Embed Size (px)

Citation preview

The Review of Economic Studies, Ltd.

Option Values in the Economics of Irreplaceable AssetsAuthor(s): Claude HenrySource: The Review of Economic Studies, Vol. 41, Symposium on the Economics of ExhaustibleResources (1974), pp. 89-104Published by: Oxford University PressStable URL: http://www.jstor.org/stable/2296373 .

Accessed: 28/08/2014 14:53

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Oxford University Press and The Review of Economic Studies, Ltd. are collaborating with JSTOR to digitize,preserve and extend access to The Review of Economic Studies.

http://www.jstor.org

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

Option Values in the Economics

of Irreplaceable Assets1 2 CLAUDE HENRY

L'Ecole Polytechnique Paris

J. V. Krutilla [8] on studying the conditions that make it economically efficient to preserve " a place of natural beauty " 3 (such as Hells Canyon, see J. V. Krutilla and C. J. Cicchetti [9], or in France the Parc National de la Vanoise, the Foret de Fontainebleau, ...) comes to the conclusion that an " option demand" or " option value " 4 for preservation must be taken into account if one aims at a really efficient allocation of resources:

[Option] demand is characterized as a willingness to pay for retaining an option to use an area or facility that would be difficult or impossible to replace and for which no close substitute is available. Moreover, such a demand may exist even though there is no current intention to use the area or facility in question and the option may never be exercised.

And also, in relation to Hell's Canyon, one finds in [9] the following argument:

Finally, since the readily observed initial year's benefits from preservation appear to be higher than the minimum required to have the present value [of total benefits from preservation] exceed the present value of [total] developmental benefits, the computation is concluded at this point. Since the analysis relies implicitly on the price compensating measure of consumer surplus and does not include consideration of option value, or other meaningful representation of the effects of uncertainty, the resulting estimate would be a lower bound estimate of the preservation value. Preliminary findings as to the effect of uncertainty on environmental costs and benefits suggest, for example, that in important cases a downward adjustment of benefits from development relative to preservation is indicated.

For a more precise definition of the " option value " and a proof of its positiveness, Krutilla refers to C. J. Cicchetti and A. M. Freeman [3] on the one hand and to K. J. Arrow and A. C. Fisher [1] on the other.

Cicchetti and Freeman consider the following situation: two goods are available for a given person I; the first of these goods may appear in any real positive quantity Y; it is assimilated into I's income. The available quantity of the second good can only take two values, D = d or D = d; the characterization of d can be interpreted as it is by R. Schmalensee [11] in a criticism of Cicchetti and Freeman's analysis: d means that Yellow- stone National Park is accessible to I, d that it is not because the land on which it was established is now used for purposes incompatible with the preservation of nature. Also I

1 First version received November 1973; final version accepted April 1974 (Eds.). 2 This paper owes a great deal to comments and suggestions by E. Malinvaud on an earlier version.

It has also benefitted from discussions, written and oral, with P. Bohm, P. Champsaur, G. M. Heal, and J. J. Laffont. The work was financed by the CNRS (ATP 62990 1).

3 To use the words appearing in the registration under the Companies Act, on 12 January 1895, of " The National Trust for Places of Historic Interest or Natural Beauty ".

4 Concepts introduced by B. A. Weisbrod [12]. 89

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

90 REVIEW OF ECONOMIC STUDIES

may be in one or other of two states of the world with respective probabilities 7t and 1-7r. I's tastes depend on the state of the world; this fact is reflected in his utility function:

U = tUl(Y1, Dl)+(l-Q)U2(Y2, D).'

As it is technically necessary to decide before the state of the world is known whether one chooses d or d, U necessarily reads:

U =-7 U1(Y1, D)+(I-ir)U2(Y2, D).

