Embed Size (px)

Citation preview

©2017 STRATMOR Group. All Rights Reserved.Proprietary & Confidential.

Digital Mortgage AdoptionEconomic and Market Drivers

1

STRATMOR Group –Proprietary & Confidential 2

DIGITAL MORTGAGE SERIOUS TOPIC

STRATMOR Group –Proprietary & Confidential

• Find Me In The App • And Start a Chat• Will reply today • Recharge Lounge

3

STRATMOR Group –Proprietary & Confidential 4

STRATMOR Group –Proprietary & Confidential

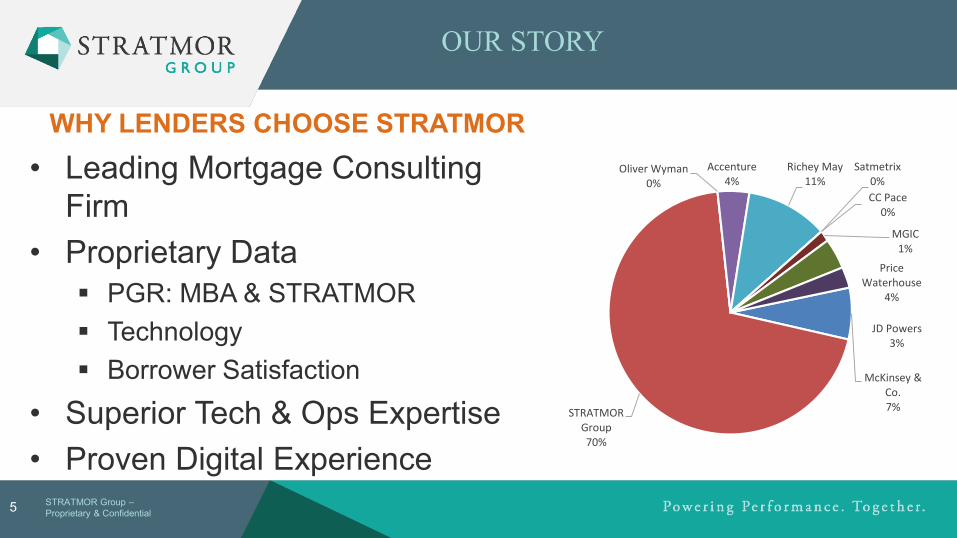

WHY LENDERS CHOOSE STRATMOR

5

OUR STORY

• Leading Mortgage Consulting Firm

• Proprietary Data▪ PGR: MBA & STRATMOR▪ Technology ▪ Borrower Satisfaction

• Superior Tech & Ops Expertise• Proven Digital Experience

McKinsey & Co.7%STRATMOR

Group70%

Oliver Wyman0%

Accenture4%

Richey May 11%

Satmetrix0%CC Pace

0%

MGIC1%

Price Waterhouse

4%

JD Powers3%

STRATMOR Group –Proprietary & Confidential

1. “Digital” (or dot.com) does not guarantee success ▪ A cautionary tale…▪ This is serious business

