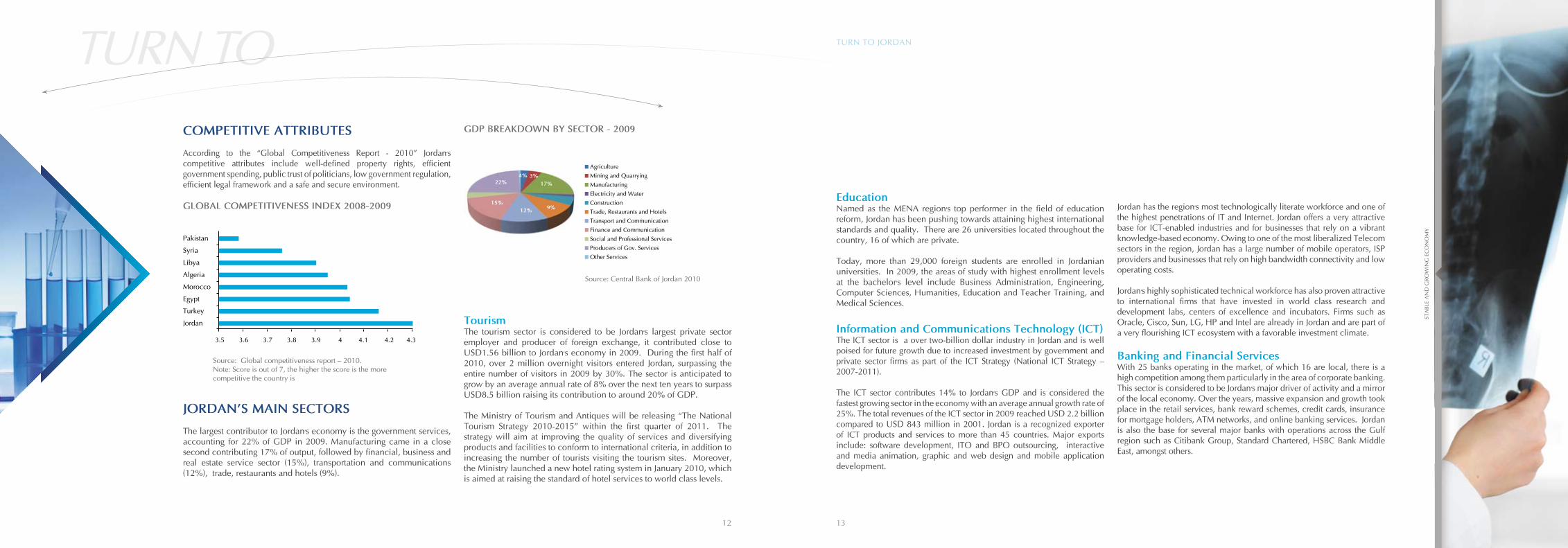

According to the “Global Competitiveness Report - 2010” Jordan’s competitive attributes include well-defined property rights, efficient government spending, public trust of politicians, low government regulation, efficient legal framework and a safe and secure environment.

GLOBAL COMPETITIVENESS INDEX 2008-2009

JORDAN’S MAIN SECTORS

The largest contributor to Jordan’s economy is the government services, accounting for 22% of GDP in 2009. Manufacturing came in a close second contributing 17% of output, followed by financial, business and real estate service sector (15%), transportation and communications (12%), trade, restaurants and hotels (9%).

TourismThe tourism sector is considered to be Jordan’s largest private sector employer and producer of foreign exchange, it contributed close to USD1.56 billion to Jordan’s economy in 2009. During the first half of 2010, over 2 million overnight visitors entered Jordan, surpassing the entire number of visitors in 2009 by 30%. The sector is anticipated to grow by an average annual rate of 8% over the next ten years to surpass USD8.5 billion raising its contribution to around 20% of GDP.

The Ministry of Tourism and Antiques will be releasing “The National Tourism Strategy 2010-2015” within the first quarter of 2011. The strategy will aim at improving the quality of services and diversifying products and facilities to conform to international criteria, in addition to increasing the number of tourists visiting the tourism sites. Moreover, the Ministry launched a new hotel rating system in January 2010, which is aimed at raising the standard of hotel services to world class levels.

STA

BLE

AN

D G

RO

WIN

G E

CO

NO

MY

TURN TO JORDAN

EducationNamed as the MENA region’s top performer in the field of education reform, Jordan has been pushing towards attaining highest international standards and quality. There are 26 universities located throughout the country, 16 of which are private.

Today, more than 29,000 foreign students are enrolled in Jordanian universities. In 2009, the areas of study with highest enrollment levels at the bachelor’s level include Business Administration, Engineering, Computer Sciences, Humanities, Education and Teacher Training, and Medical Sciences.

Information and Communications Technology (ICT)The ICT sector is a over two-billion dollar industry in Jordan and is well poised for future growth due to increased investment by government and private sector firms as part of the ICT Strategy (National ICT Strategy – 2007-2011).

The ICT sector contributes 14% to Jordan’s GDP and is considered the fastest growing sector in the economy with an average annual growth rate of 25%. The total revenues of the ICT sector in 2009 reached USD 2.2 billion compared to USD 843 million in 2001. Jordan is a recognized exporter of ICT products and services to more than 45 countries. Major exports include: software development, ITO and BPO outsourcing, interactive and media animation, graphic and web design and mobile application development.

Jordan has the region’s most technologically literate workforce and one of the highest penetrations of IT and Internet. Jordan offers a very attractive base for ICT-enabled industries and for businesses that rely on a vibrant knowledge-based economy. Owing to one of the most liberalized Telecom sectors in the region, Jordan has a large number of mobile operators, ISP providers and businesses that rely on high bandwidth connectivity and low operating costs.

Jordan’s highly sophisticated technical workforce has also proven attractive to international firms that have invested in world class research and development labs, centers of excellence and incubators. Firms such as Oracle, Cisco, Sun, LG, HP and Intel are already in Jordan and are part of a very flourishing ICT ecosystem with a favorable investment climate.

Banking and Financial ServicesWith 25 banks operating in the market, of which 16 are local, there is a high competition among them particularly in the area of corporate banking. This sector is considered to be Jordan’s major driver of activity and a mirror of the local economy. Over the years, massive expansion and growth took place in the retail services, bank reward schemes, credit cards, insurance for mortgage holders, ATM networks, and online banking services. Jordan is also the base for several major banks with operations across the Gulf region such as Citibank Group, Standard Chartered, HSBC Bank Middle East, amongst others.

