Embed Size (px)

Citation preview

Strategic Management II (15.904) Assignment #2

15 September 2003

Company / Business: Capital One® / Credit Card Business

Prepared by Group 01: Harry Reddy Yasuhiko Kiuchi Mitsuhiro Kameda Tae Soo Lee Rintaro Kurebayashi

Group 01 - Capital One / Credit Card Business 15.904

Table of Contents

1. Introduction..................................................................................................................... 3 1.1 Company History ...................................................................................................... 3 1.2 Credit Card Industry and Major Competitors ........................................................... 5

2. Strategic Positioning by the Delta Model ....................................................................... 6 3. Customer Segmentation .................................................................................................. 9

3.1. Customer Segmentation ........................................................................................... 9 3.2. Business Dimension of the Customer Tier ............................................................ 10

4. Value Proposition.......................................................................................................... 12 4.1 Tier 1 Customers..................................................................................................... 12 4.2 Tier 2 Customers..................................................................................................... 14 4.3 Tier 3 Customers..................................................................................................... 15

Exhibit 1 Capital One’s major competitors (FY 2002)..................................................... 16 Exhibit 2 List of credit cards for student market (2002 Freshman).................................. 18 Exhibit 3 UK credit card issuer shares.............................................................................. 19 Exhibit 4 Western European pay later card market .......................................................... 20 Exhibit 5 Balance Sheet .................................................................................................... 21 Exhibit 6 Income Statement.............................................................................................. 22 Exhibit 7 Statements of Cash Flows ................................................................................. 23

Page 2 of 23

Group 01 - Capital One / Credit Card Business 15.904

1. Introduction Capital One is established in 1995 as a local bank card issuer and quickly rose to the top

of the U.S. credit card industry. It has a current customer base of 47.4 million and it

managed loans totaling $59.7 billion. Through their pioneering information technology

efforts, they are in a prime position to lead the financial services marketplace.

Their success comes from the extensive use of advanced information technology for

customer acquisition and retention. By using information they have gathered by the

product tests, they tailored the products to individual customer needs and provided

services in a very efficient manner. They continue to apply their micro-segmentation

strategies to expand their business and continue to capitalize on promising markets other

than their primary credit business such as auto finance and patient finance. Now, Capital

One has been recognized for innovation, customer service, information technology, and

financial management. In this paper, our business strategy is mainly focused in the credit

card business and the rest of this section will briefly describe the company history and

credit card industry and major competitors.

1.1 Company History Capital One was founded as a new credit card division of Signet Bank. Two people,

Richard Fairbank (Chairman and CEO) and Nigel Morris (President and COO), was hired

to lead the division. Fairbank and Morris saw that traditional banking and financial

services lacked a focus on the individual customer and Information Technology could

accurately guide business and credit decisions.

Their solution was known as the Information-Based Strategy (IBS), which brought

marketing, credit, risk, operations, and Information Technology into a flexible decision-

making structure. Its purpose was to enable them to offer financial solutions tailored to

an individual customer's needs and it was referred as "micro-segmentation."

Page 3 of 23

Group 01 - Capital One / Credit Card Business 15.904

Their IBS essentially consists of two methods. First, they used sophisticated data

collection methods to gather massive amounts of information on existing or prospective

customers. Then, they used the collected information to design and mass-market

customized products to their customers.

Signet Bank invited them to launch its Bank Card division after Fairbank and Morris

pitched their IBS idea to more than 20 national retail banks. Over the next several years,

they ran thousands of product tests. After creating an enormous database and developing

sophisticated screening processes and direct-mail marketing tactics, they escalated the

credit card wars, luring customers from its rivals with the first innovative balance transfer

credit card. The card let customers of other companies transfer what they owed on

higher-interest cards to a Signet card with a lower introductory rate.

The new card immediately drew imitators (by 1997 balance-transfer cards accounted for

85% of credit card solicitations). After skimming off the least risky customers, Fairbank

and Morris began going after less desirable credit customers who could be charged higher

rates. The result was what they call second generation products -- secured and unsecured

cards with lower credit lines and higher annual percentage rates and fees for higher-risk

customers.

The credit card business had grown to five million customers by 1994, but at a high cost

to Signet, which had devoted most of its resources to finding and servicing credit card

holders. In 1995, Signet spun off its credit card division to create the publicly held

Capital One.

The company continues to expend in terms of products and geography. They expanded

into Florida and Texas in 1995 and into Canada and the UK in 1996. They also

established saving bank to offer products and services to cardholders. In 1997, they

bought a deposit portfolio from J. C. Penny and added deposit accounts to the bank. In

1998, they began marketing its products for potential high life-time NPV customers such

as immigrants and high school students.

Page 4 of 23

Group 01 - Capital One / Credit Card Business 15.904

The company's growth continued and they put more efforts in marketing and have gained

significant boosts to their non-interest income and customer base. In 2001 the company

acquired AmeriFee, which provides loans for elective medical and dental surgery and

PeopleFirst, Inc., the nation's largest online provider of direct motor vehicle loans.

In 2002, in response to industry-wide concern over sub-prime lending, Capital One

agreed to increase reserves on its sub-prime portfolio. Also in 2002, the company's UK

operations proved profitable for the first time. With nearly 3 million accounts and close

to $4 billion in loan assets, the UK is Capital One's largest international market.

In July 2003, Capital One announced the second quarter earnings per share increased by

34 percent over the same period in the prior year and the increase was driven primarily by

the improved profitability of their auto and international businesses.

1.2 Credit Card Industry and Major Competitors Capital One competes with international, national, regional and local issuers of Visa and

MasterCard credit cards. In addition, American Express, Discover Card, Diner’s Club

and, to a certain extent, smart cards and debit cards, represent additional competition to

the general purpose credit card.

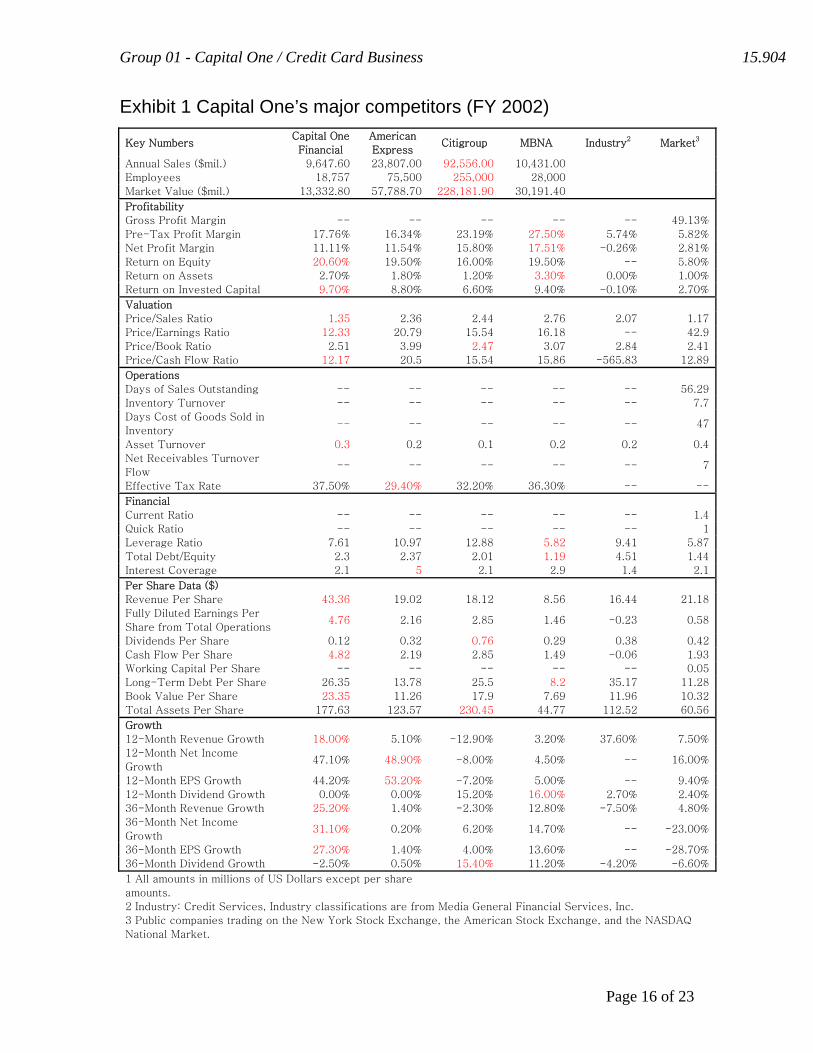

Recent financial data shows Capital One is one of the top six credit card issuers in the US.

