Embed Size (px)

Citation preview

mari%me & transport business solu%ons

Port Financing and Concessions Port Finance Interna-onal Antwerp 2016 20 April 2016

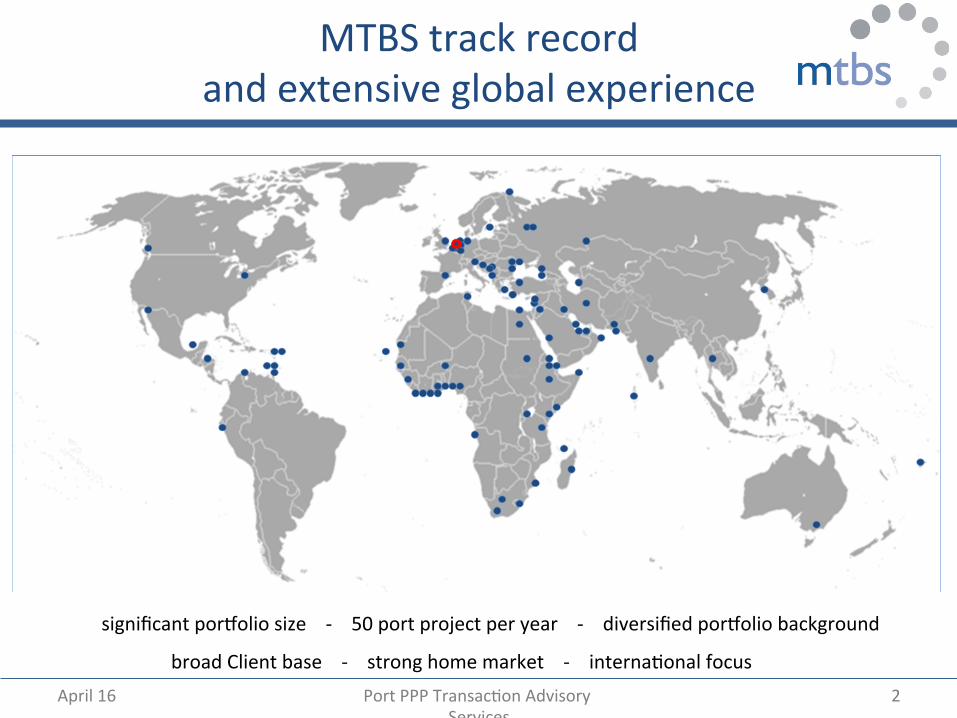

MTBS track record and extensive global experience

significant por<olio size -‐ 50 port project per year -‐ diversified por<olio background

broad Client base -‐ strong home market -‐ interna%onal focus April 16 Port PPP Transac%on Advisory

