Embed Size (px)

Citation preview

Energy Policy 28 (2000) 297}309

Structural change in Europe's gas markets: three scenariosfor the development of the European gas market to 2020q

Andrew Ellis*, Einar Bowitz, Kjell RolandECON Centre for Economic Analysis, P.O. Box 6823 St. Olavs plass, N-0130 Oslo, Norway

Received 13 July 1999

Abstract

Against the background of the European Union's gas Directive, and the emergence of new players and markets in Europe's gassector, this paper explores how company actions could shape the future for the gas industry. Starting with an examination of companystrategies this paper develops three scenarios for the future: a `Gradual Transformationa scenario where a single European gas marketdevelops that is essentially oligopolistic in nature; a `Vertical Integrationa scenario, where upstream and downstream gas companiesmerge to form a vertically integrated gas supplier; and a `Pull the Pluga scenario, where the current market structure decomposes intoa competitive market. These scenarios are examined in terms of their impact on gas prices, demand and the distribution of gas rentalong the supply chain. The paper highlights the fact that the EU's gas Directive is not su$cient for the introduction of competitioninto Europe's gas markets, but that company actions will be the key determinant, and they may favour alternative marketstructures. ( 2000 Elsevier Science Ltd. All rights reserved.

Keywords: Natural gas; Gas market liberalisation; Third party access; Industry structure

1. Introduction

Although liberalisation of Europe's energy marketshas been a common theme for the past ten years or more,it is only now that the gas industry is being opened up tocompetition. The European Union's gas Directive is pav-ing the way for a third of the EU's natural gas market tobe opened to competition, but even before the Directivecomes into force there is a momentum developing forstructural changes to Europe's gas industry.1 Newplayers and new markets have emerged onto the Euro-pean stage, from power generation companies and thedevelopment of gas-"red generation, to upstream gas

qThe article is the outcome of the project `Internationalisation andStructural Change in the European Gas marketa "nanced by theresearch council of Norway. A more detailed exposition of the resultsare given in Ellis et al. (1999).

*Corresponding author. Tel.: 0033-14887-4481; fax: 0033-14887-4482.

E-mail address: [email protected] (A. Ellis)1See e.g. Estrada et al. (1995) for a historical outline of the European

gas industry. See also Stoppard (1996) who focuses on structural cha-nges in the market.

companies keen to explore downstream opportunities.Existing companies are having to rise to the challengesposed by these new players and new markets and arethemselves part of the process of change. Mergers andacquisitions, vertical and horizontal integration, newmarketing approaches and alliances with other energyproviders are all part of today's gas industry. This isalready a di!erent world from just a few years ago, butwhat of the future? Where are these various pressures forchange taking the European gas industry?

This paper explores how these forces for change con-tain the genesis for radically di!erent market structures,and the key drivers in their development. Three alterna-tive scenarios are constructed, but all are predicated oncompany actions driving the changes, rather than regula-tory and legislative changes forcing through the changes.In this sense continental Europe does not follow the`Anglo-Saxona model towards liberalisation, as we be-lieve there is less political will in the rest of Europe for thetough regulatory approach adopted in the US and UK.In most European countries, the energy industry is stillviewed as strategically important, and although the pol-icy agenda has widened, issues such as security of supplyremain and have been supplemented by environmental

0301-4215/00/$ - see front matter ( 2000 Elsevier Science Ltd. All rights reserved.PII: S 0 3 0 1 - 4 2 1 5 ( 0 0 ) 0 0 0 1 3 - 6

2Source: IEA energy balances.

3A common held industry view articulated by the InternationalEnergy Agency (1998) amongst others.

4See Estrada et al., 1995 and Radetzki (1990, 1999) amongst others.

concerns that mean energy is not simply an adjunct toeconomic competitiveness. That is not to say that com-petition is not a factor in Europe's future gas markets,but it is more likely that pressure will come fromcompanies and not be imposed by governments. Regula-tory action is, therefore, not in the vanguard of change,but reacting to market pressure.

Starting with an examination of company strategiesthis paper develops three scenarios for the future:A Gradual Transformation scenario where a single Euro-pean gas market develops that is essentially oligopolisticin nature; a Vertical Integration scenario, where up-stream and downstream gas companies merge to forma vertically integrated gas supplier; and a Pull the Plugscenario, where the current market structure decomposesinto a competitive market. These scenarios are examinedin terms of their impact on gas prices, demand and thedistribution of gas rent along the supply chain.

2. Current structure and pressures for change

The European gas industry has developed rapidly overthe past thirty years, with natural gas now accounting for20% of Western Europe's primary energy fuel mix, com-pared to 5% in 1970.2 The capital intensive nature of thegas industry, with large up-front investments in pipelines,compression stations, storage facilities, network con-struction and gas-"eld production, have led to a marketstructure that not only seeks to spread the risk along thegas chain and over time, but also to balance the marketpower between producers and consumers.

Gas supply companies have been able to pool con-sumer demand by acquiring supply concessions or mon-opoly distribution rights to a particular region/country.This has enabled these supply companies to sign long-term contracts (10}20 yr) that have reduced the uncer-tainties for the gas producers concerning the volume ofgas they can sell. The reduction in market risk andpooling of potential consumers have encouraged the de-velopment of the required gas infrastructure and hasincreased the bargaining position of the gas supply com-pany in its negotiations with the gas producers.

The producers for their part have tended to take on theprice risk, by adjusting the price that they sell the gas inline with the price of competing fuels (mainly oil prod-ucts). This has meant that supply companies have beenable to maintain the price of gas at a level that is competi-tive with competing fuels, while minimising the impact onoperating margins of price variations. Monopoly gassupply companies have been subject to government/regulatory control to ensure that all the bene"ts of themonopolist are not completely captured in higher pro"ts

for the company, but are also re#ected in consumerprices.

This pattern of development has ensured that gas hasentered the European energy market at competitiveprices, while spreading and reducing the risks associatedwith the high capital costs along the gas chain. Thismodel is suitable for newly developing gas markets wherethere is no, or limited, gas infrastructure, but it has beenquestioned in the context of a mature market, wherethe initial investments have long been amortised andwhere existing gas supply companies face virtually novolume risk, at least by historical standards. In thiscontext, the main risk is associated with the price theproducer's receive for their gas.

However, the factors that supported this market struc-ture are shifting, and primarily because the economicsare changing. Pressures are coming from a number ofdi!erent sources including the fact that:

f The distribution of market risks have shifted as Euro-pe's gas industry has matured, which has reduced thevolume risk while the price risk remains. As a result,there is currently more of a price risk than a volumerisk.3

f Gas rent has shifted downstream as wholesale gasprices have fallen on the back of lower oil prices, whiledownstream margins have been maintained encourag-ing gas producers to chase the gas rent down the chain(International Energy Agency, 1998).

f Technological changes have opened a new market fornatural gas in base-load power generation, while in-formation technology developments have created newopportunities for gas trading and marketing * BTUvendors and Super Utilities are bundling services to-gether to o!er complete energy supply options or retailoptions to consumers. These new companies are ex-ploiting complementarities between energy marketsand other utility services as well as supply-side syner-gies to o!er least cost options to consumers and chal-lenge existing supply structures (Ellis et al., 1999).

f New players have entered the gas sector and haveattempted to contract for their gas supplies directlywith producers circumventing traditional gas sup-pliers;4

f Privatisation, mergers and acquisitions are changingthe ownership and way companies view the gas sector,as well as focusing on maximising company values(Ellis et al., 1999).

f Changes in national and super national energy policieshave reduced the emphasis on security of supplyand boosted the importance of competitiveness and

298 A. Ellis et al. / Energy Policy 28 (2000) 297}309

5See Stern (1998) amongst others.6Based on estimates from Cedigaz (News Report 7/8/98)7See Odell (1997) and Stern (1998) amongst others.8Various authors have made this point, including articles in Euro-

pean Gas Matters and the FT Gas Report.

