Embed Size (px)

Citation preview

Stormy Energy Futureand

Security Strategy for Asia

2016-9-9 Renewable Energy Institute

Former Executive Director, IEAPresident, the Sasakawa Peace FoundationNobuo TANAKA

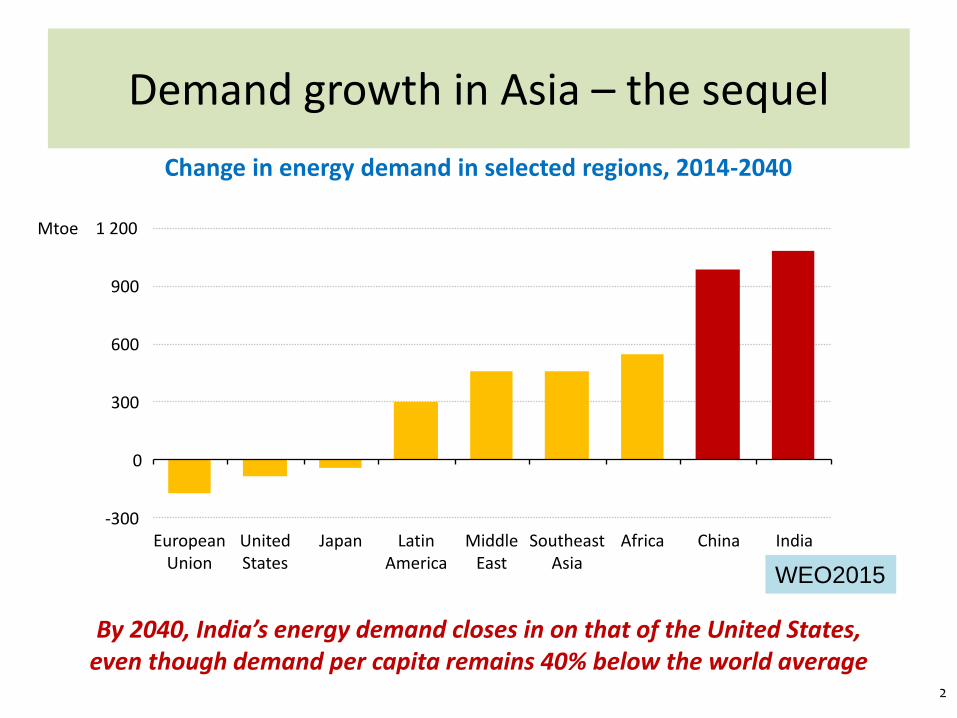

Mtoe

-300

0

300

600

900

1 200

Demand growth in Asia – the sequel

By 2040, India’s energy demand closes in on that of the United States, even though demand per capita remains 40% below the world average

EuropeanUnion

UnitedStates

Japan LatinAmerica

MiddleEast

SoutheastAsia

Africa China India

Change in energy demand in selected regions, 2014-2040

WEO2015

2

-5

+5

+10

+15

2020 2030 2040

Middle East

Brazil

CanadaUnited States

Net decline in output from other producers

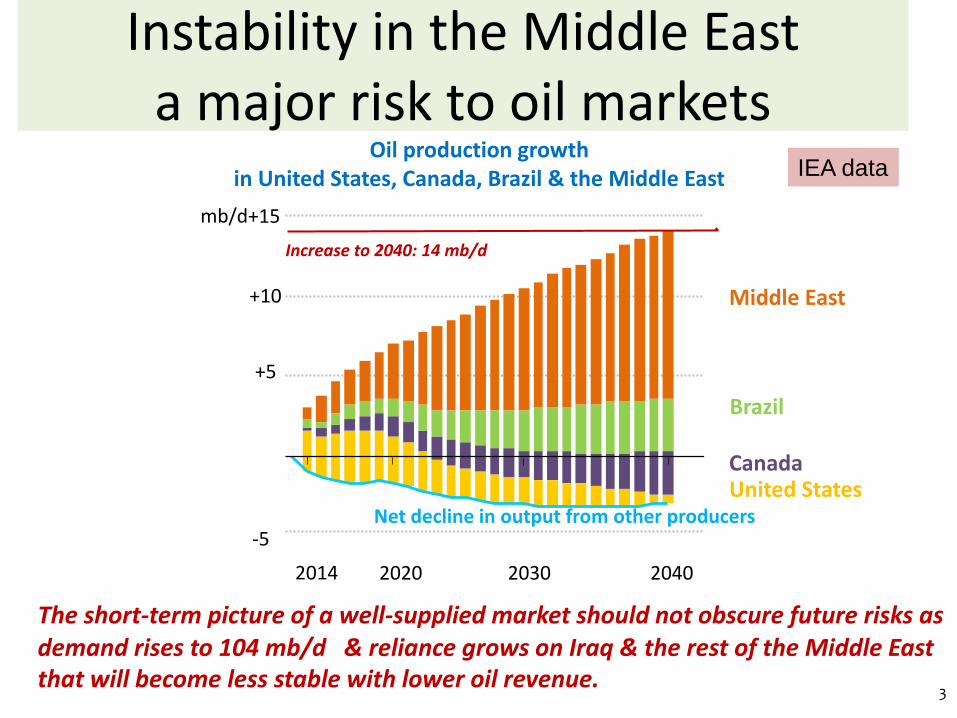

Oil production growthin United States, Canada, Brazil & the Middle East

2014

Increase to 2040: 14 mb/d

mb/d

Increase to 2040: 14 mb/d

IEA data

Instability in the Middle Easta major risk to oil markets

The short-term picture of a well-supplied market should not obscure future risks as demand rises to 104 mb/d & reliance grows on Iraq & the rest of the Middle Eastthat will become less stable with lower oil revenue.reliance grows on Iraq & the rest of the Middle East

