Embed Size (px)

Citation preview

Strategy for Success

Agenda

1

9:00 am ……...Strategic Overview……………………………………Ian Dundas

Core Area Discussion………………………………...Ray Daniels

US Oil - Bakken

US Gas - Marcellus

Canadian Oil - Waterfloods

Canadian Gas - Deep Basin

Financial Strategy……………………………………..Rob Waters

Managing Commodity & Takeaway Risk……………Eric Le Dain

11:30 am……..Summary……………………………………………….Ian Dundas

Enerplus Executive Team

2

Ian Dundas Incoming President & Chief Executive Officer

Ray Daniels Senior VP, Operations

Eric Le Dain Senior VP, Strategic Planning, Reserves & Marketing

Robert Waters Senior VP & Chief Financial Officer

Jo-Anne Caza VP, Corporate & Investor Relations

Robert Kehrig VP, Business Development and New Plays

Gord Love VP, Technical and Operations Services

David McCoy VP, Corp. Services, General Counsel & Corporate Secretary

Edward McLaughlin President, Enerplus USA

Brien Perry VP, Human Resources

Chris Stephens VP, Canadian Assets

Patrick 'Scott' Walsh VP, Information Systems

Kenneth Young VP, Land

Enerplus Board of Directors

3

Douglas R. Martin, BA, MBA, CA (Chairman)

David H. Barr, BSc

Edwin V. Dodge, BEng, MBA

Ian C. Dundas, Incoming President & Chief Executive Officer, Enerplus Corporation

