Embed Size (px)

Citation preview

Supplier Information SeminarsJanuary 2006

“Maximising Returns from Milk”

i. Introduction

ii. Overview

iii. Preview 2006

iv. Irish dairy opportunity

I. INTRODUCTION

• International Consumer Foods, Dairy Food Ingredients and Nutritionals Group

• Operations in Ireland, UK, Germany, USA and Nigeria; c. 4,000 employees

• 2004 Group turnover €1.8 billion; operating profit €84.8 million

• Free float 45%; 55% co-op ownership

• Market capitalisation c. €730 million

Vision

“To be the most relevant player in international cheese, nutritional and dairy ingredients and selected consumer foods

markets”

through a focus on international scale and growth markets

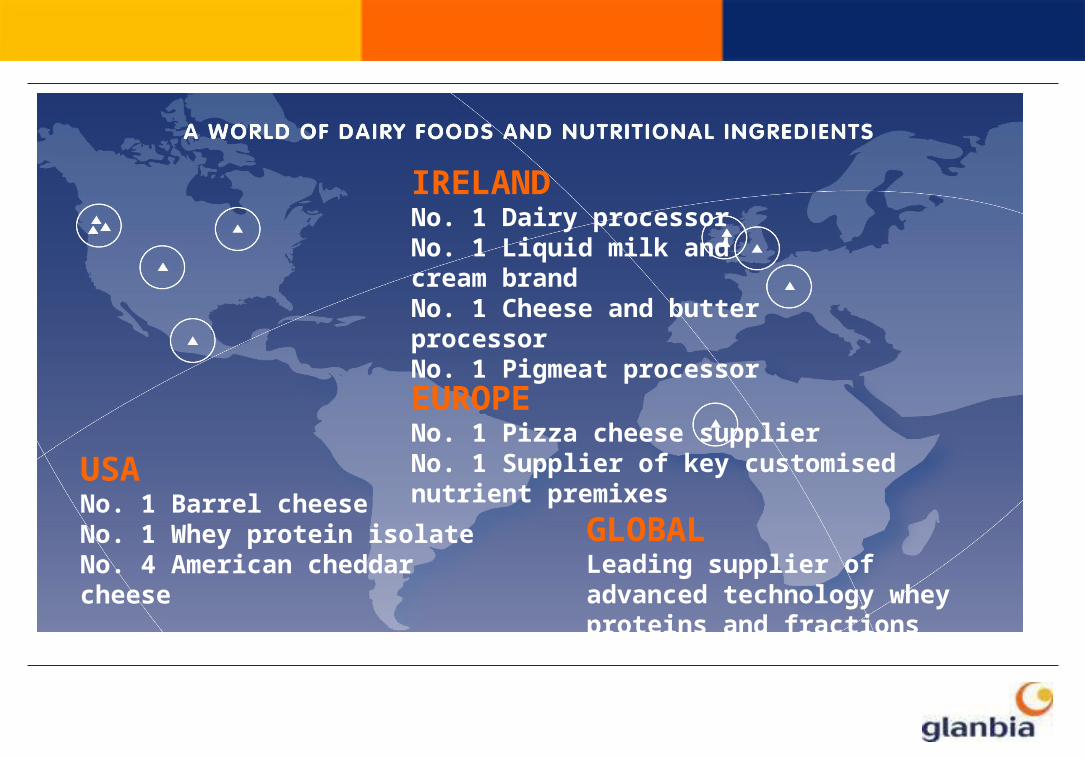

USANo. 1 Barrel cheeseNo. 1 Whey protein isolateNo. 4 American cheddar cheese

IRELANDNo. 1 Dairy processorNo. 1 Liquid milk and cream brandNo. 1 Cheese and butter processorNo. 1 Pigmeat processor

EUROPENo. 1 Pizza cheese supplierNo. 1 Supplier of key customised nutrient premixes

GLOBALLeading supplier of advanced technology whey proteins and fractions

II. OVERVIEW

Agribusiness• Challenging environment

• Turnover and margins impacted by MTR

• Pigmeat - improved performance. Recovery slower than anticipated

• Liquid Liquid Milk and Chilled Foods – tough environment in Chilled Foods and competitive market place for Liquid Milk

Consumer Foods

Food Ingredients• Food Ingredients Ireland- margin pressure; ongoing structural change in dairy markets

• Food Ingredients USA – good, strong market, increased output. Progress made on operational scale and efficiencies (incl. SWC)

III. LOOKING FORWARD 2006

Market Challenges

• Trade issues

– More certainty in EU policy, post MTR

– EU budget tight – product supports declining

– Direct income payments V fall in product revenues

– WTO trade liberalisation = uncertainty

• Deregulation - transition to more open world economy

• Changing retail customer base, discounter business model

Market Opportunities

• Globalisation of the food industry

– scale, efficiency, innovation, market positions

– networks and partnerships

• Developed Markets continue to dominate dairy consumption

• Growth opportunities in developing countries (incl. oil producers)