9Long-term is used in the economic sense where "xed costs becomevariable (i.e. the time-frame for investments), which in the gas marketare the economic life of the infrastructure* approximately 10}20 yrs.

environmental issues, which have questioned the mon-opoly position of many of Europe's gas supply com-panies. The EU gas Directive, as well as nationallegislation, is opening up the European gas market andleading to competition between existing national sup-ply companies, foreign supply companies and newentrants;5

f Supply availability exceeds European demand* ma-jor pipeline developments are occurring across West-ern Europe based on long-term contracts. However, inthe short-term these pipelines have spare capacity thatcould be utilised to bring existing spare productioncapacity to Europe from the UK and Russia, the later'sannual surplus production capacity is put at 70 BCM6

(15% of Europe's total annual demand, around two-thirds of Russia's current exports to Europe);7

f The development of a European spot gas market facil-itated by the Bacton}Zeebrugge interconnector o!ersthe potential of an alternative price setting mechanismto the current long-term take-or-pay contracts * thecurrent gas bubble could emerge on a European spotmarket.8

It can be seen, therefore, that the EU gas liberalisationprocess, and other government action designed to open upthe gas markets to increased competition, is just one of thepressures being brought to bear on the current marketstructure. The majority of the pressures stem from com-pany actions initiated by other market developments,independent of initiatives to liberalise the gas industry.

3. Company actions lead policy makers

It could be argued that at the heart of the EU's gasliberalisation process is the belief that legislative actionwill alter the structure of the industry changing companybehaviour and the overall performance/competitivenessof the industry * a structure-conduct-performancemodel for instituting change in the gas sector (the SCPmodel, Bain (1956)). The EU believes that the introduc-tion of third-party access (TPA) will change the structureof the industry by lowering the barriers to entry, enablingnew gas supply companies to enter the industry. This willchange the way the existing companies do business, andin theory lead to a much more e$cient and competitivemarket structure.

The EU is not alone in this approach to market re-form, with both the US and the UK engaged in, what has

turned out to be, a long series of regulatory changes aspolicy makers have tried to create the conditions forcompetition to reign. This unfolding regulatory processcontinues today in both the US and UK. The fact thatthere has been a series of regulations indicates that, toa certain extent, legislators have found it di$cult tolegislate for a competitive market. This not only ques-tions the emphasis on policies to change market struc-tures, but suggests that if the EU follows the UK and USpath, then the current gas Directive will be only the "rstin a series of legislative measures.

However, there are reasons to believe that continentalEurope will be less keen to embark on the legislativeroad, and that the SCP model behind this approach ismisplaced. At the heart of our view of gas market devel-opments is the belief that the balance of power betweengovernments and companies is fundamentally di!erent incontinental Europe, compared to the UK and the USwhere there is more of a tradition of government regula-tion of the market. In continental Europe, governmentin#uence has been exercised through the boardroom andgovernment ministries rather than a regulatory body. Itis, in our opinion, unlikely that the continental Europeangovernments will willingly undertake a more pro-activeregulatory role, and the balance of power will increasing-ly rest with the actors in the market; privatisation is alsoreducing the power of ministers.

To a certain extent we can see the continental Euro-pean governments adopting a Schumpeterian (Schum-peter, 1954) view of market developments. Namely thatthe pro"tability and relative market security under mon-opoly and oligopoly are important enabling conditionsfor companies to undertake risky and high cost invest-ments, such as development of a gas network, and arenecessary and acceptable conditions. Competition is notcompletely lacking in this model, but is manifest in a dif-ferent manner than that described in neoclassical eco-nomic theory.

Competition occurs in the Schumpeterian worldthrough the mere threat that other companies may o!erlower prices and take consumers away from an incum-bent supplier (i.e. a form of Bertrand competition,Bertrand et al. (1883)). As a result, the monopoly com-pany prices its product to prevent new market entrants,which may be closer to the intersection of its average costand average revenue than its marginal cost and marginalrevenue, and therefore closer to a neoclassical competi-tive price than a monopoly price. Under these conditionsthere is less of a requirement for governments to inter-cede in the market, so long as there are no long-term9

barriers to entry * to do so would impose economic

A. Ellis et al. / Energy Policy 28 (2000) 297}309 299

10This is already occurring in the UK with the development ofbase-load gas-"red power generation, which is creating a new marketand introducing a new set of gas consumers who are challenging theexisting supply structure.

costs on the industry. It may be questionable whether itcan be assumed that there are no long-term barriers toentry, although the EU single market programme shouldhelp ensure that condition is met.

What is important, is to understand the dynamicsinvolved in the development of a particular market struc-ture. This means that, unlike the SCP model, we need toplace the "rm at the centre of our analysis, to see how itseeks to mould its market environment and how it com-petes against other "rms. By understanding the collectivebehaviour of "rms we can see how government policiesmay attempt to change that behaviour to achieve a givenpolicy objective. Attempting to implement changes to thestructure without changing the behaviour of the "rms islikely to fail precisely because the "rms' will attempt tothwart such changes.

In the context of the European gas industry we can seethat there are very good economic reasons supportingthe current market structure * large up front capitalcosts, networks that constitute a major economic invest-ment, the interdependence of upstream and downstreamrisks and a balance of market power between consumersand producers * that represent strong forces againstchange. Simply allowing TPA will not diminish or re-move those forces, since TPA does not remove theireconomic rationale. Incumbent companies will continueto operate in a manner that largely supports the currentstructure and therefore limits the impact of the legislativereforms. All that the EU directive has achieved is to openthe door for change within the current market structure,it does not mean that the industry will willing enter. Forchange to occur new actors will need to take advantageof the opportunity opened up by the EU legislation andenter the gas market. These new players may have a dif-ferent set of conducts and performances that challengethe existing structure,10 but this is by no means certain.

4. Company strategies and alternative market scenarios

4.1. Pro-active versus defensive strategies

When considering the actions of the various marketplayers and their strategies, we need to bear in mind thatcompany strategies are primarily driven by the need toreduce risks and uncertainties and to maximise theirpotential. This fundamental behaviour provides themotive to reduce costs, maximise pro"ts and enhancethe company's value. In addition, companies' strategiesare also formed by the need for defensive and proactive

objectives, formulated in the face of competition, marketopportunities and changes in the regulatory regime.

Defensive objectives may be to preserve market shareand power as well as prevent competitors entering an-other company's market. Proactive objectives are to tryand acquire market share, increase the company's marketvalue and its pro"tability. In any situation there area combination of defensive and proactive actions takingplace as companies compete. The strategic decisionstaken by the market players will re#ect the balance be-tween their need to take defensive and proactive actions.Determining the balance between players is the key tothe market changes. Can the major downstream playersaccommodate the aspirations of upstream companies tomove down the gas chain, or will the actions of theupstream players undermine the existing downstreamcompanies and the structures built around them? Canexisting supply companies meet the needs of a new set ofgas consumers, or do new marketing techniques heraldtheir demise?

