Embed Size (px)

Citation preview

NYDOCS01/1000894.2 1 June 23, 2004

Supervision of Financial Conglomerates in the European Union

Michael Gruson*

I. The Purpose of Supplementary Supervision

On November 20, 2002, the European Parliament adopted Directive 2002/87/EC1 introducing supplementary supervision of financial conglomerates [herein the Supplementary Supervision Directive].

The principal reason for this Directive was the need to face the accelerating pace of consolidation in the financial industry and the intensification of links between financial markets. Over the past years, a number of cross-sector groups combining insurance companies, banks and investment firms have been created and have become of significant importance in the EU.2 Combined financial operations may create new prudential risks or exacerbate existing ones.3 Laws and regulations dealing with different financial sectors were not able to deal with these developments and such laws have traditionally adopted different approaches with different definitions of capital, different types of risks and different capital requirements.4 For instance, insurance supervisors have historically been primarily concerned with the

* Dr. jur., LL.B., M.C.L. Of Counsel and previously partner of the international law firm Shearman &

Sterling LLP.

1 Directive 2002/87/EC of the European Parliament and of the Council of 16 December 2002 on the supplementary supervision of credit institutions, insurance undertakings and investment firms in a financial conglomerate and amending Council Directives 73/239/EEC, 79/267/EEC, 92/49/EEC, 92/96/EEC, 93/6/EEC and 93/22/EEC, and Directives 98/78/EC and 2000/12/EC of the European Parliament and of the Council, O.J. Eur. Comm. No. L 35/1 (2003) [herein the Supplementary Supervision Directive]. For a detailed discussion of the Supplementary Supervision Directive, see Michael Gruson, Consolidated and Supplementary Supervision of Financial Groups in the European Union, 2004 DER KONZERN 65 (Part I), 249 (Part II) [herein Gruson, Consolidated and Supplementary Supervision]; Michael Gruson, Supervision of Financial Holding Companies in Europe: The EU Directive on Supplementary Supervision of Financial Conglomerates, 36 INT’L L. 1229 (2002).

2 Recitals (2) & (3), Supplementary Supervision Directive.

3 Explanatory Memorandum to the Proposed Supplementary Supervision Directive (Apr. 24, 2001), O.J. Eur. Comm. No. C 213/227 (2001) [herein 2001 Explanatory Memorandum], at 2 sub 1.

4 Tripartite Group of Bank, Securities and Insurance Regulators, The Supervision of Financial Conglomerates (Bank for International Settlements, July 1995) [herein Tripartite Report], at 39, sub no. 104; The Joint Forum, The Joint Forum Compendium of Documents (July 2001) [herein Joint Forum Report], Capital Adequacy Principles Paper, at 12, sub no. 6. The Tripartite Group was formed at the initiative of the Basle Committee on Banking Supervision (Basle Committee) in early 1993 to address a range of issues relating to the supervision of financial conglomerates. The Joint Forum was established in early 1996 under the aegis of the Basle Committee, the International Organization of Securities Commissions (IOSCO) and the International Association of Insurance Supervisors (IAIS) to take forward the work of the Tripartite Group. The Joint Forum Report is a compilation of papers that have been prepared by the Joint Forum since its inception in January 1996.

NYDOCS01/1000894.2 2

liability side of the balance sheet as the main source of risk, although assets are of course monitored too. Regulations in the banking sector regard the asset side of the balance sheet as the principal source of risk, although an examination of the source of funding is an important aspect of the supervisory process. Securities supervisors require securities firms to have sufficient liquid assets to repay promptly all liabilities at any time. The scope for potential supervisory problems increases if a financial conglomerate spans a number of financial markets due to the web of financial interrelationships characteristic of financial conglomerates. On the other hand, such conglomerates may gain financial solidity by diversifying that risk.5 The Supplementary Supervision Directive intends to ensure the stability of the European financial market, establish common prudential standards for the supervision of such financial groups throughout Europe, and introduce level playing fields and legal certainty between financial institutions.6

II. Relationship to Existing Solo and Consolidated Supervision

The basic philosophy of the Supplementary Supervision Directive is that the solo supervisions of individually regulated entities should continue to be the foundation for effective supervision. Furthermore, the Supplementary Supervision Directive does not replace the existing consolidated or supplementary supervision of groups that operate in one sector of the financial industry, but introduces an additional supplementary supervision of the regulated entities in groups that straddle more than one financial sector. The Supplementary Supervision Directive is based on the notion that the various supervisory authorities of different sectors of the financial industry and the supervisory authorities of the different Member States need to establish a coordinated approach in order that prudential assessment can be made from a group-wide perspective.7

In addition to solo supervision, consolidated supervision applies on a sectoral basis to groups of credit institutions, investment firms and financial institutions.8 The Banking Directive9 requires consolidated supervision of (1) every credit institution10 that has another credit institution or a financial institution11 as a subsidiary12 or that holds a participation13 in such institution, and (2) every credit 5 Tripartite Report, at 16, sub no. 41.

6 2001 Explanatory Memorandum, at 2, sub 1.

7 Tripartite Report, at 16, sub no. 42.

8 For a detailed discussion of consolidated supervision of banking groups and investment firm groups, see Gruson, Consolidated and Supplementary Supervision, at 66.

9 Directive 2000/12/EC of the European Parliament and of the Council of 20 March 2000 relating to the taking up and pursuit of the business of credit institutions, O.J. Eur. Comm. No. L 126/1 (2000), as amended [herein Banking Directive].

10 Art. 1(1), Banking Directive.

11 Art. 1(5), Banking Directive. A financial institution is an undertaking other than a credit institution, the principal activity of which is to acquire holdings or to carry on most of the activities that a credit institution may engage in, other than deposit-taking. Investment firms are financial institutions.

12 Defined in Art. 1(13), second subparagraph, Banking Directive by reference to Art. 1(1), Consolidated Accounts Directive, infra note 46. Subsidiary is, in summary, an undertaking (1) in which a parent (a) has, or controls alone, pursuant to a shareholder agreement, a majority of the shareholders’ or members’ voting rights, or (b) has the right to appoint or remove a majority of the members of the administrative, management or supervisory board and is at the same time a shareholder or a member, or (2) that can be controlled by the parent (the parent “has the right to exercise a dominant influence”) pursuant to a contract

NYDOCS01/1000894.2 3

institution whose parent is a financial holding company.14 The Capital Adequacy Directive expands consolidated supervision to groups including investment firms. 15 Consolidated supervision applies to (1) every investment firm that has a credit institution, an investment firm or another financial institution as a subsidiary or that holds a participation in such entity and (2) every investment firm whose parent is a financial holding company.16 Investment firms are in effect brokers, dealers, investment managers having discretion, and underwriters.17 Only credit institutions, investment firms and financial holding companies can head a group subject to consolidated supervision. Thus, consolidated supervision is not required for credit institutions or investment firms that are subsidiaries of companies that are neither credit institutions, investment firms nor financial holding companies. Financial institutions (other than investment firms) are part of a group subject to consolidated supervision only if they are subsidiaries of credit institutions, investment firms or financial holding companies; they are not part of a group subject to consolidated supervision if they are subsidiaries of other financial institutions that are neither investment firms nor financial holding companies.

Supervision on a consolidated basis of groups that include credit institutions means supervision on the basis of the consolidated financial situation in the following areas: 18 Consolidated calculation of own funds, consolidated computation of the solvency ratio, consolidated control of adequacy of own funds to cover market risks, consolidated control of large exposures and consolidated restriction on investments in the nonbank sector. Supervision on a consolidated basis of groups that include investment firms (but not credit institutions) means supervision on the basis of the consolidated

between the parent and the subsidiary or a provision in the subsidiary’s charter, the parent at the same time being a shareholder or a member. In addition, a subsidiary is any undertaking over which, in the opinion of the competent authorities, a parent effectively exercises a dominant influence.

13 Art. 1(9), Banking Directive (essentially 20% or more of the voting rights or capital; a lower percentage suffices if the investment by creating a durable link between the investor and the target is intended to contribute to the investor’s activities).

14 Art. 52(1) & (2), Banking Directive. Art. 1(21), Banking Directive, as amended by Art. 29(1)(b), Supplementary Supervision Directive, defines financial holding company as a financial institution, the subsidiary undertakings of which are either exclusively or mainly credit institutions or financial institutions, at least one of such subsidiaries being a credit institution, and which is not a mixed financial holding company within the meaning of [the Supplementary Supervision Directive].

15 Art. 7(2) & (3), Council Directive 93/6/EEC of 15 March 1993 on the capital adequacy of investment firms and credit institutions, O.J. Eur. Comm. No. L 141/1 (1993), as amended [herein Capital Adequacy Directive].

16 Art. 7(2) & (3), Capital Adequacy Directive. Financial holding company is defined in Art. 2(8), Capital Adequacy Directive as any financial institution, the subsidiary undertakings of which are either exclusively or mainly credit institutions, investment firms or other financial institutions, at least one of which is a credit institution or an investment firm.

