Embed Size (px)

Citation preview

CITY & COUNTY OF SAN FRANCISCO

Office of the ControllerOffice of Economic Analysis

Status of the Re-Opening of the San Francisco Economy:

August 2021

August 25, 2021

As the COVID-19 restrictions have been lifted, the Controller’s Office is tracking the pace of re-opening of the city’s economy. This is the third monthly report examining a variety of local economic indicators.

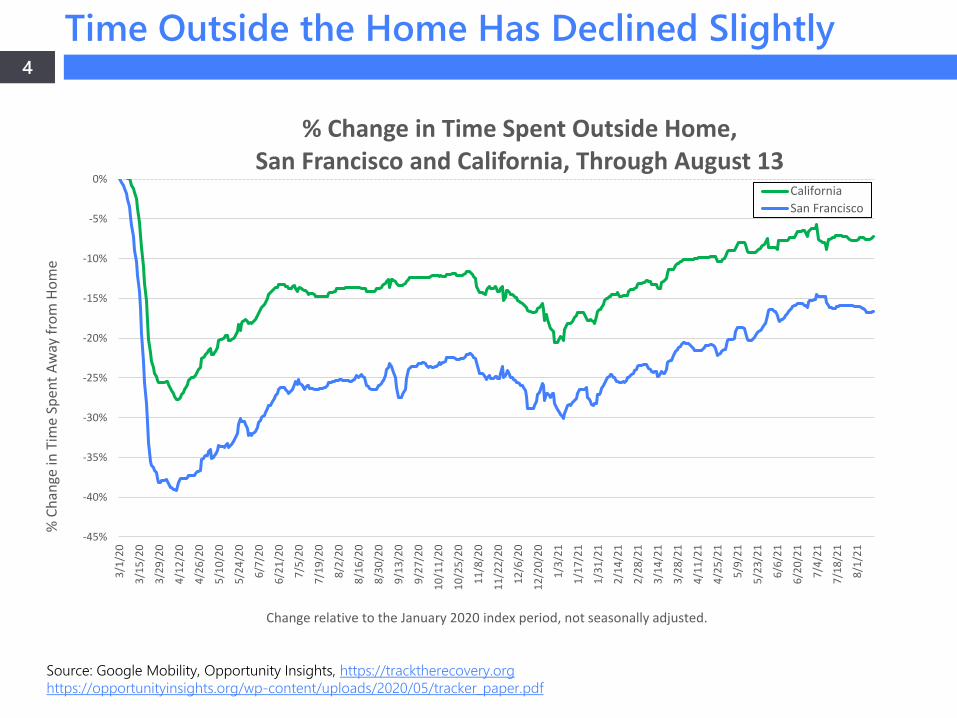

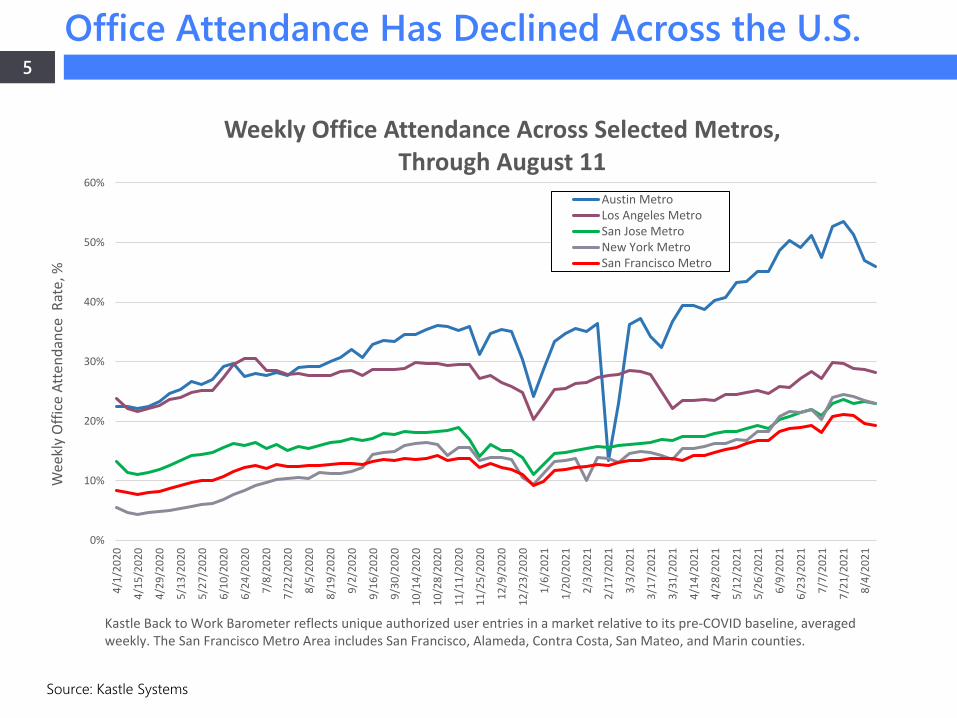

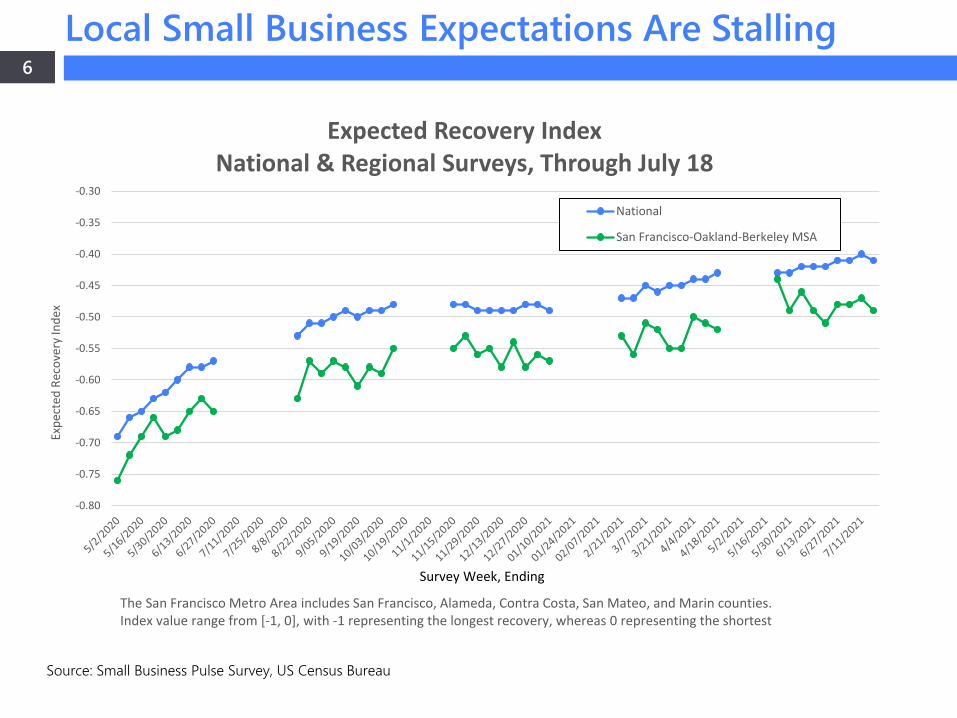

The emergence of the Delta variant has stalled aspects of the city’s economic recovery. Office attendance, time spent outside the home, and small business sentiment are all somewhat lower than in the July report.

