Embed Size (px)

Citation preview

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

STRENGTHEN FINANCIAL STABILITY

THROUGH EFFECTIVE RISK AND CAPITAL

MANAGEMENT

STEFAN DE LOMBAERT, SENIOR DIRECTOR

MARTIM ROCHA, ADVISORY BUSINESS SOLUTIONS MANAGER,

SAS RISK CENTRE OF EXCELLENCE- EMEA/AP

MAY 23, 2014

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND

CAPITAL

MANAGEMENT

AGENDA

• Context

• Risk and Capital Management

• The market status

• Status in the Banks

• Drivers for change and action

• SAS Approach

• Key points of value

• Solution Process

• Risk Modeling and Calculation

• EBA Stress-test example

• Case-studies

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

CONTEXT

RISK AND CAPITAL MANAGEMENT

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND

CAPITAL

MANAGEMENT

KEY MESSAGES

• The objective of capital management is to optimize the

Banks's capital structure given the adopted risk profile.

• With capital being the foundation of which every bank is

built upon., it is important to properly prepare for the

expected and unexpected.

• To understand and optimize the bank’s capital adequacy

for each business model, capital must be viewed from

many perspectives. Growth, credit issues, earnings,

interest rate fluctuations, and dividends have an effect on

each of these perspectives.

Financial

institutions operate

on Capital.

The best they

manage it, the

better they will do

on Returns

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTTHE MARKET STATUS

Lessons from the financial crisis:

• In the absence of information banks spent capital that could

have insulate them from losses

• Sound capital planning is critical for determining the

prudent amount, type and composition of capital that is

consistent with a longer-term strategy …, while also

withstanding a stressful event.

