Embed Size (px)

Citation preview

WE GIVE THE STEEL TRADE A LIFT.Salzgitter Mannesmann International is always performing at its best

to ensure that we give your daily steel business a lift.

Visit us at www.salzgitter-mannesmann-international.com for information.

121130_Metal_Bulletin_Supplement_Middle_East_Steel.indd 1 30.11.2012 14:00:35

Middle East Steel 2012www.metalbulletin.com

supplements

Middle East Steel 2012

supplements

Ask international plantmakers which regional markets have kept them busiest over the past few years and – alongside the BRIC countries – many of them will point to the Middle East. Ask them now where the most promising new markets are and a number will also mention Africa.

While some projects to increase steelmaking capacity in the Middle East and North Africa have proceeded more slowly than originally envisaged– large and temporarily immobile inventories of billet and rebar plunging in value in the wake of the financial crisis several years ago forced reconsideration of their pace of progress – significant advances have been made. Projects at Emirates Steel in UAE, Sulb in Bahrain and Jindal Shadeed in Oman are examples of regional expansion.

The fundamental advantages of producing steel in the region are unchanged. An abundance of reasonably priced power for such an energy-intensive industry is one of them. A plentiful supply of natural gas as a reducing agent for making direct reduced iron (DRI) is another.

Given the well-known statistic that about half of all steel production globally is used in construction, the potential for Mena consumption to grow is also particularly attractive for steel investment in the region. The internationally recognised high-rise towers of Dubai have become emblematic of world class construction, but there are plenty of other commercial, residential and industrial buildings – as well as infrastructure projects – needing steel, for which the region’s own mills are adding capacity. Specialised steel products like heavy sections or seamless tubes are amongst them. Plans for new flat product mills are under way. Investment in steelmaking capacity upstream is reducing regional demand for imported billet.

The oil & gas industry, whose revenues drive much of the capital investment in the Gulf region, is a significant steel consumer itself of course.

Infrastructure development offers a particularly promising steel market. The Gulf Co-operation Council countries of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and UAE, for example, have plans for – or are actively engaged in – airport expansion and/or reconstruction. They also have plans for rapid-transit, light-gauge railways, several of which are already under way. In addition, a $106 billion, 2,200 km inter-state Gulf Rail project is scheduled for 2017. Kuwait alone plans 60 stations.

This Metal Bulletin Focus supplement provides: a review of market developments this year, with comment on the immediate outlook in 2013; a summary of the detailed long-term analysis of the region’s steel industry recently made by Metal Bulletin Research; a country-by-country look at steelmaking projects recently completed, under construction or planned; and a review of the latest DRI capacity of the Mena region as producer of more than a third of global DRI output and home to the latest technologies for hot charging to an EAF.

No-one really needs to be reminded of the Mena area’s recent problems – among them conflict in Syria, an uneasy ceasefire between Israel and The Gaza Strip, internal tensions in Libya and Egypt as new governments evolve after the ‘Arab Spring’, and the effects of sanctions in Iran as the West continues to keep a watchful eye on development of the country’s nuclear capabilities – but no comment on the region would be complete without mentioning them either. Clearance work, scrap handling and rebuilding are essential steps for communities looking to rebuild lives shattered by conflict.

Taken as a diverse whole, the Mena region encompasses higher than average risks and rewards. It is for each investor in the region – whether internal or external – to weigh up the opportunities against the threats.

Risks and rewards

Published by the Metals, Minerals and Mining division of Metal Bulletin Ltd.Metal Bulletin Ltd, Nestor House, Playhouse Yard, London EC4V 5EX. UK registration number: 00142215. Editorial headquarters: 5-7 Ireland Yard, London EC4V 5EX. Tel: +44 20 7827 9977. Fax: +44 20 7928 6892 and +44 20 7827 6495. E-mail: [email protected] Website: http://www.metalbulletin.comMetal Bulletin Focus: Editor, Richard Barrett; Associate Editor, Steve Karpel. Tel: +44 (0)20 7827 9977Magazine design: Paul Rackstraw Publisher: Spencer WicksManaging Director: Raju DaswaniCustomer Services Department: Tel +44 (0)20 7779 7390Advertising: Tel: +44 20 7827 5220 Fax: +44 20 7827 5206.E-mail: [email protected] Sales Director: Mary ConnorsSales Team: Julius Pike, Abdul Zaidi, Susan ZouUSA Editorial & Sales: Metal Bulletin, 225 Park Avenue South, 8th Floor, New York, NY 10003.Tel: +1 (212) 213 6202.Toll free number: 1-800-METAL-25. Editorial Fax: +1 (212) 213 6617.Sales Fax: +1 (212) 213 6273.Subscription EnquiriesSales Tel: +44 (0)20 7779 7999Sales Fax: +44 (0)20 7246 5200Sales E-mail: [email protected] Bulletin Ltd is part of Euromoney InstitutionalInvestor PLC: Nestor House, Playhouse Yard, London EC4V 5EXPrinted by The Magazine Printing Company plc, Enfield EN3 7NT, UK© Metal Bulletin Limited, 2012

CONTENTSThe long viewMetal Bulletin Research analyses long-term trends in steel production and consumption in the Middle East and North Africa 4

Markets stabilise, competition growsSteel demand in the Middle East has stabilised this year, but competition between domestic steelmakers and importers to satisfy it is fierce 9

Integration, expansion and diversification aboundSteel companies across the region are increasing capacities and widening product ranges in response to local markets and anticipated demand 14

Direct reduction is the primary choiceDirect reduced iron is widely produced and used as a feedstock for steelmaking in the region, and capacity continues to climb 21

December 2012 | Middle East Steel | 3

4 | Middle East Steel | December 2012

Middle East Steel 2012

Overview

Metal Bulletin Research has been providing a very detailed study of regional markets in the Middle East and North Africa for the last twelve years and in its latest report* examines supply, demand and consumption of steel products and also gives a forecast for the next five years.

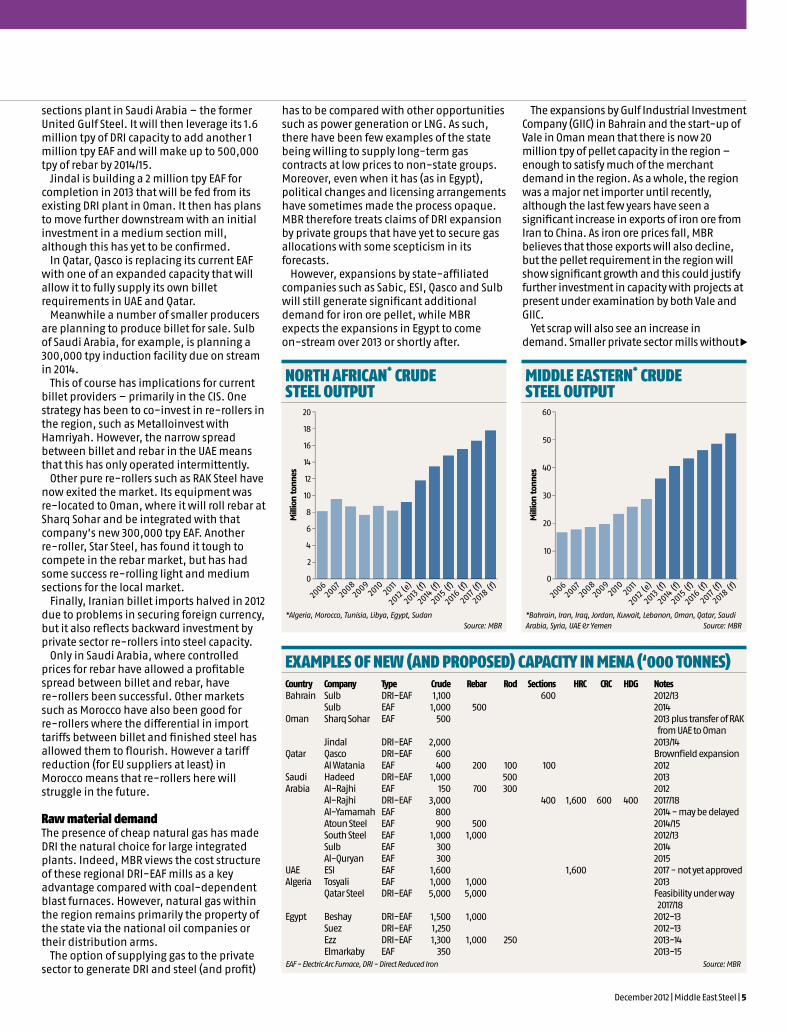

In MBR’s view, the most stunning progress will be made in steelmaking itself. It expects crude steel output to double in the Middle East to 50 million tonnes by 2018 and to almost 18 million tonnes in North Africa (see graphs).

