Embed Size (px)

Citation preview

IIL'PBROVING YOUR COMPETITIVE POSITION:

STR4 TEGIC AND FINANCIAL ASSESSMENT of

POLLUTION PREVENTION PROJECTS

TRAINING M m U A L

bY The Northeast Waste Management Officials' Association

The Massachusetts Office of Technical Assistance

1994

IMPROVING YOUR COMPETITIVE POSITION:

STRATEGIC AND FINANCUL ASSESSMENT of

POLLUTION PRE VENTION PROJECTS

TMINING MANUAL

Project Writers: Sam Perkins Andrew Gates

Project Managers: Terri Goldberg Dick Torborg Barbara Kelley

The Northeast Waste Management Officials' Association 129 Portland Street, 5th Floor

Boston, MA 021 14 617 367-8558

The Massachusetts Office of Technical Assistance Executive Office of Environmental Affairs

100 Cambridge Street, Suite 2109 Boston, MA 02202

617 727-3260

1994

copyright a1994 by the Northeast Waste Management Officials' Association and the Massachusetts Ofice of Technical Assistance

The Northeast Waste Management Officials' Association

The Northeast Waste Management Officials' Association (NEWMOA) is a non-profit interstate governmental association whose membership is composed of the hazardous and

Jersey, New York, Rhode Island and Vermont. NEWMOA was established by the

accordance with Section 1005 of the Resource Conservation and Recovery Act, has been formally recognized by the U.S. Environmental Protection Agency. NEWMOA is a forum for increased communication and cooperation among the member states, a vehicle for the development of unified positions on various issues and programs, and a source of research and training on hazardous and solid waste management and pollution prevention. NEWMOA's well-established pollution prevention (P2) program is active in the following areas: (1) managing the Northeast States Pollution Prevention Roundtable - a regional roundtable of state and EPA pollution prevention staff; (2) coordinating several committees of the NE Roundtable; (3) training state and EPA officials and industry representatives in pollution prevention concepts and methods; (4) publishing a quarterly newsletter on state pollution prevention activities; and (5) managing a clearinghouse of pollution prevention technical information.

~

solid waste program directors of Connecticut, Maine, Massachusetts, New Hampshire, New

Governors of the northeast states as an official interstate regional organization and, in

. ~~

. ~~~

~

For further information ,on NEWMOAs pollution prevention services contact:

Pollution Prevention Program NEWMOA

129 Portland Street, 5th Floor Boston, MA 02114

617 367-8558

The Massachusetts Office of Technical Assistance

The Massachusetts Office of Technical Assistance (MA OTA) was formed to provide large and small industries with a non-regulatory resource base to assist in toxics use reduction (TUR) planning. OTA offers the following free services to Massachusetts businesses: (1) performing on-site technical evaluations of source reduction opportunities, (2) conducting economic analyses that identify relative costs and benefits of TUR; (3) sponsoring conferences, workshops, and trade fairs to disseminate information on source reduction; (4) working with local agencies to train staff to recognize source reduction opportunities; and (5) responding to telephone and written requests for information

- For fbrther information on OTA services contact

MA OTA Executive Office of Environmental Affairs

100 Cambridge Street, Suite 2109 Boston, MA 02202

617 727-3260

ACKNOWLEDGMENTS

The project to develop this curriculum was hnded by a grant from the Northeast Hazardous Substance Research Center (NHSRC). Supplemental grants and services were also provided by the Massachusetts Office of Technical Assistance (MA OTA) and the Toxits Use Reduction Institute (TURI) at the University of Massachusetts, Lowell. NEWMOA is indebted to those organizations for their support.

This curriculum builds on earlier work presented in Costing and Financial Analysis of Pollution Prevention Projects: A Training Packet [ 19921, which was developed by Marlene Wittman and Terri Goldberg under the auspices of NEWMOA and MA OTA. The authors and editors wish to express their indebtedness to the predecessor publication, which provided much ofthe material, exercises and case studies that have been revised and expanded for this edition. For their advice and assistance in preparing this manual NEWMOA and MA OTA would also like to thank the following people: Patrick Demers, Doug DeVries, Jim DeWitt, Muriel Durgin, Andrew Gates, Terri Goldberg, Emily Hess, Barbara Kelley, Sam Perkins, Deborah Savage, Ken Tierney, and Dick Torborg.

DISCLAIMER

The views expressed in this report do not necessarily reflect those of NHSRC, the U.S EPA, MA OTA, MA TUN, NEWMOA, or the NEWMOA member states of any company, process or product name should not be considered an endorsement by the NHSRC, NEWMOA, the NEWMOA member states, MA OTA, MA TURI, or the U S EPA

Mention

... 111

ORGANIZATION and USE of CURRICULUM

This curriculum has been published in two parts to facilitate its use in instructional workshops. The Manual (Sections 1-59 contains the basic course material and is intended for distribution to workshop participants for additional explication, review and reference. The companion booklet, Instnutor’s Guide, contains explanatory information and teaching notes as well as exercises, case studies and overheads that can be used in the workshops. It is intended for presenters only and is published in loose-leaf form to permit easy copying of selected material.

For additional copies of the Mmunl or for information about attending or holding a workshop, please call:

Terri Goldberg, P2 Program Manager NEWMOA

129 Portland Street, 5th Fioor Boston, MA 02114

(617) 367-8558

printed on recycledpnper

iv

TABLE OF CONTENTS

Page

.. I 1

i i i iv

NEWMOA and MA OTA Descriptions Acknowledgments and Disclaimer Organization and Use of Curriculum

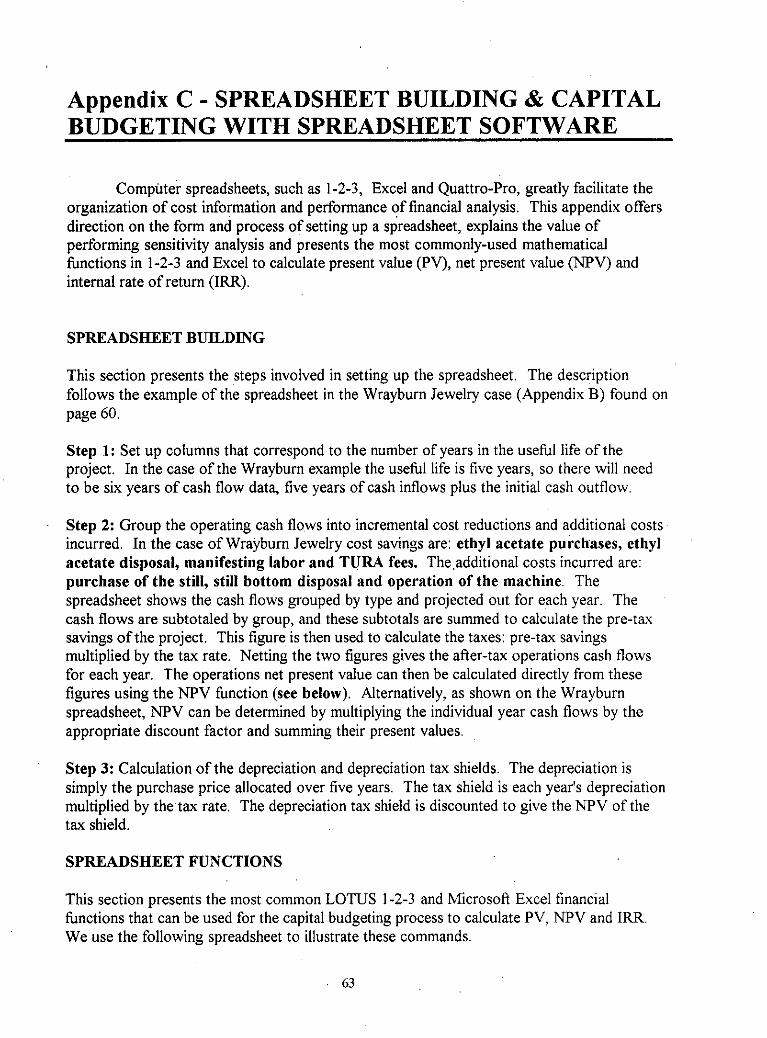

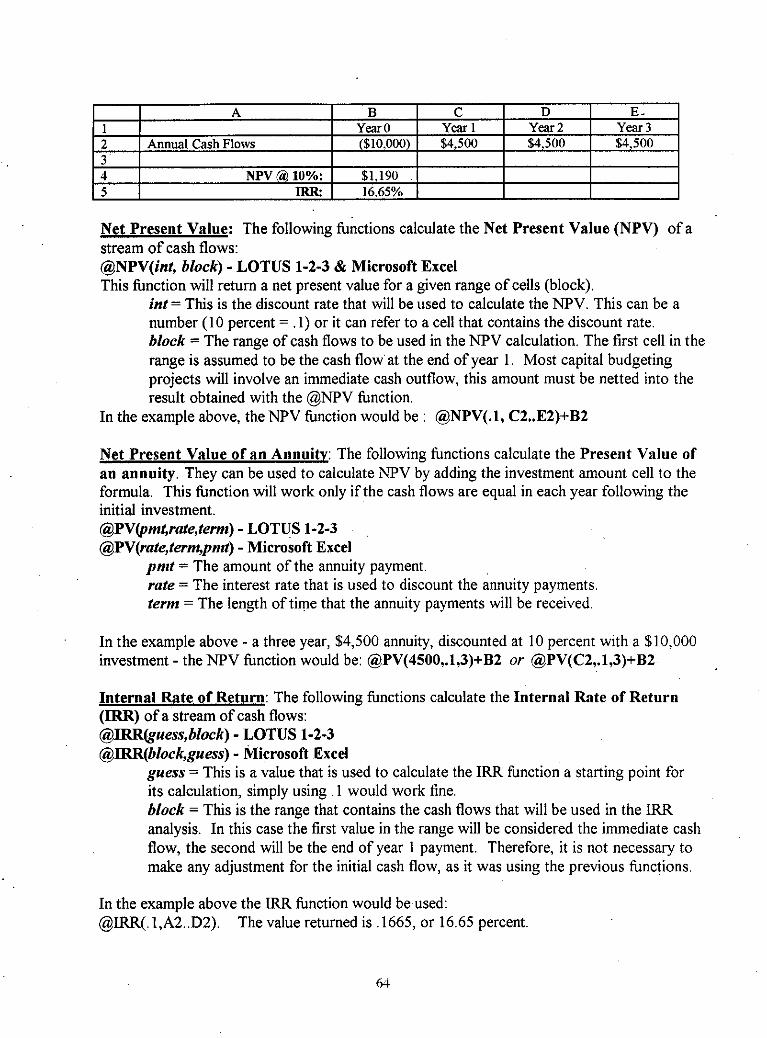

Section 1 - INTRODUCTION & OVERVIEW Purpose of this Material Capital Budgeting for Pollution Prevention Projects Financial Analysis - Objectives and Definitions

Section 2 - COST INFORMATION Definitions Process of Developing Cost Information Types and Sources of Cost Information

Section 3 - MEASURES OF PROFITABILITY Payback Period Accounting Rate of Retum Net Present Value Internal Rate of Return Inflation in Capital Budgeting

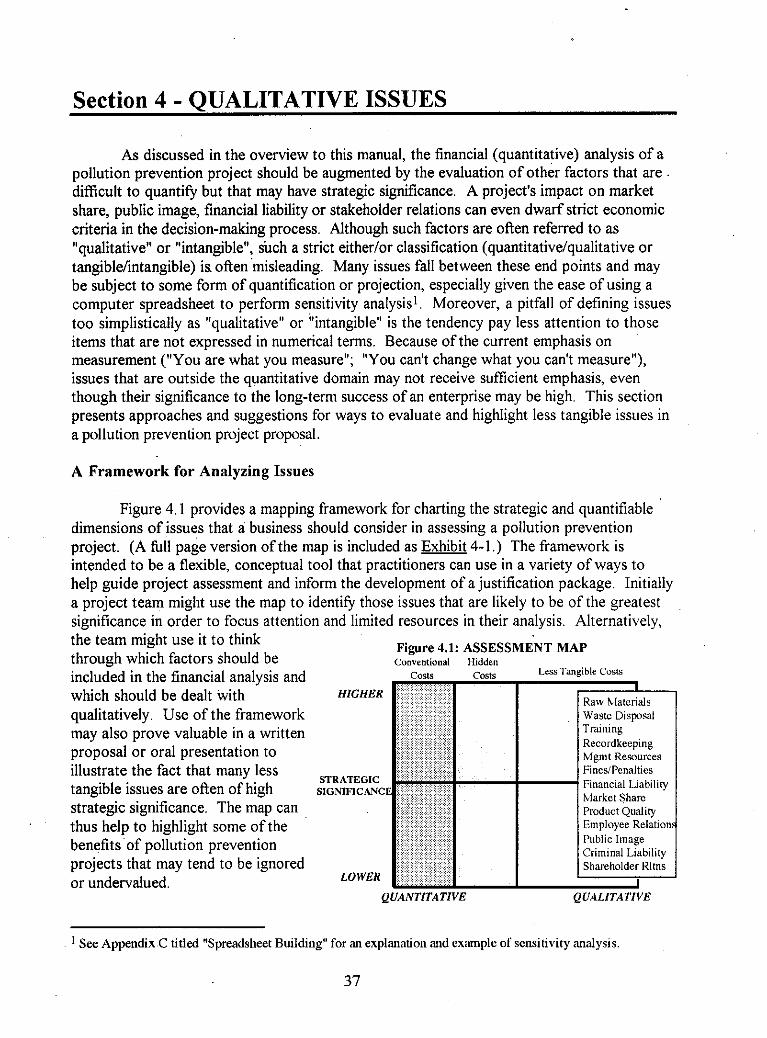

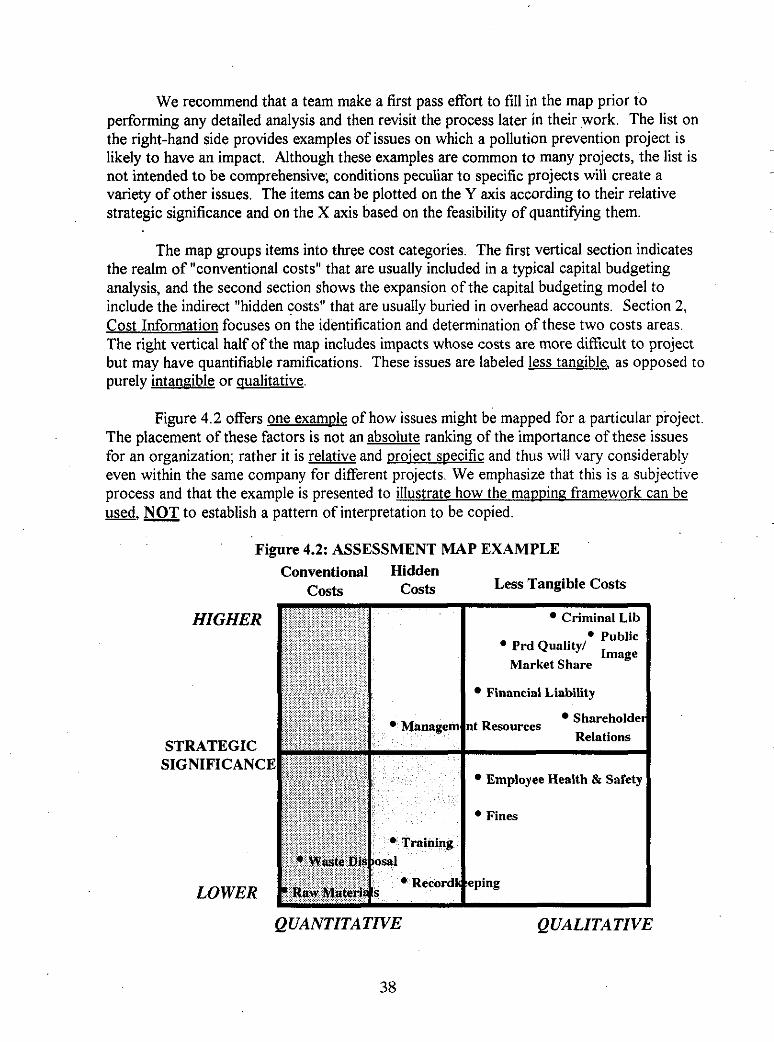

Section 4 - QUALITATIVE ISSUES Framework for Analyzing Issues Assessing Less Tangible Factors - Potential Liability Psychological Burden

1 5 7

11 12 16

27 28 28 32 34

37 39 42 45

Section 5 - APPENDICES (A) Glossary/Terminology 51 (B) Wrayburn Jewelry Case Study

(E) References 71

55 ' 63

67 (C) Spreadsheet Building & Capital Budgeting with 1-2-3 & Excel (D) Pollution Prevention Financial Assessment Models

V

Section 1 - INTRODUCTION AND OVERVIEW

PURPOSE OF THIS MATERIAL

The trend in environmental protection has shifted from end-of-pipe pollution control to process-focused pollution prevention (PZ). As the prevention strategy gains currency, a growing number of 'success stories' provide evidence that this approach can be not only more effective but also more efficient at achieving environmental targets Numerous examples across many industries catalogue the tangible savings that companies have realized through investments in pollution prevention projects. Closely allied with the more general principles of Total Quality Management, pollution prevention is increasingly being recognized both as a business opportunity and as an environmental benefit. It is an approach that all companies should adopt not only to comply with environmental regulations but even more to improve their competitive positions

POLLUTION PREVENTION P2 Act of 1990

Any practice which reduces the amount of any hazardous substance, pollutant, or contaminant entering the waste stream or otherwise released to the environment (including fugitive emissions) prior to recycling, treatment, or disposal; and reduces the hazards to public health and the environment associated with the release of such substances, pollutants, or contaminants.

Pollution prevention includes such techniques as: toxics use reduction, raw material substitution, process or equipment modification, product redesign, training, improved inventory control, production planning and sequencing, and better management practices.

