Embed Size (px)

Citation preview

Ian H. Giddy/NYU Structured Finance-1

Prof. Ian GiddyNew York University

Structured Finance& Restructuring

Copyright ©2004 Ian H. Giddy Structured Finance 2

Structured Finance

Corporate financial restructuringAsset-backed securitizationSynthetic and whole business securitizationCredit-linked structured financeStructured financing techniques

Debt-linkedEquity-linked

Leveraged finance

Ian H. Giddy/NYU Structured Finance-2

Copyright ©2004 Ian H. Giddy Structured Finance 3

Structured Finance

Copyright ©2004 Ian H. Giddy Structured Finance 4

Assignments

Individual 30%Team 30%Caselets 20%Final 40%

Ian H. Giddy/NYU Structured Finance-3

Copyright ©2004 Ian H. Giddy Structured Finance 5

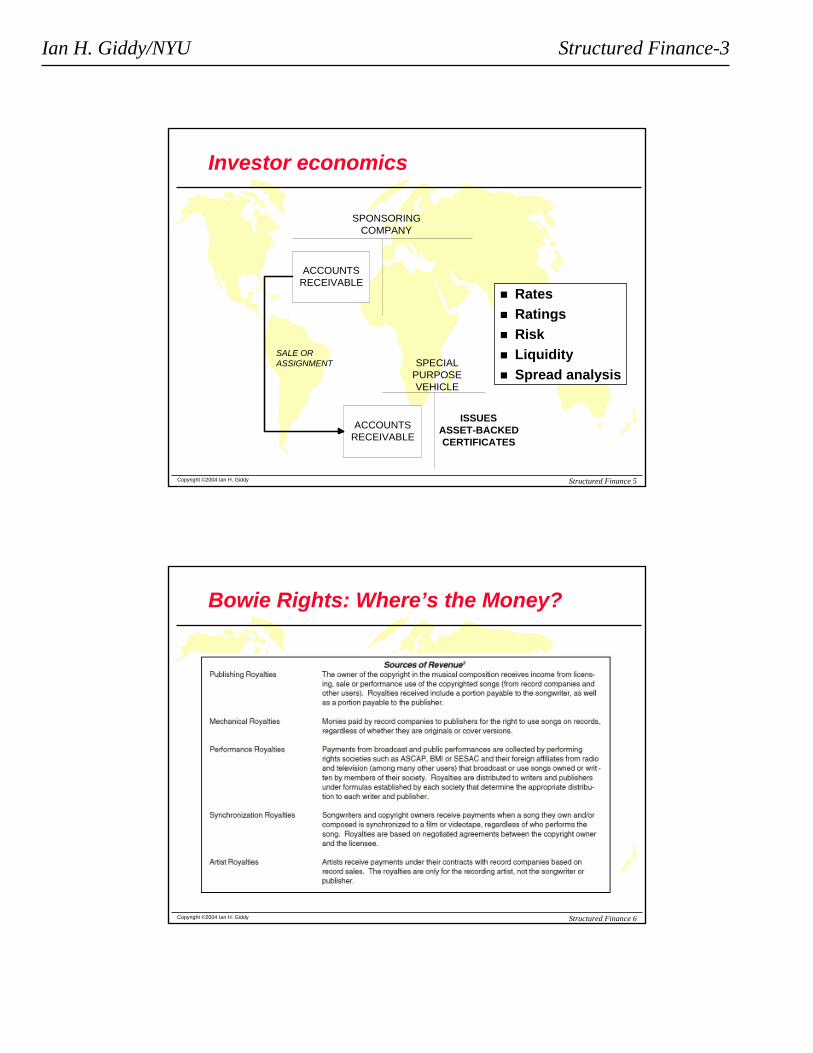

Investor economics

SPONSORINGCOMPANY

SPECIALPURPOSEVEHICLE

ACCOUNTSRECEIVABLE

ACCOUNTSRECEIVABLE

ISSUESASSET-BACKEDCERTIFICATES

SALE ORASSIGNMENT

RatesRatingsRiskLiquiditySpread analysis

Copyright ©2004 Ian H. Giddy Structured Finance 6

Bowie Rights: Where’s the Money?

