Embed Size (px)

Citation preview

1

Supermarkets and planning regulation

Rachel Griffith and Heike Harmgart

Institute for Fiscal Studies and

Economics Department, University College London

Value-added per hour (US 1995$) in retail

0

5

10

15

20

25

1980

1990

2000

2003

UKUSFrance

Source: Groningen Growth and Development Centre, 60-Industry Database, October 2005, http://www.ggdc.net/,updated from O'Mahony and van Ark (2003)

Retail labour productivity has grown faster in US and France; retail sector accounts for large part of UK-US productivity gap

2

Reforms to planning regulation

• Regulations restrict development of new out of town stores

• Highlighted as a reason for poor productivity performance:McKinsey StudyBarker Review in land use regulation and productivity

• Why impact on productivity?– fewer new stores -> slower adoption of ICT and new technologies– more smaller stores -> more stores below minimum efficient scale – less entry -> less competition

Number of new stores opened by big four supermarkets (Adsa, Sainsbury, Safeway and Tesco)

0

20

40

60

80

100

120

140

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Num

ber o

f new

sto

res

open

ed in

Eng

land

Big stores Small stores

reform to planning regulations

3

Evaluating the effect of planning reforms

• Existing evaluations do not account for other factors – demographic and labour market trends may mean optimal store

format is changing (and differs from the US?)

• We estimate an equilibrium model of consumer behaviour and firm entry that controls for many other factors– use variation in Local Authorities "economic plan" and its

implementation– control for variation in demographics across town centres

• We show that if demographics are not accounted for, then get an overestimate of the impact of planning

The model

• Two types of stores – in-town (small) – out-of-town (big)

• Consumer demand for groceries takes the following form:– consumers demand the bulk of their groceries in a one-stop shopping trip in

a big store,– they subsequently top-up with additional items that were forgotten or

unexpectedly needed in small stores

• Firms are profit maximising– make decision over entry, then engage in price competition– a store enters if profits are sufficient to cover fixed costs, and they exit the

market if they make negative net profits– planning regulation introduces differential fixed costs across store type

4

The model

profits of each firm when there are nfirms in the market

( ) jnfjfjfjfnfj RWY εγθβαλ ++++=Π

Populationfactors that affectvariable profits

factors that affectfixed costs

unobserved factorsthat affect profits

Data

• Supermarket location– Institute of Grocery Distributors (IGD)

• Geographic markets– ODPM town centres

• Planning applications– ODPM data on A1 and A3 applications

• Demographic Data– ONS and ODPM

5

Number of town centres with market configuration

845845Total2108 or more687606895

116106412410031042142592871151380

stores less than15,000 sq ft

Stores of 15,000 sq ftor moreMarket configuration

Selected coefficients in model for determinants of number of big stores

(0.2089)(0.2027)0.36760.5335% plan 97-01

(0.0014)-0.0024Retail rateable value

Fixed costs(0.0014)0.0038Office floorspace per hectare

(0.1632)0.9381Dist to nearest town centre

(0.0979)-0.2312Uemployment rate

Variable costs(0.0068)0.0377Population (1000s)