2. What is driving the Digital Mortgage trend and..3. What is the current adoption level 4. Ready to “Speed Data” ?

6

Today’s Discussion

STRATMOR Group –Proprietary & Confidential

STRATMOR GroupProprietary & Confidential Not for External Distribution

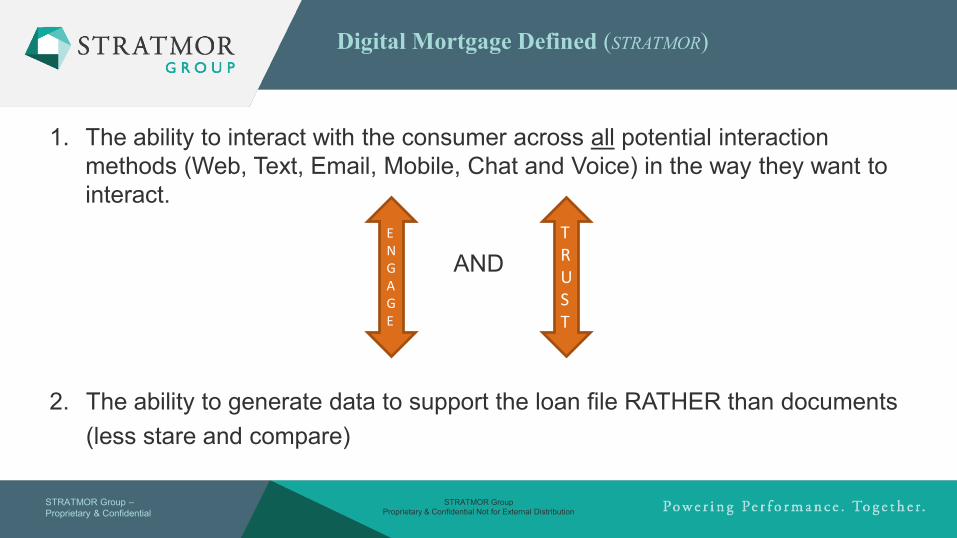

Digital Mortgage Defined (STRATMOR)

1. The ability to interact with the consumer across all potential interaction methods (Web, Text, Email, Mobile, Chat and Voice) in the way they want to interact.

AND

2. The ability to generate data to support the loan file RATHER than documents (less stare and compare)

ENGAGE

TRUST

STRATMOR Group –Proprietary & Confidential

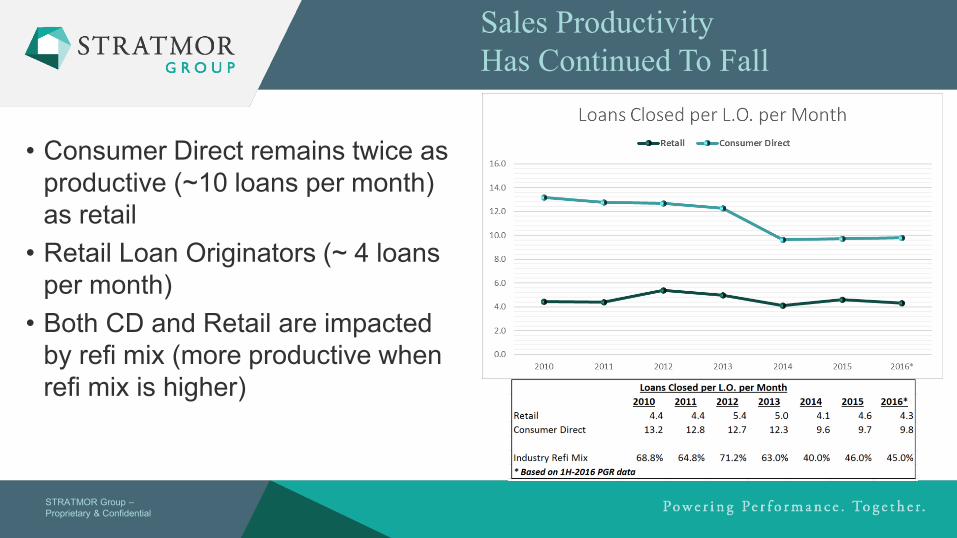

Sales Productivity Has Continued To Fall

• Consumer Direct remains twice as productive (~10 loans per month) as retail

• Retail Loan Originators (~ 4 loans per month)

• Both CD and Retail are impacted by refi mix (more productive when refi mix is higher)

STRATMOR Group –Proprietary & Confidential

Direct Expense ($/loan)

• Costs continually rising since 2010 with retail now over $6,000 per loan,

• Sales represent well over half (50%) of the expense

• Production Expense (Direct Expense) = all costs from point-of-sale through closing (LO’s, Sales Managers, Processors, Underwriters, Closers, Sales and Ops Management.)