Ian H. Giddy/NYU Structured Finance-4

Copyright ©2004 Ian H. Giddy Structured Finance 7

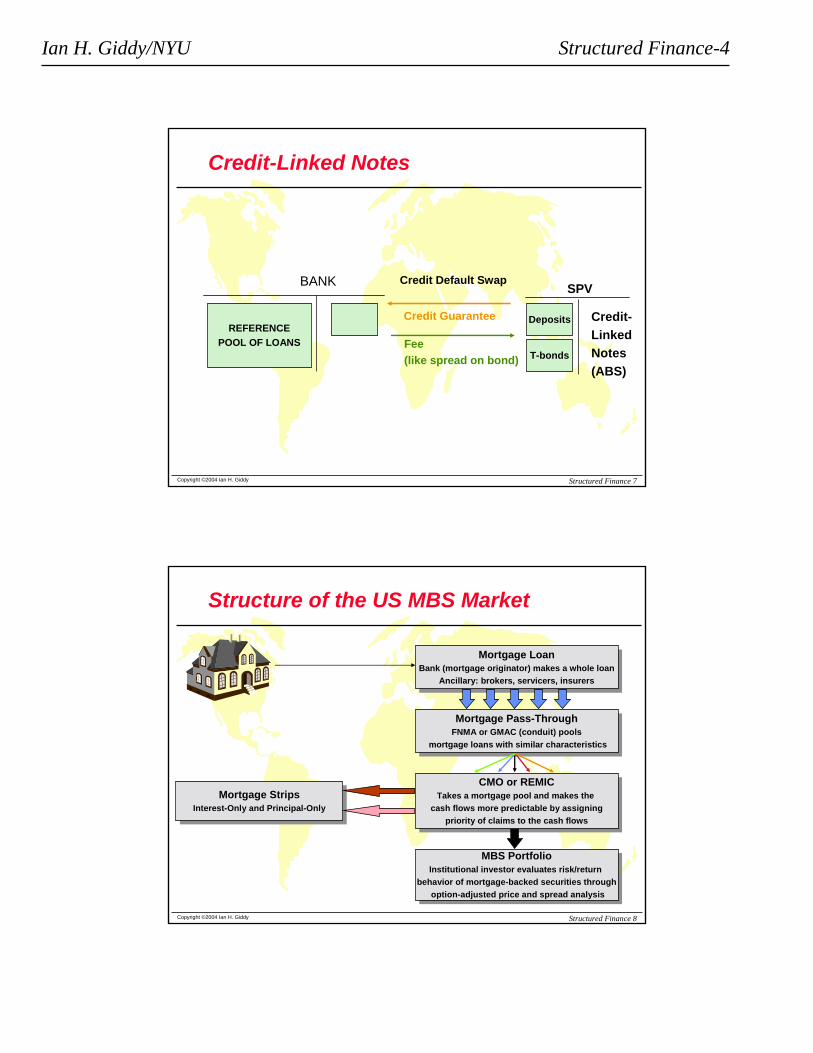

Credit-Linked Notes

BANK SPV

Credit-LinkedNotes(ABS)

REFERENCEPOOL OF LOANS

Deposits

Credit Default Swap

T-bondsFee (like spread on bond)

Credit Guarantee

Copyright ©2004 Ian H. Giddy Structured Finance 8

Structure of the US MBS Market

Mortgage LoanBank (mortgage originator) makes a whole loan

Ancillary: brokers, servicers, insurers

Mortgage LoanBank (mortgage originator) makes a whole loan

Ancillary: brokers, servicers, insurers

Mortgage Pass-ThroughFNMA or GMAC (conduit) pools

mortgage loans with similar characteristics

Mortgage Pass-ThroughFNMA or GMAC (conduit) pools

mortgage loans with similar characteristics

CMO or REMICTakes a mortgage pool and makes the

cash flows more predictable by assigningpriority of claims to the cash flows

CMO or REMICTakes a mortgage pool and makes the

cash flows more predictable by assigningpriority of claims to the cash flows

MBS PortfolioInstitutional investor evaluates risk/return

behavior of mortgage-backed securities throughoption-adjusted price and spread analysis

MBS PortfolioInstitutional investor evaluates risk/return

behavior of mortgage-backed securities throughoption-adjusted price and spread analysis