3

IEA Data

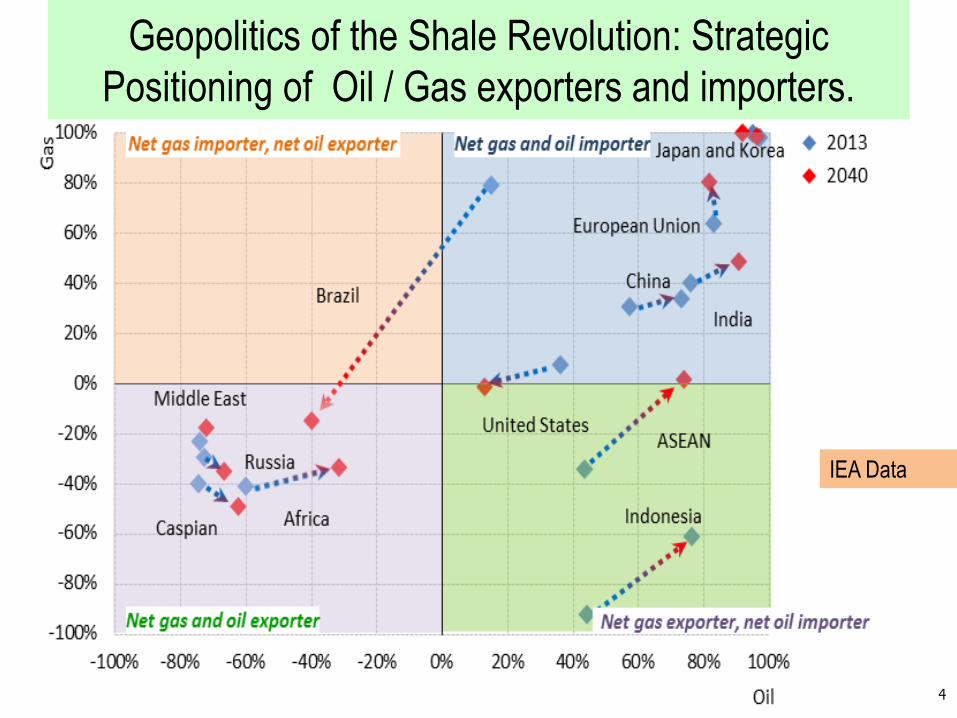

4

Geopolitics of the Shale Revolution: Strategic

Positioning of Oil / Gas exporters and importers.

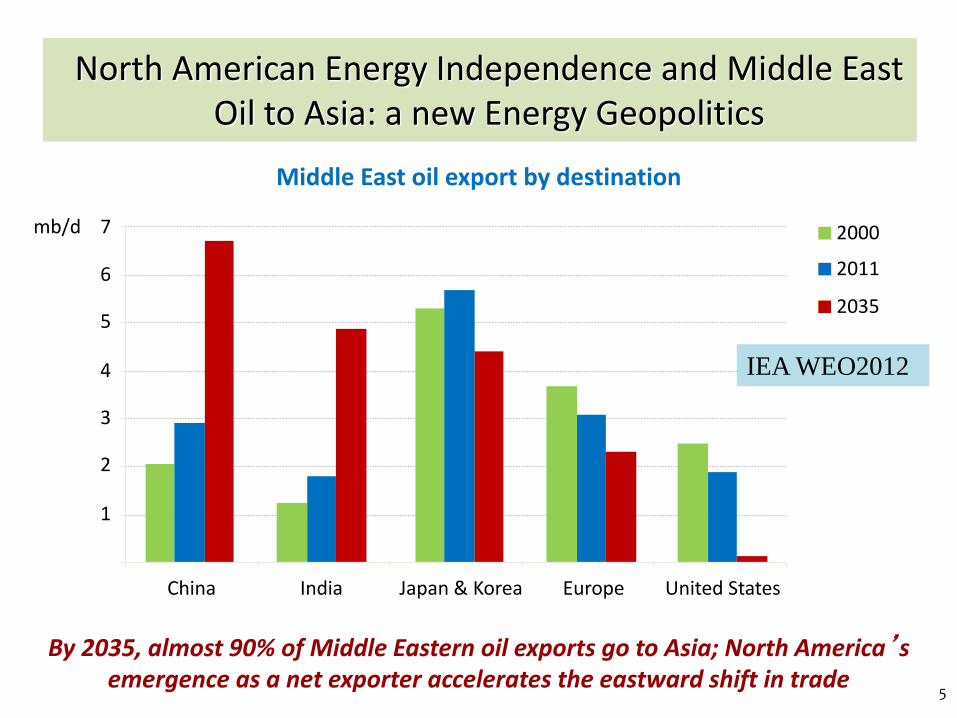

North American Energy Independence and Middle East Oil to Asia: a new Energy Geopolitics

Middle East oil export by destination

By 2035, almost 90% of Middle Eastern oil exports go to Asia; North America’s emergence as a net exporter accelerates the eastward shift in trade

7

United StatesJapan & Korea EuropeChina India

mb/d 2000

2011

2035

1

2

3

4

5

6

IEA WEO2012

5

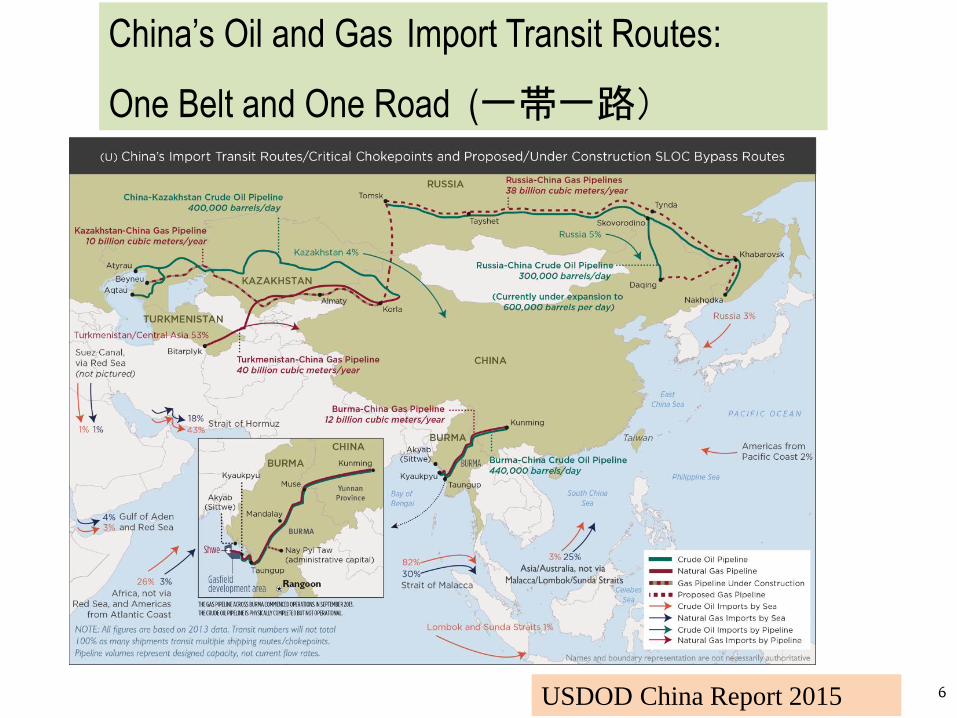

USDOD China Report 2015 6

China’s Oil and Gas Import Transit Routes:

One Belt and One Road (一帯一路)

Figure 2. China’s Import Transit Routes.