Jim Fraser, BSc

Robert B. Hodgins, Honors BA, CA

Susan M. MacKenzie, BEng, MBA

Donald J. Nelson, BSc, PEng

David. P. O’Brien, BA (Hons), BCL

Elliott Pew, BSc, MA

Glen D. Roane, BA, MBA

Sheldon Steeves, BSc

Corporate Strategy

Deliver sustainable, profitable growth and income to investors

• Annual growth target of ~5% per share with yield of ~5% provides

attractive total return

• Development of top tier growth plays and mature foundation assets

• Disciplined, return-based capital allocation and active portfolio

management

• Diligent cost control and operational efficiency

• Preservation of financial flexibility and strong balance sheet

4

5

Focus

Profitability

Sustainability

6

Focus

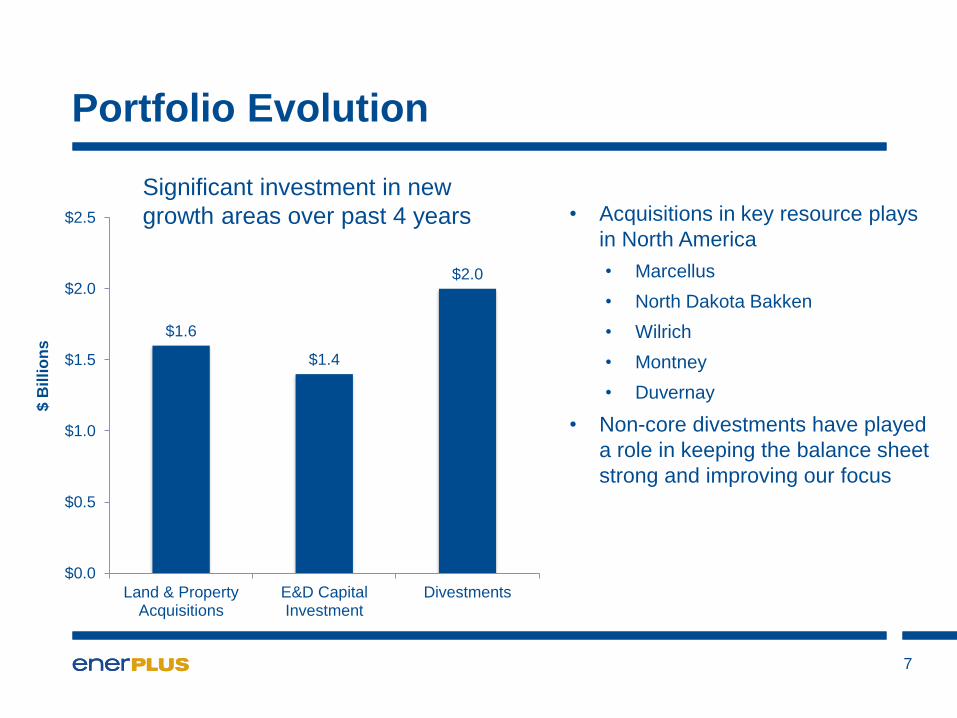

Portfolio Evolution

• Acquisitions in key resource plays

in North America

• Marcellus

• North Dakota Bakken

• Wilrich

• Montney

• Duvernay

• Non-core divestments have played

a role in keeping the balance sheet

strong and improving our focus

7

$1.6

$1.4

$2.0

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

Land & PropertyAcquisitions

E&D CapitalInvestment

Divestments

$ B

illi

on

s

Significant investment in new

growth areas over past 4 years

8