Mortgage StripsInterest-Only and Principal-Only

Mortgage StripsInterest-Only and Principal-Only

Ian H. Giddy/NYU Structured Finance-5

Copyright ©2004 Ian H. Giddy Structured Finance 9

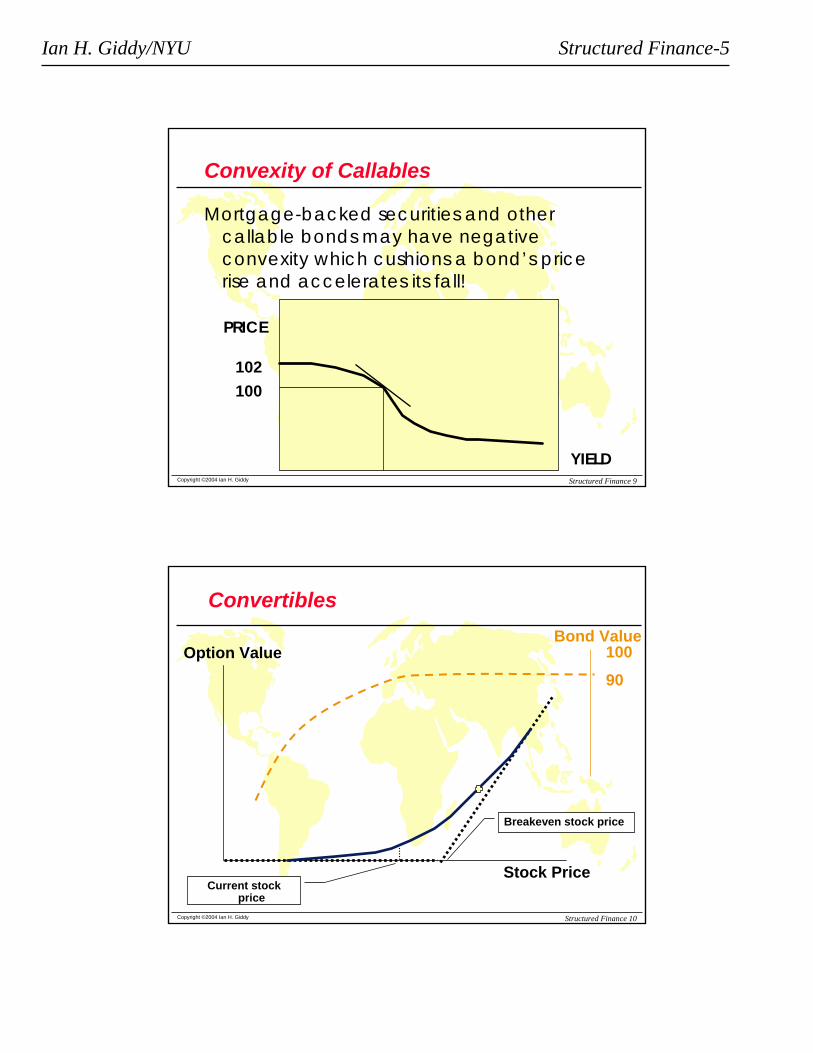

Convexity of Callables

Mortgage-backed securities and other callable bonds may have negative convexity which cushions a bond’s price rise and accelerates its fall!

PRICE

YIELD

100102

Copyright ©2004 Ian H. Giddy Structured Finance 10

Convertibles

Option Value

Stock PriceCurrent stock

price

Breakeven stock price

Bond Value100

90

Ian H. Giddy/NYU Structured Finance-6

Copyright ©2004 Ian H. Giddy Structured Finance 11

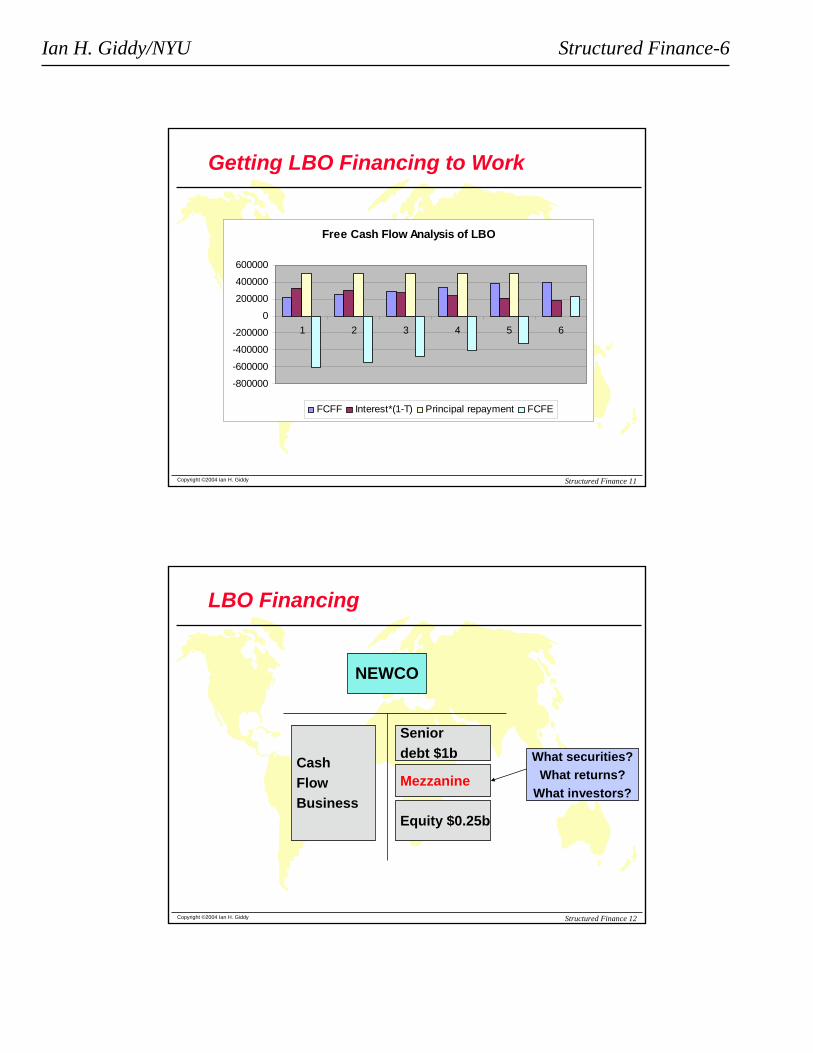

Getting LBO Financing to Work

Free Cash Flow Analysis of LBO

-800000

-600000

-400000

-200000

0

200000

400000

600000

1 2 3 4 5 6

FCFF Interest*(1-T) Principal repayment FCFE

Copyright ©2004 Ian H. Giddy Structured Finance 12

LBO Financing

NEWCO

CashFlowBusiness

Equity $0.25b

Seniordebt $1b What securities?