• Banks’ processes were(are) not sufficiently comprehensive,

appropriately forward-looking or adequately formalized

• Management teams underestimated the risks inherent in

their banks’ business strategies and, in turn, misjudged

capital needs

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENT

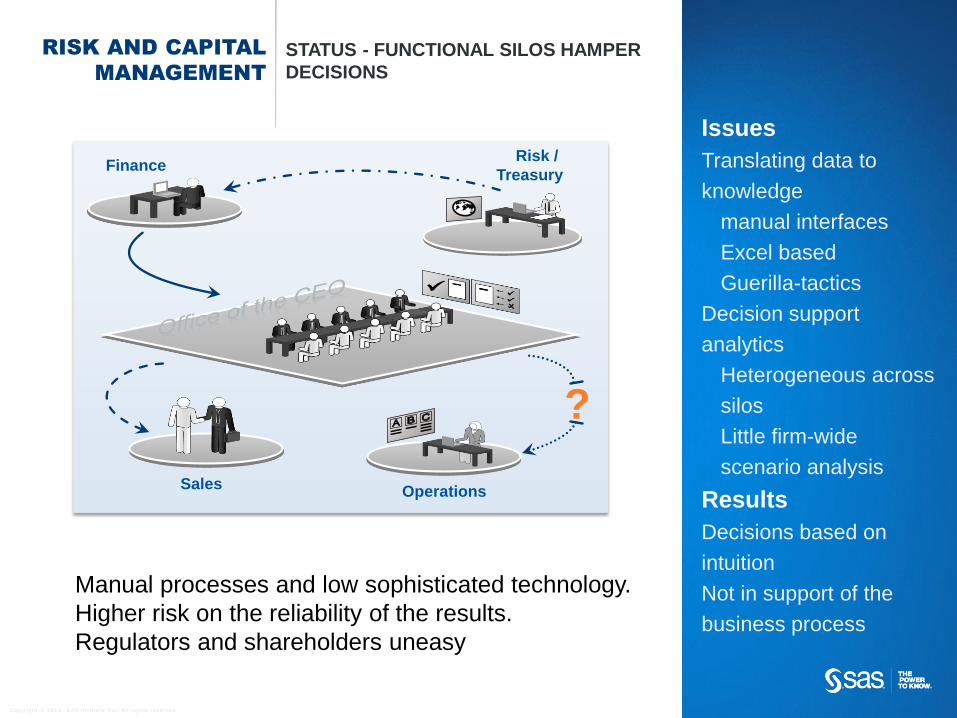

STATUS - FUNCTIONAL SILOS HAMPER

DECISIONS

Issues

Translating data to

knowledge

manual interfaces

Excel based

Guerilla-tactics

Decision support

analytics

Heterogeneous across

silos

Little firm-wide

scenario analysis

Results

Decisions based on

intuition

Not in support of the

business process

Finance

Operations

Risk /

Treasury

Sales

?

Manual processes and low sophisticated technology.

Higher risk on the reliability of the results.

Regulators and shareholders uneasy

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

IMPACT

• Data discrepancies that require added reconciliation effort• IT systems are organized by departments – each uses it’s own coding, grouping, hierarchies, time reference, …

• Combined data doesn’t match, added effort for reconciliation and data quality

• Cross reporting happens only in very aggregated levels, losing important detail and in

many cases hiding problems that could be otherwise addressed pro-actively.• To overcome the difficulties on combining data, reporting is done in very aggregated levels – limits effectiveness

• Difficulties on accurately calculate risk adjusted measures at the right level of detail,

making decision around which products and which regions to invest almost only based

on gut feeling.• The world is flat but each region, demographic group, provided service has its particular characteristics – the devil is in the

details as well as the return

• Undermine any attempt of creating a framework of predictive analytics due to the lack a

historical integrated information.• To anticipate the future you should look into the past, the more detailed you have on the past the best estimate you do on

the future

• Reduce drastically the number and depth of scenarios analyzed for planning.• The cumbersome and manual based processes you have today take too much time for each analysis you do thus limiting

the scenarios you analyze

RISK AND CAPITAL

MANAGEMENT

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTDRIVERS FOR CHANGE AND ACTION

• Banks across many developed markets remain

undercapitalized.

• Unwilling, or unable, to write down asset values

to more realistic levels and accept credit

losses.

• Many still under liquidity support from central

bank with tight repayment deadlines.

• Sub-10% ROEs have rendered many North

American and European business models

obsolete

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTDRIVERS FOR CHANGE AND ACTION

…

• EBA Stress-testing (EUR)

• Risk Appetite Framework

• CCAR – Comprehensive Capital Analysis and Review (US)

REGULATOR PUSH

Basel III ICAAP

BCBS 277 Sound Capital

Planning

BCBS239 Principles for

Risk Data Aggregation

and Reporting

Capital

Planning and

Management

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTDRIVERS FOR CHANGE AND ACTION

Standalone impact of Basel

III on Capital and Funding

of Banks is Euro 1.6 Trillion

(2019 target) : Roughly a

drop of 400 bp in RoE

Higher Costs of Capital

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTINTEGRATING RISK AND FINANCE

“lack of integration

between risk and finance

has limited the

effectiveness of

decision-making around

risk versus return, capital

management and

regulatory charge

optimization”

“Financial institutions can

boost profitability by a

better alignment of risk and

finance”

“investing more in

technology to improve their

ability to integrate risk

information into financial and

performance management”

“Integration of risk and finance reporting, together

with greater analytical capabilities, is enabling

financial institutions to manage the risk, funding,

liquidity and capital requirements of their business in

a more dynamic fashion”