The credit card business is strongly competitive market and Capital One's top competitors

are: American Express, Citigroup, and MBNA (Exhibit 1 Capital One’s major

competitors). Even though the Capital One is not No.1 in the industry, their growth to

this date is quite remarkable.

Traditionally, all the credit card businesses were trying "one-size-fits-all" approach

before Capital One introduced the credit card war. The industry started imitating Capital

One's approaches as soon as they found those are effective. Following are the list of key

strategies of major competitors including Capital One itself.

Page 5 of 23

Group 01 - Capital One / Credit Card Business 15.904

Institution Key Strategies

Capital One Invented innovative balance-transfer credit card.

The card let customers of other companies transfer what they owed on

higher-interest cards to a card with a lower introductory rate.

American Express Positioned itself as a more prestigious alternative to Visa/Master Card.

Complete line of a financial service, widespread acceptance overseas good

reputation for travel-related services.

Citigroup Global corporate brand name; strong product brands and co-brands.

MBNA Various kinds of affinity credit cards.

By 1999, MBNA offered 4,500 different affinity cards based on cardholder's

loyalties to school, pro sports teams, trade associations, etc.

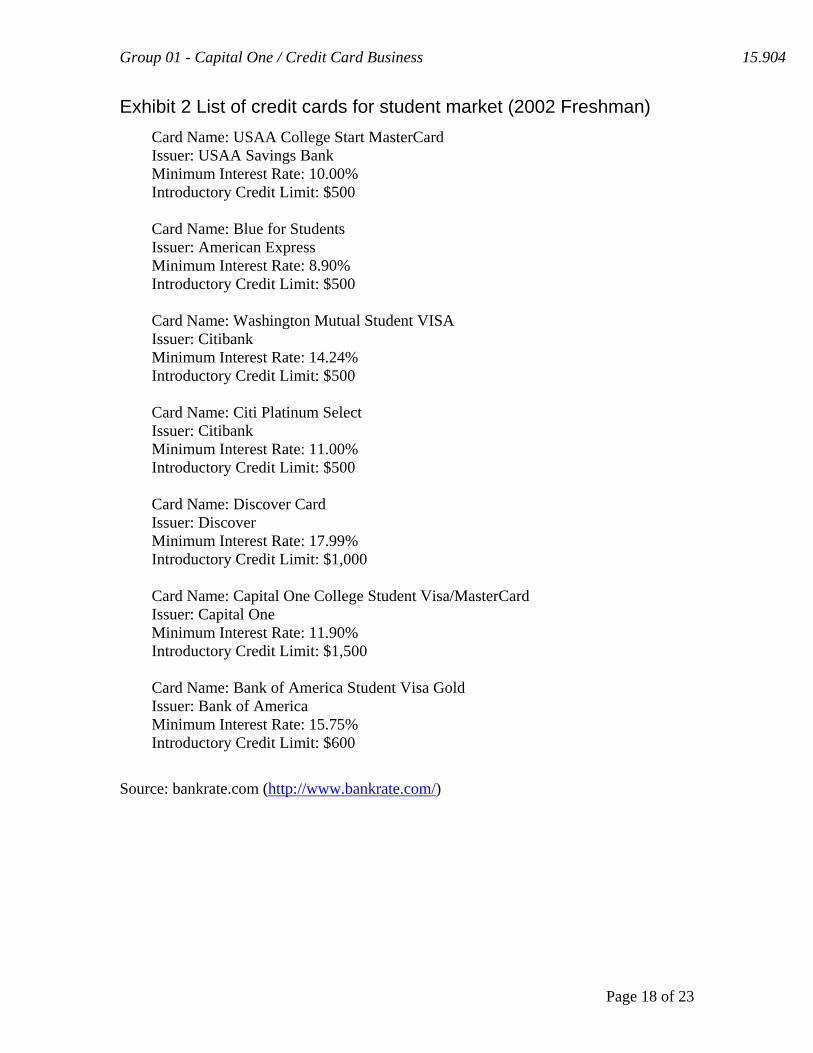

For example, the students, whose potential life-time NPV is very high for credit card

companies and a very good source to acquire new customers. Exhibit 2 is a list of some

credit cards targeted at the student market. These rates and credit limits are based on

offers to incoming freshmen for year 2002.

As shown in the example, industry competitors have continuously solicited Capital One's

customers with similar interest rate strategies. The competition has put, and will continue

to put, additional pressure on pricing strategies. In general, customers are attracted to

credit card issuers largely on the basis of price, credit limit and other product features and

customer loyalty is often limited.

Even in this tough competitive environment, their IBS allows them to more effectively

compete in both current and new markets. However, we believe to sustain future growth,

Capital One needs to address to developing right products and services to appropriate

customer segments.

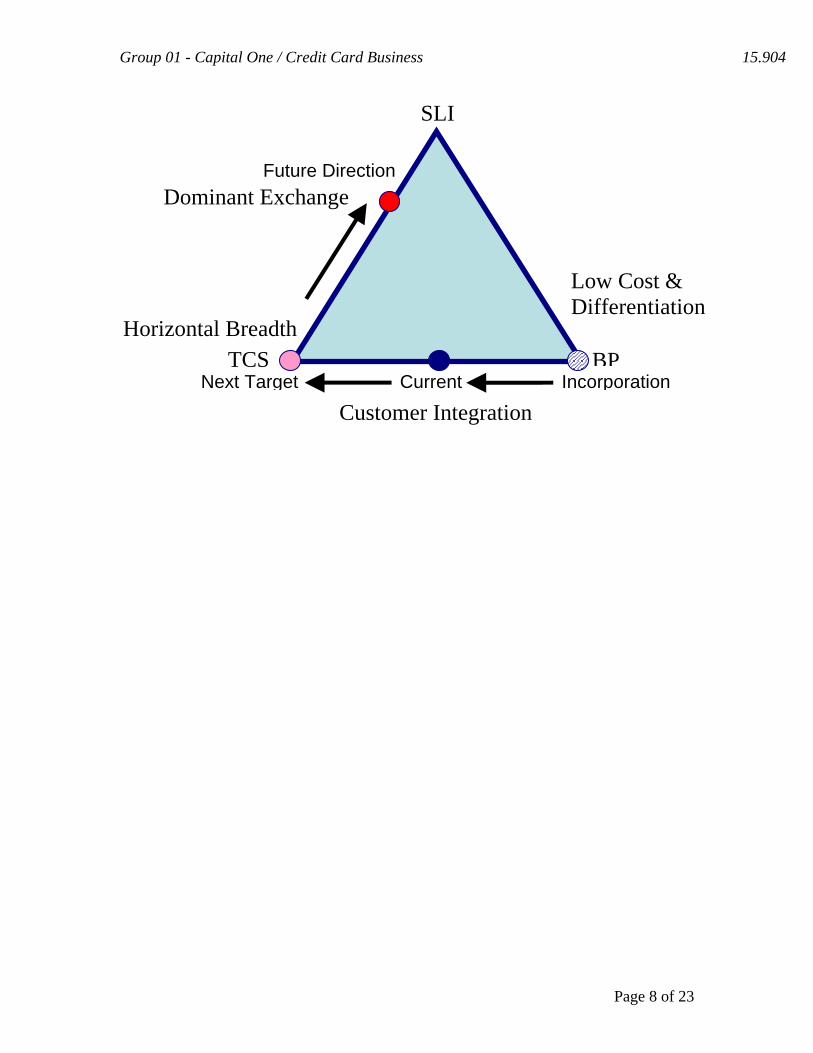

2. Strategic Positioning by the Delta Model At the time of incorporation, Capital One only had IBS implemented by their own

information division. Two years later, Capital One has both product differentiation and

low cost by innovative product, balance transfer credit card. The card provided the lower

Page 6 of 23

Group 01 - Capital One / Credit Card Business 15.904

initial rate to attract customers from other cards. Therefore, we believe the firm was

positioned in the Best Product position.

After collecting customer information by thousands of test they have performed based on

their IBS, they have started using acquired information for targeting and retaining

customers. They continue to provide innovative products such as a credit card for sub-

prime customers. Customers will receive the individual products and we can position the

company in the customer integration position.

Recently they have started expanding the operation to international locations such as UK

and Canada. The revenue and profit started to contribute to the financial numbers. In

2001, Capital One acquired the 2.2 million cards with 4.2% market share and there is still

huge potential for the growth in UK markets, total issued cards are more than 52 million

(Exhibit 4 UK credit card issuer shares). We can see potential markets in other Western

European countries. 160 million cards are used in 2001 in Western Europe. Also, there

are other emerging international markets such as China. Therefore, we believe Capital

One’s next target should be horizontal breadth in terms of international geographic

expansion.

