Embed Size (px)

Citation preview

04 Statement of Management’s Responsibility for Financial Statements

05 Independent Auditor’s Report

07 Statements of Financial Position

08 Statements of Income

10 Statements of Comprehensive Income

11 Statements of Changes in Equity

15 Statements of Cash Flows

17 Notes to Financial Statements

Financial Statements and Independent Auditor’s ReportYears Ended December 31, 2009 and 2008

Philippine Veterans Bank and Subsidiaries

4

Statement of Management Responsibility for Financial Statements

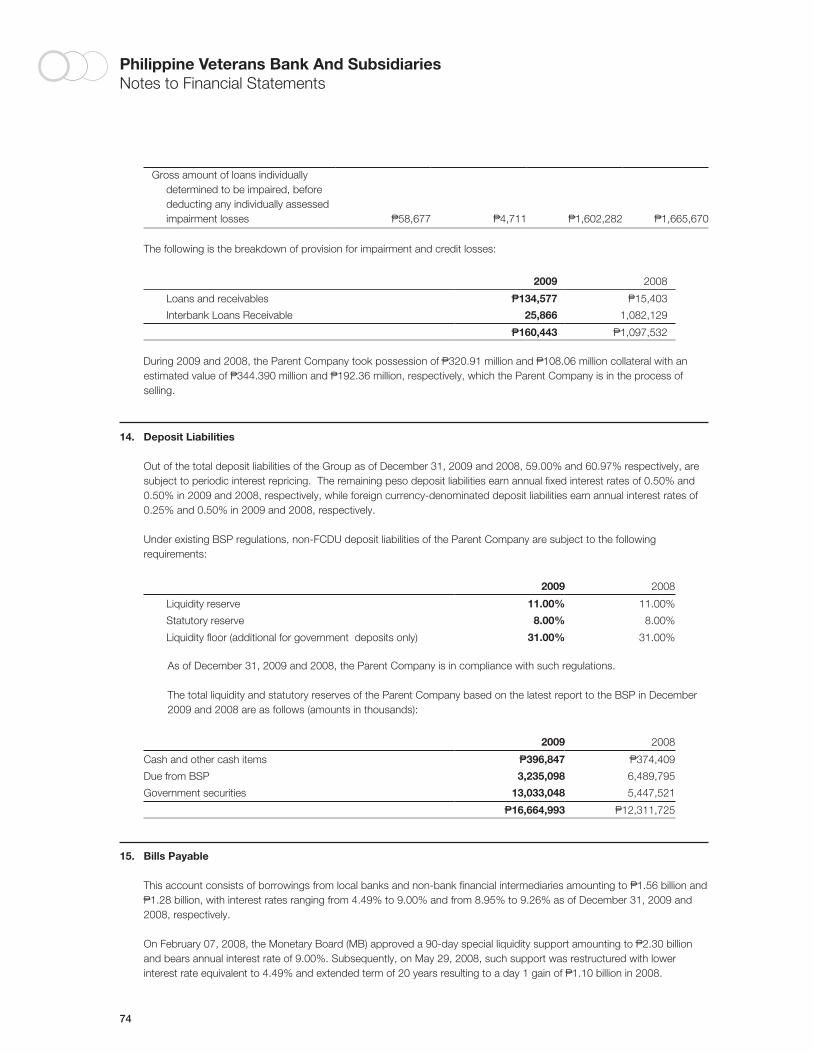

The management of Philippine Veterans Bank (the Bank) is responsible for all information and representations contained in the consolidated and parent company financial statements as of December 31, 2009 and 2008 and for the schedules referred therein as of December 31, 2009. The consolidated and parent company financial statements have been prepared in conformity with generally accounting principles in the Philippines and reflect amounts that are based on the best estimates and informed judgment of management with appropriate consideration to materiality.

In this regard, management maintains a system of accounting and reporting which provides for the necessary internal controls to ensure that transactions are properly authorized and recorded, assets are safeguarded against unauthorized use or disposition and liabilities are recognized. The management likewise discloses to the Company’s Audit Committee and to its external auditor: (i) all significant deficiencies in the design or operation of internal controls that could adversely affect its ability to record, process and report financial data; (ii) material weaknesses in internal controls; and (iii) any fraud that involves management or other employees who exercise significant roles in internal controls.

The Board of Directors reviews the consolidated and parent company financial statements before such statements are approved and submitted to the stockholders of the Bank.

SyCip Gorres Velayo & Co., the independent auditors appointed by the stockholders, have examined the consolidated and parent company financial statements in accordance with generally accepted audting standards in the Philippines and have expressed its opinion on the fairness of presentation upon completion of such examination, in its report to the Board of Directors and stockholders.

EMMANUEL V. DE OCAMPO Chairman

RICARDO A. BALBIDO, JR.President & Chief Executive Officer

TERESITA E. LOGARTASenior Vice-PresidentComptroller

Independent Auditors Report

5

The Stockholders and the Board of DirectorsPhilippine Veterans Bank

We have audited the accompanying financial statements of Philippine Veterans Bank and Subsidiaries (the Group) and of Philippine Veterans Bank (the Parent Company), which comprise the consolidated and the parent company statements of financial position as at December 31, 2009 and 2008, and the consolidated and parent company statements of income, the consolidated and the parent company statements of comprehensive income, the consolidated and the parent company statements of changes in equity and the consolidated and the parent company statements of cash flows for the years then ended, and a summary of significant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements in accordance with Philippine Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Philippine Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

6

Independent Auditors Report

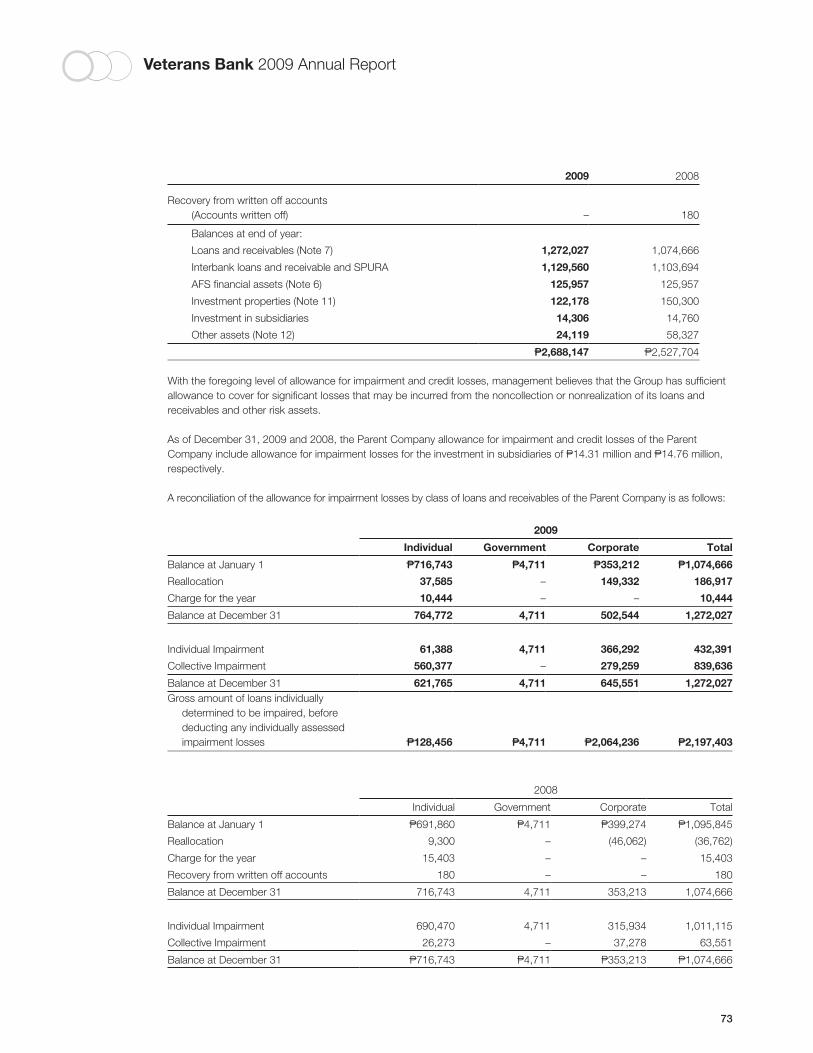

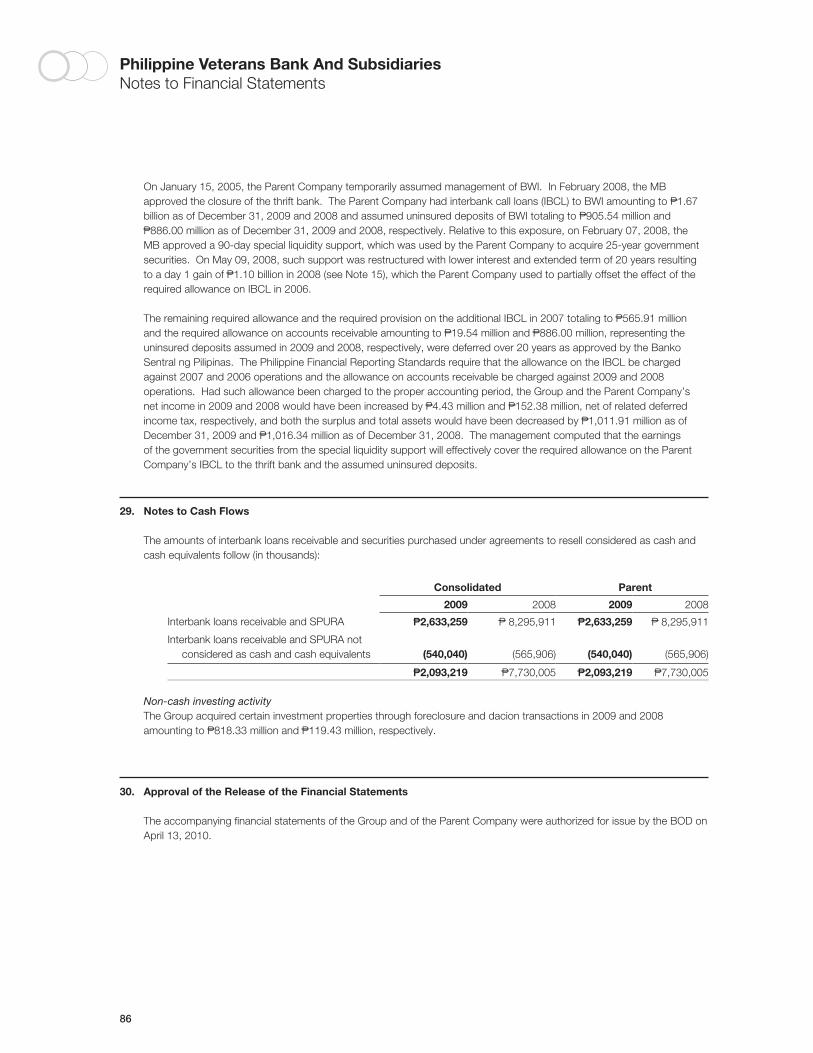

OpinionAs discussed in Note 28 to the financial statements, in 2008, the Parent Company recognized P1,103.69 million of the required allowance for probable losses on Interbank call loans (IBCL) to a thrift bank of P1,138.60 million in 2006. The remaining required allowance and the required provision on the additional IBCL in 2007 totaling to P565.91 million and the required allowance on accounts receivable amounting to P19.54 million and P886.00 million, representing the uninsured deposits assumed in 2009 and 2008, respectively, were deferred over 20 years as approved by the Banko Sentral ng Pilipinas. The Philippine Financial Reporting Standards require that the allowance on the IBCL be charged against 2007 and 2006 operations and the allowance on accounts receivable be charged against 2009 and 2008 operations. Had such allowance been charged to the proper accounting period, the Group and the Parent Company’s net income in 2009 and 2008 would have been increased by P4.43 million and P152.38 million, net of related deferred income tax, respectively, and both the surplus and total assets would have been decreased by P1,011.91 million as of December 31, 2009 and P1,016.34 million as of December 31, 2008. As further discussed in Note 28, management computed that the earnings of the government securities from the special liquidity support will effectively cover the required allowance on the Parent Company’s IBCL to the thrift bank and the assumed uninsured deposits.