17 Art. 2(2), Capital Adequacy Directive.

18 Art. 52(5) & (6), Banking Directive; Art. 7(2), Capital Adequacy Directive.

NYDOCS01/1000894.2 4

financial situation in the areas mentioned above, except that it does not apply to the restriction on investments in the nonbank sector.19

The Banking Directive hesitates to regulate directly non-EU entities. For this reason, application of the principle of supervision on a consolidated basis to credit institutions whose parents have their head offices in non-EU countries and to credit institutions situated in non-EU countries whose parents (credit institutions or financial holding companies) have their head offices in a Member State shall be made possible by virtue of reciprocal bilateral agreements to be entered into between the competent authorities of the Member States and the non-EU countries concerned.20

The Supplementary Supervision Directive, however, amended the Banking Directive to deal with the situation of an EU-authorized credit institution or investment firm that is a subsidiary of a non-EU credit institution or financial institution but is not subject to consolidated supervision – presumably because no agreement was entered into with the non-EU country of the parent. If an EU-authorized credit institution is a subsidiary of a non-EU credit institution or financial institution, the competent authority shall verify whether the EU-authorized credit institution is subject to consolidated supervision by the home country of the non-EU parent that is equivalent to that governed by the principles laid down in Art. 52, Banking Directive.21 In the absence of such equivalent supervision, Member States shall apply the provisions of Art. 52 Banking Directive to the credit institution by analogy. As an alternative, Member States shall allow their competent authorities to apply other appropriate supervisory techniques which achieve the objectives of the supervision on a consolidated basis.22 The competent authorities which would be responsible for consolidated supervision must agree on those methods; they may, in particular, require the establishment of a financial holding company which has it head office in the European Union, and apply the provision on consolidated supervision to the consolidated position of that financial holding company.23

Insurance groups are subject to a more limited supplementary supervision under the Insurance Group Directive.24 Supplementary supervision applies to any EU-authorized life or non-life insurance undertaking25 that has at least one subsidiary26 that is an EU-authorized life or non-life 19 Art. 7(3), 5th indent, Capital Adequacy Directive that excludes the application of Art. 52(5), second

subparagraph, Banking Directive. Investment firms are not restricted to their investments in the industrial or commercial sector.

20 Art. 25(1), Banking Directive. Art. 25, Banking Directive is not applicable to investment firms, and the Capital Adequacy Directive does not contain similar provisions.

21 Art. 56a, first subparagraph, Banking Directive, added by Art. 29(11), Supplementary Supervision Directive. Art. 56a, Banking Directive also applies to investment firm groups. Art. 7(2) & (3), Capital Adequacy Directive.

22 Art. 56a, fifth subparagraph, Banking Directive, added by Art. 29(11), Supplementary Supervision Directive.

23 Art. 56a, fifth subparagraph, Banking Directive, added by Art. 29(11), Supplementary Supervision Directive.

24 Directive 98/78/EC of the European Parliament and of the Council of 27 October 1998 on the supplementary supervision of insurance undertakings in an insurance group, O.J. Eur. Comm. No. L 330/1 (1998), as amended [herein Insurance Group Directive]. For a discussion of supplementary supervision of insurance groups, see Gruson, Consolidated and Supplementary Supervision, at 75.

25 Art. 1(a), Insurance Group Directive.

NYDOCS01/1000894.2 5

insurance undertaking, reinsurance undertaking,27 or non-EU insurance undertaking,28 or holds a participation29 in any such entity or is linked by a horizontal structure with any such entity.30 Supplementary supervision also applies to every EU-authorized life or non-life insurance undertaking the parent31 of which is an insurance holding company,32 a reinsurance undertaking or a non-EU insurance undertaking.33 Lastly, supplementary supervision applies to every EU-authorized life or non-life insurance undertaking the parent of which is a mixed-activity insurance holding company.34 The supplementary supervision of all insurance groups relates to: intra-group transactions,35 the computation of an adjusted or analogous solvency calculation,36 adequate internal control mechanisms for the production of any data and information relevant for the purposes of such supplementary supervision,37 and the sufficiently good repute and sufficient experience of the management of an insurance holding company.38

26 Art. 1(e), Insurance Group Directive.

27 Art. 1(c), Insurance Group Directive.

28 Art. 1(b), Insurance Group Directive.

29 Art. 1(f), Insurance Group Directive.

30 Art. 2(1), Insurance Group Directive. A horizontal structure exists if there is control in the absence of an equity investment, due to management on a unified basis or cross-membership of governing boards. See Art. 1(g), Insurance Group Directive.

31 Art. 1(d), Insurance Group Directive.

32 Insurance holding company is a parent the main business of which is to acquire and hold participations in subsidiaries, where those subsidiaries are exclusively or mainly EU-authorized insurance undertakings, reinsurance undertakings or non-EU insurance undertakings, at least one of such subsidiaries being an EU-authorized life or non-life insurance undertaking, and which is not a mixed financial holding company within the meaning of the Supplementary Supervision Directive. Art. 1(i), Insurance Group Directive.

33 Art. 2(2), Insurance Group Directive.

34 Art. 2(3), Insurance Group Directive. Mixed-activity insurance holding company is a parent, other than an

EU-authorized insurance undertaking, a non-EU insurance undertaking, a reinsurance undertaking, an insurance holding company or a mixed financial holding company as defined in the Supplementary Supervision Directive, that includes at least one EU-authorized life or non-life insurance undertaking among its subsidiaries. Art. 1(j), Insurance Group Directive.

35 Art. 8(1), Insurance Group Directive.

36 Art. 9(1), referring to Art. 2(1), Insurance Group Directive.

37 Art. 5(1), Insurance Group Directive.

38 Art. 10b, Insurance Group Directive, added by Art. 28(4), Supplementary Supervision Directive.

NYDOCS01/1000894.2 6

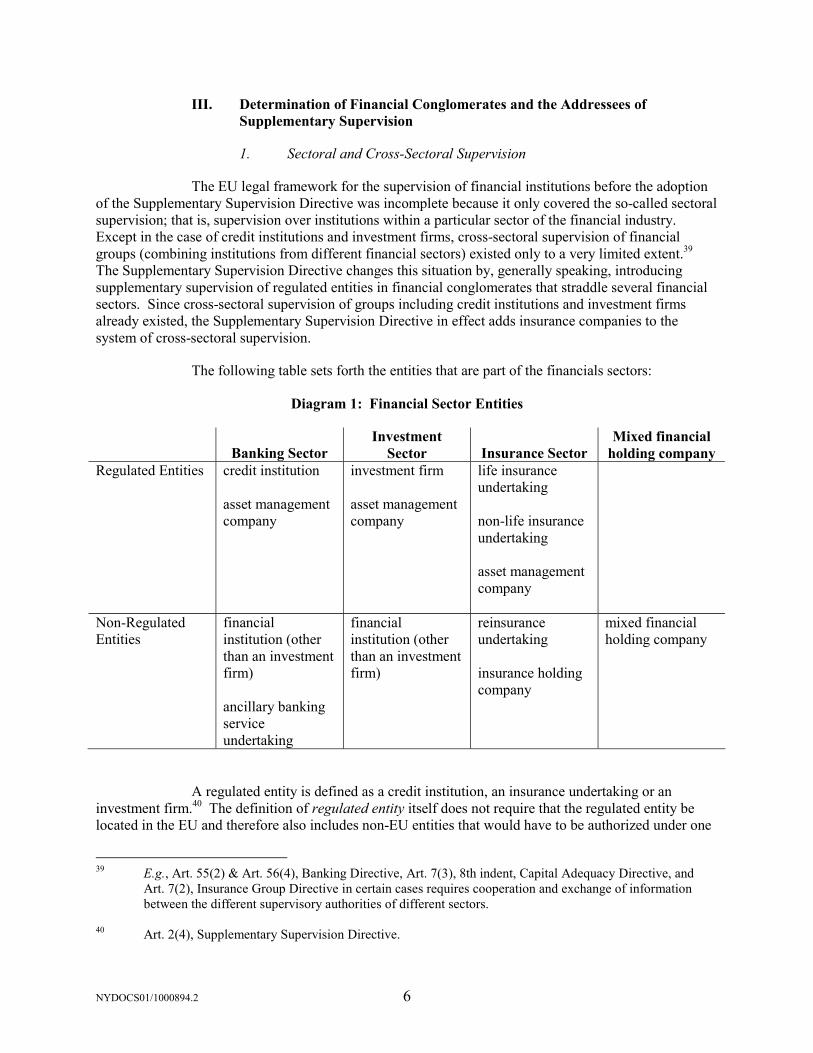

III. Determination of Financial Conglomerates and the Addressees of Supplementary Supervision

1. Sectoral and Cross-Sectoral Supervision

The EU legal framework for the supervision of financial institutions before the adoption of the Supplementary Supervision Directive was incomplete because it only covered the so-called sectoral supervision; that is, supervision over institutions within a particular sector of the financial industry. Except in the case of credit institutions and investment firms, cross-sectoral supervision of financial groups (combining institutions from different financial sectors) existed only to a very limited extent.39 The Supplementary Supervision Directive changes this situation by, generally speaking, introducing supplementary supervision of regulated entities in financial conglomerates that straddle several financial sectors. Since cross-sectoral supervision of groups including credit institutions and investment firms already existed, the Supplementary Supervision Directive in effect adds insurance companies to the system of cross-sectoral supervision.

The following table sets forth the entities that are part of the financials sectors:

Diagram 1: Financial Sector Entities

Banking Sector Investment

Sector Insurance Sector Mixed financial

holding company Regulated Entities credit institution

asset management company

investment firm asset management company

life insurance undertaking non-life insurance undertaking asset management company

Non-Regulated Entities

financial institution (other than an investment firm) ancillary banking service undertaking

financial institution (other than an investment firm)

reinsurance undertaking insurance holding company

mixed financial holding company

A regulated entity is defined as a credit institution, an insurance undertaking or an investment firm.40 The definition of regulated entity itself does not require that the regulated entity be located in the EU and therefore also includes non-EU entities that would have to be authorized under one

39 E.g., Art. 55(2) & Art. 56(4), Banking Directive, Art. 7(3), 8th indent, Capital Adequacy Directive, and

Art. 7(2), Insurance Group Directive in certain cases requires cooperation and exchange of information between the different supervisory authorities of different sectors.