As companies incorporate pollution prevention approaches in their strategic planning, capital investment priorities, and process design decisions, it is vital that they understand both the quantitative and qualitative dimensions of assessing pollution prevention projects. These projects usually reduce or eliminate costs that may not be captured in cursory financial analyses due to the way the costs are categorized and allocated by conventional management accounting systems. Additionally, pollution prevention projects often have impacts on a broad range of issues, such as market share and public image, that are difficult to quantify but that may be of strategic significance. To provide a comprehensive and accurate assessment of the potential benefits of a pollution prevention project, it is crucial that all the costs and less tangible items are identified and evaluated in a project proposal.

For a pollution prevention strategy to be successful, all employees in an organization - from the chief operating and financial officers to the line workers - should possess a basic understanding of and commitment to the philosophy and techniques. This manual is designed to be adapted to suit the needs of these different audiences. It presents material at a very elementary level for people who need basic information on certain topics but enables others to quickly review those sections about which they are already knowledgeable. For example, financial staff may be thoroughly conversant with the section Mensures of Profitability but

1 One of the most prominent examples is the 3P program - Pollution Prevention Pays - at the 3M Cotnpiuiy. The 2700 projects initiated ilnder the program have saved over $500 million since 1975.

1

may benefit from practice in constructing process flow diagrams (PFD), while engineers are likely to be proficient at PFDs but may be unfamiliar with basic financial terms contained in the Terminologv appendix. A caution, however: because this manual contains material that varies from conventional practice, it may be unwise to skip sections completely without at least a brief review.

~

.~ ~

. ~~~ While this manual attempts to address a broad audience, it does focus primarily on the anticipated needs of those employees who are likely to form the core of a pollution prevention project team. Plant personnel who design, supervise or work on operational processes and others who oversee environmental practices and compliance are usually part of the group that is designated to identify pollution prevention options, specify equipment and evaluate a project's feasibility. Although these team members (referred to here as environmental and operational [E & 01 staQ may have limited exposure to the financial and general business matters of a corporation, they are invaluable contributors to the assessment of a project's quantitative and qualitative impacts. Their involvement in plant operations provides familiarity with relevant costs and insights into less tangible issues that may be obscured from the perspective of upper management and financial controllers,

~

This curriculum is designed to familiarize environmental and operational staff with the procedures and tools for evaluating the financial aspects of a pollution prevention project. Following a general introduction to the assessment process, the material focuses on two topics central to financial analysis - cost information and measures of profitability (described below) - and concludes with a discussion of qualitative issues.

)Cost Information defines and describes the relevant costs of a pollution prevention I project and identifies likely sources of cost information. Its objective is to enhance E&O stail's existing knowledge of cost activities and enable them to provide direct assistance in the cost information gathering stage of a project

Measures of Profitability presents such measures of profitability as internal fate of return and net present value and describes how they are applied to the cost information. It is intended to familiarize E&O staff with the basic concepts and practices of these financial analysis tools to enable them to work with financial staff in the development of sound proposals.

The process of assessing pollution prevention projects, particularly the financial analysis component, fits within the framework of the standard capital budgeting model yet expands on and broadens the way capital budgeting is often practiced.2 The approach described in this curriculum attempts to rectify the tendency in financial analyses to omit environmentally-related costs, which typically are lumped into overhead accounts, arbitrarily allocated to products and overlooked in the cost identification process. Additionally, this

~

2The standard capital budgeting model costs; anecdotal evidence, however, suggests that in Dractice many "indirect costs" tend to be excluded.

should incorporate a changes in operating and adnunistrative

2

manual elevates the level of attention focused on projects' more qualitative impacts. While ours is not the only way to evaluate a project, we believe the process presented here provides an accurate method to ensure that all important benefits and potential ramifications are included in an assessment. Initiators, developers and practitioners of this approach continue to look for a name that succinctly captures both its process and its purpose yet differentiates it from other methods. There is not yet a consensus on what to call this methodology In the interim, we use the term capital budgeting forpollution prevention projects. Please send us your suggestions.

Overview of Manual

The first section of this handbook provides an overview of capital budgeting and the objectives of financial analysis Section 2 defines the parameters of cost information and describes the procedures and sources for gathering and developing this information The third section details alternative methods for using the cost data to perform a financial analysis and explains the advantages and disadvantages of the different measures of profitability The fourth section introduces the various qualitative issues to be considered in coniunction with a financial analysis to determine the impact of a proposed project

To provide a common theme for the presentation of material, this manual draws the data for many of its examples from an actual pollution prevention initiative undertaken at the Wraybum Jewelry Company (We use a fictitious name at the company's request ) The brief synopsis that follows provides the background context of that data for a better understanding of its use in the examples We strongly encourage all readers to review the full Wruyburn Jewehy Company case (Appendix B) to fully understand and tie together the information presented in the various sections

~

3

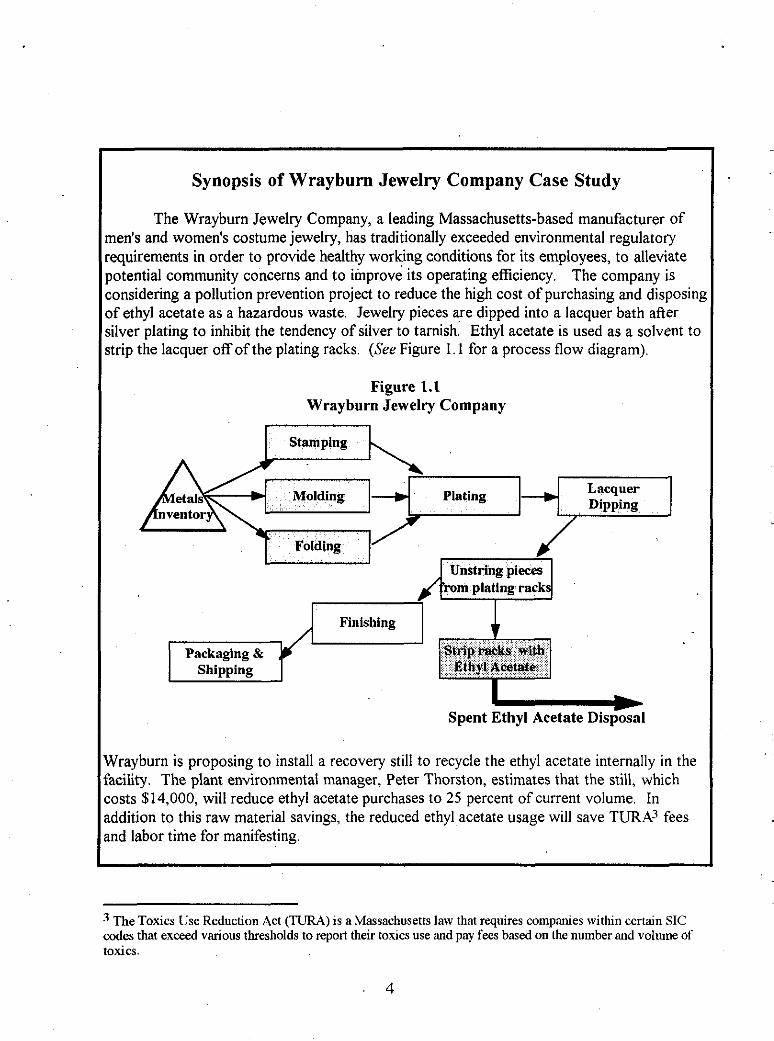

Synopsis of Wrayburn Jewelry Company Case Study

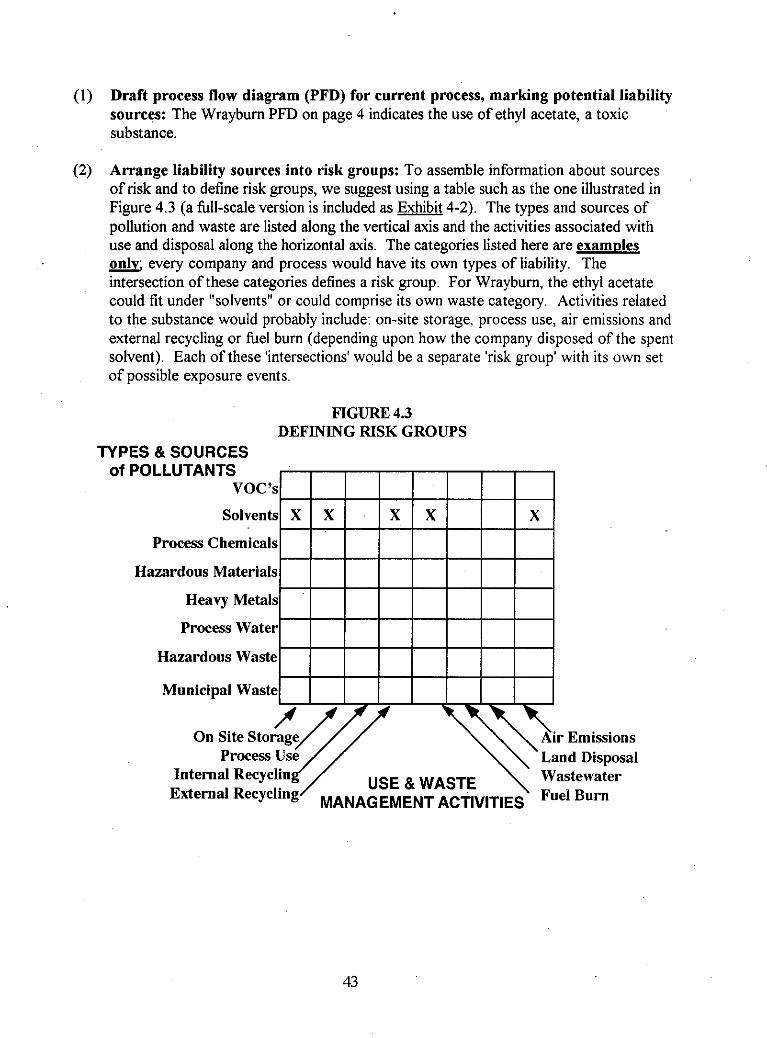

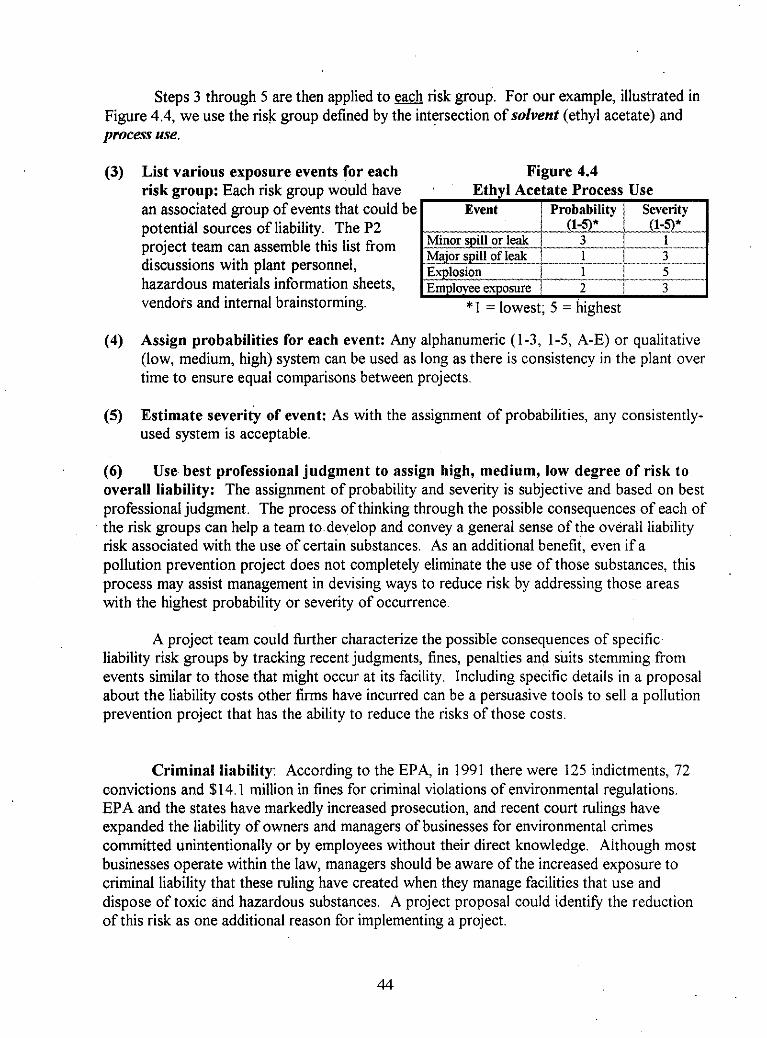

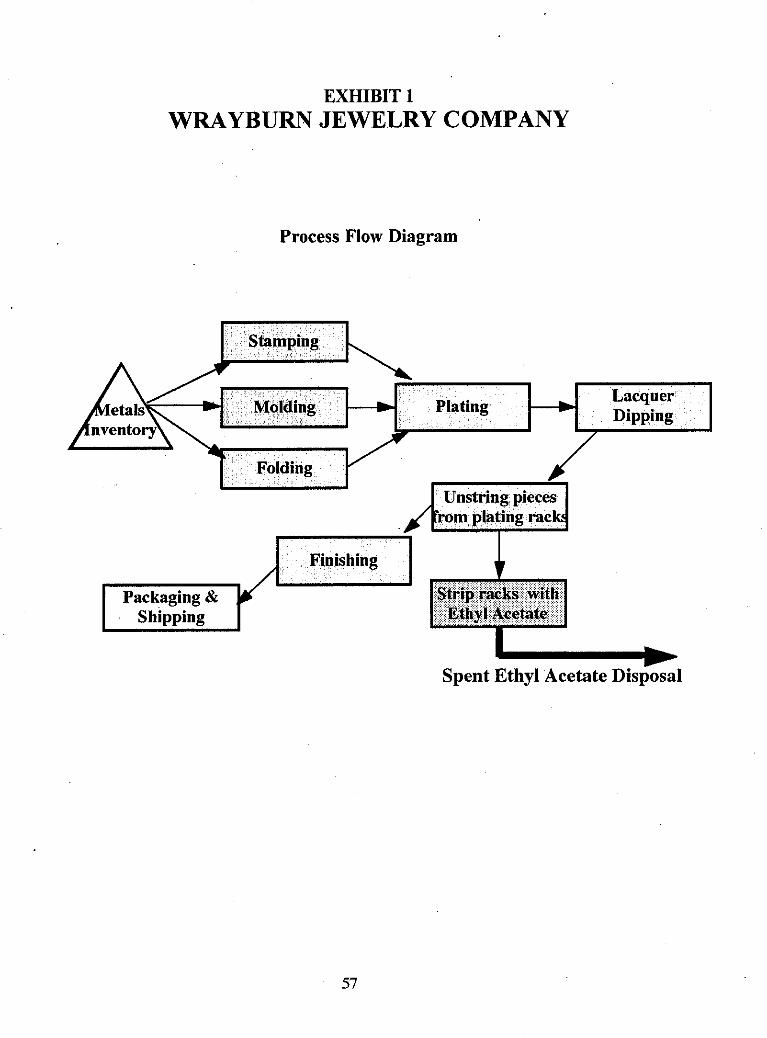

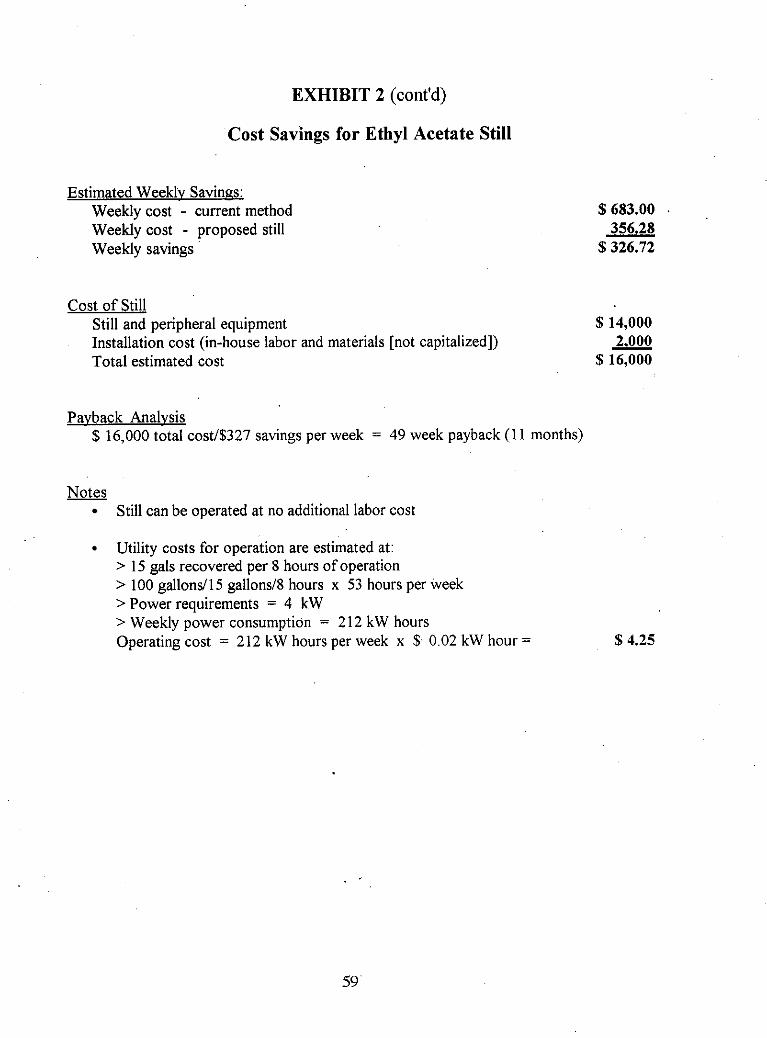

The Wrayburn Jewelry Company, a leading Massachusetts-based manufacturer of ien's and women's costume jewelry, has traditionally exceeded environmental regulatory equirements in order to provide healthy working conditions for its employees, to alleviate iotential community concerns and to improve its operating efficiency The company is onsidering a pollution prevention project to reduce the high cost of purchasing and disposing d ethyl acetate as a hazardous waste Jewelry pieces are dipped into a lacquer bath alter ilver plating to inhibit the tendency of silver to tarnish Ethyl acetate is used as a solvent to trip the lacquer off of the plating racks (See Figure 1 1 for a process flow diagram)

Figure 1.1 Wrayburn Jewelry Company

- Spent Ethyl Acetate Disposal

Vrayburn is proposing to install a recovery still to recycle the ethyl acetate internally in the icility. The plant environmental manager, Peter Thorston, estimates that the still, which osts $14,000, will reduce ethyl acetate purchases to 25 percent of current volume. In ddition to this raw material savings, the reduced ethyl acetate usage will save TURA' fees nd labor time for manifesting.

