Embed Size (px)

Citation preview

Status of Renewable Energy (RE)

in Malaysia

Ir. Ahmad Hadri [email protected] Energy Centre (PTM)

EGNRET Meeting2nd – 3rd April 2009, Honolulu Hawaii

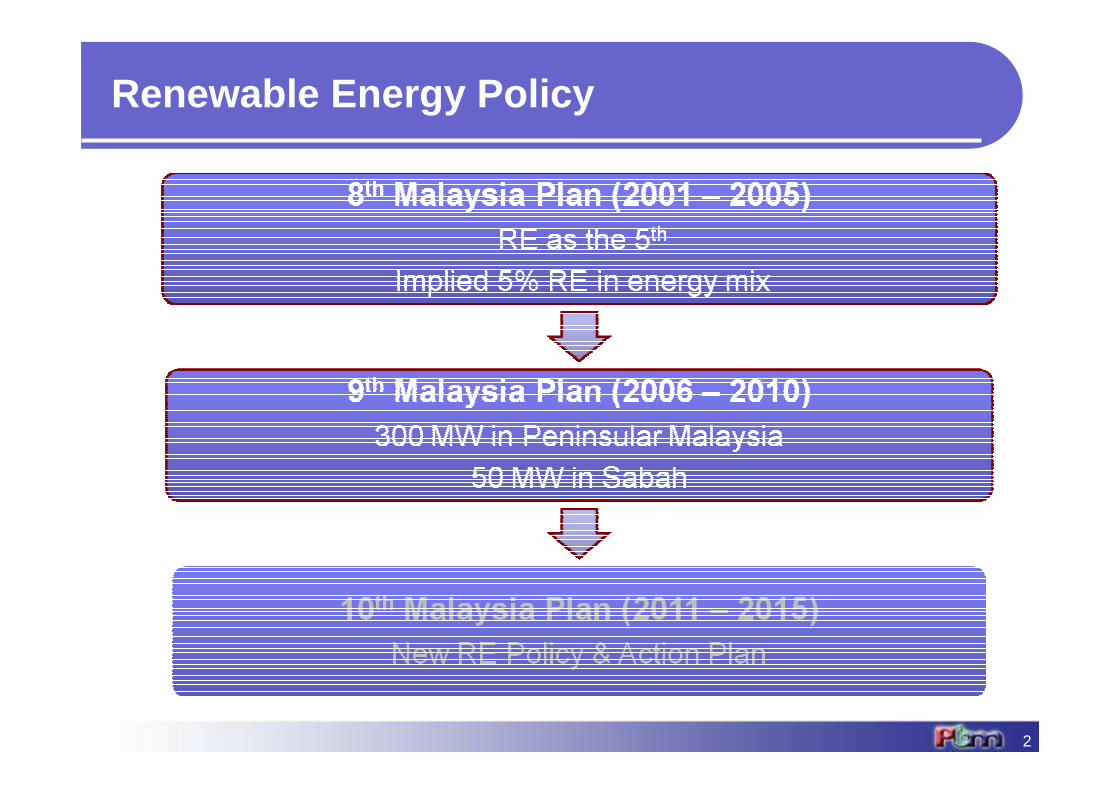

Renewable Energy Policy

2

RE Potential

3

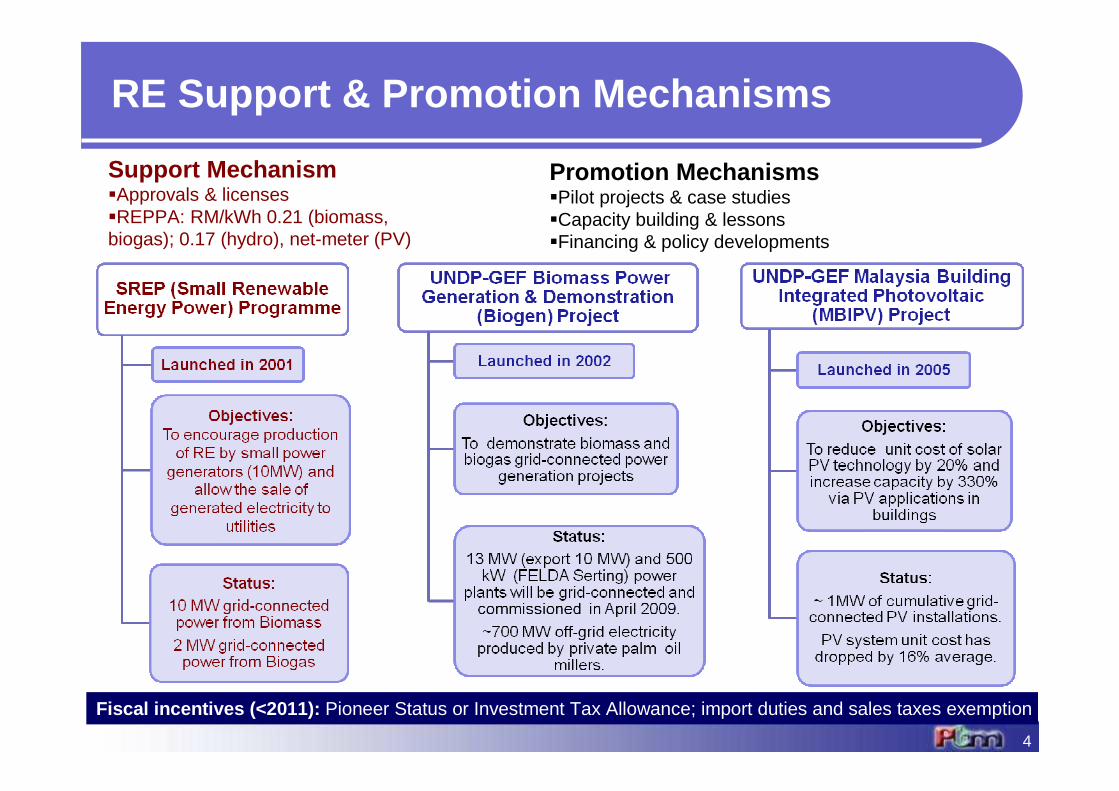

RE Support & Promotion Mechanisms

4

Support Mechanism�Approvals & licenses�REPPA: RM/kWh 0.21 (biomass, biogas); 0.17 (hydro), net-meter (PV)

Promotion Mechanisms�Pilot projects & case studies�Capacity building & lessons�Financing & policy developments

Fiscal incentives (<2011): Pioneer Status or Investment Tax Allowance; import duties and sales taxes exemption

5

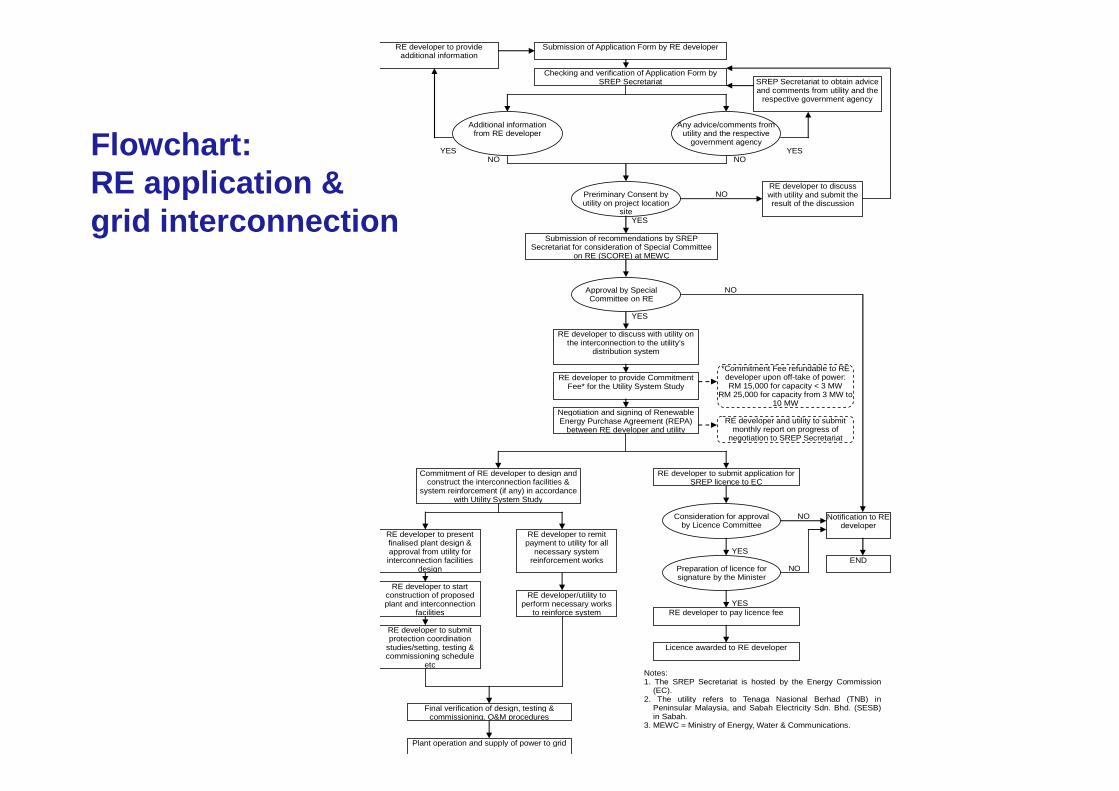

Submission of Application Form by RE developer

Checking and verification of Application Form by SREP Secretariat

RE developer to provide additional information

Additional information from RE developer

NO YES

SREP Secretariat to obtain advice and comments from utility and the

respective government agency

YES NO

Preriminary Consent by utility on project location

site

RE developer to discuss with utility and submit the result of the discussion

NO

Submission of recommendations by SREP Secretariat for consideration of Special Committee

on RE (SCORE) at MEWC

Approval by Special Committee on RE

RE developer to discuss with utility on the interconnection to the utility’s

distribution system

RE developer to provide Commitment Fee* for the Utility System Study

*Commitment Fee refundable to RE developer upon off-take of power: RM 15,000 for capacity < 3 MW

RM 25,000 for capacity from 3 MW to 10 MW

YES

YES

NO

Negotiation and signing of Renewable Energy Purchase Agreement (REPA)

between RE developer and utility RE developer and utility to submit

monthly report on progress of negotiation to SREP Secretariat

RE developer to submit application for SREP licence to EC

Consideration for approval by Licence Committee

Notification to RE developer

END

NO

YES

Preparation of licence for signature by the Minister

NO

YES RE developer to pay licence fee

Licence awarded to RE developer

Commitment of RE developer to design and construct the interconnection facilities &

system reinforcement (if any) in accordance with Utility System Study

RE developer to remit payment to utility for all

necessary system reinforcement works

RE developer to present finalised plant design & approval from utility for interconnection facilities

design

RE developer/utility to perform necessary works

to reinforce system

RE developer to start construction of proposed plant and interconnection

facilities

RE developer to submit protection coordination

studies/setting, testing & commissioning schedule

etc

Final verification of design, testing & commissioning, O&M procedures

Plant operation and supply of power to grid

Notes: 1. The SREP Secretariat is hosted by the Energy Commission

(EC). 2. The utility refers to Tenaga Nasional Berhad (TNB) in

Peninsular Malaysia, and Sabah Electricity Sdn. Bhd. (SESB) in Sabah.

3. MEWC = Ministry of Energy, Water & Communications.

Any advice/comments from utility and the respective

government agency Flowchart: RE application & grid interconnection

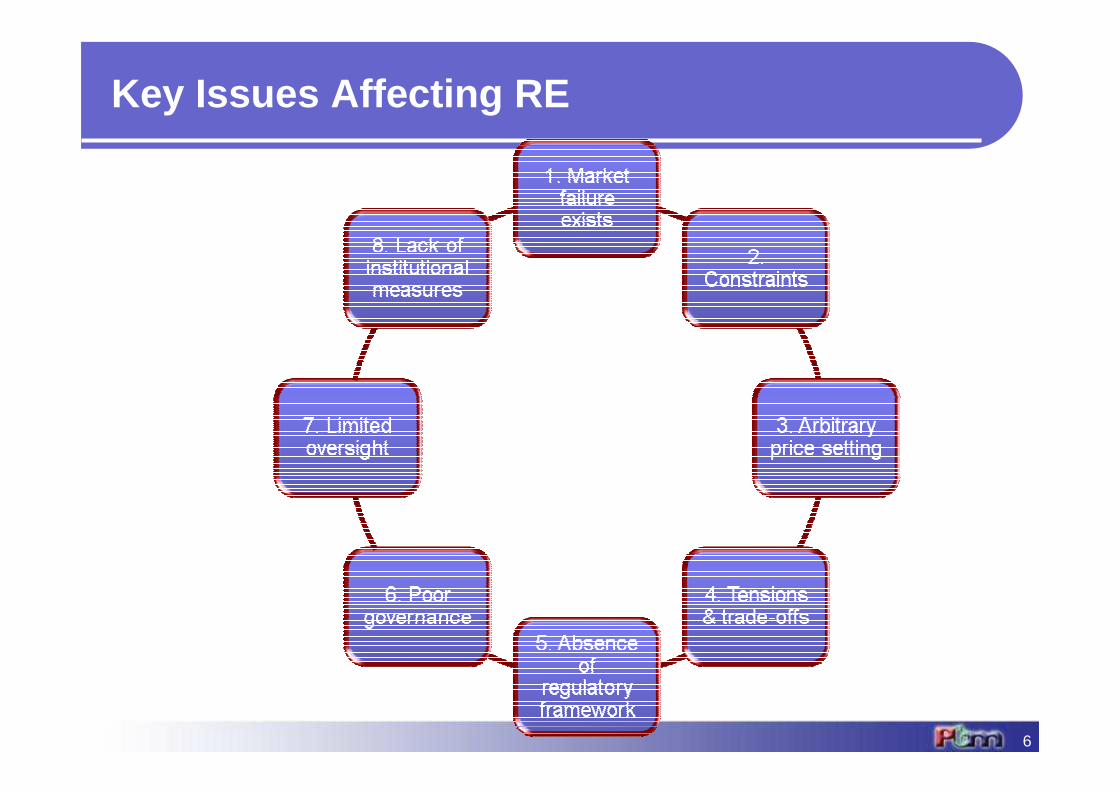

Key Issues Affecting RE

6

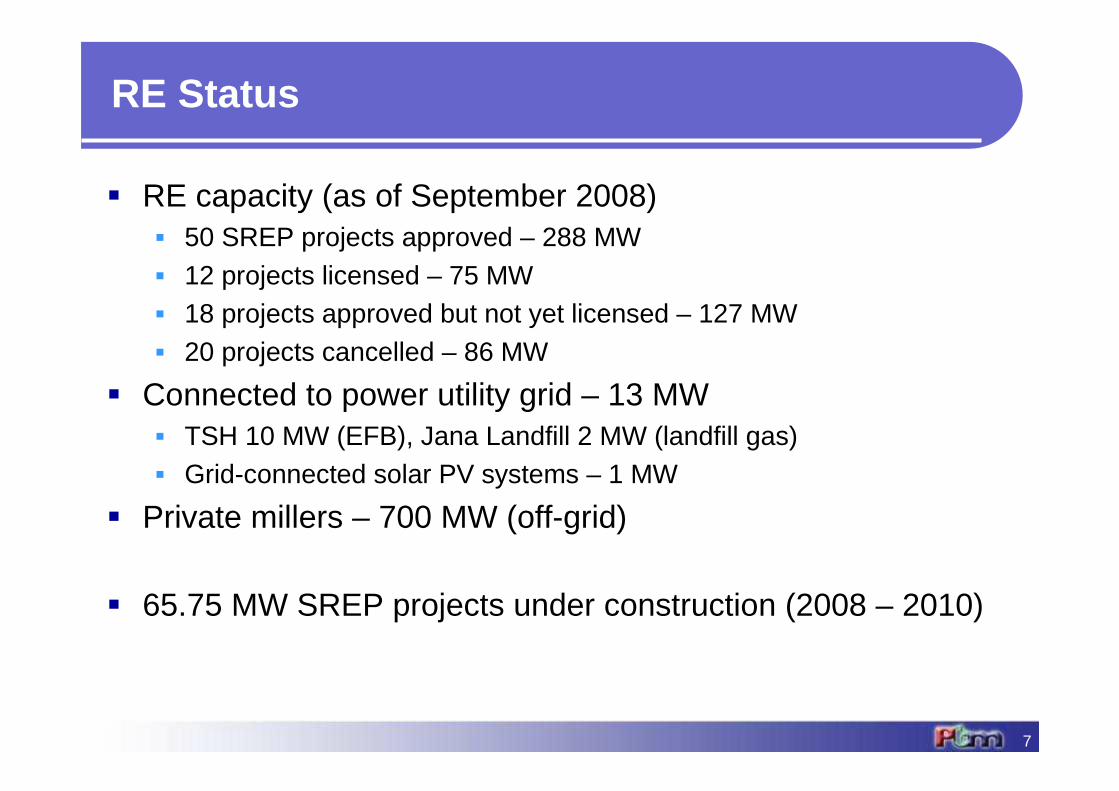

RE Status

� RE capacity (as of September 2008)� 50 SREP projects approved – 288 MW� 12 projects licensed – 75 MW� 18 projects approved but not yet licensed – 127 MW� 20 projects cancelled – 86 MW