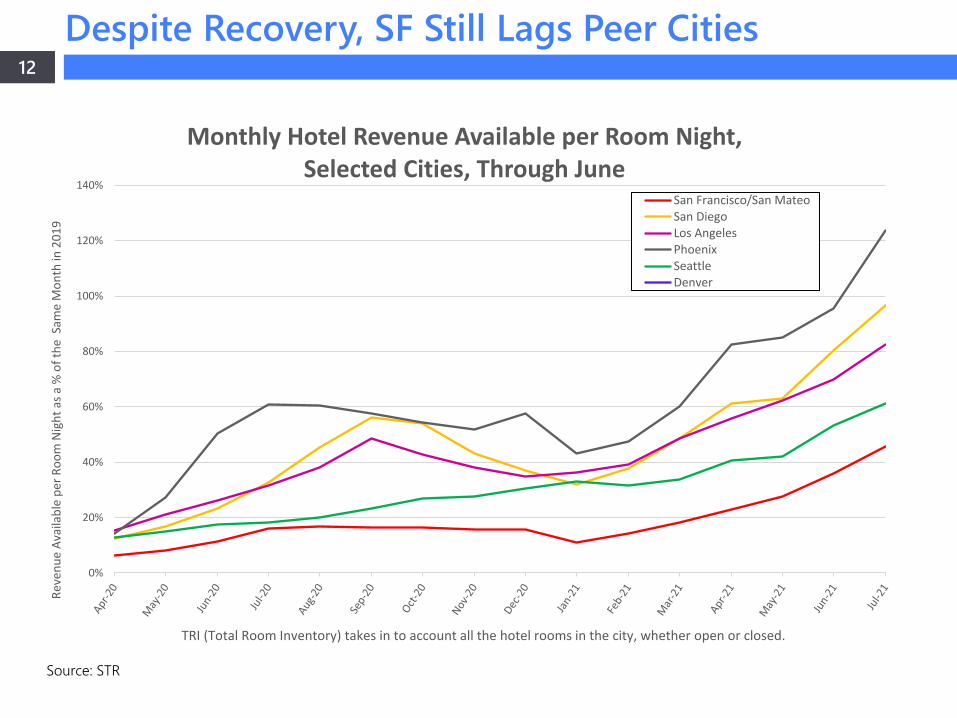

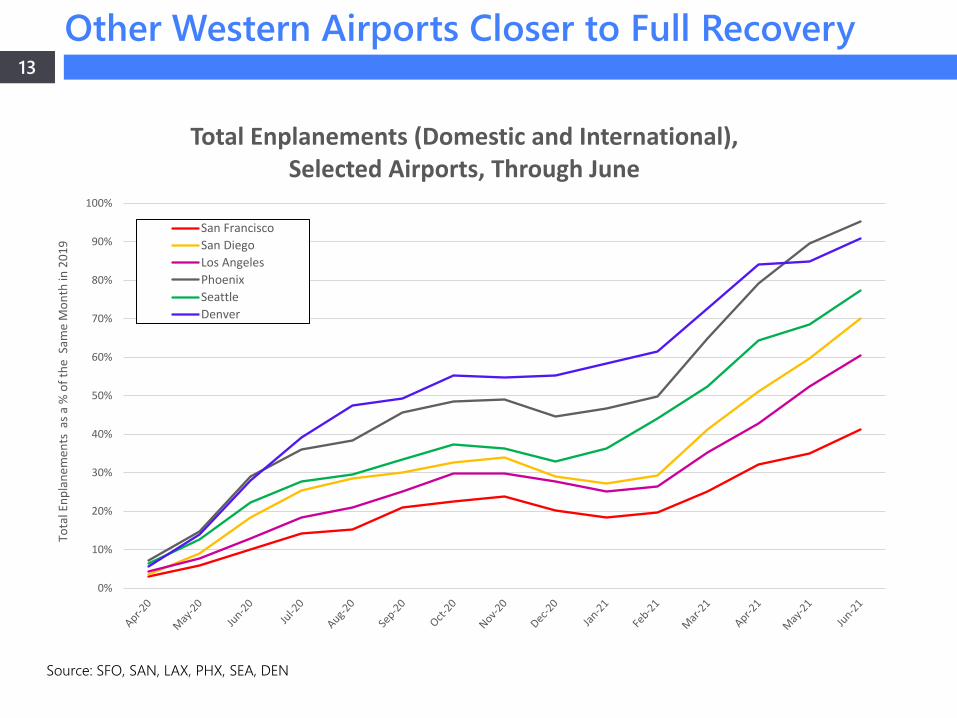

The City’s tourism industry continues to lag other major tourism centers in the Western U.S. Hotel revenues, while growing rapidly in 2021, are still well below 2019 levels, as are enplanements at San Francisco International Airport.

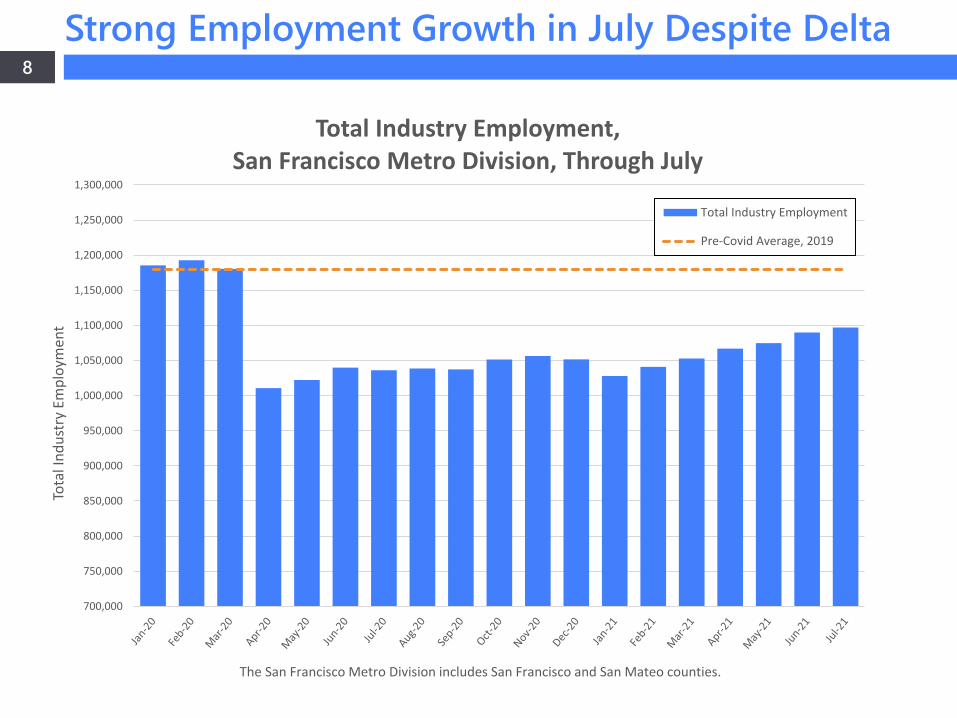

On the other hand, July represented another strong month for job growth locally, with 7,100 jobs created. After a steep drop in 2020, employment in the San Francisco metro division has risen by 7% since January, one of the fastest rates of any large metro area in the country.

Despite the weakness in hotels and air travel, employment in the Leisure and Hospitality sector has led all sectors in employment growth, with 5,400 jobs added in July, and 39,800 since January.

2

Highlights of the August Report

3

List of Economic Indicators

1. Time Spent Outside of the Home 2. Office Attendance3. Small Business Sentiment: Expected Recovery Index4. New Business Registrations5. Total Employment in San Francisco & San Mateo Counties6. Hotel Occupancy Rate7. Hotel Average Daily Rate (ADR) per Night8. Hotel Revenue Available per Room Night (RevPar): Selected Cities Comparison9. Small Business Sentiment: Expected Future Business Travel10. Airport Enplanements: Selected Cities Comparison 11. Convention Bookings At Moscone Center12. PM Freeway Speed13. Bay Bridge and Golden Bridge Traffic14. BART Exits at Downtown SF Stations15. Average Asking Rents for Apartments16. Building Permits

4

Source: Google Mobility, Opportunity Insights, https://tracktherecovery.orghttps://opportunityinsights.org/wp-content/uploads/2020/05/tracker_paper.pdf