• New groups of consumers, driven by demographics

• Requirement for products with added health benefits

1. Agribusiness

Strategic Initiatives

- Ongoing efficiency improvements

- Competitive products focused on farmer needs

- Ongoing coarse ration and grain store investments

- Reshape retail offer at branch level with targeted investment - CountyLife

- Investment in customer information systems

- Strengthen loyalty bonuses to farmers

Feed milling / marketing

Fertilizers

Grain trading

Farm inputs

Principal activities

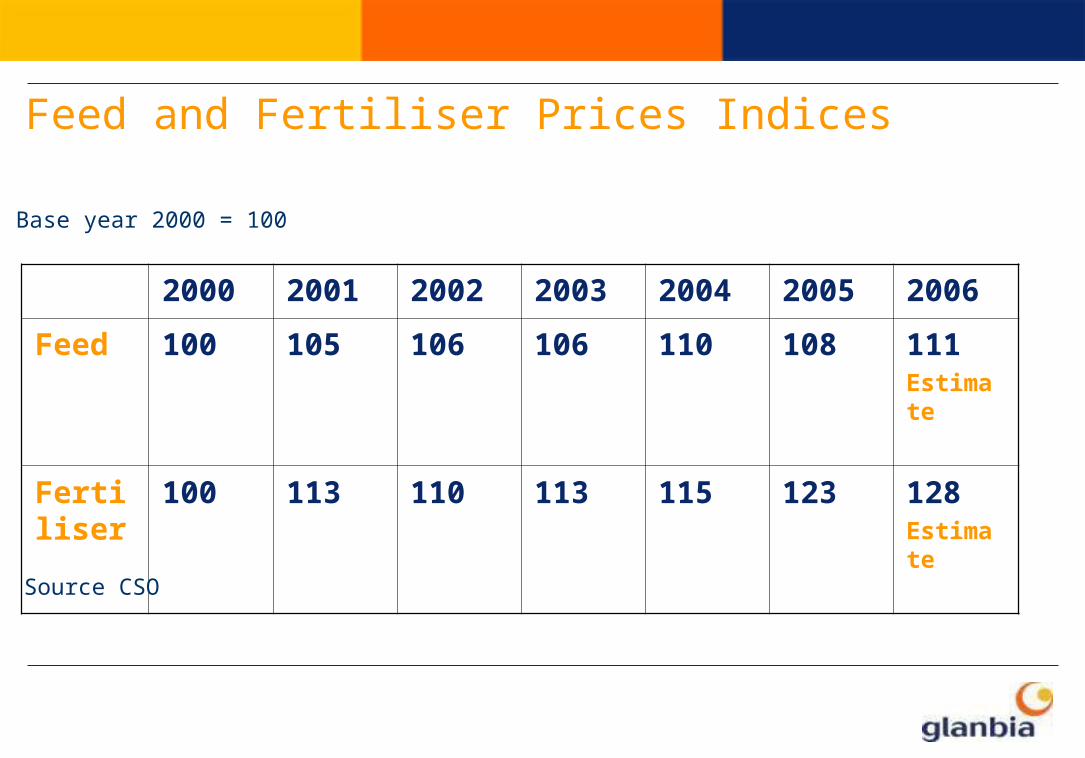

2000 2001 2002 2003 2004 2005 2006

Feed 100 105 106 106 110 108 111Estimate

Fertiliser

100 113 110 113 115 123 128Estimate

Feed and Fertiliser Prices Indices

Base year 2000 = 100

Source CSO

2. Consumer Foods

Strategic Initiatives

- Significant pipeline of new products

- Brand repositioning through

- increased marketing spend

- tighter focus

- National distribution on beverages

- Own label strategy

- Rigorous focus on cost and efficiencies

Principal activities

Liquid milk, chilled foods with leading householder brands

Pig processing for local and international markets

Mozzarella pizza cheese for European markets

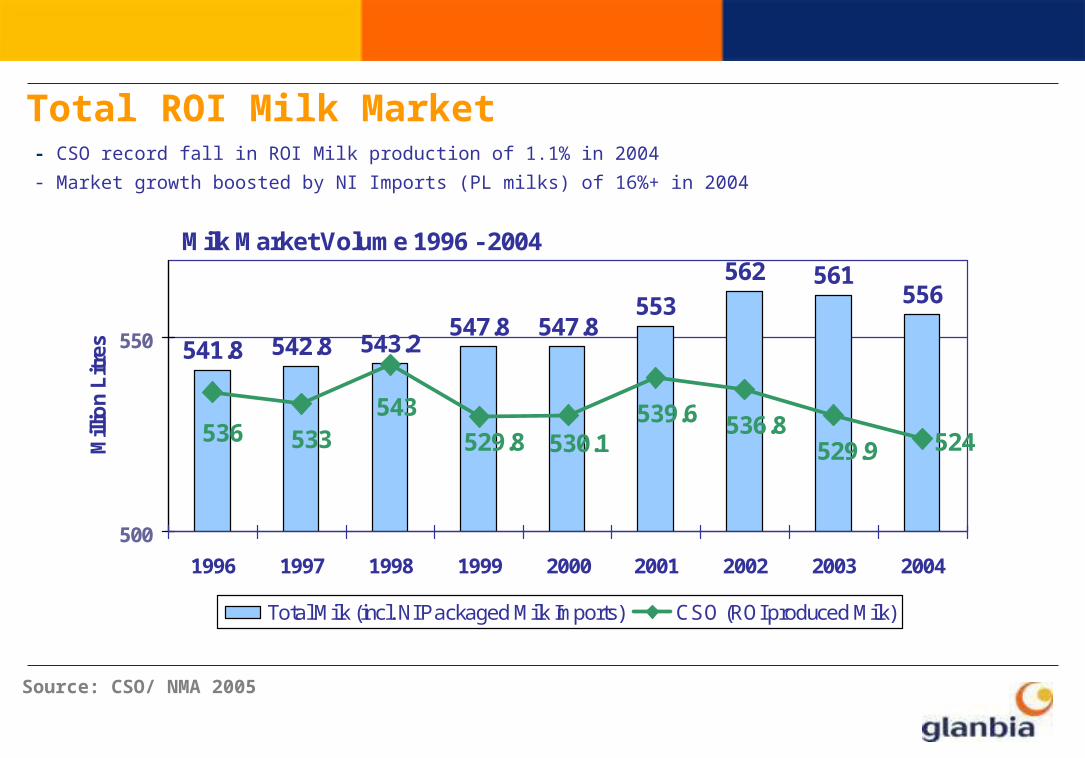

Milk Market Volume 1996 - 2004

541.8 542.8 543.2547.8 547.8

553

562 561556