The type of pro-active and defensive actions that canbe undertaken by "rms are:

f Erecting barriers to entry* where existing companiesseek to prevent other companies entering their indus-try by raising the entry costs or preventing them gain-ing access to their customers. TPA is an attempt toreduce the barrier to entry posed by the large cost oflicensing and building a gas pipeline. However, thereare other techniques for raising the barriers to entrythat may partly o!set TPA, including the terms ofaccess to a company's pipeline (e.g. hourly balancingand minimum contract lengths), cumulative discountsand contract extensions, as well as the transportationtari!s themselves.

f Horizontal integration * where companies formjoint ventures or acquire companies performingsimilar tasks in adjacent markets (for example,Germany's Ruhrgas moving into gas supply in CentralEurope);

f Unbundling/demerger* where companies choose tospecialise in one segment of the gas chain;

f Mergers & acquisitions * where companies expandinto a new market by merging or acquiring an existingcompany already operating in that market. This hasthe advantage of overcoming some of the barriers toentry that may have stood in the way of a simple entryinto the new market. However, an increase in mergerand acquisition activity could lead to companies plac-ing greater importance on the company value, possiblyto the detriment of employees and consumers (reducedwages and bene"ts for employees, higher prices forconsumers);

f Lateral integration * where a company seeks to di-versify into an adjactent industry where it feels it hasa comparative advantage and where there are links in

300 A. Ellis et al. / Energy Policy 28 (2000) 297}309

11 In determining the market impact of these strategies we draw onthe works of Cournot (1838), Golombek et al. (1995, 1996), Philips(1998), Schmalensee (1982), Spengler (1950), Sutton (1991) and Sweezy(1939).

demand and supply between the two industries (e.g.power generation, or electricity retailing);

f Vertical integration * where one company seeks tocontrol the entire gas chain and allocate risks andreturns within one company.

We have already noted that these actions tend not tobe mutually exclusive and an individual company strat-egy may involve one or more of these actions. Drawingtogether a number of common strategies will enable us todevelop alternative scenarios for the market as a whole.We have put together three scenarios that emerge fromthe company strategies.11

4.2. Gradual Transformation scenario

In this scenario the major existing players, to a largeextent, manage to contain the emerging competitive ten-dencies in the gas market and stabilise the structure ofa small number of large transmission companies. One ofthe key assumptions behind this scenario is that competi-tion is largely limited to the existing T & D companies.New companies wishing to enter the market are pre-vented from doing so by the economies of scale requiredto compete with the existing players* the large up frontcapital costs that are only marginally diminished by TPA* and limited access to additional supplies. Gas pro-ducers are unwilling to jeopardise existing gas contractsby providing gas to the competitors of the existing T&Dcompanies who the producers are currently supplying.

The possibility of producers displacing existing con-tracts with new supplies at possibly lower prices is furtherreduced if producers perceive that there is little room foradditional gas demand beyond that already contracted.In addition, existing T&D companies can be expected toerect further barriers to trade to protect their existingconsumer base and their existing capital investments.Companies wishing to enter the market may be left withthe prospect of "ghting for TPA in the courts or buildingtheir own pipeline network: both are time consuming andexpensive.

Overcoming the barriers to trade and accessing themarket can, however, be achieved by acquiring an exist-ing T&D company. This is as true for new companieswishing to enter the market as it is for existing companieswishing to restrict the number of competitors or to ex-pand into a new market. This appetite for mergers andacquisitions could also be encouraged by the possibleprivatisation of some of the publicly owned T&D com-panies. Privatisation could provide a relatively easy way

for new or existing companies to enter new marketswithout leading to a signi"cant increase in the number ofT&D companies or a change in the market structure.

Adopting the mergers and acquisitions route to com-pany expansion will result in greater emphasis beingplaced on the market value of the T&D companies. Thiscould have a quite profound impact on the balance ofinterests between consumers, owners and employees, andtherefore on prices, margins and the distribution of gasrent. Dividend payments will tend to have a higher prior-ity than salaries or consumer prices. The threat ofa merger or acquisition could be su$cient to refocusa company on maximising company value by raising itspro"tability. E!orts would be expected to be made toreduce each company's costs, to eliminate x-ine$cienciesand seek better terms for wholesale gas supplies, as wellas seeking to maximise their producer surplus at theexpense of consumers. The gas producers may be willingto o!er better terms to gas supplies if the new contractsinvolve the T&D companies taking on more of the pricerisk. Meanwhile, the T&D companies may try to exploittheir captive market in order to compensate for anyrevenue losses su!ered in the eligible market: we couldsee a widening of the gap between prices in the eligiblemarket segment and those in the captive market.

A widening of the price di!erential between the eligibleand captive market segments could lead to calls forgreater regulation of the industry to stop exploitation ofcaptive markets. However, if this process occurs in a peri-od of low or falling wholesale gas prices then the fact thatthe captive market segment does not fully re#ect thechange in the wholesale price may be politically accept-able. In other words if consumers do not feel they arebeing exploited, because they are paying low or fallinggas prices, then there will be less concern that the T&Dcompanies are earning increasingly larger marginson sales to this segment of the market. Conversely,where there are rising wholesale prices then it may bemore di$cult for the T&D companies to exploit theircaptive markets without risking government action.

4.3. Vertical Integration Scenario

In this scenario the winning strategy is for companiesto control the entire gas chain and to seek vertical integ-ration. The upstream pressure for companies to gainaccess to downstream rents and exercise greater controlin a changing market environment, is matched by down-stream companies wishing to gain access to upstreamreserves, thus ensuring their future supplies and limitingthose available for potential downstream competitors.

A vertically integrated company may enjoy additionaleconomies of scale over existing companies, due to thefact that it is able to internalise the risks and spread themmore e$ciently along the gas chain (Spengler, 1950).Essentially, one large vertically integrated company

A. Ellis et al. / Energy Policy 28 (2000) 297}309 301

12Econ estimates.

holds price and volume risks, and it is assumed that thesum of the two risks is less than their individual parts (i.e.holding the price risk can help o!set the volume risk). Inaddition, a vertically integrated company may be betterpositioned to take advantage of arbitrage opportunitiesbetween markets and to exploit its knowledge of thecomplete gas chain.

Vertical integration, under this scenario, can be ex-pected to extend down to sales of gas to the power sectorand large industrial users, it may even extend into thesmall industrial, commercial and residential sectors.However, it is quite likely that local distributioncompanies (LDCs) will remain to serve the small gasconsumers. This will be especially true if the verticallyintegrated company is able to acquire most of the rentfrom sales to the small gas consumers due to its role asthe main, or sole, source of supplies to the LDC.

In theory, this vertically integrated structure need notbe any more concentrated than today's. However, inpractice it is likely to be so, unless gas producers likeGazprom and Sonatrach are broken up into a number ofproduction companies. This seems unlikely from today'sperspective. Gas supplies to Europe are expected to beproduced from a concentrated group of companies, cen-tred on Gazprom, Sonatrach, Shell/Exxon and Statoil,which together are expected to account for aroundthree-quarters of Europe's gas production by 2020.12It is likely that any integration of these companiesdownstream will involve a number of existing T&D com-panies such that a more concentrated market structureemerges.

Overall, the balance of interest will largely lie withowners (and possibly employees) at the expense of con-sumers. In other words, where possible, the verticallyintegrated company will attempt to exploit any monop-oly power its has. This should lead to higher margins onend-use sales, including sales to LDCs. The verticallyintegrated company may have greater incentives to cutcosts, since all the bene"ts in terms of pro"ts will accrueto the company. Nevertheless, certain consumers maygain relative to today's market structure as the lower coststructure should lead to higher output and lower prices ifthe vertically integrated company seeks to maximisepro"ts and if the current T&D company is a pro"tmaximising monopoly.

