-

8/7/2019 Strategic Asset Allocation Scott

1/17

Strategicsset llocationor ension unds

Rsum

Philip. ScottNorwich nion nsuranceroup, O Box 4,

urreytreet,orwich R1 3NG, UnitedKingdom

SummaryStrategicsset llocations he ost mportantecisionor ny

ensionund. It remains,howeverhe eastnderstood.There s o rightr rong

ay of etermininghe trategicsset llocationnd in the endit s

questionf findinghe est olutiono a set f constraints,ome

implicitfundstructure)nd ome xplicitlegislation).his olutionill lso

e heavilynfluencedythe ersonalhilosophiesf the investor.An

agreedtrategicsset llocationenchmarks he italay in hich he

hoicehatasbeen ade an e communicatedo ll arties.nly n hisay can he

nvestmentrocessbe nderstoodnd he esultseasuredo nsurehe und

chievests ltimatebjective fprovidingenefitso tsembers.This aper s

ritteny an nvestmentanager who s lso n ctuary)nd t rieso

akepracticalpproacho he evelopmentf trategicsset

llocationtructures.

Rpartitiontratgiquees ctifsour les Fonds de RetraiteLa

rpartitiontratgiquees ctifsst a cisiona lus mportanteour out onds

eretraite.lle esteependanta lus connue.Il y pas e onne u de

auvaiseaon e terminerne partitiontratgiqueactifset n fin e compte,

ela e rsume rouvera eilleureolution n

ensembleecontraintes,ertainesmplicitesstructureu

fonds)autresxpliciteslgislation).ettesolutionera

galementortementnfluencear les

philosophiesersonnelleselinvestisseur.Un repreonvenue

partitiontratgiqueactifsst a aon ssentiellee communiquerle hoix

ffectu outeses arties.e nest ue de cetteaon que le

processusdinvestissementeut treomprist es sultatsesursour arantirue

e ondstteigneson bjectifltimeui st e ournires llocations es

membres.Cet rticlest critar n gestionnairee placementqui st

galementctuaire)t tentedadopterne pprocheratiqueu dveloppementes

tructurese rpartitiontratgiquedactifs.

33

2nd AFIR Colloquium 1991, 3: 33-49

-

8/7/2019 Strategic Asset Allocation Scott

2/17

-

8/7/2019 Strategic Asset Allocation Scott

3/17

1.7 The asset tructuref any long-term fund, like a pension

fund,needs to be decided sing ong-term ime horizons.his long-term

target for the fund is generally known as the StrategicAsset

Allocation tructure. t should take account of theliabilitiesf the

fund and actuarialkillsave an importantpart to play in determining

the Strategic sset Allocationstructure.

1.8 Equities old a clear dvantage in matching the

attributesflong-term nflationinked iabilities.t is therefore

cceptedwisdom in the UK that he natural osition or pension fundis

to be heavily nvested n equities.owever, short-termreturns from

equities re highly volatile nd thereforeproportion f other ssets

hould be held to diversifyhis riskand ensure hat iabilitiesan be

met.

1.9 This leads o the crucialuestion for all investors:How much

of the fund should be in equities?There is o simple answer to this

uestion nd views will eheld by both the investment anager who looks

fter heassets nd the actuary ho looks fter he liabilities.hispaper

is written y an investment anager (who is also anActuary) and it

ries o take a practical pproach to thedevelopment of the

Strategicsset llocationtructure.

1.10 Deviations rom the long-term sset tructurean often

econsidered esirableecause of short-termxpectationsboutthe return

rom the differentsset ypes. his s acticalssetAllocation,hich is ot

a subject or his aper and shouldnormally e delegated o the day to

day investment anagerof the funds.

35

-

8/7/2019 Strategic Asset Allocation Scott

4/17

2 A s s e t S t r u c t u r e s2.1 The actual asset structures

of pension funds differ significantly

between one country and another. For example:

Ta b le 1B r e a k d o w n o f p e n s i o n f u n d a s s e t s

b y t y p e - 1 9 8 9

UK%Equities 78Real Estate 10Bonds & Cash 12Source :

Various

2.2

2.3

Netherlandsermany France Japan USA% % % % %38 15 26 27 4716 10 -

1 446 75 74 72 49

Care needs to be exercised in comparing the data, not

leastbecause of very different valuation methods in

differentcountries. However, the differences are sufficiently large

for usto try and find out why they exist when the funds are

seekingto achieve the same aim.UK Pension FundsUK pension funds

have traditionally had higher weightings inequities than pension

funds in any other country. Theimportance of equity investment has

existed for many years ascan be seen from the following table.