524536 533543

529.8 530.1539.6 536.8

529.9

500

550

1996 1997 1998 1999 2000 2001 2002 2003 2004

Mill

ion

Litr

es

Total Milk (incl. NI Packaged Milk Imports) CSO (ROI produced Milk)

Total ROI Milk Market

Source: CSO/ NMA 2005

- CSO record fall in ROI Milk production of 1.1% in 2004

- Market growth boosted by NI Imports (PL milks) of 16%+ in 2004

Strategic Challenges for Fresh Milk

• Own Label sales are growing at 13% per annum

• Multiples and Symbols increased volume by 13% (1999 – 2004)

• 90% of all Own Label milk sold outside of Tesco is sourced in NI

• Households penetration at 74% for Own Label

• Food service continues to grow

• Uncertainty fuelled by abolition of Groceries Order

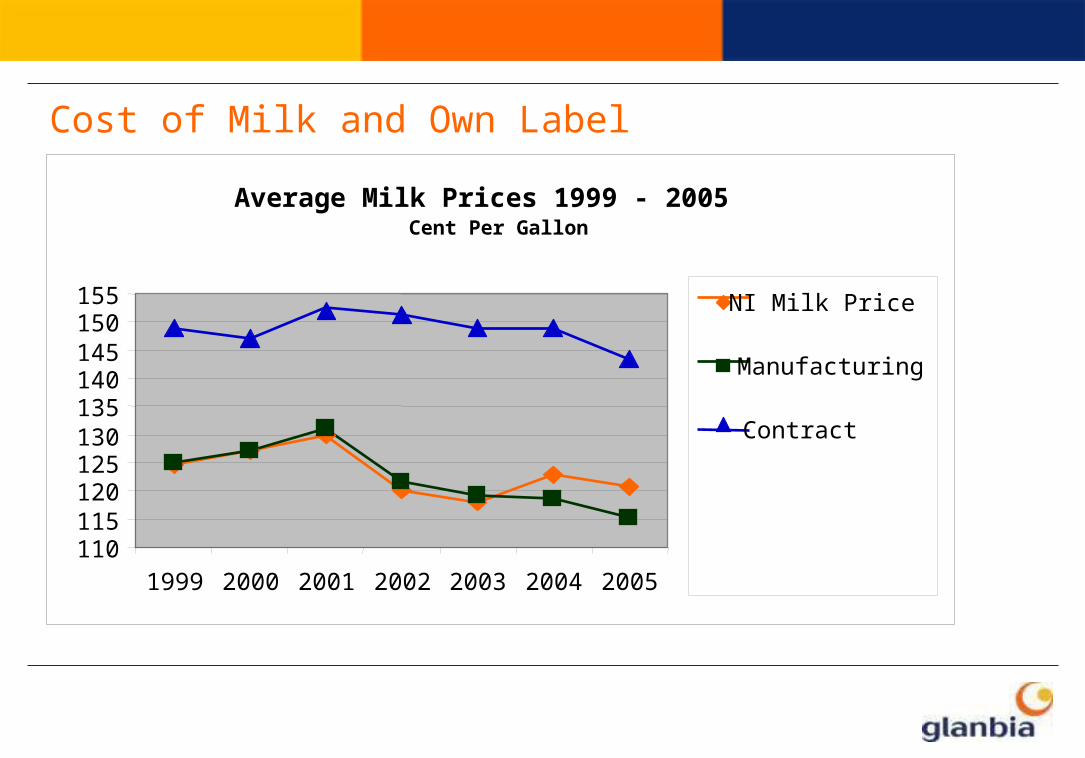

Cost of Milk and Own Label

Average Milk Prices 1999 - 2005Cent Per Gallon

110115120125130135140145150155

1999 2000 2001 2002 2003 2004 2005

NI Milk Price

Manufacturing

Contract

3. Food Ingredients

Major cheese supplier from four plants in “Magic Valley”, Idaho

Leading dairy-based ingredients supplier

Europe’s largest integrated dairy processing facility

Principal activities

Formulation of whey proteins for Nutritionals

• Ongoing progress on operational scale/ efficiency to respond to shifting markets (cost reductions)

• Contract Manufacturing (Dairygold and Connacht Gold)

