Embed Size (px)

Citation preview

The failure of a partner to make a required capital contribution

places strain on a real estate venture. It results in a capital

shortfall and puts the partners at odds. For these and other

reasons, the contribution default remedies play an important

role in many, if not most, real estate venture agreements. Unfor-

tunately, drafting these remedies can be complicated and the

partners may not always have the time or patience to

ensure that the remedies are harmonized and operate the

way they would expect had they thought about it. It is there-

fore helpful to think through these provisions in advance,

and be prepared with useful forms and guidance, to work

within the time limitations of any particular transaction.

4 BUSINESS ENTITIES November/December 2013

CAPITAL CONTRIBUTION DEFAULT

CONTRIBUTIONDEFAULT REMEDIES

CONTRIBUTIONDEFAULT REMEDIESIN A REAL ESTATE VENTURE

S T E V E N S A . C A R E Y , D A N I E L B . G U G G E N H E I M , A N D M I C H A E L D . S O E J O T O

BUSINESS ENTITIES 5

Contribution default remedies play an important rolein many real estate venture agreements, and forms or sample provisions will not work for every deal andshould be adapted to meet the needs of the parties.

Part 1: Scope and TerminologyThis article discusses the followingpoints to be considered, when draftingor choosing contribution default reme-dies: • Potential consequences (and alter-native formulations) of the right towithdraw a contribution when theother partner in a two-partner ven-ture fails to contribute.

• Alternative ways to treat a capital calladvanced by only one partner in atwo-partner venture.

• How these provisions may becomemore complicated when there aremore than two partners.

• Other remedies of the funding part-ner, and the enforceability of contri-bution default remedies generally.

• Third-party creditor issues.Partnership terminology is used in

this article, but the discussion generallyapplies equally to limited liability com-panies (LLCs). Sample contributiondefault remedy provisions (the SampleProvisions) are included in Exhibit 1 toprovide a frame of reference.1 For sim-plicity, it is assumed, unless otherwisestated, that there are only two partners—an investor and an operator. For the mostpart, discussion is presented from thevantage point of a non-defaulting investor(although many, if not most, of a non-defaulting investor’s concerns may beshared by a non-defaulting operator).

Part 2: General Drafting Approach—Less Is More; All or NothingAttorneys and clients may be tempted,when creating a form, or even a specificpartnership agreement, to cover everypossibility in order to give the client max-imum protection and flexibility. Howev-er, a balance must be struck betweenthorough drafting, on the one hand, andconsummating a transaction in a timelyand cost-effective manner, on the otherhand. This balance is clearly a concernwhen providing for contribution defaultremedies because of the potential com-plexities and interrelationships of the

alternative remedies involved. In this con-text, one is often well served by the prin-ciple that “less is more.”

Partial Contributions. A good exam-ple is the issue of partial contributions.The Sample Provisions do not allowfor partial contributions. If a partneradvances less than a l l of what isrequired of it, the Sample Provisionsprovide for a refund of any partialadvance made. Similarly, a non-default-ing partner is not permitted to advanceless than all of the deficiency (Defi-ciency) which, as used herein, meansthe entire amount required to have beencontributed by the defaulting partner.Although one might appreciate havingthe flexibility to make partial contri-butions, the approach taken here (i.e.,all or nothing) was chosen because itinvolves less language and is less com-plicated (avoiding, among other mat-ters, the need to provide for and address

the consequences of contribution cred-it for a defaulting partner’s partial con-tributions).2 This may not be a perfectsolution in all transactions, but in manytransactions it can be a helpful simpli-fication that will make the contribu-tion default remedies more manageable.With these general notions in mind,the remedies for contribution defaultswill be discussed below.

Part 3: Funding Partner InitialDecision—To Fund or Not To FundWhen there is a capital call, and onepartner timely contributes its share andthe other does not, the Sample Provi-sions (like many partnership agree-ments) require the funding partner tomake a decision either to withdraw itscontribution or to advance the contri-bution of the defaulting partner.3 Thisdecision raises questions.

Withdrawal of Contribution. If thecontribution is withdrawn: • How will the partnership meet itscapital needs without the capital thathas been called? The Sample Provi-

6 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

Stevens A. Carey and Daniel B. Guggenheim are transactional partners and Michael D. Soejoto is a tax partner withPircher, Nichols & Meeks, a real estate law firm with offices in Los Angeles and Chicago. The authors thank John Cauble,John Delnero, Ellen Fleishhacker, Richard Kaplan, Kaleb Keller, Jeff Rosenthal, and Bruce Speiser for providing com-ments on prior drafts of this article, Ariel Robinson for her research assistance, and Kaleb Keller and Tim Durkin forcite checking. This article is not intended to provide legal advice. The views expressed (which may vary dependingon the context) are not necessarily those of the individuals mentioned above or Pircher, Nichols & Meeks. Any errorsare those of the authors.

BUSINESS ENTITIES 7C APITAL CONTRIBUTION DEFAULT November/December 2013

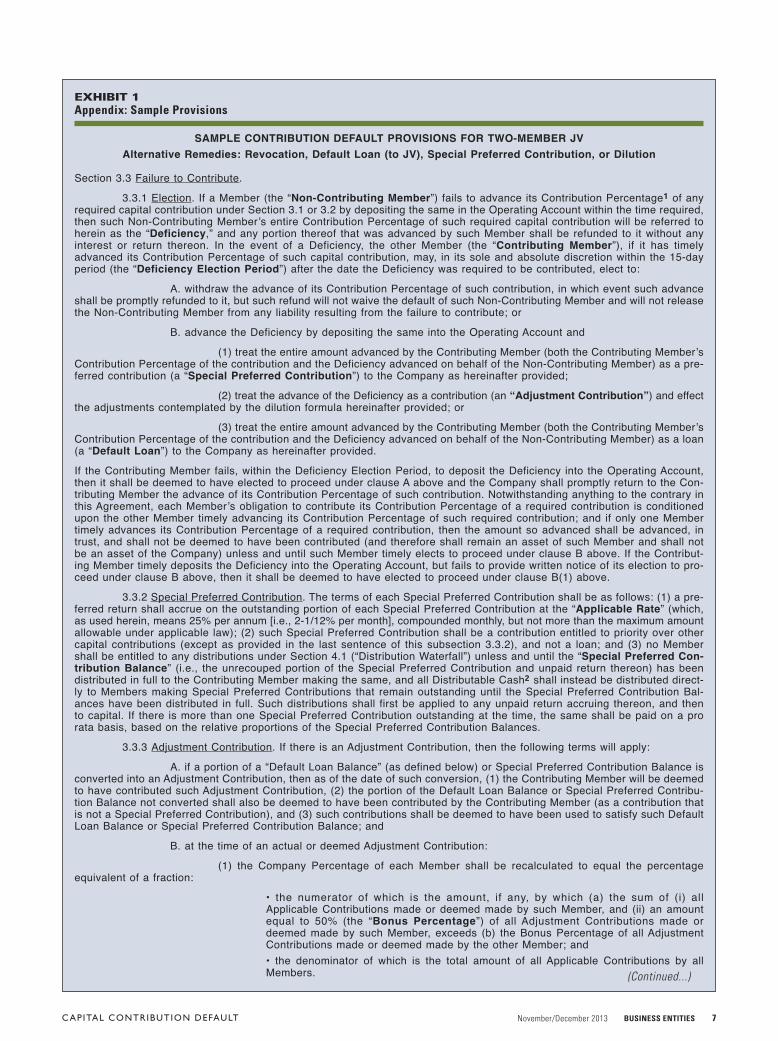

EXHIBIT 1Appendix: Sample Provisions

SAMPLE CONTRIBUTION DEFAULT PROVISIONS FOR TWO-MEMBER JVAlternative Remedies: Revocation, Default Loan (to JV), Special Preferred Contribution, or Dilution

Section 3.3 Failure to Contribute.3.3.1 Election. If a Member (the “Non-Contributing Member”) fails to advance its Contribution Percentage1 of any

required capital contribution under Section 3.1 or 3.2 by depositing the same in the Operating Account within the time required,then such Non-Contributing Member’s entire Contribution Percentage of such required capital contribution will be referred toherein as the “Deficiency,” and any portion thereof that was advanced by such Member shall be refunded to it without anyinterest or return thereon. In the event of a Deficiency, the other Member (the “Contributing Member”), if it has timelyadvanced its Contribution Percentage of such capital contribution, may, in its sole and absolute discretion within the 15-dayperiod (the “Deficiency Election Period”) after the date the Deficiency was required to be contributed, elect to:

A. withdraw the advance of its Contribution Percentage of such contribution, in which event such advanceshall be promptly refunded to it, but such refund will not waive the default of such Non-Contributing Member and will not releasethe Non-Contributing Member from any liability resulting from the failure to contribute; or

B. advance the Deficiency by depositing the same into the Operating Account and(1) treat the entire amount advanced by the Contributing Member (both the Contributing Member’s