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

SAS APPROACH

RISK AND CAPITAL MANAGEMENT

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK AND CAPITAL

MANAGEMENTTHE SAS APPROACH

Capital Planning

Capital

Allocation

Risk Adjusted

Performance

Measurement

Forward Looking Planning

Capital

Estimate surplus / deficit in

capital over projected

planning horizon

(Optimized) allocation of

capital to profit centers

Integrated Risk and Financial

reporting

Risk Adjusted Performance of

Capital

Capital

Planning and

Management

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

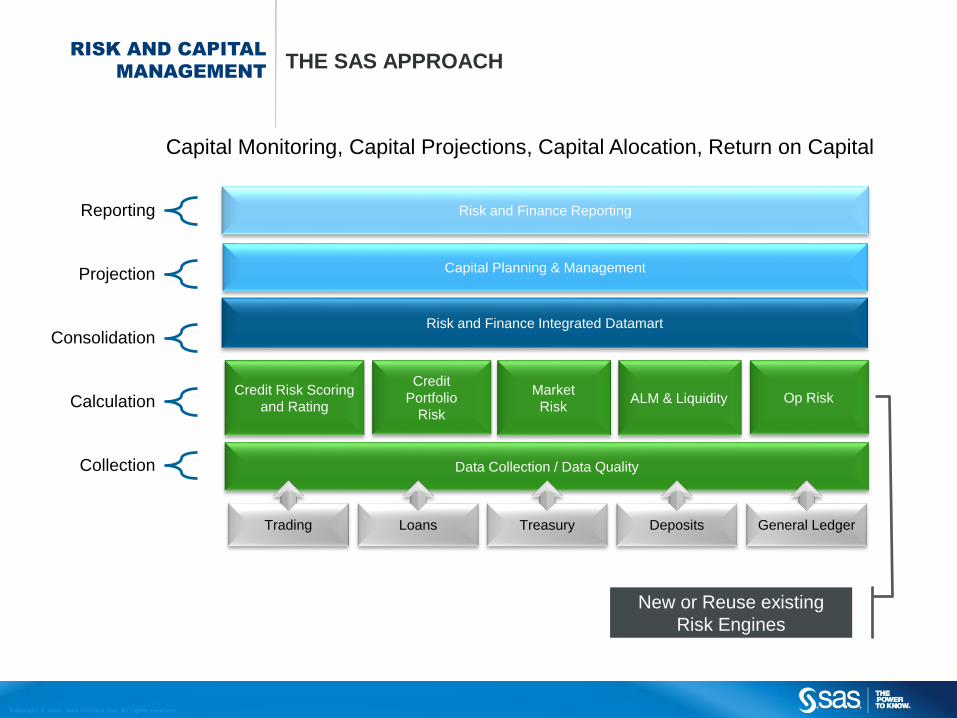

Reporting

Projection

Consolidation

Calculation

Collection

RISK AND CAPITAL

MANAGEMENTTHE SAS APPROACH

Risk and Finance Integrated Datamart

Credit

Portfolio

Risk

Market

RiskALM & Liquidity Op Risk

Capital Planning & Management

Data Collection / Data Quality

Trading Loans Treasury Deposits General Ledger

Credit Risk Scoring

and Rating

Risk and Finance Reporting

New or Reuse existing

Risk Engines

Capital Monitoring, Capital Projections, Capital Alocation, Return on Capital

