Embed Size (px)

Citation preview

AUSTRALIAN BUSINESS & CLIMATE GROUP

STEPPING UPAccelerAting the deployment of low emission technology in AustrAliA

AUgUST 2007www.businessandclimate.comAUSTRALIAN BUSINESS & CLIMATE GROUP

SantosSantos is a major Australian-based oil and gas exploration and production company with interests and operations in every major Australian petroleum province and in Indonesia, Papua New Guinea, Vietnam, India, Kyrgyzstan and Egypt. Santos is Australia’s largest domestic gas producer and sells oil, liquids and LNG to customers worldwide. www.santos.com

Swiss ReAs the world’s leading and most diversifi ed global reinsurer, Swiss Re offers fi nancial services products that enable risk taking essential to enterprise and progress. Founded in Zurich, Switzerland, in 1863, Swiss Re operates in more than 25 countries. The company’s traditional reinsurance products and related services for property and casualty, as well as the life and health business, are complemented by insurance-based corporate fi nance solutions and supplementary services for comprehensive risk management. www.swissre.com

VicSuperVicSuper Fund is one of Australia’s largest public offer superannuation funds, with over 220,000 members and more than AUD $5.8 billion in assets under management at 30 June 2007.

www.vicsuper.com.au

WestpacWestpac was founded in 1817 as the Bank of New South Wales, and was the fi rst company and the fi rst bank to be established in Australia. With over 27,000 employees and a customer base of around 7 million, Westpac is a leading provider of banking and fi nancial services in Australia, New Zealand and the Pacifi c region. www.westpac.com.au

This report was printed on paper made with process-chlorine-free, 100% recycled post-consumer waste fi bre. The paper is certifi ed by the Forest Stewardship Council (FSC), which promotes environmentally appropriate, socially benefi cial, and economically viable management of the world’s forests.

The report was printed by Oxford Printing, which is one of a small number of printers in Australia certifi ed by the FSC standards to continue the chain of custody when printing on FSC-certifi ed paper.

CONTENTS

EXECUTIVE SUMMARY 1

1. KEY MESSAGES 2

2. INTRODUCTION 4

3. THE TECHNOLOGY DEVELOPMENT CHALLENGE 6

4. EMISSIONS TRADING SCHEME 12

5. A NATIONAL LOW EMISSION TECHNOLOGY STRATEGY 16

WAY FORWARD 23

While all reasonable care has been taken in the production of this publication, the Australian Business & Climate Group and its members accept no liability or responsibility whatsoever for, or in respect of, any use or reliance upon this publication by any party.

Cert no. SCS-COC-00988

1.

Addressing the serious consequences of climate change is arguably the biggest challenge facing current and future generations globally.

Effective management of climate change requires an integrated, national response to both mitigation and adaptation challenges. The Australian Business & Climate Group strongly supports the adoption of an integrated National Climate Change Response. It will be essential to integrate the component elements of the response as they are intrinsically interlinked.

It is also critical that we seek solutions on a national basis, rather than state by state. A National Climate Change Response will also benefi t by linking with international efforts to maximise learning, share costs and expertise while minimising unnecessary duplication of effort.

Transforming the way Australia produces and uses energy must be a cornerstone of a national response aimed at signifi cantly reducing greenhouse gas emissions. While bipartisan acceptance for the establishment of an emissions trading scheme is now established, Australia must also explore complementary policies to accelerate the uptake of breakthrough low emission technologies. The rate of technology improvement and subsequent adoption must be faster than the usual commercial timeframes if these technologies are to be available at scale, performance and at an acceptable cost when required to meet challenging emission trajectories.

The Australian Business & Climate Group believes that a National Low Emission Technology Strategy is an essential element of a National Climate Change Response. The challenge is complex and the response must be comprehensive.

Business is ready to play its part in delivering the solutions and has prepared this paper as a catalyst for discussion between all stakeholders. We look forward to continuing the dialogue.

EXECUTIVE SUMMARY

2.

1. KEY MESSAGES

1. Climate change is an unprecedented global issue requiring signifi cant resources to meet the complex environmental, energy, economic and political challenges.

2. The economic risks and societal challenges presented by climate change require a globally coordinated, urgent and long-term response by governments, business and the wider community.

3. Australia’s contribution to the global response would be best managed through the urgent development of an integrated National Climate Change Response.

4.

5.

Energy is central to the climate change issue; the largest contribution to anthropogenic greenhouse gas emissions comes from burning fossil fuels – oil, gas and coal.

6.

Fundamental changes in the global energy system are required to achieve the deployment of affordable low emission technologies in order to stabilise concentrations of greenhouse gases in the atmosphere. Incremental improvements in technology will not by themselves lead to stabilisation; more is required, that is step-changes in cost, scale and emissions performance – well beyond the usual framework of commercial development.

7.

The energy challenge is essentially one of risk management – achieving the necessary technological transformations requires investments in a range of technologies at different stages of development. An investment portfolio needs a diverse range of technologies to deal effectively with critical future uncertainties. Policy certainty will be crucial to investment decisions.

8.

A transformational energy technology strategy is therefore an integral component of international and national climate change response frameworks.

• A technology strategy will provide value by reducing the costs of meeting future greenhouse gas reduction goals.• Transformational technology development and deployment takes substantial and sustained investment in research,

development and demonstration and fi rst-of-a-kind deployment.• Within Australia, technology innovation must be a cornerstone of our response to achieving deep cuts in greenhouse gas

emissions while maintaining our national long-term economic competitiveness.• Australia cannot be a leader in all relevant technologies, so it will be important to focus on options to leverage our

national comparative advantage and strategic competitiveness while continuing to generate value through international partnerships for a wider range of technologies.

9.

Transformational technologies require both ‘technology push’ and ‘market pull’ policies to drive development through the innovation cycle towards commercialisation and market diffusion.

A key incentive for technology deployment will emerge from an emissions trading scheme that has maximum ‘pull forward’ through a credible and rising carbon price signal linked to a long-term emissions target.

3.

11. In the early stages of emissions trading, there are strong reasons to support complementary policies for research, development, demonstration and fi rst-of-a-kind large-scale commercialisation of technologies. Reasons for support include:

• Need to lower the cost of breakthrough low emission technologies;• Risk sharing of technology development is needed in order to accelerate the availability of breakthrough technologies to

hasten towards stabilisation goals and limit costs of deep cuts in emissions;• Creating opportunities to export know-how of proven new energy technologies; Australia is the largest exporter of coal

in the world and a major gas exporter and, increasingly, a supplier of renewable energy technologies such as solar photovoltaic (PV);

• Demonstrating breakthrough technologies will boost the confi dence of international markets, which in turn will accelerate deployment;

• Broad global deployment of breakthrough technologies will be of benefi t to Australia in terms of potential reduced climate impacts if global emissions can be stabilised. Australia is highly vulnerable to climate impacts and reducing these threats is of great national benefi t.

12. A National Low Emission Technology Strategy will provide the necessary strategic focus to determine the full scope of the necessary complementary policy measures in the early phases of an Australian emissions trading scheme.

• The aim is to ensure that Australia uses its natural and resource advantages in a timely manner to ensure that breakthrough energy technologies are available for deployment at scale and acceptable costs when required to meet future emission targets.

• The National Low Emission Technology Strategy should deliver effective solutions to fi rst mover cost and risk barriers to breakthrough energy technology development in Australia.

• Preferred technologies should be aligned with Australia’s national interests but the National Low Emission Technology Strategy should not otherwise seek to ‘pick winners’.

• Market conditions should be promoted in order to drive a dramatic increase in investment in low emission technologies, by ensuring that it is at least as attractive to investors as investment in mature technologies.

• The National Low Emission Technology Strategy must fi nd the appropriate balance between supporting breakthrough technologies to build scale and reduce future abatement costs whilst also not impacting on business confi dence and investment by adding new unsustainable capacity to the market. All policies under the National Low Emission Technology Strategy must be transparent to the market and be technology and fuel neutral.

13. The Australian Business & Climate Group believes that climate change is a fundamental issue for business, government and the wider community. We accept the need for signifi cant and sustained reductions in greenhouse gas emissions and are strongly supportive of the early introduction of an emissions trading scheme, administered by the Australian Government. In addition, we wish to highlight the need for a complementary National Low Emission Technology Strategy to drive the development of transformational technologies which will be critical in meeting future emission targets.

10. It is acknowledged that emissions trading is now on the agenda of all Australian Governments and the Federal Opposition. We have reached this position through a number of separate processes but the result is a reasonable certainty that Australia will have emissions trading within fi ve years. It is critical that all parties work towards national consistency; for example targets, and international consistency to link trading regimes. The Australian Business & Climate Group strongly endorses this policy response and recognising that the detailed design elements are critical, we look forward to contributing to the design phase and participating in the scheme.