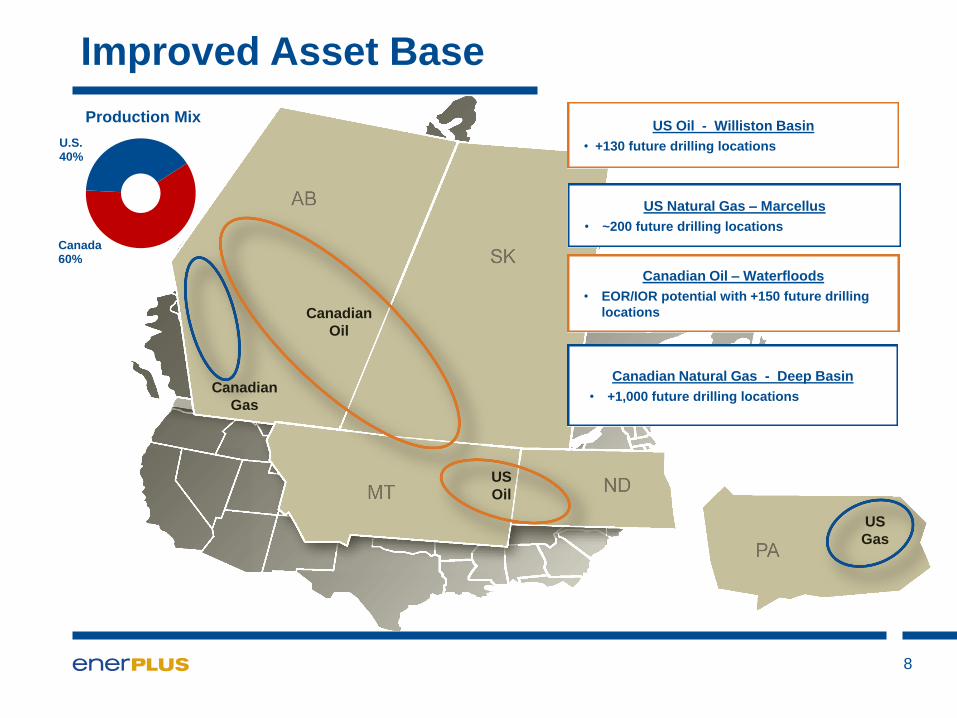

Improved Asset Base

Canadian Oil – Waterfloods

• EOR/IOR potential with +150 future drilling

locations

Canadian Natural Gas - Deep Basin

• +1,000 future drilling locations

US Natural Gas – Marcellus

• ~200 future drilling locations

Canada 60%

U.S. 40%

US

Oil

US

Gas

Canadian

Gas

Canadian

Oil

US Oil - Williston Basin

• +130 future drilling locations

Production Mix

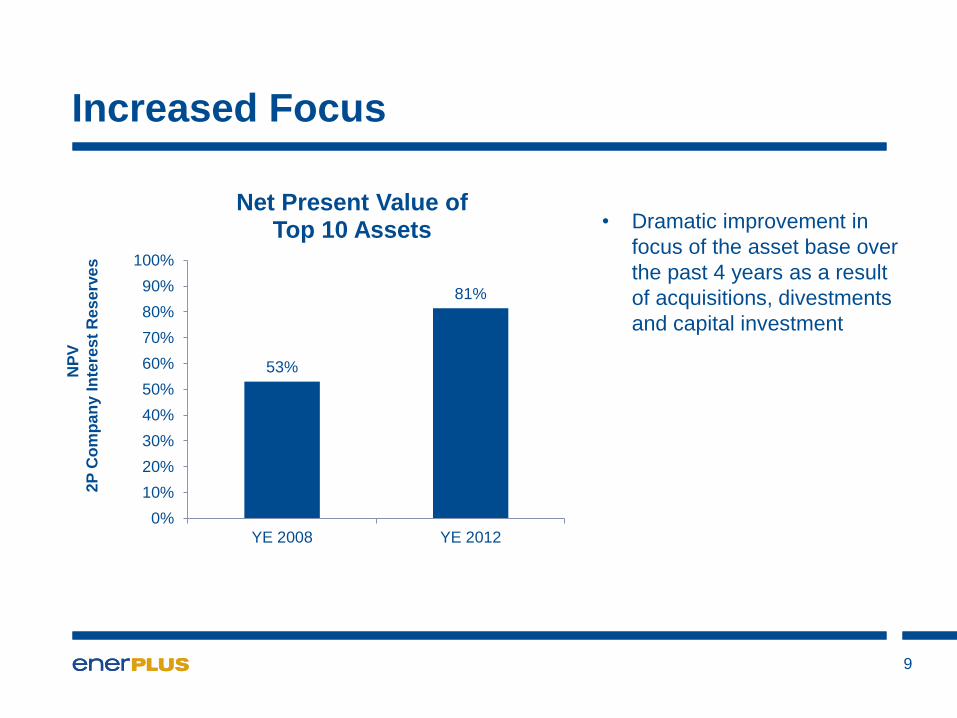

Increased Focus

9

NP

V

2P

Co

mp

an

y I

nte

res

t R

es

erv

es

• Dramatic improvement in

focus of the asset base over

the past 4 years as a result

of acquisitions, divestments

and capital investment

53%

81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

YE 2008 YE 2012

Net Present Value of Top 10 Assets

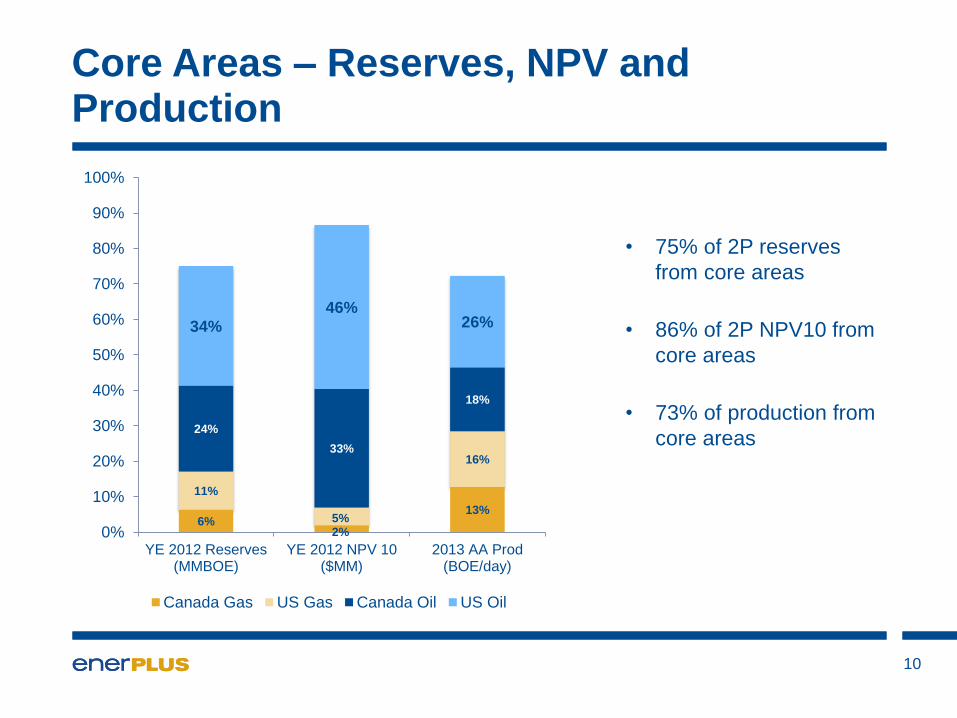

Core Areas – Reserves, NPV and Production

10

6% 2%

13%

11%

5%

16%

24%

33%

18%

34%

46% 26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

YE 2012 Reserves(MMBOE)

YE 2012 NPV 10($MM)

2013 AA Prod(BOE/day)

Canada Gas US Gas Canada Oil US Oil

• 75% of 2P reserves

from core areas

• 86% of 2P NPV10 from

core areas

• 73% of production from

core areas

How Do We Continue to Improve Our Portfolio?

