Embed Size (px)

Citation preview

1

“Sustained growth. Global scale.”March 2007

2

Table of contents

• The Tata Group - overview

• Tata Chemicals - Business overview

• Segment overview• Chemicals, including overview of Brunner Mond

• Fertilisers

• Financial overview

3

An overview of the Tata Group

4

Tata Group – India’s largest and the most respected business group

Chemicals and Fertilisers

Sales:5%

EngineeringSales:31%

EnergySales:8%

Consumer ProductsSales:6%

MaterialsSales:21%

IT and Communications

Sales:19%

ServicesSales:10%

Notes

1 Market cap (approx.) as on March 31, 2006

2 F.Y. 2006 financial data

Market cap1: US$49bn

Revenues2:

US$22bn

PAT2: US$2 billion

5

Tata ChemicalsBusiness Overview

6

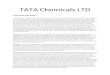

Tata Chemicals today is…

• The 3rd largest soda ash manufacturer in the world post the acquisition of the Brunner Mond group

• The #1 soda ash player in India

• A market leader in edible salt market, largest STPP player in the country

• The most energy efficient urea fertiliser manufacturer in India and amongst the most efficient globally

• 1/3rd stake holder in IMACID, Morocco – assured supply of key inputs

• A true partner of the farmer with a presence in all 3 agri inputs categories as well as an expanding number of Tata Kisan Sansars