40 Art. 2(4), Supplementary Supervision Directive.

NYDOCS01/1000894.2 7

of the sectoral Directives if they were located in the EU. However, only regulated entities that have obtained an authorization pursuant to one of the sectoral Directives41 are subject to supplementary supervision within the meaning of the Supplementary Supervision Directive.42 Such an authorization is only required for undertakings that are located in the EU.43 Thus, supplementary supervision only applies to regulated entities that are established and authorized in the EU, except that EU-regulated entities with a parent outside the EU are not subject to supplementary supervision. As further discussed below under V, if the parent of an EU-regulated entity has its head office in a country outside the EU, the Supplementary Supervision Directive yields in favor of the supervision by the home country of the parent if that supervision is equivalent to the supervision under the Supplementary Supervision Directive. Only if the parent’s home country does not have an equivalent supervision, are the EU-regulated entities subject to analogous or appropriate supplementary supervision under the Supplementary Supervision Directive.

2. Financial Conglomerates

The Supplementary Supervision Directive applies to certain EU-regulated entities (credit institutions, insurance undertakings and investment firms) that have obtained an authorization pursuant to one of the sectoral Directives.44 If such entities are part of a financial conglomerate, they may be subject

41 Art. 6, First Council Directive 73/239/EEC of 24 July 1973 on the coordination of laws, regulations and

administrative provisions relating to the taking-up and pursuit of the business of direct insurance other than life assurance, O.J. Eur. Comm. No. L 228/3 (1973), as amended [herein First Non-Life Insurance Directive]; Art. 6, First Council Directive 79/267/EEC of 5 March 1979 on the coordination of laws, regulations and administrative provisions relating to the taking up and pursuit of the business of direct life assurance, O.J. Eur. Comm. No. L 63/1 (1979), as amended [herein First Life Insurance Directive]; Art. 3(1), Council Directive 93/22/EEC of 10 May 1993 on investment services in the securities field, O.J. Eur. Comm. No. L 141/27 (1993), as amended [herein Investment Services Directive]; Art. 5(1), Directive 2004/39/EC of the European Parliament and of the Council of 21 April 2004 on markets in financial instruments amending Council Directives 85/611/EEC and 93/6/EEC and Directive 2000/12/EC of the European Parliament and of the Council and repealing Council Directive 93/22/EEC [herein Financial Instruments Markets Directive]; Art. 4, Banking Directive.

42 See Art. 1 & Art. 5(1), Supplementary Supervision Directive. The Supplementary Supervision Directive uses the term regulated entity with two meanings: As defined in Art. 2(4), Supplementary Supervision Directive, the term also includes non-EU-authorized entities. As used in Art. 1, Supplementary Supervision Directive, the term regulated entities only refers to entities which have obtained an authorization under a sectoral Directive. The Supplementary Supervision Directive calls EU-authorized regulated entities regulated entities referred to in Article 1. See, e.g., Art. 5(1), Supplementary Supervision Directive. Regulated entities referred to in Article 1 are herein sometimes called EU-regulated entities and regulated entities that are not EU-regulated entities are herein sometimes called non-EU-regulated entities.

43 Art. 6, First Non-Life Insurance Directive and Art. 6, First Life Insurance Directive require an authorization of insurance undertakings having established their head office within the territory of a Member State. Art. 3(1), in connection with Art. 1(6), Investment Services Directive states that only investment firms having their registered office or head office in a Member State are subject to authorization. Art. 5(1), in conjunction with Art. 4(20), Financial Instruments Markets Directive provides that the Member State in which the registered office is situated shall grant the necessary authorization for an investment firm. Although Art. 4, Banking Directive provides for the authorization of credit institutions prior to commencement of activities in a Member State without expressly referring to the head office or registered office of that credit institution, it is clear from the context of the Banking Directive and Arts. 23–25, Banking Directive (governing relations with third countries) that only credit institutions established under the laws of a Member State are subject to authorization pursuant to Art. 4, Banking Directive.

44 Art. 5(1), Supplementary Supervision Directive.

NYDOCS01/1000894.2 8

to supplementary prudential supervision.45 In order to determine whether a regulated entity is subject to supplementary supervision, three inquiries must be made: first, whether the regulated entity is part of a group; second, whether the group meets the requirements of a financial conglomerate; and third, whether the regulated entity is one that is the addressee of supplementary supervision.

a. Definition of Group

A group is determined (a) by a parent-subsidiary relationship, 46 (b) by a relationship based on a participation, 47 or (c) by a horizontal structure. 48

Whereas, generally speaking, a subsidiary is an undertaking in which a shareholder (the parent) has a majority of the voting rights or the right to exercise a controlling influence, and a participation is an equity investment of 20 percent or more, a horizontal structure exists without an equity relationship if undertakings are managed on a unified basis pursuant to a contract or charter provision or if the administration, management or supervisory bodies of both undertakings consist for the major part of the same persons. A horizontal structure is a case of control without equity investment.

A U.S. observer would say that a group in the meaning of the Supplementary Supervision Directive is determined by concepts very similar to the U.S. Bank Holding Company Act’s concept of control which determines whether a parent-subsidiary relationship exists.49

45 Art. 1, Supplementary Supervision Directive.

46 Parent undertaking and subsidiary undertaking are defined in Art. 2(9) & (10), Supplementary Supervision

Directive by reference to Art. 1(1) & (2), Seventh Council Directive 83/349/EEC of 13 June 1983 based on the Article 54(3)(g) of the Treaty on consolidated accounts, O.J. Eur. Comm. No. L 193/1 (1983), as amended [herein Consolidated Accounts Directive]. The definitions of parent and subsidiary are identical with the definitions of such terms in the Banking Directive, except that the Supplementary Supervision Directive (but not the Banking Directive) permits Member States to consider an undertaking as a parent undertaking if it has the power to exercise, or actually exercises, a dominant influence or control over another undertaking (a subsidiary) or manages another undertaking (the subsidiary) and the parent on a unified basis. See Art. 1(2), Consolidated Accounts Directive that is included in the subsidiary/parent definition of the Supplementary Supervision Directive, but not in those definitions of the Banking Directive.

47 Participation is defined in Art. 2(11), Supplementary Supervision Directive, referring to Art. 17, first sentence, Fourth Council Directive 78/660/EEC of 25 July 1978 based on Art. 54(3)(g) of the Treaty on the annual accounts of certain types of companies, O.J. Eur. Comm. No. L 222/11 (1978), as amended [herein Annual Accounts Directive]. A participation is (1) a right in the capital of other undertakings which “by creating a durable link with those [other] undertakings, are intended to contribute to the company’s [the holder of the participation] activities”, or (2) the ownership, directly or indirectly, of 20 percent or more of the voting rights or capital of another undertaking.

48 Art. 2(12), Supplementary Supervision Directive, referring to Art. 12(1), Consolidated Accounts Directive.

49 Section 2, Bank Holding Company Act of 1956, as amended [herein BHCA], 12 U.S.C. § 1841 (2000). See Michael Gruson, Nonbanking Activities of Foreign Banks Operating in the United States [herein Gruson, Nonbanking Activities], § 9.03 in Michael Gruson & Ralph Reisner (eds.), REGULATION OF FOREIGN BANKS, vol. 1 (4th ed., 2003).

NYDOCS01/1000894.2 9

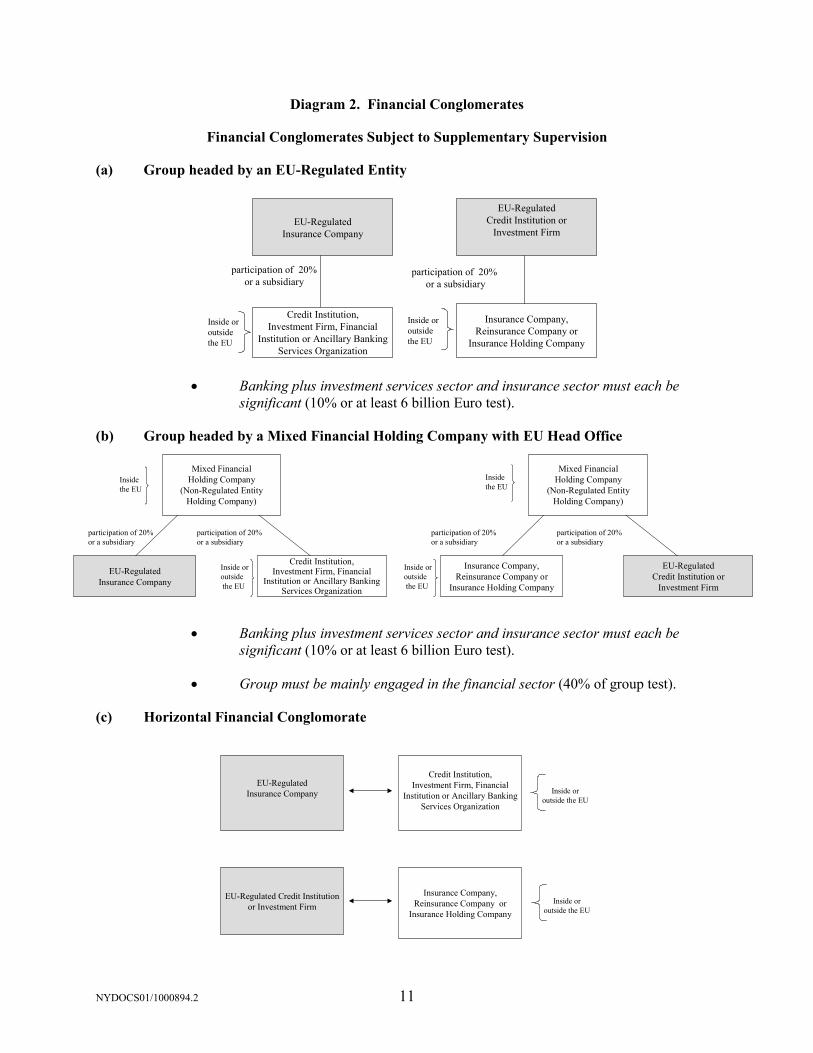

b. Definition of Financial Conglomerate

A group constitutes a financial conglomerate if it meets certain conditions. For purposes of determining a financial conglomerate, the Supplementary Supervision Directive distinguishes between groups that are headed by an EU- regulated entity and groups that are not headed by an EU-regulated entity (but by a non-EU regulated entity or by a non-regulated entity).