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

3/1/

20

3/15

/20

3/29

/20

4/12

/20

4/26

/20

5/10

/20

5/24

/20

6/7/

20

6/21

/20

7/5/

20

7/19

/20

8/2/

20

8/16

/20

8/30

/20

9/13

/20

9/27

/20

10/1

1/20

10/2

5/20

11/8

/20

11/2

2/20

12/6

/20

12/2

0/20

1/3/

21

1/17

/21

1/31

/21

2/14

/21

2/28

/21

3/14

/21

3/28

/21

4/11

/21

4/25

/21

5/9/

21

5/23

/21

6/6/

21

6/20

/21

7/4/

21

7/18

/21

8/1/

21

% C

hang

e in

Tim

e Sp

ent A

way

from

Hom

e

% Change in Time Spent Outside Home, San Francisco and California, Through August 13

CaliforniaSan Francisco

Change relative to the January 2020 index period, not seasonally adjusted.

Time Outside the Home Has Declined Slightly

5

Source: Kastle Systems

0%

10%

20%

30%

40%

50%

60%

4/1/

2020

4/15

/202

0

4/29

/202

0

5/13

/202

0

5/27

/202

0

6/10

/202

0

6/24

/202

0

7/8/

2020

7/22

/202

0

8/5/

2020

8/19

/202

0

9/2/

2020

9/16

/202

0

9/30

/202

0

10/1

4/20

20

10/2

8/20

20

11/1

1/20

20

11/2

5/20

20

12/9

/202

0

12/2

3/20

20

1/6/

2021

1/20

/202

1

2/3/

2021

2/17

/202

1

3/3/

2021

3/17

/202

1

3/31

/202

1

4/14

/202

1

4/28

/202

1

5/12

/202

1

5/26

/202

1

6/9/

2021

6/23

/202

1

7/7/

2021

7/21

/202

1

8/4/

2021

Wee

kly

Offi

ce A

tten

danc

e R

ate,

%

Weekly Office Attendance Across Selected Metros, Through August 11

Austin MetroLos Angeles MetroSan Jose MetroNew York MetroSan Francisco Metro

Kastle Back to Work Barometer reflects unique authorized user entries in a market relative to its pre-COVID baseline, averaged weekly. The San Francisco Metro Area includes San Francisco, Alameda, Contra Costa, San Mateo, and Marin counties.

Office Attendance Has Declined Across the U.S.

6

Source: Small Business Pulse Survey, US Census Bureau

-0.80

-0.75

-0.70

-0.65

-0.60

-0.55

-0.50

-0.45

-0.40

-0.35

-0.30

Expe

cted

Rec

over

y In

dex

Expected Recovery IndexNational & Regional Surveys, Through July 18

National

San Francisco-Oakland-Berkeley MSA

Survey Week, Ending

The San Francisco Metro Area includes San Francisco, Alameda, Contra Costa, San Mateo, and Marin counties.Index value range from [-1, 0], with -1 representing the longest recovery, whereas 0 representing the shortest

Local Small Business Expectations Are Stalling

7

Source: Treasurer & Tax Collector, City and County of San Francisco

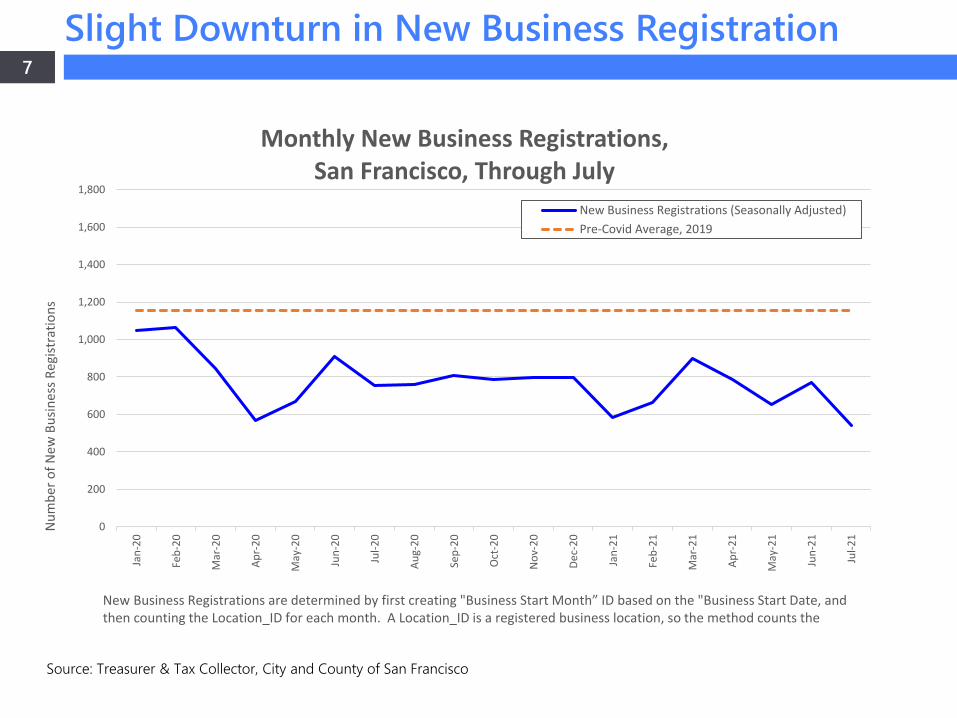

Slight Downturn in New Business Registration

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-

21

May

-21

Jun-

21

Jul-2

1

Num

ber o

f New

Bus

ines

s Reg

istra

tions

Monthly New Business Registrations,San Francisco, Through July

New Business Registrations (Seasonally Adjusted)Pre-Covid Average, 2019

New Business Registrations are determined by first creating "Business Start Month” ID based on the "Business Start Date, and then counting the Location_ID for each month. A Location_ID is a registered business location, so the method counts the