What returns?What investors?

Mezzanine

Ian H. Giddy/NYU Structured Finance-7

Copyright ©2004 Ian H. Giddy Structured Finance 13

Structured Finance

Corporate financial restructuringAsset-backed securitizationSynthetic and whole business securitizationCredit-linked structured financeStructured financing techniques

Debt-linkedEquity-linked

Leveraged finance

Copyright ©2004 Ian H. Giddy Structured Finance 14

Corporate Financial Restructuring

Why Restructure?

ProactiveExample: Sealed Air

DistressExample:

Loewen 1999

DefensiveExample:

Loewen 1996Management acts to preserve or enhance shareholder value

Management acts to protect company, stakeholders and management from change in control

Lenders and shareholders lose, but try to work out best way to minimize loss

Ian H. Giddy/NYU Structured Finance-8

Copyright ©2004 Ian H. Giddy Structured Finance 15

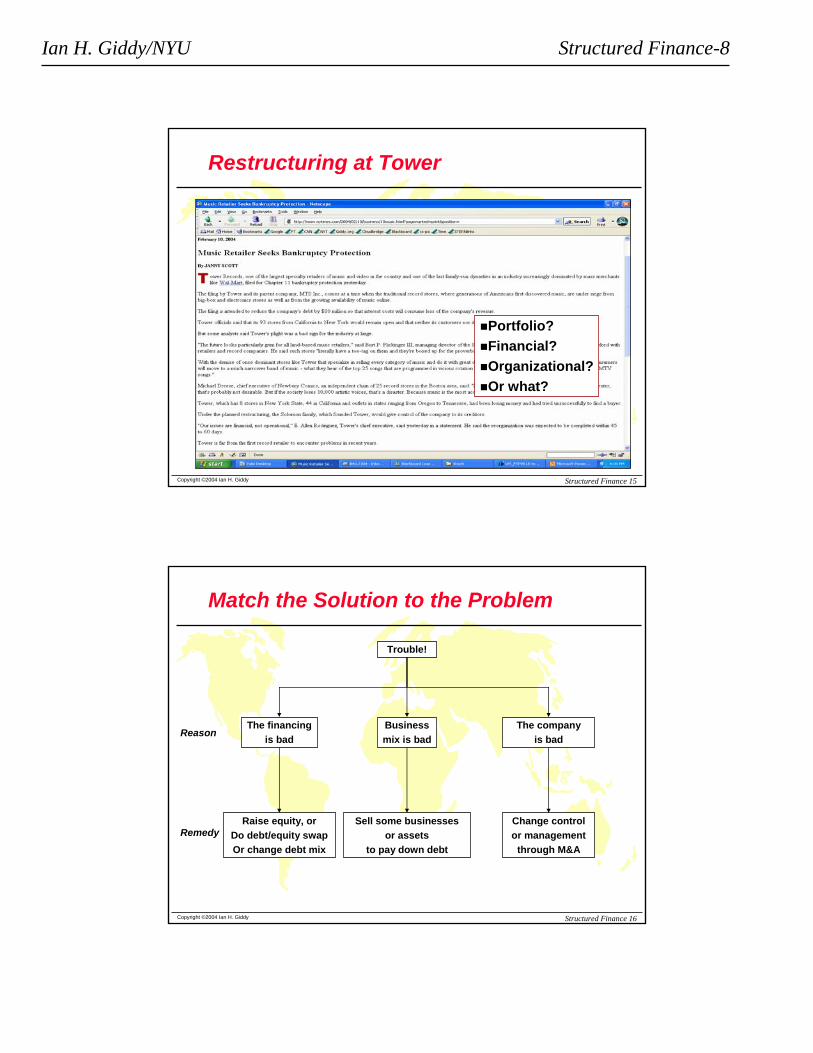

Restructuring at Tower

Portfolio?Financial?Organizational?Or what?

Copyright ©2004 Ian H. Giddy Structured Finance 16

Match the Solution to the Problem

Trouble!

The financingis bad

The companyis bad

Businessmix is bad

Raise equity, orDo debt/equity swap Or change debt mix

Change controlor management

through M&A

Sell some businessesor assets

to pay down debt

Reason

Remedy

Ian H. Giddy/NYU Structured Finance-9

Copyright ©2004 Ian H. Giddy Structured Finance 17

Dynegy

Copyright ©2004 Ian H. Giddy Structured Finance 18

What is Corporate Restructuring?