36

-

8/7/2019 Strategic Asset Allocation Scott

5/17

Ta b le 2As se t D is t r i b u t i on - U K P e n s i on F u n

d s

1965%

U K Eq u i t i e s 50O v e r s e a sE q u i t i e sR e a l E st

a t e 5B o n d s 42Cash 3Source : Central Statistical Office

1970 1980 1 9 9 0% % %56 44 53

6 2110 22 1032 23 102 5 6

2.4 One of the main reasons for this equity bias is the

inflationaryexpectations in the economy. The UK has had a high rate

ofinflation relative to many other countries and real assets,

suchas equities, have been important in achieving real (ie

inflationadjusted) returns. Bonds on the other hand tend to fare

badlyin times of high inflation. See below :

T a b l e 3Period UKAssets- RealRatesof Return

Bonds Equities% %

1950 to 1959 -2.5 +13.81960 to 1969 -1.9 +4.21970 to 1979 -4.9

+1.81980 t o 1989 +6.9 +15.3Source : BZW Equity-Gilt Study

%AverageRateof Inflation

+4.1+3.8+13.3+6.8

37

- -

-

8/7/2019 Strategic Asset Allocation Scott

6/17

2.5 In the UK attitudes towards inflation have clearly

influencedStrategic Asset Allocation. Whilst this is true in other

countries,there are also many other factors.

2.6 statutory controlsAll countries have their own particular

control mechanisms forthe management of pension funds. In the UK

there has beenconsiderable freedom to invest, whereas many other

countrieshave tended to apply investment restrictions to pension

fundseg setting a maximum on the percentage invested in equitiesor

the minimum that must be invested in Government bonds.

2.7 In the US, pension funds have been heavily influenced by

theERISA legislation and in Japan the Ministry of Finance

hasinfluenced asset allocation. All Governments will use

theirinfluence to a lesser or greater degree to ensure that

benefitpromises are met and the investment activity fits in with

othereconomic and political objectives.

2.8 Governments need to raise capital and the nature of

thatcapital will itself impact upon pension funds as they are oneof

the main sources of such funding: For example, in the UKpension

funds were investing more in Government Bonds inthe 1970s because

of the Governments substantial borrowingprogramme. In the 1980s,

the British Government raisedcapital through the disposal of shares

in privatised companies.This was one of the reasons for the 1980s

being a decade ofincreased equity weightings.

3 A t t i t u d e s3.1 Strategic Asset Allocation should produce

a target long-term

distribution of assets. It is therefore natural to seek

expertadvice to formulate the right answer. However, comparisonof

the different approaches taken around the world shows thatthere

clearly is no single right answer.

38

-

8/7/2019 Strategic Asset Allocation Scott

7/17

3.2 Strategic Asset Allocation is not purely a mathematical

processand involves many intangible considerations. In fact,

theinvestors attitudes can have the most significant impact

uponStrategic Asset Allocation. For example :. Is high or low

inflation expected?. Is international investment to be encouraged

or should

the investor remain loyal to his countrymen and invest inthe

home market?

. Should the investments be linked directly to marketvalues or

be placed with an institution which shelters thepension fund from

fluctuations in market values (ie aninsurance scheme)?

. Is investment in the employer's business to beencouraged or

avoided?

3.3 FrameworkHaving answered these questions, it is possible to

develop theframework in which the Strategic Asset Allocation

structurewill be developed. The starting point is to establish a

set ofphilosophies which will form the basis of the structure.

Thesemay include :We believe in the long term that equities will

provide a returnin excess of bonds. We believe that international

investment provides diver-sification and thereby reduces the

fluctuations in the totalreturn from the portfolio and provides the

opportunity to investin different economies.

3.4 Such a framework seems at first sight to be a very

flimsyframework for such an important decision as a Strategic

AssetAllocation of pension fund assets, It is, however, the reality

ofhow such decisions are made. There can be no certainty

thatequities will out-perform bonds but an investor must believe

itif the asset allocation is to have a high weighting in

equities.