• Implementation of cheddar rationalisation

• Further expansion in US cheese

• Nutritionals growth

Strategic Initiatives

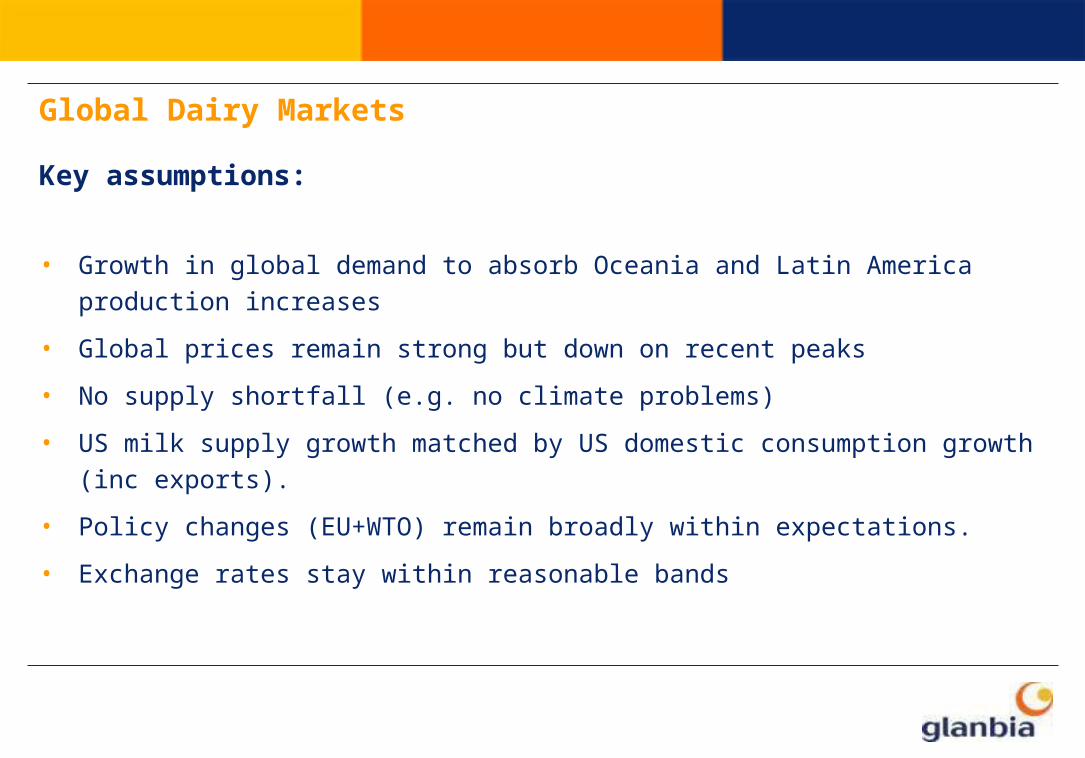

Global Dairy Markets

Key assumptions:

• Growth in global demand to absorb Oceania and Latin America production increases

• Global prices remain strong but down on recent peaks

• No supply shortfall (e.g. no climate problems)

• US milk supply growth matched by US domestic consumption growth (inc exports).

• Policy changes (EU+WTO) remain broadly within expectations.

• Exchange rates stay within reasonable bands

EU + Global Dairy Markets Short-term Prospects(Jan – June 2006)

Casein• Prices to stabilise at slightly above SMP equivalent (€5,200/t, $3.0/lb)• Scale + whey valorisation critical for success• Demand declining by 25% • Exit of small scale manufacturers

Whey Derivatives• Prices to remain firm at, whey powder equivalent €700/t • Price aligning with SMP

SMP• Prices to remain firm at €1,950 (feed) €2,020 (food)• Supply tight - Demand OK

Butter• Prices expected to weaken to €2,450/t

• Supply still exceeding demand

• Intervention cut to 50,000 tonnes - PSA conditions still unknown

Cheese • Prices expected to weaken from current high

• Limited milk supply preventing significant stock increases

• Demand growth matched by supply

EU + Global Dairy Markets Short-term Prospects(Jan – June 2006)

Butterfat Mid Term Prospects

• Butterfat will be the main EU and global problem product

• EU and world prices will not have aligned by 2008

• EU butter production is sustained due to continued proliferation of low- fat products

• Intervention is effectively eliminated with CAP at 30,000t

• EU Prices may fall well below 2008 intervention price of €2,215

• World prices will increase by 5-10% to falling EU export subsidy

• Will continue to need support

Market access - USA

• Key dairy export market for Ireland

• Population 321 million by 2015

• Record dairy demand / cheese production

• Consolidation of dairy production and processing in the West

• Glanbia No 1 U.S. producer of American-style cheese with Southwest Cheese

• No 2 U.S. producer of WPC and WPI global marketer

Southwest Cheese, Clovis New Mexico

Market access - Nigeria

• Population 140 million

• New €20m Nigerian milk powder facility with PZ Cussons plc

• Supplying evaporated milk and milk powder (from Virginia) to local market

• Nunu powder suitable for use as milk replacer, coffee and

tea whitener

• Further Opportunities

Enhanced Global Market Access

Europe

• Kortus Food Ingredients -Germany (no 1 supplier of customised nutrient premixes in Europe)

