Embed Size (px)

Citation preview

Sustainable use ofEarth’s natural resources

IR presentationQ1-Q2 2017

© Outotec – All rights reserved

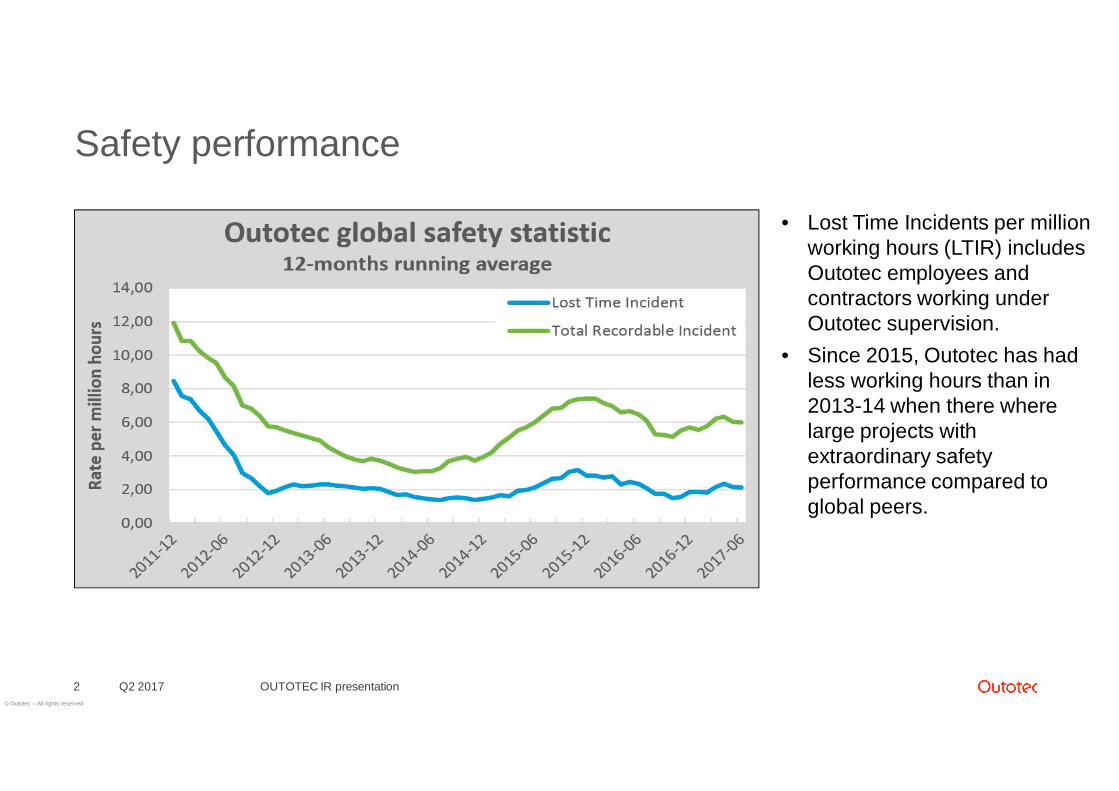

Safety performance

OUTOTEC IR presentation2 Q2 2017

• Lost Time Incidents per millionworking hours (LTIR) includesOutotec employees andcontractors working underOutotec supervision.

• Since 2015, Outotec has hadless working hours than in2013-14 when there wherelarge projects withextraordinary safetyperformance compared toglobal peers.

© Outotec – All rights reserved

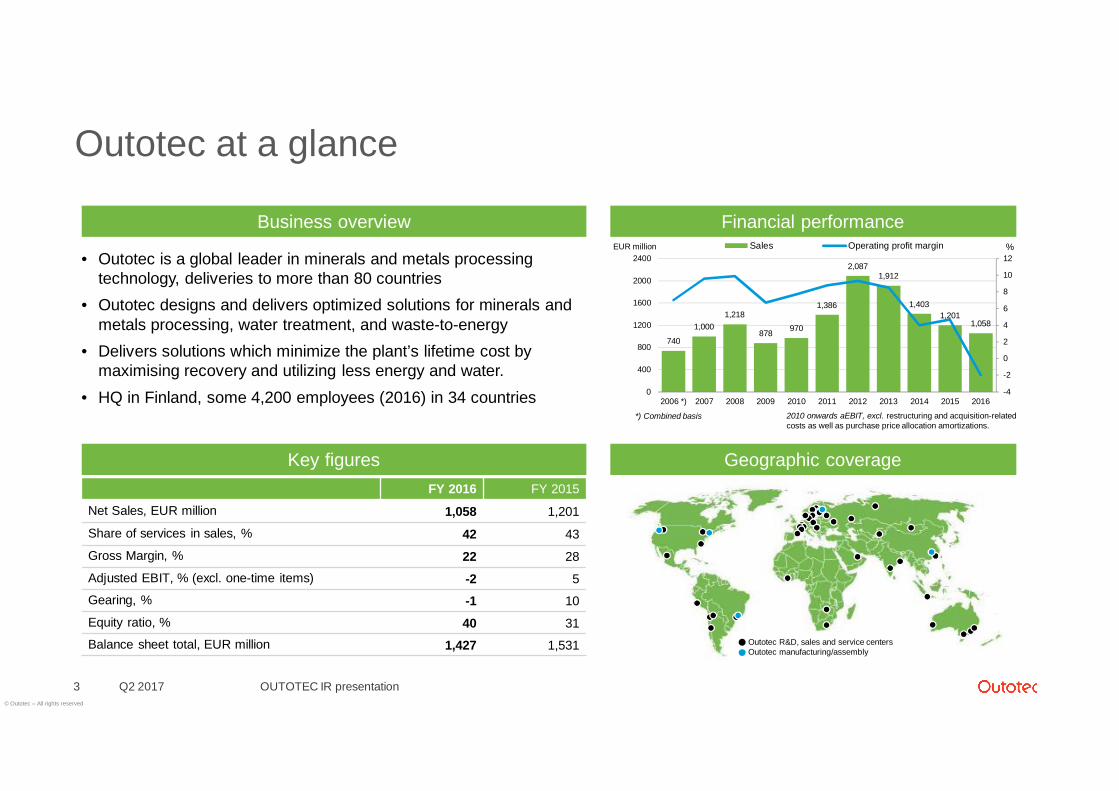

Outotec at a glance

Q2 2017 OUTOTEC IR presentation3

Key figures

Financial performance

Geographic coverage

Business overview

740

1,0001,218

878 970

1,386

2,0871,912

1,4031,201

1,058

-4

-2

0

2

4

6

8

10

12

0

400

800

1200

1600

2000

2400

2006 *) 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sales Operating profit margin

*) Combined basis 2010 onwards aEBIT, excl. restructuring and acquisition-relatedcosts as well as purchase price allocation amortizations.

EUR million %

FY 2016 FY 2015

Net Sales, EUR million 1,058 1,201

Share of services in sales, % 42 43

Gross Margin, % 22 28

Adjusted EBIT, % (excl. one-time items) -2 5Gearing, % -1 10

Equity ratio, % 40 31Balance sheet total, EUR million 1,427 1,531

• Outotec is a global leader in minerals and metals processingtechnology, deliveries to more than 80 countries

• Outotec designs and delivers optimized solutions for minerals andmetals processing, water treatment, and waste-to-energy

• Delivers solutions which minimize the plant’s lifetime cost bymaximising recovery and utilizing less energy and water.

• HQ in Finland, some 4,200 employees (2016) in 34 countries

Outotec R&D, sales and service centersOutotec manufacturing/assembly

© Outotec – All rights reserved

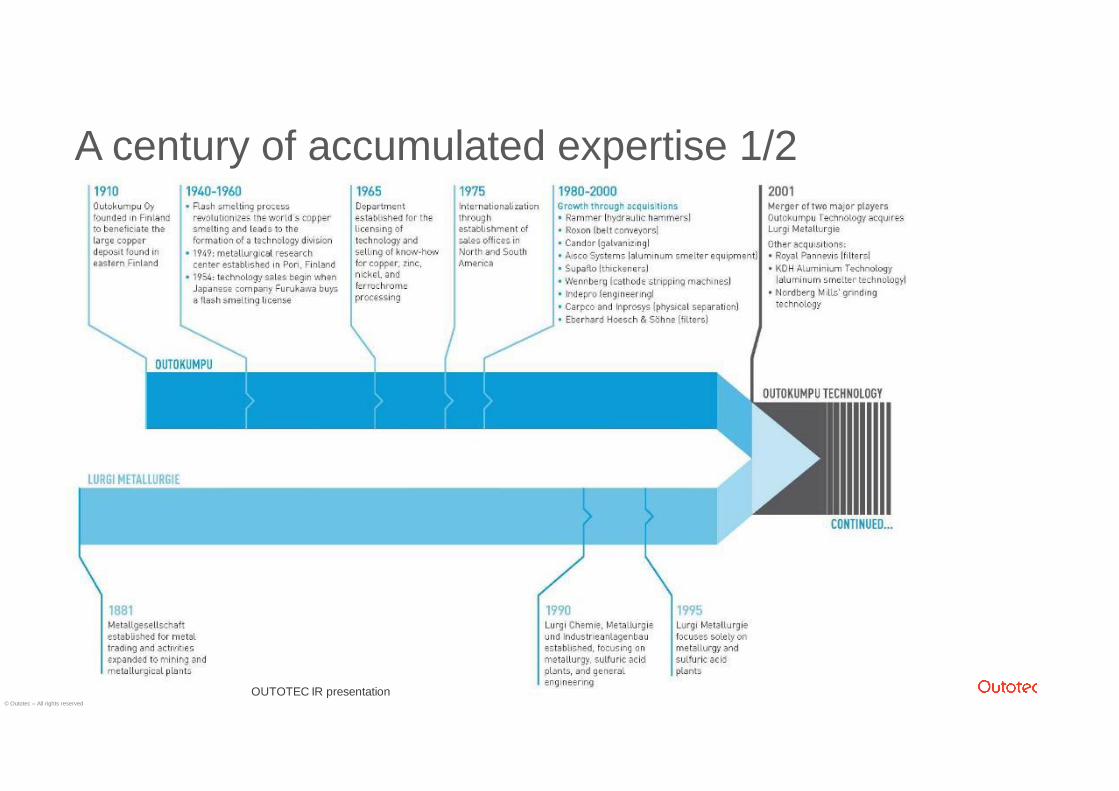

A century of accumulated expertise 1/2

Q2 2017 OUTOTEC IR presentation4 OUTOTEC IR presentation

© Outotec – All rights reserved

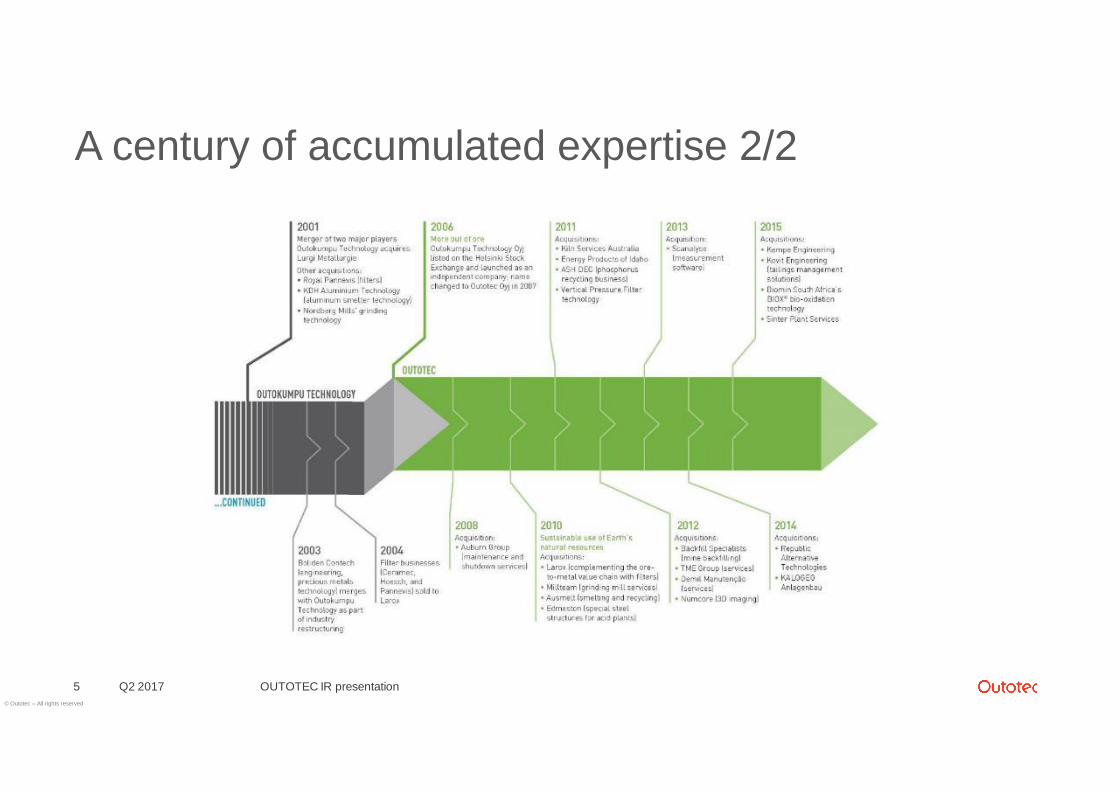

A century of accumulated expertise 2/2

Q2 2017 OUTOTEC IR presentation5

© Outotec – All rights reserved

6

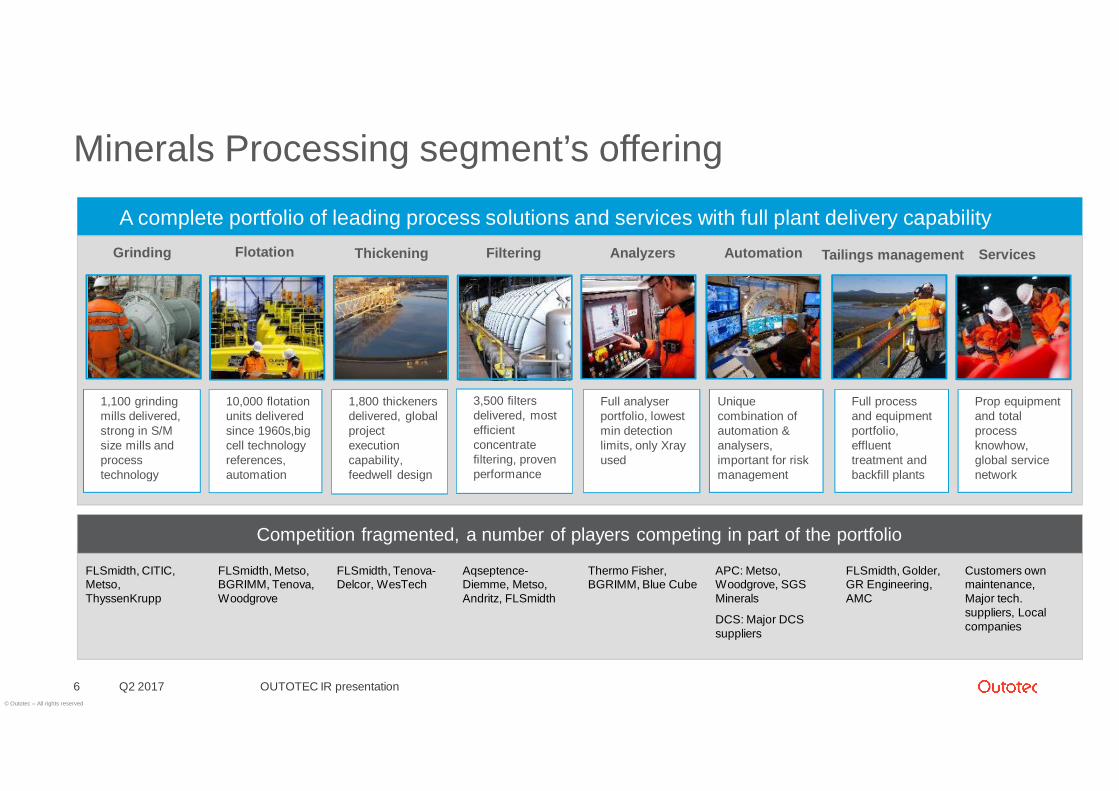

Minerals Processing segment’s offering

A complete portfolio of leading process solutions and services with full plant delivery capability

