Embed Size (px)

Citation preview

31/05/2012

1

Market developments

and trends in key steel-

using industries

DSTI/SU/SC(2012)5

72nd Steel Committee Meeting

Paris

31 May-1 June 2012

Agenda: trends in key steel-using industries

• Steel consumption by sector – in tonnage

– in value added

• Recent production trends and baseline short-term forecasts

• Long-term trends – Factors influencing steel consumption on the long-term

– Long-term (2021) forecasts by steel-using industries

• Risk related to some steel-using industries – Chinese construction sector

– Automotive sector in some developed economies

31/05/2012

2

Global steel consumption by sector in

tonnage (2007)

Construction50%

Transport16%

Machinery 14%

Metal products

14%

Domestic appliances

3%

Electrical equipment

3%

Source: World Steel Association

Global steel consumption by sector in

value added (2010)

Construction24%

Motor Vehicles

10%

Other transport

5%

Mechanical engineering

24%

Electrical & high-tech

11%

All other26%

Source: Oxford Economics

31/05/2012

3

Tonnage vs. Value added

• Measurement differences (VA uses I/O tables)

• Value added per tonne depends on the sector. – Construction sector consumes mainly structural

sections and bars which are lower value-added steel products compared to those typically consumed in other sectors.

• The approach in value uses intermediate consumption numbers, not final demand. – The wholesale sector accounts for a greater share

of the construction sector's intermediate consumption compared to that of other key sectors.

Construction

• Includes civil engineering, buildings, repair and maintenance, global value added USD 2,294 billion in 2010 (at 2005 prices & exchange rates)

• Gross output – before netting off the cost of inputs – was broadly 2¼ times that amount.

31/05/2012

4

Construction

2005-2009 2010 2011e 2012f

EU 15 -1.0 -1.7 0.4 -0.4

US -5.9 -3.2 -1.0 4.7

Japan -3.2 -2.2 -1.2 3.2

Developed countries -2.6 -1.4 0.3 2.0

Brazil 3.7 11.8 3.5 4.0

Russia 5.4 -0.2 3.6 9.2

India 9.5 8.3 4.4 8.4

China 15.5 11.3 12.6 8.3

Emerging markets 7.9 6.3 6.2 6.3

World 0.3 1.2 2.4 3.6

Construction value added, annual growth rate in %

Source: Oxford Economics

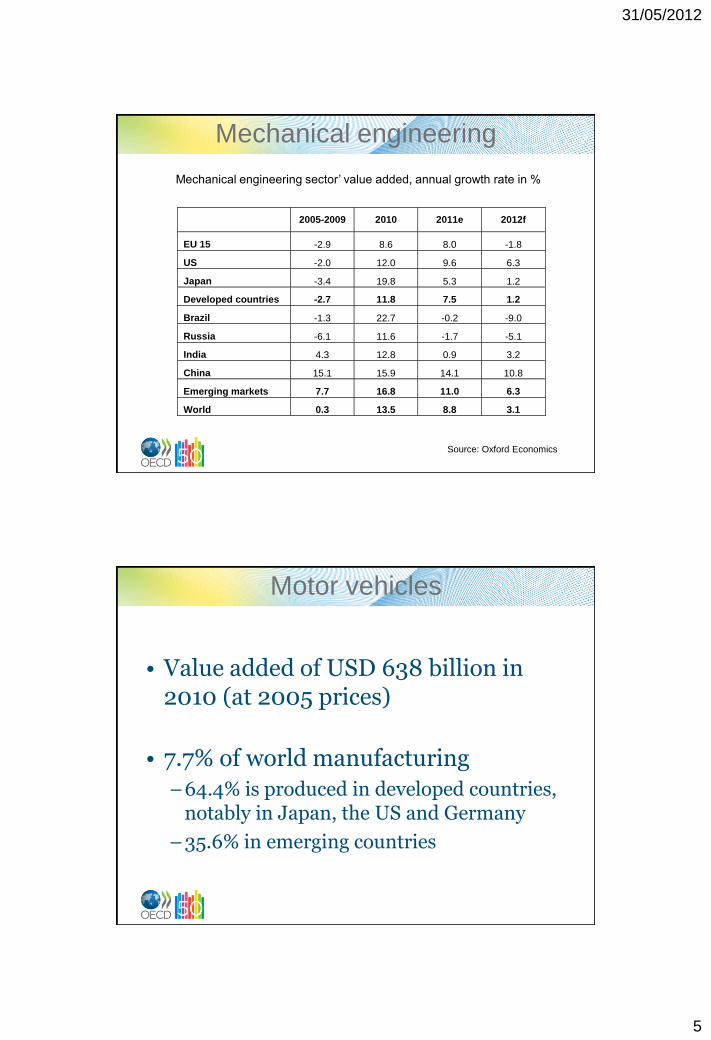

Mechanical engineering

• In 2010, global mechanical engineering value added amounted to USD 828 billion

• 10% of world manufacturing

–Special purpose machinery 5%

–General purpose machinery 4%

–Domestic appliances 1%.