Let the quantities OP, CS1, CS2 and 0 V (all four having the dimension of an income) be defined by the following equations:

itU1(Y1-OP, d)+(l-7)U2(Y2-OP, d)= 2U1(Y1, d)+(l-'A)U2(Y2, d),

Ui(Yi-CSi, d) = Ui(Yj, d), i = 1, 2,

OV = OP-E[CS] = OP-(irCS1 + (-n)CS2),

where OP is the " option price ", 0 V the " option value " and CSi the " price compensating consumer surplus " if state i obtains. Cicchetti and Freeman claim they prove the following:

OV> 0 when I is strictly risk-averse.

But they write:

To make the choice problem solvable, there must be some way of making the utilities of the two alternative mappings commensurable.

It appears that their result depends crucially on the very particular way in which they " make the utilities commensurable ". This point was first stressed by R. Schmalensee [1 1], but in a rather strange way: risk-aversion is defined there as if U1 and U2 were identical. That 0 V can take any sign even if I is strictly risk-averse is firmly established in P. Bohm [2].

K. J. Arrow and A. C. Fisher [1] and C. Henry [5] approach the problem in a way better designed to justify the opinion expressed in [4]. Both study how fuller information obtainable in the future about the state of the world that will hold may influence I's present choice between D = d and D = d.

After showing that the link between risk-aversion and the magnitude of OP is neither direct nor one-sided we will examine more precisely the role of fuller future information in the decision-making process. Our main conclusion will be that the preservation of " places of historic interest or natural beauty " always has more chance of being secured when the mere prospect of getting fuller information in the course of time is taken into account. In other words the mere prospect of getting fuller information, combined with the irreversibility of the non-preservation alternative, brings forth a positive option value in favour of preservation; this we have called the " irreversibility effect "; in [6] we explore numerical cases which show that the degree of magnitude of this " irreversibility effect" may be fairly important.

1. WHERE DOES THE OPTION VALUE COME FROM?

Continuing with Cicchetti and Freeman's framework, we first note that growing risk- aversion is as likely to bring about a decrease as an increase in the option price.

We can only talk of I's risk-attitude if he is able to compare, from the point of view of the satisfaction that they respectively procure for him, the fact of being in state I with

1 U is written after J. Hirshleifer [7] which generalizes von Neumann-Morgenstern's theorem.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 91

income Y1 and some value of D and the fact of being in state 2 with income Y2 and the same value of D. I's utility function thus has the following form:

U = S(V1(Y1, D), V2(Y2, D)),

or the less general, but here more adequate, form:

U = 7rs(V1(Y1, D))+(1-7r)s(V2(Y2, D)),

where S (resp. s) gives all the information on the attitude of I towards risk, and will help in discussing the effects of variations in risk-aversion.

To avoid any superfluous complication we suppose that V2(Y, d) = V2(Y, d) for all Y; four situations are then possible and can be drawn on four versions of a utility scale (utility once the state of the world is known):

1. I II I - V2(Y-OP) V2(Y) V1(Y, d) V1(Y-OP, d)

2. l I- I I V2(Y-OP) V1(Y, d) V2(Y) V1(Y-OP, d)

3. 1 l l I V1(Y,d) V2( Y-OP) V1(Y-OP, d) V2(y)

4. 1 l l I V1(Y,d) V1(Y-OP, d) V2(Y-OP) 2(Y)

In situations 1 and 2 the change from a lesser to a greater degree of risk-aversion causes a lowering of OP, as can immediately be seen from Figure 1 (corresponding to situation 1).

s

s more risk-averse

risk-averse

V2 (Y - OP) VZ2 (Y) V1 (Yd ) V1 (Y -?P,F)