WaterTechnology

FLSmidth, CITIC,Metso,ThyssenKrupp

FLSmidth, Metso,BGRIMM, Tenova,Woodgrove

FLSmidth, Tenova-Delcor, WesTech

Aqseptence-Diemme, Metso,Andritz, FLSmidth

Thermo Fisher,BGRIMM, Blue Cube

APC: Metso,Woodgrove, SGSMinerals

DCS: Major DCSsuppliers

FLSmidth, Golder,GR Engineering,AMC

Customers ownmaintenance,Major tech.suppliers, Localcompanies

Thickening AnalyzersGrinding Flotation AutomationFiltering ServicesTailings management

1,100 grindingmills delivered,strong in S/Msize mills andprocesstechnology

10,000 flotationunits deliveredsince 1960s,bigcell technologyreferences,automation

1,800 thickenersdelivered, globalprojectexecutioncapability,feedwell design

Full analyserportfolio, lowestmin detectionlimits, only Xrayused

Uniquecombination ofautomation &analysers,important for riskmanagement

Full processand equipmentportfolio,effluenttreatment andbackfill plants

Prop equipmentand totalprocessknowhow,global servicenetwork

3,500 filtersdelivered, mostefficientconcentratefiltering, provenperformance

Competition fragmented, a number of players competing in part of the portfolio

Q2 2017 OUTOTEC IR presentation

© Outotec – All rights reserved

Q2 2017 OUTOTEC IR presentation7

Industry-leading technologies, process solutions and services

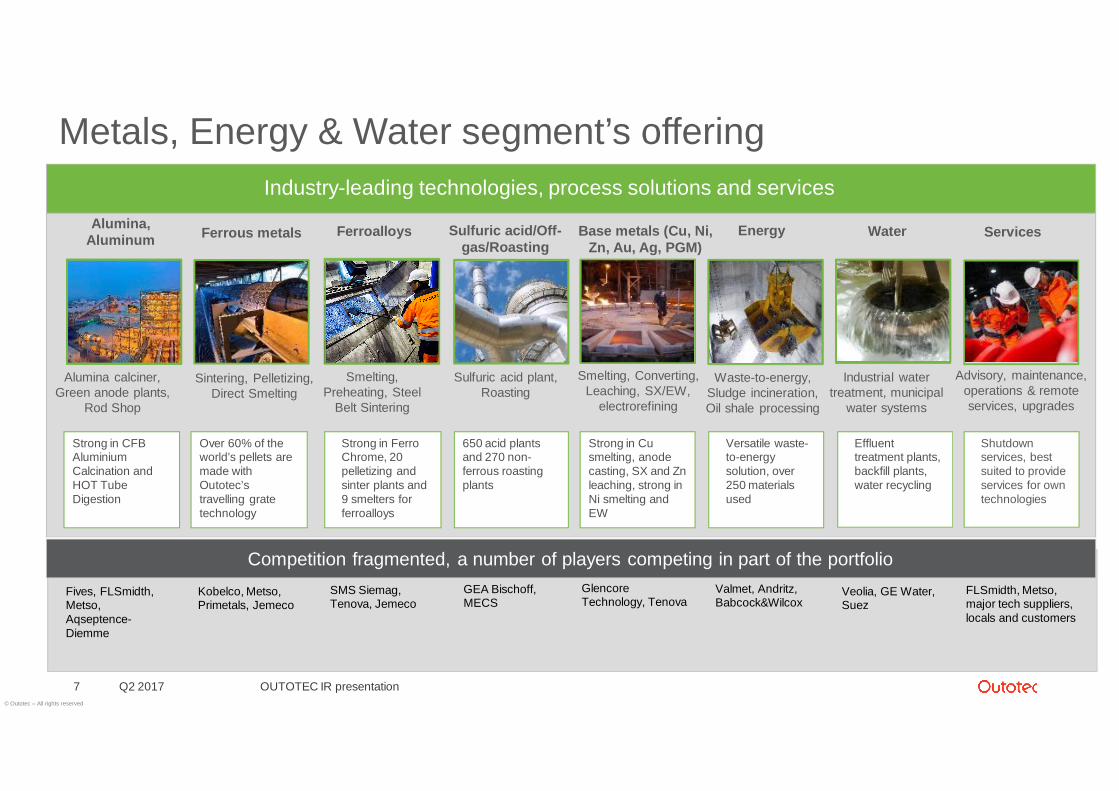

Metals, Energy & Water segment’s offering

Ferrous metals Sulfuric acid/Off-gas/Roasting

Fives, FLSmidth,Metso,Aqseptence-Diemme

Kobelco, Metso,Primetals, Jemeco

SMS Siemag,Tenova, Jemeco

GEA Bischoff,MECS

Alumina,Aluminum Base metals (Cu, Ni,

Zn, Au, Ag, PGM)Ferroalloys

GlencoreTechnology, Tenova

Strong in CFBAluminiumCalcination andHOT TubeDigestion

Over 60% of theworld’s pellets aremade withOutotec’stravelling gratetechnology

650 acid plantsand 270 non-ferrous roastingplants

Strong in Cusmelting, anodecasting, SX and Znleaching, strong inNi smelting andEW

Energy Water

Alumina calciner,Green anode plants,

Rod Shop

Sintering, Pelletizing,Direct Smelting

Sulfuric acid plant,Roasting

Smelting, Converting,Leaching, SX/EW,

electrorefining

Smelting,Preheating, Steel

Belt Sintering

Waste-to-energy,Sludge incineration,Oil shale processing

Industrial watertreatment, municipal

water systems

Competition fragmented, a number of players competing in part of the portfolio

Services

Advisory, maintenance,operations & remoteservices, upgrades

Valmet, Andritz,Babcock&Wilcox

Veolia, GE Water,Suez

FLSmidth, Metso,major tech suppliers,locals and customers

Strong in FerroChrome, 20pelletizing andsinter plants and9 smelters forferroalloys

Versatile waste-to-energysolution, over250 materialsused

Effluenttreatment plants,backfill plants,water recycling

Shutdownservices, bestsuited to provideservices for owntechnologies

© Outotec – All rights reserved

Long-term customer relationships with the industry’s topcompanies

Q2 2017 OUTOTEC IR presentation8

In history, top ten customers have accounted for some 35% of sales.

Major global mining companies Local mining and metallurgicalcompanies in emerging regionsIntermediate sized companies

Selected reference customers of Outotec

© Outotec – All rights reserved

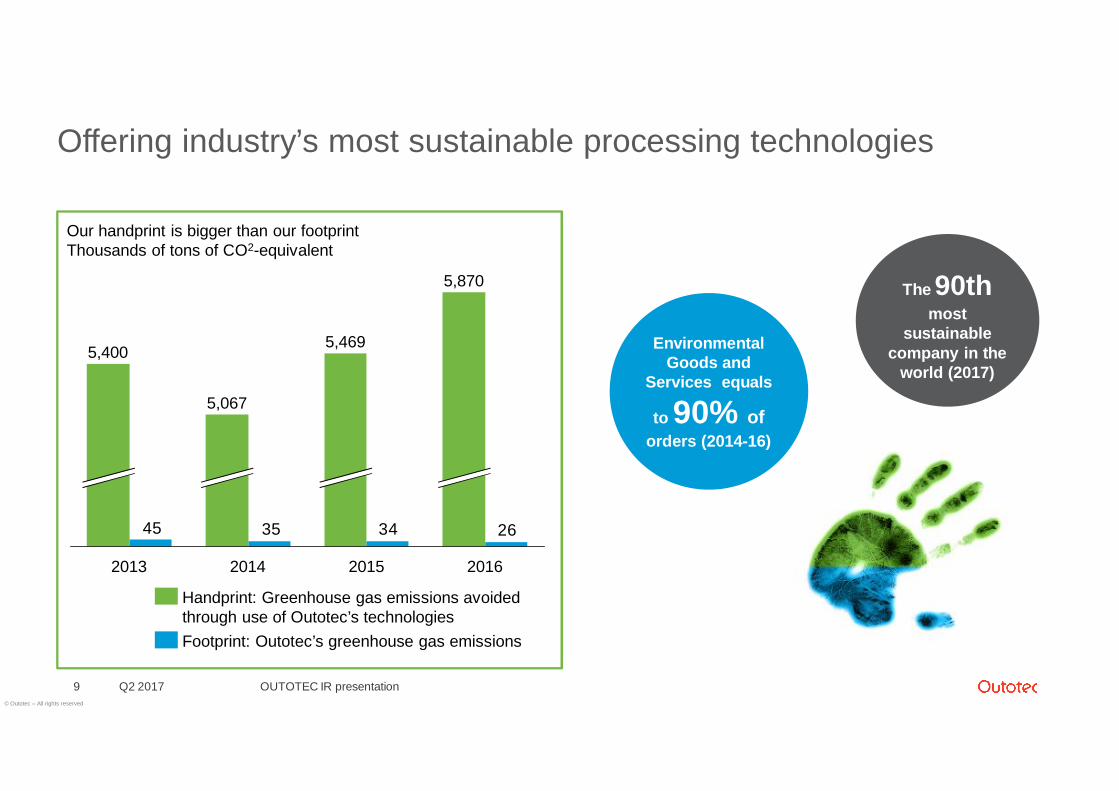

Offering industry’s most sustainable processing technologies

Q2 2017 OUTOTEC IR presentation9

26343545

5,870

2015

5,469

2014

5,067

2013

5,400

2016

Our handprint is bigger than our footprintThousands of tons of CO2-equivalent

Footprint: Outotec’s greenhouse gas emissions

Handprint: Greenhouse gas emissions avoidedthrough use of Outotec’s technologies

The 90thmost

sustainablecompany in the

world (2017)

EnvironmentalGoods and

Services equals

to 90% oforders (2014-16)