Contribution Percentage of the contribution and the Deficiency advanced on behalf of the Non-Contributing Member) as a pre-ferred contribution (a “Special Preferred Contribution”) to the Company as hereinafter provided;

(2) treat the advance of the Deficiency as a contribution (an “Adjustment Contribution”) and effectthe adjustments contemplated by the dilution formula hereinafter provided; or

(3) treat the entire amount advanced by the Contributing Member (both the Contributing Member’sContribution Percentage of the contribution and the Deficiency advanced on behalf of the Non-Contributing Member) as a loan(a “Default Loan”) to the Company as hereinafter provided.If the Contributing Member fails, within the Deficiency Election Period, to deposit the Deficiency into the Operating Account,then it shall be deemed to have elected to proceed under clause A above and the Company shall promptly return to the Con-tributing Member the advance of its Contribution Percentage of such contribution. Notwithstanding anything to the contrary inthis Agreement, each Member’s obligation to contribute its Contribution Percentage of a required contribution is conditionedupon the other Member timely advancing its Contribution Percentage of such required contribution; and if only one Membertimely advances its Contribution Percentage of a required contribution, then the amount so advanced shall be advanced, intrust, and shall not be deemed to have been contributed (and therefore shall remain an asset of such Member and shall notbe an asset of the Company) unless and until such Member timely elects to proceed under clause B above. If the Contribut-ing Member timely deposits the Deficiency into the Operating Account, but fails to provide written notice of its election to pro-ceed under clause B above, then it shall be deemed to have elected to proceed under clause B(1) above.

3.3.2 Special Preferred Contribution. The terms of each Special Preferred Contribution shall be as follows: (1) a pre-ferred return shall accrue on the outstanding portion of each Special Preferred Contribution at the “Applicable Rate” (which,as used herein, means 25% per annum [i.e., 2-1/12% per month], compounded monthly, but not more than the maximum amountallowable under applicable law); (2) such Special Preferred Contribution shall be a contribution entitled to priority over othercapital contributions (except as provided in the last sentence of this subsection 3.3.2), and not a loan; and (3) no Membershall be entitled to any distributions under Section 4.1 (“Distribution Waterfall”) unless and until the “Special Preferred Con-tribution Balance” (i.e., the unrecouped portion of the Special Preferred Contribution and unpaid return thereon) has beendistributed in full to the Contributing Member making the same, and all Distributable Cash2 shall instead be distributed direct-ly to Members making Special Preferred Contributions that remain outstanding until the Special Preferred Contribution Bal-ances have been distributed in full. Such distributions shall first be applied to any unpaid return accruing thereon, and thento capital. If there is more than one Special Preferred Contribution outstanding at the time, the same shall be paid on a prorata basis, based on the relative proportions of the Special Preferred Contribution Balances.

3.3.3 Adjustment Contribution. If there is an Adjustment Contribution, then the following terms will apply:A. if a portion of a “Default Loan Balance” (as defined below) or Special Preferred Contribution Balance is

converted into an Adjustment Contribution, then as of the date of such conversion, (1) the Contributing Member will be deemedto have contributed such Adjustment Contribution, (2) the portion of the Default Loan Balance or Special Preferred Contribu-tion Balance not converted shall also be deemed to have been contributed by the Contributing Member (as a contribution thatis not a Special Preferred Contribution), and (3) such contributions shall be deemed to have been used to satisfy such DefaultLoan Balance or Special Preferred Contribution Balance; and

B. at the time of an actual or deemed Adjustment Contribution:(1) the Company Percentage of each Member shall be recalculated to equal the percentage

equivalent of a fraction:• the numerator of which is the amount, if any, by which (a) the sum of (i) all Applicable Contributions made or deemed made by such Member, and (ii) an amount equal to 50% (the “Bonus Percentage”) of all Adjustment Contributions made or deemed made by such Member, exceeds (b) the Bonus Percentage of all AdjustmentContributions made or deemed made by the other Member; and• the denominator of which is the total amount of all Applicable Contributions by all Members. (Continued...)

8 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

EXHIBIT 1Appendix: Sample Provisions (Continued...)

As used herein, “Applicable Contributions” means all contributions made or deemed made to the Company by all Mem-bers, (x) including all Adjustment Contributions (whether actually made or deemed made by reason of a conversion undersubsection 3.3.5B below) and the portions of any Default Loan Balance or Special Preferred Contribution Balance deemedto have been contributed by the Contributing Member under subsection 3.3.3A above, but (y) excluding (i) any contributionmade by Operator in accordance with Section 3.5 (“Reverse Waterfall”) to the extent attributable to distributions under thePromote Clauses3, and (ii) any Special Preferred Contributions;

(2) if Operator is the Non-Contributing Member, then, in addition to the adjustment underclause (1) above, the distributions to Operator under the Promote Clauses shall be reduced by the same proportion as thereduction in Operator’s Company Percentage (and the distributions that are no longer made under the Promote Clauses byreason of this clause (2) shall instead be distributed in accordance with the Company Percentages, as modified underclause (1) above). For example, but without limitation on the foregoing, if Operator’s Company Percentage were reducedfrom 10% to 6% (i.e., a 40% reduction) under subsection 3.3.3B(1) above, and if 20% of the distributions under a particularsubsection of Section 4.1 (“Distribution Waterfall”) were payable under a Promote Clause under that subsection, then such20% amount would be reduced to 12% (i.e., a corresponding 40% reduction) and the remaining 8% would be distributed inaccordance with Company Percentages, as modified above; and

(3) without limitation on the foregoing, if a Member’s Company Percentage is reduced to 0%,then it shall be deemed to have automatically withdrawn from the Company and to have transferred all of such Members’right, title and interest in, and claims against, the Company and all of its rights under this Agreement (including its rights toprofits, capital, distributions, loan repayments, voting and management) to the other Member (and shall execute such docu-mentation as the other Member may reasonably request to confirm the foregoing).

3.3.4 Default Loan. Each Default Loan shall bear interest at the Applicable Rate and shall be due and payableupon written demand, but in no event later than the earlier to occur of dissolution and liquidation of the Company or ten(10) years after the date made. All amounts which would otherwise be distributed to the Members shall be paid instead tothe Contributing Member that makes such Default Loan until the “Default Loan Balance” (i.e., the outstanding amount ofprincipal and interest thereunder) has been paid in full. (For avoidance of doubt, Distributable Cash available for distributionto the Members shall not include amounts payable in respect of any Default Loan, but rather shall be net of all suchamounts.) Such payments shall be applied first to interest and then to principal. If there is more than one Default Loan out-standing at the time, payments shall be allocated to such Default Loans pro rata in accordance with the relative DefaultLoan Balances.

3.3.5 Default Loans and Special Preferred Contributions; Priority and Conversion.A. There shall be no distributions in respect of any Special Preferred Contribution, or any return thereon,

while there is any outstanding principal or interest under any Default Loan.B. For so long as any Default Loan Balance or Special Preferred Contribution Balance is outstanding,

the Contributing Member shall have the right to convert a portion (equal to the ratio of the Deficiency to the aggregate ofthe capital call that gave rise to the Deficiency) of the then balance of the same to an Adjustment Contribution effectiveimmediately upon written notice to the Non-Contributing Member.

3.3.6 Non-Exclusive Remedies. The rights of the Company and the Members pursuant to this Section 3.3 are notexclusive and shall not be deemed to waive any other right or remedy of the Company or any Member under this Agree-ment, at law or in equity, against any Non-Contributing Member for failure to make any required capital contribution. Once aDefault Loan, Special Contribution or Adjustment Contribution has been made (or deemed made), no subsequent paymentor tender by the Non-Contributing Member in respect of the Default Loan, Special Preferred Contribution or AdjustmentContribution may be made to reduce the same or affect the Company Percentages of the Members, as adjusted in accor-dance with this Section.1 This Contribution Percentage is defined to be the Company Percentage unless the contribution in question is governed by a reverse waterfall(as discussed in Carey, “Real Estate JV Promote Calculations: Recycling Profits,” Real Est. Fin. J. (Summer 2006), in which event it means theapplicable percentage required by the reverse waterfall.2 Distributable Cash might typically be defined as the amount of cash determined to be available for distribution after taking into account futurecapital requirements, reserves, and restrictions under loan documents.3 If, for example, a particular level of the distribution waterfall provides for cash to be distributed (a) 80% to the members in proportion to theirrespective company percentages and (b) 20% to the operator as promote, then such clause (b) might typically be defined as a “Promote Clause”

1 Partnership terminology is used in the body ofthis article because real estate professionals in ajoint venture commonly refer to one another aspartners. However, with occasional exception(e.g., due to state or foreign tax concerns or forfund documentation), LLCs are most frequentlyused in the authors’ experience, and thereforethe Sample Provisions are LLC provisions.

2 One might not worry about giving any contribu-tion credit to a defaulting partner, but unless par-tial contributions are expressly addressed, equi-table arguments that some credit is appropriateand intended may be raised. It may be expresslyprovided that there is no credit for a partial contri-

bution, but that is likely, in practice, to yield thesame result, namely no partial contributions.