The Toxics Use Reduction Act (TURA) is a Massachusetts law that requires companies within certain SIC codes that exceed various thresholds to report their toxics use and pay fees based on the nuniber and volume of toxics.

4

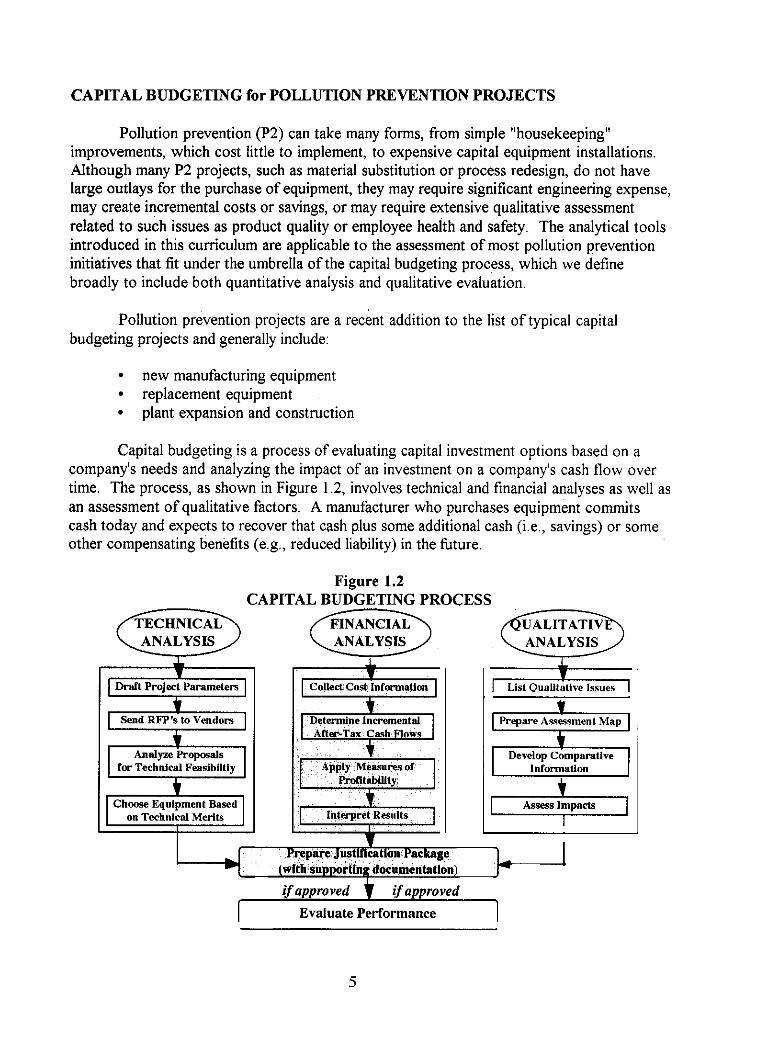

CAPITAL BUDGETING for POLLUTION PREVENTION PROJECTS

Pollution prevention (P2) can take many forms, from simple "housekeeping" improvements, which cost little to implement, to expensive capital equipment installations. Although many P2 projects, such as material substitution or process redesign, do not have large outlays for the purchase of equipment, they may require significant engineering expense, may create incremental costs or savings, or may require extensive qualitative assessment related to such issues as product quality or employee health and safety. The analytical tools introduced in this curriculum are applicable to the assessment of most pollution prevention initiatives that fit under the umbrella of the capital budgeting process, which we define broadly to include both quantitative analysis and qualitative evaluation.

Pollution prevention projects are a recent addition to the list of typical capital budgeting projects and generally include:

new manufacturing equipment replacement equipment plant expansion and construction

Capital budgeting is a process of evaluating capital investment options based on a company's needs and analyzing the impact of an investment on a company's cash flow over time. The process, as shown in Figure 1.2, involves technical and financial analyses as well as an assessment of qualitative factors. A manufacturer who purchases equipment commits cash today and expects to recover that cash plus some additional cash (i.e., savings) or some other compensating benefits (e.g., reduced liability) in the future.

Figure 1.2 CAPITAL BUDGETING PROCESS

Draft Project Parameten

. Prepare Justincation Package

(with supporting documentotioni I

= List QuaUtative Issues

Develop Comparative information

c Assess Impacts -

ifapproved f if approved

I Evaluate Performance 1

5

While accounting organizes and analyzes information about events that have already taken place, caoital budgeting tries to forecast the future and necessarily requires estimation of how events will unfold. The four principal issues that need to be estimated in capital budgeting are:

. .

cashflows, discount rate, impact of a project on a business' other cash flows, and impact on a business' future opportunities.

This curriculum deals explicitly with the first of these issues - identifying costs in order to estimate cash flows. The estimation of discount rates is best performed by a firm's financial management, and P2 project teams should ask them for that information. While the last two issues are beyond the scope of this curriculum to discuss in detail, they are important problems that need to be considered in the evaluation of all capital budgeting projects.

The capital budgeting process varies substantially between companies, depending upon size, corporate culture, ownership, management philosophy and other variables. In a small, family-owned company, the process may be very informal: the environmental engineer might approach the presidentlowner with a request for pollution prevention equipment based only a "back-of-the envelope" calculation of its merits. Conversely, in larger companies, the capital budgeting process might be so formal as to warrant a standardized evaluation format and justification package as well as a multi-level review and approval.

Regardless of the formality or complexity of the capital budgeting process at a particular company, the basic'evaluation of a project involves the following steps, which form the substance of this manual:

Collecting cost information;

* Interpreting quantitative results; and Considering qualitative factors.

Although this curriculum concentrates on the financial analysis aspects of the process,

Determining incremental after-tax cash flows; Applying financial analysis tools (measures of profitability);

qualitative issues and other intangible factors also greatly influence the outcome of a P2 project proposal and may often outweigh the quantitative analysis. Central to the consideration of many projects are such issues as:

relief from liability green marketing regulatory compliance public image worker safety technology upgrades

' pro-active environmental policy community exposure reduction customer satisfaction

6

Decision-Making Criteria

Capital budgeting - technical, financial and qualitative analysis - provides information to guide the decision-making process, a complex mechanism in most companies that is usually dependent on various contextual factors. A pollution prevention project team should be aware of the other elements that influence decision-making in order to craft a justification package that has the optimal chance of success. Some of the most common factors are:

internal Dolitics. such as rivalrv between functions or divisions: this issue is best preempted by having broad representation on the project team.

proiect sourcehitiator status: a project directive issued by top management may be evaluated according to different criteria than an effort generated by the plant engineer.

proiect obiectives: a P2 project driven by concern about a company's public image as a polluter may be judged more by its qualitative benefits while the replacement of existing machinery may require a strong financial justification.

*

.

FlCNANCIAL ANALYSIS - OBJECTIVES AND DEFINITIONS

Except for those rare cases where management has no option other than to install specific equipment, financial evaluation of a project is one of the most important too'1.s in the decision-making process. Even where a regulatory mandate may restrict choices, financial analysis remains important to understanding the economic impact of an activity on an enterprise. The financial evaluation determines whether or not an investment will add' economic value to a business, given a company's current situation and investment options and the availability and cost of financing a project.

The financial assessment of a pollution prevention project has two phases:

Collecting cost information: identifying and assembling the relevant cost information.

Auolving measures of profitability: - analyzing the cost information using one or several measures of profitability: payback, accounting rate of return, net present value (NPV), internal rate of return (IRR).

.

The objective of these steps is to determine the after-tax cash flow produced by the investment over its economic lifetime and to calculate the value of those cash flows to a business based on a measure of profitability. The definitions of these key terms follow.

7

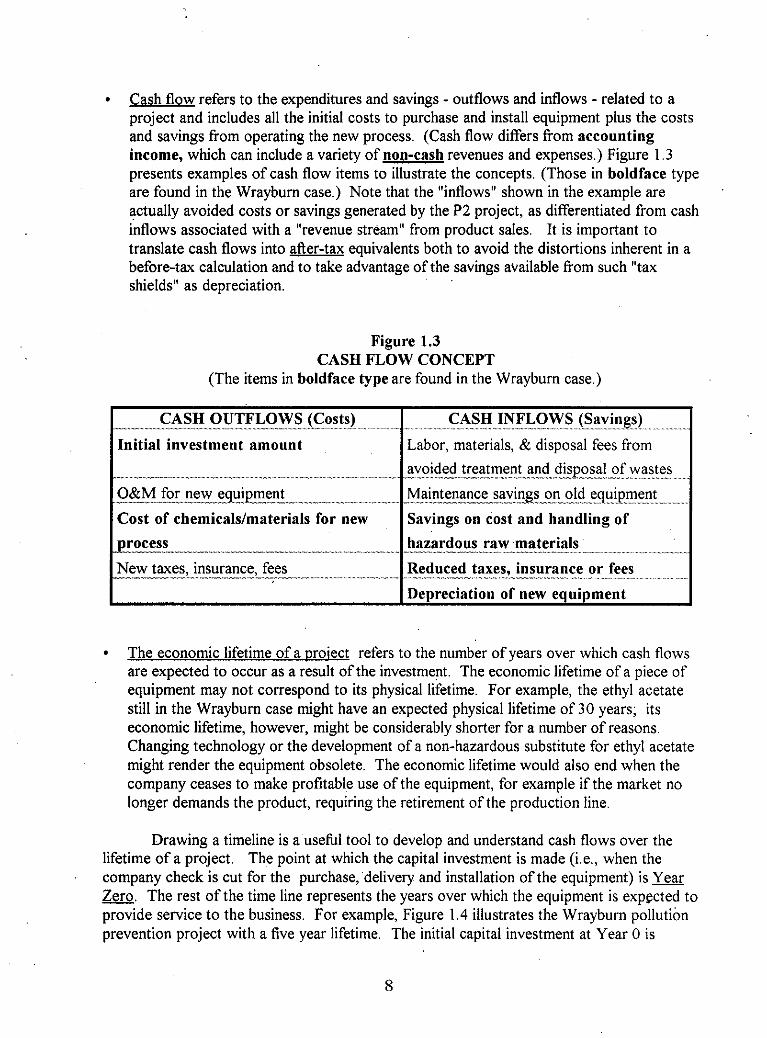

Cash flow refers to the expenditures and savings - outflows and inflows - related to a project and includes all the initial costs to purchase and install equipment plus the costs and savings from operating the new process. (Cash flow differs from accounting income, which can include a variety of non-cash revenues and expenses.) Figure 1.3 presents examples of cash flow items to illustrate the concepts. (Those in boldface type are found in the Wrayburn case.) Note that the "inflows" shown in the example are

inflows associated with a "revenue stream" from product sales. It is important to translate cash flows into after-tax equivalents both to avoid the distortions inherent in a before-tax calculation and to take advantage of the savings available from such "tax shields" as depreciation.

~

actually avoided costs or savings generated by the P2 project, as differentiated from cash . ~~

~

Figure 1.3 CASH FLOW CONCEPT

(The items in boldface type are found in the Wrayburn case.)

itial investment amount

.....

avings on cost and handling of hazardous raw materials

The economic lifetime of a oroiect refers to the number of years over which cash flows are expected to occur as a result of the investment. The economic lifetime of a piece of equipment may not correspond to its physical lifetime. For example, the ethyl acetate still in the Wrayburn case might have an expected physical lifetime of 30 years; its economic lifetime, however, might be considerably shorter for a number of reasons. Changing technology or the development of a non-hazardous substitute for ethyl acetate might render the equipment obsolete. The economic lifetime would also end when the company ceases to make profitable use of the equipment, for example if the market no longer demands the product, requiring the retirement of the production line.

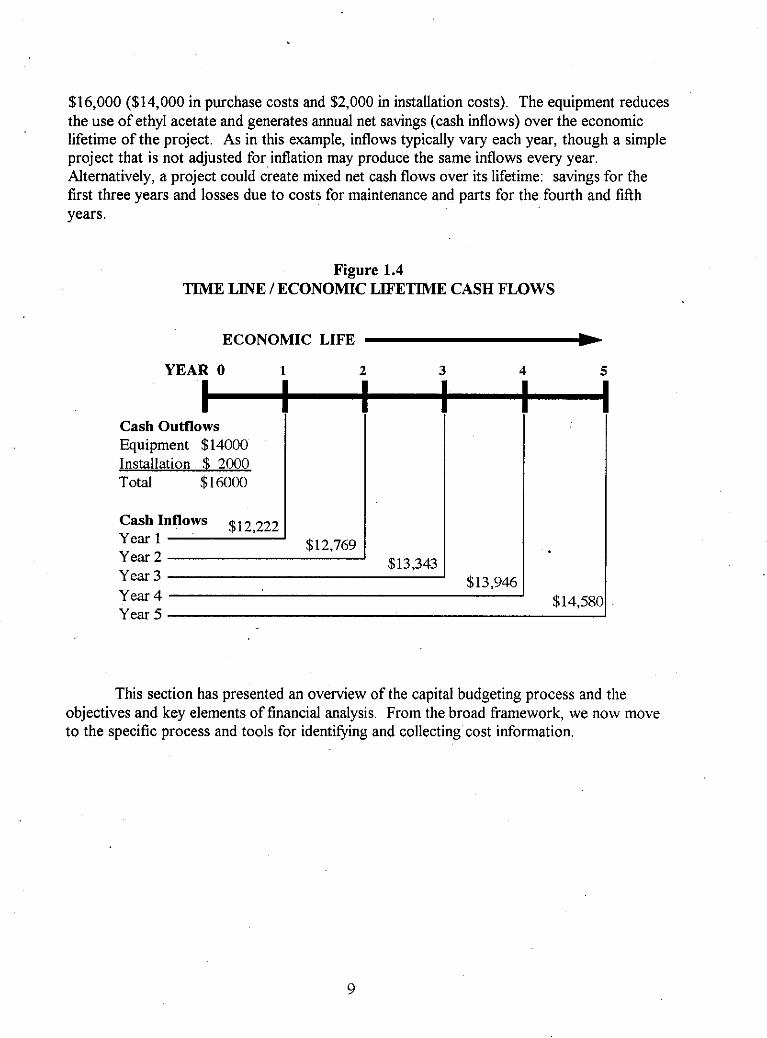

Drawing a timeline is a useful tool to develop and understand cash flows over the lifetime of a project. The point at which the capital investment is made (Le., when the company check is cut for the purchase,'delivery and installation of the equipment) is Year - Zero. The rest of the time line represents the years over which the equipment is expected to provide service to the business. For example, Figure 1.4 illustrates the Wrayburn pollution prevention project with a five year lifetime. The initial capital investment at Year 0 is

8

$16,000 ($14,000 in purchase costs and $2,000 in installation costs) The equipment reduces the use of ethyl acetate and generates annual net savings (cash inflows) over the economic lifetime of the project As in this example, inflows typically vary each year, though a simple project that is not adjusted for inflation may produce the same inflows every year Alternatively, a project could create mixed net cash flows over its lifetime savings for the first three years and losses due to costs for maintenance and parts for the fourth and fifth years

Figure 1.4 TIME LINE /ECONOMIC LIFETIME CASH FLOWS

ECONOMIC LIFE b YEAR 0 +

Cash Oufflows Equipment $14000 Installation $ 2000 Total $16000

Cash Inflows $12,222 Year 1 $12.769

3

$13.343 ' $13,945 Year 3 Year 4 $14.581 Year 5

This section has presented an overview of the capital budgeting process and the objectives and key elements of financial analysis. From the broad framework, we now move to the specific process and tools for identifying and collecting cost information.

9

Section 2 - COST INFORMATION

A financial analysis is only as accurate and realistic as the cost information it employs. Mathematical manipulation cannot compensate for the distorted effects of outdated, incomplete cost information, nor can financial analysis "fix" the lack of appropriate and relevant data. Therefore, the first phase of the financial analysis of a pollution prevention project entails gathering complete and accurate cost data in the form of relevant incremental costs calculated on an annualized basis, as defined below.

DEFINITIONS

Incremental costs: These costs, alternatively referred to as differential costs, are the changes, or differences, between the costs of the current process and the projected costs of the proposed project. These costs include one-time capital costs', such as equipment purchase, and ooerational costs, such as maintenance, waste disposal and utilities, which continue over the life-time of the project.

Relevant costs: Although this term is used in a variety of ways, we define it to mean those incremental costs that have a material impact on the decision and that are useful to those who evaluate the project proposal. The test for relevance depends on the circumstances of the particular case and must be considered within the context of a given project. For example, the elimination of one of twenty toxic chemicals may save only a few hours a year in employee safety training and manifesting, not enough to be relevant to the analysis. On the other hand, the discontinued use of the same amount of the & toxic chemical in a facility may enable the elimination of a range of activities with corresponding significant and relevant savings for the business.

- NOTE: A determination of relevunce should be mude only nfter the identification and initial review of glJ costs. Deciding a oriori thut a particulur item is not relevunt may lead to the exclusion of costs whose relevance only becomes apparent through its relationship to other issues or in projections of the 'out years' of a project.

Annualized basis: Costs should be converted to total annual amounts in order to perform the financial analysis with common metrics. For labor activities, the formula for this conversion could be expressed as:

Hours Spent on the Activity x Number of Occurrences per Year x Wage Rate

"Capital costs" refer to expenditures l'or'wpital assets, i .e,, items (such ils equipment) that Iiave a useful life of greater than one year and will be" capitalized" on a balance sheet. I t is distinguished from "cost of capital". which refers to the interest rate (cost) finns pay to use money (capit$). "Operating costs" are expenses for itenis that are consumed within one year.