The capacity expansion needed for this growth in production is from both greenfield and brownfield sites. Moreover, mills that have started up in 2012, such as at Maghreb Steel in Morocco, ESI in UAE, as well as a re-start of Lisco in Libya, will contribute to higher production levels in the short term. In addition, MBR expects higher output in Iran as well as the development of

a small steelmaking industry in Iraq by the end of the forecast period.

Most of the investment will be in long products and this reflects the consumption pattern in the region, of which 75% is long products. Nevertheless, one key trend is the backward integration into crude steel that

to some extent will displace the region’s key deficit, which is currently served by imported billet.

Sulb in Bahrain, for example, is building a 1 million tpy EAF plant that will supply its own new 600,000 tpy section mill as well as supply 400,000 tpy of billet to its acquired

The long viewDespite the immediate conflicts and political unrest in parts of the Middle East and North Africa, there is a different story to tell about the region’s steel industry, which is burgeoning. Metal Bulletin Research analyses the long-term outlook

Metal Bulletin Research expects crude steel output in the Middle East to reach 50 million tpy by 2018

DAN

IELI

December 2012 | Middle East Steel | 5

sections plant in Saudi Arabia – the former United Gulf Steel. It will then leverage its 1.6 million tpy of DRI capacity to add another 1 million tpy EAF and will make up to 500,000 tpy of rebar by 2014/15.

Jindal is building a 2 million tpy EAF for completion in 2013 that will be fed from its existing DRI plant in Oman. It then has plans to move further downstream with an initial investment in a medium section mill, although this has yet to be confirmed.

In Qatar, Qasco is replacing its current EAF with one of an expanded capacity that will allow it to fully supply its own billet requirements in UAE and Qatar.

Meanwhile a number of smaller producers are planning to produce billet for sale. Sulb of Saudi Arabia, for example, is planning a 300,000 tpy induction facility due on stream in 2014.

This of course has implications for current billet providers – primarily in the CIS. One strategy has been to co-invest in re-rollers in the region, such as Metalloinvest with Hamriyah. However, the narrow spread between billet and rebar in the UAE means that this has only operated intermittently.

Other pure re-rollers such as RAK Steel have now exited the market. Its equipment was re-located to Oman, where it will roll rebar at Sharq Sohar and be integrated with that company’s new 300,000 tpy EAF. Another re-roller, Star Steel, has found it tough to compete in the rebar market, but has had some success re-rolling light and medium sections for the local market.

Finally, Iranian billet imports halved in 2012 due to problems in securing foreign currency, but it also reflects backward investment by private sector re-rollers into steel capacity.

Only in Saudi Arabia, where controlled prices for rebar have allowed a profitable spread between billet and rebar, have re-rollers been successful. Other markets such as Morocco have also been good for re-rollers where the differential in import tariffs between billet and finished steel has allowed them to flourish. However a tariff reduction (for EU suppliers at least) in Morocco means that re-rollers here will struggle in the future.

Raw material demandThe presence of cheap natural gas has made DRI the natural choice for large integrated plants. Indeed, MBR views the cost structure of these regional DRI-EAF mills as a key advantage compared with coal-dependent blast furnaces. However, natural gas within the region remains primarily the property of the state via the national oil companies or their distribution arms.

The option of supplying gas to the private sector to generate DRI and steel (and profit)

has to be compared with other opportunities such as power generation or LNG. As such, there have been few examples of the state being willing to supply long-term gas contracts at low prices to non-state groups. Moreover, even when it has (as in Egypt), political changes and licensing arrangements have sometimes made the process opaque. MBR therefore treats claims of DRI expansion by private groups that have yet to secure gas allocations with some scepticism in its forecasts.

However, expansions by state-affiliated companies such as Sabic, ESI, Qasco and Sulb will still generate significant additional demand for iron ore pellet, while MBR expects the expansions in Egypt to come on-stream over 2013 or shortly after.

The expansions by Gulf Industrial Investment Company (GIIC) in Bahrain and the start-up of Vale in Oman mean that there is now 20 million tpy of pellet capacity in the region – enough to satisfy much of the merchant demand in the region. As a whole, the region was a major net importer until recently, although the last few years have seen a significant increase in exports of iron ore from Iran to China. As iron ore prices fall, MBR believes that those exports will also decline, but the pellet requirement in the region will show significant growth and this could justify further investment in capacity with projects at present under examination by both Vale and GIIC.

Yet scrap will also see an increase in demand. Smaller private sector mills without

ExaMplES of nEw (and pRopoSEd) capaciTy in MEna (‘000 TonnES)Country Company Type Crude Rebar Rod Sections HRC CRC HDG NotesBahrain Sulb DRI-EAF 1,100 600 2012/13 Sulb EAF 1,000 500 2014Oman Sharq Sohar EAF 500 2013 plus transfer of RAK from UAE to Oman Jindal DRI-EAF 2,000 2013/14Qatar Qasco DRI-EAF 600 Brownfield expansion Al Watania EAF 400 200 100 100 2012Saudi Hadeed DRI-EAF 1,000 500 2013Arabia Al-Rajhi EAF 150 700 300 2012 Al-Rajhi DRI-EAF 3,000 400 1,600 600 400 2017/18 Al-Yamamah EAF 800 2014 - may be delayed Atoun Steel EAF 900 500 2014/15 South Steel EAF 1,000 1,000 2012/13 Sulb EAF 300 2014 Al-Quryan EAF 300 2015UAE ESI EAF 1,600 1,600 2017 - not yet approvedAlgeria Tosyali EAF 1,000 1,000 2013 Qatar Steel DRI-EAF 5,000 5,000 Feasibility under way 2017/18Egypt Beshay DRI-EAF 1,500 1,000 2012-13 Suez DRI-EAF 1,250 2012-13 Ezz DRI-EAF 1,300 1,000 250 2013-14 Elmarkaby EAF 350 2013-15EAF - Electric Arc Furnace, DRI - Direct Reduced Iron Source: MBR

MiddlE EaSTERn* cRudE STEEl ouTpuT

0

60

10

20M

illio

n to

nnes

30

40

50

2006

2007

2008

2009

2010

2011

2012

(e)

2013 (f

)

2014

(f)

2015

(f)

2016

(f)

2017

(f)

2018

(f)

noRTh afRican* cRudE STEEl ouTpuT

0

20

2006

2007

2008

2009

2010

2011

2012

(e)

2013 (f

)

2014

(f)

2015

(f)

2016

(f)

2017

(f)

2018

(f)

2

4

6

8

10

12

14

16

18

Mill

ion

tonn

es

*Algeria, Morocco, Tunisia, Libya, Egypt, Sudan Source: MBR

*Bahrain, Iran, Iraq, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syria, UAE & Yemen Source: MBR

Middle East Steel 2012

Overview

December 2012 | Middle East Steel | 7

gas supply agreements, such as South Steel in Saudi Arabia or United Steel in Kuwait, have built scrap-based EAFs. Some of this has been secured locally, although increasingly imports will play a factor. Al Yamamah, Atoun Steel and Sulb in Saudi Arabia and Tosyali in Algeria are all building scrap-fed EAFs.

Moreover, even DRI-EAFs will increase their proportion of scrap utilised. Rather than relying on 90-95% DRI and just utilising internally-generated scrap, MBR believes that these mills may drop their DRI rates to 75% or so and supplement with scrap. For example, ESI is examining its flat product expansion of 1.6 million tpy without adding a new DRI module and it appears that Sulb of Bahrain may do the same as it adds a 1 million tpy EAF in 2014.

Both trends will result in rising scrap imports, but will be complemented by improved scrap collection chains that will result in increased domestic scrap collection. Nevertheless, this will lead to more competition to secure scrap imports and to secure raw materials domestically. Over the last few years, there has been an increase in scrap export bans, with Algeria, Saudi Arabia and Morocco implementing them. There will be more to come, in MBR’s opinion.

Merchant DRI/HBI therefore becomes an option for steelmakers. Flat product mills in Morocco and Turkey are buyers of merchant DRI, as are regional long product EAFs such as South Steel. However, MBR sees some constriction in supply here and consequently mills may need to secure material from outside the region. Jindal will largely exit this market in 2013, as it brings its steel mill on line. MBR estimates that it will sell around 1.5-1.7 million tonnes in 2012, although MBR also believes that it will continue to sell a more limited amount.

Qasco is also likely to reduce its sales from 2013, as will ESI once it brings on its flat product mill around 2017. While Sulb will be selling some DRI from the second half of 2013, it too is likely to exit sales after bringing on its second EAF in 2014. As a result, external suppliers such as Lebedinsky and Lisco will see increased opportunities.

demand growthOf course investment in steelmaking capacity in the region only makes sense if demand growth is strong enough to justify local sourcing and if it is cost-effective. In terms of demand, that is certainly the case. Even in 2011 and 2012, when consumption in certain markets fell dramatically due to civil disturbance and political uncertainty – Egypt, Libya, Tunisia, Syria – long product consumption in the region rose by 4.5% and an estimated 5.0%, respectively.