4.

2. INTRODUCTIONIn the course of the last 12 months, the issue of climate change has been dominant in the policy debate, both in Australia and overseas. There is broad scientifi c consensus that climate change is real, is human induced and that urgent action is required to avoid dangerous levels of global warming1. The groundswell of public opinion is now driving government policy, but it is also beginning to impact more signifi cantly on business, where the carbon intensity of a company’s operations is increasingly becoming a factor determining longer term competitiveness.

Recognising the urgency and importance of this challenge, nine companies from the mining, smelting and exploration, resource, fi nance, real estate and infrastructure investment, and energy industries have come together to assess how Australia can best address climate change. Called the Australian Business & Climate Group, the companies involved are Anglo Coal, BP Australia, Deloitte, Mirvac, Rio Tinto, Santos, Swiss Re, VicSuper and Westpac. It is the fi rst time these companies have collaborated to review and recommend the mechanisms needed to reduce Australia’s greenhouse gas (GHG) emissions. Our interests are global and signifi cant with a combined international market capitalisation in excess of A$600 billion.

The Australian Government understands that it needs to respond on a number of levels to the challenge of climate change. The Australian Business & Climate Group recommends the urgent development of an integrated National Climate Change Response. This integrated response will have fi ve main elements as shown in Figure 1.

FIRST, global action is clearly essential over a long period if the problem of climate change is to be addressed effectively. Australia has been able to maintain an important role in international forums on future climate change policy. Australian scientists make a signifi cant contribution to the Inter-governmental Panel on Climate Change (IPCC) process and an Australian offi cial has been chosen to represent the Annex 1 countries as co-chair of the group examining a post-2012 global approach2. Its support for the formation of the Asia Pacifi c Forum on Clean Development and Climate (AP6) is signifi cant and the Government has been able to place the climate change issue high on the agenda for the 2007 APEC meeting in Sydney.

It is now important that Australia set a long-term aspirational goal to signifi cantly reduce GHG emissions as our contribution to a global effort designed to avert signifi cant climate impacts.

The SECOND area where action is necessary is to send a carbon price signal into all aspects of the Australian economy. The Australian Business & Climate Group believes that the most effi cient way to do this is via an emissions trading scheme (ETS). An ETS is necessary to change behaviour both on the demand and supply side. The issue is particularly important in the electricity generation sector, where new plant involves a very high capital cost and the assets have a long economic life of 40 to 50 years. We welcome the announcements by both major parties of the introduction of an Australian emissions trading scheme before 2012.

Australia must set a shorter term binding target, for example 20203, to facilitate a smooth transition to a low-emission economy and as a milestone towards achieving the long-term goal.

THIRD, an ETS needs to be complemented, initially at least, by regulatory measures in sectors where emissions trading may not be fully effective. In the transport sector, for example, a moderate carbon price will have such a limited impact on the price of petrol that it is unlikely to drive behavioural change. Similarly, the practical challenges of implementing an ETS for the agricultural sector mean that complementary measures are essential.

‘No regrets’4 measures, particularly related to energy effi ciency and conservation will still be important complements to an ETS. Most research in this area suggests that there is an enormous ‘free kick’ available in this area in Australia if more imaginative policy instruments were to be devised. The National Framework on Energy Effi ciency (NFEE) must be aimed at changing attitudes and behaviour; it is notable that the community generally is currently much more attuned to conserving water than energy. More information will assist energy consumers in understanding their opportunities to apply a wider range of energy effi ciency practices. The Australian Building Code provides a vehicle where greater energy effi ciency and environmental performance could be achieved across all building sectors.

1 IPCC (2007), Summary for Policymakers. In: Climate Change 2007: The Physical Science Basis. Contribution of Working Group I to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change [Solomon, S., D. Qin, M. Manning, Z. Chen, M. Marquis, K.B. Averyt, M.Tignor and H.L. Miller (eds.)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

2 United Nations Framework Convention on Climate Change, Dialogue on long-term cooperative action to address climate change by enhancing implementation of the Convention, retrieved 2007, <http://unfccc.int/meetings/dialogue/items/3668.php>

3 2020 targets have been discussed by Stern, European Union, the Australian States’ Emissions Trading Taskforce and the Prime Minister’s Emissions Trading Task Group.

4 No regrets = actions that have immediate or attractive paybacks, including reputational or marketing benefi ts.

5.

FOURTH, if global engagement is essential for addressing climate change effectively, technological progress provides the essential vehicle for delivering the necessary behavioural changes. There is an important role for strong, effi cient and effective partnerships between business and government in driving transformational technological change at both a national and international level. This is particularly true when, initially at least, the global response, and hence the international carbon price, is likely to lag behind what is required to drive the urgent necessary developments in technology.

FIFTH, adaptation strategies are required to build resilience and reduce vulnerability to climate impacts. Adaptation strategies must be fully integrated into economy-wide development and planning processes to address for example, water resources, health responses, biodiversity, heritage areas and climate-dependent industries.

While recognising the imperative of all aspects of a National Climate Change Response, this report focuses on the fourth issue, namely the need for government to work more closely with business in driving essential step-wise technological change.

Recent modelling suggests that in the absence of new technology development and deployment, Australian greenhouse gas emissions will increase by 170 percent from 2001 to 20505. Australia and the rest of the world must transform the way it produces and uses energy if it is to signifi cantly reduce its greenhouse gas emissions and avert the consequences of climate change. No single technology will meet our low emissions and energy security needs at an acceptable cost. The solution will require a portfolio of technologies to play a role.

Transformational technology development and deployment can take decades of sustained investment in research, development and testing to achieve breakthrough improvements. It is highly capital intensive and investors face considerable barriers in recovering their investment from the marketplace.

Overcoming these challenges requires a coordinated, urgent and long term response by government, business and the wider community. We have therefore recommended Australia introduce a National Low Emission Technology Strategy comprising a range of policies that reduce uncertainty and allow business to capture the opportunities and manage the risks created by the policy framework.

The strategy recognises that while a carbon price is essential, it alone will not drive the required level of investment to transform Australia’s energy landscape. An aspirational emissions reduction target and a range of technology push and demand pull measures are essential. Importantly, a National Low Emission Technology Strategy should focus on technologies in which Australia has a comparative advantage to ultimately drive economic growth and social well-being.

These measures should sit within a broader framework that is driven by climate science and incorporates international cooperation, a national risk assessment, a national energy security policy, forestry, water and land policies, adaptation requirements and ongoing monitoring and review as shown in Figure 1.

While we acknowledge an all-encompassing solution is needed to address climate change, in this paper we have focused on the range of measures we believe will accelerate the development, deployment and commercialisation of low and zero emission technologies. We have also outlined the inherent challenges in commercialising low emission technology that must be overcome by the policy response.

FIGURE 1AUSTRALIAN BUSINESS & CLIMATE GROUP’S RECOMMENDED NATIONAL CLIMATE CHANGE RESPONSE FRAMEWORK.

5 Allen Consulting Group (2006), Deep Cuts in Greenhouse Gas Emissions. Economic, Social and Environmental Impacts for Australia, Melbourne, Australia <http://www.allenconsult.com.au/publications/view.php?id=316>

6.

3. THE TECHNOLOGY DEVELOPMENT CHALLENGE

7.

The development challenge for breakthrough low emission energy technologies centres primarily on increasing scale and reducing cost so that they can substitute globally for current fossil fuel based technologies on a cost effective basis. Accelerating the rate of technology cost and performance improvement will be a key factor in enabling the early widespread deployment of low emissions technologies required for major reductions in global emissions.