Source: Central Bank of Jordan 2010

GDP BREAKDOWN BY SECTOR - 2009

Source: Global competitiveness report – 2010. Note: Score is out of 7, the higher the score is the more competitive the country is

12 13

Agriculture Mining and Quarrying Manufacturing Electricity and Water Construction Trade, Restaurants and Hotels Transport and Communication Finance and Communication Social and Professional Services Producers of Gov. Services Other Services

4% 3%17%

9%12%15%

22%

TURN TO

STA

BLE

AN

D G

RO

WIN

G E

CO

NO

MY

TURN TO JORDAN

14 15

PharmaceuticalsPharmaceutical production is one of Jordan’s largest and most significant industries, recruiting almost 8,000 employees. The total investment in this sector reached USD400 million, with exports exceeding USD$470 million in 2009.

The pharmaceutical industry's importance also stems from the fact that it is Jordan’s only significant “next-generation” industry. A large number of these firms are “home-grown,” with collaboration of international companies.

Jordan’s pharmaceutical manufacturing industry contains modern and well-equipped manufacturing facilities, high quality products in compliance with local and international regulations, manufacturing & formulation expertise as well as an-educated and skilled staff with relatively lower wages. Most companies export to regional countries, and a number of them have achieved international certification, enabling them to sell products in non-traditional and more competitive markets such as Europe and the United States. The future prospects include building strategic alliances and joint ventures, as well as producing biotechnology products, hormones and injectables.

Healthcare and WellnessHealthcare in Jordan is among the best in the Middle East and has quickly emerged as a hub for high-quality and specialized medical care. In 2008, the Kingdom was ranked as number one in the region and fifth in the world as a medical tourism hub by the World Bank (WB) medical tourism experts.

According to the WB report, with treatment costs as low as 25% of those in the West, along with high medical care standards, the abundance of highly qualified physicians and medical staff (More than 90% of the physicians are educated internationally), and medical centers equipped with cutting-edge technology, the sector has witnessed a 10% annual increase in the number of foreign patients since 2004. Jordan’s medical tourism is renowned in areas of oncology, bone marrow transplant, organ transplantation, orthopedic surgeries, cardiac procedures, plastic and neurological surgeries as well as dental treatments to name a few.

In 2009, Jordan attracted more than 200,000 foreign patients, generating over one billion US Dollars. Many hospitals have the national HCAC accreditation and six private hospitals have international accreditation through the Joint Commission International (JCI).

In the area of wellness, Jordan is famous for the Dead Sea with its healing powers, which is being promoted as both a medical and a leisure destination. The Dead Sea is the largest natural spa on earth, and is known for the medical properties of its waters and mud and the curative powers of its salty water. Moreover, the high concentration level of oxygen in the Dead Sea area makes it an ideal cure for patients with asthma or chest problems.

Dead Sea products are known worldwide and are used for beauty and cosmetics. Close by is Maeen Hot Springs, which are known for their thermal powers.

Energy, Water and EnvironmentJordan possesses the essential elements needed for global firms to establish regional hubs for renewable energy and clean technology operations. Jordan’s strengths lie in its location as a potential linking point for oil, gas, and electrical networks in the region, as well as its potential in key verticals such as solar power. Jordan has more than 3,000 hrs/year of solar radiance, making it not only a prime location for solar power generation, but also for the development of components and research technology for the solar industry.

Jordan’s primary value proposition in renewable energy and clean technology lies in its access to a huge market for products and services, its high quality and cost-effective workforce, and its support network for companies/investors in the sector. Coupled with the country’s attractive business-friendly incentives, stable political system, and strategic location, these advantages make Jordan a sound business decision for investment in renewable energy and clean technology.

TURN TO

CO

MPE

TITI

VE

AN

D E

DU

CA

TED

WO

RK

FOR

CE

Modern technologies and methods have been introduced to the educational system to ensure technology proficiency from an early age and to build on a strong foundation in both sciences and humanities. In fact, Jordan is ranked first in the Arab world by the World Bank in terms of educational reform.

English language is taught from the first grade in all public schools and is widely spoken in Jordan, while the Jordanian accent in Arabic is broadly understood within the region. 20.6% of the Government public expenditure is spent on the educational system. The gross enrollment ratio for basic education is 96% and decreases to 68% for the secondary cycle.

Jordan has set a regional example in modernizing and developing its educational system. A number of public-private initiatives have been launched to ensure that the outputs of the educational system meet the evolving demands of the global economy and that students are equipped with the tools to compete and excel in the market place. The initiatives were focused on accelerating Jordan's transition into a knowledge-based economy, enhancing the management and governance of the sector, integrating technology into the classroom, and equipping teachers with the necessary IT skills.

Competitive And

Educated Workforce

Source: Ministry Of Higher Education And Scientific Research 2010

JORDAN’S EDUCATIONALSYSTEM

Being a country with limited natural resources, Jordan realizes the importance of capitalizing on its abundant human resources to foster economic growth and development. With a population of almost 6 million that is growing at approximately 2.2% per year, Jordan boasts a relatively young population with almost 70% under the age of 30.

Jordan has built one of the most successful education systems in the region. The country currently has the highest regional literacy rate of 92%, and ensures equal access to education at all levels. Moreover, girls’ education is a top priority with a female enrollment rate of 51% in undergraduate studies and 46% in graduate studies.

Source: Department Of Statistics - 2010

ENROLLED UNDERGRADUATE STUDENTS BY GENDER 2010

Source: Ministry Of Higher Education And Scientific Research 2010

POPULATION OF JORDAN, MILLION

ENROLLED UNIVERSITY STUDENTS IN UNDERGRADUATE AND GRADUATE LEVELS

TURN TO JORDAN

16 17Section 3

TURN TO

CO

MPE

TITI

VE

AN

D E

DU

CA

TED

WO

RK

FOR

CE

Main Education Initiatives

As part of Jordan's comprehensive e-learning strategy, the government is providing all public schools and universities with computer labs. The government is also in the process of deploying a comprehensive, country-wide broadband network that will connect all public schools, universities, community colleges, and community access centers. Main initiatives include:

Jordan Education Initiative: Launched in June 2003, JEI focuses on improving the development and delivery of education to Jordan’s students through a rigid public-private partnership. To date, JEI incorporates over 17 global corporations, 17 Jordanian entities, and 11 governmental and non-governmental organizations as stakeholders in achieving its goals.