Any substantial change in a company’s financial structure, or ownership or control, or business portfolio.Designed to increase the value of the firm Restructuring

Improvecapitalization

Change ownershipand control

Improvedebt composition

Ian H. Giddy/NYU Structured Finance-10

Copyright ©2004 Ian H. Giddy Structured Finance 19

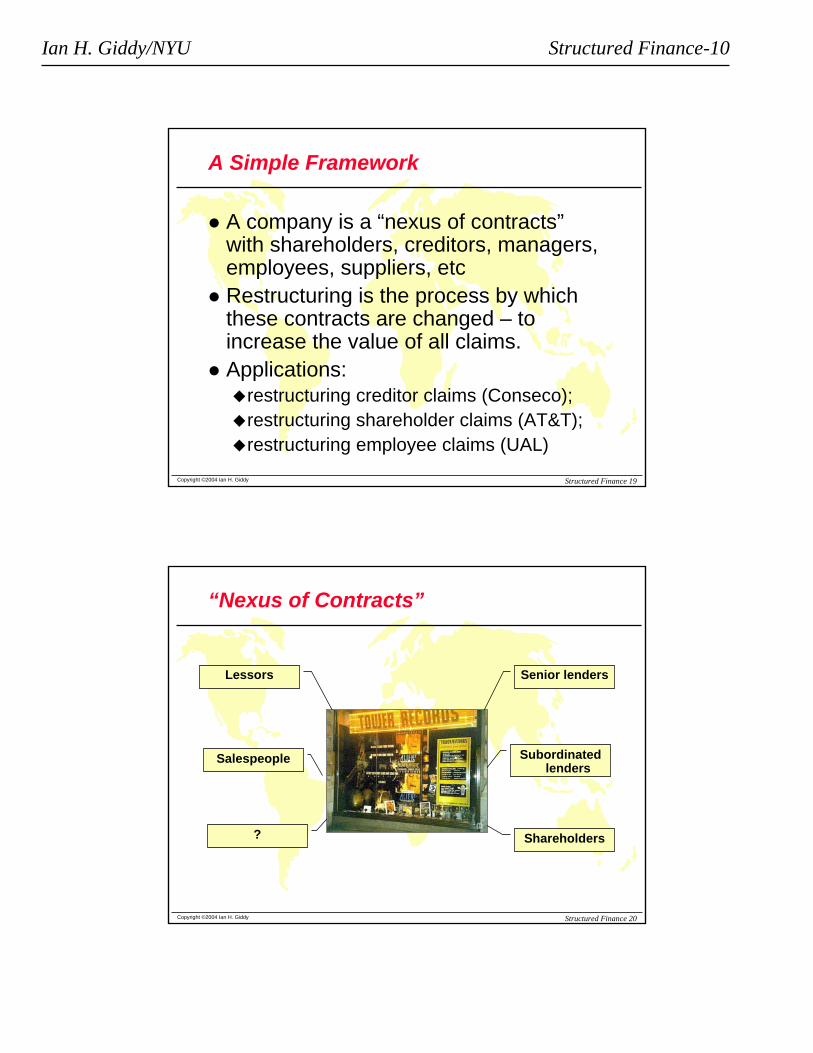

A Simple Framework

A company is a “nexus of contracts” with shareholders, creditors, managers, employees, suppliers, etcRestructuring is the process by which these contracts are changed – to increase the value of all claims.Applications:

restructuring creditor claims (Conseco);restructuring shareholder claims (AT&T);restructuring employee claims (UAL)

Copyright ©2004 Ian H. Giddy Structured Finance 20

“Nexus of Contracts”

Shareholders

Senior lenders

Subordinated lenders

Lessors

Salespeople

?