As discussed in Note 7 to the financial statements, the Parent Company sold a non-performing asset (NPA) to a special purpose vehicle (SPV) company on a without recourse basis. In accordance with regulatory accounting policies prescribed by the Bangko Sentral ng Pilipinas for banks and financial institutions availing of the provisions of RA No. 9182, the Special Purpose Vehicle Act of 2002, losses amounting to P63.4 million from the sale of the NPA to the SPV company were deferred and are being amortized over a ten-year period. Had the loss from the sale of NPA been charged against current operations as required by the Philippine Financial Reporting Standards, the Group and the Parent Company’s total assets as of December 31, 2009 and net income in 2009 would have been decreased by P61.1 million.

In our opinion, except for the effects on the 2009 and 2008 consolidated and parent company financial statements of the matters discussed in the preceding paragraphs, the consolidated and the parent company financial statements present fairly, in all material respects, the financial position of the Group and of the Parent Company as of December 31, 2009 and 2008, and their financial performance and their cash flows for the years then ended in accordance with Philippine Financial Reporting Standards.

SYCIP GORRES VELAYO & CO.

Janet A. ParaisoPartnerCPA Certificate No. 92305SEC Accreditation No. 0778-ATax Identification No. 193-975-241PTR No. 2087360, January 4, 2010, Makati City

April 13, 2010

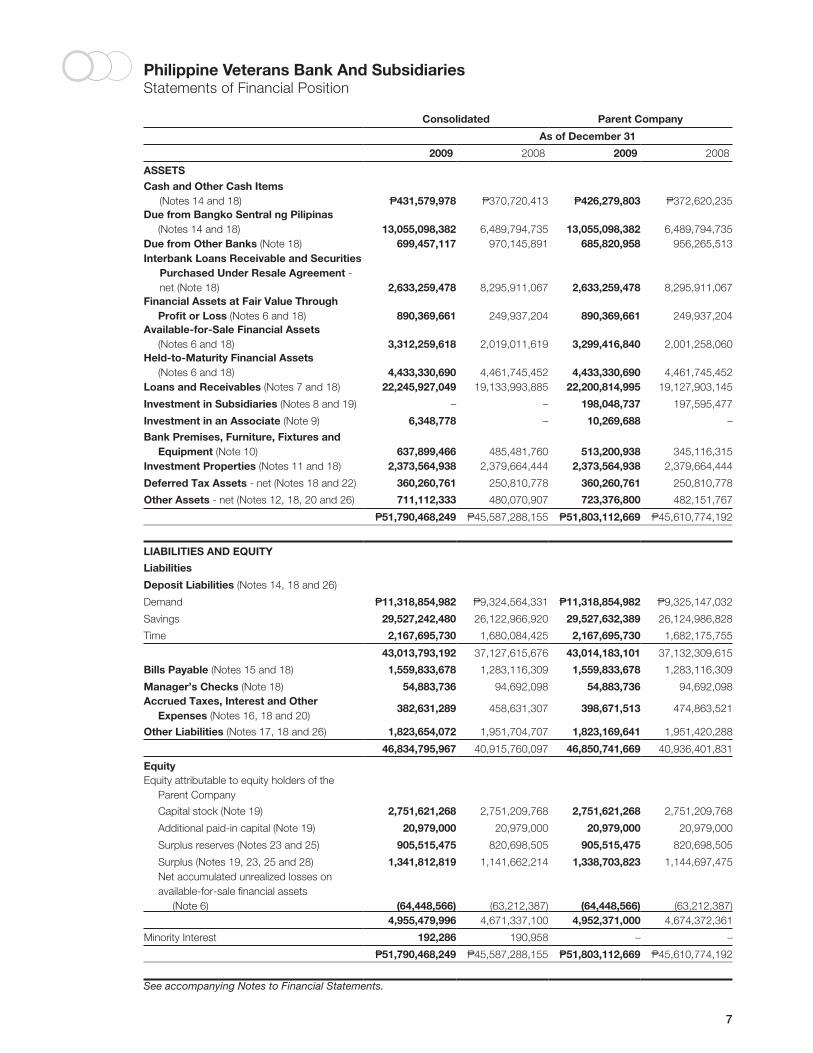

Philippine Veterans Bank And SubsidiariesStatements of Financial Position

7

Consolidated Parent Company

As of December 31

2009 2008 2009 2008

ASSETSCash and Other Cash Items

(Notes 14 and 18) P431,579,978 P370,720,413 P426,279,803 P372,620,235Due from Bangko Sentral ng Pilipinas

(Notes 14 and 18) 13,055,098,382 6,489,794,735 13,055,098,382 6,489,794,735Due from Other Banks (Note 18) 699,457,117 970,145,891 685,820,958 956,265,513Interbank Loans Receivable and Securities

Purchased Under Resale Agreement - net (Note 18) 2,633,259,478 8,295,911,067 2,633,259,478 8,295,911,067

Financial Assets at Fair Value Through Profit or Loss (Notes 6 and 18) 890,369,661 249,937,204 890,369,661 249,937,204

Available-for-Sale Financial Assets (Notes 6 and 18) 3,312,259,618 2,019,011,619 3,299,416,840 2,001,258,060

Held-to-Maturity Financial Assets (Notes 6 and 18) 4,433,330,690 4,461,745,452 4,433,330,690 4,461,745,452

Loans and Receivables (Notes 7 and 18) 22,245,927,049 19,133,993,885 22,200,814,995 19,127,903,145

Investment in Subsidiaries (Notes 8 and 19) – – 198,048,737 197,595,477

Investment in an Associate (Note 9) 6,348,778 – 10,269,688 –

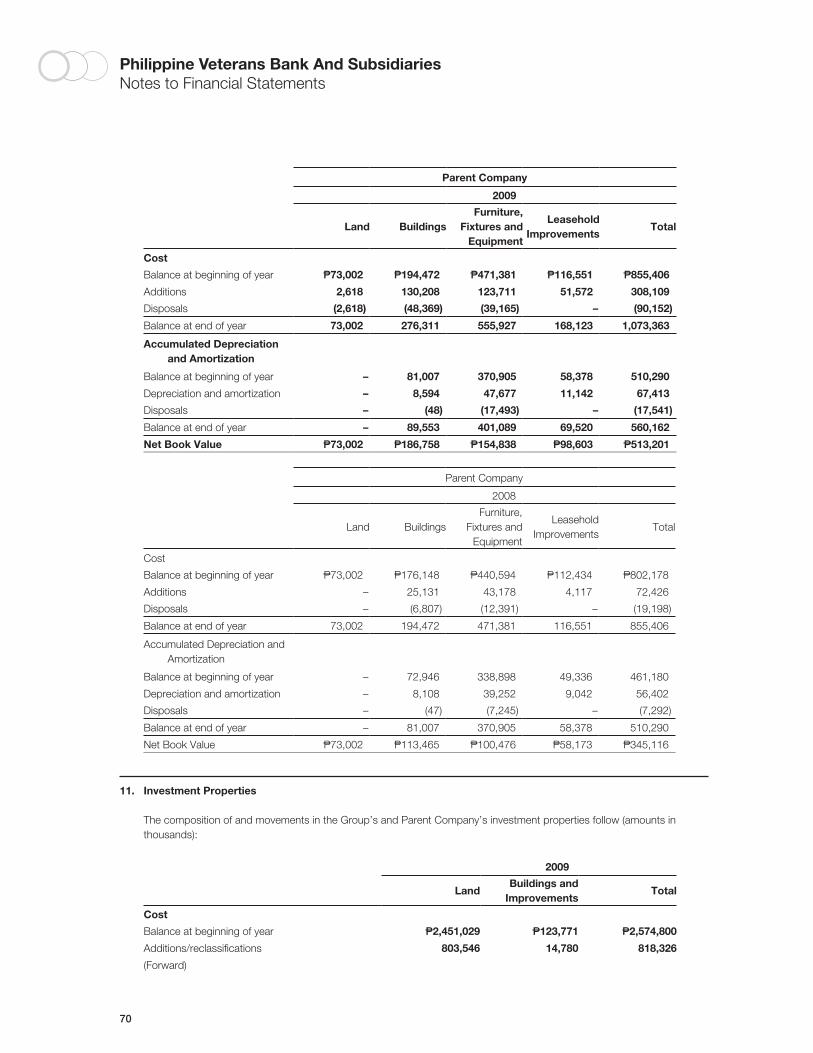

Bank Premises, Furniture, Fixtures and Equipment (Note 10) 637,899,466 485,481,760 513,200,938 345,116,315

Investment Properties (Notes 11 and 18) 2,373,564,938 2,379,664,444 2,373,564,938 2,379,664,444

Deferred Tax Assets - net (Notes 18 and 22) 360,260,761 250,810,778 360,260,761 250,810,778

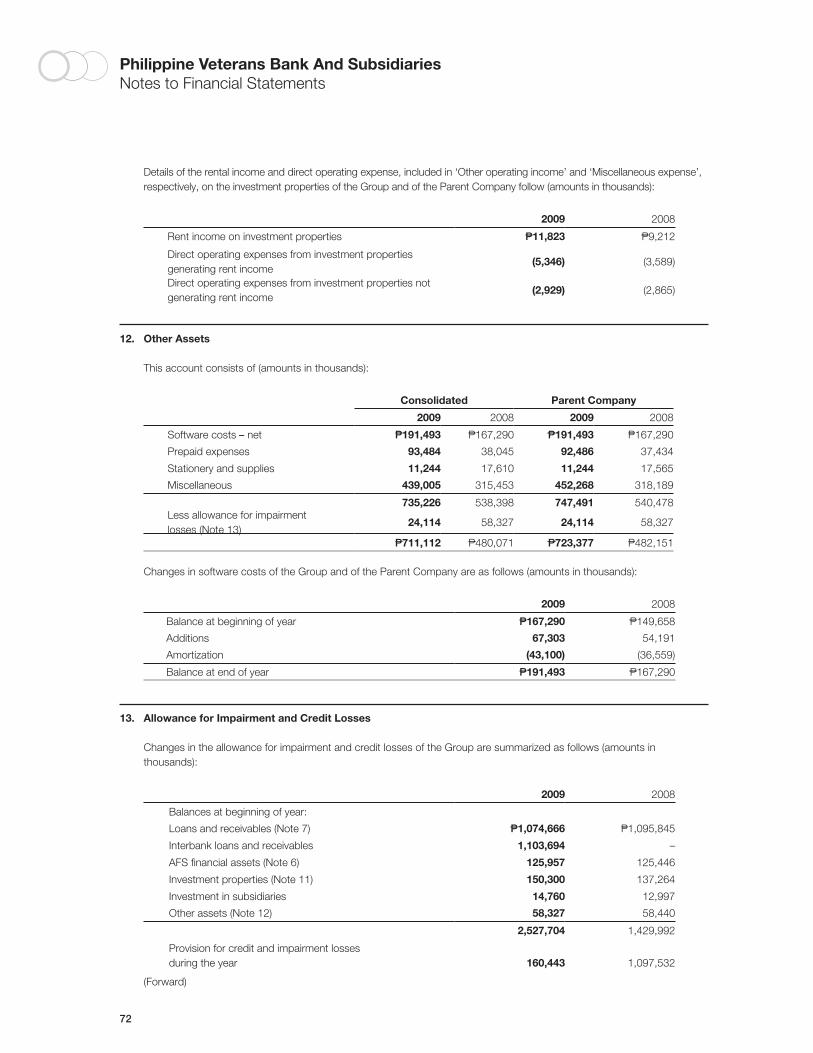

Other Assets - net (Notes 12, 18, 20 and 26) 711,112,333 480,070,907 723,376,800 482,151,767