Source: PGR: MBA and STRATMOR Peer Group Roundtables

STRATMOR Group –Proprietary & Confidential 10

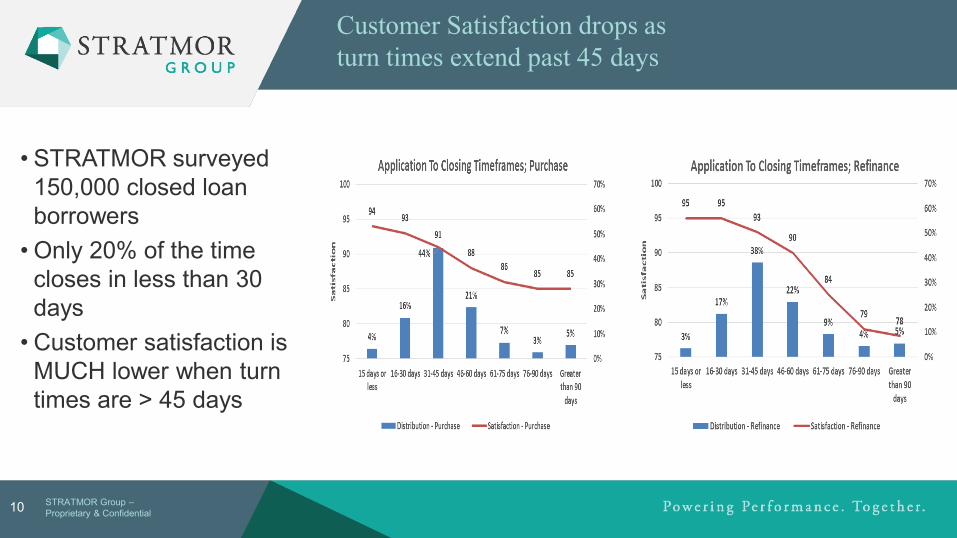

Customer Satisfaction drops as turn times extend past 45 days

• STRATMOR surveyed 150,000 closed loan borrowers

• Only 20% of the time closes in less than 30 days

• Customer satisfaction is MUCH lower when turn times are > 45 days

STRATMOR Group –Proprietary & Confidential 11

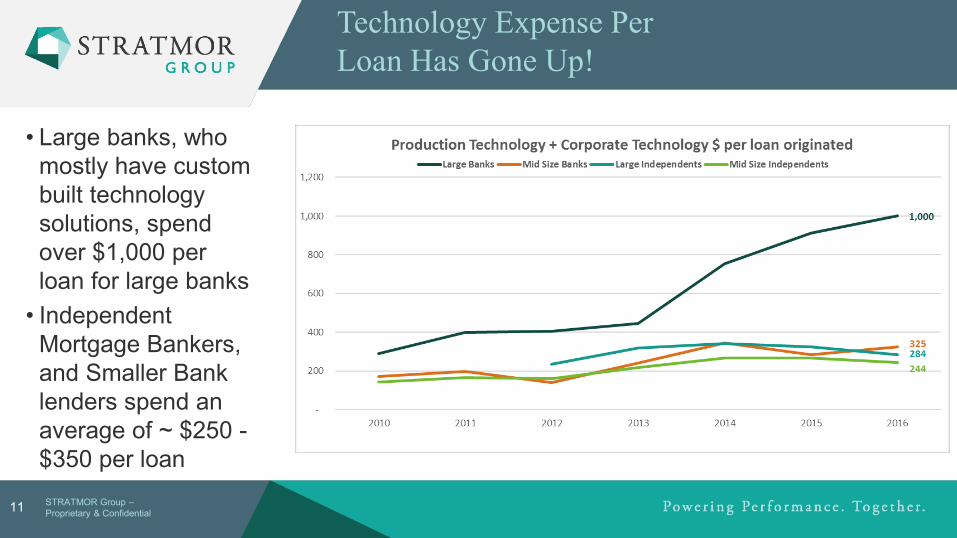

Technology Expense Per Loan Has Gone Up!

• Large banks, who mostly have custom built technology solutions, spend over $1,000 per loan for large banks

• Independent Mortgage Bankers, and Smaller Bank lenders spend an average of ~ $250 -$350 per loan

STRATMOR Group –Proprietary & Confidential

The Obvious Conclusion….

It’s almost IMPOSSIBLE for a lender to spend TOO MUCH money on Technology if the ROI is delivered.