FIGURE I

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

92 REVIEW OF ECONOMIC STUDIES

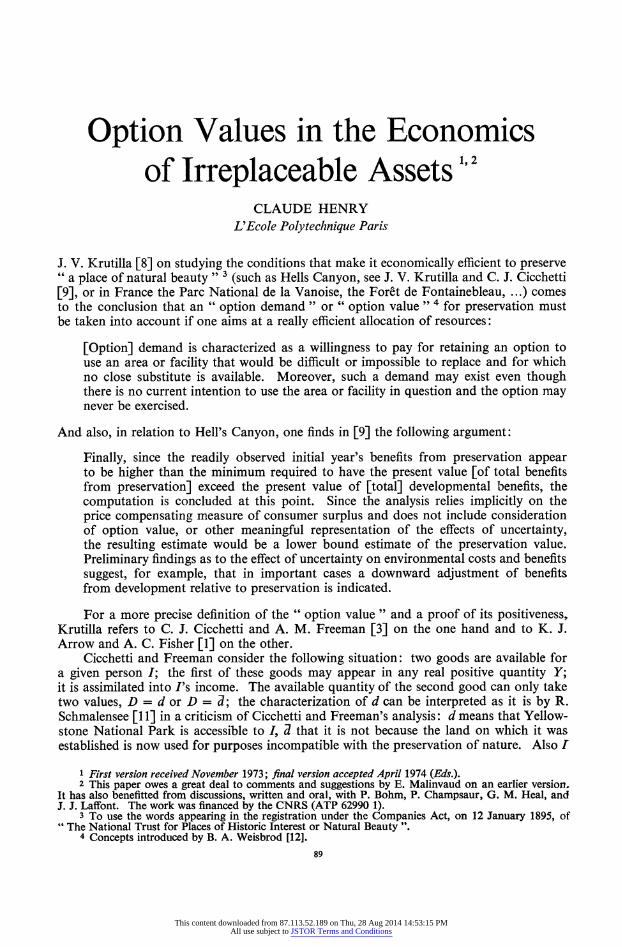

On the other hand in situations 3 and 4 a similar change brings about an increase of OP, as can immediately be seen from Figure 2 (corresponding to situation 3). Figures 1 and 2 are drawn for ir =

s

V1 (Y,d) V2 (Y-OP) V1 (Y OP,d) V2 (Y)

FIGURE 2

The relationship so established between risk-aversion and option-price appears rather obvious when it is viewed as being encountered in a " timeless world" (terminology from Schmalensee) where I has one and only one decision to take; in a world of this type any decision is just as irreversible as any other and it is impossible to introduce Krutilla's option value which is nothing but a risk premium in favour of " irreplaceable assets ". Krutilla's idea can only be examined in a " sequential world " where I really has a succession of decisions to take.

Let us now consider the same problem as in the introduction, but with two periods j 1, 2 and with I's utility function

2 2 U= E Ui(YJ Di),

knowing that if D' = d the choice remains open between D2 d and D2 = d, whereas if D' = d one inevitably has D2 = d.

Suppose that it costs ' Ci to have Di = d rather than Di = d. So as not to introduce here a different and additional problein, that of the allocation of costs and benefits between the two periods, we also suppose that C' must be exactly financed at instant l if one wants to have D' = d (i.e. during the first period) 2 and that C2 must be exactly financed at instant 2 if one wants to have D2 = d. 'To avoid any superfluous complications 3 we will in addition suppose that costs C' and incomes Yi (i.e. income before payment of cost Ci) are certain and that

2 2

f -r 1UW(d) < nM1z1U(d).

1 CJ may be an " opportunity cost". 2 Period j starts at time j. 3 See the corresponding general case in Section 2. 4 It is thus possible to simplify the notation in the following manner:

UJ(YJ, d) = UJ(d) UJ( YJ-CJ, d) = UJ(d).

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 93

Let us first consider the case where no new information is available between instant 1 and instant 2 (everything happens as if we were still in a " timeless world "); the following equation defines the option price:

2 2 2 2

Z 7Ut(Y'-OP, d)+ 7 rrWUi(d)= E 0U! (d), i=l i=l j=l1i=l

and d is chosen at instant 1 if OP> C1. Let us now consider a case 1 where further information does become available between

instant 1 and instant 2 so that I will know with certainty at instant 2 which state of the world will obtain during the second period. He must then answer the following question: what is the total amount (option price OP plus option value OV) that he is prepared to pay at instant 1 in order to be able

(1) to enjoy Yellowstone National Park during the first period, i.e. DI = d, (2) to choose at instant 2, this choice being made after the state of the world is known,

between

(i) Yellowstone National Park during the second period, i.e. D2 = d, and pay C2;

(ii) No Yellowstone National Park any longer, i.e. D2 = d?