31/05/2012

5

Mechanical engineering

2005-2009 2010 2011e 2012f

EU 15 -2.9 8.6 8.0 -1.8

US -2.0 12.0 9.6 6.3

Japan -3.4 19.8 5.3 1.2

Developed countries -2.7 11.8 7.5 1.2

Brazil -1.3 22.7 -0.2 -9.0

Russia -6.1 11.6 -1.7 -5.1

India 4.3 12.8 0.9 3.2

China 15.1 15.9 14.1 10.8

Emerging markets 7.7 16.8 11.0 6.3

World 0.3 13.5 8.8 3.1

Mechanical engineering sector’ value added, annual growth rate in %

Source: Oxford Economics

Motor vehicles

• Value added of USD 638 billion in 2010 (at 2005 prices)

• 7.7% of world manufacturing

–64.4% is produced in developed countries, notably in Japan, the US and Germany

–35.6% in emerging countries

31/05/2012

6

Motor Vehicles

2005-2009 2010 2011e 2012f

EU 15 -6.1 20.9 11.8 -3.8

US -9.3 33.4 7.7 5.7

Japan -2.5 27.6 -11.9 16.9

Developed countries -5.9 26.2 1.3 5.8

Brazil 3.2 25.8 3.5 1.9

Russia -4.7 32.0 16.7 8.0

India 6.3 38.3 13.1 4.6

China 15.9 24.2 2.4 9.8

Emerging markets 6.3 22.8 9.6 4.7

World -2.4 25.0 4.3 5.4

Motor vehicles sector’s value added, annual growth rate in %

Source: Oxford Economics

Other means of transport

• Value added of USD 304 billion in 2010 (at 2005 prices)

• 3.7% of world manufacturing. – Aerospace: USD 137 billion,

– Ships, rolling stock, etc. USD 167 billion

• Share of developed countries: 56%

31/05/2012

7

World Shipbuiding completions

-

10,000

20,000

30,000

40,000

50,000

60,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Others 6,196 6,153 6,508 6,103 6,083 6,394 7,631 8,203 8,713 7,952 8,194 6,273

China 1,145 1,367 1,561 2,599 2,929 4,343 5,112 6,795 9,347 12,749 18,966 19,737

Korea 6,482 6,095 6,650 7,167 8,348 10,136 11,764 11,277 14,600 14,411 15,012 15,954

Japan 6,409 6,477 6,570 6,887 7,996 8,479 9,598 8,913 9,793 9,625 9,863 9,162

CG

T (

,00

0)

Sources: IHS-Fairplay, World shipbuilding Statistics – various editions, OECD

Long-term trends of steel using industries

• Issues that will influence the level and location of steel consumption both over the next decade and over the longer term – Costs of using substitute materials

– Climate change policy

– Demographics

– Changing consumption patterns

31/05/2012

8

Costs of using substitute materials

• Steel competes with other materials, examples: – aluminium in motor vehicles

– plastics in food & beverage packaging;

– timber in housing frames;

– concrete in reinforced concrete.

• Substitution depends notably on: – the capacity to change the production process;

– the sensitivity of demand to price.

Climate change policy (1/2)

• Big impact for motor vehicles and energy

• Motor vehicles impacted by the implementation of fuel efficiency targets

– It favours alternative, lighter materials such as aluminium or carbon

– But is also boosting technological progress in the steel industry

• Green cars’ sales in total automobile sales expected to range from 2% to 12% by 2020

31/05/2012

9

Climate change policy (2/2): Energy sector

• Energy production +1/3 from 2010 to 2035

• Global investment in the energy supply infrastructure : USD 38 trillion (in year-2010 dollars) 2011 to 2035 (2/3 outside of the OECD).

• Non-hydro renewable energies, (mostly wind and solar energies), which are more steel-intensive than other energy sources, will increase from 3% of the total in 2009 to over 15% in 2035.

Source: IEA’s Energy Outlook 2011:

Demographics

• World population is expected to reach 7.7 billion people by 2021 (vs. 6.9 bn in 2011).

• The increase in population is likely, other things being equal, to lead to higher steel consumption as more goods and services are consumed.

• However, population trends vary significantly across countries.

• The construction sector may feel the burden of a falling population more acutely than manufacturing.