� Connected to power utility grid – 13 MW � TSH 10 MW (EFB), Jana Landfill 2 MW (landfill gas)� Grid-connected solar PV systems – 1 MW

� Private millers – 700 MW (off-grid)

� 65.75 MW SREP projects under construction (2008 – 2010)

7

8

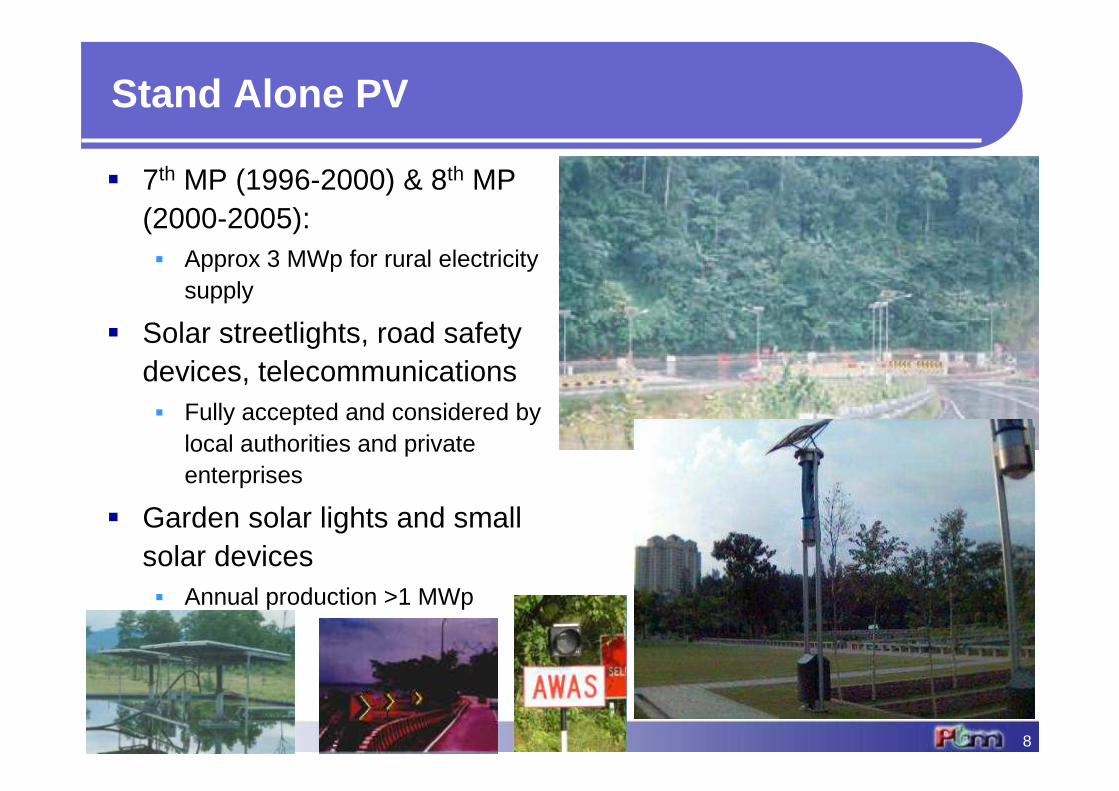

Stand Alone PV

� 7th MP (1996-2000) & 8th MP (2000-2005): � Approx 3 MWp for rural electricity

supply

� Solar streetlights, road safety devices, telecommunications� Fully accepted and considered by

local authorities and private enterprises

� Garden solar lights and small solar devices� Annual production >1 MWp

9

Solar Hybrid Systems

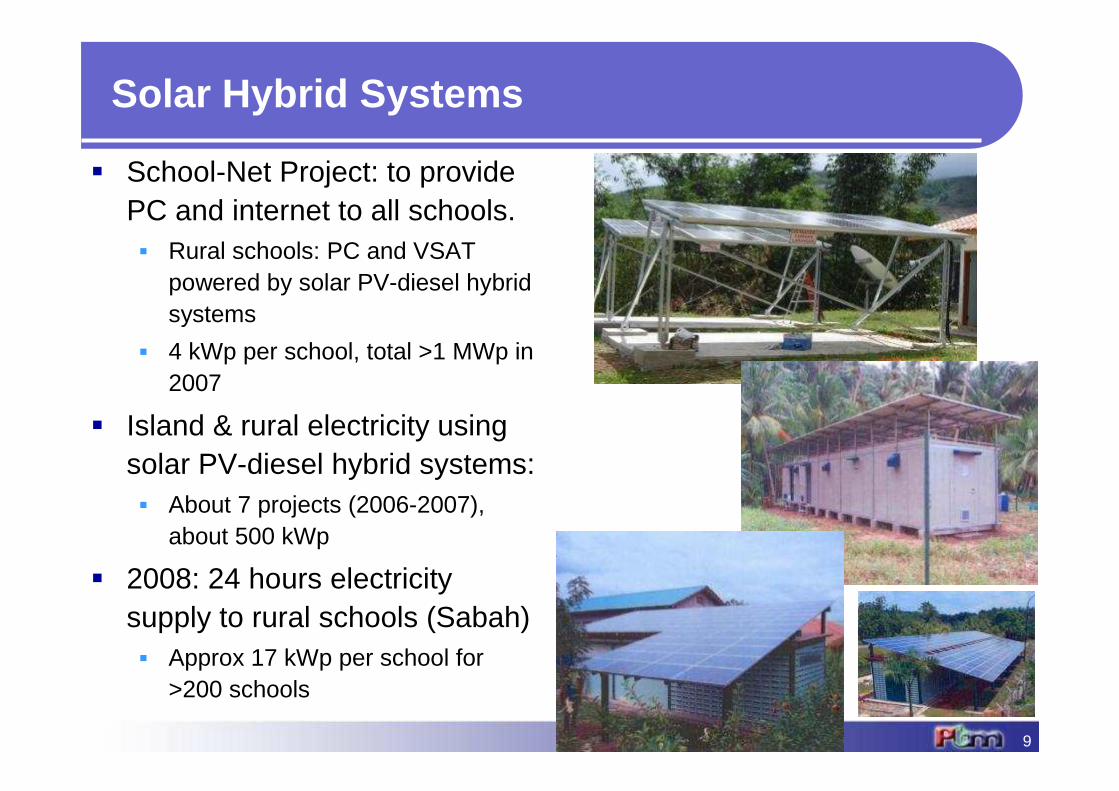

� School-Net Project: to provide PC and internet to all schools.� Rural schools: PC and VSAT

powered by solar PV-diesel hybrid systems

� 4 kWp per school, total >1 MWp in 2007

� Island & rural electricity using solar PV-diesel hybrid systems: � About 7 projects (2006-2007),

about 500 kWp

� 2008: 24 hours electricity supply to rural schools (Sabah)� Approx 17 kWp per school for

>200 schools

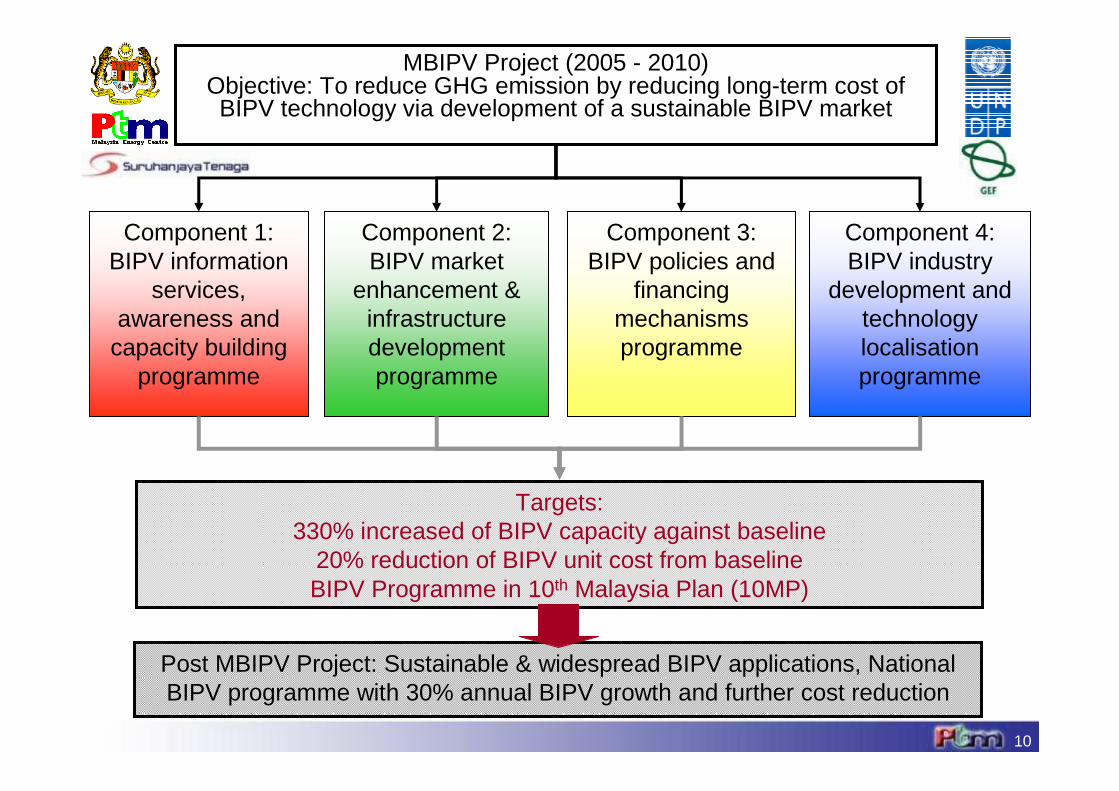

MBIPV Project (2005 - 2010)Objective: To reduce GHG emission by reducing long-term cost of BIPV technology via development of a sustainable BIPV market

Component 1: BIPV information

services, awareness and

capacity building programme

Component 4: BIPV industry

development and technology localisation programme

Component 2:BIPV market

enhancement & infrastructure development programme

Component 3: BIPV policies and

financing mechanisms programme

Targets:330% increased of BIPV capacity against baseline

20% reduction of BIPV unit cost from baseline BIPV Programme in 10th Malaysia Plan (10MP)

Post MBIPV Project: Sustainable & widespread BIPV applications, National BIPV programme with 30% annual BIPV growth and further cost reduction

10

11

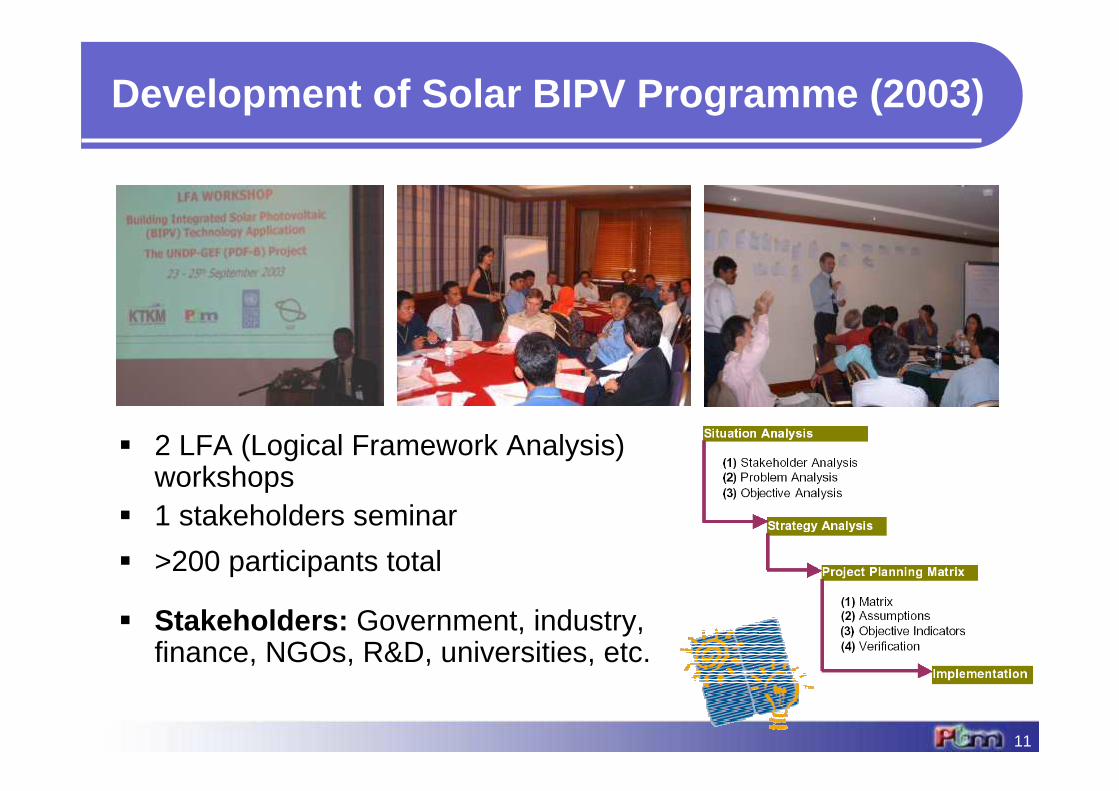

� 2 LFA (Logical Framework Analysis) workshops

� 1 stakeholders seminar

� >200 participants total

� Stakeholders: Government, industry, finance, NGOs, R&D, universities, etc.