One of the strongest regions for growth has been in the Gulf Co-operation Council (GCC) market. High oil and gas prices have provided a budgetary boost to governments. In turn, they appear to have undertaken a political commitment to invest in infrastructure and to diversify into manufacturing in what remain quite centrally-driven economies. This is hugely steel-intensive and will underpin medium-term steel demand growth for at least the next 2-3 years, with Saudi Arabia the key example. This is not only important for rebar and structural sections, but also for products such as wire rod. As an example, the Omani government’s private investment group Takamul is building a 60,000 tpy galvanized wire plant in 2013 in conjunction with Singapore’s Global Steel Industries.

North African long product demand has been hit in the last couple of years by political uncertainty in Tunisia and Egypt and the civil war in Libya. While it may be too early for a definitive call, it is MBR’s view that long product demand will return to these markets by 2013/14 and could accelerate later in the forecast period. A key imperative in these economies is to provide housing for young populations, while infrastructure investments will be a relatively simple way to generate employment growth. Both will be enormously steel-intensive.

An example of the astonishing growth rates possible is the performance of Iraq. Imports of rebar are expected to touch 2 million tonnes in 2012 for example – to the huge benefit of Turkish and Ukrainian suppliers. Structural sections imports are also growing fast. While again this is subject to political uncertainty, MBR believes that strong growth rates will remain in place for the near term.

Iran, however, is of some concern. At over 20 million tpy of finished steel consumption at its peak, MBR estimates that demand will fall by more than 10% in 2012 and imports have borne the brunt of this as tightening sanctions have limited foreign exchange availability. We expect that imports will fall again. Meanwhile the development of the indigenous DRI industry remains well behind schedule and struggles to source equipment.

Despite this, MBR is forecasting an average annual demand growth of 7.2% for regional long product consumption out to 2018. Consumption will surpass 80 million tonnes compared to an estimated 58 million tonnes in 2012.

Approximately 25% of finished steel demand is for flat products. The key consumers are tubular manufacturers and the construction product industry, which between them account for over 80% of regional demand. There are a number of smaller markets including shipbuilding, transformers, barrels and containers,

packaging, automotive as well as some light industrial manufacturing, while Turkey and Iran produce a wider range of manufactured products.

Flat products will see demand growth, but in MBR’s opinion this will be slower than for long products. MBR is forecasting average annual demand growth of 5.8% out to 2018. Iran will be a key drag on growth as it currently consumes a third of the regional total.

There are growth opportunities nevertheless. Tubular facilities such as Kuwait Pipe Industries’ new LSAW mill are due on-stream, while there are a number of spiral linepipe projects in Iraq. Construction products such as purlins, sandwich panels and HVAC equipment are increasingly made locally and are likely to show significant growth.

Yet regional projects in the Middle East are some way away with none confirmed. The furthest progressed is the ESI 1.5 million tpy hot rolled coil project that is scheduled for 2016-17. Al-Rajhi of Saudi Arabia has another 1.5 million tpy project, but this will not be ready before 2018. Moreover, Turkish EAF mills are operating below capacity thanks to compressed spreads between scrap and finished products.

import implicationsThe regional net deficit in long products has slipped in the last couple of years to around 4-5 million tpy, although this includes the net exporter Turkey shipping to Iraq and the GCC region. With much of the investment going into long products, MBR believes that this deficit will be relatively stable looking forward. Rising capacity will also mean that the inflows will shift more to North Africa and Iraq and away from Iran and the GCC area.

On the other hand, the integration back into crude steel production along with the poor economics for re-rollers means that the net deficit for billet will drop sharply. Over 2007-09, this net deficit was almost 10 million tpy. By the end of the forecast period, however, MBR expects that this will more than halve. Iran is likely to exit the slab import market completely as well.

In flat products, however, the lack of local supply growth combined with rising demand will result in a widening deficit. Already a significant 10 million tpy, MBR expects it to rise to almost 14-15 million tpy by 2018. European, Asian and CIS mills will target this market.

*Metal Bulletin Research’s report The Five-Year Strategic Outlook for the Middle East & North African Steel Industry covers the following countries: Algeria, Bahrain, Egypt, Iran, Iraq, Israel, Kuwait, Lebanon, Libya, Morocco, Oman, Qatar, Saudi Arabia, Sudan, Syria, Turkey, Tunisia, United Arab Emirates, Yemen.

8 | Middle East Steel | December 2012

Coil-Tainer Limited

Middle East Steel 2012

Market outlook

December 2012 | Middle East Steel | 9

The Middle East steel industry has had a difficult time this year and there are no signs that there will be an improvement in demand or consumption levels in 2013 due to the bleak outlook for the global economy.

The region has recovered reasonably well from the political turmoil caused by the Arab Spring in 2011 and most markets are back to stability, which supports healthy steel demand and consumption levels.

The biggest sales markets for Turkish, Russian and Ukrainian rebar exporters continue to be the usual players in the Gulf Co-operation Council (GCC), with Saudi Arabia and the United Arab Emirates particularly important due to their steady demand from the construction sector.

The Saudi government is investing its huge revenues from oil and gas exports to invest in steel-intensive projects. It has several multi-billion dollar investment plans in the pipeline to improve infrastructure and housing for its growing young population.

“There is always good demand from Saudi Arabia, but compared to five years ago when there were about eight traders selling into Saudi,

maybe now there are about 150. So the rebar market is very good in Saudi, but the profits [for the traders] are not good,” said one trader in the GCC region.

Construction coolsConstruction activity by private real estate companies is continuing in the UAE, although it has fallen immensely since the global financial crisis in 2008 when the market was inundated with developers keen to cash in on the building boom in Dubai. Those days are gone.

Despite the overall slump in the building market in the UAE since the financial crisis, government orchestrated projects for housing citizens in Abu Dhabi have become the biggest consumers of rebar in the UAE. The majority of Abu Dhabi’s rebar requirements are sourced from its state-owned domestic mill Emirates Steel.

Rebar demand and consumption levels have plummeted significantly in the Middle East over the last four years. Several major construction projects not backed by governments were cancelled or put on hold due to financial

constraints and have yet to materialise.Traders and stockists in the GCC region still have

vivid memories of when their rebar inventories plummeted in value from record highs of $1,450/tonne in July 2008 to less than $450/tonne in December that year.

Numerous international rebar trading, distribution and re-rolling companies were forced to write off large inventories worth many millions of US dollars. Some smaller companies went out of business or focused on other products like sections.

The events in 2008 have changed the psychology of the rebar market in the Middle East from speculating about prices, generating high stocks and intensive selling into the current situation of purchasing small tonnages sporadically, on a hand-to-mouth basis, to avoid being caught out by an uncertain market.

Demand steadiesLong product demand from end-users has remained scant throughout 2012 and buying activity has been cautious. Some traders have been struggling to stay in business and have switched to trading other commodities since their customers in the Middle East have reduced their rebar purchasing volumes. They are buying small tonnages of a few thousand tonnes to serve their immediate needs instead of tens of thousands of tonnes four years ago.

Rebar stockists have been keeping low-to-medium inventories levels and they are more interested in trying to liquidate their existing stocks to generate cash flow, rather than building stock levels, when demand is scant and market outlook is uncertain. There is currently an oversupply of rebar in the UAE according to market participants in the region.

Distributors have plentiful stocks to serve the needs of a local market characterised by the sporadic purchasing of small volumes to replenish stocks of certain rebar sizes and grades. There has not been immediate demand for imports from Turkey, China or CIS countries for most of the fourth quarter.

China offersThe Middle East was flooded with cheap hot rolled coil and rebar import offers from Chinese mills in August, September and October. China was desperate to reduce its stocks due to significant over-supply and weak demand in its domestic market which in turn led to cut-price deals and quick delivery to Gulf clients.

Rebar from Turkey is still the first choice for buyers in the Gulf region due to its quality, but the lower-priced offers from China attracted purchases from consumers who were keen to cash in on lower prices despite low demand.

During this period there was as much as 100,000 tonnes of ready-made inventory sitting among the major Chinese mills that they were struggling to sell.

Markets stabilise,competition growsSteel demand in the Middle East has stabilised at a healthy level this year, but competition between domestic steelmakers and semis and steel importers to satisfy it is fierce. The outlook for 2013 is for more of the same, reports Stacy Irish

By some estimates, Mena regional demand for heavy sections – like these produced at Emirates Steel in UAE - will reach 8.5 million tpy in 2020

DAN

IELI

10 | Middle East Steel | December 2012

The mobile app is now liveGet your latest global metals news on the move

www.metalbulletin.com/mobile-app

Available for iPad and iPhoneFree to download from the App Store

Middle East Steel 2012

Market outlook

December 2012 | Middle East Steel | 11

At the end of September hot rolled coil import transaction prices from China to the GCC region plummeted by $50 per tonne to $550-560 per tonne cfr main Gulf port , compared with the previous price of $600-630 cfr.

