Embed Size (px)

Citation preview

STOP ACTING

LIKE AUDITORS!

THE HUMAN SIDE

OF AUDITING

May 6, 2016

Steve Goodson, Lecturer

The University of Texas, McCombs School of Business

CIA, CGAP, CCSA, CISA, CRMA, CLEA

Internal Audit Mission

To enhance and protect

organizational value by providing risk-

based and objective assurance,

advice, and insight.

Session Objectives

Discuss the characteristics of the internal audit profession in 2016

Discuss the teachings and philosophy of Larry Sawyer, the “father of modern internal auditing”

Discuss the importance of “the human side of auditing”

Share experiences of group members

Session Objectives(Continued)

Review examples of “things to avoid” in working with management and staff

Given enough time:

Provide an overview of the “Johari Window” model for interpersonal communication

Develop a personal development plan for enhancing interpersonal, communication, and facilitation skills.

IIA Common Body of

Knowledge Study

Feedback from more than 13,500 audit

practitioners in over 160 countries

IIA Common Body of

Knowledge Study

Characteristics of an Internal Audit Activity

Core Competencies for Today’s Internal Auditor

Characteristics of Internal Audit

2016

The IA focus has changed significantly

Less emphasis on:

* operational and compliance audits

* financial risks

* fraud investigations

* internal control evaluations

Characteristics of Internal Audit

2016

New emphasis on:

corporate governance

Enterprise Risk Management

strategic reviews

ethics audits

migration to IFRS Standards

integrated Reporting

Top Core Competencies

Communication skills

Problem identification and solution skills

Understanding the business

Interpersonal skills

Other Core Competencies

Ability to promote the value of IA

Organizational skills

Conflict resolution/negotiation skills

Staff training & development

Change management skills

Actg frameworks, tools, & techniques

IT / ICT frameworks, tools, & techniques

Data Analytics

IIA Guidance

IIA Standard 2420

Quality of Communications

“Communications must be accurate, objective, clear, concise, constructive, complete, and timely.”

Practice Advisory 2420-1

Lawrence B. Sawyer

Father of Modern Internal Auditing

(1911 – 2002)

Sawyer Internal Auditor Articles

1988-1992

The Human Side of Auditing

The Leadership Side of Auditing

The Political Side of Auditing

The Creative Side of Auditing

Sawyer’s Words of Wisdom

Popular IIA publication (2004)

Idea came from Texas Leadership Program

Compilation of 25 Internal Auditor articles

Timeless Advice

Sawyer’s

Internal Audit Philosophy

When you point your finger, make sure your fingernail is

clean.

The best question is “Mr. or Ms. Manager, how do you

satisfy yourself that . . . ?”

Politics and culture will win over rules and regulations.

Leave every place a little better than you found it.

Sawyer’s

Internal Audit Philosophy

Know the objectives.

Nothing ever happens until somebody sells something.

Every deficiency is rooted in the violation of some

principle of good management.

Sawyer’s Key PointsThe Audit Process

Reasons for conflict:

Fear of change, exposure, and noncompliance

Audits breed conflict and differences in opinion

Every audit finding is an implied criticism

Sawyer’s Key PointsAuditor Image

General perception of auditors not flattering

Arrogant, demanding, and overbearing vs.

professional, helpful, and supportive

Downputters and naysayers. Looking for

something wrong

Sawyer’s Key PointsRelating to the Auditee

Auditor style and approach makes a difference

Understand management’s needs, motivations

and styles

Emphasize condition and action to correct

Sawyer’s Key PointsReporting

Discuss potential issues and recommendations

well in advance

No nitpicking

Explain the positive results of audits

Give credit for outstanding achievements

No surprises

Sawyer’s Key PointsThe Road Ahead

Cultivate a better understanding of feelings

Don’t attach blame

Explain the audit process

Adopt a more positive reporting style

Obtain top management support

Use a cooperative, problem-solving approach

Improving Communications

How can you better assure that you

communicate more effectively?