Development of Solar BIPV Programme (2003)

12

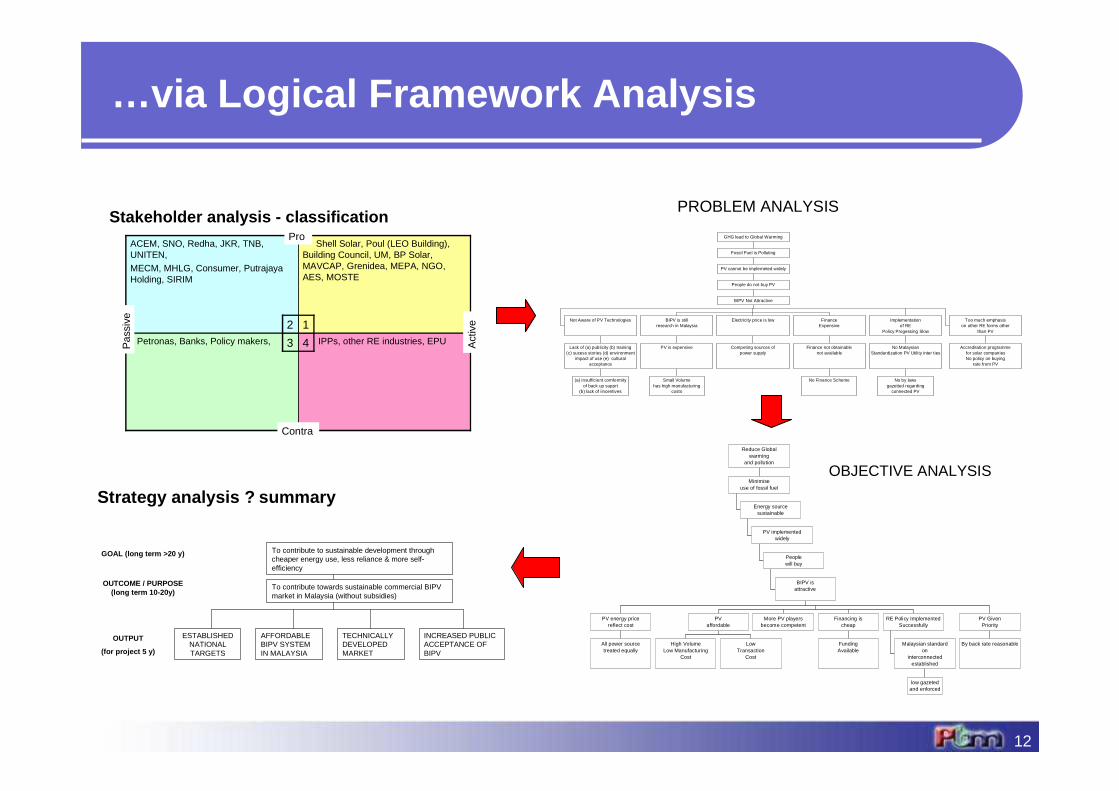

Stakeholder analysis - classification

IPPs, other RE industries, EPU Petronas, Banks, Policy makers,

Shell Solar, Poul (LEO Building),Building Council, UM, BP Solar,MAVCAP, Grenidea, MEPA, NGO,AES, MOSTE

ACEM, SNO, Redha, JKR, TNB,UNITEN,MECM, MHLG, Consumer, PutrajayaHolding, SIRIM

Pro

Contra

Pas

sive

Act

ive

43

12

All power sourcetreated equally

PV energy pricereflect cost

High VolumeLow Manufacturing

Cost

LowTransaction

Cost

PVaffordable

More PV playersbecome competent

FundingAvailable

Financing ischeap

low gazetedand enforced

Malaysian standardon

interconnectedestablished

RE Policy ImplementedSuccessfully

By back rate reasonable

PV GivenPriority

BIPV isattractive

Peoplewill buy

PV implementedwidely

Energy sourcesustainable

Minimiseuse of fossil fuel

Reduce Globalwarming

and pollution

OBJECTIVE ANALYSIS

(a) insufficient comformityof back up supprt

(b) lack of iincentives

Lack of (a) publicity (b) training(c) sucess stories (d) environment

impact of use (e) culturalacceptance

Not Aware of PV Technologies

Small Volumehas high manufacturing

costs

PV is expensive

BIPV is stillresearch in Malaysia

Competing sources ofpower supply

Electricity price is low

No Finance Scheme

Finance not obtainablenot available

FinanceExpensive

No by lawsgazetted regarding

connected PV

No MalaysianStandardization PV Utility inter ties

Implementationof RE

Policy Progessing Slow

Accreditation programmefor solar companiesNo policy on buying

rate from PV

Too much emphasison other RE forms other

than PV

BIPV Not Attractive

People do not buy PV

PV cannot be implemeted widely

Fossil Fuel is Polluting

GHG lead to Global Warming

PROBLEM ANALYSIS

Strategy analysis ? summary

ESTABLISHEDNATIONALTARGETS

AFFORDABLEBIPV SYSTEMIN MALAYSIA

TECHNICALLYDEVELOPEDMARKET

INCREASED PUBLICACCEPTANCE OFBIPV

To contribute towards sustainable commercial BIPVmarket in Malaysia (without subsidies)

To contribute to sustainable development throughcheaper energy use, less reliance & more self-efficiency

OUTPUT

(for project 5 y)

OUTCOME / PURPOSE(long term 10-20y)

GOAL (long term >20 y)

…via Logical Framework Analysis

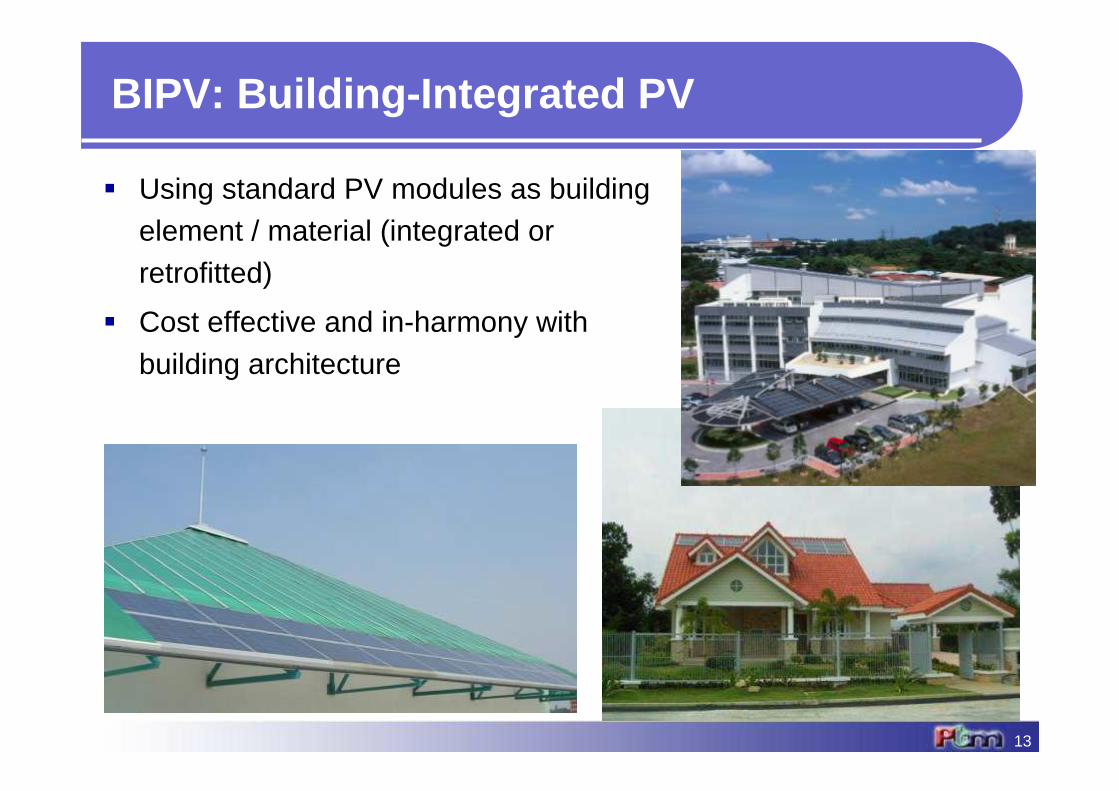

� Using standard PV modules as building element / material (integrated or retrofitted)

� Cost effective and in-harmony with building architecture

BIPV: Building-Integrated PV

13

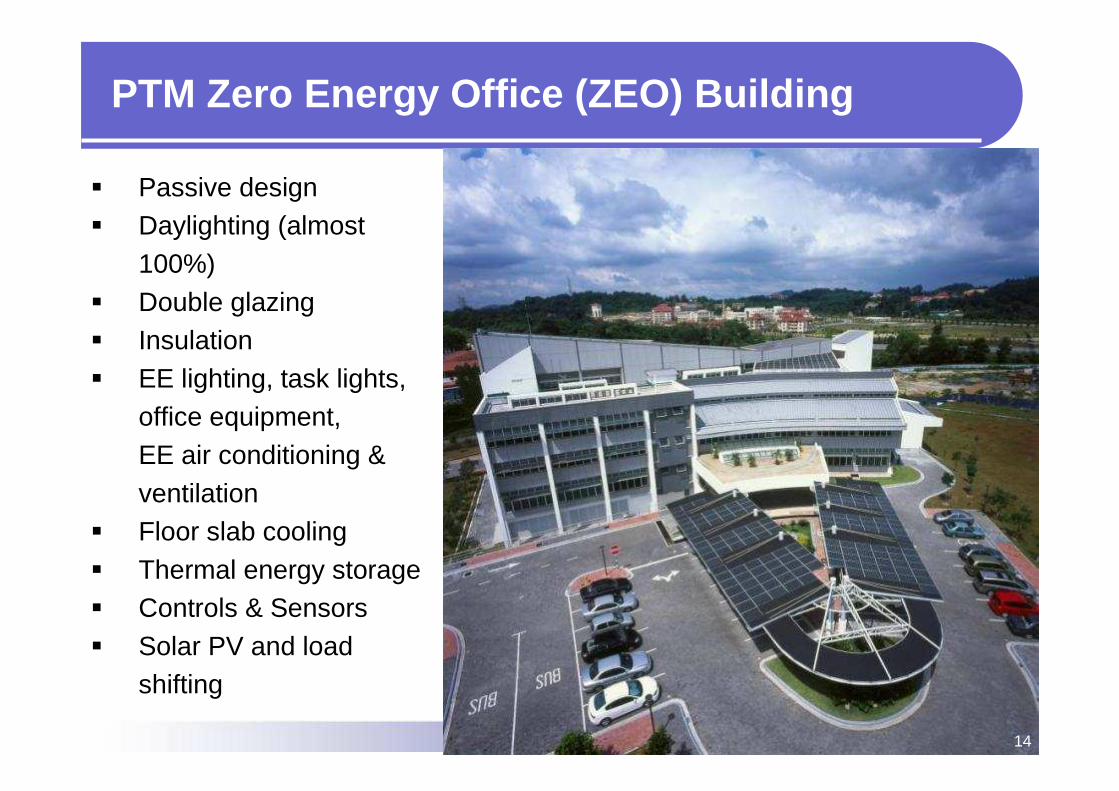

� Passive design� Daylighting (almost

100%)� Double glazing� Insulation� EE lighting, task lights,

office equipment, EE air conditioning & ventilation

� Floor slab cooling� Thermal energy storage� Controls & Sensors� Solar PV and load

shifting

PTM Zero Energy Office (ZEO) Building

14

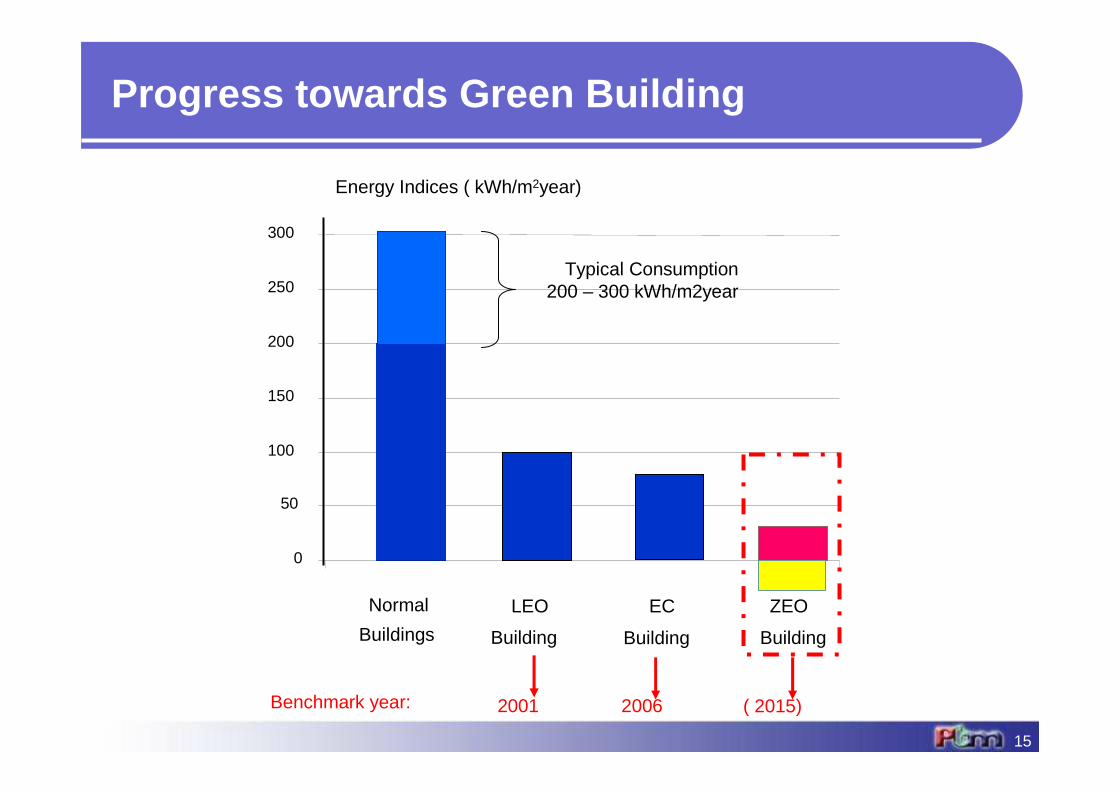

Energy Indices ( kWh/m2year)

0

50

100

150

200

250

300

Normal

Buildings

LEO

Building

ZEO

Building

EC

Building

Typical Consumption200 – 300 kWh/m2year

2001 2006 ( 2015) Benchmark year:

Progress towards Green Building

15

16

AB

C

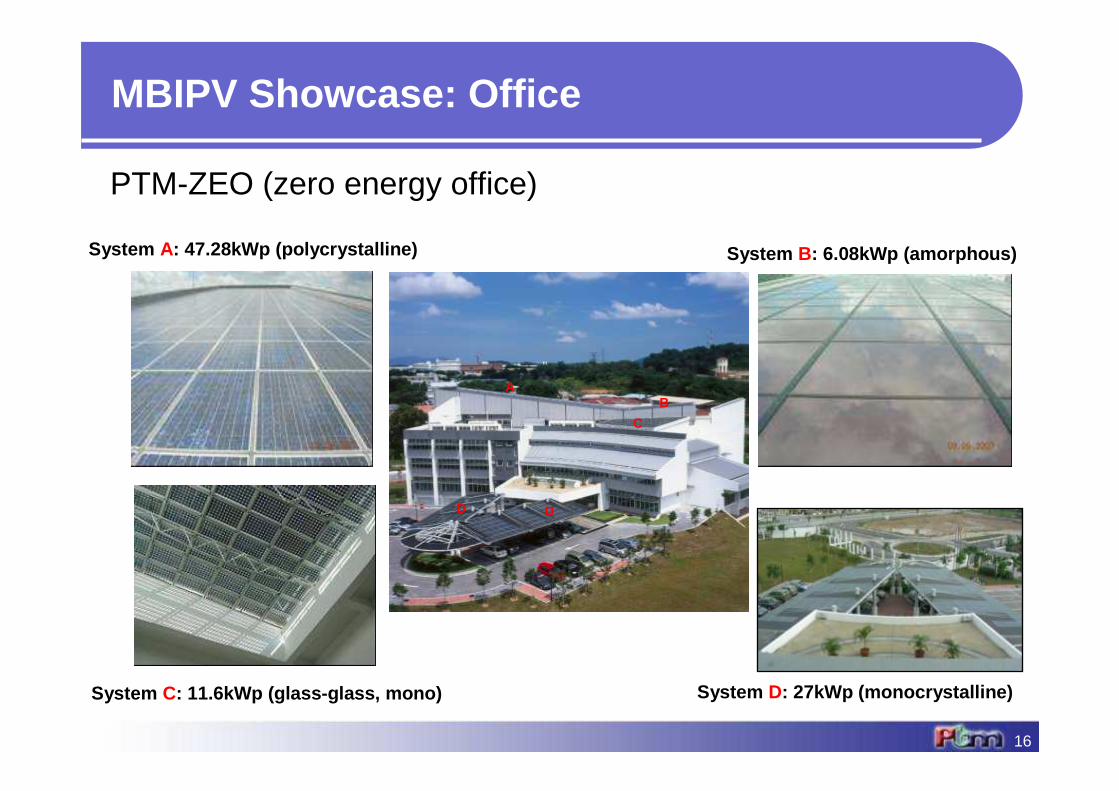

D D

System A: 47.28kWp (polycrystalline) System B: 6.08kWp (amorphous)