3 It is also possible to allow for the funding ofnone, or less than all, of the Deficiency. But, asdiscussed earlier in connection with partial con-tributions, allowing for this additional flexibilitymay get complicated (particularly when thepartnership agreement allows for loans to thedefaulting partner). These additional alterna-tives are not covered by the Sample Provisions.

4 See, e.g., Cal. Corp. Code §§ 15905.02(c) and17704.03(c) (2013); 6 Del. C. §§ 17-502(b)(1)and 18-502(b) (2013). Cf. Cal. Corp. Code§ 17201. See also Part 7.1, infra. Note that this

article presumes that the California RevisedUniform Limited Liability Company Act (i.e.,Cal. Corp. Code 17701.01 et seq.) will takeeffect on 1/1/2014, without having beenamended after this article was submitted to thepublisher, and will thereupon apply to the cir-cumstances discussed in this article in all rele-vant respects. See Cal. Corp. Code § 17713.04(a). Cf. Cal. Corp. Code § 17713.04(b).However, at least one commentator has ques-tioned the constitutionality of the new Act, andseveral have raised concern that confusionmay arise because new Section 17713.04(a)provides that (except as provided in the new

sions do not address this problem,but it should be considered, espe-cially at the time the election is made.

• Might the withdrawn contributionbe subject to a clawback by part-nership creditors if a creditor hadrelied on the underlying contribu-tion obligation4 or if the refund wasa fraudulent transfer5 or a distribu-tion in violation of the applicablepartnership or limited liability com-pany act?6 The Sample Provisionsattempt to mitigate this concern byproviding that each partner’s oblig-ation to contribute its share of arequired contribution is conditionedupon the timely advance of the oth-er partner’s share, and that, if theother partner fails to timely advanceits share, the funding partner is notdeemed to have made a contribu-tion (and thus has not created apartnership asset) unless it affir-matively elects not to withdraw itsadvance during a 15-day electionperiod.7

• Should the funding partner receive areturn on its money for the periodthe money is held by the partnership?Unlike the Sample Provisions, somepartnership agreements provide forsuch a return. But consider where themoney to pay such a return will comefrom—will an additional capital callbe necessary to pay it, and if so doesa nominal amount of money warrantdealing with such logistical concerns?Moreover, is payment of a return(unless it is made solely and directly

by the defaulting partner) inconsistentwith the position suggested above, inthe discussion of partnership credi-tors, that the refunded advance wasnever an asset of the partnership?

• Will the default be forgiven? TheSample Provisions provide that therewill be no release of liability by rea-son of the withdrawal of the fundingpartner’s contribution.8 However,some partnership agreements pro-vide otherwise.Advance of Deficiency. If the con-

tribution is not withdrawn, and insteadthe Deficiency is advanced by the fund-ing partner, how should the Deficien-cy (and the funding par tner’scontribution of its share of the capitalcall) be treated? There are several alter-natives, including the following: • Preferred contribution: treating thetotal amount funded (i.e., both theregular contribution of the fundingpar tner and the Deficiency itadvances on behalf of the defaultingpartner) as a preferred contribution.

• Dilution: treating the total amountfunded as a contribution and adjust-ing the partnership interests in someway that increases the partnershipinterest of the funding partner (witha corresponding reduction in thepartnership interest of the default-ing partner).

• Loan to partnership: treating the totalamount funded as a loan to the part-nership.

• Loan to defaulting partner: treatingthe advance of the Deficiency as a

loan to the defaulting partner (whichis deemed used by the defaultingpartner to fund its contribution).Not all of these alternatives will be

appropriate in any given transaction andonly the first three are included in theSample Provisions. Each of the alterna-tives identified above will be discussedin more detail below.

3.1. Preferred Contribution to the PartnershipOne alternative is to provide that thefunding partner’s advance of the Defi-ciency, and the funding partner’s regu-lar contribution, are collectively treatedas a preferred contribution to the part-nership, which is recouped together witha return (the “preferred return”)—usu-ally based on a relatively high com-pounded rate—before any otherdistributions are made.

3.1.1 Preferred Contributions:How Much Is Preferred?In the authors’ experience, the Defi-ciency and the funding partner’s regu-lar contribution are usually collectivelytreated as a preferred contribution, asindicated above. In some transactions,however, this collective treatment hasbeen a source of confusion. Some part-ners think that only the Deficiencyshould be preferred. They do not thinkit is fair for the funding partner to get thehigh return that is typically associatedwith a preferred (default) contributionon the entire capital call.

Comparing a Loan to the Default-ing Partner. As a frame of reference,one can compare the preferred contri-bution with a loan to the defaulting part-ner, an alternative remedy discussed inPart 3.4 below. When the funding part-ner makes a loan to the defaulting part-ner, only the Deficiency is loaned andthen repaid together with interest (whichfor purposes of comparison, is assumedto accrue at an interest rate equal to therate of return on a preferred contribu-tion). However, such a default loanwould be repaid by the defaulting part-ner only (and typically the repaymentwould be paid from the distributionsthat would have gone only to the default-ing partner). By contrast, a preferredcontribution is effectively paid by both

BUSINESS ENTITIES 9C APITAL CONTRIBUTION DEFAULT November/December 2013

Act) existing entities will become subject tothe new Act, and new Section 17713.04(b) pro-vides that (except as provided in the new Act)existing contracts entered into by the LLC orby the members of an existing entity (Areexisting “contracts” limited to third-party con-tracts or could they include the operatingagreement?) and will remain subject to theexisting Act. See, e.g., Bishop, “California’sNew LLC Act—Call Me Laocoon, But I ForeseeA Mess!,” Cal. Corp. & Sec. L., 9/24/2012,http://calcorporatelaw.com/2012/09/californias-new-llc-act-call-me-laocoon-but-what-a-mess.Issues might include, for example, whether the

existing Act or the new Act will govern a credi-tor’s enforcement (in 2014 or later) of a contri-bution obligation on which the creditor relied inextending credit to the company (prior to2014). These transition issues are beyond thescope of this article.

5 See, e.g., 11 U.S.C. section 548; Cal. Civ. Code§ 3439.05.

6 See, e.g., Cal. Corp. Code §§ 15905.08, 17254,and 17704.05; 6 Del. C. §§ 17-607 and 18-607.

7 Creditor issues are discussed in more detail inPart 7, infra.

8 See Part 5, infra.

A balance must be struckbetween thorough draftingand consummating a cost-

effective transaction.

partners (being paid by distributionsthat would have gone to both partners).

What is often overlooked (or is notunderstood) is that if distributions aremade in the same proportions as theapplicable contributions were to bemade, then regardless of the rate ofreturn (and equivalent loan interestrate), the partnership will be required todistribute the same amount of total cash(all of which will end up in the fundingpartner’s pocket) (1) to repay a pre-ferred contribution (together with thepreferred return) based on the entirecapital call, or (2) to provide the default-ing partner with the amount necessaryto repay the Deficiency, together withinterest at the equivalent interest rate.9Under these circumstances, the fund-ing partner’s share of the capital calland the preferred return on that amountare effectively paid by the funding part-ner itself (from the portion of the pre-ferred distributions that would havebeen distributed to the funding partnerif they had not been preferred).

Disproportionate Regular Contribu-tions. If only the Deficiency is treated asa preferred contribution, then the part-ners’ regular contributions may be outof sync (e.g., no longer in the same pro-portion as partnership percentages).10

Example 3.1.1. Assume the followingfacts: (1) there is a partnership betweentwo partners, each of which has a 50%interest, and (absent a default) all con-tributions and distributions are to bemade equally; (2) the partners initiallycontribute $100X each, and the only oth-er capital call is for an additional $100X;and (3) one partner fails to make its $50Xadditional contribution, while the otherpartner makes its $50X additional con-tribution and advances the defaultingpartner’s $50X Deficiency. If the entire$100X of additional capital is treated asa preferred contribution, then all distri-butions will be made to the funding part-ner until it receives $100X plus theagreed-upon return. Once that amounthas been distributed, the unrecoupedcontributions would be 50/50, so thatallocating the remaining distributionsequally makes sense. However, if onlythe Deficiency were treated as a preferredcontribution, then the funding partnerwould get all distributions until itrecouped its $50X advance plus the req-uisite return; once the preferred contri-

bution and its return were satisfied, theoutstanding contributions would be$150X for the funding partner and $100Xfor the defaulting partner so that 50/50distributions would be unfair to the fund-ing partner (because of its extra $50X).

This problem could be solved by ahybrid remedy. For example, the part-ners could adjust the distributions sothat after the $50X preferred contribu-tion (and any associated return) is dis-tributed to the funding partner, capitalis refunded 60/40, which matches therat io of remaining contributions($150/$100), and then subsequent dis-tributions remain 50/50 (without adjust-ment). However, that approach is notlikely to be acceptable because it is worsefor the funding partner than having thefunding partner finance the defaultingpartner’s share of the extra $50X ofunpreferred contributions at 0% (tomake the unpreferred contributions$75/$75): the funding partner would begetting neither a return nor a priority onthe extra $50X. Moreover, the fundingpartner would not be getting a propor-tionate increase in its share of profits.