Note that such a question would be meaningless had no further information come in between instant 1 and instant 2, because then (2) should be of interest only with the realization of (2.i) in view.

The answer to the preceding question is given by the following equation: 2 2 2 2

E rrUi'(Y'-OP-OV, d)+ E rr2max {UW(d), UW(d)} = E itUi((d). i=1 1=1 j=I i= 1

Consider, for example, the case 2 where

U2(d)> U2 (d) and U2 (d)<U2(d);

the preceding equation then reads: 2 2 2

S irl'Ut(Y' -OP-OV, d)+l(g)2U2() = d Z(d) i=l1 j=l i=1

2

As 7rr U2(d) +7r2U2(d)> n W U2(d), it follows that 0 V> 0, and d is chosen at instant 1

if OP+OV>C'.

2. PROGRESSING TOWARDS FULLER INFORMATION GENERATES THE OPTION VALUE

It thus seems that a positive option value can only appear if three conditions are brought together:

(1) the future is uncertain; (2) some of the possible decisions are more irreversible than others; (3) the process of decision-taking is sequential and use will be made of the better

information acquired in the course of time. If, in addition, a fourth condition is fulfilled:

(4) option d is indivisible, 1 It is an extreme case; we get the same result however when considering intermediate cases as in

C. Henry [6]. 2 It is easily seen that, in all other cases, either O V> 0, or O V = 0.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

94 REVIEW OF ECONOMIC STUDIES

the existence of a (positive) option value is a very general property, true whatever the number of periods, the ways of coming to fuller information, the intertemporal shape of the utility function and the lesser or greater the uncertainty of the benefits and costs.

Consider for example the three-period utility function: N N(i) N(i, j)

E E E ZijkUijk, i= I j= I k= I

where UiJk = UiJk(Yi ' Dl ; YI, DIj; Yk, Dijk)

and where the states of the world are labelled as (i, j, k), i = 1, ..., N; j = 1, ..., (i); k = 1, ..., N(i, j). Choose either D?j = d for every k = 1, ...,N(i, j), or Djk = d for every k = 1, ..., N (i, j), so as to maximize:

N(i. j)

Ui E Z ijk U k = 1 7ij.

where Uijk = Uijk(Yi -OP, d; Yi2j D; Yi Di)

ii' ii ijk ijk)

and OP so far represents any real quantity less than min {Yi},; also Jijr -E ijk; more- i k

over, the incomes YV and y are net of the corresponding production costs (production of D 2 and Dik respectively). Let UZ.(Yl -OP, d; YV, Di)= max Uij. Then choose either DW = d for everyj = 1, ..., N(i), or D32 = a for everyj = 1,..., N(i), so as to maximize

N(i)

ui E i U!*(Yj'-OP, d; yi2j, Dz2), j= 1 7C.

where zi.= E ij.. Let U(Yi' - OP, d) = max Ui.

OP is then defined by the following equation: N N N(i) N(i, j)

Z zi. U (Yj'-OP, d) = Z Z Z 2IJkUijkO'i, d; Yi, d; Yi, d) i=1 i=1j=1 k=1

Consider now the following way of progressing towards fuller information: the state of the world is completely unknown at instant 1; at instant 2 it is known as far as i and j (but not k) are concerned; it is completely specified at instant 3. We can thus choose DA7jk (resp. DWj) with reference to i, j and k (resp. i and]); so we get t?ij (resp. tj) at least as great as U!J (resp. Un). Hence

N N N(i) N(i, j)

E i.i(Yi' OP, d) >-E E ijkUijk(Y ;Yj,d Yijk, ) i= 1 i= 1 j= k=

with in general a strict inequality; it is thus in general possible to obtain a strictly positive option value OV such that E' rri( &j(Yj1 - OP -0 V, d) equals the right-hand side of the latter inequality. In other words it can be said that to take into account the prospect of getting fuller information in the course of time leads to preserving a " place of historic interest or natural beauty " at least as often as-which in general means more often than- if it has been ignored.