7

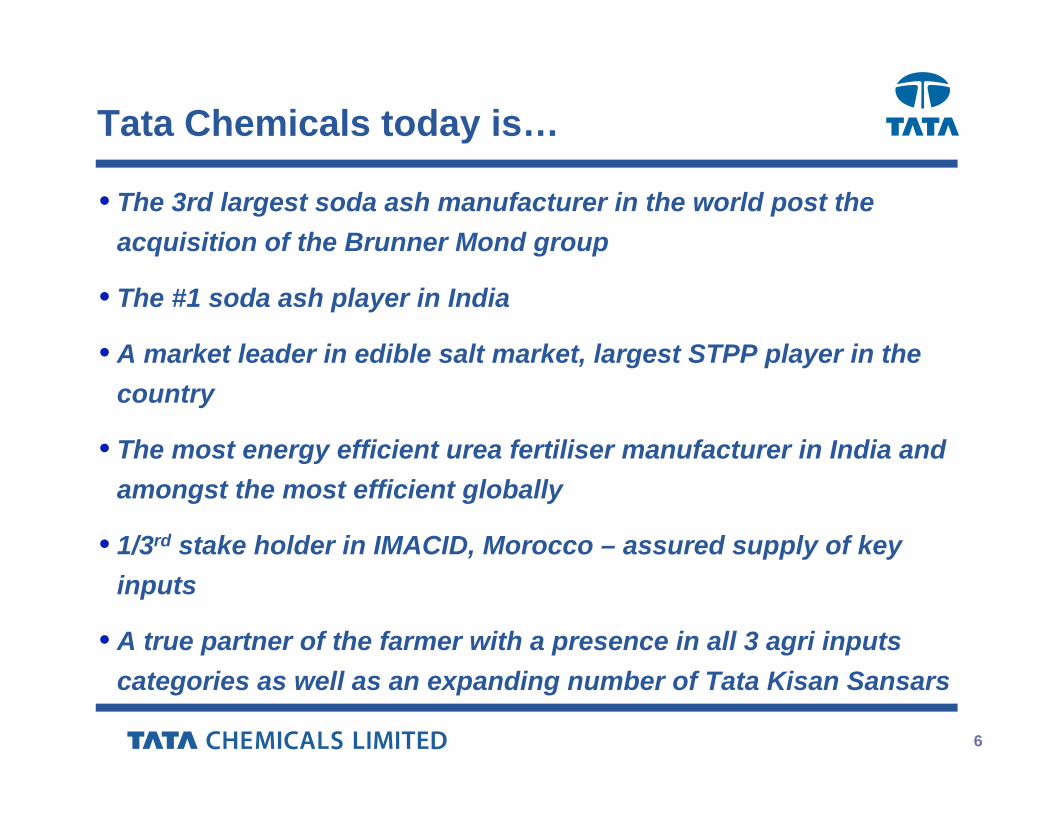

Global Presence

MoroccoMorocco

UKUK

IndiaIndiaKenyaKenya

NetherlandsNetherlands

Manufacturing locations

Markets

South Africa South Africa

8

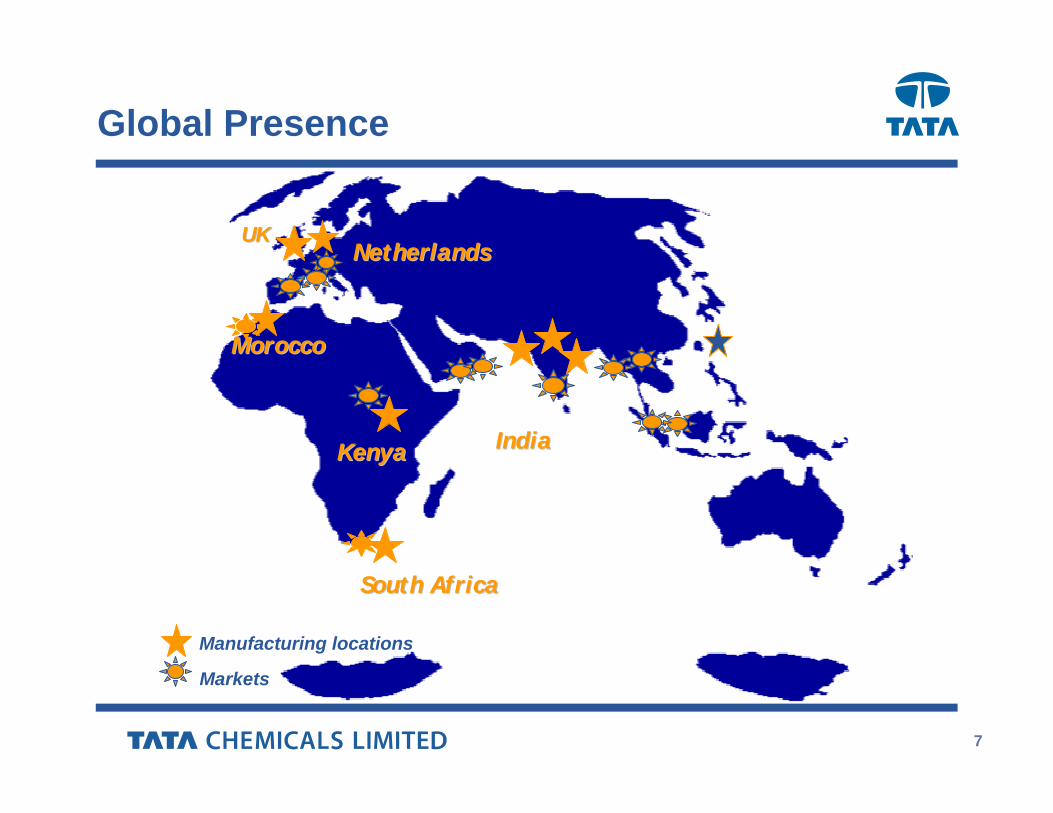

At a glance• Listing: Stock Exchange, Mumbai (BSE) and

National Stock Exchange (NSE)

• Ticker: TTCH IN

• Founded: 1939

• Market Capitalization US$ 1051mn

• Revenue3 (US$mm): 910 (Chemicals – 431, Fertilisers – 479)

• EBITDA3 (US$mm): 166

• EBITDA Margin3: 18.2%

• Employees: 3,500

• Ownership: Sponsor Group 31.6 %Institutional Investors 33.8 %Indian Public 34.6 %Note:

1: INR/USD Conversion rate of 44.12 as on 29th December 2006 for Market cap data

2: FY 2006 data, INR/USD Conversion rate of 44.27

3: Financial Performance relates to FY 2006 consolidated performance. These numbers include only 3 months of the BMGL’s FY 2006 performance

9

Business segments

10

Chemicals - Soda ashRevenue Mix

Chemicals – 54%

11

International Markets

• Global demand at 37 million mt, China - 21% of demand; to grow at 4%pa led by glass

• Synthetic production dominates – 73%

• Increasing natural gas, coal, coke prices & freight rates• Selling prices increasing after seven years of weak prices

Domestic Markets• Domestic demand 2.2 million mt growing at 4-5%

• Demand driven primarily by the float glass segment

• Synthetic soda ash accounts for 100% of domestic production

• Capacity utilisation levels at all-time high

Soda ash industry perspective

Source: British Sulphur Consultants

12

Overview of the Brunner Mond Group

13

Brunner Mond – a transformational acquisition

Major step towards becoming a truly globally competitive company

Resultant synergies will drive Tata Chemicals’ profitabilityResultant synergies will drive Tata Chemicals’ profitability

BMGL – 2nd largest producer in Europe ~1500 customers

Total Soda Ash production capacity ~2.0 mn tons with three plants

• (Before Brunner Mond, soda ash capacity: 0.87mn tons)

• Facilities now in Asia, Europe & Africa, close to high-growth markets

TCL combined turnover to go up ~40%

BMGL – 2nd largest producer in Europe ~1500 customers

Total Soda Ash production capacity ~2.0 mn tons with three plants

• (Before Brunner Mond, soda ash capacity: 0.87mn tons)