Alternatively, the partners could adjustthe partnership percentages to 60/40 ora more favorable ratio for the fundingpartner (using a bonus or penalty factorto give the funding partner credit formore than its 60% share of actual con-tributions) and provide that all distri-butions are made in this new ratio. But,for reasons discussed in Part 3.2 below,the funding partner may not want to be

10 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

9 The foregoing assumption (i.e., that distributionsare made in the same proportion as the applica-ble contributions are to be made) may not alwaysbe true. Disproportionate distribution schemesare in fact common in partnerships with promotestructures. See Part 3.1.3, infra.

10 The partners’ regular contributions may not beproportionate to their partnership percentages ifthere has previously been a dilution based on abonus or penalty formula; even then, the regularcontributions may not be proportionate to theadjusted partnership percentages (as previouslyadjusted by the dilution formula) if only theDeficiency is treated as a preferred contribution.

11 See Section 511 et seq. regarding UBTI generally.12 See Sections 514(c)(9)(B)(vi)(III), 514(c)(9)(E);McKee, Nelson and Whitmire, Federal Taxation ofPartnerships and Partners, 4th ed. ¶ 9.03[3][c][i](Thomson Reuters/WG&L, 2007) (“Generally,[the fractions] rule requires that allocations to anytax-exempt partner cannot result in that partnerhaving a percentage share of overall partnershipincome for any taxable year greater than thatpartner’s percentage share of overall partnershiploss for the taxable year for which that partner’spercentage loss share will be the smallest...”);Lokey and Loft, “Ventures with Tax-Exempt andForeign Investors,” Wm. & Mary Tax Conf.,

§ IID5d(5)(c) at 18 (2008) (“Any time that a taxablepartner’s capital is subordinate to a qualified orga-nization’s capital, the allocations will not complywith the fractions rule because the tax-exemptpartner will always have a share of net profitshigher than its fractions rule percentage.(Because the tax-exempt partner’s capital issenior, either the agreement must provide thatprofits build its capital account first, to the extentcapital has been torn down, giving the tax-exempt member a 100% share of profits, or itmust tear down the capital of the subordinatedmembers first, giving the tax-exempt member a0% share of overall losses.)”). See also Kahn,“Help With Fractions: A Fractions Rule Primer,”126 Tax Notes 953 (2/22/2010); Fass, Haft,Loffman, and Presant, Tax Aspects of Real EstateInvestments (West Publishing, 2005), 1A § 13:20.

13 See Section 514(c)(9)(E)(ii)(II); Regs. 1.514(c)-2(c)(1)(ii) and 1.514(c)-2(d) (as amended in 2003).

14 Reg. 1.514(c)-2(d)(4)(ii).15 Kahn, note 12, supra, at 963 n.52.16 See note 12, supra.17 Reg. 1.514(c)-2(g).18 For concerns regarding the application of the frac-tions rule to preferred contributions resultingfrom a contribution default, see Letter from Chair

forced to elect a dilution remedy (even ifthere is a bonus or penalty factor). Forthese reasons (and to avoid the atten-dant complications), no such hybrid rem-edy is included in the Sample Provisions.

3.1.2 Preferred Contributions: Tax IssuesPreferred contributions may cause taxproblems for certain tax-exempt part-ners (or direct or indirect tax-exemptinvestors in a partner) that are subjectto tax on unrelated business taxableincome (UBTI).11 Specifically, preferredcontributions may violate the “fractionsrule” (which, in general terms, limitsthe shifting of losses from a tax-exemptpartner to a taxable partner or incomefrom a taxable partner to a tax-exemptpartner).12 There are exceptions for“reasonable preferred returns” and “rea-sonable guaranteed payments.”13 Butthe safe harbor “commercially reason-able” rate14 is usually (in the authors’experience) much less than the desiredrate of return for preferred contribu-tions in the default context, and “[t]hereis an absence of guidance on how adetermination regarding reasonable-ness would be made.”15 Moreover, evenif one ignores the preferred return oncapital, the repayment of the capitalitself is still preferred and the resultingsubordination of the other capital mayresult in a fractions rule violation(because it could cause losses to be allo-cated away from the fractions rule sen-sitive partner).16

There is an exclusion for “unlikelylosses,”17 but the examples in the regu-lations do not include unanticipateddefaults and many practitioners are notwilling to rely on this exclusion.18 Tomake matters worse, a fractions ruleviolation may occur even if the pre-ferred contributions are never made (i.e.,the right to make preferred contribu-tions may in itself be violative).19 How-ever, compliance with the fractions ruleis relevant only if there is at least onedirect or indirect partner in the part-nership that is a “qualified organiza-tion”20 and (as is usually the case) thereis at least one direct or indirect partnerin the partnership that is not,21 and maybe avoided with appropriate structur-ing, typically by investing through a realestate investment trust (REIT) or a cor-

BUSINESS ENTITIES 11C APITAL CONTRIBUTION DEFAULT November/December 2013

of Taxation Section of ABA to IRS Commissionerregarding “Comments Concerning PartnershipAllocations Permitted Under Section 514(c)(9)(E)”(1/19/2010), available at http://www.americanbar.org/content/dam/aba/migrated/tax/pubpoli-cy/2010/comments_concerning_partnership_allo-cations.authcheckdam.pdf [hereinafter ABATaxation Section Letter].

19 The fractions rule applies on both an actual andprospective basis. Reg. 1.514(c)-2(b)(2)(i). “Thus,subject to [certain exceptions], if the partnershipcould allocate a percentage of overall partnershipincome in any year to a qualifying tax-exemptpartner in excess of that partner’s fractions rulepercentage, the partnership violates the fractionsrule.” Kahn, note 12, supra at 961.

20 The term “qualified organization” is defined inSection 514(c)(9)(C) and includes trusts forming apart of a qualified employee benefit plan andexempt educational organizations (e.g., collegesand universities) and certain affiliated supportorganizations (endowments). The Section514(c)(9) exception is available only to “qualifiedorganizations” in connection with debt incurred inacquiring or improving real property (or debtincurred after acquisition or improvement if incur-ring such debt was “reasonably foreseeable”),and only when the several requirements of

Section 514(c)(9), of which the fractions rule isone, are met. The fractions rule may seem irrele-vant if (1) the Section 514(c)(9) exemption is nototherwise available (e.g., because the acquisitiondebt relates to personal rather than real propertyor one of the other requirements of Section514(c)(9), aside from the fractions rule, is notmet), or (2) subject to the next sentence, allincome from the partnership’s investment will beUBTI anyway (e.g., if the only income is from thedevelopment and sale of residential lots as inven-tory). However, if a tax-exempt investor investingthrough the partnership is a qualified organizationand has or may have other partnership invest-ments, fractions rule compliance may still beimportant. See ABA Taxation Section Letter, note18, supra, at 4 (“in a tiered partnership setting,there is concern that violation of the fractions rulewith respect to a lower-tier partnership maycause an upper-tier real estate fund to be treatedas violating the fractions rule with respect to all ofits investments”); id., § VIII at 26-32.

21 Compliance with the fractions rule is not requiredif all of the partners are qualified organizations.Section 514(c)(9)(B)(vi)(I). For this purpose, anorganization is not treated as qualified “if anyincome of such organization is unrelated businesstaxable income.” Section 514(c)(9)(B) (see finalsentence).

poration.22 Consequently, the preferredcontribution remedy is often, if not usu-ally, omitted in deals involving quali-fied organizations that do not use aREIT or a corporate blocker.

3.1.3 Preferred Contributions:Impact on PromotePreferred contributions may accelerateor defer the operator’s promote relative toa loan to the operator as defaulting part-ner (depending on whether the preferredcontribution rate is lower or higher thanthe promote hurdle rate). However, in theauthors’ experience, promote considera-tions generally have not been a deterrentto using preferred contributions. Thissubject is addressed in another article,which discusses a possible solution thatmay avoid any impact on the timing andamount of the promote (relative to thetiming and amount when there is a loanto the defaulting partner).23

3.2 DilutionAnother alternative is to treat the entireamount funded by the funding partner(i.e., both its regular contribution andits advance of the Deficiency) as a capi-tal contribution and adjust the partner-ship interests through what is often calleda “dilution” or “squeeze-down” formula.There are many possible dilution for-mulas.24 Most dilution formulas encoun-tered by the authors are either (1)“non-punitive” or “pro rata” formulas thatadjust the partnership percentages to beproportionate to capital contributions or(2) penalty or bonus formulas that inflatethe capital credit for the capital con-tributed by the funding partner.