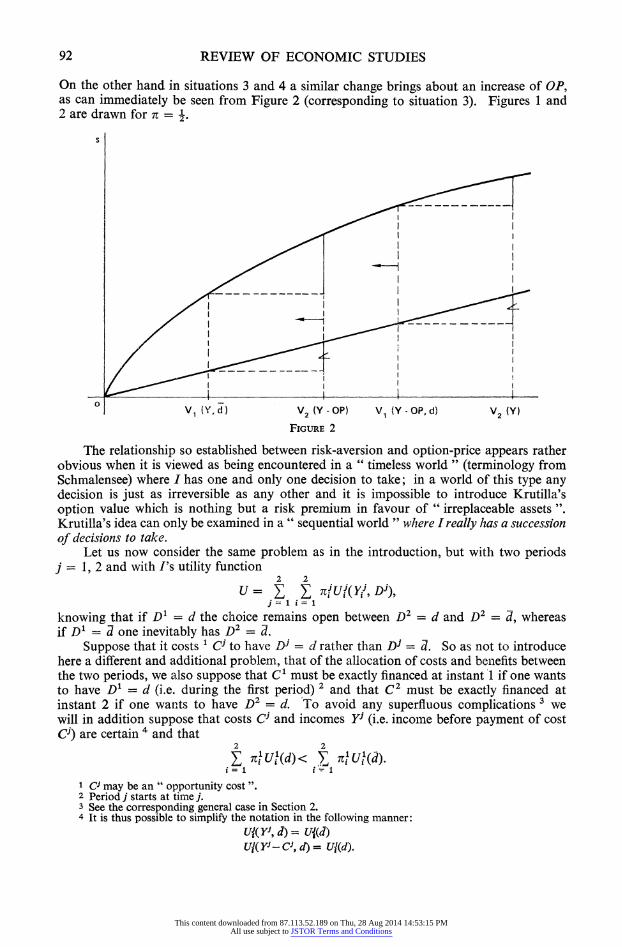

3. DIVISIBILITY OF THE ENVIRONMENTAL VARIABLE D

Here D can take any real positive value related to Y through a strictly decreasing and concave production function Y = f(D) (see fig. 3). I has to choose an optimal pair

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 95

y

0 Dmax D

FIGURE 3

(Y', D1); if he does not see any prospect of getting fuller information or if he ignores such a prospect, he solves the following problem (that we will first consider in two periods only):

max [U(Y', Dl)+ U2(Y2, D2; cw)dp(w)]

s.t. Y' =f'(D')

y2 =f2 (D2)

D2 < D'

y, D, y2 and D2 > 0,

where the state of the world co is a point in a measure space (Q, dp) and where the Uj, j = 1, 2, are strictly quasi-concave utility functions. Let Y', Y2, D 1, D 2 solve this problem.

On the other hand if the state of the world that obtains during the second period is known with certainty at instant 2 and if at instant 1 I takes this fact into account, he solves the following two-stage problem:

(1) Vco, VD', max U2(Y2, D2;

s.t. 2 =f2(D2

D2 ? D'

y2 and D2 > 0;

let 5i2(D'; co), b)2(D'; co) solve this problem.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

96 REVIEW OF ECONOMIC STUDIES

(2) max [U'(Y', D')+ f U2(2(D,; )), D2(D'; co); co)dM(co)]

s.t. Y' = f '(D')

Y' andD' >0;

let f', 13' solve this problem.