8

Source: California Employment Development Department (EDD)

Strong Employment Growth in July Despite Delta

700,000

750,000

800,000

850,000

900,000

950,000

1,000,000

1,050,000

1,100,000

1,150,000

1,200,000

1,250,000

1,300,000

Tota

l Ind

ustr

y Em

ploy

men

t

Total Industry Employment, San Francisco Metro Division, Through July

Total Industry Employment

Pre-Covid Average, 2019

The San Francisco Metro Division includes San Francisco and San Mateo counties.

9

Source: California Employment Development Department (EDD)

Hospitality and Professional Services Lead Growth

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

Employment Change by Industry Sector, June-July 2021:San Francisco Metropolitan Division

10

Source: STR

0

10

20

30

40

50

60

70

80

90

100

10/1

0/20

20

10/2

4/20

20

11/7

/202

0

11/2

1/20

20

12/5

/202

0

12/1

9/20

20

1/2/

2021

1/16

/202

1

1/30

/202

1

2/13

/202

1

2/27

/202

1

3/13

/202

1

3/27

/202

1

4/10

/202

1

4/24

/202

1

5/8/

2021

5/22

/202

1

6/5/

2021

6/19

/202

1

7/3/

2021

7/17

/202

1

7/31

/202

1

8/14

/202

1

Occ

upan

cy (%

)

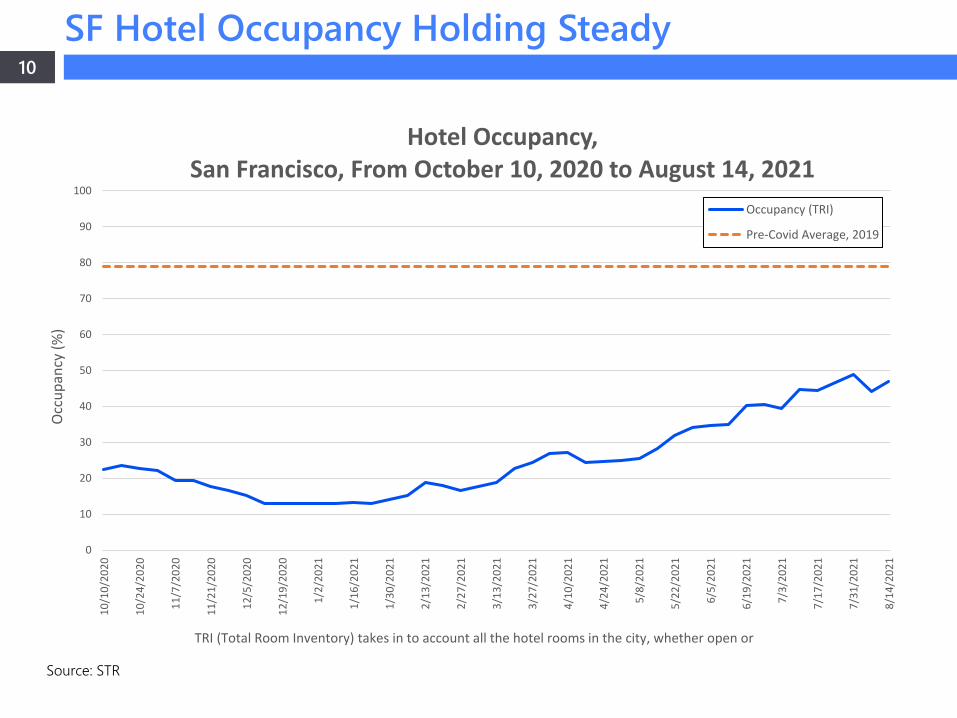

Hotel Occupancy,San Francisco, From October 10, 2020 to August 14, 2021

Occupancy (TRI)

Pre-Covid Average, 2019

TRI (Total Room Inventory) takes in to account all the hotel rooms in the city, whether open or

SF Hotel Occupancy Holding Steady

11

Source: STR

$0

$50

$100

$150

$200

$250

$300

$350

$400

4/4/

2020

4/18

/202

0

5/2/

2020

5/16

/202

0

5/30

/202

0

6/13

/202

0

6/27

/202

0

7/11

/202

0

7/25

/202

0

8/8/

2020

8/22

/202

0

9/5/

2020

9/19

/202

0

10/3

/202

0

10/1

7/20

20

10/3

1/20

20

11/1

4/20

20

11/2

8/20

20

12/1

2/20

20

12/2

6/20

20

1/9/

2021

1/23

/202

1

2/6/

2021

2/20

/202

1

3/6/

2021

3/20

/202

1

4/3/

2021

4/17

/202

1

5/1/

2021

5/15

/202

1

5/29

/202

1

6/12

/202

1

6/26

/202

1

7/10

/202

1

7/24

/202

1

8/7/

2021

Aver

age

Daily

Rat

e pe

r Nig

ht ($

)