4.4. Pull-the-Plug scenario

In this scenario we assume that e!orts to erect barriersto entry and restrict new entrants are not the success-ful strategies. New companies are able to enter the mar-ket, but their success rests on being able to o!er lowerprices to consumers. Given that there are monopoly

pro"ts currently being earnt, there appears to be roomfor new companies to o!er price cuts but this begsthe question where will the gas supplies come from giventhat existing long-term contracts cover today's gas re-quirements?

As we noted earlier, there is currently an excess supplyavailability that could be tapped into, but in the short-to-medium term any new gas would displace existinglong-term contracted volumes. It could be that a singlegas producer displaces gas sales from one set of T&Dcompanies and shift it to another with no net volumegain. Alternatively, competition between gas producerscould encourage one producer to increase sales in thebelief that they will displace another producer's supplies.The displaced volumes will either have to be absorbed bythe gas producers or made available, possibly via a spotmarket, at lower prices.

Whatever the mechanism, this scenario requires thegas bubble to be brought to market. Initially those lowcost supplies could be the UK gas bubble arriving atZeebruK gge, but subsequently it would be Russia's gasbubble. It is the arrival of the Russian gas bubble thatposes the serious threat to the existing long-term contractmarket. Therefore, the actions of Gazprom are decisive indetermining the outcome of this scenario.

It is one thing to have low cost gas, but it is quiteanother to equate it with end-use markets. ExistingT&D companies, tied to long-term contract gas, arelikely to be resistant to allowing competitors to usetheir pipelines to deliver gas to their customers atlower prices. In this scenario, eligible and would-be eli-gible customers along with new supply companies haveto argue strongly for more transparency and easieraccess to these low cost sources of gas. Recourse to thecourts or the regulatory authorities will be necessaryto ensure real access and ultimately it may requiregreater government involvement to ensure that lowerwholesale gas prices are passed through to consumersand competition between distribution companies isbrought about.

Competition could ensure that the price customers arecharged for their gas re#ects the marginal cost of supply.This competitive market means that companies areforced to compete on prices and to that extent con-sumers interests increase relative to those of owners andemployees (i.e. relative to dividends and salaries).However, a proliferation of downstream companies sup-plying gas could lead to a shift in the balance of marketpower towards the producers who are able to exploitthis power to capture some of the bene"ts accruing toconsumers.

This scenario leads to a much more competitive mar-ket environment, but to achieving it requires greaterregulatory control. In other words, regulated TPA needsto be introduced, where there is an integrated transmis-sion and distribution company, to ensure equal access to

302 A. Ellis et al. / Energy Policy 28 (2000) 297}309

13Model structure and elasticities draw on earlier work by Econ(1990, 1997A) and others (Atkinson and Manning, 1995; Brubakk et al.,1995).

the transmission network. Essentially the monopolytransmission (high pressure and low pressure) compon-ent of the gas chain has to be isolated from the potentiallycompetitive supply and production components. Themonopoly component then needs to be regulated toensure it does not exploit its position, whether it operatesas part of a T&D company or as an independent unbun-dled entity in its own right. Although there is currentlylittle political will to intervene in continental Europe'sgas markets, in the medium term this may change. Thisscenario requires that greater regulatory controls areintroduced after 2005 to enable consumers to gain accessto low-cost gas supplies.

4.5. Scenario Comparisons

The di!erent scenarios have radically di!erent marketstructures, but each emerges from company strategiesthat are present in today's gas market and are initiallyindependent of government action, beyond the introduc-tion of TPA. To that extent they are policy neutral,although they produce results that are more or lessfavourable for policy makers.

The Gradual Transformation scenario maintains theexisting market structure, but the behaviour of com-panies is radically di!erent as they balance the need topreserve their traditional consumer base with the desireto take advantage of new market opportunities. In thisscenario, the adage that `he who owns the consumercontrols the marketa is true, while the balance betweenupstream and downstream companies is more-or-lessmaintained* control of upstream reserves is less signi"-cant, however, in a period of excess supply availability. Inthe Vertical Integration scenario control of customers isnot su$cient to guarantee success, but must be joined bycontrol of supplies. This greater control from the well-head to burner tip lowers the risk premium on invest-ments and should lead to lower costs, although primarilyto the bene"t of the company and less so to consumers.The Pull-the-Plug scenario leads to the most competitivedownstream market structure, but in the long-term mar-ket power shifts towards the producers (i.e. by about2010). Nevertheless, prices, costs and margins are ex-pected to be the lowest of all the scenarios, even in thelong term, due to the intense competitive pressure experi-enced in the short term.

5. Market implications

5.1. Modelling approach

The scenarios may give rise to widely di!erent out-comes as regards prices, quantities and revenues alongthe gas chain. We have illustrated the possible outcomesby utilising a numerical model of the European gas

market (see Econ, 1997B). End-user prices of gas aregenerated by sector and country-speci"c mark-ups overborder prices, which vary between scenarios. The modeldescribes gas demand and transport tari!s in Germany,France, the Netherlands and Belgium in some detail (5demand sectors) while the rest of Continental and UKgas demands are given an aggregate treatment.13

The price sensitivity of demand varies across country,sector and time, e.g. entailing little short run but quitesubstantial long run price e!ects on demand. There aresmall price e!ects in countries where gas has alreadypenetrated the energy sector and stronger e!ects in coun-tries where there seems to be a noticeable growth poten-tial for the market share of gas (Germany and France).The e!ects are in general assumed to be larger in energy-intensive industry than in the service sector.

The scenarios di!er from each other and the presentsituation in the mechanisms governing the level of pricesand margins, and the e!ects of di!erent outcomes onincome distribution. We outline the quantitative di!er-ences between the scenarios by looking at border prices,downstream costs and margins, and the outcome in theform of end user prices, gas demand and pro"ts.

5.2. Border prices

The mechanisms determining border prices will di!erconsiderably between the scenarios. Up until now, long-term (up to 25 yr) contracts between national monopoliesin production and transmission have been negotiated.Each contract has generally consisted of a base price andan indexation clause where changes in oil, coal or con-sumer prices automatically trigger changes in the gasprice. In addition, the contracts include re-negotiationsclauses if the underlying market conditions changesigni"cantly.

Under the Gradual Transformation scenario, the exist-ing long-term gas contracts will continue into the future,with gas prices re#ecting changes in oil and coal prices.Gas prices for power generation will be priced accordingto the `indi!erence principlea, i.e. the gas price is set so asto make the buyer more or less indi!erent to choosinga coal "red plant. Other gas sales are priced accordingto the costs of using oil products as energy source;the market value principle. Since gas for power willincrease its share of total gas demand, there will in thelong run be an increasing discrepancy between averagegas and oil prices. A spot market could develop asa mechanism for pricing swing gas, and this componentcould be removed from the long-term gas contract.In this situation, long-term contracts would set the