© Outotec – All rights reserved

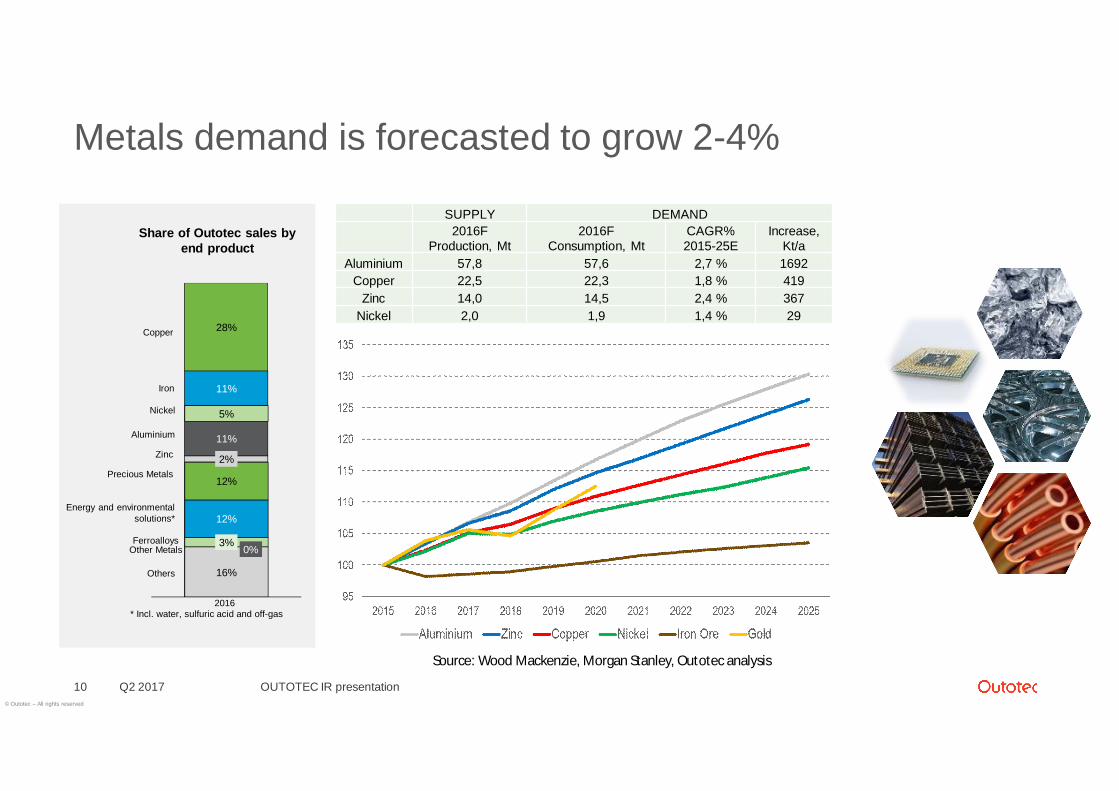

Metals demand is forecasted to grow 2-4%

Q2 2017 OUTOTEC IR presentation10

SUPPLY DEMAND2016F

Production, Mt2016F

Consumption, MtCAGR%2015-25E

Increase,Kt/a

Aluminium 57,8 57,6 2,7 % 1692Copper 22,5 22,3 1,8 % 419

Zinc 14,0 14,5 2,4 % 367Nickel 2,0 1,9 1,4 % 29

Source: Wood Mackenzie, Morgan Stanley, Outotec analysis

Share of Outotec sales byend product

* Incl. water, sulfuric acid and off-gas

16%

0%3%

12%

12%

2%

11%

5%

11%

28%

Others

Copper

Precious Metals

Zinc

Aluminium

Ferroalloys

Iron

Nickel

Other Metals

2016

Energy and environmentalsolutions*

© Outotec – All rights reserved

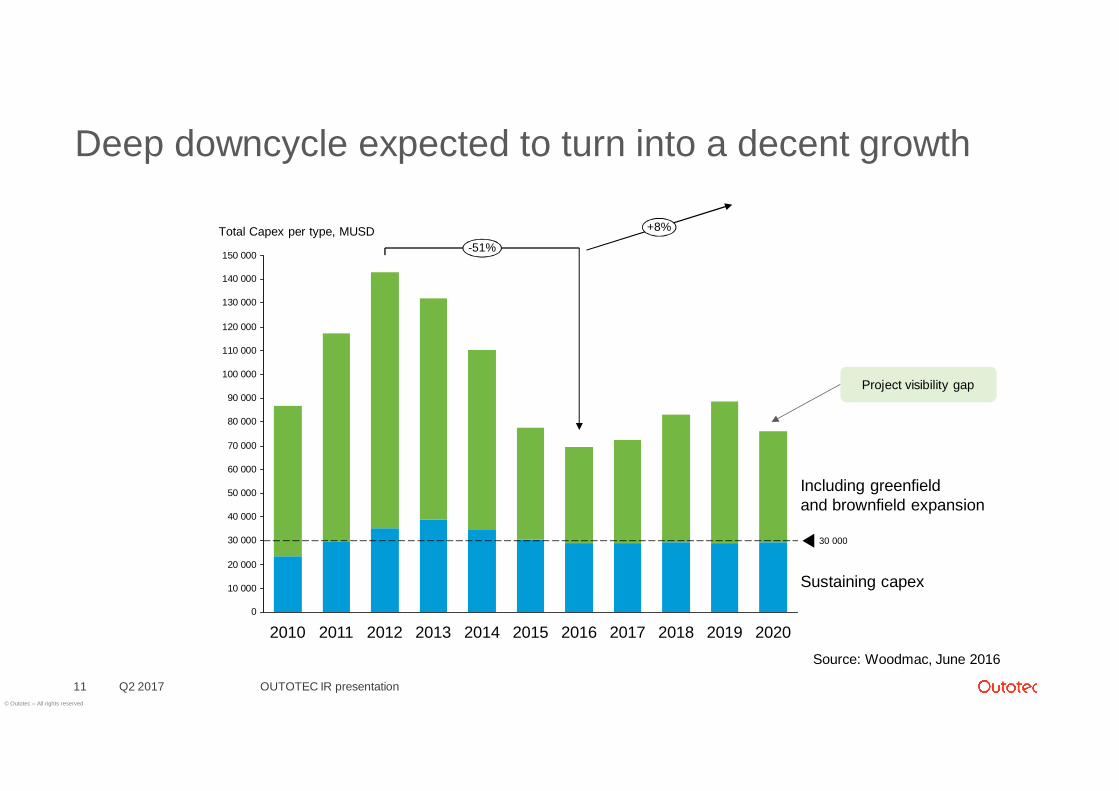

Deep downcycle expected to turn into a decent growth

Q2 2017 OUTOTEC IR presentation11

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

110 000

120 000

130 000

140 000

150 000

2019 2020201820172016201520142013201220112010

30 000

+8%

-51%

Sustaining capex

Including greenfieldand brownfield expansion

Total Capex per type, MUSD

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

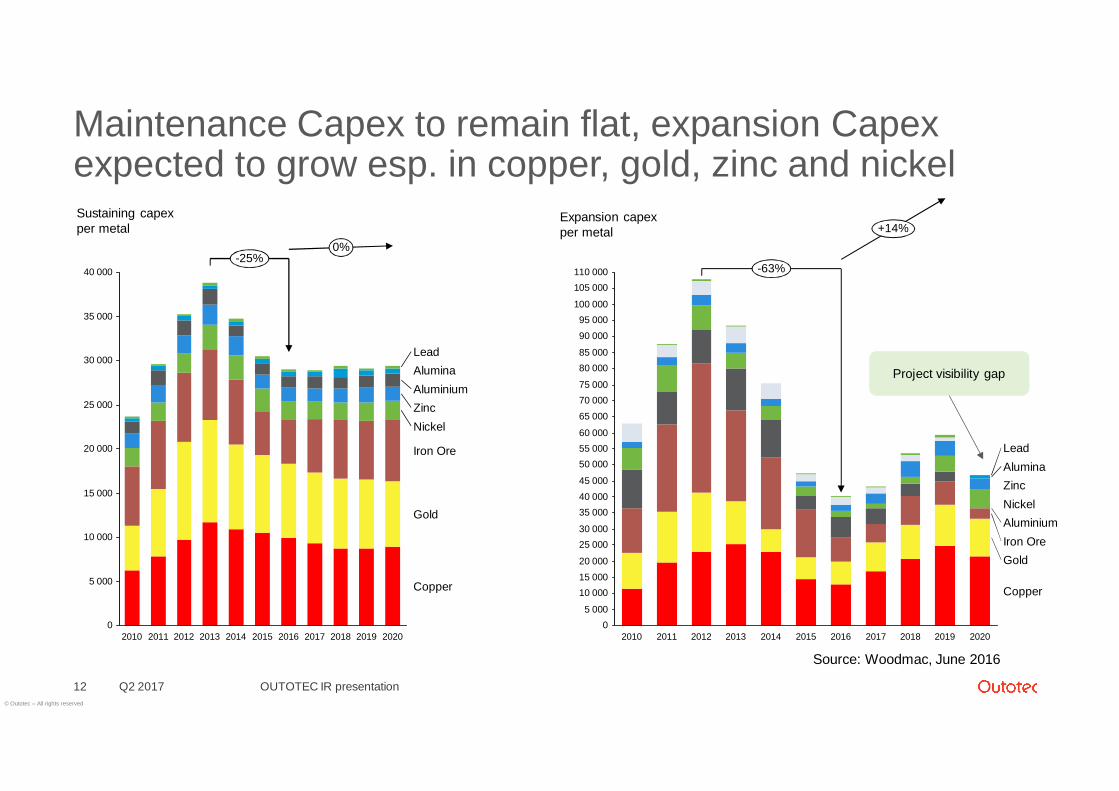

Maintenance Capex to remain flat, expansion Capexexpected to grow esp. in copper, gold, zinc and nickel

Q2 2017 OUTOTEC IR presentation12

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

0%-25%

Copper

Gold

Iron Ore

NickelZincAluminiumAluminaLead

202020192018201720162015201420132012201120100

5 000

10 00015 00020 000

25 00030 000

35 00040 00045 000

50 00055 00060 000

65 00070 00075 000

80 00085 000

90 00095 000

100 000

105 000110 000

20152014201320122011 201820172010 2016

+14%

-63%

Copper

GoldIron OreAluminiumNickelZincAluminaLead

20202019

Sustaining capexper metal

Expansion capexper metal

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

Long-term financial targets - Road map to 2020

Q2 2017 OUTOTEC IR presentation13

10%2020

CurrentaEBIT*

aEBIT*

ServicesR&D,Design-to-cost

Bestcostcountrysourcing

Efficiency

Annual averageservice sales growth5-15% (incl. M&A)

Gearing at max 50%

* Excluding restructuring and acquisition-related costs as well as purchase price allocation amortizations.

© Outotec – All rights reserved

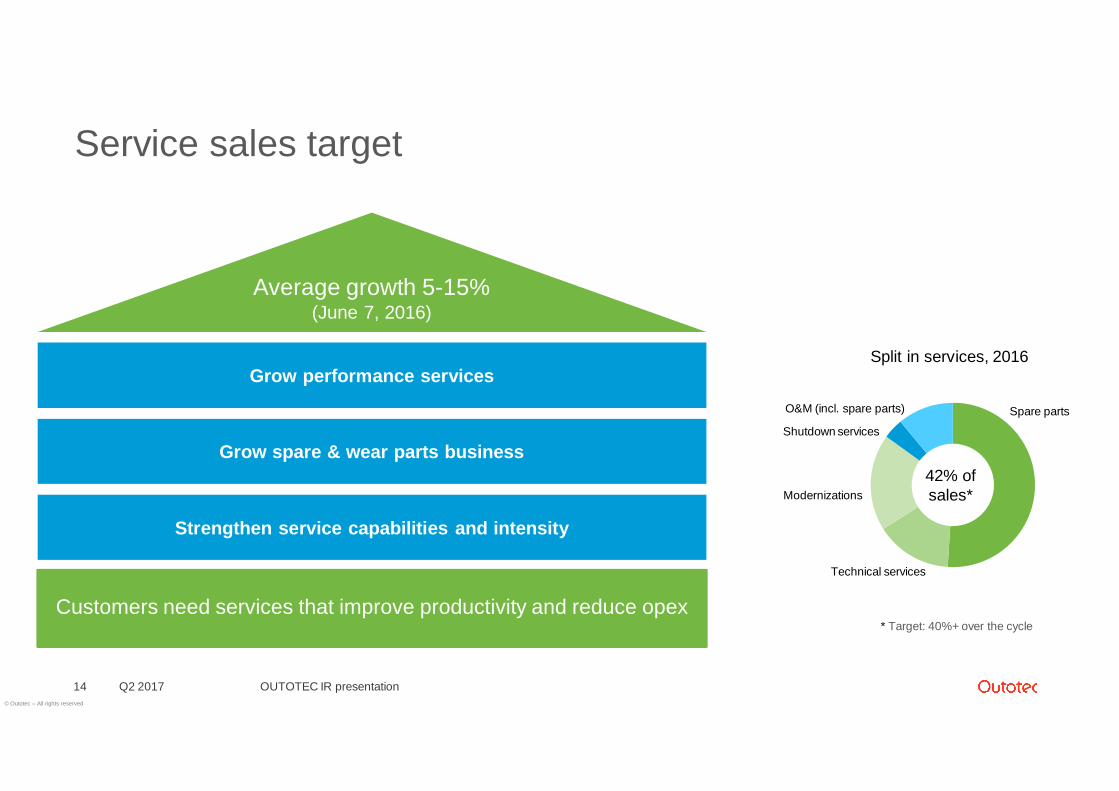

Service sales target

Q2 2017 OUTOTEC IR presentation14

Grow performance services

Grow spare & wear parts business

Strengthen service capabilities and intensity

Customers need services that improve productivity and reduce opex

Average growth 5-15%(June 7, 2016)

Spare parts

Technical services

Modernizations

Shutdown services

O&M (incl. spare parts)

Split in services, 2016

42% ofsales*

* Target: 40%+ over the cycle

© Outotec – All rights reserved

Q2 2017 financial information

Q2 2017 OUTOTEC IR presentation15

© Outotec – All rights reserved

Service ordersup 15%

Goodperformance in

MP

Order intakeimproved 34%

MEW’s recoverypending, actions

continue

Markets in SEA,Australia and

Europeactivated in Q2

H1 in a nutshell

Q2 2017 OUTOTEC IR presentation16

© Outotec – All rights reserved

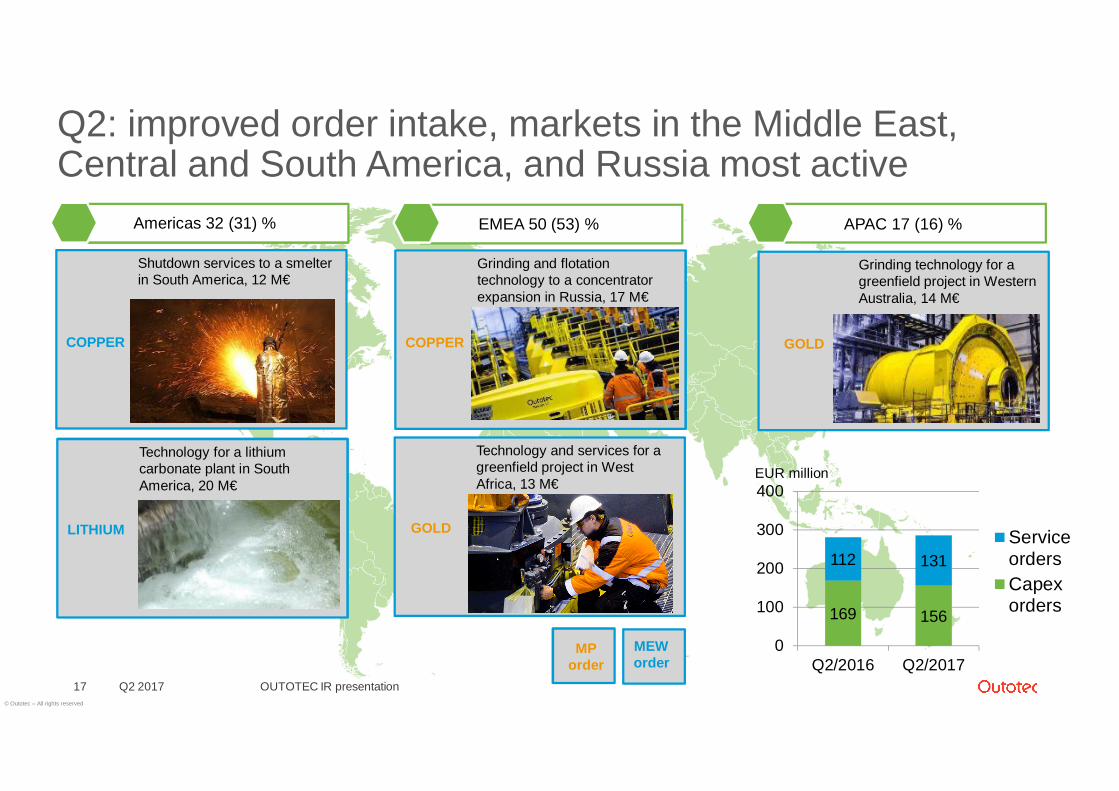

Q2: improved order intake, markets in the Middle East,Central and South America, and Russia most active

Q2 2017 OUTOTEC IR presentation17

Americas 32 (31) %

GOLD

Technology and services for agreenfield project in WestAfrica, 13 M€

COPPER

Shutdown services to a smelterin South America, 12 M€

GOLD

Grinding technology for agreenfield project in WesternAustralia, 14 M€

169 156

112 131

0

100

200

300

400

Q2/2016 Q2/2017

ServiceordersCapexorders

MEWorder

MPorder

EUR million

COPPER

Grinding and flotationtechnology to a concentratorexpansion in Russia, 17 M€

LITHIUM

Technology for a lithiumcarbonate plant in SouthAmerica, 20 M€

EMEA 50 (53) % APAC 17 (16) %

© Outotec – All rights reserved

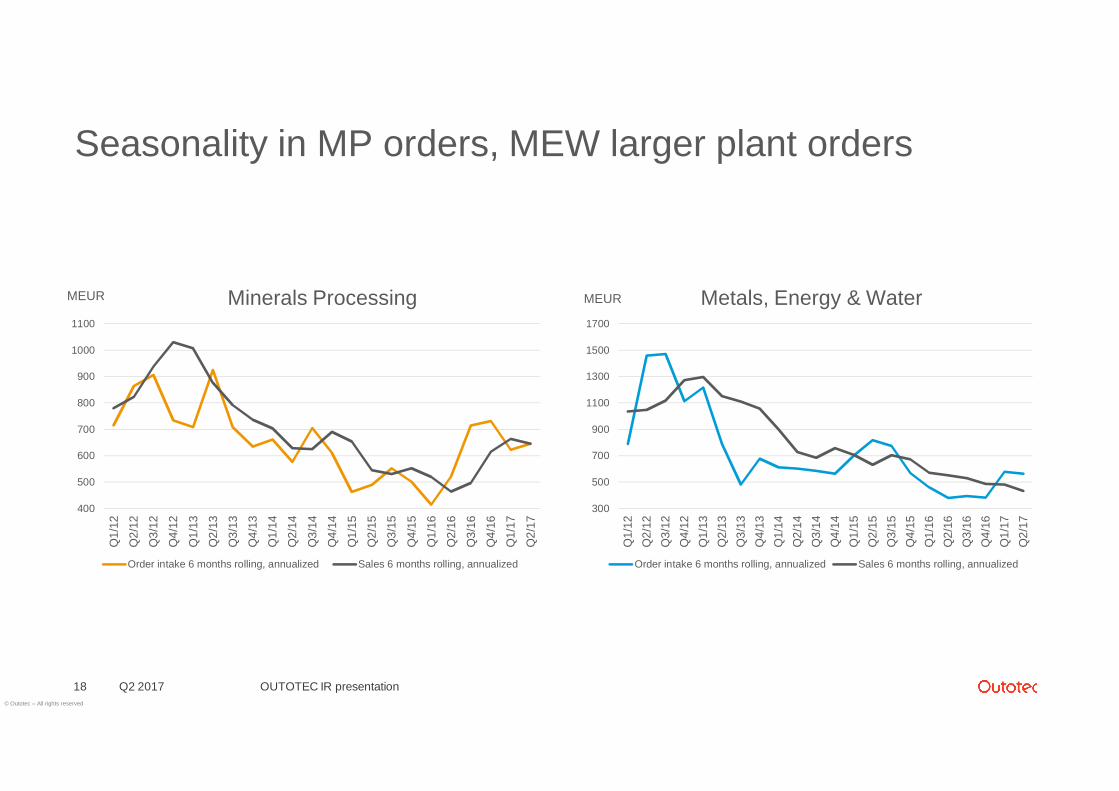

Seasonality in MP orders, MEW larger plant orders

Q2 2017 OUTOTEC IR presentation18

MEUR MEUR

300

500

700

900

1100

1300

1500

1700

Q1/

12Q

2/12

Q3/

12Q

4/12

Q1/

13Q

2/13

Q3/

13Q

4/13

Q1/

14Q

2/14

Q3/

14Q

4/14

Q1/

15Q

2/15

Q3/

15Q

4/15

Q1/

16Q

2/16

Q3/

16Q

4/16

Q1/

17Q

2/17

Metals, Energy & Water

Order intake 6 months rolling, annualized Sales 6 months rolling, annualized

400

500

600

700

800

900

1000

1100

Q1/

12

Q2/

12

Q3/

12

Q4/

12

Q1/

13

Q2/

13

Q3/

13

Q4/

13

Q1/

14

Q2/

14

Q3/

14

Q4/

14

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Minerals Processing

Order intake 6 months rolling, annualized Sales 6 months rolling, annualized

© Outotec – All rights reserved

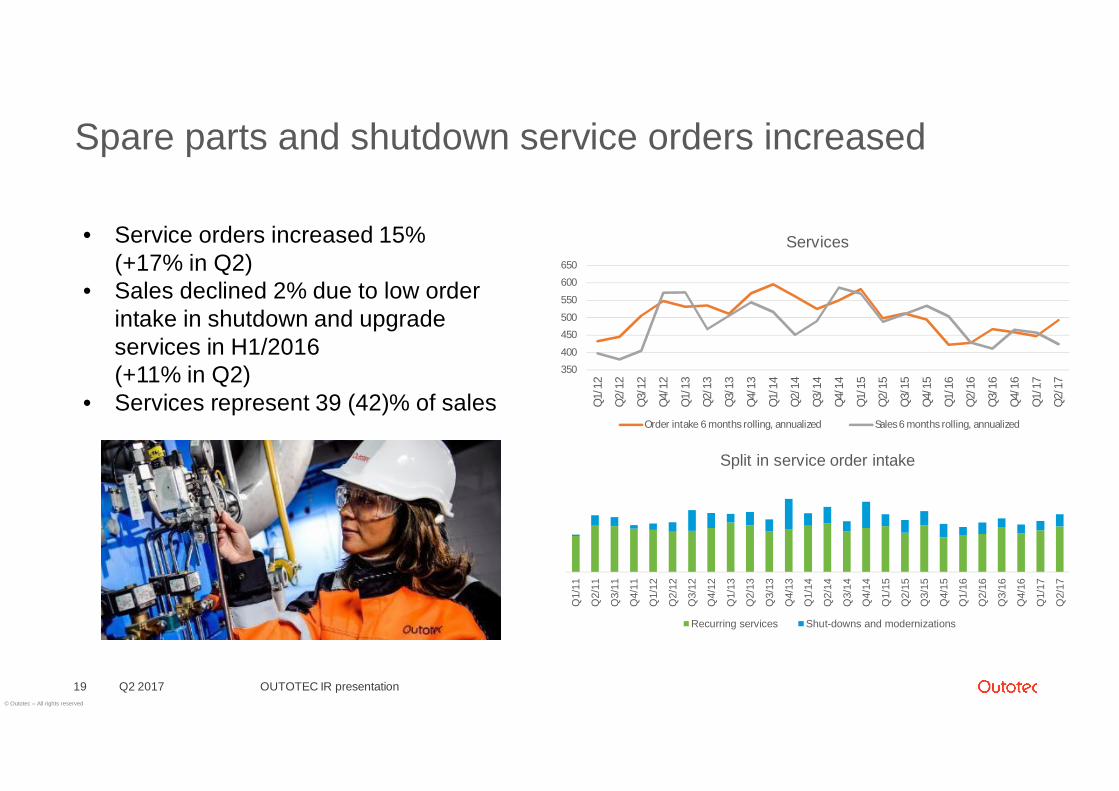

Spare parts and shutdown service orders increased

Q2 2017 OUTOTEC IR presentation19

• Service orders increased 15%(+17% in Q2)