Mexico

• Marketing JV with Conaprole of Uruguay, selling dairy ingredients into central and South America (three sales offices)

• Dairy blending and processed cheese manufacturing Zylamact de Mexico (ZDM)

• Manufacturing facility in Toluca, 60 km from Mexico city

China• Sales HQ for nutritional products for pharmaceutical and food applications

Innovation

• Essential for differentiation and to move

up the value chain

• Innovation balances volatility in

commodity markets

• To compete effectively with large world

dairy commodity producers

Innovation• Glanbia operates two innovation centres (Ireland and US)

• The Group Innovation Centre in Kilkenny was a first for the Irish food industry when announced in April 2004. €15m investment

• Currently employing 52 development professionals and research scientists in Kilkenny

• Focus: – nutritional solutions – functional ingredients – hand-held consumer snacks and beverages

Recent ingredient innovations

• Defined cook-time rennet casein for US cheese

• Heat stable formulated FFMP

• Hi Gel WPC for Yoplait

• Recombined cheese ingredients (Mexico)

• Avonol – skim milk solid replacer in ice cream

• Corman Miloko Ireland– Added-value route to market for butterfat products– Fractionation technology and know-how

• Dairy processing revenues falling with costs rising

• Focus on continuous improvement in operational efficiency – Cheddar cheese rationalisation– Rationalisation in Ballyragget

• Strategic alliances to maximise utilisation – Contract Manufacturing agreements (Dairygold, Connacht Gold)– Corman Miloko Ireland

Cost Management Challenges GII

Inflation Impact GII (2000 -2004)

• CPI 2000 – 2004 was 14% cumulative

• Energy 280% higher today than in 2000

• Insurance costs doubled

• Payroll inflation 30%

• Glanbia Ingredients has contained inflation at 1/3 of CPI

2022

24262830

3234

36

€ /

100 K

g

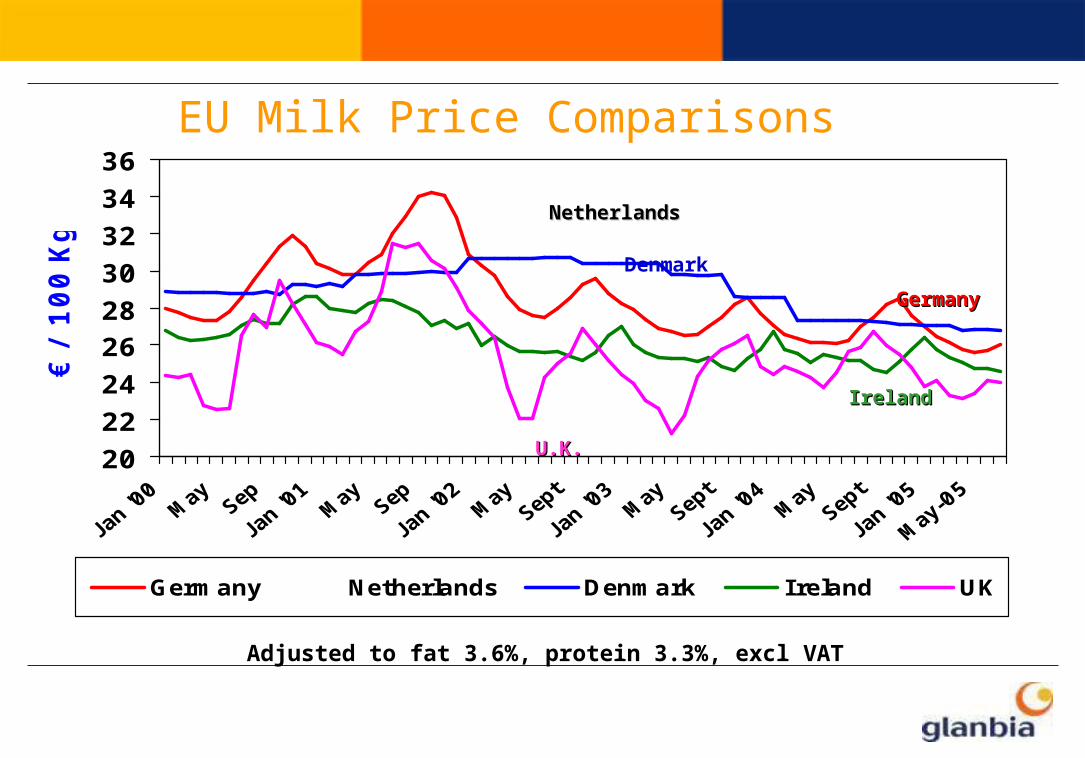

Germany Netherlands Denmark Ireland UK

EU Milk Price Comparisons

Denmark

GermanyGermany

U.K.U.K.