A. Ellis et al. / Energy Policy 28 (2000) 297}309 303

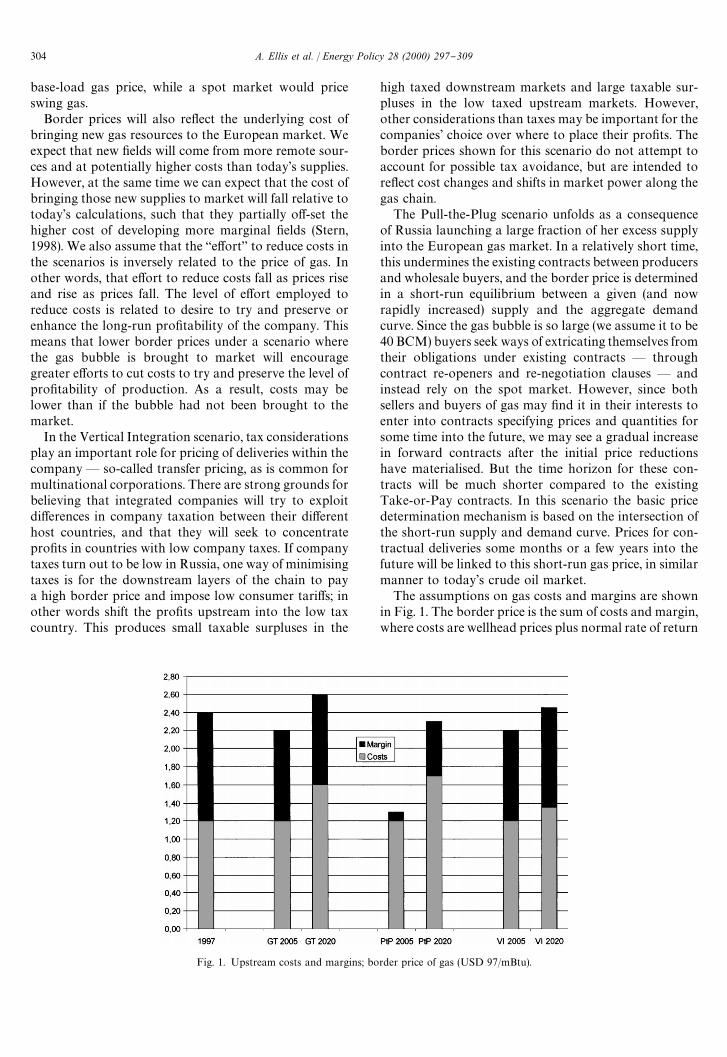

Fig. 1. Upstream costs and margins; border price of gas (USD 97/mBtu).

base-load gas price, while a spot market would priceswing gas.

Border prices will also re#ect the underlying cost ofbringing new gas resources to the European market. Weexpect that new "elds will come from more remote sour-ces and at potentially higher costs than today's supplies.However, at the same time we can expect that the cost ofbringing those new supplies to market will fall relative totoday's calculations, such that they partially o!-set thehigher cost of developing more marginal "elds (Stern,1998). We also assume that the `e!orta to reduce costs inthe scenarios is inversely related to the price of gas. Inother words, that e!ort to reduce costs fall as prices riseand rise as prices fall. The level of e!ort employed toreduce costs is related to desire to try and preserve orenhance the long-run pro"tability of the company. Thismeans that lower border prices under a scenario wherethe gas bubble is brought to market will encouragegreater e!orts to cut costs to try and preserve the level ofpro"tability of production. As a result, costs may belower than if the bubble had not been brought to themarket.

In the Vertical Integration scenario, tax considerationsplay an important role for pricing of deliveries within thecompany* so-called transfer pricing, as is common formultinational corporations. There are strong grounds forbelieving that integrated companies will try to exploitdi!erences in company taxation between their di!erenthost countries, and that they will seek to concentratepro"ts in countries with low company taxes. If companytaxes turn out to be low in Russia, one way of minimisingtaxes is for the downstream layers of the chain to paya high border price and impose low consumer tari!s; inother words shift the pro"ts upstream into the low taxcountry. This produces small taxable surpluses in the

high taxed downstream markets and large taxable sur-pluses in the low taxed upstream markets. However,other considerations than taxes may be important for thecompanies' choice over where to place their pro"ts. Theborder prices shown for this scenario do not attempt toaccount for possible tax avoidance, but are intended tore#ect cost changes and shifts in market power along thegas chain.

The Pull-the-Plug scenario unfolds as a consequenceof Russia launching a large fraction of her excess supplyinto the European gas market. In a relatively short time,this undermines the existing contracts between producersand wholesale buyers, and the border price is determinedin a short-run equilibrium between a given (and nowrapidly increased) supply and the aggregate demandcurve. Since the gas bubble is so large (we assume it to be40 BCM) buyers seek ways of extricating themselves fromtheir obligations under existing contracts * throughcontract re-openers and re-negotiation clauses * andinstead rely on the spot market. However, since bothsellers and buyers of gas may "nd it in their interests toenter into contracts specifying prices and quantities forsome time into the future, we may see a gradual increasein forward contracts after the initial price reductionshave materialised. But the time horizon for these con-tracts will be much shorter compared to the existingTake-or-Pay contracts. In this scenario the basic pricedetermination mechanism is based on the intersection ofthe short-run supply and demand curve. Prices for con-tractual deliveries some months or a few years into thefuture will be linked to this short-run gas price, in similarmanner to today's crude oil market.

The assumptions on gas costs and margins are shownin Fig. 1. The border price is the sum of costs and margin,where costs are wellhead prices plus normal rate of return

304 A. Ellis et al. / Energy Policy 28 (2000) 297}309

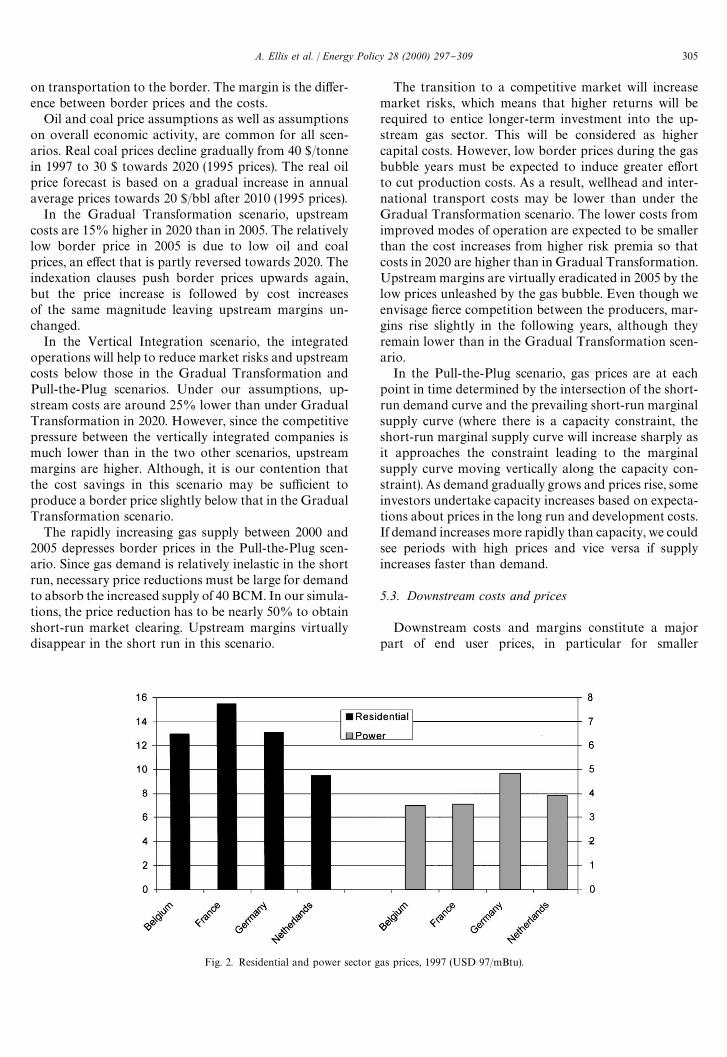

Fig. 2. Residential and power sector gas prices, 1997 (USD 97/mBtu).

on transportation to the border. The margin is the di!er-ence between border prices and the costs.