• Facilities now in Asia, Europe & Africa, close to high-growth markets

TCL combined turnover to go up ~40%

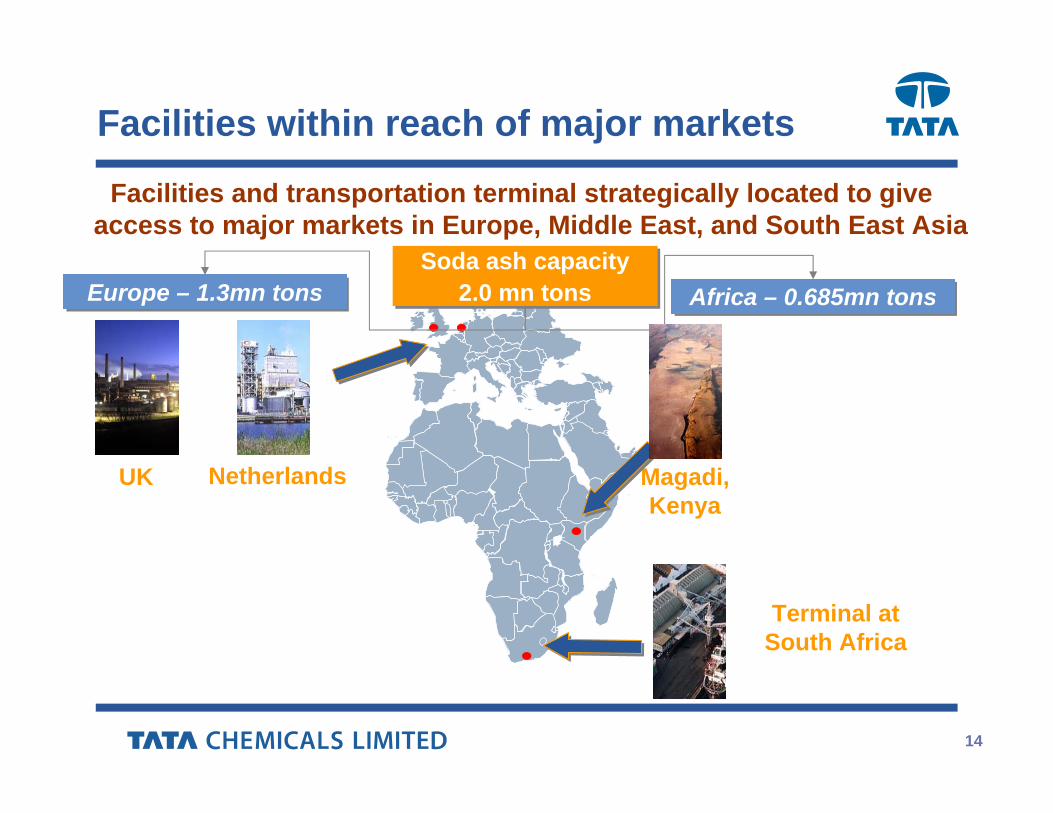

14

Facilities within reach of major markets

Europe – 1.3mn tons Europe – 1.3mn tons Africa – 0.685mn tons Africa – 0.685mn tons

UK Netherlands Magadi, Kenya

Terminal at South Africa

Soda ash capacity 2.0 mn tons

Soda ash capacity 2.0 mn tons

Facilities and transportation terminal strategically located to give access to major markets in Europe, Middle East, and South East Asia

15

Competitive advantages of Magadi Soda Ash

• Magadi has unique competitive advantages

Close to key growth markets e.g. Middle East and Asia

Self-replenishing proven trona reserve - life of 100 years

Duration - Lease extended for 30 years – upto 2053

Area – 227,000 acres

• Significant cost savings for producing natural soda ash

The use of trona makes Magadi Soda Ash lowest cost producer in the world

Cost of prodn of natural soda ash ~ 50% of synthetic soda ash

16

MIDDLE EAST & AFRICA

OmanUAE

KenyaSouth Africa

NigeriaSaudi Arabia

Morocco

ASIA

IndiaBangladeshSri LankaIndonesiaThailandPakistan

PhilippinesVietnamMalaysia

EUROPE

UKNetherlands

GermanyFranceBelgiumSwedenIrelandNorwayDenmark

TCL-BMGL Combined Markets

17

Working with leading brands

Gujarat Glass

18

Food additives

• Market leader - 47% share in India

• “Superbrand” - Ranked # 1 food brand by Economic Times

• High brand equity and premium perception

Tata Salt’ - pioneer in branded salt market

Nationwide distribution - over 40 million consumers

Integrated operations at Chemical site - Embedded competitive advantage

Business with social objective – first Iodized Salt (goitre), now Fortified (iron deficiency)