6

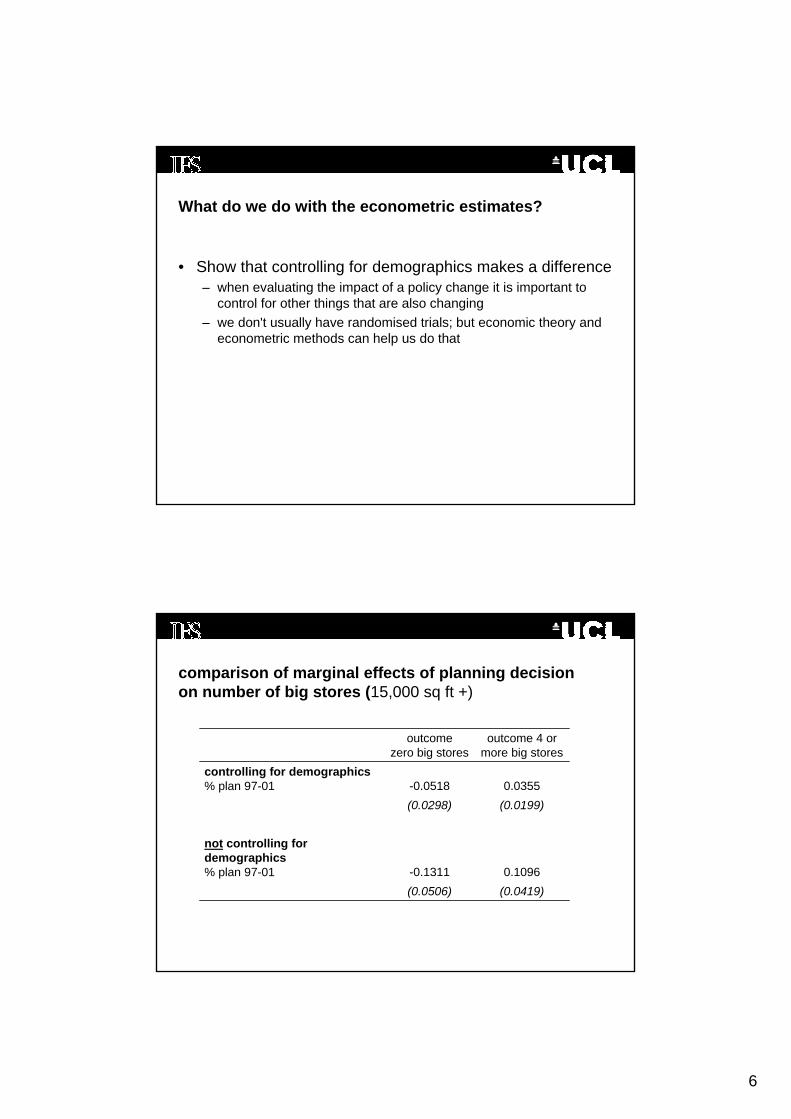

What do we do with the econometric estimates?

• Show that controlling for demographics makes a difference– when evaluating the impact of a policy change it is important to

control for other things that are also changing– we don't usually have randomised trials; but economic theory and

econometric methods can help us do that

comparison of marginal effects of planning decisionon number of big stores (15,000 sq ft +)

(0.0419)(0.0506)0.1096-0.1311

not controlling for demographics% plan 97-01

(0.0199)(0.0298)0.0355-0.0518

controlling for demographics% plan 97-01

outcome 4 or more big stores

outcomezero big stores

7

What do we do with the econometric estimates?

• Show that controlling for demographics makes a difference– when evaluating the impact of a policy change it is important to

control for other things that are also changing– we don't usually have randomised trials; but economic theory and

econometric methods can help us do that

• Use our model to quantify (some of) the costs of restrictive planning regulations

How can we quantify the costs?

• Concern about impact of planning regulations has been that they lead to inefficiencies and reduced competition– what impact on prices?

• Use data on a large number of food products purchased in different areas– how do prices of food in supermarkets differ when there is one big

store compared to two big stores, three big stores, ....

8

Estimated difference in price of food compared to a town centre with 1 big store

-1.88%-1.88%number of big stores=4+-1.73%-1.68%number of big stores=3-1.88%-1.70%number of big stores=2

median of 109 food categories

mean across 109food categories

Estimated difference in prices in town centres with 4 big stores compare to those with 1 big store

9

Predicted change in market structures if all existing planning applications were approved

0.014-0.001-0.005-0.0084+0.0110.004-0.001-0.01430.0080.0080.006-0.02120.0030.0060.012-0.0210 or 1

4+320 or 1Actual equilibrium structure

Predicted equilibrium structure

Combine information on (1) estimated differences in equilibrium number of stores with (2) estimated price differences

-0.03276%Total-0.01561%4+-0.02649%3-0.03744%2-0.03615%0 or 1

Mean % reduction in

price

Actual equilibrium structure

10

Combine that with average weekly houehold expenditure £41.90 per week (from Expenditure and Food Survey 2001/2002)

-1.37-0.03276%Total-0.65-0.01561%4+-1.11-0.02649%3-1.56-0.03744%2-1.51-0.03615%0 or 1

Mean reduction in pence on weekly household

food expenditure

Mean % reduction in

price

Actual equilibrium structure

Multiply that times the number of households in town centres with that equilibrium number of stores

-£210,187-1.37-0.03276%Total-£21,475-0.65-0.01561%4+-£26,029-1.11-0.02649%3-£67,326-1.56-0.03744%2-£95,357-1.51-0.03615%0 or 1

Total £ reduction in weekly household food expenditure

Mean reduction in pence on weekly household

food expenditure

Mean % reduction in

price

Actual equilibrium structure

The total savings in terms of weekly expenditure is £210,187Multiply that times 52 weeks to get an annual estimated increasein consumer surplus of £11m

11

Variation in prices directly linked to planning approvals

• Further corroborative evidence – we look directly at how prices of groceries vary across markets with

different levels of land use regulations

• We do this for the same 109 food categories– we find that the mean coefficient is -0.0454, the median is -0.0439

• What impact does this imply?– compare a market that sits at the 25th percentile in terms of the

rate of approval of land use applications (this is 0.75) – with one that sits at the 75th percentiles (this is 0.95) – we would see a difference in prices of around 1% on average

Policy implications

• Store size may be important determinant of output per worker, but are planning regulations the main driver of smaller store size?– Important to get the counterfactual right when evaluating policies – May still want to reform planning regulations, but don’t necessarily

expect big impact on productivity

• Using economic theory and econometric methods we can obtain estimates of the monetary costs of planning regulation, e.g. in terms of prices consumers pay– these need to be offset against the anticipated benefits, e.g. in

terms of reduced congestion etc.