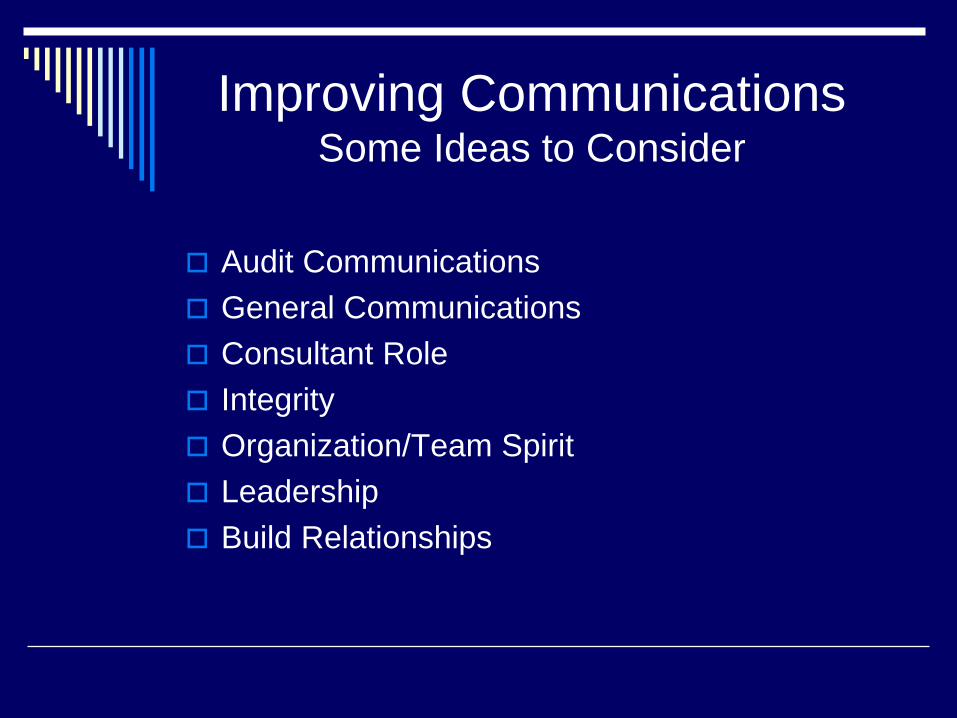

Improving CommunicationsSome Ideas to Consider

Audit Communications

General Communications

Consultant Role

Integrity

Organization/Team Spirit

Leadership

Build Relationships

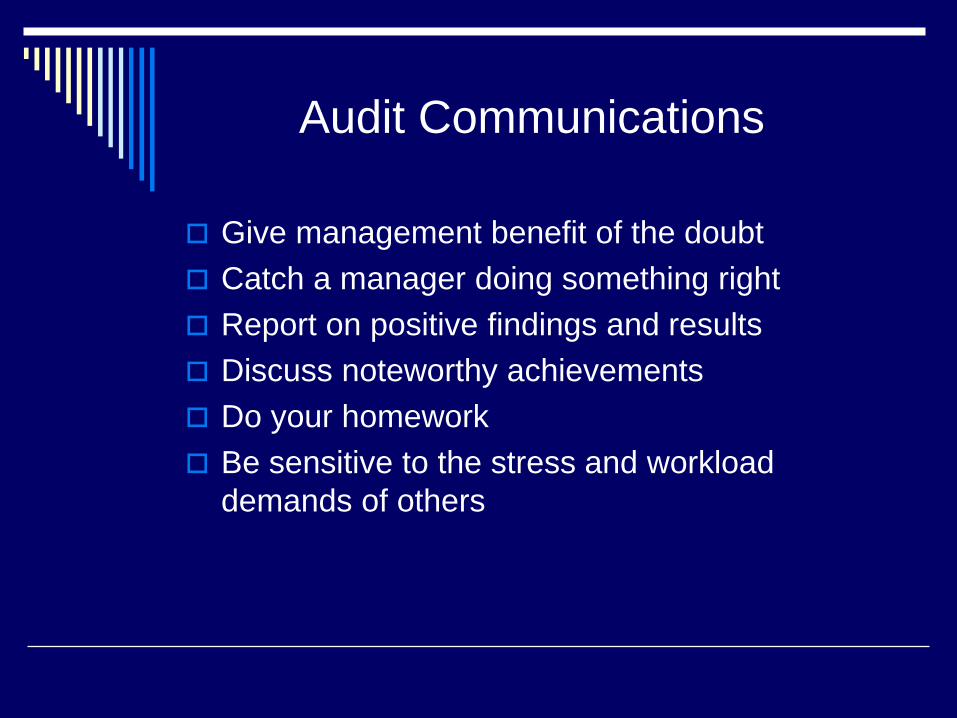

Audit Communications

Give management benefit of the doubt

Catch a manager doing something right

Report on positive findings and results

Discuss noteworthy achievements

Do your homework

Be sensitive to the stress and workload

demands of others

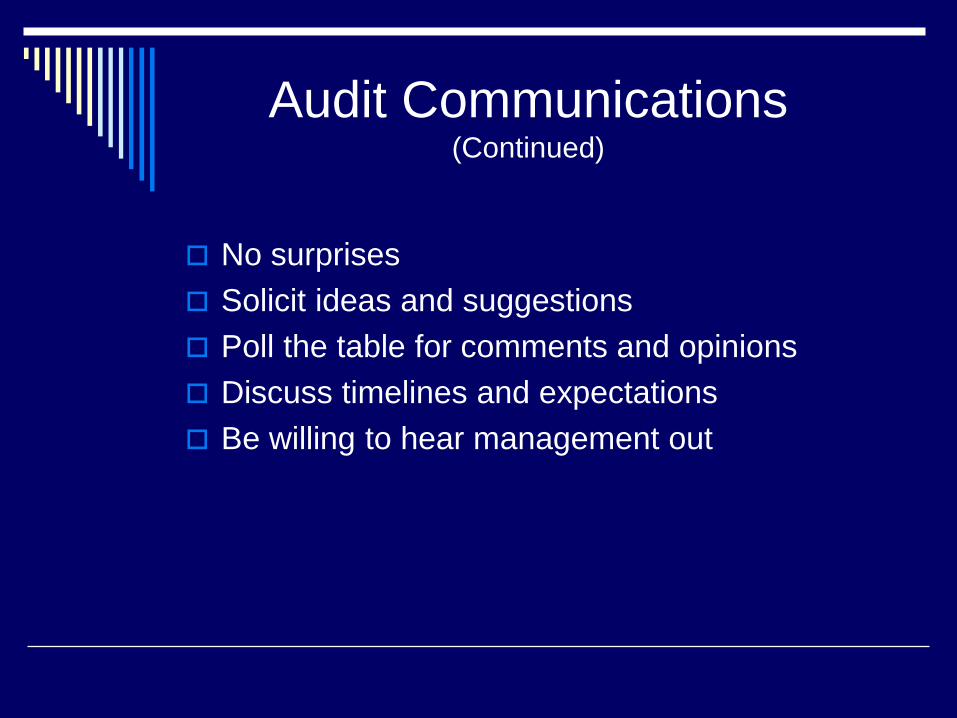

Audit Communications(Continued)

