Embed Size (px)

Citation preview

Stepping It Up: Achieve a Top-Notch Financial Operation

CHARACTERISTICS OF TOP FINANCE LEADERSHIP

Session Objective

Sharing Perceptions and Perspectives on Finance

Leadership

Polling Questions - How to Participate

Using your mobile device:

➢ Start a new text message. Enter 22333 in the ‘to’ line

➢ Type TTVOTE in the body of the message, and then hit Send.

➢ You’ll get a response saying you’ve joined the session which means you’re ready to enter your response

TTVOTE

22333

How Is Finance Perceived Management & The Board?

https://www.youtube.com/watch?v=XD_lR47Zbtk

https://www.youtube.com/watch?v=ingAVhzkcco

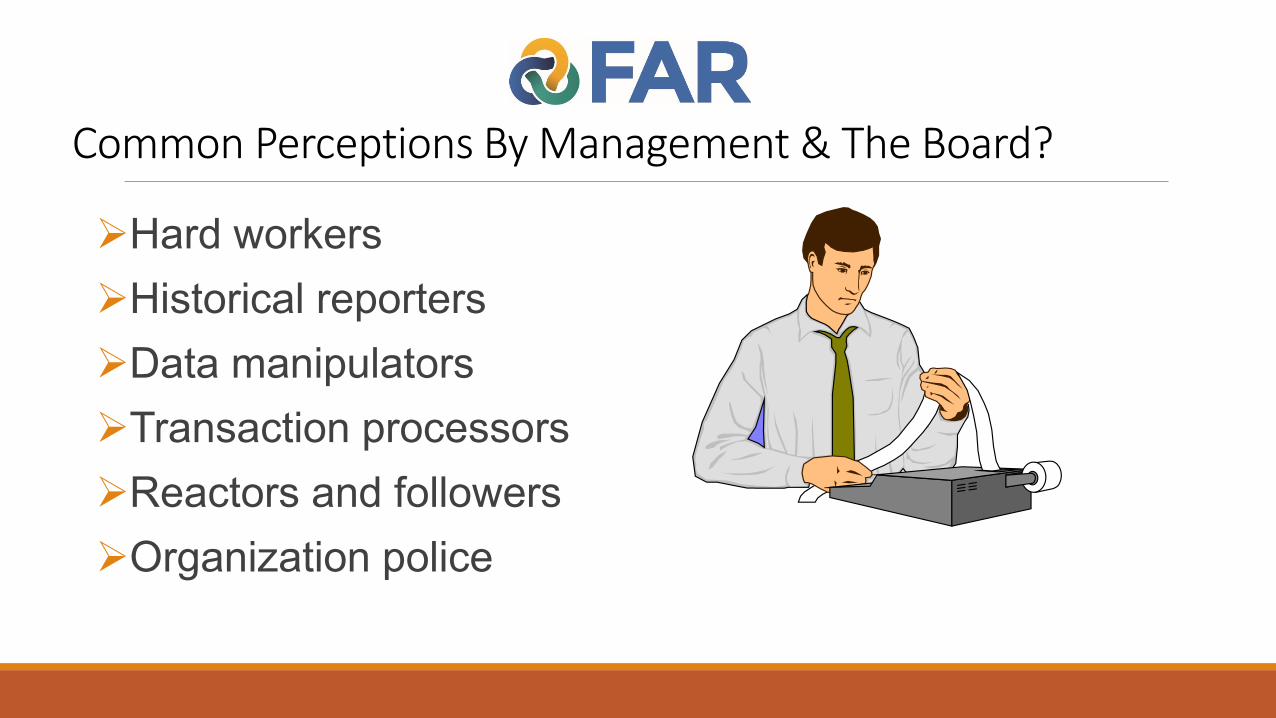

Common Perceptions By Management & The Board?

➢Hard workers

➢Historical reporters

➢Data manipulators

➢Transaction processors

➢Reactors and followers

➢Organization police

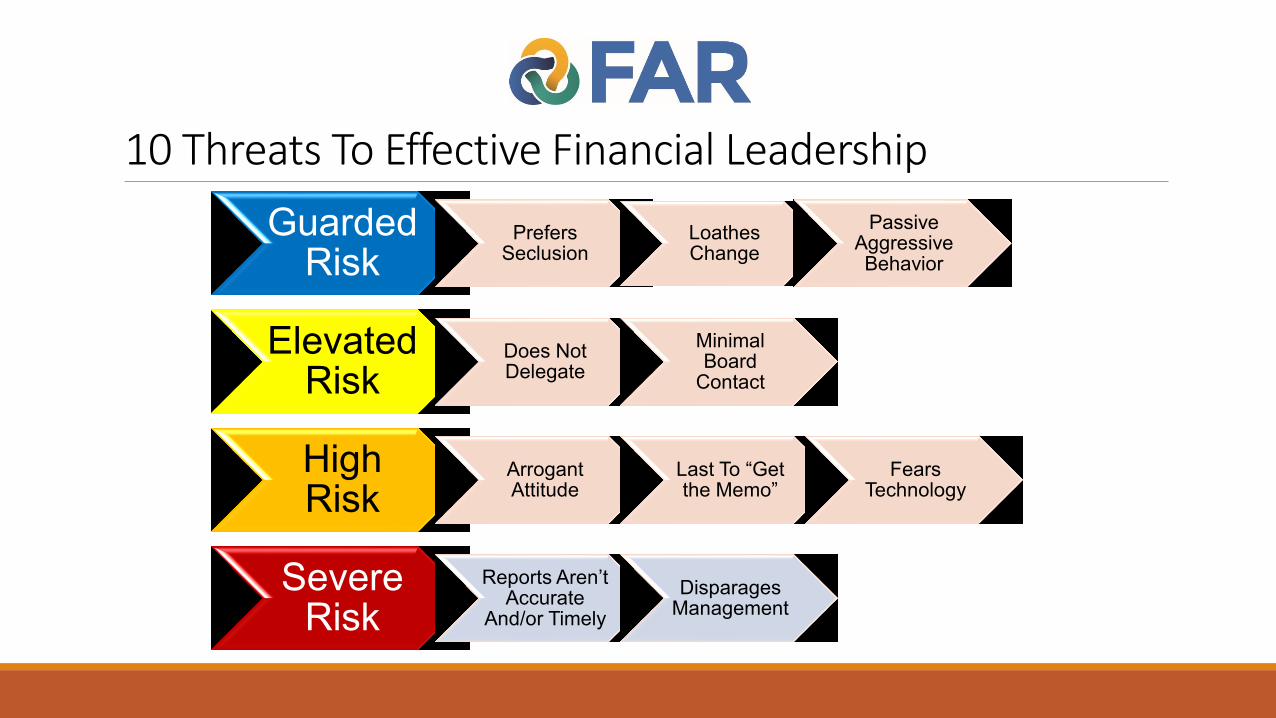

10 Threats To Effective Financial Leadership

Guarded Risk

Prefers Seclusion

Loathes Change

Passive Aggressive Behavior

Elevated Risk

Does Not Delegate

Minimal Board

Contact

High Risk

Arrogant Attitude

Last To “Get the Memo”

Fears Technology

Severe Risk

Reports Aren’t Accurate

And/or Timely

Disparages Management

Characteristics of a Top Finance Team

These are desirable skills but in reality, one or more of these characteristics are typically lacking in many nonprofit finance operations.

Integrity

High ethical standard and trustworthy

Competence

Technical skills in finance &

accounting

Foresight

Anticipate events and their

probable impact

Strategy

Develop plans for accomplishing

objectives

Implementation

Execute operational and financial plans

Communication

Synthesize in non-technical

terms

What Management and Boards Want to Know?

Is Finance Functioning Effectively?

What Finance Needs to Ask? The Self Evaluation

Can my finance function moreeffectively?

Or

Finance is perfect – we get a clean audit every year

The Self Evaluation

1) Is my Finance Department providing timely, meaningful, and cost-effective services?

2) Can my Finance Department increase its effectiveness, efficiency, and support of the organization’s objectives?

3) Do I want to focus more on high-value decision-support services and provide information critical to the decision-making process?

1. Assess Staff Duties & Competencies

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring

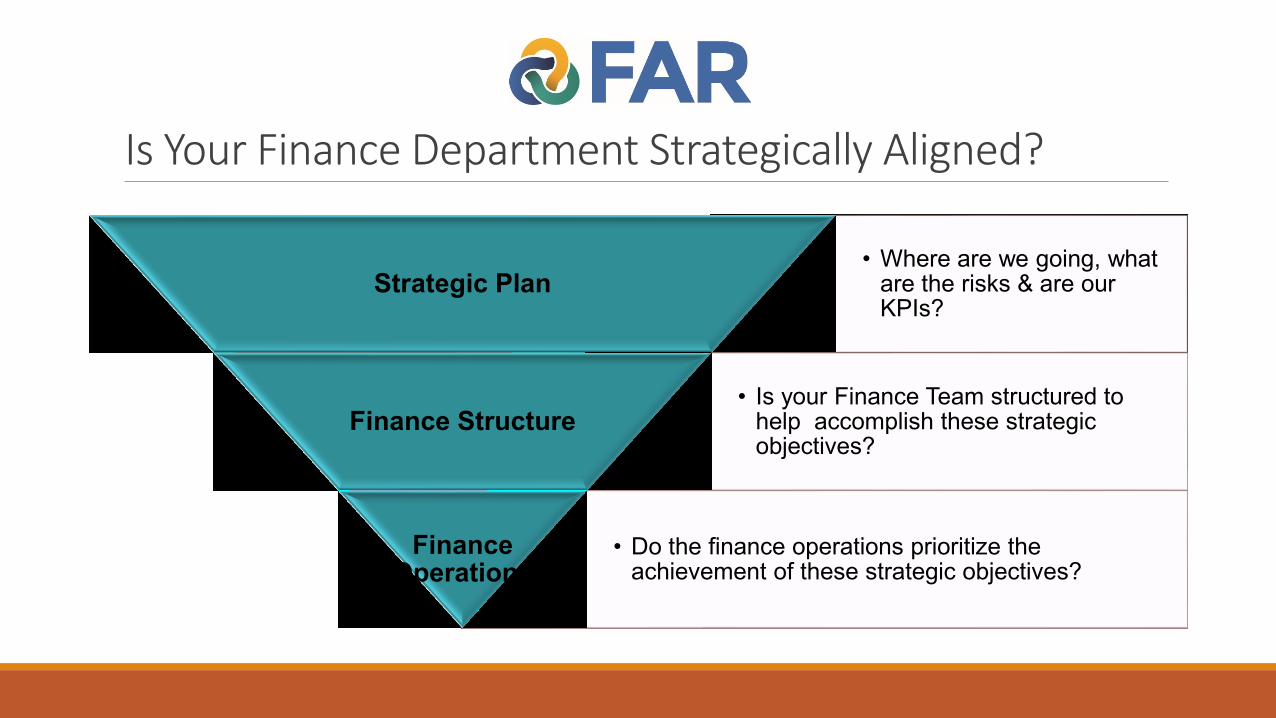

Is Your Finance Department Strategically Aligned?

