Embed Size (px)

Citation preview

© Allen & Overy 2016

Strengthening the market

abuse framework – what you

need to know about MAR and

MAD II Etay Katz, Partner – Financial Services Regulatory

Jodi Norman, Associate – Financial Services Regulatory

Sarah Hitchins, Associate – Litigation

14 April 2016

2 © Allen & Overy 2016

Allen & Overy LLP

One Bishops Square, London E1 6AD, United Kingdom Tel +44 20 3088 0000 Fax +44 20 3088 0088.

If you would like to attend one or more of our seminars, please visit www.aoseminars.com where you can register.

If you have any queries or require further information please email [email protected]

2016 Seminar schedule

Thursday 14 April

8.30am – 9.30am

Bishops Square

Strengthening the market abuse framework – what you need to know about MAR and

MAD II

Etay Katz, Partner – Financial Services Regulatory

Jodi Norman, Associate – Financial Services Regulatory

Sarah Hitchins, Associate – Litigation

Friday 15 April

8.30am – 9.30am

Bishops Square

The 2016 U.S. Elections and Your Company’s Political Law Compliance Program

Charles Borden – Washington, DC, Partner

Claire Rajan – Washington, DC, Associate

Samuel Brown – Washington, DC, Associate

Thursday 28 April

12.30pm – 1.30pm

Bishops Square

Global trends in hostile M&A

Hartmut Krause, Partner – Frankfurt

Richard Hough, Partner – Corporate

Seth Jones, Partner – Corporate

Jaya Gupta, PSL Counsel – Corporate

Maarten Muller, Of Counsel – Netherlands

Tuesday 17 May

9.00am – 10.00am

Bishops Square

A basic guide to BEPS for non–tax specialists

Charles Yorke, Partner – Taxation

Lydia Challen, Partner – Taxation

Thursday 19 May

8.30am – 9.30am

Bishops Square

Internal investigations: managing increased expectations and challenges

Arnondo Chakrabarti, Partner – Litigation

Jonathan Hitchin, Partner – Litigation

Blair Keown, Senior Associate – Litigation

Brandon O’Neil, Senior Associate – Litigation

Sarah Hitchins, Associate – Litigation

Wednesday 25 May

8.30am – 9.30am

Bishops Square

Sanctions update

Matt Townsend, Partner – Corporate

© Allen & Overy 2016 3

Strengthening the market abuse framework – what you

need to know about MAR and MAD II

8:00 – 10:00

Etay Katz

Jodi Norman

Sarah Hitchins

Summary

The European Commission reviewed the existing Market Abuse Directive following the financial crisis and introduced

proposals in 2014 to strengthen the regime. A new Market Abuse Regulation (MAR) and a new Directive on criminal

sanctions (MAD 2) will become applicable for most purposes in July 2016. This seminar will provide an update on the scope

and impact of the Directive and Regulation, looking at areas such as the disclosure of inside information, the maintaining of

Insider Lists and the communication protocol for market soundings and the likely impact for cases that the FCA takes to

enforcement under the new regime.

4 © Allen & Overy 2016

Speaker biographies

Etay Katz Partner – Financial Services

Regulatory

Contact Tel +44 20 3088 3823

Etay advises a wide range of financial services providers on the impact of both national and

international regulatory regimes on their operations. He also advises on the regulation of both

retail and wholesale financial products and services.

Etay is the author of a chapter in Oxford University Press’ prominent publication Financial

Services Law and is the General Editor of Oxford University Press’ Financial Services

Regulation in Europe. He has been recognised as a leading individual for regulatory advice by

IFLR1000 and Legal 500 and is regularly quoted in the press on regulatory matters.

Jodi Norman

Associate – Financial Services

Regulatory

Contact

Tel +44 20 3088 4259

Jodi advises on a wide range of financial services regulatory matters, including large–scale

regulatory change projects. Jodi holds a Diploma in ‘Investment Compliance’ and regularly

advises on governance, risk and compliance arrangements (including in respect of financial

crime: anti–money laundering, anti–bribery and corruption and market abuse). Her experience

covers both contentious and non–contentious matters and she has been involved in a number

of internal and independent investigations and remediation exercises on behalf of clients. In

2013, Jodi was awarded ‘Regulatory Lawyer of the Year’ by Thomson Reuters.