In both cases (financial conglomerate headed by an EU-regulated entity and financial conglomerate not so headed), the activities of the entities in the insurance sector and the activities of the entities in the banking and investment services sector (taken together) must be significant (i.e., based on ratios of balance sheets and solvency ratio requirements, each financial sector must represent at least 10 percent of the group or the balance sheets of the smallest sector in the group must exceed € 6 billion).50 A group that is not headed by an EU-regulated entity only qualifies as a financial conglomerate if the group’s activities mainly occur in the financial sector (i.e., based on the balance sheets, the financial sector entities must represent at least 40 percent of the group). On the other hand, a group that is headed by an EU-regulated entity qualifies as a financial conglomerate even though its activities do not mainly occur in the financial sector.51

The Supplementary Supervision Directive introduces and defines the term mixed financial holding company to cover financial conglomerates headed by a non-regulated entity holding company. In fact, every non-regulated entity head of a financial conglomerate by definition is a mixed financial holding company.52 The Supplementary Supervision Directive could have called such entities “non-regulated entity holding companies”. The mixed financial holding company could be a non-regulated financial sector entity, such as a financial institution other than an investment firm (a mere holding company without its own activities would likely be a financial institution) or a reinsurance undertaking, or it could be a commercial or industrial company. The definitions of financial conglomerate and mixed financial holding company do not require that the head of the financial conglomerate or the mixed financial holding company must be established or have its head office in the EU. However, if a financial conglomerate headed by a mixed financial holding company is to be covered by supplementary supervision, the mixed financial holding company must be located in the EU.53 In the same way, if the financial conglomerate is headed by a regulated entity, it is subject to supplementary supervision only if the regulated entity is an EU-regulated entity.54 A financial conglomerate headed by a non-EU-regulated entity and a financial conglomerate headed by a mixed financial holding company having its head office outside the EU are still financial conglomerates but the regulated entities in those financial conglomerates are not subject to supplementary supervision; as discussed below under V, they may, however, be subject to equivalent supplementary supervision by the home country of the non-EU-

50 Art. 2(14)(e), Supplementary Supervision Directive.

51 Art. 2(14)(c), Supplementary Supervision Directive.

52 Compare Art. 2(15) with Art. 5(2)(b), Supplementary Supervision Directive. If the head of a financial conglomerate is a non-EU-regulated entity, it is not a mixed financial holding company. See Art. 5(3), Supplementary Supervision Directive.

53 See Art. 5(2)(b), Supplementary Supervision Directive.

54 See Art. 2(14), in connection with Art. 5(2), Supplementary Supervision Directive. Art. 5(2)(a), Supplementary Supervision Directive refers to regulated entities in Art. 5(1), Supplementary Supervision Directive which covers only EU-authorized regulated entities (regulated entities referred to in Art. 1, Supplementary Supervision Directive).

NYDOCS01/1000894.2 10

regulated entity or the mixed financial holding company or to analogous or appropriate supplementary supervision by a Member State under the Supplementary Supervision Directive.55

The following table sets forth the entities that are part of a financial conglomerate:

55 See Art. 5(3) & Art. 18, Supplementary Supervision Directive. The Supplementary Supervision Directive

does not address the case of a horizontal group of which one member has its head office outside the EU.

NYDOCS01/1000894.2 11

Diagram 2. Financial Conglomerates

Financial Conglomerates Subject to Supplementary Supervision

(a) Group headed by an EU-Regulated Entity

EU-Regulated Insurance Company

Credit Institution,Investment Firm, Financial

Institution or Ancillary Banking Services Organization

EU-Regulated Credit Institution or

Investment Firm

Insurance Company,Reinsurance Company or

Insurance Holding Company

Inside or outside the EU

Inside or outside the EU

participation of 20% or a subsidiary

participation of 20% or a subsidiary

• Banking plus investment services sector and insurance sector must each be significant (10% or at least 6 billion Euro test).

(b) Group headed by a Mixed Financial Holding Company with EU Head Office

Mixed FinancialHolding Company

(Non-Regulated EntityHolding Company)

EU-Regulated Insurance Company

Credit Institution,Investment Firm, Financial

Institution or Ancillary Banking Services Organization

Inside or outsidethe EU

Mixed FinancialHolding Company

(Non-Regulated EntityHolding Company)

Insurance Company,Reinsurance Company or

Insurance Holding Company

EU-Regulated Credit Institution or

Investment Firm

Inside or outsidethe EU

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

Insidethe EU

Insidethe EU

• Banking plus investment services sector and insurance sector must each be

significant (10% or at least 6 billion Euro test).

• Group must be mainly engaged in the financial sector (40% of group test).

(c) Horizontal Financial Conglomorate

EU-Regulated Insurance Company

EU-Regulated Credit Institution or Investment Firm

Credit Institution,Investment Firm, Financial

Institution or Ancillary Banking Services Organization

Insurance Company,Reinsurance Company or

Insurance Holding CompanyInside or

outside the EU

Inside or outside the EU

NYDOCS01/1000894.2 12

• Banking plus investment services sector and insurance sector must each be significant (10% or at least 6 billion Euro test).

• Group must be mainly engaged in the financial sector (40% of group test).

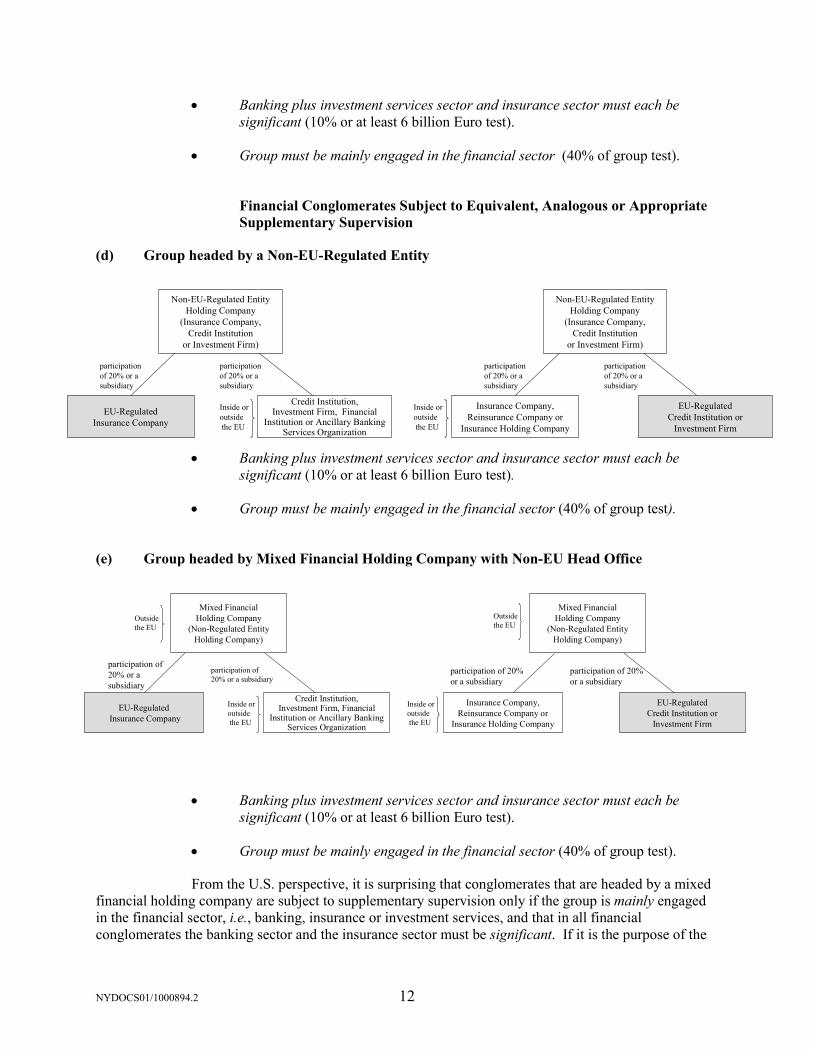

Financial Conglomerates Subject to Equivalent, Analogous or Appropriate Supplementary Supervision

(d) Group headed by a Non-EU-Regulated Entity

Non-EU-Regulated Entity Holding Company

(Insurance Company,Credit Institution

or Investment Firm)

EU-Regulated Insurance Company

Credit Institution, Investment Firm, Financial

Institution or Ancillary Banking Services Organization

Inside or outsidethe EU

Non-EU-Regulated Entity Holding Company

(Insurance Company,Credit Institution

or Investment Firm)

Insurance Company,Reinsurance Company or

Insurance Holding Company

EU-Regulated Credit Institution or

Investment Firm

Inside or outsidethe EU

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

• Banking plus investment services sector and insurance sector must each be

significant (10% or at least 6 billion Euro test).

• Group must be mainly engaged in the financial sector (40% of group test).

(e) Group headed by Mixed Financial Holding Company with Non-EU Head Office

Mixed FinancialHolding Company

(Non-Regulated EntityHolding Company)

EU-Regulated Insurance Company

Credit Institution,Investment Firm, Financial

Institution or Ancillary Banking Services Organization

Inside or outsidethe EU

Mixed FinancialHolding Company

(Non-Regulated EntityHolding Company)

Insurance Company,Reinsurance Company or

Insurance Holding Company

EU-Regulated Credit Institution or

Investment Firm

Inside or outsidethe EU

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

participation of 20% or a subsidiary

Outsidethe EU

Outsidethe EU

• Banking plus investment services sector and insurance sector must each be

significant (10% or at least 6 billion Euro test).

