Embed Size (px)

Citation preview

St.George’s Regional B k P tf liBank Portfolio

Rob ChapmanRob ChapmanChief Executive St.George Bank

Morgan Stanley Financials Forum 17 March 2011

Westpac Banking Corporation ABN 33 007 457 141

Overview of St.George

Merger with The Westpac Group completed successfully ith ll j il t hi dwith all major milestones achieved

Repositioned St.George in 2010, acknowledging regional diffdifferences

1Q11 delivered higher cash earnings than average of 3Q10 and 4Q10

Initiatives in place to drive growth and improve efficiency

Launching Bank of Melbourne, a local bank for Victorians

2 St.George presentation - Morgan Stanley Financials Forum, March 2011

Journey so far for St.George post merger

2008

Merger effective

Increased The Westpac Group’s distribution by 40% and added 3 million customers

Group now covers a broader set of customers – those preferring a Big 4 major bank g17 November

p p g g jand those preferring a local bank

2009

Merger

Merger benefits, integration and sharing of best practice exceeded expectations

All milestones achieved reciprocal ATM use IT connectivity and single GLMerger integration

All milestones achieved, reciprocal ATM use, IT connectivity, and single GL

In-depth research completed on multi-brands and customer preferences

Began distributing BT insurance products and launched BT Super for Life

2010

St.George repositioned

Merger largely completed, including Basel II advanced accreditation and move to a single ADI

Moved to a regional management structure

Undertook detailed work on Victorian local bank opportunity pp y

Further consolidation of Westpac/St.George platforms under SIPs investment

2011

Multi brand taken

Appointed Rob Chapman as CEO

Slow growth in 1Q11 but early traction on initiatives to lift growthMulti-brand taken to the next level

Slow growth in 1Q11 but early traction on initiatives to lift growth

Announced launch of Bank of Melbourne

Finalised tax consolidation which in total delivered $1.8bn

Creating headroom for investment through efficiency measures

3 St.George presentation - Morgan Stanley Financials Forum, March 2011

Repositioned St.George in 2010

Restructured operations into five geographic regions

Reduced exposure to commercial property. Commercial property now represents 41% of business portfolio, down f 4 % M h 2009from 45% at March 2009