• Sales declined 2% due to low orderintake in shutdown and upgradeservices in H1/2016(+11% in Q2)

• Services represent 39 (42)% of sales350

400

450

500

550

600

650

Q1/

12

Q2/

12

Q3/

12

Q4/

12

Q1/

13

Q2/

13

Q3/

13

Q4/

13

Q1/

14

Q2/

14

Q3/

14

Q4/

14

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Services

Order intake 6 months rolling, annualized Sales 6 months rolling, annualized

Q1/

11

Q2/

11

Q3/

11

Q4/

11

Q1/

12

Q2/

12

Q3/

12

Q4/

12

Q1/

13

Q2/

13

Q3/

13

Q4/

13

Q1/

14

Q2/

14

Q3/

14

Q4/

14

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Split in service order intake

Recurring services Shut-downs and modernizations

© Outotec – All rights reserved

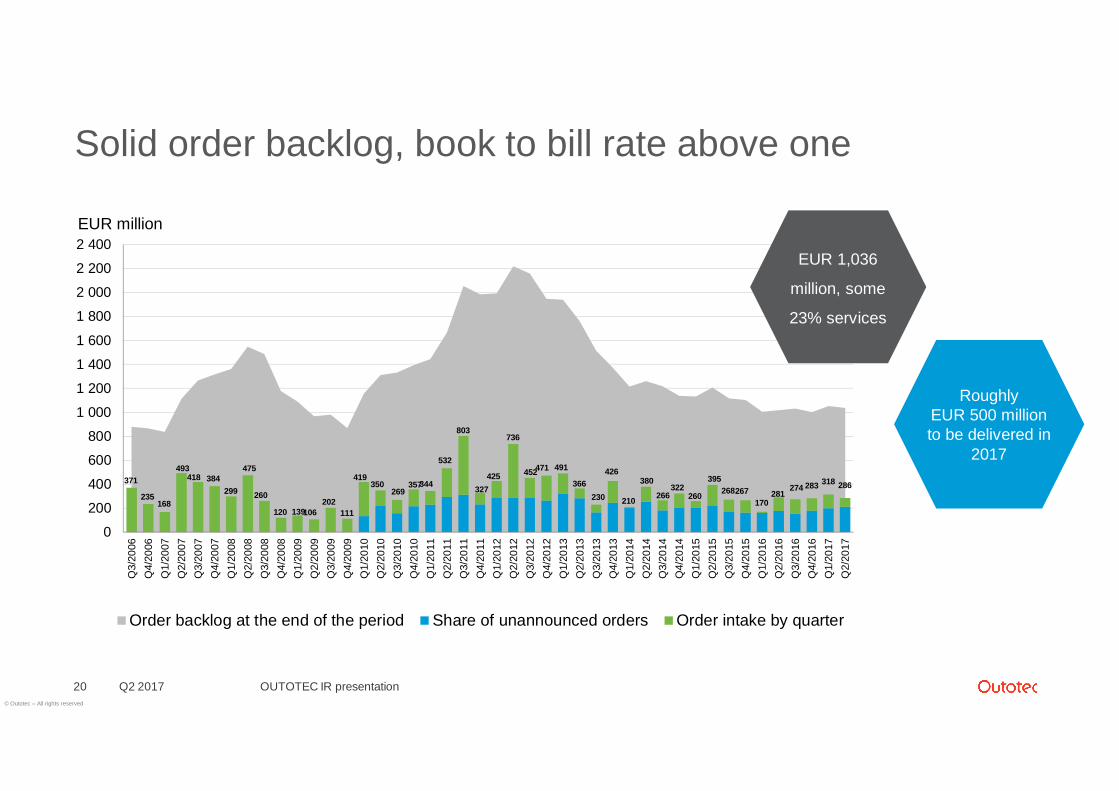

Solid order backlog, book to bill rate above one

Q2 2017 OUTOTEC IR presentation20

EUR million

371

235168

493418 384

299

475

260

120 139106202

111

419350

269357344

532

803

327425

736

452471 491

366230

426

210

380

266322

260

395268267

170281

274 283 318 286

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

Q3/

2006

Q4/

2006

Q1/

2007

Q2/

2007

Q3/

2007

Q4/

2007

Q1/

2008

Q2/

2008

Q3/

2008

Q4/

2008

Q1/

2009

Q2/

2009

Q3/

2009

Q4/

2009

Q1/

2010

Q2/

2010

Q3/

2010

Q4/

2010

Q1/

2011

Q2/

2011

Q3/

2011

Q4/

2011

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Q4/

2016

Q1/

2017

Q2/

2017

Order backlog at the end of the period Share of unannounced orders Order intake by quarter

RoughlyEUR 500 millionto be delivered in

2017

EUR 1,036

million, some

23% services

© Outotec – All rights reserved

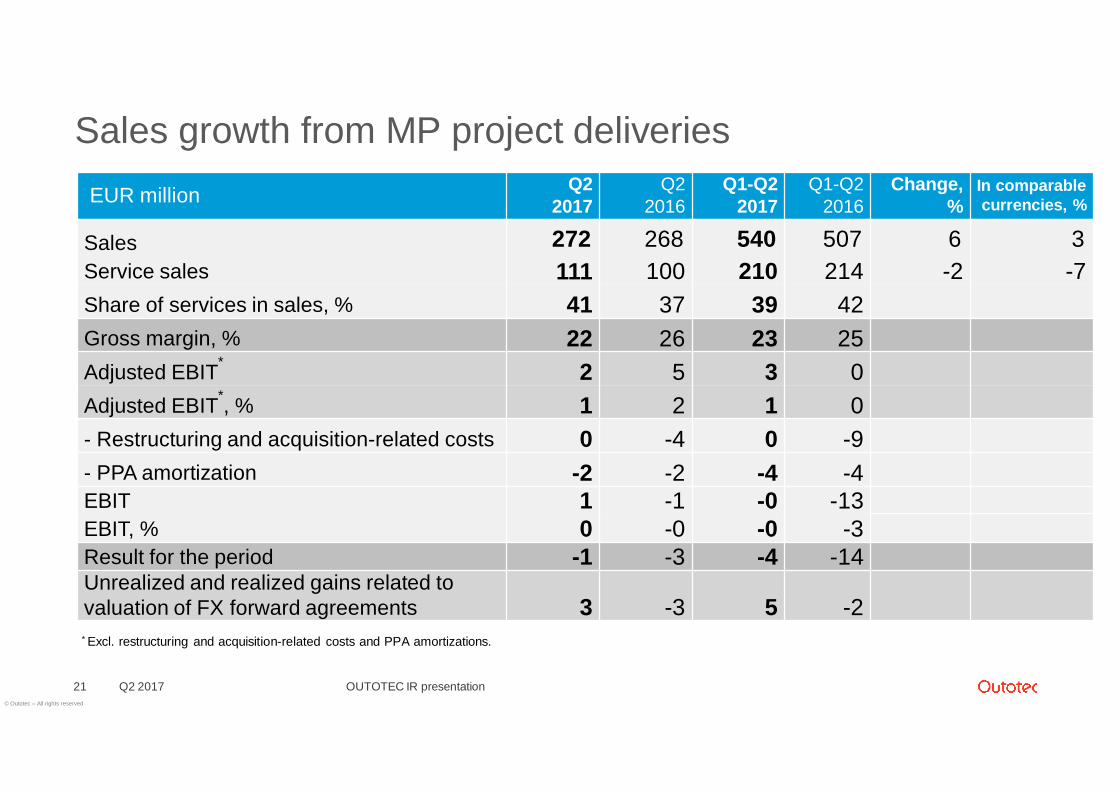

Sales growth from MP project deliveries

Q2 2017 OUTOTEC IR presentation21

EUR million Q22017

Q22016

Q1-Q22017

Q1-Q22016

Change,%

In comparablecurrencies, %

Sales 272 268 540 507 6 3Service sales 111 100 210 214 -2 -7Share of services in sales, % 41 37 39 42Gross margin, % 22 26 23 25Adjusted EBIT* 2 5 3 0Adjusted EBIT*, % 1 2 1 0- Restructuring and acquisition-related costs 0 -4 0 -9- PPA amortization -2 -2 -4 -4EBIT 1 -1 -0 -13EBIT, % 0 -0 -0 -3Result for the period -1 -3 -4 -14Unrealized and realized gains related tovaluation of FX forward agreements 3 -3 5 -2* Excl. restructuring and acquisition-related costs and PPA amortizations.

© Outotec – All rights reserved

3

0

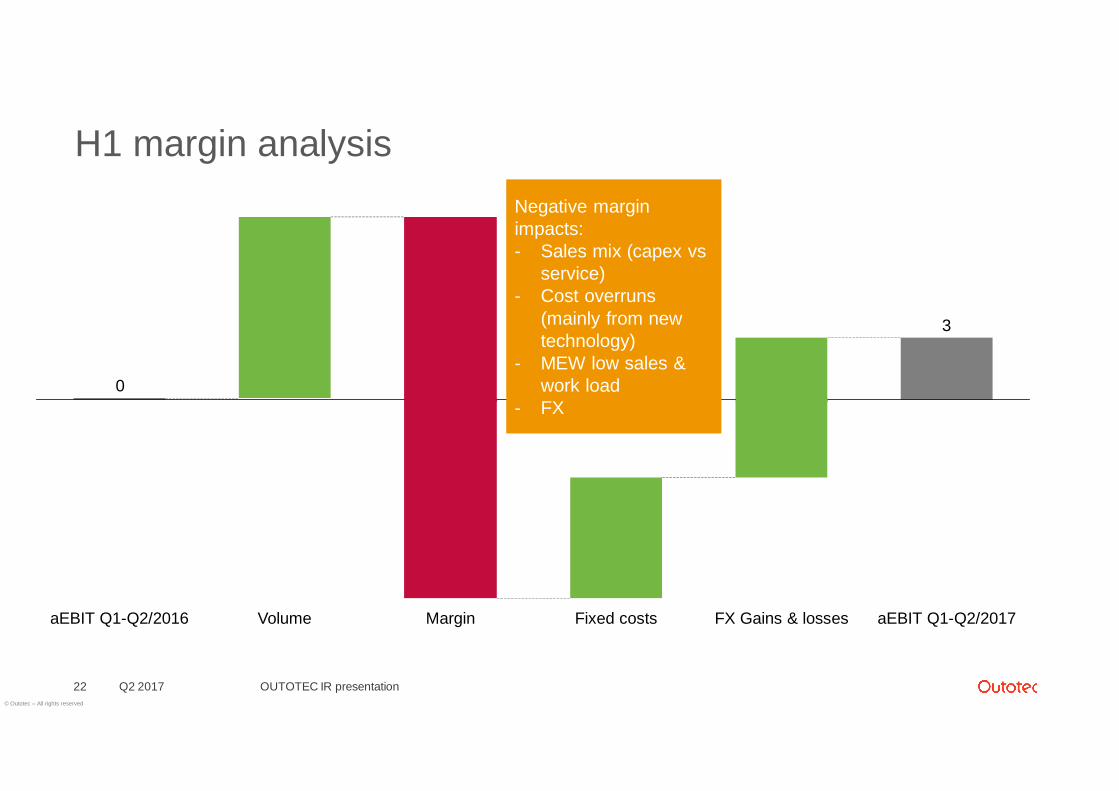

H1 margin analysis

Q2 2017 OUTOTEC IR presentation22

Negative marginimpacts:- Sales mix (capex vs

service)- Cost overruns

(mainly from newtechnology)

- MEW low sales &work load

- FX

FX Gains & losses aEBIT Q1-Q2/2017Fixed costsVolumeaEBIT Q1-Q2/2016 Margin

© Outotec – All rights reserved

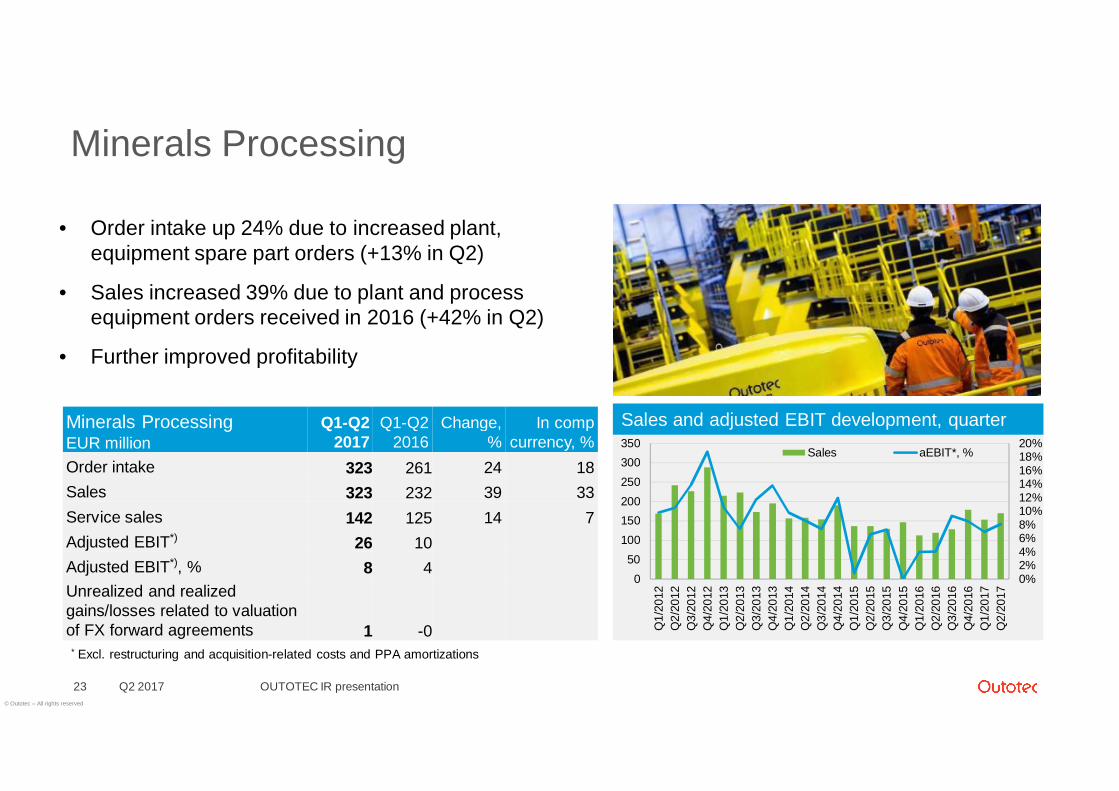

Minerals Processing

Q2 2017 OUTOTEC IR presentation23

0%2%4%6%8%10%12%14%16%18%20%

050

100150200250300350

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Q4/

2016

Q1/

2017

Q2/

2017

Sales aEBIT*, %

Sales and adjusted EBIT development, quarter

• Order intake up 24% due to increased plant,equipment spare part orders (+13% in Q2)

• Sales increased 39% due to plant and processequipment orders received in 2016 (+42% in Q2)