No surprises

Solicit ideas and suggestions

Poll the table for comments and opinions

Discuss timelines and expectations

Be willing to hear management out

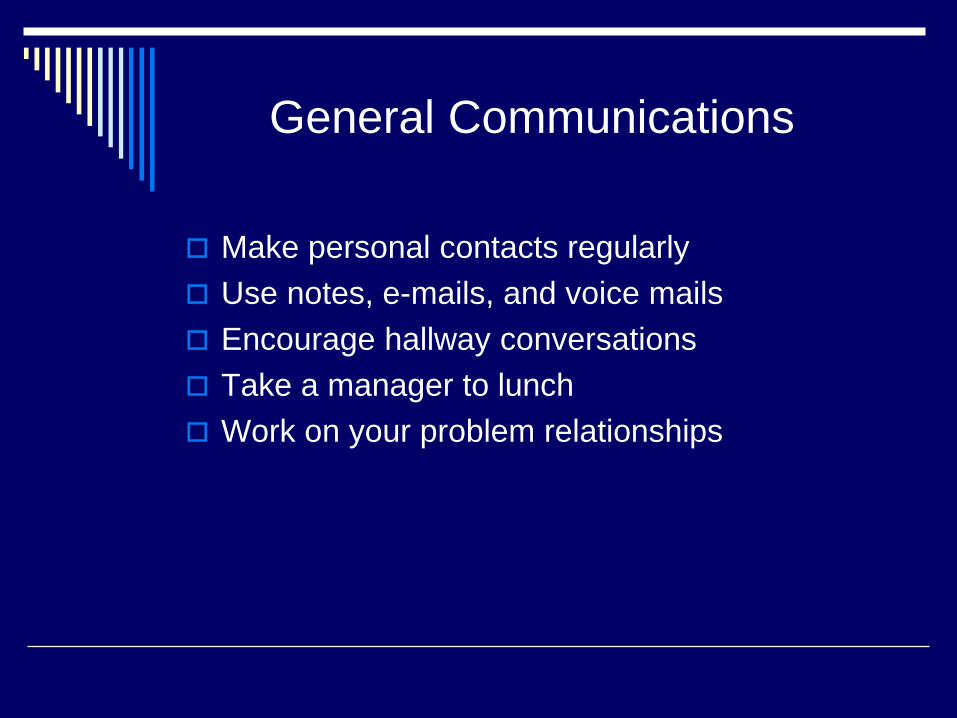

General Communications

Make personal contacts regularly

Use notes, e-mails, and voice mails

Encourage hallway conversations

Take a manager to lunch

Work on your problem relationships

General Communications(Continued)

Have some knowledge about the person and

the subject matter

Listen to what the others are saying

Don’t interrupt

Confirm and expand on areas of agreement

Seek and find opportunities to negotiate

Consultant Role

Share relevant information (external auditors,

IIA, industry audit groups)

Provide copies of articles of interest

Obtain relevant policies, procedures, and

practices from other organizations

Share “heads up” information on audits and

other items (non-confidential)

Integrity

Follow-up on commitments made

Live by the “Golden Rule”

Show trust and respect

Get involved with accountability, ethics, and

governance issues

Build and keep trust

Organization/Team Spirit

Serve on committees, workgroups, etc.

Volunteer for activities benefiting the

organization

Establish partnerships with CFO, Legal, HR, IT,

Communications, and others

Initiate contacts with new managers

Enhance and nourish current relationships

Leadership

Attend management & Board meetings

Invite managers to IA staff meetings

Welcome opportunities to talk about risk,

controls, and governance

Lead by example

Have a positive attitude

Balance organizational and professional duties

Leadership(Continued)

Consider serving in a management position

Be flexible

Develop a sense of humor

Ask for feedback and listen to it

Be approachable

Practice MBWA

Building More Effective

Relationships

Survey of Chief Audit Executives

What are their ideas?

What can we learn about effective

relationships?

Ideas from Several

Chief Audit Executives

Peer group informal survey

9 experienced CAEs responded

Tips on how to build good relationships with

management?

Things to avoid in working with management?

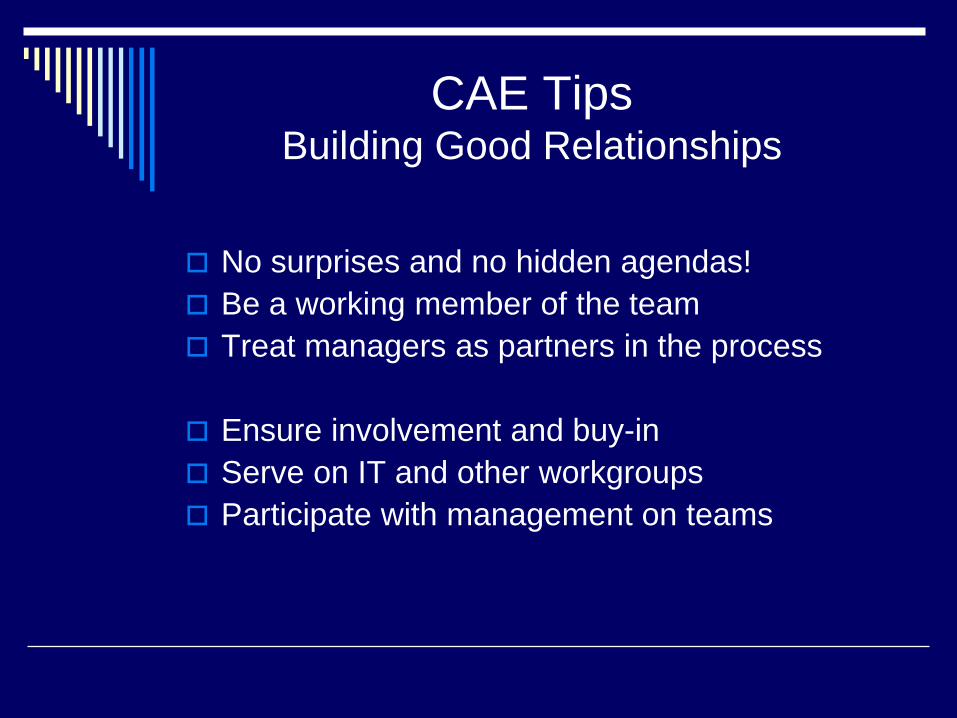

CAE TipsBuilding Good Relationships

No surprises and no hidden agendas!