Ian H. Giddy/NYU Structured Finance-11

Copyright ©2004 Ian H. Giddy Structured Finance 21

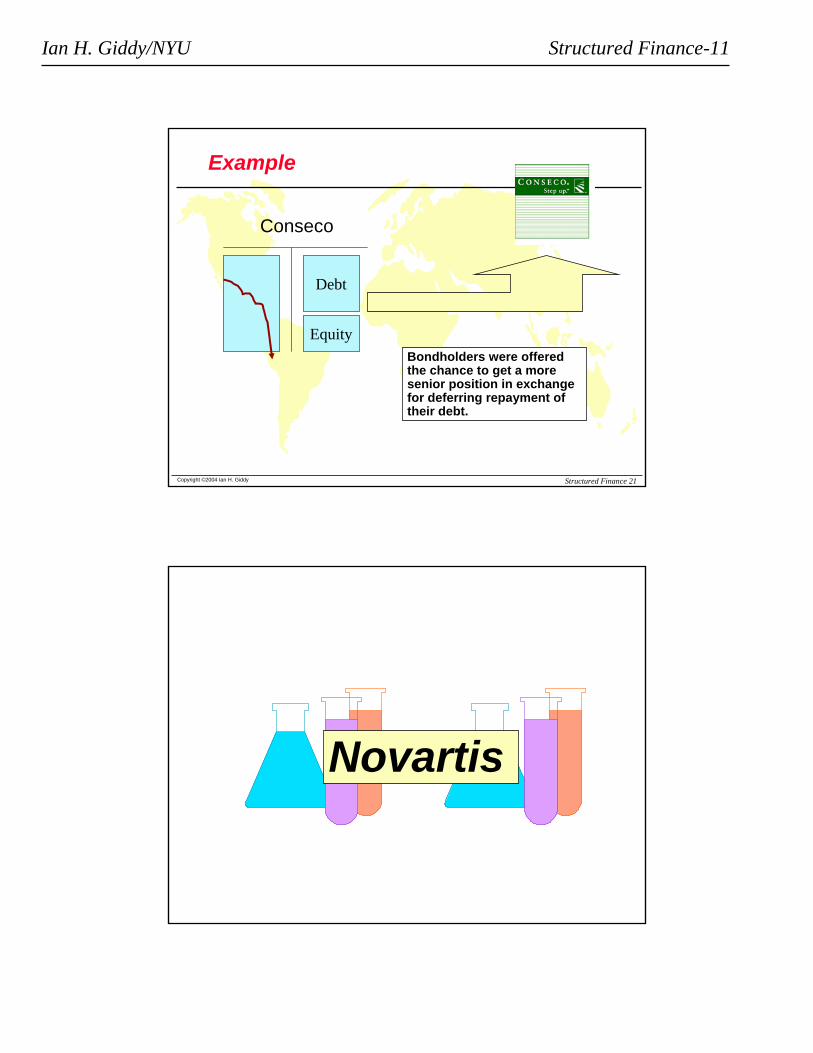

Example

Conseco

Debt

EquityBondholders were offered the chance to get a more senior position in exchange for deferring repayment of their debt.

Novartis

Ian H. Giddy/NYU Structured Finance-12

Copyright ©2004 Ian H. Giddy Structured Finance 23

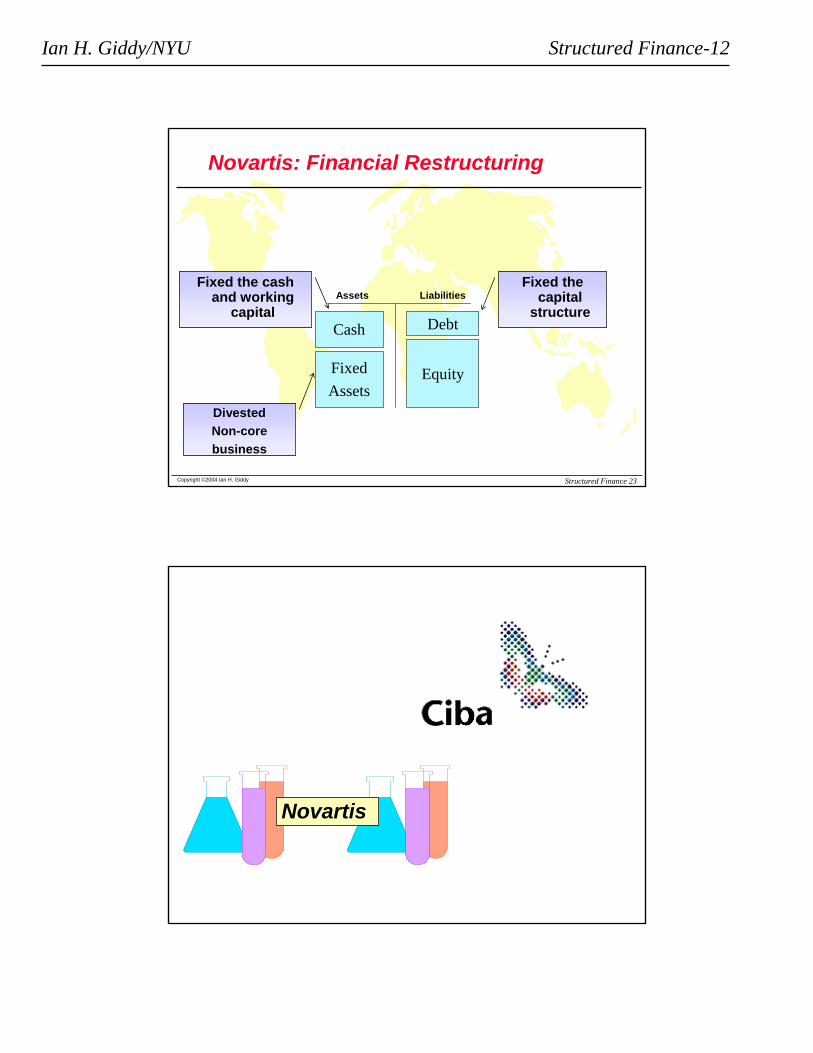

Novartis: Financial Restructuring

FixedAssets

Debt

Equity

Assets LiabilitiesFixed the cash

and working capital

Fixed the capital

structureCash

DivestedNon-corebusiness

Novartis

Ian H. Giddy/NYU Structured Finance-13

Copyright ©2004 Ian H. Giddy Structured Finance 25

Financial Restructuring

The increase in value that comes from a purely financial effect:Lower taxesHigher debt capacityBetter use of idle cash

Copyright ©2004 Ian H. Giddy Structured Finance 26

Corporate Restructuring:It’s All About Value

How can corporate and financial restructuring create value?