P51,790,468,249 P45,587,288,155 P51,803,112,669 P45,610,774,192

LIABILITIES AND EQUITY

Liabilities

Deposit Liabilities (Notes 14, 18 and 26)

Demand P11,318,854,982 P9,324,564,331 P11,318,854,982 P9,325,147,032

Savings 29,527,242,480 26,122,966,920 29,527,632,389 26,124,986,828

Time 2,167,695,730 1,680,084,425 2,167,695,730 1,682,175,755

43,013,793,192 37,127,615,676 43,014,183,101 37,132,309,615

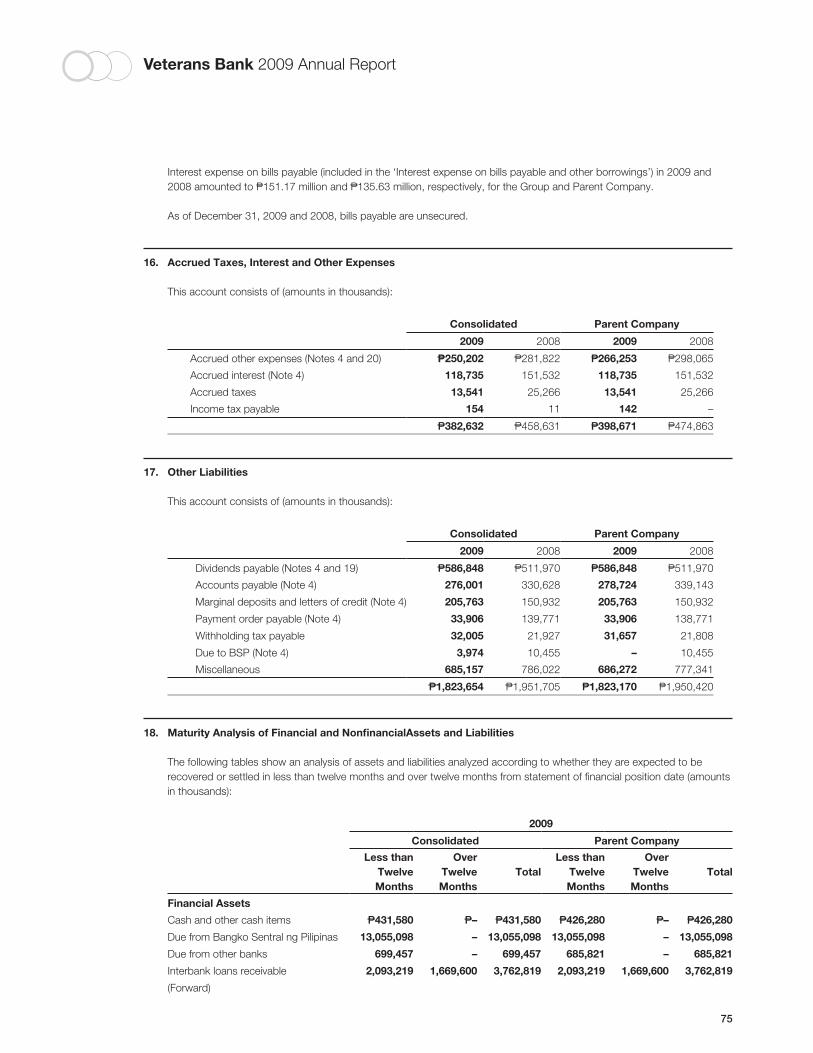

Bills Payable (Notes 15 and 18) 1,559,833,678 1,283,116,309 1,559,833,678 1,283,116,309

Manager’s Checks (Note 18) 54,883,736 94,692,098 54,883,736 94,692,098Accrued Taxes, Interest and Other

Expenses (Notes 16, 18 and 20)382,631,289 458,631,307 398,671,513 474,863,521

Other Liabilities (Notes 17, 18 and 26) 1,823,654,072 1,951,704,707 1,823,169,641 1,951,420,288

46,834,795,967 40,915,760,097 46,850,741,669 40,936,401,831

EquityEquity attributable to equity holders of the

Parent Company

Capital stock (Note 19) 2,751,621,268 2,751,209,768 2,751,621,268 2,751,209,768

Additional paid-in capital (Note 19) 20,979,000 20,979,000 20,979,000 20,979,000

Surplus reserves (Notes 23 and 25) 905,515,475 820,698,505 905,515,475 820,698,505

Surplus (Notes 19, 23, 25 and 28) 1,341,812,819 1,141,662,214 1,338,703,823 1,144,697,475 Net accumulated unrealized losses on

available-for-sale financial assets (Note 6) (64,448,566) (63,212,387) (64,448,566) (63,212,387)

4,955,479,996 4,671,337,100 4,952,371,000 4,674,372,361

Minority Interest 192,286 190,958 – –

P51,790,468,249 P45,587,288,155 P51,803,112,669 P45,610,774,192

See accompanying Notes to Financial Statements.

8

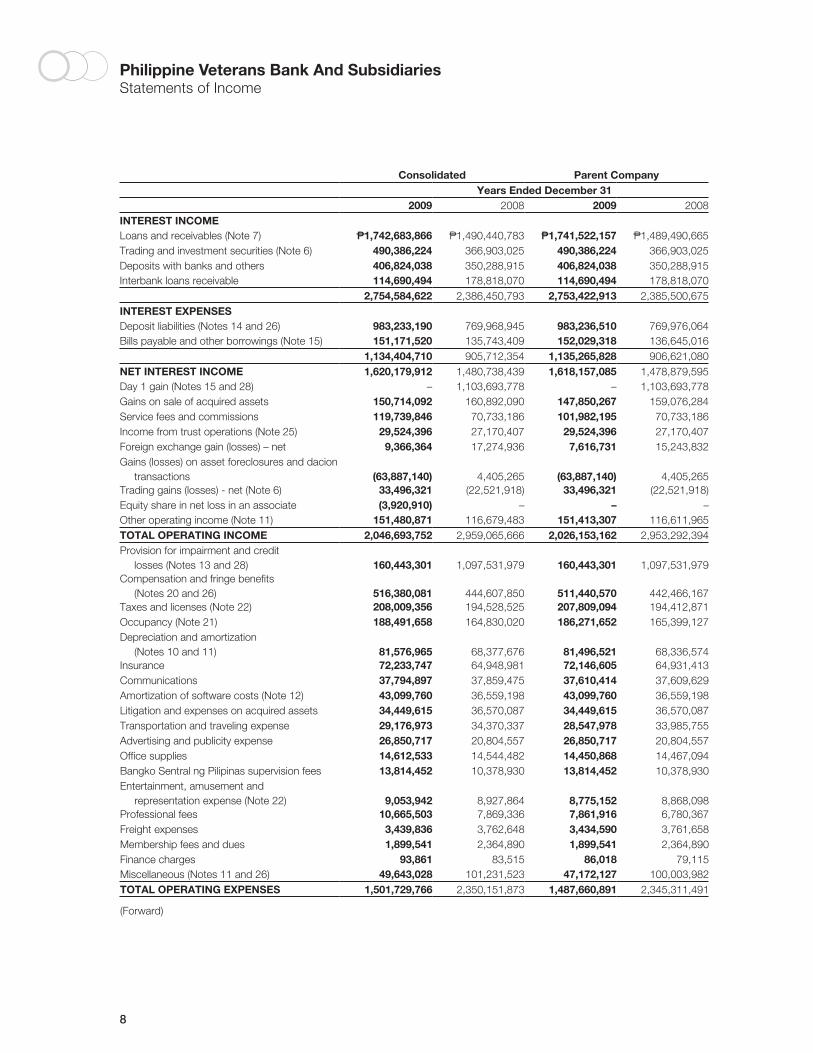

Consolidated Parent CompanyYears Ended December 31

2009 2008 2009 2008INTEREST INCOMELoans and receivables (Note 7) P1,742,683,866 P1,490,440,783 P1,741,522,157 P1,489,490,665Trading and investment securities (Note 6) 490,386,224 366,903,025 490,386,224 366,903,025Deposits with banks and others 406,824,038 350,288,915 406,824,038 350,288,915Interbank loans receivable 114,690,494 178,818,070 114,690,494 178,818,070

2,754,584,622 2,386,450,793 2,753,422,913 2,385,500,675INTEREST EXPENSESDeposit liabilities (Notes 14 and 26) 983,233,190 769,968,945 983,236,510 769,976,064Bills payable and other borrowings (Note 15) 151,171,520 135,743,409 152,029,318 136,645,016

1,134,404,710 905,712,354 1,135,265,828 906,621,080NET INTEREST INCOME 1,620,179,912 1,480,738,439 1,618,157,085 1,478,879,595Day 1 gain (Notes 15 and 28) – 1,103,693,778 – 1,103,693,778Gains on sale of acquired assets 150,714,092 160,892,090 147,850,267 159,076,284Service fees and commissions 119,739,846 70,733,186 101,982,195 70,733,186Income from trust operations (Note 25) 29,524,396 27,170,407 29,524,396 27,170,407Foreign exchange gain (losses) – net 9,366,364 17,274,936 7,616,731 15,243,832Gains (losses) on asset foreclosures and dacion

transactions (63,887,140) 4,405,265 (63,887,140) 4,405,265Trading gains (losses) - net (Note 6) 33,496,321 (22,521,918) 33,496,321 (22,521,918)Equity share in net loss in an associate (3,920,910) – – –Other operating income (Note 11) 151,480,871 116,679,483 151,413,307 116,611,965TOTAL OPERATING INCOME 2,046,693,752 2,959,065,666 2,026,153,162 2,953,292,394Provision for impairment and credit

losses (Notes 13 and 28) 160,443,301 1,097,531,979 160,443,301 1,097,531,979Compensation and fringe benefits

(Notes 20 and 26) 516,380,081 444,607,850 511,440,570 442,466,167Taxes and licenses (Note 22) 208,009,356 194,528,525 207,809,094 194,412,871Occupancy (Note 21) 188,491,658 164,830,020 186,271,652 165,399,127Depreciation and amortization