11

• Continued sale of non-strategic assets

• Accelerating the pace, but at the right valuation

• Shallow gas assets are not part of the core

• Small amount of conventional oil production in Canada is not part of

the core

• Divestments will provide a funding source for de-risking and

development of our early stage assets

• Will continue to add to our existing core areas where we already

possess internal technical and operational strengths

The Next Area of Growth - Advancing Early Stage Plays

12

• Divestment proceeds and capital savings providing funding to

advance early stage plays

• Wilrich – Development ready

• Montney – Appraisal

• Duvernay – Appraisal

13

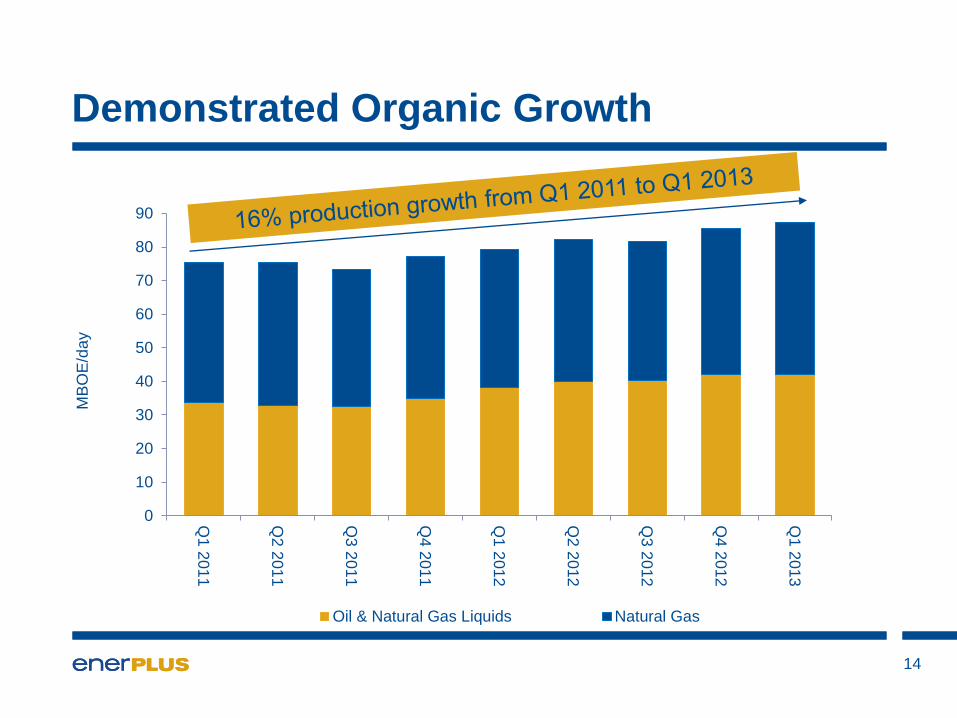

Profitability

0

10

20

30

40

50

60

70

80

90

Q1 2

01

1

Q2 2

01

1

Q3 2

01

1

Q4 2

01

1

Q1 2

01

2

Q2 2

01

2

Q3 2

01

2

Q4 2

01

2

Q1 2

01

3

MB

OE

/da

y

Oil & Natural Gas Liquids Natural Gas

Demonstrated Organic Growth

14

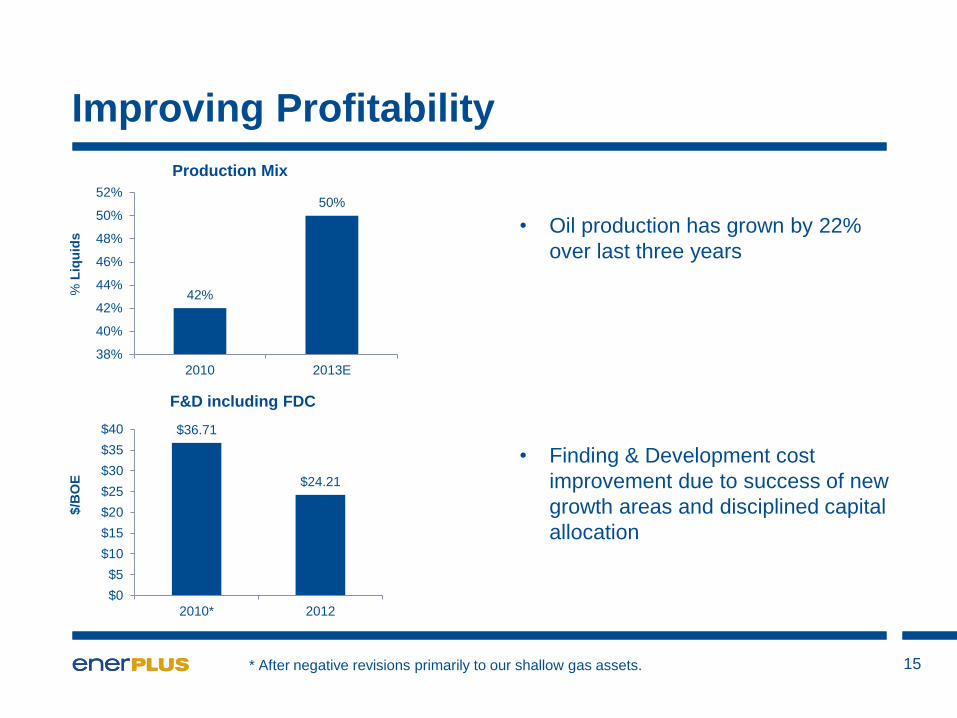

Improving Profitability

15

Production Mix

42%

50%

38%

40%

42%

44%

46%

48%

50%

52%

2010 2013E

* After negative revisions primarily to our shallow gas assets.