In future, Capital One should seek the opportunities to reach the system lock-in position

by providing dominant exchange for the customers. Following is the illustration of the

simplified delta model to illustrate the business positioning of the Capital One. By

integrating other financial products such as auto loans, mortgages, and life insurances,

potentially, Capital One can acquire the dominant exchange position in financial service

industry. Their IBS can be applied to other financial services and their integrated CTI

(Computer Telephony Integration) system can serve as the integral interface to the

customers. Also, they can improve customer service by improving IBS. For example,

they can add the frequency of telephone call and can specially treat first time or less

frequent customers.

Page 7 of 23

Group 01 - Capital One / Credit Card Business 15.904

SLI

Low Cost & Differentiation

Horizontal Breadth

Dominant Exchange

Customer Integration

B

CurrentPIncorporation

TCS Next Target

Future Direction

Page 8 of 23

Group 01 - Capital One / Credit Card Business 15.904

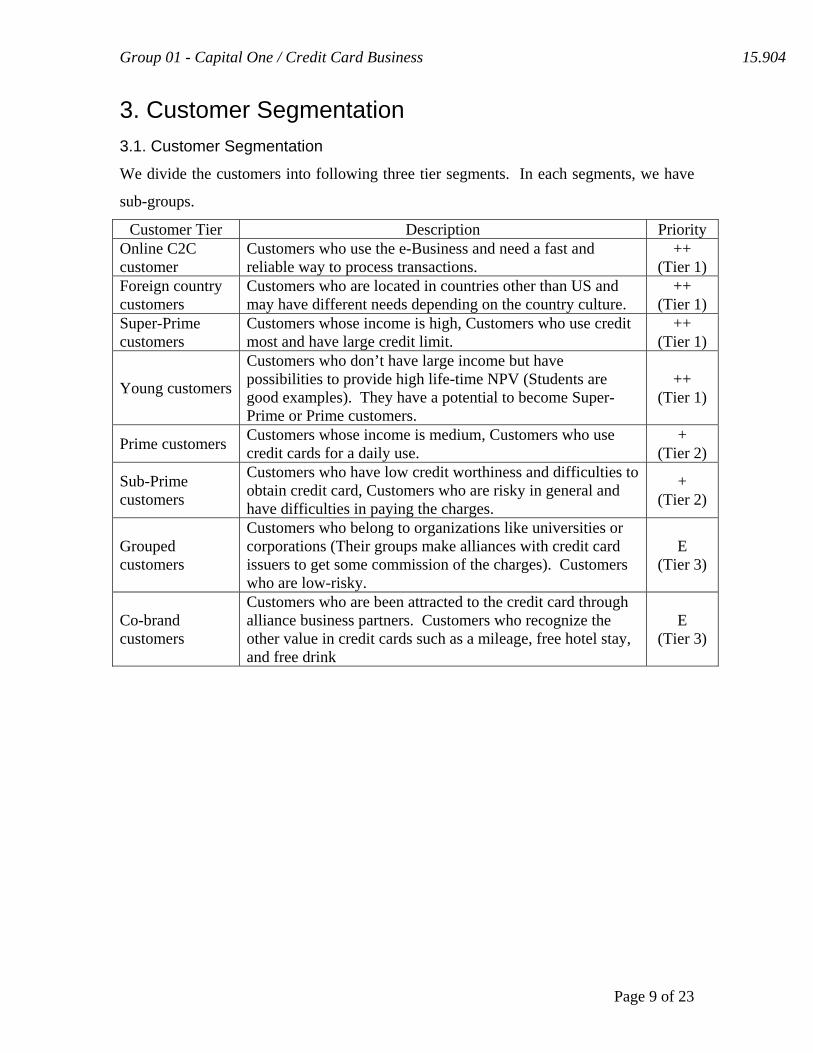

3. Customer Segmentation 3.1. Customer Segmentation

We divide the customers into following three tier segments. In each segments, we have

sub-groups.

Customer Tier Description Priority Online C2C customer

Customers who use the e-Business and need a fast and reliable way to process transactions.

++ (Tier 1)

Foreign country customers

Customers who are located in countries other than US and may have different needs depending on the country culture.

++ (Tier 1)

Super-Prime customers

Customers whose income is high, Customers who use credit most and have large credit limit.

++ (Tier 1)

Young customers

Customers who don’t have large income but have possibilities to provide high life-time NPV (Students are good examples). They have a potential to become Super-Prime or Prime customers.

++ (Tier 1)

Prime customers Customers whose income is medium, Customers who use credit cards for a daily use.

+ (Tier 2)

Sub-Prime customers

Customers who have low credit worthiness and difficulties to obtain credit card, Customers who are risky in general and have difficulties in paying the charges.

+ (Tier 2)

Grouped customers

Customers who belong to organizations like universities or corporations (Their groups make alliances with credit card issuers to get some commission of the charges). Customers who are low-risky.

E (Tier 3)

Co-brand customers

Customers who are been attracted to the credit card through alliance business partners. Customers who recognize the other value in credit cards such as a mileage, free hotel stay, and free drink

E (Tier 3)

Page 9 of 23

Group 01 - Capital One / Credit Card Business 15.904

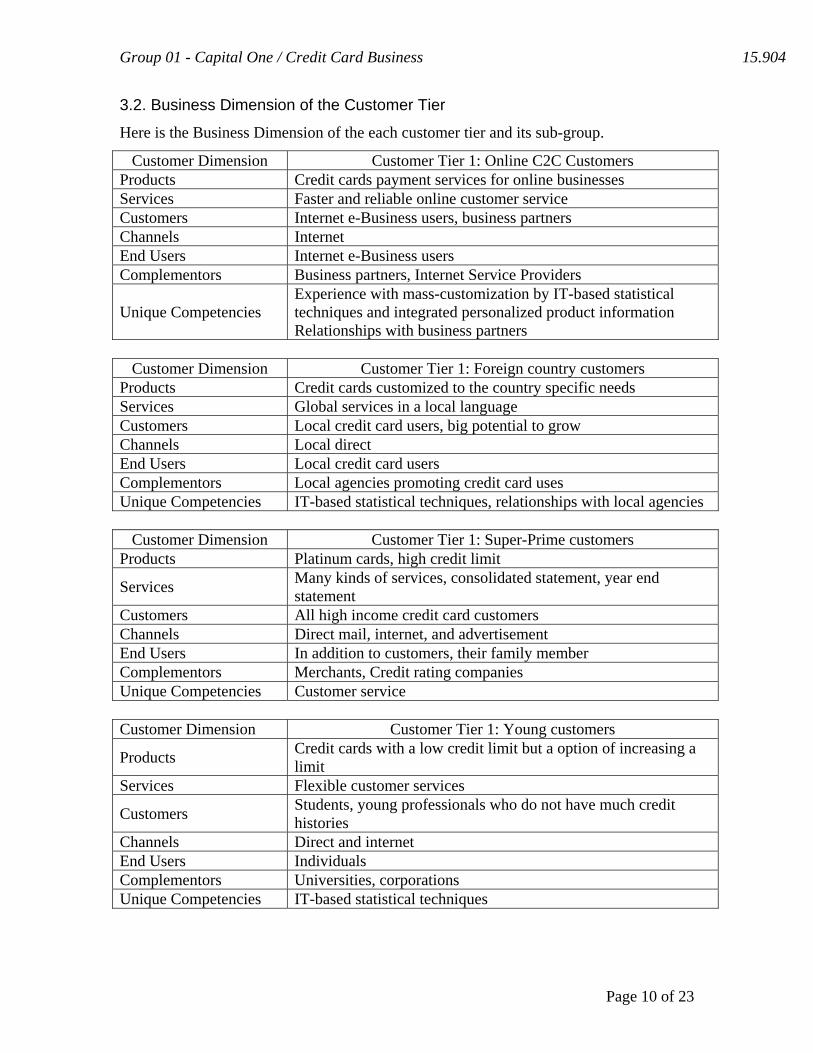

3.2. Business Dimension of the Customer Tier

Here is the Business Dimension of the each customer tier and its sub-group.