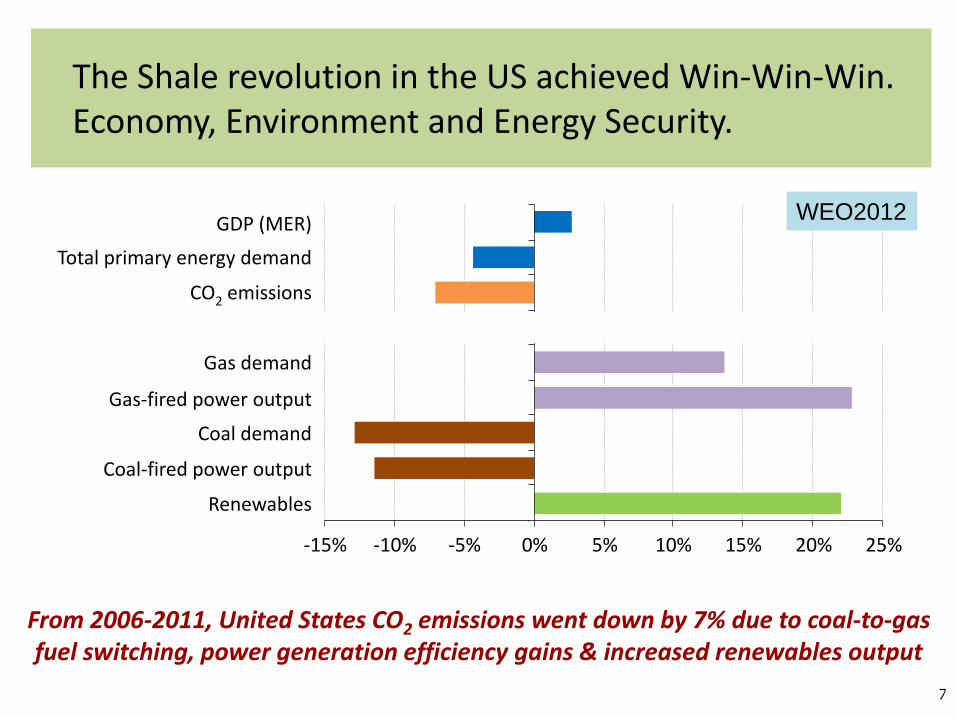

The Shale revolution in the US achieved Win-Win-Win. Economy, Environment and Energy Security.

-15% -10% -5% 0% 5% 10% 15% 20% 25%

Renewables

Coal-fired power output

Coal demand

Gas-fired power output

Gas demand

CO2 emissions

Total primary energy demand

GDP (MER)

From 2006-2011, United States CO2 emissions went down by 7% due to coal-to-gas fuel switching, power generation efficiency gains & increased renewables output

WEO2012

7

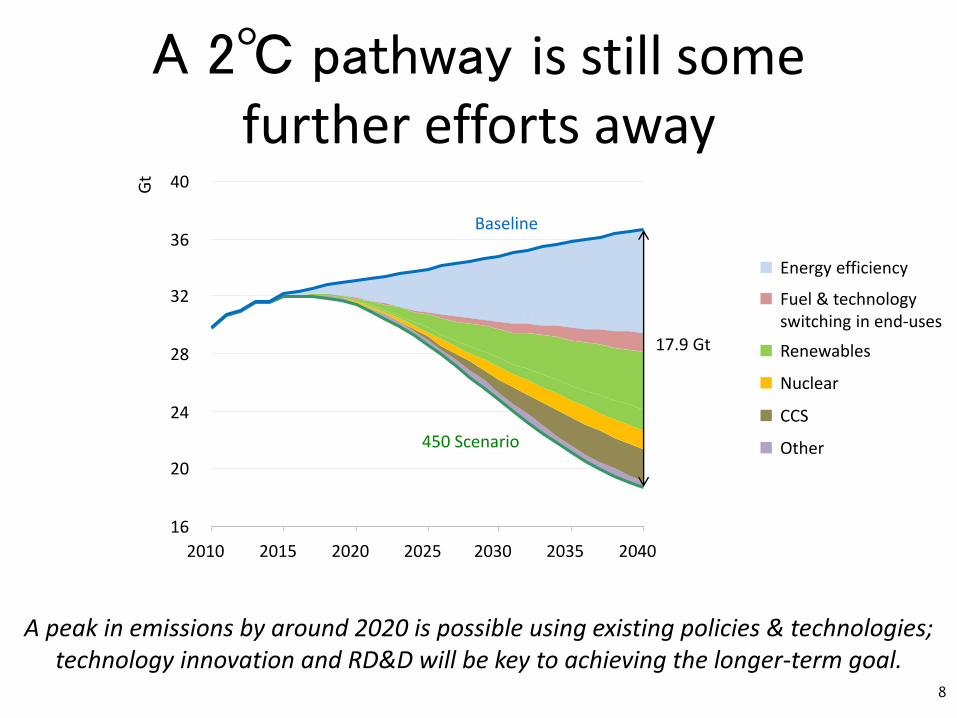

A 2℃ pathway is still some further efforts away

16

20

24

28

32

36

40

2010 2015 2020 2025 2030 2035 2040

Gt

Baseline

450 Scenario

17.9 Gt

A peak in emissions by around 2020 is possible using existing policies & technologies; technology innovation and RD&D will be key to achieving the longer-term goal.