Education Reform for Knowledge Economy: Launched in 2003 by the Ministry of Education and implemented through two distinct phases, the “Education Reform for Knowledge Economy” (ERFKE) focuses on re-orienting the educational policies, plans and strategies.

Jordan Education Reform Support Program: ERSP will support ERFKE by building a system for the professional

development of teachers and principals, provide high-quality early childhood education, give high school students the skills they need to participate productively in the workforce, and help schools and directorates make decisions based on broad participation and sound data.

Intel Teach Initiative: A world-wide initiative that focuses on assisting teachers in expanding the boundaries of their creativity and that of their students beyond the classroom through addressing computer technology as a powerful teaching tool.

Thinking Tools: Launched in 2006, this initiative trains teachers on how to assist students in taking advantage of the available technological tools to express their ideas, actively construct knowledge, share opinions and solve problems.

World Links: Introduced in 2003, a world-wide initiative that focuses on initiating a change in the learning environment and transforming it into a student-centered learning environment.

Partners in Learning Program: An MOU was signed between Microsoft and the Ministry of Education in 2003. According to the MOU, Microsoft will focus on the creation of an Innovative Teachers Network (ITN), a School Technology Innovation Center (SITC) and an Education Support Center.

As a result, Jordan's education system has become one of the most advanced in the region, allowing Jordanian universities to attract increasing numbers of regional and international students. Jordan also possesses a high number of technical, highly skilled, and ICT proficient professionals.

Jordan’s main educational faculties and institutions include: Twenty six state and private accredited universities Jordanian universities are highly ranked for their quality of education, and are sought by many students in the region

There are over 40 institutions producing highly skilled technicians and machinists

Most Jordanian universities have international research collaborations and exchange programs with international institutions

TURN TO JORDAN

18 19

TURN TO

CO

MPE

TITI

VE

AN

D E

DU

CA

TED

WO

RK

FOR

CE

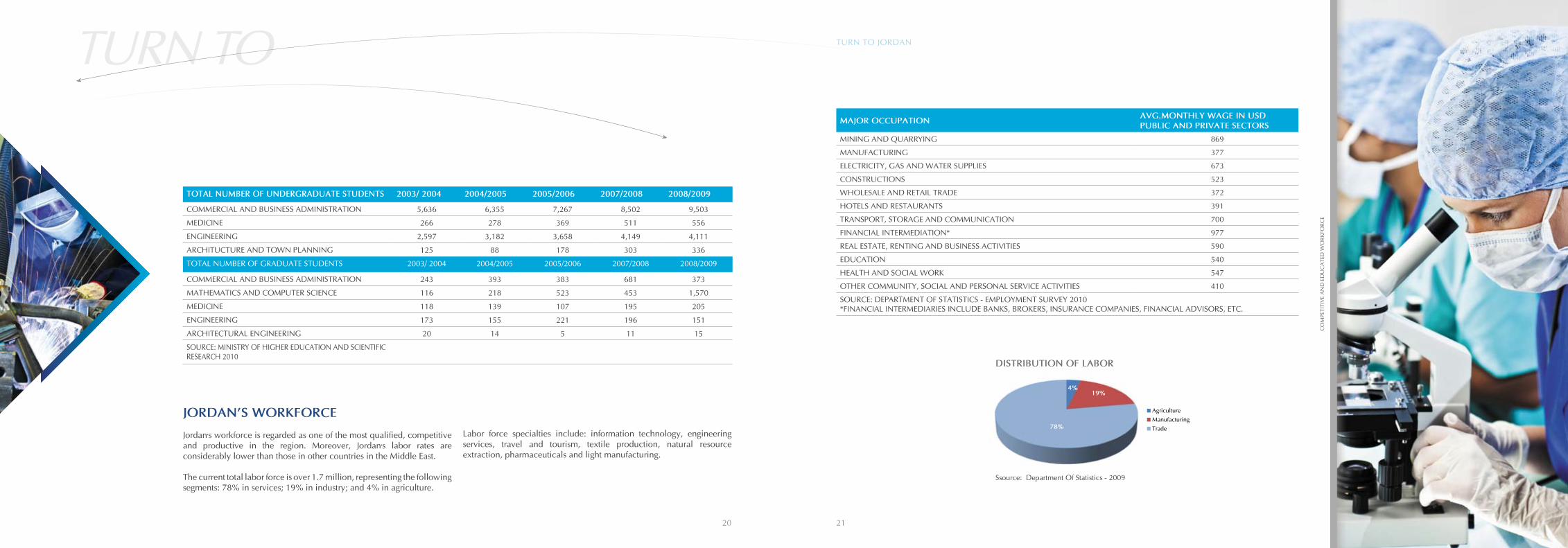

JORDAN’S WORKFORCE

Jordan’s workforce is regarded as one of the most qualified, competitive and productive in the region. Moreover, Jordan’s labor rates are considerably lower than those in other countries in the Middle East.

The current total labor force is over 1.7 million, representing the following segments: 78% in services; 19% in industry; and 4% in agriculture.

Labor force specialties include: information technology, engineering services, travel and tourism, textile production, natural resource extraction, pharmaceuticals and light manufacturing.

DISTRIBUTION OF LABOR

Ssource: Department Of Statistics - 2009

TURN TO JORDAN

20 21

TOTAL NUMBER OF UNDERGRADUATE STUDENTS 2003/ 2004 2004/2005 2005/2006 2007/2008 2008/2009

COMMERCIAL AND BUSINESS ADMINISTRATION 5,636 6,355 7,267 8,502 9,503

MEDICINE 266 278 369 511 556

ENGINEERING 2,597 3,182 3,658 4,149 4,111

ARCHITUCTURE AND TOWN PLANNING 125 88 178 303 336

TOTAL NUMBER OF GRADUATE STUDENTS 2003/ 2004 2004/2005 2005/2006 2007/2008 2008/2009

COMMERCIAL AND BUSINESS ADMINISTRATION 243 393 383 681 373

MATHEMATICS AND COMPUTER SCIENCE 116 218 523 453 1,570

MEDICINE 118 139 107 195 205

ENGINEERING 173 155 221 196 151

ARCHITECTURAL ENGINEERING 20 14 5 11 15

SOURCE: MINISTRY OF HIGHER EDUCATION AND SCIENTIFIC RESEARCH 2010

MAJOR OCCUPATION AVG.MONTHLY WAGE IN USDPUBLIC AND PRIVATE SECTORS

MINING AND QUARRYING 869

MANUFACTURING 377

ELECTRICITY, GAS AND WATER SUPPLIES 673

CONSTRUCTIONS 523

WHOLESALE AND RETAIL TRADE 372

HOTELS AND RESTAURANTS 391

TRANSPORT, STORAGE AND COMMUNICATION 700

FINANCIAL INTERMEDIATION* 977

REAL ESTATE, RENTING AND BUSINESS ACTIVITIES 590

EDUCATION 540

HEALTH AND SOCIAL WORK 547

OTHER COMMUNITY, SOCIAL AND PERSONAL SERVICE ACTIVITIES 410

SOURCE: DEPARTMENT OF STATISTICS - EMPLOYMENT SURVEY 2010*FINANCIAL INTERMEDIARIES INCLUDE BANKS, BROKERS, INSURANCE COMPANIES, FINANCIAL ADVISORS, ETC.