Discouraging importsGCC import prices for billet, rebar and hot rolled coil have steadily declined since April this year (see graph). Competition between Turkish and CIS exporters and domestic producers, such as Hadeed and the Al-Tuwairqi group in Saudi Arabia, Qatar Steel and Emirates Steel, in Abu Dhabi, is fierce.

Governments in the GCC region have encouraged their citizens to purchase steel made in the Middle East to prevent large volumes of imported material, which puts pressure on its domestic prices.

Hilal Al-Tuwairqi, chairman of Saudi Arabian steel producer Al-Tuwairqi Holdings and former president of the Arab Iron & Steel Union, is urging governments in the GCC region to impose a 20% import tax on rebar imports to put an end to what he refers to as ‘dumping practices’.

Also, Saeed Al Romaithi, ceo from Emirates Steel, is working closely with the Abu Dhabi government to impose customs duties on steel imports to the UAE. He wants an additional 5% customs duty on rebar imports to support domestic steel producers in the UAE.

The UAE government has an existing 5% customs duty on imported rebar, which was reinstated in February 2009. But it is not enough to fend off the large import volumes from Turkey and the CIS, which have been cashing in on the stable demand for construction steel in the region.

Emirates Steel adjusts its domestic rebar prices on a month basis to compete with cheaper rebar imports from Turkish suppliers. The state-owned company is offering rebar to domestic consumers at 2,245 UAE dirhams ($611) per tonne ex works for December production and shipment.

Also, UAE re-roller Conares is offering rebar at 2,225 UAE dirhams ($606) per tonne ex works for December rolling.

This compares with the latest Turkish rebar import price of $595-605 per tonne cfr main Gulf Port for December shipment. Sales have been few and far between due to sufficient stocks levels in the UAE.

Companies such as Emirates Steel have invested in increasing steel production capacity and a diversification of products to serve the needs of its domestic market and to remain competitive against low-cost imported material.

Expansion plannedAt the end of September Emirates Steel completed the second stage of its $1.9 billion expansion plan, which pushed its total steel production to 3.5 million tpy.

The company aims to increase production further to about 5.5 million tpy over the next three years. It now has the capacity to produce 1 million tpy of jumbo and heavy sections from its facility in Musaffah, Abu Dhabi. Production is sold mainly to countries in the Middle East and North Africa (Mena) region.

Demand for heavy sections in Mena countries is now about 5.5 million tpy and is expected to increase to 8.5 million tpy in 2020, according to the company’s estimates. The heavy sections mill was supplied by Italian plantmaker Danieli and will be integrated with an existing 1.4 million tpy meltshop and 1.6 million tpy direct reduced iron (DRI) plant (see projects article).

Level outlookSteel demand in the Mena region is expected to increase by 5.7% in 2012 – up after a 2% fall in 2011 due political instability – and is expected to grow by 8.4% in 2013, supported by government-funded construction projects financed by oil and gas revenues, according to a joint paper by Frost & Sullivan and the World Steel Association.

The report argues that regional production of finished products is expected to reach about 85 million tonnes by 2013, with crude steel production projected at more than 50 million tonnes – up from 27.4 million tonnes in 2010.

Despite the promising growth figures from various industry reports and associations, traders, stockists and distributors in the GCC region have a gloomy outlook for 2013.

“Next year will be as dull as 2012, I’m optimistic for 2014. I don’t think we’ll see an upswing in demand in 2013. The overall economic situation

in all markets is not good. There is oversupply in Japan and China. The European market is showing no signs of improvements and it’s unlikely to get better anytime soon,” said a trader in Dubai.

“The US and Canadian market is ticking along. I can’t see that there will be a big jump in demand or prices in 2013. The only thing that might happen that will help the market is that there will be more distributors, traders [speculators] that will go out of business. It will calm down the market and give it breathing space. There are too many people fishing for business and they need to be removed to regulate the market,” he concluded.

A second trader in Dubai agreed that the market will remain unchanged in 2013.

“The first quarter of 2013 will stay as quiet as 2012. The second quarter of 2013 will show some improvement. China has been dumping HRC to the Middle East and Turkey has been selling large volumes of rebar to the Middle East. We are having a tough time,” said a source from a pipe producer in the GCC area.

Several market sources in the GCC region say that they are expecting the market to remain unchanged in 2013.

“I don’t think that 2013 will be any different to 2012. It will be a tough year for billet and rebar producers and traders. The market will stay stagnant. I don’t think we will see any big price rises or falls and there will be no volatility, which is not good for traders,” said a prominent UAE based long products trader.

“There will not be a great deal of demand. Europe is not doing well and demand is weak there. The USA has its problems and consumption levels are unlikely to change any time soon. China is not showing any signs of cutting production which will add to the oversupply problem. I don’t think there will be a great deal of excitement in 2013,” he concluded.

The author is senior correspondent for Metal Bulletin’s sister publication Steel First

I don’t think that 2013 will be any different to 2012. It will be a tough year for billet and rebar producers and traders

GULF CO-OPERATION COUNCIL AREA IMPORT PRICES*

6/12/

11

6/2/1

2

6/4/

12

6/6/

12

6/8/

12

6/10

/12

27/11

/12

500

600

700

550

650

750

800

Billet

Rebar

Hot rolled coil

$ /ton

ne

Source: Metal Bulletin*cfr main Gulf port

www.danieli.com

DANIELI ENGINEERING AND DANIELI CONSTRUCTION INTERNATIONAL TURNKEY PROJECTS TRULY ENSURE OVERALL INTEGRATED PLANT PERFORMANCES, SAFETY AND OPERABILITY IN ADDITION TO OPTIMIZED AND GUARANTEED PROJECT FINAL COSTSAND COMPLETION SCHEDULE.

ESI 1 and 2, UAE

Two DRI-based minimillsfeaturing EAF hot charge for the production of 3.2 Mtpy of heavy sections, rebars andwirerod. 45,000 tons of steelstructural buildings, 300,000m3 of concrete works.Full LSTK project includingall auxiliary plants, systems and plant infrastructures.

Jesco, Saudi Arabia

400,000-tpy seamless pipecomplex featuring FQM™Fine Quality Mill for theproduction of 16” steelpipes and finishing lines.Full LSTK projectincluding all auxiliaryplants, systems and plantinfrastructures.

Ezz Flat, Egypt

1-Mtpy minimill complex for hot band featuring thinslab casting-rolling process. New DRI plant andexpansion for long productproduction. TK project including allauxiliary plants, systems and plant infrastructures.

Sabic (Hadeed), Saudi Arabia

1-Mtpy minimill for bar and wirerod production. New meltshop and rolling mill expansion (second rolling mill). Full LSTK project includingall auxiliary plants, systemsand plant infrastructures.

DANIELI TURNKEY PROJECTSSINGLE-POINT RESPONSIBILITYFOR A RELIABLE SCHEDULEAND COST CONTROL

Four main references out of total 134, worldwide

Turnkey plantsand Systems Engineering

Turnkey construction, Erection and Systems Engineering

Danieli Headquarters

33042 Buttrio (Udine) ItalyTel (39) 0432.1958111

DCI_TK plants_418_274_MB_Layout 1 29/11/12 14.42 Pagina 1

www.danieli.com

DANIELI ENGINEERING AND DANIELI CONSTRUCTION INTERNATIONAL TURNKEY PROJECTS TRULY ENSURE OVERALL INTEGRATED PLANT PERFORMANCES, SAFETY AND OPERABILITY IN ADDITION TO OPTIMIZED AND GUARANTEED PROJECT FINAL COSTSAND COMPLETION SCHEDULE.

ESI 1 and 2, UAE

Two DRI-based minimillsfeaturing EAF hot charge for the production of 3.2 Mtpy of heavy sections, rebars andwirerod. 45,000 tons of steelstructural buildings, 300,000m3 of concrete works.Full LSTK project includingall auxiliary plants, systems and plant infrastructures.

Jesco, Saudi Arabia

400,000-tpy seamless pipecomplex featuring FQM™Fine Quality Mill for theproduction of 16” steelpipes and finishing lines.Full LSTK projectincluding all auxiliaryplants, systems and plantinfrastructures.

Ezz Flat, Egypt

1-Mtpy minimill complex for hot band featuring thinslab casting-rolling process. New DRI plant andexpansion for long productproduction. TK project including allauxiliary plants, systems and plant infrastructures.

Sabic (Hadeed), Saudi Arabia

1-Mtpy minimill for bar and wirerod production. New meltshop and rolling mill expansion (second rolling mill). Full LSTK project includingall auxiliary plants, systemsand plant infrastructures.

