Embed Size (px)

Citation preview

STRATMOR | GROUP

We want your feedback REAL TIME

• Please use your phone and browse to the URL below

• You do NOT need a login • You will be asked a series of questions

throughout this session • Answer on phone, and results appear

instantly• You can also ask questions through web

page

www.PollEv.com/STRATMOR

STRATMOR | GROUP2

Who and What We ArePractice Description Practice Leader

Benchmarking, and Financial Analysis

• The type of work required by CFO’s, whether independent or bank owned • MBA / STRATMOR Peer Group Program (PRG), with over 80 of the top lenders participating • We use our extensive industry data, going back years and through multiple rate cycles• Build financial models for lenders – 5 year P&L, Balance Sheet and Capital projections

Jim Cameron

Nicole Yung

Strategic Planning Services

• Strategic planning and executive leadership coaching • Consideration of entering and exiting channels and markets, competitive positioning

Dr. Matt Lind

IT Procurement and Advisory

• Independent evaluation of 26 primary LOS• Typically an exercise in reducing the list, and assisting with procurement• Executive coaching and IT readiness•Implementation and rescue efforts

Len Tichy

STRATMOR | GROUP3

“Torture The Data Until It Confesses”Practice Description Practice Leader

Capital Markets • From Best Efforts to Mandatory• Agency delivery • Alternate Investors• Pricing strategy and execution

Rob Chrisman

Mergers and Acquisition

• Buy side advisory• Sell side representation • Middle man for interested parties

Jeff Babcock

Sales and Marketing • Consumer Direct and Retail• Lead generation and Lead Management • E-Commerce and Direct Marketing

Garth Graham

Herding • Making sure everything works well • Making sure the partnership is moving in the right direction • Helping us meet the product needs of our clients

Lisa Springer

STRATMOR | GROUP

We want your feedback REAL TIME

• Please use your phone and browse to the URL below

• You do NOT need a login • You will be asked a series of questions

throughout this session • Answer on phone, and results appear

instantly• You can also ask questions through web

page

www.PollEv.com/STRATMOR

STRATMOR | GROUP5

Projected Changes in the Population by Age(2012 – 2022)

Baby Boomers:Net Sellers

Gen XNet Buyers

MillennialsHome Buyers

STRATMOR | GROUP6

Owner and Renter Occupied Households &Homeownership Rate

STRATMOR | GROUP7

Sum of a Niche!

1. First time buyers

2. Millennials under 35

3. Minority borrowers

4. Evolving Product

Sum of Niches!

STRATMOR | GROUP

We want your feedback REAL TIME

• Please use your phone and browse to the URL below

• You do NOT need a login • You will be asked a series of

questions throughout this session • Answer on phone, and results appear

instantly• You can also ask questions through

web page

www.PollEv.com/STRATMOR

STRATMOR | GROUP9

How Do the Groups Compare?

1 Source: Ethics Reource Center, Ethics.org

STRATMOR | GROUP10

World Events Drive Perceptions

Source: Ethics Resource Center, Ethics.org

Foreclosure!

STRATMOR | GROUP11

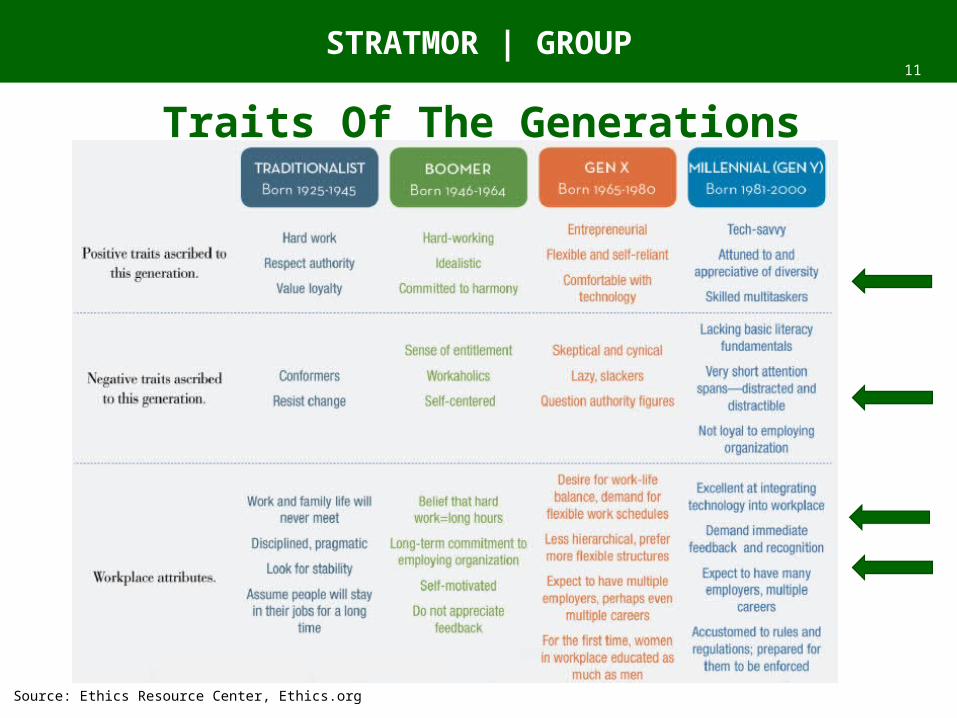

Traits Of The Generations

Source: Ethics Resource Center, Ethics.org

STRATMOR | GROUP12

Workplace Attributes

Source: Ethics Resource Center, Ethics.org

STRATMOR | GROUP13

How many social media accounts do you actively use?

STRATMOR | GROUP14

How active are you in Social Media?

STRATMOR | GROUP15

Do you have a formalized Social Media program?