IrelandIreland

NetherlandsNetherlands

Adjusted to fat 3.6%, protein 3.3%, excl VAT

IDB on Account Price Relative to Current Milk Price

• Present IDB on account price for basic butter and SMP

- 126c/gallon or 99.24p/gallon

• Current manufacturing price

- 114.65c/gal or 90.29p/gal excl.VAT

• Available to processor

- 11.35 c/gal or 8.95 p/gal

Source IDB

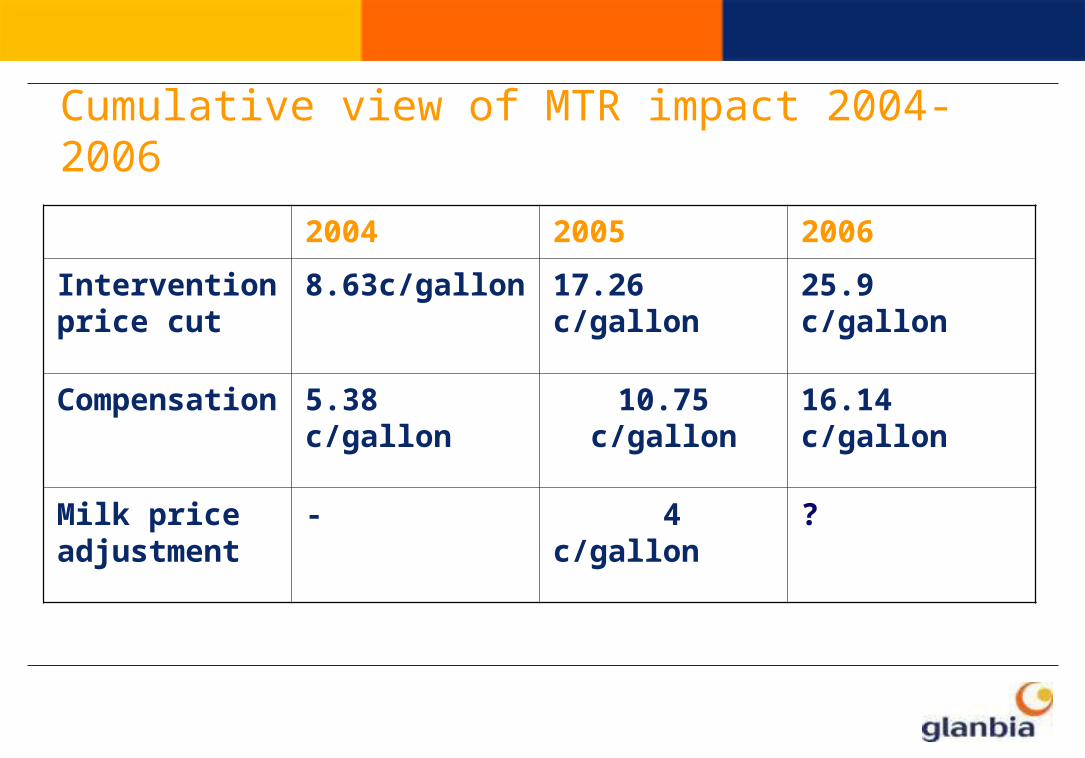

Cumulative view of MTR impact 2004-2006

2004 2005 2006

Intervention price cut

8.63c/gallon 17.26 c/gallon 25.9 c/gallon

Compensation 5.38 c/gallon 10.75 c/gallon 16.14 c/gallon

Milk price adjustment

- 4 c/gallon ?