Reduced 3rd party mortgage origination

Re-engineered business to create headroom for further investment

Detailed analysis and preparation for Bank of Melbourne launch

4 St.George presentation - Morgan Stanley Financials Forum, March 2011

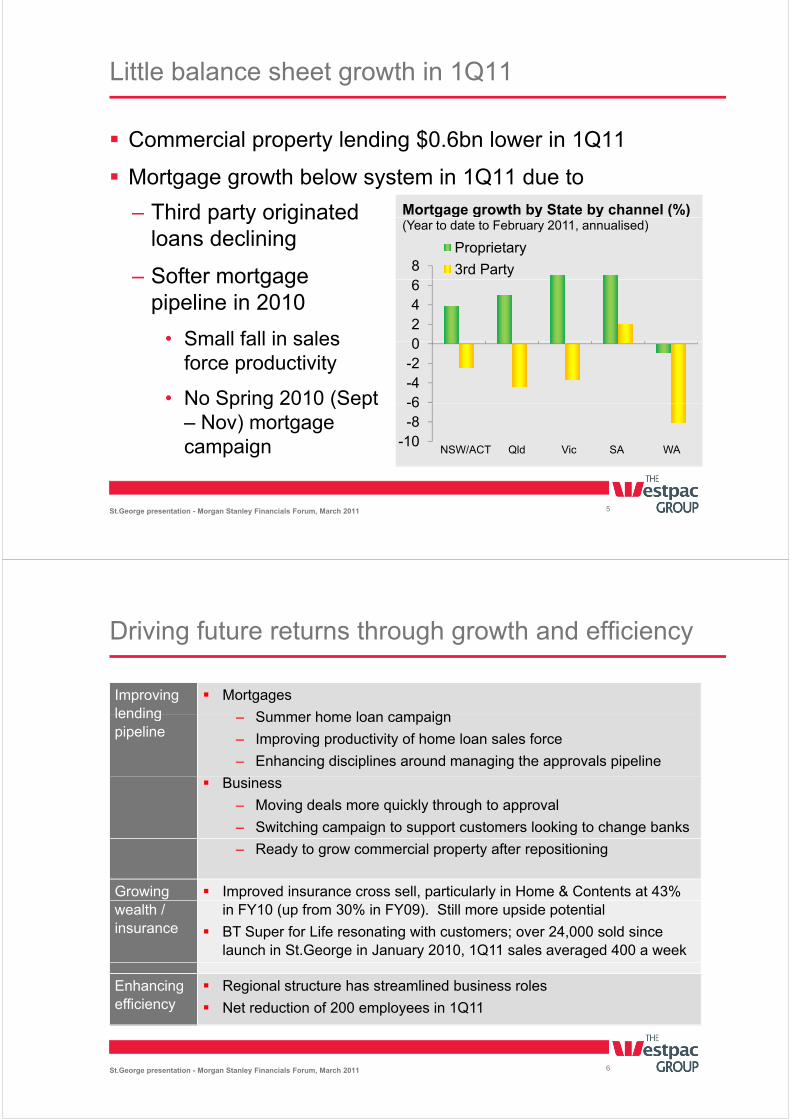

Little balance sheet growth in 1Q11

Commercial property lending $0.6bn lower in 1Q11

Mortgage growth below system in 1Q11 due to

– Third party originated Mortgage growth by State by channel (%) Third party originated loans declining

– Softer mortgage8

Proprietary

3rd Party

g g g y y ( )(Year to date to February 2011, annualised)

Softer mortgage pipeline in 2010

• Small fall in sales 02 4 6

Small fall in sales force productivity

• No Spring 2010 (Sept -6-4 -2 0

No Spring 2010 (Sept – Nov) mortgage campaign -10

-8 -6

NSW/ACT Qld Vic SA WA

5

St.George presentation - Morgan Stanley Financials Forum, March 2011

Driving future returns through growth and efficiency

Improving lending

Mortgages

Summer home loan campaignlending pipeline

– Summer home loan campaign

– Improving productivity of home loan sales force

– Enhancing disciplines around managing the approvals pipeline

Business

– Moving deals more quickly through to approval

– Switching campaign to support customers looking to change banks

– Ready to grow commercial property after repositioning

Growing Improved insurance cross sell, particularly in Home & Contents at 43% wealth / insurance

in FY10 (up from 30% in FY09). Still more upside potential

BT Super for Life resonating with customers; over 24,000 sold since launch in St.George in January 2010, 1Q11 sales averaged 400 a week

Enhancing efficiency

Regional structure has streamlined business roles

Net reduction of 200 employees in 1Q11

6 St.George presentation - Morgan Stanley Financials Forum, March 2011

Bank of Melbourne a unique strategic opportunity

Building our multi-brand franchise

Westpac, nationwide brand and network across Australia franchise

Victoria is a very large and attractive banking market

a d e o ac oss us a a

g

There is no sizable ‘strong local bank’ presence

Customers are seeking a strong local player

St.George already well placed with around 4%

k t h dmarket share and opportunity to leverage proven multi-brand capability

7 St.George presentation - Morgan Stanley Financials Forum, March 2011

Victoria: an attractive banking market

Attractive Market Victoria is the second largest

Regional bank footings by State1 (% of consumer footings)

Regionals outside home state 25%

Victoria is the second largest banking market in Australia with a consistent growth profile C t f ti hi hl

(% of consumer footings)

Non-local regionals (includes St.George in Vic, Qld and WA)

24% 23%

20%

Customer footings highly concentrated in Melbourne

Bendigo &

Average Regional

Share

23% 22%

18%

Bank of Qld

10%

15% Missing Player Regional financial institutions have around 20% market share

Bendigo & Adelaide

Bank 12%

BankSA

Suncorp 5%

10%

in each state. In Victoria the share is only around 12% Other local Victorian players

Bankwest

Bendigo & Ad l id

St.George

0% SA WA QLD NSW &

ACT VIC

Other local Victorian players perceived as rural or too small to be considered a ‘strong local’

Adelaide Bank

8 St.George presentation - Morgan Stanley Financials Forum, March 2011

1. Source: Roy Morgan Research Jan-Dec 2010, Respondents aged 14+, mainly excludes small business. Footings include Deposits and Transactions, Mortgages, Personal Lending and Major Cards.

Well positioned to capitalise on the local opportunity

The Bank of Melbourne brand is unique

Through BankSA and St.George, The Group has a successful track record of managing regional banks

The bulk of new customers expected to come from other major banks

Ability to grow the franchise will be supported by

– Strong customer preferences making it difficult for tit t d f d hcompetitors to defend share

– National networks limit the ability of competitors to respond locallyrespond locally

– Difficult for competitors to replicate

9 St.George presentation - Morgan Stanley Financials Forum, March 2011

Bank of Melbourne - Victoria’s brand

Bank of Melbourne launching in August 20112011

– Rebranding 34 St.George branches

– Tripling the size of the network over 5 years

– Building a bank for Victorians

Significant changes to the networkSignificant changes to the network including a new format of branches and moving responsibility closer to the front lineline