$36.71

$24.21

$0

$5

$10

$15

$20

$25

$30

$35

$40

2010* 2012

F&D including FDC

$/B

OE

%

Liq

uid

s • Oil production has grown by 22%

over last three years

• Finding & Development cost

improvement due to success of new

growth areas and disciplined capital

allocation

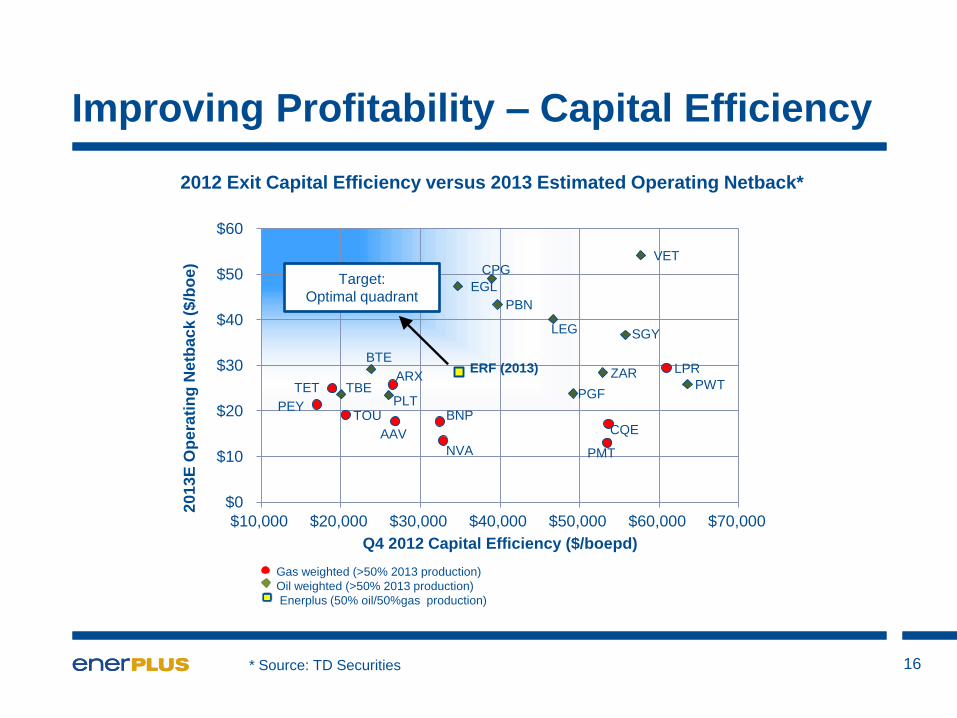

Improving Profitability – Capital Efficiency

16

AAV

ARX

BNP

BTE

CPG

CQE

EGL

ERF (2013)

LEG

LPR

NVA

PBN

PEY PGF

PLT

PMT

PWT TBE

SGY

TET

TOU

VET

ZAR

$0

$10

$20

$30

$40

$50

$60

$10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000

20

13

E O

pe

rati

ng

Netb

ac

k (

$/b

oe

)

Q4 2012 Capital Efficiency ($/boepd)

Target:

Optimal quadrant

Gas weighted (>50% 2013 production)

Oil weighted (>50% 2013 production)

Enerplus (50% oil/50%gas production)