Customer Dimension Customer Tier 1: Online C2C Customers Products Credit cards payment services for online businesses Services Faster and reliable online customer service Customers Internet e-Business users, business partners Channels Internet End Users Internet e-Business users Complementors Business partners, Internet Service Providers

Unique Competencies Experience with mass-customization by IT-based statistical techniques and integrated personalized product information Relationships with business partners

Customer Dimension Customer Tier 1: Foreign country customers

Products Credit cards customized to the country specific needs Services Global services in a local language Customers Local credit card users, big potential to grow Channels Local direct End Users Local credit card users Complementors Local agencies promoting credit card uses Unique Competencies IT-based statistical techniques, relationships with local agencies

Customer Dimension Customer Tier 1: Super-Prime customers Products Platinum cards, high credit limit

Services Many kinds of services, consolidated statement, year end statement

Customers All high income credit card customers Channels Direct mail, internet, and advertisement End Users In addition to customers, their family member Complementors Merchants, Credit rating companies Unique Competencies Customer service Customer Dimension Customer Tier 1: Young customers

Products Credit cards with a low credit limit but a option of increasing a limit

Services Flexible customer services

Customers Students, young professionals who do not have much credit histories

Channels Direct and internet End Users Individuals Complementors Universities, corporations Unique Competencies IT-based statistical techniques

Page 10 of 23

Group 01 - Capital One / Credit Card Business 15.904

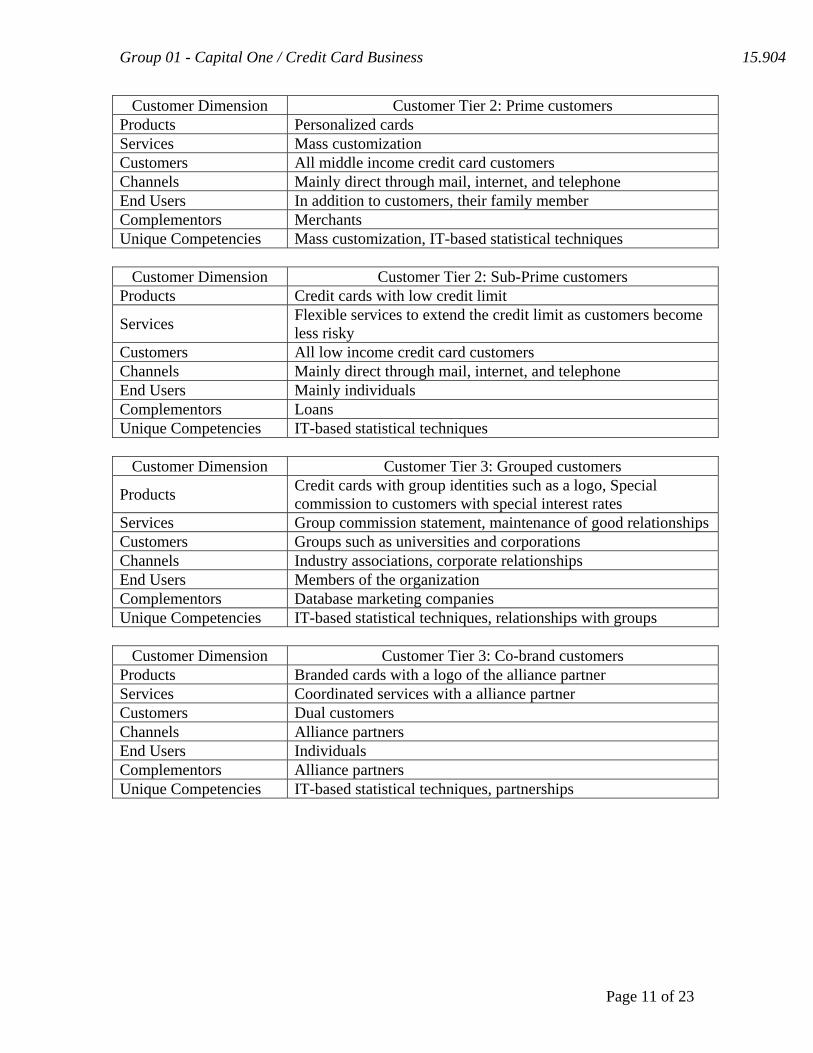

Customer Dimension Customer Tier 2: Prime customers Products Personalized cards Services Mass customization Customers All middle income credit card customers Channels Mainly direct through mail, internet, and telephone End Users In addition to customers, their family member Complementors Merchants Unique Competencies Mass customization, IT-based statistical techniques

Customer Dimension Customer Tier 2: Sub-Prime customers Products Credit cards with low credit limit

Services Flexible services to extend the credit limit as customers become less risky

Customers All low income credit card customers Channels Mainly direct through mail, internet, and telephone End Users Mainly individuals Complementors Loans Unique Competencies IT-based statistical techniques

Customer Dimension Customer Tier 3: Grouped customers

Products Credit cards with group identities such as a logo, Special commission to customers with special interest rates

Services Group commission statement, maintenance of good relationships Customers Groups such as universities and corporations Channels Industry associations, corporate relationships End Users Members of the organization Complementors Database marketing companies Unique Competencies IT-based statistical techniques, relationships with groups

Customer Dimension Customer Tier 3: Co-brand customers Products Branded cards with a logo of the alliance partner Services Coordinated services with a alliance partner Customers Dual customers Channels Alliance partners End Users Individuals Complementors Alliance partners Unique Competencies IT-based statistical techniques, partnerships

Page 11 of 23

Group 01 - Capital One / Credit Card Business 15.904

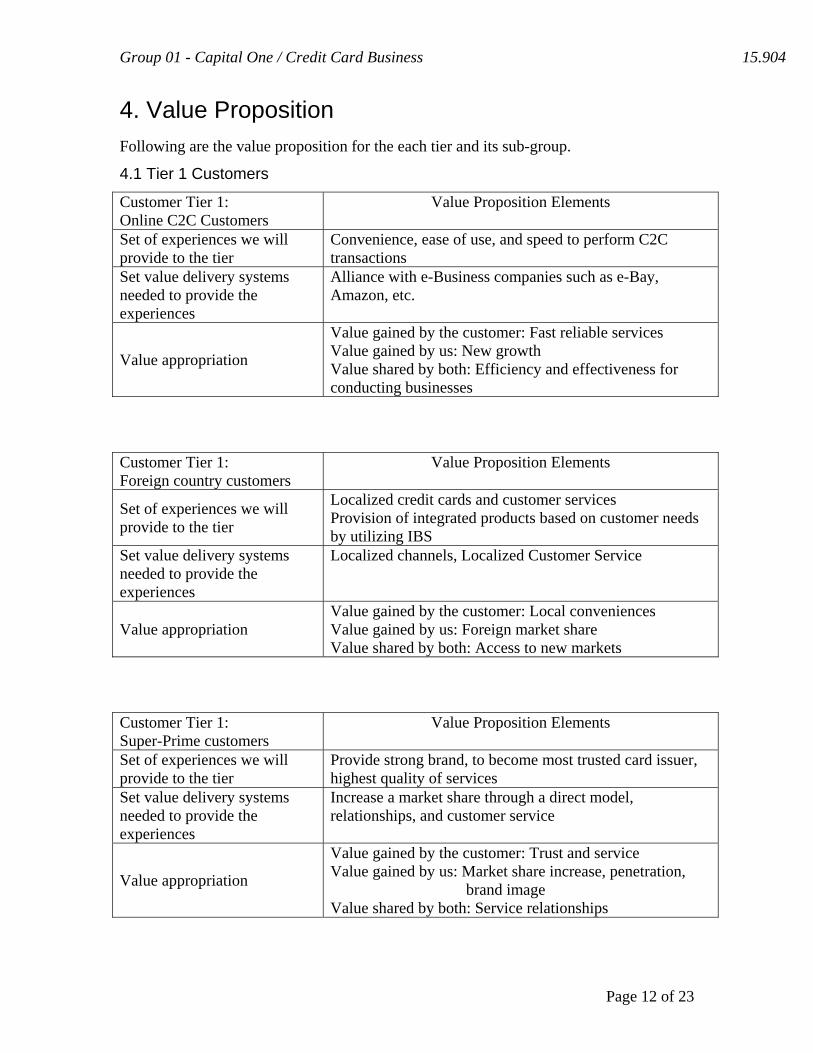

4. Value Proposition Following are the value proposition for the each tier and its sub-group.

4.1 Tier 1 Customers Customer Tier 1: Online C2C Customers

Value Proposition Elements

Set of experiences we will provide to the tier

Convenience, ease of use, and speed to perform C2C transactions

Set value delivery systems needed to provide the experiences

Alliance with e-Business companies such as e-Bay, Amazon, etc.