STRATMOR | GROUP16

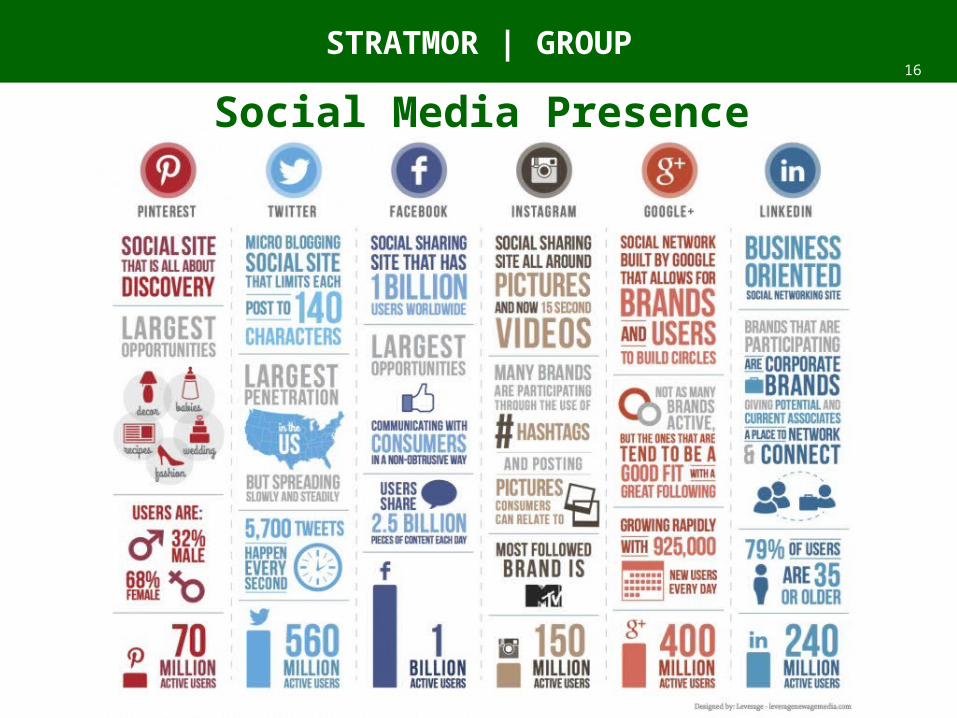

Social Media Presence

STRATMOR | GROUP17

Millennials and Money Millennials keep more of their assets in

cash, less in stocks - UBS report described them as “the most conservative generation since the Great Depression”

The average Millennial investor has 52 percent of their savings in cash, compared to 23 percent for other age groups

Accenture survey found high levels of mistrust of financial institutions among Millennials and a greater reliance on the Internet, social media, and personal networks for financial advice

The ten least-liked brands among members of this generation include four of the nation’s most powerful banks—Chase, BofA, Wells Fargo and Citigroup

STRATMOR | GROUP18

Millennials and Money 70 percent of Millennials thought that the way to pay for things five years from

now will be totally different and one-third said they didn’t believe that they will need a bank at all in the future

Almost all (88%) of Millennials do their banking online and half of those use their smart phone to do so

Three-fourths of Millennials (73%) to be “more excited about a new offering in financial services from Google, Amazon, Apple, Paypal or Square” than from a nationwide bank

STRATMOR | GROUP19

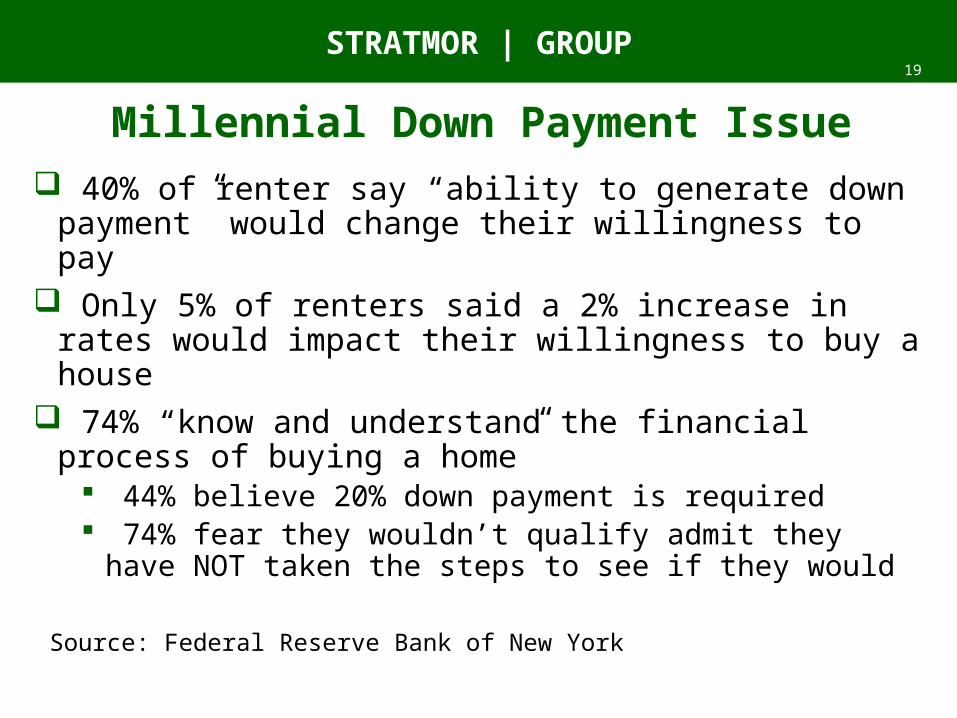

Millennial Down Payment Issue 40% of renter say “ability to generate down payment” would

change their willingness to pay Only 5% of renters said a 2% increase in rates would impact their

willingness to buy a house 74% “know and understand the financial process of buying a

home” 44% believe 20% down payment is required 74% fear they wouldn’t qualify admit they have NOT taken the steps

to see if they would

Source: Federal Reserve Bank of New York

STRATMOR | GROUP20

STRATMOR Originator Census and Compensation

STRATMOR | GROUP21

What percent of Retail Loan Originators are less than 35 years old?

STRATMOR | GROUP22

Millennial originators (less than 35 years old) are less productive than older originators?

STRATMOR | GROUP23

Background STRATMOR believes that the more you can understand and measure the key

attributes of your sales force, the better you will be able to proactively manage them

STRATMOR Originator Census survey focuses on five key areas: Production Distribution - Consistent with conventional wisdom, do 20% of your

Originators close 80% of your volume? Productivity by Quintile - What is the average productivity of your top quintile

of producers versus peers? Originator Age - What is the average age of your originators overall? By

production quintile? Turnover - What is your Originator turnover overall? By Age? By production

quintile? Many lenders maintain that they keep their core group and that turnover is limited to lower producing quintiles. Is that really true?