Oil and coal price assumptions as well as assumptionson overall economic activity, are common for all scen-arios. Real coal prices decline gradually from 40 $/tonnein 1997 to 30 $ towards 2020 (1995 prices). The real oilprice forecast is based on a gradual increase in annualaverage prices towards 20 $/bbl after 2010 (1995 prices).

In the Gradual Transformation scenario, upstreamcosts are 15% higher in 2020 than in 2005. The relativelylow border price in 2005 is due to low oil and coalprices, an e!ect that is partly reversed towards 2020. Theindexation clauses push border prices upwards again,but the price increase is followed by cost increasesof the same magnitude leaving upstream margins un-changed.

In the Vertical Integration scenario, the integratedoperations will help to reduce market risks and upstreamcosts below those in the Gradual Transformation andPull-the-Plug scenarios. Under our assumptions, up-stream costs are around 25% lower than under GradualTransformation in 2020. However, since the competitivepressure between the vertically integrated companies ismuch lower than in the two other scenarios, upstreammargins are higher. Although, it is our contention thatthe cost savings in this scenario may be su$cient toproduce a border price slightly below that in the GradualTransformation scenario.

The rapidly increasing gas supply between 2000 and2005 depresses border prices in the Pull-the-Plug scen-ario. Since gas demand is relatively inelastic in the shortrun, necessary price reductions must be large for demandto absorb the increased supply of 40 BCM. In our simula-tions, the price reduction has to be nearly 50% to obtainshort-run market clearing. Upstream margins virtuallydisappear in the short run in this scenario.

The transition to a competitive market will increasemarket risks, which means that higher returns will berequired to entice longer-term investment into the up-stream gas sector. This will be considered as highercapital costs. However, low border prices during the gasbubble years must be expected to induce greater e!ortto cut production costs. As a result, wellhead and inter-national transport costs may be lower than under theGradual Transformation scenario. The lower costs fromimproved modes of operation are expected to be smallerthan the cost increases from higher risk premia so thatcosts in 2020 are higher than in Gradual Transformation.Upstream margins are virtually eradicated in 2005 by thelow prices unleashed by the gas bubble. Even though weenvisage "erce competition between the producers, mar-gins rise slightly in the following years, although theyremain lower than in the Gradual Transformation scen-ario.

In the Pull-the-Plug scenario, gas prices are at eachpoint in time determined by the intersection of the short-run demand curve and the prevailing short-run marginalsupply curve (where there is a capacity constraint, theshort-run marginal supply curve will increase sharply asit approaches the constraint leading to the marginalsupply curve moving vertically along the capacity con-straint). As demand gradually grows and prices rise, someinvestors undertake capacity increases based on expecta-tions about prices in the long run and development costs.If demand increases more rapidly than capacity, we couldsee periods with high prices and vice versa if supplyincreases faster than demand.

5.3. Downstream costs and prices

Downstream costs and margins constitute a majorpart of end user prices, in particular for smaller

A. Ellis et al. / Energy Policy 28 (2000) 297}309 305

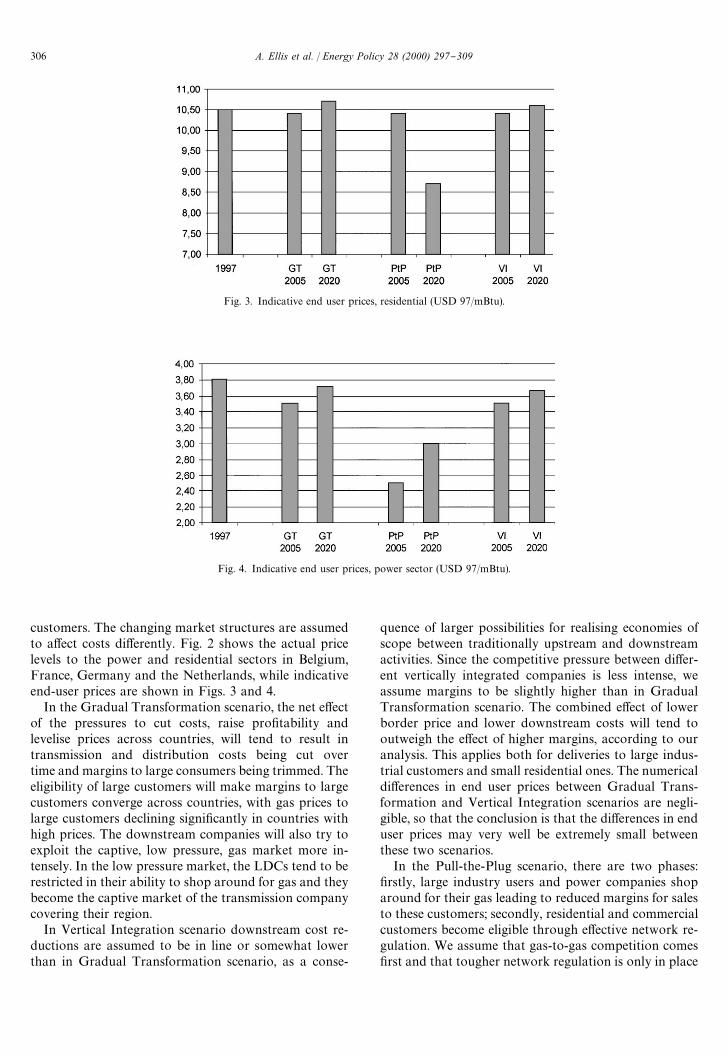

Fig. 3. Indicative end user prices, residential (USD 97/mBtu).

Fig. 4. Indicative end user prices, power sector (USD 97/mBtu).

customers. The changing market structures are assumedto a!ect costs di!erently. Fig. 2 shows the actual pricelevels to the power and residential sectors in Belgium,France, Germany and the Netherlands, while indicativeend-user prices are shown in Figs. 3 and 4.

In the Gradual Transformation scenario, the net e!ectof the pressures to cut costs, raise pro"tability andlevelise prices across countries, will tend to result intransmission and distribution costs being cut overtime and margins to large consumers being trimmed. Theeligibility of large customers will make margins to largecustomers converge across countries, with gas prices tolarge customers declining signi"cantly in countries withhigh prices. The downstream companies will also try toexploit the captive, low pressure, gas market more in-tensely. In the low pressure market, the LDCs tend to berestricted in their ability to shop around for gas and theybecome the captive market of the transmission companycovering their region.

In Vertical Integration scenario downstream cost re-ductions are assumed to be in line or somewhat lowerthan in Gradual Transformation scenario, as a conse-

quence of larger possibilities for realising economies ofscope between traditionally upstream and downstreamactivities. Since the competitive pressure between di!er-ent vertically integrated companies is less intense, weassume margins to be slightly higher than in GradualTransformation scenario. The combined e!ect of lowerborder price and lower downstream costs will tend tooutweigh the e!ect of higher margins, according to ouranalysis. This applies both for deliveries to large indus-trial customers and small residential ones. The numericaldi!erences in end user prices between Gradual Trans-formation and Vertical Integration scenarios are negli-gible, so that the conclusion is that the di!erences in enduser prices may very well be extremely small betweenthese two scenarios.