Services 2

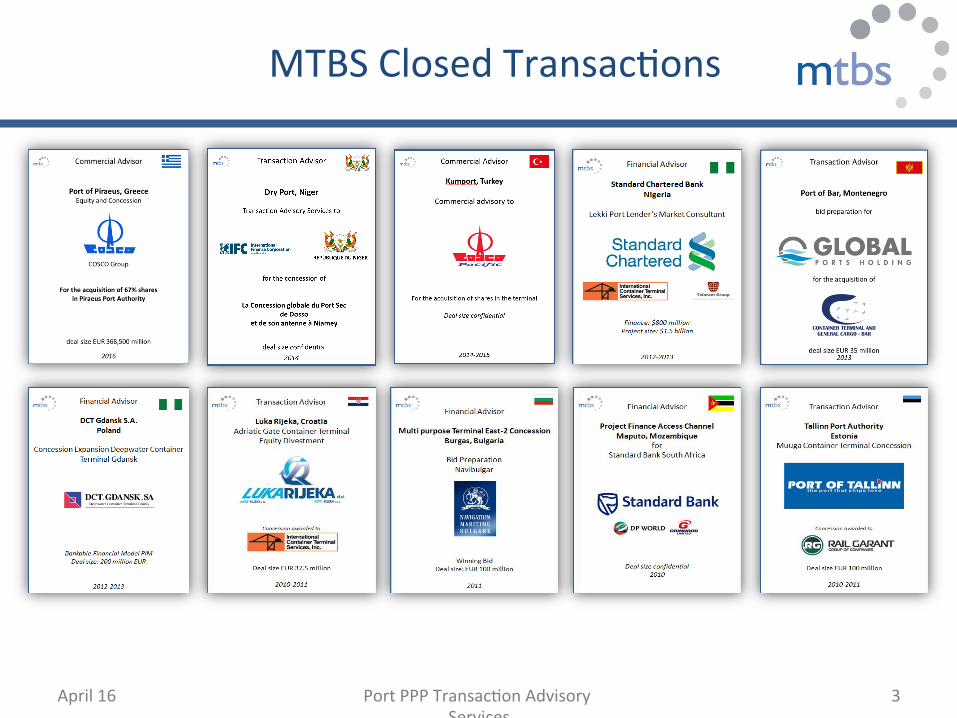

MTBS Closed Transac%ons

April 16 Port PPP Transac%on Advisory Services

3

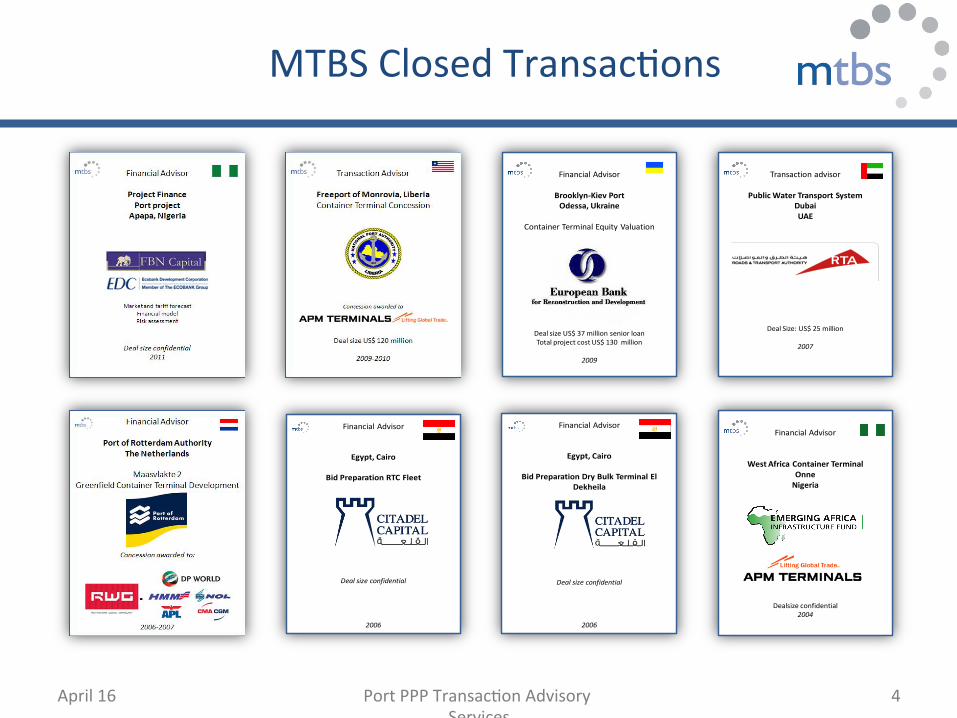

MTBS Closed Transac%ons

April 16 Port PPP Transac%on Advisory Services

4

Transaction advisor

Public Water Transport SystemDubaiUAE

Deal Size: US$ 25 million

2007

Financial Advisor

Brooklyn-‐Kiev PortOdessa, Ukraine

Container Terminal Equity Valuation

Deal size US$ 37 million senior loanTotal project cost US$ 130 million

2009

Financial Advisor

West Africa Container TerminalOnneNigeria

Dealsize confidential2004

Financial Advisor

Egypt, Cairo

Bid Preparation RTC Fleet

2006

Deal size confidential

Flag of Country

Financial Advisor

Egypt, Cairo

Bid Preparation Dry Bulk Terminal El Dekheila

2006

Deal size confidential

Flag of Country