2012 Exit Capital Efficiency versus 2013 Estimated Operating Netback*

* Source: TD Securities

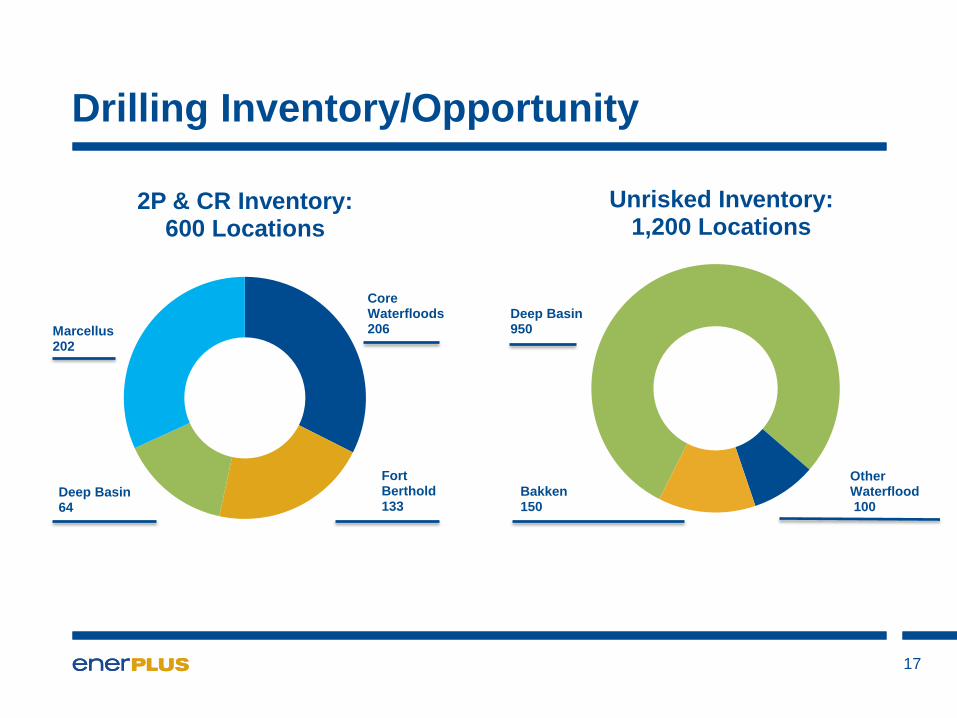

Drilling Inventory/Opportunity

17

Core Waterfloods 206

Fort Berthold 133

Deep Basin 64

Marcellus 202

2P & CR Inventory: 600 Locations

Deep Basin 950

Other Waterflood 100

Bakken 150

Unrisked Inventory: 1,200 Locations

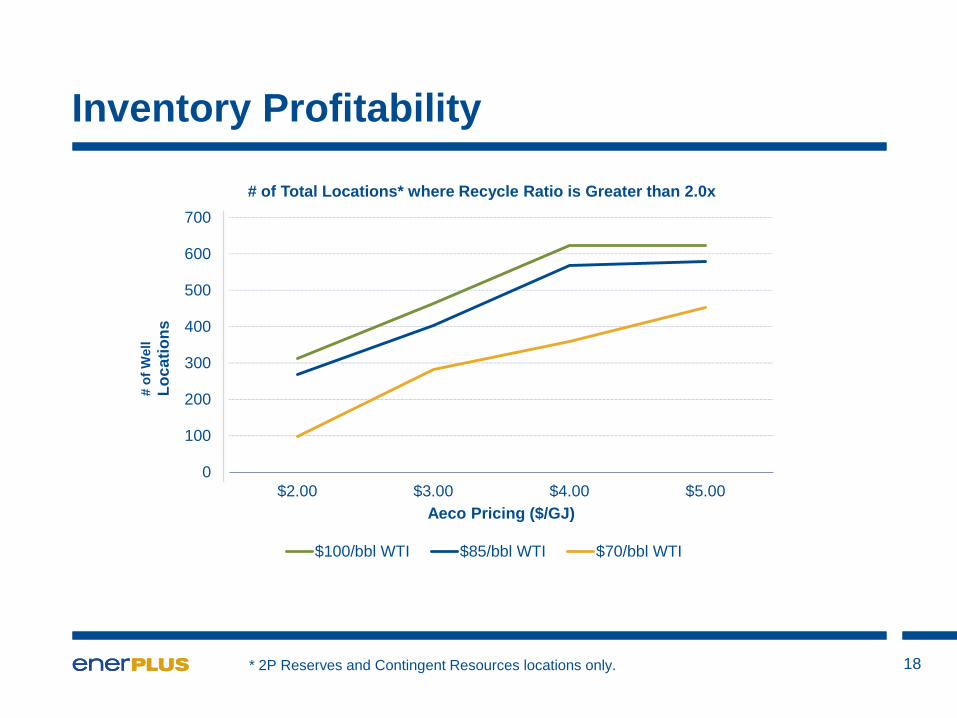

Inventory Profitability

18

0

100

200

300

400

500

600

700

$2.00 $3.00 $4.00 $5.00

Aeco Pricing ($/GJ)

# of Total Locations* where Recycle Ratio is Greater than 2.0x

$100/bbl WTI $85/bbl WTI $70/bbl WTI

# o

f W

ell

Lo

ca

tio

ns

* 2P Reserves and Contingent Resources locations only.