3 9

-

8/7/2019 Strategic Asset Allocation Scott

8/17

3.5 Some investors will regard substantial equity investment as

toorisky for their pension fund. If so, then the Strategic

AssetAllocation structure must reflect this desire for caution

byincluding a much higher weighting in bonds or otherdiversifying

assets.

4 M o d e l s4.1 The weakness of basing the Strategic Asset

Allocation decision

upon a collection of philosophies can be overcome to someextent

by using computer simulation techniques. However, itis important to

remember that a model can only illustrate theoutcome of different

asset structures. This is because theoutput is highly dependent

upon the input which in the caseof investment models always

includes subjective judgement.

4.2 Asset Allocation models using the optimisation

techniquesdeveloped under Modern Portfolio Theory can be used

tosimulate different asset structures. Many such models can

bebought cheaply to run on a personal computer. They tend totake

the form :I n p u t s. Expected rates of return from the different

asset type.. Expected risks (as defined as the standard deviation

of

returns).. Expected correlations amongst the assets.o u t p u t

s. Efficient Portfolios for different levels of risk (as defined)..

Illustrations of the probability of the fund obtaining a

negative return in a particular year.

40

-

8/7/2019 Strategic Asset Allocation Scott

9/17

4.3 Such models can be used as a tool for maximising returns

forDefined Contribution funds given the chosen level of risk

butthey do suffer from the weakness of not taking account of

theliabilities when used for a Defined Benefit pension fund.

Thisweakness can be overcome to a large extent by the use

ofAsset/Liability models.

4.4 Asset/Liability models can help in developing a Strategic

AssetAllocation structure which is the most efficient portfolio

givenboth the actual and expected liability profile of the fund

andthe preferences of the investor. They can take account of

thefunds surplus position and the nature of future

contributions.

4.5 It is not a purpose of this paper to develop further the

detailin respect of Asset/Liability models. Most consulting

actuariesoffer services in this field and, in my view, they

represent asignificant step forward in the contribution that

actuaries canmake to the Strategic Asset Allocation decision. The

resultswill always be very sensitive to the assumptions made,

manyof which are highly subjective. However, if the assumptionsused

are consistent with those used in calculating thecontribution rates

then much insight is gained.

5 E c o n o m i c T r e n d s5.1 The Strategic Asset Allocation

decision should only beinfluenced by the expected long-term trends

such as inflation

and the yield from bonds and equities. Shorter term viewsshould

be taken into account by the investment manager inhis Tactical

Asset Allocation.

5.2 The global shortage of capital arising from

fundingPerestroika, the US budget deficit and the banking

systemsreserve ratio requirements is one long-term trend which

islikely to increase the return from bond investments. My own

41

-

8/7/2019 Strategic Asset Allocation Scott

10/17

philosophy for the 1990s is that equities will continue

toprovide greater returns than bonds over the long term but thatthe

difference between the return from these two asset typeswill be

smaller than existed in the 1980s.

5.3 In Europe, the economic convergence triggered off by the1992

initiative will also impact upon the relative attractivenessof

equities and bonds. From a UK investors perspective thiscould also

lead to an increased weighting of bonds,particularly if the UKs

entry into the Exchange RateMechanism is effective and there is a

sustainable lowering ofinflationary expectations in the economy.

There is also likelyto be a greater supply of bonds as the UK

Governmentresumes its funding of a new budget deficit.

6.1 There are a number of parties to the Strategic Asset

Allocationdecision :. The governing body of the pension fund

(trustees in the

UK). The finance director of the company sponsoring the fund.

The investment manager charged with day to day fund

m a na ge m e n t. Any Consultants including the Actuary.

6.2 Strategic Asset Allocation cannot be delegated to any one

ofthese parties alone since the asset allocation decision needs

totake account of all risks - although the risks are differentfor

the various parties.

42

6 Strategic Asset Allocation-Whose decision is it?

-

8/7/2019 Strategic Asset Allocation Scott

11/17

6.3 To the chairman of the governing body, the risk is that

thefund fails to fulfil the benefit expectations of the

membership.To the finance director, the risk is that poor asset

allocationmay cause a need to increase funding and hence cause

adrain on the resources of the company. To the investmentmanager,

and the consultant, the risk is that they will losebusiness if the

fund is not managed correctly.