Energy efficiency

Fuel & technology switching in end-uses

Renewables

Nuclear

CCS

Other

8

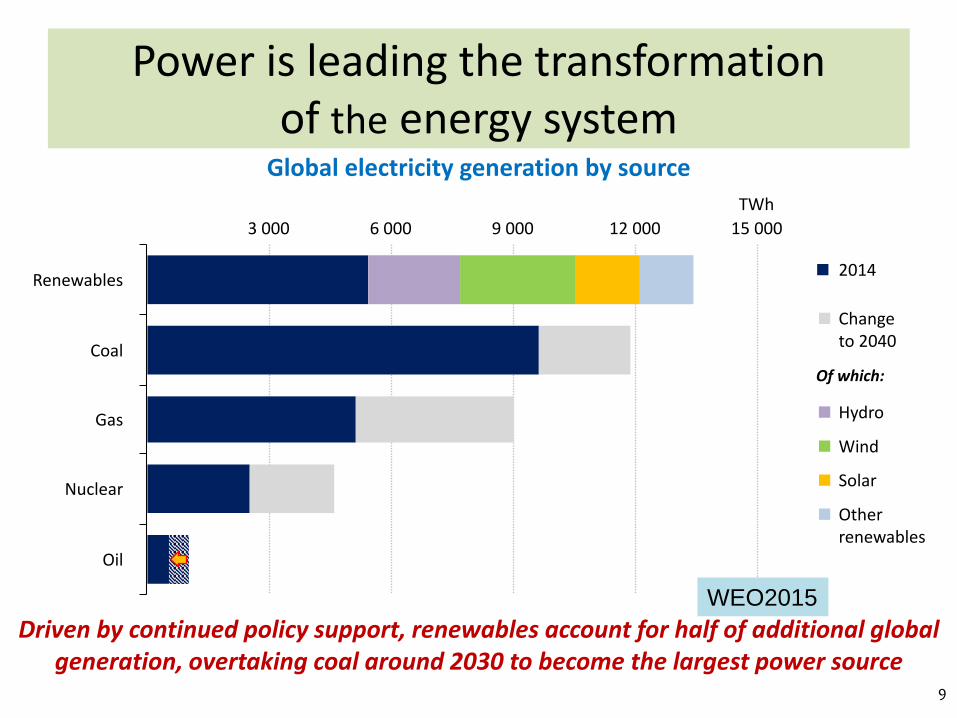

Power is leading the transformationof the energy system

Global electricity generation by source

Driven by continued policy support, renewables account for half of additional global generation, overtaking coal around 2030 to become the largest power source

3 000 12 000 15 000

TWh

Changeto 2040

2014Renewables

Coal

Gas

Nuclear

Oil

Hydro

Wind

Solar

Otherrenewables

Of which:

6 000 9 000

WEO2015

9

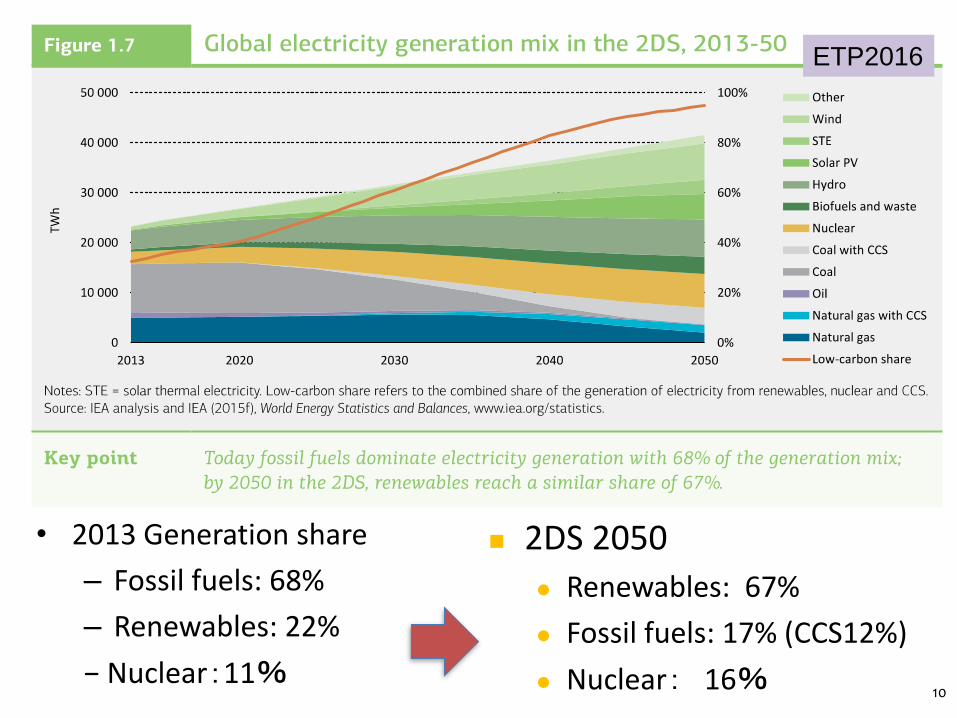

• 2013 Generation share

– Fossil fuels: 68%

– Renewables: 22%

− Nuclear:11%

2DS 2050

Renewables: 67%

Fossil fuels: 17% (CCS12%)

Nuclear: 16%

ETP2016

10

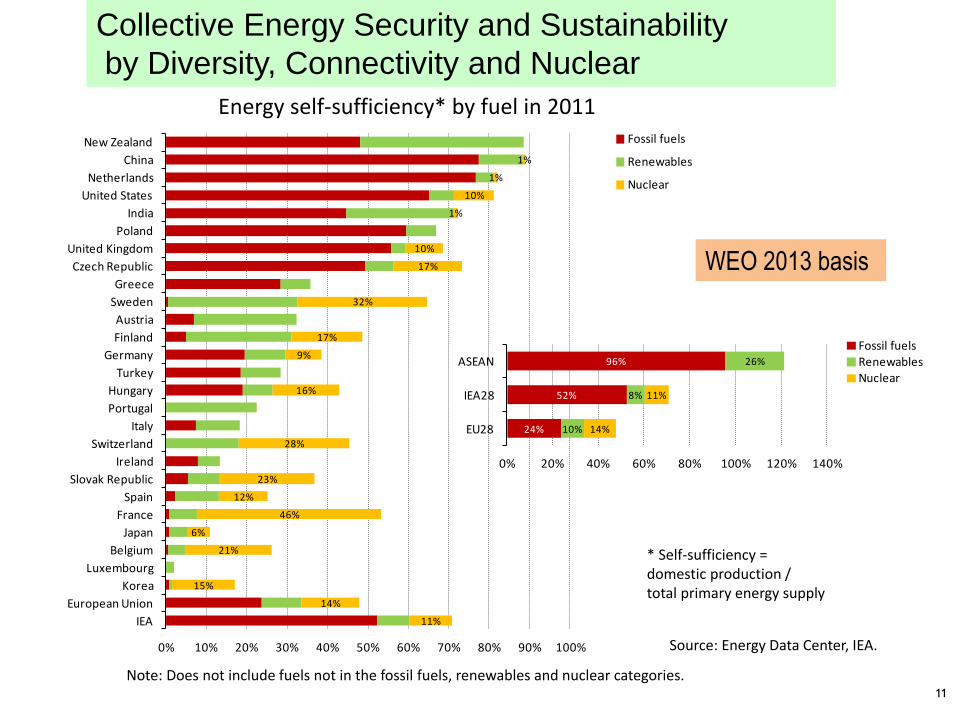

Energy self-sufficiency* by fuel in 2011

Source: Energy Data Center, IEA.

* Self-sufficiency =domestic production /total primary energy supply

Note: Does not include fuels not in the fossil fuels, renewables and nuclear categories.