Sarah Hitchins

Associate – Litigation

Contact Tel +44 20 3088 3948

Sarah is an associate in Allen & Overy’s Banking, Finance and Regulatory Litigation Group.

Sarah specialises in representing firms and individuals involved in financial services

regulatory investigations and enforcement action in relation to a broad variety of wholesale

and retail issues. Sarah has also completed a secondment to the Enforcement Division of the

FSA (as it then was). In 2015, Sarah was selected by Global Investigations Review (GIR) as

one of the top 100 women in investigations.

© Allen & Overy 2016 5

Notes

© Allen & Overy 2016

Strengthening the market abuse framework - what

you need to know about MAR and MAD IIEtay Katz, Jodi Norman and Sarah Hitchins

14 April 2016

6 © Allen & Overy 2016

Notes

© Allen & Overy 2016 22

MAR/MAD II – Why should you care?

The scope of instruments falling within the market abuse regime will be

significantly expanded‒ Concerns around identifying in-scope financial instruments

‒ Extra-territorial effect of the market abuse regime widened

New procedural requirements increase firms’ compliance requirements‒ Some examples: market soundings, investment recommendations,

prevention and detection of market abuse

Pursuing firms and individuals for market abuse is a priority for the FCA‒ Regulators are increasingly focusing on activity with a cross-border

element

‒ FCA increasingly focusing on market misconduct outside of equities

markets

‒ Will there be an increase in enforcement based on inadequate market

abuse systems and controls?

Increased

Scope

Increased

complexity

Increased

enforcement?

© Allen & Overy 2016 7

Notes

© Allen & Overy 2016

Practical Impact: Firms’ market abuse controls

3

Policies/Procedures Record keeping STORs

Oversight and monitoring Governance Management Information

8 © Allen & Overy 2016

Notes

© Allen & Overy 2016 44

What changes to the market abuse regime are

occurring at the European level?

Background: MAR

– MAR will directly apply in all Member States from 3 July 2016,

replacing the current EU Market Abuse Directive

– MAR relies on concepts introduced by MiFID II and accordingly

some provisions will not apply until MiFID II becomes operational

(anticipated: 3 January 2018)