Tenure - What is the average tenure of originators by production quintile? Are your veterans out-producing the less experienced originators? How does your average tenure compare with peer group averages?

STRATMOR | GROUP24

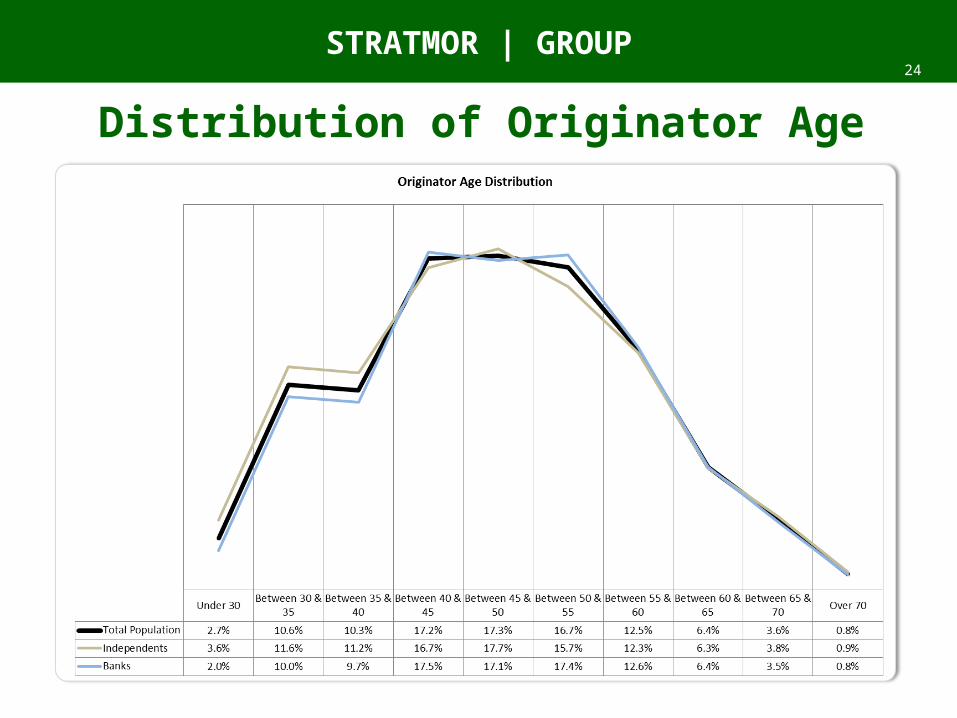

Distribution of Originator Age

STRATMOR | GROUP25

Key Findings from 2013 LO Census 40% of the originators do 80% of the business

Top 20% doing 55-57% of the total production Independent Mortgage companies originators top 20% do 61% of the

production The Top 20% of originators averaged 10 loans per month which is twice

the average production of the next quintile who originated 4.4 loans per month

The Bottom 20% of originators averaged less than one loan per month About 50% of the originator population is between the ages of 40-55

with an average age of 47 There was no material difference in ages by quintile

We had expected to see the Top 20% age to skew older than the average and the lower production quintiles to skew younger

The millennials productivity was the same as the older after normalizing for tenure

STRATMOR | GROUP26

# of Companies

Count of Originators Turnover % Avg Tenure Avg Age

Annual Avg Production per

Originator % of Total

Monthly Production per FTE Equivalent Purchase %

Annual Avg Production per

Originator % of Total

Monthly Production per FTE Equivalent Purchase %

Independent Mortgage Company 9 2,756.0 29.3% 2.7 47.2 7,621,111 100.0% 768,339 49.9% 32.0 100.0% 3.2 51.5%Bank Owned/Affi liated Mortgage 12 4,072.0 30.7% 3.5 47.9 11,484,877 100.0% 1,112,148 44.0% 57.5 100.0% 5.5 45.6%

Over $5 Billion 6 3,718.0 33.9% 3.2 47.2 10,556,731 100.0% 1,037,614 47.4% 50.1 100.0% 4.9 49.1%Between $2 Billion and $5 Billion 6 2,166.0 27.0% 3.3 48.1 9,743,958 100.0% 906,265 44.8% 47.8 100.0% 4.4 46.3%Between $1 Billion and $2 Billion 3 349.0 8.3% 3.6 50.0 11,040,492 100.0% 1,150,508 44.4% 48.0 100.0% 4.7 45.0%Under $1 Billion 6 595.0 29.1% 1.9 46.9 5,986,104 100.0% 688,406 47.0% 26.6 100.0% 3.0 48.6%

LO Primarily Stand-Alone Branches 12 4,276.0 32.7% 2.4 47.3 8,842,044 100.0% 906,701 50.0% 38.9 100.0% 4.0 51.7%LO Primarily Bank Branches 3 871.0 21.6% 5.7 46.7 11,929,307 100.0% 1,123,163 34.6% 66.9 100.0% 6.3 36.3%LO Mixed Bank & Stand-Alone Branches 6 1,681.0 28.3% 3.8 49.0 11,642,589 100.0% 1,060,293 43.1% 58.1 100.0% 5.3 44.3%Overall 6,828.0 30.1% 3.2 47.6 9,925,337 100.0% 971,707 46.4% 47.2 100.0% 4.6 48.0%

All OriginatorsOriginator Statistics Origination Dollars Origination Units

Key Statistics from 2013

Turnover averaged 30.1% for our sample in 2013 Average age of our survey group was 48 years old An average originator originated 4.6 loans in 2013 with 48% of