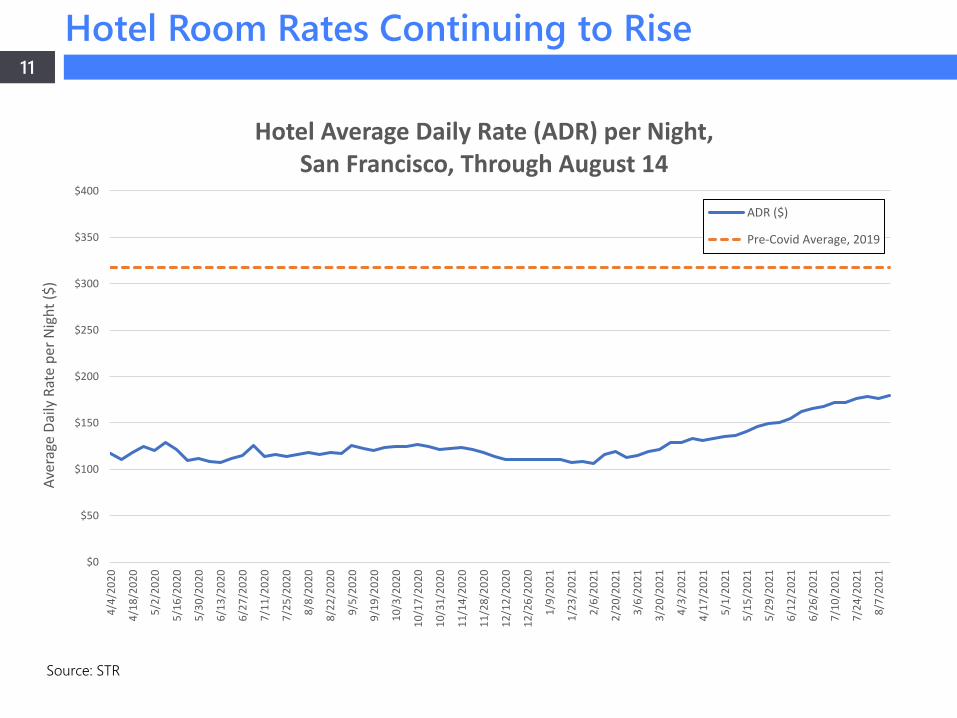

Hotel Average Daily Rate (ADR) per Night,San Francisco, Through August 14

ADR ($)

Pre-Covid Average, 2019

Hotel Room Rates Continuing to Rise

12

Source: STR

Despite Recovery, SF Still Lags Peer Cities

0%

20%

40%

60%

80%

100%

120%

140%

Reve

nue

Avai

labl

e pe

r Roo

m N

ight

as a

% o

f the

Sam

e M

onth

in 2

019

Monthly Hotel Revenue Available per Room Night,Selected Cities, Through June

San Francisco/San MateoSan DiegoLos AngelesPhoenixSeattleDenver

TRI (Total Room Inventory) takes in to account all the hotel rooms in the city, whether open or closed.

13

Source: SFO, SAN, LAX, PHX, SEA, DEN

Other Western Airports Closer to Full Recovery

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Tota

l Enp

lane

men

ts a

s a %

of t

he S

ame

Mon

th in

201

9

Total Enplanements (Domestic and International), Selected Airports, Through June

San FranciscoSan DiegoLos AngelesPhoenixSeattleDenver

14

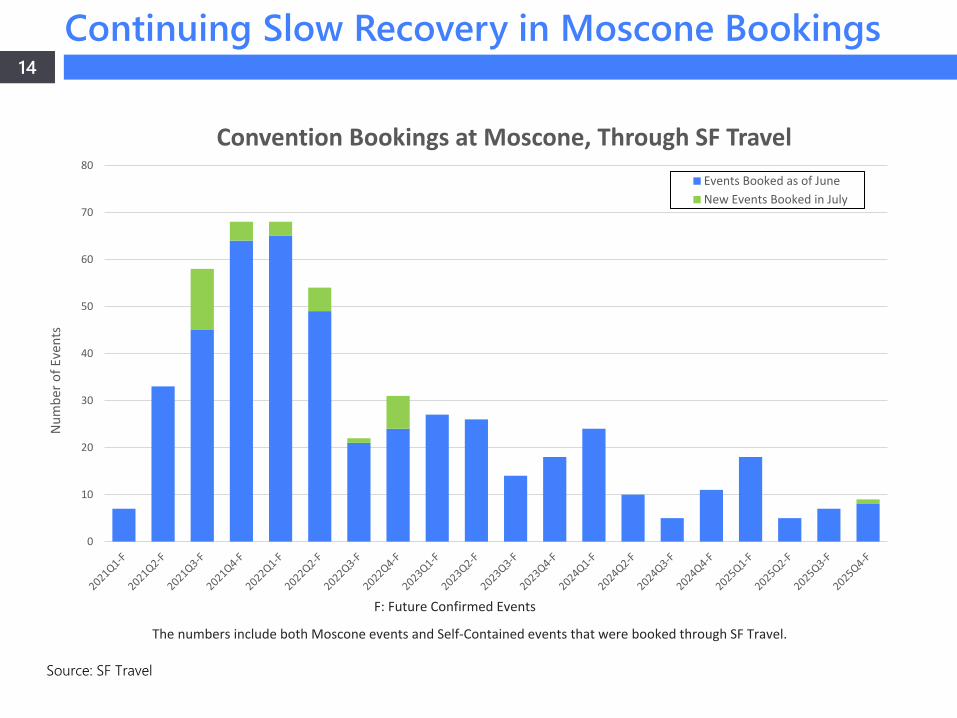

Source: SF Travel

Continuing Slow Recovery in Moscone Bookings

0

10

20

30

40

50

60

70

80

Num

ber o

f Eve

nts

Convention Bookings at Moscone, Through SF TravelEvents Booked as of JuneNew Events Booked in July

F: Future Confirmed Events

The numbers include both Moscone events and Self-Contained events that were booked through SF Travel.