(Notes 10 and 11) 81,576,965 68,377,676 81,496,521 68,336,574Insurance 72,233,747 64,948,981 72,146,605 64,931,413Communications 37,794,897 37,859,475 37,610,414 37,609,629Amortization of software costs (Note 12) 43,099,760 36,559,198 43,099,760 36,559,198Litigation and expenses on acquired assets 34,449,615 36,570,087 34,449,615 36,570,087Transportation and traveling expense 29,176,973 34,370,337 28,547,978 33,985,755Advertising and publicity expense 26,850,717 20,804,557 26,850,717 20,804,557Office supplies 14,612,533 14,544,482 14,450,868 14,467,094Bangko Sentral ng Pilipinas supervision fees 13,814,452 10,378,930 13,814,452 10,378,930Entertainment, amusement and

representation expense (Note 22) 9,053,942 8,927,864 8,775,152 8,868,098Professional fees 10,665,503 7,869,336 7,861,916 6,780,367Freight expenses 3,439,836 3,762,648 3,434,590 3,761,658Membership fees and dues 1,899,541 2,364,890 1,899,541 2,364,890Finance charges 93,861 83,515 86,018 79,115Miscellaneous (Notes 11 and 26) 49,643,028 101,231,523 47,172,127 100,003,982TOTAL OPERATING EXPENSES 1,501,729,766 2,350,151,873 1,487,660,891 2,345,311,491

(Forward)

Philippine Veterans Bank And SubsidiariesStatements of Income

Philippine Veterans Bank And SubsidiariesStatements of Income

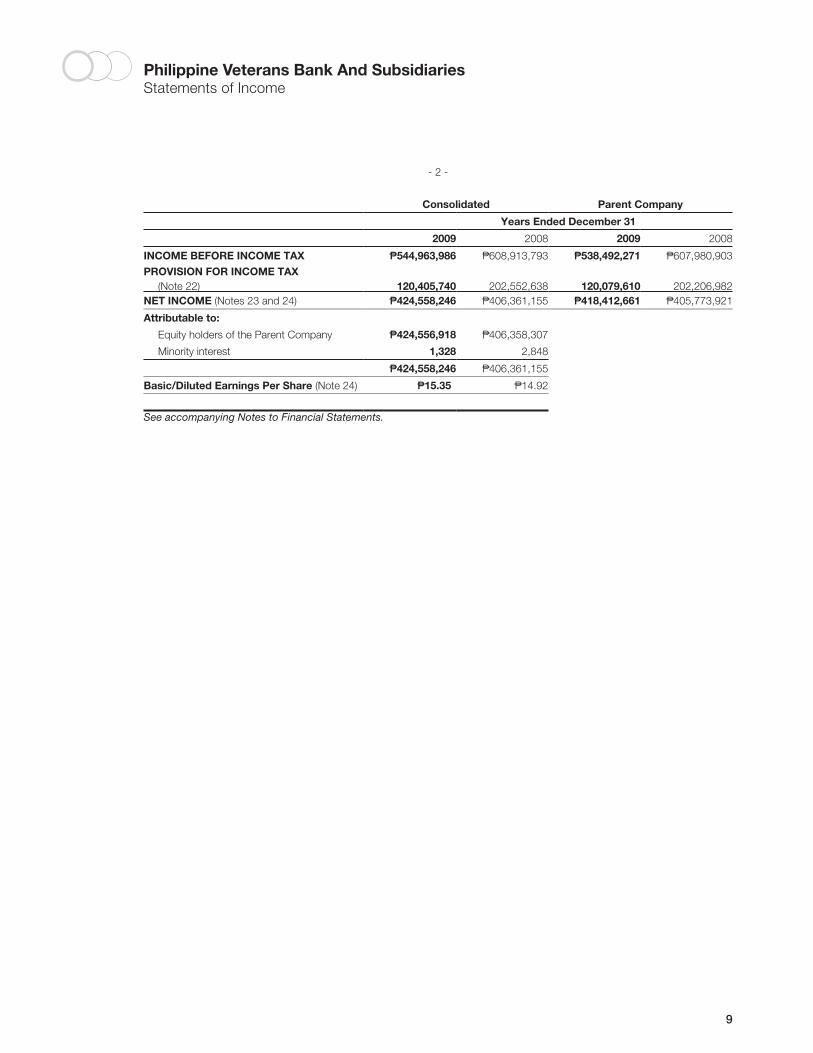

9

- 2 -

Consolidated Parent Company

Years Ended December 31

2009 2008 2009 2008

INCOME BEFORE INCOME TAX P544,963,986 P608,913,793 P538,492,271 P607,980,903

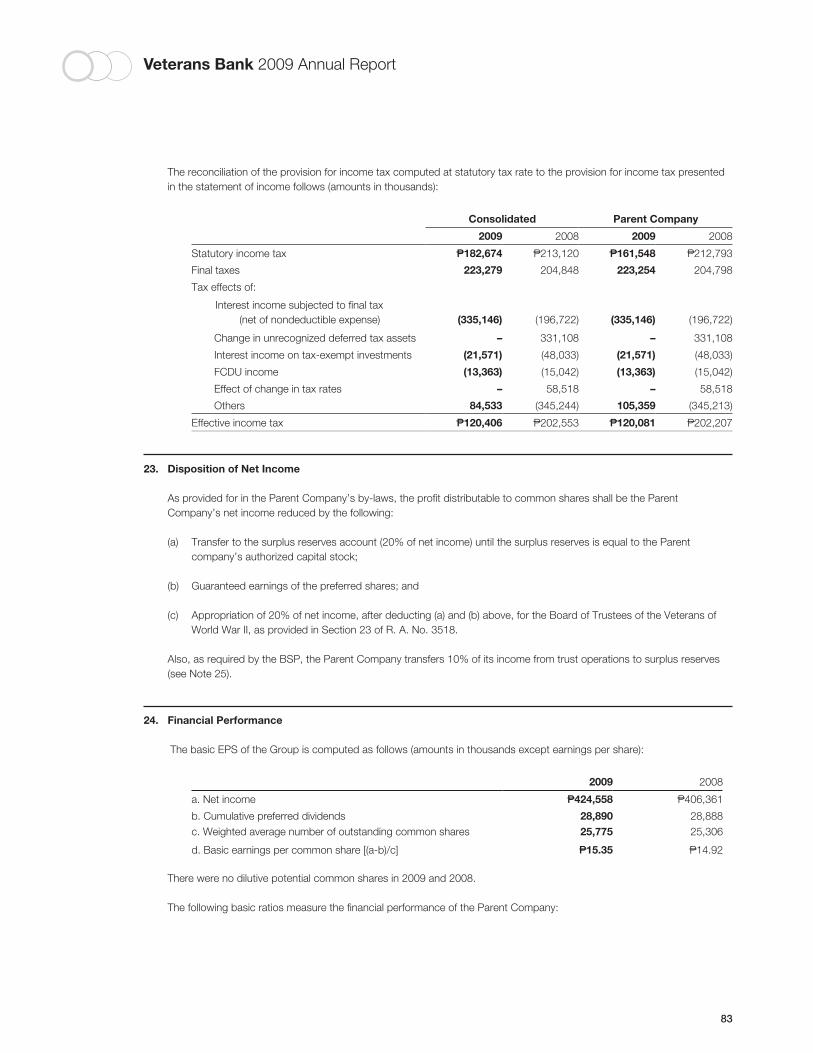

PROVISION FOR INCOME TAX (Note 22) 120,405,740 202,552,638 120,079,610 202,206,982

NET INCOME (Notes 23 and 24) P424,558,246 P406,361,155 P418,412,661 P405,773,921

Attributable to:

Equity holders of the Parent Company P424,556,918 P406,358,307

Minority interest 1,328 2,848

P424,558,246 P406,361,155

Basic/Diluted Earnings Per Share (Note 24) P15.35 P14.92

See accompanying Notes to Financial Statements.

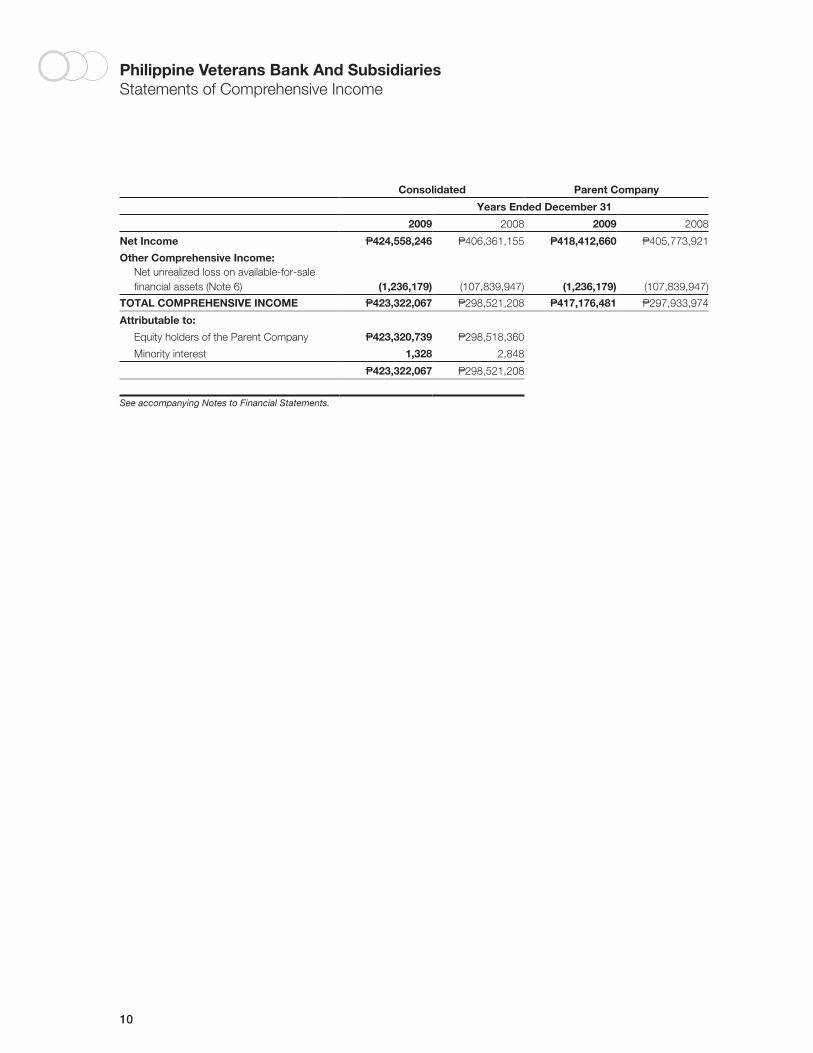

10

Consolidated Parent Company

Years Ended December 31

2009 2008 2009 2008

Net Income P424,558,246 P406,361,155 P418,412,660 P405,773,921

Other Comprehensive Income: Net unrealized loss on available-for-sale

financial assets (Note 6) (1,236,179) (107,839,947) (1,236,179) (107,839,947)

TOTAL COMPREHENSIVE INCOME P423,322,067 P298,521,208 P417,176,481 P297,933,974

Attributable to:

Equity holders of the Parent Company P423,320,739 P298,518,360

Minority interest 1,328 2,848

P423,322,067 P298,521,208

See accompanying Notes to Financial Statements.