• Group must be mainly engaged in the financial sector (40% of group test).

From the U.S. perspective, it is surprising that conglomerates that are headed by a mixed financial holding company are subject to supplementary supervision only if the group is mainly engaged in the financial sector, i.e., banking, insurance or investment services, and that in all financial conglomerates the banking sector and the insurance sector must be significant. If it is the purpose of the

NYDOCS01/1000894.2 13

Supplementary Supervision Directive to protect regulated entities, the relative size of such regulated entities should not be a relevant factor. However, the Supplementary Supervision Directive goes further than the rules on consolidated supervision. The rules on consolidated supervision require consolidated supervision for credit institutions in which another credit institution holds a participation or that are subsidiaries of another credit institution or of a financial holding company, i.e., a company the subsidiaries of which are exclusively or mainly credit institutions or financial institutions and that has at least one credit institution subsidiary.56 Consolidated supervision does not extend to a group headed by a mixed-activity holding company, which is defined as a parent other than a financial holding company, a credit institution or a mixed financial holding company, whose subsidiaries include at least one credit institution.57 Thus, neither the proverbial steel company that acquires a bank nor the acquired bank is subject to consolidated supervision under EU law because the steel company is not a financial holding company.

However, if the steel company is located in the EU and acquires a bank and an insurance company, and their combined balance sheet total of both amounts to 40 percent of the balance sheet total of the group, the steel company would be a mixed financial holding company heading a financial conglomerate and the financial conglomerate would be subject to supplementary supervision under the Supplementary Supervision Directive. A holding company without its own business activities whose principal activity consists of acquiring holdings in industrial and financial companies is a financial institution58 and if the subsidiaries of such financial institution mainly consist of credit institutions or financial institutions, it is a financial holding company59 and the group headed by it is subject to consolidated supervision.60 If the subsidiaries do not mainly consist of credit or financial institutions, it is not a financial holding company subject to consolidated supervision. If the above holding company holds a credit institution and an insurance company, one of which is a subsidiary, and both of which are significant and if the group’s activities mainly (based on the 40 percent test) consist of financial sector activities, it is a mixed financial holding company that heads a financial conglomerate subject to supplementary supervision. If its activities do not consist mainly of financial sector activities, it is neither subject to consolidated nor to supplementary supervision.61

c. Discretionary Expansion of Financial Conglomerate

The Supplementary Supervision Directive gives the competent authorities discretion to apply supplementary supervision to groups that do not meet the definition of financial conglomerate or

56 Art. 52(1) & (2), Banking Directive.

57 Art. 1(22), Banking Directive.

58 Art. 1(5), Banking Directive.

59 Art. 1(21), Banking Directive.

60 Art. 52(2), Banking Directive.

61 It must be noted, however, that the “mainly” test for purposes of the definition of a financial holding company, differs from the “mainly” test for purposes of the definition of a mixed financial holding company: a financial holding company must exclusively or mainly hold credit institution or financial institution subsidiaries, whereas a group headed by a mixed financial holding company must mainly be engaged in the financial sector based on the 40 percent test.

NYDOCS01/1000894.2 14

even the definition of group and to carry out supplementary supervision “as if they constitute a financial conglomerate”.62

The competent authorities may exercise supplementary supervision over regulated entities that are controlled by another entity or in which another entity has a capital investment, even though the relationship does not qualify as a group or as a financial conglomerate. Regulated entities in such quasi financial conglomerates are, in the discretion of the relevant competent authorities, subject to supplementary supervision if (1) at least one of the regulated entities is an EU-regulated entity, (2) at least one of the entities in the quasi financial conglomerate is within the insurance sector and at least one is within the banking or investment services sector, and (3) the consolidated and/or aggregated activities of the entities in the quasi financial conglomerate within the insurance sector and the consolidated and/or aggregated activities of the entities within the banking and investment services sector are each significant.63

d. Determination of Financial Conglomerate

The Supplementary Supervision Directive does not impose on financial conglomerates a duty to report to or file with any supervisory authority the fact that they are financial conglomerates. The competent authorities themselves must make that determination. If a competent authority is of the opinion that a regulated entity authorized by it is a member of a group that may be a financial conglomerate, which has not already been identified according to the Supplementary Supervision Directive, the competent authority shall communicate its view to the other competent authorities concerned. The coordinator, as discussed below, shall inform the parent of the group (or in the absence of a parent, the regulated entity with the largest balance sheet held in the most important financial sector in the group) that the group has been identified as a financial conglomerate and of the appointment of the coordinator.64 The coordinator shall also inform the competent authorities that have authorized regulated entities in the group and the competent authorities of the Member States in which the mixed financial holding company has its head office, as well as the EU Commission.65

The high degree of discretion given to the Member States and their supervisory authorities in determining whether a group or a financial conglomerate exists could lead to substantial differences among the Member States in the determination of whether supplementary supervision applies. This would not only create legal uncertainties but could also cause competitive distortions.

3. Undertakings in a Financial Conglomerate that Are the Addressees of Supplementary Supervision

The Supplementary Supervision Directive does not envision that all companies in a financial conglomerate be subject to supplementary supervision and the scope of supplementary supervision differs among certain categories of companies in a financial conglomerate. The Supplementary Supervision Directive distinguishes between entities that are the addressees of supplementary supervision, entities that are subject to certain obligations under the Supplementary

62 Art. 5(4), first subparagraph, Supplementary Supervision Directive.

63 Art. 5(4), second subparagraph, Supplementary Supervision Directive.

64 Art. 4(2), Supplementary Supervision Directive.

65 Art. 4(2), Supplementary Supervision Directive.

NYDOCS01/1000894.2 15

Supervision Directive and entities that are only indirectly affected by the Supplementary Supervision Directive.

The Supplementary Supervision Directive refers to entities that are the addressees of the supplementary supervision as entities that are “subject to supplementary supervision at the level of the financial conglomerate”.66 Only certain EU-regulated entities [herein the Responsible Entities] are “subject to supplementary supervision at the level of the financial conglomerate”:

• every EU-regulated entity that is at the head of a financial conglomerate,

• every EU-regulated entity, whose parent undertaking is a mixed financial holding company having its head office in the EU, and

• every EU-regulated entity linked with another financial sector entity by a relationship of a horizontal group, that is, every EU-regulated entity in a horizontal financial conglomerate.

These Responsible Entities must verify compliance with the requirements of supplementary supervision and are responsible for compliance by the financial conglomerate. In particular, the Responsible Entities must submit reports to the coordinator.67 If a financial conglomerate is headed by an EU-regulated entity, only that entity (and not the other regulated entities in the financial conglomerate) must meet the requirements that must be met “at the level of the financial conglomerate”. In this case supervision “on the level of the financial conglomerate” means supervision on the holding company level. On the other hand, if a financial conglomerate is headed by a mixed financial holding company having its head office in the EU, each EU-regulated entity in the financial conglomerate must meet the requirements that must be met “at the level of the financial conglomerate”.68

The Supplementary Supervision Directive imposes certain obligations on all regulated entities in a financial conglomerate in order to make supplementary supervision at the level of the financial conglomerate possible.69 However, to the extent the regulated entities are non-EU-regulated entities, the supplementary supervision at the level of the financial conglomerate does not imply that the competent authorities play a supervisory role with respect to such non-EU-regulated entities.70 Furthermore, the Supplementary Supervision Directive assigns duties and obligations in connection with supplementary supervision at the level of the financial conglomerate to mixed financial holding companies.71 Again, this does not imply that the competent authorities play a supervisory role with respect to mixed financial holding companies.72

66 Art. 5(2), Supplementary Supervision Directive. See, e.g., Arts. 6(2), 7(2) & 9(1), Supplementary

Supervision Directive.

67 Arts. 6(2), 7(2) & 8(2), Supplementary Supervision Directive.

68 Art. 5(2)(a) & (b), Supplementary Supervision Directive.

69 See, e.g., Arts. 6(2), 7(2), 8(2) & 9(1), Supplementary Supervision Directive.

70 Art. 5(5), Supplementary Supervision Directive.

71 See, e.g., Art. 6(2), fourth and fifth subparagraphs, Art. 7(2) & Art. 8(2), second subparagraph, Supplementary Supervision Directive.