System C: 11.6kWp (glass-glass, mono) System D: 27kWp (monocrystalline)

MBIPV Showcase: Office

PTM-ZEO (zero energy office)

17

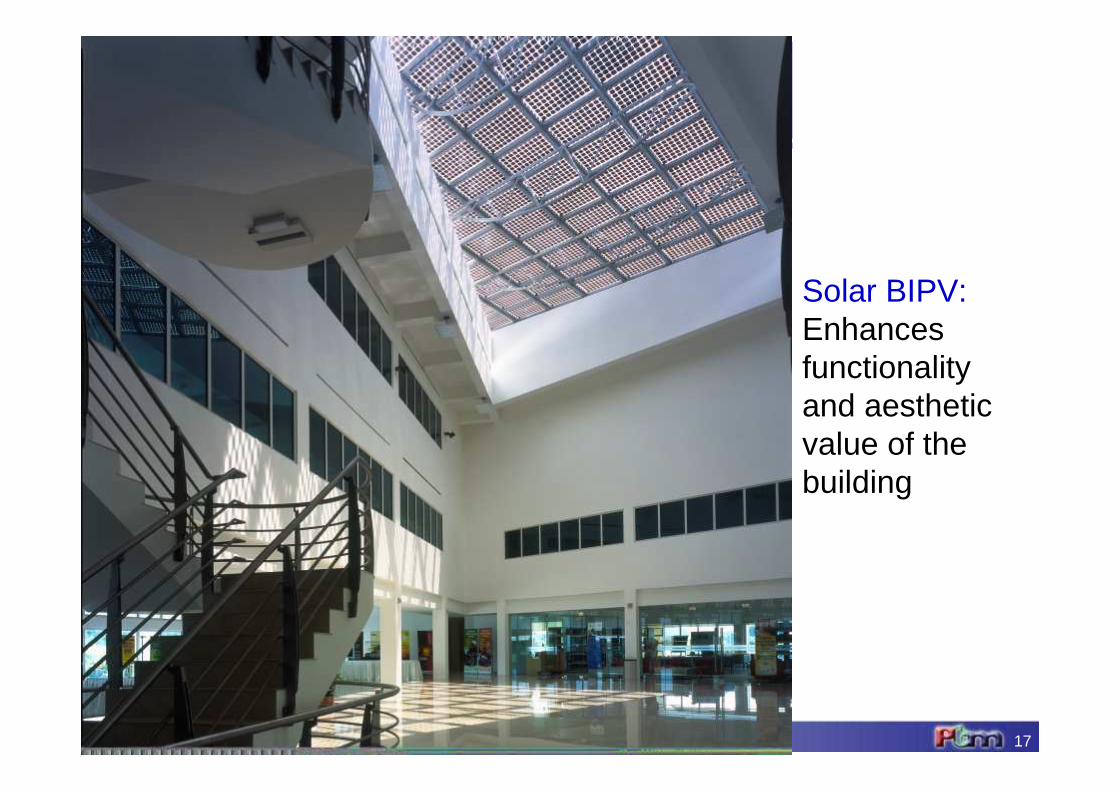

Solar BIPV: Enhances functionality and aesthetic value of the building

18

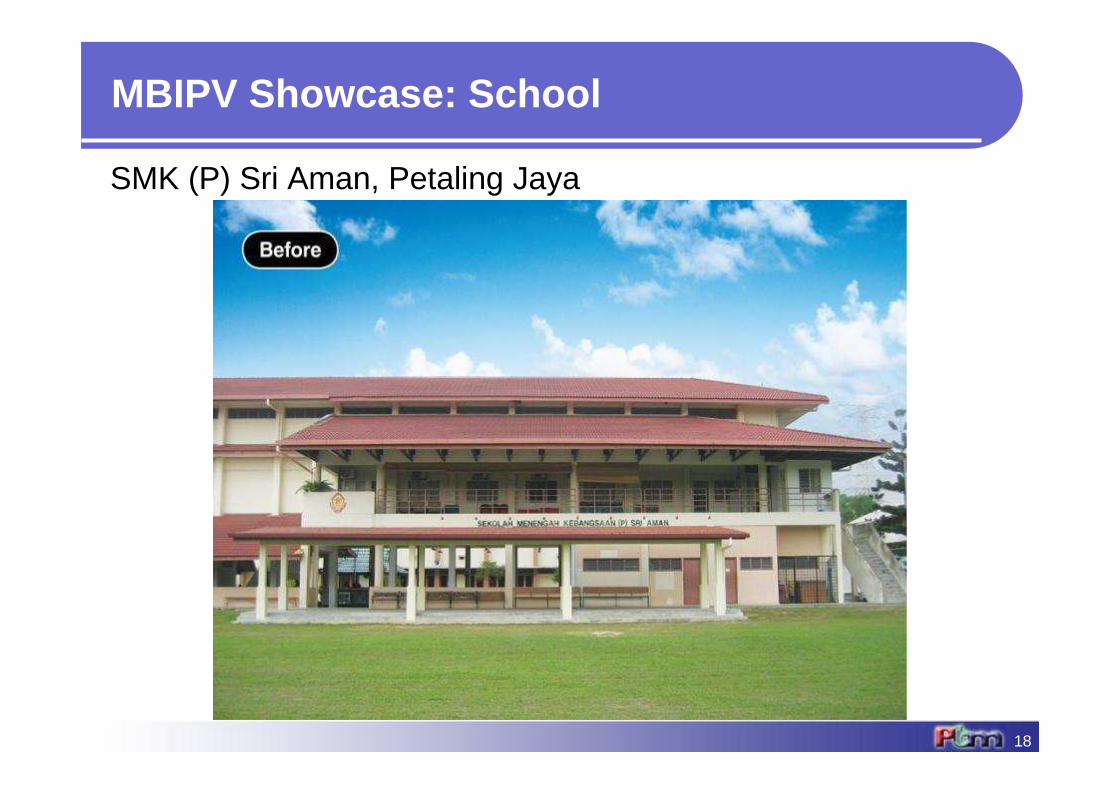

MBIPV Showcase: School

SMK (P) Sri Aman, Petaling Jaya

19

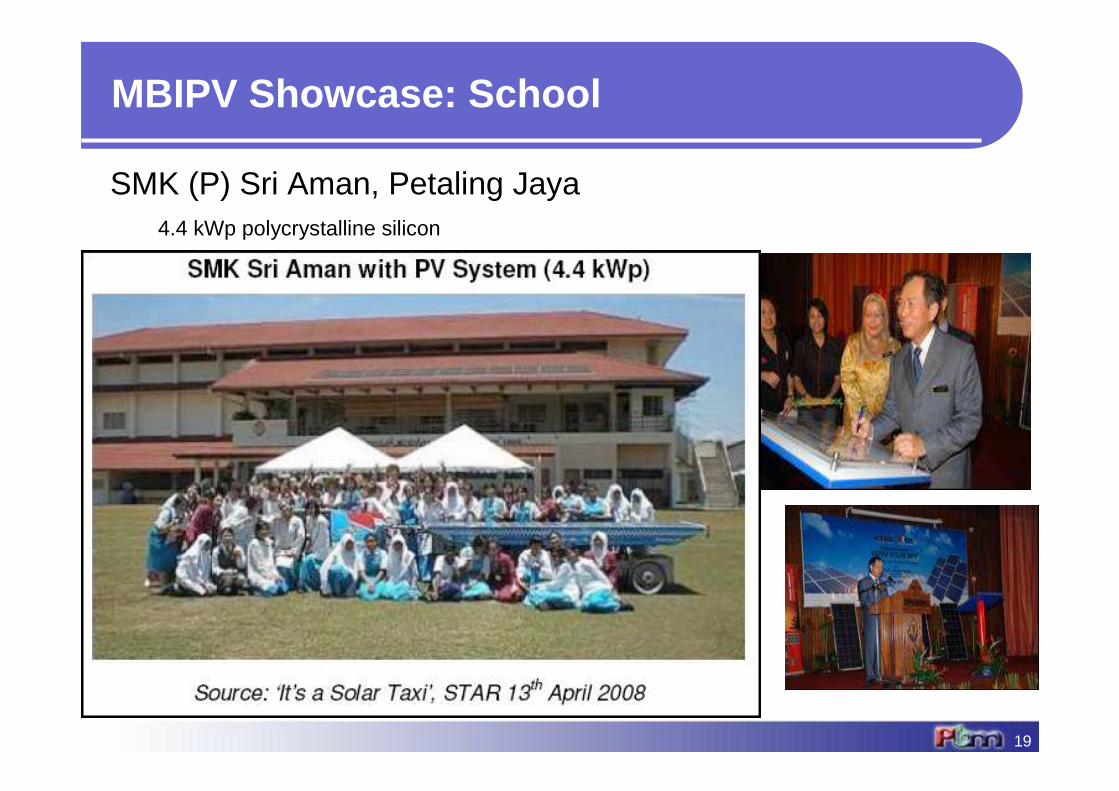

MBIPV Showcase: School

SMK (P) Sri Aman, Petaling Jaya4.4 kWp polycrystalline silicon

20

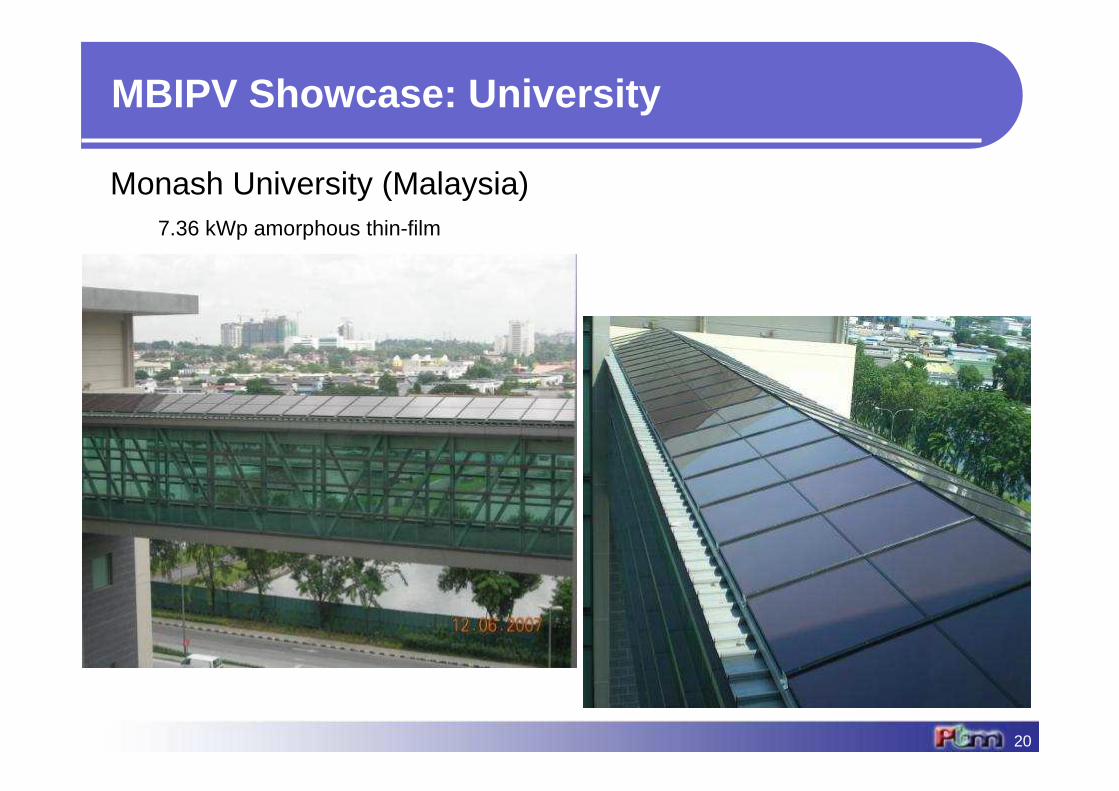

MBIPV Showcase: University

Monash University (Malaysia)7.36 kWp amorphous thin-film

21

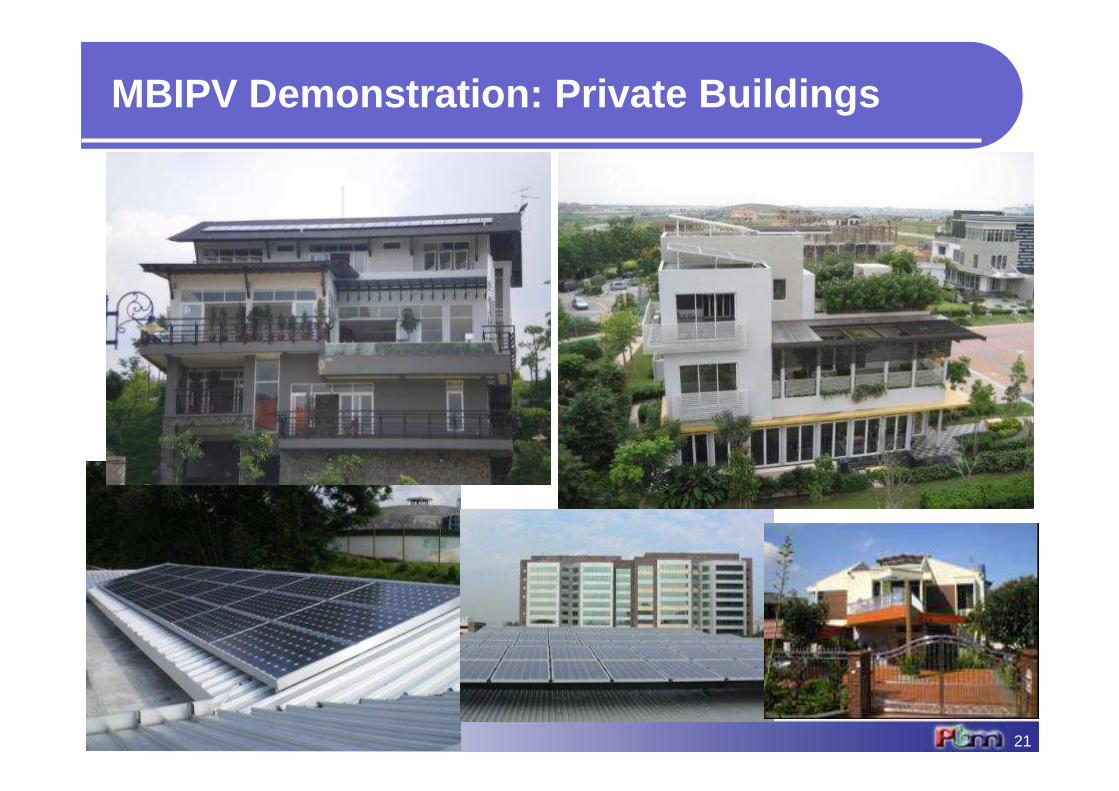

MBIPV Demonstration: Private Buildings