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

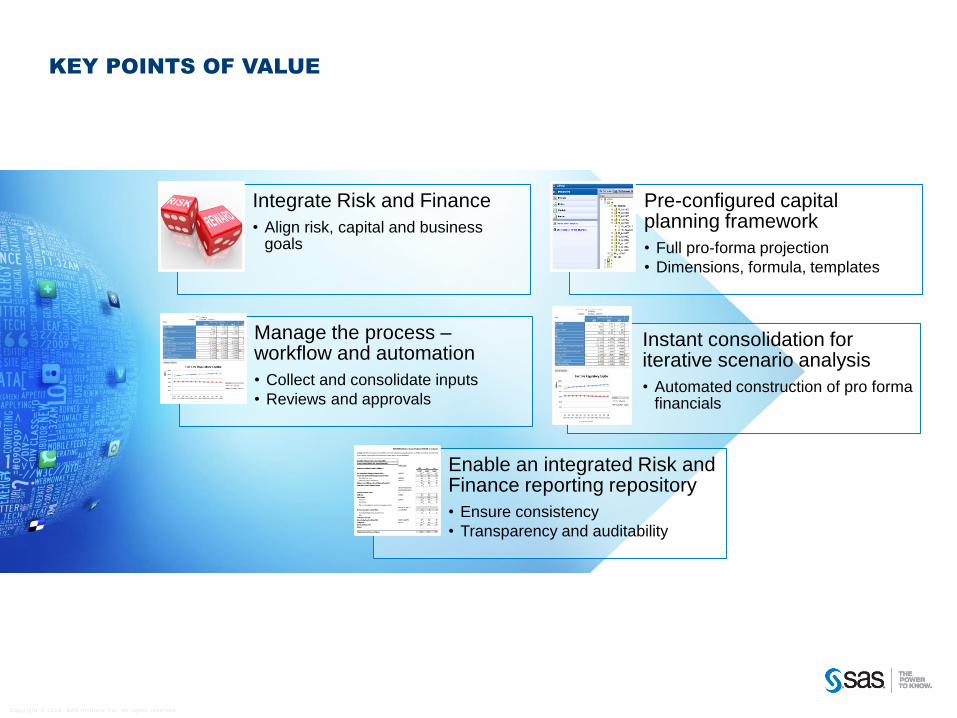

KEY POINTS OF VALUE

Integrate Risk and Finance

• Align risk, capital and business goals

Pre-configured capital planning framework

• Full pro-forma projection

• Dimensions, formula, templates

Manage the process –workflow and automation

• Collect and consolidate inputs

• Reviews and approvals

Instant consolidation for iterative scenario analysis

• Automated construction of pro forma financials

Enable an integrated Risk and Finance reporting repository

• Ensure consistency

• Transparency and auditability

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

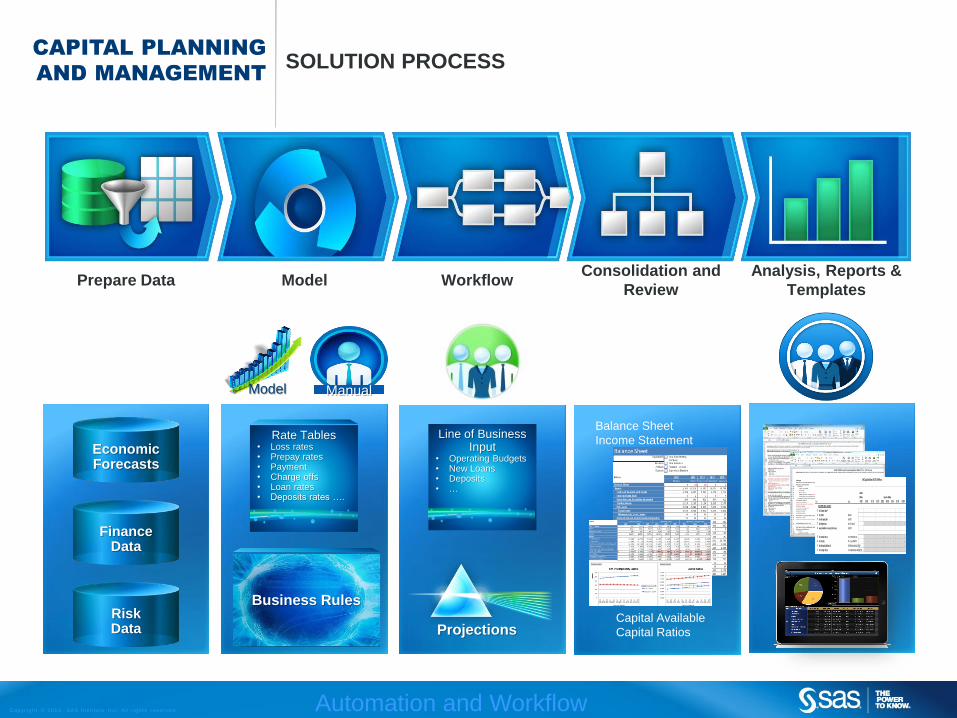

Prepare Data ModelAnalysis, Reports &

Templates

Consolidation and

ReviewWorkflow

Line of Business Input

• Operating Budgets• New Loans• Deposits• …

Economic Forecasts

Finance Data

Risk Data

Balance Sheet

Income Statement

Capital Available

Capital Ratios

CAPITAL PLANNING

AND MANAGEMENTSOLUTION PROCESS

Business Rules

Rate Tables• Loss rates• Prepay rates• Payment• Charge offs• Loan rates• Deposits rates ….