72 See Art. 5(5), Supplementary Supervision Directive.

NYDOCS01/1000894.2 16

Finally, supplementary supervision of a financial conglomerate will indirectly affect all entities in a financial conglomerate, including non-EU-regulated entities, non-regulated entities and the mixed financial holding company in the financial conglomerate. For instance, intra-group transactions73 and risk concentrations74 are defined to include relations between regulated entities (EU-regulated or non-EU-regulated) in a financial conglomerate and other entities or undertakings in the financial conglomerate. For purposes of calculating the capital adequacy requirements of a financial conglomerate, mixed financial holding companies, non-EU-regulated entities and even non-regulated financial sector entities are included.75 This does not imply that the competent authorities play a supervisory role with respect to those unregulated entities.76

Not all EU-regulated entities in a financial conglomerate are subject to supplementary supervision. EU-regulated entities that are members of a financial conglomerate headed by an EU-regulated entity77 are not addressees of supplementary supervision, although they are included in the supplementary supervision of the EU-regulated entity head of the financial conglomerate. EU-regulated entities that are members of a financial conglomerate headed by a mixed financial holding company are subject to supplemental supervision only if the mixed financial holding company has its head office in the EU.78

EU-regulated entities in a financial conglomerate headed by a non-EU-regulated entity or by a mixed financial holding company, that has its head office outside the EU, are not at all subject to supplementary supervision.79 If the parent undertaking of an EU-regulated entity is a regulated entity having its head office outside the EU or is a mixed financial holding company having its head office outside the EU, the EU-regulated entity, as discussed below under V, is either subject to equivalent supervision by the home country of the parent or subject to analogous or appropriate supplementary supervision by a Member State pursuant to Art. 18, Supplementary Supervision Directive.80

Where a financial conglomerate is a subgroup of another financial conglomerate (the main financial conglomerate), Member States may apply the provisions of the Supplementary Supervision Directive relating to supplementary supervision81 only to regulated entities within the main financial conglomerate and not to the subgroup.82 The nonfinancial activities of a nonregulated entity heading a

73 Art. 2(18), Supplementary Supervision Directive.

74 Art. 2(19), Supplementary Supervision Directive.

75 Art. 6(3), Supplementary Supervision Directive.

76 Art. 5(5), Supplementary Supervision Directive.

77 Art. 5(2)(a), Supplementary Supervision Directive.

78 See Art. 5(2), Supplementary Supervision Directive.

79 Art. 2(15), Supplementary Supervision Directive.

80 Art. 5(3) & Art. 18, Supplementary Supervision Directive

81 Arts. 6–17, Supplementary Supervision Directive.

82 Art. 5(2), second subparagraph, Supplementary Supervision Directive.

NYDOCS01/1000894.2 17

group could have the effect that the group does not meet the financial conglomerate tests.83 In that case, one has to determine whether the non-qualifying group comprises subgroups that qualify as financial conglomerates.84

In order to avoid possible moral hazards,85 the Supplementary Supervision Directive emphasizes that the exercise of supplementary supervision at the level of the financial conglomerate shall not imply that the competent authorities are required to play a supervisory role in relation to mixed financial holding companies, unregulated entities or non-EU-regulated entities in a financial conglomerate, on a stand-alone basis, even though such entities are affected by the supplementary supervision.86 However, certain entities in a financial conglomerate that are not EU-regulated entities are subject to supervision in their relations with the EU-regulated entities, for instance, in the computation of capital adequacy at the level of the financial conglomerate or in the evaluation of intra-group transactions.

The Supplementary Supervision Directive requires the inclusion of asset management companies in the sectoral and supplementary supervision. The Supplementary Supervision Directive provides that Member States shall include asset management companies in the scope of consolidated supervision of credit institutions and investment firms, and/or in the scope of supplementary supervision of insurance undertakings in an insurance group, and – where the group is a financial conglomerate – in the scope of supplementary supervision within the meaning of the Supplementary Supervision Directive.87 Asset management companies that are part of a financial conglomerate must be regarded as regulated entities.88

IV. Supplementary Supervision

The Supplementary Supervision Directive introduces a series of rules with regard to the supplementary supervision of regulated entities in a financial conglomerate. They relate in particular to capital adequacy, intra-group transactions and risk concentration, and to the management. The Supplementary Supervision Directive also requires that for each financial conglomerate a single coordinator be appointed from among the competent authorities of the Member States concerned who

83 See Art. 2(14)(c), Supplementary Supervision Directive. The entity heading the group is not a mixed

financial holding company if the group does not constitute a financial conglomerate. See Art. 2(15), Supplementary Supervision Directive.

84 The prohibition of separate regulation of subgroups set forth in Art. 5(2), second subparagraph, Supplementary Supervision Directive does not apply in that case because the subgroup is not a subgroup of another financial conglomerate.

85 See 2001 Explanatory Memorandum, at 6, sub 2, Art. 4, and Tripartite Report, at 36, sub no. 96 (the impression that the activities of unregulated entities in the financial conglomerate are in some way being monitored or supervised, even if only informally, creates a moral hazard).

86 Art. 5(5) & Art. 12(4), Supplementary Supervision Directive.

87 Art. 30, first and second subparagraphs, Supplementary Supervision Directive.

88 Art. 30, third subparagraph, Supplementary Supervision Directive.

NYDOCS01/1000894.2 18

shall be responsible for coordination and exercise of supplementary supervision.89 The competent authorities are also required to cooperate and exchange information.90

It must be emphasized that supplementary supervision does not mean supervision on a consolidated basis like the supervision provided by some of the sectoral rules. The Supplementary Supervision Directive follows a so-called “solo-plus” approach to supervision. The basis of supervision is the supervision of individual group entities on a solo basis by their respective sectoral regulators. The solo supervision of individual entities is complemented by a general quantitative assessment of the group as a whole and by a quantitative group-wide assessment of the adequacy of capital.91 The Supplementary Supervision Directive does not require any additional consolidation of the accounts of the financial conglomerate as a whole if existing Directives do not impose such consolidation.

1. Capital Adequacy

One of the most important issues regarding the supervision of financial conglomerates is the supervision of the group’s financial condition. Therefore, Article 6 and Annex I of the Supplementary Supervision Directive require the competent authorities to exercise supplementary supervision of the capital adequacy of the regulated entities in a financial conglomerate.92 Eliminating any inappropriate intra-group creation of own funds,93 such as double or multiple gearing,94 or excessive leveraging is the major goal of such supplementary group-wide capital adequacy requirements.95 In such situations, the same own funds are used simultaneously as a buffer more than once – to cover the capital requirements of the parent company, as well as those of a subsidiary (and possibly also those of a subsidiary of a subsidiary).96 Thus, the Member States must require regulated entities in a financial conglomerate to ensure that there are own funds at the level of the financial conglomerate that are always at least equal to the capital adequacy requirements as calculated in accordance with Annex I.97 That means that all

89 Art. 10 & Art. 11, Supplementary Supervision Directive.

90 Art. 12, Supplementary Supervision Directive.

91 Tripartite Report, at 17, sub no. 43.

92 Art. 6(1), Supplementary Supervision Directive.

93 Annex I, sub I, 2(i), Supplementary Supervision Directive.

94 Double gearing occurs whenever one entity holds regulatory capital issued by another entity within the

same group and the issuer is allowed to count the capital in its own balance sheet; multiple gearing occurs when the dependant in the previous instance itself down streams regulatory capital to a third-tier entity, and the parent’s externally generated capital is geared up a third time. Annex I, sub I, 2(i), Supplementary Supervision Directive, refers to multiple gearing as the multiple use of elements eligible for the calculation of own funds at the level of the financial conglomerate. See Joint Forum Report, Capital Adequacy Principles Paper, at 13, sub no. 18.

95 See 2001 Explanatory Memorandum, at 4, sub 1(b). The Joint Forum Report, Capital Adequacy Principles Paper, at 14, sub no. 23, defines excessive leverage as situations where a parent issues debt (or other instruments not acceptable as regulatory capital in the downstream entity) and down streams the proceeds as equity or other forms of regulatory capital to its regular subsidiaries.

96 Tripartite Report, at 17, sub no. 44. 97 Art. 6(2), first subparagraph, in connection with Art. 5(2), Supplementary Supervision Directive.

NYDOCS01/1000894.2 19

Responsible Entities in a financial conglomerate must see to it that at the level of the financial conglomerate, the capital adequacy requirements calculated in accordance with Annex I are met. In addition to the regulated entities in a financial conglomerate, certain specifically mentioned nonregulated financial sector entities in the financial conglomerate that may not be subject to capital adequacy requirements on a stand-alone basis must nonetheless be included for the purpose of calculating capital adequacy at the level of the financial conglomerate.98 The solvency requirements for nonregulated financial sector entities that are not included in the sectoral solvency requirement computation are computed on a notional basis.99

The solvency requirements for each separate financial sector represented in a financial conglomerate continue to be covered by own funds elements in accordance with the corresponding sectoral rules.100 In case of a deficit of own funds at the financial conglomerate level, only own funds elements that are eligible according to each of the sectoral rules (cross-sector capital) shall qualify for the verification of the compliance with the solvency requirements at the financial conglomerate level.101

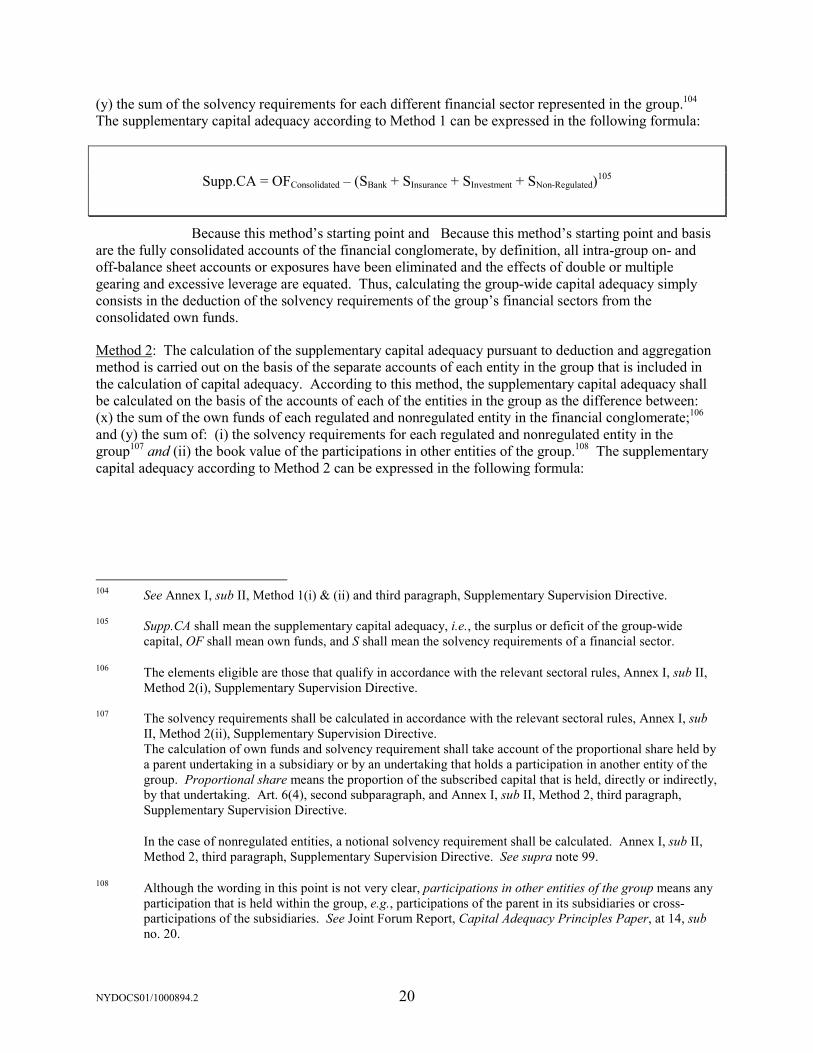

a. Methods for Calculating the Solvency Position

Annex I sets forth three different methods for calculating the solvency position on the level of a financial conglomerate. The competent authorities or the coordinator have the authority to choose which method shall be applied to a financial conglomerate102 and they may also apply a combination of the three methods.103 These methods are (1) accounting consolidation, (2) deduction and aggregation, and (3) requirement deduction.