• Further improved profitability

Minerals ProcessingEUR million

Q1-Q22017

Q1-Q22016

Change,%

In compcurrency, %

Order intake 323 261 24 18Sales 323 232 39 33Service sales 142 125 14 7Adjusted EBIT*) 26 10Adjusted EBIT*), % 8 4Unrealized and realizedgains/losses related to valuationof FX forward agreements 1 -0

* Excl. restructuring and acquisition-related costs and PPA amortizations

© Outotec – All rights reserved

-40%

-30%

-20%

-10%

0%

10%

20%

050

100150200250300350400

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Q4/

2016

Q1/

2017

Q2/

2017

Sales aEBIT*, %

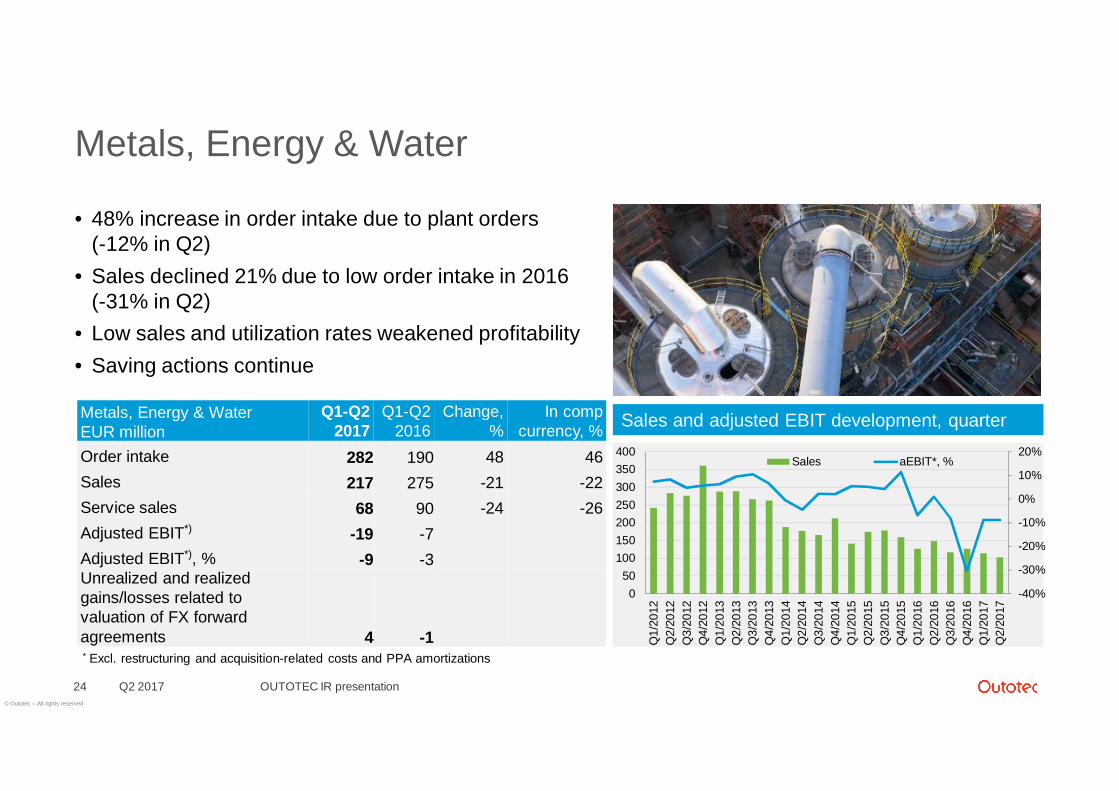

Metals, Energy & Water

• 48% increase in order intake due to plant orders(-12% in Q2)

• Sales declined 21% due to low order intake in 2016(-31% in Q2)

• Low sales and utilization rates weakened profitability• Saving actions continue

Q2 2017 OUTOTEC IR presentation24

Metals, Energy & WaterEUR million

Q1-Q22017

Q1-Q22016

Change,%

In compcurrency, %

Order intake 282 190 48 46Sales 217 275 -21 -22Service sales 68 90 -24 -26Adjusted EBIT*) -19 -7Adjusted EBIT*), % -9 -3Unrealized and realizedgains/losses related tovaluation of FX forwardagreements 4 -1* Excl. restructuring and acquisition-related costs and PPA amortizations

Sales and adjusted EBIT development, quarter

© Outotec – All rights reserved

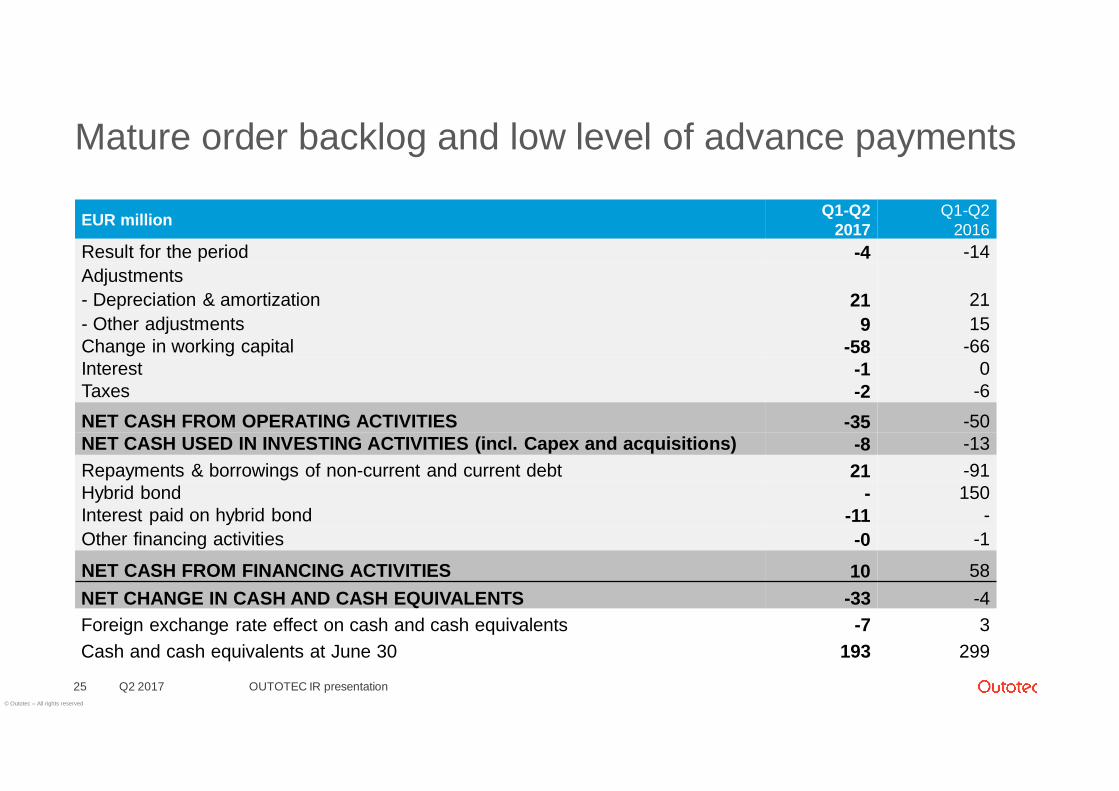

Mature order backlog and low level of advance payments

Q2 2017 OUTOTEC IR presentation25

EUR million Q1-Q22017

Q1-Q22016

Result for the period -4 -14Adjustments- Depreciation & amortization 21 21- Other adjustments 9 15Change in working capital -58 -66Interest -1 0Taxes -2 -6NET CASH FROM OPERATING ACTIVITIES -35 -50NET CASH USED IN INVESTING ACTIVITIES (incl. Capex and acquisitions) -8 -13Repayments & borrowings of non-current and current debt 21 -91Hybrid bond - 150Interest paid on hybrid bond -11 -Other financing activities -0 -1

NET CASH FROM FINANCING ACTIVITIES 10 58NET CHANGE IN CASH AND CASH EQUIVALENTS -33 -4Foreign exchange rate effect on cash and cash equivalents -7 3Cash and cash equivalents at June 30 193 299

© Outotec – All rights reserved

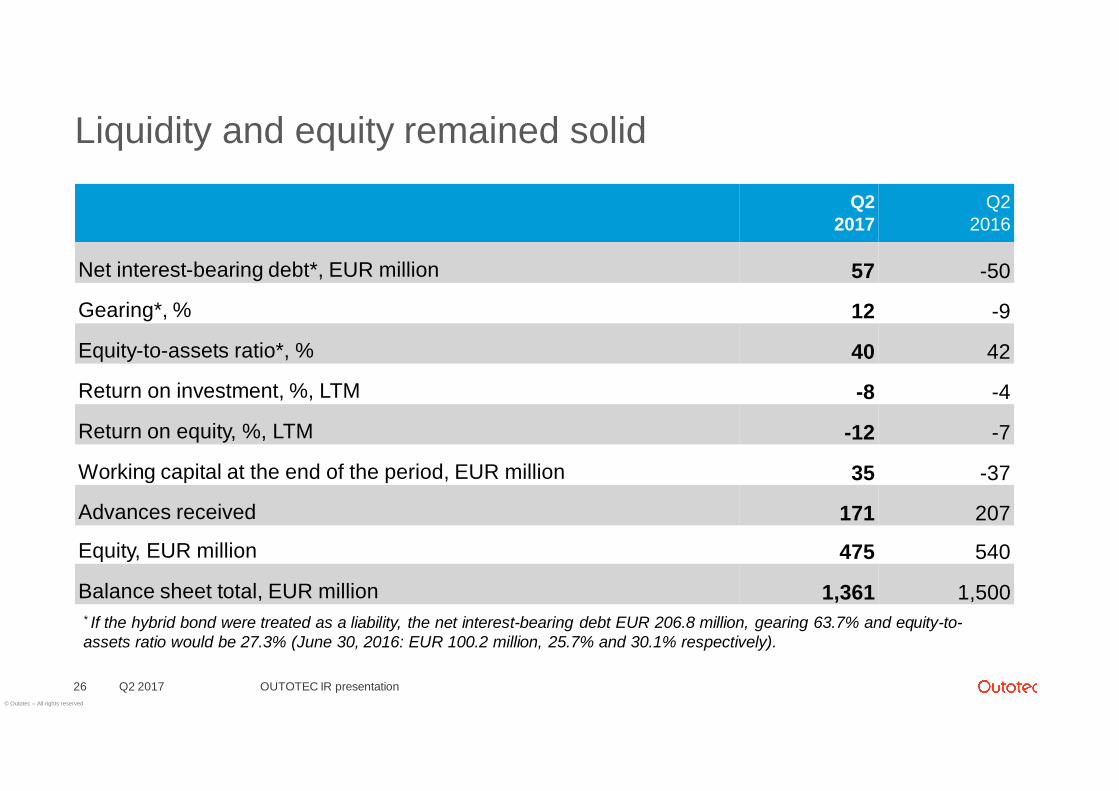

Liquidity and equity remained solid

Q2 2017 OUTOTEC IR presentation26

Q22017

Q22016

Net interest-bearing debt*, EUR million 57 -50

Gearing*, % 12 -9

Equity-to-assets ratio*, % 40 42

Return on investment, %, LTM -8 -4

Return on equity, %, LTM -12 -7

Working capital at the end of the period, EUR million 35 -37

Advances received 171 207

Equity, EUR million 475 540

Balance sheet total, EUR million 1,361 1,500* If the hybrid bond were treated as a liability, the net interest-bearing debt EUR 206.8 million, gearing 63.7% and equity-to-assets ratio would be 27.3% (June 30, 2016: EUR 100.2 million, 25.7% and 30.1% respectively).

© Outotec – All rights reserved

Market outlook

Q2 2017 OUTOTEC IR presentation27

Serviceopportunities inall categories

Several basemetals, lithium,sulfuric acid and

energyprospects

Stable marketfor MP

expected tocontinue

Timing of largeMEW orders

difficult toforesee

© Outotec – All rights reserved

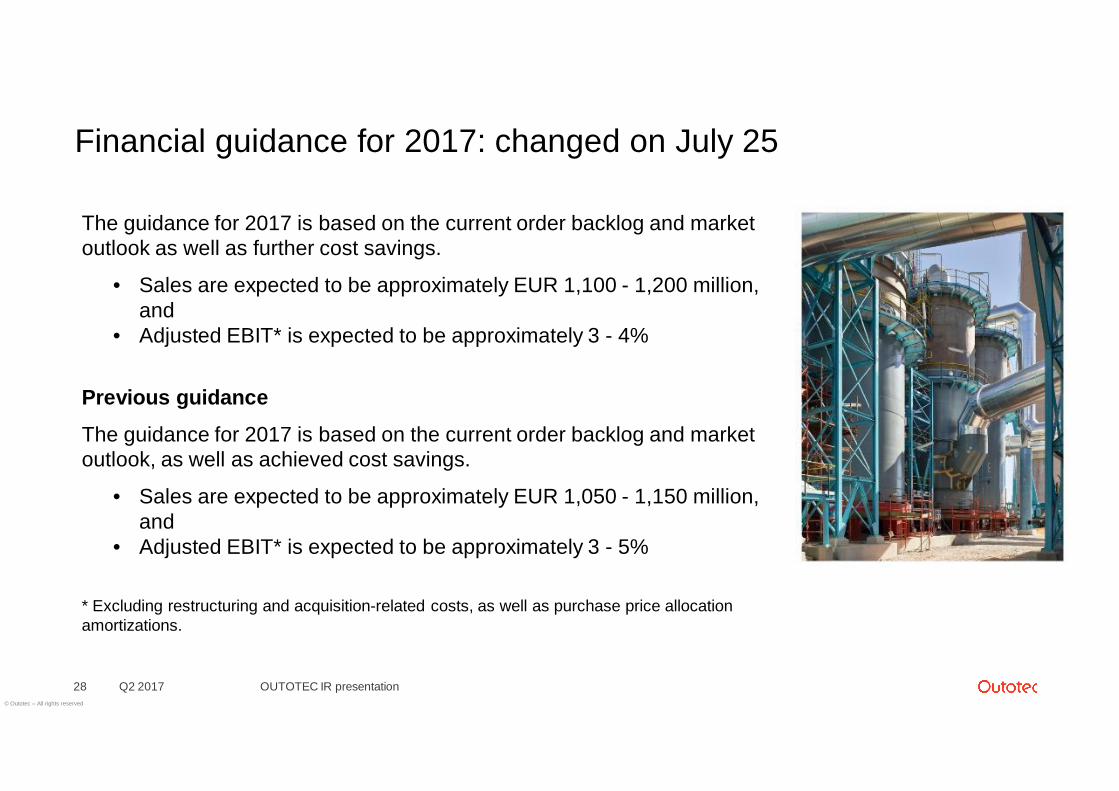

Financial guidance for 2017: changed on July 25

Q2 2017 OUTOTEC IR presentation28

The guidance for 2017 is based on the current order backlog and marketoutlook as well as further cost savings.

• Sales are expected to be approximately EUR 1,100 - 1,200 million,and

• Adjusted EBIT* is expected to be approximately 3 - 4%

Previous guidance

The guidance for 2017 is based on the current order backlog and marketoutlook, as well as achieved cost savings.

• Sales are expected to be approximately EUR 1,050 - 1,150 million,and

• Adjusted EBIT* is expected to be approximately 3 - 5%

* Excluding restructuring and acquisition-related costs, as well as purchase price allocationamortizations.

© Outotec – All rights reserved

Our focus areas for 2017 - towards profitable growth!

Q2 2017 OUTOTEC IR presentation29

• Continue to win orders in a competitivemarket

• Continue cost savings

• Strong focus on service business

• Improve cost competitiveness ofproducts

• Strengthen customer centricityCMD - September 21

Outotec House - Espoo

© Outotec – All rights reserved

POC and cash flow profile example

Q2 2017 OUTOTEC IR presentation30

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27POC Cumulative cashflow

MEUR

Month

Total order backlogstructure in 2012

Total order backlogstructure in 2015

0% 100%

Percentage of Completion, %Timing of large projectcompletions, andpossible release ofprovisions, affectsquarterly earnings.