ManualModel

Projections

Automation and Workflow

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

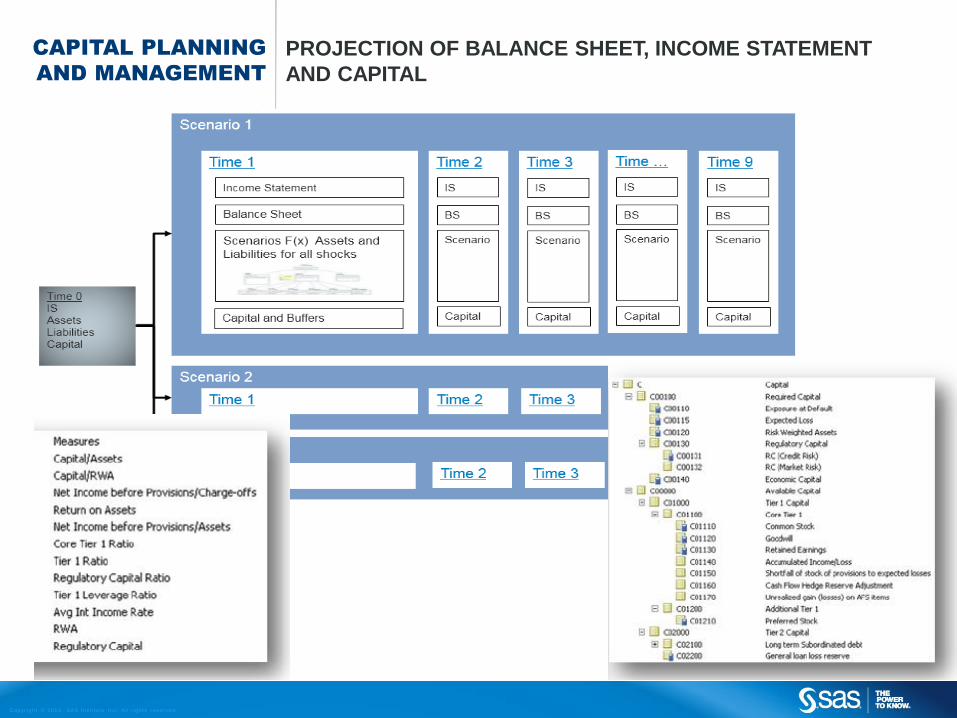

CAPITAL PLANNING

AND MANAGEMENT

PROJECTION OF BALANCE SHEET, INCOME STATEMENT

AND CAPITAL

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

RISK MODELLING & CALCULATIONS

RISK AND CAPITAL MANAGEMENT

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

HOT TOPIC : EBA STRESS TESTS

• EBA issued macro-economic scenarios, developed

by ESRB.

• Exercise runs from May till Oct 2014.

• For 124 banks in Europe, on Group level.

• GR : Alpha Bank – NBG – Piraeus Bank – Eurobank

• CY : BoC – Hellenic Bank – Coop Central Bank

• Local regulators assess, EBA coordinates, stores &

publishes results.

• Scenarios for 3 years, with hurdle rates;

• Base scenario : 8% Common Equity Tier 1 Capital

• Adverse scenario : 5,5% Common Equity Tier 1 Capital

RISK MODELLING &

CALCULATIONS

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

MORE DETAILS

• Starting Point : Figures as of 31-12-2013 with STATIC Balance Sheet.