11%

14%

15%

21%

6%

46%

12%

23%

28%

16%

9%

17%

32%

17%

10%

1%

10%

1%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

IEA

European Union

Korea

Luxembourg

Belgium

Japan

France

Spain

Slovak Republic

Ireland

Switzerland

Italy

Portugal

Hungary

Turkey

Germany

Finland

Austria

Sweden

Greece

Czech Republic

United Kingdom

Poland

India

United States

Netherlands

China

New Zealand Fossil fuels

Renewables

Nuclear

24%

52%

96%

10%

8%

26%

14%

11%

0% 20% 40% 60% 80% 100% 120% 140%

EU28

IEA28

ASEANFossil fuelsRenewablesNuclear

Collective Energy Security and Sustainability

by Diversity, Connectivity and Nuclear

WEO 2013 basis

11

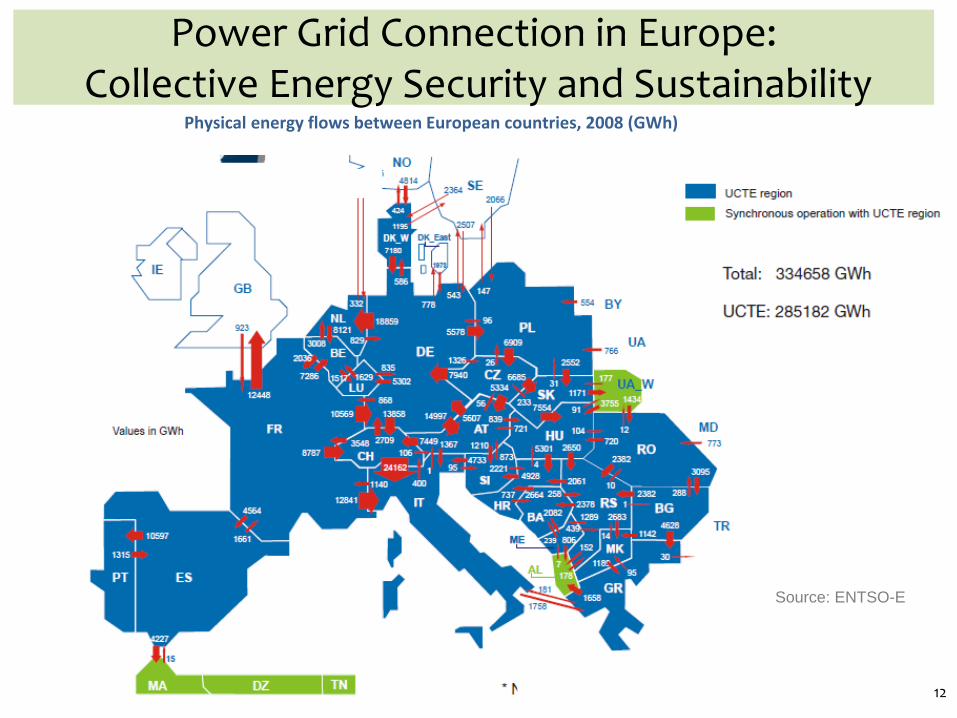

Power Grid Connection in Europe:Collective Energy Security and Sustainability

Physical energy flows between European countries, 2008 (GWh)