• Where are we going, what are the risks & are our KPIs?

Strategic Plan

• Is your Finance Team structured to help accomplish these strategic objectives?

Finance Structure

• Do the finance operations prioritize the achievement of these strategic objectives?

Finance Operations

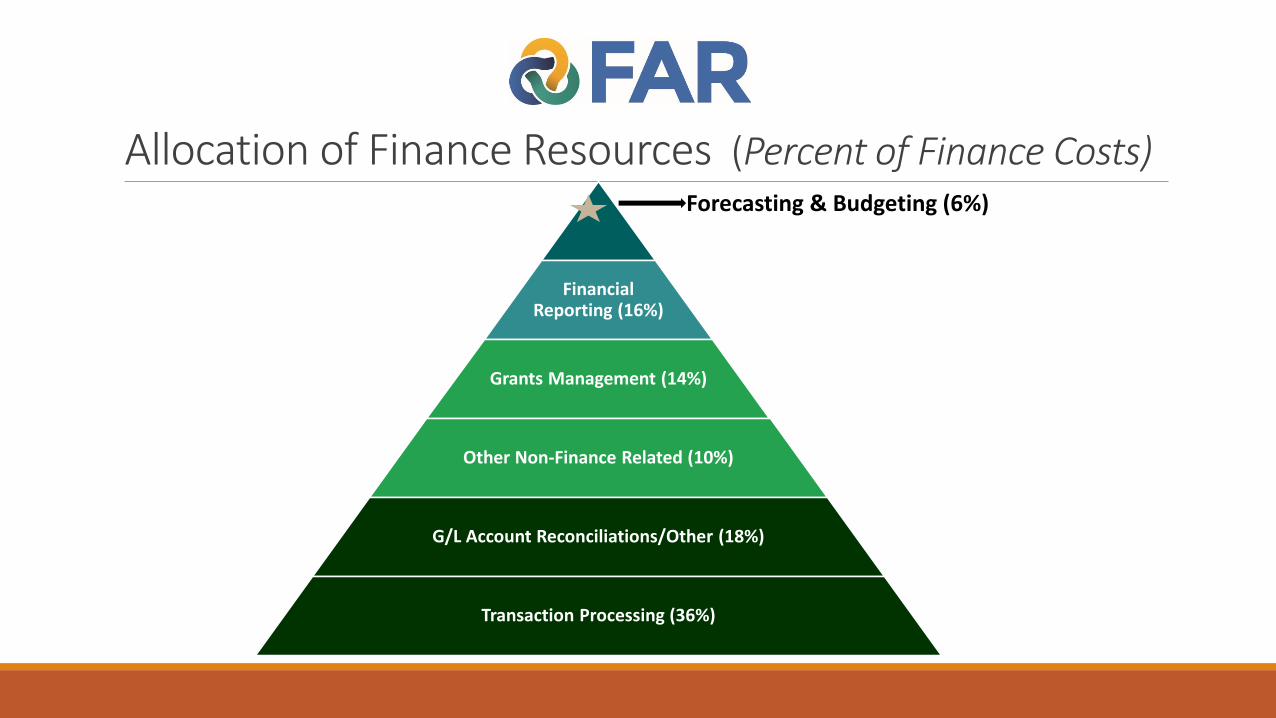

Allocation of Finance Resources (Percent of Finance Costs)

Financial Reporting (16%)

Grants Management (14%)

Other Non-Finance Related (10%)

G/L Account Reconciliations/Other (18%)

Transaction Processing (36%)

Forecasting & Budgeting (6%)