Agriculture Manufacturing Trade

4%19%

78%

TURN TO

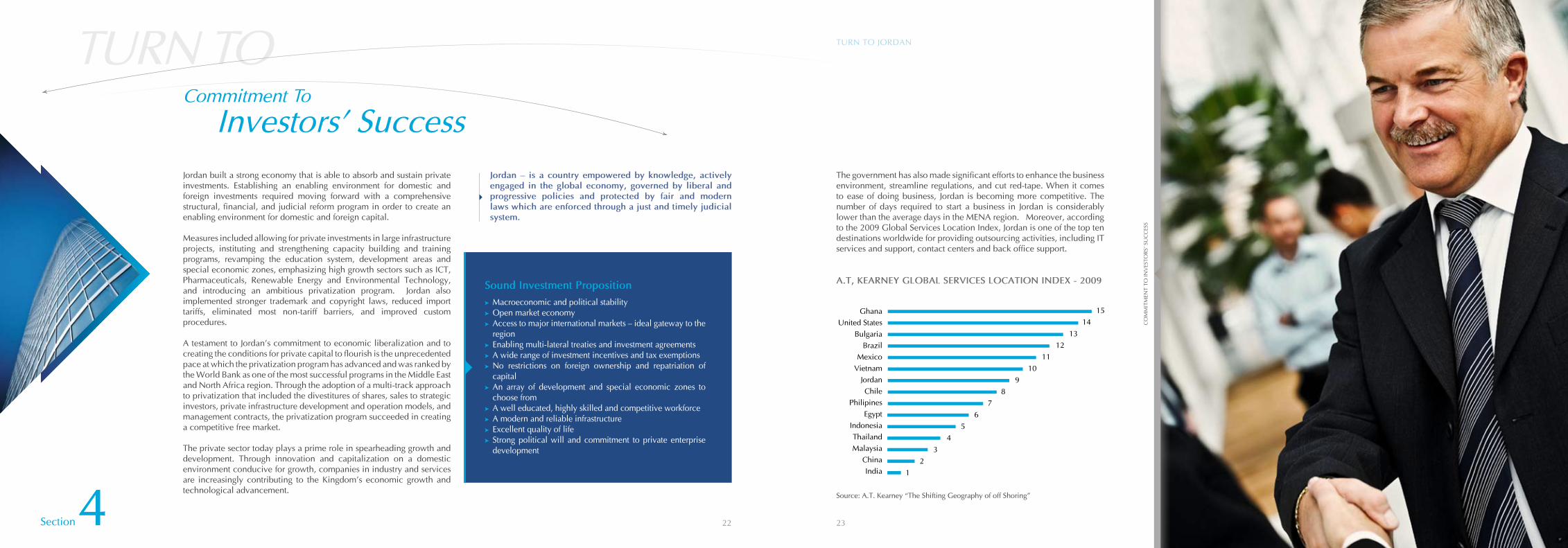

Jordan built a strong economy that is able to absorb and sustain private investments. Establishing an enabling environment for domestic and foreign investments required moving forward with a comprehensive structural, financial, and judicial reform program in order to create an enabling environment for domestic and foreign capital.

Measures included allowing for private investments in large infrastructure projects, instituting and strengthening capacity building and training programs, revamping the education system, development areas and special economic zones, emphasizing high growth sectors such as ICT, Pharmaceuticals, Renewable Energy and Environmental Technology, and introducing an ambitious privatization program. Jordan also implemented stronger trademark and copyright laws, reduced import tariffs, eliminated most non-tariff barriers, and improved custom procedures.

A testament to Jordan's commitment to economic liberalization and to creating the conditions for private capital to flourish is the unprecedented pace at which the privatization program has advanced and was ranked by the World Bank as one of the most successful programs in the Middle East and North Africa region. Through the adoption of a multi-track approach to privatization that included the divestitures of shares, sales to strategic investors, private infrastructure development and operation models, and management contracts, the privatization program succeeded in creating a competitive free market.

The private sector today plays a prime role in spearheading growth and development. Through innovation and capitalization on a domestic environment conducive for growth, companies in industry and services are increasingly contributing to the Kingdom's economic growth and technological advancement.

Jordan – is a country empowered by knowledge, actively engaged in the global economy, governed by liberal and progressive policies and protected by fair and modern laws which are enforced through a just and timely judicial system.

Commitment To

Investors’ SuccessThe government has also made significant efforts to enhance the business environment, streamline regulations, and cut red-tape. When it comes to ease of doing business, Jordan is becoming more competitive. The number of days required to start a business in Jordan is considerably lower than the average days in the MENA region. Moreover, according to the 2009 Global Services Location Index, Jordan is one of the top ten destinations worldwide for providing outsourcing activities, including IT services and support, contact centers and back office support.