3.1 TECHNOLOGY DEVELOPMENT IS COMPLEX, TIME CONSUMING AND EXPENSIVE

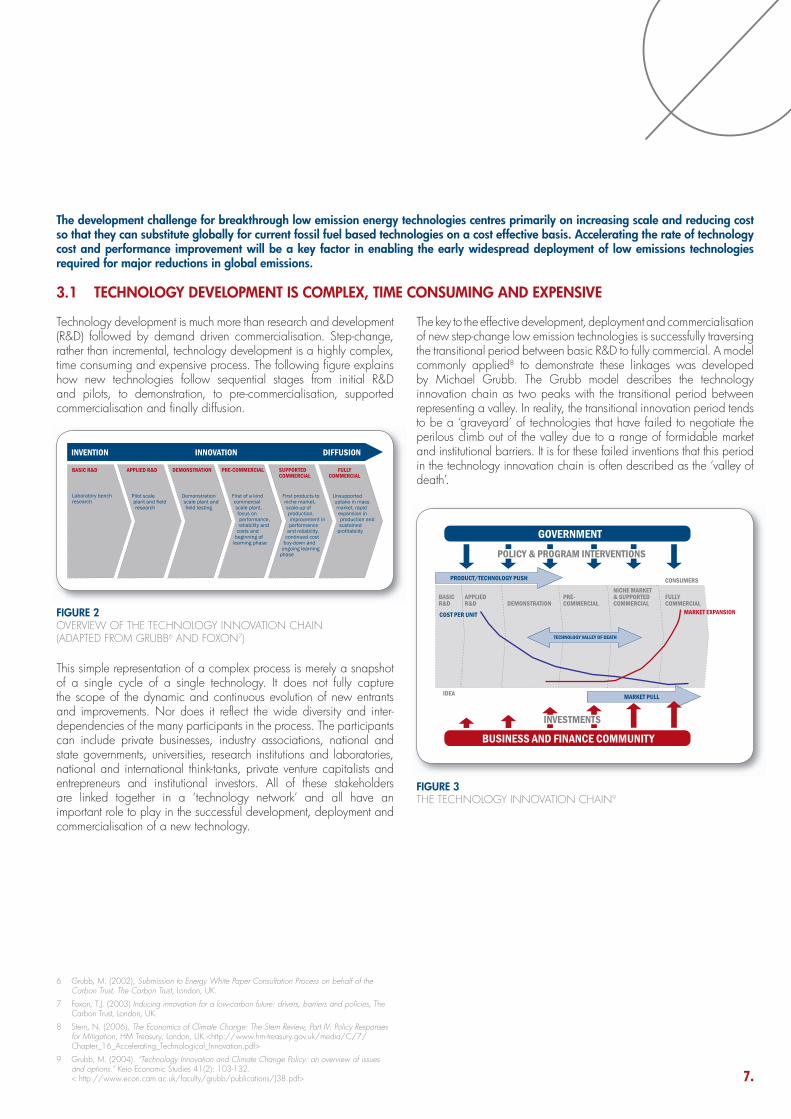

Technology development is much more than research and development (R&D) followed by demand driven commercialisation. Step-change, rather than incremental, technology development is a highly complex, time consuming and expensive process. The following fi gure explains how new technologies follow sequential stages from initial R&D and pilots, to demonstration, to pre-commercialisation, supported commercialisation and fi nally diffusion.

FIGURE 2OVERVIEW OF THE TECHNOLOGY INNOVATION CHAIN(ADAPTED FROM GRUBB6 AND FOXON7) This simple representation of a complex process is merely a snapshot of a single cycle of a single technology. It does not fully capture the scope of the dynamic and continuous evolution of new entrants and improvements. Nor does it refl ect the wide diversity and inter-dependencies of the many participants in the process. The participants can include private businesses, industry associations, national and state governments, universities, research institutions and laboratories, national and international think-tanks, private venture capitalists and entrepreneurs and institutional investors. All of these stakeholders are linked together in a ‘technology network’ and all have an important role to play in the successful development, deployment and commercialisation of a new technology.

The key to the effective development, deployment and commercialisation of new step-change low emission technologies is successfully traversing the transitional period between basic R&D to fully commercial. A model commonly applied8 to demonstrate these linkages was developed by Michael Grubb. The Grubb model describes the technology innovation chain as two peaks with the transitional period between representing a valley. In reality, the transitional innovation period tends to be a ‘graveyard’ of technologies that have failed to negotiate the perilous climb out of the valley due to a range of formidable market and institutional barriers. It is for these failed inventions that this period in the technology innovation chain is often described as the ‘valley of death’.

FIGURE 3THE TECHNOLOGY INNOVATION CHAIN9

6 Grubb, M. (2002), Submission to Energy White Paper Consultation Process on behalf of the Carbon Trust, The Carbon Trust, London, UK.

7 Foxon, T.J. (2003) Inducing innovation for a low-carbon future: drivers, barriers and policies, The Carbon Trust, London, UK.

8 Stern, N. (2006), The Economics of Climate Change: The Stern Review, Part IV: Policy Responses for Mitigation, HM Treasury, London, UK.<http://www.hm-treasury.gov.uk/media/C/7/Chapter_16_Accelerating_Technological_Innovation.pdf>

9 Grubb, M. (2004). “Technology Innovation and Climate Change Policy: an overview of issues and options.” Keio Economic Studies 41(2): 103-132.< http://www.econ.cam.ac.uk/faculty/grubb/publications/J38.pdf>

8.

3. THE TECHNOLOGY DEVELOPMENT CHALLENGE

3.2 FIRST-MOVER BARRIERS

Each stage of low emission technology development and deployment often confronts extraordinary fi rst-mover costs and barriers. These barriers are quite specifi c to initial development and deployment, and are not experienced in the subsequent stages of widespread deployment. Failure to overcome these barriers will stifl e the leadership and innovation needed to move these low emissions technologies to full commercialisation. These barriers compound and can prove to be insurmountable in terms of project developers securing fi nance. The overall risk needs to be reduced in order to provide suffi cient incentive to investors who are seeking to accelerate the deployment of breakthrough technologies. Six types of fi rst-mover barriers are described below.

3.2.1 LOW LEVELS OF COMMUNITY ACCEPTANCE AND UNDERSTANDING Broad community acceptance of a new technology is a pre-requisite to the regulatory and fi nancial support critical for widespread deployment.

All stakeholders must work together to ensure that appropriate technologies are available at scale and acceptable cost to meet future emission constraints.

Engaging with the community is a joint responsibility for government and business. It should be a phased approach and incorporate the following:

• Wide dissemination of broad technology information through a range of suitable communication streams;

• Public consultations to increase awareness of the new

technologies;

• Provision of specifi c and targeted education on the necessity of breakthrough technologies to mitigate the worst impacts of climate change;

• Detailed stakeholder engagement for specifi c projects.

Community acceptance in Australia is also a stepping stone to broader international acceptance. Undertaking effective community consultation in Australia to facilitate the effi cient deployment of breakthrough technologies will also enhance export opportunities. Developing countries have strongly indicated that it is for developed countries to show leadership and to prove the validity of breakthrough technologies, fi rm up costs and reduce technical risks.

First-mover technology developers carry the main burden of gaining community acceptance. At the lower-end of the scale that may be an abnormally high expenditure on community engagement, but it may also require the construction of capital-intensive demonstration projects to give the community confi dence that the technology is safe and effective. The benefi ts of these measures to gain community acceptance fl ow on to all subsequent developers, not specifi cally to the fi rst-mover investors who bear the cost.

3.2.2 REGULATORY UNCERTAINTY

Areas of regulatory uncertainty exist in relation to constraining GHG emissions and to specifi c technologies. Uncertainty is hindering long-term investment decisions today in next generation assets.

Some low emission technologies rely on specifi c geological resources and follow an exploration process as complex and expensive as other mineral resource exploration. Locating large amounts of high quality, secure and low cost hot dry rocks, for example, is as complex and expensive as exploring and defi ning any ore body. These costs can only be recovered when titles can be granted and the project’s carbon value can be determined. As a result, considerable fi rst-mover risks exist for investments made before regulation is determined.

Government, business and broader stakeholders must work together to examine current regulation, its application and in addition identify new regulation. For example, technologies such as carbon capture and storage (CCS) require a new and complex regulatory framework, including:

• The licensing of carbon dioxide storage sites and activities;

• Approvals for critical infrastructure eg carbon dioxide (CO2) pipelines;

• The decommissioning and long-term liabilities associated with storage facilities.

There is also some uncertainty with the treatment of CCS projects under proposed emissions trading schemes, with two alternative approaches being considered, that is, an abatement model and an offset model10. These issues must be resolved promptly to facilitate acceleration of project development.

These regulatory issues continue to give rise to investment uncertainty and compound the already high costs of demonstration and deployment of breakthrough technologies. They are not unique to any particular technology, fossil fuels or renewables, but such uncertainty is

10 Abatement model assumes that the actual emissions of the power station or stripping plant are reported ie tonnes emitted to the atmosphere. A new clean coal + CCS power station should be ~0.1-0.2 tonnes/MWh compared with current conventional coal-fi red power station at ~0.8 tonne/MWh. The offset model requires a plant to report the emissions that would have occurred without the CCS technology and then be granted a credit for the tonnes sequestered.

9.

a signifi cant barrier, particularly for fi rst-of-a-kind plant, as it is virtually impossible to recover these costs from the market.

3.2.3 INSUFFICIENT FUNDING FOR TECHNOLOGY DEMONSTRATION

Technology demonstrations are required to prove and optimise new technologies and to gain community acceptance. Because demonstration projects are developed at much less than commercial-scale, they are almost never commercially competitive. They are also often completely redundant once the demonstration has been completed. While some costs may be recovered by technology providers benefi ting from the improvement of specifi c technical components, these costs are essentially written off on completion of the demonstration.