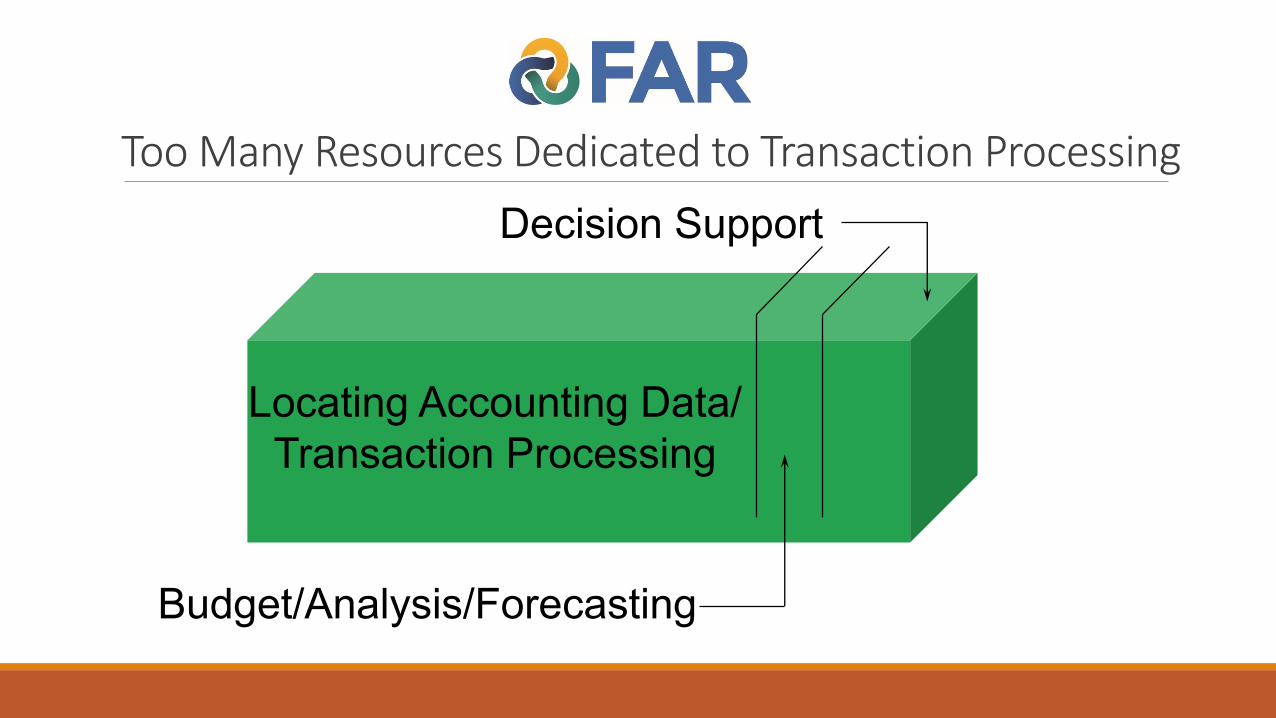

Too Many Resources Dedicated to Transaction Processing

Locating Accounting Data/

Transaction Processing

Decision Support

Budget/Analysis/Forecasting

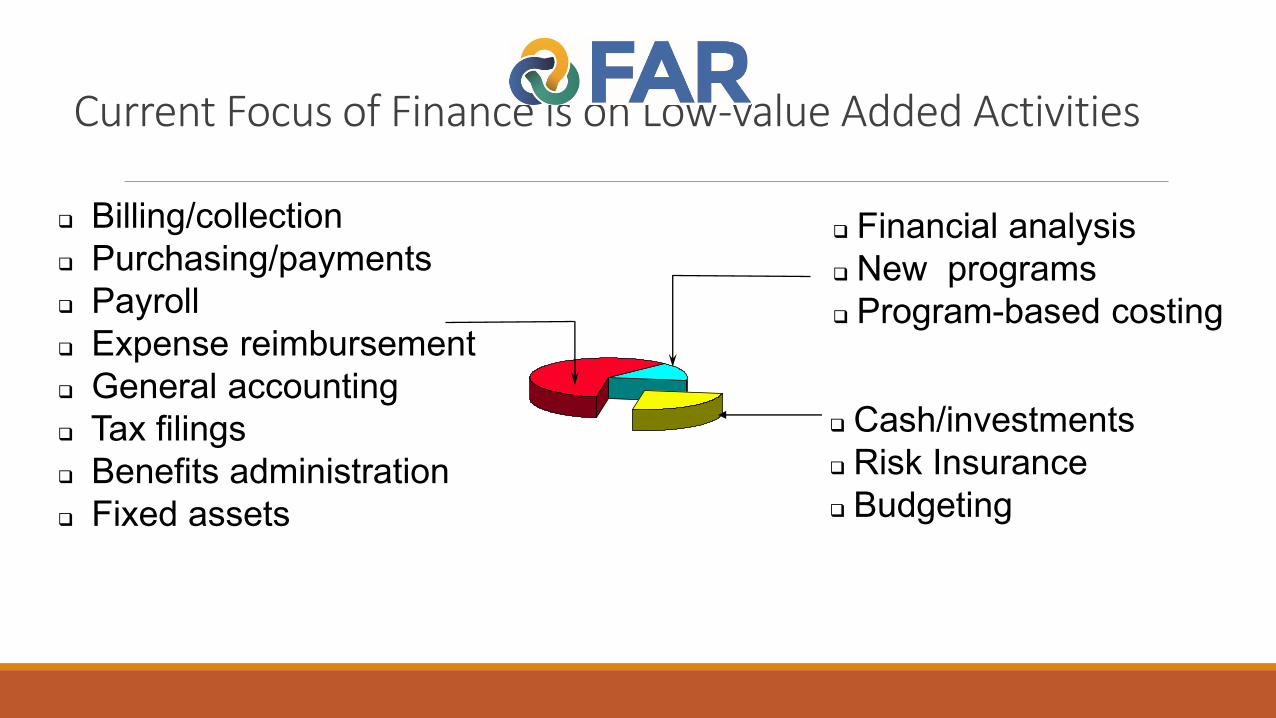

Current Focus of Finance is on Low-value Added Activities

TRANSACTION

PROCESSING

DECISION

SUPPORT

CONTROL

MANAGEMENT

❑ Billing/collection

❑ Purchasing/payments

❑ Payroll

❑ Expense reimbursement

❑ General accounting

❑ Tax filings

❑ Benefits administration

❑ Fixed assets

❑ Financial analysis

❑ New programs

❑ Program-based costing

❑ Cash/investments

❑ Risk Insurance

❑ Budgeting

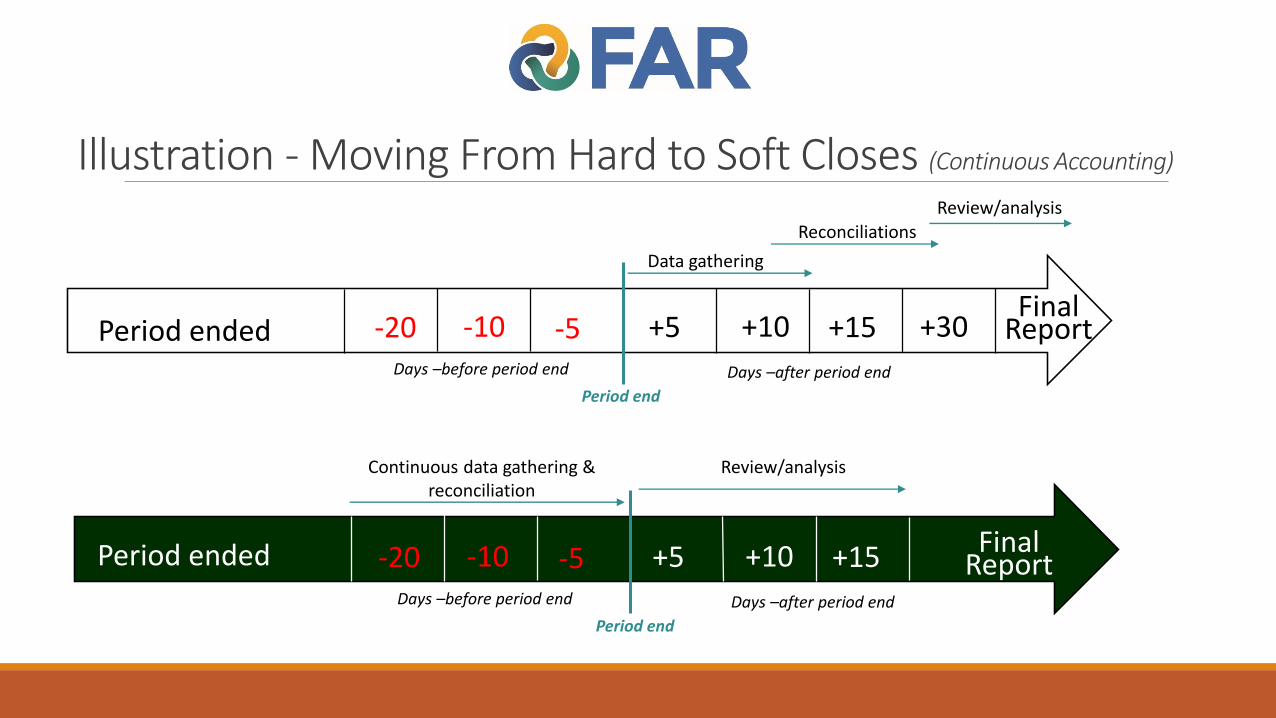

Illustration - Moving From Hard to Soft Closes (Continuous Accounting)

Period ended -20 -10 -5 +5 +10 +15 +30Final

Report

Data gathering

ReconciliationsReview/analysis

Days –before period end Days –after period end

Period end

Period ended -20 -10 -5 +5 +10 +15 Final Report

Continuous data gathering & reconciliation

Review/analysis

Days –before period end Days –after period end

Period end

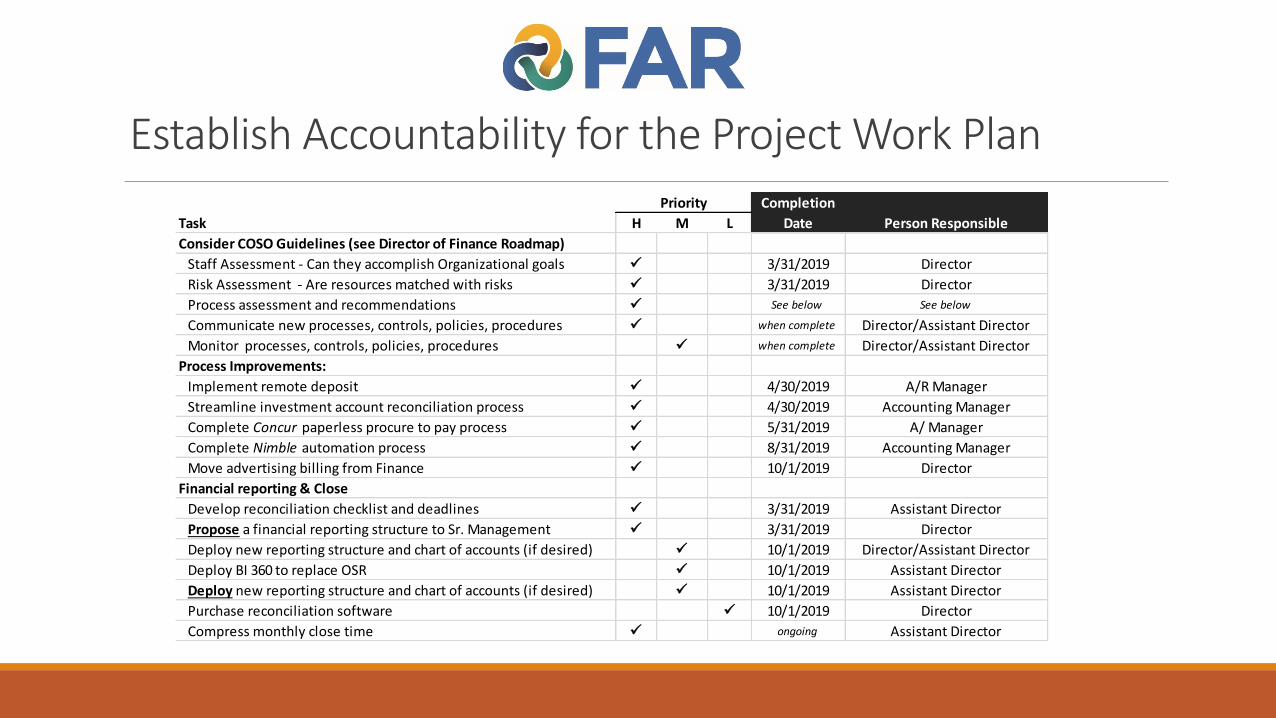

Establish Accountability for the Project Work Plan

Task H M L

Consider COSO Guidelines (see Director of Finance Roadmap)

Staff Assessment - Can they accomplish Organizational goals ✓ 3/31/2019 Director

Risk Assessment - Are resources matched with risks ✓ 3/31/2019 Director

Process assessment and recommendations ✓ See below See below

Communicate new processes, controls, policies, procedures ✓ when complete Director/Assistant Director

Monitor processes, controls, policies, procedures ✓ when complete Director/Assistant Director

Process Improvements:

Implement remote deposit ✓ 4/30/2019 A/R Manager

Streamline investment account reconciliation process ✓ 4/30/2019 Accounting Manager

Complete Concur paperless procure to pay process ✓ 5/31/2019 A/ Manager

Complete Nimble automation process ✓ 8/31/2019 Accounting Manager

Move advertising billing from Finance ✓ 10/1/2019 Director

Financial reporting & Close

Develop reconciliation checklist and deadlines ✓ 3/31/2019 Assistant Director

Propose a financial reporting structure to Sr. Management ✓ 3/31/2019 Director

Deploy new reporting structure and chart of accounts (if desired) ✓ 10/1/2019 Director/Assistant Director

Deploy BI 360 to replace OSR ✓ 10/1/2019 Assistant Director

Deploy new reporting structure and chart of accounts (if desired) ✓ 10/1/2019 Assistant Director

Purchase reconciliation software ✓ 10/1/2019 Director

Compress monthly close time ✓ ongoing Assistant Director

Priority Completion

Date Person Responsible

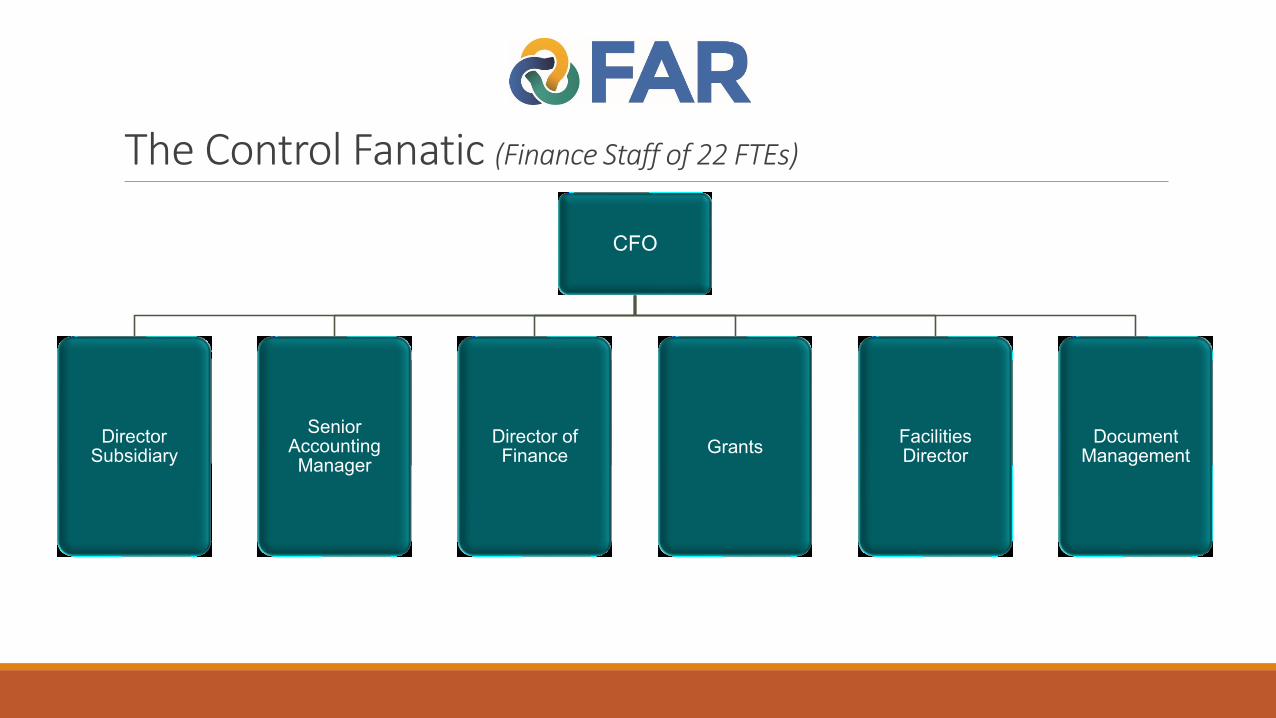

The Control Fanatic (Finance Staff of 22 FTEs)