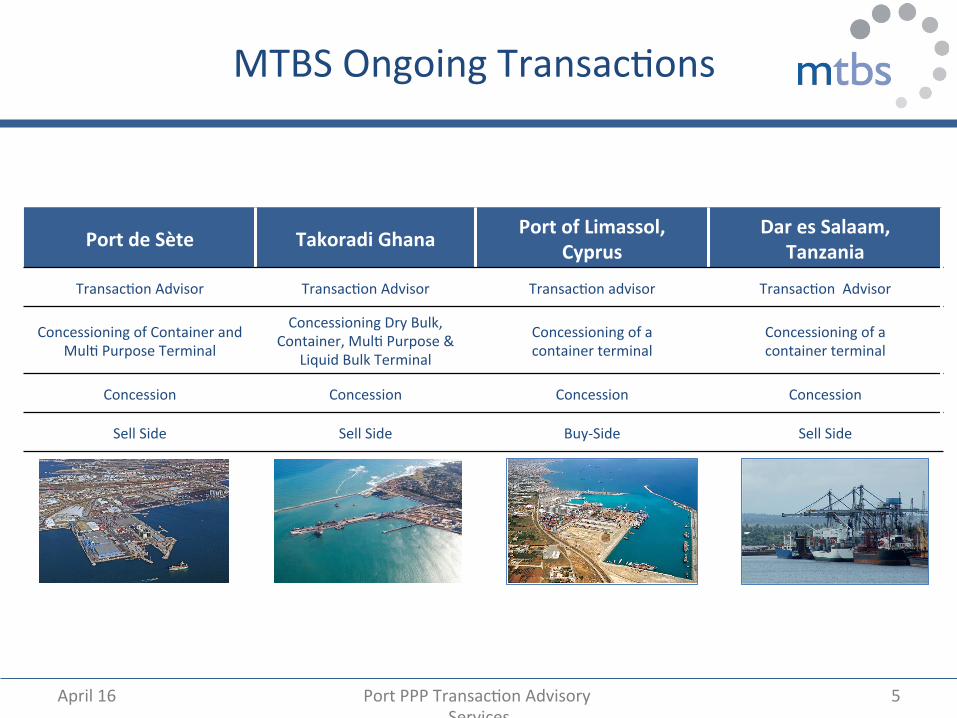

MTBS Ongoing Transac%ons

Port de Sète Takoradi Ghana Port of Limassol, Cyprus

Dar es Salaam, Tanzania

Transac%on Advisor Transac%on Advisor Transac%on advisor Transac%on Advisor

Concessioning of Container and Mul% Purpose Terminal

Concessioning Dry Bulk, Container, Mul% Purpose &

Liquid Bulk Terminal

Concessioning of a container terminal

Concessioning of a container terminal

Concession Concession Concession Concession

Sell Side Sell Side Buy-‐Side Sell Side

April 16 Port PPP Transac%on Advisory Services

5

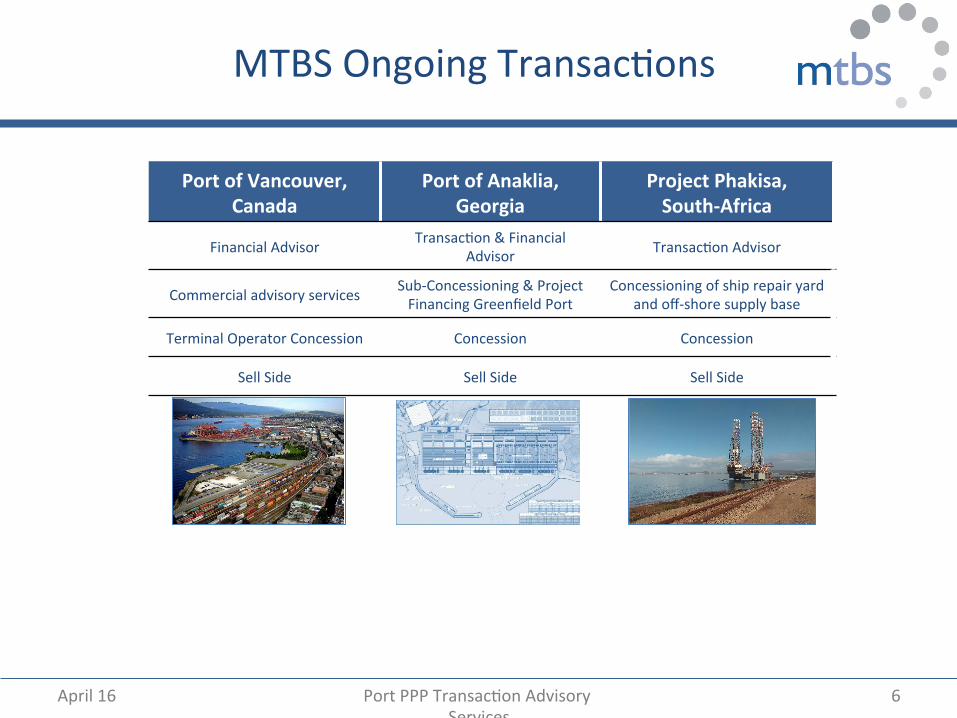

MTBS Ongoing Transac%ons

Port of Vancouver, Canada

Port of Anaklia, Georgia

Project Phakisa, South-‐Africa

Financial Advisor Transac%on & Financial Advisor Transac%on Advisor

Commercial advisory services Sub-‐Concessioning & Project Financing Greenfield Port