In the Pull-the-Plug scenario, there are two phases:"rstly, large industry users and power companies shoparound for their gas leading to reduced margins for salesto these customers; secondly, residential and commercialcustomers become eligible through e!ective network re-gulation. We assume that gas-to-gas competition comes"rst and that tougher network regulation is only in place

306 A. Ellis et al. / Energy Policy 28 (2000) 297}309

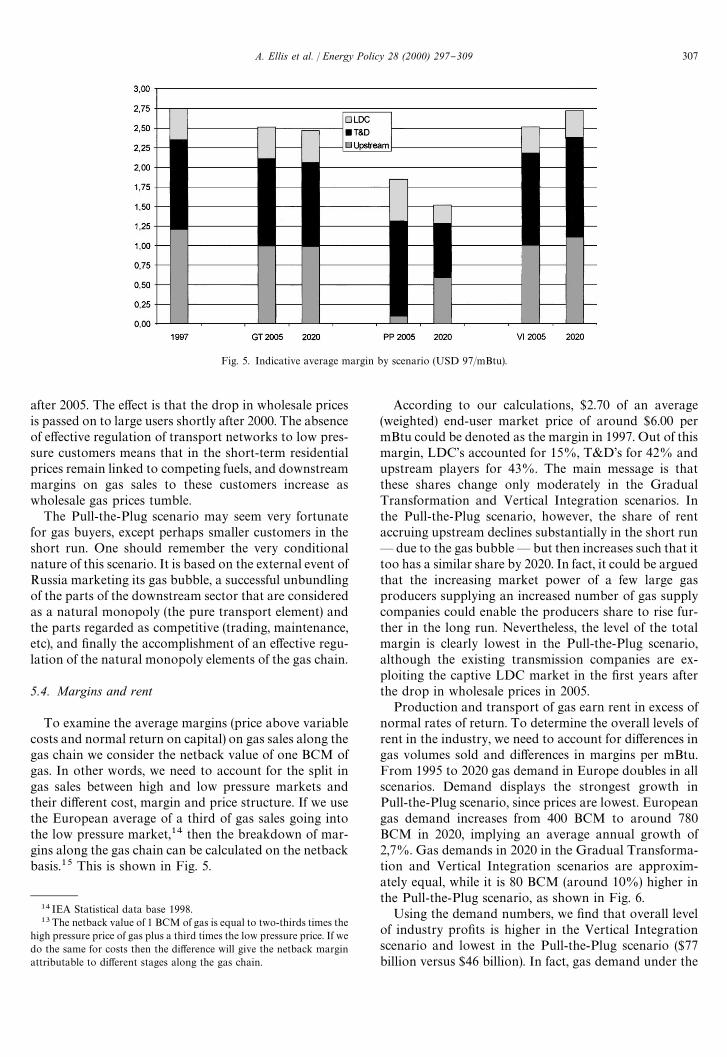

Fig. 5. Indicative average margin by scenario (USD 97/mBtu).

14 IEA Statistical data base 1998.13The netback value of 1 BCM of gas is equal to two-thirds times the

high pressure price of gas plus a third times the low pressure price. If wedo the same for costs then the di!erence will give the netback marginattributable to di!erent stages along the gas chain.

after 2005. The e!ect is that the drop in wholesale pricesis passed on to large users shortly after 2000. The absenceof e!ective regulation of transport networks to low pres-sure customers means that in the short-term residentialprices remain linked to competing fuels, and downstreammargins on gas sales to these customers increase aswholesale gas prices tumble.

The Pull-the-Plug scenario may seem very fortunatefor gas buyers, except perhaps smaller customers in theshort run. One should remember the very conditionalnature of this scenario. It is based on the external event ofRussia marketing its gas bubble, a successful unbundlingof the parts of the downstream sector that are consideredas a natural monopoly (the pure transport element) andthe parts regarded as competitive (trading, maintenance,etc), and "nally the accomplishment of an e!ective regu-lation of the natural monopoly elements of the gas chain.

5.4. Margins and rent

To examine the average margins (price above variablecosts and normal return on capital) on gas sales along thegas chain we consider the netback value of one BCM ofgas. In other words, we need to account for the split ingas sales between high and low pressure markets andtheir di!erent cost, margin and price structure. If we usethe European average of a third of gas sales going intothe low pressure market,14 then the breakdown of mar-gins along the gas chain can be calculated on the netbackbasis.15 This is shown in Fig. 5.

According to our calculations, $2.70 of an average(weighted) end-user market price of around $6.00 permBtu could be denoted as the margin in 1997. Out of thismargin, LDC's accounted for 15%, T&D's for 42% andupstream players for 43%. The main message is thatthese shares change only moderately in the GradualTransformation and Vertical Integration scenarios. Inthe Pull-the-Plug scenario, however, the share of rentaccruing upstream declines substantially in the short run* due to the gas bubble* but then increases such that ittoo has a similar share by 2020. In fact, it could be arguedthat the increasing market power of a few large gasproducers supplying an increased number of gas supplycompanies could enable the producers share to rise fur-ther in the long run. Nevertheless, the level of the totalmargin is clearly lowest in the Pull-the-Plug scenario,although the existing transmission companies are ex-ploiting the captive LDC market in the "rst years afterthe drop in wholesale prices in 2005.

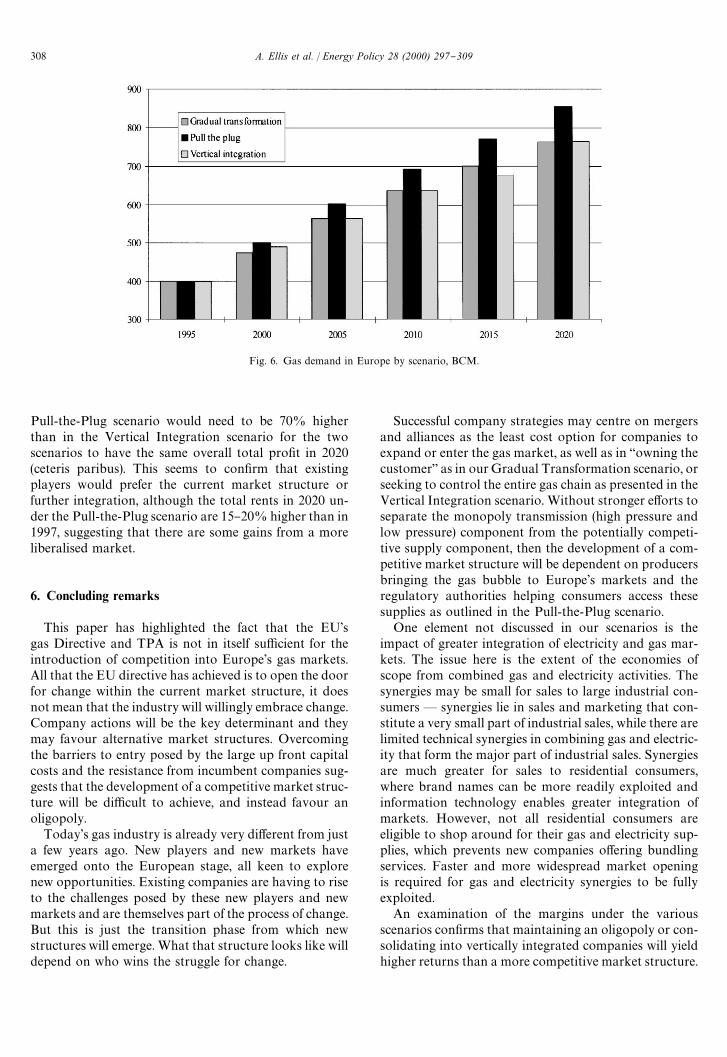

Production and transport of gas earn rent in excess ofnormal rates of return. To determine the overall levels ofrent in the industry, we need to account for di!erences ingas volumes sold and di!erences in margins per mBtu.From 1995 to 2020 gas demand in Europe doubles in allscenarios. Demand displays the strongest growth inPull-the-Plug scenario, since prices are lowest. Europeangas demand increases from 400 BCM to around 780BCM in 2020, implying an average annual growth of2,7%. Gas demands in 2020 in the Gradual Transforma-tion and Vertical Integration scenarios are approxim-ately equal, while it is 80 BCM (around 10%) higher inthe Pull-the-Plug scenario, as shown in Fig. 6.