15

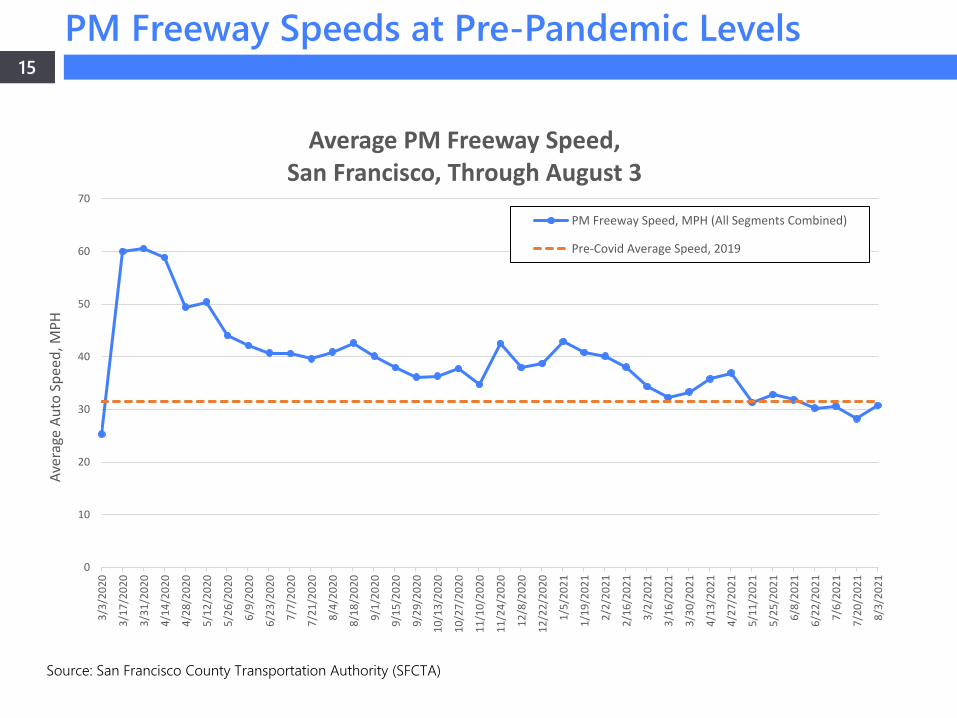

Source: San Francisco County Transportation Authority (SFCTA)

PM Freeway Speeds at Pre-Pandemic Levels

0

10

20

30

40

50

60

70

3/3/

2020

3/17

/202

0

3/31

/202

0

4/14

/202

0

4/28

/202

0

5/12

/202

0

5/26

/202

0

6/9/

2020

6/23

/202

0

7/7/

2020

7/21

/202

0

8/4/

2020

8/18

/202

0

9/1/

2020

9/15

/202

0

9/29

/202

0

10/1

3/20

20

10/2

7/20

20

11/1

0/20

20

11/2

4/20

20

12/8

/202

0

12/2

2/20

20

1/5/

2021

1/19

/202

1

2/2/

2021

2/16

/202

1

3/2/

2021

3/16

/202

1

3/30

/202

1

4/13

/202

1

4/27

/202

1

5/11

/202

1

5/25

/202

1

6/8/

2021

6/22

/202

1

7/6/

2021

7/20

/202

1

8/3/

2021

Aver

age

Auto

Spe

ed, M

PH

Average PM Freeway Speed,San Francisco, Through August 3

PM Freeway Speed, MPH (All Segments Combined)

Pre-Covid Average Speed, 2019

16

Source: Bay Area Toll Authority (BATA), Golden Gate Bridge Highway & Transportation District

Bridge Traffic Steady at 90% of Normal

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

Tota

l Mon

thly

Tra

ffic

Volu

me

Bay Bridge and Golden Gate Bridge Monthly Traffic Volume,San Francisco, Through July

Bay BridgeGolden Gate BridgePre-Covid Average, 2019

Includes Bay Bridge (Westbound Trips) and Golden Gate Bridge (Southbound Trips)