CFO

Director Subsidiary

Senior Accounting Manager

Director of Finance

GrantsFacilities Director

Document Management

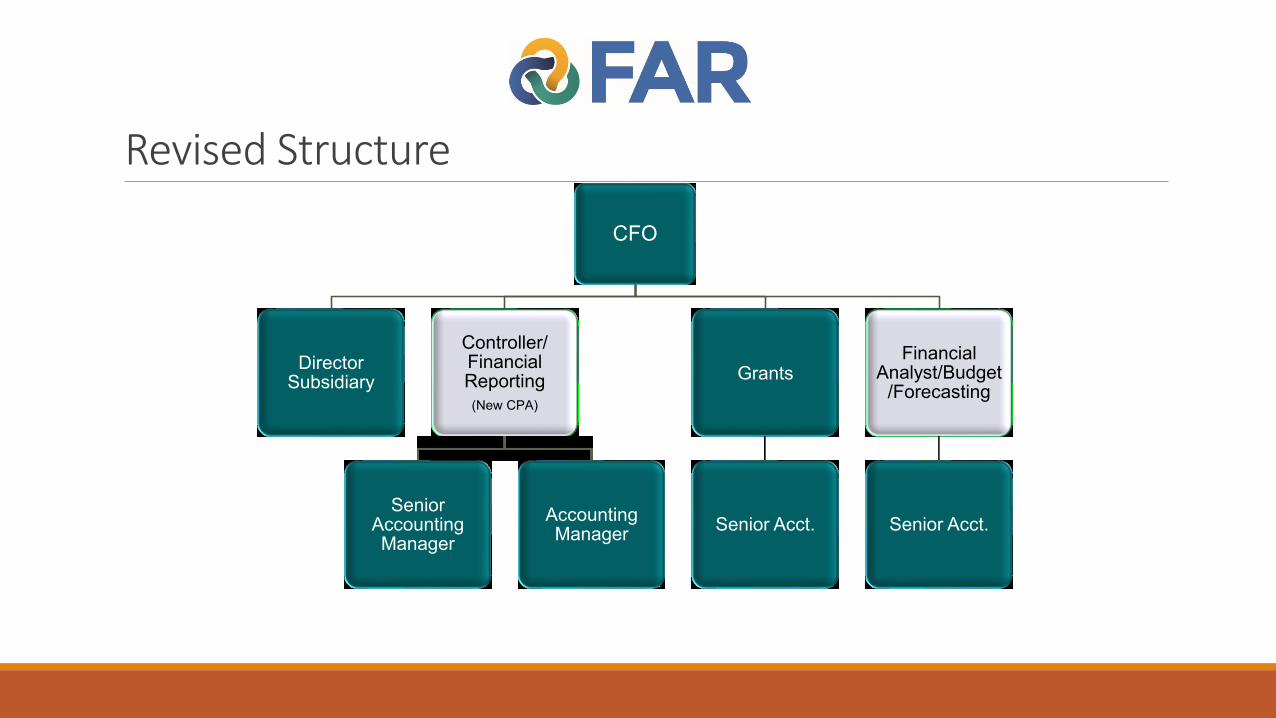

Revised Structure

CFO

Director Subsidiary

Controller/Financial Reporting

(New CPA)

Senior Accounting Manager

Accounting Manager

Grants

Senior Acct.

Financial Analyst/Budget

/Forecasting

Senior Acct.

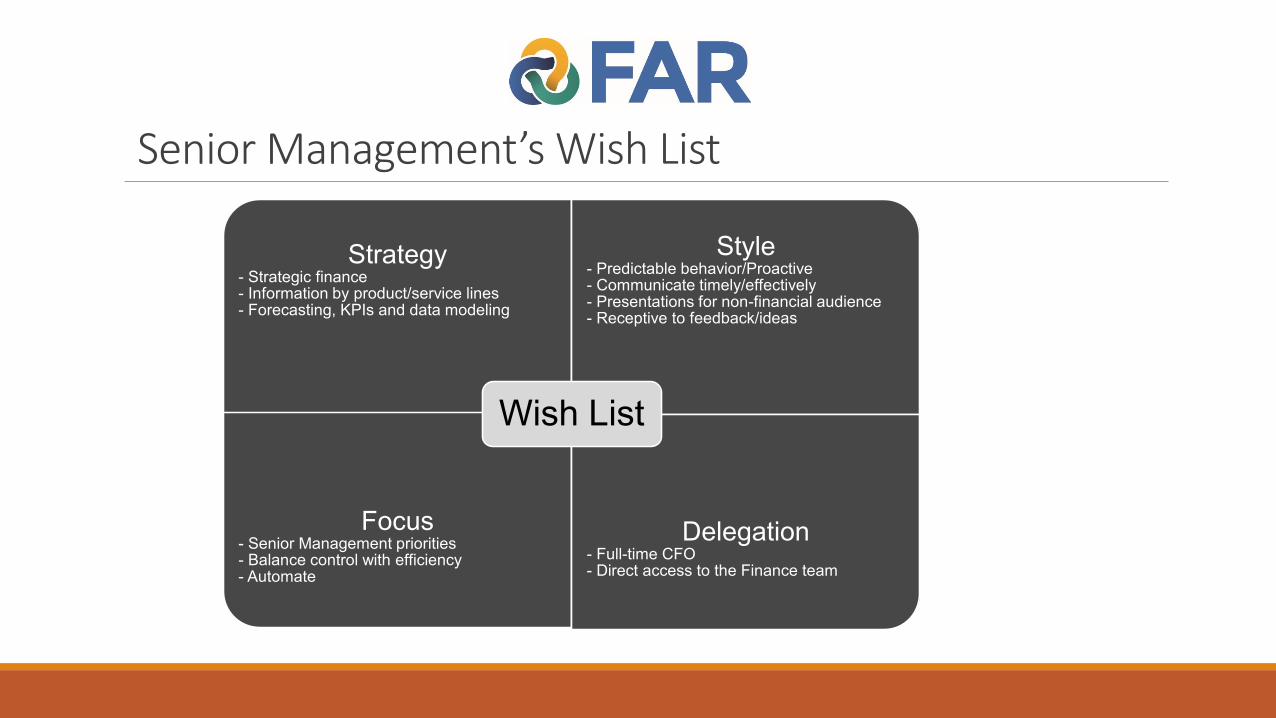

Senior Management’s Wish List

Strategy- Strategic finance- Information by product/service lines- Forecasting, KPIs and data modeling

Style- Predictable behavior/Proactive- Communicate timely/effectively- Presentations for non-financial audience- Receptive to feedback/ideas