– European Commission must approve delegated measures under

MAR

– European Commission must also adopt regulatory and

implementing technical standards submitted by ESMA

– MAR is complemented by the Directive on Criminal Sanctions for

Market Abuse (CSMAD), the provisions of which must be

transposed by participating Members States by 3 July 2016

Q&A

© Allen & Overy 2016 9

Notes

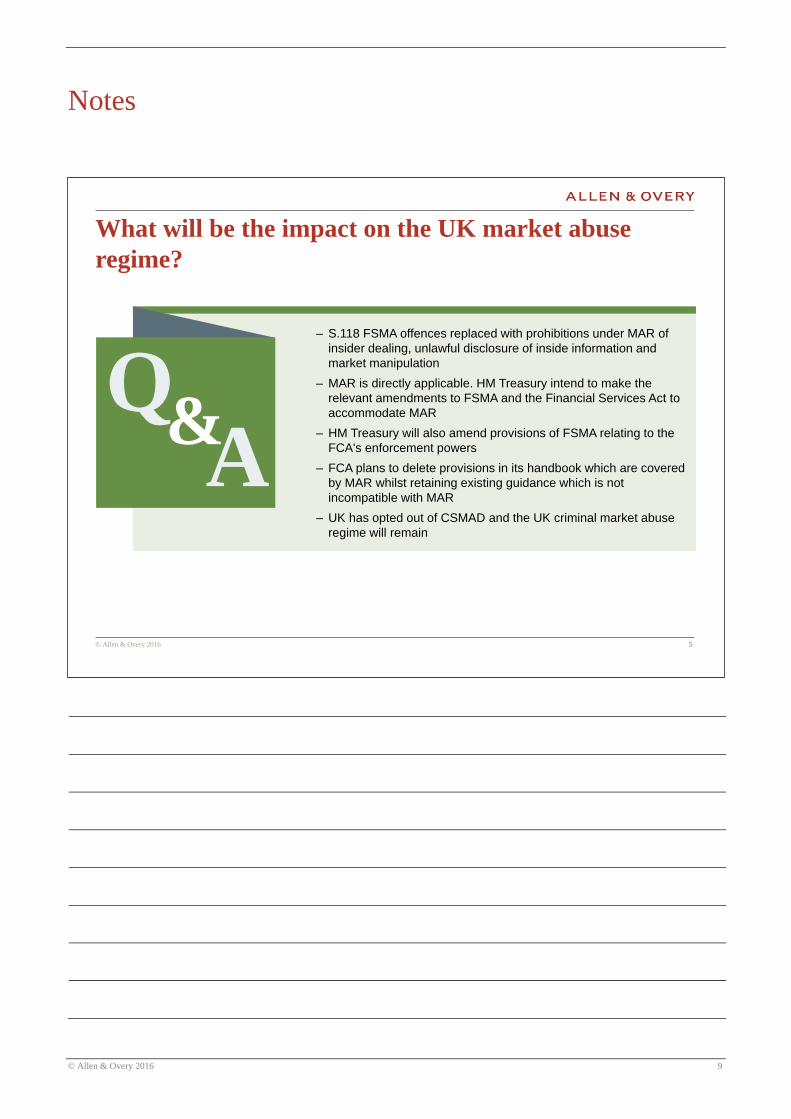

© Allen & Overy 2016 55

What will be the impact on the UK market abuse

regime?

– S.118 FSMA offences replaced with prohibitions under MAR of

insider dealing, unlawful disclosure of inside information and

market manipulation

– MAR is directly applicable. HM Treasury intend to make the

relevant amendments to FSMA and the Financial Services Act to

accommodate MAR

– HM Treasury will also amend provisions of FSMA relating to the

FCA's enforcement powers

– FCA plans to delete provisions in its handbook which are covered

by MAR whilst retaining existing guidance which is not

incompatible with MAR

– UK has opted out of CSMAD and the UK criminal market abuse

regime will remain

Q&A

10 © Allen & Overy 2016

Notes

© Allen & Overy 2016 66

Increased Scope: New markets & trading venues

Financial Instruments

The price of value of which depends on

or has an effect on the price or value of

financial instruments (inc. CDS/CFDs)

Financial Instruments

– Traded on a Regulated Market

– Traded on a Multilateral Trading

Facility (from 3 July)

– Traded on an Organised Trading

Facility (from MIFID II

Implementation)

For the purposes of Market

Manipulation:

– Spot commodity contracts having

effect on price or value

– Financial instruments having effect

on spot commodity contracts

– Benchmarks

© Allen & Overy 2016 11

Notes

© Allen & Overy 2016 77

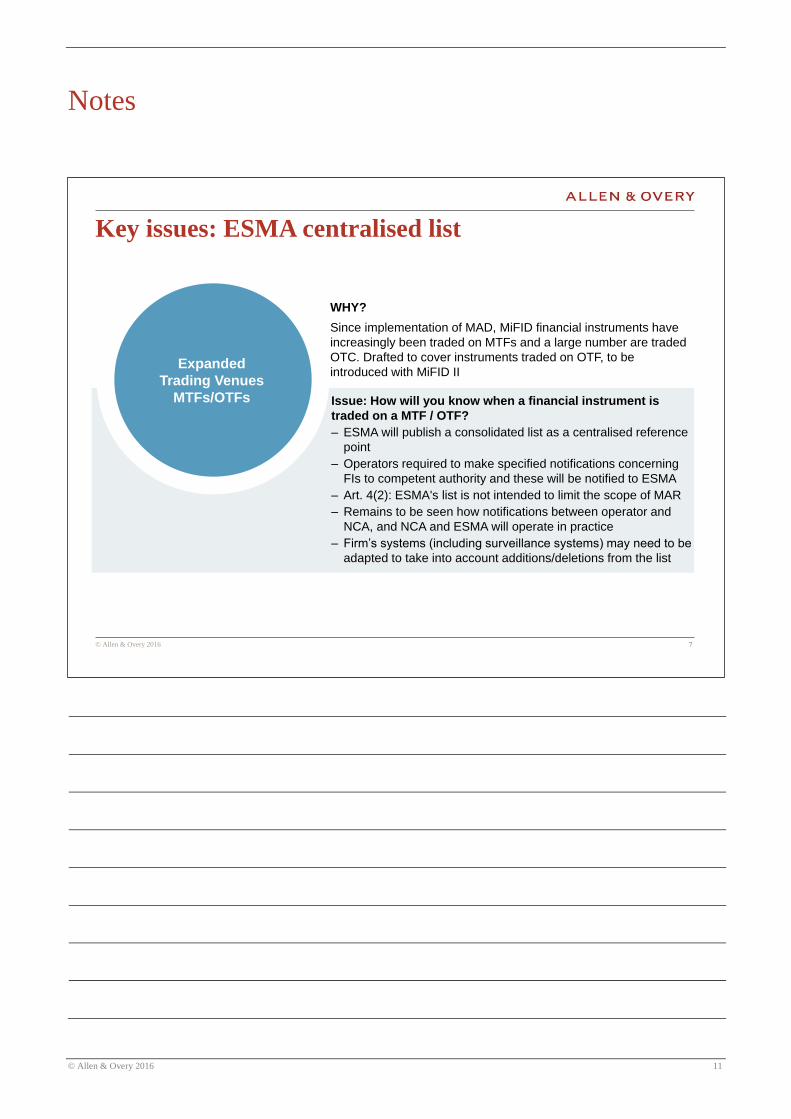

Key issues: ESMA centralised list

Issue: How will you know when a financial instrument is

traded on a MTF / OTF?

– ESMA will publish a consolidated list as a centralised reference

point

– Operators required to make specified notifications concerning

FIs to competent authority and these will be notified to ESMA

– Art. 4(2): ESMA's list is not intended to limit the scope of MAR

– Remains to be seen how notifications between operator and

NCA, and NCA and ESMA will operate in practice

– Firm’s systems (including surveillance systems) may need to be

adapted to take into account additions/deletions from the list

WHY?