Advancepayment~10-30%

NOTE: The figures are illustrative and vary project by project

Timing of large project completions affects quarterly earnings

© Outotec – All rights reserved

Interest bearing loans and hybrid bond - repayment profile

Q2 201731

0

50

100

150

200

250

300

350

400

450

Q2/

17Q

3/17

Q4/

17Q

1/18

Q2/

18Q

3/18

Q4/

18Q

1/19

Q2/

19Q

3/19

Q4/

19Q

1/20

Q2/

20Q

3/20

Q4/

20Q

1/21

MEUR

Hybrid bond

EIB R&D loan

Senior unsecured bond

Other IB debt

OUTOTEC IR presentation

© Outotec – All rights reserved

Customer solutions

Q2 2017 OUTOTEC IR presentation32

© Outotec – All rights reserved

Minerals Processing: Laiva Gold mine in FinlandOre sorting

Q2 2017 OUTOTEC IR presentation33

Outotec solution• Sensor-based ore sortingsolution removing wasterock and improving thehead grade

• Less ore feed to thecrushing and grindingcircuit, reducing energy andwater consumption

Customer challenge• Mine is closed because of lowhead grade ore

• Ore sorting solution for reopeningthe mine

“The economic assessment for theLaiva Gold Mine indicated thepotential for restarting the site.Base-case net present value of €77million, producing 529,000 troyounces of gold over a seven-yearmine life.”

© Outotec – All rights reserved

Minerals Processing: reducing mill downtime at a gold mineComminution

Q2 2017 OUTOTEC IR presentation34

Customer challenge• Excessive grinding mill downtime• Unplanned downtime due to liner failure• Inadequate tooling• Limited shutdown planning• Coordination between maintenance vendors• Over 340 hours downtime due to mill maintenance

Outotec solution• Pre shutdown planning• Liner redesign (to reduce number of pieces)• Tooling improvements (liner handler, skid steers & hand tooling)• Changes to liner fixtures & fittings• Continuous Improvement Program• Optimizing with Outotec patented MillMapper™ software

Customer benefits• 50% less downtime due to

mill maintenance• Reduction of 170 hours of

reline incurred downtime• Safer, less labor intensive

relines• C. 12-14 million USD in

additional production revenue

© Outotec – All rights reserved

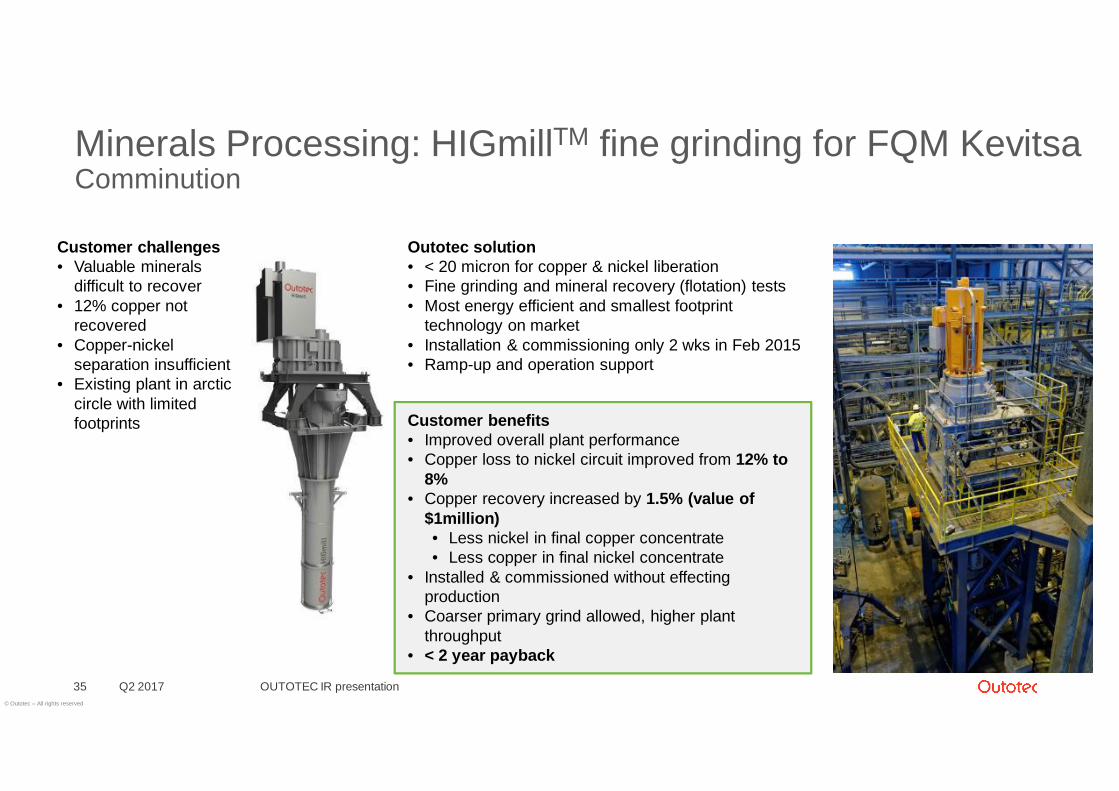

Minerals Processing: HIGmillTM fine grinding for FQM KevitsaComminution

Customer challenges• Valuable minerals

difficult to recover• 12% copper not

recovered• Copper-nickel

separation insufficient• Existing plant in arctic

circle with limitedfootprints

Q2 2017 OUTOTEC IR presentation35

Outotec solution• < 20 micron for copper & nickel liberation• Fine grinding and mineral recovery (flotation) tests• Most energy efficient and smallest footprint

technology on market• Installation & commissioning only 2 wks in Feb 2015• Ramp-up and operation support

Customer benefits• Improved overall plant performance• Copper loss to nickel circuit improved from 12% to

8%• Copper recovery increased by 1.5% (value of

$1million)• Less nickel in final copper concentrate• Less copper in final nickel concentrate

• Installed & commissioned without effectingproduction

• Coarser primary grind allowed, higher plantthroughput

• < 2 year payback

© Outotec – All rights reserved

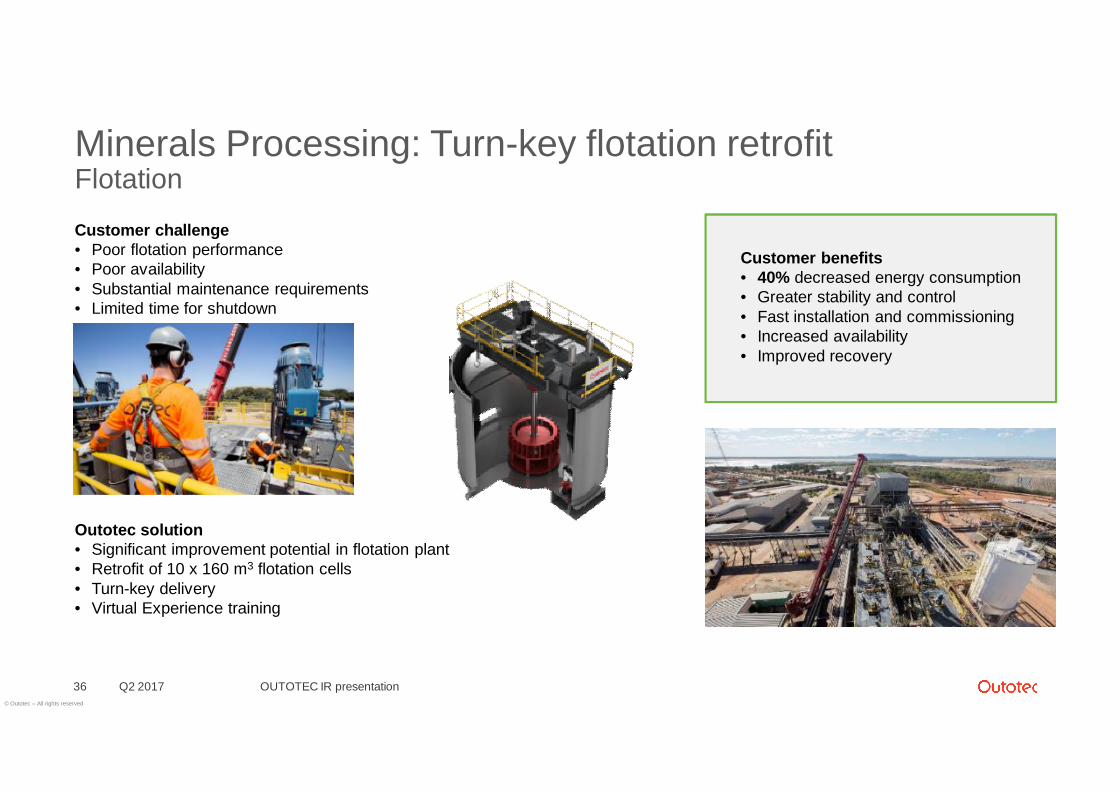

Minerals Processing: Turn-key flotation retrofitFlotation

Customer challenge• Poor flotation performance• Poor availability• Substantial maintenance requirements• Limited time for shutdown

Q2 2017 OUTOTEC IR presentation36

Customer benefits• 40% decreased energy consumption• Greater stability and control• Fast installation and commissioning• Increased availability• Improved recovery

Outotec solution• Significant improvement potential in flotation plant• Retrofit of 10 x 160 m3 flotation cells• Turn-key delivery• Virtual Experience training

© Outotec – All rights reserved

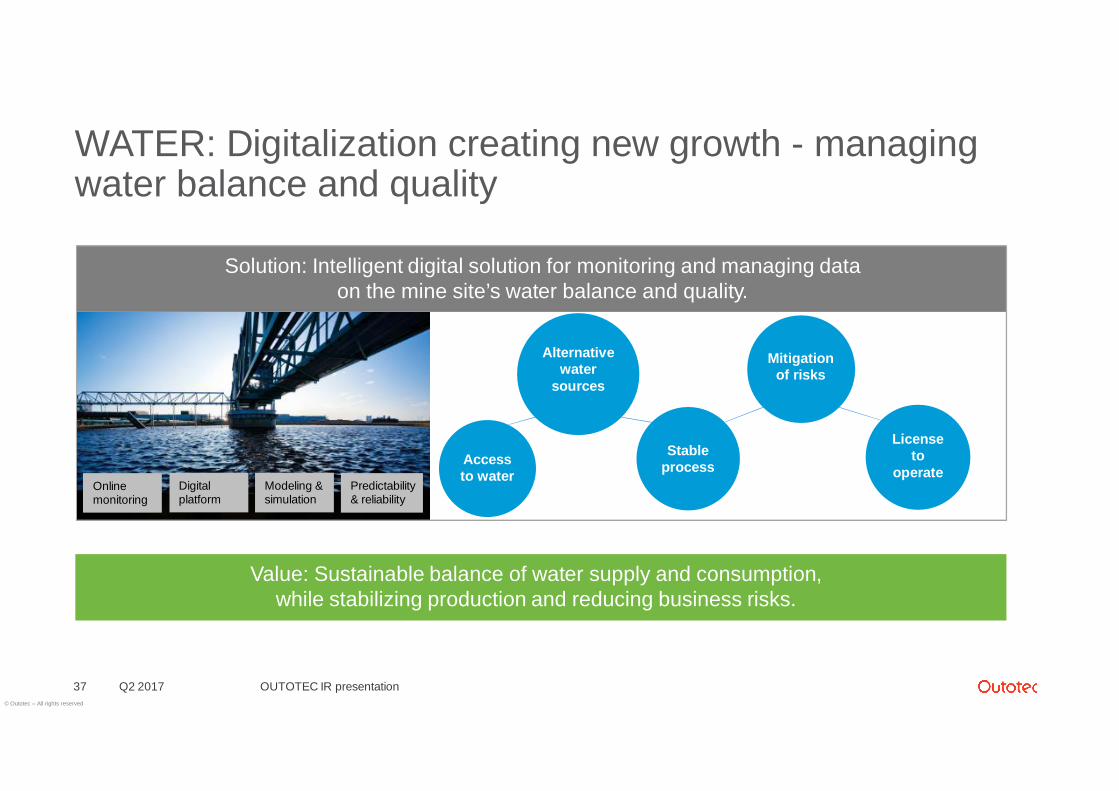

WATER: Digitalization creating new growth - managingwater balance and quality

Q2 2017 OUTOTEC IR presentation37

Solution: Intelligent digital solution for monitoring and managing dataon the mine site’s water balance and quality.

Value: Sustainable balance of water supply and consumption,while stabilizing production and reducing business risks.

Onlinemonitoring

Digitalplatform

Modeling &simulation

Predictability& reliability

Accessto water

Alternativewater

sources

Stableprocess

Mitigationof risks

Licenseto

operate

© Outotec – All rights reserved

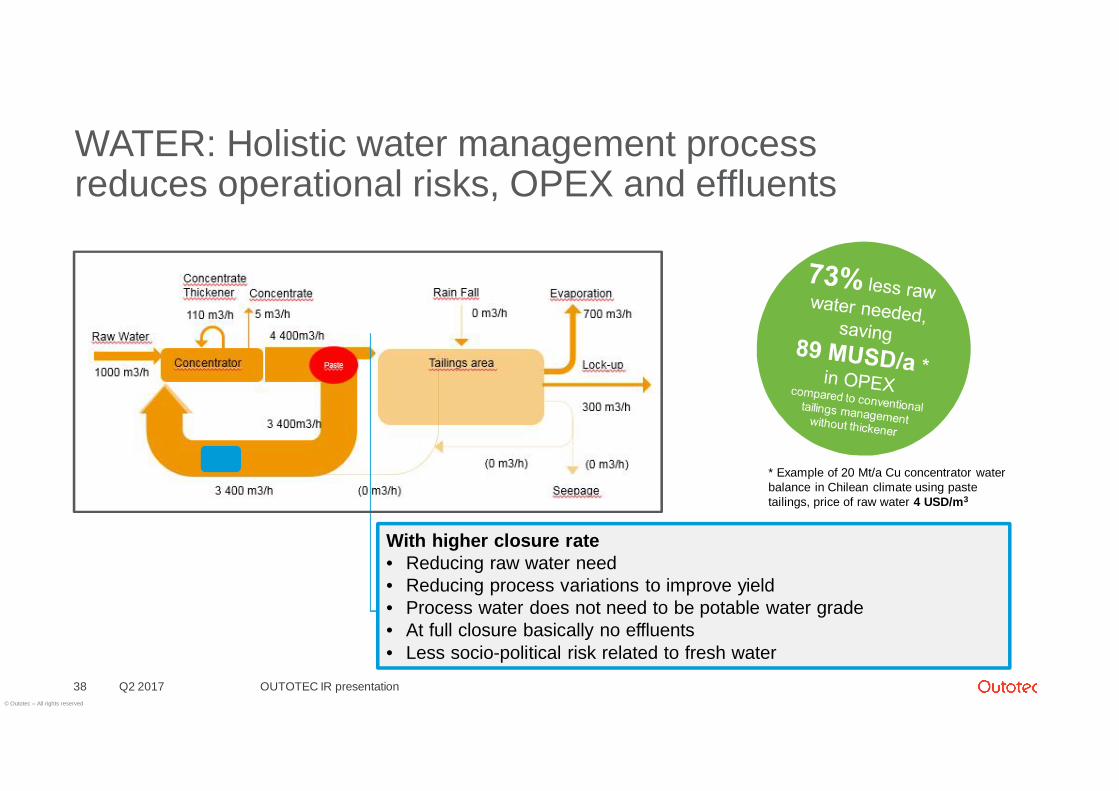

WATER: Holistic water management processreduces operational risks, OPEX and effluents

Q2 201738

With higher closure rate• Reducing raw water need• Reducing process variations to improve yield• Process water does not need to be potable water grade• At full closure basically no effluents• Less socio-political risk related to fresh water

OUTOTEC IR presentation

* Example of 20 Mt/a Cu concentrator waterbalance in Chilean climate using pastetailings, price of raw water 4 USD/m3

© Outotec – All rights reserved

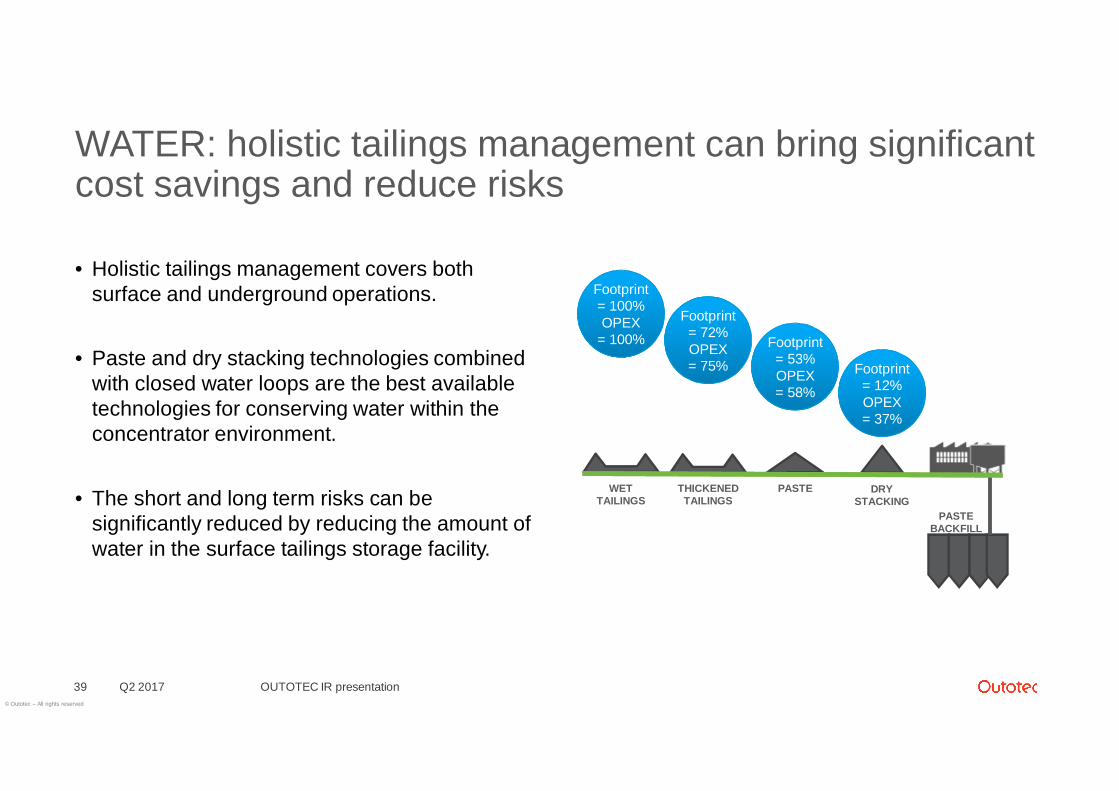

WATER: holistic tailings management can bring significantcost savings and reduce risks

• Holistic tailings management covers bothsurface and underground operations.