Scott Tanner the new Chief Executive

Local advisory board appointedLocal advisory board appointed

Third local brand of The Westpac Group, adding to St.George and BankSA

10 St.George presentation - Morgan Stanley Financials Forum, March 2011

Bank of Melbourne – a unique opportunity

Taking multi-brand Multi-brand strategy provides more choice and further customer reach

to the next level Supports customers with a preference for a strong local brand

Victoria Australia’s second largest state is under-represented byUnique opportunity

Victoria, Australia s second largest state, is under-represented by regional brands and Victorians are looking for choice

St George has established a strong foundation

Strong brand St.George has established a strong foundation

Launching a well recognised brand combined with further investment will drive higher customer consideration and conversion rates

Ability to deliver The Westpac Group is ‘brand ready’ with established systems, proven capability and depth of experience to develop a bank for Victorians

Financially attractive

Organically expanding in an under-represented market with minimal costs, creates a new growth option with solid returns Australia is limited in the number of regional banks it can support. The Westpac Group will hold three of those positions

11 St.George presentation - Morgan Stanley Financials Forum, March 2011

Summary

St.George has been repositioned with a greater regional focusfocus

Initiatives in place to drive growth and improve efficiency

Our local brands hold a unique and strong position throughout Australia

– St.George repositioned and has business and consumer advocacy levels ahead of all the majors

– BankSA is the largest bank in South Australia and considered their local bank

– Bank of Melbourne has a unique opportunity in Victoria with significant expansion plans

12 St.George presentation - Morgan Stanley Financials Forum, March 2011

Disclaimer

The material contained in this presentation is intended to be general background information on Westpac Banking Corporation (“Westpac”) and its activities.

The information is supplied in summary form and is therefore not necessarily complete Also it is not intended that it be relied upon as advice toThe information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs.

The material contained in this presentation may include information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information.

All t i A t li d ll l th i i di t dAll amounts are in Australian dollars unless otherwise indicated.

Disclosure regarding forward-looking statements

This presentation contains statements that constitute ‘future matters’ within the meaning of Section 728(2) of the Corporations Act 2001 and/or ‘forward looking statements’ within the meaning of Section 21E of the US Securities Exchange Act of 1934 The forward looking statementsforward- looking statements within the meaning of Section 21E of the US Securities Exchange Act of 1934. The forward-looking statements include statements regarding our intent, belief or current expectations with respect to our business and operations, strategy, market conditions, results of operations and financial condition.

We use words such as ‘will’, ‘may’, ‘expect’, 'indicative', ‘intend’, ‘seek’, ‘would’, ‘should’, ‘could’, ‘continue’, ‘plan’, ‘probability’, ‘risk’, ‘forecast’, ‘likely’, ‘estimate’, ‘anticipate’, ‘believe’, or similar words to identify forward-looking statements. These statements reflect our current views with respect to future events and are subject to change certain risks uncertainties and assumptions which are in many instances beyond our controlrespect to future events and are subject to change, certain risks, uncertainties and assumptions which are, in many instances, beyond our control and have been made based upon management’s expectations and beliefs concerning future developments and their potential effect upon us. Should one or more of the risks or uncertainties materialise, or should underlying assumptions prove incorrect, actual results may vary materially from the expectations described in this presentation. Factors that may impact on the forward-looking statements made include those described in the section entitled In Westpac’s 2010 Annual Report available at www.westpac.com.au. When relying on forward-looking statements to make decisions with respect to us, investors and others should carefully consider such factors and other uncertainties and events. We are under no obligation, and do not intend, to update any forward-looking statements contained in this presentation.

13 St.George presentation - Morgan Stanley Financials Forum, March 2011

St.George’s Regional B k P tf liBank Portfolio

APPENDIX

Westpac Banking Corporation ABN 33 007 457 141

Regional bank customers prefer a strong local bank

% agree with statement Regionals

Care Bank Wary

Rational Buyer

Prefer Big 4

N Bi 4 b k lik l t b t dNon-Big 4 banks are more likely to care about me and my needs

96% 43% 49% 16%

The best thing about the non-Big 4 banks is that they care more about customers

93% 35% 42% 18%

The Big 4 banks just care about making money, not helping customers

92% 98% 30% 32%

If they had the same rates and fees I would prefer to bank with a non-Big 4 bank

89% 53% 42% 7%

g

If they had the same network, I'd prefer to bank with a non-Big 4 bank

87% 60% 52% 8%

The best non-Big 4 banks are the ones that are local to our state

58% 39% 33% 27% our state

Customer service in the Big-4 banks has improved in recent years

22% 6% 55% 58%

The non-Big 4 banks just care about making money, h l i

12% 53% 15% 21%not helping customers

12% 53% 15% 21%

I'd avoid using anyone but a Big 4 bank because of the risk of losing my money

9% 16% 13% 67%

Clear preference for a strong local bankClear preference for a strong local bank

St.George presentation - Morgan Stanley Financials Forum, March 2011