4. Irish Dairy Opportunity

• Irish grass based system = competitive advantage

• Irish farmers among most efficient, least cost European milk producers

• Continuing demand for low cost, high volume,value added dairy products

• Strong farmer / processor partnerships

There is a future for efficient and flexible dairy farmers

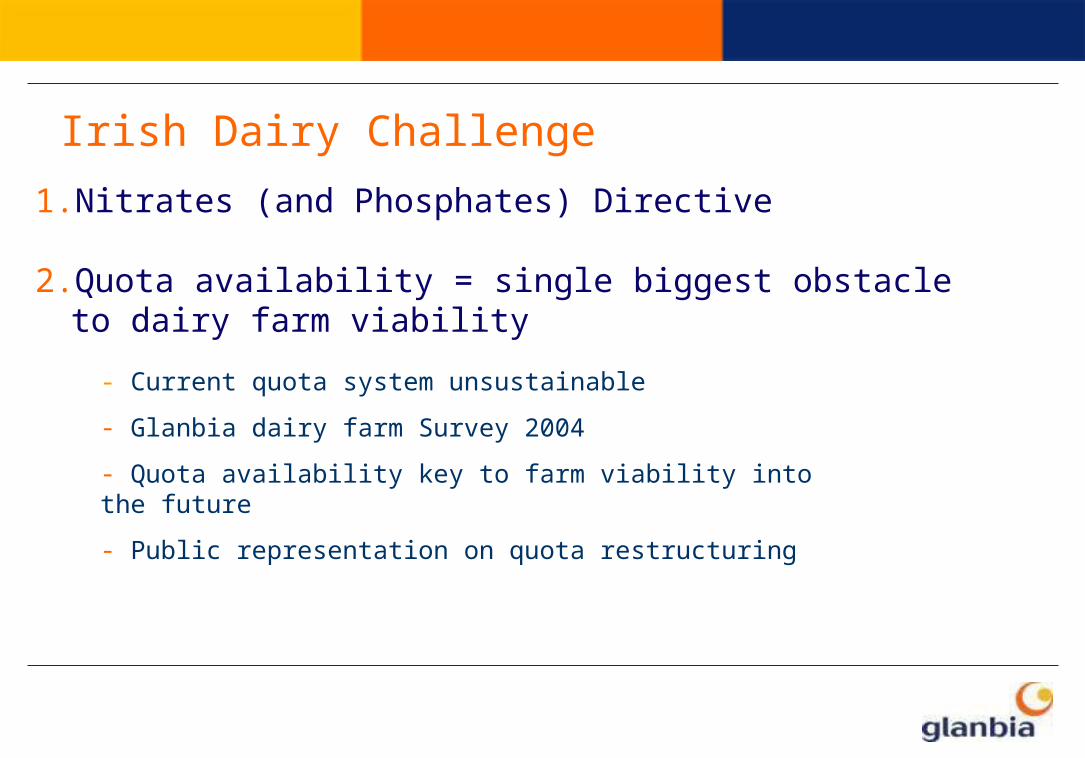

1.Nitrates (and Phosphates) Directive

2.Quota availability = single biggest obstacle to dairy farm viability

Irish Dairy Challenge

- Current quota system unsustainable

- Glanbia dairy farm Survey 2004

- Quota availability key to farm viability into the future

- Public representation on quota restructuring

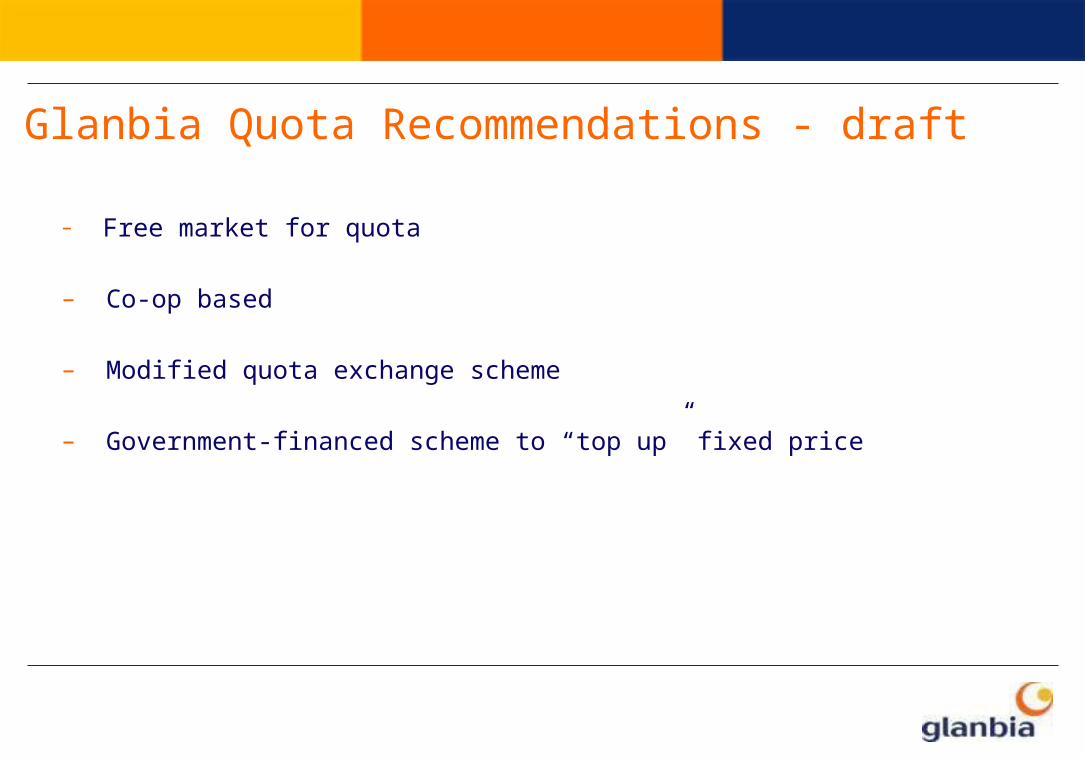

Glanbia Quota Recommendations - draft

– Free market for quota

– Co-op based

– Modified quota exchange scheme

– Government-financed scheme to “top up” fixed price

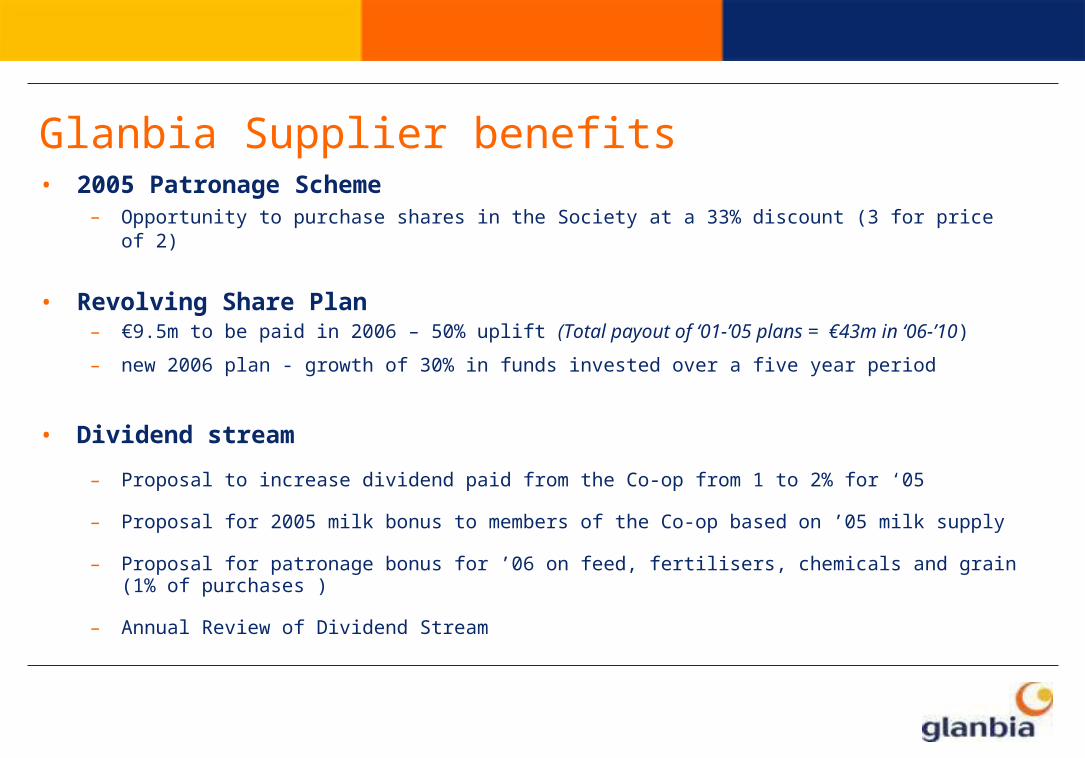

Glanbia Supplier benefits • 2005 Patronage Scheme

– Opportunity to purchase shares in the Society at a 33% discount (3 for price of 2)

• Revolving Share Plan– €9.5m to be paid in 2006 – 50% uplift (Total payout of ‘01-’05 plans = €43m in ‘06-’10)