Concessioning of ship repair yard and off-‐shore supply base

Terminal Operator Concession Concession Concession

Sell Side Sell Side Sell Side

April 16 Port PPP Transac%on Advisory Services

6

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

7

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

8

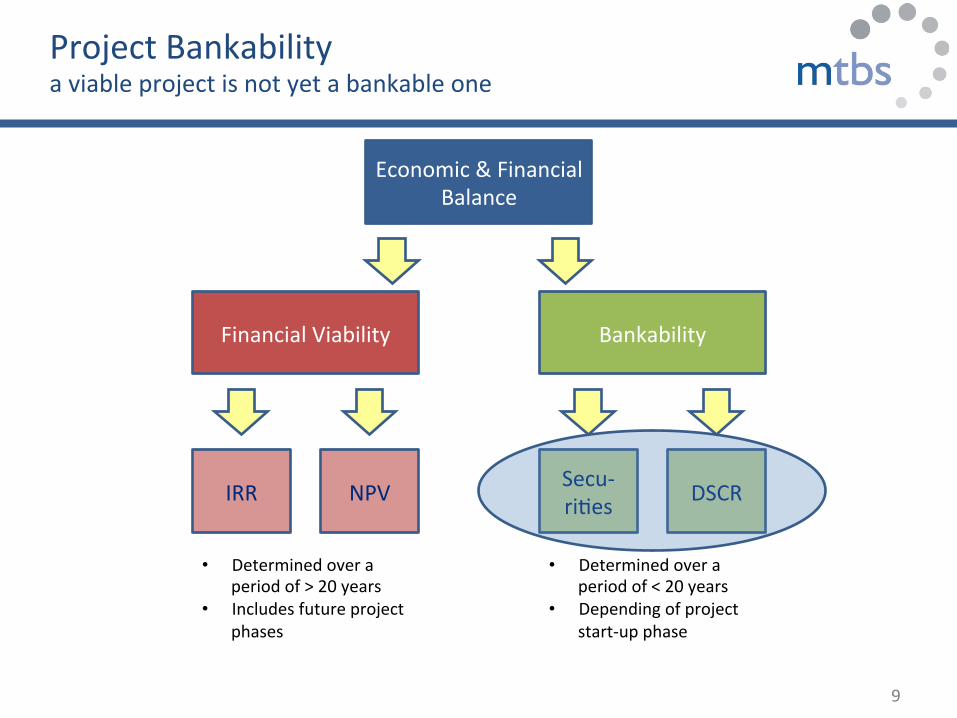

Project Bankability a viable project is not yet a bankable one

9

Economic & Financial Balance

Financial Viability Bankability

IRR NPV Secu-‐ri%es DSCR

• Determined over a period of > 20 years

• Includes future project phases

• Determined over a period of < 20 years

• Depending of project start-‐up phase

10

(400)

(300)

(200)

(100)

-‐

100

200

300

400

0 5 10 15 20

mio USD

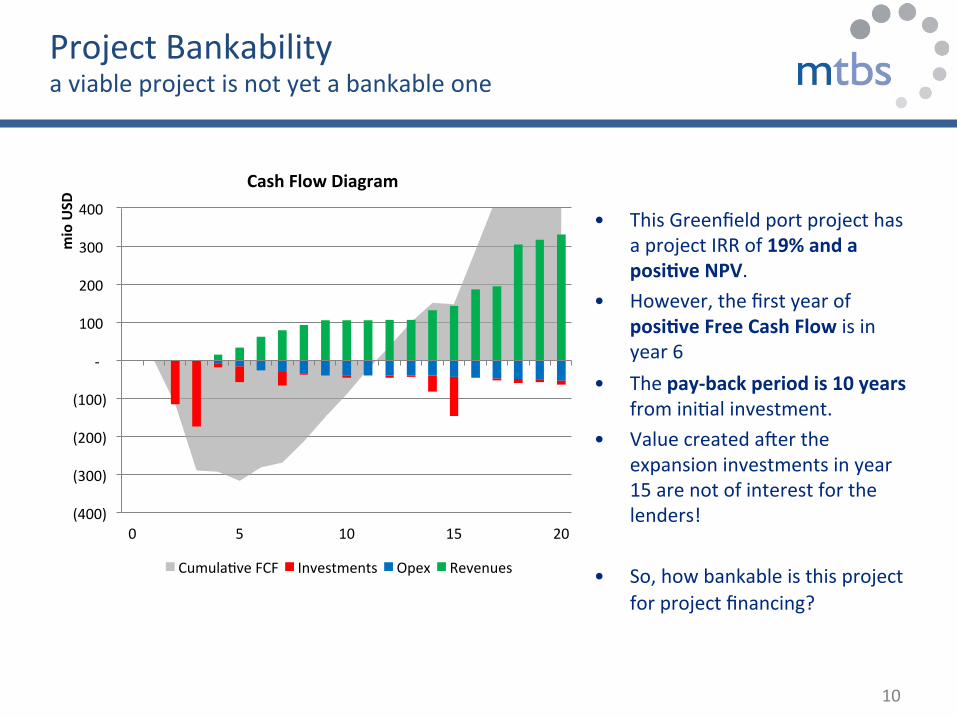

Cash Flow Diagram

Cumula%ve FCF Investments Opex Revenues

• This Greenfield port project has a project IRR of 19% and a posiJve NPV.

• However, the first year of posiJve Free Cash Flow is in year 6

• The pay-‐back period is 10 years from ini%al investment.

• Value created ager the expansion investments in year 15 are not of interest for the lenders!

• So, how bankable is this project for project financing?