A.T, KEARNEY GLOBAL SERVICES LOCATION INDEX - 2009Sound Investment Proposition Macroeconomic and political stability Open market economy Access to major international markets – ideal gateway to the region

Enabling multi-lateral treaties and investment agreements A wide range of investment incentives and tax exemptions No restrictions on foreign ownership and repatriation of capital

An array of development and special economic zones to choose from

A well educated, highly skilled and competitive workforce A modern and reliable infrastructure Excellent quality of life Strong political will and commitment to private enterprise development

Source: A.T. Kearney “The Shifting Geography of off Shoring”

TURN TO JORDAN

22 23Section 4

CO

MM

ITM

ENT

TO IN

VES

TOR

S' S

UC

CES

S

TURN TO

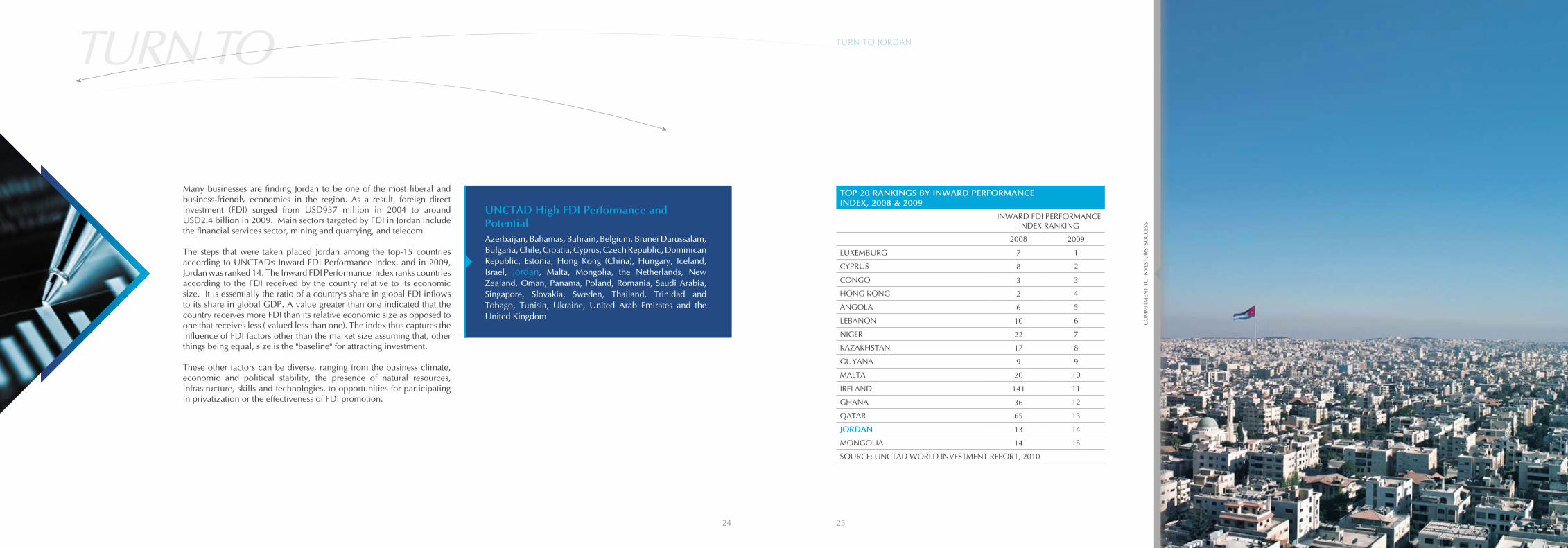

Many businesses are finding Jordan to be one of the most liberal and business-friendly economies in the region. As a result, foreign direct investment (FDI) surged from USD937 million in 2004 to around USD2.4 billion in 2009. Main sectors targeted by FDI in Jordan include the financial services sector, mining and quarrying, and telecom.

The steps that were taken placed Jordan among the top-15 countries according to UNCTAD’s Inward FDI Performance Index, and in 2009, Jordan was ranked 14. The Inward FDI Performance Index ranks countries according to the FDI received by the country relative to its economic size. It is essentially the ratio of a country’s share in global FDI inflows to its share in global GDP. A value greater than one indicated that the country receives more FDI than its relative economic size as opposed to one that receives less ( valued less than one). The index thus captures the influence of FDI factors other than the market size assuming that, other things being equal, size is the "baseline" for attracting investment.

These other factors can be diverse, ranging from the business climate, economic and political stability, the presence of natural resources, infrastructure, skills and technologies, to opportunities for participating in privatization or the effectiveness of FDI promotion.

CO

MM

ITM

ENT

TO IN

VES

TOR

S' S

UC

CES

S

UNCTAD High FDI Performance and PotentialAzerbaijan, Bahamas, Bahrain, Belgium, Brunei Darussalam, Bulgaria, Chile, Croatia, Cyprus, Czech Republic, Dominican Republic, Estonia, Hong Kong (China), Hungary, Iceland, Israel, Jordan, Malta, Mongolia, the Netherlands, New Zealand, Oman, Panama, Poland, Romania, Saudi Arabia, Singapore, Slovakia, Sweden, Thailand, Trinidad and Tobago, Tunisia, Ukraine, United Arab Emirates and the United Kingdom

TURN TO JORDAN

24 25

TOP 20 RANKINGS BY INWARD PERFORMANCE INDEX, 2008 & 2009

INWARD FDI PERFORMANCE INDEX RANKING

2008 2009

LUXEMBURG 7 1

CYPRUS 8 2

CONGO 3 3

HONG KONG 2 4

ANGOLA 6 5

LEBANON 10 6

NIGER 22 7

KAZAKHSTAN 17 8

GUYANA 9 9

MALTA 20 10

IRELAND 141 11

GHANA 36 12

QATAR 65 13

JORDAN 13 14

MONGOLIA 14 15

SOURCE: UNCTAD WORLD INVESTMENT REPORT, 2010

TURN TO

CO

MM

ITM

ENT

TO IN

VES

TOR

S' S

UC

CES

S

DEVELOPMENT ZONES

TURN TO JORDAN

26 27

In a quest to ensure a qualitative leap in the sustainable development of Jordan, a timely ambitious initiative led by His Majesty King Abdullah II was launched, creating Development Zones across the kingdom that provide investors with a globally competitive combination of Location, infrastructure, services and labor, all located strategically to access major regional and global markets.

Development Zones Commission (DZC)The Development Zones Law No. 2 for the year 2008 provides a world class legal foundation that facilitates and ensures a business-friendly environment, and a governance framework manifested in the Development Zone Commission (DZC), a financially and administratively autonomous entity responsible for creating, regulating, facilitating and monitoring the Development Zones in Jordan.

Established in 2008, the DZC aims at increasing investment into the Kingdom, empowering the private sector to lead in the Zones’ development and management, stimulating the economic growth and enhancing local living standards.

As the only point of contact for investors, DZC carries out the Development Zones Law mandates through it’s One Stop Shop that expedites business

entry and operations, offering a highly efficient, streamlined services and transparent implementation, coupled with a number of investment incentive and tax and customs exemptions.

DZC’s vision is directed and supervised by a Board of Commissioners and supported by a highly qualified team that works in partnership with the Development Zones Master Developers; charged with managing the building, development and operation of the Zones, and representing a true Public Private Partnership model.