DANIELI TURNKEY PROJECTSSINGLE-POINT RESPONSIBILITYFOR A RELIABLE SCHEDULEAND COST CONTROL

Four main references out of total 134, worldwide

Turnkey plantsand Systems Engineering

Turnkey construction, Erection and Systems Engineering

Danieli Headquarters

33042 Buttrio (Udine) ItalyTel (39) 0432.1958111

DCI_TK plants_418_274_MB_Layout 1 29/11/12 14.42 Pagina 1

14 | Middle East Steel | December 2012

Middle East Steel 2012

Project review

AlgeriaArcelorMittal Annaba, Algeria’s sole steel producer, is undergoing a $500 million investment to increase its steelmaking capacity from 1 million to 1.4 million tpy by 2014. This will involve blast furnace relining, revamping the sinter plant and installing a new coke battery. The expansion will focus on long products, although the company makes a wide range of products including hot-rolled and cold-rolled sheet and coil, hot-dip galvanized coil, tinplate, and OCTG/tube and pipe. Commissioning is expected from 2013.

With the government investing in several large infrastructure and housing projects, local steel demand is being boosted, attracting the attention of other steelmakers.

Qatar Steel is studying the possibility of establishing a 2.5 million tpy rebar mill in Algeria. A new government-owned joint venture between Qatar Steel and Qatar Mining

called Qatar Steel International has been formed, which will have a 39% stake in the plant, with the Algerian government holding the remaining 61%.

It is envisaged that the plant will initially produce 2.5 million tpy of rebar and then later double capacity with the addition of 2.5 million tpy of flat-rolled products, a Qasco spokesman told Metal Bulletin in July.

BahrainSince construction is one of the biggest areas of activity in the Middle East, it is not surprising to find further investments in the types of steel required in this sector. Although there are many regional bar and light section producers, heavy sections and beams have been absent from the product mix until recently. This gap is now being filled by Emirates Steel in the UAE, which started up its 1 million tpy heavy sections mill in January, and now the United Steel Company (Sulb) in

Bahrain is commissioning its 850,000 tpy beams and sections mini-mill.

Sulb is owned 51% by the Gulf United Steel Holding Company (Foulath) and 49% by Japanese heavy sections producer Yamato Kogyo. Foulath is also the sole owner of the two Gulf Industrial Investment Co iron ore pelletizing plants which are adjacent to the Sulb steel mill at the Hidd Industrial Area. These pelletizing plants, of total capacity 11 million tpy, will supply a 1.5 million tpy Midrex DRI plant, which will in turn provide feedstock for Sulb’s 850,000 tpy EAF.

The Sulb mini-mill comprises a 120-tonne ultra-high-power EAF and ladle furnace. The bloom/beam blank caster was originally designed for three strands, but was upgraded to four strands some six months after ordering. The heavy section mill has an initial capacity of 600,000 tpy and will eventually be capable of 1 million tpy, says Foulath. The mill is said to be highly flexible in terms of product mix and sizes, and the line is designed for programme changes in just 20 minutes. SMS Concast supplied the meltshop and SMS Meer the rolling mill.

Integrated from iron ore pellets to finished products, Sulb will be the lowest-cost producer of its type in the world, the company claims, and when fully operational will replace about 14% of the medium and heavy beams being imported into the Middle East.

EgyptEgypt is the home of Ezz Steel, the largest independent steel producer in the Mena region with a total capacity of 5.8 million tpy of finished steel, including 3.5 million tpy of long and 2.3 million tpy of flat-rolled products.

The company’s planned next stage of investment is a 1.9 million tpy Energiron III DRI module at its Ezz Flat Steel (EFS) plant, Ain Sokhna, near Suez, to provide feedstock for both the EFS mini-mill (which is also to be expanded in capacity) and another group mini-mill at Ezz Steel Rebars. Phase 2 involves erecting another DRI module at the same site to supply the

Regional expansion and diversification aboundSteel companies across the Middle East and North Africa are increasing capacities and widening product ranges in response to local markets and anticipated demand. Steve Karpel reviews projects that have come on stream this year and what is moving through the pipeline for the near future

Suez Steel’s DRI-based steelmaking complex will feature a 1.95 million tpy Energiron module feeding a 1.3 million tpy meltshop for long products

SUEZ

STE

EL

December 2012 | Middle East Steel | 15

expanded EFS meltshop. The two new DRI modules will reduce these steel plants’ dependency on imported scrap.

The overthrow of the Mubarak regime in Egypt, however, resulted in legal obstructions to these investments arising from allegations that the DRI construction licences were acquired from the then-government illegally. Egypt’s Court of First Instance annulled both licences in September 2011, since when construction has stopped, with the first DRI plant 80% complete. The court also annulled the DRI licences that had been awarded at the same time (2008) to three other Egyptian steelmakers, including Beshay Steel and Suez Steel.

Ezz Steel announced last month that the court had awarded a new licence on 14 November, replacing the annulled one, to company subsidiary Ezz Rolling Mills for the construction of the DRI plant plus additional meltshop facilities at Ain Sokhna. The licence terms require a total payment of EGP 330 million over the next six and a half years.

The licensing dispute has not affected the normal operations of Ezz Steel, which reported a 10% increase in net sales in the first half of 2012 to EGP 10.31 billion ($1.72 billion), although Ebitda fell by 11% to EGP 1.1 billion.

A new licence was also awarded to Suez Steel in mid-year. The steelmaker, a part of the Solb Misr group, is building a 1.95 million py HYL/Energiron DRI plant linked to a 1.3 million tpy billet and beam blank meltshop.

The new integrated steel mill is almost finished, and is expected to start up early in 2013, bringing the company’s steelmaking capacity up to 2 million tpy. Products will supply the Egyptian market, with any surplus billet exported to the local region, says a spokesman.

Other investments in Egypt are proceeding. Rebar roller Elmarakby Steel has ordered a 350,000 tpy meltshop from SMS Siemag to produce 130 sq mm billet. This will supply its 240,000 tpy rolling mill in 6th of October City, with excess billet to be sold on the market pending the construction of a second rolling mill. The meltshop is expected to start up by December 2013, fed by imported scrap.

IraqThe steady rebuilding of Iraq’s infrastructure has meant a continuing focus on the basic industries such as steel, cement and power, as well as its dominant economic base – oil and gas. One of the major steel projects is by Iraq’s Mass Global Investment, which has been active in the cement and power sectors with several plants completed or in progress. Turning its attention to steel, it is building a 1 million tpy mini-mill in the north of the country (Kurdistan), which will focus initially on rebar.

The mill, supplied by Danieli with power supply by ABB, comprises a 120-tonne FastArc™ EAF, a 120-tonne ladle furnace, a 5-strand

FastCast™ caster for 130 mm and 150 mm sq billet, a 120 tph walking hearth furnace and a 650,000 tpy rolling mill for 10-32 mm diameter deformed bars. The mill is scheduled to start up in the second half of 2013, says Mass Global. The company is also constructing another rolling mill for small and medium sections, which is expected to start in early 2014.

The EAF will be scrap-fed, but the company is studying the possibility of building a DRI plant, together with an iron ore pelletizing facility. It also says that it plans to double the mini-mill steel capacity eventually.

Indian pipemaker Jindal Saw has instigated a $200 million project to build a new pipe mill in Iraq, sited in a new industrial city outside Basra. It will produce 300,000-350,000 tpy of longitudinal submerged arc-welded pipe, 16-65in (406-1,651 mm) in diameter with wall thickness up to 1in. It is planned to start up at the end of 2013, while an anti-corrosion coating line will commission earlier in the year.

Fully-owned by Jindal Saw, the company will sell into Iraq’s oil and gas transmission sector.

An expansion phase is also planned six months after start-up with the introduction of hot induction bending, and the company says it intends to add spiral welded pipe as well at a later stage.

OmanOne of the biggest planned investments in the region is the Jindal Shadeed integrated steel mill in Oman, which will eventually comprise a 7 million tpy iron ore pelletizing plant, a Midrex DRI/HBI plant, a 2 million tpy meltshop and a long products rolling mill.

India’s Jindal Steel & Power (JSPL) acquired the Shadeed DRI project for $464 million in 2010, and the 1.5 million tpy Midrex DRI/HBI module started up at the end of that year. Prior to the meltshop commissioning next year, Shadeed has been exporting the HBI produced – just over 1 million tonnes were sold last year.

JSPL is now engaged in expanding the project at Sohar Industrial Port into a complete steelmaking complex, and a 2.0 million tpy meltshop is scheduled to commission in the

Assembling the 120 tonne EAF at United Steel Co, Bahrain (Sulb)

SMS

SIEM

AG

The Sulb mini-mill includes an efficient dedusting plant

SMS

SIEM

AG

a new Era in industrial drive solutions is dawningAs of June 1st we are part of the Nidec group, strengthening our market presence:we are ready to help our customers form the future with precision and control.

110393-AnsaldoNidec215x280-Metals.indd 1 29-11-2012 12:55:06

Middle East Steel 2012

Project review

December 2012 | Middle East Steel | 17

final quarter of 2013. The Danieli-built meltshop will be fed directly by hot DRI, and comprise a 150-tonne EAF, a 150-tonne ladle furnace, a 200-tonne twin-tank vacuum degasser, and a 2 million tpy 6-strand billet/bloom caster. The associated infrastructure also includes an air separation plant, a 4,800 cu metre/day desalination plant and extensive port facilities.