6.4 Some of these risks can be quantified but many are

qualitativein their nature. As pension funds grow in monetary

value, it isnatural to seek more and more sophisticated

quantification ofthe risks.

6.5 Most people would agree that the medical profession are

theexperts on medical issues. For investment issues,

however,everyone considers themselves to be an expert on

theinvestment of funds of limited size. A poor man will decide

onhis investment of $100 in a savings account, whereas anexpert is

needed to decide how to invest $1,000 million.

6.6 The question remains, who is the expert on Strategic

AssetAllocation? I would argue that the expert does not exist

andStrategic Asset Allocation should be viewed as an

agreementbetween all parties, each of which has their expertise to

addto the final decision. The importance being that the issues

arediscussed and agreement is reached from the

differentperspectives.

7 B e n c h m a r k s7.1 One of the best ways of confirming this

agreement is to

establish a Benchmark asset structure which is the

normalstructure for the fund. Such a Benchmark can be used

tomonitor the progress of the fund and be the neutral portfoliofrom

which to determine whether the actual investmentoutcome has been

successful or not.

43

-

8/7/2019 Strategic Asset Allocation Scott

12/17

7.2

7.3

7.4

The poor man mentioned previously will consider hisinvestment

successful if his capital of $100 is secure and willprobably regard

any interest on the money as a bonus. Hisimplicit Benchmark is 100%

in cash.For those responsible for the management of pension

fundassets, then clearly a Benchmark of 100% in cash is

almostalways inappropriate, not least because the pension fundneeds

to obtain real rates of return. Too often, however,investors of

pension funds do not have an agreed Benchmarkand are also unaware

of the implicit Benchmark being usedby the investment manager of

the fund. This greatly increasesthe chance that the investment

outcome will disappointbecause the objectives are not clear at

outset.A Benchmark for a pension fund can typically be expressed

inthe form of long-term target distribution or range ofdistribution

of assets. For example :

Ta b le 4I llu s t r a t i v e B e n c h m a r k fo r a U K P e

n s io n F u n d

Asset

U K E q u i t ie sNon-UKE q u i t i e sR e a l E st a t eB o n d

sC a s h

Target%5525

515

0100

or Range%

50 - 6 015 - 300 - 1010 - 200 - 10

44

-

8/7/2019 Strategic Asset Allocation Scott

13/17

7.5

88.1

8.2

Benchmarks can remain as fixed percentages or beautomatically

updated for the relative movements betweenasset types. As described

above, the Benchmark can bederived from a detailed technical

analysis, such asAsset/Liability modelling, or alternatively it can

be derived bychoosing an investment strategy with an Implicit

Benchmark.

I m p l i c i t B e n c h m a r k sMany pension fund trustees

and consultants in the UK continueto regard performance relative to

the average pension fund as ameasure of the success of their

investment managers. In my viewsuch a belief means that by default

they are using the averagepension fund as an Implicit Benchmark.

This Benchmark maystill be an appropriate way of determining

Strategic AssetAllocation for average pension funds but care needs

to beexercised for Defined Benefit funds to ensure that the

liabilityprofile does not require a different approach to be

taken.Data is readily available on the actual asset structure of

theaverage fund and the total return achieved from such a fund.For

example :

Ta b le 5WM Universe of UK Pension Funds

%AssetType1985 1986 1987 1988 1989

Equities 66 71 68 69 74Real Estate 11 9 10 11 10Bonds & Cash

23 20 22 20 16

100 100 100 100 100Annual Rate of Return 14.5% 22.5% 3.4% 13.8%

30.3%

45

-

8/7/2019 Strategic Asset Allocation Scott

14/17

8.3 Trustees may feel that by setting an objective for the fund

toout-perform the average fund then there is no need toconsider the

Strategic Asset Allocation decision because thishas been delegated

to the investment manager. In practice,most investment managers who

take on the Strategic AssetAllocation decision for the client do in

fact ensure that theasset structure does not deviate too far from

the average ascan be seen from the following table.