22

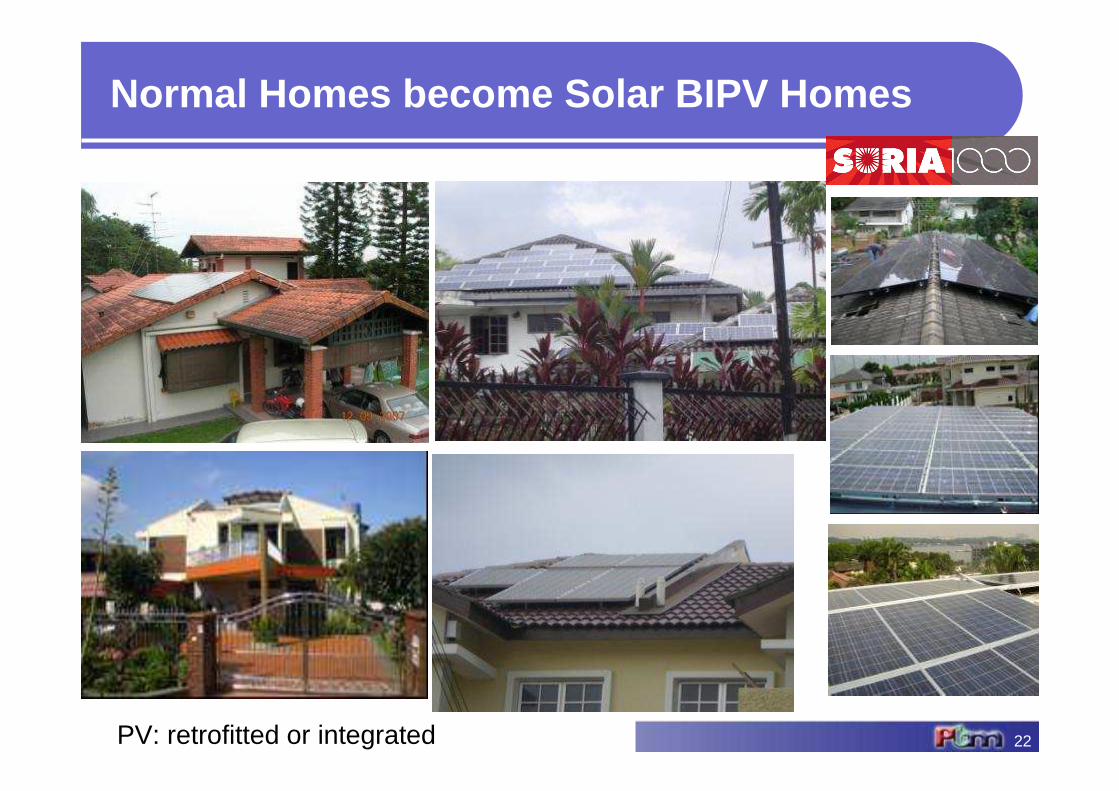

Normal Homes become Solar BIPV Homes

PV: retrofitted or integrated

23

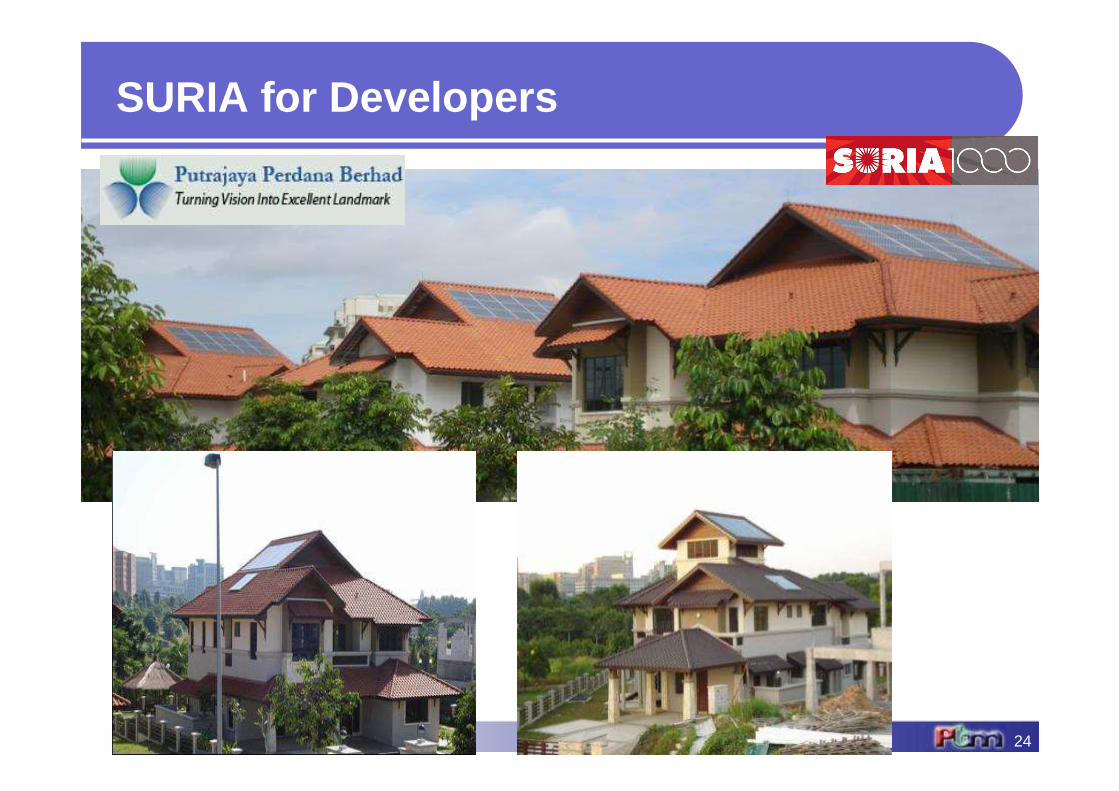

National PV Conference 2008

SURIA for Developers

24

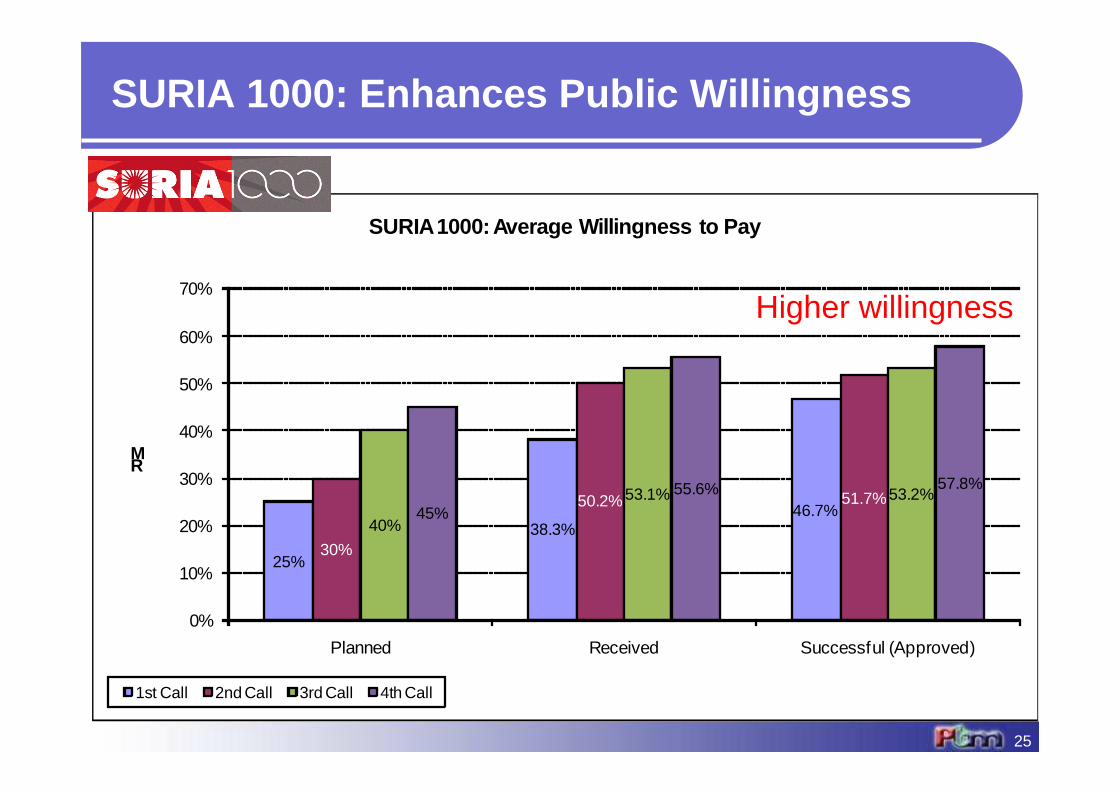

SURIA for Developers

25%

38.3%46.7%

30%

50.2% 51.7%

40%

53.1% 53.2%45%

55.6% 57.8%

0%

10%

20%

30%

40%

50%

60%

70%

Planned Received Successful (Approved)

RM

SURIA 1000: Average Willingness to Pay

1st Call 2nd Call 3rd Call 4th Call

Key Impact

Higher willingness

SURIA 1000: Enhances Public Willingness

25

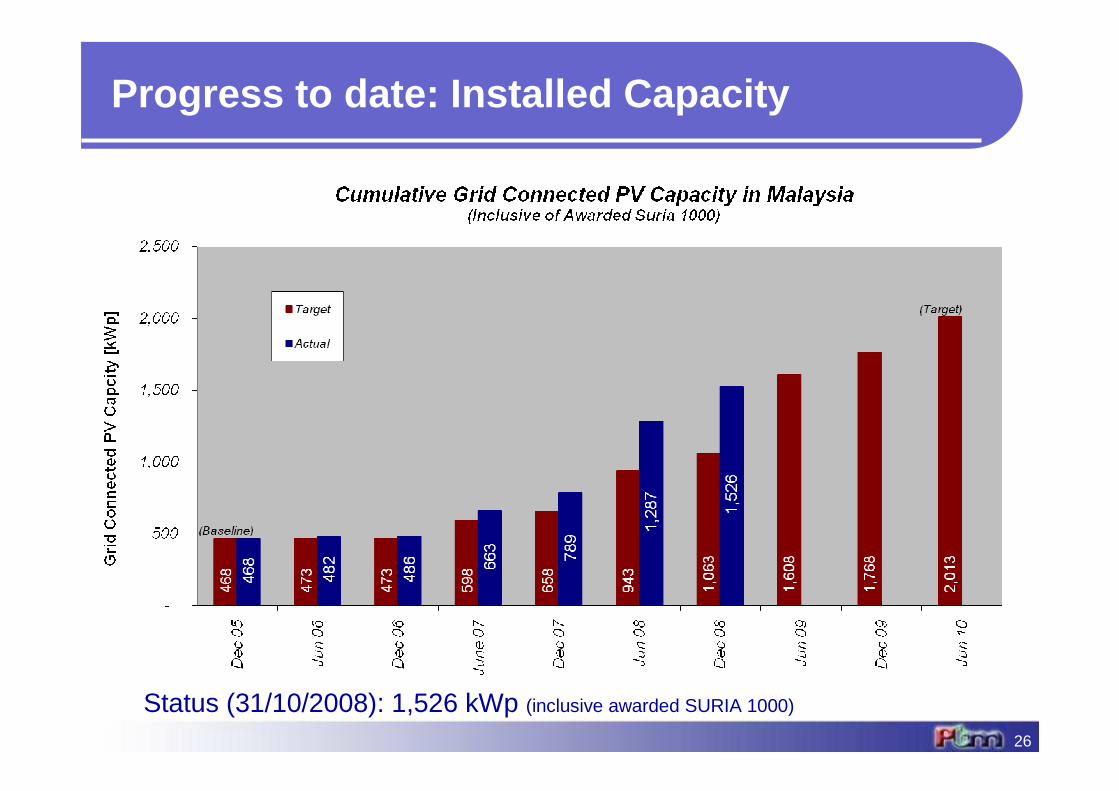

Status (31/10/2008): 1,526 kWp (inclusive awarded SURIA 1000)