The semis produced will be initially targeted mainly at the Saudi market, as well as domestic re-rollers supplying Oman’s infrastructure projects. In time, however, it is planned that much of the billet produced will be taken up by a 1 million tpy rolling mill for rebar and merchant bar, plus a seamless pipe mill, which are expected to start around 2015. These represent a $400 million investment, while the meltshop is put at $475 million.

Jindal foresees the DRI plant expanding from 1.5 million to 5 million tpy over the next five years, which will be fed by a 7 million tpy iron ore pelletizing plant now in the planning stage.

Like several steel mills in the region, Oman’s Sohar Steel started out as a pure rolling mill for rebar, and has since integrated back into steelmaking. The rolling company, Sharq Sohar Steel Rolling Mills (SSSRM), has a capacity for 300,000 tpy of 8-32 mm diameter rebar, which can be epoxy coated. Sister company Sohar Steel was built with a 36-tonne EAF and ladle furnace feeding a 3-strand caster for 100, 120 and 130 mm sq billet. It can produce 250,000 tpy of billet.

Sohar Steel is now being upgraded by Danieli Centro Met with a 75-tonne FastArc™ EAF, increasing steel output to 700,000 tpy. Danieli is also supplying a 140-tonne teeming crane to handle the larger tapping weights. The new meltshop is due to start up in mid-2013.

The port of Sohar is developing into a focus for steel products in the Gulf, with Al Jazeera Steel Products also being established there. This company buys billet and has four ERW tubemaking lines with a total capacity of 300,000 tpy of international-standard tube products with plain, threaded and coupled ends. It also has three galvanizing lines for corrosion-protected tube up to 219 mm diameter.

Al Jazeera Steel has subsequently commissioned a 300,000 tpy merchant bar mill for producing angles, channels, squares, flats and rounds. The company says it is exporting products to 25 countries, including North America, Europe and Australia.

QatarQatar Steel (Qasco) started production in 1978 as one of the first DRI-based integrated steelmakers in the Gulf, and has continued to augment its capabilities, both in Qatar and also elsewhere in the region: it established a subsidiary rolling mill – Qatar Steel Co FZE – in Dubai in 2003.

Last year the company awarded Siemens VAI a contract to supply a new 1.1 million tpy billet meltshop for its Mesaieed site, comprising a 110-tonne EAF, a 110-tonne ladle furnace, a 6-strand billet caster plus a new dedusting plant and all auxiliary equipment. This new mill is expected to go into operation in 2013.

The $250 million investment was originally intended to replace the company’s existing meltshop in Mesaieed, but because of increasing steel demand in the Gulf, it has been decided to employ it as an additional facility, with the original 95-tonne EAF and ladle furnaces ordered also being enlarged to 110 tonnes. Qatar Steel’s current capacities are 2.4 million tpy of DRI/HBI, 1.9 million tpy of raw steel, 1.8 million tpy of rebar and 0.3 million tpy of wire rod.

Looking further afield, Qatar Steel is also studying the possibility of establishing a 2.5 million tpy rebar mill in Algeria (see earlier section in article).

Saudi ArabiaThe Kingdom’s biggest steel company, Saudi Iron & Steel Co (Hadeed) is continuing to invest in new capacity to meet the needs of its domestic market. A new 1 million tpy mini-mill from Danieli is under construction at Al-Jubail, consisting of a 150-tonne EAF, a 150-tonne ladle furnace, a 6-strand caster for 130 mm and 150 mm sq billet, with materials handling for ferro-alloys and cold DRI, and fume treatment facilities.

A 120 tph walking beam furnace will charge directly into an 18-stand wire rod rolling mill. This rolling mill is being put together by upgrading and augmenting an existing rolling

mill. The new wire rod mini-mill is in the final stages of construction and is expected to start up in the second quarter.

This investment will increase Hadeed’s total capacity to 6 million tpy, with long products accounting for two-thirds of this. The new plant will also make Hadeed self-sufficient in billet, says Abdulaziz Al-Humaid, Hadeed chairman and Sabic executive vp for metals: “We import 400,000 tpy of billet, but we will substitute these imports and produce about 4 million tpy of both billet and finished long products,” he says.

Alongside other grades, the new rolling mill will produce high-carbon wire rod, which is now imported. The Saudi market for this is estimated at some 200,000 tpy.

Hadeed has five DRI modules with total capacity of about 5.4 million tpy. The company uses a mix of DRI and scrap in its five electric arc furnaces; the ratio varies according to product, but averages about 20% scrap, which is imported. “We import about 600,000 tpy of scrap now, but when the new mini-mill starts up, an additional 600,000 tpy of imported scrap may be needed,” Al-Humaid says, and points out that most of Hadeed’s products, 95-96%, are sold to its domestic market.

Another Saudi steelmaker, Rajhi Steel, commissioned a 1.0 million tpy high-speed bar and rod mill in May at its site at Alkhumra, south of Jeddah. It produces 10-40 mm diameter debar, and 5.5-16.0 mm smooth and deformed wire rod. In order to feed this mill, the company’s 0.85 million tpy meltshop here has been upgraded to produce more billet, with a 200 tph walking beam reheat furnace connected directly to the billet caster. All plant has been

Saudi Iron & Steel’s latest investment will make it self-sufficient in billet and introduce new long product grades

SABIC

Excellent engineering services stand out from the crowd … especially when it comes to intelligent revamps. It’s about nothing less than upgrading existing plants to meet future market demands – one of today’s central challenges.

That’s where our whole wealth of experience comes in. After all, our job is to help you increase your productivity while improving quality. Equally signifi cant here is smart

planning, for instance taking advantage of scheduled main-tenance stoppages and minimizing production losses. Your bottom line: You save time and money.

Countless completed projects prove our quality and reliability as a global specialist in metallurgical plant and rolling mill technology.

Modernizations for quality and reliability

Boost productivity.Cut costs.

SMS SIEMAG AG

Eduard-Schloemann-Strasse 4 Phone: +49 211 881-0 E-mail: [email protected] Düsseldorf, Germany Fax: +49 211 881-4902 Internet: www.sms-siemag.com

Modernisierung_209x274_e.indd 1 19.11.12 11:06

Middle East Steel 2012

Project review

December 2012 | Middle East Steel | 19

supplied by Danieli, which also designed a 4,000 HP 120 tph scrap shredder for the steelmaker.

The company has another 1 million tpy mini-mill for Jeddah in the feasibility study phase.

Sister company Rajhi Heavy Industry and India’s state-owned Rashriya Ispat Nigam (RINL, or Vizag Steel) are discussing the possibility of a joint-venture 3 million tpy integrated DRI-fed steel mill to be built in Saudi Arabia. The $8 billion plant would take five years to build, and produce long and flat-rolled products.

ArcelorMittal and Saudi Arabia’s Al Tanmiah Industrial and Commercial Investment Co plan to commission their joint venture 600,000 tpy seamless pipe plant in 2013. The $800 million mill, based in Jubail Industrial City 2, will supply its oil, gas and petrochemicals industries.

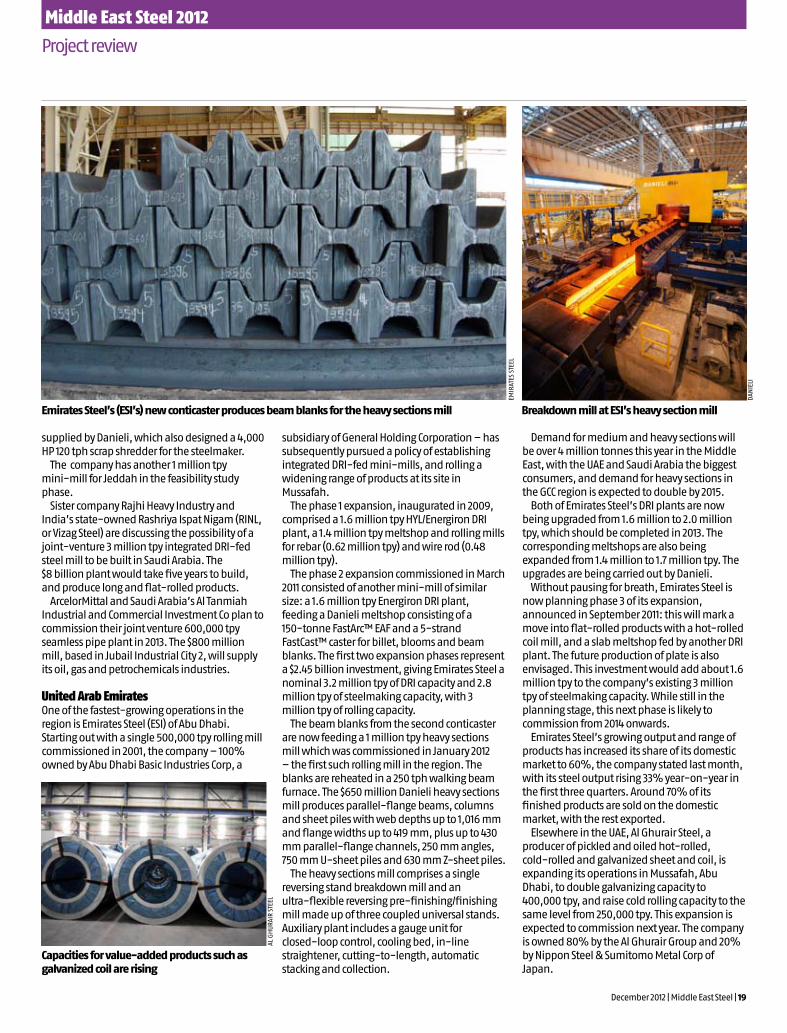

United Arab EmiratesOne of the fastest-growing operations in the region is Emirates Steel (ESI) of Abu Dhabi. Starting out with a single 500,000 tpy rolling mill commissioned in 2001, the company – 100% owned by Abu Dhabi Basic Industries Corp, a

subsidiary of General Holding Corporation – has subsequently pursued a policy of establishing integrated DRI-fed mini-mills, and rolling a widening range of products at its site in Mussafah.