Value appropriation

Value gained by the customer: Fast reliable services Value gained by us: New growth Value shared by both: Efficiency and effectiveness for conducting businesses

Customer Tier 1: Foreign country customers

Value Proposition Elements

Set of experiences we will provide to the tier

Localized credit cards and customer services Provision of integrated products based on customer needs by utilizing IBS

Set value delivery systems needed to provide the experiences

Localized channels, Localized Customer Service

Value appropriation Value gained by the customer: Local conveniences Value gained by us: Foreign market share Value shared by both: Access to new markets

Customer Tier 1: Super-Prime customers

Value Proposition Elements

Set of experiences we will provide to the tier

Provide strong brand, to become most trusted card issuer, highest quality of services

Set value delivery systems needed to provide the experiences

Increase a market share through a direct model, relationships, and customer service

Value appropriation

Value gained by the customer: Trust and service Value gained by us: Market share increase, penetration,

brand image Value shared by both: Service relationships

Page 12 of 23

Group 01 - Capital One / Credit Card Business 15.904

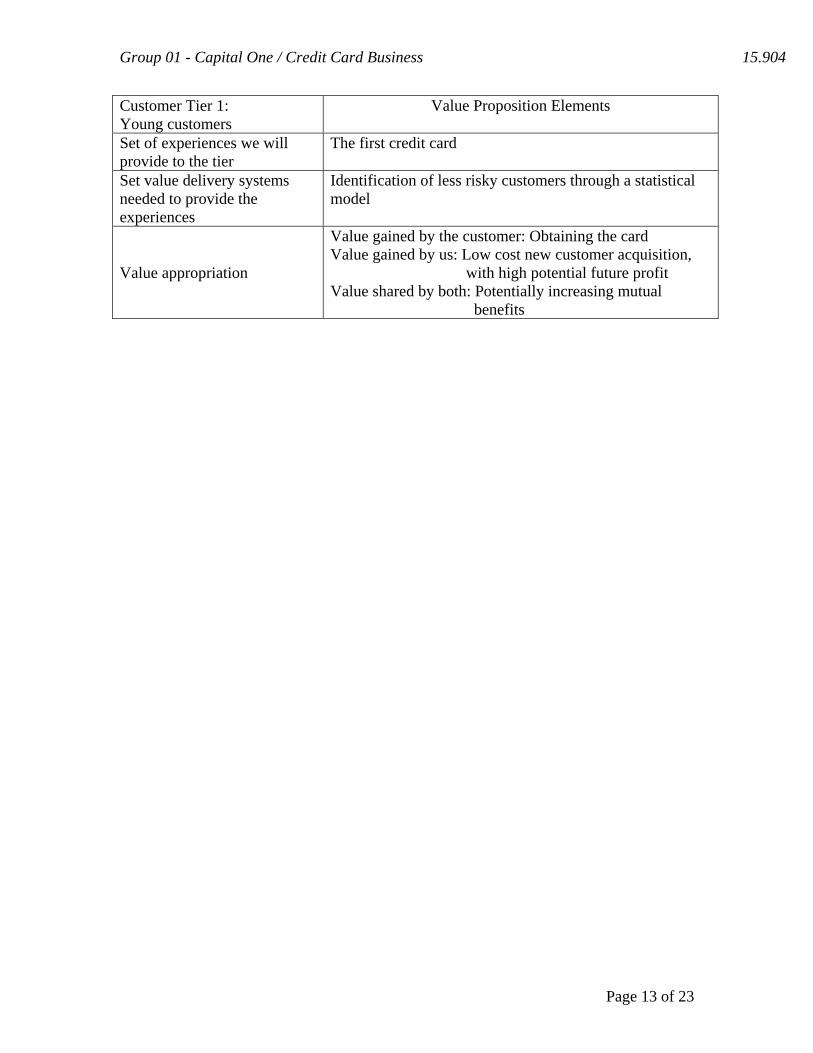

Customer Tier 1: Young customers

Value Proposition Elements

Set of experiences we will provide to the tier

The first credit card

Set value delivery systems needed to provide the experiences

Identification of less risky customers through a statistical model

Value appropriation

Value gained by the customer: Obtaining the card Value gained by us: Low cost new customer acquisition,

with high potential future profit Value shared by both: Potentially increasing mutual

benefits

Page 13 of 23

Group 01 - Capital One / Credit Card Business 15.904

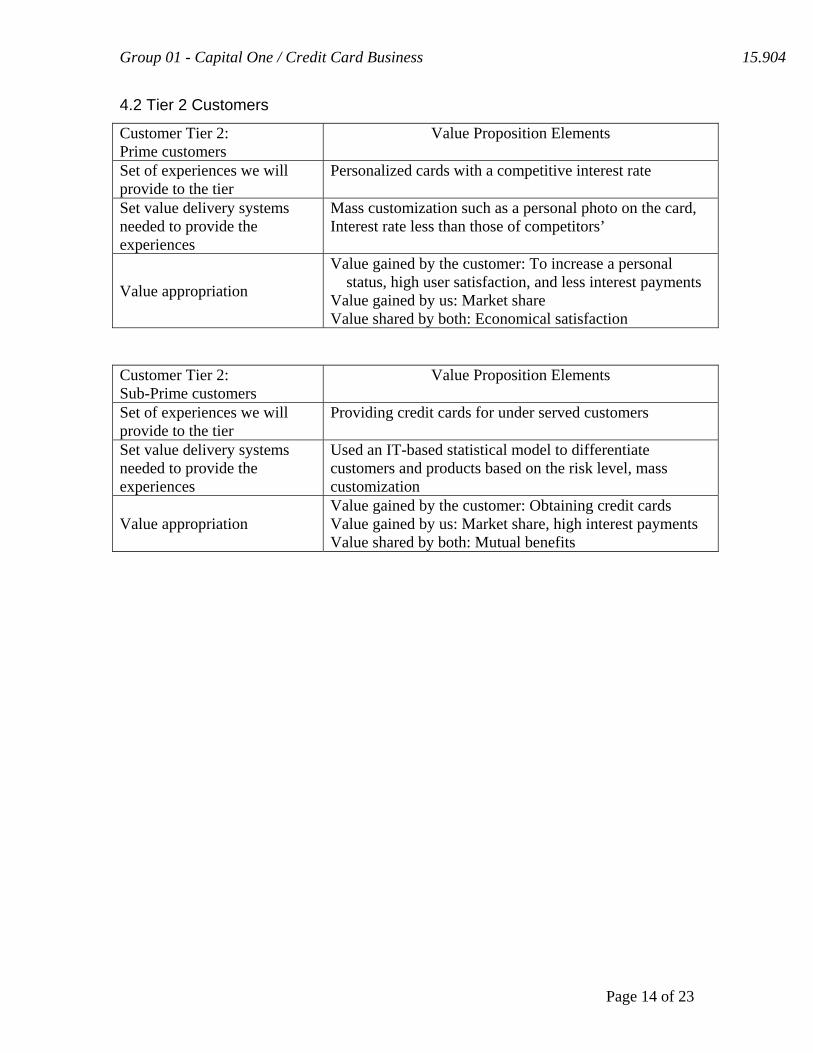

4.2 Tier 2 Customers Customer Tier 2: Prime customers

Value Proposition Elements

Set of experiences we will provide to the tier

Personalized cards with a competitive interest rate

Set value delivery systems needed to provide the experiences

Mass customization such as a personal photo on the card, Interest rate less than those of competitors’

Value appropriation

Value gained by the customer: To increase a personal status, high user satisfaction, and less interest payments

Value gained by us: Market share Value shared by both: Economical satisfaction

Customer Tier 2: Sub-Prime customers

Value Proposition Elements

Set of experiences we will provide to the tier

Providing credit cards for under served customers

Set value delivery systems needed to provide the experiences

Used an IT-based statistical model to differentiate customers and products based on the risk level, mass customization

Value appropriation Value gained by the customer: Obtaining credit cards Value gained by us: Market share, high interest payments Value shared by both: Mutual benefits

