Embed Size (px)

Citation preview

Stock Valuation

Lesson 1

Learning Objectives

£ To be able to explain what STOCK is

££ To be able to state the difference between FIFO and AVCO methods of valuation

£££ Be able to reconcile stock values with actual stock

Starter Activity

What Is Stock?

Raw materials and componentsStock purchased before production.

Work-In-ProgressStock that is currently in the Production process, may takeWeeks to become a finished product

Finished GoodsA stock of finished Goods may be built upBy the producer

Goods For ResaleAn example of this is the Stock that TESCO mayHold on its shelves

ConsumablesItems used by the Business which are notIntended for resale, an Office may have a stock Of paper or envelopes

Used for the calculationFor cost of sales. VERY IMPORTANT

Why Value Stock?

Sign of an efficient Business

So you know what stockYou have on the premises

Helps with the Production of theFinal accounts

Makes sure that theProfit is not over valuedPRUDENCE CONCEPT

Auditors may visit a business and audit stock and cash on the premisesAt any time, without warning!!!!!!!!!!

Importance of Stock Valuation

Stock can be valued in a number of ways1. What it actually Cost to buy the stock (this will

include delivery costs and possibly making the product into a saleable item)

2. Net realisable value, the actual or estimated price, minus any additional costs

IS THE COST PRICE LOWERTHAN SELLING

PRICE?

YES NOVALUE STOCK ATCOST PRICE

VALUE STOCK AT SELLINGPRICE (NRV)

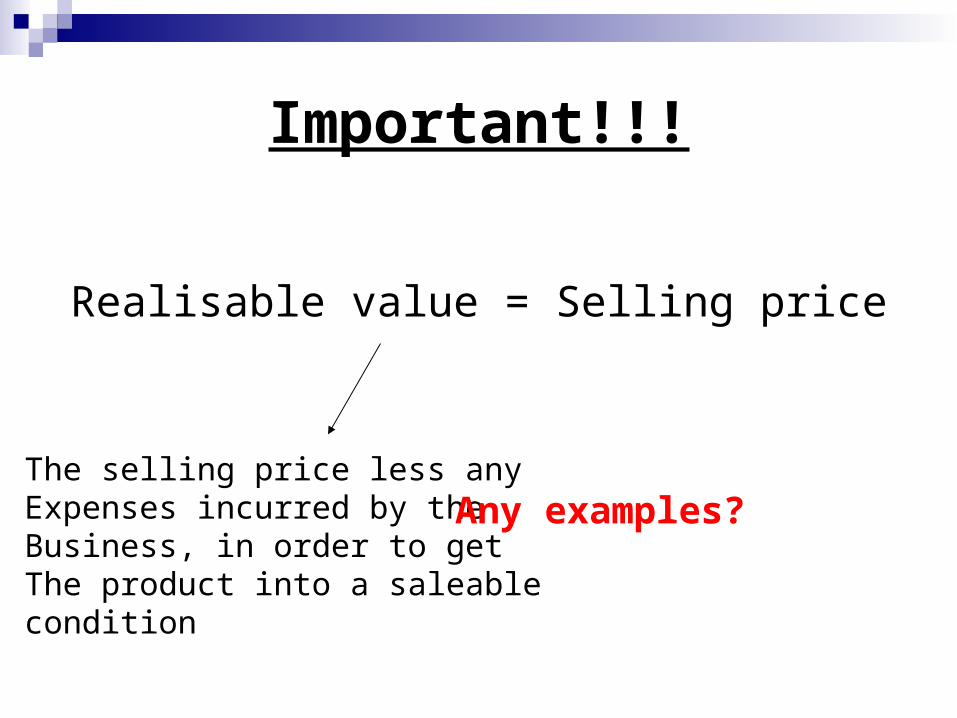

Important!!!

Realisable value = Selling price

The selling price less anyExpenses incurred by theBusiness, in order to getThe product into a saleablecondition

Any examples?

Activity onto boardPRODUCT COST PRICE SELLING PRICE

A 12 31

B 23 22

C 8 14

D 42 40

E 17 15

How much would you value each PRODUCT?

ActivityPRODUCT UNITS COST SELLING

PRICE

W 21 16 20 X 13 41 50 Y 8 18 15

Z 32 10 20

What is the total value of stock held on the 12th June2009

(@c 336)

(@c 533)

(@realisable 120)

(@c 320)

Calculate the Selling Price

£1,309

Methods of Stock ValuationStock valuation is made tricky because of the purchase price, which may vary over a year (petrol) At the end of the year the business may not know the actual prices of the items left in stock. As a result different methods can be used to value the cost of stocks, Three methods that help us do this are:

1. FIFO first in first out

2. LIFO last in first out

3. AVCO average cost

Get pupils to research from the Rob Jones book- PAGE 194

Research the following:

FIFO

AVCO

Stock Valuation

Lesson 2

Lesson Objectives

£ To be able to define FIFO and AVCO

££ To be able to calculate both methods

£££ To evaluate the most appropriate method of stock valuation

Starter Activity

1. Why does a business need sources of finance?

2. What is the difference between internal and external sources of finance?

3. State 2 long term sources of finance

4. Name the world cup winners in backwards order from 2006 to the date of your birth.

World Cup1966 England1970 Brazil1974 Germany 1978 Argentina1982 Italy1986 Argentina1990 Germany1994 Brazil1998 France2002 Brazil2006 Italy

Importance of inventory valuation

The value of stock appears on both the trading profit and loss account and also the balance sheet

If the closing stock value is placed too high then both the profit and the assets will be overstated, and vice versa

After completing your homework you should be able to answer the following

1. Define FIFO

2. Define AVCO

3. State one advantage of using the FIFO method

4. What kind of business would use FIFO? Explain your answer

5. How will fluctuations in unit price impact both methods of valuation?

FIFO

This method assumes that stock is used in the order in which it was bought

Any unused stock is therefore the most recently bought

Advantages A realistic method, Easily to calculate, using actual prices of stock.