Pro Rata Capital Formulas: Adjust-ment Based on Actual Capital of Fund-ing Partner. The simplest dilutionformula adjusts partnership percent-ages so that they are proportionate tothe actual capital contributed. In theauthors’ experience, this formula is typ-ically based on total capital contribu-t ions ( i .e . , gross contr ibut ionsdetermined without regard to distri-butions) as in Example 3.2.1A below.Alternatively, the formula may be basedon outstanding capital contributions(i.e., net contributions determined bydeducting distributions, but not a neg-ative amount) as in Example 3.2.1B

below. In either case, such a formula issometimes called a “pro rata” or “non-punitive” dilution formula. But, asexplained below, it can be punitive toeither the defaulting or the fundingpartner depending on whether theequity value (i.e., the net fair marketvalue of the partnership’s assets at thetime of comparison, after deductingdebt and other liabilities) is more orless than the equity capital (i.e., actu-al capital contributions) taken intoaccount.25 To protect against unin-tended bad results for the funding part-ner, it is common to provide for one ormore alternatives to dilution, such asthe preferred contribution remedydescribed above and the loan reme-dies described below.

Penalty Capital Formulas: Adjust-ment Based on Inflated Capital ofFunding Partner. More often than not,in the experience of the authors, a dilu-tion formula gives the funding part-ner credit for more than 100% of thecapital it advances on behalf of thedefaulting partner (and sometimeseven the capital it contributes on itsown behalf ).26 This approach obvi-ously increases the benefit to the fund-ing partner when equity value is equalto or more than the equity capital tak-en into account, but may or may notavoid an additional loss to the fundingpartner when equity value is less thanequity capital. For this reason, the pre-cautions taken for pro rata dilutionformulas are commonly taken forpenalty formulas as well. A dilutionformula rarely appears in isolation asthe only remedy for the funding part-ner, and it is not likely to be used whenthe equity value is less than the equitycapital taken into account in the dilu-tion formula.

3.2.1 Dilution: Capital vs. Value-Based FormulasThe dilution formulas described above(and the formulas in the Sample Provi-sions) are based on capital invested with-out regard to the actual value of eachpartner’s interest or the partnership’sassets. The consequences may vary (dra-matically and perhaps unexpectedly)depending on the discrepancy, at thetime of the adjustment, between thepartners’ respective shares of total cap-

ital taken into account in the dilutionformula and the partners’ respectiveshares of equity value.

Not Sufficiently Protective. Some-times the dilution formula may notprotect the funding partner and couldeven benefit the defaulting partner.Consider the following example:

Example 3.2.1A. Assume the follow-ing facts: (1) there is a 50/50 partnership;(2) there is a $20 million aggregate cap-ital commitment; (3) the partnershipagreement provides that if a partner failsto put in its share of capital, the part-nership interests will be adjusted toreflect the relative proportions of capi-tal contributed (for simplicity, no bonusfactor is included); (4) each of the part-ners contributes $5 million to acquire a$10 million office building, which isimmediately sold for a huge profit beforeany further contributions are made; and(5) the remaining $10 million is latercalled to purchase a second building.

Under the facts of this example, eachof the partners has a 50% interest at thetime of the second capital call and eachpartner has received a return of all itsprior capital contributions. If one of thepartners elects not to fund its share, andthe other partner funds the entireamount, of the second capital call, thenthe partnership interests would beadjusted to 75% and 25%, respectively.Despite failing to fund any portion ofthe $10 million investment, the default-ing partner would end up with the wind-fall of a 25% interest in the partnership!

Too Protective. One might quibblewith the prior example because thepartners had no outstanding capital atthe time of the second capital call.

12 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

22 See, e.g., Taylor, ‘Blockers,’ ‘Stoppers,’ and theEntity Classification Rules,” 64 Tax Law. 6 (Fall2010); Berg, Fisch, and Tattenbaum, “UsingPrivate REITs to Minimize UBTI in Real EstateInvestment Funds,” 18 Real Est. Fin. J. 36 (Winter2003); Morgan and Tomlinson, “Tax-ExemptsChallenge Private Fund Sponsors,” N.Y. L.J.(10/3/2006).

23 See Carey, “Partner Loans to Fund Capital CallShortfalls in Real Estate Partnerships: Loan toNon-Contributing Partner vs. Loan to Partnership,”5 Real Est. Industry L. Rep. 26, at 917 (12/25/2012) (hereinafter Carey, Partner Loans).

24 See Carey, “Squeeze-down Formulas: Do TheyWork the Way You Think They Do?,” Real Est. Fin.J. 43 (Fall 1997) (hereinafter Carey, Squeeze-down Formulas).

25 Id.26 See Carey, Squeeze-down Formulas at 50 (dis-cussion of “entire base” formulas).

27 See Carey, Squeeze-down Formulas at 45-47.

Would basing the dilution formula onoutstanding capital be a better solu-tion? Unfortunately, this alternativeapproach also has problems and maysometimes be too punitive, as illus-trated by the following example:

Example 3.2.1B.Assume the followingfacts: (1) there is a 50/50 partnershipwhich acquires an office building at abelow-market price in a rising market;(2) the partnership refinances the build-ing and each of the partners recoups allof its capital and there are still millionsof dollars of equity; (3) there is then arelatively small capital call (the first addi-tional capital contribution) for $10,000to cover an operating deficit; and (4) thepartnership agreement provides that if apartner defaults in its obligation to con-tribute required capital, the partnershipinterests will be adjusted to reflect the rel-ative proportions of the partners’ out-standing capital contributions.

At the time of the small capital call,the partners have no outstanding capi-tal. Consequently, if one of the partners

fails to contribute its share, it would loseits entire interest in the partnership (andits share of millions of dollars of equity)!

Discrepancies with Value. The bot-tom line is that a capital-based dilutionformula may yield strange results whenthe partnership’s equity value is signifi-cantly different than the capital takeninto account in the dilution formula. Inthe examples above, the disparities wereexaggerated by distributions: the equi-ty value was much less than the rele-vant capital in Example 3.2.1A ($10million of equity value vs. $20 million ofcapital); and the equity value was muchmore than the relevant capital in Exam-ple 3.2.1B (millions of value vs. nomi-nal capital). But the problem may existeven before any distribution has beenmade: if there has been appreciation orloss in the partnership’s equity value,then the corresponding value associat-ed with each new dollar of capital maybe more or less than $1 respectively.

Why not use a fair market valueadjustment to avoid this problem? While

a fair market value dilution formulamight be more precise, such formulasare rare in the authors’ experiencebecause of the time and costs involvedin determining value and the potentialfor disputes.27

3.2.2 Dilution: What Is Being Adjusted?It is important that the partners under-stand what is being adjusted under thedilution remedy. Partnership percent-ages are usually modified under a dilu-tion remedy, but what does this meanand is it the only modification?

Right to Receive Future Distribu-tions. Partnership percentages are typ-ically used to establish how certain(and sometimes all) distributions aremade. Thus, the partners’ shares of dis-tributions that are made in accordancewith partnership percentages will beadjusted accordingly. As illustrated inPart 3.2.3 below, the impact of theadjustment to distribution sharing mayvary depending on the other provi-sions of the partnership agreement.

Obligation to Make Future Contri-butions. Partnership percentages mayalso be used to establish how the obli-gation to make certain (and sometimesall) contributions is shared. But notalways. Sometimes a dilution formuladoes not adjust the partners’ shares offuture contributions. Although suchan approach might be important to apartner with limited capital who maynot be able to meet the burden of alarger capital commitment, it maybecome very draconian depending onhow distributions are adjusted. To takean extreme example, imagine a partner,whose original partnership percentagewas 50%, is entitled to only 5% of part-nership distributions (by reason of theapplication of a dilution formula) butis still required to contribute 50% of allcontributions.

Pro Rata vs. Penalty Capital Adjust-ment Formulas. In a pro rata capitaladjustment formula, the adjustmentsare straightforward. The funding part-ner has contributed more capital thanexpected and the defaulting partnerhas contr ibuted less capital thanexpected, but each is simply creditedwith what it has actually contributed.Such a formulation results in obvious

BUSINESS ENTITIES 13C APITAL CONTRIBUTION DEFAULT November/December 2013

adjustments to the total amount of cap-ital each partner has contributed, itscapital account, and its partnershippercentage. The adjustments are morecomplicated and varied when a penal-ty capital adjustment formula is useddue to the additional hypothetical cap-ital credited to the funding partner.

There is a range of possibilities as towhat may be adjusted under the part-nership agreement by the additionalhypothetical contribution. Some part-nership agreements purport to adjust(1) all distributions, (2) only profit dis-tributions after capital contributions havebeen recouped, or (3) only the final lev-el of profit distributions. Some partner-ship agreements also adjust the capitalaccounts by, for example, reducing thedefaulting partner’s capital account, andincreasing the funding partner’s capitalaccount, by the additional hypotheticalcapital.28 Some partners may expect thatsuch a capital shift will occur if the part-nership agreement merely adjusts all ofthe distributions even if there is noexpress adjustment of capital accounts(assuming no capital has been recoupedat the time of the adjustment). Howev-er, it may not. For example, if there isno capital account adjustment and thepartnership agreement requires liquida-tion in accordance with (i.e., in propor-tion to) capital accounts, then thedefaulting partner may get back thebonus penalty (resulting from the addi-tional hypothetical contribution) uponliquidation. Even if there are adjustmentsto the capital accounts, they may be eco-nomically undone by tax allocations.29

Tax Adjustments. Of course, anyadjustment to the economics may alsocause or require adjustments to the taxallocations, but discussion of taxadjustments (and compliance with thefractions rule) in connection with dilu-tion formulas is beyond the scope ofthis article.