those being purchase loans

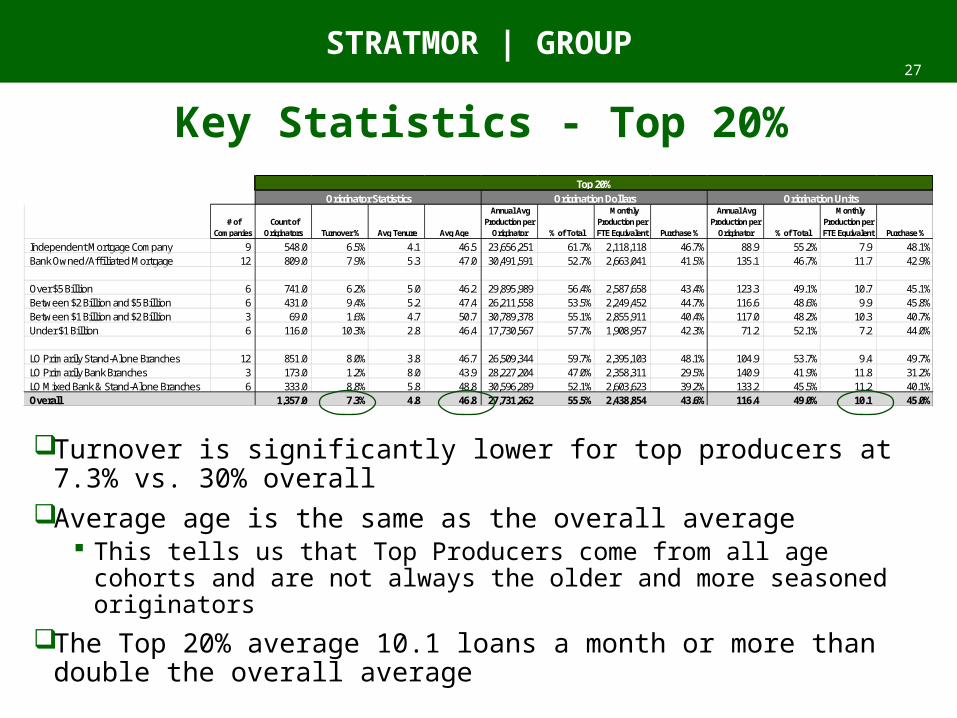

STRATMOR | GROUP27

Key Statistics - Top 20%

Turnover is significantly lower for top producers at 7.3% vs. 30% overall

Average age is the same as the overall average This tells us that Top Producers come from all age cohorts and are not

always the older and more seasoned originatorsThe Top 20% average 10.1 loans a month or more than double the

overall average

# of Companies

Count of Originators Turnover % Avg Tenure Avg Age

Annual Avg Production per

Originator % of Total

Monthly Production per FTE Equivalent Purchase %

Annual Avg Production per

Originator % of Total

Monthly Production per FTE Equivalent Purchase %

Independent Mortgage Company 9 548.0 6.5% 4.1 46.5 23,656,251 61.7% 2,118,118 46.7% 88.9 55.2% 7.9 48.1%Bank Owned/Affi liated Mortgage 12 809.0 7.9% 5.3 47.0 30,491,591 52.7% 2,663,041 41.5% 135.1 46.7% 11.7 42.9%

Over $5 Billion 6 741.0 6.2% 5.0 46.2 29,895,989 56.4% 2,587,658 43.4% 123.3 49.1% 10.7 45.1%Between $2 Billion and $5 Billion 6 431.0 9.4% 5.2 47.4 26,211,558 53.5% 2,249,452 44.7% 116.6 48.6% 9.9 45.8%Between $1 Billion and $2 Billion 3 69.0 1.6% 4.7 50.7 30,789,378 55.1% 2,855,911 40.4% 117.0 48.2% 10.3 40.7%Under $1 Billion 6 116.0 10.3% 2.8 46.4 17,730,567 57.7% 1,908,957 42.3% 71.2 52.1% 7.2 44.0%

LO Primarily Stand-Alone Branches 12 851.0 8.0% 3.8 46.7 26,509,344 59.7% 2,395,103 48.1% 104.9 53.7% 9.4 49.7%LO Primarily Bank Branches 3 173.0 1.2% 8.0 43.9 28,227,204 47.0% 2,358,311 29.5% 140.9 41.9% 11.8 31.2%LO Mixed Bank & Stand-Alone Branches 6 333.0 8.8% 5.8 48.8 30,596,289 52.1% 2,603,623 39.2% 133.2 45.5% 11.2 40.1%Overall 1,357.0 7.3% 4.8 46.8 27,731,262 55.5% 2,438,854 43.6% 116.4 49.0% 10.1 45.0%

Top 20%Originator Statistics Origination Dollars Origination Units

STRATMOR | GROUP28

Consumer Research Online / Offline Behavior

STRATMOR | GROUP29

REALTOR® Challenges Sixty-nine percent of REALTORS® reported

having a website for at least five years, 12 percent reported having a real estate blog, and 61 percent are using social media.

Realtors NEED more access to mortgage credit – it’s a need that must be met to expand their business

Only 17% of REALTORS have personal assistants, and 1/3 of those are shared, so they generally don’t have a lot of help in marketing and other lead generation activities

The typical REALTOR® is a 56-year-old white female who attended college and is a homeowner, (Fifty-seven percent of all REALTORS® are female)

They are absolutely desperate for the deal to close And there are 100k loan officers calling on 1M realtors --- if each LO can secure

10 relationships, and can convert every referral, that is only 50 deals per YEAR!

STRATMOR | GROUP30

Lengthy research period provides multiple opportunities to connect

Typical buyers search for 12 weeks Buyers who use agent, typically contact agents after 3 weeks

(which means the keep searching after that) 78% of home shoppers visit 3 or more sites prior to taking action

on real estate site Only 24% take action (generate lead) the same day they begin

search 36% take up to 60 days And 40% do not take action for up to 120 days

STRATMOR | GROUP31

Age of Internet User Much Different than Typical REALTOR®

86% of those who take action on site are LESS than 55 years old 67% of those take action are less than 44 years old And average age of Realtor is 56 years old! Understanding Realtors is key to being successful AND Diversify the bet into evolving Realtors or direct methods of

communication?