12

Further work on retail food prices

• If firms very inefficient then would expect higher prices (driven by higher costs)

• Also, repeated competition investigations in food retail– would expect higher mark-ups

• Perception of high food prices by consumers

• How do prices of food compare between the UK and US?

-5%

0%

5%

10%

15%

20%

25%

30%

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

12-m

onth

infla

tion

rate

GB US

Food at home inflation rates (US and UK), 1975 – 2006

13

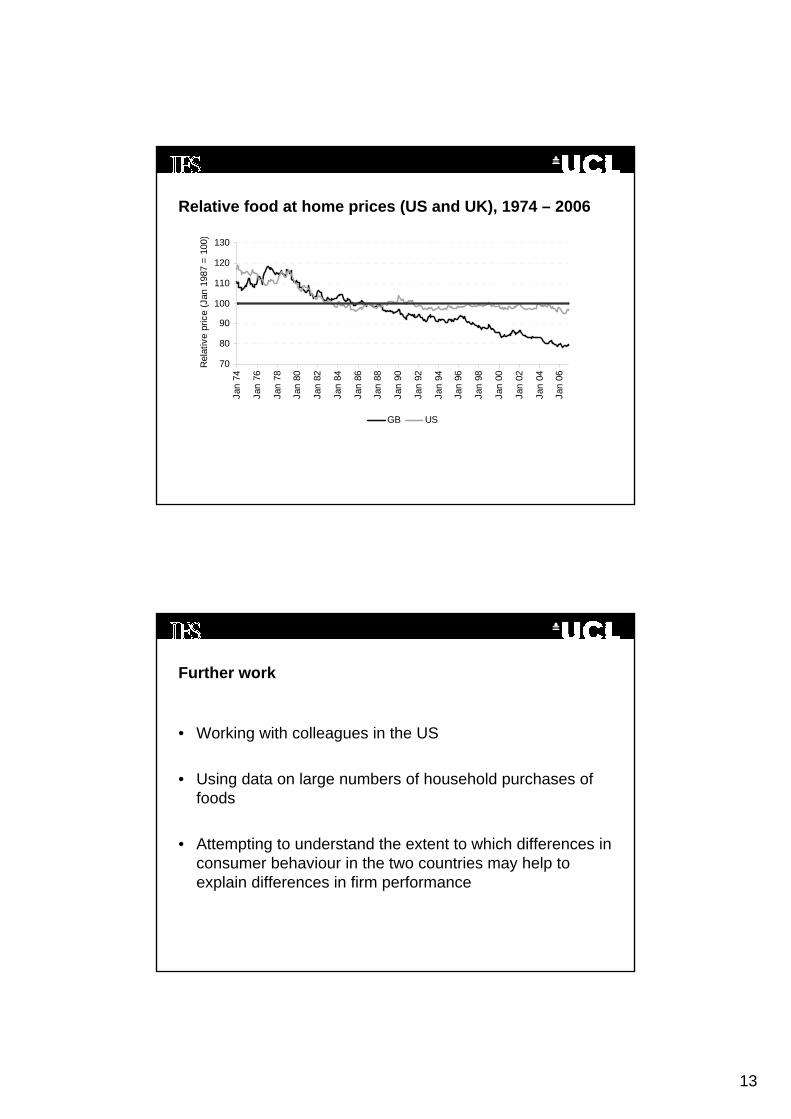

Relative food at home prices (US and UK), 1974 – 2006

70

80

90

100

110

120

130Ja

n 74

Jan

76

Jan

78

Jan

80

Jan

82

Jan

84

Jan

86

Jan

88

Jan

90

Jan

92

Jan

94

Jan

96

Jan

98

Jan

00

Jan

02

Jan

04

Jan

06

Rel

ativ

e pr

ice

(Jan

198

7 =

100 )

GB US

Further work

• Working with colleagues in the US

• Using data on large numbers of household purchases of foods

• Attempting to understand the extent to which differences in consumer behaviour in the two countries may help to explain differences in firm performance