Embed Size (px)

Citation preview

Presentation On

Board Of Financial

Supervision

Presented To:

Amol Mahajan Sir

By:

Somnath Pagar Abhishek Mahale

Sneha Mahale Snehal Aher

Manoj Narwade Swati Karande

1926- Hilton young commission recommends establishment of central

bank of India.

1934- RBI act pass.

1935- RBI commences operation at calcutta as a shareholder’s bank

1937- RBI’s central office moves to bombay

1942- The Reserve Bank ceased to be the currency issuing authority of

Burma (now Myanmar).

1947: The Reserve Bank stopped acting as banker to the Government of

Burma

1948: The Reserve Bank stopped rendering central banking services to

Pakistan.

1949: The Government of India nationalised the Reserve Bank under the

Reserve Bank (Transfer of Public Ownership) Act, 1948.

Origin Of RBI

MET,IOM, Nashik.

Core Functions of RBI

Banking

Supervision

Currency

Management Financial

&

Monetary

Stability

MET,IOM, Nashik.

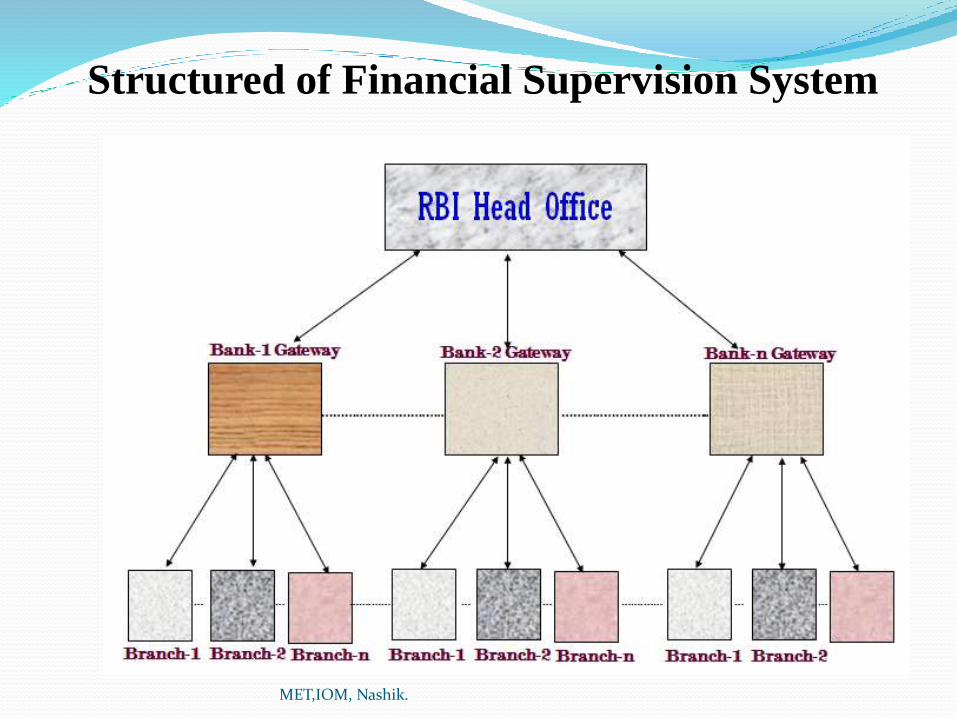

Structured of Financial Supervision System

MET,IOM, Nashik.

RBI Departments1) Market

Department of eternal investments and operation

Financial Markets Department

Financial Stability Unit

Internal Debt Management Department

Monetary Policy Department

2) Regulation and supervision

Department of Banking Operations and Development

Department of Banking Supervision

Department of Non-Banking Supervision

Foreign Exchange Department

Rural Planning and Credit Department

Urban Banks Department

MET,IOM, Nashik.

3) Research

Department of Economic Analysis and Policy

Department of Statistics and Information Management

4) Services

Customer Service Department

Department of Currency Management

Department of Government and Bank Accounts

Department of Payment and Settlement Systems

MET,IOM, Nashik.

5) Support

Department of Administration and Personnel Management

Department of Communication

Department of Expenditure and Budgetary Control

Department of Information Technology

Human Resources Development Department

Inspection Department

Legal Department

MET,IOM, Nashik.

Board of Financial Supervision

Under Section 58 of the RBI Act, the Board for Financial Supervision

(BFS) was constituted in November 1994, as a committee of the Central Board.