Be a working member of the team

Treat managers as partners in the process

Ensure involvement and buy-in

Serve on IT and other workgroups

Participate with management on teams

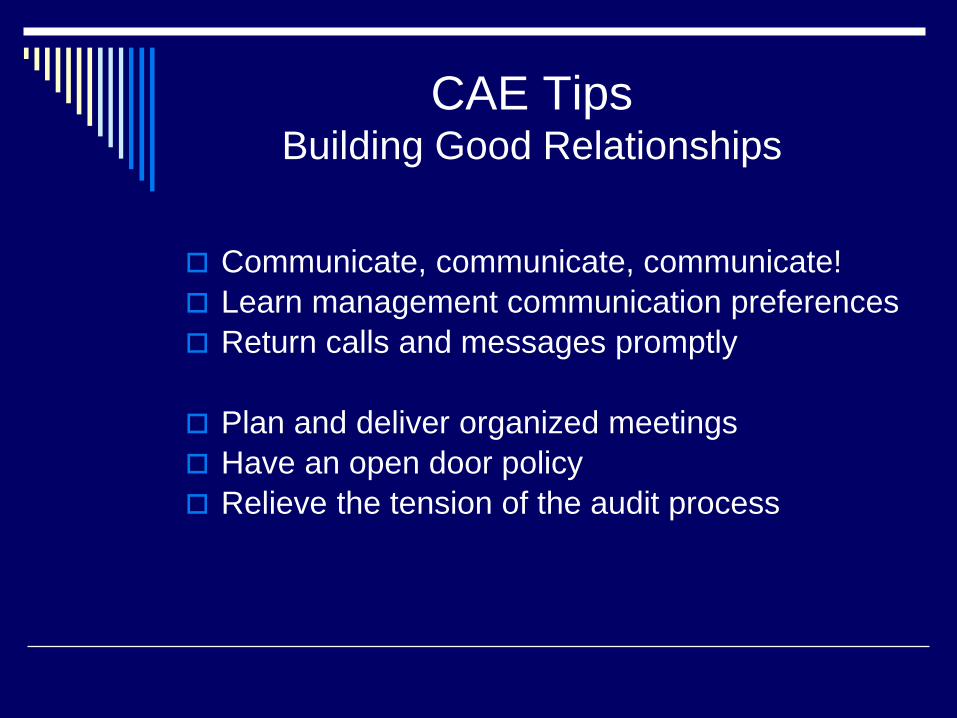

CAE TipsBuilding Good Relationships

Communicate, communicate, communicate!