11

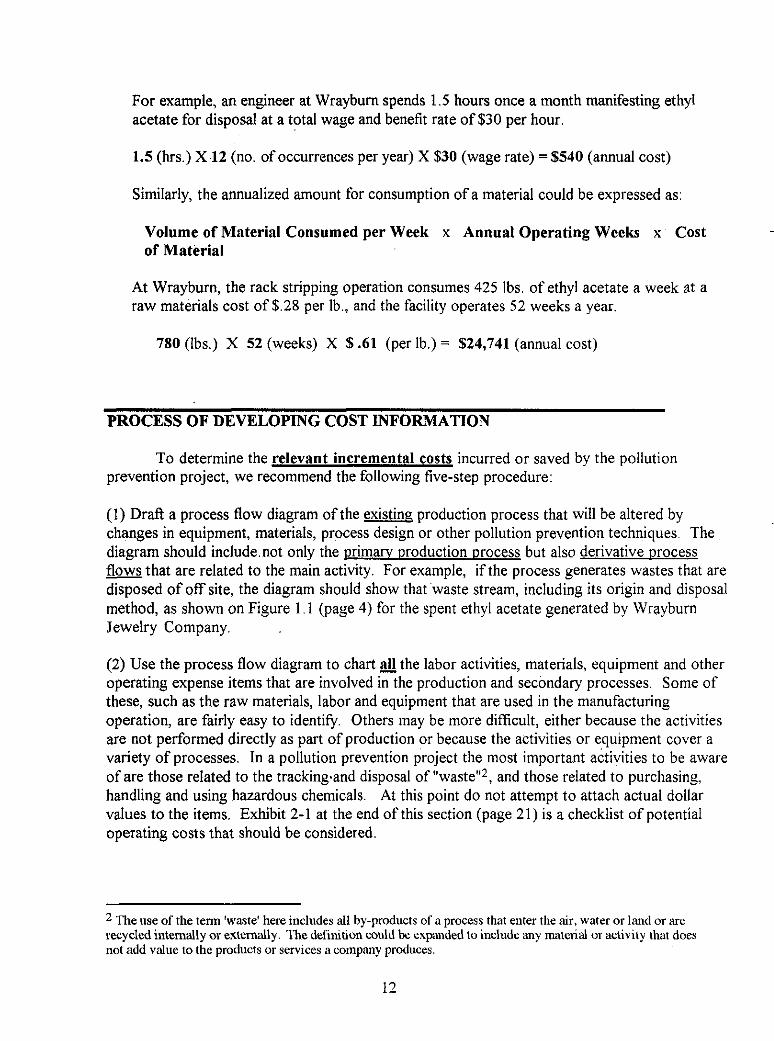

For example, an engineer at Wrayburn spends 1.5 hours once a month manifesting ethyl acetate for disposal at a total wage and benefit rate of $30 per hour.

1.5 (hrs.) X 12 (no. of occurrences per year) X $30 (wage rate) = $540 (annual cost)

Similarly, the annualized amount for consumption of a material could be expressed as:

Volume of Material Consumed per Week x Annual Operating Weeks x Cost of Material

~

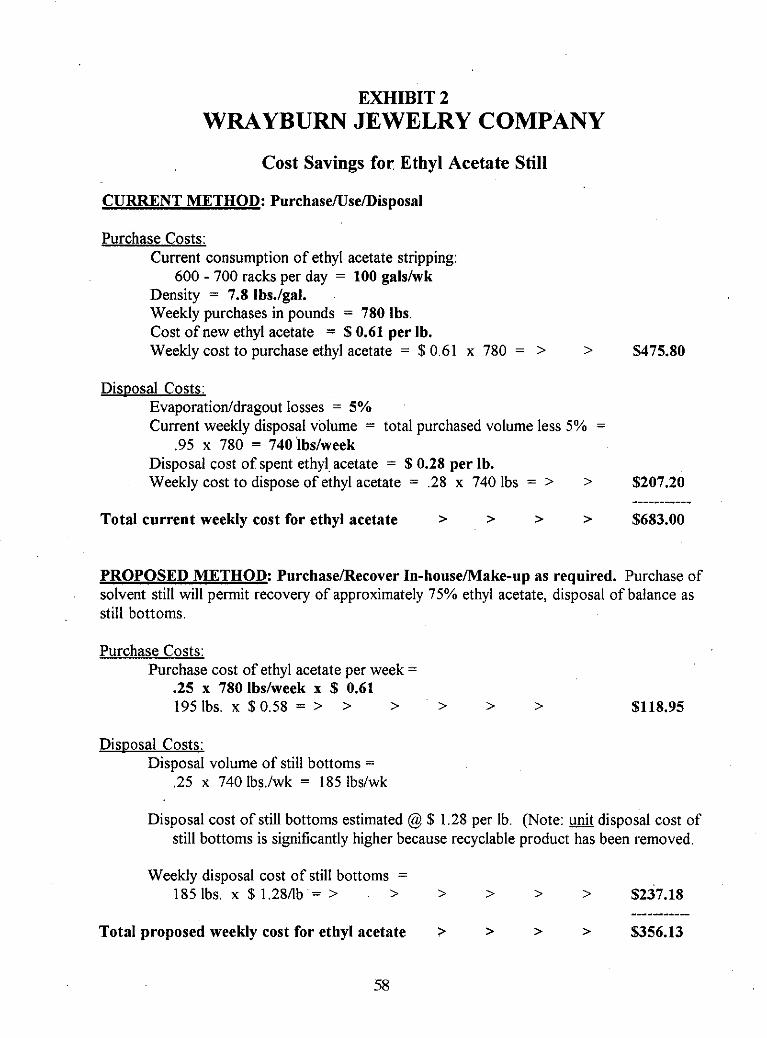

At Wrayburn, the rack stripping operation consumes 425 Ibs. of ethyl acetate a week at a raw materials cost of $.28 per Ib., and the facility operates 52 weeks a year.

780 (Ibs.) X 52 (weeks) X $ .61 (per Ib.) = $24,741 (annual cost)

PROCESS OF DEVELOPING COST INFORMATION

To determine the relevant incremental costs incurred or saved by the pollution prevention project, we recommend the following five-step procedure:

(I) Draft a process flow diagram of the existing production process that will be altered by changes in equipment, materials, process design or other pollution prevention techniques. The diagram should include.not only the primaw production process but also derivative process flows that are related to the main activity. For example, if the process generates wastes that are disposed of off site, the diagram should show that.waste stream, including its origin and disposal method, as shown on Figure 1.1 (page 4) for the spent ethyl acetate generated by Wrayburn Jewelry Company.

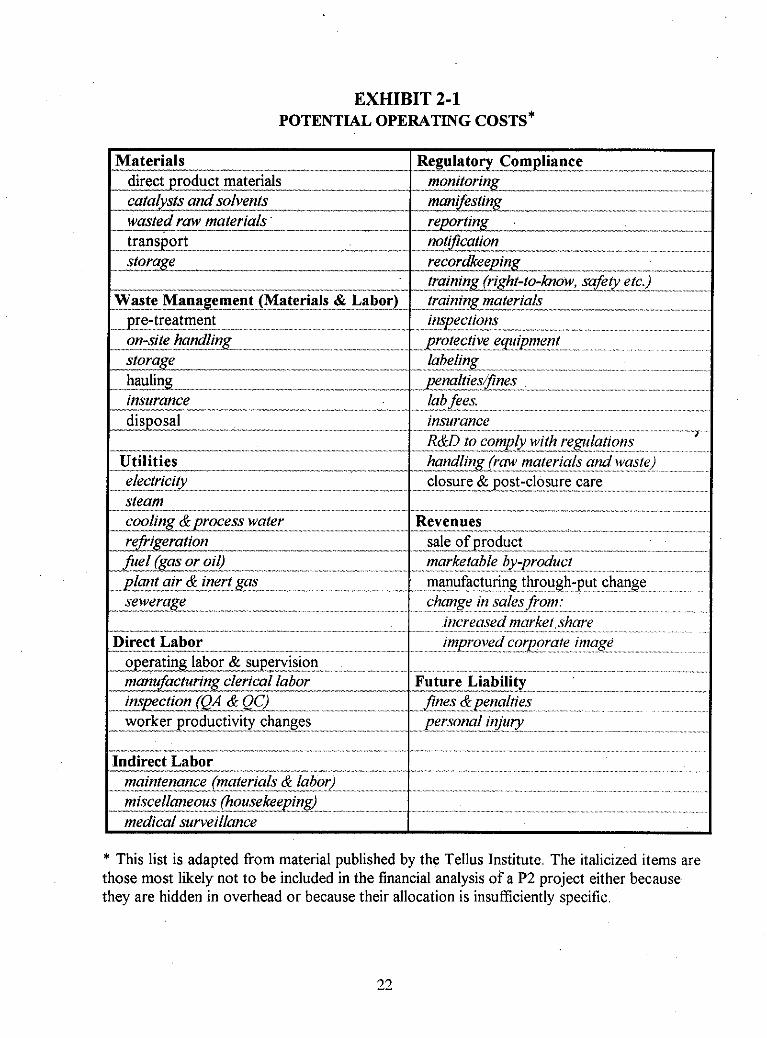

(2) Use the process flow diagram to chart fl the labor activities, materials, equipment and other operating expense items that are involved in the production and secondary processes. Some of these, such as the raw materials, labor and equipment that are used in the manufacturing operation, are fairly easy to identify. Others may be more difficult, either because the activities are not performed directly as part of production or because the activities or equipment cover a variety of processes. In a pollution prevention project the most important activities to be aware of are those related to the trackingand disposal of "waste"', and those related to purchasing, handling and using hazardous chemicals. At this point do not attempt to attach actual dollar values to the items. Exhibit 2-1 at the end of this section (page 21) is a checklist of potential operating costs that should be considered.

~

2 The nse of the term 'waste' here includes all by-products of a process that enter the air, water or land or are recycled intemally or externally. The definition could be expanded to include any inaterial or actitivity that does not add valne to the products or services a company produces.

12

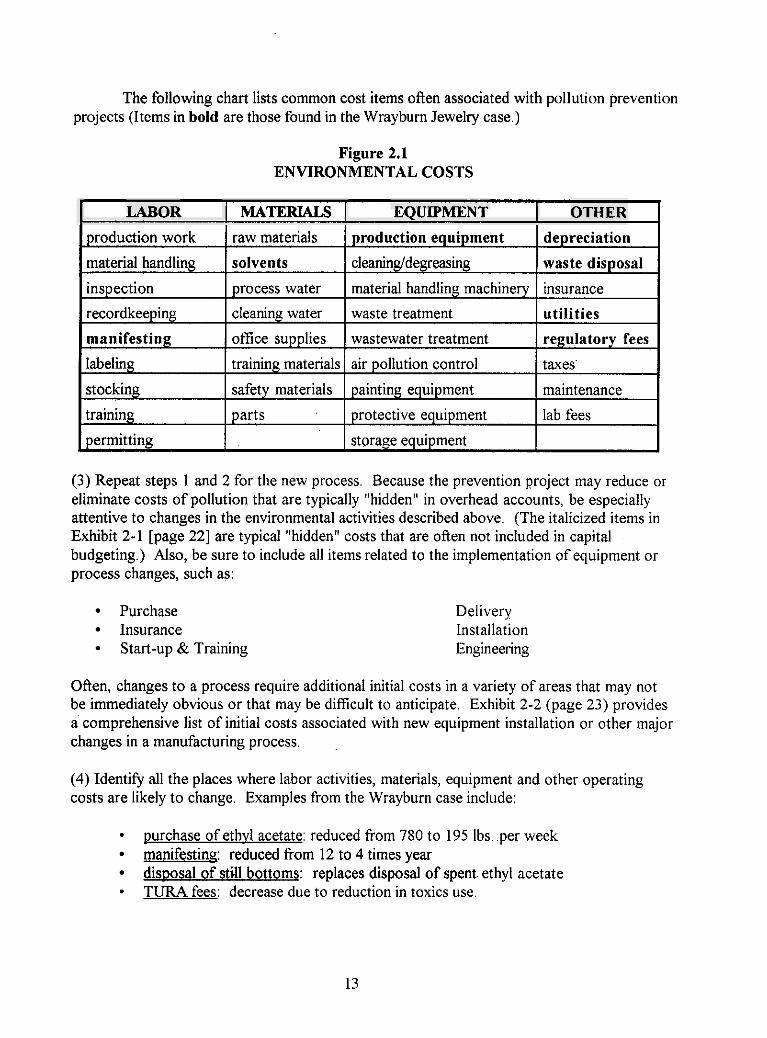

The following chart lists common cost items often associated with pollution prevention projects (Items in bold are those found in the Wrayburn Jewelry case.)

Figure 2.1 ENVIRONMENTAL COSTS

I LABOR EQUIPMENT OTHER i

(3) Repeat steps 1 and 2 for the new process. Because the prevention project may reduce or eliminate costs of pollution that are typically "hidden" in overhead accounts, be especially attentive to changes in the environmental activities described above. (The italicized items in Exhibit 2-1 [page 221 are typical "hidden" costs that are often not included in capital budgeting.) Also, be sure to include all items related to the implementation of equipment or process changes, such as:

Purchase Insurance Start-up & Training

Delivery Installation Engineering

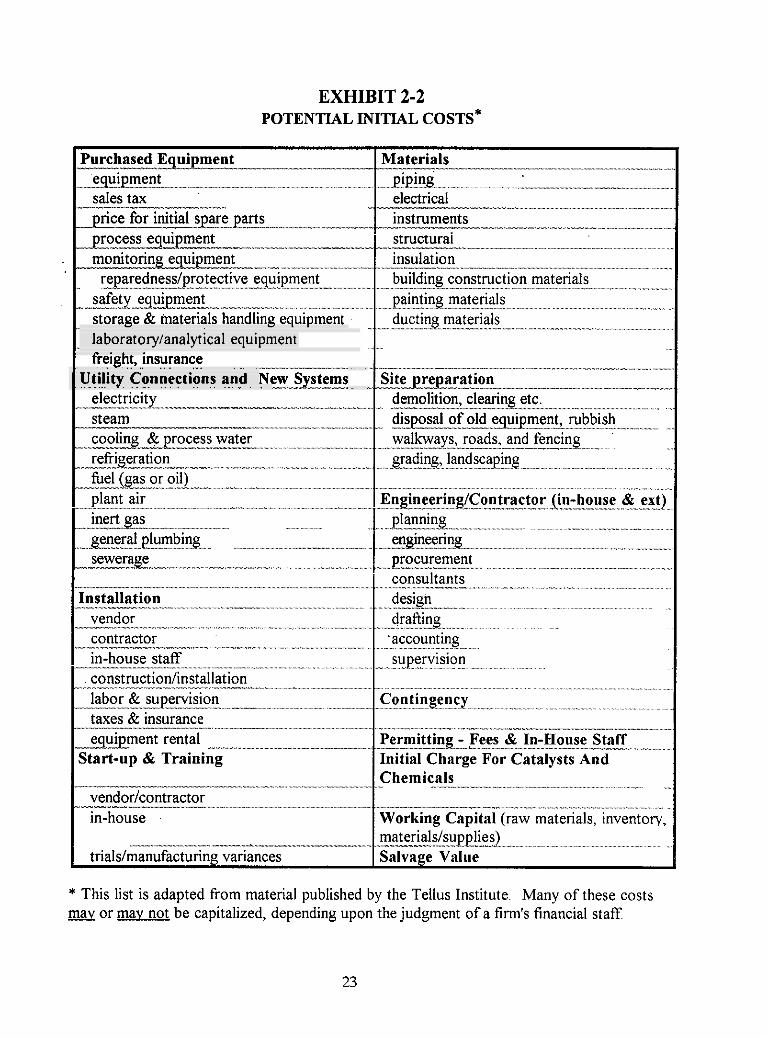

Ofien, changes to a process require additional initial costs in a variety of areas that may not be immediately obvious or that may be difficult to anticipate. Exhibit 2-2 (page 23) provides a comprehensive list of initial costs associated with new equipment installation or other major changes in a manufacturing process.

(4) Identify all the places where labor activities, materials, equipment and other operating costs are likely to change. Examples from the Wrayburn case include:

purchase of ethvl acetate: reduced from 780 to 195 Ibs. .per week manifestinq: reduced from 12 to 4 times year disoosal of still bottoms: replaces disposal of spent. ethyl acetate

* TURA fees: decrease due to reduction in toxics use.

13

(5) Determine the costs in the current process and in the proposed project for those activities and items that will change because of the proposed project. Remember to translate all cost information to an annual basis. (Although it is possible to use a weekly, monthly or quarterly basis, an annual basis is preferable.) The following section - Types and Sources of Cost Information - describes how to find the information needed to determine the costs of various activities.

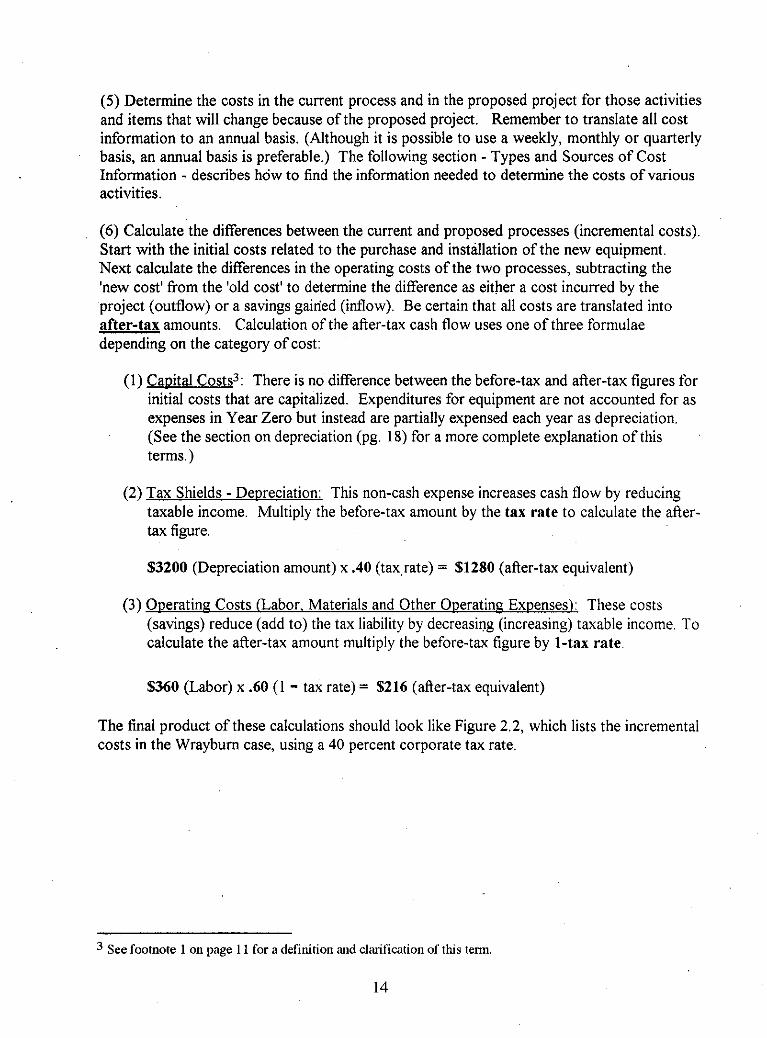

(6) Calculate the differences between the current and proposed processes (incremental costs). Start with the initial costs related to the purchase and installation of the new equipment. Next calculate the differences in the operating costs of the two processes, subtracting the 'new cost' from the 'old cost' to determine the difference as either a cost incurred by the project (outflow) or a savings gained (inflow). Be certain that all costs are translated into after-tax amounts. Calculation of the after-tax cash flow uses one of three formulae depending on the category of cost:

~

__

. ~ ~~~

~

(1) CaDital Costs3: There is no difference between the before-tax and after-tax figures for initial costs that are capitalized. Expenditures for equipment are not accounted for as expenses in Year Zero but instead are partially expensed each year as depreciation. (See the section on depreciation (pg. 18) for a more complete explanation of this terms.)