The Reserve Bank of India performs its supervision functions under the

guidance of the Board for Financial Supervision (BFS).

Formation

1949- Banking regulation act comes into force

1966- cooperative banks come under RBI Regulation

1992- Basel Norms made applicable to Indian banking system

1994- Board of financial supervision constituted

1997- Regulation of non-banking finance companies strengthened.

MET,IOM, Nashik.

Objective

Primary objective of BFS is to undertake consolidated supervision of

the financial sector comprising commercial banks, financial institutions and non-

banking finance companies.

Constitution

The Board is constituted by co-opting four Directors from the Central

Board as members for a term of two years and is chaired by the Governor. The

Deputy Governors of the Reserve Bank are ex-officio members. One Deputy

Governor, usually, the Deputy Governor in charge of banking regulation and

supervision, is nominated as the Vice-Chairman of the Board.

MET,IOM, Nashik.

The Board for Financial Supervision constituted –

The sub-committees main focus is up gradation of the quality of the

statutory audit and concurrent internal audit functions in banks and

development financial institutions.

Guidelines, norms , rules and regulation for growth development of

banking sector , nonbanking sector, financial institution etc

focuses on statutorily mandated areas of solvency, liquidity and

operational health of the bank. It is based on internationally adopted

CAMEL model modified as CAMELS, i.e., capital adequacy, asset

quality, management, earning, liquidity and system control.

MET,IOM, Nashik.

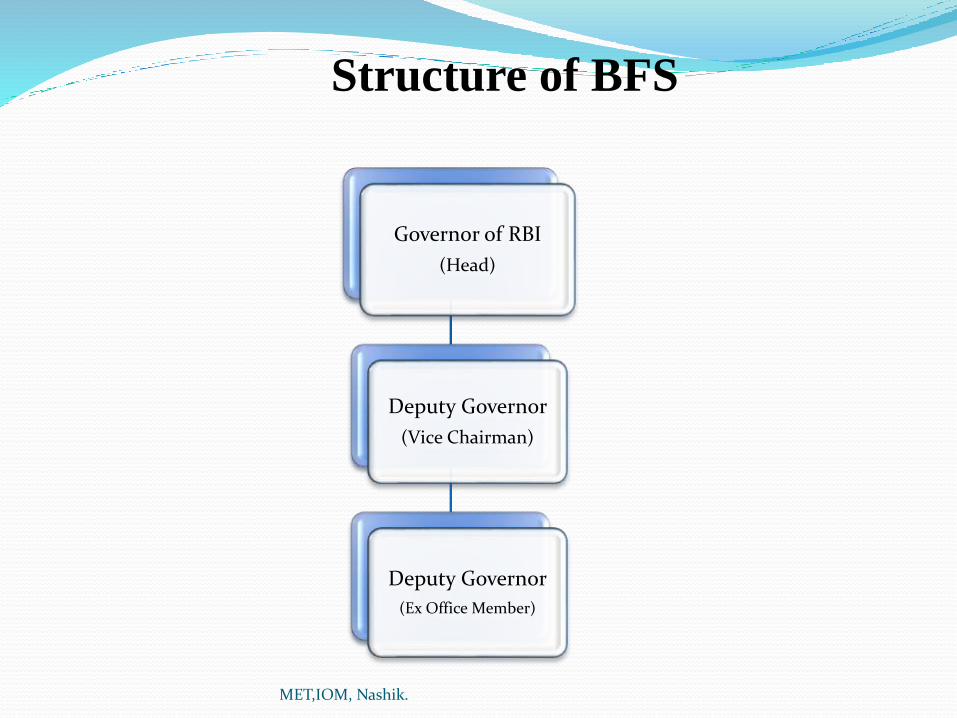

Governor of RBI

(Head)

Deputy Governor

(Vice Chairman)

Deputy Governor

(Ex Office Member)

Structure of BFS

MET,IOM, Nashik.

BFS meetings

The Board is required to meet normally once every month. It

considers inspection reports and other supervisory issues placed before it by the

supervisory departments.

BFS through the Audit Sub-Committee also aims at upgrading the

quality of the statutory audit and internal audit functions in banks and

financial institutions. The audit sub-committee includes Deputy Governor as

the chairman and two Directors of the Central Board as members.

The BFS oversees the functioning of Department of Banking

Supervision (DBS), Department of Non-Banking Supervision (DNBS) and

Financial Institutions Division (FID) and gives directions on the regulatory and

supervisory issues.