Learn management communication preferences

Return calls and messages promptly

Plan and deliver organized meetings

Have an open door policy

Relieve the tension of the audit process

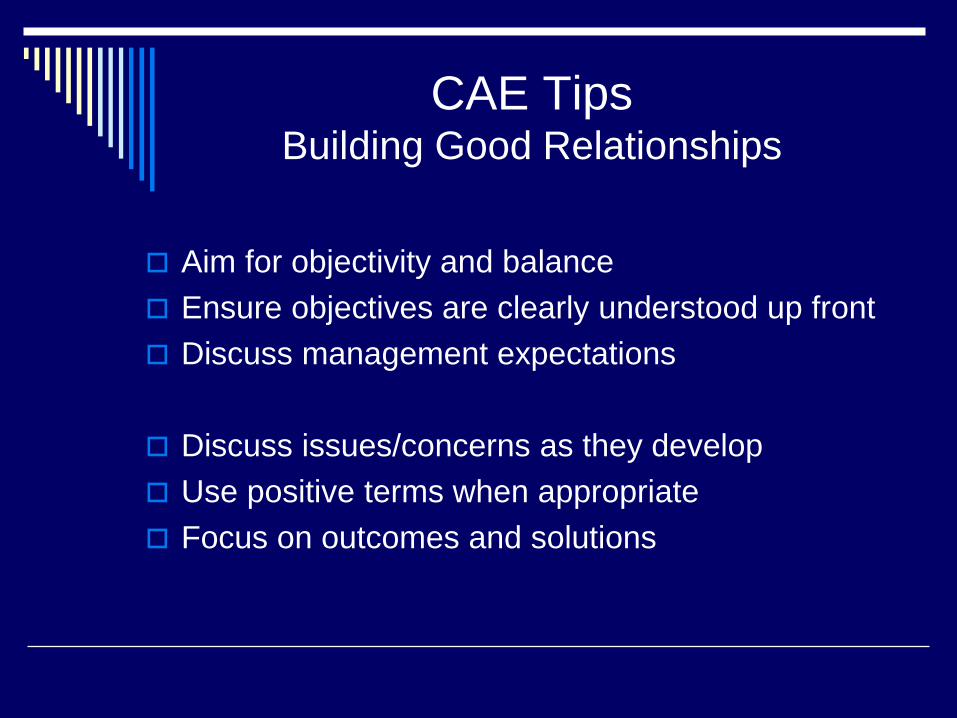

CAE TipsBuilding Good Relationships

Aim for objectivity and balance

Ensure objectives are clearly understood up front

Discuss management expectations

Discuss issues/concerns as they develop

Use positive terms when appropriate

Focus on outcomes and solutions

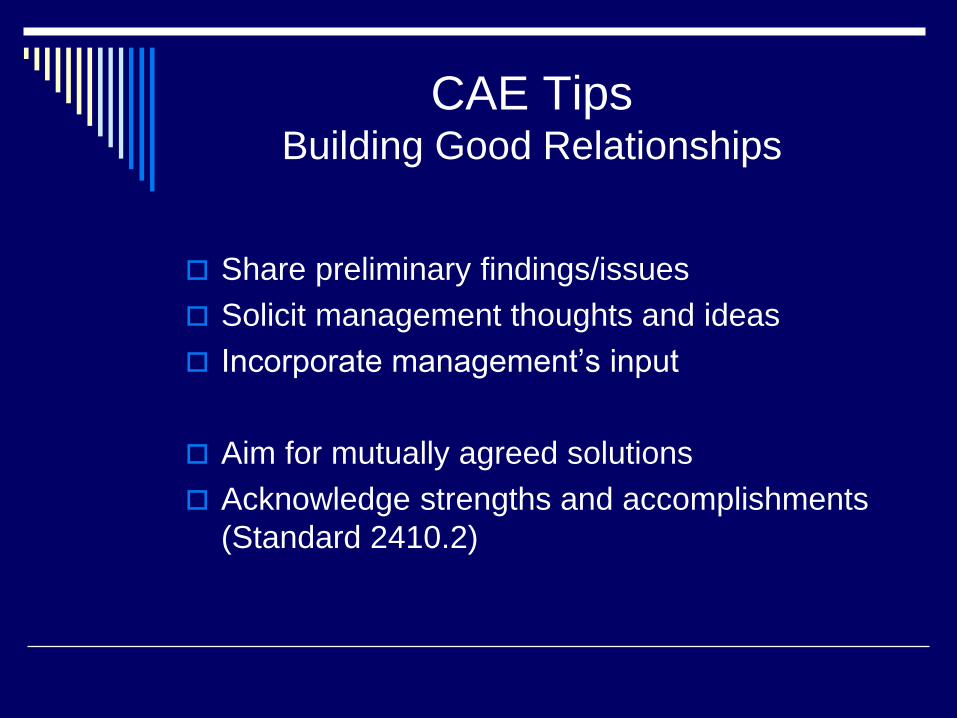

CAE TipsBuilding Good Relationships

Share preliminary findings/issues

Solicit management thoughts and ideas

Incorporate management’s input

Aim for mutually agreed solutions

Acknowledge strengths and accomplishments

(Standard 2410.2)

CAE TipsBuilding Good Relationships

Remember that relationships are long term

Trust and respect are important

Gain knowledge of operations and management

Be available in times of crisis

Cover the who, what, when, where, why and how

CAE TipsBuilding Good Relationships

Have a customer service attitude

Be a problem solver

Get involved in understanding the complexities of programs and activities

Attend Board committee meetings and learn more about the organization

Attend training on organization initiatives

CAE TipsBuilding Good Relationships

Get involved with strategic planning, IT planning and the budget process

Check laws, regulations, policies and history

Attend legislative and other regulatory oversight meetings

Obtain a seat at the management table

Keep executive management & Board informed

Be an effective liaison with external auditors

CAE TipsOpportunities to Provide Courtesy Information

Provide status on internal or external audits

Share the perspective of a Board member/ manager on an issue or concern

Provide draft information on Audit Committee meeting topics

CAE Tips

Opportunities to Provide Courtesy Information

Provide “heads up” on coming events

Give news of IA staff members achieving certification

Congratulate on good presentation or other achievement

CAE Tips

Opportunities to Send Thank You Notes

Participation in risk assessment/Audit Plan interviews

Presentations at Audit Committee meetings

Attendance at staff meetings (yours or theirs)

CAE Tips

Opportunities to Send Thank You Notes

Timely and relevant information/referral provided

Important advice or assistance rendered

Participation in IA-sponsored initiatives

CAE TipsThings to Avoid

Don’t:

Play “us vs. them” games

Spring audit findings on management

Take on special project requests which should

be done by management

Give information that is a “difficult read”

(technicalities, volume)

CAE Tips

Defuse personality conflicts and focus on the work

Understand management’s priorities

Focus on what happened and how to fix it (rather than

assessing blame)

Don’t let office location hurt your communications with management

CAE Tips

When you make a mistake, admit it!

Keep your promises

Be aware of your limitations (avoid “over

promising” and “under delivering”)

Avoid auditing and accounting jargon

Avoid the infamous “gotcha” mentality

CAE TipsThings to Avoid

Don’t:

Make decisions for management

Take sides in a turf battle

Focus on insignificant issues

Project defensiveness when a manager takes exception

Turn away a business partner

CAE TipsThings to Avoid

Don’t:

Project arrogance

Use your position power inappropriately

Surprise the CEO or Committee Chair at

Board/Audit Committees meetings

Lose your integrity and reputation

Lose your independence and objectivity

Johari Window

Johari Window

Model of awareness and group dynamics

Impact of disclosure and feedback

Interpersonal communication and group development

Joseph Luft and Harry Inghan (1955)