• Zero growth, just replace matured positions

• Same currency mix

• Same business mix

• No capitalisation measures allowed

• No workout of defaulted assets (they disappear from the BS)

• Base scenario assumes low inflation (< 1.5%) and is based on Winter 2014

forecasts of DG ECFIN, with a 2016 model-based extension.

• Adverse scenario looks at most pertinent systemic risks (PD decrease,

Bond Yield increase, Funding Cost increase, ….)

• Russian Gas, UK Housing ????

• Reporting Templates

RISK MODELLING &

CALCULATIONS

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

WHICH SCENARIOS (1/3) ?

5 Broad Categories

• Focus Area

• Market Risk

• Credit Risk

• Other areas

• Securitization Risk

• Sovereign Risk

• Funding Cost & NII

RISK MODELLING &

CALCULATIONS

Market Risk

List of individual RF values provided under

Base, Adverse & 4 Historic Crises Scenarios

=> Worst of 6

Credit Risk

Starting from existing PD/LGD, moving to

projected Point-in-Time PD/LGD (ev. Rating

Migration), per COREP Asset Class, based on

2 macro-economic scenarios

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

WHICH SCENARIOS (2/3) ?

5 Broad Categories

• Focus Area

• Market Risk

• Credit Risk

• Other areas

• Securitization Risk

• Sovereign Risk

• Funding Cost & NII

RISK MODELLING &

CALCULATIONS

Securitization Risk

Stressed RW for STD (5 Ctp Risk levels) & IRB

Approach (12 Ctp Risk levels) and 3 Product Buckets

under Base & Adverse Scenarios;

- Low Risk ABS + EMEA RMBS

- Medium Risk EMEA CMBS + CDO

- High Risk NA RMBS + CMBS + CDO

Sovereign Risk

Bond Valuation haircuts for M-to-M Approach, by

Country & Tenor

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

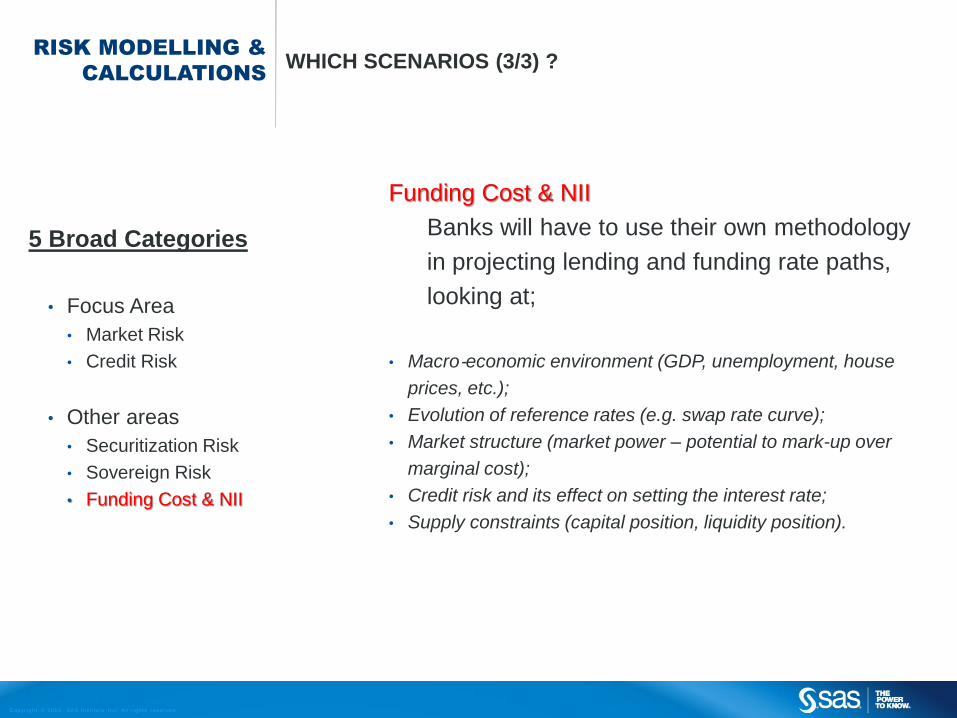

WHICH SCENARIOS (3/3) ?