MET,IOM, Nashik.

Current Focus

Supervision of financial institutions

Consolidated accounting

Legal issues in bank frauds

Divergence in assessments of non-performing assets and

Supervisory rating model for banks.

MET,IOM, Nashik.

Legal Framework

Umbrella Acts

Reserve Bank of India Act, 1934 : governs the Reserve Bank functions

Banking Regulation Act, 1949: governs the financial sector

Acts governing specific functions

Public Debt Act, 1944/Government Securities Act (Proposed): Governs government debt

market.

Securities Contract (Regulation) Act, 1956: Regulates government securities market.

Indian Coinage Act, 1906:Governs currency and coins.

Foreign Exchange Regulation Act, 1973/Foreign Exchange Management Act,

1999: Governs trade and foreign exchange market.

"Payment and Settlement Systems Act, 2007: Provides for regulation and supervision of

payment systems in India“.

MET,IOM, Nashik.

Acts governing Banking Operations

Companies Act, 1956:Governs banks as companies.

Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970/1980:

Relates to nationalization of banks.

Bankers' Books Evidence Act.

Banking Secrecy Act.

Negotiable Instruments Act, 1881.

Acts governing Individual Institutions

State Bank of India Act, 1954.

The Industrial Development Bank (Transfer of Undertaking and Repeal) Act, 2003.

The Industrial Finance Corporation (Transfer of Undertaking and Repeal) Act, 1993.

National Bank for Agriculture and Rural Development Act.

National Housing Bank Act.

Deposit Insurance and Credit Guarantee Corporation Act.MET,IOM, Nashik.

Basel Norms

Set by Global Bank

Basel Committee on Banking Supervision (BCBS).

Basel – I (1988) In 1988, BCBS introduced capital measurement system

called Basel capital accord, also called as Basel 1. It focused almost entirely

on credit risk. It defined capital and structure of risk weights for banks. The

minimum capital requirement was fixed at 8% of risk weighted assets

(RWA). RWA means assets with different risk profiles. For example, an asset

backed by collateral would carry lesser risks as compared to personal loans,

which have no collateral. India adopted Basel 1 guidelines in 1992.

MET,IOM, Nashik.

Basel – II (2004) In 2004, Basel II guidelines were published by BCBS, which

were considered to be the refined and reformed versions of Basel I accord. The

guidelines were based on three parameters. Banks should maintain a minimum

capital adequacy requirement of 8% of risk assets, banks were needed to develop and

use better risk management techniques in monitoring and managing all the three

types of risks that is credit and increased disclosure requirements. Banks need to

mandatorily disclose their risk exposure, etc to the central bank. Basel II norms in

India and overseas are yet to be fully implemented.

Basel – III (2010) These guidelines were introduced in response to the financial

crisis of 2008. A need was felt to further strengthen the system as banks in the

developed economies were under-capitalized, over-leveraged and had a greater

reliance on short-term funding. Also the quantity and quality of capital under Basel

II were deemed insufficient to contain any further risk. Basel III norms aim at

making most banking activities such as their trading book activities more capital-

intensive. The guidelines aim to promote a more resilient banking system by

focusing on four vital banking parameters viz. capital, leverage, funding and

liquidity.MET,IOM, Nashik.

Banking Operations

MET,IOM, Nashik.

Cash Reserve Ratio – 4%

It is the % of Bank deposit that has to be kept with the RBI

If RBI increases this rate, the amount available with banks comes

down.

RBI increases the CRR to pull out excess money from the banks

It is also known as cash asset ratio or Liquidity ratio

Used as a tool of monetary policy that influences country’s

economy, Borrowings and interest rates across the country

MET,IOM, Nashik.

Statutory Liquidity Reserve/Ratio – 22%

SLR is the percentage of deposits the bank has to maintain in

form of Gold, Cash or other securities. It regulates the credit

growth in India.

Restricts the expansion of bank credit

Augments the investment of the banks in Government

securities

Ensures solvency of banks. A reduction of SLR rates looks

eminent to support the credit growth in India

MET,IOM, Nashik.

Prime lending Rate PLR is the rate that banks charge to their most credit worthy

customers

It is the minimum lending rate at which credit line is offered to prime

borrowers

MET,IOM, Nashik.