Focus- Senior Management priorities- Balance control with efficiency- Automate

Delegation- Full-time CFO- Direct access to the Finance team

Wish List

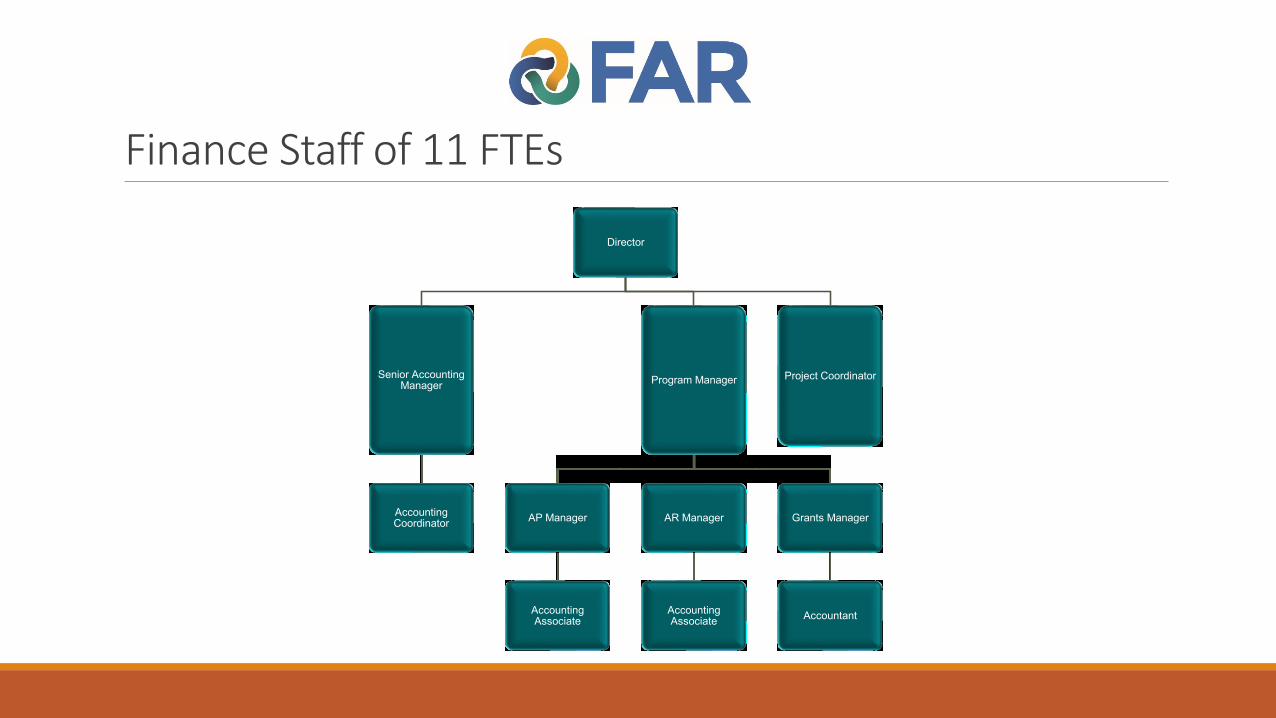

Finance Staff of 11 FTEs

Director

Senior Accounting Manager

Accounting Coordinator

Program Manager

AP Manager

Accounting Associate

AR Manager

Accounting Associate

Grants Manager

Accountant

Project Coordinator

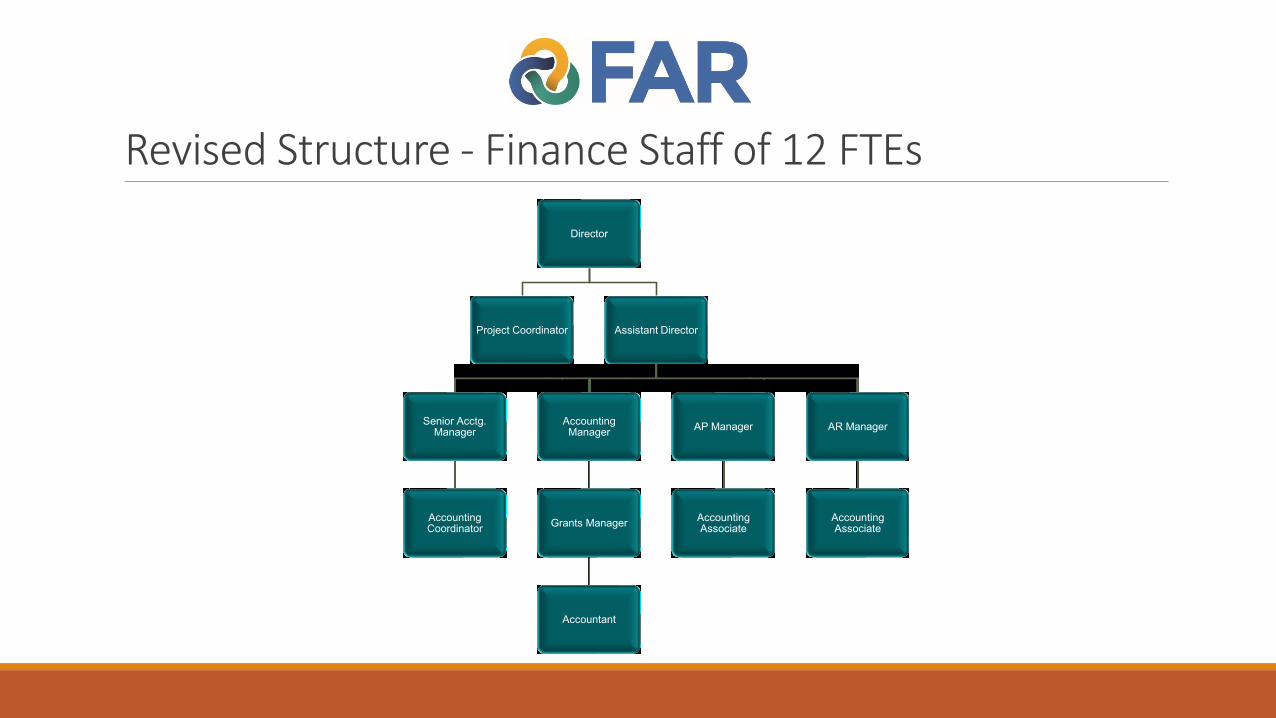

Revised Structure - Finance Staff of 12 FTEs

Director

Project Coordinator Assistant Director

Senior Acctg. Manager

Accounting Coordinator

Accounting Manager

Grants Manager

Accountant

AP Manager

Accounting Associate

AR Manager

Accounting Associate

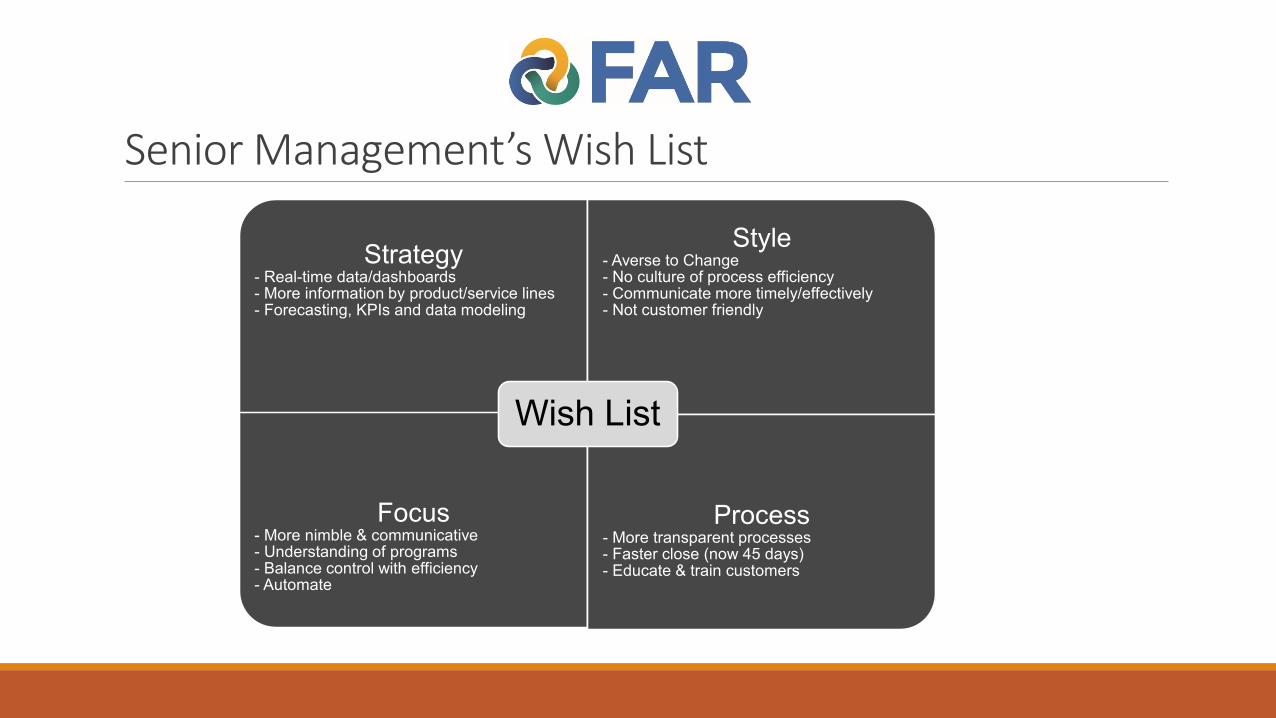

Senior Management’s Wish List

Strategy- Real-time data/dashboards- More information by product/service lines- Forecasting, KPIs and data modeling

Style- Averse to Change- No culture of process efficiency- Communicate more timely/effectively- Not customer friendly

Focus- More nimble & communicative- Understanding of programs- Balance control with efficiency- Automate

Process- More transparent processes - Faster close (now 45 days)- Educate & train customers