19

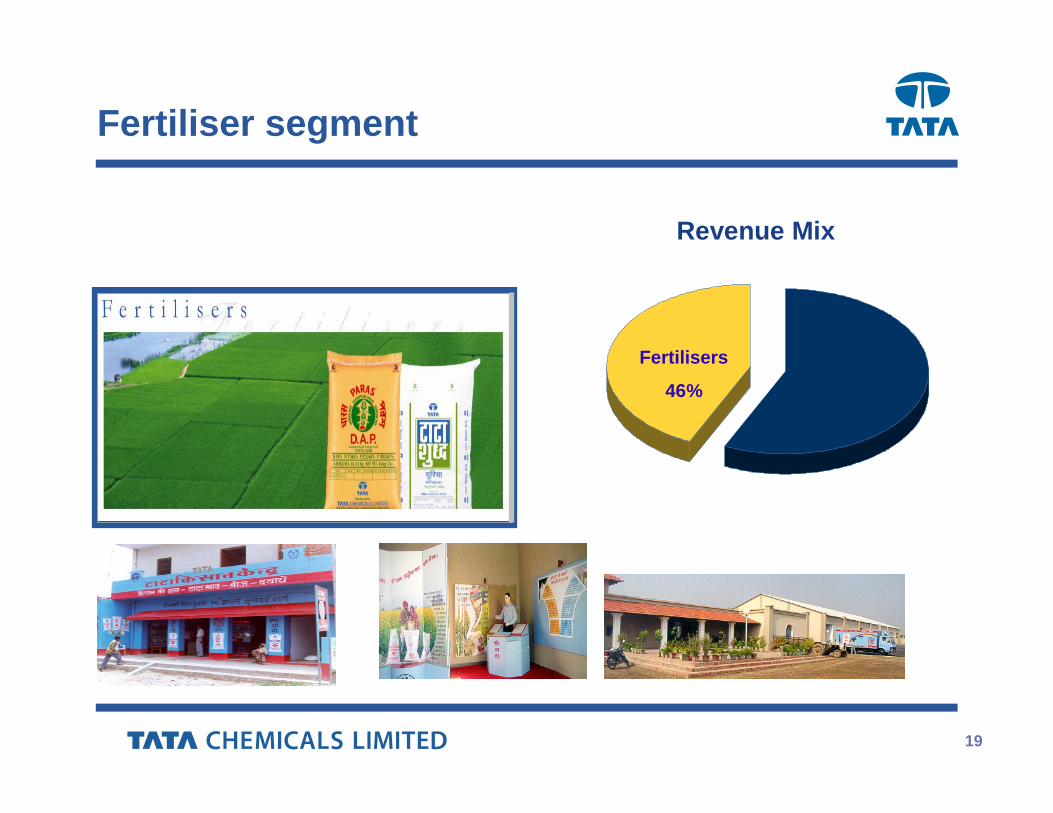

Fertiliser segment

Revenue Mix

Fertilisers

46%

20

The Indian Fertiliser sector

• Consumption skewed towards nitrogenous fertilisers: Urea constitutes 85% of nitrogenous fertiliser consumption and 58% of total consumption

• Recent gas finds create huge opportunity for urea business. Strong medium to long term outlook for DAP

India is the third largest producer and consumer of Fertilisers

Urea policy perspective

• Prices determined by Government

• Feed stock price a pass through• Equal playing field for efficient

and non efficient manufacturers

Phosphatic Policy perspective

• Feedstock prices based on average international prices

• Price announcements often delayed by Government

• Delay in settlement of raw material prices

21

• Leading player in urea and phosphatic fertiliser segments

• Dual feedstock Babrala facility - most efficient in India

• Strategic stake in IMACID, Morocco ensures continuous availability of phosphoric acid

• Presence in high consumption north and east regions

Tata Chemicals’ Fertiliser business

Source of stable revenues in a pre-dominantly government-controlled environment

Baroda(Nikohead office)

INDIABaroda(Nikohead office)

INDIA

Punjab Haryana

Uttar Pradesh

W. Bengal

Jharkhand

Bihar

Baroda(Nikohead office)

INDIABaroda(Nikohead office)

INDIA

Punjab Haryana

Uttar Pradesh

Jharkhand

Bihar

• Tata Kisan Sansars, a one-stopshop for agricultural solutions

22

Tata Kisan Sansar

23

Tata Kisan Sansar (TKS) - creating rural entrepreneurship

• Provide value add services• Create a new distribution channel for agricultural inputs• Improve supply chain efficiencies and provide farm-gate

linkages.. NCDEX• Create market driven R&D solutions• Retailing of fresh agricultural produce – tie up with TOTAL