Sub-prime Lending Lending at a higher rate than the Prime rate

These are the loans offered to the individuals who do not qualify for

Prime lending

It includes – Subprime Mortgages, Subprime Car loans, Subprime

credit cards, etc.

MET,IOM, Nashik.

Base Rate 10% to 10.25%

It is the minimum rate of interest that a bank is allowed to

charge from its customers.

Unless mandated by the government, RBI rule stipulates that

no bank can offer loans at a rate lower than BR to any of its

customers.

Factors like the cost of deposits, administrative costs, a bank’s

profitability in the previous financial year and a few other

parameters, with stipulated weights, are considered while

calculating a lender’s BR.

MET,IOM, Nashik.

Repo Rate – 8%

The rate at which RBI lends to the commercial Banks

Low repo rate implies that banks are getting cheaper loans

from RBI

When Repo rates increase, borrowings from RBI becomes

more expensive

MET,IOM, Nashik.

Reverse Repo Rate – 7% Rate at which RBI borrows money from Banks

Safeguarding the money and earn good interest

Increase in Reverse repo rates can lead to banks to transfer

more money to RBI, reducing money in the banking system

MET,IOM, Nashik.

Bank Rate 9% Also referred to as the discount rate

The rate of interest which a central bank charges on the loans

and advances that it extends to commercial banks and other

financial intermediaries.

MET,IOM, Nashik.

Major function of BFS

1) Commercial Banks

Licensing

For commencing banking operations in India, whether by an Indian

or a foreign bank, a license from the Reserve Bank is required.

The opening of new branches by banks and change in the location of

existing branches are also regulated as per the Branch Authorisation

Policy.

MET,IOM, Nashik.

The Reserve Bank’s policy objective is to ensure high-quality

corporate governance in banks.

It has issued guidelines stipulating ‘fit and proper’ criteria for

directors of banks.

In terms of the-

special knowledge or practical experience in various relevant

areas

The Reserve Bank also has powers to appoint additional

directors on the board of a banking company.

2) Corporate Governance

MET,IOM, Nashik.

3) Statutory Pre-emptions

Commercial banks are required to maintain a certain portion of

their Net Demand and Time Liabilities (NDTL) in the form of cash

with the Reserve Bank, called

Cash Reserve Ratio (CRR)

Statutory Liquidity Ratio (SLR).

MET,IOM, Nashik.

4) Interest Rate

The interest rates on most of the categories of deposits and

lending transactions have been deregulated and are largely

determined by banks.

However, the Reserve Bank regulates-

Interest rates on savings bank accounts and deposits of

non-resident Indians (NRI),,export credits

MET,IOM, Nashik.

5) Prudential Norms

In order to strengthen the balance sheets of banks, the Reserve

Bank has been prescribing appropriate prudential norms for them in

regard to income recognition, asset classification and provisioning, capital

adequacy, investments portfolio and capital market exposures, to name a

few. A brief description of these norms is furnished below:

Capital Adequacy

Loans and Advances

Investments

MET,IOM, Nashik.

6) Rural Financial Banks

Rural cooperative banks

Short-term (3tier structure)

State cooperative bank(StCBs) -State level

District central cooperative bank(DCCBs)-District Level

Primary Agriculture Credit Societies(PACS)-Village Level

Long-term

State Cooperative Agriculture and Rural Development Banks

(SCARDBs)- State level.

Primary Cooperative Agriculture and Rural Development Banks

(PCARDBs)-District level.

Regional Rural Banks

Register under regional rural banks act 1976MET,IOM, Nashik.

7) Urban cooperative Bank

Providing banking services to the middle and lower income groups of

society in urban and semi urban areas.

8) Non-Banking financial companies (NBFCs)

An NBFC is defined as a company engaged in the business of lending,

investment in shares and securities, hire purchase, chit fund, insurance or

collection of monies.

9) Primary Dealers

In 1995, the Reserve Bank introduced the system of Primary Dealers in

the Government Securities Market, which comprised independent entities

undertaking Primary Dealer activity.

MET,IOM, Nashik.

10) Credit Information Companies

Credit Information Companies (Regulation) Act 2005 empowers the

Reserve Bank to regulate CICs.

Credit Information Companies (CIC) play an important role in

facilitating credit to various borrowers on the basis of their track

record.

11) Financial Market

Realising the growth potential of an economy.

MET,IOM, Nashik.

MET,IOM, Nashik.

Thank You..!

MET,IOM, Nashik.