Wish List

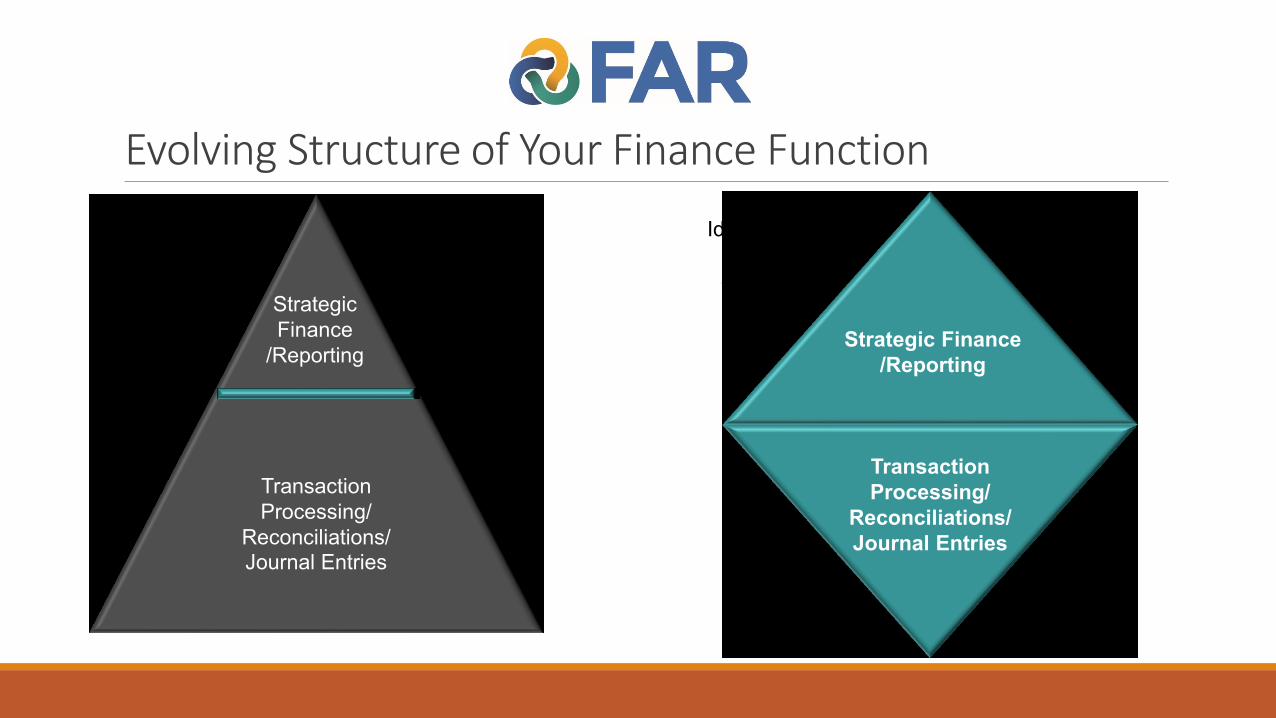

Evolving Structure of Your Finance Function

Transaction

Processing/

Reconciliations/

Journal Entries

Traditional

Finance

Structure

Strategic

Finance

/ReportingStrategic Finance

/Reporting

Transaction

Processing/

Reconciliations/

Journal Entries

Ideal/Future

Finance

Structure

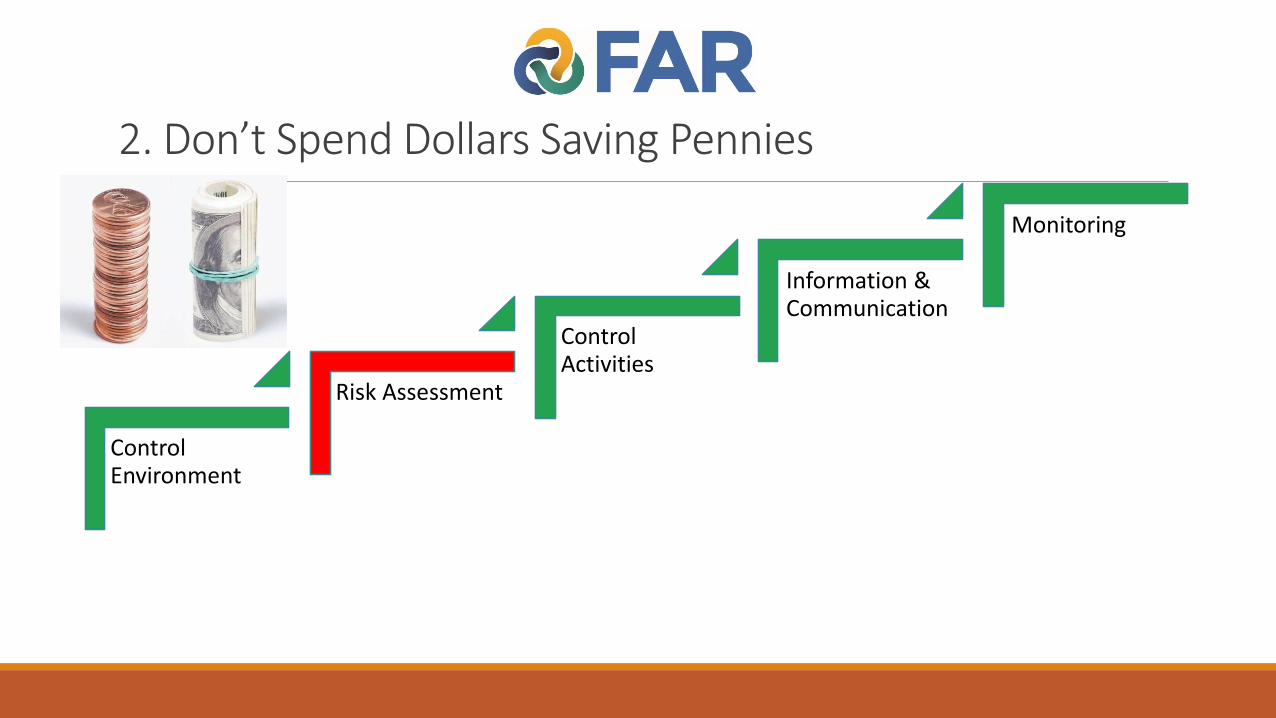

2. Don’t Spend Dollars Saving Pennies

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring

Balance Sheet AccountAmount (in millions) %

F/S Impac

tAccou

ntProce

ssFraud Risk

Entity-Wide Factor

s

Overall Risk Rating

Cash & cash equivalents $8.0 8% M M L H L L

Receivables 12.0 12% M H H M M M

Investments 58.0 58% H M L L L L

Property & equipment 20.0 20% M L L L L L

Prepaids & Other 2.0 2% L L L L L L

Total assets 100.0 100%

Accounts payable 15.0 15% M H H H H H

Deferred revenue 25.0 25% H H H L H H

Mortgage payable 15.0 15% M M L L L M

Total Liabilities 55.0 44%

Restricted net assets 25.0 25% H H M L M L

Unrestricted net assets 20.0 20% H L L M L M

Total Liabilities & Net Assets $100.0 100%

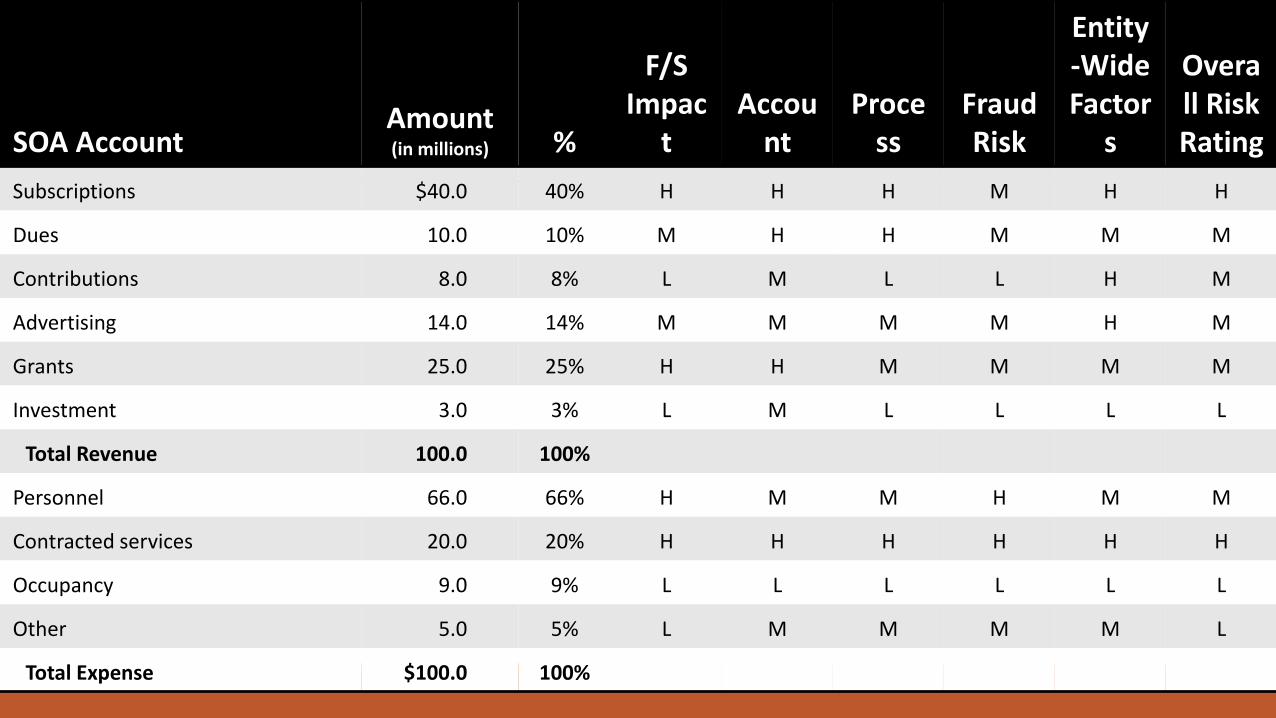

SOA AccountAmount (in millions) %

F/S Impac

tAccou

ntProce

ssFraud Risk

Entity-Wide Factor

s

Overall Risk Rating

Subscriptions $40.0 40% H H H M H H

Dues 10.0 10% M H H M M M

Contributions 8.0 8% L M L L H M

Advertising 14.0 14% M M M M H M

Grants 25.0 25% H H M M M M

Investment 3.0 3% L M L L L L

Total Revenue 100.0 100%

Personnel 66.0 66% H M M H M M

Contracted services 20.0 20% H H H H H H

Occupancy 9.0 9% L L L L L L

Other 5.0 5% L M M M M L

Total Expense $100.0 100%

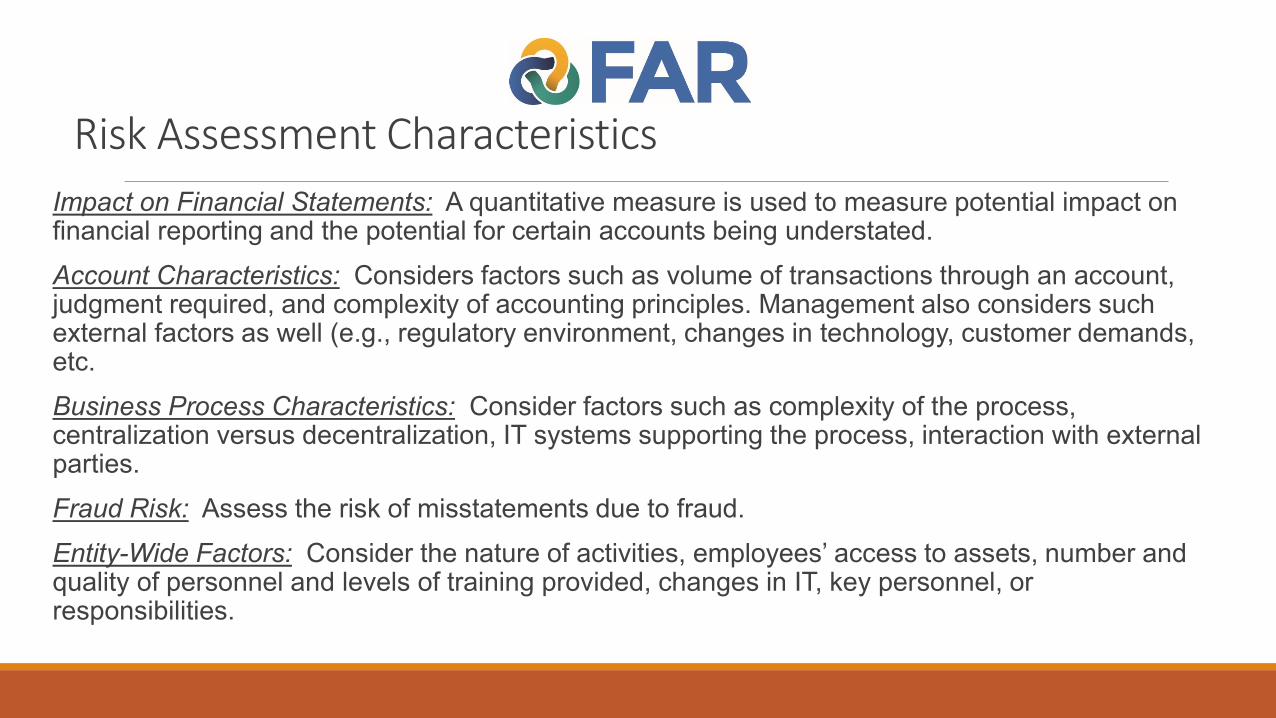

Risk Assessment Characteristics

Impact on Financial Statements: A quantitative measure is used to measure potential impact on financial reporting and the potential for certain accounts being understated.

Account Characteristics: Considers factors such as volume of transactions through an account, judgment required, and complexity of accounting principles. Management also considers such external factors as well (e.g., regulatory environment, changes in technology, customer demands, etc.

Business Process Characteristics: Consider factors such as complexity of the process, centralization versus decentralization, IT systems supporting the process, interaction with external parties.

Fraud Risk: Assess the risk of misstatements due to fraud.

Entity-Wide Factors: Consider the nature of activities, employees’ access to assets, number and quality of personnel and levels of training provided, changes in IT, key personnel, or responsibilities.