(2) Tax Shields - Depreciation: This non-cash expense increases cash flow by reducing taxable income. Multiply the before-tax amount by the tax rate to calculate the after- tax figure.

$3200 (Depreciation amount) x .40 (tax,rate) = $1280 (after-tax equivalent)

(3) Operating Costs (Labor, Materials and Other Oueratine Expenses): These costs

~

(savings) reduce (add to) the tax liability by decreasing (increasing) taxable income. To calculate the after-tax amount multiply the before-tax figure by 1-tax rate

$360 (Labor) x .60 (1 - tax rate) = $216 (after-tax equivalent)

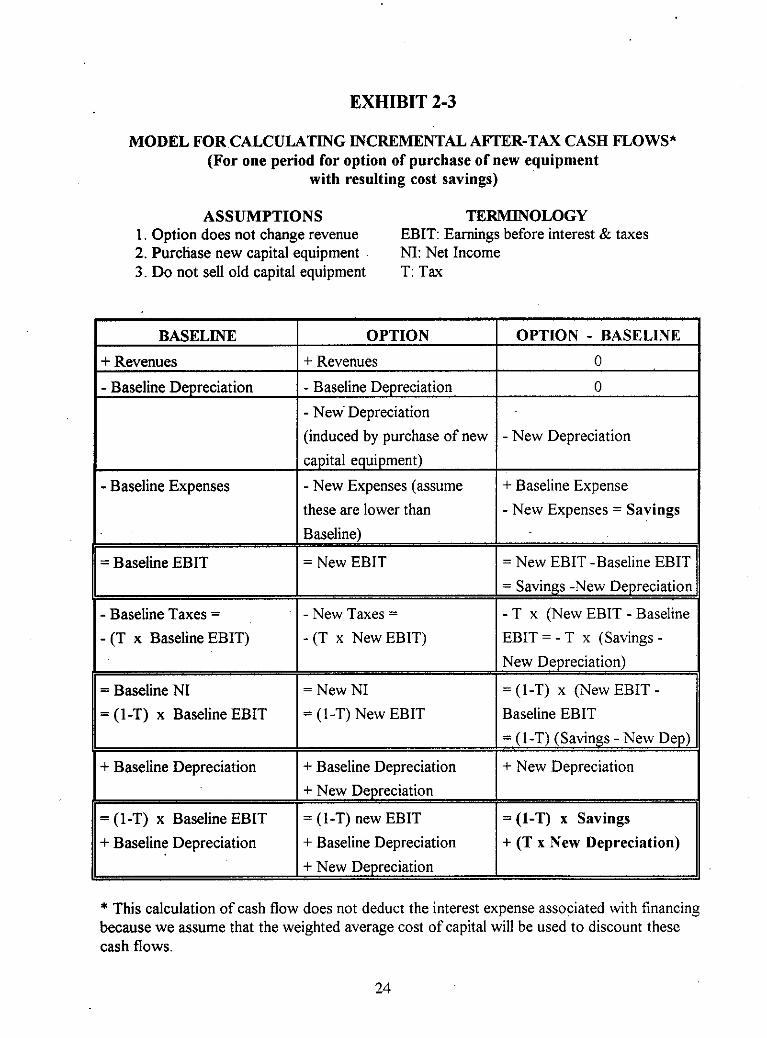

The final product of these calculations should look like Figure 2.2, which lists the incremental costs in the Wrayburn case, using a 40 percent corporate tax rate.

See footnote 1 on page 11 for a definition and cl. 'UI 'f' iwtion ofthis term.

14

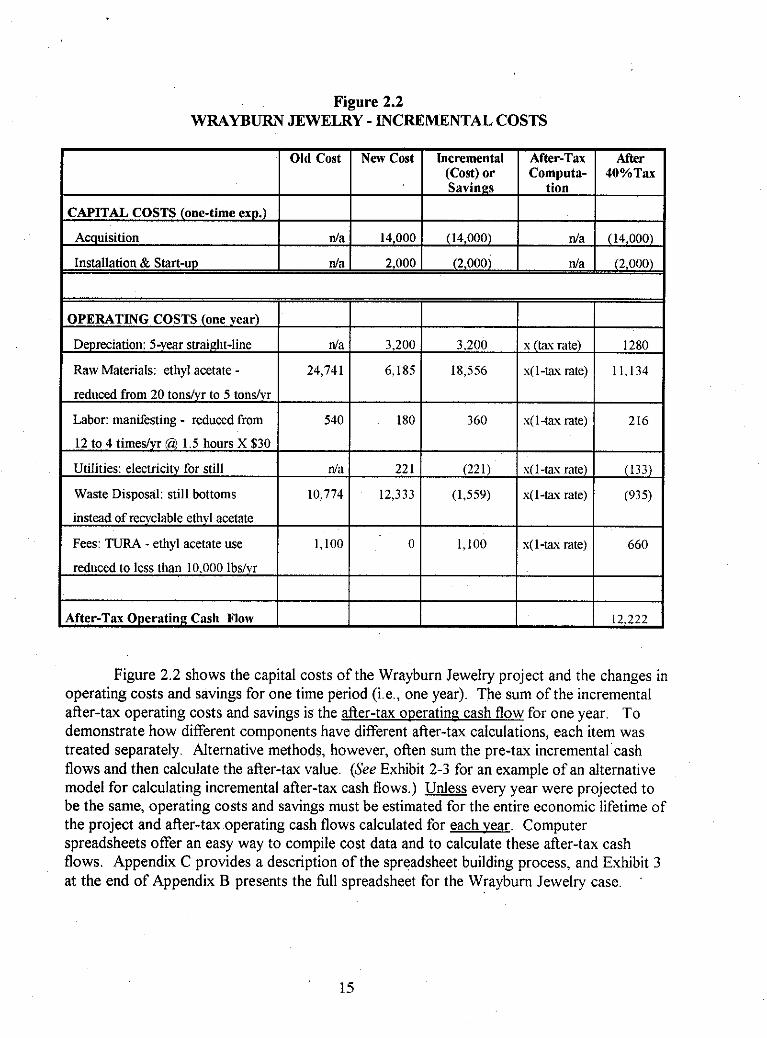

Figure 2.2 WRAYBURN JEWELRY - INCREMENTAL COSTS

CAPITAL COSTS (one-time exy.)

Acquisition

Installation & Start-up

Old Cost New Cost Incremental After-Tax After (Cost) or Computa- 40%Tax Savings tion

d a 14,000 (14,000) d a (14,000)

d a 2,000 (2,oooj n/a (2.000)

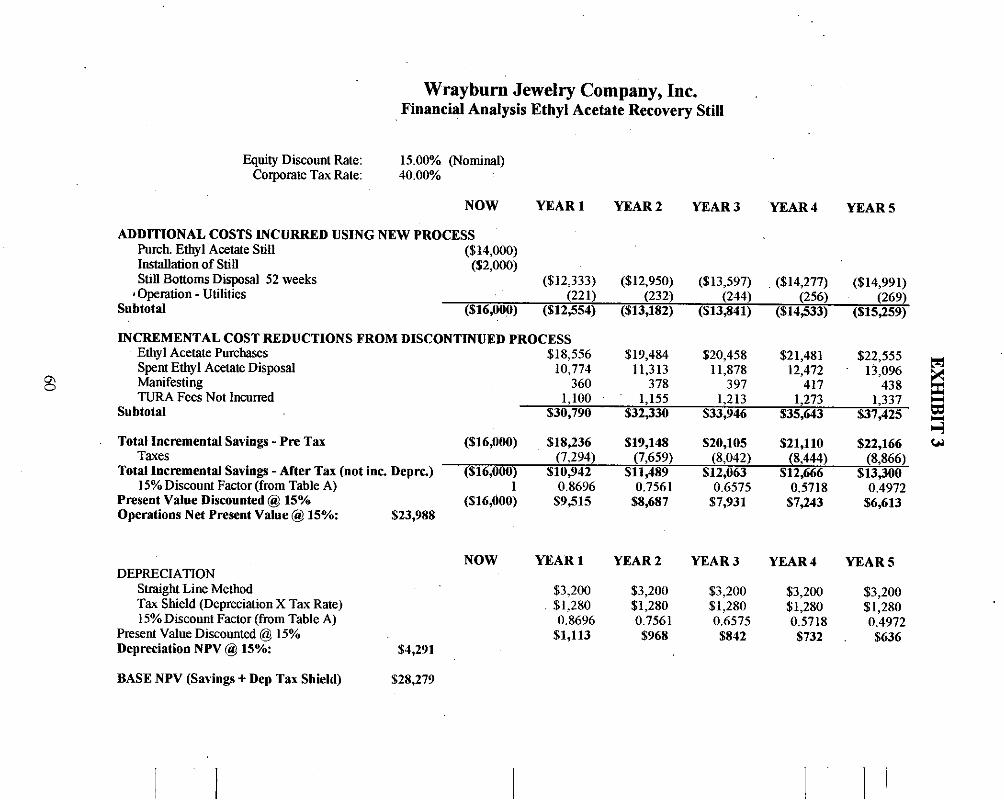

Figure 2.2 shows the capital costs of the Wrayburn Jewelry project and the changes in operating costs and savings for one time period (i.e., one year). The sum of the incremental after-tax operating costs and savings is the after-tax operating cash flow for one year. To demonstrate how different components have different after-tax calculations, each item was treated separately. Alternative methods, however, often sum the pre-tax incremental'cash flows and then calculate the after-tax value. (See Exhibit 2-3 for an example of an alternative model for calculating incremental after-tax cash flows.) Unless every year were projected to be the same, operating costs and savings must be estimated for the entire economic lifetime of the project and after-tax operating cash flows calculated for each year. Computer spreadsheets offer an easy way to compile cost data and to calculate these after-tax cash flows. Appendix C provides a description of the spreadsheet building process, and Exhibit 3 at the end of Appendix B presents the full spreadsheet for the Wrayburn Jewelry case. '

reduced to less than 10.000 lbs/vr

After-Tax Operating Cash Flow 12.222

TYPES AND SOURCES OF COST INFORMATION

The preceding section describes a method of determining the differential activities between old and new processes and calculating the incremental costs. To perform this procedure a project team must be able to attach accurate dollar amounts to each cost item. Finding this cost information, however, is rarely straightforward and may require both ingenuity and persistence, for the process will involve more than simply extracting numbers from a company's financial and cost accounting systems. As mentioned earlier, many environmental costs are "hidden" in a conventional cost accounting system and are therefore not readily accessible from that source. In addition to accounting records, the sources of cost information may include outside vendors, raw data such as purchase orders, and the subjective estimations of employees from various departments.

~

__

__

Before describing the means to uncover the cost information, the following section discusses how conventional cost accounting systems can distort the true impacts of environmental costs on products or processes. Because of these distortions, companies may have a poor understanding of these costs and thus neglect to include them when performing financial analyses. The purpose of this material is not to try to change the way companies do their cost accounting but rather to illustrate why it is so important to look beyond the information furnished by accounting reports and go directly to primary. sources for raw data.

Conventional Cost Accounting

In conventional cost accounting, costs are traditionally placed into one of three categories direct labor, direct materials, or overhead, all described more fully below

Direct Labor - Wages and benefits (including pension plan, vacation, holidays, etc ) As a ball park figure we suggest adding 25 percent to the gross hourly wage to account for labor-related costs paid to workers who assemble goods, operate equipment or directly supervise the production process

Direct Materials - all raw materials used in the production process that can be traced to individual products

Overhead - includes

> indirect labor: labor activities that S U D D O ~ ~ production and are performed by employees from support departments [e g , equipment maintenance],

> indirect materials: materials that are consumed in production but that are not part of the finished product [e g , cleaning solvent],

> operating costs: costs related to the operation of a production process [e g , electricity] (These are often lumped in with indirect materials )

> general corporate overhead: costs associated with corporate administration and other general facility costs

~

16

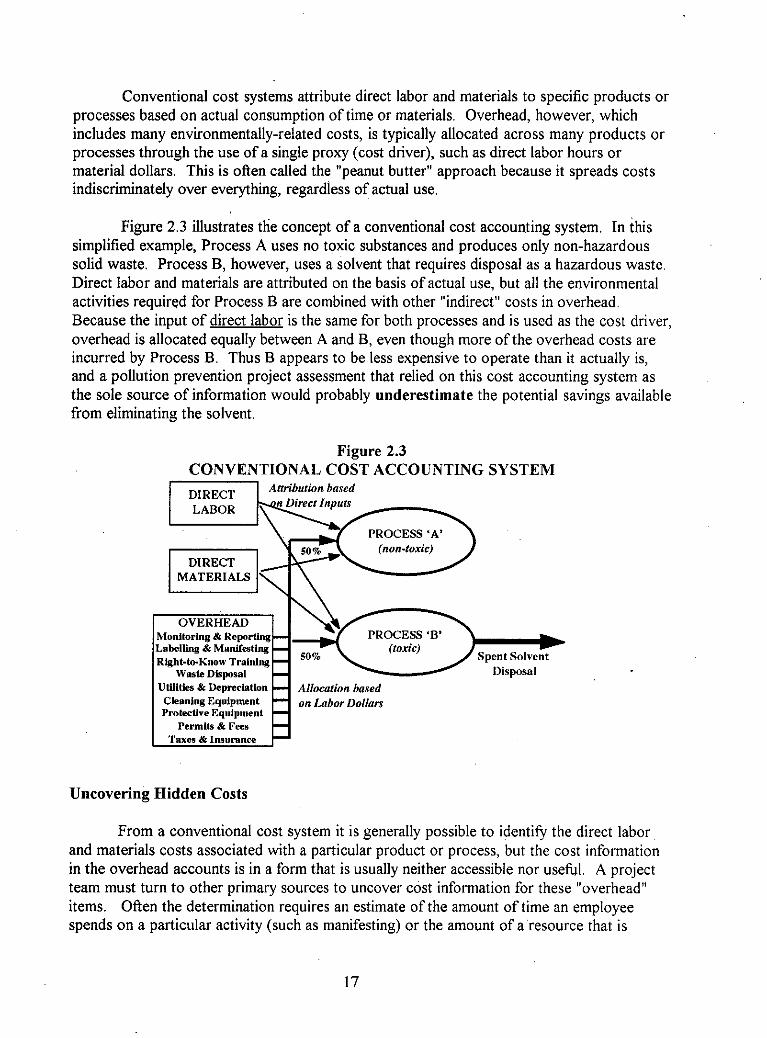

Conventional cost systems attribute direct labor and materials to specific products or processes based on actual consumption of time or materials. Overhead, however, which includes many environmentally-related costs, is typically allocated across many products or processes through the use of a single proxy (cost driver), such as direct labor hours or material dollars. This is often called the "peanut butter" approach because it spreads costs indiscriminately over everything, regardless of actual use.

Figure 2.3 illustrates the concept of a conventional cost accounting system. In this simplified example, Process A uses no toxic substances and produces only non-hazardous solid waste. Process B, however, uses a solvent that requires disposal as a hazardous waste. Direct labor and materials are attributed on the basis of actual use, but all the environmental activities required for Process B are combined with other "indirect" costs in overhead. Because the input of direct labor is the same for both processes and is used as the cost driver, overhead is allocated equally between A and B, even though more of the overhead costs are incurred by Process B. Thus B appears to be less expensive to operate than it actually is, and a pollution prevention project assessment that relied on this cost accounting system as the sole source of information would probably underestimate the potential savings available from eliminating the solvent.