31/05/2012

10

Changing consumption patterns (1/2)

• Changes in the composition of private consumption: key drivers for steel demand.

• As emerging markets grow and become more prosperous, demand for consumer goods as a whole will increase.

Changing consumption patterns (2/2)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

0 100 200 300 400 500 600 700 800 900 1000

personal vehicles per '000 driving population

GDP per capita (US$ 2005 prices)

US

UK

Germany

Italy

JapanKorea

Spain

China

TurkeyMexico

Brazil

India

Egypt

Slovakia

South Africa

Poland

Personal vehicle density and GDP - 2010

Sources: Oxford Economics, JD Power.

31/05/2012

11

Long-term forecasts by sector

• Compound annual growth rate 2011-2021 of the global value added for selected steel using industries:

–Construction +5.1%

–Motor vehicles +5.4%

–Other means of transport +5.8%

Long-term forecasts by sector

ConstructionMechanical

engineering

Motor

Vehicles

Other means

of transport

China 11.2>16.3 18.0>36.0 14.2>23.3 22.1>30.5

India 4.0>6.0 1.5>2.0 0.8>1.1 3.0>4.4

Japan 9.8>6.7 15.0>13.0 24.4>17.2 4.5>2.9

US 17.8>19.8 14.6>9.0 13.3>16.0 23.9>19.3

"EU 5" 22.8>16.6 24.4>16.0 20.7>16.4 20.4>16.8

Share of global value added Value added in 2010>2021 (in %)

31/05/2012

12

Risks: Chinese construction (1/2)

-20

-10

0

10

20

30

40

50

94

96

98

100

102

104

106

108

Real Estate Climate Index, LHS

Steel production annual growth rate, RHS, %

Sources: CEIC, World steel Association.

Risks: Chinese construction (2/2)

-20

0

20

40

60

80

100

Floor space sold (commodity building), yearly growth rate, %

31/05/2012

13

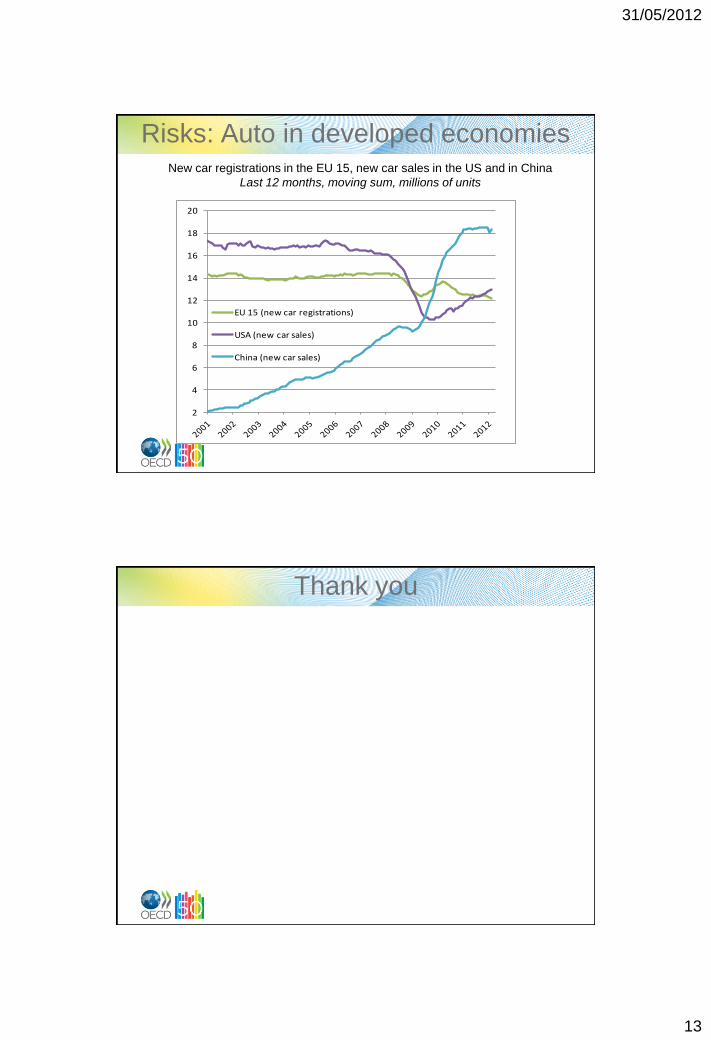

Risks: Auto in developed economies

2

4

6

8

10

12

14

16

18

20

EU 15 (new car registrations)

USA (new car sales)

China (new car sales)

New car registrations in the EU 15, new car sales in the US and in China

Last 12 months, moving sum, millions of units

Thank you