STRATMOR Group –Proprietary & Confidential 13

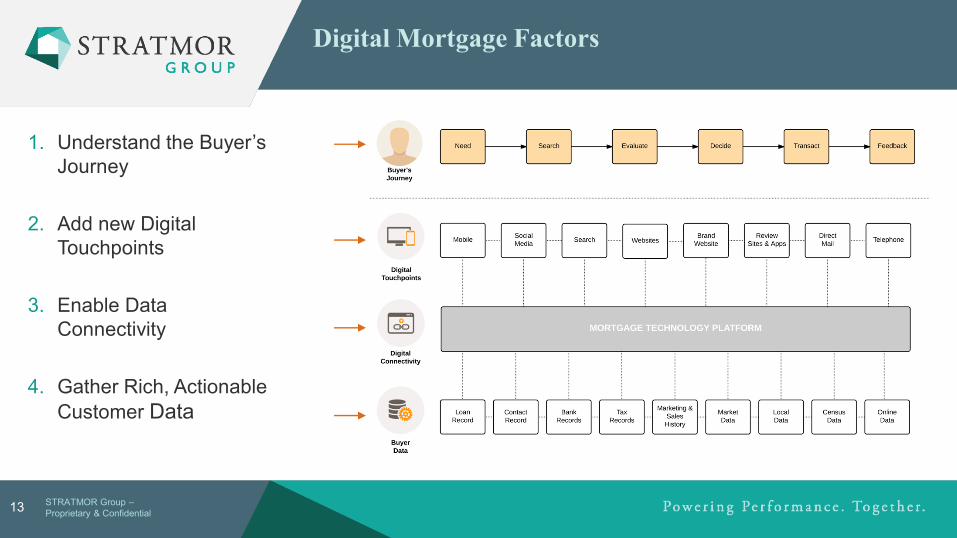

1. Understand the Buyer’s Journey

2. Add new Digital Touchpoints

3. Enable Data Connectivity

4. Gather Rich, Actionable Customer Data

Digital Mortgage Factors

a

STRATMOR Group –Proprietary & Confidential

DIGITAL MORTGAGE

14

STRATMOR Group –Proprietary & Confidential

Survey Structure and Analysis Approach• The results presented represent sample of top 200

companies• The survey asked lenders the level of adoption for 28

unique capabilities across 4 functional areas.

1. General Communications with Borrowers Capabilities2. Application and Approval Capabilities3. Loan Processing Capabilities4. Closing Capabilities

Proprietary and ConfidentialNot for External Distribution15

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

STRATMOR Group –Proprietary & Confidential

Survey Structure and Analysis Approach• For each of the capabilities, lenders had the follow choice in

regards to their level of adoption of digital mortgage1. In Production (Live)2. In Development3. In Planning4. Not Started5. Not Doing6. Not Sure / Do Not Know

• Because our focus is on which capabilities are currently live or in active development, our analysis will focus on responses for these top 2 categories – In Production and In Development.

Proprietary and ConfidentialNot for External Distribution16

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Key Findings – Adoption of Digital Capabilities• The adoption of Digital Mortgage is well underway with many key capabilities across a range of

functions and with many lenders reporting that the capabilities are “Live” or “In Development”.• While it didn’t hold true for every capability surveyed, in general, the Independents have adopted

more Digital Mortgage functionality than the Banks. ▪ Because the Independents have more control over their corporate technology and project management than the Banks, who

often are beholden to the corporate bank parent for these services, they can develop and deploy Digital Mortgage faster.

• Our results show that Lenders who are active in Consumer Direct are farther along in adopting Digital Mortgage capabilities. ▪ Because these groups tend to more centralized and technology driven, the new systems and processes are easier to roll out than

to a distributed Retail sales force.

• We also found that Large Lenders were more advanced than Mid-Size Lenders. ▪ Given the larger technology staff, Large Lenders are more likely to have resources devoted to researching, selecting,

implementing and integrating Digital Mortgage capabilities.

17

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

As Lenders adoption increases, STRATMOR believes that Digital Mortgage will be the driving organizing principle for the mortgage industry going forward.

Proprietary and ConfidentialNot for External Distribution

18

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Proprietary and ConfidentialNot for External Distribution