Since implementation of MAD, MiFID financial instruments have

increasingly been traded on MTFs and a large number are traded

OTC. Drafted to cover instruments traded on OTF, to be

introduced with MiFID IIExpanded

Trading Venues

MTFs/OTFs

12 © Allen & Overy 2016

Notes

© Allen & Overy 2016 88

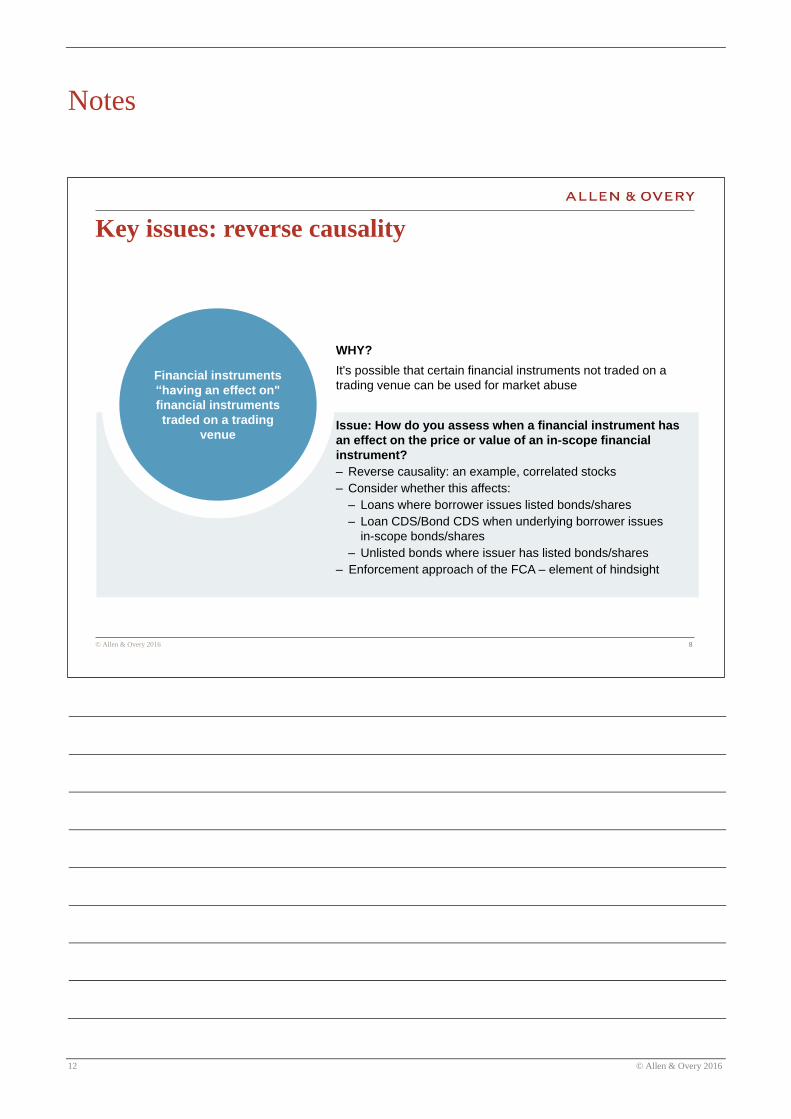

Key issues: reverse causality

Issue: How do you assess when a financial instrument has

an effect on the price or value of an in-scope financial

instrument?

– Reverse causality: an example, correlated stocks

– Consider whether this affects:

– Loans where borrower issues listed bonds/shares

– Loan CDS/Bond CDS when underlying borrower issues

in-scope bonds/shares

– Unlisted bonds where issuer has listed bonds/shares

– Enforcement approach of the FCA – element of hindsight

Financial instruments

“having an effect on"

financial instruments

traded on a trading

venue

WHY?

It's possible that certain financial instruments not traded on a

trading venue can be used for market abuse

© Allen & Overy 2016 13

Notes

© Allen & Overy 2016 9

Inside information

Definition relating to securities broadly unchanged

If made public it

would have a

significant effect on

price

Information a

reasonable investor

would be likely to

use as part of their

investment decision

Is precise

Clarifies that steps

in a process

leading to events or

circumstances may

be precise

Reflects Geltl v.

Daimler

Has not been made

public

Relates directly or

indirectly to issuers

of financial

instruments

Definition in relation to commodity derivatives is still more restrictive

– Information should be such that it is disclosable on the markets in accordance with legislation, market

rules, contract or custom

ESMA has consulted on future MAR list of information regarding commodity and spot markets

– Non exhaustive indicative list of information required to be published on commodity derivatives markets

or spot markets (Art. 7(5) MAR)

“Insider” definition remains the same

14 © Allen & Overy 2016

Notes

© Allen & Overy 2016 1010

Insider dealing and unlawful disclosure

Insider dealing offence

broadly the same

Now includes cancelling

and amending an order

No changes to the

definition of an insider

"Requiring or

encouraging" insider

dealing replaced with

"recommending or

inducing"

Insider dealing and

unlawful disclosure

Minor changes

Improper disclosure is

replaced with unlawful

disclosure

Still applies where

disclosure is made

outside the normal

exercise of employment,

profession or duties

© Allen & Overy 2016 15

Notes

© Allen & Overy 2016 1111

Insider dealing: legitimate behaviours

– Information barriers: dealing

subject to effective internal

arrangements

– previously MAR 1.33-5

– Pre-existing obligations

– Dealing on own trading intent

– previously MAR 1.3.8

– Legitimate execution of client

orders

– previously MAR 1.3.12/14

MAR 1.3.15 remains

– Market making or authorised

counterparty

– previously MAR 1.3.7

removal of "trading

information" carve out

– Public takeover or merger

– previously MAR 1.3.17

disapplied from stake-

building

– All subject to the "illegitimate reasons“

carve-out

– Recital 31 refers to both the standards

expected of the profession and

standards embodied by MAR (namely

market integrity and inversion

protection)

– Principle 5 requirements?