Source: ENTSO-E

12

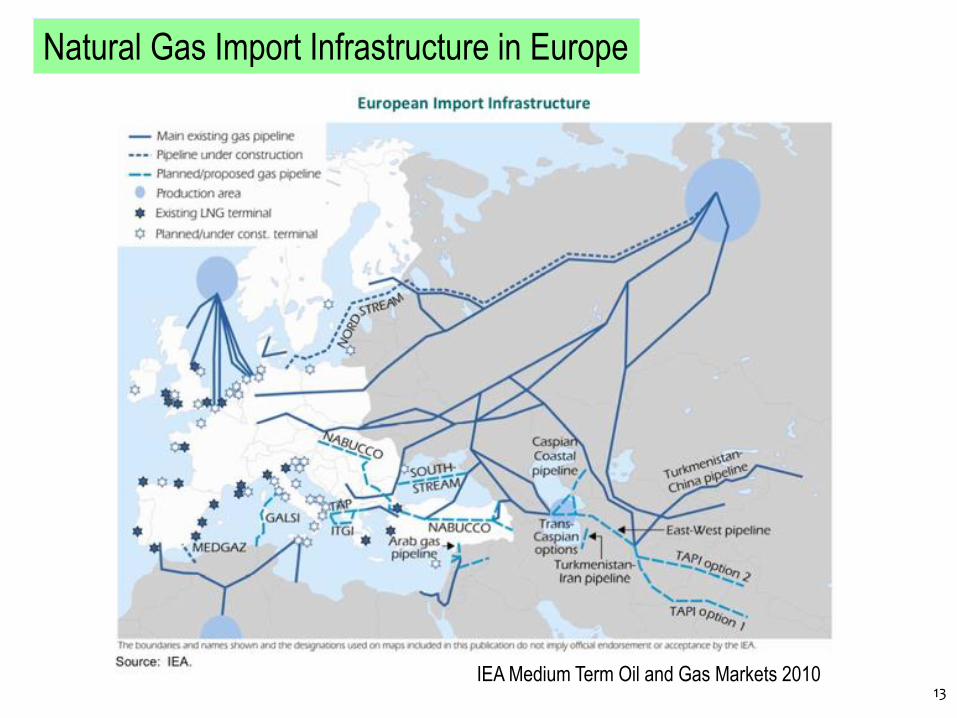

Natural Gas Import Infrastructure in Europe

IEA Medium Term Oil and Gas Markets 201013

Mid-Term Oil & Gas Market 2010, IEA

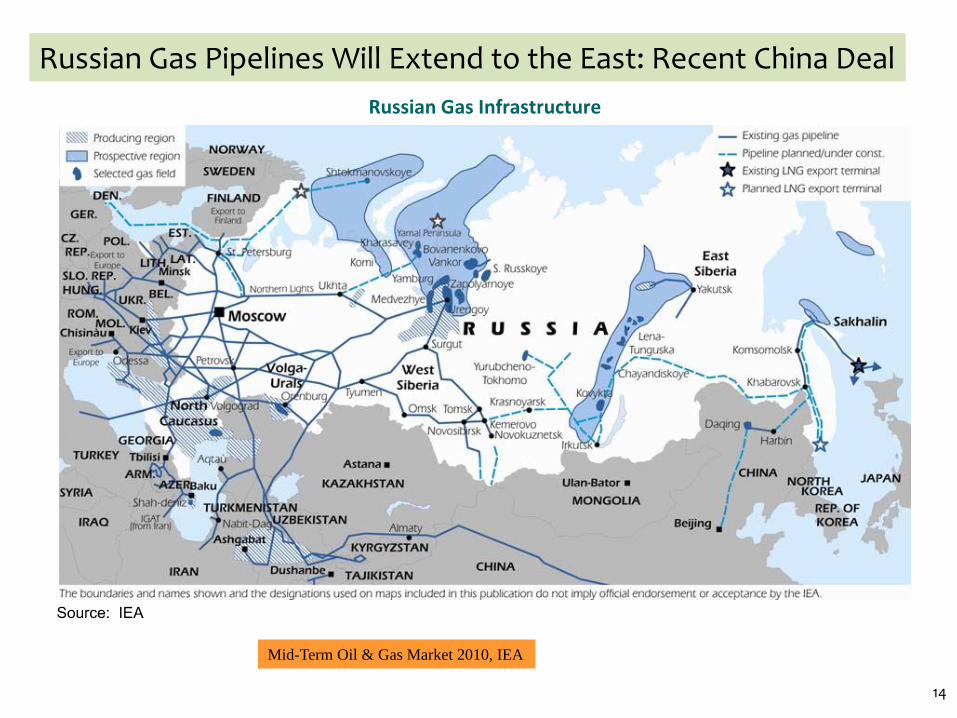

Russian Gas Pipelines Will Extend to the East: Recent China Deal

14

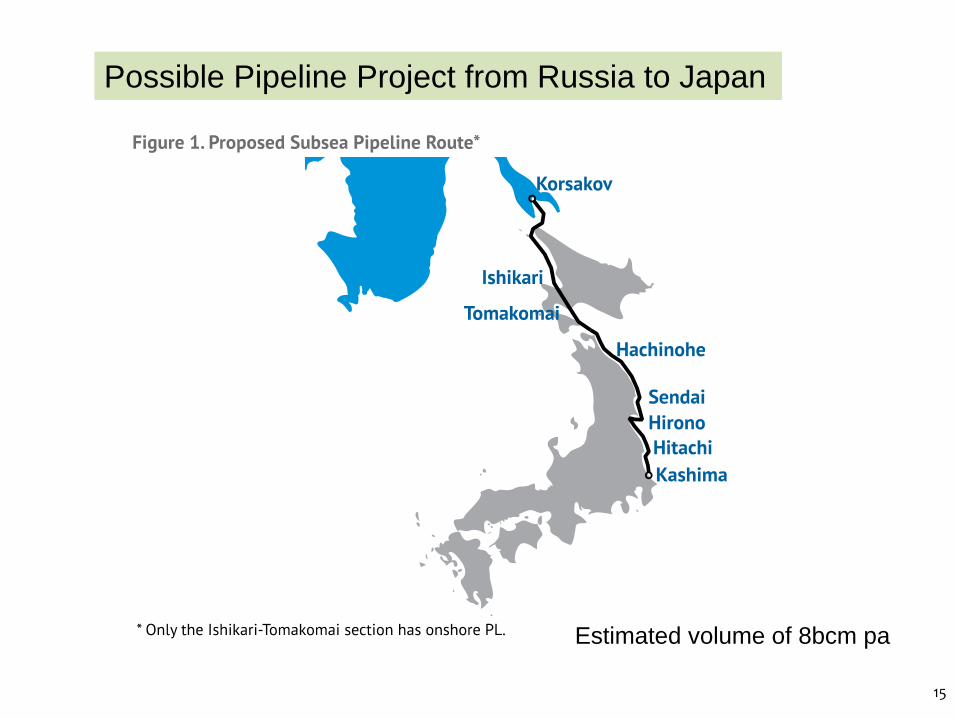

Possible Pipeline Project from Russia to Japan

Estimated volume of 8bcm pa

15

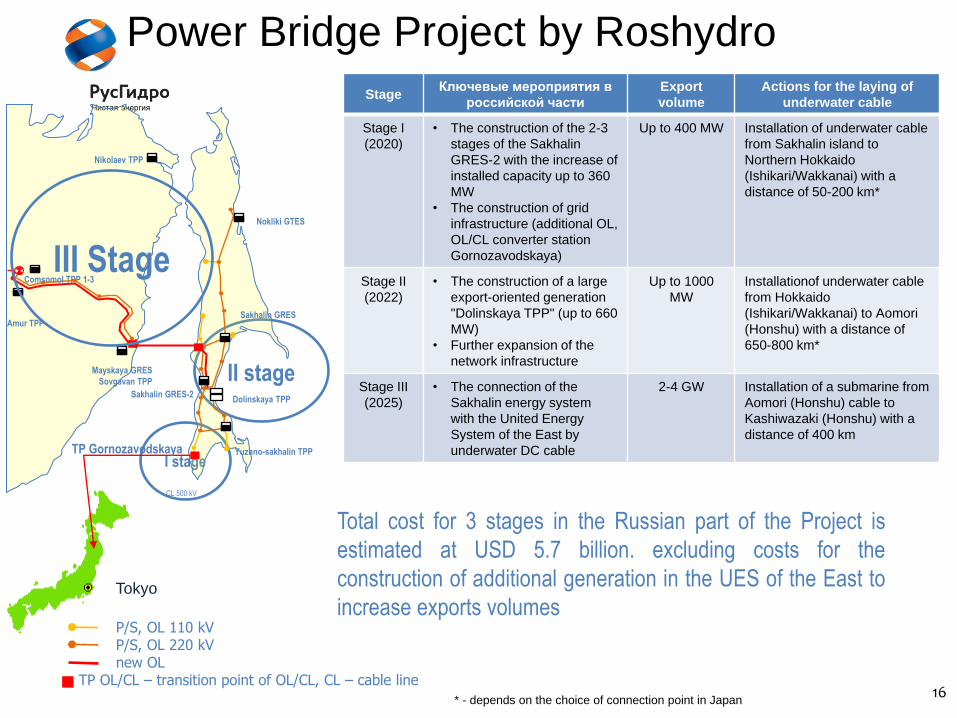

Чистая энергия

387

I stage

II stage

Sakhalin GRES

Nokliki GTES

Sakhalin GRES-2

Yuzhno-sakhalin TPP

Mayskaya GRES

Sovgavan TPP

Comsomol TPP 1-3

Amur TPP

Nikolaev TPP

CL 500 kV

III Stage

TP Gornozavodskaya

Dolinskaya TPP

Total cost for 3 stages in the Russian part of the Project is

estimated at USD 5.7 billion. excluding costs for the

construction of additional generation in the UES of the East to

increase exports volumesP/S, OL 110 kVP/S, OL 220 kVnew OL

TP OL/CL – transition point of OL/CL, CL – cable line

Tokyo

StageКлючевые мероприятия в

российской части

Export

volume

Actions for the laying of

underwater cable

Stage I

(2020)

• The construction of the 2-3

stages of the Sakhalin

GRES-2 with the increase of

installed capacity up to 360

MW

• The construction of grid

infrastructure (additional OL,

OL/CL converter station

Gornozavodskaya)

Up to 400 MW Installation of underwater cable

from Sakhalin island to

Northern Hokkaido

(Ishikari/Wakkanai) with a

distance of 50-200 km*

Stage II

(2022)