Although governments in Australia generally recognise the diffi culty in recovering demonstration costs, the scale of the climate change issue requires signifi cant and continued public and private support to promote the technology transformation required to achieve the deep emissions cuts.

A National Low Emission Technology Strategy should defi ne Australia’s objectives and priorities for low emission technology demonstrations. A useful starting point is the successful Low Emissions Technology Demonstration Fund (LETDF). The recent Report of the Task Group on Emissions Trading11 suggests that “there is a case for government involvement in sharing the high risks involved in demonstrating low-emission technologies, particularly in the early stages of a trading scheme”. Such support is justifi ed on the basis that market

demonstration of technologies shows potential purchasers and users that the technology works in real-world application under Australian conditions and promotes market potential.

3.2.4 LACK OF PUBLIC/PRIVATE PARTNERSHIP FRAMEWORK FOR INITIAL COMMERCIAL DEPLOYMENT

Although commercial-scale plants cost more than demonstration plants, they generally benefi t from effi ciencies of scale and should be commercially viable in principle.

However, some ineffi ciencies in fi rst-of-a-kind commercial-scale plants can only be overcome by experience. These learnings ultimately deliver lower costs and higher effi ciencies in subsequent plants, which can be recovered only in part as intellectual property.

This issue has been addressed on a case by case basis by governments in Australia. The next step is to develop an appropriate framework to defi ne the relative share of public and private funding and other mechanisms needed to support the commercialisation of fi rst-of-a-kind low emission technologies. Australia requires a comprehensive mitigation strategy including an emissions trading scheme combined with a continued focus on technology cooperation and a concerted international strategy to maximise Australia’s contribution to global action. A National Low Emission Technology Strategy will complement a national emissions trading scheme to ensure that investors have suffi cient incentive to develop breakthrough technologies through to commercial scale.

11 Prime Ministerial Task Group on Emissions Trading (2007), Report of the Task Group on Emissions Trading, The Department of the Prime Minister and Cabinet, Barton, Australia, pp. 130.http://www.pmc.gov.au/publications/emissions/index.cfm#viewing

‘Community acceptance in Australia is also a stepping stone to broader international acceptance.’

10.

3.2.5 INSUFFICIENT FUNDING FOR INFRASTRUCTURE REQUIREMENTS

Low emission power generation on the scale required to meaningfully impact on greenhouse gas emissions requires substantial amounts of new infrastructure such as carbon dioxide transport for CCS technology or electricity transmission in the case of geothermal or other renewable resources. While future carbon price signals will enable market participants to better judge investments, it is anticipated that a partnership of public and private support will still be needed to help infrastructure development to overcome the fi rst-mover barriers.

Initial over-sizing of capacity incurs short term costs but should facilitate future, larger-scale developments by spreading the cost over a larger energy production base, for example the use of carbon dioxide pipeline hubs. Public funding may be required initially and then decline over time, once the initial infrastructure is in place and the carbon dioxide market is mature.

The requirements, objectives and criteria for public funding or participation should be defi ned as part of a National Low Emission Technology Strategy to assist in the initial deployment of infrastructure to support low emission technologies in Australia.

3.2.6 SKILLS DEFICIT

The current skills defi cit in Australia, specifi cally related to technical expertise, is a barrier for fi rst-of-a-kind projects as the investment is higher than would be expected for following projects. First-of-a-kind projects will need to contribute directly to training programs, international recruitment and specialised on-site skills development. As an example, the growth of the Solar PV manufacturing industry in Australia has required signifi cant investment in a skilled worksforce.

The skills and competencies of the workforce are of growing importance to the energy sector, as they are for the economy as a whole. It is crucial that employers have the trained staff they need for the safe and effi cient operation of their businesses and the reliable supply of energy to their customers. It is also crucial that workers have the skills and fl exibility to handle the new technologies and business practices that will emerge in the coming decades.

As an example, The United Kingdom (UK) Government’s Skills Strategy12 aims to ensure that employers across all sectors can recruit people who have the right skills. The recent Leitch Review13 illustrated

the signifi cant challenges that face the UK and recommended that the UK should commit to becoming a world leader in skills by 2020, benchmarked against the upper quartile of the Organisation for Economic Co-operation and Development (OECD).

Australia must also place a great emphasis on developing a skilled workforce to meet the requirements of these specialised new technology projects as we will be competing internationally for qualifi ed resources.

Government has an important role to play in providing the right framework and to work with employer organisations and trade unions to ensure that education and training is delivering the right skills. However, it is for employers to ensure that the workforce is equipped with the work-specifi c skills they need.

Skills gaps in the energy sector are also increasing because the workforce is faced with unfamiliar processes and technologies. Skills shortages, on the other hand, are likely to increase because the workforce profi le is older than the population profi le and many workers will retire in the coming decade. Workforce retirement will coincide with higher demand for people to deliver the increased investment needed to replace old power stations and infrastructure. Where they occur, skills shortages will affect all levels from apprentices to graduates and above.

Workforce mobility and retention place additional pressures on the energy sector. Skills shortages tend to produce a churn of workers as they move around the industry. Internationally, while Australia remains attractive to workers from overseas, there are also rewarding opportunities for our own workers in other countries. Australia must continue to be an attractive investment option for the companies currently operating here, who have a key role in skills development and to new companies seeking to invest.

3. THE TECHNOLOGY DEVELOPMENT CHALLENGE

12 Department for Education and Skills (2005), White Paper: Skills – Getting on in business, getting on at work, Department for Education and Skills, UK.<http://www.dfes.gov.uk/publications/skillsgettingon/>

13 Leitch, S. (2006) Leitch Review of Skills, Prosperity for all in the global economy – world class skills, HM Treasury, London, UK.< http://www.hm-treasury.gov.uk/independent_reviews/leitch_review/review_leitch_index.cfm>

11.

Australia has signifi cant world-class fossil fuel reserves – brown coal, black coal and gas. These fuels have underpinned the relatively cheap energy supply in Australia, which in turn has contributed to the highly competitive nature of energy-intensive industries. The climate change challenge requires a re-evaluation of the use of these greenhouse-intensive fossil fuels, in Australia and globally.

Due to economic, environmental and social considerations, there is a strong desire to develop low emission technologies that will allow the continued but cleaner utilisation of these fuels. Many will also point to the need for diversity and security of supply as compelling reasons to ensure Australia has a broad portfolio of supply options.

Effective carbon capture and storage (CCS) of greenhouse gas (GHG) emissions from power stations would allow Australia to signifi cantly reduce its national GHG emissions. Electricity generation currently accounts for about 200 million tonnes (Mt) per annum of GHG emissions and 2020 projections with current policy settings are 241 Mtpa. These emissions are at least 33 per cent of total national emissions. Obviously if deep cuts are to be made in national GHG emissions, electricity generation must be a key target industry.

The processing of natural gas also provides opportunities for the deployment of CCS to reduce GHG emissions. These industrial processes produce high-concentration carbon dioxide (CO2) as a by-product, drastically reducing the cost of capture relative to other processes such as power generation. This concentrated CO2 stream therefore provides opportunities for early deployment of relatively low-cost CCS. Coal gasifi cation for the production of liquid fuels or chemicals has similar early deployment characteristics.

Australia also exports fossil fuels; Australia is the largest exporter of coal in the world and a major exporter of LNG. A clear, demonstrated affordable pathway to less carbon-intensive uses of fossil fuels would signifi cantly boost the ability of coal-reliant countries to reduce their emissions. In pure economic terms, there are opportunities for Australia to demonstrate cleaner technologies utilising these fuels for customers. As an example China builds one new 1GW1 power station every four days2. If it were possible to provide China with access to affordable CCS, then for each of these power stations it is possible that rather than adding the equivalent of ~8Mtpa GHG emissions every four days, this could be reduced to between to between 0-0.8Mtpa per plant.

Broad global deployment of power generation with CCS also is of benefi t to Australia in terms of potential reduced climate impacts if global emissions can be stabilised. Australia is highly vulnerable to climate impacts and reducing these threats is of great national benefi t.

Australia is relatively well served with potential storage sites for CCS and has a number of high concentration CO2 sources that provide an opportunity for early low-cost deployment. By exploiting this national advantage through early adoption of the technology, Australia can demonstrate leadership in CCS development which in turn could foster additional international collaboration.

Successful demonstration of CCS in Australia should contribute to the eventual deployment internationally and give Australian businesses a lead in the design, construction and operation of CCS technologies. Early commercial demonstration is of national benefi t by building the skills base and expertise to export the know-how.