MAR enshrines principle in

Spector Photo group:

where a person is in

possession of inside

information there is a

rebuttable presumption that

any dealing is on the basis

of that inside information

Art. 8(1) MAR; Recital 24

16 © Allen & Overy 2016

Notes

© Allen & Overy 2016 1212

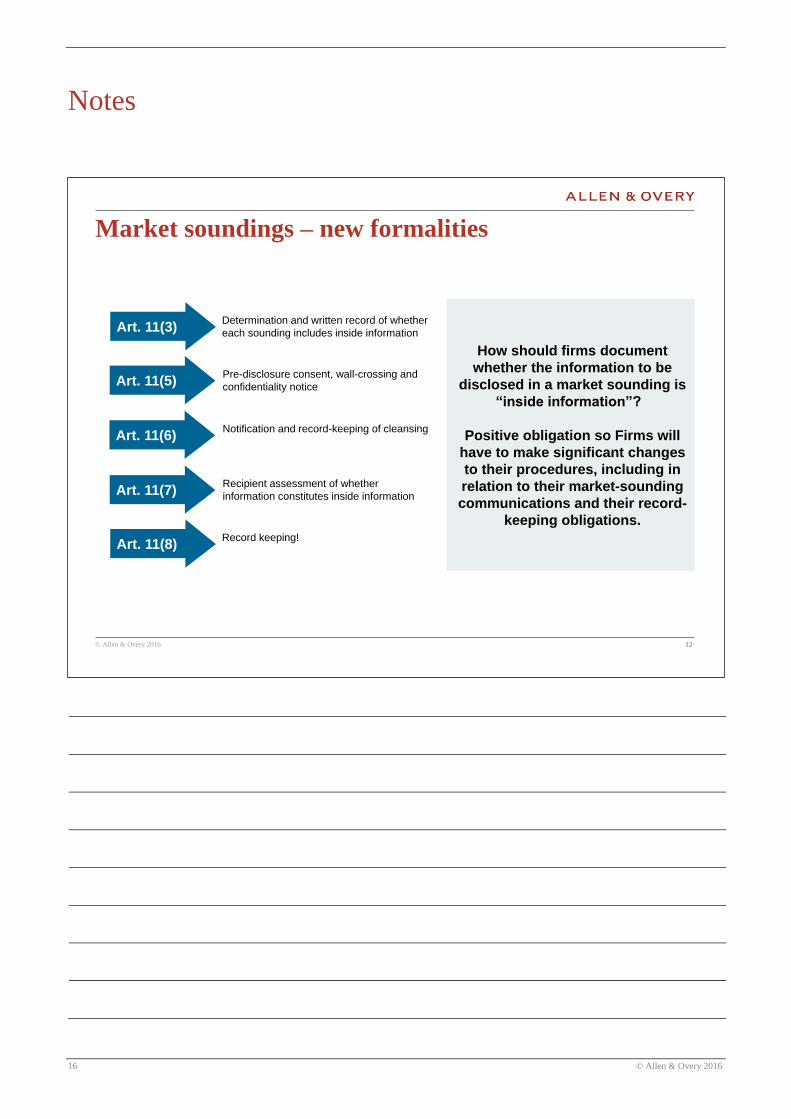

Market soundings – new formalities

How should firms document

whether the information to be

disclosed in a market sounding is

“inside information”?

Positive obligation so Firms will

have to make significant changes

to their procedures, including in

relation to their market-sounding

communications and their record-

keeping obligations.

Art. 11(3)

Art. 11(7)

Art. 11(8)

Art. 11(5)

Art. 11(6)

Determination and written record of whether

each sounding includes inside information

Pre-disclosure consent, wall-crossing and

confidentiality notice

Notification and record-keeping of cleansing

Recipient assessment of whether

information constitutes inside information

Record keeping!