Page 14 of 23

Group 01 - Capital One / Credit Card Business 15.904

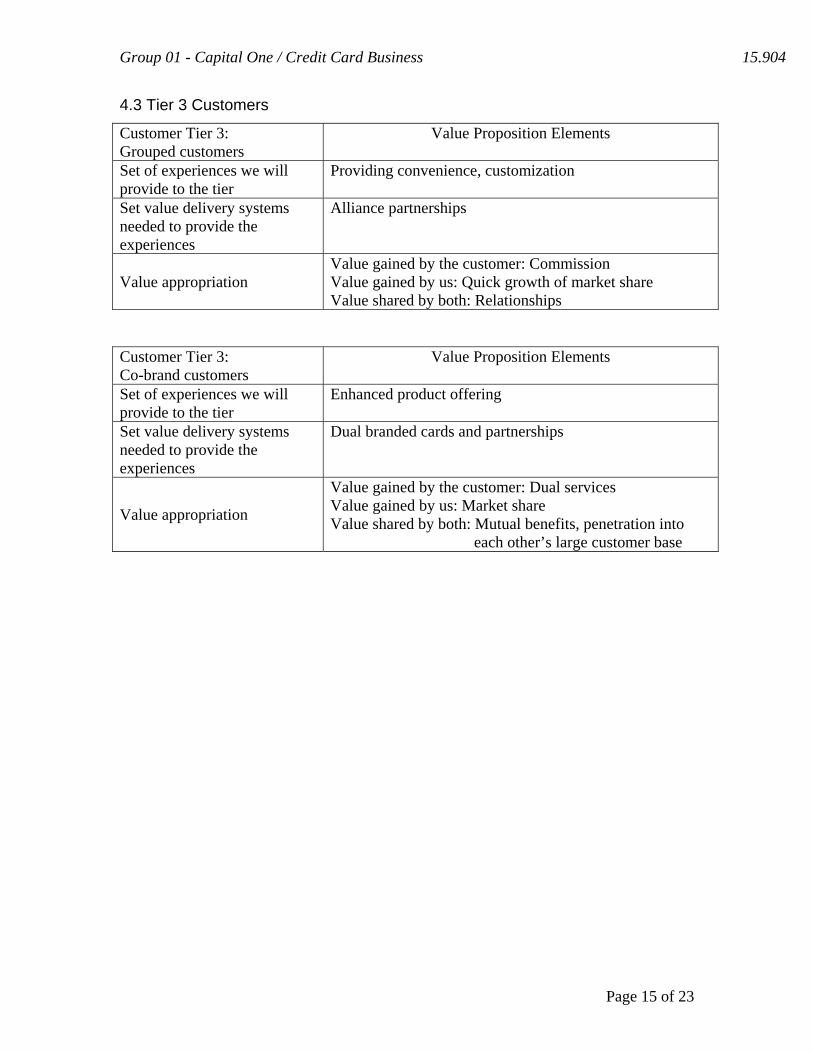

4.3 Tier 3 Customers Customer Tier 3: Grouped customers

Value Proposition Elements

Set of experiences we will provide to the tier

Providing convenience, customization

Set value delivery systems needed to provide the experiences

Alliance partnerships

Value appropriation Value gained by the customer: Commission Value gained by us: Quick growth of market share Value shared by both: Relationships

Customer Tier 3: Co-brand customers

Value Proposition Elements

Set of experiences we will provide to the tier

Enhanced product offering

Set value delivery systems needed to provide the experiences

Dual branded cards and partnerships

Value appropriation

Value gained by the customer: Dual services Value gained by us: Market share Value shared by both: Mutual benefits, penetration into

each other’s large customer base

Page 15 of 23

Group 01 - Capital One / Credit Card Business 15.904

Exhibit 1 Capital One’s major competitors (FY 2002)

Key Numbers Capital One

Financial

American

Express Citigroup MBNA Industry2 Market3

Annual Sales ($mil.) 9,647.60 23,807.00 92,556.00 10,431.00

Employees 18,757 75,500 255,000 28,000

Market Value ($mil.) 13,332.80 57,788.70 228,181.90 30,191.40

Profitability

Gross Profit Margin -- -- -- -- -- 49.13%

Pre-Tax Profit Margin 17.76% 16.34% 23.19% 27.50% 5.74% 5.82%

Net Profit Margin 11.11% 11.54% 15.80% 17.51% -0.26% 2.81%

Return on Equity 20.60% 19.50% 16.00% 19.50% -- 5.80%

Return on Assets 2.70% 1.80% 1.20% 3.30% 0.00% 1.00%

Return on Invested Capital 9.70% 8.80% 6.60% 9.40% -0.10% 2.70%

Valuation

Price/Sales Ratio 1.35 2.36 2.44 2.76 2.07 1.17

Price/Earnings Ratio 12.33 20.79 15.54 16.18 -- 42.9

Price/Book Ratio 2.51 3.99 2.47 3.07 2.84 2.41

Price/Cash Flow Ratio 12.17 20.5 15.54 15.86 -565.83 12.89

Operations

Days of Sales Outstanding -- -- -- -- -- 56.29

Inventory Turnover -- -- -- -- -- 7.7

Days Cost of Goods Sold in

Inventory -- -- -- -- -- 47

Asset Turnover 0.3 0.2 0.1 0.2 0.2 0.4

Net Receivables Turnover

Flow -- -- -- -- -- 7

Effective Tax Rate 37.50% 29.40% 32.20% 36.30% -- --

Financial

Current Ratio -- -- -- -- -- 1.4

Quick Ratio -- -- -- -- -- 1

Leverage Ratio 7.61 10.97 12.88 5.82 9.41 5.87

Total Debt/Equity 2.3 2.37 2.01 1.19 4.51 1.44

Interest Coverage 2.1 5 2.1 2.9 1.4 2.1

Per Share Data ($)

Revenue Per Share 43.36 19.02 18.12 8.56 16.44 21.18

Fully Diluted Earnings Per

Share from Total Operations 4.76 2.16 2.85 1.46 -0.23 0.58

Dividends Per Share 0.12 0.32 0.76 0.29 0.38 0.42

Cash Flow Per Share 4.82 2.19 2.85 1.49 -0.06 1.93

Working Capital Per Share -- -- -- -- -- 0.05

Long-Term Debt Per Share 26.35 13.78 25.5 8.2 35.17 11.28

Book Value Per Share 23.35 11.26 17.9 7.69 11.96 10.32

Total Assets Per Share 177.63 123.57 230.45 44.77 112.52 60.56

Growth

12-Month Revenue Growth 18.00% 5.10% -12.90% 3.20% 37.60% 7.50%

12-Month Net Income

Growth 47.10% 48.90% -8.00% 4.50% -- 16.00%

12-Month EPS Growth 44.20% 53.20% -7.20% 5.00% -- 9.40%

12-Month Dividend Growth 0.00% 0.00% 15.20% 16.00% 2.70% 2.40%

36-Month Revenue Growth 25.20% 1.40% -2.30% 12.80% -7.50% 4.80%

36-Month Net Income

Growth 31.10% 0.20% 6.20% 14.70% -- -23.00%

36-Month EPS Growth 27.30% 1.40% 4.00% 13.60% -- -28.70%

36-Month Dividend Growth -2.50% 0.50% 15.40% 11.20% -4.20% -6.60%

1 All amounts in millions of US Dollars except per share

amounts.

2 Industry: Credit Services, Industry classifications are from Media General Financial Services, Inc.

3 Public companies trading on the New York Stock Exchange, the American Stock Exchange, and the NASDAQ

National Market.

Page 16 of 23

Group 01 - Capital One / Credit Card Business 15.904

Source: Hoover’s Online (http://www.hoovers.com/)

Page 17 of 23

Group 01 - Capital One / Credit Card Business 15.904

Exhibit 2 List of credit cards for student market (2002 Freshman) Card Name: USAA College Start MasterCard Issuer: USAA Savings Bank Minimum Interest Rate: 10.00% Introductory Credit Limit: $500 Card Name: Blue for Students Issuer: American Express Minimum Interest Rate: 8.90% Introductory Credit Limit: $500 Card Name: Washington Mutual Student VISA Issuer: Citibank Minimum Interest Rate: 14.24% Introductory Credit Limit: $500 Card Name: Citi Platinum Select Issuer: Citibank Minimum Interest Rate: 11.00% Introductory Credit Limit: $500 Card Name: Discover Card Issuer: Discover Minimum Interest Rate: 17.99% Introductory Credit Limit: $1,000 Card Name: Capital One College Student Visa/MasterCard Issuer: Capital One Minimum Interest Rate: 11.90% Introductory Credit Limit: $1,500 Card Name: Bank of America Student Visa Gold Issuer: Bank of America Minimum Interest Rate: 15.75% Introductory Credit Limit: $600

Source: bankrate.com (http://www.bankrate.com/)

Page 18 of 23

Group 01 - Capital One / Credit Card Business 15.904

Exhibit 3 UK credit card issuer shares

(For this table, see Table 3.24 in Datamonitor Cards and Payments Database, 2001.)

Page 19 of 23

Group 01 - Capital One / Credit Card Business 15.904

Exhibit 4 Western European pay later card market

(For this table, see Table 6.33 in Datamonitor Cards and Payments Database, 2001.)