We will show that, under suitable assumptions,

131>2151

i.e. that the prospect of getting fuller information leads to fewer irreversible decisions. If U is strictly quasi-concave, then U(f(.), .): D-* U(f(D), D) is pseudoconcave '

with a unique maximum at D = 3 (see figs. 4 and 5). Suppose that 1'<DL'; we will show that this assumption leads to a contradiction. Use will systematically be made of U(D) instead of U(f(D), D). It is clear that

and D2 = D' (see fig. 6).

F ([S ) = 0 t l ~~~~~~~~~~~~~~~~U (Y, D} -

_ I ~ ~ ~ ~~~~~~~~~~~~~~~~~~~~~~~~~~~I I L

0 ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~" DD max

FIGURE 4

1 For a detailed study of concave, pseudoconcave and quasi-concave functions, see chapter 9 in 0. L. Mangasarian [10].

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 97

U(f(D), D)

I D

+ I ~ ~ ~~~~~~I I I

D' (S D" D~~~~~maX D

FIGURE 5

U (D) U2 (D2 ;t

/ with .c, e

v / /t \ U 1~~~~~~~~~~~~~~U (Dl)

~~~~~~~~~~I II

O (52 ({a)) (51 D ~~~D1 DmaX D

F'IGuRE 6

G-SYM

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

98 REVIEW OF ECONOMIC STUDIES

Define the following two subsets of Q:

E= ) j1>52(I> )}

=>Vwo e E*, 2(D1; co) = P(c),

and Vco weQ-E*, D21; () = D';

P = {I I l > 62(w)}(=t cE*)

=>Vwj e- f, 2(b'l* w) = 10) wYc) ES ^ D2( 201; a)) = = 'lo9

and Vco e Q_,2(b'; w)=Db

From the optimality of 13' for the second problem (to simplify the presentation, b' is assumed to be unique), one has:

U1(bl) -U'(D1)> U2(D2'; co); co)dt&ov)- U2(b2(b'; co); w)dM(w).

Let

A = U2(D2(D1; co); w)d(co)- U2-52Q3'; co); co)dM(co)

-{UkbD2(D'; co); w)dM&o)+ |Uk2Q3'(D; co); co)di(co)

= LJ U2(D'; co)dII(co)+ fJ* U2(52(CO); co)d,u(cv)- f Ukb'; co)d,u(co);

and

B = { U2(D2; u2)d!(f)2-L U2(; c)dM(c)

= { U2(D; )d4u((Dw)-; Ud'(D; c)d,u(dc);

Q Q~~~~~~-

A-B --{ U2(1; U)dM()2+ { U2(D1; 2)dM( )

+ J U2(52(); co)dM(co)+ U2(b'; co)di(o) _ 0;

Q-E*- a-I

=A > B,

which contraU2(di 1; tO)dpility o U2(Dl} fteit ob

D D

which U2trdit

th opialt Uf{1

2} fo th1

is polm

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 99

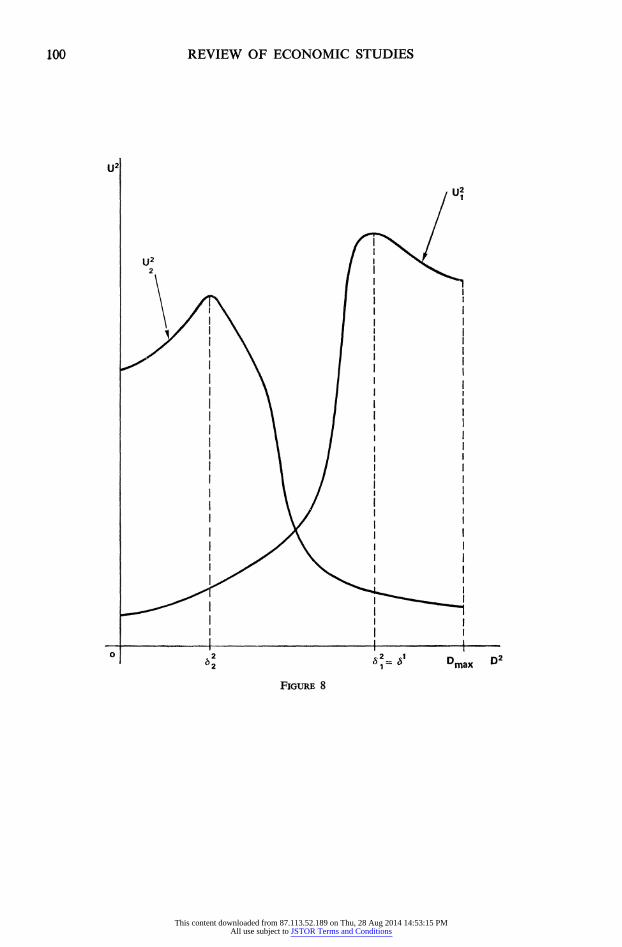

It is worth stressing the fact that, to a certain extent, the quasi-concavity assumption used in the above proof is a necessary assumption. Indeed consider a case where

={W)1, ),2}

and where U'(D'), U2(D2) = U2(D2; 2 1) and U2(D2) = U2(D2; w2) are shown in Figures 7 and 8. Of course the above result can be applied here, in a rather trivial way since

*2 =62 j31 2 j5bl = 2 21 =2

bD(b') = 31 and D2(D) _2

But if u2 is changed into V2 (see fig. 9) then neither D', nor f2(t1), nor b2(f(1) are changed, whilst Di1 is moved to the right.

With this restriction in mind we can generalize the preceding result to more than two periods and apply it to the following controversy. Some people think (e.g. Resources for the Future) that, with the continuous growth of income generated by what is known as economic growth, a demand will appear for higher standards of environment; such

ul

/ ~ ~ ~~~~~~I I

II

0 61 52 Dmax

FIGURE 7

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

100 REVIEW OF ECONOMIC STUDIES

U2

U2

u2 U, ~~~~~~~~I i