Incentives under the Development Zones Law of 2008: A flat 5% corporate income tax rate Exemption from sales tax Exemption from Customs duties Exemption from social services and dividends tax 100% foreign ownership Flexibility of foreign employment, including expedited immigration, transit, business, and family residence visas

Streamlined registration and licensing procedures All applicable tax and fee related incentives and exemptions as set forth in the Free Zone Law or any other law applicable in Jordan

One Stop Shop Services: Business registration, licensing, and permitting Labor licenses, including work permits and visas, and all other employment related procedures and approvals

Collection of fees, taxes and customs duties Ongoing procedures necessary for business operations

The Development Zones:The Development Zones established in key locations across the country offer specialized business clusters, reliable infrastructure, and proximity to resources and access to markets.

To date, six Development Zones are currently operational, offering diversified investment opportunities that build on each Zone’s competitive advantage:

King Hussein Bin Talal Development Area- Mafraq Ma’an Development Area Irbid Development Area Dead Sea Development Zone Jabal Ajloun Development Area Business Park Development Area in Dabouq- Amman

TURN TO

REL

IAB

LE IN

FRA

STR

UC

TUR

E

Reliable

InfrastructureJordan enjoys a modern and robust infrastructure. Its land transportation network covers 7,816 km2 of well-developed roads and highways connecting Jordan to its neighbors, providing access to a core market of more than 330 million consumers. Five key regional ports are within 500 kilometers from Jordan's main cities, while Jordan's port in Aqaba provides a key access point for international trade. The Aqaba port benefits from world-class operations and infrastructure and utilizes state-of-the art handling technologies.

Jordan's three airports provide ready access to many international destinations. 72 airlines provide service to Jordan's main airports including major airlines such as Air France, British Airways, Emirates Airlines and Lufthansa. Jordan's national air carrier, Royal Jordanian, has a modern fleet that carries well over two million passengers annually aboard scheduled flights to 55 destinations on four continents.

Jordan also boasts a sophisticated telecommunications network, developed through a robust infrastructure base and a fully liberalized sector.

CONNECTIVITY

Supported by sound policy measures, strong government backing, a solid telecommunications infrastructure and a highly skilled labor force, Jordan today has become a regional leader in the ICT industry. In fact, Jordan’s ICT sector is the fastest growing sector in Jordan’s economy, growing at an annual average rate of 25% and offering more than 80,000 jobs.

A number of public-private initiatives drove the growth of the sector. Such initiatives were aimed at raising the sector's competitiveness, boosting

exports of ICT goods and services, and encouraging job creation in the industry. Building on these efforts, and to create a favorable environment for foreign and domestic investments, the government fully liberalized the telecommunication market, modernized ICT-related laws, eased investment requirements, and passed legislation to protect intellectual property rights.

As part of the modernization process, information technology has also been integrated into the educational system. The Broadband Learning and Educational Network Initiative managed to link eight public universities, 3,200 public schools, 23 community colleges and 75 knowledge stations.

Jordan's National ICT Strategy outlines a number of objectives for the country to reach within the next three years, including fostering a USD 3billion ICT sector, encouraging the development of 35,000 jobs and pushing the internet penetration rate towards 50%.

A testament to the success and vitality of Jordan’s ICT sector is the increasing presence of foreign ICT companies in Jordan. Industry heavyweight Cisco Systems, for example, selected Jordan as a training center for its Middle East and North Africa operations.

The future of ICT in Jordan, and particularly outsourcing by foreign companies, is promising. The sector continues its exponential growth and is well positioned to compete internationally. Jordan is connected to the Fiber-Optic Link around the Glob (FLAG), SEA-ME-WE 3 and SEA-ME-WE 4. Later in 2010, Jordan will be connected by a second Terabit submarine cable, facilitating Jordan’s emergence as an information technology and communication hub in the Middle East.

TURN TO JORDAN

Jordan’s ICT Initiatives

National ICT Strategy of Jordan 2007-2011: Identifies the sub-sectors that national ICT sector leadership will be best-suited for growth given the environment in Jordan. Moreover, it defines actions that Government must take to do its part to facilitate ICT sector growth. Thus, the strategy also poses a mandate to which the Government must respond to execute its commitment.National Broadband Network: Connecting approximately 1.5 million learners through linking eight public universities, 3,200 public schools, 23 community colleges, and 75 knowledge stations.E-Government: Aimed to drive the nation’s transformation into a knowledge society founded on a competitive, dynamic economy. Jordan remains committed to this national vision.Other ICT initiatives include Laptop for Every University Student, Women in Technology Program, Shabakat Tawasol, and Graduates Internship Programs.

28 29Section 5

KEY ICT INDICATORS 2004-2009

2004 2005 2006 2007 2008 2009

PENETRATION RATES %

LANDLINE 11.9 11.6 11 10 8.9 8.4

MOBILE 30.4 57 78 83.8 91 101

INTERNET 10 13.2 13.7 20 26 29

INVESTMENT USD MILLION

LANDLINE 14.1 17.3 17.9 17.2 32.4 33.8

MOBILE 141.1 193.2 195.8 130.5 91.5 169.2

INTERNET 0.98 7.9 3.24 15.6 31 43.7

SOURCE: TELECOM REGULATORY COMMISSION, ANNUAL REPORT 2009

TURN TO

REL

IAB

LE IN

FRA

STR

UC

TUR

E

UTILITIES AND SERVICES IN JORDAN

Utilities and services are delivered throughout the Kingdom. Running water and electricity reach more than 99% of the population and communities. Electricity and water rates vary by use (domestic and non-domestic). Growth in consumer demand for electricity has reached almost 10% per annum in recent years.

TELECOMMUNICATION SECTOR

The telecommunication sector includes three mobile operators; Zain, Orange and Umniah and one radio trunking operator (Xpress).

From the standpoint of telecommunications, Jordan has made significant strides over the past decade. In addition to the efficiencies still being realized by the deregulation of the telecom sector in 2005, Jordanian telecoms have invested over USD400 million in recent years in a number of technology solutions designed to make Jordan more accessible to the rest of the world, which include: ADSL service availability to 95% of Jordan’s populated areas; three terrestrial redundancies; and reduced call-pricing to offshore locations. Services have also been improved through the deployment of digital switching equipment.

In 2009, Jordan’s total telecom revenue reached USD1.3 billion, up from USD 673 million in 2001.