Page 20 of 23

Group 01 - Capital One / Credit Card Business 15.904

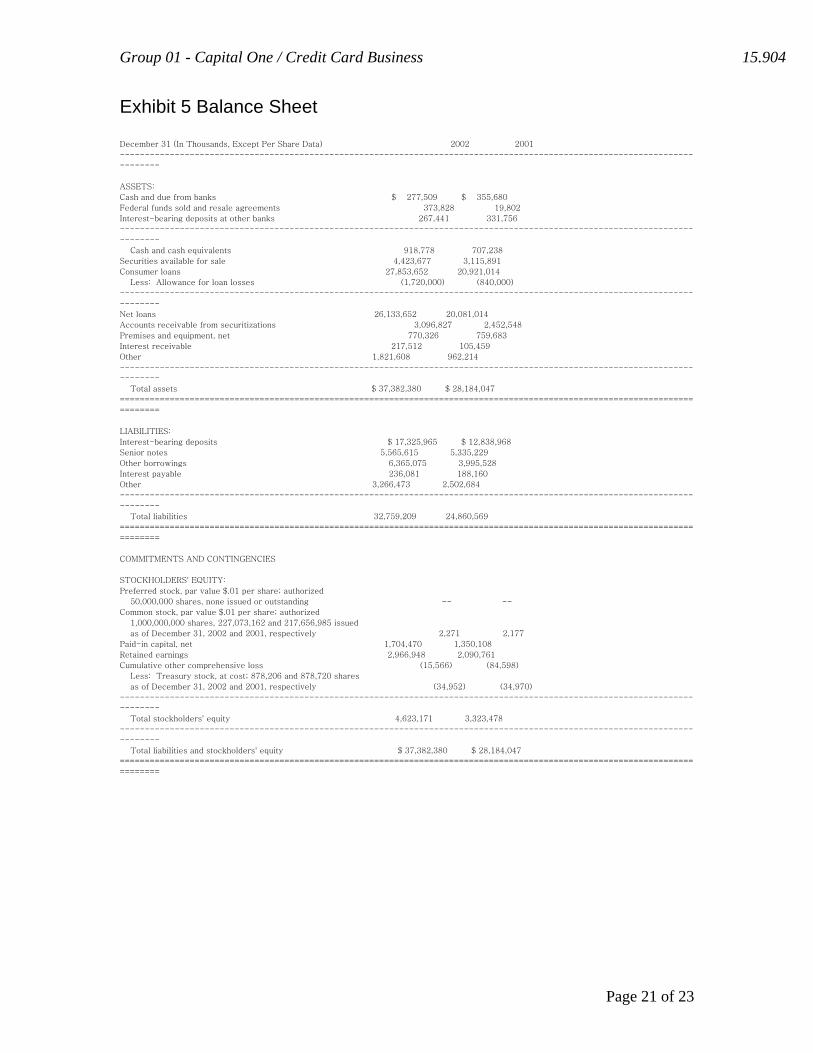

Exhibit 5 Balance Sheet

December 31 (In Thousands, Except Per Share Data) 2002 2001

-------------------------------------------------------------------------------------------------------------------

--------

ASSETS:

Cash and due from banks $ 277,509 $ 355,680

Federal funds sold and resale agreements 373,828 19,802

Interest-bearing deposits at other banks 267,441 331,756

-------------------------------------------------------------------------------------------------------------------

--------

Cash and cash equivalents 918,778 707,238

Securities available for sale 4,423,677 3,115,891

Consumer loans 27,853,652 20,921,014

Less: Allowance for loan losses (1,720,000) (840,000)

-------------------------------------------------------------------------------------------------------------------

--------

Net loans 26,133,652 20,081,014

Accounts receivable from securitizations 3,096,827 2,452,548

Premises and equipment, net 770,326 759,683

Interest receivable 217,512 105,459

Other 1,821,608 962,214

-------------------------------------------------------------------------------------------------------------------

--------

Total assets $ 37,382,380 $ 28,184,047

===================================================================================================================

========

LIABILITIES:

Interest-bearing deposits $ 17,325,965 $ 12,838,968

Senior notes 5,565,615 5,335,229

Other borrowings 6,365,075 3,995,528

Interest payable 236,081 188,160

Other 3,266,473 2,502,684

-------------------------------------------------------------------------------------------------------------------

--------

Total liabilities 32,759,209 24,860,569

===================================================================================================================

========

COMMITMENTS AND CONTINGENCIES

STOCKHOLDERS' EQUITY:

Preferred stock, par value $.01 per share; authorized

50,000,000 shares, none issued or outstanding -- --

Common stock, par value $.01 per share; authorized

1,000,000,000 shares, 227,073,162 and 217,656,985 issued

as of December 31, 2002 and 2001, respectively 2,271 2,177

Paid-in capital, net 1,704,470 1,350,108

Retained earnings 2,966,948 2,090,761

Cumulative other comprehensive loss (15,566) (84,598)

Less: Treasury stock, at cost; 878,206 and 878,720 shares

as of December 31, 2002 and 2001, respectively (34,952) (34,970)

-------------------------------------------------------------------------------------------------------------------

--------

Total stockholders' equity 4,623,171 3,323,478

-------------------------------------------------------------------------------------------------------------------

--------

Total liabilities and stockholders' equity $ 37,382,380 $ 28,184,047

===================================================================================================================

========

Page 21 of 23

Group 01 - Capital One / Credit Card Business 15.904

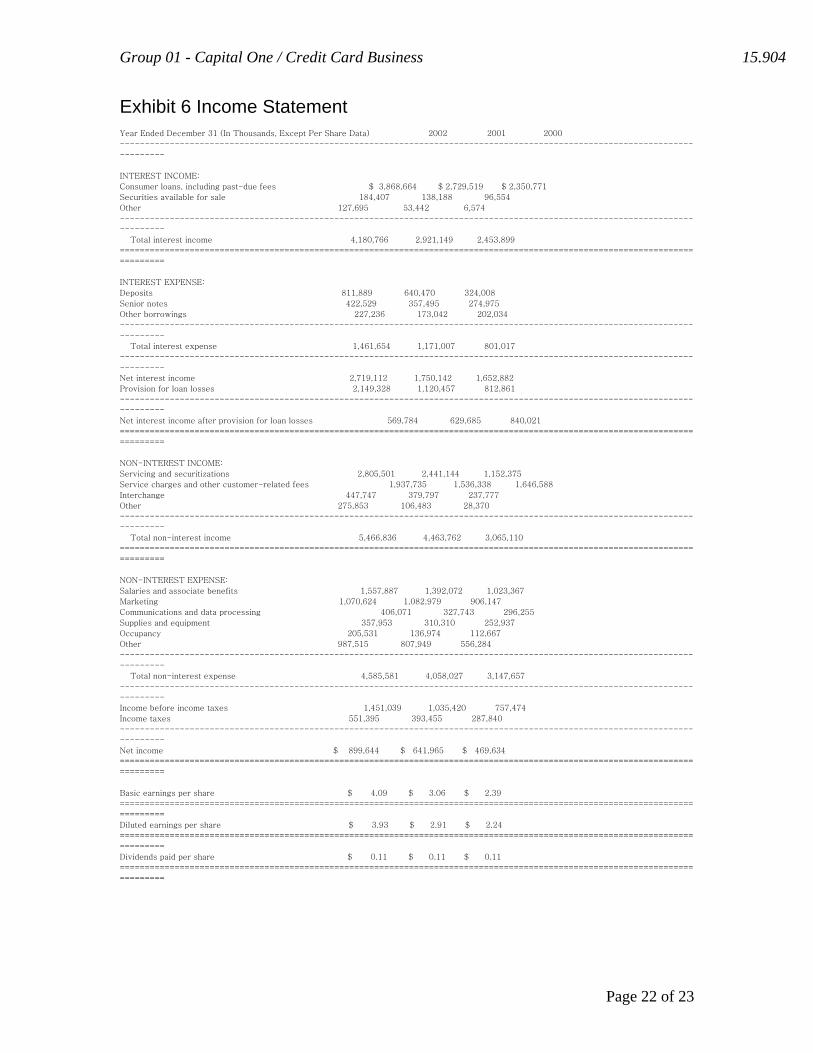

Exhibit 6 Income Statement Year Ended December 31 (In Thousands, Except Per Share Data) 2002 2001 2000

-------------------------------------------------------------------------------------------------------------------

---------

INTEREST INCOME:

Consumer loans, including past-due fees $ 3,868,664 $ 2,729,519 $ 2,350,771

Securities available for sale 184,407 138,188 96,554

Other 127,695 53,442 6,574

-------------------------------------------------------------------------------------------------------------------

---------

Total interest income 4,180,766 2,921,149 2,453,899

===================================================================================================================

=========

INTEREST EXPENSE:

Deposits 811,889 640,470 324,008

Senior notes 422,529 357,495 274,975

Other borrowings 227,236 173,042 202,034

-------------------------------------------------------------------------------------------------------------------

---------

Total interest expense 1,461,654 1,171,007 801,017

-------------------------------------------------------------------------------------------------------------------

---------

Net interest income 2,719,112 1,750,142 1,652,882

Provision for loan losses 2,149,328 1,120,457 812,861

-------------------------------------------------------------------------------------------------------------------

---------

Net interest income after provision for loan losses 569,784 629,685 840,021

===================================================================================================================

=========

NON-INTEREST INCOME:

Servicing and securitizations 2,805,501 2,441,144 1,152,375

Service charges and other customer-related fees 1,937,735 1,536,338 1,646,588

Interchange 447,747 379,797 237,777

Other 275,853 106,483 28,370

-------------------------------------------------------------------------------------------------------------------

---------

Total non-interest income 5,466,836 4,463,762 3,065,110

===================================================================================================================

=========

NON-INTEREST EXPENSE:

Salaries and associate benefits 1,557,887 1,392,072 1,023,367

Marketing 1,070,624 1,082,979 906,147

Communications and data processing 406,071 327,743 296,255

Supplies and equipment 357,953 310,310 252,937

Occupancy 205,531 136,974 112,667

Other 987,515 807,949 556,284

-------------------------------------------------------------------------------------------------------------------

---------

Total non-interest expense 4,585,581 4,058,027 3,147,657

-------------------------------------------------------------------------------------------------------------------

---------

Income before income taxes 1,451,039 1,035,420 757,474

Income taxes 551,395 393,455 287,840

-------------------------------------------------------------------------------------------------------------------

---------

Net income $ 899,644 $ 641,965 $ 469,634

===================================================================================================================

=========

Basic earnings per share $ 4.09 $ 3.06 $ 2.39

===================================================================================================================

=========

Diluted earnings per share $ 3.93 $ 2.91 $ 2.24

===================================================================================================================

=========

Dividends paid per share $ 0.11 $ 0.11 $ 0.11

===================================================================================================================

=========

Page 22 of 23

Group 01 - Capital One / Credit Card Business 15.904

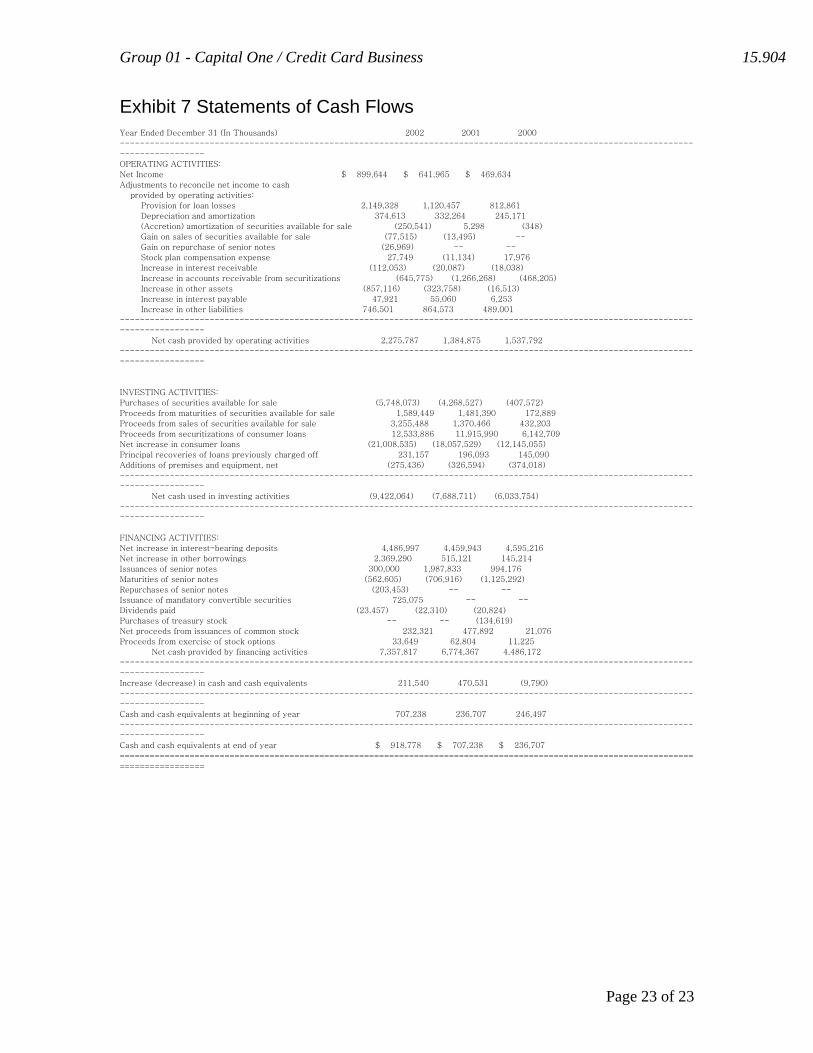

Exhibit 7 Statements of Cash Flows Year Ended December 31 (In Thousands) 2002 2001 2000

-------------------------------------------------------------------------------------------------------------------

-----------------

OPERATING ACTIVITIES:

Net Income $ 899,644 $ 641,965 $ 469,634

Adjustments to reconcile net income to cash

provided by operating activities:

Provision for loan losses 2,149,328 1,120,457 812,861

Depreciation and amortization 374,613 332,264 245,171

(Accretion) amortization of securities available for sale (250,541) 5,298 (348)

Gain on sales of securities available for sale (77,515) (13,495) --

Gain on repurchase of senior notes (26,969) -- --

Stock plan compensation expense 27,749 (11,134) 17,976

Increase in interest receivable (112,053) (20,087) (18,038)

Increase in accounts receivable from securitizations (645,775) (1,266,268) (468,205)

Increase in other assets (857,116) (323,758) (16,513)

Increase in interest payable 47,921 55,060 6,253

Increase in other liabilities 746,501 864,573 489,001

-------------------------------------------------------------------------------------------------------------------

-----------------

Net cash provided by operating activities 2,275,787 1,384,875 1,537,792

-------------------------------------------------------------------------------------------------------------------

-----------------

INVESTING ACTIVITIES:

Purchases of securities available for sale (5,748,073) (4,268,527) (407,572)

Proceeds from maturities of securities available for sale 1,589,449 1,481,390 172,889

Proceeds from sales of securities available for sale 3,255,488 1,370,466 432,203

Proceeds from securitizations of consumer loans 12,533,886 11,915,990 6,142,709

Net increase in consumer loans (21,008,535) (18,057,529) (12,145,055)

Principal recoveries of loans previously charged off 231,157 196,093 145,090

Additions of premises and equipment, net (275,436) (326,594) (374,018)

-------------------------------------------------------------------------------------------------------------------

-----------------

Net cash used in investing activities (9,422,064) (7,688,711) (6,033,754)

-------------------------------------------------------------------------------------------------------------------

-----------------

FINANCING ACTIVITIES:

Net increase in interest-bearing deposits 4,486,997 4,459,943 4,595,216

Net increase in other borrowings 2,369,290 515,121 145,214

Issuances of senior notes 300,000 1,987,833 994,176

Maturities of senior notes (562,605) (706,916) (1,125,292)

Repurchases of senior notes (203,453) -- --

Issuance of mandatory convertible securities 725,075 -- --

Dividends paid (23,457) (22,310) (20,824)

Purchases of treasury stock -- -- (134,619)

Net proceeds from issuances of common stock 232,321 477,892 21,076

Proceeds from exercise of stock options 33,649 62,804 11,225

Net cash provided by financing activities 7,357,817 6,774,367 4,486,172

-------------------------------------------------------------------------------------------------------------------

-----------------

Increase (decrease) in cash and cash equivalents 211,540 470,531 (9,790)

-------------------------------------------------------------------------------------------------------------------

-----------------

Cash and cash equivalents at beginning of year 707,238 236,707 246,497

-------------------------------------------------------------------------------------------------------------------

-----------------

Cash and cash equivalents at end of year $ 918,778 $ 707,238 $ 236,707

===================================================================================================================

=================

Page 23 of 23