Project Bankability a viable project is not yet a bankable one

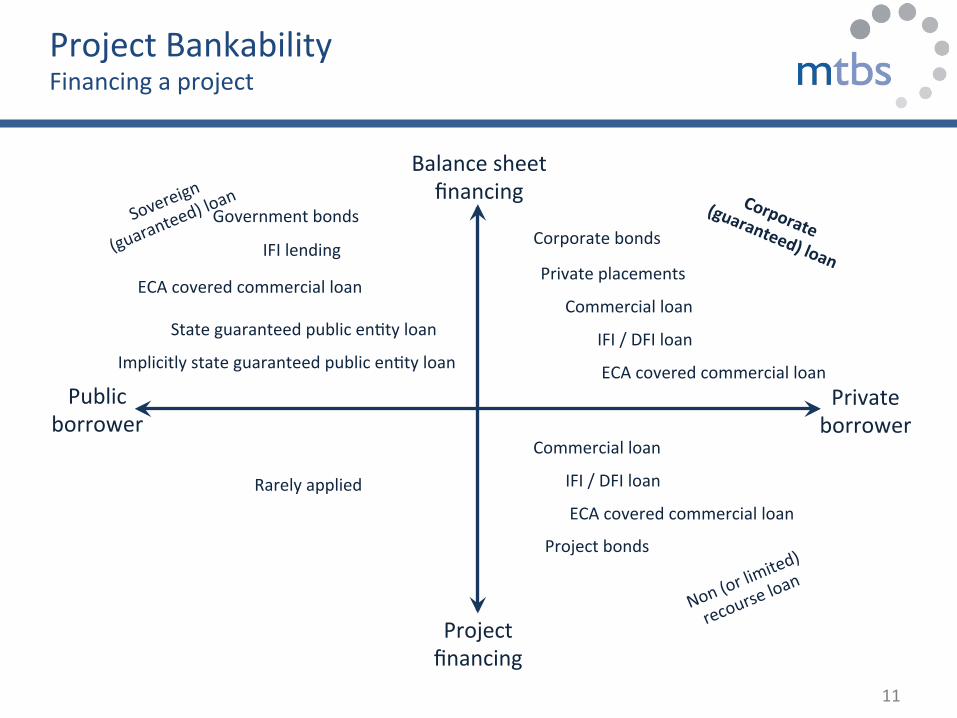

Project Bankability Financing a project

11

Balance sheet financing

Project financing

Public borrower

Private borrower

Government bonds

IFI lending

ECA covered commercial loan

Rarely applied

Corporate bonds

Private placements

Commercial loan State guaranteed public en%ty loan

Implicitly state guaranteed public en%ty loan IFI / DFI loan

ECA covered commercial loan

Commercial loan

IFI / DFI loan

ECA covered commercial loan

Project bonds

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

12

2nd MED Ports 2014 Exhibi%on and Conference Marrakech 23 & 24 April 2014 13

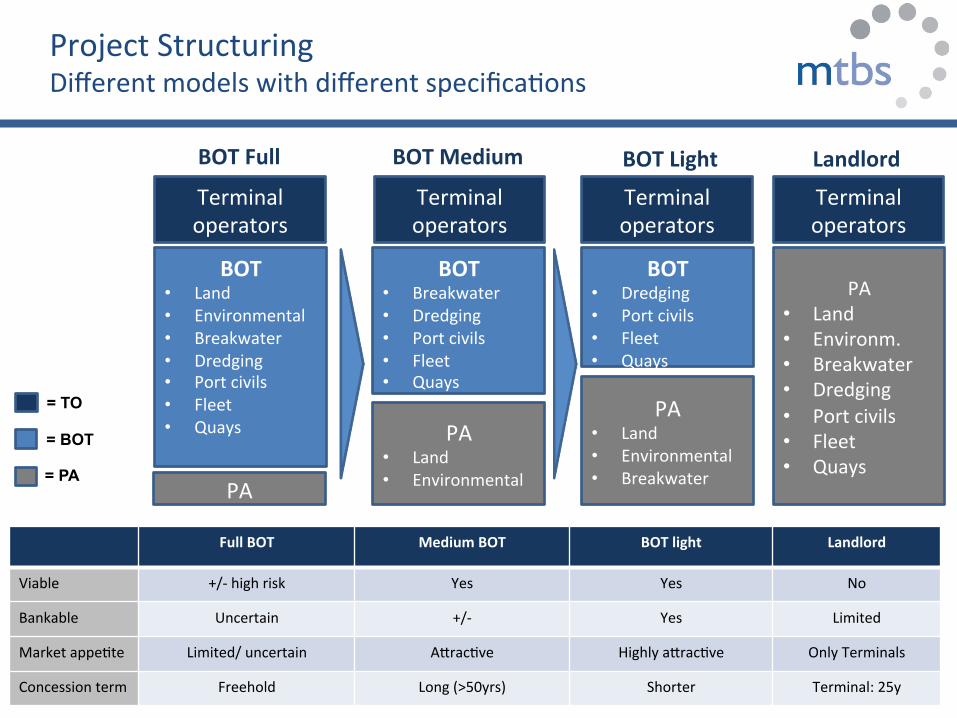

Full BOT Medium BOT BOT light Landlord

Viable +/-‐ high risk Yes Yes No

Bankable Uncertain +/-‐ Yes Limited

Market appe%te Limited/ uncertain Anrac%ve Highly anrac%ve Only Terminals

Concession term Freehold Long (>50yrs) Shorter Terminal: 25y

BOT • Land • Environmental • Breakwater • Dredging • Port civils • Fleet • Quays

Terminal operators

PA

PA • Land • Environmental

PA • Land • Environmental • Breakwater

BOT • Breakwater • Dredging • Port civils • Fleet • Quays

BOT • Dredging • Port civils • Fleet • Quays

Terminal operators

Terminal operators

BOT Full BOT Medium BOT Light

= BOT

= PA

PA • Land • Environm. • Breakwater • Dredging • Port civils • Fleet • Quays