Sample Provisions. The SampleProvisions explicitly address only theadjustment of partnership percentagesand the promote percentages. As illus-trated in Part 3.2.3 below, the effect ofthese adjustments may vary dependingon the rest of the partnership agree-ment (e.g., tax and distribution provi-sions) and what actually happens inthe partnership (e.g., the actual con-tributions and distributions).

14 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

28 The capital shift effected by such capital accountprovisions may have a significant tax impact (inaddition to the apparent economic impact).Indeed, such tax consequences are sometimesthe driving force for using these stronger formsof dilution formula, because they may cause capi-tal account balances, future income and loss allo-cations and the determination of a partner’s “frac-tions rule percentage” (i.e., a partner’s smallestshare of overall partnership loss) to be in line withthe intended economic dilution.

29 See, e.g., Cuff, “Drafting Real Estate Partnershipand Entity Agreements,” L.A. Law., January 2006,at 12.

30 See, e.g., id. at 14; Cuff, “Tax Aspects ofPartnership Dilution Procedures,” 1 BET 16(Mar./Apr. 1999); Schneider & O’Connor, “LLCCapital Shifts: Avoiding Problems When ApplyingCorporate Principles”, 92 J. Tax’n 13 (Jan. 2000);BNA Tax Management Portfolio 591-2nd: RealEstate Transactions by Tax-Exempt Entities,II.G.5.a., n.243 (“(changes, resulting from closingor default adjustments during real estate venture,in partners’ shares of partnership’s income andlosses did not cause partnership’s tax allocationsto contravene fractions rule)”) (describing Ltr. Rul.200351032)); Lokey and Loft, note 12, supra,§ IID5d(5)(a) at 18 (“Many partnership agree-ments have a dilution provision in the event apartner fails to make its pro rata share of addition-al capital contributions. The regulations providethat changes in partnership allocations that resultfrom transfers or shifts of partnership interestswill be closely scrutinized, but that they generallywill only be taken into account in determining

whether the agreement satisfies the fractionsrule in the taxable year of the change and subse-quent taxable years. See Reg. 1.514(c)-2(k)(1). Thechange will be closely scrutinized to determinewhether there was a prior agreement, under-standing or plan to cause a shift in partnershipallocations, or if the change was expected fromthe structure of the transaction. See id. Thus,although not free from doubt, a dilution causedby these types of provisions generally shouldconstitute a shift in partnership interests withinthe meaning of this rule, and therefore should notbe taken into account until the dilution provisionsare actually triggered.”); ABA Taxation SectionLetter, note 18, supra (“there is little, if any, guid-ance for determining whether changes to thepartners’ shares of income and losses resultingfrom either a default or reduction in committed orcontributed capital causes a partnership to vio-late, on a prospective basis (after the default orlowered capital contribution), the fractions rule.”).

31 Cal. Rev. and Tax Code § 50 (change in ownershipresults in revised base year value); § 64(c)(1)(“When a person obtains control through director indirect ownership or control of more than 50percent of any corporation, or obtains a majorityownership interest in any legal entity through thetransfer of interests, the transfer shall be achange of ownership of the real property ownedby the entity in which the controlling interest isobtained.”). See also Cal. Rev. and Tax Code§ 64(d) for a possible change in ownership result-ing from transfers of more than 50% of the inter-ests of “original co-owners” who previously tookadvantage of a change in form exemption.

BUSINESS ENTITIES 15C APITAL CONTRIBUTION DEFAULT November/December 2013

3.2.3 Dilution: Interplay withOther Provisions and FactsDilut ion formulas should not beviewed in isolation. To properly assessthe impact of a dilution adjustment,one needs to analyze the entire part-nership agreement, especially the con-t r ibut ion , d is t r ibut ion , and t axallocation provisions, and also theactual contributions, distributionsand allocations. The results may varysignificantly depending on these fac-tors, as illustrated by the followingexamples:

Example 3.2.3. Assume the followingfacts: (1) the partnership agreementprovides that (a) an investor and oper-ator are partners starting with part-nership percentages of 75% and 25%,respectively, and (b) if a partner fails tomake its share of a contribution, thepartnership percentages are adjustedin accordance with the dilution reme-dy in the Sample Provisions; (2) exceptas provided in Example 3.2.3C below,the partnership agreement does notrequire that liquidating distributionsbe made in accordance with capitalaccounts; (3) the partners initially con-tribute $100X in accordance with theirpartnership percentages; (4) a secondcontribution of $25X is contributed byinvestor alone, and there are no furthercontributions; and (5) the only distri-bution is a liquidating distribution of$150X. Thus, the total contributionswould be $125X ($100X and $25X), andfollowing the second and final contri-bution, the adjusted partnership per-centages would be 85% ([$75X + $25X+ (50% of 25% of $25X)] / $125X) and15% ([$25X + $0 - (50% of 25% of$25X)] / $125X). Now, consider threedifferent distribution schemes and notethe differing results:

Loss of Profit and Capital forDefaulting Partner. The defaultingpartner could lose capital even thoughthere is no debit to the defaulting part-ner’s (or credit to the funding part-ner’s) capital account for the additionalhypothetical contribution. Such a lossis possible even if the partnership doesnot have a loss:

Example 3.2.3A. Assume the facts inExample 3.2.3 and that all distributionsare made in accordance with the thenpartnership percentages. Under this for-mulation, (1) the $150X would be dis-

tributed $127.5X to the investor and$22.5X to the operator, and (2) the oper-ator would have a whole-dollar loss of$2.5X ($25X - $22.5X) or 10% of itsinvestment.

Loss of Profit Only for DefaultingPartner. It is also possible, of course,that the defaulting partner would notlose capital under such a formula:

Example 3.2.3B. Assume the facts inExample 3.2.3 and that distributionsare made in accordance with (actual)outstanding capital until all capital con-tributions are recouped, and the bal-ance is distributed in accordance withthe then partnership percentages. Underthis formulation, the adjusted partner-ship percentages are the same as in theprior example, but (1) $125X of the$150X would be distributed $100X tothe investor and $25X to the operator,and the remaining $25X would be dis-tributed $21.25X to the investor and$3.75X to the operator, and (2) the

operator would have a whole-dollarprofit of $3.75X.

The effect of the dilution formulaunder the two examples, which involvethe same dilution formula and the samecash flows, is a loss of both profits andcapital in Example 3.2.3A and a loss ofonly profits in Example 3.2.3B. This resultis not surprising. In Example 3.2.3B part-nership percentages are used only in theportion of the distribution waterfall thatallocates profit distributions so that onlyprofit distributions are adjusted. Similarexamples are easily constructed byadjusting the amount of distributionsand using any two different distributionwaterfalls where one is less favorable tothe defaulting partner for the assumedamount of distributable cash.

No Loss for Defaulting Partner. Itis also possible that a requirement toliquidate in accordance with capitalaccounts could eliminate the impactof a dilution remedy.

Example 3.2.3C. Assume the factsin Example 3.2.3 except that (1) the

partnership agreement provides thatdistributions (other than liquidatingdistributions) are made in accor-dance with partnership percentages,as in Example 3.2.3A, and liquidatingdistributions are required to be madein accordance with capital accounts,(2) the property is unencumbered rawland that produces no income ordepreciation (and therefore there areno tax profits or losses to allocate),and (3) the liquidating distribution isin the amount of $125X (rather than$150X). After the second and finalcontribution, the capital accountswould be $100X and $25X, respec-tively. Thus, the total distributions toinvestor and operator would be $100Xand $25X, and the operator wouldhave no whole-dollar profit or loss.

In the preceding three examples, thesame dilution provisions yield very dif-ferent results: in Example 3.2.3A, theoperator loses capital even though the

property is sold for a profit; in Example3.2.3B (where the only change to Exam-ple 3.2.3A is how distributions aremade), the operator merely loses someof its profits; and in Example 3.2.3C,the bonus factor is effectively eliminat-ed because of the amount of the liqui-dating distribution and the fact that itwas made in accordance with capitalaccounts without the benefit of currenttax items to allocate (or a “book-up” or“book-down” to adjust the capitalaccounts) to achieve the intended eco-nomic consequences of the dilution.

3.2.4 Dilution: Timing of ElectionThe Sample Provisions permit the fund-ing partner to make an election toimplement a dilution remedy concur-rently with its advance of the Deficien-cy, or subsequently by way of convertingthe outstanding balance of a preferredcontribution or loan to the partnershipto common equity. However, sometimesa dilution remedy might be subject to a

It may be possible tocombine a dilution remedywith other contribution

default remedies.

lockout period by providing that dilu-tion is available only by way of conver-sion of a preferred contribution ordefault loan that has not been repaid(together with the applicable interest orreturn) within a certain period of time.