19

Sustainability

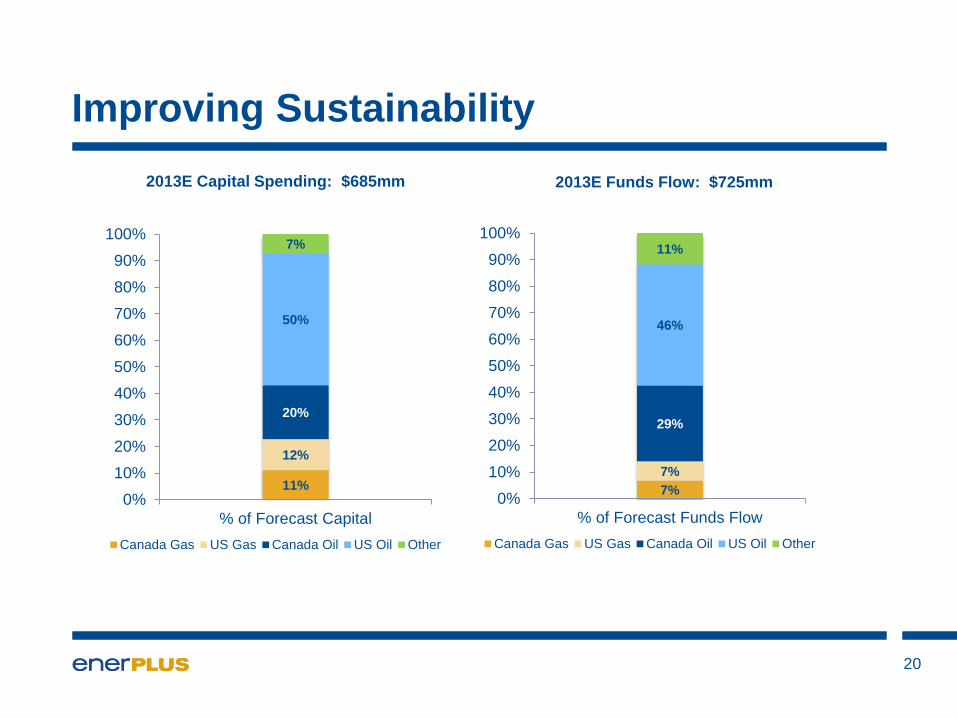

Improving Sustainability

20

2013E Capital Spending: $685mm 2013E Funds Flow: $725mm

7%

7%

29%

46%

11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% of Forecast Funds Flow

Canada Gas US Gas Canada Oil US Oil Other

11%

12%

20%

50%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% of Forecast Capital

Canada Gas US Gas Canada Oil US Oil Other

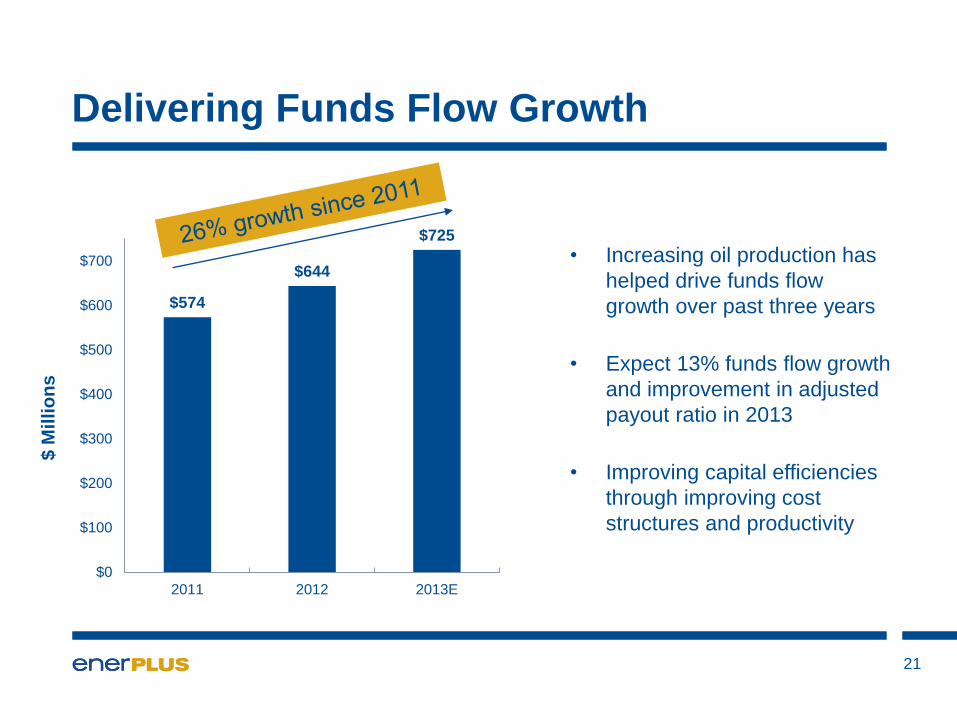

Delivering Funds Flow Growth

• Increasing oil production has

helped drive funds flow

growth over past three years

• Expect 13% funds flow growth

and improvement in adjusted

payout ratio in 2013

• Improving capital efficiencies

through improving cost

structures and productivity

$574

$644

$725

$0

$100

$200

$300

$400

$500

$600

$700

2011 2012 2013E

$ M

illio

ns

21

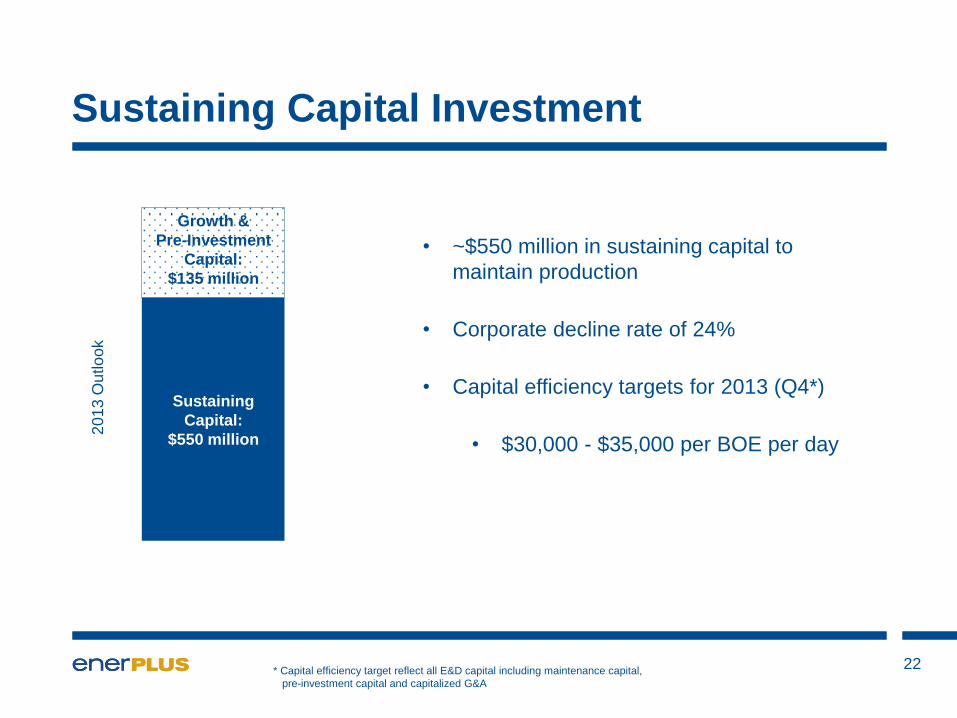