Terminal operators

Landlord

= TO

Project Structuring Different models with different specifica%ons

14

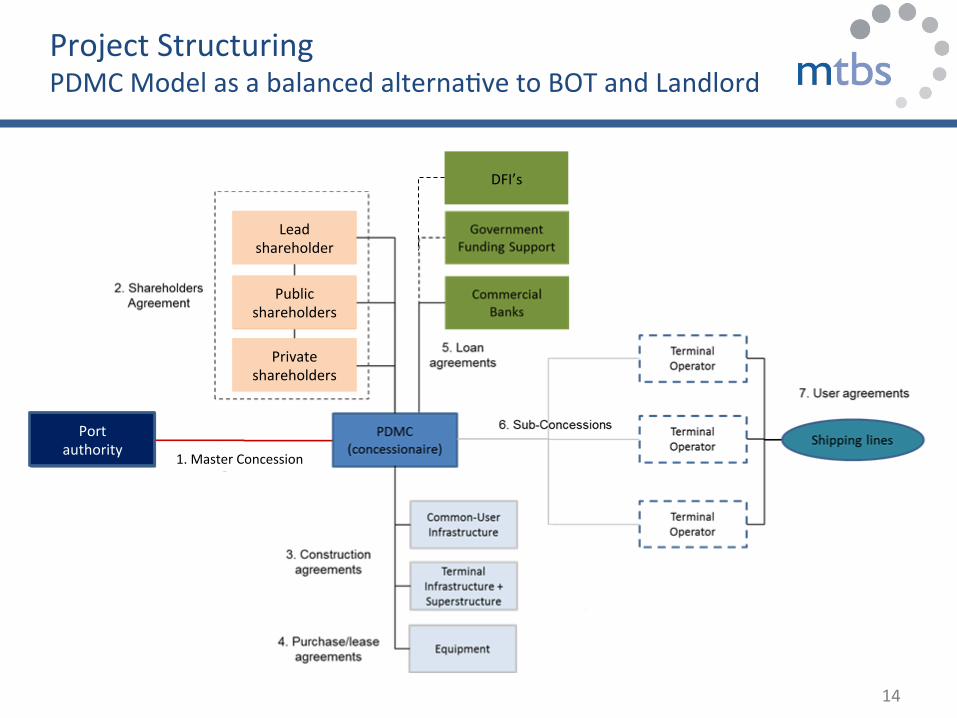

Lead shareholder

Public shareholders

Private shareholders

DFI’s

Port authority 1. Master Concession

Project Structuring PDMC Model as a balanced alterna%ve to BOT and Landlord

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

15

• Consor%a and/or PDMC structures result in mul%ple shareholders, hence the project needs to be a ring-‐fenced stand-‐alone en%ty (Special Purpose Company)

• Debt is non-‐recourse (or limited recourse) to shareholders • Corporate financing looks at the Mother Company’s past performance and balance

sheet: not to the future cash flows of the new project, while a PF loan is provided on SPC’s cash flows

• High leverage (can be up to 90%, if market risk is excluded)

• Important repercussion on PPP and Concession Arrangements

16

Project Finance There is an increased need for Project Finance

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

17

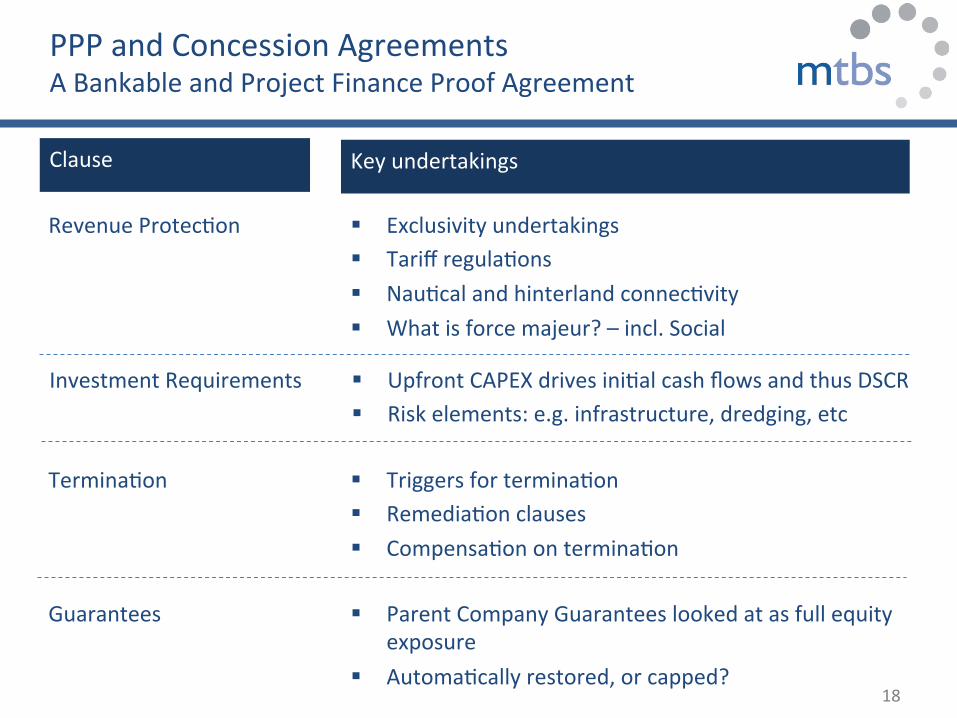

Investment Requirements

18

§ Upfront CAPEX drives ini%al cash flows and thus DSCR § Risk elements: e.g. infrastructure, dredging, etc

Termina%on

§ Triggers for termina%on § Remedia%on clauses § Compensa%on on termina%on

Guarantees

§ Parent Company Guarantees looked at as full equity exposure

§ Automa%cally restored, or capped?