TURN TO JORDAN

30

ELECRCITY RATES AS SET BY ERC RATE

DOMESTIC (USD/ KWH PER MONTH)

FIRST BLOCK (FROM 1-160 KWH) 0.047

SECOND BLOCK (FROM 161-300 KWH) 0.102

THIRD BLOCK (FROM 301-500 KWH) 0.121

FOURTH BLOCK (MORE THAN 500 KWH) 0.161

SMALL INDUSTRIES 0.071

COMMERCIAL (USD$/ KWH PER MONTH) 0.123

AGRICULTURE (USD/ KWH PER MONTH)

FLAT RATE 0.068

WATER PUMPING (USD/ KWH PER MONTH) 0.059

HOTELS (USD/ KWH PER MONTH)

FLAT RATE 0.123

BROADCAST

FLAT RATE 0.123

DOMESTIC (USD/ KWH PER MONTH)

SOURCE: NATIONAL ELECTRIC POWER COMPANY

Opportunities in Jordan’s Telecommunications Sector

•Liberalizedtelecomsector

•Liberalizedmobiletelephonesubsector

•Liberalizedfixedlinesubsector

•Independentregulator–TRC

•LicensedWiMAX&3GInfrastructure

•Morethan6millionmobilephonesubscribers

31

WATER AND SEWAGE RATES WATER RATE (USD)

SEWAGE RATE (USD)

DOMESTIC CONSUMPTION (M3)

0-20 6.28 7.22

30 11.07 12.65

40 13.05 15.26

50 22.18 27.62

60 30.63 39.90

70 40.93 54.93

80 53.07 72.73

90 67.07 93.29

100 82.91 116.61

110 100.61 142.70

120 120.15 171.54

IF CONSUMPTION EXCEEDS 130 M3, THE WATER RATE IS 0.120 PER CU-BIC METER AND 0.553 FOR SEWAGE RATE.

NON- DOMESTIC

THE MINIMUM CONSUMPTION RATE FOR NON-DOMESTIC USE IS 5 M3. IF CONSUMPTION IS BELOW 20M3, AN ADDITIONAL CHARGE OF USD 5.85 WILL BE INCURRED. IF CONSUMPTION EXCEEDS THIS LEVEL, THEN AN ADDITIONAL CHARGE OF USD 7.26 WILL BE INCURRED.

SOURCE: JORDAN WATER COMPANY-MIYAHUNA

TURN TO

REL

IAB

LE IN

FRA

STR

UC

TUR

E

SHIPPING COST TO AQABA

SHIPPING COST FROM AQABA

REAL ESTATE PERFORMANCE INDICATORS

TURN TO JORDAN

32 33

SPEED UP (TO)

128 KBPS-512 KBPS 169-280

1MB-8MBS 379-1,128

1 MB-20 GB 563-743

2 MB- 30 GB 845- 927

4 MB- 35 GB 986-1,318

8 MB – 50 GB 1,127 – 1,843

SOURCE: INTERNET SERVICE PROVIDERS - ZAIN, ORANGE AND BATEL-CO TELECOM RATES 2010

CONSTRUCTION SECTOR Contributing over 5% of Jordan’s GDP in 2009, the construction sector performed strongly in the past few years and is set to continue doing so going forward. According to “MENA Regional Real Estate Overview – Q1 2010”, the average office rents stood at USD 150 per m2 compared to USD 415/m2 in Dubai, USD 570/m2 in Abu Dhabi, and USD 500/m2 in Doha.

AREA COST (USD/20 FOOT)

COST (USD/40 FOOT)

FAR EAST 1450 2800

JAPAN 1800 2800

INDIAN SUB CONTINENT 1000 1600

EUROPE 1100 1600

MEDITERRANEAN 1100 1750

BLACK SEA 1400 1900

NORTH AMERICA (VIA NEW YORK) 2100 2500

NORTH AMERICA (VIA LOS ANGELES) 2400 3000

SOUTH AMERICA 1300 1700

NORTH AFRICA 1100 2000

SOUTH AFRICA 1700 2700

EAST AFRICA 500 800

A. GULF COUNTRIES 1000 1350

SOURCE: NAOURI GROUP

ABU DHABI

DUBAI DOHA RIYADH JEDDAH AMMAN CAIRO DAMAS-CUS

AVERAGE RENT USD/ M2² PA 570 415 500 310 278 150 260 370

PREMIUM RENT USD/ M2² PA 650 860 595 413 395 190 750 887

AVERAGE SALES PRICE USD/ M2² 4,490 4,870 4,670 2,716 2,650 1,508 2,960 5,430

AVERAGE YIELD 11% 8.50% 11% 11.5% 10.5% 10.0% 8.8% 6.8%

VACANCY RATE 1% 10%** 10% 24% 5.5% 9.9% 1% 10%

SOURCE: COLLIERS INTERNATIONAL, MENA REGIONAL REAL ESTATE OVERVIEW – Q1 2010* DUBAI: (ESTABLISHED BUILDINGS) & 58% (NEWLY COMPLETED BUILDINGS)* *THIS DOES NOT INCLUDE RECENTLY COMPLETED OFFICE BUILDINGS, WHICH ARE CURRENTLY RECORDING AN AVERAGE OCCUPANCY RATE OF 41%

AREA COST (USD/20 FOOT)

COST (USD/40 FOOT)

FAR EAST 450 700

JAPAN 550 800

INDIAN SUB CONTINENT 730 1035

EUROPE 1000 1150

MEDITERRANEAN 940 1712

BLACK SEA 1080 1730

NORTH AMERICA (VIA NEW YORK) 2080 2985

NORTH AMERICA (VIA LOS ANGELES) 2800 3500

SOUTH AMERICA 1530 2740

NORTH AFRICA 1105 1735

SOUTH AFRICA 1430 1530

EAST AFRICA 730 1035

A. GULF COUNTRIES 430 630

SOURCE: NAOURI GROUP

International internet redundancy has been applied in Jordan since the beginning of internet service in 1992-1993.