STRATMOR | GROUP32

Home Search in the Information Age1. Look at online listings

2. Check out Mortgage rates

3. Look at more information about homes

4. Find an agent (after several weeks)

5. Look up agent on internet, AND social media

6. Talk to agent

7. Receive referral, Pre-Approval encouraged

8. Search online for comps

9. Check out neighborhood stats

10. Send link to house to influencer

11. Drive through neighborhood

12. Look at house

13. Listen to Realtor spiel about mortgage

14. Look up loan officer on social media and internet

STRATMOR | GROUP34

Customer Satisfaction MortgageSAT survey system launched August 2013 with over

~45,000 customers surveyed We provide lenders insights into how their customer service

performs across a broad range of transaction, demographic, and organizational aspects

This reveals details in overall satisfaction Critical points in the process Preference of how contacted How applied Millennials vs previous generations

STRATMOR | GROUP35

Millennial Satisfaction Based on 45,000 surveys, Millennials (those borrowers under age

34) have roughly same satisfaction then older borrowers (88 vs 89)

They are even less likely to recommend (87 vs 89) but more likely to comment on social media (74 on a 100 point scale)

Under 34 Over 34 TOTAL Survey Size 12706 32797 45503Survey percent of Total 28% 72% 100%Satisfaction 89 89 89Likelihood to use again 88 90 89Likelihood to Comment 74 71 72Likelihood to Recommend 87 89 88

STRATMOR | GROUP36

First source of information For purchase borrowers, millennials are far more likely to seek internet and

friends/family for information 23% friends and family vs 14% older borrowers – highest satisfaction

with 91 11% internet vs 7% internet from older borrowers Millennials less likely (7%) to contact a branch office

Millennials Internet Realtor Other personal finance

professionalFamily or friends Branch office

Pct of Total 11% 42% 5% 23% 7%Sample Size 1172 4681 538 2517 758Satisfaction 87 88 86 91 92Likelihood to use again 88 89 86 92 93Likelihood to Comment 68 71 67 74 81Likelihood to Recommend 87 88 86 91 93

Previous GenerationsInternet Realtor Other personal finance

professionalFamily or friends Branch office

Pct of Total 7% 46% 5% 14% 9%Sample Size 1362 9090 1064 2803 1758Satisfaction 88 89 87 91 91Likelihood to use again 89 90 88 92 93Likelihood to Comment 70 72 68 75 76Likelihood to Recommend 89 90 88 92 93

STRATMOR | GROUP37

Relationships can be established via Internet or Phone

Less than 10% of purchase borrowers completed the application face to face, but have slightly higher satisfaction

19% completed it via the internet 69% completed via phone Customer satisfaction in all three methods was very similar

although face to face is more likely to comment on social media

Face to Face Internet Mail TelephonePct of Total 9% 19% 2% 69%

Sample Size 2900 5807 712 21447Satisfaction 90 88 89 89Likelihood to use again 90 89 89 90Likelihood to Comment 76 72 72 72Likelihood to Recommend 90 89 89 89

STRATMOR | GROUP38

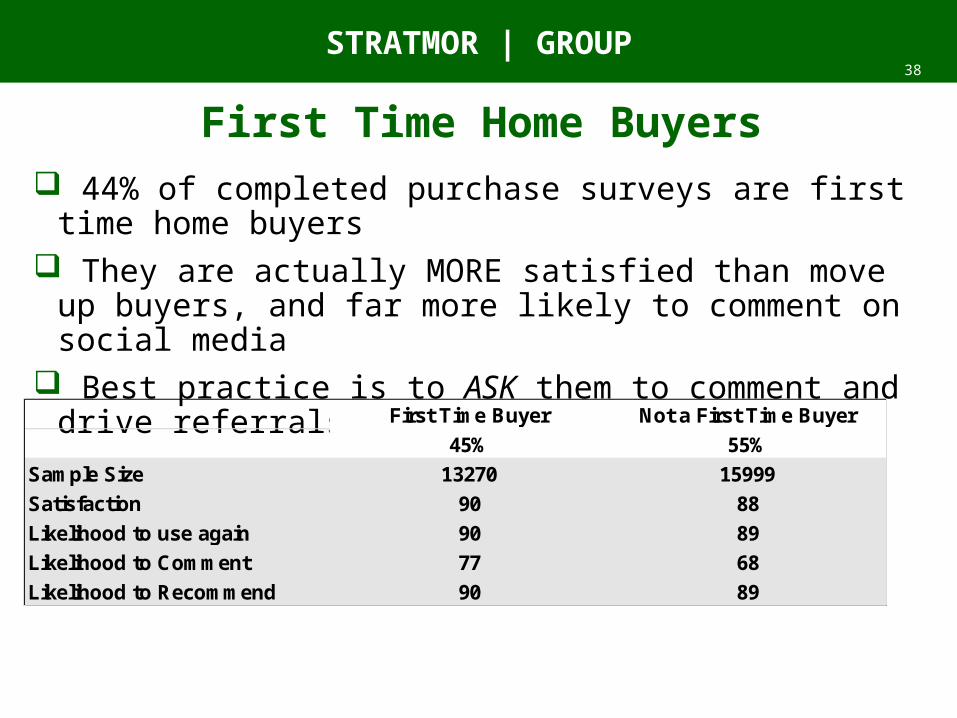

First Time Home Buyers 44% of completed purchase surveys are first time home buyers They are actually MORE satisfied than move up buyers, and far

more likely to comment on social media Best practice is to ASK them to comment and drive referrals

First Time Buyer Not a First Time Buyer45% 55%

Sample Size 13270 15999Satisfaction 90 88Likelihood to use again 90 89Likelihood to Comment 77 68Likelihood to Recommend 90 89

STRATMOR | GROUP

Importance of Alerts• MortgageSAT

automatically alerts lenders when customers are dissatisfied

• Quick call back from Senior Mgt has a huge impact on turning around satisfaction

• Having that push notification is a key to driving the quick call

• Note – Interaction with originator is a key driver of why choose a lender, AND big driver of satisfaction

Satisfaction Segment Percent Frequency SatisfactionSatisfaction 1-6 8% 1,405 24Satisfaction 7-8 10% 1,718 72Satisfaction 9-10 82% 14,651 97Number of Respondents

Response Count

17,774

Reason for choosing lender Percent Frequency SatisfactionInteraction with originator or loan officer 59% 4,037 94Lender of my previous mortgage 18% 1,245 85Other 11% 784 73Ability to close loan on time 5% 355 89Good reputation 4% 264 92Have other financial products 1% 72 83Material that was mailed to me 1% 85 83Good web-based tools 0% 27 89

Response Count

STRATMOR | GROUP

SPOC for origination?• Higher satisfaction

appears to exist when consumer only talks to one person

• Providing a checklist at application is a key driver of satisfaction (33 point difference!)