3.2.5 Dilution: Tax IssuesPartners are strongly advised to consultwith a tax expert regarding the tax con-sequences of dilution remedies. Dilutionraises a myriad of income tax issues (e.g.,taxable capital shifts or deemed transfersof partnership interests, and fractionsrule compliance), which are beyond thescope of this article.30 In addition toincome tax issues, consider whethertransfer tax and real property taxreassessment issues may be implicated.For example, in California, if dilutioncauses certain changes of control in thepartnership, such changes could give riseto a “change in ownership” triggering areassessment and establishment of a new“base year value” for the real propertyowned by the partnership.31 In addition,a documentary transfer tax may beimposed (as though all the real proper-ty owned by the partnership were trans-ferred) in connection with a transfer of50% or more of the partnership interests(and more generally, any “708 termina-tion”) and, in certain cities and coun-ties in California, a documentary transfertax may also be payable if dilution resultsin certain changes in control.32

3.3 Loan to PartnershipAnother alternative remedy is to pro-vide that the funding partner’s advanceof the Deficiency, collectively with thefunding partner’s regular contribution,may be treated as a loan to the part-nership. This loan typically bears inter-est at a relatively high compounded rateand is repaid, together with interest, pri-or to any distributions. This remedyraises a number of issues.

3.3.1 What Is Amount of Loan?Should the loan to the partnership belimited to the amount of the Defi-ciency? For the same reasons discussedin Part 3.1.1 above in connection withpreferred contributions, the entireamount advanced by the funding part-ner (both its regular share of the cap-ital call and the amount advanced on

behalf of the defaulting partner) is typ-ically treated as a loan to the partner-ship (if that remedy is elected).

3.3.2 Loan to Partnership: TaxIssues. Tax considerations include thefollowing: • Loan interest may generate ordinaryincome for taxable partners.33

• Default loans may raise issues if apartner (or any investor in a part-ner) is a REIT. Although interestunder a loan qualifies for the 95%(passive income) test,34 it may notqualify for the 75% (real estateincome) test35 unless it is “securedby mortgages on real property or oninterests in real property.”36 In theauthors’ experience, default loans tothe partnership are rarely, if ever,secured. Often, however, the amountof default loan interest income maybe sufficiently small (when comparedto the REIT’s other income) that it isnot a significant concern. A REITmust also meet certain asset tests toensure that its assets consist primar-ily of real estate. In particular, nomore than 25% of the value of itstotal assets may be represented bycertain securit ies,37 which mayinclude default loans. Moreover, withcertain exceptions, REITs may notown more than 10% of the securities(by vote or value) of a single issuer.38

Fortunately, debt of the partnership

16 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

32 According to the California Revenue and TaxationCode statutes regarding documentary transfertaxes, “If there is a termination of any partner-ship or other entity treated as a partnership forfederal income tax purposes, within the meaningof Section 708 of the Internal Revenue Code, thepartnership or other entity shall be treated ashaving conveyed all realty held by the partnershipor other entity at the time of termination.” Cal.Rev. and Tax Code § 11925(b). Section 708 pro-vides, in part, that “a partnership shall be consid-ered as terminated if (A) no part of any businesscontinues to be carried on in a partnership, or (B)within a 12-month period there is a sale orexchange of 50 percent or more of the totalinterest in partnership capital and profits.”Section 708(b)(1). The documentary transfer taxrules (and tax rates) contained in the CaliforniaRevenue and Taxation Code may be modified bylocal ordinance in “charter cities.” See, for exam-ple, San Francisco Business and Tax RegulationsCode, Article 12-C, in particular, Section 1114,which imposes a documentary transfer tax on“any acquisition or transfer of ownership inter-ests in a legal entity that would be a change ofownership of the entity’s real property underCalifornia Revenue and Taxation Code § 64.”

33 Section 61(a)(4); BNA Tax Management Portfolio551-2nd: Section 482 Allocations: GeneralPrinciples in the Code and Regulations,§ IV.C.3.d(5) (“In general, interest income isincluded in gross income as ordinary income.”).

34 Section 856(c)(2)(B).

35 Section 856(c)(3).36 Section 856(c)(3)(B).37 Section 856(c)(4)(B)(i).38 See Sections 856(c)(4)(B)(iii)(II) and (III). Althougha “security” does not, for this purpose, include aREIT’s interest as partner (Section 856(m)(3)(A)(i))or its share, as a partner, of a debt instrumentissued by the partnership (Section 856(m)(4)(A)),a default loan to the partnership may not beentirely excluded. Although there are furtherexceptions to the rule, they may not apply.Section 856(m). For a more detailed discussion ofthe 10% rule, see BNA Tax Management Portfolio742-3rd: Real Estate Investment Trusts, III.B.3.

39 Section 856(m)(4)(B). Many REIT partners willtake steps to ensure that the partnership is oper-ated in such a manner to meet this test.

40 For loans, the lender must accrue interest.Regs. 1.446-1(c)(1)(ii) and 1.446-2(a)(1); BNA TaxManagement Portfolio 570-3rd: AccountingMethods—General Principles, IV.C.1 (“Accrualmethod taxpayers recognize income when ‘allthe events have occurred which fix the right toreceive such income and the amount thereofcan be determined with reasonable accuracy.’Ordinarily, a taxpayer’s right to income is fixedunder this ‘all events test’ when either theamount is unconditionally due or the taxpayerhas performed. As a result, the general rule isfrequently stated that accrual taxpayers recog-nize income when it is paid, due, or earned,whichever occurs first.”) (citations omitted).

is not considered a security underthe 10% rule if the partnership meetsthe 75% (real estate income) test.39

• The partner making the loan will berequired to accrue interest incomecurrently, regardless of whether inter-est is actually paid.40 This is in con-trast to a preferred return, where, inthe authors’ experience, many taxadvisors take the posit ion thatincome in respect of the return isallocated to the contributing partneronly if and when the partnership hasnet income to be allocated, or whenthe accrual of the preferred returngives the funding partner a distri-bution right that effectively shiftscapital from the capital account ofthe defaulting partner to pay the pre-ferred return of the funding partner.3.3.3 Loan to Partnership: Debt

Restrictions. It is relatively commonfor mortgage loans to include debtrestrictions (in the single purpose enti-ty (SPE) covenants or elsewhere) thatprohibit the borrower from incurringany other debt (except for certain tradepayables and whatever addit ionalexceptions the borrower is able tonegotiate). It may therefore be impor-tant to negotiate an exception to thedebt restrictions in a partnership mort-gage loan to allow contribution defaultloans to the partnership (or to incurthe mortgage debt through a partner-ship subsidiary if that al lows the partnership to avoid such debt restric-tions). Otherwise, this remedy may notbe available without creating a defaultunder the partnership’s mortgage loan.

3.3.4 Loan to Partnership: Usury/Lender Licensing. Will the loan give riseto usury or lender licensing issues? Mostpartnership and LLC statutes providethat the law of the state of formationgoverns the internal affairs of a foreignpartnership or LLC.41And in some juris-dictions, loans to a partnership (or to apartner that is an entity) may be exemptfrom the defense of usury under a com-mercial transaction exemption underthe laws of the state of formation.42 (InDelaware, there is also a usury exemptionfor obligations among partners whicharise under the partnership agreement,although such exemption does notexpressly apply to obligations of the part-nership to its partners.43) Would it mat-ter if the partnership is formed in

BUSINESS ENTITIES 17C APITAL CONTRIBUTION DEFAULT November/December 2013

However, the interest payable by the partner-ship may (but not in all cases) be deductible bythe partnership. Such deduction (if allowable)would be taken into account in determining thepartnership’s net income or loss for the tax yearallocated to the partners. In such event, theoverall tax impact to the lending partner wouldbe the difference between the amount of inter-est income it is required to accrue and its allo-cable share of such interest deduction of thepartnership.

41 See, e.g., Ribstein & Keatinge, Ribstein andKeatinge on Limited Liability Companies (West,2012), § 13:3, at 48 (“Most LLC statutes providethat the law of a formation jurisdiction governsthe organization, internal affairs, and member lia-bility of a foreign LLC.”) (endnote omitted);Rutledge, Jacobson & Ludwig, State LimitedLiability Company & Partnership Laws, (2011-1Supp.) 11 § 5.1, at 31 (“Generally the LLC actsprovide that the laws of the jurisdiction underwhich a foreign LLC is organized govern its inter-nal affairs and the liability of its members andmanagers.”) (endnote omitted); Bromberg &Ribstein, Bromberg and Ribstein on Partnership(Aspen, 2011-1 Supp.) § 1.04(a), at 63 (“the inter-nal affairs rule applies under the Revised UniformLimited Partnership Act”); Cal. Corp. Code§ 15909.01(a) (“The laws of the jurisdiction underwhich a foreign limited partnership is organizedgovern relations among the partners andbetween the partners and the partnership”); Cal.Corp. Code § 17450(a) (“The laws of the state

under which a foreign limited liability company isorganized shall govern its organization and inter-nal affairs.”); Cal. Corp. Code § 17708.01(a)(1)(“The law of the jurisdiction under which a for-eign limited liability company is formed governs[its] organization [and] internal affairs.”); 6 Del. C.§§ 15-106(a), 17-901(a)(1), and 18-901(a)(1). Cf.Cal. Corp. Code § 16106(a) (subject to certainexceptions for limited liability partnerships, “...thelaw of the jurisdiction in which a partnership hasits chief executive office governs relations amongthe partners and between the partners and thepartnership.”).