Progress to date: Installed Capacity

26

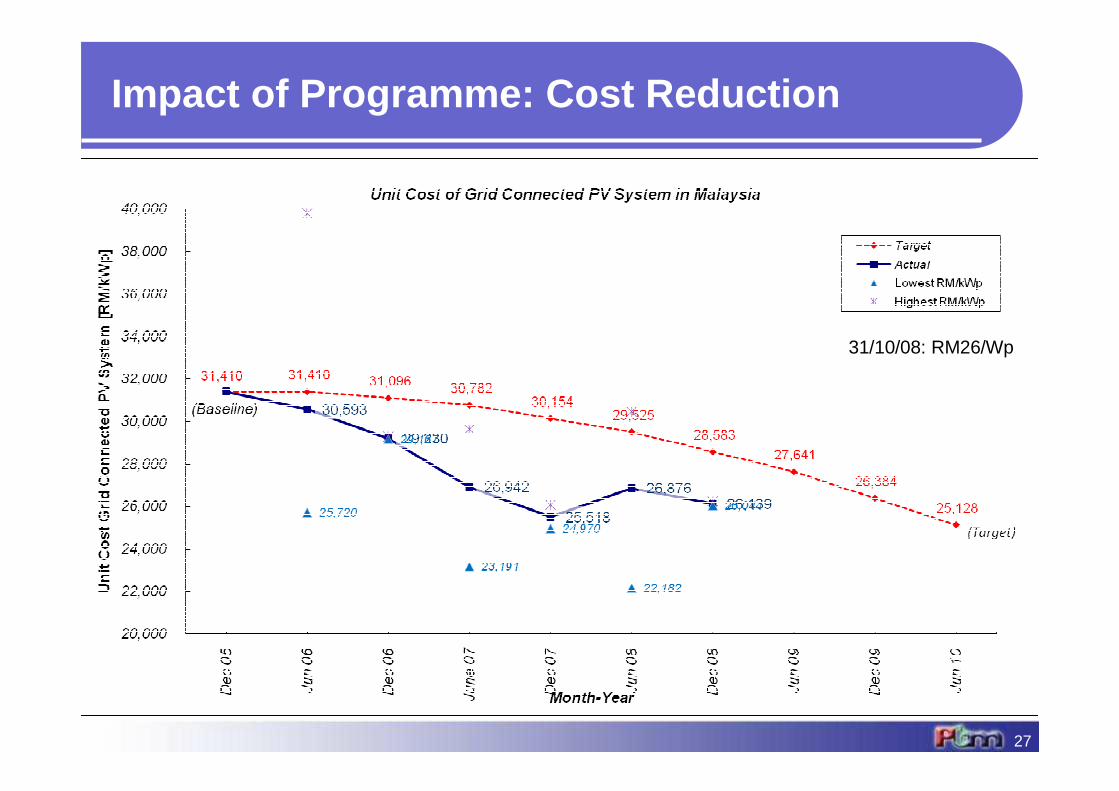

31/10/08: RM26/Wp

Impact of Programme: Cost Reduction

27

28

� ISP accredited training

� 10 days: theory, practical, exam

Competency Training

Quality Standards

29

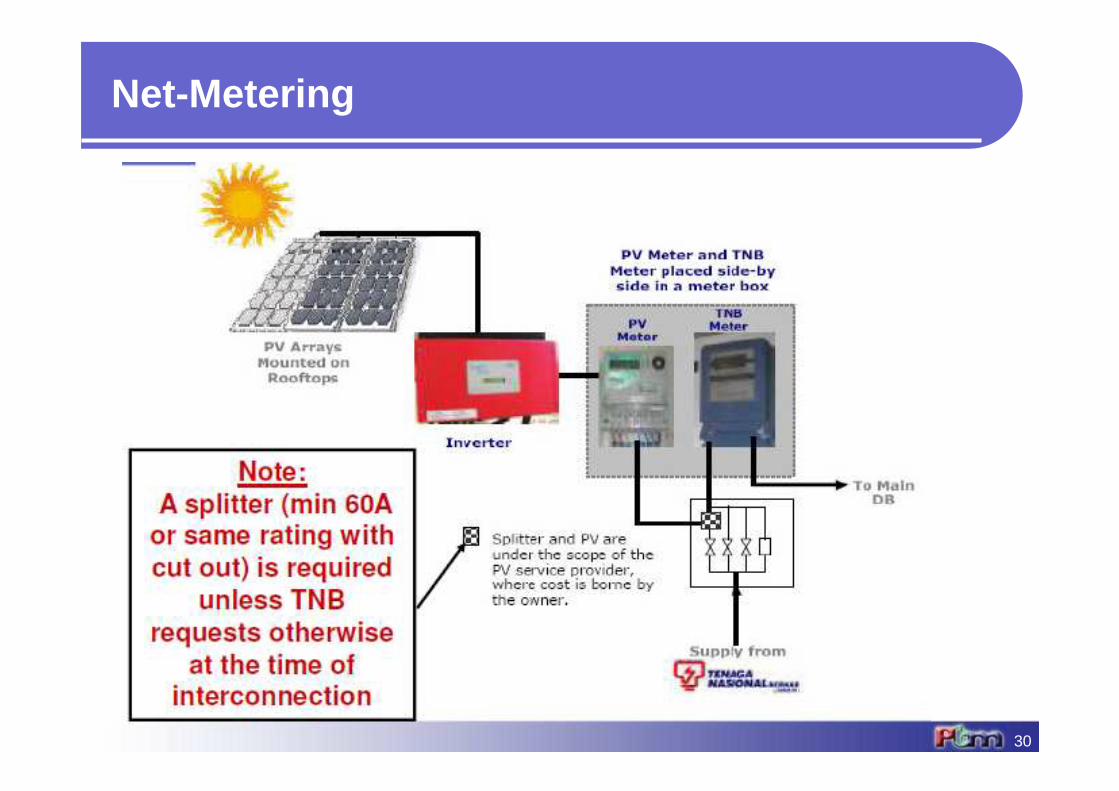

Net-Metering

30

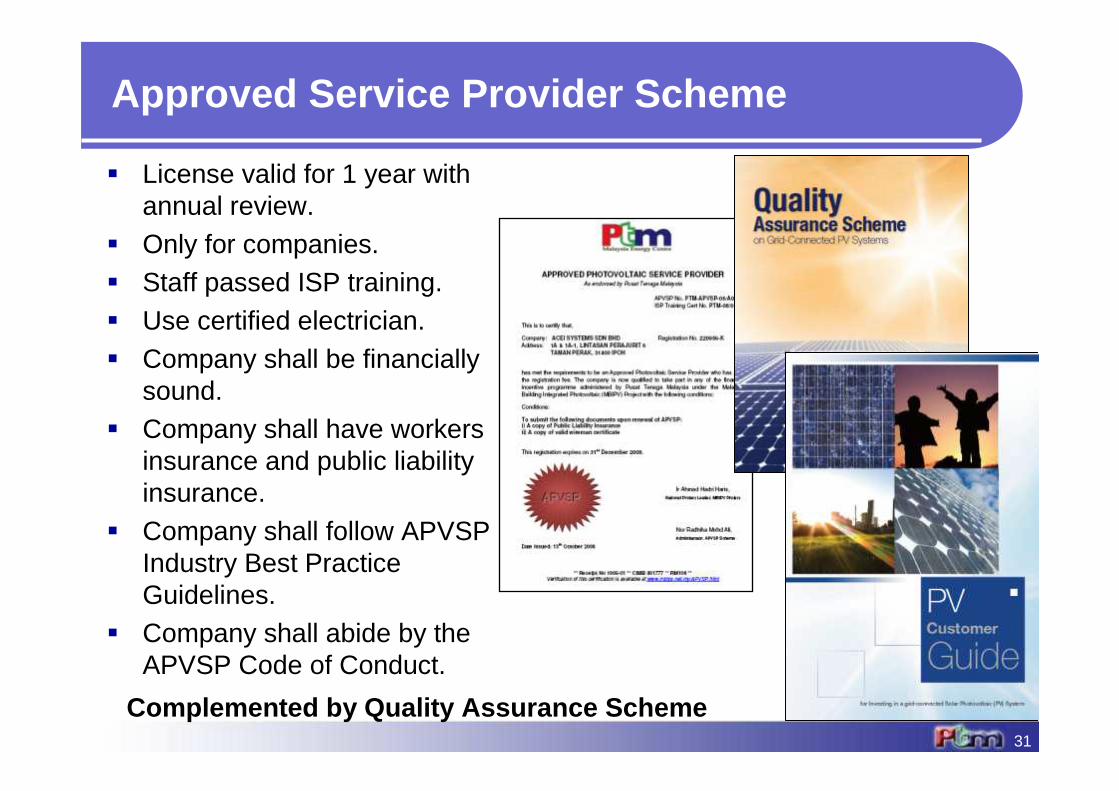

Approved Service Provider Scheme

� License valid for 1 year with annual review.

� Only for companies.� Staff passed ISP training.� Use certified electrician.� Company shall be financially

sound.� Company shall have workers

insurance and public liability insurance.

� Company shall follow APVSP Industry Best Practice Guidelines.

� Company shall abide by the APVSP Code of Conduct.

31

Complemented by Quality Assurance Scheme

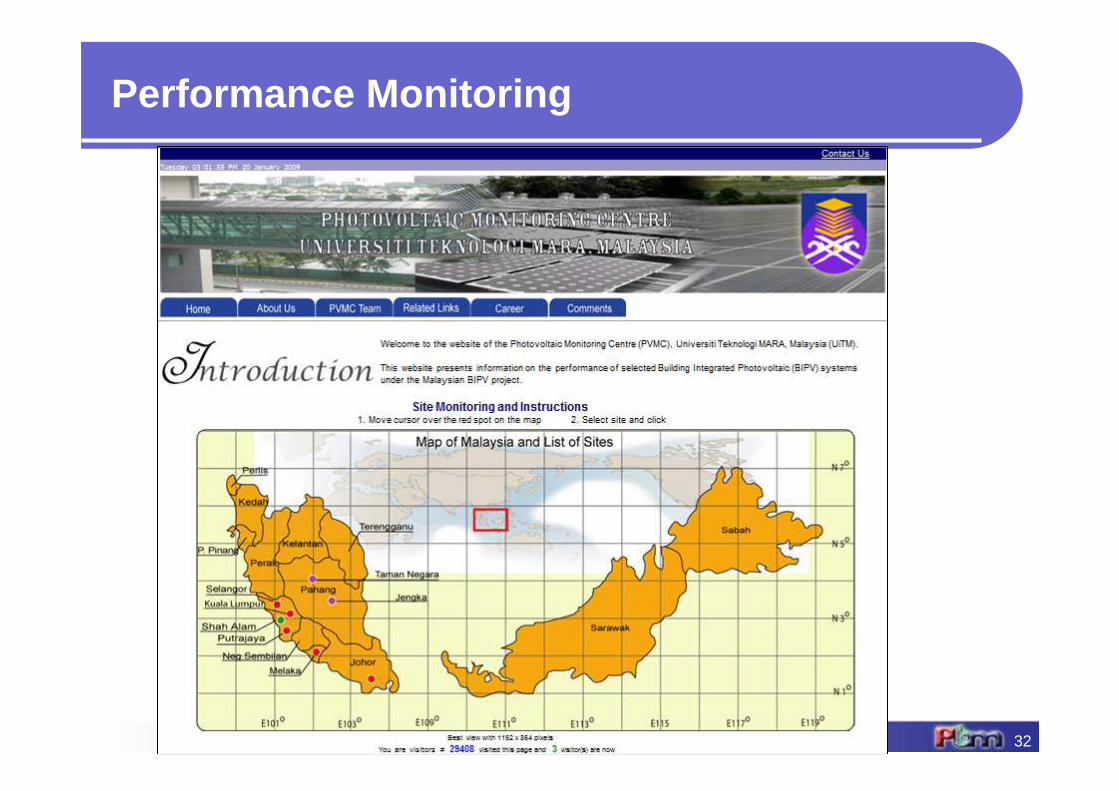

Performance Monitoring

32

First Solar

Q-Cells

Tokuyama

Renesola

Sunpower

PV Manufacturing

33

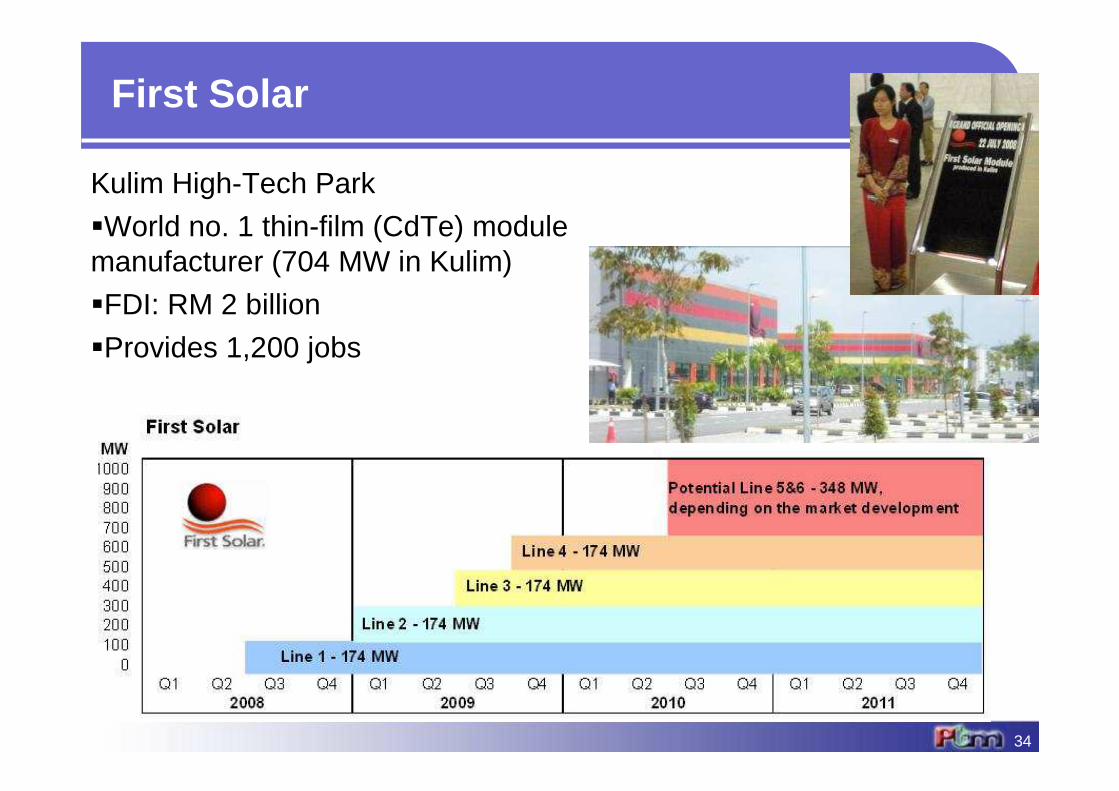

First Solar

34

Kulim High-Tech Park

�World no. 1 thin-film (CdTe) module manufacturer (704 MW in Kulim)

�FDI: RM 2 billion

�Provides 1,200 jobs

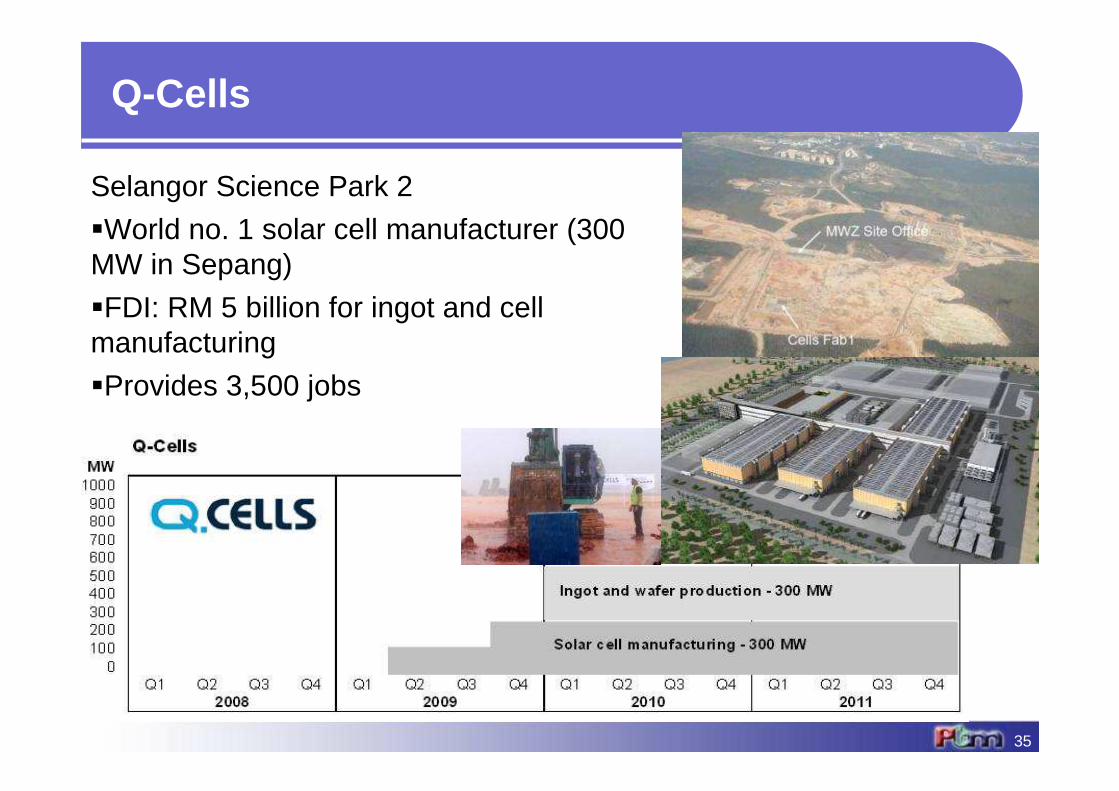

Selangor Science Park 2

�World no. 1 solar cell manufacturer (300 MW in Sepang)

�FDI: RM 5 billion for ingot and cell manufacturing

�Provides 3,500 jobs

Q-Cells

35

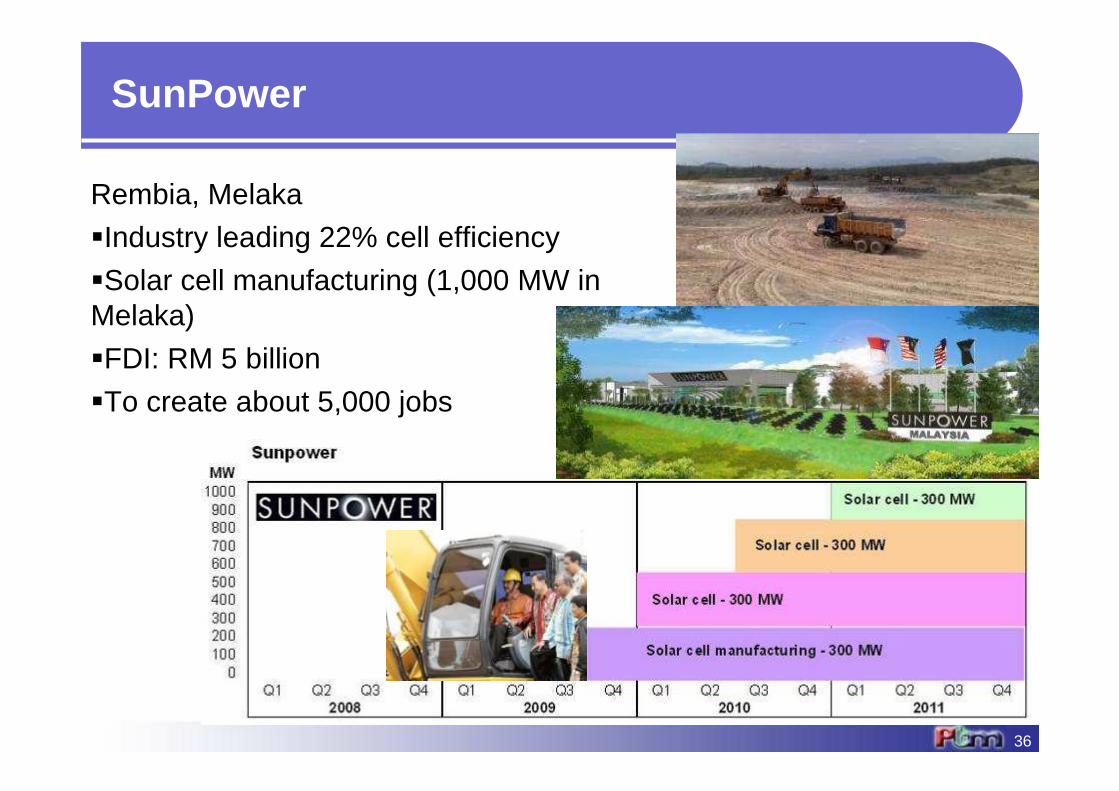

Rembia, Melaka

�Industry leading 22% cell efficiency

�Solar cell manufacturing (1,000 MW in Melaka)