© Allen & Overy 2016 17

Notes

© Allen & Overy 2016 1313

Market manipulation

Manipulation of benchmarks

– Already a criminal offence in the UK to

make false or misleading statements

relating to benchmarks

– MAR offence currently has a higher

threshold than the equivalent UK provision

– Little expectation that MAR will

change the UK offences in

relation to benchmarks

Guidance

– CoMC 16 to 18 largely disappearing

– MAR provides an indicative list of market

manipulation

– Annexes to the Commission Delegated

Regulation contain descriptions of

practices

– Where do spot commodity contracts

transactions affect financial instruments and

vice versa?

– Accepted market practices

– NCAs can, following notification

to ESMA, establish AMPs

– UK has no existing AMPs and it is not

intended to establish any going

forward

– Market manipulation broadly

similar to the offences

currently set out in s.118

FSMA

– Art. 15 MAR introduces a

new prohibition on

attempting to engage in

market manipulation

18 © Allen & Overy 2016

Notes

© Allen & Overy 2016 1414

Pursuing firms and individuals for market abuse

continues to be a priority for the FCA

‘Market abuse is a serious offence… we

will not hesitate in taking action against

individuals who act on inside information’.

(Georgina Philippou, Acting Director of Enforcement)

(March 2015)

The FSA is committed to taking whatever steps are necessary

to protect the integrity of our markets whatever the techniques

used and wherever the perpetrators are located’.

(Tracey McDermott, Director of Enforcement) (January 2013)

‘Today’s judgment shows the FCA’s

ability and determination to stamp out

abusive market practice wherever it may

occur in UK markets’

(Georgina Philippou, Acting Director of Enforcement)

(August 2015)

© Allen & Overy 2016 19

Notes

© Allen & Overy 2016 1515

But the FCA has had limited success in this area

20 © Allen & Overy 2016

Notes

© Allen & Overy 2016

The FCA has reported a strong pipeline of market

abuse cases

16

‘It discussed the work being undertaken in respect of wholesale and

other market abuse cases and noted there were some delays as a

result of cases being significantly more complex than others or

affected by external factors. It noted there was a strong pipeline of

cases expected’.