42 See, e.g., Cal. Corp. Code § 25118 (providing ausury exemption for certain loans of at least$300,000 or to borrowers with total assets of atleast $2 million but not if made or guaranteed byan individual); 6 Del. C. § 2301(c) (“Notwithstand-ing any other provision in this chapter to the con-trary, there shall be no limitation on the rate ofinterest which may be legally charged for the loanor use of money, where the amount of moneyloaned or used exceeds $100,000, and whererepayment thereof is not secured by a mortgageagainst the principal residence of any borrower.”);6 Del. C. § 2306 (“No corporation, limited part-nership, statutory trust, business trust or limitedliability company, and no association or joint stockcompany having any of the powers and privilegesof corporations not possessed by individuals orpartnerships, shall interpose the defense of usuryin any action.”).

43 See 6 Del. C. §§ 17-505, 18-505.

Delaware, but the partner not makingthe loan (i.e., the defaulting partner) andthe partnership have their principaloffices in California? What if the partnerthat is not making the loan is a Califor-nia entity and the property is located inCalifornia?44 Should lender licensing betreated any differently than usury?45

3.3.5 Loan to Partnership: EquitableSubordination and Recharacterization.If it is important that these loans arerespected as debt (e.g., for tax reasonsor priority), they should have a maturi-ty date, expressly have priority over equi-ty (including preferred contributions)and otherwise reflect the indicia of a truedebt transaction. Ignoring tax concerns,the general priority of debt over equitymay make loans a more attractive rem-edy than preferred contributions whenboth are available (recognizing that onlyone of these two remedies may be avail-able in any particular deal due to the taxramifications for REITs and tax-exemptinvestors and the possible prohibitionagainst partnership debt in the partner-ship’s mortgage loan documents). How-ever, because of the relationship betweenthe lender and debtor in such circum-stances (i.e., because the funding partneris an “insider”), there may be a risk thatsuch loans might be equitably subordi-nated to the partnership’s obligations tothird-party creditors, or recharacterizedas equity.46 But equitable subordinationto the claims of other creditors general-ly requires inequitable conduct by thelender, and the recharacterization riskmay be mitigated if the partnershipagreement includes terms and provisionsin respect of such loans that are reflectiveof a true debt transaction.47 Moreover, inthe authors’ experience, the primary con-cern of the funding partner regardingpriority is having priority over thedefaulting partner (rather than overthird-party creditors).

3.3.6 Loan to Partnership: Fiducia-ry Duties. Partners may owe fiduciaryduties to each other and to their part-nership. Query whether such duties mayprohibit or impede enforcement of apartner’s loan to the partnership?48 Themere making of the loan and its enforce-ment would not appear, as a generalrule, to result in a breach of fiduciaryduty in light of the express statutoryauthorization allowing a partner to makeloans to the partnership in many, if not

most, limited partnership and LLCstatutes.49 Moreover, in some jurisdic-tions, such duties (but not the impliedcovenant of good faith and fair dealing)may be, and, in the authors’ experience,typically are, limited or (at least underthe Delaware statutes) waived altogeth-er in the partnership agreement.50

Accordingly, absent inequitable con-duct, if the partners have agreed to per-mit loans to the partnership inconnection with contribution defaultsby providing for such loans in the part-nership agreement, and the partnershipagreement includes typical limitationson or waivers of fiduciary duties in con-formance with governing law, then itseems unlikely that making or enforcinga loan to the partnership in connectionwith a contribution default entails mate-rial risk of breach of fiduciary duty.

3.3.7 Loan to Partnership: Impacton Promote. Like preferred contribu-tions, loans to the partnership mayaccelerate or defer the operator’s pro-mote relative to a loan to the operator

18 BUSINESS ENTITIES November/December 2013 C APITAL CONTRIBUTION DEFAULT

44 See Continuing Education of the Bar, CounselingCalifornia Corporations (3d ed., updated Apr.2013) § 3A.22, at 474.24–.26 (discussingCalifornia’s internal affairs doctrine for foreign cor-porations, which is codified in Cal. Corp. CodeSection 2116, and possible exceptions to the doc-trine, such as insider trading, which violatesCalifornia’s securities laws).

45 In California, Cal. Fin. Code § 22050(c) provides alicensing exemption for entities that make notmore than one commercial loan per year.However, it is important to realize that a partner’sfailure to contribute may indicate an inability tomake future contributions as well, and thus suchexemption may be cold comfort if multiple defaultloans may be made.

46 See, e.g., 11 U.S.C. section 105(a) (“The court mayissue any order, process, or judgment that is nec-essary or appropriate to carry out the provisions ofthis title.”); 11 U.S.C. section 510(c)(“Notwithstanding subsections (a) and (b) of thissection, after notice and a hearing, the court may(1) under principles of equitable subordination, sub-ordinate for purposes of distribution all or part of anallowed claim to all or part of another allowed claimor all or part of an allowed interest to all or part ofanother allowed interest”); In re Fitness HoldingsInt’l, Inc., 714 F.3d 1141 (CA-9, 2013) (holding that abankruptcy court has the authority to recharacterizea shareholder loan as equity, in connection with anallegation that the company’s repayment of suchloan was a fraudulent transfer).

47 See, e.g., In re Broadstripe, LLC, 444 Bkrptcy.Rptr. 51 (Bkrptcy. D. Del., 2010) (noting that“inequitable conduct” is a required element forequitable subordination under Fifth Circuit prece-dent, but that heightened scrutiny of insider con-

as defaulting partner (depending onwhether the interest rate is lower orhigher than the promote hurdle rate).See discussion of this issue for pre-ferred contributions in Part 3.1.3 above.

3.4 Loan to Defaulting PartnerMany partnership agreements providethat the funding partner’s advance ofthe Deficiency may be treated as a loanto the defaulting partner. Typically, thedefaulting partner is then deemed tohave used the loan to make its requiredcontribution and all distributions to thedefaulting partner are used to repay theloan (together with interest) before thedefaulting partner is allowed to receiveand retain any of its distributions.

3.4.1 Loan to Partner: Issues inCommon with Loan to PartnershipMany of the issues with loans to thepartnership also apply here. However,the loan itself will have a smaller prin-cipal balance and, consequently, themagnitude of the issues may dimin-ish.51 Additionally, the debt restrictionsdescribed in Part 3.3.3 above are gen-erally not a concern in this context,and it seems unlikely that a loan to thedefaulting partner might be equitablysubordinated or recharacterized asequity. Moreover, the tax concerns ofREIT partners (or investors) are dif-ferent in this context because the REITmay not be able to rely on the fact thatthe partnership is being operated in amanner that satisfies the 75% (realestate income) test,52 but may be ableto mitigate its concerns by securing theloan with the defaulting partner’s part-nership interest.53

3.4.2 Loan to Partner: BankruptcyOne of the primary reasons why loansto the default ing par tner are notaddressed in the Sample Provisions is toavoid having a loan to a bankrupt part-ner. A partner may have some controlover a bankruptcy filing by the part-nership (to the extent the partnershipagreement requires such partner toapprove, or perhaps even initiate, anybankruptcy filing by the partnership),but it may not be possible to preventthe bankruptcy of the other partner

BUSINESS ENTITIES 19C APITAL CONTRIBUTION DEFAULT November/December 2013

duct is appropriate because inequitable conductseems more likely to occur when the lender is aninsider); In re Lighthouse Lodge, LLC, 2010 Bankr.LEXIS 4574 (Bkrptcy. N.D. Cal., 12/14/2010)(declining to recharacterize a loan from an affiliateof a member to the related limited liability compa-ny, and citing In re Dornier Aviation (N. Am.), Inc.,453 F.3d 225 (CA-4, 2006) for a non-exhaustivelist of considerations relevant to the determina-tion of whether to recharacterize a debt as equi-ty); Tucker, “Debt Recharacterization During anEconomic Trough: Trashing Historical Tests toAvoid Discouraging Insider Lending,” 71 Ohio St.L.J. 187 (2010); Robertson and Cicarella,“Developments in the World of Loan-to-Own,”ABI Comm. News—Unsecured Trade CreditorsComm. (Aug. 2008); Kuhl and Wells, “Buddy, CanYou Spare A Dime?,” Inst. Real Est. Letter—N.Am. (October 2010).

48 See, e.g., Cal. Corp. Code §§ 15904.08, 17153,17704.09(a); BT-I v. Equitable Life AssuranceSoc’y of the United States, 75 Cal. App. 4th 1406(1999); Kuhl and Wells, note 47, supra. But see,e.g., Cal. Corp. Code §§ 15903.05 and 17704.09(f).