Philippine Veterans Bank And SubsidiariesStatements of Comprehensive Income

Phi

lipp

ine

Vete

rans

Ban

k A

nd S

ubsi

dia

ries

Sta

tem

ents

of C

hang

es in

Equ

ity

11

Co

nso

lidat

ed

Eq

uity

Att

rib

utab

le t

o E

qui

ty H

old

ers

of

the

Par

ent

Co

mp

any

Pre

ferr

edS

tock

(Not

e 19

)

Co

mm

on

Sto

ck(N

ote

19)

Tre

asur

yS

tock

(Not

e 19

)T

ota

lC

apit

al S

tock

Ad

dit

iona

lP

aid

-in

Cap

ital

(Not

e 19

)

Sur

plu

sR

eser

ves

(Not

es 2

3 an

d 25

)

Sur

plu

s(N

otes

19,

23,

25

and

28)

Net

A

ccum

ulat

edU

nrea

lized

Gai

ns (L

oss

) o

n A

vaila

ble

-fo

r-S

ale(

AFS

) Fi

nanc

ial

Ass

ets

(Not

e 6)

To

tal

Min

ori

tyIn

tere

stT

ota

lE

qui

ty

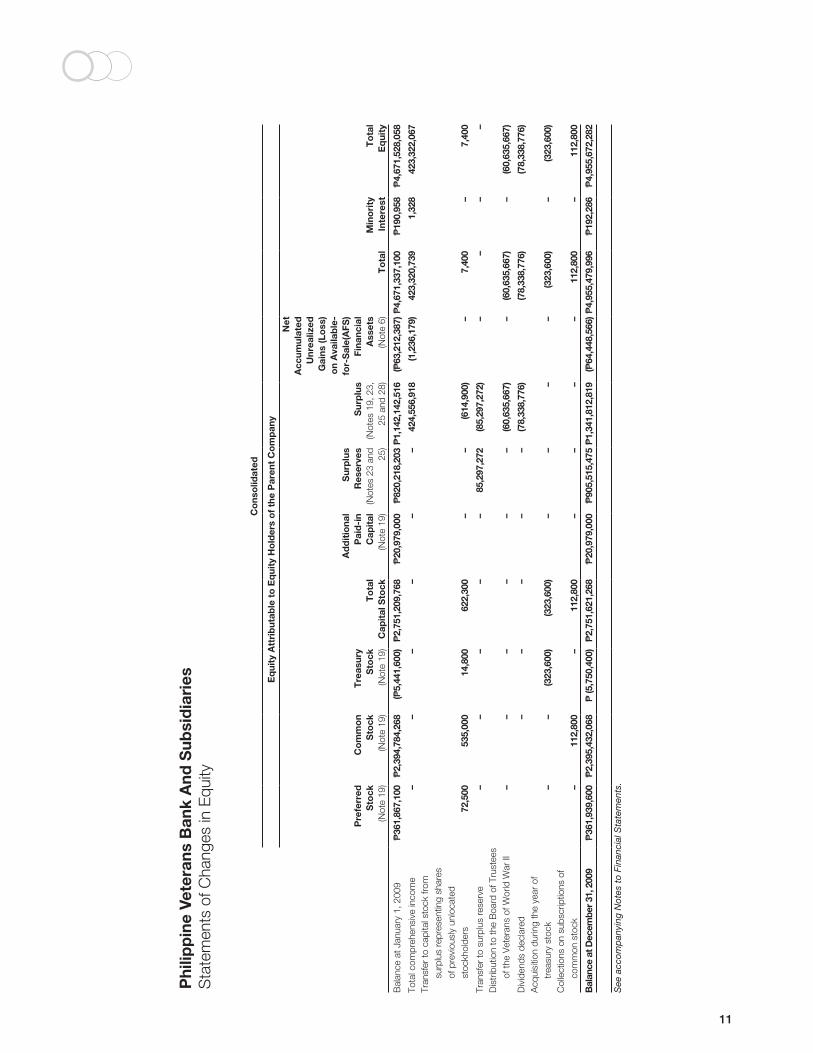

Bal

ance

at J

anua

ry 1

, 200

9P

361,

867,

100

P2,

394,

784,

268

(P5,

441,

600)

P2,

751,

209,

768

P20

,979

,000

P82

0,21

8,20

3P

1,14

2,14

2,51

6(P

63,2

12,3

87)

P4,

671,

337,

100

P19

0,95

8P

4,67

1,52

8,05

8

Tota

l com

preh

ensi

ve in

com

e–

––

––

–42

4,55

6,91

8(1

,236

,179

)42

3,32

0,73

91,

328

423,

322,

067

Tran

sfer

to c

apita

l sto

ck fr

om

surp

lus

repr

esen

ting

shar

es

of p

revi

ousl

y un

loca

ted

stoc

khol

ders

72,5

0053

5,00

014

,800

622,

300

––

(614

,900

)–

7,40

0–

7,40

0

Tran

sfer

to s

urpl

us r

eser

ve

––

––

–85

,297

,272

(85,

297,

272)

––

––

Dis

trib

utio

n to

the

Boa

rd o

f Tru

stee

s of

the

Vet

eran

s of

Wor

ld W

ar II

––

––

––

(60,

635,

667)

–(6

0,63

5,66

7)–

(60,

635,

667)

Div

iden

ds d

ecla

red

––

––

–(7

8,33

8,77

6)(7

8,33

8,77

6)(7

8,33

8,77

6)A

cqui

sitio

n du

ring

the

year

of

trea

sury

sto

ck–

–(3

23,6

00)

(323

,600

)–

––

–(3

23,6

00)

–(3

23,6

00)

Col

lect

ions

on

subs

crip

tions

of

com

mon

sto

ck–

112,

800

–11

2,80

0–

––

–11

2,80

0–

112,

800

Bal

ance

at D

ecem

ber 3

1, 2

009

P36

1,93

9,60

0P

2,39

5,43

2,06

8P

(5,7

50,4

00)

P2,

751,

621,

268

P20

,979

,000

P90

5,51

5,47

5P

1,34

1,81

2,81

9(P

64,4

48,5

66)

P4,

955,

479,

996

P19

2,28

6P

4,95

5,67

2,28

2

See

acc

omp

anyi

ng N

otes

to

Fina

ncia

l Sta

tem

ents

.

12

Con

solid

ated

Equ

ity A

ttrib

utab

le to

Equ

ity H

olde

rs o

f the

Par

ent C

ompa

ny

Pre

ferr

edS

tock

(Not

e 19

)

Com

mon

Sto

ck(N

ote

19)

Trea

sury

Sto

ck(N

ote

19)

Tota

lC

apita

l Sto

ck

Add

ition

alP

aid-

inC

apita

l(N

ote

19)

Sur

plus

Res

erve

s(N

otes

23

and

25)

Sur

plus

(Not

es 1

9, 2

3,

25 a

nd 2

8)

Net

A

ccum

ulat

edU

nrea

lized

Gai

ns (L

oss)

on

Ava

ilabl

e-fo

r-S

ale(

AFS

) Fi

nanc

ial

Ass

ets

(Not

e 6)

Tota

lM

inor

ityIn

tere

stTo

tal

Equ

ity

Bal

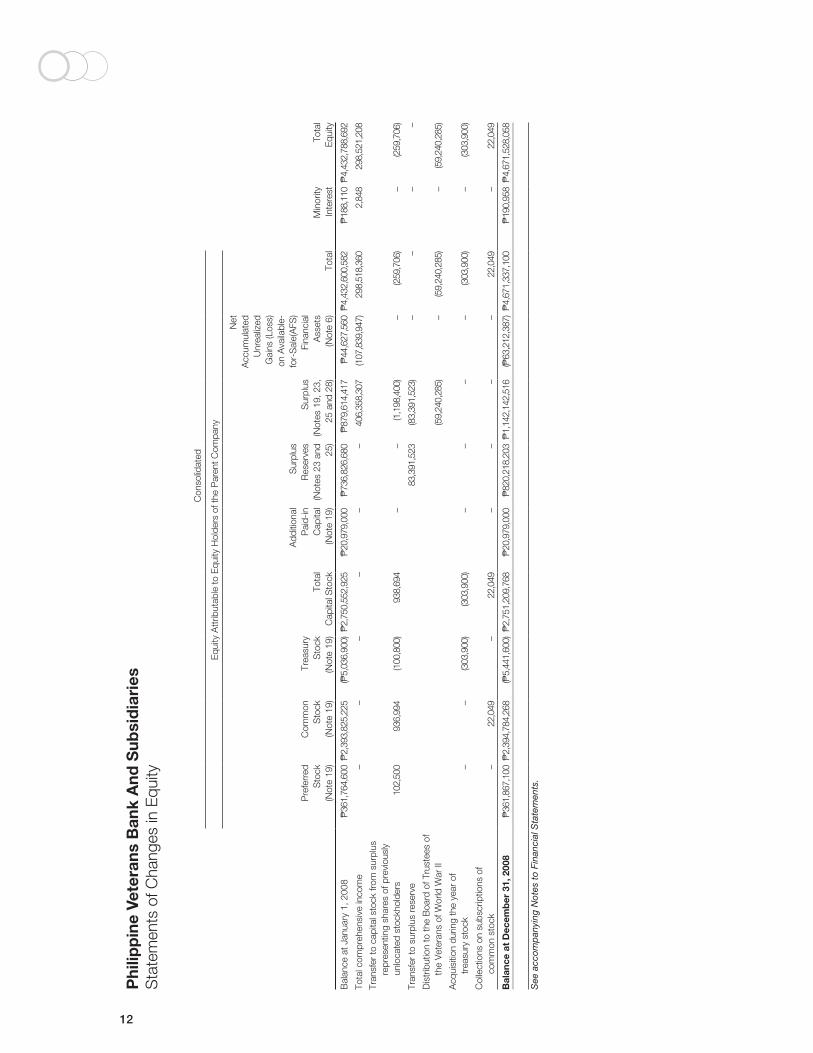

ance

at J

anua

ry 1

, 200

8P

361,

764,

600

P2,

393,

825,

225

(P5,

036,

900)

P2,

750,

552,

925

P20

,979

,000

P73

6,82

6,68

0P

879,

614,

417

P44

,627

,560

P4,

432,

600,

582

P18

8,11

0P

4,43

2,78

8,69

2

Tota

l com

preh

ensi

ve in

com

e–

––

––

–40

6,35

8,30

7(1

07,8

39,9

47)

298,

518,

360

2,84

829

8,52

1,20

8

Tran

sfer

to c

apita

l sto

ck fr

om s

urpl

us

repr

esen

ting

shar

es o

f pre

viou

sly

unlo

cate

d st

ockh

olde

rs10

2,50

093

6,99

4(1

00,8

00)

938,

694

––

(1,1

98,4

00)

–(2

59,7

06)

–(2

59,7

06)

Tran

sfer

to s

urpl

us r

eser

ve

83,3

91,5

23(8

3,39

1,52

3)–

––

–

Dis

trib

utio

n to

the

Boa

rd o

f Tru

stee

s of

th

e V

eter

ans

of W

orld

War

II(5

9,24

0,28

5)–

(59,

240,

285)

–(5

9,24

0,28

5)

Acq

uisi

tion

durin

g th

e ye

ar o

f tr

easu

ry s

tock

––

(303

,900

)(3

03,9

00)

––

––

(303

,900

)–

(303

,900

)

Col

lect

ions

on

subs

crip

tions

of

com

mon

sto

ck–

22,0

49–

22,0

49–

––

–22

,049

–22

,049

Bal

ance

at

Dec

emb

er 3

1, 2

008

P36

1,86

7,10

0P

2,39

4,78

4,26

8(P

5,44

1,60

0)P

2,75

1,20

9,76

8P

20,9

79,0

00P

820,

218,

203

P1,

142,

142,

516

(P63

,212

,387

)P

4,67

1,33

7,10

0P

190,

958

P4,

671,

528,

058

See

acc

omp

anyi

ng N

otes

to

Fina

ncia

l Sta

tem

ents

.