OperatingCashFlows

Debt

Equity

Assets Liabilities

Fix the business

Or fix the financing

Ian H. Giddy/NYU Structured Finance-14

Copyright ©2004 Ian H. Giddy Structured Finance 27

Restructuring Checklist

What mix of debt is best suited to this business?

Fix the kind of debt or hybrid financing

What can be done to make the equity more valuable to investors?

Fix the kind of equity

Value the changes new control would produce

Fix management or control

Revalue firm under different leverage assumptions – lowest WACC

Fix the financing – improve D/E structure

Value the merged firm with synergies

Fix the business – strategic partner or merger

Value assets to be soldFix the business mix – divestitures

Use valuation model – present value of free cash flows

Figure out what the business is worth now

Copyright ©2004 Ian H. Giddy Structured Finance 28

Getting the Financing RightStep 1: The Proportion of Equity & Debt

Debt

Equity

Achieve lowest weighted average cost of capitalMay also affect the business side

Ian H. Giddy/NYU Structured Finance-15

Copyright ©2004 Ian H. Giddy Structured Finance 29

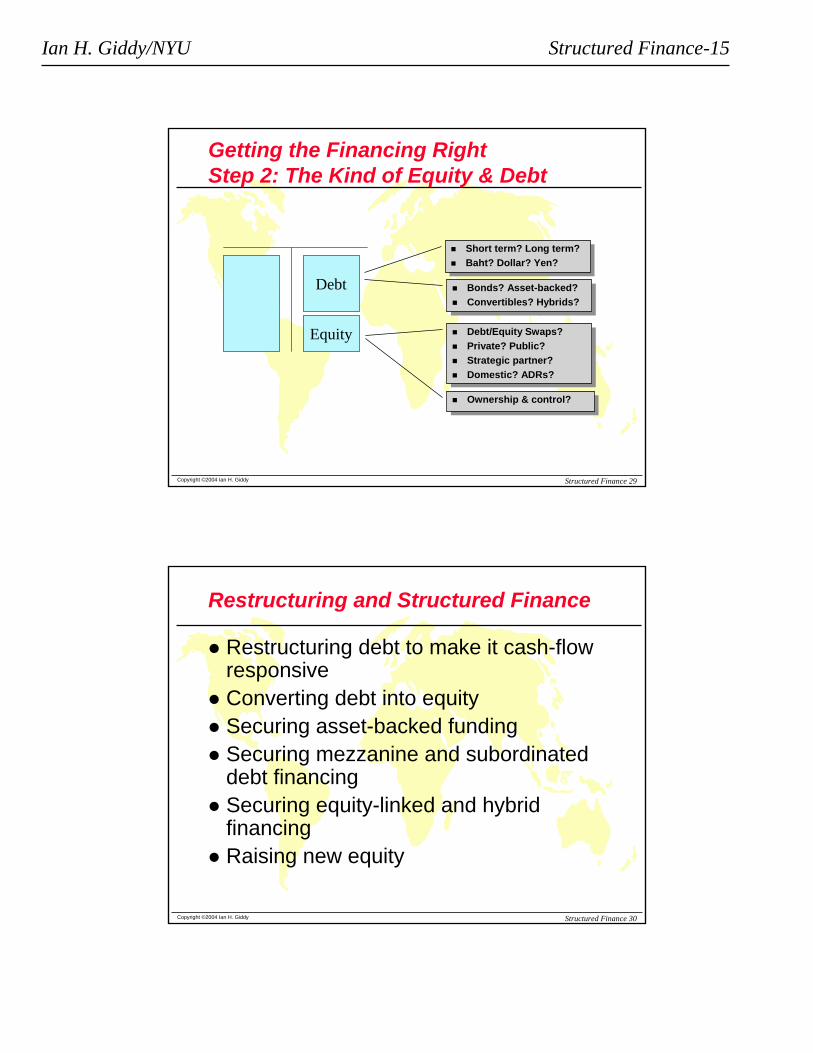

Getting the Financing RightStep 2: The Kind of Equity & Debt

Debt

Equity

Short term? Long term?Baht? Dollar? Yen?

Short term? Long term?Baht? Dollar? Yen?

Bonds? Asset-backed?Convertibles? Hybrids?

Bonds? Asset-backed?Convertibles? Hybrids?

Debt/Equity Swaps?Private? Public?Strategic partner?Domestic? ADRs?