�FDI: RM 5 billion

�To create about 5,000 jobs

SunPower

36

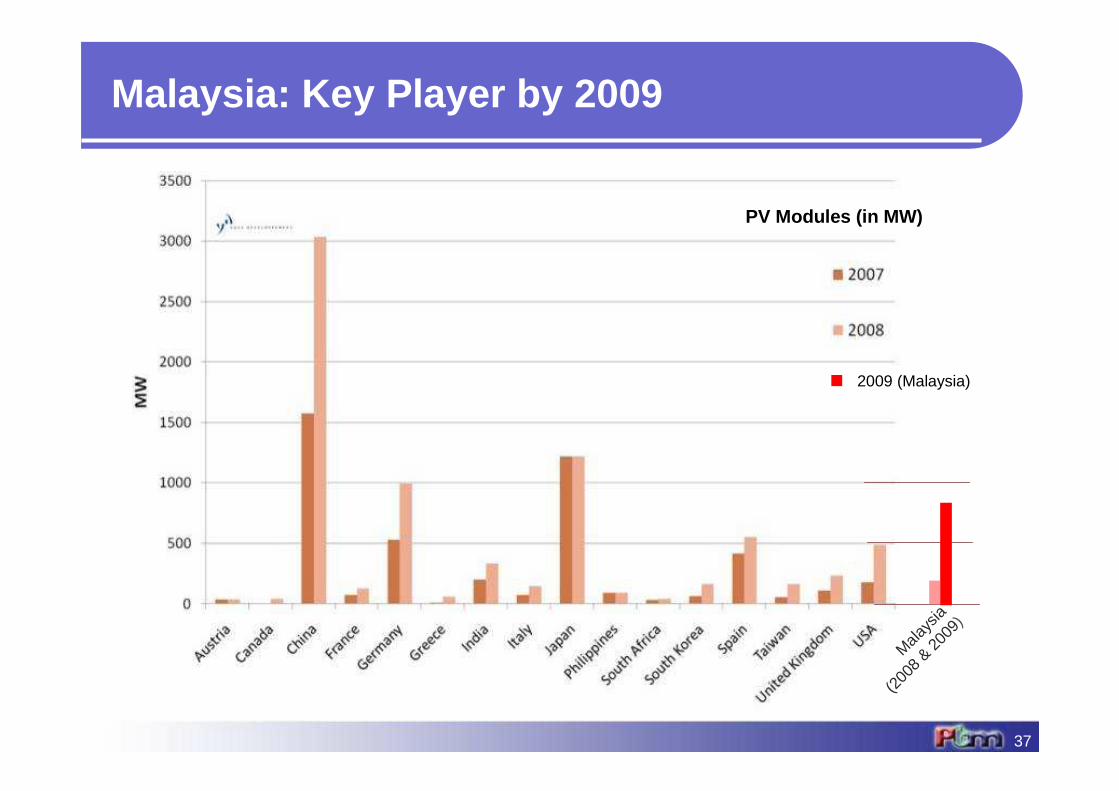

Malaysia: Key Player by 2009

37

Mala

ysia

(200

8 & 20

09)

PV Modules (in MW)

2009 (Malaysia)

Oct 2008: Malaysia joins IEA PVPS

38

Malaysia has been an active observer since 2004. Effective 22 Oct 2008, Malaysia became a full member of IEA PVPS.Malaysia’s representative at Executive Committee:1. Main: Pn Badriyah Abdul Malek, Undersecretary, Sustainable Energy

Development Division, MEWC2. Alternate: Ir Ahmad Hadri Haris, National Project Leader, MBIPV

Project, PTM

Malaysia participantion in IEA-PVPS:� Task 1: PTM� Task 10: PTM� Task 11: UiTM� Task 13 (Task 2): UiTM, UTM

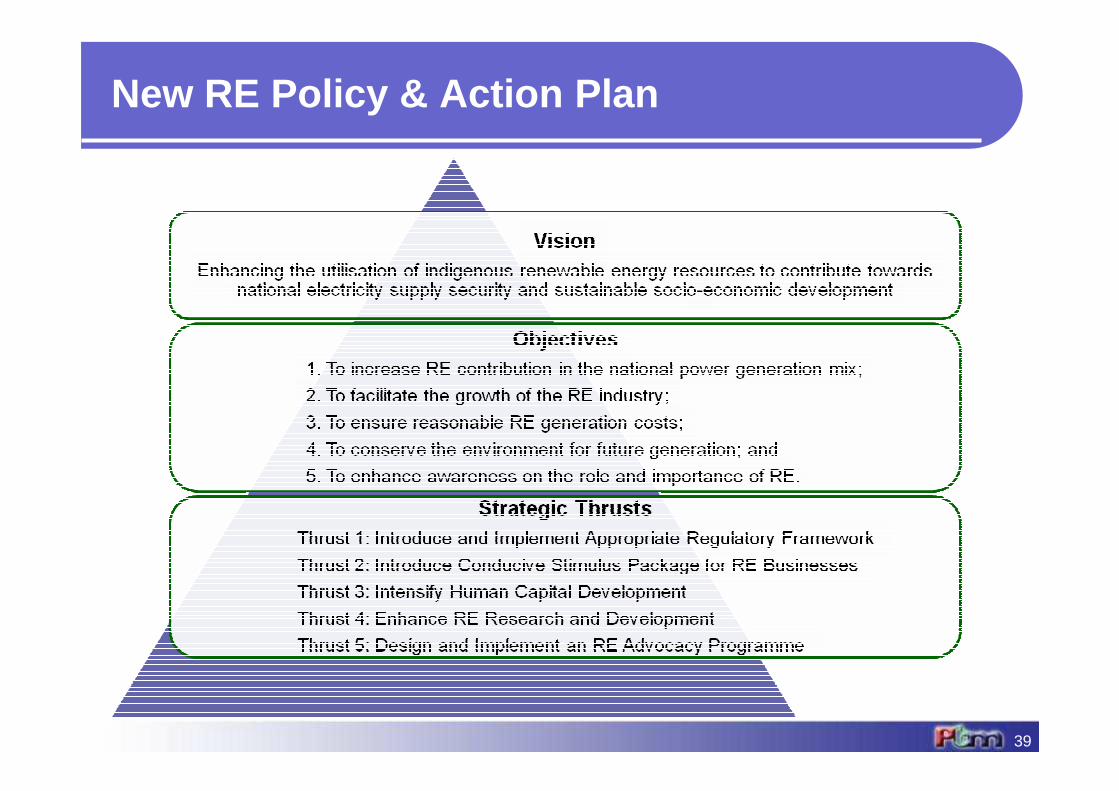

New RE Policy & Action Plan

39

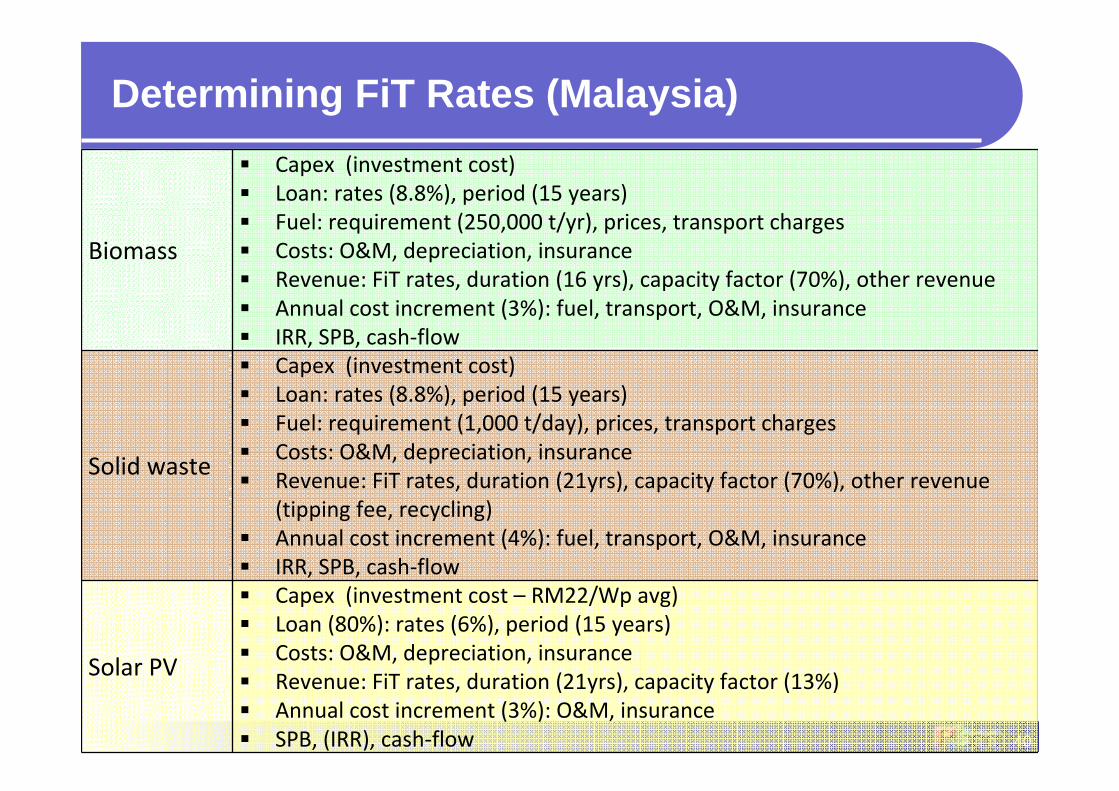

Determining FiT Rates (Malaysia)

40

Biomass

� Capex (investment cost)

� Loan: rates (8.8%), period (15 years)

� Fuel: requirement (250,000 t/yr), prices, transport charges

� Costs: O&M, depreciation, insurance

� Revenue: FiT rates, duration (16 yrs), capacity factor (70%), other revenue

� Annual cost increment (3%): fuel, transport, O&M, insurance

� IRR, SPB, cash-flow

Solid waste

� Capex (investment cost)

� Loan: rates (8.8%), period (15 years)

� Fuel: requirement (1,000 t/day), prices, transport charges

� Costs: O&M, depreciation, insurance

� Revenue: FiT rates, duration (21yrs), capacity factor (70%), other revenue

(tipping fee, recycling)

� Annual cost increment (4%): fuel, transport, O&M, insurance

� IRR, SPB, cash-flow

Solar PV

� Capex (investment cost – RM22/Wp avg)

� Loan (80%): rates (6%), period (15 years)

� Costs: O&M, depreciation, insurance

� Revenue: FiT rates, duration (21yrs), capacity factor (13%)

� Annual cost increment (3%): O&M, insurance

� SPB, (IRR), cash-flow

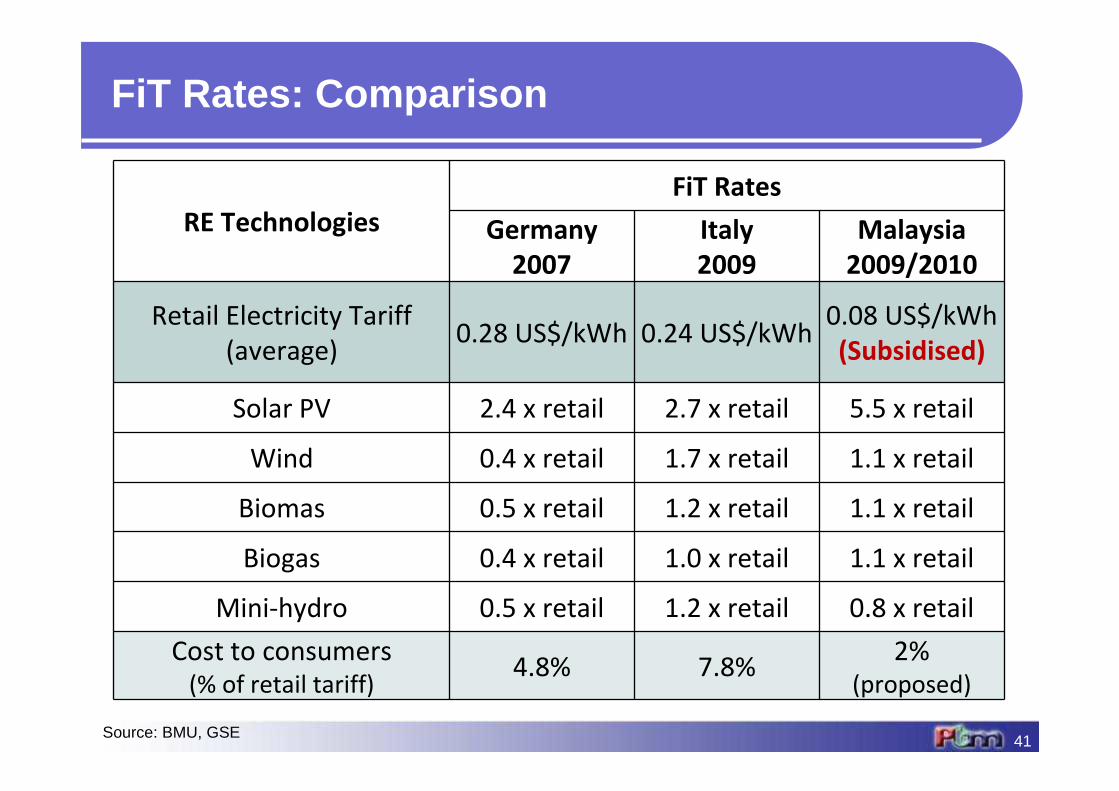

FiT Rates: Comparison

41

RE Technologies

FiT Rates

Germany

2007

Italy

2009

Malaysia

2009/2010

Retail Electricity Tariff

(average)0.28 US$/kWh 0.24 US$/kWh

0.08 US$/kWh

(Subsidised)

Solar PV 2.4 x retail 2.7 x retail 5.5 x retail

Wind 0.4 x retail 1.7 x retail 1.1 x retail

Biomas 0.5 x retail 1.2 x retail 1.1 x retail

Biogas 0.4 x retail 1.0 x retail 1.1 x retail

Mini-hydro 0.5 x retail 1.2 x retail 0.8 x retail

Cost to consumers(% of retail tariff)

4.8% 7.8%2%

(proposed)