~~~~~~~~~I I

_ I ~ ~ ~~~~~~I I l~~~~~~ l

O ^ 2 ax 2 1 Dmax D

FIGURE 8

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 101

2 V

2

I~~~~~~~~~~~~

I E I

I~~~~~~

- ~~~~III

t 1~~2 ! i D D 2

' D maxD

FIGURE 9

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

102 REVIEW OF ECONOMIC STUDIES

an evolution can be formalized by utility functions U2(D2) ..., U(D), ..., such as repre- sented in Fig. 10. U'(D1) is drawn on Figure 11. The concavity that we assume for all these functions may be seen as a consequence of a decreasing marginal utility of D.

Un

u2 /I1

0 2 n Dmax D

FIGURE 10

U11

'Si

ul

o b1 Dmax D

FIGURE 11

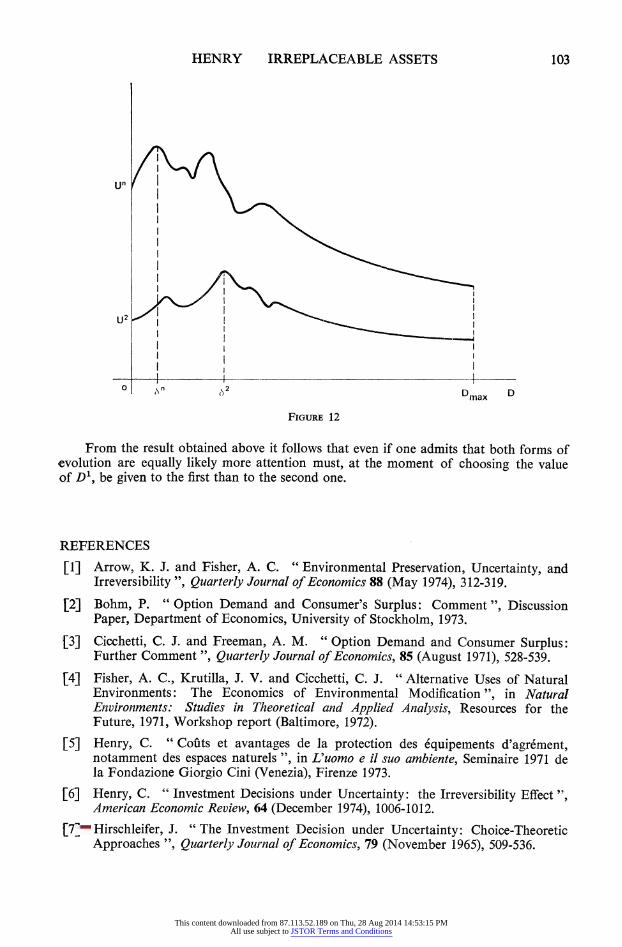

Others (e.g. Japanese engineers and planners) think that the progress of technology will be such that people, provided they have been properly conditioned and taught the new ways to happiness, will be satisfied by an almost entirely artificial world. This evolution can be formalized by utility functions U2(D2), ..., Un(Dn), ..., such as represented on Figure 12. The idiosyncrasies 1 of these functions on the left-hand side of 62 reflect the total ignorance in which one stands with respect to the contours of the utility functions in the artificially laid out environment.

1 These idiosyncrasies have no influence on the result obtained above as can easily be checked in the proof; all what is required from these functions is the monotonic decrease to the right of 82.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

HENRY IRREPLACEABLE ASSETS 103

Un I

U2

O (n 52 Dma D Dmax D

FIGURE 12

From the result obtained above it follows that even if one admits that both forms of evolution are equally likely more attention must, at the moment of choosing the value of D1, be given to the first than to the second one.

REFERENCES

[1] Arrow, K. J. and Fisher, A. C. "Environmental Preservation, Uncertainty, and Irreversibility ", Quarterly Journal of Economics 88 (May 1974), 312-319.