Using the demand numbers, we "nd that overall levelof industry pro"ts is higher in the Vertical Integrationscenario and lowest in the Pull-the-Plug scenario ($77billion versus $46 billion). In fact, gas demand under the

A. Ellis et al. / Energy Policy 28 (2000) 297}309 307

Fig. 6. Gas demand in Europe by scenario, BCM.

Pull-the-Plug scenario would need to be 70% higherthan in the Vertical Integration scenario for the twoscenarios to have the same overall total pro"t in 2020(ceteris paribus). This seems to con"rm that existingplayers would prefer the current market structure orfurther integration, although the total rents in 2020 un-der the Pull-the-Plug scenario are 15}20% higher than in1997, suggesting that there are some gains from a moreliberalised market.

6. Concluding remarks

This paper has highlighted the fact that the EU'sgas Directive and TPA is not in itself su$cient for theintroduction of competition into Europe's gas markets.All that the EU directive has achieved is to open the doorfor change within the current market structure, it doesnot mean that the industry will willingly embrace change.Company actions will be the key determinant and theymay favour alternative market structures. Overcomingthe barriers to entry posed by the large up front capitalcosts and the resistance from incumbent companies sug-gests that the development of a competitive market struc-ture will be di$cult to achieve, and instead favour anoligopoly.

Today's gas industry is already very di!erent from justa few years ago. New players and new markets haveemerged onto the European stage, all keen to explorenew opportunities. Existing companies are having to riseto the challenges posed by these new players and newmarkets and are themselves part of the process of change.But this is just the transition phase from which newstructures will emerge. What that structure looks like willdepend on who wins the struggle for change.

Successful company strategies may centre on mergersand alliances as the least cost option for companies toexpand or enter the gas market, as well as in `owning thecustomera as in our Gradual Transformation scenario, orseeking to control the entire gas chain as presented in theVertical Integration scenario. Without stronger e!orts toseparate the monopoly transmission (high pressure andlow pressure) component from the potentially competi-tive supply component, then the development of a com-petitive market structure will be dependent on producersbringing the gas bubble to Europe's markets and theregulatory authorities helping consumers access thesesupplies as outlined in the Pull-the-Plug scenario.

One element not discussed in our scenarios is theimpact of greater integration of electricity and gas mar-kets. The issue here is the extent of the economies ofscope from combined gas and electricity activities. Thesynergies may be small for sales to large industrial con-sumers* synergies lie in sales and marketing that con-stitute a very small part of industrial sales, while there arelimited technical synergies in combining gas and electric-ity that form the major part of industrial sales. Synergiesare much greater for sales to residential consumers,where brand names can be more readily exploited andinformation technology enables greater integration ofmarkets. However, not all residential consumers areeligible to shop around for their gas and electricity sup-plies, which prevents new companies o!ering bundlingservices. Faster and more widespread market openingis required for gas and electricity synergies to be fullyexploited.

An examination of the margins under the variousscenarios con"rms that maintaining an oligopoly or con-solidating into vertically integrated companies will yieldhigher returns than a more competitive market structure.

308 A. Ellis et al. / Energy Policy 28 (2000) 297}309

The incumbent companies have a lot to lose in any movetowards greater competition, which will strengthen theirresolve to maintain the existing market structure andresist new entrants. Only stronger government interven-tion could pave the way for greater competition, and onlythen if it focuses on changing company behaviour suchthat company actions lead to a more competitive marketenvironment. Competition is unlikely to emerge in sup-plies to end-users unless access is unrestricted to existinggas networks. How this is to be achieved is open todebate and beyond the scope of this paper, but separ-ation of the monopoly component of the gas chain couldbe a starting point.

References

Atkinson, J., Manning, N., 1995. A survey of international energyelasticities. In: Barker, T., Ekins, P., Johnstone, N. (Eds.), GlobalWarming and Energy Demand. Routledge, London (Chapter 3).

Bain, J.S., 1956. Barriers to New Competition: Their Character andConsequences in Manufacturing Industries. Harvard UniversityPress, Cambridge, MA.

Bertrand, J., 1883. Book review of Recherches sur les PrincipesMatheHmatiques de la TheH orie des Richesses. Journal des Savants 67,pp. 499}508.

Brubakk, L., Aaserud, M., Pellekaan, W., Ostvoorn, F.V., 1995.SEEM } An Energy Demand Model for Western Europe. Reports95/24, Statistics Norway, Oslo.

Cournot, A., 1838. Recherches sur les Principes MatheHmatiques de laTheH orie des Richesses. Hachette, Paris.

Econ, 1990. ECON-ENERGY: Et modellapparat for globale energi- ogmilj+-analyser (A model system for global energy- and environmentalanalyses). Report 11, ECON Centre for Economic Analysis, Oslo.

Econ, 1997A. Modelling gas markets * a survey. Report 89/97, Econcentre for economic analysis, Oslo.

Econ, 1997B. ECONGAS-model structure. Report 90/97, Econ centrefor economic analysis, Oslo.

Ellis, A., Bowitz, E., Roland, K., 1999. Internationalisation and struc-tural change in the European gas market. Econ-Report 43/98, Econcentre for economic analysis, Oslo.

Estrada, J., Moe, A., Martinsen, K.D., 1995. The Development ofEuropean Gas Markets. Wiley, Chichester.

Golombek, R., Gjelsvik, E., Rosendal, K.E., 1995. E!ects of liberalizingthe natural gas markets in Western Europe. The Energy Journal16 (1), 85}111.

Golombek, R., Gjelsvik, E., Rosendahl, K.E., 1996. Increased competi-tion on the supply side of the Western European Natural GasMarket. Memorandum 11, Department of Economics, University ofOslo.

International Energy Agency, 1998. Natural Gas Pricing in Competi-tive Markets. OECD/IEA, Paris.

Odell, P., 1997. Europe's gas consumption and imports to increase withadequate low cost supplies. Energy Exploration and Exploitation15 (1), 35}54.

Philips, L., 1998. Applied Industrial Economics. Cambridge UniversityPress, Cambridge.

Radetzki, M., 1999. European natural gas: market forces will bringabout competition in any case. Energy Policy 27, 17}24.

Schmalensee, R., 1982. Product di!erentiation: advantages of pioneer-ing brands. American Economic Review 72, 349}365.

Schumpeter, J.A., 1954. Capitalism, Socialism and Democracy.Unwin.

Spengler, J.J., 1950. Vertical integration and Antitrust policy. Journal ofPolitical Economy 58, 347}352.

Sutton, J., 1991. Sunk Costs and Market Structure: Price Competition,Advertising, and the Evolution of Concentration. MIT Press,Cambridge, MA.

Stern, J., 1998. Competition and Liberalisation in European GasMarkets. The Royal Institute of International A!airs, London.

Stoppard, M., 1996. A new order for gas in Europe? Oxford Institute forEnergy Studies, Monographs NG-2, Oxford.

Sweezy, P.M., 1939. Demand under conditions of oligopoly. Journal ofPolitical Economy 47, 568}573.

A. Ellis et al. / Energy Policy 28 (2000) 297}309 309