Phi

lipp

ine

Vete

rans

Ban

k A

nd S

ubsi

dia

ries

Sta

tem

ents

of C

hang

es in

Equ

ity

13

Par

ent

Co

mp

any

Pre

ferr

edS

tock

(Not

e 19

)

Co

mm

on

Sto

ck(N

ote

19)

Tre

asur

yS

tock

(Not

e 19

)T

ota

lC

apit

al S

tock

Ad

dit

iona

lP

aid

-in

Cap

ital

(Not

e 19

)

Sur

plu

sR

eser

ves

(Not

es 2

3 an

d 25

)

Sur

plu

s(N

otes

19,

23,

25

and

28)

Net

A

ccum

ulat

edU

nrea

lized

Gai

ns (L

oss

) on

Ava

ilab

le-f

or-

Sal

e Fi

nanc

ial

Ass

ets

(Not

e 6)

To

tal

Bal

ance

at J

anua

ry 1

, 200

9P

361,

867,

100

P2,

394,

784,

268

(P5,

441,

600)

P2,

751,

209,

768

P20

,979

,000

P82

0,21

8,20

3P

1,14

5,17

7,77

7(P

63,2

12,3

87)

P4,

674,

372,

361

Tota

l com

preh

ensi

ve in

com

e–

––

––

–41

8,41

2,66

1(1

,236

,179

)41

7,17

6,48

2

Tran

sfer

to c

apita

l sto

ck fr

om s

urpl

us

repr

esen

ting

shar

es o

f pre

viou

sly

unlo

cate

d st

ockh

olde

rs72

,500

535,

000

14,8

0062

2,30

0–

–(6

14,9

00)

–7,

400

Tran

sfer

to s

urpl

us r

eser

ve

––

––

–85

,297

,272

(85,

297,

272)

––

Dis

trib

utio

n to

the

Boa

rd o

f Tru

stee

s of

the

Vet

eran

s of

Wor

ld W

ar II

––

––

––

(60,

635,

667)

–(6

0,63

5,66

7)

Div

iden

ds d

ecla

red

––

––

––

(78,

338,

776)

–(7

8,33

8,77

6)

Acq

uisi

tion

durin

g th

e ye

ar o

f tre

asur

y st

ock

––

(323

,600

)(3

23,6

00)

––

––

(323

,600

)

Col

lect

ions

on

subs

crip

tions

of c

omm

on s

tock

–11

2,80

0–

112,

800

––

––

112,

800

Bal

ance

at

Dec

emb

er 3

1, 2

009

P36

1,93

9,60

0P

2,39

5,43

2,06

8(P

5,75

0,40

0)P

2,75

1,62

1,26

8P

20,9

79,0

00P

905,

515,

475

P1,

338,

703,

823

(P64

,448

,566

)P

4,95

2,37

1,00

0

See

acc

omp

anyi

ng N

otes

to

Fina

ncia

l Sta

tem

ents

.

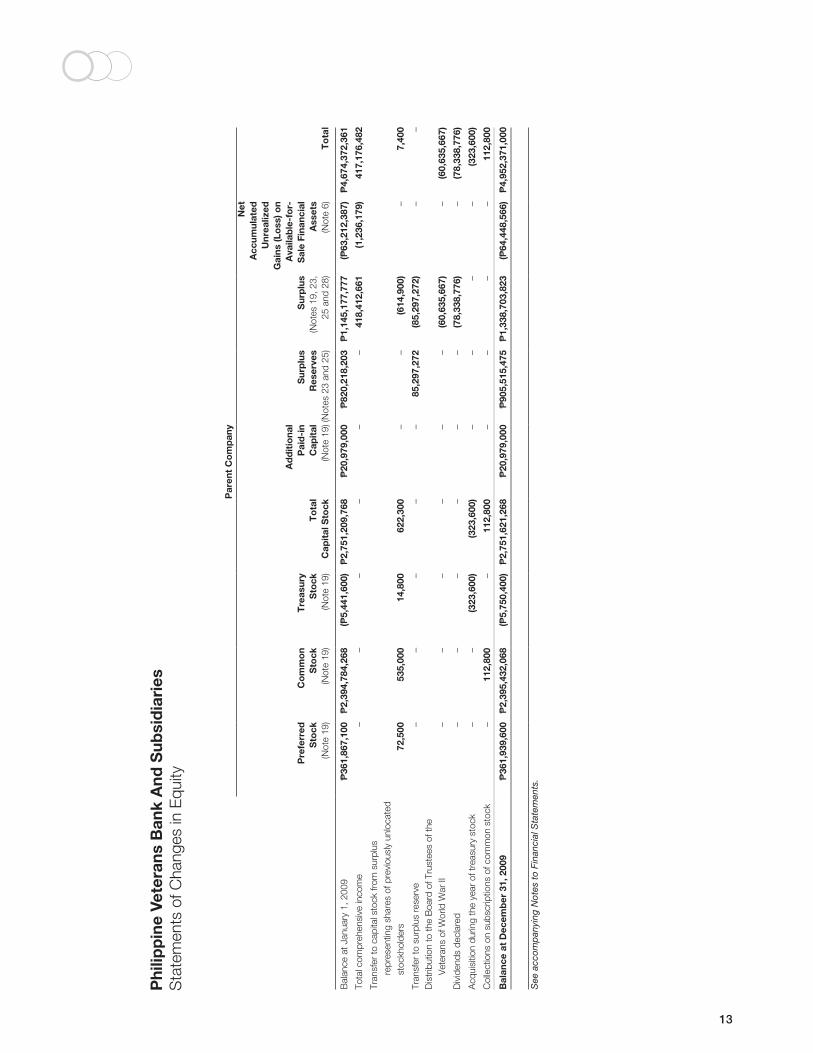

Phi

lipp

ine

Vete

rans

Ban

k A

nd S

ubsi

dia

ries

Sta

tem

ents

of C

hang

es in

Equ

ity

14

Par

ent C

ompa

ny

Pre

ferr

edS

tock

(Not

e 19

)

Com

mon

Sto

ck(N

ote

19)

Trea

sury

Sto

ck(N

ote

19)

Tota

lC

apita

l Sto

ck

Add

ition

alP

aid-

inC

apita

l(N

ote

19)

Sur

plus

Res

erve

s(N

otes

23

and

25)

Sur

plus

(Not

es 1

9, 2

3,

25 a

nd 2

8)

Net

Acc

umul

ated

Unr

ealiz

edG

ains

(Los

s) o

nA

vaila

ble-

for-

Sal

e Fi

nanc

ial

Ass

ets

(Not

e 6)

Tota

l

Bal

ance

at J

anua

ry 1

, 200

8P

361,

764,

600

P2,

393,

825,

225

(P5,

036,

900)

P2,

750,

552,

925

P20

,979

,000

P73

6,82

6,68

0P

883,

234,

064

P44

,627

,560

P4,

436,

220,

229

Tota

l com

preh

ensi

ve in

com

e–

––

––

–40

5,77

3,92

1(1

07,8

39,9

47)

297,

933,

974

Tran

sfer

to c

apita

l sto

ck fr

om s

urpl

us

repr

esen

ting

shar

es o

f pre

viou

sly

unlo

cate

d st

ockh

olde

rs10

2,50

093

6,99

4(1

00,8

00)

938,

694

––

(1,1

98,4

00)

–(2

59,7

06)

Tran

sfer

to s

urpl

us r

eser

ve

––

––

–83

,391

,523

(83,

391,

523)

––

Dis

trib

utio

n to

the

Boa

rd o

f Tru

stee

s of

the

Vet

eran

s of

Wor

ld W

ar II

––

––

––

(59,

240,

285)

–(5

9,24

0,28

5)

Acq

uisi

tion

durin

g th

e ye

ar o

f tre

asur

y st

ock

––

(303

,900

)(3

03,9

00)

––

––

(303

,900

)

Col

lect

ions

on

subs

crip

tions

of c

omm

on s

tock

–22

,049

–22

,049

––

––

22,0

49

Bal

ance

at

Dec

emb

er 3

1, 2

008

P36

1,86

7,10

0P

2,39

4,78

4,26

8(P

5,44

1,60

0)P

2,75

1,20

9,76

8P

20,9

79,0

00P

820,

218,

203

P1,

145,

177,

777

(P63

,212

,387

)P

4,67

4,37

2,36

1

See

acc

omp

anyi

ng N

otes

to

Fina

ncia

l Sta

tem

ents

.