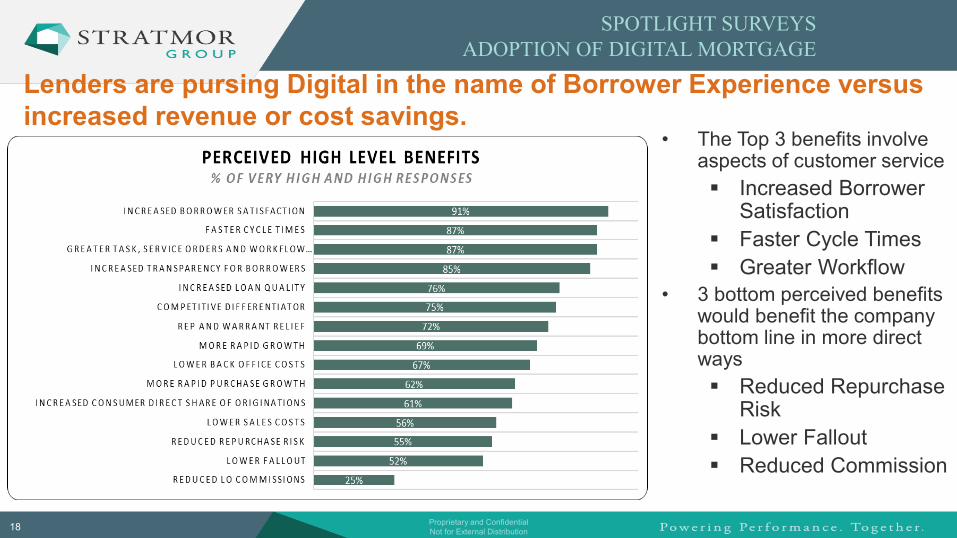

• The Top 3 benefits involve aspects of customer service▪ Increased Borrower

Satisfaction▪ Faster Cycle Times▪ Greater Workflow

• 3 bottom perceived benefits would benefit the company bottom line in more direct ways▪ Reduced Repurchase

Risk▪ Lower Fallout▪ Reduced Commission

Lenders are pursing Digital in the name of Borrower Experience versus increased revenue or cost savings.

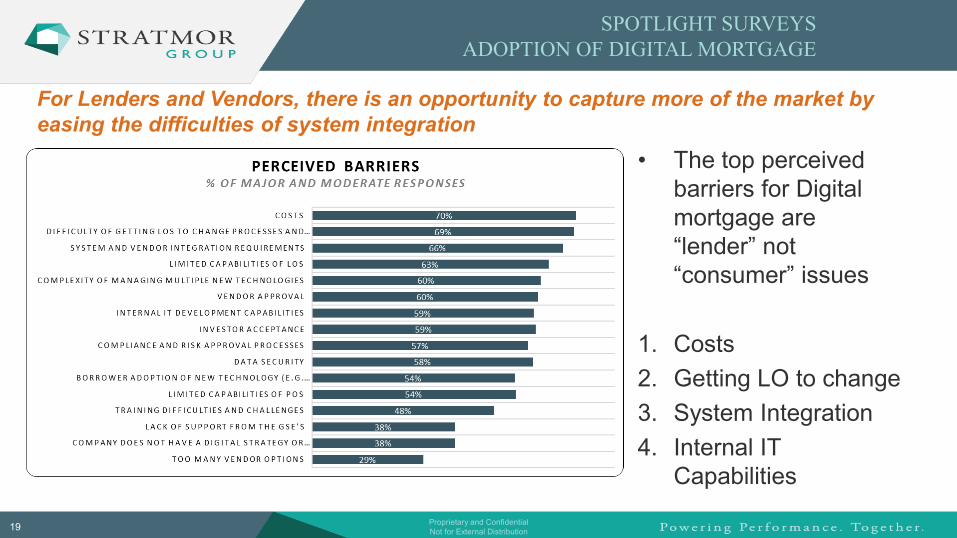

For Lenders and Vendors, there is an opportunity to capture more of the market by easing the difficulties of system integration

19

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Proprietary and ConfidentialNot for External Distribution

• The top perceived barriers for Digital mortgage are “lender” not “consumer” issues