Figure 2.3 CONVENTIONAL COST ACCOUNTING SYSTEM

PROCESS 'A' (non-toxic)

DIRECT MATERIALS

PROCESS 'B'

Spent Solvent Wash DLwosal Disposal

UUlities & Depreciation Allocution based I Cleaning Equipment onLaborDollan Protective Equipment

Permlls & Fees Taxes .4 Insursnce

Uncovering Hidden Costs

From a conventional cost system it is generally possible to identify the direct labor and materials costs associated with a particular product or process, but the cost information in the overhead accounts is in a form that is usually neither accessible nor useful. A project team must turn to other primary sources to uncover cost information for these "overhead" items. Often the determination requires an estimate of the amount of time an employee spends on a particular activity (such as manifesting) or the amount of a resource that is

17

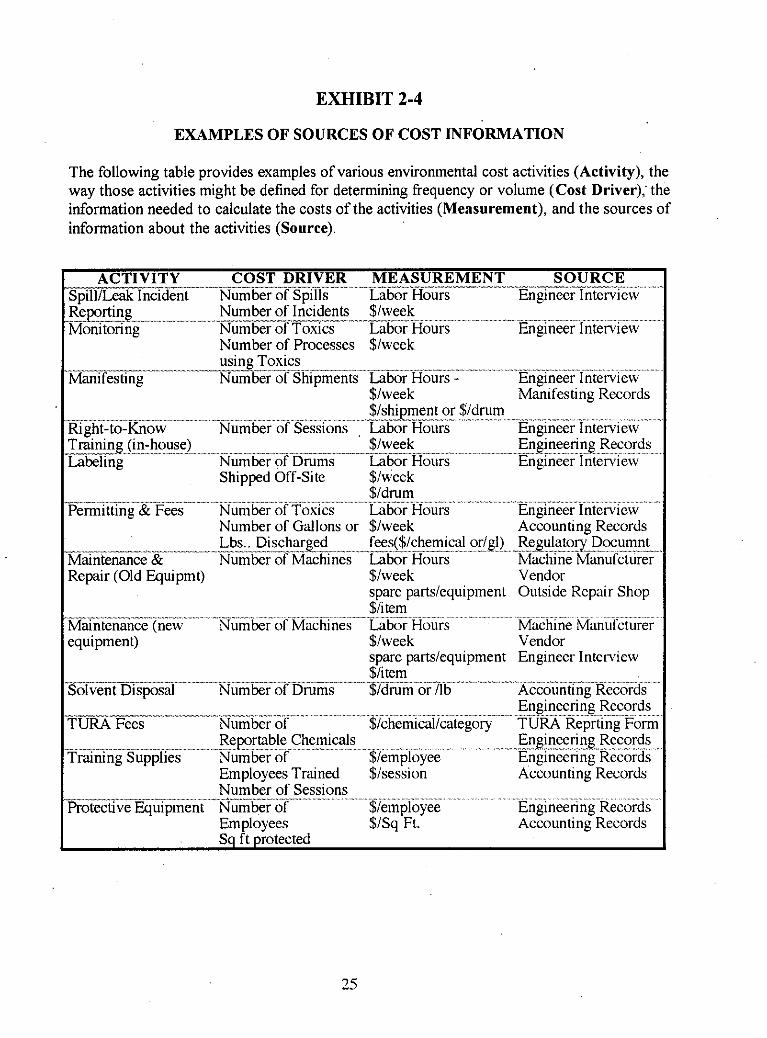

consumed in the production process (such as the electricity used by a piece of equipment). Although such estimates often lack precision, if they are made by the people who actually perform the work or who are knowledgeable about a process, the information should be sufficiently accurate. Moreover, with planning it may be possible to conduct actual measurements of these activities to provide more accurate cost data. The following sections provide suggestions about where and how to locate information for examples of the kinds of costs usually hidden in the overhead pools. (See Exhibit 2-4 for a more comprehensive list of sources of cost information.)

__ __

Indirect Labor Costs

Manifesting, labeling and recordkeeping of wastes: the environmental or manufacturing staff can provide an estimate of the number of hours per week, per shipment, or per ton.

Purchase, handling and recordkeeping of toxic materials: actual purchase orders are probably completed by the purchasing department, which could also estimate time spent on paperwork. Other incoming recordkeeping and handling may be performed by materials handlers, the stockroom andor environmental staff

Indirect Material Costs

Waste disposal, protective and safety equipment, miscellaneous supplies: the accounting (payables) department can supply invoices for these items. Alternatively, vendors are often an excellent source for such information. Estimates of the use of a material in a particular process or its presence in a waste stream can be determined by observation and by operational staff.

~

Indirect Costs of Operating Eouioment

These are the costs associated with the use of capital equipment: insurance, maintenance, utilities and depreciation. In a conventional corporate accounting system they might be included in either manufacturing or corporate overhead. Rarely will general facility costs (e.g., heating, property taxes) change with a pollution prevention project unless the project is of such a scale as to require enlargement or reduction in the overall space used or a change in an operating environment, such as the construction of a temperature and moisture- controlled room. Changes in the costs associated with replacement or addition of equipment, however, are significant and have a major impact on the financial evaluation. Several specific operational costs related to equipment include: -

0 ' Depreciation: Depreciation is an accounting convention used to record the using 'up of assets - plant and equipment - in the normal course of business operation. Assets that have a useful life of longer than one-year are not treated as current expenses but are "capitalized" to reflect their value to the company over their useful lifetime - usually 3-10 years for equipment and up to 30 years for buildings. To record a company's use of these assets, a fraction of the asset's cost is charged as an expense in

__

18

each of the accounting periods that it provides service to the business. This gradual conversion of plant and equipment from "capital" into an expense is called depreciation, and the annual amount charged is the depreciation expense. In addition to the cost of the buildings and equipment themselves, many other initial costs (detailed in Exhibit 2-2) that are incurred in planning, construction, installation or start-up are also depreciable expenses that can be capitalized. It is important to check with a company's financial staff to determine the costs of a proposed project that should be depreciated.

As a non-cash exuense, depreciation is a source of cash flow because annual depreciation charges decrease taxable income, and thus the tax that is not Daid represents a cash savings that should be included in a project analysis. This use of depreciation is known as a tax shield because the expense "shields" income from taxes.

There are a number of ways to calculate the annual depreciation expense, but this curriculum considers only the straight line method, which assumes that the asset provides service in a level stream over the economic lifetime of a project. This method charges as an expense an equal fraction of the cost of the assets each year. Consider a piece of equipment costing $16,000 with no salvage value and a useful service life of 5 years:

Annual Depreciation

.

= (Machine Cost - Salvage)/Lifetime of Machine

= $16,000 - 0 5

Depreciation Charge

The depreciation charge reduces taxable income and lowers taxes and thus represents a cash savings to a company For example.

Depreciation Charge = $3,200 per year

Tax Rate 40% x- .40 T a d c a s h Savings = $1,280

= $3,200 per year

Insurance may be either a cost or a savings, or may not be affected by a pollution prevention project. If a project dramatically changes a facility's waste disposal status, for example eliminating the use of all toxic and hazardous substances, environmental liability insurance may be reduced. On the other hand, expensive new equipment might necessitate an increase in fire and property insurance. An insurance agent should be able to provide an estimate of a project's potential impacts on insurance premiums.

19

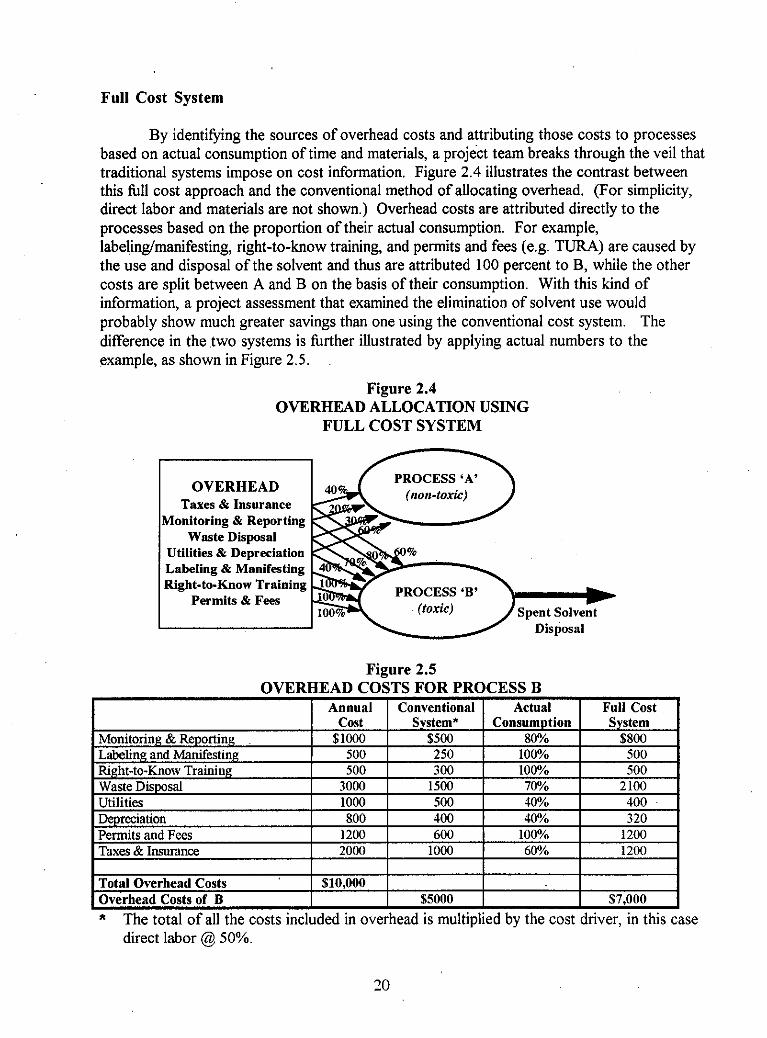

Full Cost System

By identifying the sources of overhead costs and attributing those costs to processes based on actual consumption of time and materials, a project team breaks through the veil that traditional systems impose on cost information. Figure 2.4 illustrates the contrast between this full cost approach and the conventional method of allocating overhead. (For simplicity,

processes based on the proportion of their actual consumption. For example, labeling/manifesting, right-to-know training, and permits and fees (e.g. TURA) are caused by the use and disposal of the solvent and thus are attributed 100 percent to B, while the other costs are split between A and B on the basis of their consumption. With this kind of information, a project assessment that examined the elimination of solvent use would probably show much greater savings than one using the conventional cost system. The difference in the two systems is further illustrated by applying actual numbers to the example, as shown in Figure 2.5.

~

~

direct labor and materials are not shown.) Overhead costs are attributed directly to the . ~~

__

Figure 2.4 OVERHEAD ALLOCATION USING

FULL COST SYSTEM - n OVERHEAD

Taxes & Insurance Monitoring & Reporting

Waste Disposal Utilities & Depreciation Labeling & Manifesting Right-to-Know Training

Permits & Fees

’ x PRoCESS‘A’ (non-toxic)

Spent Solvent PROCESS ‘B’

(toxic) - \ / Disposal

Figure 2.5 OVERHEAD COSTS FOR PROCESS B

I Overhead Costs of B $5000 I $7,000 I * The total of all the costs included in overhead is multiplied by the cost driver. in this case

direct labor @ 50%.

As stated earlier, it is not the intention of this curriculum to persuade companies to change their entire cost accounting structures. The full cost system described above, however, does represent the recommended procedure for identifying and calculating the costs of those indirect activities that are changed by a particular project. The accurate inclusion of such costs can have a significant impact on the measurement of a project's economic value

Avoidable Vs. Non-Avoidable Costs

There are two other ways to classify costs that are useful to the planning, analysis and evaluation of pollution prevention projects. In the discussion above, we include all costs that are related to the process affected by the pollution prevention project. Although it is appropriate to include all costs in the financial analysis, it is important to understand that while some of those categories represent real operating cost reductions for the plant or company, others imply re-allocations of labor and may or may not represent immediate gains to the facility as a whole. This distinction between costs that "go away" and those that are "movedaound", we refer to as "avoidable" and "non-avoidable" costs.

6 Avoidable costs: Reductions in these costs stem from changes in activities, materials or capital. They flow directly to the bottom line of a plant or company and are quickly (depending on inventory levels) seen as lower cost of goods sold or lower overhead costs. Examples would be: purchases of toxic chemicals or reduced waste disposal costs.

Non-avoidable costs: Though no longefattributable to the product or process under consideration, these costs do not end with the implementation of the pollution prevention project. They are usually indirect labor costs associated with pollution control activities, such as manifesting, training, ordering or handling toxics. A plant as a whole does not see any immediate gain from a reduction in these costs unless the reduction is so great that it enables a decrease in actual headcount, or unless the employees involved are being paid overtime to complete the tasks. For instance, the reduction in time for manifesting containers from 4 to 2 hours a week by someone earning $20 per hour may not necessarily translate into an actual $40 per week cost saving to the company.

The distinction is important in order to avoid the mistaken impression that all the cost reductions enabled by the project translate into immediate bottom-line savings. While non- avoidable costs may have minor immediate financial benefit, the reduction in these indirect costs can have long-term pay-off. The company stands to gain significantly by having its professional staff freed up from performing tasks that add no value to the product. The ability of the company to redirect those freed-up hours to more useful (value-added) tasks will determine the added benefit from the reduction in non-avoidable costs. Because of the long-term potential benefits of reducing non-avoidable costs, we include these savings in the financial analysis.

21

EXHIBIT 2-1 POTENTIAL OPERATING COSTS*

_I Materials ,,-II_ - Regulatory Compliance

2--"".-"-_---- catal sts and solvents - ....

~- transjeort **"I .... 11 ......... -... ........ nohication .._-__l____l__

direct product materials *"ll_."" monitoring

wasted raw materials

-I "___ ,I_._II_I_Ix__-___

m9es t ing .--I ".-."I"III-II.I ll..ll.." ..... r e p o r t i n c l l l . . ~ _ _ -

....... recordkeeping ................ ........................... .... .. ............. training ..... (rig&-to-know, safety .... etc.) .... .................

......................

s tor ze _l _l_-_.-____"____^""__-_I_ ,.._ ,._. *l.**___ll ...., ..., Waste Management

" re-treatment .........................................

....................

.................

. . . . . . . . . . . . . . . .

... ...................... .......

........ __ ..................

........... "

. . . . . . . . . . . . . .

. . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

............... -. .. .- ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

* This list is adapted from material published by the Tellus Institute. The italicized items are those most likely not to be included in the financial analysis of'a P2 project either because they are hidden in overhead or because their allocation is insufficiently specific.

EXHIBIT 2-2 POTENTIAL INITIAL COSTS*

~ - - - - . ~ - - _ _ - l

..".-.-._I__.- equipment ----- --~-" .. .................................... ......

monitoring -I equipment -.l ....... reEredness/grotective .____.I . equipment .............

.................... safety equipment ".I _l.....l.**l.._l.* ............................................... storage & materials handling equipment laboratory/analyticaI equipment freight, insurance . . . . . . . . . . .

Utility .... Connections and I . . . . . . . . . . . . . . . . . . . . . . electricity . - steam cooling & process water

.................. ..... ....................................

- --"-*"~-"IxI .....................

............... ................................... refrigeration .... ....... "."_-l""".. .......................

...............................................

I .........................................

.......... erdplumbing __._ ................... ....................... .......

sewerage I --,._ .............. .....*....._ll.. ................................

I vendor Installation ..II.""I._l.__I..". ..................... . . . . . . . . . . . . . . . . . . . . . . . .

... ......................................................................

...-....-...........-......-....I . . . . . . . . . . . . . . . . . . .

............................................

.... .................. taxes & insurance ........... ....... .- ...........

*ll_"_l .. ...

vendorlcontractor in-house

............ .....,..., ........................

..,.--...ll_...,.,.I.. . ...... ..

Materials .......................... "- .... ...............

..................................................................................

..I .................

..........................................

......................................

..........................................................................

-. .._ll.-_.ll--.-......--..-. ............................. Site ll_l_ preparation l-*-" ~

demolition, clearing etc disposal of old equipment, rubbish

.........".."..".".....I walkwys, ... ".,l roads, and fencing .................. . . . .

.

Engineering/Contractor ... -. ....... ........ (in-house & ext) ^ * plannin8 I ..........

ineering .."ll I *.

curement ..... consultants - ...... design

drafting -. 'accounting supervision

Contingency ...................

Permitting .__^-_I_-" - Fees ,.,--.... "l__" & In-House Staff [nitial Charge For Catalysts And Zhemicals

.........................................................

....... ....

....................... -. ........................

. . . . ....... ........

..... . . . . . . . ,,.x . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

..I" . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

.... . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

................. . . ..... *_ .. ....

"-.l.._.. ............

~ .--.__^_.Ix..I. ...... ... ".___ .............. .I..

,.I .. ..-"I ....................... ." ............................. Working Capital (raw materials, inventory, nateriaIs/sup$ies) "..I* ....... ,"

3alvage Value ................................................

* This list is adapted from material published by the Tellus Institute. Many of these costs mav or mav not be capitalized, depending upon the judgment of a firm's financial staff,

23

EXHIBIT 2-3

MODEL FOR CALCULATING INCREMENTAL AFTJCR-TAX CASH FLOWS* (For one period for option of purchase of new equipment

with resulting cost savings)

ASSUMPTIONS TERMINOLOGY 1. Option does not change revenue 2. Purchase new capital equipment 3. Do not sell old capital equipment

EBIT: Earnings before interest & taxes NI: Net Income T: Tax

- Baseline Expenses t- = Baseline EBIT

- Baseline Taxes =

- (T x Baseline EBIT)

= Baseline NI = (1-T) x Baseline EBIT

+ Baseline Depreciation

= (1-T) x Baseline EBIT + Baseline Depreciation

OPTION + Revenues - Baseline Depreciation - New- Depreciation (induced by purchase of new capital equipment) - New Expenses (assume these are lower than Baseline)

= New EBIT

- New Taxes =

- (T x New EBIT)

= New NI = (I-T) New EBIT

+ Baseline Depreciation + New Depreciation

= (1-T) new EBIT + Baseline Depreciation + New Depreciation

OPTION - BASELINE 0 - New Depreciation

+ Baseline Expense 1 - New Expenses = Savings

- T x (New EBIT - Baseline E B I T = - T x (Savings- New Depreciation)

=(I-T) x (NewEBIT- Baseline EBIT = (I-T) (Savings -New Dep)

+ New Depreciation

+ (T x New Depreciation)

* This calculation of cash flow does not deduct the interest expense associated with financing because we assume that the weighted average cost of capital will be used to discount these cash flows.

24

EXHIBIT 2-4

EXAMPLES OF SOURCES OF COST INFORMATION

The following table provides examples of various environmental cost activities (Activity), the way those activities might be defined for determining frequency or volume (Cost Driver); the information needed to calculate the costs of the activities (Measurement), and the sources of information about the activities (Source).

ACTIVITY COST DRIVER MEASUREMENT . S O U R C E ...... Spill/Leak Incident Number of Spills Labor Hours ngineer Intervie Reporting Number . of ll____l__ Incidents ... $/week . ........... Monitoring Number of Toxics Labor Hours Engineer Interview

Manifesting Number of Shipments Labor rvi

_.__x -_ll --ll-ll_l_ll. _" .I __..---_" I _-

--..I ..........................

Number of Processes $/week __lll_ll.-lll...ll*~..,~.,,.,...~-.---~-.,...~. using Toxics .. . . ....