5 Broad Categories

• Focus Area

• Market Risk

• Credit Risk

• Other areas

• Securitization Risk

• Sovereign Risk

• Funding Cost & NII

RISK MODELLING &

CALCULATIONS

Funding Cost & NII

Banks will have to use their own methodology

in projecting lending and funding rate paths,

looking at;

• Macro‐economic environment (GDP, unemployment, house

prices, etc.);

• Evolution of reference rates (e.g. swap rate curve);

• Market structure (market power – potential to mark-up over

marginal cost);

• Credit risk and its effect on setting the interest rate;

• Supply constraints (capital position, liquidity position).

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

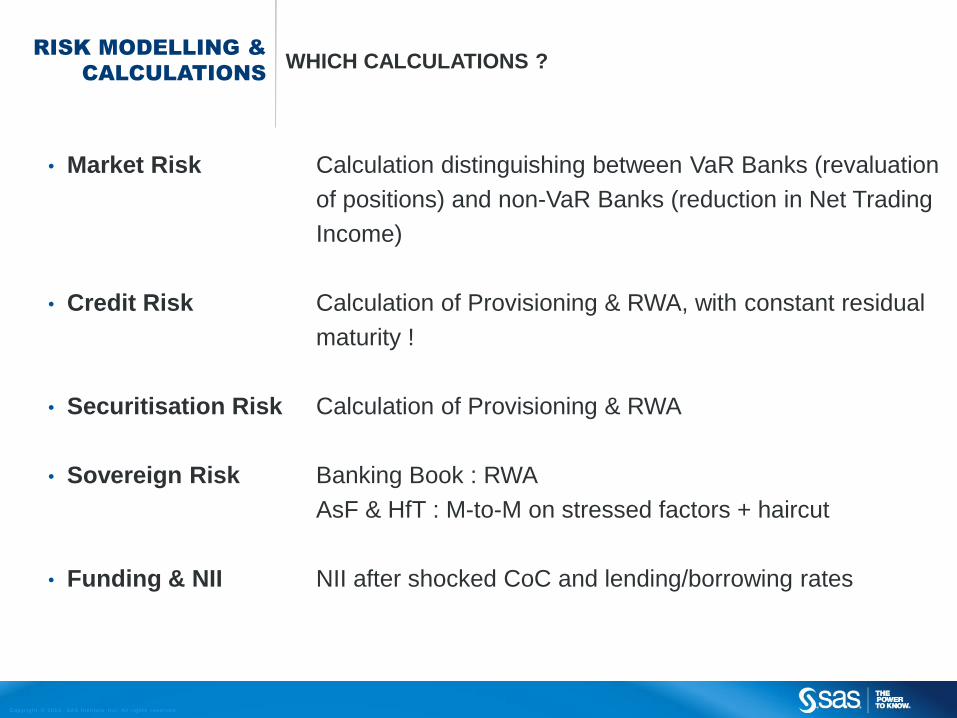

WHICH CALCULATIONS ?

• Market Risk Calculation distinguishing between VaR Banks (revaluation

of positions) and non-VaR Banks (reduction in Net Trading

Income)

• Credit Risk Calculation of Provisioning & RWA, with constant residual

maturity !

• Securitisation Risk Calculation of Provisioning & RWA

• Sovereign Risk Banking Book : RWA

AsF & HfT : M-to-M on stressed factors + haircut

• Funding & NII NII after shocked CoC and lending/borrowing rates

RISK MODELLING &

CALCULATIONS

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

CONCLUSION

• From the details of the methodology & the scenarios it should be clear that as

much as possible calculations need to be executed with existing tools &

methodologies, except for the simplifications.

• But…..since this will involve indeed a multitude of systems and entities, there

is a need for a central scenario repository and a central result data repository.

• One can expect that in a later stage the stable BS restriction will be removed

- at least for internal stress purposes - in which case a central set of

projection rules become a vital part of the solution as well.