Source: BMU, GSE

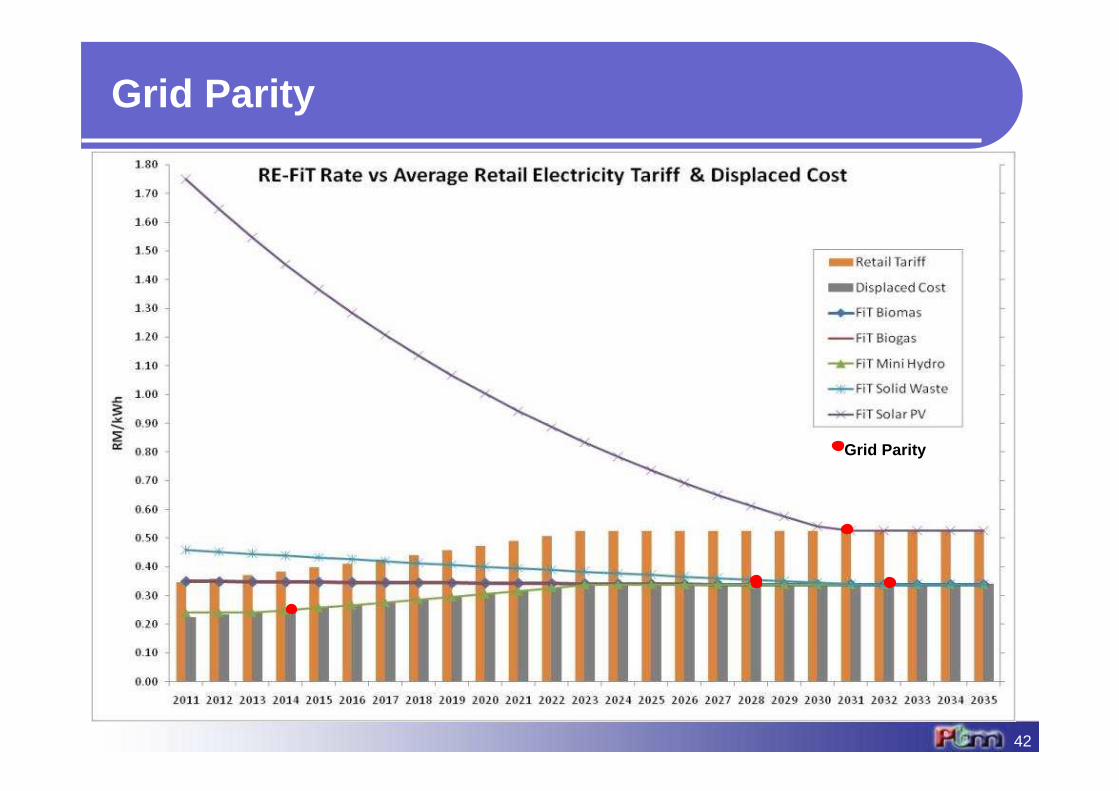

Grid Parity

42

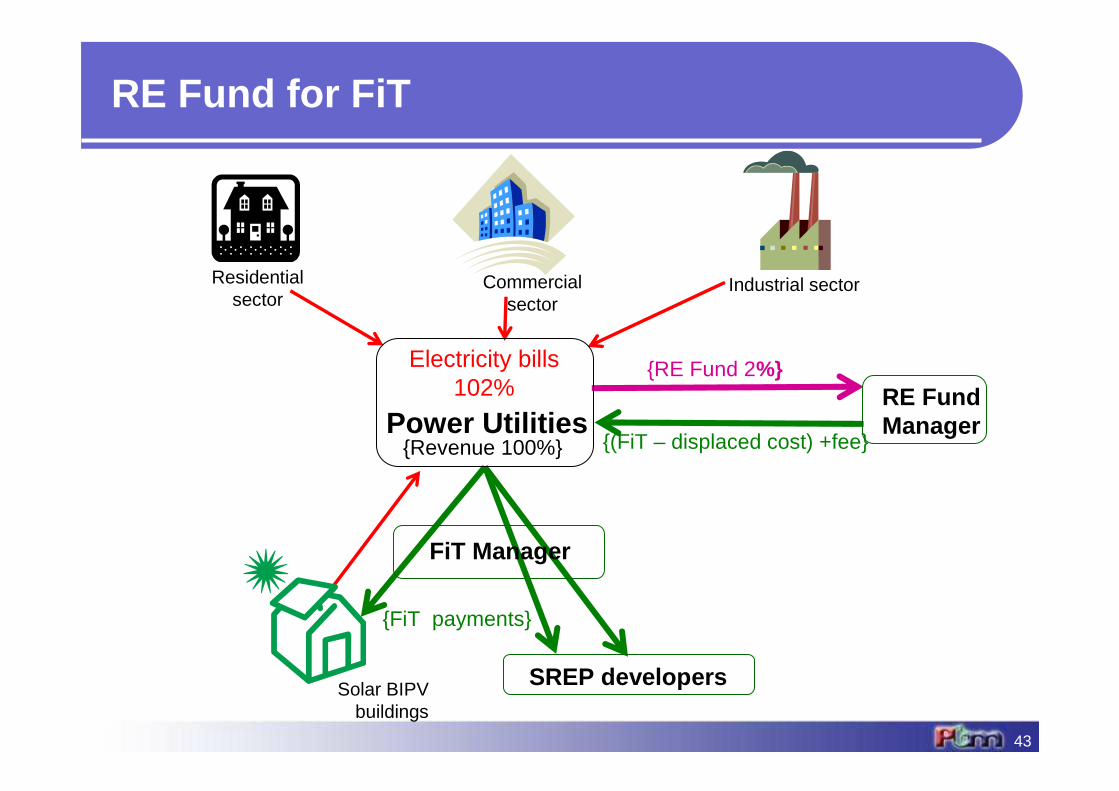

Grid Parity

{RE Fund 2%}

Residential sector

Electricity bills 102%

Solar BIPV buildings

Commercial sector

{FiT payments}

{(FiT – displaced cost) +fee}

Industrial sector

Power UtilitiesRE Fund Manager

FiT Manager

SREP developers

{Revenue 100%}

RE Fund for FiT

43

-

200

400

600

800

1,000

1,200

1,400

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

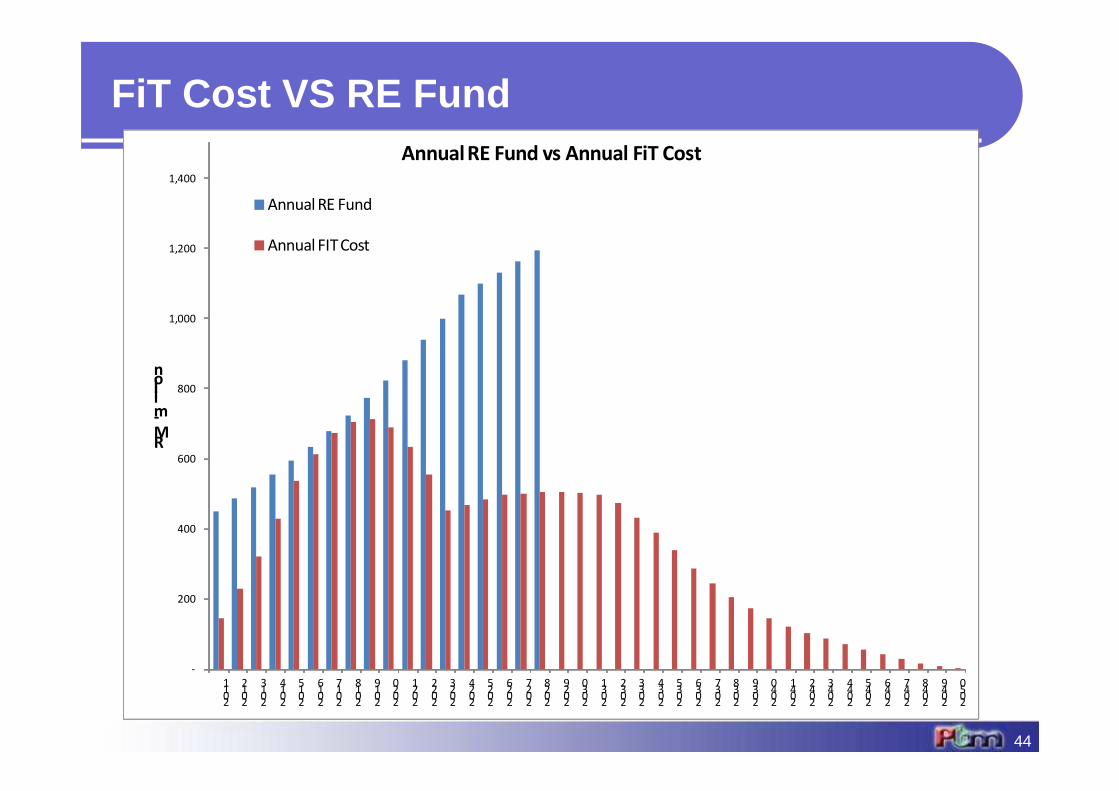

RM-million

Annual RE Fund vs Annual FiT Cost

Annual RE Fund

Annual FIT Cost

FiT Cost VS RE Fund

44

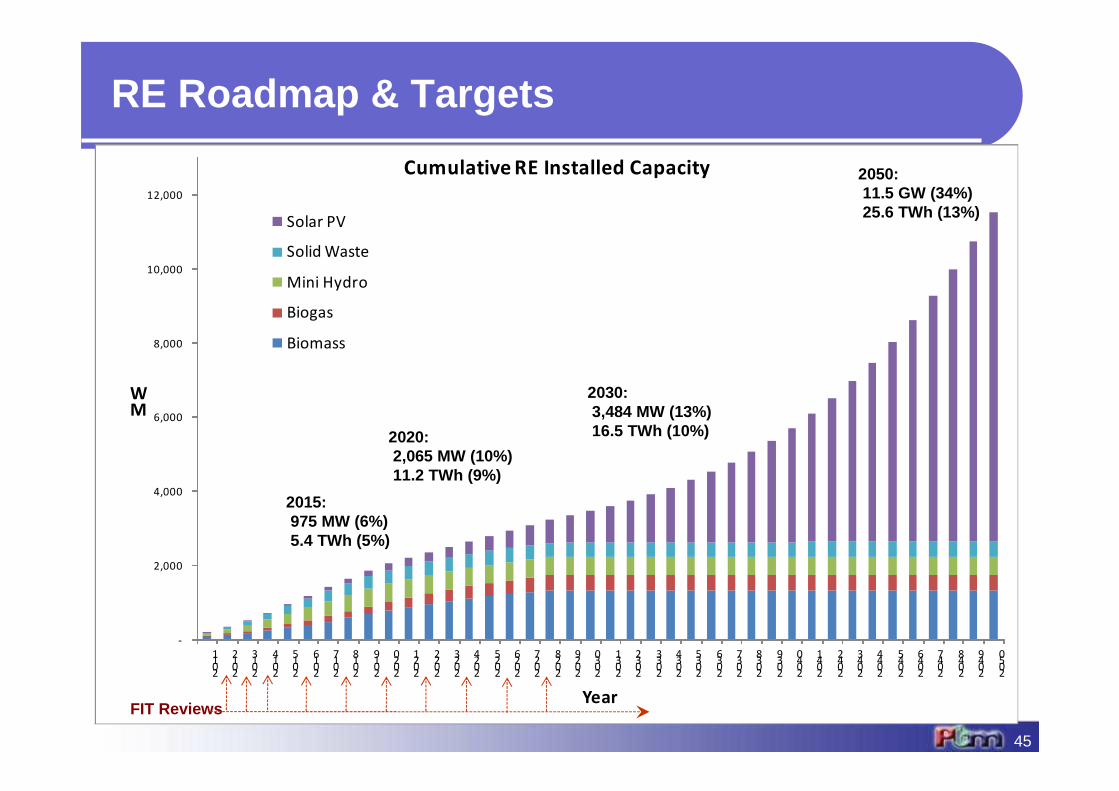

RE Roadmap & Targets

45

-

2,000

4,000

6,000

8,000

10,000

12,000

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

MW

Year

Cumulative RE Installed Capacity

Solar PV

Solid Waste

Mini Hydro

Biogas

Biomass

2020:2,065 MW (10%)11.2 TWh (9%)

2030:3,484 MW (13%)16.5 TWh (10%)

2050:11.5 GW (34%)25.6 TWh (13%)

2015:975 MW (6%)5.4 TWh (5%)

FIT Reviews

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

50,000,000

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

MWh

Year

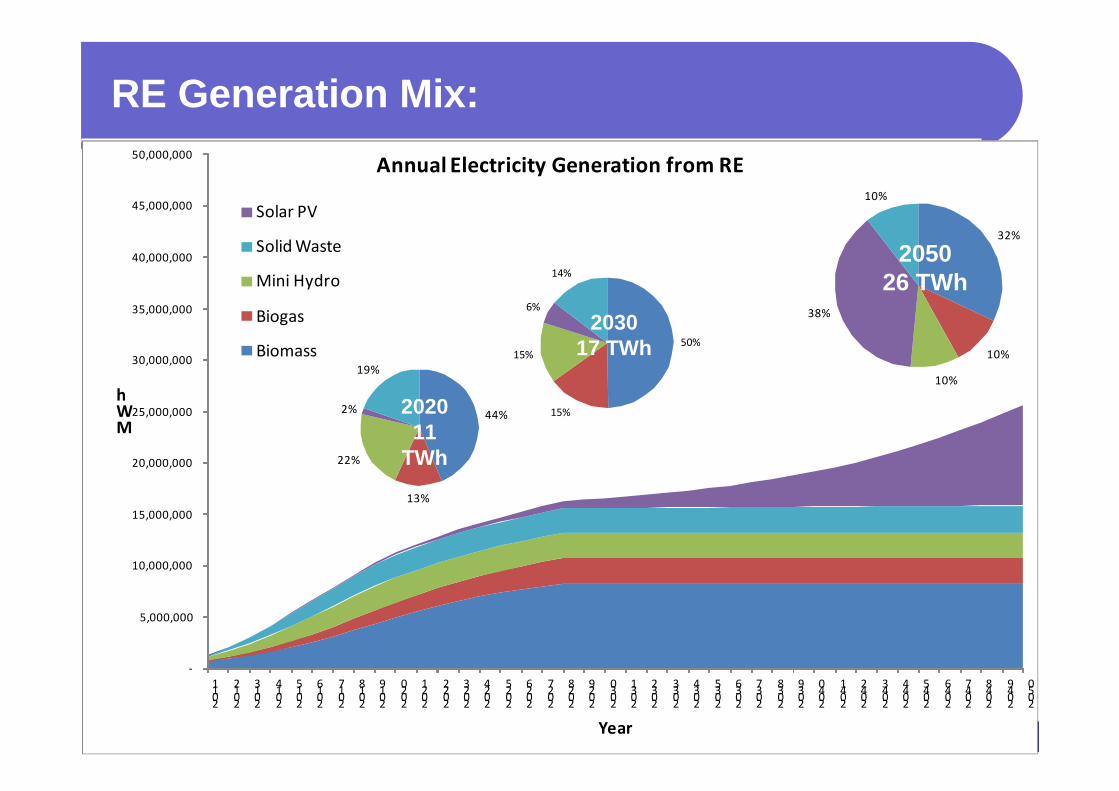

Annual Electricity Generation from RE

Solar PV

Solid Waste

Mini Hydro

Biogas

Biomass50%

15%

15%

6%

14%

32%

10%

10%

38%

10%

44%

13%

22%

2%

19%

203017 TWh

2050 26 TWh

202011

TWh

RE Generation Mix:

46

MBIPV ProjectPusat Tenaga Malaysia

No.2 Jalan 9/10, Persiaran Usahawan, Seksyen 943650 Bandar Baru Bangi, Malaysia

P: +603 8921 0865 F: +603 8921 0911 E: [email protected]

www.mbipv.net.my

Thank you

47

![S REPORT MALAYSIA [] 2019.pdf · ers with the new skills re-quired by a another gen-eration of businesses. Starting off as a semi-conductor manufacturer in the mid-1990s, when Malaysia:](https://img.pdfslide.us/doc/110x75/5fd754ae6ce50878b92bde29/s-report-malaysia-2019pdf-ers-with-the-new-skills-re-quired-by-a-another.jpg)

![PP v. AZILAH HADRI & ORS - Malaysian Law · PDF filePP v. AZILAH HADRI & ORS High Court Malaya, Shah Alam Mohd Zaki Yasin J ... 3 MLJ 516 (refd) Chan Chwen Kong v. PP [1962] MLJ 307](https://img.pdfslide.us/doc/110x75/5a78ee767f8b9a43758b54be/pp-v-azilah-hadri-ors-malaysian-law-v-azilah-hadri-ors-high-court-malaya-shah.jpg)