1 1GW = 1 gigawatt of thermal power = 1000 megawatt (MW)2 World Energy Outlook 2006, IEA http://www.worldenergyoutlook.org/

CASE STUDY 1: CARBON CAPTURE AND STORAGE IN AUSTRALIA

4. EMISSIONS TRADING SCHEME

13.

Emissions trading is a key component of a National Climate Change Response. Emissions trading, if well designed, provides a clear medium-long term abatement pathway and an explicit carbon price.

4.1 A SIGNIFICANT AND CLEAR LONG-TERM EMISSIONS REDUCTION TARGET

14 Factsheet: Setting a Long-Term Aspirational Emissions Goal, www.pmc.gov.au/publications/climate_policy/docs/long-term_emissions_goal.rtf

An important component of an emissions trading scheme are the forward targets. A long-term aspirational goal for reducing GHGs is essential. It is important to commit early to this target to communicate the magnitude of the challenge, to drive investment in low emission technologies and to drive behavioural change in the use of energy, in particular.

In early August 2007, the Federal Government stated it intends to introduce a long-term emissions reduction target next year, following analysis of the impact on Australia’s economy and on families14.

Knowing the likely trajectory of future emission prices is necessary for public and private sector decision-makers to rationally plan their R&D and capital investment decisions.

Some overseas governments and the Federal Opposition have suggested a goal of 60 per cent reduction on 2000 levels by 2050 based on IPCC advice about the need to stabilise emissions. Some State governments have legislated for a 60 per cent reduction by 2050. This target is signifi cant and challenging but will give Australians a clear sense of the task.

The Australian Business and Climate Group did not review the environmental, equity or economic merits of any specifi c long-term target.

It is expected that climate change science will drive modifi cations to long-term goals over time, so the critical issue is to set an aspirational goal as soon as possible with a mechanism to recalibrate this as technologies, markets and knowledge of climate science develops.

A clear long-term goal would provide the vision and clarity needed to deliver greater regulatory certainty and to guide the scope, development and deployment of technology over the long times associated with major energy infrastructure.

The Australian Business and Climate Group believes that an emissions trajectory, with interim targets needs to be established in line with the long-term aspirational goal to provide an explicit guide for business investment and community engagement. It is expected that such an overall emissions trajectory would commence moderately and progressively stabilise and then reduce signifi cantly over time as breakthrough technologies become available at scale and acceptable cost.

14.

4. EMISSIONS TRADING SCHEME

The Norwegian Government has set a double ambition: to strengthen Norway’s role as a provider of both energy security and climate security. It is certainly a dilemma – Norway with an ambition of being both a leading petroleum producer and a leading player in efforts to limit climate change. As the world’s third largest exporter of oil and gas, the Norwegian Government has accepted a special responsibility for securing supply to a broad range of customers.

The Norwegian Government has developed a range of policies to drive the commercialisation of low emission technologies. These policies are in addition to its decision to join the European Emissions Trading Scheme in 2008.

It has successfully driven the uptake of carbon capture and storage (CCS) technology through the introduction of tough regulatory measures, in addition to strong project support through public funding. The Sleipner project – offshore geosequestration – has been operated since 1996 by Statoil as a direct result of the Norwegian regulatory measures. Since this process began, just under eight million tonnes of carbon dioxide (CO2) have been deposited.

The result is that today, the Norwegian continental shelf is the most energy-effi cient petroleum producing region in the world, with CO2 emissions that amount to less than one third of the global average per unit produced.

Norway’s gas reserves have not previously been used for domestic power generation but the Government has now identifi ed the need to demonstrate integrated gas-fi red power generation with CCS for its global customers and to contribute to climate security. The Government has announced that these new gas-fi red power plants must have CCS and has committed to cooperating with industry to develop the projects. Offi cial requirements for carbon capture means that such projects would not be industrially profi table without government aid. One approach has been to establish a state-owned company to manage the government’s interests in carbon dioxide capture and storage projects, The Norwegian Government aims to contribute to technological development and broad use of CCS.

While the Government will initially own equity in these projects in order to accelerate development, the intention is to bring in more industrial partners and thereby decrease the state’s ownership. This approach will also ensure that technological developments in Norway will have broad international relevance and will not be project-specifi c to Norway. The Norwegian Government has accepted the high commercial risk in the early phases of these projects and has been willing to put in public money in the early phases. In order to further reduce technical and fi nancial risks, several technological solutions will be tested in parallel in the fi rst phase of the project.

The Norwegian model is based on the justifi cation that public/private joint investment in these gas-fi red power projects with carbon capture and storage offer the potential for a win-win-win outcome for industry, the environment and society.

Source: Statoil Magazine No 2, 2006 http://www.statoil.com/statoilcom/svg00990.nsf/Attachments/co2/$FILE/co2_eng.pdf

BOX 1: INNOVATIVE NORWEGIAN GOVERNMENT POLICIES

Industry• Large-scale CO2 for enhanced oil

recovery• Improved security of supply

Environment• Reduction of CO2 and NOX emissions

through offshore electrifi cation• Industrial utilisation of greener fossil fuel• Technologies with a global market

potential

Society• Prolonged fi eld life and increased oil

recovery• National electricity grid benefi ts

POLICIES DESIGNED TO ACCELERATE THE DEPLOYMENT OF LOW EMISSION TECHNOLOGIES CAN LEAD TO SUCCESSFUL OUTCOMES FOR ALL STAKEHOLDERS.

15.

4.2 A NATIONAL EMISSIONS TRADING SCHEME

The Australian Business & Climate Group strongly supports the introduction of an emissions trading scheme as an appropriate mechanism to deliver emission reductions and believes the resulting carbon price should immediately drive the uptake of mature and some near-commercial low emission technologies.

An Australian emissions trading scheme, with a carbon price set by the market, would improve business investment certainty and strengthen the incentives to develop low-emissions technologies. This was the view of the recent Prime Minister’s Emissions Trading Task Group15 and the States and Territories’ National Emissions Trading Taskforce16. While this is true, the stringency of the carbon constraint will affect the pricing of carbon and accordingly the fundamental economics and potential competitiveness of technologies.

It is now fully expected that Australia will have a domestic emissions trading scheme by at least 2012 but there are no fi rm design rules. And the devil will be in the detail. A domestic Australian scheme is likely to be the second largest scheme operating internationally, after the European Union Emissions Trading Scheme. The complexity of the proposed Australian scheme, in terms of sectoral and greenhouse gas coverage, will mean that other countries will be interested in assessing its performance. It will be important to work collaboratively with other jurisdictions to determine the most effective option for linking the domestic scheme with international trading regimes.

There are a number of design parameters that will directly impact on the commercialisation prospects for low emission technologies, for example:

• Initial emission target (cap) and future targets linked to the aspirational goal;

• Allocation rules;

• Inclusion of international offsets and any limitation on these offsets.

The design of such an Australian emissions trading scheme will have signifi cant impacts on:

• Market demand to increase energy effi ciency and reduce emissions intensity;

• The level of uptake of existing low emission technologies;

• Market confi dence and pricing of risk into market decisions;

• The confi dence of private investors to support R&D of new technologies and their willingness to bring fi rst-of-a-kind technologies to commercial scale within Australia.

As the carbon price increases, low emission projects appear relatively more commercially attractive to energy suppliers, private investors and consumers. Introducing carbon risk into existing fi nancial markets is also likely to deliver new capital markets such as carbon derivatives, increasing the capital pool.

15 ibid., p. 9, May 2007

16 National Emissions Trading Taskforce (2006) Discussion Paper: Possible Design for a National Greenhouse Gas Emissions Trading Scheme.http://www.emissionstrading.net.au/key_documents/discussion_paper

‘A domestic Australian scheme is likely to be the second largest scheme operating internationally, after the European Union Emissions Trading Scheme.’

16.

5. NATIONALLOW EMISSION TECHNOLOGY STRATEGY

17.

5.1 CLEANER ENERGY PRODUCTION

Energy is central to the climate change issue; the largest contributing sectors for GHG emissions are fossil fuel-fi red power generation and combustion of fossil fuels. Investments in power generation typically have a long lead time, including commercial scale demonstrations, thus there is a premium on early action.

A cleaner, demonstrated affordable pathway to a lower carbon future would signifi cantly boost the confi dence of fossil fuel dependent countries such as Australia, China, India and USA and increase the prospects for a long-term international abatement framework. The global challenge therefore is how to accelerate the deployment of technologies that allow us to balance the use of fossil fuel fi red energy while reducing GHG emissions. Urgent action is required as current international policies are projected to lead to about 70 per cent of global electricity to be still fossil fuel dependent in 2030. New energy systems are required and development timeframes are long.