Method 1: Accounting consolidation uses the consolidated accounts as a basis for calculating the supplementary capital adequacy. Thus, it is only applicable for consolidated groups. According to this method, the supplementary capital adequacy shall be calculated as the difference between: (x) the own funds of the financial conglomerate calculated on the basis of the consolidated position of the group, and

98 Art. 6(3), Supplementary Supervision Directive.

99 See Annex I, sub II, Method 1, fourth paragraph, Method 2, third paragraph, and Method 3, third paragraph,

Supplementary Supervision Directive. Notional solvency requirement means the capital requirement with which such an entity would have to comply under the relevant sectoral rules as if it were a regulated entity of that particular financial sector; a mixed financial holding company shall be treated according to the sectoral rules of the most important financial sector in the financial conglomerate. In the case of asset management companies, solvency requirements means the capital requirement set out in Art. 5a(1)(a), Council Directive 85/611/EEC of 20 December 1985 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS), O.J. Eur. Comm. No. L 375/3 (1985), as amended [herein UCITS Directive]. Annex I, sub I, 2(ii), last paragraph, Supplementary Supervision Directive.

100 Annex I, sub I, 2(ii), first paragraph, Supplementary Supervision Directive.

101 Annex I, sub I, 2(ii), first and second paragraphs, Supplementary Supervision Directive.

102 It would have been desirable to leave the choice of the calculation method to the financial conglomerate in order to give companies more flexibility.

103 See Annex I, second and third paragraphs, and Annex I, sub II, Method 4, Supplementary Supervision Directive.

NYDOCS01/1000894.2 20

(y) the sum of the solvency requirements for each different financial sector represented in the group.104 The supplementary capital adequacy according to Method 1 can be expressed in the following formula:

Supp.CA = OFConsolidated – (SBank + SInsurance + SInvestment + SNon-Regulated)105

Because this method’s starting point and Because this method’s starting point and basis are the fully consolidated accounts of the financial conglomerate, by definition, all intra-group on- and off-balance sheet accounts or exposures have been eliminated and the effects of double or multiple gearing and excessive leverage are equated. Thus, calculating the group-wide capital adequacy simply consists in the deduction of the solvency requirements of the group’s financial sectors from the consolidated own funds.

Method 2: The calculation of the supplementary capital adequacy pursuant to deduction and aggregation method is carried out on the basis of the separate accounts of each entity in the group that is included in the calculation of capital adequacy. According to this method, the supplementary capital adequacy shall be calculated on the basis of the accounts of each of the entities in the group as the difference between: (x) the sum of the own funds of each regulated and nonregulated entity in the financial conglomerate;106 and (y) the sum of: (i) the solvency requirements for each regulated and nonregulated entity in the group107 and (ii) the book value of the participations in other entities of the group.108 The supplementary capital adequacy according to Method 2 can be expressed in the following formula:

104 See Annex I, sub II, Method 1(i) & (ii) and third paragraph, Supplementary Supervision Directive.

105 Supp.CA shall mean the supplementary capital adequacy, i.e., the surplus or deficit of the group-wide

capital, OF shall mean own funds, and S shall mean the solvency requirements of a financial sector.

106 The elements eligible are those that qualify in accordance with the relevant sectoral rules, Annex I, sub II, Method 2(i), Supplementary Supervision Directive.

107 The solvency requirements shall be calculated in accordance with the relevant sectoral rules, Annex I, sub II, Method 2(ii), Supplementary Supervision Directive.

The calculation of own funds and solvency requirement shall take account of the proportional share held by a parent undertaking in a subsidiary or by an undertaking that holds a participation in another entity of the group. Proportional share means the proportion of the subscribed capital that is held, directly or indirectly, by that undertaking. Art. 6(4), second subparagraph, and Annex I, sub II, Method 2, third paragraph, Supplementary Supervision Directive.

In the case of nonregulated entities, a notional solvency requirement shall be calculated. Annex I, sub II, Method 2, third paragraph, Supplementary Supervision Directive. See supra note 99.

108 Although the wording in this point is not very clear, participations in other entities of the group means any participation that is held within the group, e.g., participations of the parent in its subsidiaries or cross-participations of the subsidiaries. See Joint Forum Report, Capital Adequacy Principles Paper, at 14, sub no. 20.

NYDOCS01/1000894.2 21

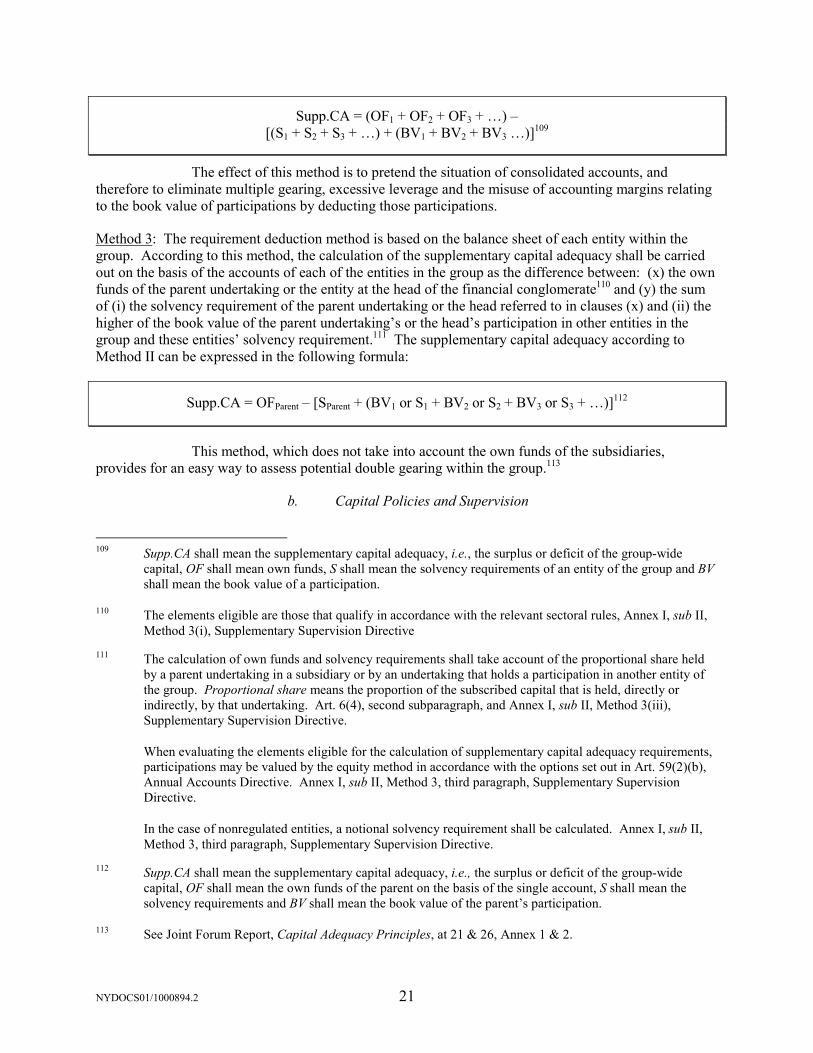

Supp.CA = (OF1 + OF2 + OF3 + …) – [(S1 + S2 + S3 + …) + (BV1 + BV2 + BV3 …)]109

The effect of this method is to pretend the situation of consolidated accounts, and therefore to eliminate multiple gearing, excessive leverage and the misuse of accounting margins relating to the book value of participations by deducting those participations.

Method 3: The requirement deduction method is based on the balance sheet of each entity within the group. According to this method, the calculation of the supplementary capital adequacy shall be carried out on the basis of the accounts of each of the entities in the group as the difference between: (x) the own funds of the parent undertaking or the entity at the head of the financial conglomerate110 and (y) the sum of (i) the solvency requirement of the parent undertaking or the head referred to in clauses (x) and (ii) the higher of the book value of the parent undertaking’s or the head’s participation in other entities in the group and these entities’ solvency requirement.111 The supplementary capital adequacy according to Method II can be expressed in the following formula:

Supp.CA = OFParent – [SParent + (BV1 or S1 + BV2 or S2 + BV3 or S3 + …)]112

This method, which does not take into account the own funds of the subsidiaries, provides for an easy way to assess potential double gearing within the group.113

b. Capital Policies and Supervision

109 Supp.CA shall mean the supplementary capital adequacy, i.e., the surplus or deficit of the group-wide

capital, OF shall mean own funds, S shall mean the solvency requirements of an entity of the group and BV shall mean the book value of a participation.