• The construction of a large

export-oriented generation

"Dolinskaya TPP" (up to 660

MW)

• Further expansion of the

network infrastructure

Up to 1000

MW

Installationof underwater cable

from Hokkaido

(Ishikari/Wakkanai) to Aomori

(Honshu) with a distance of

650-800 km*

Stage III

(2025)

• The connection of the

Sakhalin energy system

with the United Energy

System of the East by

underwater DC cable

2-4 GW Installation of a submarine from

Aomori (Honshu) cable to

Kashiwazaki (Honshu) with a

distance of 400 km

* - depends on the choice of connection point in Japan

Power Bridge Project by Roshydro

16

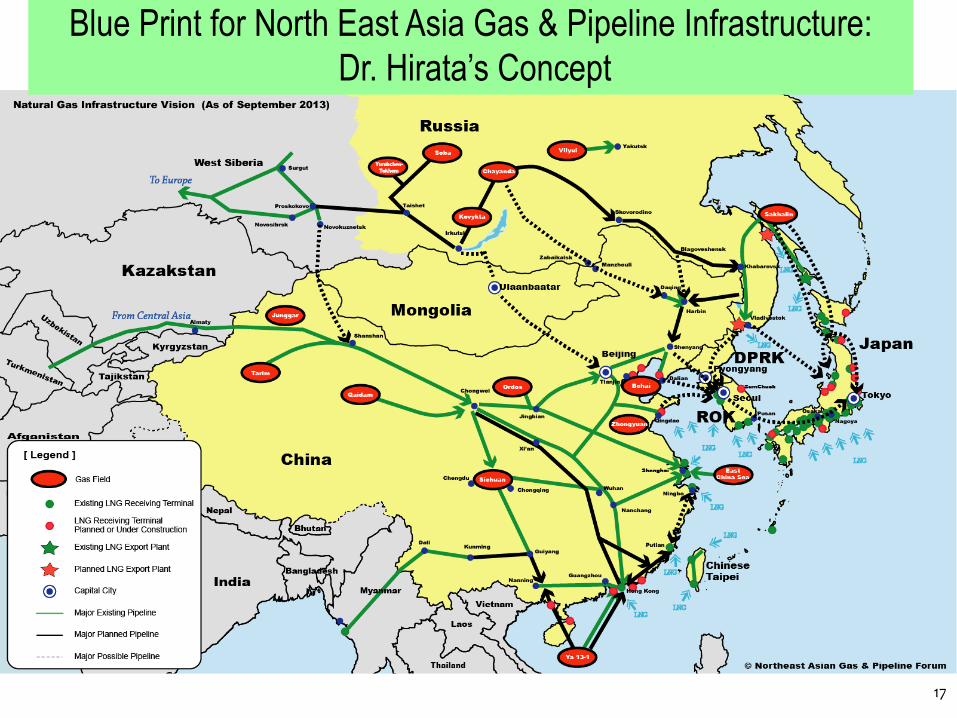

Blue Print for North East Asia Gas & Pipeline Infrastructure:

Dr. Hirata’s Concept

17

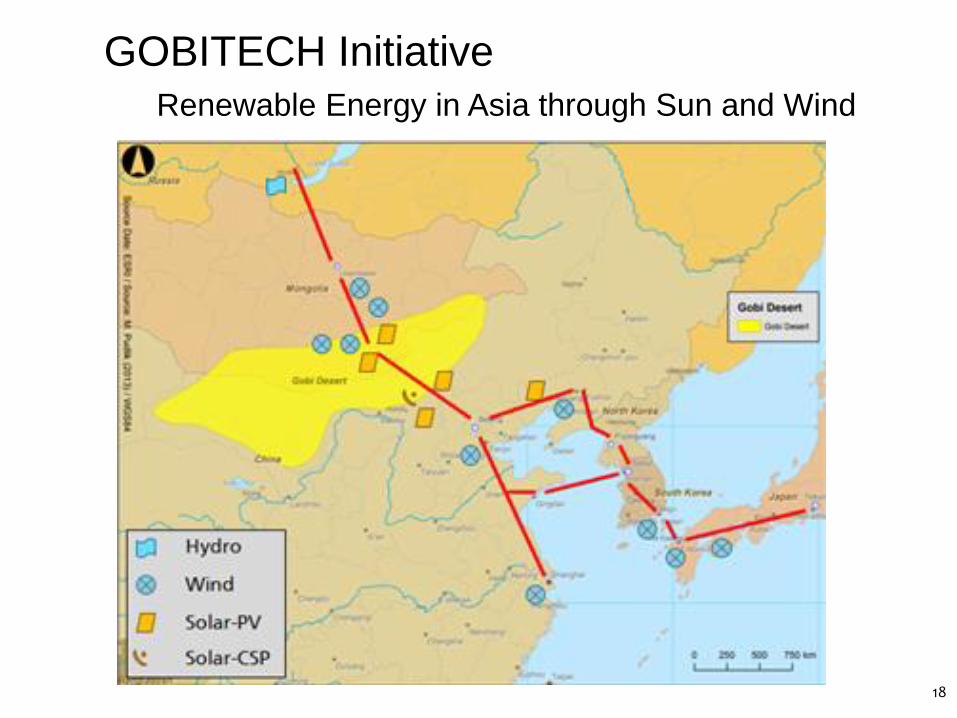

GOBITECH Initiative

Renewable Energy in Asia through Sun and Wind

18

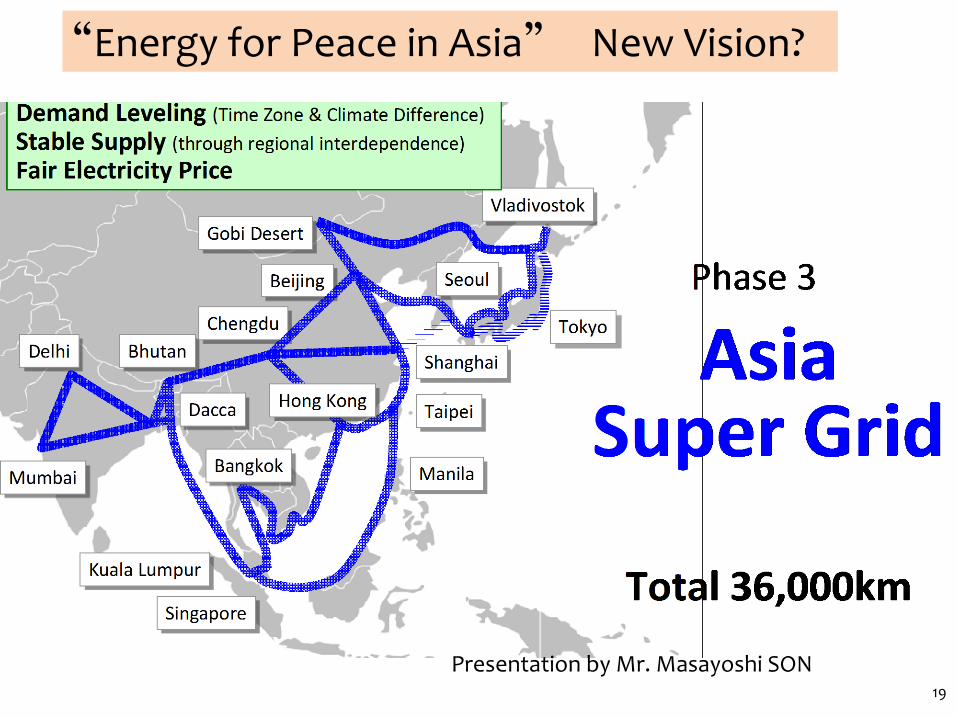

Presentation by Mr. Masayoshi SON19

“Energy for Peace in Asia” New Vision?

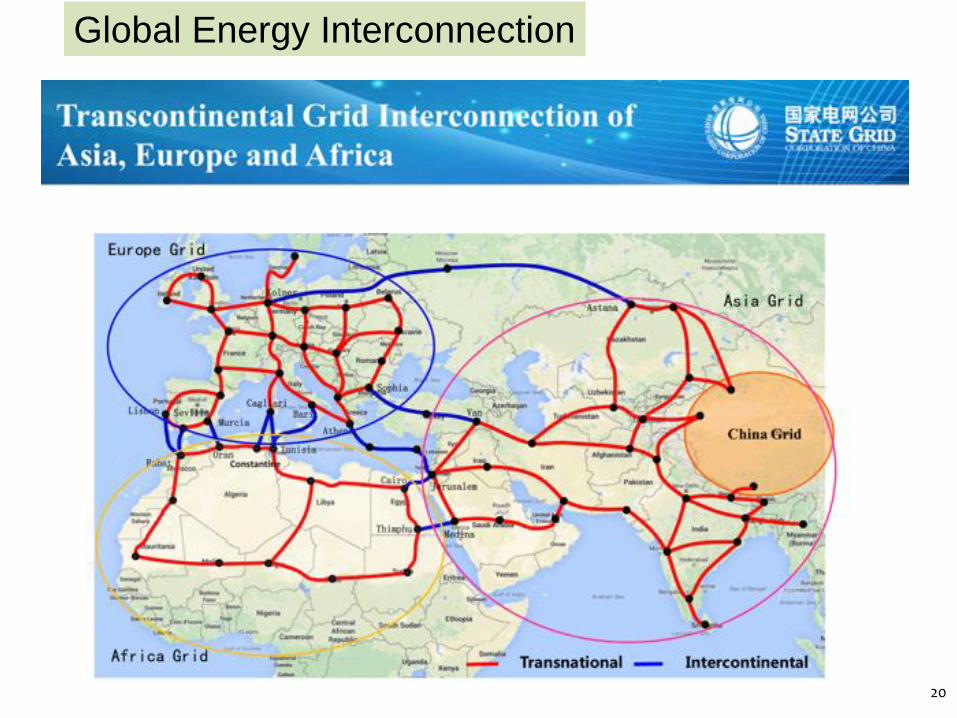

Global Energy Interconnection

20

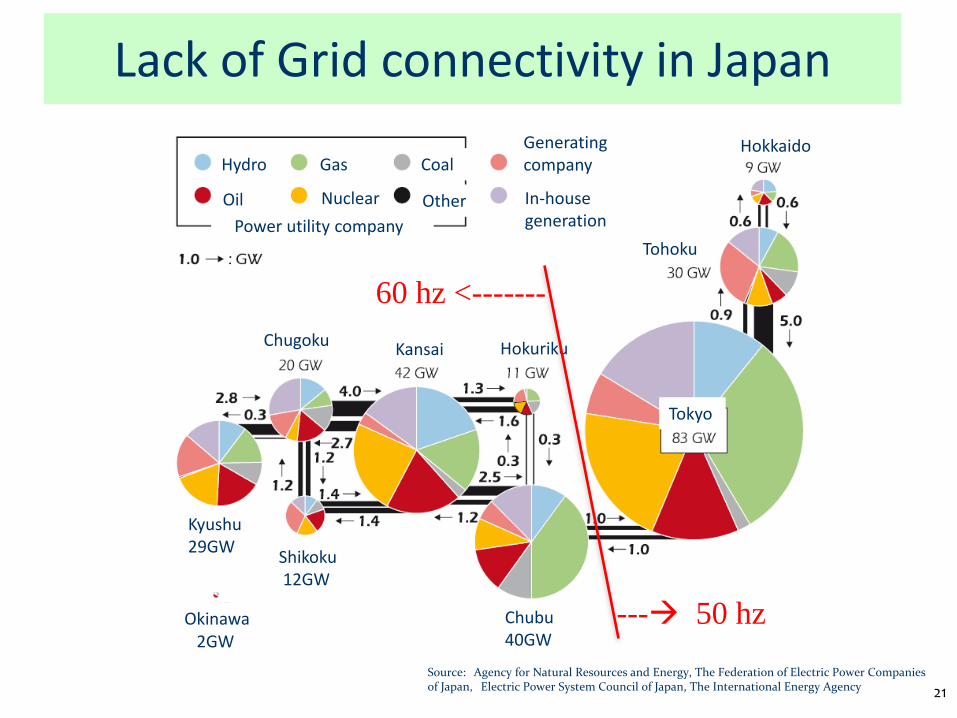

Lack of Grid connectivity in Japan

Source: Agency for Natural Resources and Energy, The Federation of Electric Power Companies of Japan, Electric Power System Council of Japan, The International Energy Agency

Tokyo

Hokkaido

Tohoku

HokurikuKansaiChugoku

Kyushu29GW

Shikoku12GW

Chubu 40GW

Okinawa2GW

Hydro

Oil

Gas

Nuclear

Coal

Other

Power utility company

Generating company

In-house generation

--- 50 hz

60 hz <-------

21

Asian Super Grid in SPIEF

22

![Head of Middle East/ South Asia Markets ICIS · PDF fileHead of Middle East/ South Asia Markets ICIS Singapore ... Head of Middle East, South Asia Markets. ... [Pata] GAIL HDPE/LLDPE](https://img.pdfslide.us/doc/110x75/5aa1714f7f8b9a84398ba14c/head-of-middle-east-south-asia-markets-icis-of-middle-east-south-asia-markets.jpg)