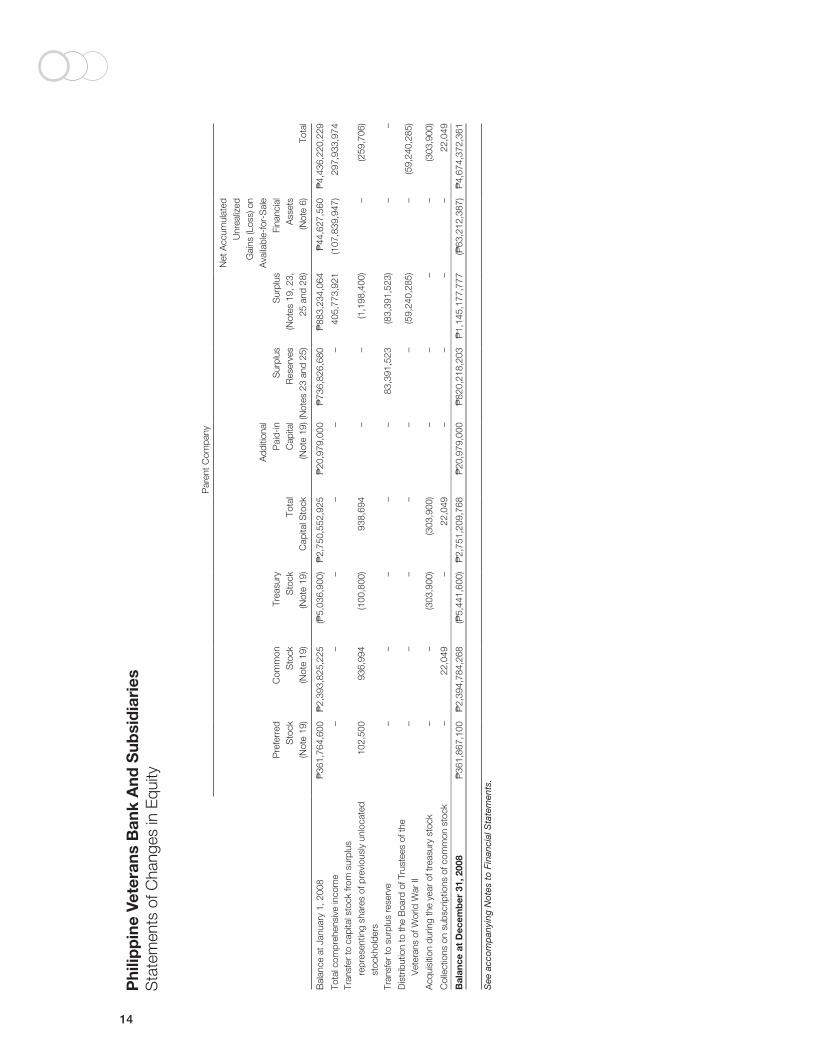

Phi

lipp

ine

Vete

rans

Ban

k A

nd S

ubsi

dia

ries

Sta

tem

ents

of C

hang

es in

Equ

ity

15

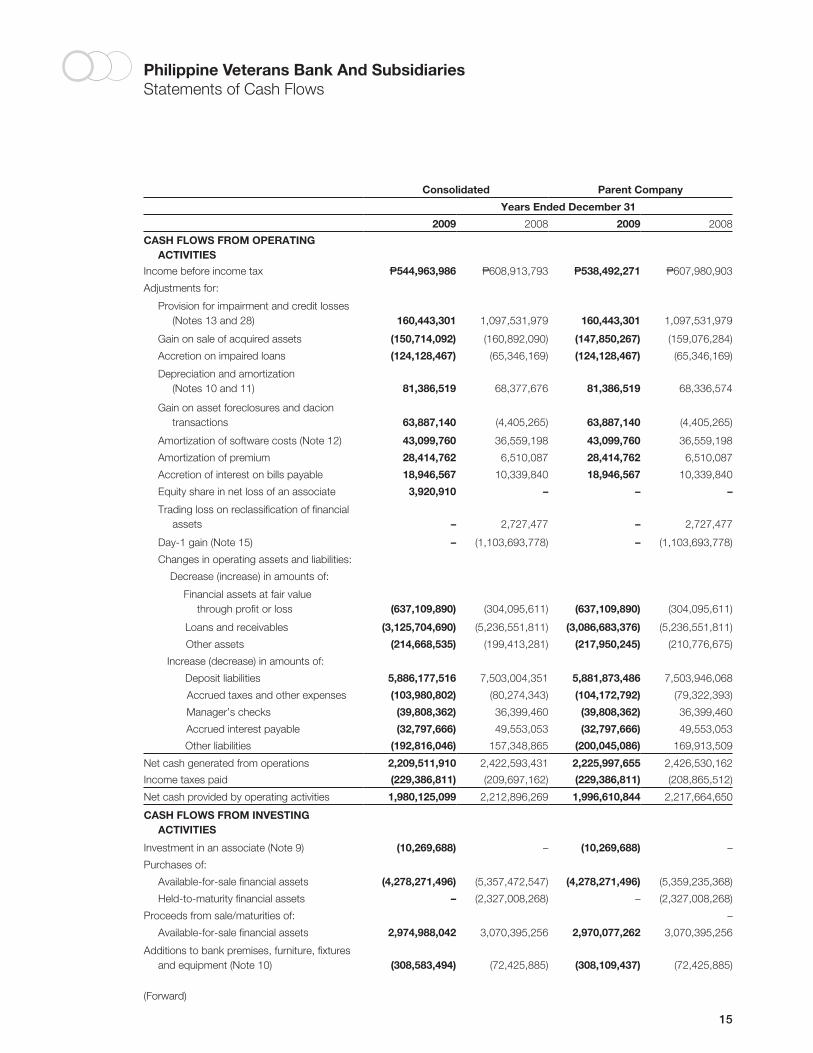

Consolidated Parent Company

Years Ended December 31

2009 2008 2009 2008

CASH FLOWS FROM OPERATING ACTIVITIES

Income before income tax P544,963,986 P608,913,793 P538,492,271 P607,980,903

Adjustments for:

Provision for impairment and credit losses (Notes 13 and 28) 160,443,301 1,097,531,979 160,443,301 1,097,531,979

Gain on sale of acquired assets (150,714,092) (160,892,090) (147,850,267) (159,076,284)

Accretion on impaired loans (124,128,467) (65,346,169) (124,128,467) (65,346,169)

Depreciation and amortization (Notes 10 and 11) 81,386,519 68,377,676 81,386,519 68,336,574

Gain on asset foreclosures and dacion transactions 63,887,140 (4,405,265) 63,887,140 (4,405,265)

Amortization of software costs (Note 12) 43,099,760 36,559,198 43,099,760 36,559,198

Amortization of premium 28,414,762 6,510,087 28,414,762 6,510,087

Accretion of interest on bills payable 18,946,567 10,339,840 18,946,567 10,339,840

Equity share in net loss of an associate 3,920,910 – – –

Trading loss on reclassification of financial assets – 2,727,477 – 2,727,477

Day-1 gain (Note 15) – (1,103,693,778) – (1,103,693,778)

Changes in operating assets and liabilities:

Decrease (increase) in amounts of:

Financial assets at fair value through profit or loss (637,109,890) (304,095,611) (637,109,890) (304,095,611)

Loans and receivables (3,125,704,690) (5,236,551,811) (3,086,683,376) (5,236,551,811)

Other assets (214,668,535) (199,413,281) (217,950,245) (210,776,675)

Increase (decrease) in amounts of:

Deposit liabilities 5,886,177,516 7,503,004,351 5,881,873,486 7,503,946,068

Accrued taxes and other expenses (103,980,802) (80,274,343) (104,172,792) (79,322,393)

Manager’s checks (39,808,362) 36,399,460 (39,808,362) 36,399,460

Accrued interest payable (32,797,666) 49,553,053 (32,797,666) 49,553,053

Other liabilities (192,816,046) 157,348,865 (200,045,086) 169,913,509

Net cash generated from operations 2,209,511,910 2,422,593,431 2,225,997,655 2,426,530,162

Income taxes paid (229,386,811) (209,697,162) (229,386,811) (208,865,512)

Net cash provided by operating activities 1,980,125,099 2,212,896,269 1,996,610,844 2,217,664,650

CASH FLOWS FROM INVESTING ACTIVITIES

Investment in an associate (Note 9) (10,269,688) – (10,269,688) –

Purchases of:

Available-for-sale financial assets (4,278,271,496) (5,357,472,547) (4,278,271,496) (5,359,235,368)

Held-to-maturity financial assets – (2,327,008,268) – (2,327,008,268)

Proceeds from sale/maturities of: –

Available-for-sale financial assets 2,974,988,042 3,070,395,256 2,970,077,262 3,070,395,256

Additions to bank premises, furniture, fixtures and equipment (Note 10) (308,583,494) (72,425,885) (308,109,437) (72,425,885)

Philippine Veterans Bank And SubsidiariesStatements of Cash Flows

(Forward)

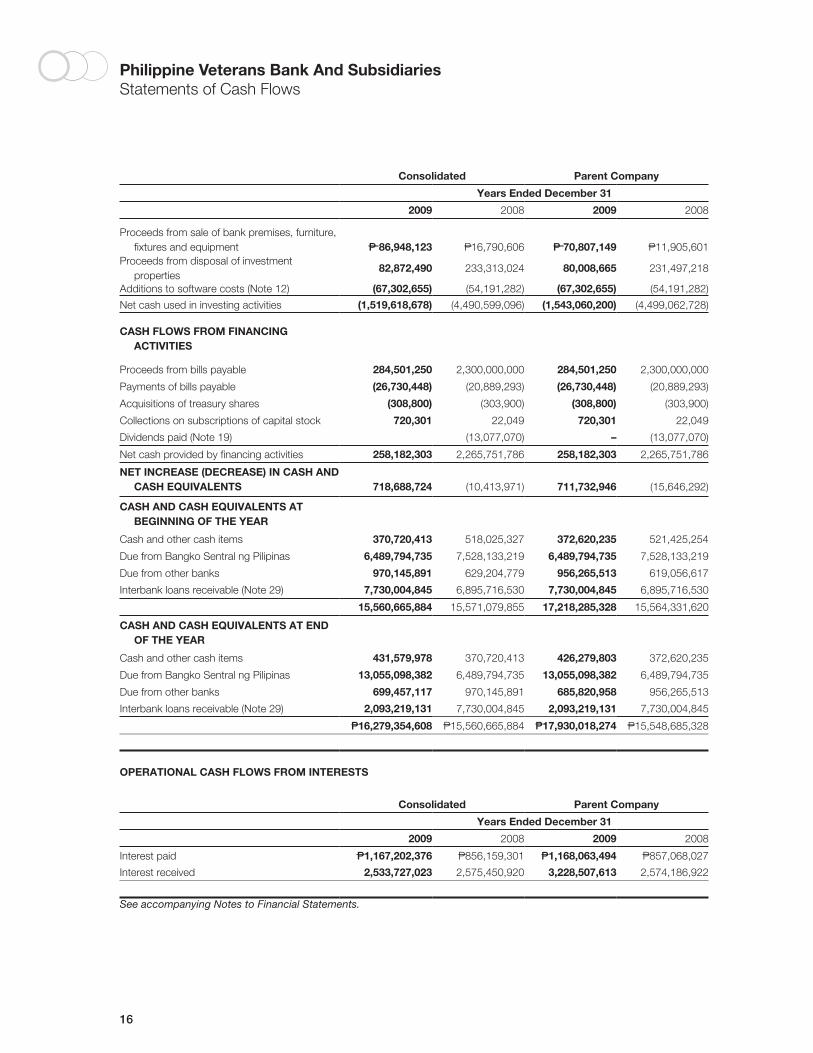

16

Consolidated Parent Company

Years Ended December 31

2009 2008 2009 2008

Proceeds from sale of bank premises, furniture, fixtures and equipment P 86,948,123 P16,790,606 P 70,807,149 P11,905,601

Proceeds from disposal of investment properties

82,872,490 233,313,024 80,008,665 231,497,218

Additions to software costs (Note 12) (67,302,655) (54,191,282) (67,302,655) (54,191,282)

Net cash used in investing activities (1,519,618,678) (4,490,599,096) (1,543,060,200) (4,499,062,728)

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from bills payable 284,501,250 2,300,000,000 284,501,250 2,300,000,000

Payments of bills payable (26,730,448) (20,889,293) (26,730,448) (20,889,293)

Acquisitions of treasury shares (308,800) (303,900) (308,800) (303,900)

Collections on subscriptions of capital stock 720,301 22,049 720,301 22,049

Dividends paid (Note 19) (13,077,070) – (13,077,070)

Net cash provided by financing activities 258,182,303 2,265,751,786 258,182,303 2,265,751,786

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 718,688,724 (10,413,971) 711,732,946 (15,646,292)

CASH AND CASH EQUIVALENTS AT BEGINNING OF THE YEAR

Cash and other cash items 370,720,413 518,025,327 372,620,235 521,425,254

Due from Bangko Sentral ng Pilipinas 6,489,794,735 7,528,133,219 6,489,794,735 7,528,133,219

Due from other banks 970,145,891 629,204,779 956,265,513 619,056,617

Interbank loans receivable (Note 29) 7,730,004,845 6,895,716,530 7,730,004,845 6,895,716,530

15,560,665,884 15,571,079,855 17,218,285,328 15,564,331,620

CASH AND CASH EQUIVALENTS AT END OF THE YEAR

Cash and other cash items 431,579,978 370,720,413 426,279,803 372,620,235

Due from Bangko Sentral ng Pilipinas 13,055,098,382 6,489,794,735 13,055,098,382 6,489,794,735

Due from other banks 699,457,117 970,145,891 685,820,958 956,265,513

Interbank loans receivable (Note 29) 2,093,219,131 7,730,004,845 2,093,219,131 7,730,004,845

P16,279,354,608 P15,560,665,884 P17,930,018,274 P15,548,685,328

OPERATIONAL CASH FLOWS FROM INTERESTS

Consolidated Parent Company

Years Ended December 31

2009 2008 2009 2008

Interest paid P1,167,202,376 P856,159,301 P1,168,063,494 P857,068,027

Interest received 2,533,727,023 2,575,450,920 3,228,507,613 2,574,186,922

See accompanying Notes to Financial Statements.