1. Costs2. Getting LO to change3. System Integration 4. Internal IT

Capabilities

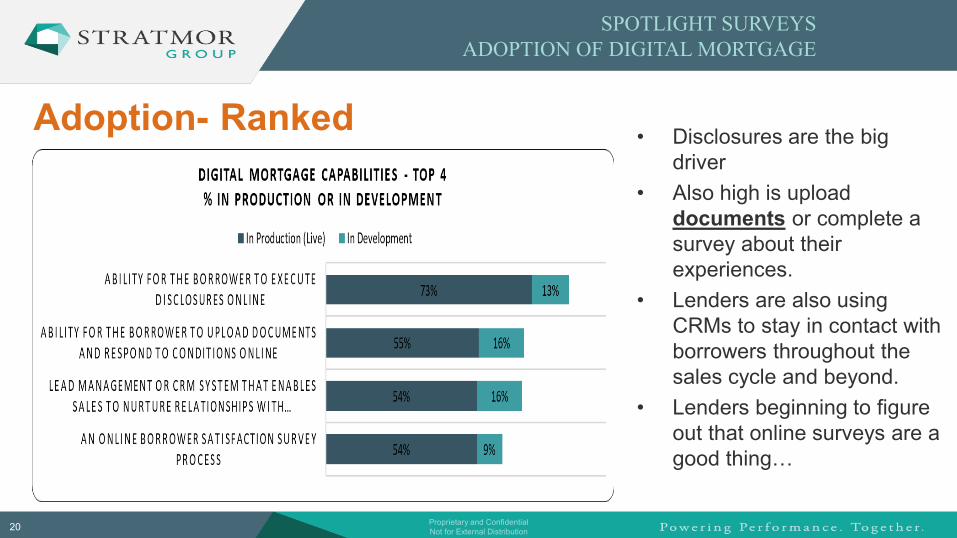

Adoption- Ranked

20

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Proprietary and ConfidentialNot for External Distribution

• Disclosures are the big driver

• Also high is upload documents or complete a survey about their experiences.

• Lenders are also using CRMs to stay in contact with borrowers throughout the sales cycle and beyond.

• Lenders beginning to figure out that online surveys are a good thing…

Next

21

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Proprietary and ConfidentialNot for External Distribution