Johari Window

Arena

Unknown

Façade

Blind Spot

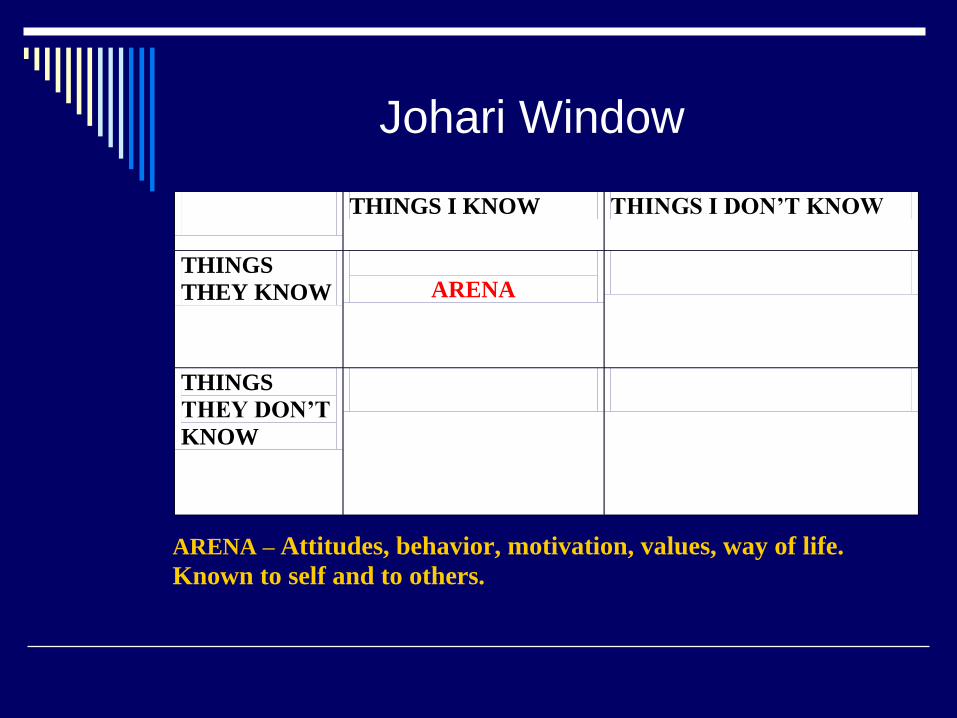

Johari Window

THINGS I KNOW THINGS I DON’T KNOW

THINGS

THEY KNOW

ARENA

THINGS

THEY DON’T

KNOW

ARENA – Attitudes, behavior, motivation, values, way of life.

Known to self and to others.

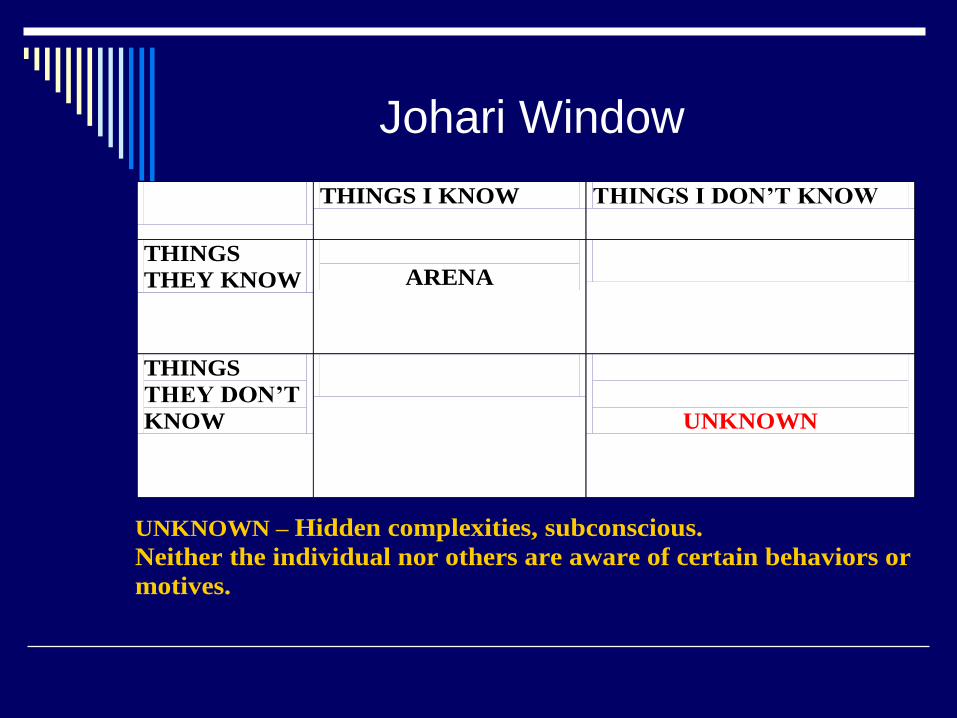

Johari Window

THINGS I KNOW THINGS I DON’T KNOW

THINGS

THEY KNOW

ARENA

THINGS

THEY DON’T

KNOW

UNKNOWN

UNKNOWN – Hidden complexities, subconscious.

Neither the individual nor others are aware of certain behaviors or

motives.

Johari Window

THINGS I KNOW THINGS I DON’T KNOW

THINGS

THEY KNOW

ARENA

THINGS

THEY DON’T

KNOW

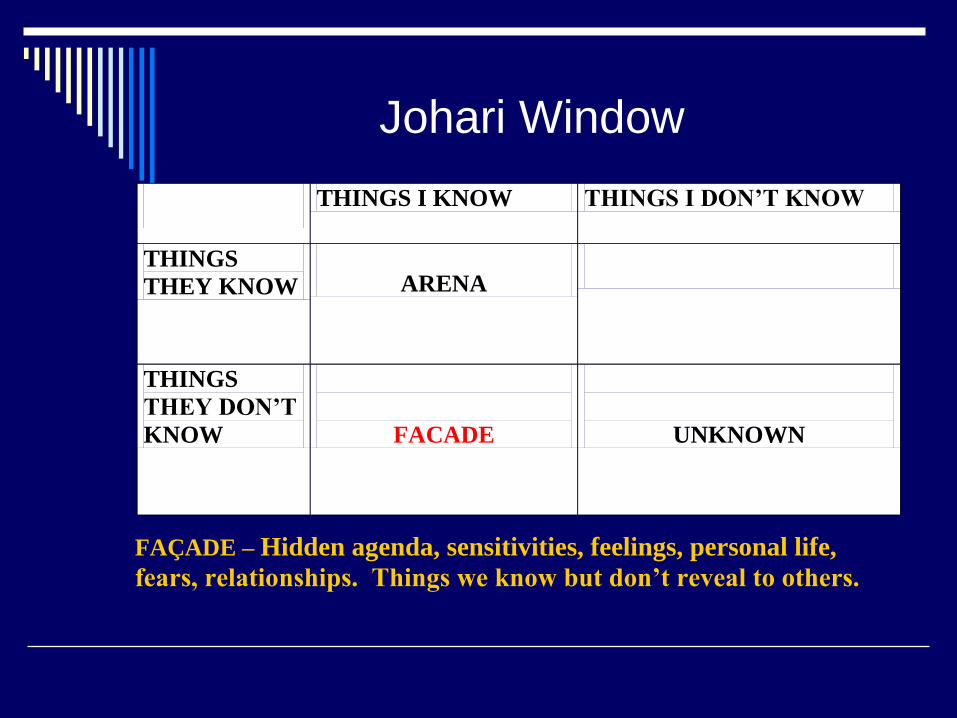

FACADE

UNKNOWN

FAÇADE – Hidden agenda, sensitivities, feelings, personal life,

fears, relationships. Things we know but don’t reveal to others.

