Embed Size (px)

Citation preview

Study on Regulatory Options for Further Market Opening in Rail Passenger Transport

Stakeholder Meeting

10 February 2010

Session 2AGerman Case Study

Presented by Kay Mitusch

1. Key Features

2. Structure

3. Experience

4. Points made by stakeholders

5. Conclusions

6. Discussion session

Index

1. Key features

Financial developments:

Subsidies: Total government support (Regional and Infra) rises with inflation, now at about 10 bn. EUR per annum

Access charges: account for about 40% of RU’s costs recently have been increasing faster than inflation structure quite stable

1. Key features

The reform of 1994-1999 was always seen as an unfinished project

Railway Reform of 2006-ongoing: Transport & Logistics companies of DB have been combined into a sub-

holding (DB ML, 2008) that will be semi-privatised (25%) in the future

Economic regulation by independent “Federal Network Agency” (BNetzA) since 2006 (non-discrimination, cost-plus like regulation of access charges)

Multi-annual contract for rail infrastructure quality (LuFV, 2009)

Possibly incentive-regulation (price cap) in the future

1. Key features

2. Structure Distinction between regional and long-distance passenger markets

Regarded as commercially viable

No direct public funding to RUs Almost no entry by competitors

(with 3 exception), although legally possible (open access)

No direct regulation either – but several government interventions with DB Fernverkehr

RegionalRegional Long-distanceLong-distance

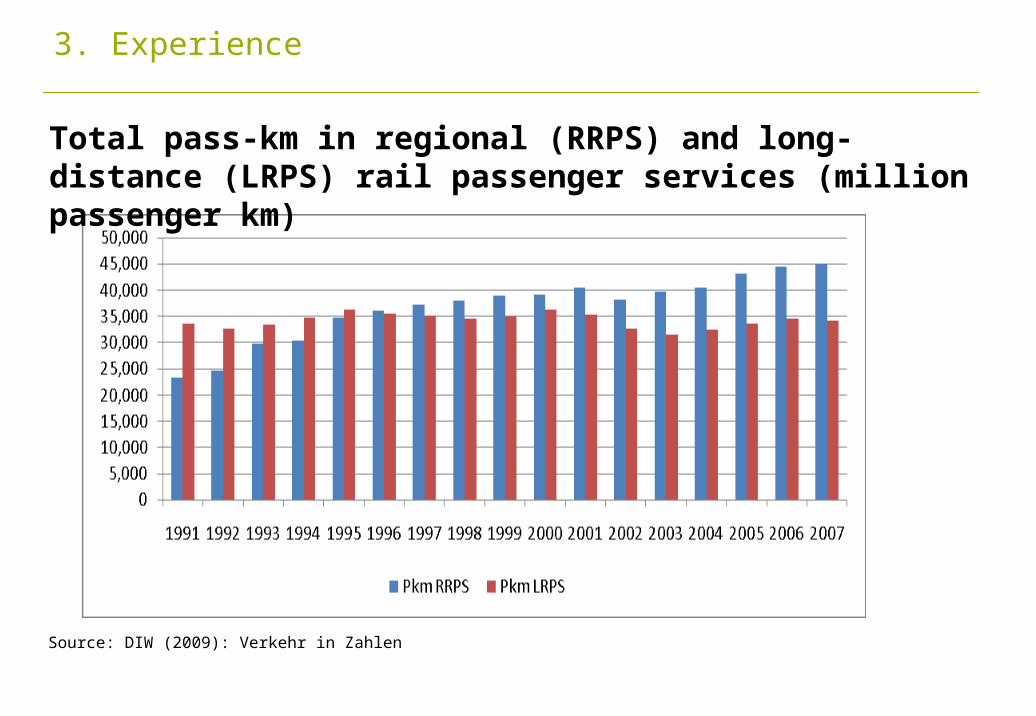

3. Experience

Total pass-km in regional (RRPS) and long-distance (LRPS) rail passenger services (million passenger km)

Source: DIW (2009): Verkehr in Zahlen

3. Experience

All market segments have improved

Long-distance: stable pass-km with a changing structure

DB abolished trains connecting smaller cities (InterRegio) that were unprofitable

Some 30% of these cuts were replaced by publicly contracted services now counting as “regional” services

Spread of a high-speed transport network with increasing passenger volume

DB long-distance unit currently operating profitably, despite increased airline competition (but based on huge government financing of new high-speed infrastructure)

3. Experience

3. Experience

In regional traffic, public authorities define service requirements too tightly, leaving insufficient scope for entrepreneurial decisions

Views on awarding procedures for regional service contracts: In addition to open tenders, the use of restricted or negotiated

procedures can be part of an overall competitive and efficient market

The use of direct awarding should be abolished, since it favours the incumbent

The interplay between two regulatory agencies (EBA and regulator BNetzA) is not always coordinated and creates problems

The incumbent’s ability to discriminate against new entrants are still too strong - need for an incentive regulation and separation of infrastructure and incumbent’s transport branches.

4. Stakeholders’ views

Neighbouring states’ railway systems are less open than in Germany. Thus, RUs in these states can use their protected market base as a source of cross-subsidy to compete with DB

The closed markets in neighbouring states threatens the political commitment to market opening in Germany

More money is needed for the infrastructure

Access charges are quite high in Germany – heightening the importance of a regulatory reform towards an incentive regulation (since the LuFV contract is silent on access charges)

4. Stakeholders’ views

Regional: passengers now benefit from a well-organised and quite dense service

network with a modern fleet at moderate prices Modal share has increased from 3.4% to 4.1% (a relative improvement

of 19%) DB’s market share fell from 100% to 90%, its success rate in open

tenders is below 50%

Long-distance: Fares for long-distance travel are generally viewed as quite high by the

public Lack of punctuality is also a public concern Apart from recent irregularities (mainly caused by the rolling stock

industry) the high quality of long-distance services is also acknowledged

Modal share has declined from 3.5% to 3.1% (a relative decline of 12%) DB’s market share is still almost 100%

5. Conclusions Passenger Railway markets since the Railway Reform of 1994-1999

Overall, the Railway Reform of 1994-1999 has led to a more reasonable railway system

The incumbent didn’t vanish or topple after the introduction of competition – on the contrary, it reorganised quite successfully

Regionalisation is seen as a success – reorganisation, public planning & elements of franchise competition seem to go hand in hand – but the level of competition is still low

Development of long-distance traffic poses more questions and concerns, as does infrastructure management

For long-distance, alternative organisation models are currently discussed

At the same time, there seem to be chances for some more entry in the near future

For infrastructure management, an introduction of a price cap regulation is announced by the new government (incentives for efficiency, more reliability in future access charges)

5. Conclusions

Questions:

Do you agree with this analysis?

Are there any other issues of equal importance that need to be brought out?

What lessons can we learn from the German experience?

6. Discussion session