• Not asking for additional document drive satisfaction from 87 - 93

Worked with person other than Loan Officer Percent Frequency SatisfactionWorked with someone else 61% 4,172 87Worked only with Loan Officer 39% 2,697 93Number of Respondents

Response Count

6,869

Provided Checklist Percent Frequency SatisfactionProvided 88% 15,735 91Not provided 4% 737 58Don´t remember 7% 1,331 81Number of Respondents

Asked for additional docs Percent Frequency SatisfactionAsked 39% 6,214 87Not asked 45% 7,063 93Don´t remember 16% 2,458 92Number of Respondents

Response Count17,803

15,735

STRATMOR | GROUP

Customer preference

• Customers are most satisfied when lender proactively provides status to lender

• 67% of customers say they want status by email or outbound phone call

Method for receiving status updates Percent Frequency SatisfactionEmail from lender 59% 4,062 91Lender called me 24% 1,680 94I called 7% 508 67Other 6% 393 80Text message 2% 116 93Logging into website 1% 73 83Mobile app 0% 8 88Letter mailed to home 0% 29 88Number of Respondents

Preferred method for receiving updates Percent Frequency SatisfactionEmail 67% 4,580 90Phone call from lender 24% 1,618 88Text message 3% 216 88Other 3% 214 84Placing a phone call 2% 136 81Logging into website 1% 50 88Letter mailed to home 1% 42 81Mobile app 0% 13 87Number of Respondents

Response Count

Response Count6,869

6,869

STRATMOR | GROUP

People matter• Benchmarking

performance by all four primary individuals (LO, Processor, Underwriter, and Closer) and

• Benchmarking up to all levels of management (i.e. branch, region, area, division)

STRATMOR | GROUP43

Power of Big Data Data gives you ability to predict likelihood of consumers taking

action So, a consumer who is qualified for a mortgage is a better lead

than one that is not… But it’s a better lead if you know they had a life change event … If they are doing online search for real estate … If they recent listed their home for sale … Had a recent credit pull …. Are active on social media … Have a valid email address

STRATMOR | GROUP44

Monitor Households

Corporate Campaign Management - 3rd party Data to drive marketing efforts - Monitor for life change events, such as marriage and divorce- Monitor for property events: change of address, recent home listing, increase home value - Monitor for credit events, such as recent mortgage inquiries

Corporate Lead Management- Create corporate standards regarding lead assignment, including involvement of retail and consumer direct loan officers- Recruit and retain better LO’s through a commitment to retail marketing support using best of breed consumer components - Protect relationship with consumer when LO departs - Leverage corporate systems for lead management and referral management - Ensure compliance with regulatory standards, including CFPB, FCRA and Fair Lending13.5

Call Center Leads50% of leads

Retail Leads 50% of total leads

STRATMOR | GROUP

• 91% said that enhanced tools for lenders to monitor regulatory compliance during the loan cycle and/or to minimize the risk of regulatory non-compliance were “extremely important

• Both document management and system security tied for the next most important consideration. Overall, 82% of respondents said that greater use of document management or enhancement to imaging technology (e.g. OCR, data extraction, etc.) to improve the efficiency of the staff and the quality of the loan files was “extremely important.”

STRATMOR GROUP – PROPRIETARY & CONFIDENTIALNOT FOR EXTRNAL DISTRIBUTION

STRATMOR Executive Survey: Most Important

STRATMOR | GROUP

Technology Developments – Less Important

• Innovations such as mobile devices (46%) and CRM (41%) and Self Service tools (41%) all were considered less important by lenders.

46

STRATMOR GROUP – PROPRIETARY & CONFIDENTIALNOT FOR EXTRNAL DISTRIBUTION

STRATMOR | GROUP47

Questions and Comments --

STRATMOR | GROUP48

Strategies to Generate Millennial Mortgage Opportunities

Hire and retain millennials Consider mentoring by successful older staff Creating meaning and inclusiveness Recognition and feedback – “catch them doing something right” Patience – accept the differences, and give them time to grow

Millennial Outreach Hire millennials Focus on their needs – down payment for example Embrace their tools – mobile, text and online Self service is expected Use alternative referral sources

Embrace Data

STRATMOR | GROUP

Garth Graham, Managing Director 954-325-7816 [email protected]

What You Can Do

1. The consumer is central to the process – produce happy customers NOT just compliant loans

2. Embrace transparency – Millennials don’t trust!

3. Need to hire younger and need to mentor be successful

4. Invest in technology that enables you to connect with consumers

5. Big Data can generate big results

6. Measure and manage to high customer satisfaction

Check out my weekly column in National Mortgage News

STRATMOR | GROUP50

Questions and Comments --

STRATMOR | GROUP52

Women and Marriage Women are as satisfied as men They are also more likely to comment on social media And borrowers who are separated are happier then the others

Gender Percent Frequency Satisfaction

Male 67% 3,917 90

Female 32% 1,879 90

Information Not Provided 1% 69 86

Number of Respondents 5,865

Marital Status Percent Frequency Satisfaction

Married 63% 3,672 90

Unmarried 37% 2,162 90

Separated 0% 26 92

Number of Respondents 5,860

STRATMOR | GROUP53

The importance of Social Media A way to engage for professionals to engage other professionals

and build brand So, use linked in, twitter and facebook to find Realtors and other

referral sources Provide value added information – something happens nearly every

day that is deserving of commentary Make it professional and personal – how do things make you feel?

What do you think about changes in the market Engaging consumers in a compliant way – not “offering” loans, but

sharing your experience in the industry Use what you are good at – not being phony

STRATMOR | GROUP54

Power of data aggregation Outlook has plug-ins for facebook and linked in (FREE!) Let’s you see picture and immediately link to social media page

for those you are connected to Let’s you immediately look up people on social media based on

email – new borrowers (before you call them), or new Realtors before you walk in office

STRATMOR | GROUP56

Sales Activity may not be a Funnel Old model was a funnel, with the

opportunities always flowing down, with fallout reducing the amount that comes out the bottom.

New Model is more like a flight path, with customers bouncing from spot to spot seeking out information.