• Paste and dry stacking technologies combinedwith closed water loops are the best availabletechnologies for conserving water within theconcentrator environment.

• The short and long term risks can besignificantly reduced by reducing the amount ofwater in the surface tailings storage facility.

Q2 2017 OUTOTEC IR presentation39

PASTEBACKFILL

DRYSTACKING

Footprint= 12%OPEX= 37%

PASTE

Footprint= 53%OPEX= 58%

THICKENEDTAILINGS

Footprint= 72%OPEX= 75%

WETTAILINGS

Footprint= 100%OPEX

= 100%

© Outotec – All rights reserved

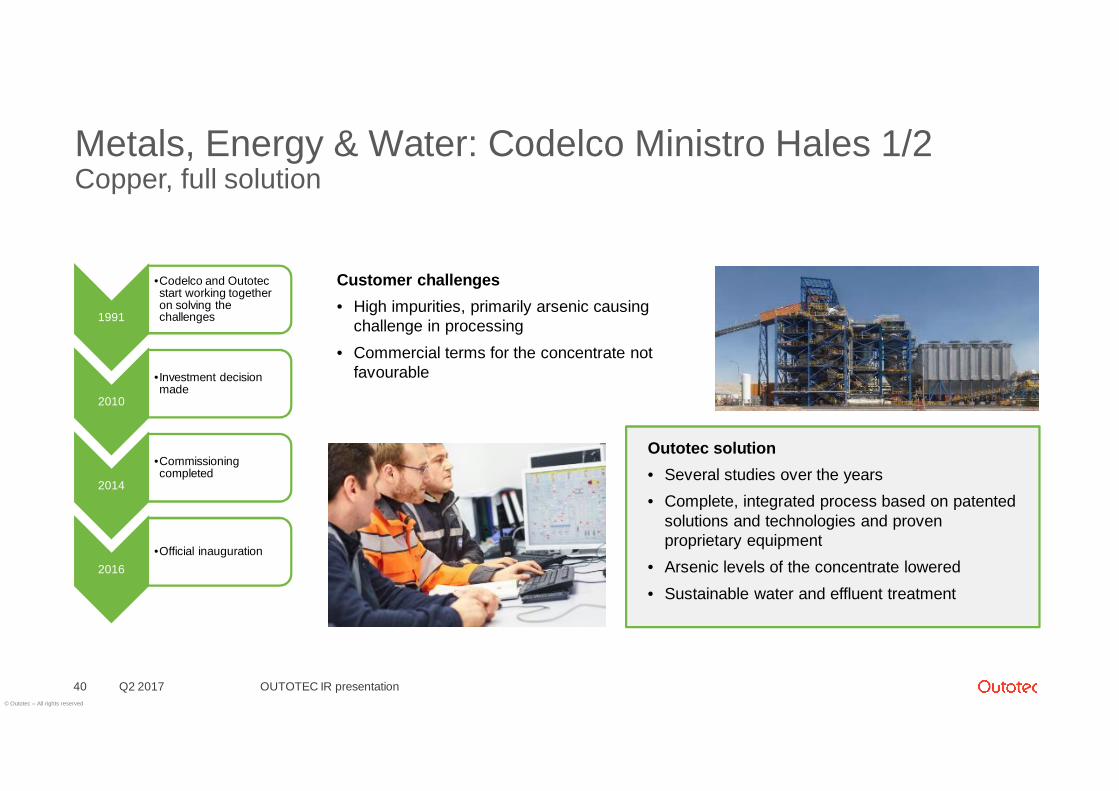

Metals, Energy & Water: Codelco Ministro Hales 1/2Copper, full solution

Q2 201740

Customer challenges• High impurities, primarily arsenic causing

challenge in processing• Commercial terms for the concentrate not

favourable

OUTOTEC IR presentation

Outotec solution• Several studies over the years• Complete, integrated process based on patented

solutions and technologies and provenproprietary equipment

• Arsenic levels of the concentrate lowered• Sustainable water and effluent treatment

1991

•Codelco and Outotecstart working togetheron solving thechallenges

2010

•Investment decisionmade

2014

•Commissioningcompleted

2016•Official inauguration

© Outotec – All rights reserved

Codelco Ministro Hales 2/2Copper, full solution

Q2 2017 OUTOTEC IR presentation41

Partial roasting• Patented solution which removes over

90% of the arsenic in the oreconcentrate

• Exceeding 605,000 tpa concentrate(110%)

Gas Cleaning• Gas cleaning and sulfuric acid

production technology eliminates over99.9% of the gaseous emission of thefacility

Effluent Treatment• Process effluents are cleaned and recirculated back to the process

© Outotec – All rights reserved

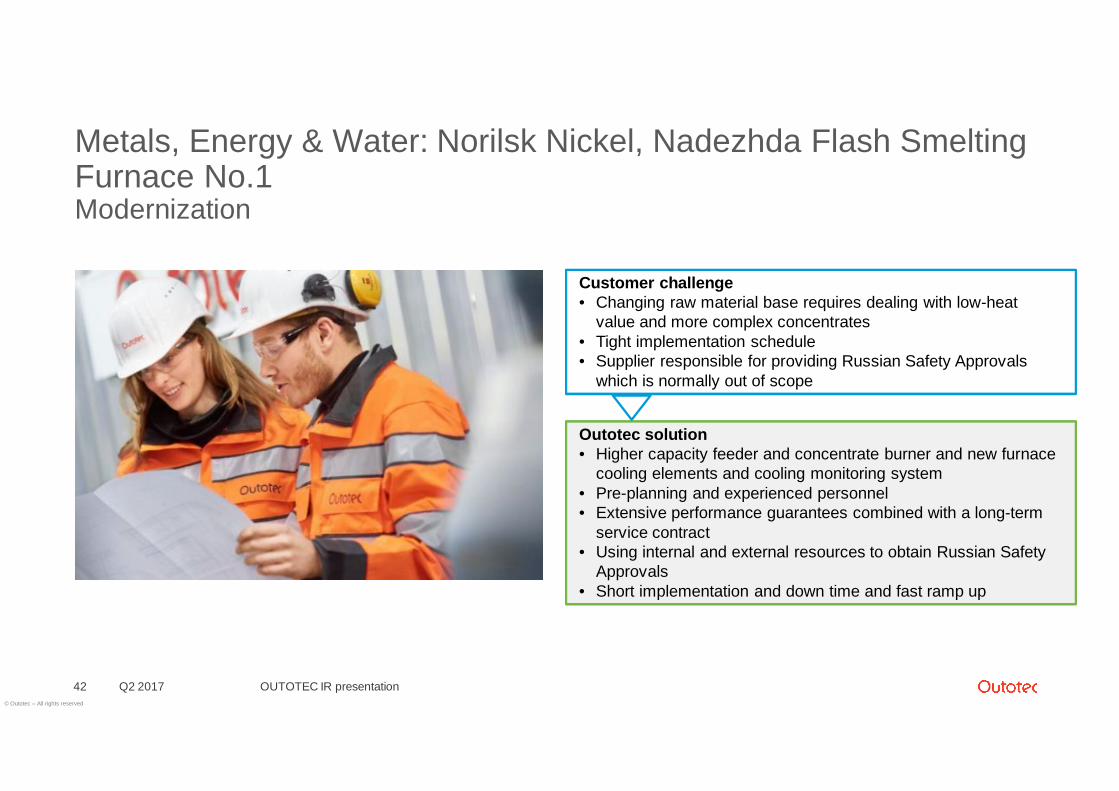

Metals, Energy & Water: Norilsk Nickel, Nadezhda Flash SmeltingFurnace No.1Modernization

Q2 201742 OUTOTEC IR presentation

Customer challenge• Changing raw material base requires dealing with low-heat

value and more complex concentrates• Tight implementation schedule• Supplier responsible for providing Russian Safety Approvals

which is normally out of scope

Outotec solution• Higher capacity feeder and concentrate burner and new furnace

cooling elements and cooling monitoring system• Pre-planning and experienced personnel• Extensive performance guarantees combined with a long-term

service contract• Using internal and external resources to obtain Russian Safety

Approvals• Short implementation and down time and fast ramp up

© Outotec – All rights reserved

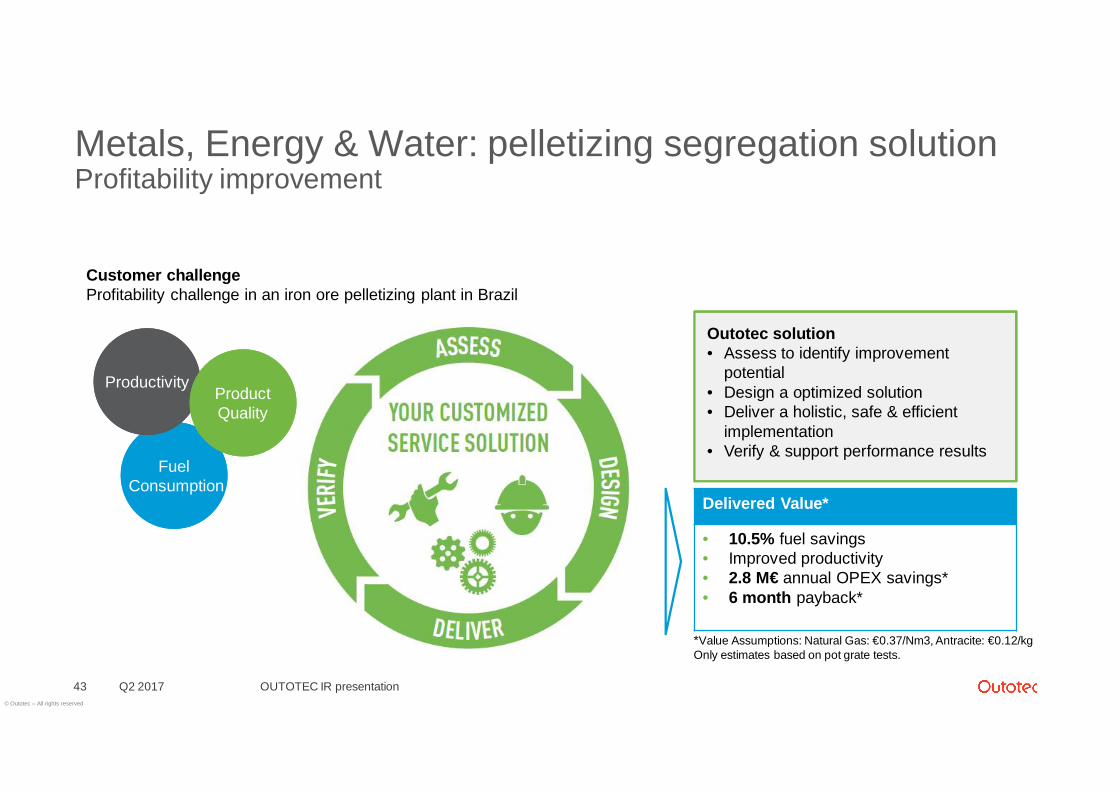

Metals, Energy & Water: pelletizing segregation solutionProfitability improvement

OUTOTEC IR presentationQ2 201743

Customer challengeProfitability challenge in an iron ore pelletizing plant in Brazil

FuelConsumption

FuelConsumption

ProductivityProductivityProductQualityProductQuality

Outotec solution• Assess to identify improvement

potential• Design a optimized solution• Deliver a holistic, safe & efficient

implementation• Verify & support performance results

Delivered Value*

• 10.5% fuel savings• Improved productivity• 2.8 M€ annual OPEX savings*• 6 month payback*

*Value Assumptions: Natural Gas: €0.37/Nm3, Antracite: €0.12/kgOnly estimates based on pot grate tests.

© Outotec – All rights reserved

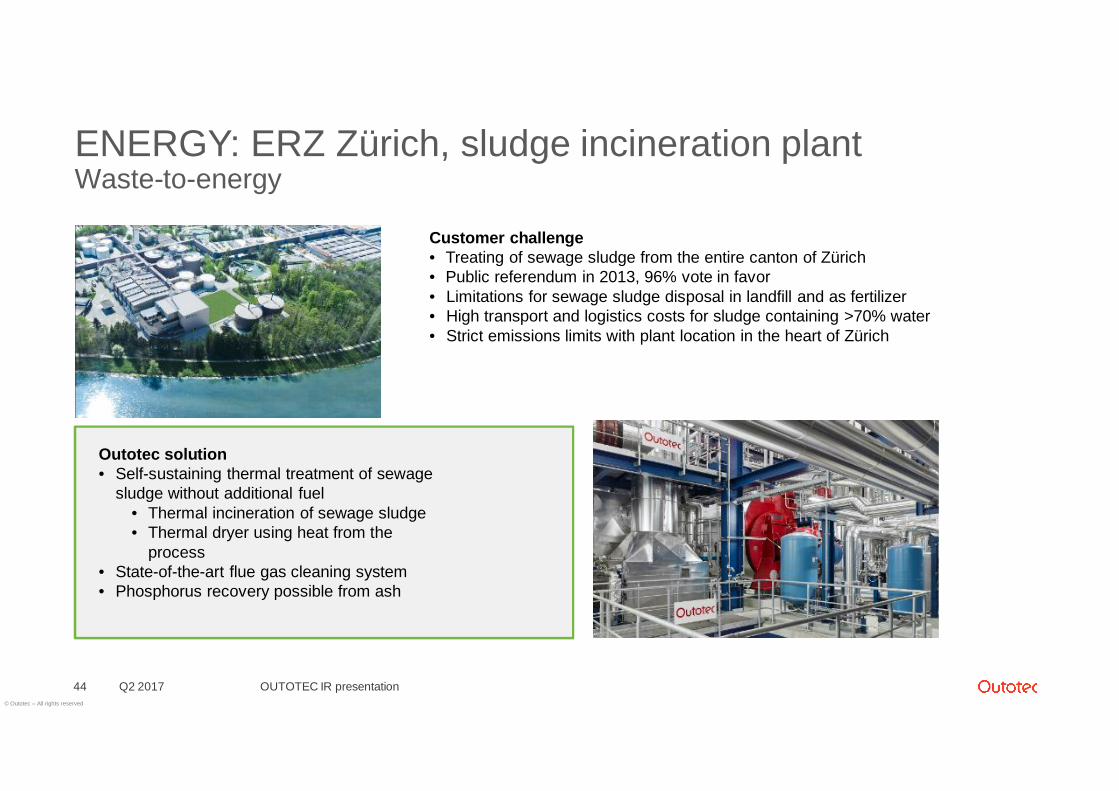

ENERGY: ERZ Zürich, sludge incineration plantWaste-to-energy

Q2 201744

Customer challenge• Treating of sewage sludge from the entire canton of Zürich• Public referendum in 2013, 96% vote in favor• Limitations for sewage sludge disposal in landfill and as fertilizer• High transport and logistics costs for sludge containing >70% water• Strict emissions limits with plant location in the heart of Zürich