Debt/Equity Swaps?Private? Public?Strategic partner?Domestic? ADRs?

Ownership & control?Ownership & control?

Copyright ©2004 Ian H. Giddy Structured Finance 30

Restructuring and Structured Finance

Restructuring debt to make it cash-flow responsiveConverting debt into equitySecuring asset-backed fundingSecuring mezzanine and subordinated debt financingSecuring equity-linked and hybrid financingRaising new equity

Ian H. Giddy/NYU Structured Finance-16

Copyright ©2004 Ian H. Giddy Structured Finance 31

The Challenge

Solving corporate financing problems by creating securities that are responsive to investors’ and issuers’ needs, constraints and views.Example: Getronics (how did this work?)

Copyright ©2004 Ian H. Giddy Structured Finance 32

Ian H. Giddy/NYU Structured Finance-17

Copyright ©2004 Ian H. Giddy Structured Finance 33

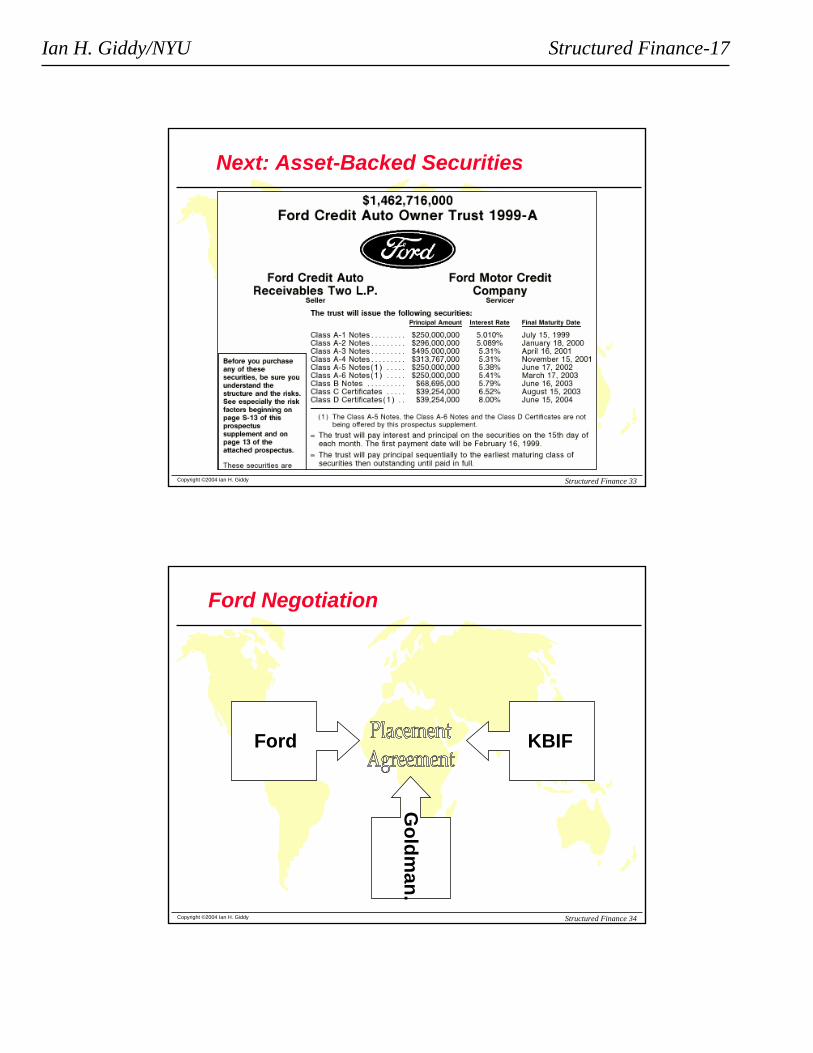

Next: Asset-Backed Securities

Copyright ©2004 Ian H. Giddy Structured Finance 34

Ford Negotiation

Ford KBIF

Goldm

an.

Ian H. Giddy/NYU Structured Finance-18

Copyright ©2004 Ian H. Giddy Structured Finance 35

Ford In-Class Negotiation Assignment

Three teams:Ford: why does the ABS deal it make sense? What are the cost andfunding advantages?Goldman: how can I persuade both parties, and make good money onthis deal?Korean Bond Investment Fund: which tranche should I buy, if any?

Assignment:Study the Ford Motor Credit prospectus, and define the key differences among the securities being offeredNegotiate a placement agreement that specifies how much money Ford raises, and at what cost; and how much KBIF invests, and inwhich securitiesTurn in your Team Report (2 pages plus exhibits) listing the terms of the agreement by 6pm Friday 20th. (Send it by email to [email protected], with cc to [email protected])

Copyright ©2004 Ian H. Giddy Structured Finance 40

Contact Info

Ian H. GiddyNYU Stern School of BusinessTel 212-998-0426; Fax [email protected]://giddy.org