Revenue Protec%on

§ Exclusivity undertakings § Tariff regula%ons § Nau%cal and hinterland connec%vity § What is force majeur? – incl. Social

PPP and Concession Agreements A Bankable and Project Finance Proof Agreement

Clause

Key undertakings

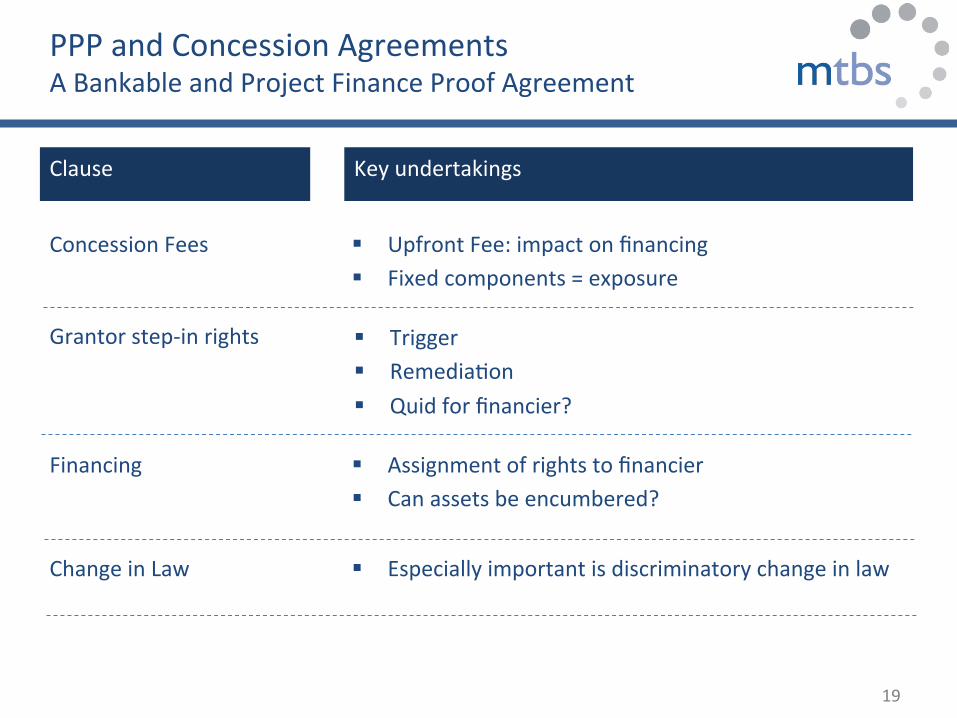

Grantor step-‐in rights

19

§ Trigger § Remedia%on § Quid for financier?

Financing

§ Assignment of rights to financier § Can assets be encumbered?

Change in Law

§ Especially important is discriminatory change in law

Concession Fees

§ Upfront Fee: impact on financing § Fixed components = exposure

PPP and Concession Agreements A Bankable and Project Finance Proof Agreement

Clause

Key undertakings

Challenges for investors

Project Bankability: the seVng Suitable Port Models Increased Need for Project Finance Repercussions for Concession Agreements Role of DFIs