OUTOTEC IR presentation

Outotec solution• Self-sustaining thermal treatment of sewage

sludge without additional fuel• Thermal incineration of sewage sludge• Thermal dryer using heat from the

process• State-of-the-art flue gas cleaning system• Phosphorus recovery possible from ash

© Outotec – All rights reserved

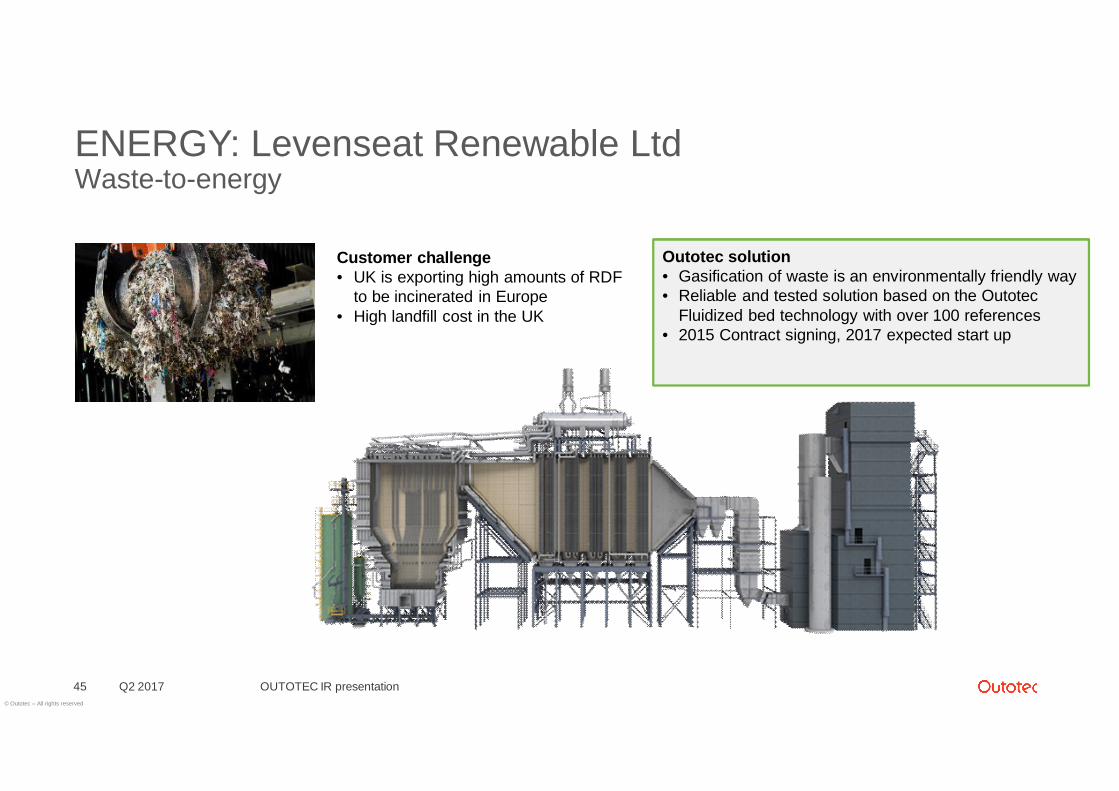

ENERGY: Levenseat Renewable LtdWaste-to-energy

Q2 201745

Customer challenge• UK is exporting high amounts of RDF

to be incinerated in Europe• High landfill cost in the UK

OUTOTEC IR presentation

Outotec solution• Gasification of waste is an environmentally friendly way• Reliable and tested solution based on the Outotec

Fluidized bed technology with over 100 references• 2015 Contract signing, 2017 expected start up

© Outotec – All rights reserved

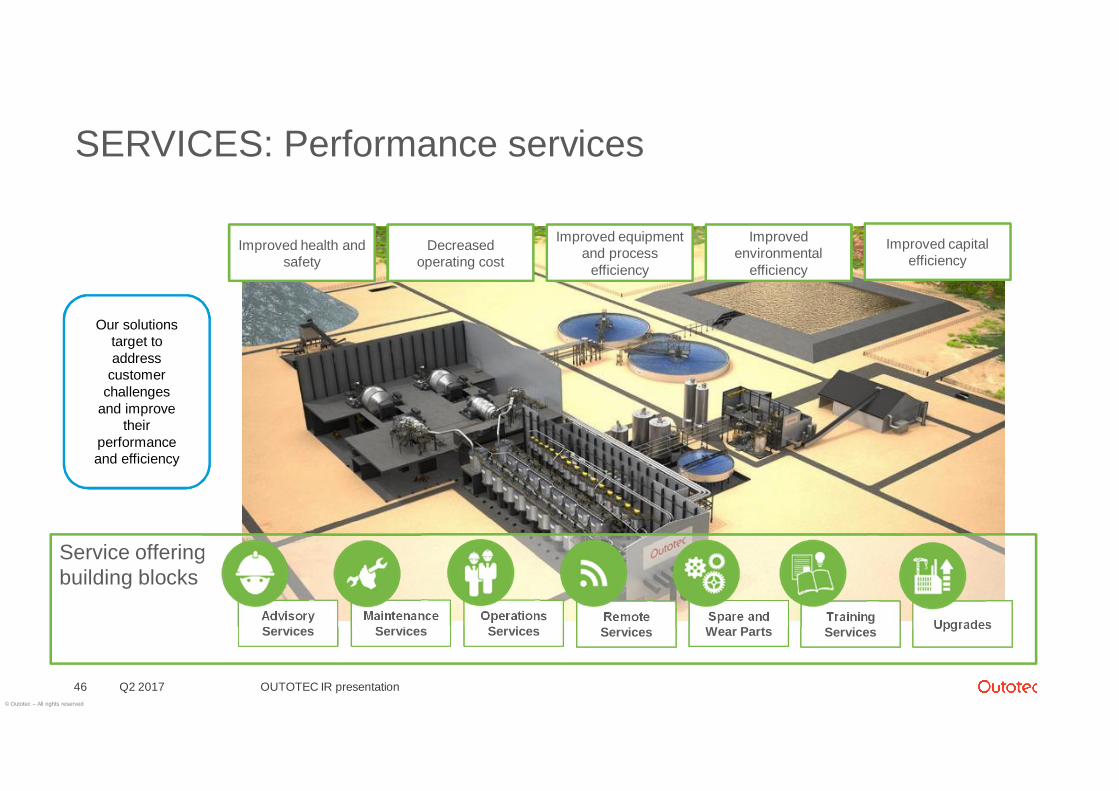

Service offeringbuilding blocks

SERVICES: Performance services

Q2 2017 OUTOTEC IR presentation46

OperationsServices

AdvisoryServices

MaintenanceServices

RemoteServices

TrainingServices

Spare andWear Parts Upgrades

Decreasedoperating cost

Improved health andsafety

Improvedenvironmental

efficiency

Improved capitalefficiency

Improved equipmentand process

efficiency

Our solutionstarget toaddress

customerchallenges

and improvetheir

performanceand efficiency

© Outotec – All rights reserved

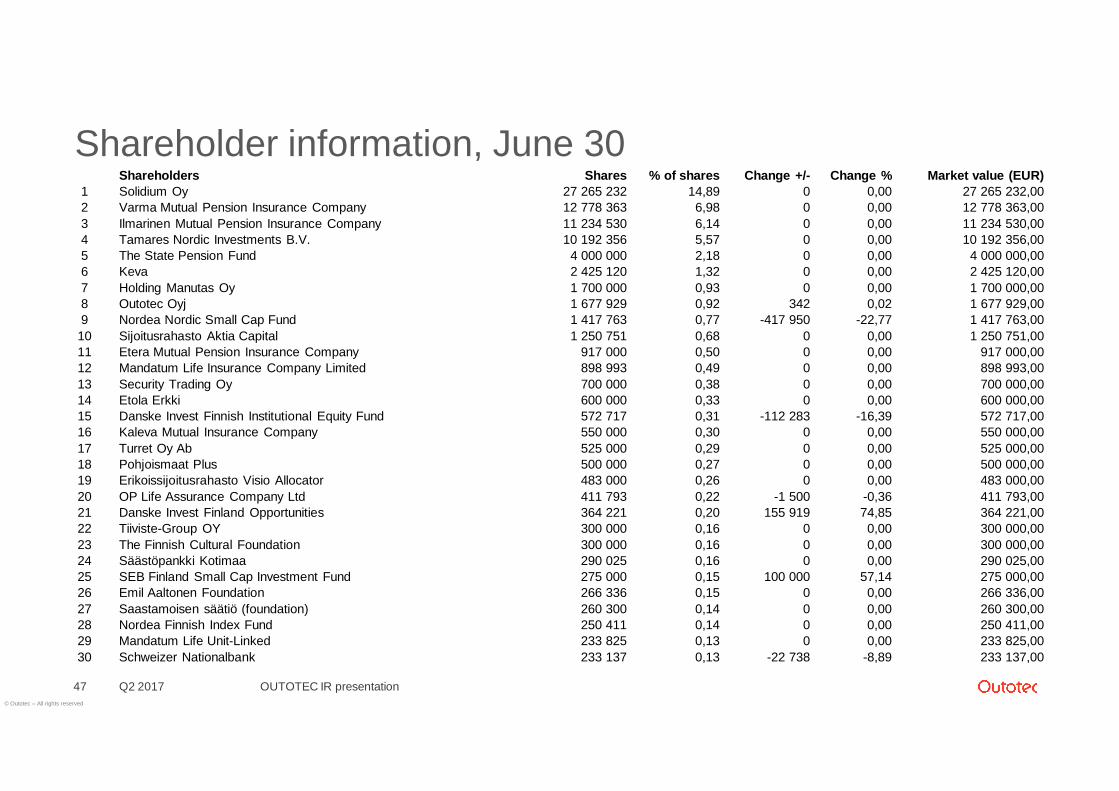

Shareholder information, June 30

Q2 2017 OUTOTEC IR presentation47

Shareholders Shares % of shares Change +/- Change % Market value (EUR)1 Solidium Oy 27 265 232 14,89 0 0,00 27 265 232,002 Varma Mutual Pension Insurance Company 12 778 363 6,98 0 0,00 12 778 363,003 Ilmarinen Mutual Pension Insurance Company 11 234 530 6,14 0 0,00 11 234 530,004 Tamares Nordic Investments B.V. 10 192 356 5,57 0 0,00 10 192 356,005 The State Pension Fund 4 000 000 2,18 0 0,00 4 000 000,006 Keva 2 425 120 1,32 0 0,00 2 425 120,007 Holding Manutas Oy 1 700 000 0,93 0 0,00 1 700 000,008 Outotec Oyj 1 677 929 0,92 342 0,02 1 677 929,009 Nordea Nordic Small Cap Fund 1 417 763 0,77 -417 950 -22,77 1 417 763,0010 Sijoitusrahasto Aktia Capital 1 250 751 0,68 0 0,00 1 250 751,0011 Etera Mutual Pension Insurance Company 917 000 0,50 0 0,00 917 000,0012 Mandatum Life Insurance Company Limited 898 993 0,49 0 0,00 898 993,0013 Security Trading Oy 700 000 0,38 0 0,00 700 000,0014 Etola Erkki 600 000 0,33 0 0,00 600 000,0015 Danske Invest Finnish Institutional Equity Fund 572 717 0,31 -112 283 -16,39 572 717,0016 Kaleva Mutual Insurance Company 550 000 0,30 0 0,00 550 000,0017 Turret Oy Ab 525 000 0,29 0 0,00 525 000,0018 Pohjoismaat Plus 500 000 0,27 0 0,00 500 000,0019 Erikoissijoitusrahasto Visio Allocator 483 000 0,26 0 0,00 483 000,0020 OP Life Assurance Company Ltd 411 793 0,22 -1 500 -0,36 411 793,0021 Danske Invest Finland Opportunities 364 221 0,20 155 919 74,85 364 221,0022 Tiiviste-Group OY 300 000 0,16 0 0,00 300 000,0023 The Finnish Cultural Foundation 300 000 0,16 0 0,00 300 000,0024 Säästöpankki Kotimaa 290 025 0,16 0 0,00 290 025,0025 SEB Finland Small Cap Investment Fund 275 000 0,15 100 000 57,14 275 000,0026 Emil Aaltonen Foundation 266 336 0,15 0 0,00 266 336,0027 Saastamoisen säätiö (foundation) 260 300 0,14 0 0,00 260 300,0028 Nordea Finnish Index Fund 250 411 0,14 0 0,00 250 411,0029 Mandatum Life Unit-Linked 233 825 0,13 0 0,00 233 825,0030 Schweizer Nationalbank 233 137 0,13 -22 738 -8,89 233 137,00

© Outotec – All rights reserved

0

5

10

15

20

25

30

35

40

45

50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

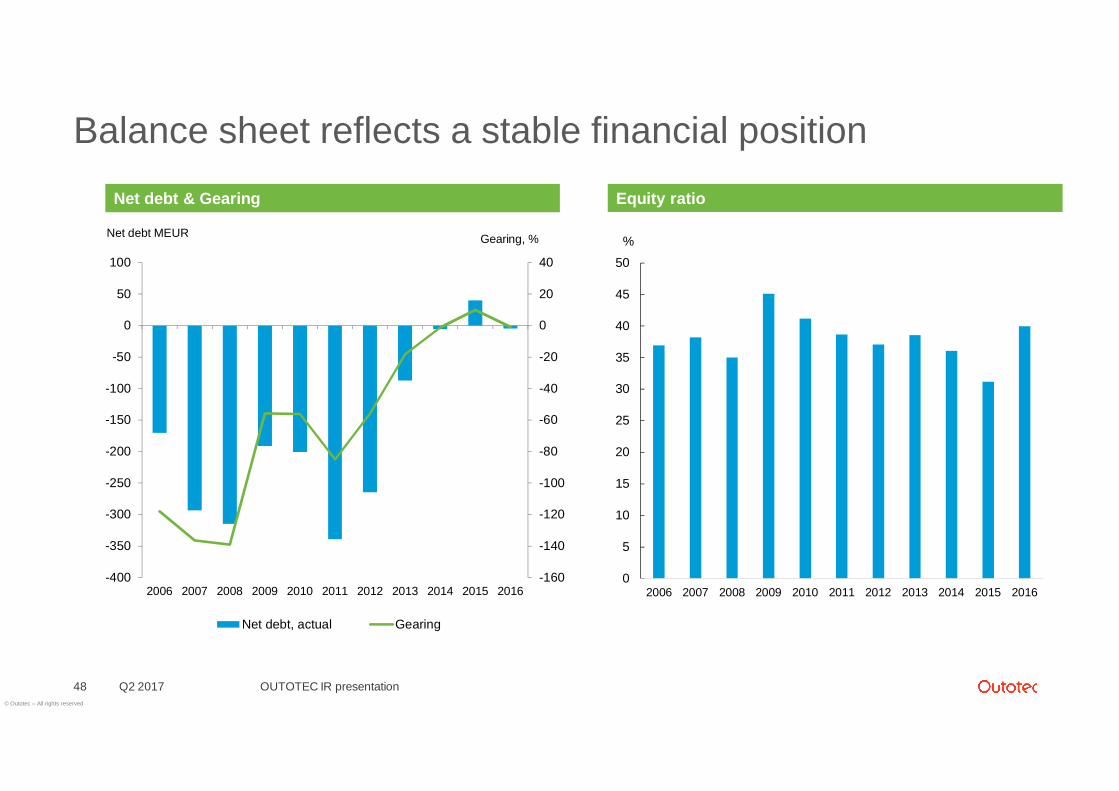

Balance sheet reflects a stable financial position

Q2 2017 OUTOTEC IR presentation48

-160

-140

-120

-100

-80

-60

-40

-20

0

20

40

-400

-350

-300

-250

-200

-150

-100

-50

0

50

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gearing, %Net debt MEUR

Net debt, actual Gearing

Net debt & Gearing Equity ratio

%

![WOODGROVE SECONDARY SCHOOL COACH! …...(Caa 27 June 2019) WOODGROVE SECONDARY SCHOOL COACH! (COme to AChieve new Heights!) PROGRAMME 2019 [for 4 Express / 5 Normal (Academic)] When?](https://img.pdfslide.us/doc/110x75/5e53254c6a5c3008ce4dcd65/woodgrove-secondary-school-coach-caa-27-june-2019-woodgrove-secondary-school.jpg)