17

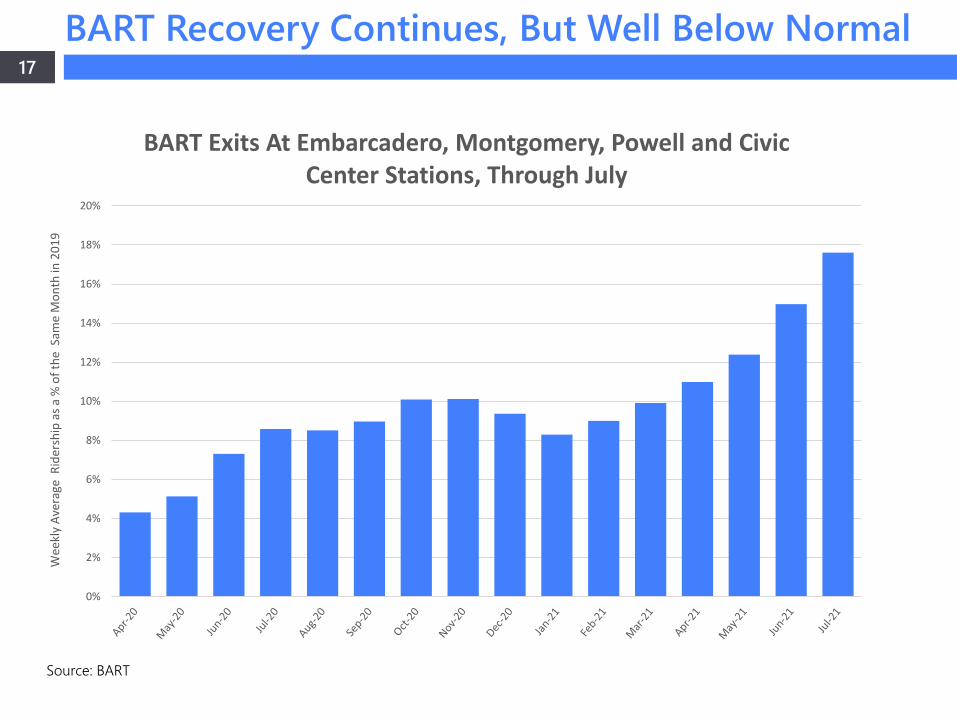

Source: BART

BART Recovery Continues, But Well Below Normal

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Wee

kly

Aver

age

Rid

ersh

ip a

s a %

of t

he S

ame

Mon

th in

201

9

BART Exits At Embarcadero, Montgomery, Powell and Civic Center Stations, Through July

18

Source: Apartment List

Apartment Rents Continue Rising; Still Down 17%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Aver

age

Aski

ng A

part

men

t Re

nt

Average Asking Apartment Rent,San Francisco, Through July

Average Asking Apartment RentPre-Pandemic Average, 2019

Overall Average, Blended Across All Unit Sizes

19

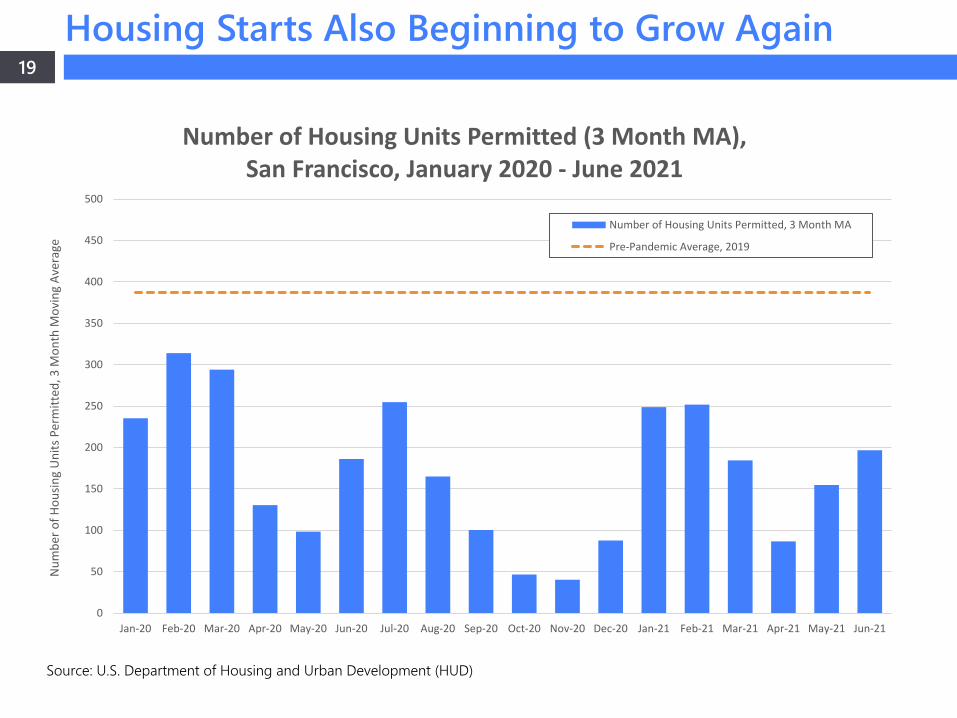

Source: U.S. Department of Housing and Urban Development (HUD)

Housing Starts Also Beginning to Grow Again

0

50

100

150

200

250

300

350

400

450

500

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21

Num

ber o

f Hou

sing

Uni

ts P

erm

itted

, 3 M

onth

Mov

ing

Aver

age

Number of Housing Units Permitted (3 Month MA), San Francisco, January 2020 - June 2021

Number of Housing Units Permitted, 3 Month MA

Pre-Pandemic Average, 2019

Ted Egan, Ph.D., Chief Economist

Asim Khan, Ph.D., Senior Economist

20

Staff Contact