FCA Board Minutes, July 2015

© Allen & Overy 2016 21

Notes

© Allen & Overy 2016

Firms’ market abuse controls may come under scrutiny

17

Policies/Procedures Record keeping STORs

Oversight and monitoring Governance Management Information

22 © Allen & Overy 2016

Notes

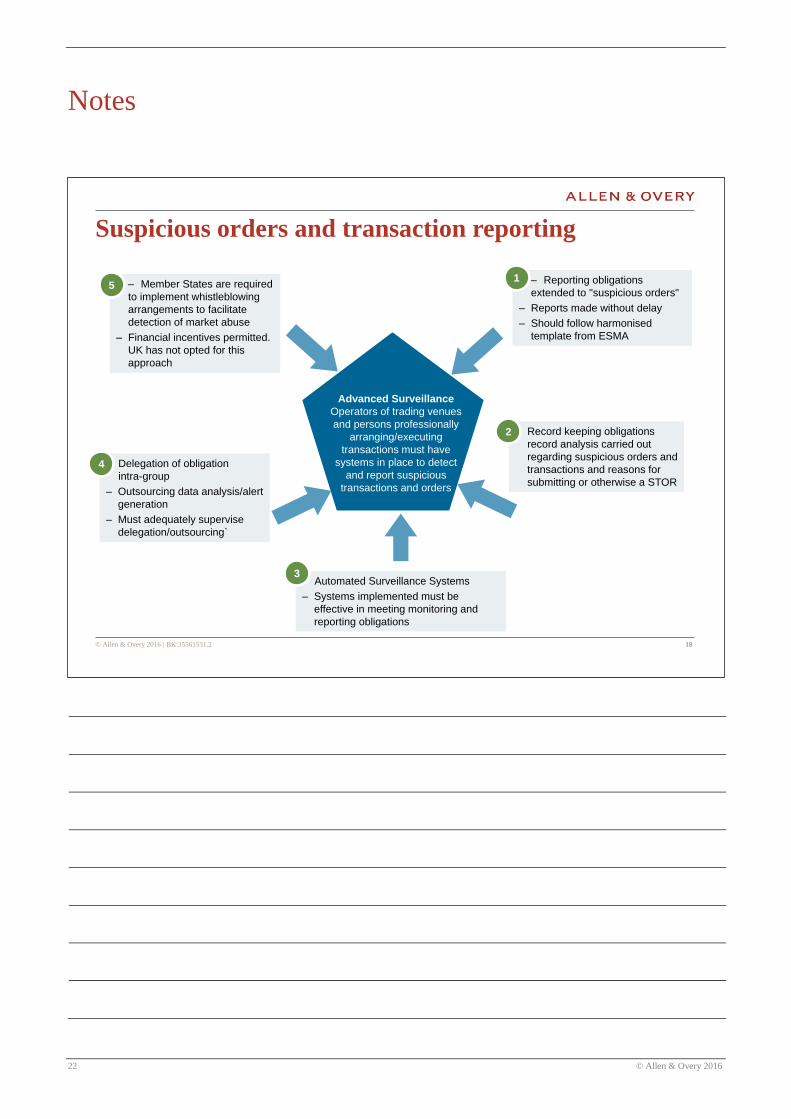

© Allen & Overy 2016 1818

Suspicious orders and transaction reporting

Delegation of obligation

intra-group

– Outsourcing data analysis/alert

generation

– Must adequately supervise

delegation/outsourcing`

Record keeping obligations

record analysis carried out

regarding suspicious orders and

transactions and reasons for

submitting or otherwise a STOR

– Reporting obligations

extended to "suspicious orders"

– Reports made without delay

– Should follow harmonised

template from ESMA

– Member States are required

to implement whistleblowing

arrangements to facilitate

detection of market abuse

– Financial incentives permitted.

UK has not opted for this

approach

Automated Surveillance Systems

– Systems implemented must be

effective in meeting monitoring and

reporting obligations

Advanced Surveillance

Operators of trading venues

and persons professionally

arranging/executing

transactions must have

systems in place to detect

and report suspicious

transactions and orders

1

2

4

5

3

| BK:35561531.2

© Allen & Overy 2016 23

Notes

24 © Allen & Overy 2016

Allen & Overy LLP

One Bishops Square, London E1 6AD United Kingdom | Tel +44 (0)20 3088 0000 | Fax +44 (0)20 3088 0088 | www.allenovery.com

In this document, Allen & Overy means Allen & Overy LLP and/or its affiliated undertakings. The term partner is used to refer to a member of Allen & Overy LLP or an

employee or consultant with equivalent standing and qualifications or an individual with equivalent status in one of Allen & Overy LLP's affiliated undertakings.

Allen & Overy LLP or an affiliated undertaking has an office in each of: Abu Dhabi, Amsterdam, Antwerp, Bangkok, Barcelona, Beijing, Belfast, Bratislava, Brussels, Bucharest

(associated office), Budapest, Casablanca, Doha, Dubai, Düsseldorf, Frankfurt, Hamburg, Hanoi, Ho Chi Minh City, Hong Kong, Istanbul, Jakarta (associated office),

Johannesburg, London, Luxembourg, Madrid, Milan, Moscow, Munich, New York, Paris, Perth, Prague, Riyadh (associated office), Rome, São Paulo, Shanghai, Singapore,

Sydney, Tokyo, Toronto, Warsaw, Washington, D.C., and Yangon. | MKT:5629651.1

![POLITECNICO DI TORINO · Figure 2.2 FCA Regions [FCA presentation].....24 Figure 2.3 FCA Sales 2017-2018 [Personal processing of FCA data ... This present thesis concerns the subject](https://img.pdfslide.us/doc/110x75/602c67dbc5d9f6029526a4a8/politecnico-di-torino-figure-22-fca-regions-fca-presentation24-figure-23.jpg)