Deployment of technologies that have overcome the technical hurdles brings opportunities for service organisations, from small scale installers of solar photovoltaic (PV) systems through entrepreneurial project developers to the major construction and fi nance houses required to develop, for example, integrated gasifi ed combined cycle (IGCC) plant with CCS. Some technologies create business opportunities by bringing together new groupings of existing industries, for example carbon capture and storage where utilities, oil companies and process plant design experts are developing new relationships.

Development and deployment of low emission technologies in Australia contributes to our international emission reduction objectives. We can build on experience and expertise in Australia to develop our strategy overseas, establishing relationships at both a strategic and technical

level. These relationships will infl uence the international debate on new carbon technologies and help to facilitate the cost-effective roll-out of technologies globally.

The global technical challenge is unprecedented; managing the risks of climate change will require a profound, systematic and global transformation in the production and consumption of energy. Incremental improvements in technology will help but will not by themselves lead to stabilisation. Currently available technologies can slow the growth of emissions, however considerable technology advancement is needed to reduce the cost of the much larger reductions required for stabilisation. Successful investments in technologies that are not yet in widespread commercial use, eg geosequestration, can save trillions of dollars in the cost of addressing climate change17.

However, government assistance to deploy high-cost technologies will not provide cost-effective abatement in the very near-term, therefore such policies must meet very high thresholds of policy justifi cation. As an example, there must be an objective to drive signifi cant cost reductions for subsequent Australian and international application of the technologies. This is the technology dilemma – Australia’s current energy costs are relatively low and even with a modest price of carbon, will remain so but we will need breakthrough technologies at scale and acceptable cost within the next 20 years in order to meet tightening carbon constraints.

The National Low Emission Technology Strategy should defi ne the Australian objectives and priorities for low emission technology demonstrations and fi rst-of-a-kind commercial plant, and the rationale and criteria for sustained public support.

17 Global Energy Technology Strategy Program (2007) Global Energy Technology Strategy Addressing Climate Change: Phase 2 Findings from an International Public-Private Sponsored Research Program, Joint Global Change Research Institute, MD, USA.http://www.pnl.gov/gtsp/publications/

18.

5. NATIONAL LOW EMISSION TECHNOLOGY STRATEGY

5.2 GUIDING PRINCIPLES

This paper seeks to be a catalyst for discussion between all stakeholders in order to develop appropriate policies to accelerate the uptake of breakthrough technologies. The Australian Business & Climate Group believes this discussion will lead to the implementation of a National Low Emission Technology Strategy which should be a key element of a National Climate Change Response.

The technology strategy must adopt the following guiding principles to be effi cient and effective in delivering signifi cant and sustained emission reductions in Australia over the long term. The strategy must:

• Provide a national approach to low emission technology development, and integrate it into an international collaboration to maximise the effi ciency and pace of development while avoiding wasteful duplication;

• Support key step-change technologies that have globally signifi cant emissions reduction potential and are aligned with Australia’s national interests but otherwise be technology and fuel neutral;

• Be suffi ciently fl exible so that Australia can respond to international developments and continuously benefi t from the learnings that will arise during the early stages of its implementation;

• Be built around the specifi c characteristics of the key technologies and the processes underpinning their development, deployment and commercialisation;

• Sustain Australia’s economic resilience and ensure that leadership in technology development compares favourably with investment in conventional technologies;

• Encourage a collaborative approach between business and governments to capture signifi cant national benefi ts;

• Ensure that government support must not confl ict with price signals provided by the market; and

• Include a rigorous assessment of public good/value for money and technical scrutiny.

In terms of the assessment of public good/value for money, it is important that innovative approaches be considered so that where public funds are contributed, there is a mechanism where the Australian public benefi ts. Benefi ts may include returns through tax, employment, meeting policy objectives and in some cases, a direct return on investment. As an example, the Federal Government assists Australians to gain tertiary education through HECS, but there is also a payback from the benefi ciaries if they secure employment.

5.3 TECHNOLOGY PUSH MECHANISMS

Technology push policies are designed to move untested innovations through the valley of death and into commercialisation. These policies recognise that large-scale investors are mostly unwilling to fi nance untested technology development, increasing the reliance on push mechanisms to accelerate the development and initial deployment of early stage technologies.

GOVERNMENT FUNDING

To signifi cantly reduce greenhouse gas emissions, Australia must invest tens of billions of dollars in addition to planned capital commitments. While the private sector is prepared to fund much of this incremental expenditure on a commercial basis, governments must ensure public sector investment and support is commensurate with the magnitude of the challenge. Government support is particularly important in the initial technology development phase.

The Australian Business & Climate Group acknowledges government support given to date, in particular the Low Emissions Technology Demonstration Fund, however governments need to contribute additional funds over the long term and within a strategic framework to support technologies through the valley of death within the required timeframe.

Non-commercial expenditure on demonstration projects undertaken to gain global community acceptance of the technology is clearly not recoverable by the project proponents. The requirement for such projects suggests not only a need for public funding, but also the need for development under international collaborative programs designed to avoid unnecessary duplication and costs.

Government support could include capital grants, tax incentives and accelerated depreciation, as well as other assistance mechanisms. A research and development fund for new technologies and a parallel fund to fi nance fi rst-of-a-kind demonstration/ commercial plants are also needed. These initiatives should complement existing approaches such as the Federal Government’s Innovation Investment Fund.

Public investment in infrastructure that supports emerging technologies, such as refuelling infrastructure for alternative-fuel vehicles or pipeline infrastructure for new CCS technologies, is also needed.

PUBLIC/PRIVATE FUNDING AND RISK SHARING SCHEMES

Transformational technology development risk is too substantial to be borne by any one participant, so direct government participation is needed to reduce project risks and facilitate preferential fi nancing. This could include third party covenant and tri-partite contracts between government, technology suppliers and project developers or fi nancing vehicles, such as a national low emission technology fund.

19.

Australia is home to the largest Solar PV manufacturing plant in the southern hemisphere, and is well recognised for having pioneered world leading technology and innovation.

Australian manufacturers of Solar PV and components export a signifi cant volume and value of product to markets all over the world. This trend is expected to strengthen as current overseas markets mature and new markets emerge.

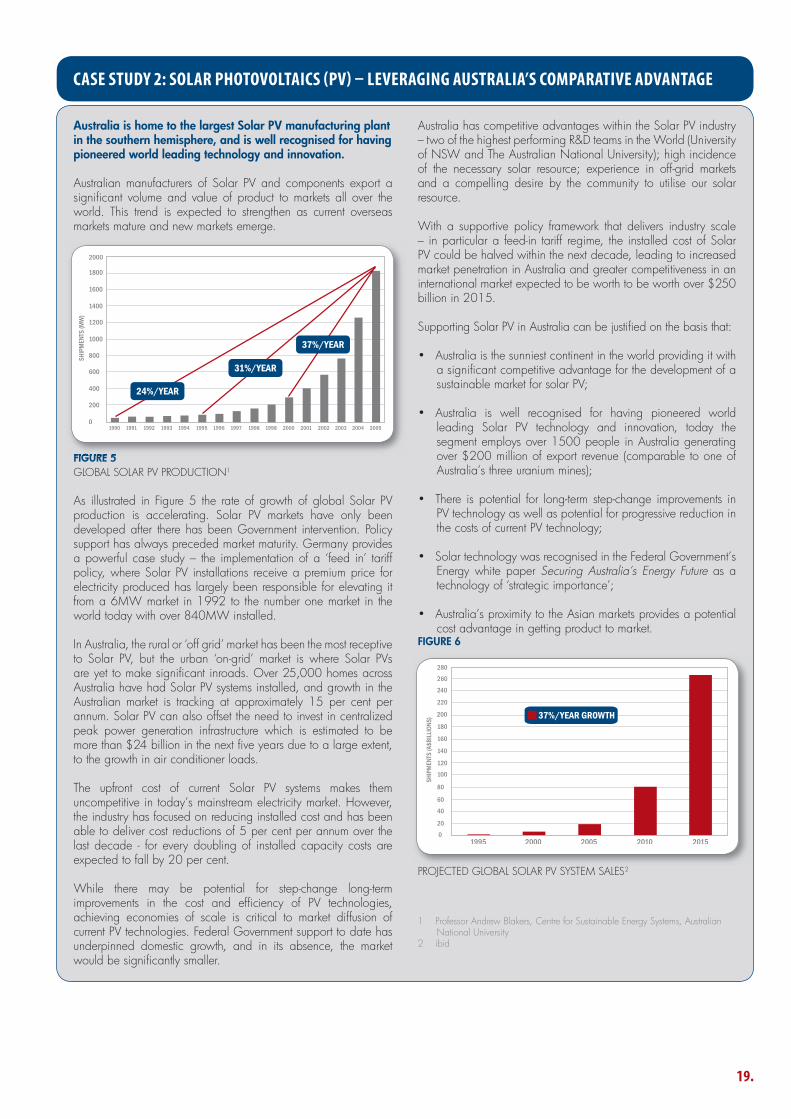

FIGURE 5GLOBAL SOLAR PV PRODUCTION1

As illustrated in Figure 5 the rate of growth of global Solar PV production is accelerating. Solar PV markets have only been developed after there has been Government intervention. Policy support has always preceded market maturity. Germany provides a powerful case study – the implementation of a ‘feed in’ tariff policy, where Solar PV installations receive a premium price for electricity produced has largely been responsible for elevating it from a 6MW market in 1992 to the number one market in the world today with over 840MW installed.