Sustaining Capital Investment

22

Sustaining

Capital:

$550 million

Growth &

Pre-Investment

Capital:

$135 million

• ~$550 million in sustaining capital to

maintain production

• Corporate decline rate of 24%

• Capital efficiency targets for 2013 (Q4*)

• $30,000 - $35,000 per BOE per day

20

13

Ou

tlo

ok

* Capital efficiency target reflect all E&D capital including maintenance capital,

pre-investment capital and capitalized G&A

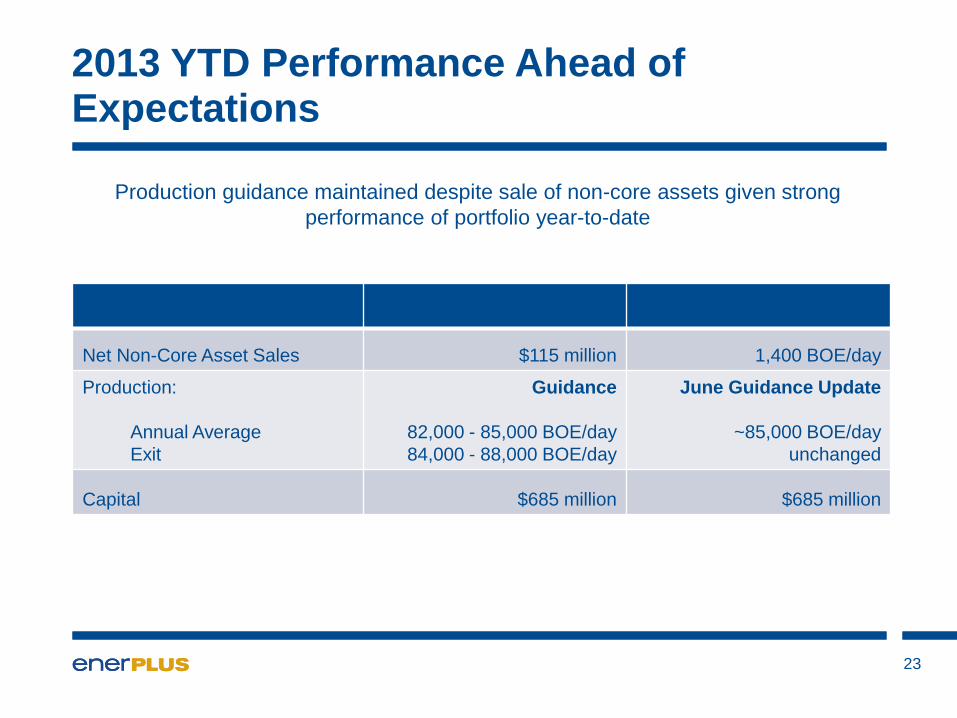

2013 YTD Performance Ahead of Expectations

23

Net Non-Core Asset Sales $115 million 1,400 BOE/day

Production:

Annual Average

Exit

Guidance

82,000 - 85,000 BOE/day

84,000 - 88,000 BOE/day

June Guidance Update

~85,000 BOE/day

unchanged

Capital $685 million $685 million

Production guidance maintained despite sale of non-core assets given strong

performance of portfolio year-to-date