R-~g-h~ .................................................................................................................................................................

$/week Manifesting Records ... $/shipment or $/drum

Number of Sessions , Labor Hours

Shipped Off-Site $/week

Engineer Interview Training (in-house) Labeling Engineer 1 nterview

............... Engineering Records . -. ..... - .......................

~~

$/drum ._

S Labor Hours .........................

Number of Gallons or $/week -_-I_ 11111-"1 Lbs.. Discharged fees($/chemical or/ Maintenance & Number of Machines Labor Hours Repair (Old Equipmt) $/week

Il"l-,.II.."IxI." I **"_ ^- II___.,_.,__ ........

spare partsiequipment $/item

I_II. I. ....x..I.".-..*..... ................ ............................... . . . . . . . . . . . . Maintenance (new Number of Machines Labor Hours equipment) $/week

Solvent Disoosal Number of Drums rum or Ilb

spare partdequipment $/item

-.---Ix*",-_.l__I1.. ___I__-.-_.-

........................................ Engineer Interview Accounting Records

Machine Manufcturer Vendor Outside Repair Shop

Machine Manurciurer Vendor Engineer Interview

Accounting Records

............

....... . Engineerinlg Records

TURA Fees Number of chemical/category TURA Reprting Forn Engineering Records

$/employee Engineering Records Employees Trained $/session Accounting Records Number of Sessions

Protective Equipment Number of employee Engineering Records Employees $/Sq Ft. Accounting Records

..*._-.**...*..__....*.................*..I ..........xx.._l_l.... ...... ......................... .~-/.. .............................................................. ............ .........

......................................................................................................................

.lllx _. .. ......*..I.......I. I. .................. . ~ / . . .............. . . . . . . . . . . . . . . . . .

25

Section 3 - MEASURES OF PROFITABILITY

After the relevant costs and savings have been identified and translated into cash flows, the information can be analyzed to determine the potential economic value a pollution prevention project might add to a business There are four common methods - measures of profitability - for performing the analysis Payback Period, Accounting Rate of Return (ROR), Net Present Value (NPV), and Internal Rate of Return (IRR) The following section demonstrates these methods, explains the interpretation of their results and discusses their appropriate uses, advantages and limitations As a general rule Net Present Value and Internal Rate of Return are superior to Payback and Accounting ROR, due principally to the consideration of the time value of money, a concept discussed later in this section Because companies can employ any of the four methods (with variations), however, it is important that P2 practitioners be familiar with their use and interpretation This section will demonstrate each method using the cash flow information from the Wrayburn Jewelry example seen in the previous sections1 It is important to keep in mind that while financial analysis is an intrinsic aspect of the assessment of pollution prevention projects, the results must be considered in conjunction with potential positive and negative qualitative impacts, which are discussed in Section 4

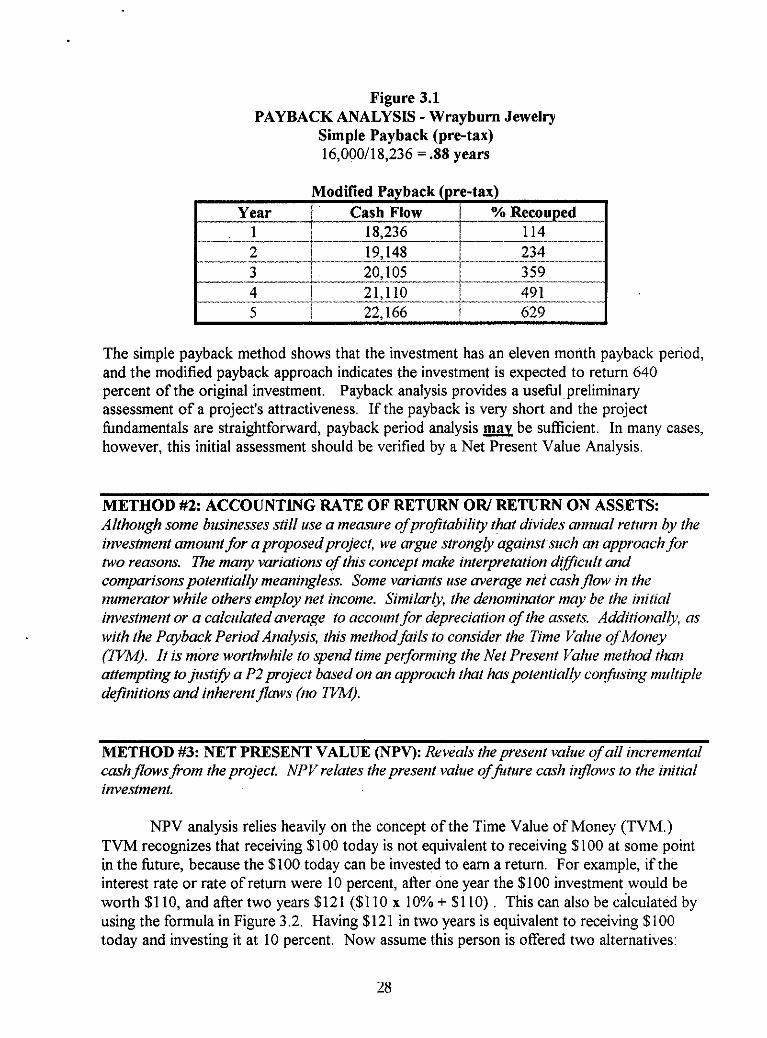

METHOD #1: PAYBACK PERIOD ANALYSIS: Reveals the amount of t h e needed for an investment to return the initial capital expenditures.

Payback period analysis is the simplest of the four financial analysis methods. It measures how long a project will take to return its original investment and ranks projects according to the length of the period: the shorter the payback period, the more attractive the project. The calculation to determine the payback period is more intuitive than formulaic; and it changes depending on the nature of the cash flows:

If annual cash flows are equal, the initial investment amount is divided by the annual cash flow. If the first year cash flow is greater than the initial investment, the initial investment amount is divided by the first year cash flow. If cash flows vary, and the initial investment is greater than the first year cash flow, succeeding years' cash flows are added incrementally until they equal the initial investment amount.

Payback period analysis has two drawbacks: it ignores the time value of money, and it ignores cash flows that occur after the initial investment has been recouped. A chart that tracks the percentage payback of all the cash flows over the life of the project offers one response to the latter objection. This refinement preserves the simplicity of the payback method yet increases its usefulness. Figure 3 . 1 shows both the simple and the modified payback period methods.

A synopsis of Wraybnrn Jewelry can be found on page 4 of Section 1. and the.full case with Exhibits is included as Appendix B.

27

Figure 3.1 PAYBACK ANALYSIS - Wrayburn Jewelry

Simple Payback (pre-tax) 16,000/18,236 = .88 years

The simple payback method shows that the investment has an eleven month payback period, and the modified payback approach indicates the investment is expected to return 640 percent of the original investment. Payback analysis provides a useful preliminary assessment of a project's attractiveness. If the payback is very short and the project fundamentals are straightforward, payback period analysis mav be sufficient. In many cases, however, this initial assessment should be verified by a Net Present Value Analysis.

METHOD #2: ACCOUNTING RATE OF RETURN OR/ RETURN ON ASSETS: Although some businesses still use a measure ofprofitability that divides annual return by the investment amount for a proposed project, we argue strongly against such an approach for two reasons. The many variations of this concept make interpretation dij$cult and comparisons potentially meaningless. Some variants use average net cash flow in the numerator while others employ net income. Similarly? the denominator may be the initial investment or a calculated average to account for depreciation of the assets. Additionally, os with the Payback Period Analysis, this method fails to consider the Time Value of Money (W). It is more worthwhile to spend time performing the Net Present Value method than attempting to justih a P2 project based on an approach that has potentially confusing multiple definitions and inherent flaws (no m).

~

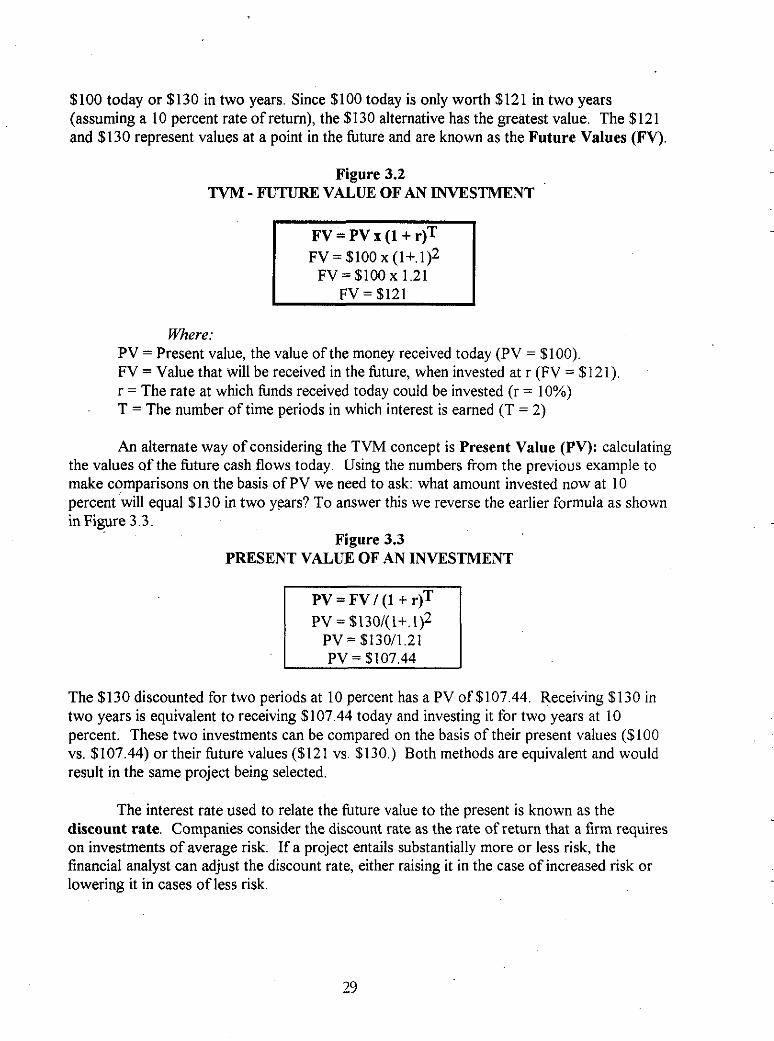

METHOD #3: NET PRESENT VALUE (NPV): Reveals the present value of all incremental cashflowsfrom the project. NPV relates the present value offture cash iilflows to the initial investment.

NPV analysis relies heavily on the concept of the Time Value of Money (TVM.) -

TVM recognizes that receiving $100 today is not equivalent to receiving $100 at some point in the future, because the $100 today can be invested to earn a return For example, if the interest rate or rate of return were 10 percent, after one year the $100 investment would be worth $1 10, and after two years $121 ($1 10 x 10% + $1 10) This can also be calculated by using the formula in Figure 3 2 Having $121 in two years is equivalent to receiving $100 today and investing it at 10 percent Now assume this person is offered two alternatives

__

28

$100 today or $130 in two years. Since $100 today is only worth $121 in two years (assuming a 10 percent rate of return), the $130 alternative has the greatest value. The $121 and $130 represent values at a point in the future and are known as the Future Values (FV).

Figure 3.2 TVM - "I'URJC VALUE OF AN INVESTMENT

FV = $100 x 1.21

Where: PV = Present value, the value of the money received today (PV = $100). FV = Value that will be received in the future, when invested at r (FV = $121). r = The rate at which funds received today could be invested (r = 10%) T = The number of time periods in which interest is earned (T = 2)

An alternate way of considering the TVM concept is Present Value (PV): calculating the values of the future cash flows today. Using the numbers from the previous example to make comparisons on the basis of PV we need to ask: what amount invested now at 10 percent will equal $130 in two years? To answer this we reverse the earlier formula as shown in Figure 3.3.

Figure 3.3 PRESENT VALUE OF AN INVESTMENT

PV = FV / ( I + r)T PV = $130/(1+.1)2

P V = $130/1.21

The $130 discounted for two periods at 10 percent has a PV of $107 44. Receiving $130 in two years is equivalent to receiving $107.44 today and investing it for two years at 10 percent. These two investments can be compared on the basis of their present values ($100 vs. $107.44) or their future values ($121 vs $130.) Both methods are equivalent and would result in the same project being selected.

The interest rate used to relate the future value to the present is known as the discount rate. Companies consider the discount rate as the rate of return that a firm requires on investments of average risk. If a project entails substantially more or less risk, the financial analyst can adjust the discount rate, either raising it in the case of increased risk or lowering it in cases of less risk.

29

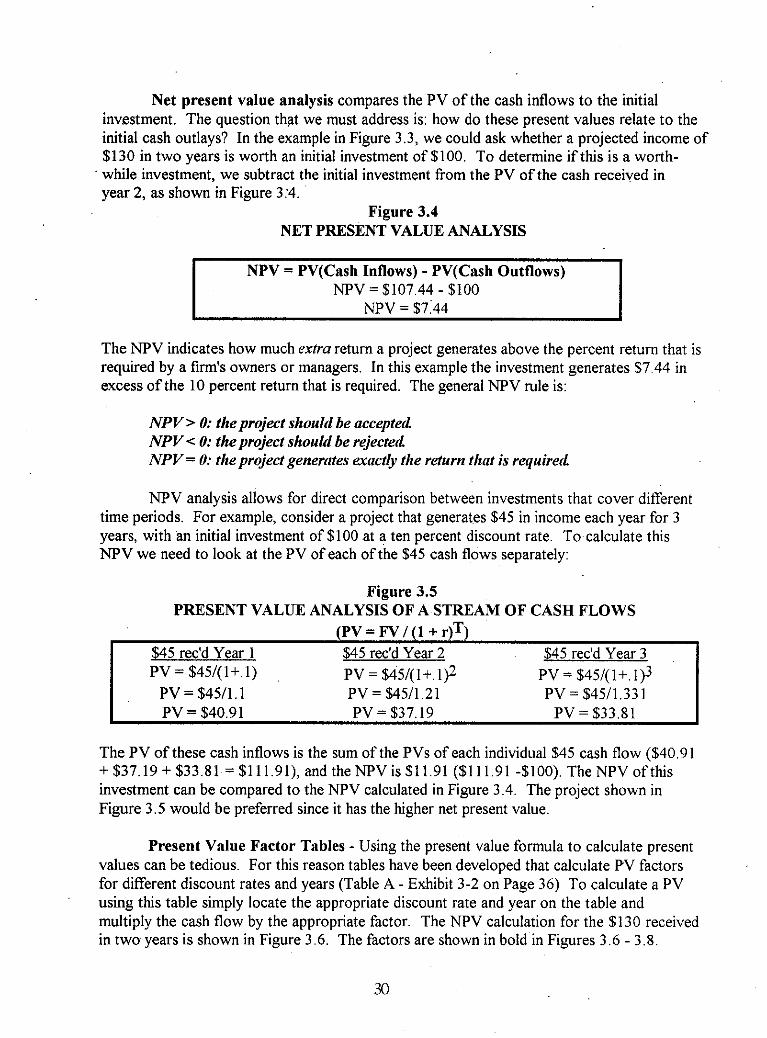

Net present value analysis compares the PV of the cash inflows to the initial investment. The question that we must address is: how do these present values relate to the initial cash outlays? In the example in Figure 3.3, we could ask whether a projected income of $130 in two years is worth an initial investment of $100. To determine if this is a worth-

year 2, as shown in Figure 3:4.

__

' while investment, we subtract the initial investment from the PV of the cash received in __

Figure 3.4 NET PRESENT VALUE ANALYSIS

NPV = PV(Cash Inflows) - PV(Cash Outflows) NPV=$107.44 - $100

NPV = $7'44

The NPV indicates how much extra return a project generates above the percent return that is required by a firm's owners or managers. In this example the investment generates $7.44 in excess of the 10 percent return that is required. The general NPV rule is:

NPV =. 0: the project should be nccepterl NPV < 0: the project should be rejectell NPV = 0: the project generates exactly the return thnt is requirerl

NPV analysis allows for direct comparison between investments that cover different time periods. For example, consider a project that generates $45 in income each year for 3 years, with an initial investment of $100 at a ten percent discount rate. To calculate this NPV we need to look at the PV of each of the $45 cash flows separately:

Figure 3.5 PRESENT VALUE ANALYSIS OF A STREAM OF CASH FLOWS

(PV = FV / (I + r)T) $45 redd Year 2 PV = $45/(1+ 1)2 PV = $45/1 21

$45 redd Year 1 PV = $45/(1+ 1)

PV = $45/1 1

$45 rec'd Year 3 PV = $45/(1+ l)3 PV = $4511 33 1

I PV = $33.81 PV = $40.91 PV= $37.19

The PV of these cash inflows is the sum of the PVs of each individual $45 cash flow ($40.91 + $37.19 + $33.8 1 = $1 1 1.91), and the NPV is $1 1.91 ($1 1 1.9 1 -$loo). The NPV of this investment can be compared to the NPV calculated in Figure 3.4. The project shown in Figure 3.5 would be preferred since it has the higher net present value. -