TURN TO

QU

ALI

TY O

F LI

FE

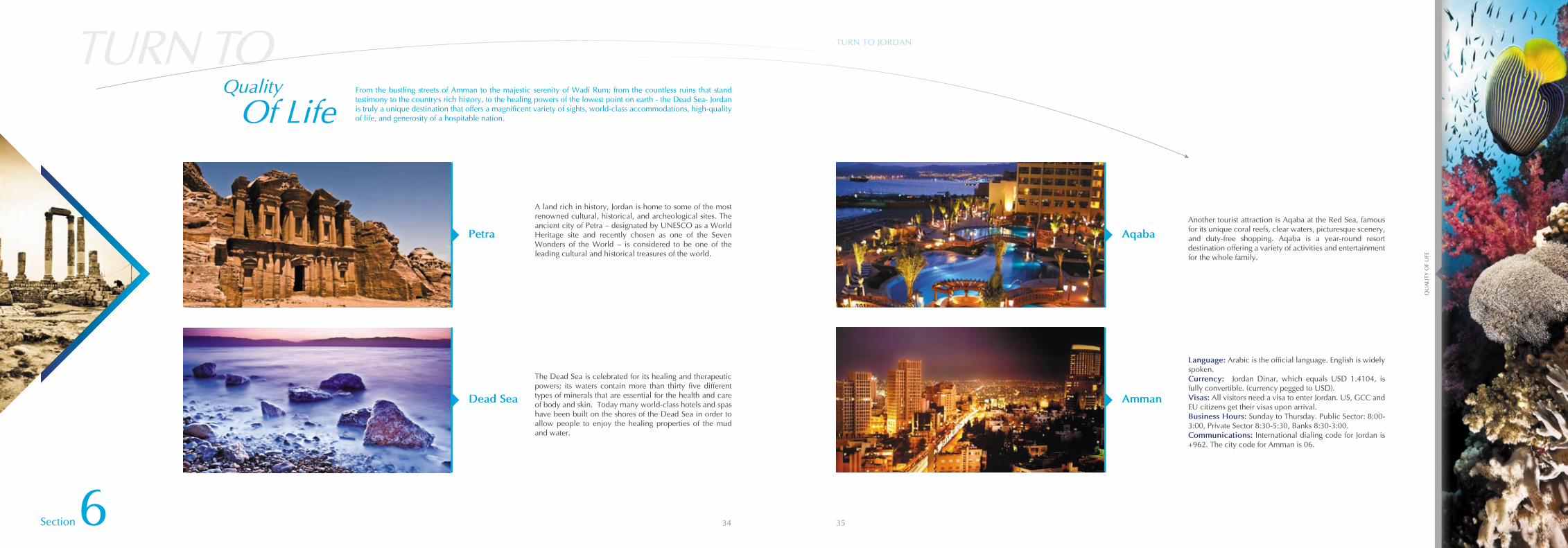

A land rich in history, Jordan is home to some of the most renowned cultural, historical, and archeological sites. The ancient city of Petra – designated by UNESCO as a World Heritage site and recently chosen as one of the Seven Wonders of the World – is considered to be one of the leading cultural and historical treasures of the world.

From the bustling streets of Amman to the majestic serenity of Wadi Rum; from the countless ruins that stand testimony to the country’s rich history, to the healing powers of the lowest point on earth - the Dead Sea- Jordan is truly a unique destination that offers a magnificent variety of sights, world-class accommodations, high-quality of life, and generosity of a hospitable nation.

Another tourist attraction is Aqaba at the Red Sea, famous for its unique coral reefs, clear waters, picturesque scenery, and duty-free shopping. Aqaba is a year-round resort destination offering a variety of activities and entertainment for the whole family.

The Dead Sea is celebrated for its healing and therapeutic powers; its waters contain more than thirty five different types of minerals that are essential for the health and care of body and skin. Today many world-class hotels and spas have been built on the shores of the Dead Sea in order to allow people to enjoy the healing properties of the mud and water.

Language: Arabic is the official language. English is widely spoken. Currency: Jordan Dinar, which equals USD 1.4104, is fully convertible. (currency pegged to USD). Visas: All visitors need a visa to enter Jordan. US, GCC and EU citizens get their visas upon arrival.Business Hours: Sunday to Thursday. Public Sector: 8:00-3:00, Private Sector 8:30-5:30, Banks 8:30-3:00.Communications: International dialing code for Jordan is +962. The city code for Amman is 06.

TURN TO JORDAN

Petra Aqaba

Dead Sea Amman

34 35Section 6

Quality

Of Life

TURN TO

QU

ALI

TY O

F LI

FE

TURN TO JORDAN

Healthcare in Jordan is one of the best in the region and has in fact emerged as a hub for high-quality and specialized medical care.

“One of the best in the region, offering relatively high-quality care at comparatively inexpensive rates”. The National Capacity Self Assessment for Global Environmental Management (NCSA)- Jordan project

Foreign patients from the region and around the world are increasingly seeking medical treatment in Jordan because of the country’s high medical standards, and competitive costs.

In the area of education, Jordan also boasts another success story. The country has the most successful education system in the region, the highest literacy and female education rates in the region, and the largest number of engineers relative to the population in the world.

“In terms of quality, Jordan ranks above international averages in science.” World Bank, Country Overview.

Jordan also offers excellent education facilities for all ages, including 26 major universities and a host of many accredited international schools including American, British, and French schools.

Jordan also houses numerous cultural centers, a variety of restaurants, sporting facilities, attractive shopping malls, and a number of traditional souqs. Jordan is also blessed with ample sunlight and pleasant, comfortable weather all year-round.

The Kingdom consistently ranks among the safest and most corruption-free locations for business in the world in general and among Arab nations in particular.

As per the World Economic Forum Global Competitiveness Report 2009-2010, Jordan ranks as a very safe country as seen by both global and regional standards in comparison with 133 countries studied:

Jordan enjoys a high level of transparency in government, ranking 5th among Arab countries in the 2009 Corruption Perceptions Index issued by Transparency International.

36 37

Reliability of Police Services

Business Costs of Crime & Violence

Business Costs of Terrorism

Prevention ofOrganized Crime

Jordan 17th worldwide

Jordan 17th worldwide

Jordan 56th worldwide

Jordan 8thworldwide

Egypt 54th Israel 93rd UK 33rdUSA 21stIndia 52ndChina 49th

Egypt 53rd Israel 30th UK 73rd USA 74thIndia 50th China 43rd

Egypt 106th Israel 109th UK 113th USA 121st India 117th China 66th

Egypt 15th Israel 45th UK 54th USA 72ndIndia 63rd China 71st

This publication was produced with the support from the United States Agency for International Development through the USAID Jordan

Economic Development Program

JIB is the investment promotion agency for the government of the Hashemite Kingdom of Jordanwith its headquarters in Amman, an office in Zarqa and representative offices in

USA, UAE, Qatar, Kuwait, and China.For more information, please visit www.jordaninvestment.com

E-mail: [email protected]: +962 65608400 ext. 403