20

21

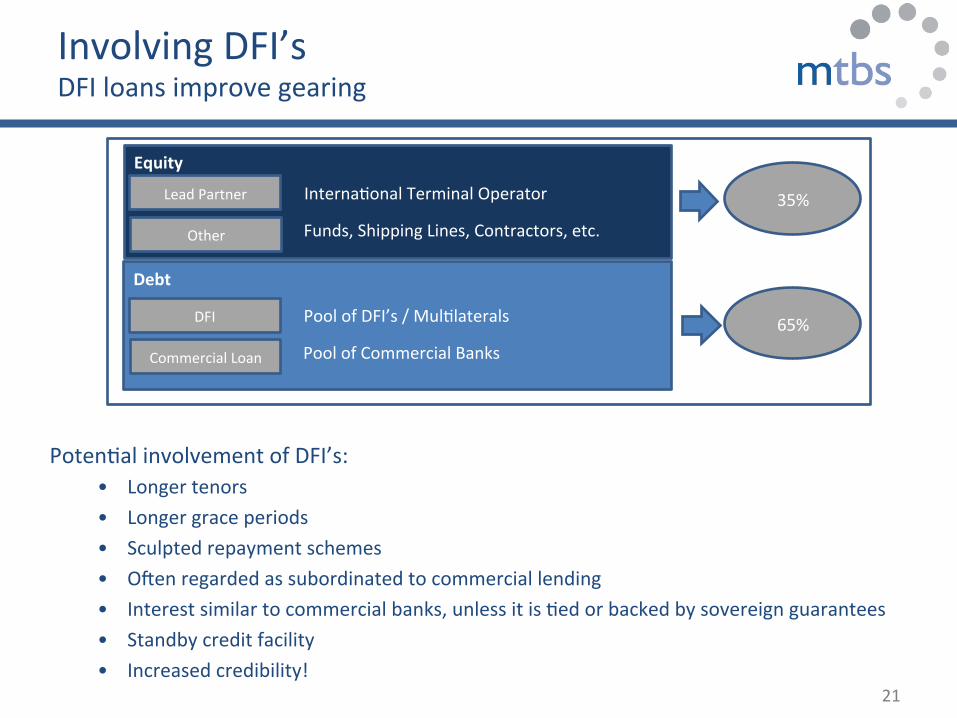

Involving DFI’s DFI loans improve gearing

Poten%al involvement of DFI’s: • Longer tenors • Longer grace periods • Sculpted repayment schemes • Ogen regarded as subordinated to commercial lending • Interest similar to commercial banks, unless it is %ed or backed by sovereign guarantees • Standby credit facility • Increased credibility!

Equity

Debt

Lead Partner

Other

Interna%onal Terminal Operator

Funds, Shipping Lines, Contractors, etc.

DFI

Commercial Loan

Pool of DFI’s / Mul%laterals

Pool of Commercial Banks

35%

65%

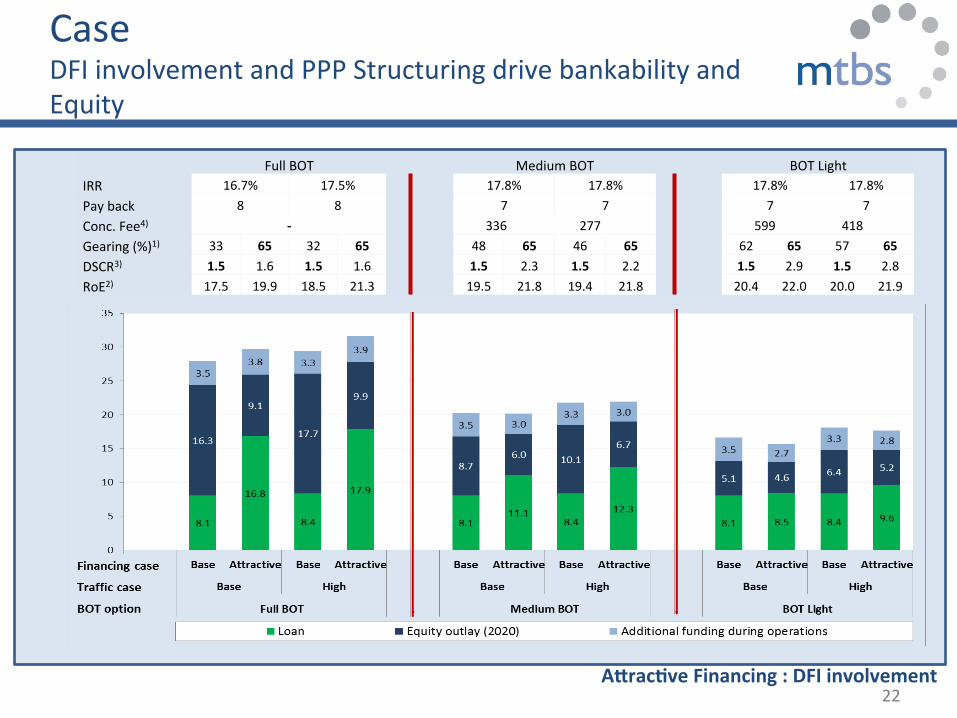

Case DFI involvement and PPP Structuring drive bankability and Equity

ASracJve Financing : DFI involvement 22

Full BOT Medium BOT BOT Light IRR 16.7% 17.5% 17.8% 17.8% 17.8% 17.8% Pay back 8 8 7 7 7 7 Conc. Fee4) -‐ 336 277 599 418 Gearing (%)1) 33 65 32 65 48 65 46 65 62 65 57 65 DSCR3) 1.5 1.6 1.5 1.6 1.5 2.3 1.5 2.2 1.5 2.9 1.5 2.8 RoE2) 17.5 19.9 18.5 21.3 19.5 21.8 19.4 21.8 20.4 22.0 20.0 21.9

• Nowadays bankability is all about Security and Debt Service Security • Increased Project Size and Complexity increase need for Project Finance • Increased importance of the PPP Contract: more possible deal breakers • Mul%lateral Banks can increase gearing poten%al

Any approach is tailor-‐made and requires ac-ve dialogue between mul-ple players. Compe--ve dialogue in PPP tendering

23

Conclusions

mariJme & transport business soluJons mariJme strategy & finance advisors

| +31 10 2865940 | [email protected] | www.mtbs.nl

Wijnhaven 3E P.O. Box 601

3000 AP RoSerdam The Netherlands

White House, Ronerdam

t e w