The phase 1 expansion, inaugurated in 2009, comprised a 1.6 million tpy HYL/Energiron DRI plant, a 1.4 million tpy meltshop and rolling mills for rebar (0.62 million tpy) and wire rod (0.48 million tpy).

The phase 2 expansion commissioned in March 2011 consisted of another mini-mill of similar size: a 1.6 million tpy Energiron DRI plant, feeding a Danieli meltshop consisting of a 150-tonne FastArc™ EAF and a 5-strand FastCast™ caster for billet, blooms and beam blanks. The first two expansion phases represent a $2.45 billion investment, giving Emirates Steel a nominal 3.2 million tpy of DRI capacity and 2.8 million tpy of steelmaking capacity, with 3 million tpy of rolling capacity.

The beam blanks from the second conticaster are now feeding a 1 million tpy heavy sections mill which was commissioned in January 2012 – the first such rolling mill in the region. The blanks are reheated in a 250 tph walking beam furnace. The $650 million Danieli heavy sections mill produces parallel-flange beams, columns and sheet piles with web depths up to 1,016 mm and flange widths up to 419 mm, plus up to 430 mm parallel-flange channels, 250 mm angles, 750 mm U-sheet piles and 630 mm Z-sheet piles.

The heavy sections mill comprises a single reversing stand breakdown mill and an ultra-flexible reversing pre-finishing/finishing mill made up of three coupled universal stands. Auxiliary plant includes a gauge unit for closed-loop control, cooling bed, in-line straightener, cutting-to-length, automatic stacking and collection.

Demand for medium and heavy sections will be over 4 million tonnes this year in the Middle East, with the UAE and Saudi Arabia the biggest consumers, and demand for heavy sections in the GCC region is expected to double by 2015.

Both of Emirates Steel’s DRI plants are now being upgraded from 1.6 million to 2.0 million tpy, which should be completed in 2013. The corresponding meltshops are also being expanded from 1.4 million to 1.7 million tpy. The upgrades are being carried out by Danieli.

Without pausing for breath, Emirates Steel is now planning phase 3 of its expansion, announced in September 2011: this will mark a move into flat-rolled products with a hot-rolled coil mill, and a slab meltshop fed by another DRI plant. The future production of plate is also envisaged. This investment would add about 1.6 million tpy to the company’s existing 3 million tpy of steelmaking capacity. While still in the planning stage, this next phase is likely to commission from 2014 onwards.

Emirates Steel’s growing output and range of products has increased its share of its domestic market to 60%, the company stated last month, with its steel output rising 33% year-on-year in the first three quarters. Around 70% of its finished products are sold on the domestic market, with the rest exported.

Elsewhere in the UAE, Al Ghurair Steel, a producer of pickled and oiled hot-rolled, cold-rolled and galvanized sheet and coil, is expanding its operations in Mussafah, Abu Dhabi, to double galvanizing capacity to 400,000 tpy, and raise cold rolling capacity to the same level from 250,000 tpy. This expansion is expected to commission next year. The company is owned 80% by the Al Ghurair Group and 20% by Nippon Steel & Sumitomo Metal Corp of Japan.

Capacities for value-added products such as galvanized coil are rising

AL G

HU

RAIR

STE

EL

Breakdown mill at ESI’s heavy section mill

DAN

IELI

Emirates Steel’s (ESI’s) new conticaster produces beam blanks for the heavy sections mill

EMIR

ATES

STE

EL

Real Innovation, Real Solutions…Real Progress.

Learn more at: www.midrex.com © 2012 Midrex Technologies, Inc. All rights reserved.

These are our technologies,these are our results.

While others boast of technical advancements, Midrex delivers real world results for the steel industry. MIDREX® Plants provide energy efficiency and flexibility, from natural gas to various options for using coal, including gasifiers, coke ovens or BOFs. Steelmakers worldwide rely on Midrex.

Hot DRI for increased EAF production & environmentalbenefits with multiple hot DRI transport options installed and proven

HBI with outstandingchemical & physical quality

Modules operating more than 8,000 hours annually with available capacity up to 2.5 MTPY

Coal-based DRI, HBI & Hot DRI production via and COREX®/MIDREX®

pioneeringforward-thinking

proven

Metal Bulletin full 10.12.indd 1 10/26/12 10:41 AM

Middle East Steel 2012

DRI

December 2012 | Middle East Steel | 21

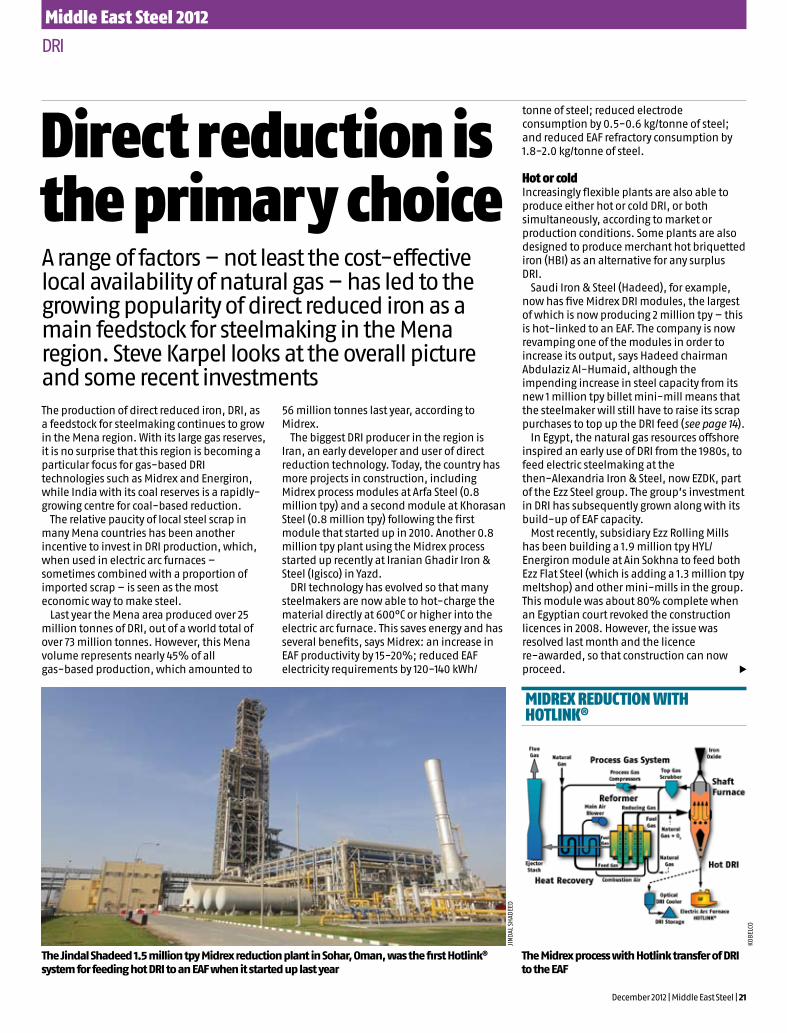

The production of direct reduced iron, DRI, as a feedstock for steelmaking continues to grow in the Mena region. With its large gas reserves, it is no surprise that this region is becoming a particular focus for gas-based DRI technologies such as Midrex and Energiron, while India with its coal reserves is a rapidly-growing centre for coal-based reduction.

The relative paucity of local steel scrap in many Mena countries has been another incentive to invest in DRI production, which, when used in electric arc furnaces – sometimes combined with a proportion of imported scrap – is seen as the most economic way to make steel.

Last year the Mena area produced over 25 million tonnes of DRI, out of a world total of over 73 million tonnes. However, this Mena volume represents nearly 45% of all gas-based production, which amounted to

56 million tonnes last year, according to Midrex.