[2] Bohm, P. " Option Demand and Consumer's Surplus: Comment ", Discussion Paper, Department of Economics, University of Stockholm, 1973.

[3] Cicchetti, C. J. and Freeman, A. M. " Option Demand and Consumer Surplus: Further Comment ", Quarterly Journal of Economics, 85 (August 1971), 528-539.

[4] Fisher, A. C., Krutilla, J. V. and Cicchetti, C. J. " Alternative Uses of Natural Environments: The Economics of Environmental Modification ", in Natural Environments: Studies in Theoretical and Applied Analysis, Resources for the Future, 1971, Workshop report (Baltimore, 1972).

[5] Henry, C. " Cofits et avantages de la protection des equipements d'agrement, notamment des espaces naturels ", in L'uomo e il suo ambiente, Seminaire 1971 de la Fondazione Giorgio Cini (Venezia), Firenze 1973.

[6] Henry, C. " Investment Decisions under Uncertainty: the Irreversibility Effect ", American Economic Review, 64 (December 1974), 1006-1012.

[7] Hirschleifer, J. " The Investment Decision under Uncertainty: Choice-Theoretic Approaches ", Quarterly Journal of Economics, 79 (November 1965), 509-536.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions

104 REVIEW OF ECONOMIC STUDIES

[8] Krutilla, J. V. "Conservation Reconsidered ", American Economic Review, 57 (September 1967), 777-786.

[9] Krutilla, J. V. and Cicchetti, C. J. " Evaluating Benefits of Environmental Resources with Special Application to the Hells Canyon ", Natural Resources Journal, 12 (January 1972), 1-29.

[10] Mangasarian, 0. L. Nonlinear Programming (New York, 1969).

[11] Schmalensee, R. "Option Demand and Consumer's Surplus: Valuing Price Changes Under Uncertainty ", American Economic Review, 62 (December 1972), 813-824.

[12] Weisbrod, B. A. "Collective Consumption Services of Individual Consumption Goods ", Quarterly Journal of Economics, 77 (August 1964), 71-77.

This content downloaded from 87.113.52.189 on Thu, 28 Aug 2014 14:53:15 PMAll use subject to JSTOR Terms and Conditions