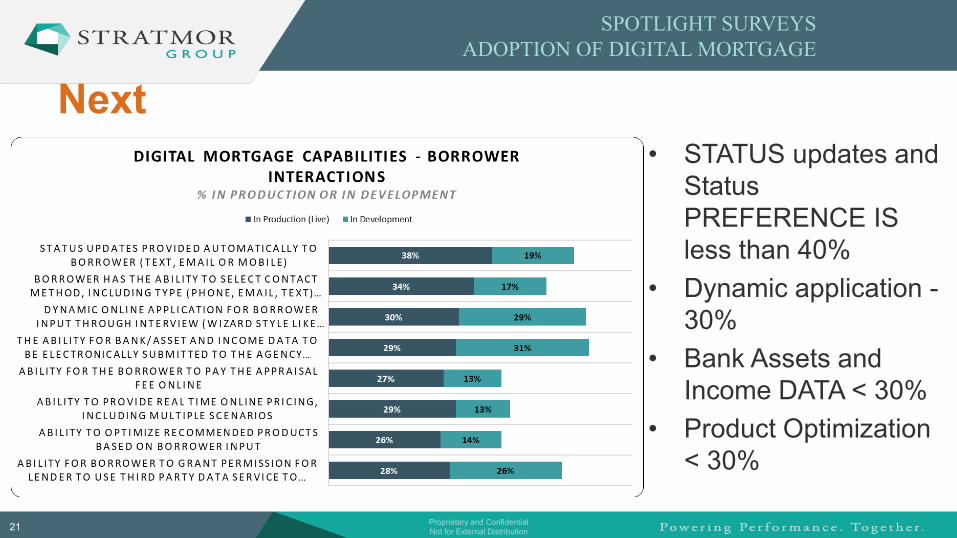

• STATUS updates and Status PREFERENCE IS less than 40%

• Dynamic application -30%

• Bank Assets and Income DATA < 30%

• Product Optimization < 30%

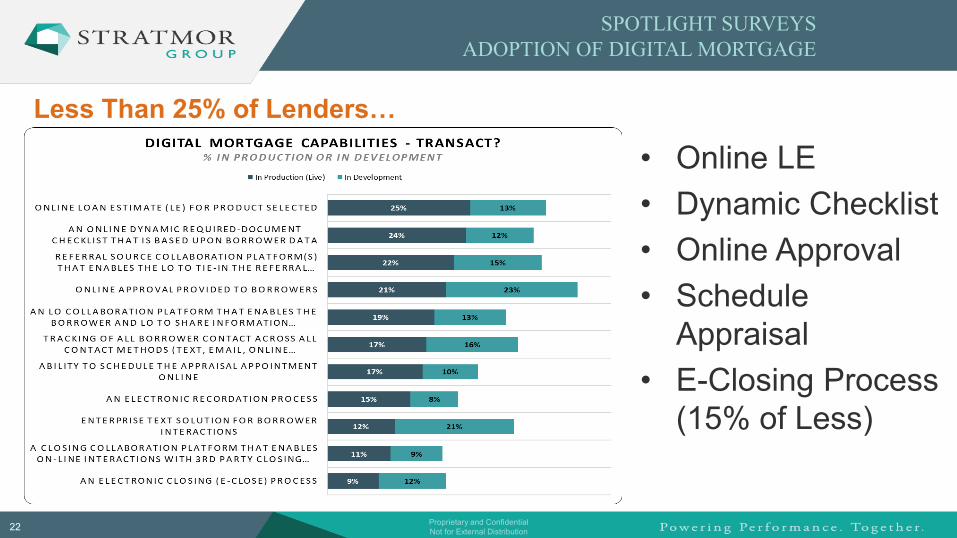

Less Than 25% of Lenders…

22

SPOTLIGHT SURVEYSADOPTION OF DIGITAL MORTGAGE

Proprietary and ConfidentialNot for External Distribution

• Online LE• Dynamic Checklist • Online Approval • Schedule

Appraisal • E-Closing Process

(15% of Less)

STRATMOR Group –Proprietary & Confidential

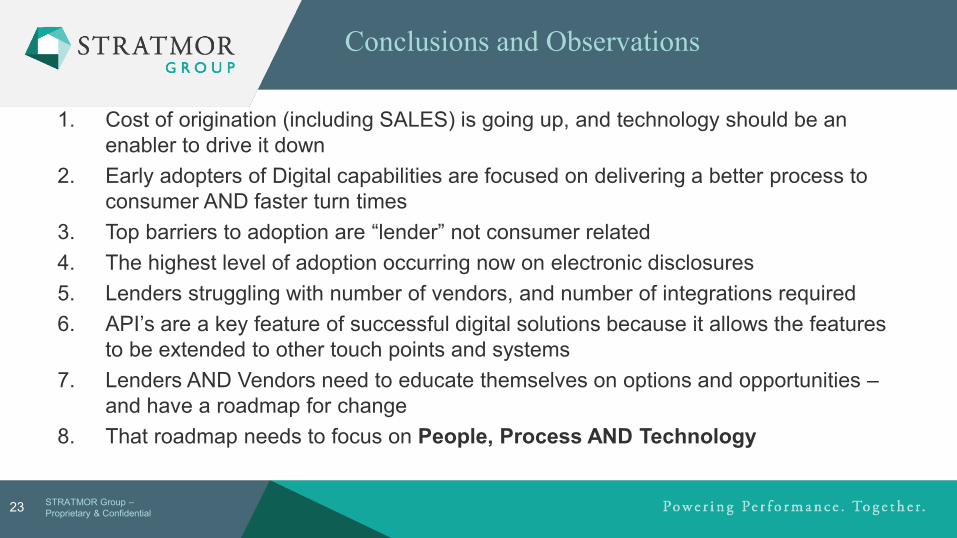

1. Cost of origination (including SALES) is going up, and technology should be an enabler to drive it down

2. Early adopters of Digital capabilities are focused on delivering a better process to consumer AND faster turn times

3. Top barriers to adoption are “lender” not consumer related 4. The highest level of adoption occurring now on electronic disclosures 5. Lenders struggling with number of vendors, and number of integrations required 6. API’s are a key feature of successful digital solutions because it allows the features

to be extended to other touch points and systems 7. Lenders AND Vendors need to educate themselves on options and opportunities –

and have a roadmap for change 8. That roadmap needs to focus on People, Process AND Technology

23

Conclusions and Observations

STRATMOR Group –Proprietary & Confidential

• Find Me In The App • And Start a Chat• Will reply today • Recharge Lounge

24

STRATMOR Group –Proprietary & Confidential

CONNECT WITH ME STRATMOR GROUP.COM

GARTH GRAHAM

www.linkedin.com/in/garthgraham/http://www.stratmorgroup.com/stratmor-insights/https://twitter.com/garthgraham

https://www.nationalmortgagenews.com/author/garth-graham-nmn871

(954) 325-7816

©2017 STRATMOR Group. All Rights Reserved.Proprietary & Confidential.

Digital Mortgage Trends

26