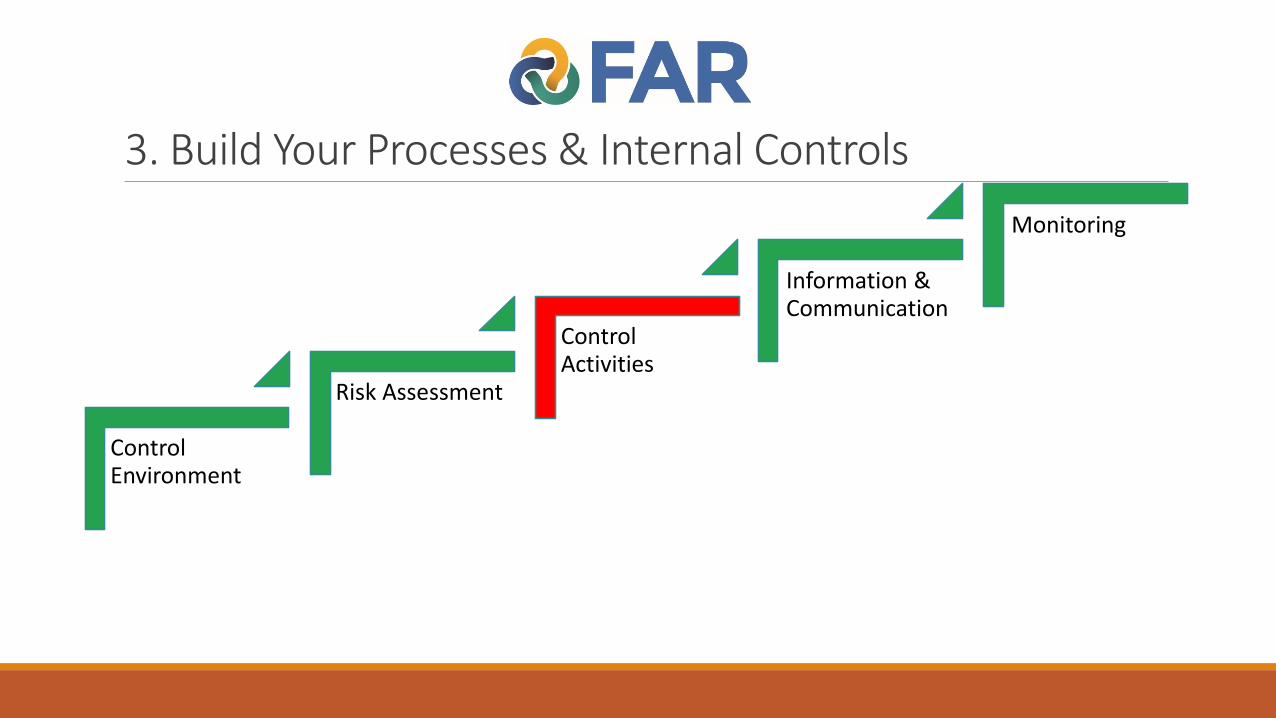

3. Build Your Processes & Internal Controls

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring

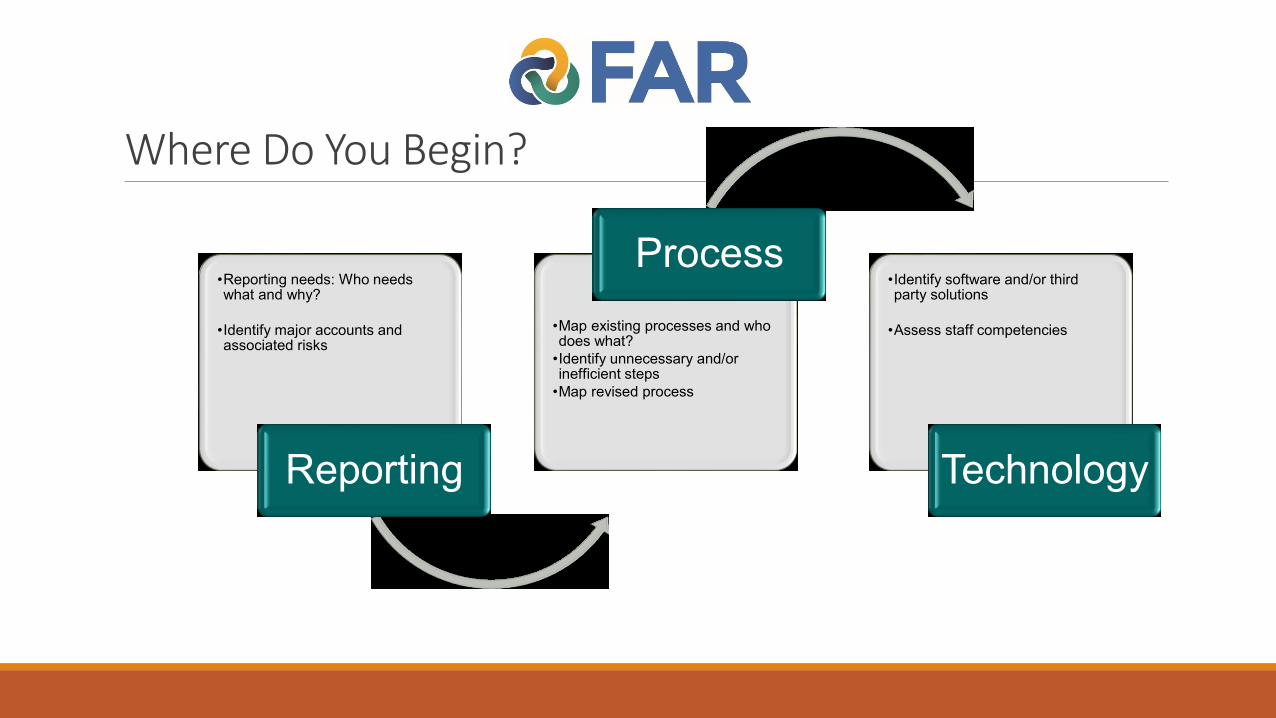

•Reporting needs: Who needs what and why?

•Identify major accounts and associated risks

Reporting

•Map existing processes and who does what?

•Identify unnecessary and/or inefficient steps

•Map revised process

Process•Identify software and/or third party solutions

•Assess staff competencies

Technology

Where Do You Begin?

Major Processes for Every Nonprofit

1) Record to Report

2) Order to Cash

3) Procure to Pay

4) Hire to Pay

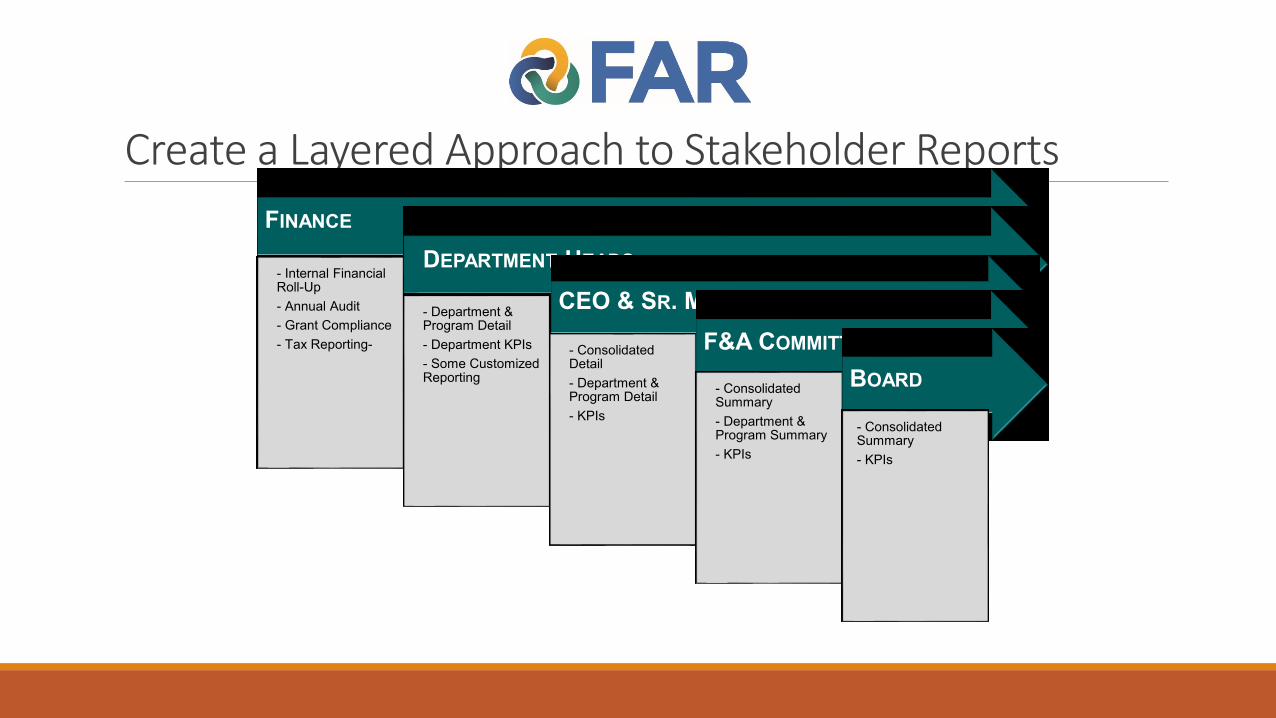

Create a Layered Approach to Stakeholder Reports

FINANCE

- Internal Financial Roll-Up

- Annual Audit

- Grant Compliance

- Tax Reporting-

DEPARTMENT HEADS

- Department & Program Detail

- Department KPIs

- Some Customized Reporting

CEO & SR. MANAGEMENT

- Consolidated Detail

- Department & Program Detail

- KPIs

F&A COMMITTEE

- Consolidated Summary

- Department & Program Summary

- KPIs

BOARD

- Consolidated Summary

- KPIs

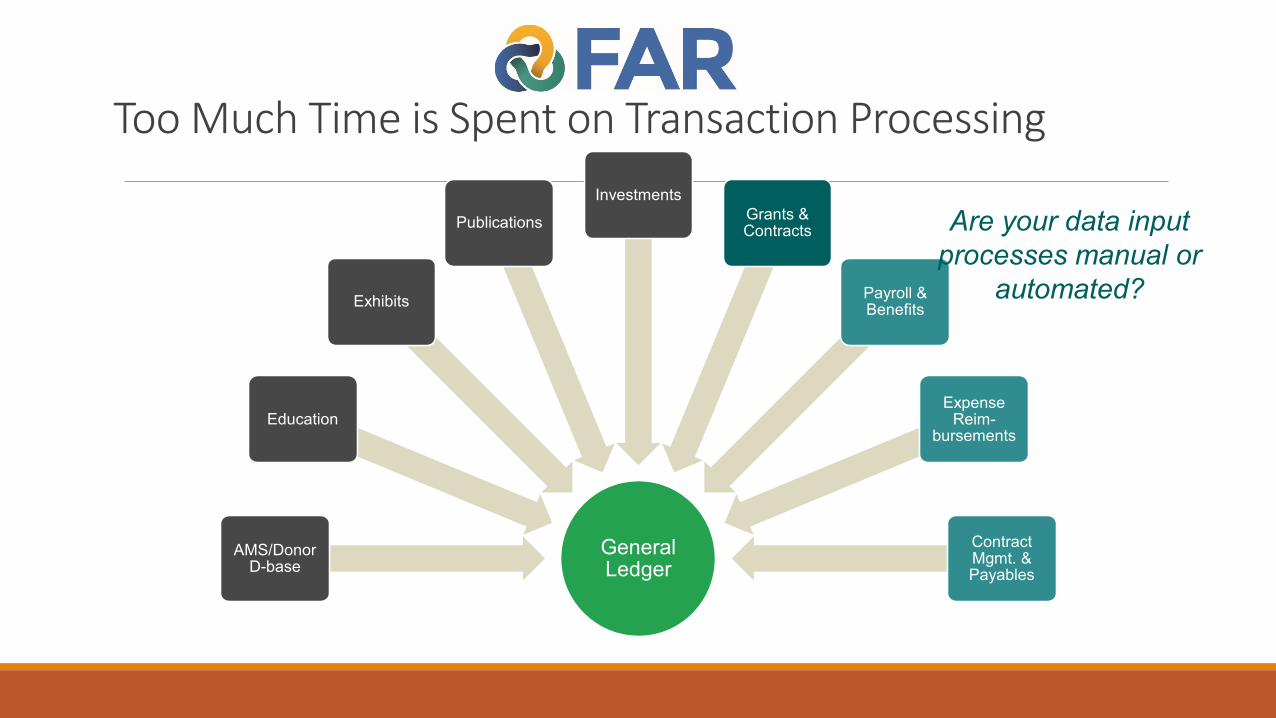

General Ledger

AMS/Donor D-base

Education

Exhibits

Publications

Investments

Grants & Contracts

Payroll & Benefits

Expense Reim-

bursements

Contract Mgmt. & Payables

Too Much Time is Spent on Transaction Processing

Are your data input

processes manual or

automated?

Do You Have Multiple Data Repositories?

GL(Lawson)

Licensing (30%)

Salesforce/ Advantage

M-ship (8.5%)

Advantage

Subscriptions (4.6%)

Advantage

Other (3%)

Raiser’s Edge

Reprints (4.3%)

Outsourced/JEAnnual

Meeting (1%)

Experient

Other (1.5%)

Salesforce/ Financial Force

Investment & Lease (5.8%)

Manual JEs

Grants (28%)

PTS/Grants D-Bases/Fed. Sys.