Closing stock will be based on the most recent prices

FIFO cont..

Disadvantages The stock taken for production may have

an out of date price, this may mean that the selling price is not taking into consideration the more recent prices

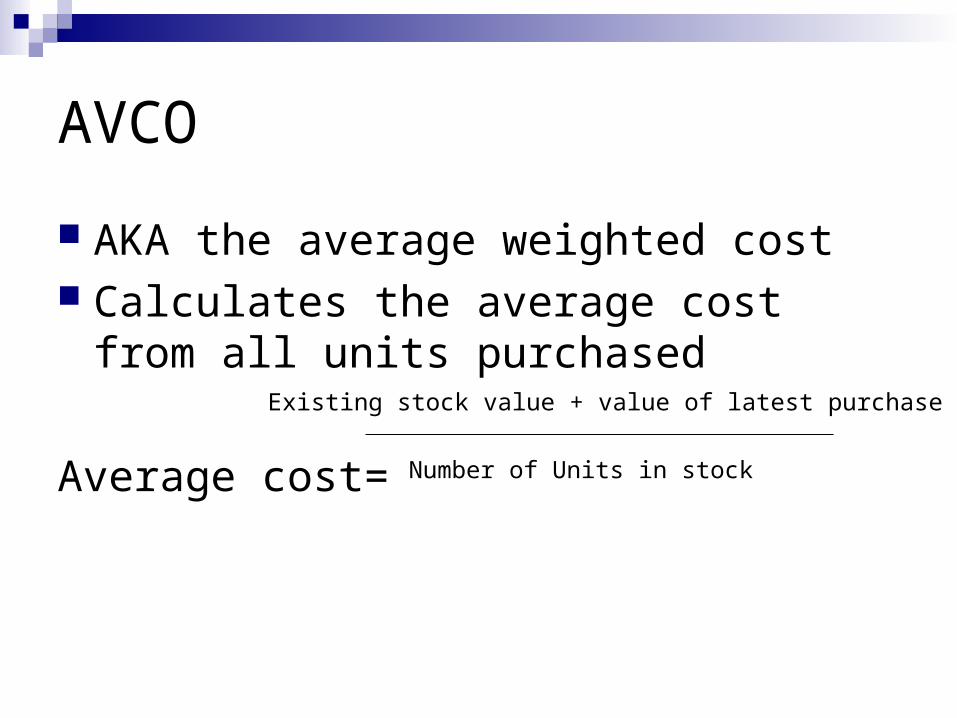

AVCO

AKA the average weighted cost Calculates the average cost from all units

purchased

Average cost=

Existing stock value + value of latest purchase

Number of Units in stock

AVCO continued Advantages It makes sense to use this method since all units are

given equal value Fluctuations in unit price are evened out Conforms to the accounting standards Disadvantages Average cost needs to be re calculated every time that

price of purchased stock changes Average cost may not be the same as any of the

purchased prices Stock prices rise rapidly, average cost will be much

lower than replacement price

LIFO-just for your information Last in first out method, newest stock is always

used first Unused stock is based on the cost of earlier

purchases ADVANTAGES

Based on the prices of most recently purchased goods, selling price can reflect this, easy to calculate

DISADVANTAGES May be difficult to use up new stock first, for instance

when dealing with food. Closing stock will use out of date prices, so may go against inland revenue requirements

Activity

Sorensen Mills is a food processing company. It refines and packs flour for large supermarkets. The business’ main raw material is grain that it buys from a Canadian supplier. During April, the following stock transactions were recorded:

3rd 20 tonnes delivered @£100 per tonne

10th 40 tonnes delivered @ £110 per tonne

12th 40 tonnes were used in production

18th 40 tonnes were delivered @ £120 per tonne

29th 40 tonnes were used in production

a) Assuming that the opening stock was zero, calculate the value of closing stock atthe end of April using the FIFO, LIFO and AVCO methodb) Which method of valuation is most appropriate for Sorensen Mills? Explain youranswer

Activity 2

Luke runs an electrical shop he has asked for your help when considering the value of the following items

COST NRV Comment1. Washing machine220 350

2. Dish Washer 330 280 replacement cost is £290

3. Television 250 325 case scratched, needs replacing at a cost of £90

4. DVD Player 75 125 Remote lost, will cost £20

ADVISE LUKE OF THE VALUE OF EACH ITEM

Answer

1) Cost price is lower 2) Net realisable value of £280 used. Replacement

cost is not used as it does not apply to the stock valuation

3) Replacements are needed before the sale, so deduct the cost of replacements from the NRV, compare this figure with the cost and use the lowest, NRV is used giving £235

4) Needs a control, 125-20 = 105, compare with cost of 75, cost is lower so use the £75

Homework

Complete sheet

Due in next lesson

Impact on profit

This is a common exam question… Assess the effect each of the two methods

of inventory (stock) valuation would have on profits: i) in the short term ii) in the long term

Typically 3-4 marks

Impact on profit (answer)

Long termProfits will be the same, as all stock will be

used up Short term

FIFO produces higher profits than AVCO Any impact on cash? No as the same price is paid to the

suppliers for the stock

Plenary

Put your name on the POST IT note, and complete the following sentences

I am ….% confident with stock valuation

I would like to …. To help me fully grasp stock valuation

Stick the POST IT note on the door frame,

Lesson Objectives

£ To be able to define FIFO and AVCO

££ To be able to calculate both methods

£££ To evaluate the most appropriate method of stock valuation