Produce, Europe’s largest fresh produce Company

24

Financial overview – Standalone*

*Pre Acquisition of the Brunner Mond Group

25

Facilities in India

Babrala - Urea

Haldia – DAP, NPKMithapur – Soda Ash, Cement, Salt

26

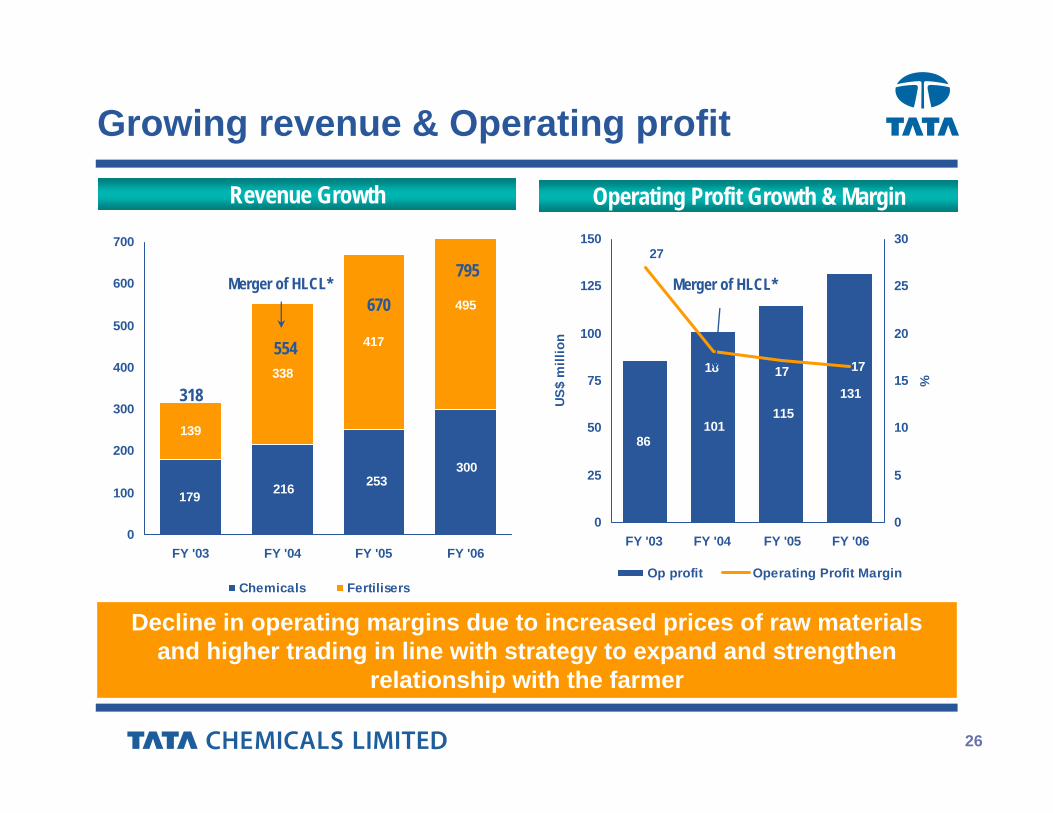

139

338

417

495

253300

179 216

0

100

200

300

400

500

600

700

FY '03 FY '04 FY '05 FY '06

Chemicals Fertilisers

Growing revenue & Operating profit

Revenue Growth Operating Profit Growth & Margin

318

554

670

795Merger of HLCL*

115131

86101

18

27

17 17

0

25

50

75

100

125

150

FY '03 FY '04 FY '05 FY '06US

$ m

illio

n

0

5

10

15

20

25

30

%

Op profit Operating Profit Margin

Merger of HLCL*

* Hind Lever Chemicals LtdDecline in operating margins due to increased prices of raw materials and higher trading in line with strategy to expand and strengthen

relationship with the farmer

27

Debt-Equity Perspective

4.54.4

7.9

9.7

11.7

0

2

4

6

8

10

12

14

FY 02 FY 03 FY 04 FY 05 FY 06

(%)

Reducing interest cost (%)

303 326

457 486

0

100

200

300

400

500

600

700

800

900

FY 2005 FY 2006

USD

mill

ion

Total Debt Shareholder's Equity

FY 2006 Debt Split 2%9%

44%45%

FCCBShort Term LoansTerm LoansCash/ Packing Credit

760 812

Debt : Equity at 0.66 : 1

28

Credit Ratios

3.9 7.4

56

19.4

0.2

0.30.570.36

0

10

20

30

40

50

60

FY03 FY04 FY05 FY06

Interest Coverage ratio Net Debt/Equity

29

Financial overview – Consolidated

30

TBEM 2006

Beyond Boundaries, Brunner Mond …

Babrala India

Haldia India

Morocco Africa

Mithapur India

Brunner Mond, UK –Soda Ash

Brunner Mond, Netherlands – Soda

Ash, Bicarb

31

TBEM 2006Durban SABabrala India

Haldia India

Morocco Africa

Mithapur India

Brunner Mond, Kenya, Lake Magadi - Soda

Ash

Dredge on lake Magadi, Kenya

Brunner Mond …..

32

TBEM 2006Durban SABabrala India

Haldia India

Morocco Africa

Mithapur India

IMACID, Morocco

33

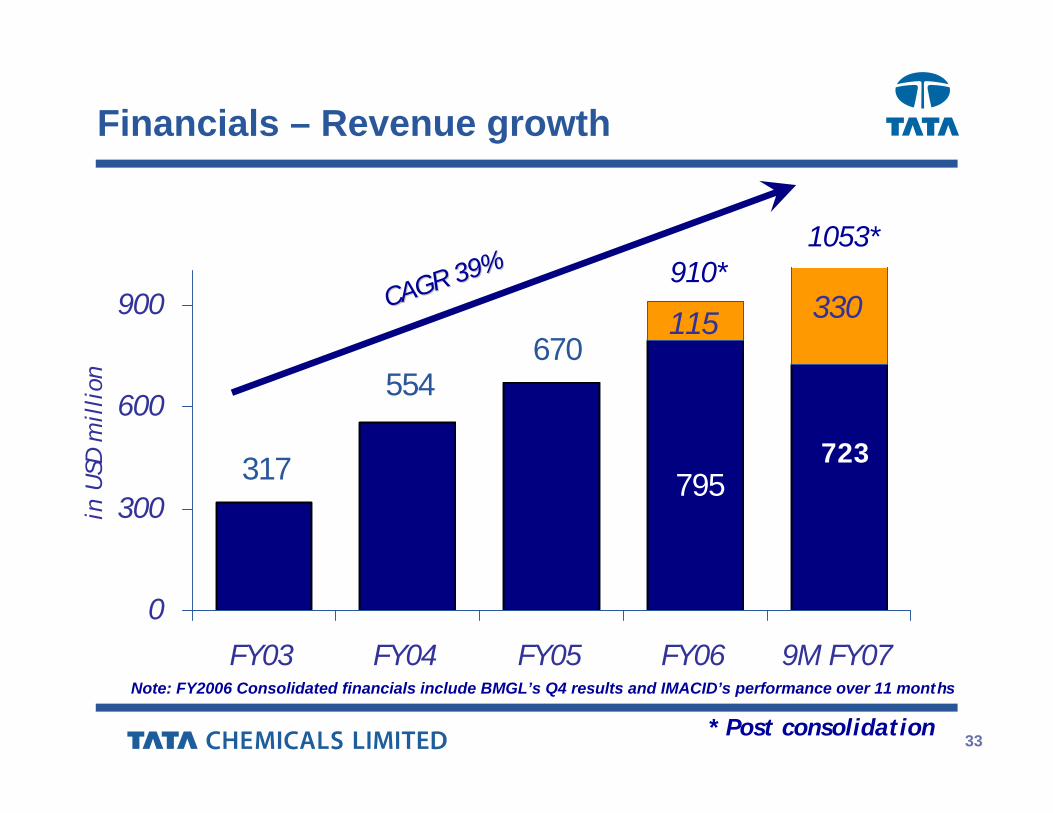

Financials – Revenue growth

330670

795723317

554

115

0

300

600

900

FY03 FY04 FY05 FY06 9M FY07

in U

SD m

illi

on

CAGR 39%CAGR 39% 910*

* Post consolidation

Note: FY2006 Consolidated financials include BMGL’s Q4 results and IMACID’s performance over 11 months