Advertising (14.3%)

Salesforce/WebOE/Financi

al Force

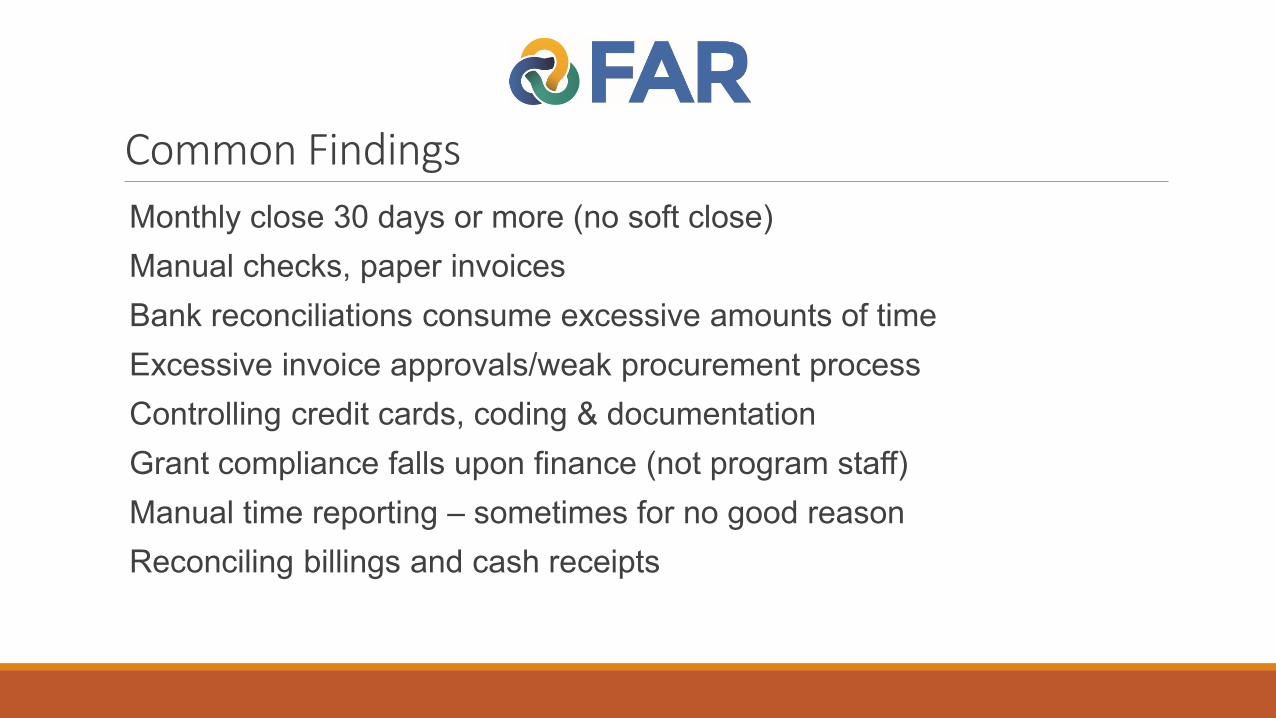

Common Findings

Monthly close 30 days or more (no soft close)

Manual checks, paper invoices

Bank reconciliations consume excessive amounts of time

Excessive invoice approvals/weak procurement process

Controlling credit cards, coding & documentation

Grant compliance falls upon finance (not program staff)

Manual time reporting – sometimes for no good reason

Reconciling billings and cash receipts

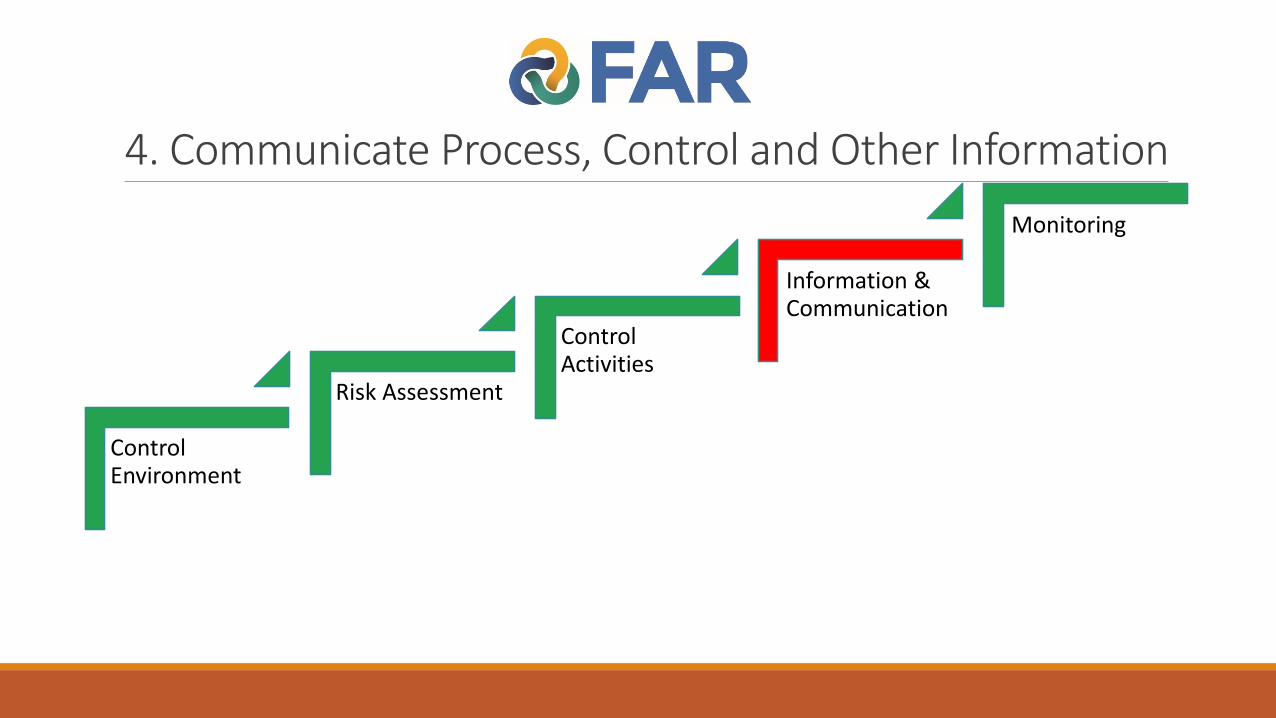

4. Communicate Process, Control and Other Information

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring

What Kind of Information and How Is It Communicated?

Concept: Information must be disseminated for people to comply

Examples:

◦ Basic meetings (Internal and Board/Committee)

◦ Employee portal – where controls/policies are described (for employees and the board)

◦ Diagrams

◦ Nonfinancial information

◦ Whistleblower program (internal and external parties)

◦ Ethics Hotline

◦ Communications with outsourced service providers and/or customers

5. Monitor Your Processes & Controls

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring

What is Monitored?

Examples:

Are controls functioning as designed/documented?

Any changes in personnel/technology/business that affect the controls?

KPIs

Budget to actual

Reserves

Financial Governance

1. Establish clear lines of communication with the committee chair

2. Challenge the need for separate audit and finance committees

3. Consider a financial orientation for the Board

4. Risk management

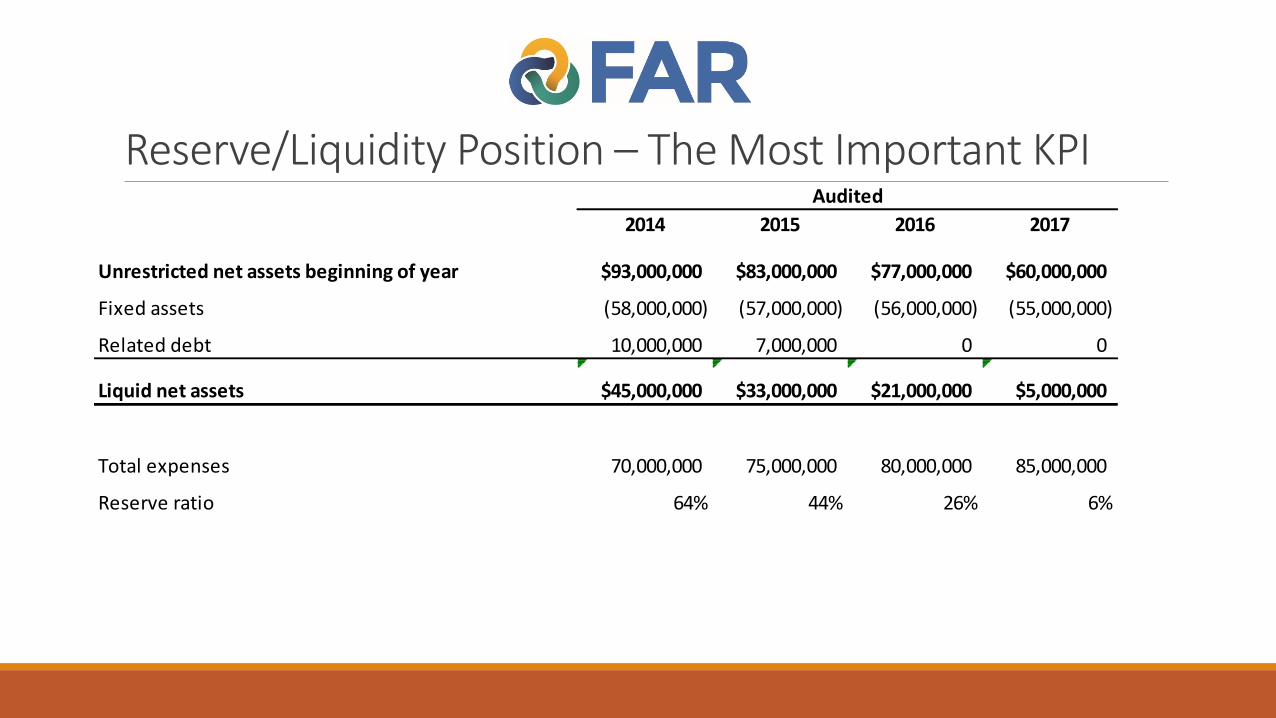

Reserve/Liquidity Position – The Most Important KPI

2014 2015 2016 2017

Unrestricted net assets beginning of year $93,000,000 $83,000,000 $77,000,000 $60,000,000

Fixed assets (58,000,000) (57,000,000) (56,000,000) (55,000,000)

Related debt 10,000,000 7,000,000 0 0

Liquid net assets $45,000,000 $33,000,000 $21,000,000 $5,000,000

Total expenses 70,000,000 75,000,000 80,000,000 85,000,000

Reserve ratio 64% 44% 26% 6%

Audited

Questions?

C H A R L E S TAT E , C PA

M A N A G I N G PA R T N E R

2 0 2 - 4 1 9 - 5 1 0 1

C TAT E @ TAT E T R YO N .C O M

H T T P S : / / W W W. L I N K E D I N . C O M / I N / C H A R L E S TAT E /