Johari Window

THINGS I KNOW THINGS I DON’T KNOW

THINGS

THEY KNOW

ARENA

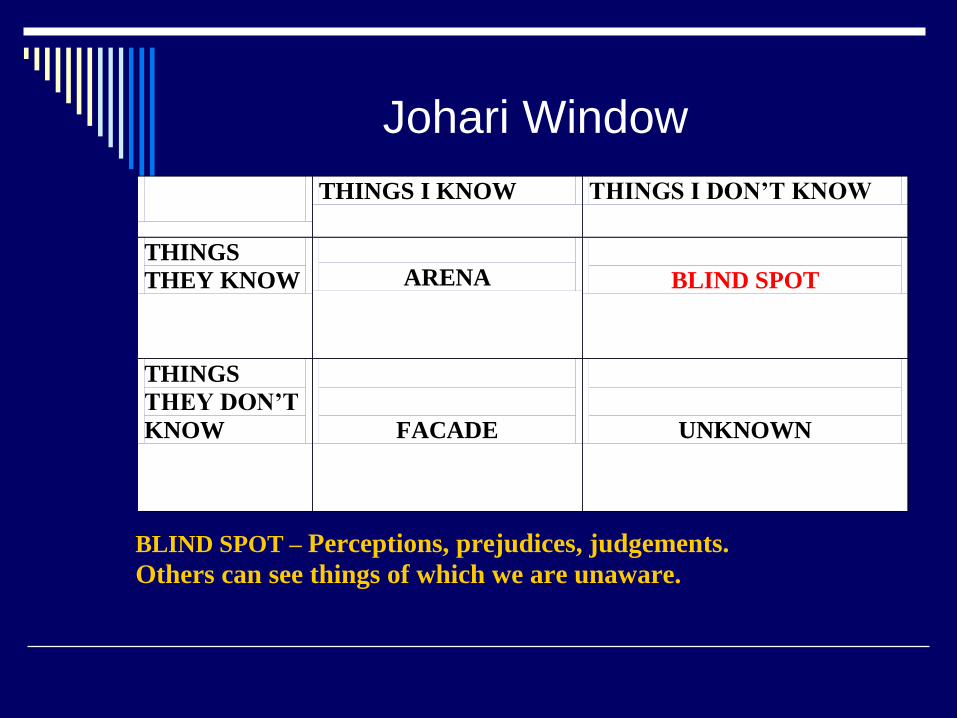

BLIND SPOT

THINGS

THEY DON’T

KNOW

FACADE

UNKNOWN

BLIND SPOT – Perceptions, prejudices, judgements.

Others can see things of which we are unaware.