1053*

34

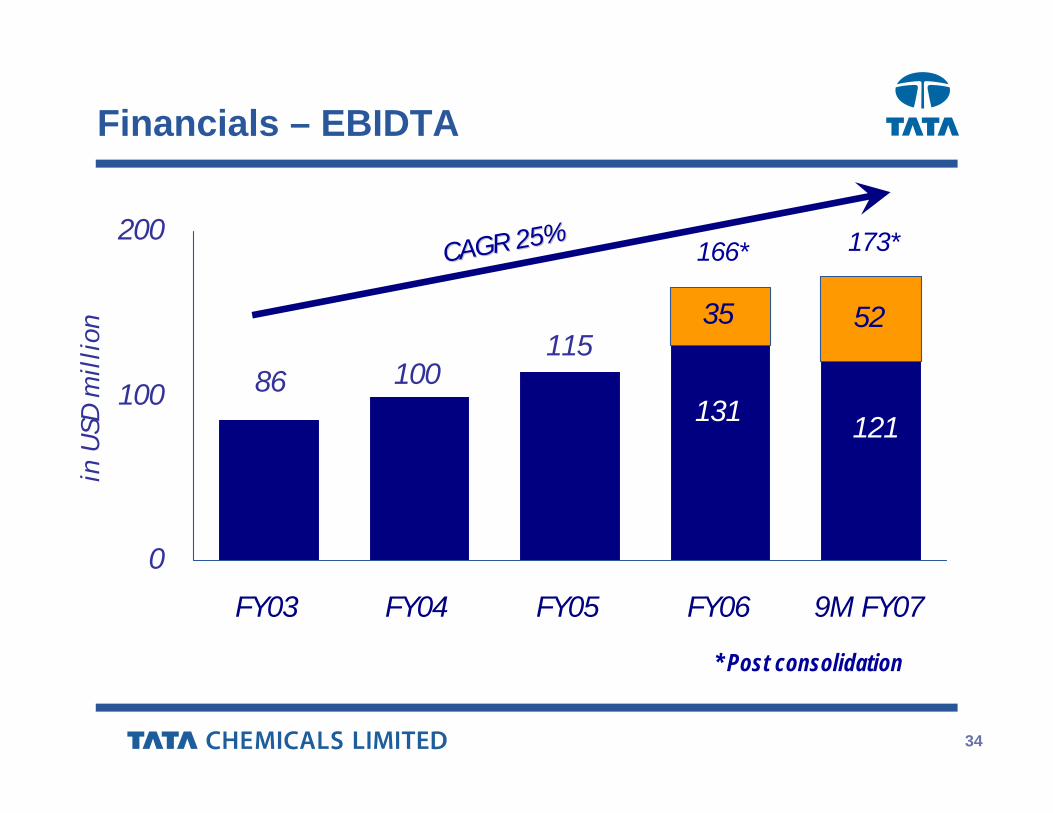

Financials – EBIDTA

52

10086

121131

11535

0

100

200

FY03 FY04 FY05 FY06 9M FY07

in U

SD m

illi

on

166*

* Post consolidation

CAGR 25%CAGR 25% 173*

35

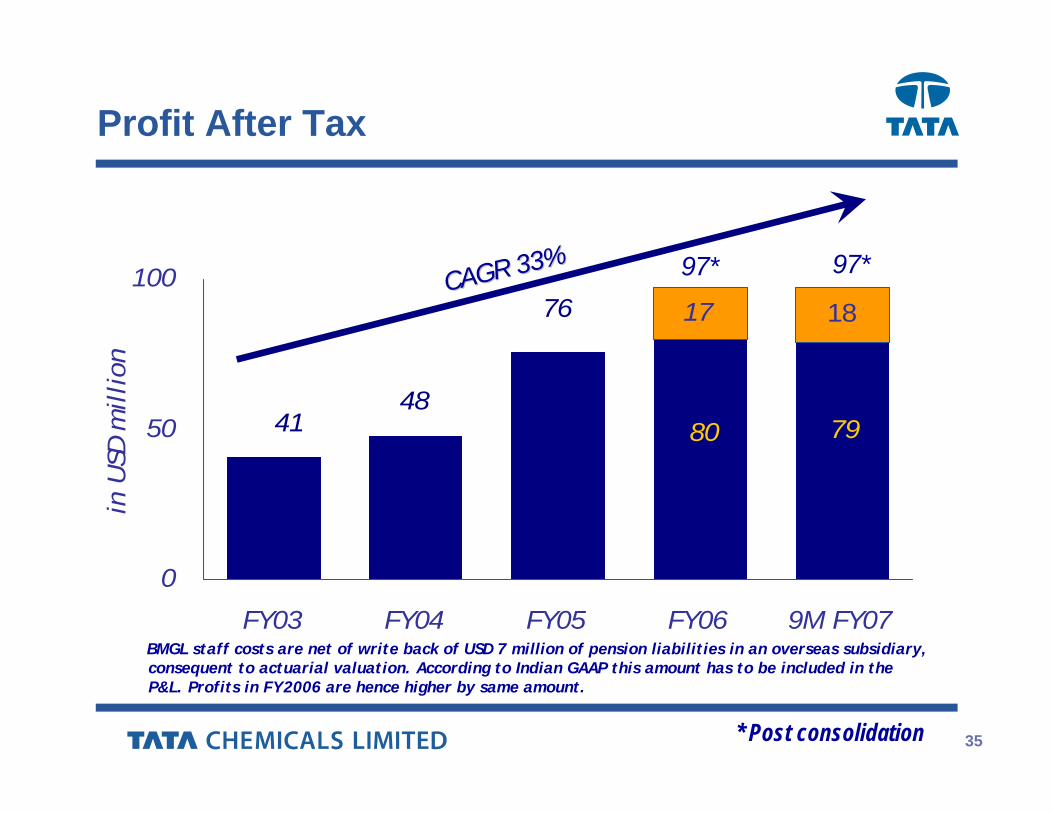

Profit After Tax

1776

80 794148

18

0

50

100

FY03 FY04 FY05 FY06 9M FY07

in U

SD m

illion

97*

* Post consolidation

BMGL staff costs are net of write back of USD 7 million of pension liabilities in an overseas subsidiary, consequent to actuarial valuation. According to Indian GAAP this amount has to be included in the P&L. Profits in FY2006 are hence higher by same amount.

CAGR 33%CAGR 33% 97*

36

Consolidated financials

1 After reducing provision of USD 58.7 mn for the deficit in BMG’s pension liability)

0.45

97

147

192

1035

Consolidated

33

53

330

IMACID / BMGL (Apr to Dec 06)

0.37

79

114

140

723

TCL

9M FY 2007**FY 2006

971680Net Income

0.440.37EPS

20

31

135

IMACID / BMGL (Jan to Mar 06)

125100EBIT

166131EBITDA

910795Sales

ConsolidatedTCL