Data analyzed by Google (search history and behavior) and Compete (click steam behavior) reveals the trend

STRATMOR | GROUP57

New Sales Funnel 90% of home buyers rely on the

internet as one of their primary research sources

52% turn to internet as their first step Our MortgageSAT data for last month

showed Realtors the first step for financing less than 40% of the time

Real Estate search up 50% in the past year, and up 253% in the past 4 years

40% of Real Estate search on mobile devices, an increase of 120% in past year

89% of Real Estate Consumers ALSO use a Real Estate Agent

STRATMOR | GROUP58

Do you have use texts to communicate with borrowers?

STRATMOR | GROUP

MGIC.com/social

2005:Q4 2006:Q4 2007:Q4 2008:Q4 2009:Q4 2010:Q4 2011:Q4 2012:Q4 2013:Q40%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Share borrowers age 25 - 30 years old with new mortgage originations

no student debt with current student debt with current student debt of 100K+

with 90+ delinquent student debt with student debt, current or delinquent

Source: New York Fed Consumer Credit Panel / Equifax

STRATMOR | GROUP60

BackgroundThe STRATMOR Compensation Connection is an annual survey of compensation

amounts and structure.Survey is set up in modules:

Executive Management Retail Sales Consumer Direct Sales TPO Sales Fulfillment (All Channels) Production Support

Results are available to participants and include: Cross tabulation based on:

• Independents vs. bank-owned lenders • Production scale brackets to differentiate between large and mid-size lenders• Relevant position-related metrics (tenure, management scope)

Key executive, sales, and back office roles within your organization Compensation structures along with compensation levels

STRATMOR | GROUP61

Positions Surveyed for CD SalesSenior Consumer Direct Production Executive The top sales position in the Consumer Direct channel

Call Center Manager Responsible for recruiting, hiring, managing, and training call center personnel including loan officers in a particular call center

Campaign Manager Coordinates and assists with the marketing activities, including database and direct mail marketing, and ecommerce marketing

campaigns.

Producing Team Leader Manages the activities of a call center team, including training and managing loan officers; Also acts as a loan officer by originating

loans

Non-Producing Team Leader Manages the activities of a call center team, including training and managing loan officers; Does not originate loans

Loan Officer Located in call center; receives incoming calls (leads) and attempts to convert to application; may make outbound marketing calls;

counsel borrowers, recommend loan products ; Takes original application directly with borrower and coordinates with loan processors and underwriters in obtaining information necessary to close the loan.

Call Screener Assists the sales consultants by taking inbound calls from clients including providing clients with product, program and rate

information

STRATMOR | GROUP62

Sample Results – CD Loan Officer

Bank Independent Under $1B Over $1B Retention New Customer12 6 6 6 6 7 5 8

Using the average for the year, how many Loan Officers - Non-Exempt did your organization employ in 2013? 83.7 35.7 131.7 15.7 151.7 62.2 113.8 49.8

What was your Loan Officer - Non-Exempt turnover for 2013? 64% 40% 87% 100% 27% 84% 35% 33%

How many loans, on average, did an Loan Officer close per month? 14.5 11.6 16.9 9.0 20.8 9.9 21.7 25.2

What was the average compensation for the Loan Officers -Non-Exempt for 2013?Base Salary 24,407 26,594 22,219 26,403 22,410 27,454 20,141 27,582 Overtime 2,039 2,805 1,272 2,070 2,008 2,295 1,680 928 Incentive / Variable Compensation 63,450 58,499 68,401 56,890 70,010 62,007 65,470 55,679 Total 89,895 87,898 91,892 85,363 94,427 91,755 87,291 84,189

What was the average compensation for the Loan Officers -Non-Exempt for 2013?Base Salary 27% 30% 24% 31% 24% 30% 23% 33%Overtime 2% 3% 1% 2% 2% 3% 2% 1%Incentive / Variable Compensation 71% 67% 74% 67% 74% 68% 75% 66%Total 100% 100% 100% 100% 100% 100% 100% 100%

Is the monthly Base Salary paid to Loan Officers -Non-Exempt a recoverable amount?Yes 0% 0% 0% 0% 0% 0% 0% 0%No 100% 100% 100% 100% 100% 100% 100% 100%

Loan Officer - Non-Exempt

Job Description - Located in call center; receives incoming calls (leads) and attempts to convert to application; may make outbound marketing calls; counsel borrowers, recommend loan products. Takes original application directly with borrower (over the phone or in person) and coordinates with loan processors and underwriters in obtaining information necessary to close the loan. Classified as Inside Sales under Department of Labor guidelines. Typically classified as Non-Exempt employees and are eligible for Overtime.

2013 Survey Average

Type of Company Annual VolumeCross-Tabulated Results

Source of Loans 2012 Survey Average

STRATMOR | GROUP

Bank Independent Under $1B Over $1B Retention New Customer12 6 6 6 6 7 5 8

Please enter the percentage breakdown of the variable portion of Cash Compensation paid to the Loan Officers - Non-Exempt for 2013.FLAT % based on production VOLUMES 23% 33% 12% 33% 12% 0% 36% 24%TIERED % based on production VOLUMES 37% 19% 55% 37% 37% 31% 46% 21%Based on FLAT $/loan 15% 30% 0% 30% 0% 26% 0% 0%Based on TIERED $/loan 15% 15% 15% 0% 30% 0% 36% 24%HYBRID commission equal to greater of % or $/loan 0% 0% 0% 0% 0% 0% 0% 0%Based on the achievement of quantitative and/or qualitative OBJECTIVES 10% 3% 17% 0% 19% 15% 2% 18%DISCRETIONARY 1% 0% 2% 0% 2% 0% 2% 13%OTHER 0% 0% 0% 0% 0% 0% 0% 1%Total 100% 100% 100% 100% 100% 71% 122% 100%

Loan Officer - Non-Exempt commissions vary by:Purchase vs. Refinance 25% 17% 33% 0% 50% 0% 60% 13%New vs. Existing Customers 0% 0% 0% 0% 0% 0% 0% 25%Other: Lead Source - Capture Rate - Customer Service 8% 17% 0% 17% 0% 14% 0% 13%

Do your offer more than one compensation plan to Loan Officers - Non-Exempt?Yes, Loan Officers can choose among a variety of plans 0% 0% 0% 0% 0% 0% 0% 13%Yes, but compensation plans vary by geography/branch 17% 0% 33% 17% 17% 14% 20% 25%No, we only offer one Loan Officer plan 83% 100% 67% 83% 83% 86% 80% 50%

Loan Officer - Non-Exempt plans have the following features:Minimum Payout 33% 50% 17% 33% 33% 29% 40% 25%Maximum Payout 33% 33% 33% 50% 17% 43% 20% 13%Quarterly volume add-on 0% 0% 0% 0% 0% 0% 0% 25%Annual volume add-on 17% 33% 0% 17% 17% 14% 20% 38%Quality Control Components 50% 67% 33% 50% 50% 43% 60% 50%

Loan Officer - Non-Exempt

Job Description - Located in call center; receives incoming calls (leads) and attempts to convert to application; may make outbound marketing calls; counsel borrowers, recommend loan products. Takes original application directly with borrower (over the phone or in person) and coordinates with loan processors and underwriters in obtaining information necessary to close the loan. Classified as Inside Sales under Department of Labor guidelines. Typically classified as Non-Exempt employees and are eligible for Overtime.