Johari Window

THINGS I KNOW THINGS I

DON’T KNOW

THINGS

THEY KNOW

ARENA

BLIND SPOT

THINGS

THEY DON’T

KNOW

FACADE

UNKNOWN

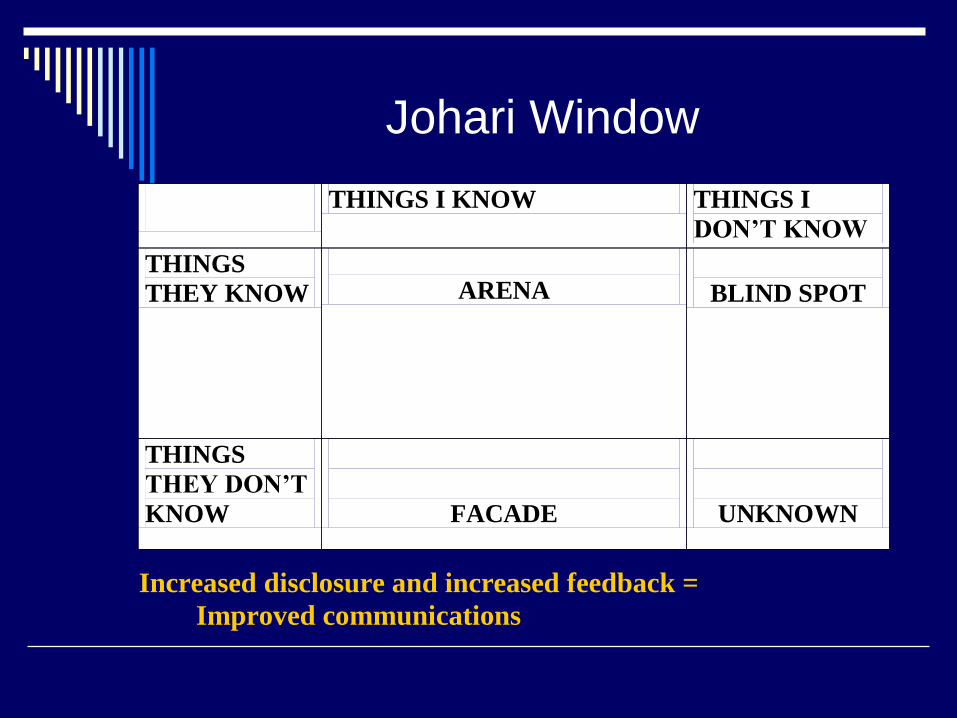

Increased disclosure and increased feedback =

Improved communications

Johari Window

THINGS I KNOW THINGS I

DON’T KNOW

THINGS

THEY KNOW

ARENA

BLIND SPOT

THINGS

THEY DON’T

KNOW

FACADE

UNKNOWN

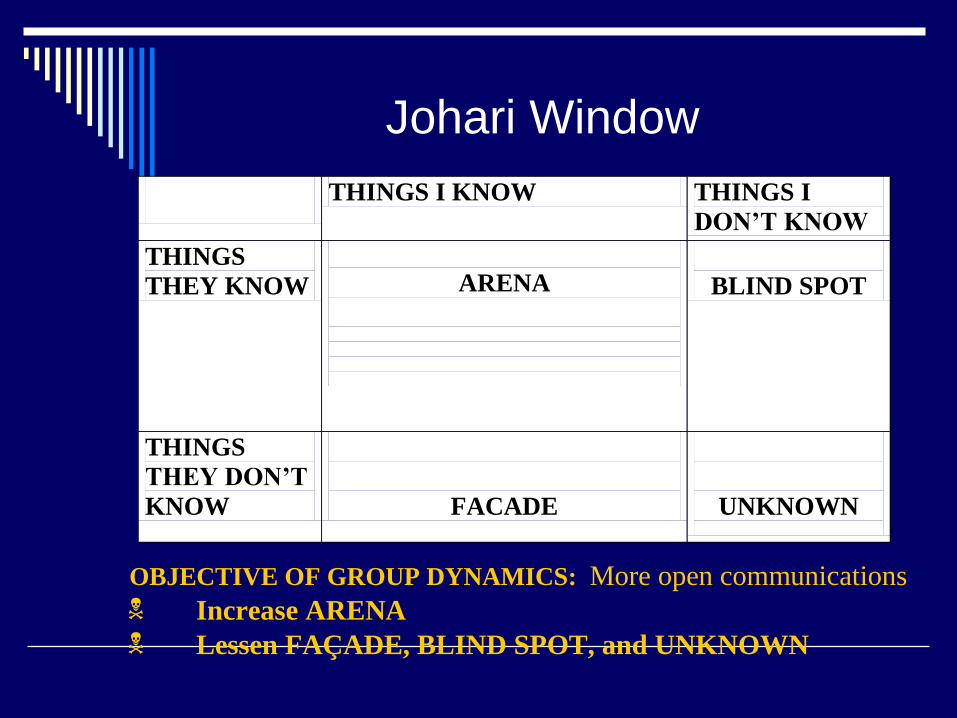

OBJECTIVE OF GROUP DYNAMICS: More open communications

Increase ARENA

Lessen FAÇADE, BLIND SPOT, and UNKNOWN

Johari WindowMore Information

Luft, Joseph

“Group Processes: An Introduction to Group Dynamics”

National Press Books, Palo Alto, California

(1970, 2nd edition)

Personal Development Plans

So what does today’s topic mean to you?

What can you do to enhance the quality and effectiveness of interpersonal, communication and facilitation skills?

Complete a personal development plan

Discuss this with your CAE (or Department Chair) within the next 10 work days

Personal Development Plan

What can you do to enhance the quality and effectiveness of interpersonal, communication

and facilitation skills with:

Students/ Faculty?

Fellow staff members?

the CAE / Audit Director?

Executive and Line Management?

External Auditors?

Fellow Audit Professionals?

Coordination

An act reluctantly entered into by two or more

partially consenting bodies.

-- Fred Allen

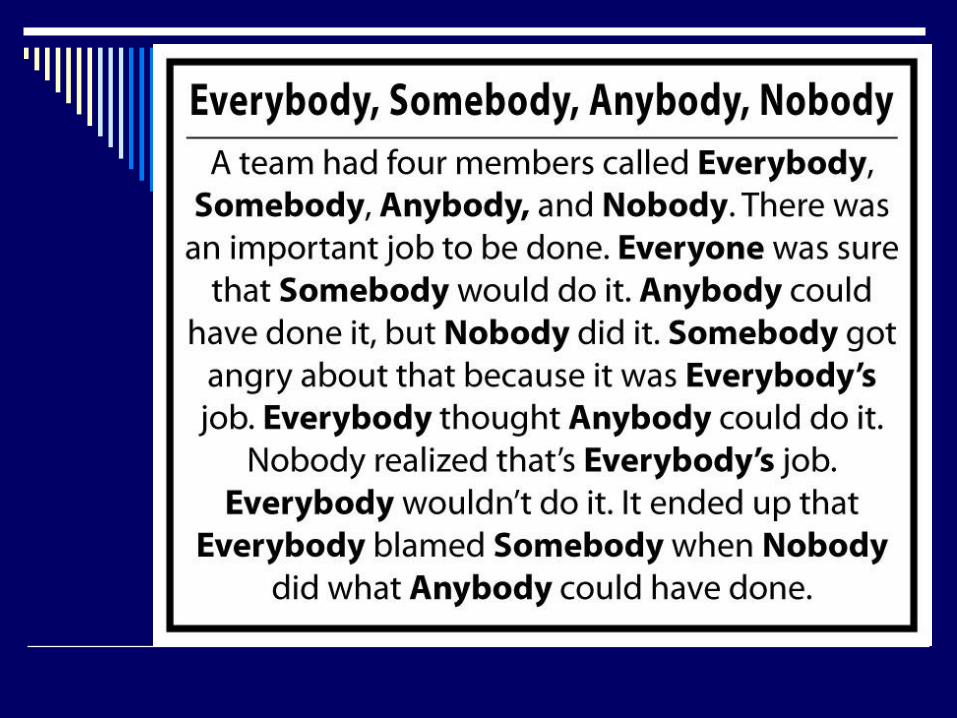

Old Story Everybody

Somebody

Anybody

Nobody

Questions?

Stop acting like auditors –

Start acting like humans.