• And….a central set of reports will conclude the infrastructure

RISK MODELLING &

CALCULATIONS

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

Reporting

Projection

Consolidation

Calculation

Collection

RISK AND CAPITAL

MANAGEMENTTHE SAS APPROACH

Risk and Finance Integrated Datamart

Credit

Portfolio

Risk

Market

RiskALM & Liquidity Op Risk

Capital Planning & Management

Data Collection / Data Quality

Trading Loans Treasury Deposits General Ledger

Credit Risk Scoring

and Rating

Risk and Finance Reporting

New or Reuse existing

Risk Engines

Capital Monitoring, Capital Projections, Capital Alocation, Return on Capital

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

CASE STUDIES

RISK AND CAPITAL MANAGEMENT

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

UNICREDIT GROUP RISK AND FINANCE INTEGRATION IN ACTION

Roberto Monachino, CFO Head of Data Governance - UniCredit Group

• Data governance organization is an enabler to apply the target performance risk adjusted measurement framework starting

from product, customer and business area consolidated by legal entity and country up to group level, reconciled with

accounting with integration of risk related data. Consistent Group Golden Profitability Rules (PGR) and Data Governance Rules

were adopted across the organization and laid down in a single vocabulary and a common logical data model to ensure

comparability at Group level. Therefore, business data elements (BDEs) were produced locally and merged into a unique DWH

repository aimed at avoiding overlapping and redundancies, creating a common language and optimizing data flows. BDEs for

local needs may be added but require Central approval before implementation. A governance tool within the DWH controls

transparent workflows for parameters, rules and adjustments across business areas. Alignment between business and IT is

also enabled by a data lab environment. It fills the gap between a business idea and the ability to implement it. Existing data

can be accessed and new data be added into a „sandbox‟ to prototype new BI deliverables for business. When approved they

can be implemented in the production database.

In this presentation he will go through all the above steps, showing concrete experience on how the entire value chain from

Data Production to Data Delivery has been considered a success experience for the final business community. Shorten the

data process is a key element for having more time to do better analysis and support the decision making process.

UniCredit is one of 25 banks operating worldwide with extensive international presence spanning 50 markets and about 9,400

branches. The company is the result of the merger of nine of Italy‟s largest banks, the Capitalia Group and their combination

with the German HVB Group, including Bank Austria and its 19 Eastern European country organisations. The divisional

business model structured by customer segments and regions is supported by global services including the Group‟s centralised

risk management and information technologies.

Risk Adjusted Performance by Product, Customer

Segment, Business Area, Legal Entity and Group

Risk and Finance Reconciled

Single Vocabulary and a Common Logical Model

One Unified source for Capital Planning and Regulatory Exercises

– EBA Stress-test, ICAAP and BCBS239 compliant

Business Model supported by Global Services for about

9400 branches and 50 markets where Unicredit is present

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

PART OF BIG DUCTH

FINANCIAL

SERVICES GROUP

FRIS: FINANCE & RISK INTEGRATED SOLUTION

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .

FRANCO-GERMAN

REGIONAL BANKCAPITAL PLANNING AND MANAGEMENT

• The bank has integrated already finance

and risk figures using SAS.

• Recently enhanced the application with

sales planning

• and is now moving forward to an integrated

finance and risk plan.

• Next project will be RWA planning, using

Portfolio based Asset plans and applying

migration matrices on customers rating to

determine the change of RWA over the plan

period of 5 years

AROUND 20 BILLION

TOTAL ASSETS

Improve timeliness and

accuracy of reporting.

Streamline budgeting and

forecasting process

Minimize manual spreadsheet

processing

Support various reporting

requirements from dashboard

to KPIs, from static reports to

multidimensional analysis

Roadmap for Risk Adjusted

Performance Management

Copyr i g ht © 2014, SAS Ins t i tu t e Inc . A l l r ights reser ve d .sas.com

THANK YOU