In Australia, the rural or ‘off grid’ market has been the most receptive to Solar PV, but the urban ‘on-grid’ market is where Solar PVs are yet to make signifi cant inroads. Over 25,000 homes across Australia have had Solar PV systems installed, and growth in the Australian market is tracking at approximately 15 per cent per annum. Solar PV can also offset the need to invest in centralized peak power generation infrastructure which is estimated to be more than $24 billion in the next fi ve years due to a large extent, to the growth in air conditioner loads.

The upfront cost of current Solar PV systems makes them uncompetitive in today’s mainstream electricity market. However, the industry has focused on reducing installed cost and has been able to deliver cost reductions of 5 per cent per annum over the last decade - for every doubling of installed capacity costs are expected to fall by 20 per cent.

While there may be potential for step-change long-term improvements in the cost and effi ciency of PV technologies, achieving economies of scale is critical to market diffusion of current PV technologies. Federal Government support to date has underpinned domestic growth, and in its absence, the market would be signifi cantly smaller.

Australia has competitive advantages within the Solar PV industry – two of the highest performing R&D teams in the World (University of NSW and The Australian National University); high incidence of the necessary solar resource; experience in off-grid markets and a compelling desire by the community to utilise our solar resource.

With a supportive policy framework that delivers industry scale – in particular a feed-in tariff regime, the installed cost of Solar PV could be halved within the next decade, leading to increased market penetration in Australia and greater competitiveness in an international market expected to be worth to be worth over $250 billion in 2015.

Supporting Solar PV in Australia can be justifi ed on the basis that:

• Australia is the sunniest continent in the world providing it with a signifi cant competitive advantage for the development of a sustainable market for solar PV;

• Australia is well recognised for having pioneered world

leading Solar PV technology and innovation, today the segment employs over 1500 people in Australia generating over $200 million of export revenue (comparable to one of Australia’s three uranium mines);

• There is potential for long-term step-change improvements in

PV technology as well as potential for progressive reduction in the costs of current PV technology;

• Solar technology was recognised in the Federal Government’s Energy white paper Securing Australia’s Energy Future as a technology of ‘strategic importance’;

• Australia’s proximity to the Asian markets provides a potential cost advantage in getting product to market.

FIGURE 6

PROJECTED GLOBAL SOLAR PV SYSTEM SALES2

1 Professor Andrew Blakers, Centre for Sustainable Energy Systems, Australian National University

2 ibid

CASE STUDY 2: SOLAR PHOTOVOLTAICS (PV) – LEVERAGING AUSTRALIA’S COMPARATIVE ADVANTAGE

20.

In order to meet this unprecedented technology challenge to mitigate the impacts of climate change, innovative and creative mechanisms will be required. This paper seeks to draw out discussion on these options. There are some innovation policies emerging internationally that provide interesting examples for Australia to consider. These creative policies are outlined in Box 1 (Norway) and Box 2 (UK).

APPROPRIATE RISK MANAGEMENT APPROACHES

Financing instruments can be tailored to meet the risk/return profi le of specifi c technology investment opportunities. Aligned to the technological development pathway, there is a parallel fi nancial pathway from speculative to mature fi nance. Many of these fi nancial instruments already exist and will be deployed for new industries and technologies, particularly as risk/return payoffs become more feasible. Similarly, with appropriate market demand, insurers will develop products to manage and transfer risk across the technology spectrum.

PUBLIC AWARENESS AND ENGAGEMENT

Campaigns to raise public awareness and acceptance of new technologies and to facilitate behavioural change, similar to those used to promote sun protection, water conservation and to eliminate drink driving, would contribute to more thorough community understanding and thus widespread growth in consumer demand.

Broad community acceptance of carbon storage, for example, is generally recognised as a pre-requisite for widespread commercial deployment, and there is an equally general recognition that broad community acceptance will require a substantial number of large-scale storage demonstration projects world-wide, to allay community concerns over the viability and environmental credentials of the technology.

The National Low Emission Technology Strategy should seek alignment and rationalisation of community acceptance projects in Australia with complementary projects around the world, providing suffi cient funding to ensure Australia plays its part in low emission technology development while leveraging the value of comparable projects undertaken in other parts of the world.

5.4 DEMAND PULL MECHANISMS

A carbon pricing signal, introduced through an Australian emissions trading scheme is critical for the effective pull-through of breakthrough low emission technologies. The Australian Business & Climate Group strongly supports the current bi-partisan government support for the introduction of a domestic scheme that is capable of being linked to international regimes. From a fi nancing perspective, having a carbon price signal means investors who might hesitate to take on an uncertain liability are better able to price the risk, determine the actual level of liability,

5. NATIONAL LOW EMISSION TECHNOLOGY STRATEGY

Following the 2007 UK Budget announcement, the UK Government is engaged in designing a competition framework for carbon capture and storage (CCS) demonstration. The intention is to launch the competition in November 2007.

The criteria against which proposals will be assessed are likely to include the need for any project proposal to:

• Be located in the UK;

• Cover the full chain of CCS technology on a commercial scale power station (capture, transport and storage);

• Be based on sound engineering design (reliable and safe) underpinned by a full front-end engineering and design study;

• Set out the quantum of fi nancial support requested;

• Be at least 300MW, and capture and store around 90 per cent of the carbon dioxide and thereby contribute at least an additional 0.25 Mt/yr of carbon savings to the UK’s domestic abatement targets (relative to a gas-fi red power station of equivalent size without CCS);

• Start demonstrating the full chain of CCS at some point between 2011 and 2014;

• Address its contribution to the longer term potential of CCS in the UK, (for example, through the potential of shared infrastructure) and to the international development of CCS; and

• Be supported by a creditworthy developer entity.

As part of the competition, project developers will therefore also be expected to include proposals for knowledge and know-how transfer to third parties. These will need to be suffi cient to meet the Government’s aims to encourage the wider deployment of CCS in the UK, Europe and internationally, particularly in countries with signifi cant future energy needs such as China and India. The UK is working with the European Commission to ensure that the development of CCS in the UK fi ts with the objective agreed at the European Council in March 2007 to have in place up to 12 CCS demonstration projects in Europe by 2015.

Source: Department of Trade and Industry (2007), A White Paper on Energy: Meeting the Energy Challenge, The Stationery Offi ce, Norwich, UK.<http://www.dti.gov.uk/energy/whitepaper/page39534.html>

BOX 2: CCS UK COMPETITION

21.

18 Chapman, P (2001), Stimulating economic growth: fl ow through investment structures for venture capital, Australian Venture Capital Association Limited, Sydney, Australia.

19 Sources: Venture Source (US); GBS, Quay Partners, Access Economics (Australia) as referenced in lecture material Financing Entrepreneurial Ventures, University of Melbourne Business School

and estimate whether they can earn an adequate return for that risk. Carbon risk can be actively managed, retained, transferred or bought and sold. Low emissions projects will therefore appear increasingly attractive since the carbon liability is lower than for high emissions projects.

A range of complementary measures will be required for sectors not covered by an emissions trading scheme or where a market failure is clearly identifi ed. Examples may include performance benchmarking and nationally uniform performance standards to drive energy effi ciency in residential and commercial buildings and more effi cient motor vehicles.

5.5 SUPPORT MECHANISMS

The following additional mechanisms are essential in enabling the implementation of technology push and demand pull measures.

INSTITUTIONAL FRAMEWORK

National legislative and governance arrangements are needed to support policy development and implementation. These arrangements should ensure that the relevant commercial and public institutions operate at arms length from the political process given the long-term nature of the challenge and the need for policy stability.