The biggest DRI producer in the region is Iran, an early developer and user of direct reduction technology. Today, the country has more projects in construction, including Midrex process modules at Arfa Steel (0.8 million tpy) and a second module at Khorasan Steel (0.8 million tpy) following the first module that started up in 2010. Another 0.8 million tpy plant using the Midrex process started up recently at Iranian Ghadir Iron & Steel (Igisco) in Yazd.

DRI technology has evolved so that many steelmakers are now able to hot-charge the material directly at 600°C or higher into the electric arc furnace. This saves energy and has several benefits, says Midrex: an increase in EAF productivity by 15-20%; reduced EAF electricity requirements by 120-140 kWh/

tonne of steel; reduced electrode consumption by 0.5-0.6 kg/tonne of steel; and reduced EAF refractory consumption by 1.8-2.0 kg/tonne of steel.

Hot or coldIncreasingly flexible plants are also able to produce either hot or cold DRI, or both simultaneously, according to market or production conditions. Some plants are also designed to produce merchant hot briquetted iron (HBI) as an alternative for any surplus DRI.

Saudi Iron & Steel (Hadeed), for example, now has five Midrex DRI modules, the largest of which is now producing 2 million tpy – this is hot-linked to an EAF. The company is now revamping one of the modules in order to increase its output, says Hadeed chairman Abdulaziz Al-Humaid, although the impending increase in steel capacity from its new 1 million tpy billet mini-mill means that the steelmaker will still have to raise its scrap purchases to top up the DRI feed (see page 14).

In Egypt, the natural gas resources offshore inspired an early use of DRI from the 1980s, to feed electric steelmaking at the then-Alexandria Iron & Steel, now EZDK, part of the Ezz Steel group. The group’s investment in DRI has subsequently grown along with its build-up of EAF capacity.

Most recently, subsidiary Ezz Rolling Mills has been building a 1.9 million tpy HYL/Energiron module at Ain Sokhna to feed both Ezz Flat Steel (which is adding a 1.3 million tpy meltshop) and other mini-mills in the group. This module was about 80% complete when an Egyptian court revoked the construction licences in 2008. However, the issue was resolved last month and the licence re-awarded, so that construction can now proceed.

Direct reduction is the primary choiceA range of factors – not least the cost-effective local availability of natural gas – has led to the growing popularity of direct reduced iron as a main feedstock for steelmaking in the Mena region. Steve Karpel looks at the overall picture and some recent investments

The Jindal Shadeed 1.5 million tpy Midrex reduction plant in Sohar, Oman, was the first Hotlink® system for feeding hot DRI to an EAF when it started up last year

MiDrEx rEDuction witH Hotlink®

JIn

DAL

SH

ADEE

D

The Midrex process with Hotlink transfer of DRI to the EAF

KoB

ELCo

Middle East Steel 2012

DRI

22 | Middle East Steel | December 2012

This implies that the DRI licences for other Egyptian steelmakers which were annulled at the same time could also be re-awarded. one of the projects was a 1.76 million tpy Midrex plant for Egyptian Sponge Iron & Steel Co (Esisco, owned by the Beshay group) in Sadat City. Another project, for a 1.95 million tpy Danieli/Tenova HYL/Energiron plant for Suez Steel in Attaka, had its licence re-awarded in mid-year, and a Suez Steel spokesman expects both the DRI plant and new meltshop to start up early in 2013. The latter module is reported to be complete, and training of personnel is under way.

Another DRI plant which is just about to commission is the United Steel Company of Bahrain’s 1.5 million tpy Midrex plant, which will feed a meltshop with 0.8 million tpy heavy sections rolling mill. nameplate capacities for DRI plants are often conservative, and 51% owner Gulf United Steel Holding Company (Foulath) states that the module will actually be capable of producing 1.8 million tpy. The plant has an adjacent source of iron ore pellets from the Gulf Industrial Investment Company (GIIC), the 11.0 million tpy pelletizing company which is wholly owned by Foulath.

Flexible facilities A modern example of the flexible DRI modules now being built are the two Energiron plants that started up at Emirates Steel, Abu Dhabi, in 2009 and 2011. These 1.6 million tpy modules can produce either cold DRI or hot product charged directly to the

electric arc furnaces. They are now being upgraded to 2 million tpy each, which should be complete in 2013.

Cold DRI is stored in an open stockyard and transferred to the meltshops by means of belt conveyors. Hot DRI can be discharged at 700°C and sent directly to either the meltshop or the cooler; the Energiron plant uses the enclosed Hytemp® pneumatic transport for handling hot DRI, developed jointly by Danieli and Tenova HYL.

The direct reduction process uses a steam reformer to convert natural gas into the hydrogen and carbon monoxide reducing agents, which reduce the iron oxide to (impure) iron inside the reactor. In the process, wet reformed gas is first dried in a quench tower and then injected into the circuit, where it joins the recycled gas coming from the reactor.

The reducing gas is heated and sent to the reactor distribution ring. oxygen injection is provided between the heater and reactor in order to increase the gas carburization potential when higher percentages of carbon – above 2.5% – are required by the meltshop.

The top gas leaving the reactor is treated to clean it and remove the water and carbon dioxide formed in the reactions. Its heat content is recovered and delivered to the process gas heater. This treated gas, having been cleaned of dust, is sent to a carbon dioxide absorber where this gas is removed by a liquid absorber. This absorber also removes hydrogen sulphide, giving an almost sulphur-free process gas and minimising sulphur addition to the DRI.

The gas leaving the absorber is free of oxidised components and has regained its reduction potential. It then rejoins the reformed gas and passes again through the process gas heater, forming a closed loop.

Shortly after commissioning, the plant was able to better most of its nameplate guaranteed parameters, says Danieli. It achieved a 250 tph capacity, compared with a guarantee of 200 tph. DRI metallization was above 94%, with carbon content above 2.5%. natural gas consumption was 2.45 Gcal/tonne compared with a guaranteed 2.6

Gcal/tonne, and electrical energy consumption was 25 kWh/tonne against a guaranteed 35 kWh/tonne.

Oman first The first Hotlink® Midrex DRI plant was the 1.50 million tpy module at Jindal Shadeed in oman, which commissioned at the end of 2010. The plant, with its adjacent steel plant now being built, is situated at Sohar Port, with a dedicated quay having a draft of 19 metres. This means that it can receive Capesize vessels of 180,000 dwt, which the company claims results in substantially reduced costs of raw materials.

A Capesize vessel can be discharged within five working days, and the raw material handling and stacking system is designed to handle 3,600 tph. The discharge facility comprises two ship unloaders, plus belt conveyors and a stacker/reclaimer.

The raw material furnace charging facility is designed for a capacity of 400 tph, with weigh feeders, vibro screens, belt conveyors and hoppers.

The Hotlink system delivers hot DRI at 650°C by gravity feed to the EAF, in a fully sealed link (see diagram). The DRI can also be fed to a briquette machine for producing hot briquetted iron, HBI. The capacity was designed for a production rate of 187.5 tph, allowing for 1.1 million tpy of hot DRI and 0.4 million tpy of HBI. The port loading facility can handle 850 tph of HBI, with a soft loading facility of 1,600 tph being built.

Shadeed points to various features of its direct reduction plant which have been designed for increased productivity and product quality. Combustion air is preheated to 675°C and feed gas to 580°C. An oxygen injection system with ten injection nozzles for the bustle reduction gas is used to increase bustle gas temperature: this allows for increased productivity while maintaining product quality. An oxygen flow of up to 4,000 cu metres/h is employed. The gas reformer consists of 16 bays with 30 tubes per bay.

Higher reduction temperatures are assisted by the on-site iron ore pellet coating system, which coats the iron oxide pellets with lime solution, at a design rate of 1.5 kg/tonne of iron ore. A coating of lime hydrate on the pellets allows a significant increase in reducing gas temperature, says Midrex, which results in a production increase of up to 20%.

The DRI’s nominal specification is 93% minimum metallization with 1.5% minimum carbon, and a discharge temperature of 650°C.

other plant which has been built as part of the greenfield steel complex includes an air separation plant and 4,800 cu metre/day desalination plant.

Dri proDuction*

Country 2009 2010 2011Egypt 2.91 2.86 2.97Iran 8.20 9.35 10.37Libya 1.11 1.27 0.30oman - - 1.11Qatar 2.10 2.16 2.23Saudi Arabia 5.03 5.51 5.81UAE - 1.18 2.25World total 64.44 70.37 73.32

*million tonnes. Includes HBI. Source: Midrex Technologies

The second 1.6 million tpy Tenova HYL DRI module at Emirates Steel in Abu Dhabi started up this year, and, along with the first identical module, is already being expanded to produce 2.0 million tpy

TEn

ovA

HYL

Emirates Steel Industry Magazine Ad.pdf 1 12/4/12 3:58 PM