2013 Survey Average

Type of Company Annual VolumeCross-Tabulated Results

Source of Loans 2012 Survey Average

STRATMOR | GROUP64

Consumer Direct Percent of Units High of 46%

of units in 2012

35% of units in 2014 and actually rising YTD 2015

By state is very interesting…

Highest percent of CD volume

VT OK MS LA NH RI AR ME AL NM

STRATMOR | GROUP65

CD is rising for both Refinance and Purchase

Refinance volume was over 50% of units 2013-2014 Purchase units have risen from 12% of units to over 21% of units in the past 5

years

STRATMOR | GROUP66

Value Proposition For CD CD refinance loans typically have higher rates than traditional retail while…. (4

bps higher in 2015, avg 3 bps over 7 years) CD purchase loans are typically offered at lower rates than retail – 14 bps

average over 7 years

2008 2009 2010 2011 2012 2013 2014 2015 AverageTraditional Retail 6.10 5.12 4.76 4.45 3.71 3.85 4.14 3.83 4.50 Consumer Direct 5.96 4.93 4.60 4.34 3.59 3.74 4.00 3.66 4.35 Average Delta (0.14) (0.19) (0.16) (0.11) (0.12) (0.11) (0.14) (0.17) (0.14)

Purchase Only Average Interest Rate2008 2009 2010 2011 2012 2013 2014 2015 Average

Traditional Retail 5.87 4.93 4.67 4.36 3.77 3.70 4.18 3.87 4.42 Consumer Direct 5.84 4.96 4.71 4.39 3.81 3.73 4.24 3.91 4.45 Average Delta (0.03) 0.04 0.04 0.03 0.04 0.03 0.05 0.04 0.03

Refi & Cash Out Only Average Interest Rate

STRATMOR | GROUP67

36% of eligible voters are Millennials $1.6T (Trillion) home purchases by 2018 (in a market that is only

….) More racially diverse - Minority young householders = 28% in

1995; 41% in 2014 Married later - Young adult householders living with a spouse:

60% in the 1980s; 50% during housing boom; 42% in 2014 Higher education - Young adult householders that are college

grads: 32% in the 1995; nearly half in 2014 12% of renters or 5.2 million renters nationwide plan to buy in the

next year

STRATMOR | GROUP68

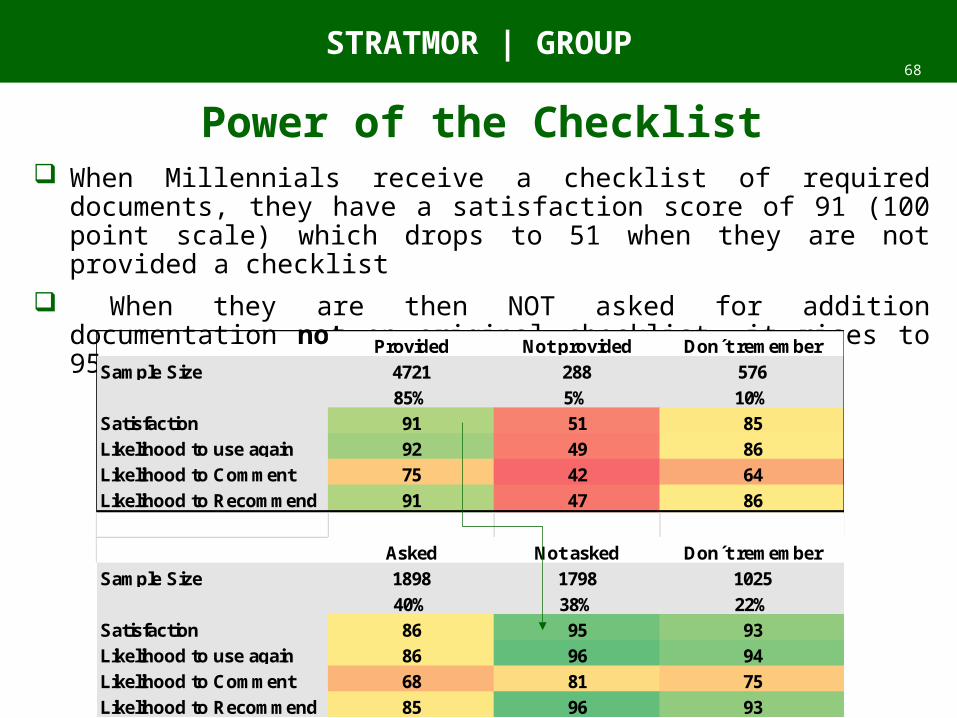

Power of the Checklist When Millennials receive a checklist of required documents, they have a

satisfaction score of 91 (100 point scale) which drops to 51 when they are not provided a checklist

When they are then NOT asked for addition documentation not on original checklist, it rises to 95

Provided Not provided Don t rememberSample Size 4721 288 576

85% 5% 10%Satisfaction 91 51 85Likelihood to use again 92 49 86Likelihood to Comment 75 42 64Likelihood to Recommend 91 47 86

Asked Not asked Don t rememberSample Size 1898 1798 1025

40% 38% 22%Satisfaction 86 95 93Likelihood to use again 86 96 94Likelihood to Comment 68 81 75Likelihood to Recommend 85 96 93

STRATMOR | GROUP69

Mobile Messaging Younger generations over 100 messages per day, and growing