INTERNATIONAL ARRANGEMENTS

The timing and scale of the challenges presented by climate change are such that sustained large scale international action is required. Australia is well positioned to contribute to an international technology-led response and should play a lead role in fostering global cooperation. Australian leadership in the development of clean coal technologies for instance, can contribute to emissions reductions in coal-dependent emerging economies such as China and India – a pre-requisite for reducing global emissions. Our respected track record in developing technological intellectual property and capacity for innovation will also support our international position. The Australian Business & Climate Group believes that initiatives such as the AP6 and the Australia-China Joint Coordination Group on Clean Coal Technology are useful in this regard.

Any national technology response needs to refl ect wider global technology developments in key jurisdictions.

5.6 FINANCING OF LOW EMISSION TECHNOLOGY IN AUSTRALIA

In order to secure suffi cient private capital to fund the development and deployment of new technologies, it is important to address the fi nancial risk landscape.

The key element determining decisions around private capital deployment is risk, and more specifi cally the risk/return relationship. In simple terms, the more uncertainty exists, the higher the risk, the more scarce, and expensive the capital. Aligned to the technological development pathway explored above, leading from invention to commercial deployment, there is a parallel fi nancial pathway from speculative to mature fi nance. In the early ‘speculative’ stages of fi nancing, that is venture capital, there is a high degree of uncertainty and a steep risk landscape, arising from the inability to accurately assess the duration of risk exposure, the fruits of success, or the ultimate cost of failure. Revenue streams are generally small or non-existent.

As a result, investors in this developmental phase apply strongly speculative strategies, typically deploying small amounts of capital in a broad range of opportunities, with a high required rate of return. This is a particular problem for investments in clean energy, which is highly capital intensive. Those with suffi cient capital, that is the debt markets, do not normally operate in the venture capital space.

Hence capital for these projects is scarce, fragmented and expensive, usually with a short term investment horizon.

Financing low emission technologies, whether in the R&D phase or throughout the commercialisation process, involves careful balancing of a number of risks other than the core fi nancial and technology risks. A clear regulatory framework governing each investment area is essential in determining risk. This would need to address key questions around how the new technology would be regulated, what the costs of compliance would be and any other constraints on economic outcomes.

Attracting suffi cient capital to fi nance low emission technology development and deployment in Australia is a signifi cant challenge. The venture capital sector in Australia is small relative to countries such as the United States. It does not have the scale to fund substantial pre-commercial development of breakthrough low-emissions technologies18. By way of contrast, the United States between 1998 and 2005 had 52 times the number of new venture capital funds than Australia, with average fund sizes roughly double those of Australian funds19.

As a result, there is much more reliance in Australia on government support to bring forward new technologies to a point where private capital will be attracted. Policy enablers are therefore needed to bring forward this entry point, lower the investment risk and help bridge the technology ‘valley of death’.

Addressing the major risk drivers helps mitigate uncertainty and ‘fl attens’ the investment risk landscape. As a result, the ‘risk premium’ costed into investment hurdle rates is reduced, and additional funds start to fl ow into capital projects from investors who are willing to accept a lower return but with more certainty.

22.

5. NATIONAL LOW EMISSION TECHNOLOGY STRATEGY

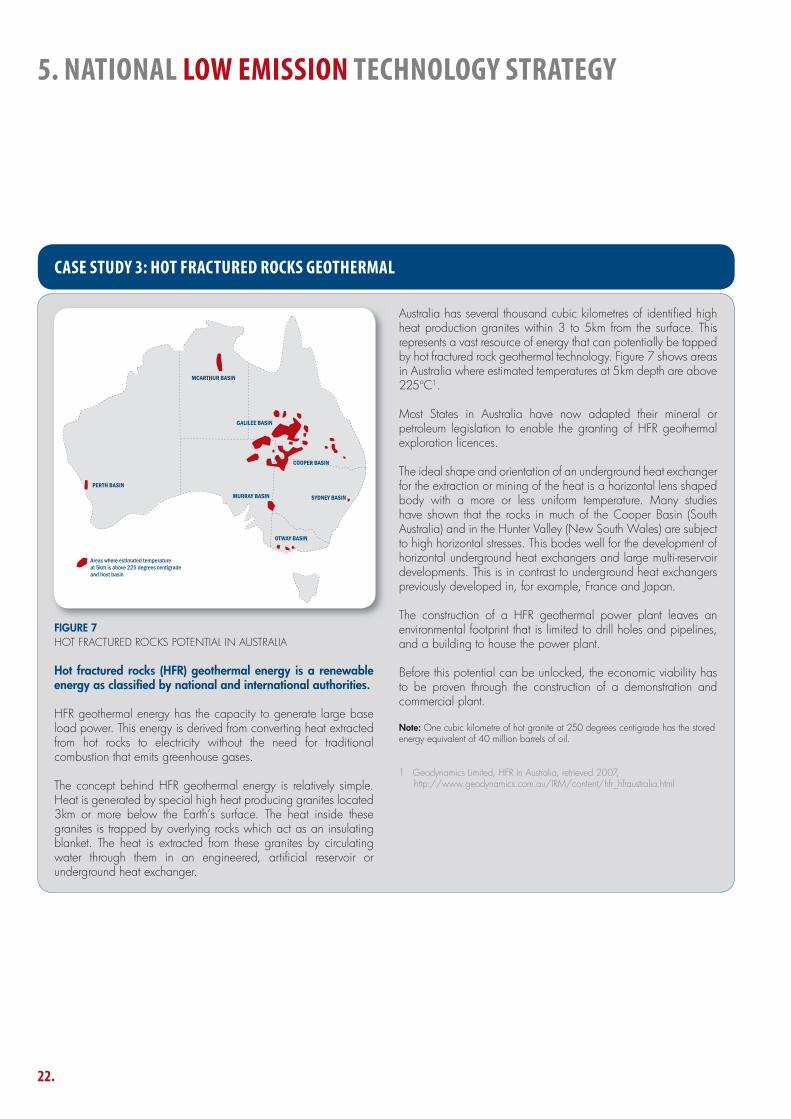

FIGURE 7HOT FRACTURED ROCKS POTENTIAL IN AUSTRALIA

Hot fractured rocks (HFR) geothermal energy is a renewable energy as classifi ed by national and international authorities.

HFR geothermal energy has the capacity to generate large base load power. This energy is derived from converting heat extracted from hot rocks to electricity without the need for traditional combustion that emits greenhouse gases.

The concept behind HFR geothermal energy is relatively simple. Heat is generated by special high heat producing granites located 3km or more below the Earth’s surface. The heat inside these granites is trapped by overlying rocks which act as an insulating blanket. The heat is extracted from these granites by circulating water through them in an engineered, artifi cial reservoir or underground heat exchanger.

Australia has several thousand cubic kilometres of identifi ed high heat production granites within 3 to 5km from the surface. This represents a vast resource of energy that can potentially be tapped by hot fractured rock geothermal technology. Figure 7 shows areas in Australia where estimated temperatures at 5km depth are above 225oC1.

Most States in Australia have now adapted their mineral or petroleum legislation to enable the granting of HFR geothermal exploration licences.

The ideal shape and orientation of an underground heat exchanger for the extraction or mining of the heat is a horizontal lens shaped body with a more or less uniform temperature. Many studies have shown that the rocks in much of the Cooper Basin (South Australia) and in the Hunter Valley (New South Wales) are subject to high horizontal stresses. This bodes well for the development of horizontal underground heat exchangers and large multi-reservoir developments. This is in contrast to underground heat exchangers previously developed in, for example, France and Japan.

The construction of a HFR geothermal power plant leaves an environmental footprint that is limited to drill holes and pipelines, and a building to house the power plant.

Before this potential can be unlocked, the economic viability has to be proven through the construction of a demonstration and commercial plant.

Note: One cubic kilometre of hot granite at 250 degrees centigrade has the stored energy equivalent of 40 million barrels of oil.

1 Geodynamics Limited, HFR In Australia, retrieved 2007,http://www.geodynamics.com.au/IRM/content/hfr_hfraustralia.html

CASE STUDY 3: HOT FRACTURED ROCKS GEOTHERMAL

23.

WAY FORWARDClimate change is an unprecedented global issue requiring signifi cant resources to meet the complex environmental, energy, economic and political challenges. Fundamental changes in the global energy system are required to achieve the deployment of affordable low emission technologies in order to stabilise concentrations of GHG in the atmosphere. Incremental improvements in technology will not by themselves lead to stabilisation; more is required, that is step-changes in cost, scale and emissions performance.

Transforming the way Australia produces and uses energy must be a cornerstone of a national response aimed at signifi cantly reducing GHG emissions. The introduction of a national emissions trading scheme will be critical for investors in breakthrough technologies; however if we are to accelerate the commercialisation of low emission technologies, Australia must also explore complementary policies.

The Australian Business & Climate Group believes that a National Low Emission Technology Strategy is an essential element of a National Climate Change Response. The challenge is complex and the response must be comprehensive.