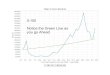

Ta b l e 6Distribution of Discretionary UK Pension Fund

AssetsProportion in Equities (as at 30.6.90)

Source : Mercer Fraser

46

-

8/7/2019 Strategic Asset Allocation Scott

15/17

8.4 The average roportion n equitiesf this ample of UK

basedinvestment anagers of pension funds was 77% a s at 30

June1990. hese managers had full iscretion ver both theStrategic nd

Tactical sset Allocation ecisions. hosemanagers who are within ay+

or 10% of the average quityexposure (shaded portion) re likely o be

using his verageas an Implicitenchmark.

8.5 Those investment anagers whose asset istributions

verydifferentrom the average re taking ubstantialusiness risksin

that the investment outcome is likely to be

significantlydifferentrom that f the average fund. In such cases it

sdifficulto identifyhe approach being taken towards StrategicAsset

llocation.

8.6 During the last 0 years in the UK the highest eturns

avealmost always been achieved from equities and a StrategicAsset

Allocation f 100% in equities as produced the bestfund performance.

owever, during the 1990s t s xpectedthat returns will be far more

volatile nd to allow theinvestment anager to invest p to 100% in

equitiess highrisk trategy,ven for rapidly rowing fund.

8.7 Therefore here the investment ecision s delegated o

aninvestment manager there is still need to agree on

theStrategicsset Allocation enchmark in order that here isagreement

between all artiesn the investment bjectivesfthe fund. Put another

way, if he fund does not have anExplicitenchmark then there hould

be an understanding fthe Implicit Benchmark and the degree to which

theinvestment anager will eviate rom that enchmark.

8.8 It an be said hat sing he average und as a Benchmark

issimply following the herd. I would argue that a skilledmanager

can stillroduce superior eturns rom TacticalssetAllocationy being

the ight istancerom the herd at the righttime e he will e

overweight n equitiesn risingarkets ndunderweight n allingarkets

elativeo an agreed enchmark.

47

-

8/7/2019 Strategic Asset Allocation Scott

16/17

9 Defined Contribution PensionFunds

9.1 Since a Defined Contributionension fund does not promiseto

provide pecificetirementenefits hen the StrategicssetAllocation

ecision oes not need to take specificccount ofthe

liabilities.owever, it s stillecessary o determine anExplicit

enchmark or choose an investment ype with anImplicitenchmark.

9.2 In a Defined Contribution fund the member will

usuallyreceive he investment eturns dded to his account ie

themember is aking he investment isk nd not the fund or

hisemployer. t s herefore tilln important uestion s to howmuch

equity content should be within the Benchmark,particularlys the

member nears etirementge when adversemarket fluctuationsan

adversely ffectenefits.

9.3 One solution s or he Benchmark to include high weightingin

cash or short-term onds although his s ikely o lead tolower

returns. lternatively,he investment ould be madewith an

institutionhich itselfas a high exposure to equitiesand offers

nvestments hat smooth the fluctuationsn thereturns o the

members.

9.4 In the UK the long establishedWith Profitunds of the

LifeInsurance ompanies are an ideal xample of such an assettype. n

developing he Strategicsset llocation enchmarkfor Defined

Contributionension fund one should considerincluding uch

investments.

48

-

8/7/2019 Strategic Asset Allocation Scott

17/17

10 Conclusion10.1

10.2

10.3

10.4

10.5

All those involved with the investment management ofPension

Funds should understand the Strategic ssetAllocation enchmark being

used for the fund. his shouldform a major part of the agreement

amongst those responsiblefor the fund.The type of Benchmark chosen

should take account of theliabilitiesf the fund but will iffer

onsiderably rom onecountry to the next. his is because of

differingttitudes,investment expectations and a variety of

investmentconstraints.Simulation echniques an be used to determine

he array fpossible outcomes of a particular investment

strategy.Wherever possible xplicitenchmarks can then be set.If the

strategicsset Allocation ecision s delegated o aninvestment anager

then it emains necessary o understandthe Implicitenchmark. If his

annot be establishednd themanagers strategy s

significantlyifferentrom the averagethen performance esultsan be

erratic.Finally, or Defined Contribution funds it should

beremembered that it s often the case that the member isbearing the

investment risk. ome form of risk sharinginvestment rom insurance

ompanies should be consideredas part f the investmentsor such

funds.