110 The elements eligible are those that qualify in accordance with the relevant sectoral rules, Annex I, sub II, Method 3(i), Supplementary Supervision Directive

111 The calculation of own funds and solvency requirements shall take account of the proportional share held by a parent undertaking in a subsidiary or by an undertaking that holds a participation in another entity of the group. Proportional share means the proportion of the subscribed capital that is held, directly or indirectly, by that undertaking. Art. 6(4), second subparagraph, and Annex I, sub II, Method 3(iii), Supplementary Supervision Directive.

When evaluating the elements eligible for the calculation of supplementary capital adequacy requirements, participations may be valued by the equity method in accordance with the options set out in Art. 59(2)(b), Annual Accounts Directive. Annex I, sub II, Method 3, third paragraph, Supplementary Supervision Directive.

In the case of nonregulated entities, a notional solvency requirement shall be calculated. Annex I, sub II, Method 3, third paragraph, Supplementary Supervision Directive.

112 Supp.CA shall mean the supplementary capital adequacy, i.e., the surplus or deficit of the group-wide capital, OF shall mean the own funds of the parent on the basis of the single account, S shall mean the solvency requirements and BV shall mean the book value of the parent’s participation.

113 See Joint Forum Report, Capital Adequacy Principles, at 21 & 26, Annex 1 & 2.

NYDOCS01/1000894.2 22

The Member States shall require regulated entities to have in place adequate capital adequacy policies at the level of the financial conglomerate. The requirement that regulated entities in financial conglomerates must ensure that on the level of the financial conglomerates the capital adequacy requirements of Annex I are met and that regulated entities have in place adequate capital adequacy policies on the level of the financial conglomerate must be subject to supervisory overview by the coordinator. The regulated entities or the mixed financial holding company must calculate the sufficiency of own funds on the level of the financial conglomerate at least annually. The EU-regulated entity at the head of the financial conglomerate or the mixed financial holding company at the head of the financial conglomerate must submit the result of the calculation to the coordinator.114

One can question the rationale for requiring adequate capital for a financial conglomerate on the group level, because in case of need of a regulated entity in the group, the group capital is not available to the needy regulated entity. The Supplementary Supervision Directive does not establish a source of strength doctrine. Under that doctrine a U.S. bank holding company and indirectly its subsidiaries are expected to support a deposit-taking subsidiary in case of need. The Gramm-Leach-Bliley Act of 1999 amendments to the U.S. Bank Holding Company Act of 1956 affirm this doctrine with certain limitations.115

2. Intra-Group Transactions and Risk Concentration

Another core regulation of the Supplementary Supervision Directive is the requirement of supplementary supervision on intra-group transactions and risk concentration of regulated entities in a financial conglomerate.116

a. Intra-Group Transactions

Intra-group transactions may cause supervisory concerns when they: (1) result in capital or income being inappropriately transferred from the regulated entity; (2) are on terms or under circumstances which parties operating at arm’s length would not allow and may be disadvantageous to a regulated entity; (3) can adversely affect the solvency, the liquidity and the profitability of individual entities within a group; or (4) are used as a means of supervisory arbitrage, thereby evading capital or other regulatory requirements altogether.117 Monitoring intra-group transactions is also an important factor in dealing with the risk of contagion within a financial conglomerate. Contagion entails the risk that, if certain parts of a conglomerate are experiencing financial difficulties, they may infect other healthy parts of the conglomerate as a result of which the operation of the healthy parts may be hampered

114 Art. 6(2), Supplementary Supervision Directive.

115 See Michael Gruson, Foreign Banks and the Financial Holding Company [herein Gruson, Foreign Banks

and the Financial Holding Company], § 10.07[1] in Michael Gruson & Ralph Reisner (eds.), REGULATION OF FOREIGN BANKS, vol. 1 (4th ed. 2003); Jeffrey D. Berman, Arthur S. Long & Tomer Seifan, U.S. Law Conditions Applicable to Foreign Bank Acquisitions of U.S. Banking Institutions, § 3.06[2] in Michael Gruson & Ralph Reisner (eds.), REGULATION OF FOREIGN BANKS, vol. 1 (4th ed. 2003).

116 Arts. 7(1) & 8(1), in connection with Annex II, Supplementary Supervision Directive.

117 The Joint Forum Report, Intra-Group Transactions and Exposure Principles, at 134, sub no. 12. See also Tripartite Report, at 21, sub no. 55.

NYDOCS01/1000894.2 23

or even made impossible.118 Therefore, intra-group transactions can significantly exacerbate problems for a regulated entity once contagion spreads.119

Intra-group transactions as defined in the Supplementary Supervision Directive are transactions by a regulated entity in a financial conglomerate with any other undertaking in the financial conglomerate.120 However, intra-group transactions go beyond transactions with members of the group. Intra-group transactions include transactions with natural or legal persons linked to the undertakings within the group by close links, even though such linked persons are not members of the group, and, consequently, not members of the financial conglomerate.121 The intra-group transactions are not limited to transactions of EU-regulated entities within a financial conglomerate but are transactions of any regulated entity.122 The Supplementary Supervision Directive does not provide for quantitative limits or qualitative requirements with regard to intra-group transactions within a financial conglomerate. The introduction of such limits and requirements or the introduction of other supervisory measures that would achieve the objectives of supplementary supervision with regard to intra-group transactions is left to the Member States.123

The scope of the provisions in the Supplementary Supervision Directive that deals with intra-group transactions is broader than the scope of the equivalent U.S. rules, Sections 23A and 23B, Federal Reserve Act,124 because the Supplementary Supervision Directive applies to all transactions between all regulated entities within a financial conglomerate and other entities in the group,125 whereas Sections 23A and 23B, Federal Reserve Act apply only to transactions between an insured depository institution, i.e., a U.S. bank, and its affiliates.

118 Tripartite Report, at 18, sub no. 47.

119 Tripartite Report, at 19, sub no. 50; see Joint Forum Report, Intra-Group Transactions and Exposure Principles, at 131, sub no. 4 for an enumeration of types of intra-group transactions and exposures.

120 Art. 2(18), Supplementary Supervision Directive.

121 Art. 2(18), Supplementary Supervision Directive. Close link is defined as a situation in which two or more natural or legal persons are linked by (1) a participation (20 percent of voting rights or capital), (2) control (parent-subsidiary relationship), (3) a similar relationship between any natural or legal person and an undertaking or (4) by each being in a control relationship to the same third person (common control). Art. 2(13), Supplementary Supervision Directive. It is difficult to imagine cases in which an undertaking in a group has a close link to another undertaking by means of a participation or control but the other undertaking is not a member of the group. However, the link with a natural person and the link created through permanent control relationships by two natural or legal persons to a third person does not create a group relationship.

122 See Art. 2(18) and Art. 8(1) & (2 ), Supplementary Supervision Directive, referring generally to regulated entities.

123 Art. 8(3), Supplementary Supervision Directive.

124 Sections 23A & 23B, Federal Reserve Act, 12 U.S.C. § 371c & 371c-1 (2000). See Robert E. Mannion & Lisa R. Chavarria, Transactions Between Banks and Affiliated Enterprises [herein Mannion, Transactions with Affiliates], ch. 12, in Michael Gruson & Ralph Reisner (eds.), REGULATION OF FOREIGN BANKS, vol. 1 (4th ed. 2003); Gruson, Foreign Banks and the Financial Holding Company, § 10.07[4].

125 Art. 2(18), Supplementary Supervision Directive. See also Art. 55a, first subparagraph, Banking Directive, added by Art. 29(9), Supplementary Supervision Directive (transactions between a credit institution and its mixed-activity holding company).

NYDOCS01/1000894.2 24

b. Risk Concentration

As to the problem of risk concentration,126 supervisors of the different financial sectors use various approaches to monitor large exposures, due to the different risks they are facing. In all three sectors, financial institutions face an increased risk of loss when their assets, liabilities or business activities are not diversified. As not all risk concentrations are inherently bad (a certain degree of concentration is the inevitable result of a well-articulated business strategy as well as product specialization, the targeting of a customer base or a sound strategy of outsourcing data processing activities), supervisors need to balance the benefits against the risks of concentrations at the conglomerate level. In identifying risks, the competent authorities have to take into account the different ways in which large losses can develop in a conglomerate as a result of risk concentration.127

Risk concentration means all exposures with a loss potential borne by entities (the exposures are not limited to those borne by regulated entities) within a financial conglomerate that are large enough to threaten the solvency or the financial position in general of the regulated entities in the financial conglomerate. Such exposures may be caused by counterparty risk/credit risk, investment risk, insurance risk, market risk, other risks, or a combination or interaction of these risks.128

Like in the case of intra-group transactions, the Supplementary Supervision Directive does not provide for quantitative limits or quantitative requirements with regard to risk concentration at the level of the financial conglomerate. The introduction of such limits and requirements or the introduction of other supervisory measures that would achieve the objectives of supplementary supervision with regard to risk concentration is left to the Member States.129

c. Common Provisions

To avoid the risks resulting from intra-group transactions and risk concentration, the Member States shall require regulated entities to have in place at the level of the financial conglomerate adequate risk management processes and internal control mechanisms – including sound reporting and accounting procedures.130 In addition, regulated entities that are Responsible Entities must have adequate internal control mechanism for the production of any data and information that would be relevant for the purpose of supplementary supervision.131

In addition, the Member States shall require regulated entities or mixed financial holding companies to report on a regular basis and at least annually to the coordinator any significant risk concentration at the level of the financial conglomerate and significant intra-group transactions of regulated entities within a financial conglomerate.132 The necessary information shall be submitted to the 126 Defined in Art. 2(19), Supplementary Supervision Directive.

127 The Joint Forum Report, Risk Concentrations Principles, at 141–46, sub nos. 4, 8–10, 11, 22 & 23.