** Exchange rate of $1=Rs.44.12 as on 29th December 2006

37

Financial ratios

* Post consolidation

7259No. of DaysCash cycle

6564No. of DaysAvg Inventory Turnover

6049No. of DaysAvg Debtors Velocity

2.21.9TimesFixed Asset Turnover

Activity

22.119.4TimesInterest Coverage

0.80.7TimesDebt : Equity Stability

121131115USD MillionEBITDA Cash Generation

21.5TimesMarket to Book Value

35%Dividend Yield

10393INRNetworth per Share

16.319.915.8INREarnings per share

Shareholder Returns

111111%Net Profit Margin

171817%EBITDA Margin Profitability

9M FY 2007*FY 2006*FY 2005UnitCategory

38

Shareholder Returns

7.0

10.9 10.3

19.915.8

5.06.5

5.55.5

7.0

4055

103

201

138

0

4

8

12

16

20

24

FY '02 FY '03 FY '04 FY '05 FY '06

Rs.

per

shar

e

20

40

60

80

100

120

140

160

180

200

220

240

Rs

EPS Dividend Average Market Price

Consistent and healthy dividend payoutConsistent and healthy dividend payout

*

* Post consolidation (Standalone EPS : Rs. 16.41)

39

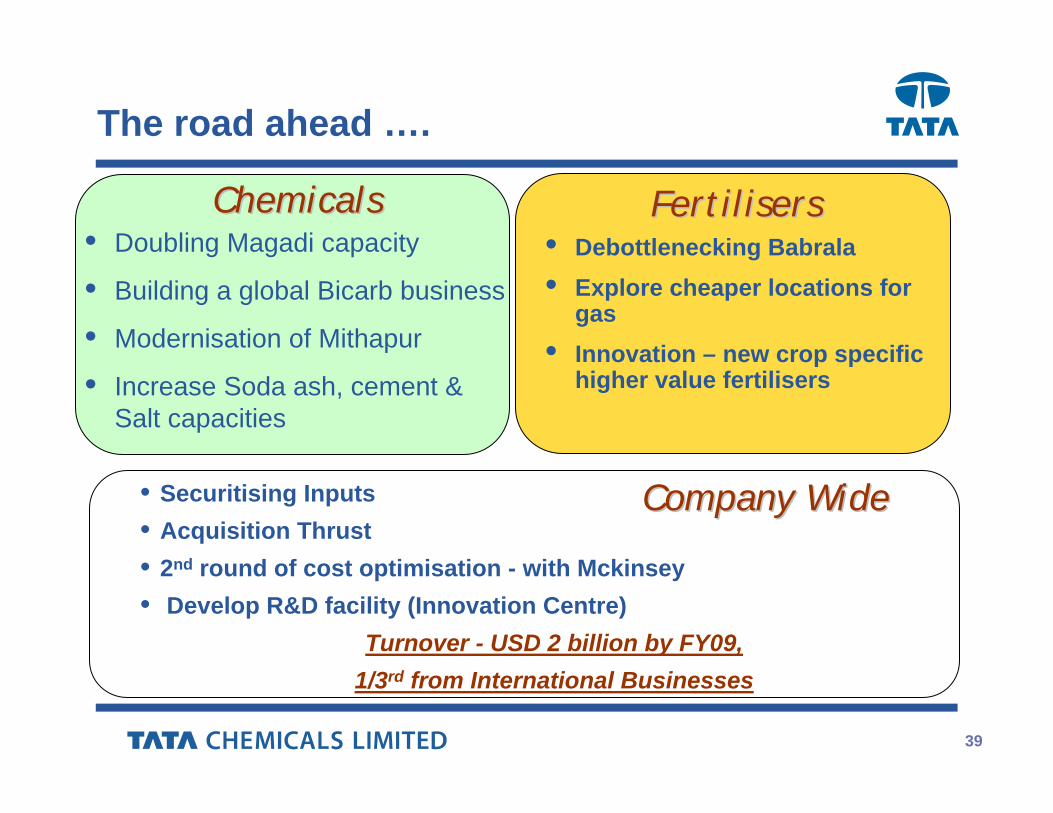

The road ahead ….