– new 2006 plan - growth of 30% in funds invested over a five year period

• Dividend stream

– Proposal to increase dividend paid from the Co-op from 1 to 2% for ‘05

– Proposal for 2005 milk bonus to members of the Co-op based on ’05 milk supply

– Proposal for patronage bonus for ’06 on feed, fertilisers, chemicals and grain (1% of purchases )

– Annual Review of Dividend Stream

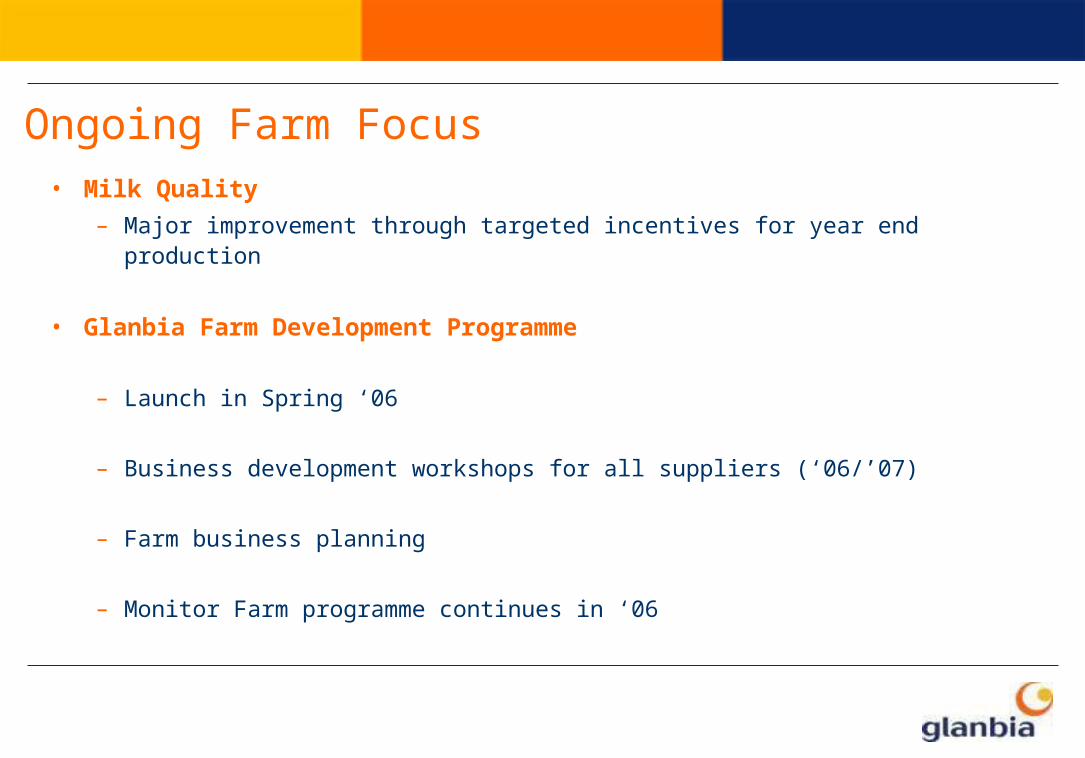

Ongoing Farm Focus • Milk Quality

– Major improvement through targeted incentives for year end production

• Glanbia Farm Development Programme

– Launch in Spring ‘06

– Business development workshops for all suppliers (‘06/’07)

– Farm business planning

– Monitor Farm programme continues in ‘06

Conclusion

“Irish dairying is in transition but has a good future”

Four ingredients for success are :

1. Scale and efficiency at farm and processing level

- Quota restructuring critical

2. Global market reach

3. Investment (innovation & marketing)

4. Realism - in transition and competing at lower prices and making step-changes in costs

Thank You