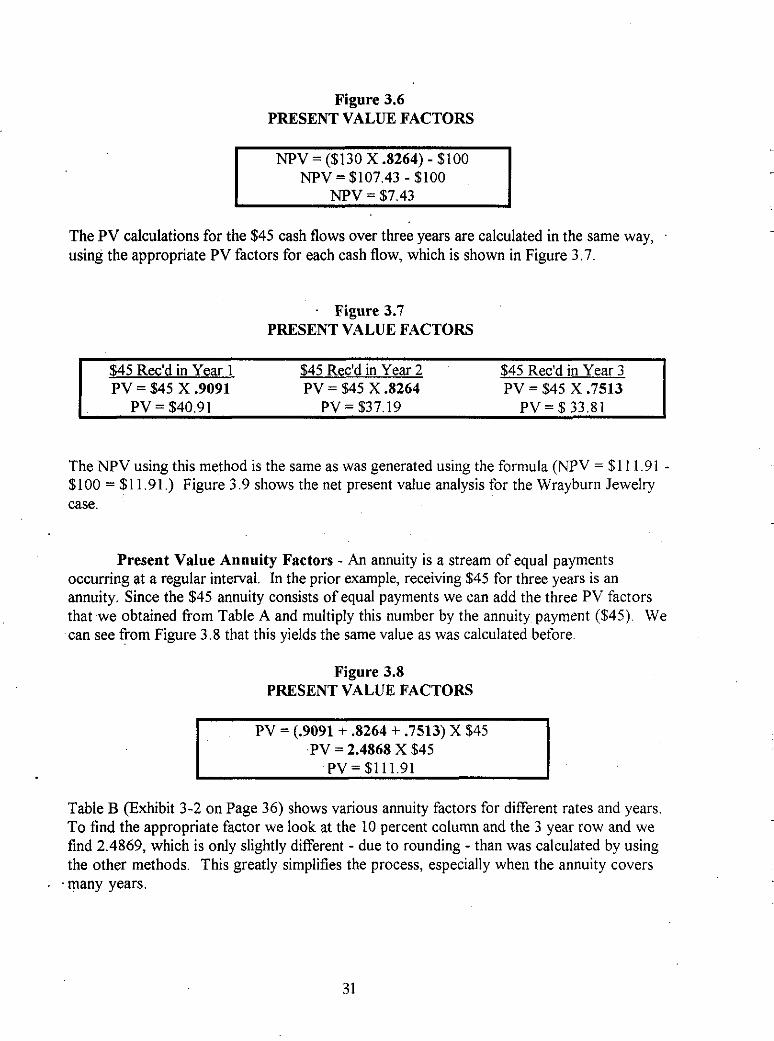

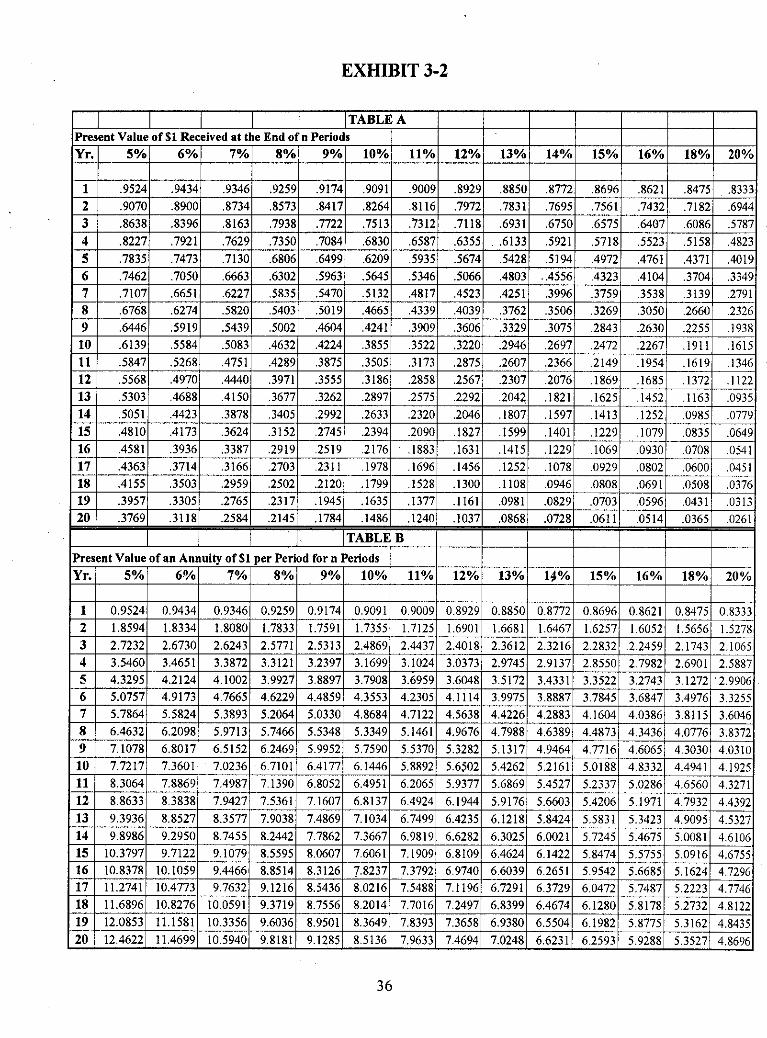

Present Value Factor Tables - Using the present value formula to calculate present values can be tedious. For this reason tables have been developed that calculate PV factors for different discount rates and years (Table A - Exhibit 3-2 on Page 36) To calculate a PV using this table simply locate the appropriate discount rate and year on the table and multiply the cash flow by the appropriate factor. The NPV calculation for the $130 received in two years is shown in Figure 3.6. The factors are shown in bold in Figures 3.6 - 3.8.

-

Figure 3.6 PRESENT VALUE FACTORS

The PV calculations for the $45 cash flows over three years are calculated in the same way, . using the appropriate PV factors for each cash flow, which is shown in Figure 3.7.

. Figure 3.7 PRESENT VALUE FACTORS

$45 Rec'd in Year 1 PV = $45 X .9091

$45 Rec'd in Year 2 PV = $45 X .8264

$45 Rec'd in Year 3 PV = $45 X .7513

PV = $40.91 PV= $37.19 PV=$33 .81

The NPV using this method is the same as was generated using the formula (NPV = $ 1 11 91 - $100 = $1 1.91.) Figure 3.9 shows the net present value analysis for the Wrayburn Jewelry case.

Present Value Annuity Factors - An annuity is a stream of equal payments occurring at a regular interval. In the prior example, receiving $45 for three years is an annuity. Since the $45 annuity consists of equal payments we can add the three PV factors that we obtained from Table A and multiply this number by the annuity payment ($45) We can see from Figure 3 8 that this yields the same value as was calculated before

Figure 3.8 PRESENT VALUE FACTORS

I PV = (.9091+ ,8264 + .7513) X $45 I -PV = 2.4868 X $45

PV=$111.91

Table B (Exhibit 3-2 on Page 36) shows various annuity factors for different rates and years. To find the appropriate factor we look at the 10 percent column and the 3 year row and we find 2.4869, which is only slightly different - due to rounding - than was calculated by using the other methods. This greatly simplifies the process, especially when the annuity covers

.many years.

31

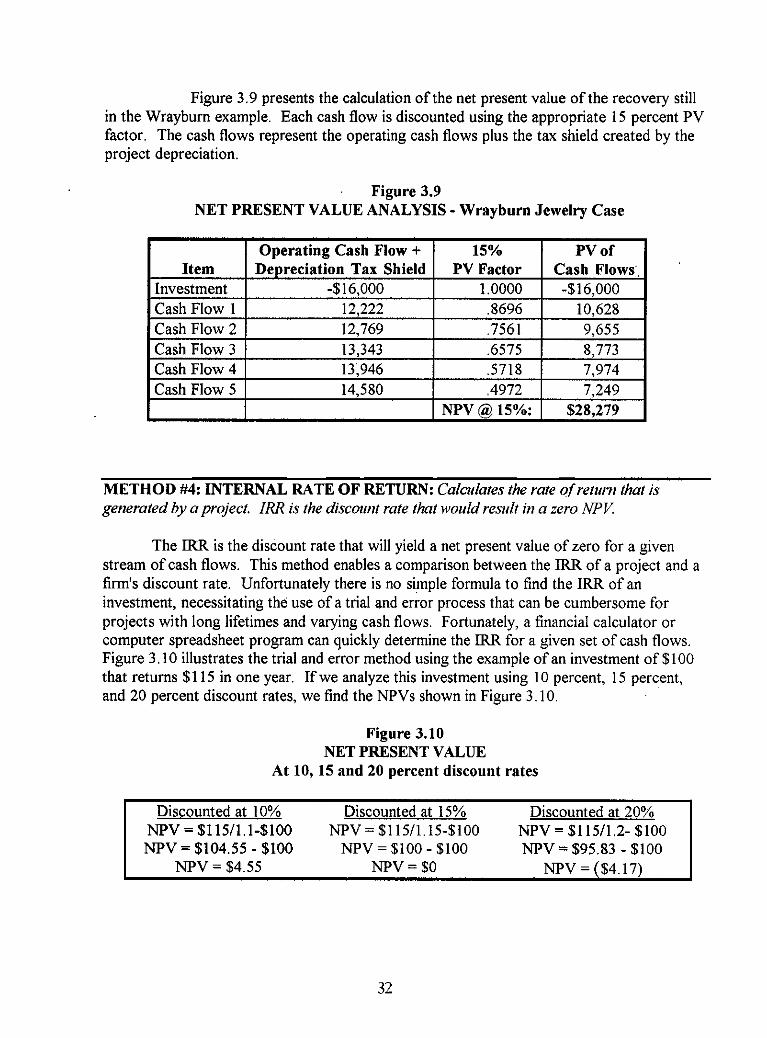

Figure 3.9 presents the calculation of the net present value of the recovery still in the Wrayburn example. Each cash flow is discounted using the appropriate 15 percent PV factor. The cash flows represent the operating cash flows plus the tax shield created by the project depreciation.

Discounted at 10% Discounted at 15% Discounted at 20% NPV = $1 15/1. 15-$100 NPV = $1 lY1.1-$100 NPV= $115/1.2- $100

Figure 3.9 NET PRESENT VALUE ANALYSIS - Wrnyburn Jewelry Case

-

METHOD #4: INTERNAL RATE OF RETURN: C’a/cti/a/rs ihe role ofrertu7t /ha/ 1,s

generated by a project. IRR is the discount rate that would result in a zero NPK

The IRR is the discount rate that will yield a net present value of zero for a given stream of cash flows. This method enables a comparison between the IRR of a project and a firm’s discount rate. Unfortunately there is no simple formula to find the IRR of an investment, necessitating the use of a trial and error process that can be cumbersome for projects with long lifetimes and varying cash flows. Fortunately, a financial calculator or computer spreadsheet program can quickly determine the IRR for a given set of cash flows. Figure 3.10 illustrates the trial and error method using the example of an investment of $100 that returns $1 15 in one year. If we analyze this investment using 10 percent, 15 percent, and 20 percent discount rates, we find the NPVs shown in Figure 3.10.

Figure 3.10 NET PRESENT VALUE

At 10, 15 and 20 percent discount rates

NPV=$104.55 - $100 Npv = $100 - $100 NPV = $4.55 NPV = $0 NPV = ($4.17)

NPV = $95 83 - $100

__

32

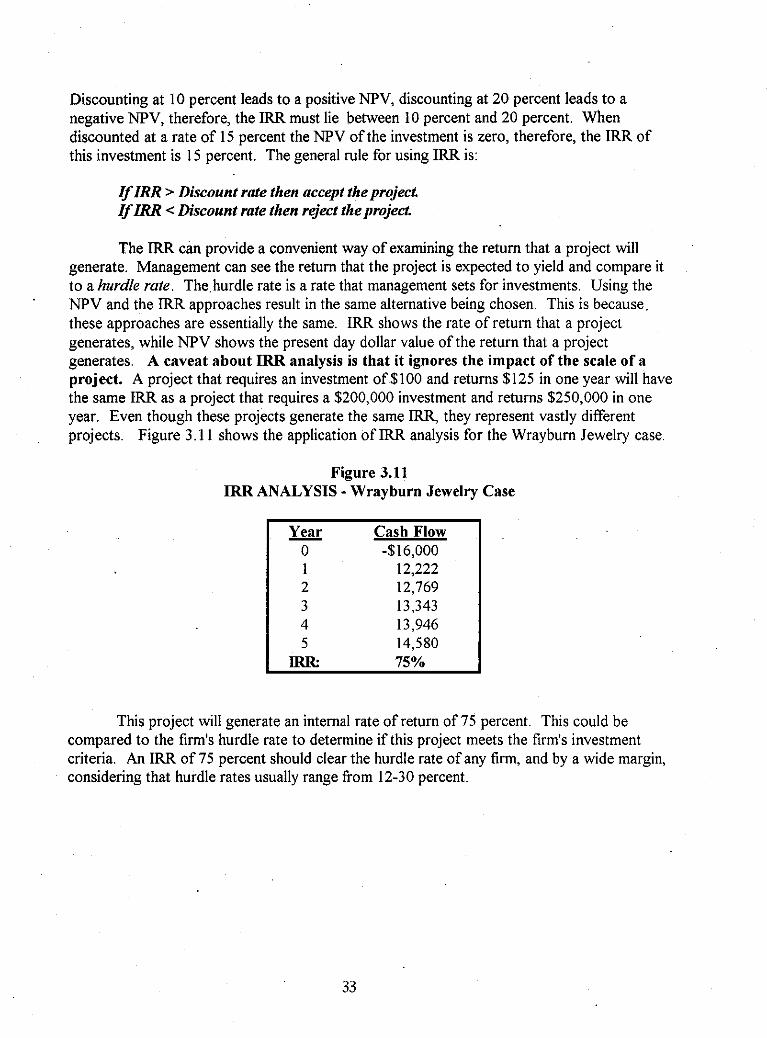

Discounting at 10 percent leads to a positive NPV, discounting at 20 percent leads to a negative NPV, therefore, the IRR must lie between 10 percent and 20 percent. When discounted at a rate of 15 percent the NPV of the investment is zero, therefore, the IRR of this investment is 15 percent. The general rule for using IRR is:

If IRR > Discount rate then accept the project. If IRR < Discount rate then reject theproject.

The IRR can provide a convenient way of examining the return that a project will generate. Management can see the return that the project is expected to yield and compare it to a hurdle rate. The,hurdle rate is a rate that management sets for investments. Using the NPV and the IRR approaches result in the same alternative being chosen. This is because. these approaches are essentially the same. IRR shows the rate of return that a project generates, while NPV shows the present day dollar value of the return that a project generates. A caveat about IRR analysis is that it ignores the impact of the scale of a project. A project that requires an investment of $100 and returns $125 in one year will have the same IRR as a project that requires a $200,000 investment and returns $250,000 in one year. Even though these projects generate the same IRR, they represent vastly different projects. Figure 3.1 1 shows the application of IRR analysis for the Wraybum Jewelry case.

'

Figure 3.11 IRR ANALYSIS - Wrayburn Jewelry Case

- Year Cash Flow 0 -$16,000 1 12,222 2 12,769 3 13,343 4 13,946 5 14,580

IRR: 75%

This project will generate an internal rate of return of 75 percent This could be compared to the firm's hurdle rate to determine if this project meets the firm's investment criteria. An IRR of 75 percent should clear the hurdle rate of any firm, and by a wide margin, considering that hurdle rates usually range from 12-30 percent.

33

INFLATION IN CAPITAL BUDGETING

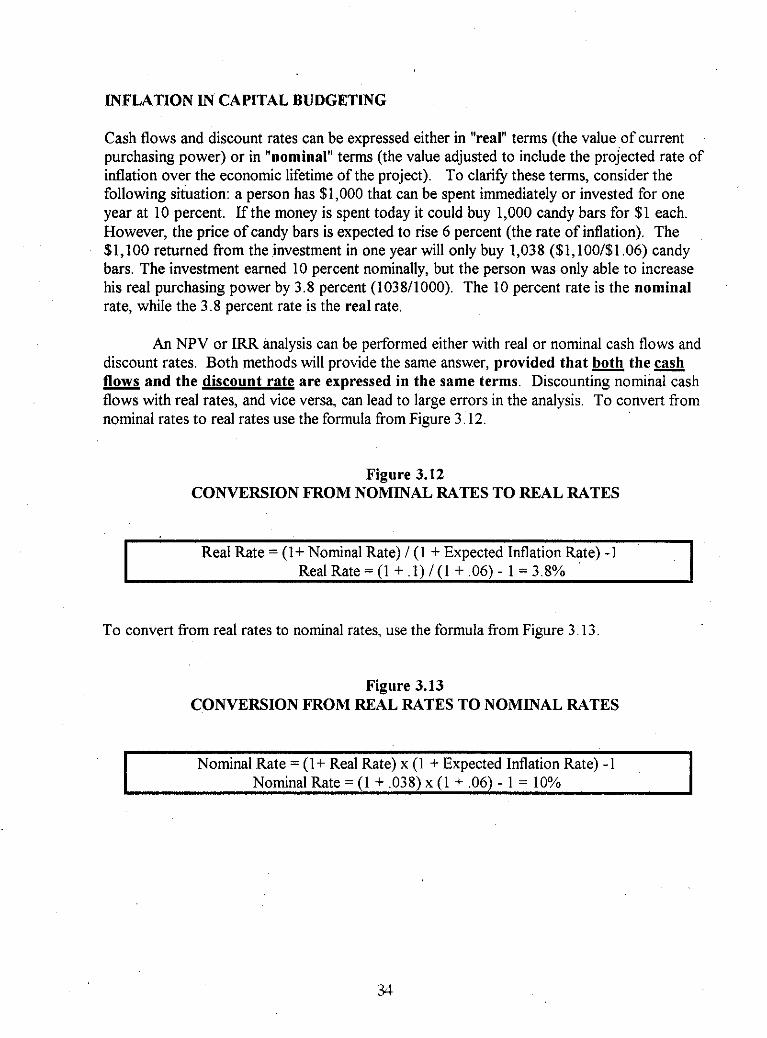

Cash flows and discount rates can be expressed either in "real" terms (the value of current purchasing power) or in "nominal" terms (the value adjusted to include the projected rate of inflation over the economic lifetime of the project). To clarify these terms, consider the following situation: a person has $1,000 that can be spent immediately or invested for one year at 10 percent. If the money is spent today it could buy 1,000 candy bars for $1 each. However, the price of candy bars is expected to rise 6 percent (the rate of inflation). The $1,100 returned from thelnvestment in one year will only buy 1,038 ($1,100/$1.06) candy bars. The investment earned 10 percent nominally, but the person was only able to increase his real purchasing power by 3.8 percent (1038/1000). The 10 percent rate is the nominal rate, while the 3.8 percent rate is the real rate.

~

~

__

An NPV or IRR analysis can be performed either with real or nominal cash flows and discount rates. Both methods will provide the same answer, provided that both the - flows and the discount rate are expressed in the same terms. Discounting nominal cash flows with real rates, and vice versa, can lead to large errors in the analysis. To convert from nominal rates to real rates use the formula from Figure 3.12.

Figure 3.12 CONVERSION FROM NOMINAL RATES TO REAL RATES