• Doubling Magadi capacity

• Building a global Bicarb business

• Modernisation of Mithapur

• Increase Soda ash, cement & Salt capacities

• Debottlenecking Babrala• Explore cheaper locations for

gas • Innovation – new crop specific

higher value fertilisers

FertilisersFertilisers

• Securitising Inputs• Acquisition Thrust• 2nd round of cost optimisation - with Mckinsey• Develop R&D facility (Innovation Centre)

Turnover - USD 2 billion by FY09, 1/3rd from International Businesses

Company WideCompany Wide

ChemicalsChemicals

40

The New Emerging Portfolio

41

1. Fresh Produce Business

1. Leveraging the TKS Network

2. Focusing on what matters – the supply chain

3. Partnering with experience – 100 years of expertise (TPL – earlier Fyffes)

4. Sequential roll-out – Punjab and West Bengal

5. In 2007-08 – 2 Distribution Centres

• In 3 years – 20 Distribution Centres

• In 5 years – 40 Distribution Centres

A 160,000 Cr. market

42

2. Biofuels

1. Entry into both Bio Diesel and Bio Ethanol

2. Trial cultivation of non-food agricultural feedstock commenced in both cases

3. Dual approach – conventional technology & advanced new technologies (concurrent development)

4. Development of novel technologies is the responsibility of

the Innovation Centre (Pune)

43

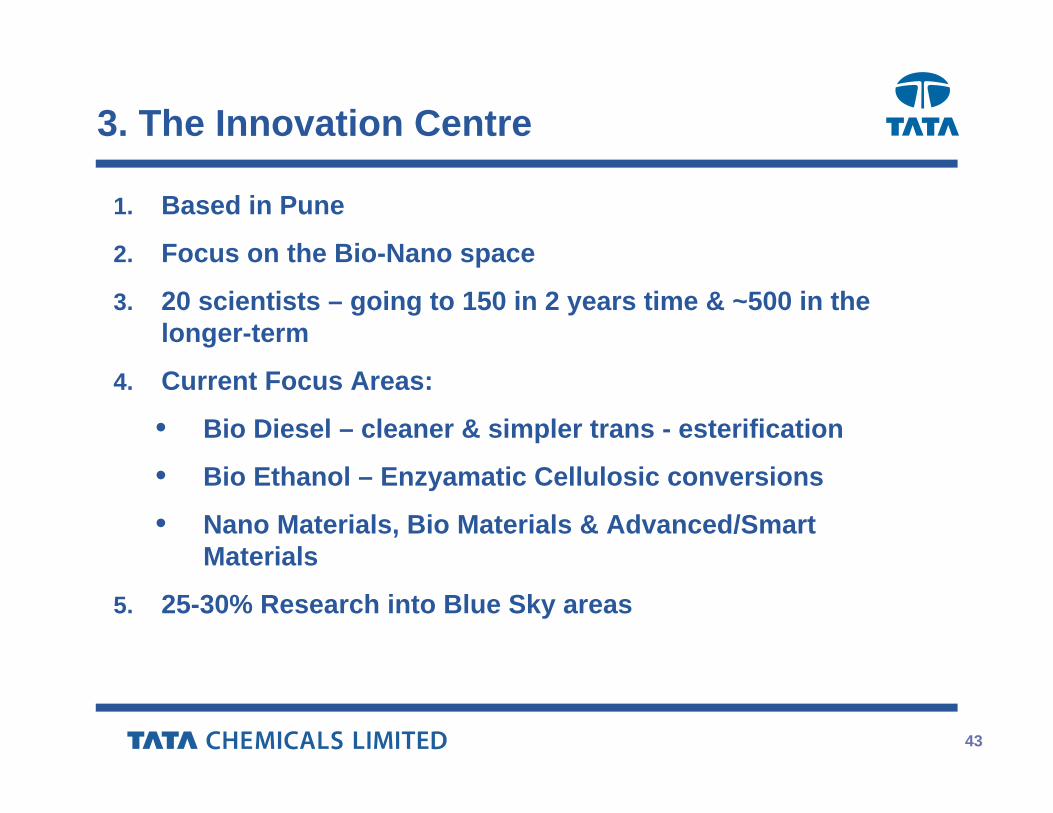

3. The Innovation Centre

1. Based in Pune

2. Focus on the Bio-Nano space

3. 20 scientists – going to 150 in 2 years time & ~500 in the longer-term

4. Current Focus Areas:

• Bio Diesel – cleaner & simpler trans - esterification

• Bio Ethanol – Enzyamatic Cellulosic conversions

• Nano Materials, Bio Materials & Advanced/Smart Materials

5. 25-30% Research into Blue Sky areas

44

Thank you