Philippine Veterans Bank And SubsidiariesStatements of Cash Flows

17

1. Corporate Information

Philippine Veterans Bank (the Parent Company) operates as a domestic commercial bank and provides services such as deposit-taking, loans and trade finance, domestic and foreign fund transfers, treasury, foreign exchange and trust services. The subsidiaries are engaged primarily in real estate and insurance business. Principal place of business is of the Parent Company at 101 V.A. Rufino corner Dela Rosa Streets, Legaspi Village, Makati City.

On June 18, 1963, the Philippine Veterans Bank was created with the enactment of Republic Act No. 3518, which became its charter.

On October 30, 2003, the Board of Directors (BOD) approved the merger of Monarch Properties, Inc. (MPI), a wholly owned subsidiary, with the Parent Company. The merger was subsequently approved by the Parent Company’s stockholders on May 30, 2005. As of December 31, 2009, the approval of the merger is still pending with the SEC and BSP.

2. Summary of Significant Accounting Policies

Basis of PreparationThe accompanying financial statements have been prepared on a historical basis except for financial assets at fair value through profit or loss (FVPL) and available-for-sale (AFS) financial assets that are measured at fair value.

The accompanying financial statements of the Parent Company include the accounts maintained in the Regular Banking Unit (RBU) and Foreign Currency Deposit Unit (FCDU).

For financial reporting purposes, FCDU accounts and foreign currency denominated accounts in the RBU are translated into their equivalents in Philippine Peso (see accounting policy on Foreign currency translation). The financial statements of these units are combined after eliminating inter-unit accounts.

The consolidated financial statements are presented in Philippine Peso (P) which is also the Parent Company’s functional currency.

Statement of ComplianceThe Group and the Parent Company prepared its financial statements in accordance with Philippine Financial Reporting Standards (PFRS), except for the recognition in 2008 of the allowance for credit losses on interbank call loans (IBCL) to a thrift bank required in 2007 and 2006, and the staggered recognition of the remaining required allowance for credit losses on IBCL and the required allowance for credit losses on accounts receivable over 20 years approved by BSP as discussed in Note 28 and the deferral of loss on sale of non-performing assets to a Special Purpose Vehicle as discussed in Note 7.

Basis of ConsolidationThe financial statements which include the financial statements of the Parent Company and its subsidiaries (collectively referred to as “the Group”) are prepared for the same reporting year as the Parent Company, using consistent accounting policies.

The Parent Company has the following wholly and majority owned subsidiaries:

SubsidiaryCountry ofIncorporation

Principal ActivitiesEffectivePercentageof Ownership

Vetgroup Intervest Projects, Inc. Philippines Real estate 100.00Monarch Properties, Inc. Philippines Real estate 100.00Veterans Venture Capital Corporation Philippines Financing 60.00

All significant intra-group balances, transactions, income and expenses and profits and losses resulting from intra-group transactions are eliminated in full in the consolidation.

Subsidiaries are fully consolidated from the date on which control is transferred to the Group. Control is achieved where the Group has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. Consolidation of subsidiaries ceases when control is transferred out of the Group or Parent Company.

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

18

The results of subsidiaries acquired or disposed of during the year are included in the consolidated statement of income from the date of acquisition or up to the date of disposal, as appropriate.

Minority InterestMinority interest represents the portion of profit or loss and the net assets not held by the Group and is presented separately in the consolidated statement of income and within equity in the consolidated statement of financial position, separately from Parent Company’s equity. Acquisitions of minority interest are accounted for using the entity concept method, whereby the difference between the consideration and the book value of the share of the net assets acquired is recognized as an equity transaction. Minority interest represents the equity interest in Veterans Venture Capital Corporation, a 60% owned subsidiary.

Changes in Accounting PolicesThe accounting policies are consistent with the previous year except for the adoption of the following amendments to PFRS and Philippine Interpretations starting January 1, 2009:

New Standards and Interpretations• PAS1,Presentation of Financial Statements effective January 1, 2009• PAS23,Borrowing Cost (Revised) effective January 1, 2009• PFRS8,Operating Segments effective January 1, 2009• PhilippineInterpretationIFRIC13,Customer Loyalty Programmes effective July 1, 2008• PhilippineInterpretationIFRIC16,Hedges of a Net Investment in a Foreign Operations effective October 1, 2008• PhilippineInterpretationIFRIC18,Transfer of Assets from Customers effective July 1, 2009

Amendments to Standards• PAS1andPAS32Amendments,Puttable Financial Instruments and Obligations Arising on Liquidation effective January 1, 2009• PFRS1andPAS27Amendments,Cost of an Investment in a Subsidiary, Joint Controlled Entity or Associate effective January 1, 2009• PFRS2Amendment,Vesting Conditions and Cancellations effective January 1, 2009• PFRS7Amendment,Improving Disclosures about Financial Instruments effective January 1, 2009• PhilippineInterpretationIFRIC9andPAS39Amendments,Embedded Derivatives effective June 30, 2009• ImprovementstoPFRSs(2008)• ImprovementstoPFRSs(2009),withrespecttotheamendmenttotheAppendixtoPAS18,Revenue

New and amended standards that have been adopted and that have impact on the financial statements and disclosures of the Group are described below:

Philippine Accounting Standards (PAS) 1, Presentation of Financial StatementsThe revised standard separates owner and non-owner changes in equity. The statement of changes in equity includes only details of transactions with owners, with non-owner changes in equity presented in a reconciliation of each component of equity. In addition, the standard introduces the statement of comprehensive income: it presents all items of recognized income and expense, either in one single statement, or in two linked statements. The Group has elected to present two linked statements.

Amendments to StandardsPFRS 7 Amendments - Improving Disclosures about Financial InstrumentsThe amendments to PFRS 7, Financial Instruments: Disclosures, require additional disclosures about fair value measurement and liquidity risk. Fair value measurements related to items recorded at fair value are to be disclosed by source of inputs using a three level fair value hierarchy, by class, for all financial instruments recognized at fair value. In addition, a reconciliation between the beginning and ending balance for level 3 fair value measurements is now required, as well as significant transfers between levels in the fair value hierarchy. The amendments also clarify the requirements for liquidity risk disclosures with respect to derivative transactions and financial assets used for liquidity management. The fair value measurement disclosures are presented in Note 5. The liquidity risk disclosures are not significantly impacted by the amendments and are presented in Note 4.

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

Veterans Bank 2009 Annual Report

19

Improvements to PFRS 2008The omnibus amendments to PFRSs issued in 2008 were issued primarily with a view to remove inconsistencies and clarify wordings. There are separate transitional provisions for each standard. The adoption of the amendments resulted in changes in accounting policies but did not have any impact on the financial position or performance of the Group.

Significant Accounting Policies

Foreign Currency TranslationTransactions and balancesThe books of accounts of the RBU are maintained in Philippine pesos, while those of the FCDU are maintained in USD. For financial reporting purposes, foreign currency-denominated monetary assets and liabilities of the RBU are translated in Philippine peso based on the Philippine Dealing and Exchange Corporation (PDEx) closing rate prevailing at end of the year. Transactions denominated in foreign currencies are recorded using the exchange rates prevailing at the transaction dates. Foreign exchange differences are recognized in the statement of income.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates as at the dates of the initial transactions. Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

FCDUAs at the reporting date, the assets and liabilities of FCDU are translated into the Parent Company’s presentation currency (the Philippine peso) at PDEx closing rate prevailing at the statement of financial position date, and their income and expenses are translated at PDEx weighted average rates for the period. Exchange differences arising on translation are taken to statement of comprehensive income.

Financial Instruments - Initial Recognition and Subsequent MeasurementDate of recognitionPurchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace are recognized on the settlement date - the date that an asset is delivered to or by the Group. Securities transactions are also recognized on settlement date basis. Deposits, amounts due to banks and customers and loans are recognized when cash is received by the Group or advanced to the borrowers.

Initial recognition of financial instrumentsAll financial assets and financial liabilities are initially recognized at fair value. Except for financial assets and financial liabilities at FVPL, the initial measurement of financial assets and financial liabilities includes transaction costs. The Group classifies its financial assets in the following categories: financial assets at FVPL, HTM financial assets, AFS financial assets, and loans and receivables. The financial liabilities, on the other hand, are classified into (a) financial liabilities at FVPL and (b) other financial liabilities. The classification depends on the purpose for which the financial assets were acquired and whether they are quoted in an active market and for HTM financial assets, the ability and intention to hold the investment until maturity. Management determines the classification of its investments at initial recognition and, where allowed and appropriate, re-evaluates such designation at every reporting date.

Reclassification of financial assetsA financial asset is reclassified out of the FVPL category when the following conditions are met:

• thefinancialassetisnolongerheldforthepurposeofsellingorrepurchasingitinthenearterm;and• thereisararecircumstance.

A financial asset that is reclassified out of the FVPL category is reclassified at its fair value on the date of reclassification. Any gain or loss already recognized in the statement of is not reversed. The fair value of the financial asset on the date of reclassification becomes its new cost or amortized cost, as applicable.

For financial assets reclassified out of the AFS category to held-to-maturity investments, any previous gain or loss on that asset that has been recognized under other comprehensive income in the statement of comprehensive income is amortized to profit or loss over the remaining life of the investment using the effective interest rate (EIR) method. Any

20

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

difference between the new amortize cost and the expected cash flows is also amortized over the remaining life of asset using EIR method. If the asset is subsequently determined to be impaired then the amount recorded under other comprehensive income is recycled to the statement of income.

Determination of fair valueThe fair value for financial instruments traded in active markets at the statement of financial position date is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and asking prices are not available, the price of the most recent transaction provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction.

For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable prices exist, options pricing models, and other relevant valuation models.

‘Day 1’ differenceWhere the transaction price in a non-active market is different from the fair value based on other observable current market transactions in the same instrument or based on a valuation technique whose variables include only data from observable market, the Group recognizes the difference between the transaction price and fair value (‘Day 1’ difference) in the statement of income unless it qualifies for recognition as some other type of assets. In cases where use is made of data which is not observable, the difference between the transaction price and model value is only recognized in the statement of income when the inputs become observable or when the instrument is derecognized. For each transaction, the Group determines the appropriate method of recognizing the ‘Day 1’ difference amount.

Financial assets or financial liabilities held for tradingFinancial assets or financial liabilities held for trading are recorded in the statement of financial position at fair value. Changes in fair value relating to the held-for-trading positions are recognized in ‘Trading gains (losses) - net’. Interest earned or incurred is recorded in ‘Interest income or expense’, respectively, while dividend income is recorded in ‘Other operating Income’ when the right to receive payment has been established.

Included in this classification are debt and equity securities which have been acquired principally for the purpose of selling or repurchasing in the near term. As of December 31, 2009 and 2008, the Group does not have financial liabilities held for trading.

Financial assets or financial liabilities designated at FVPLFinancial assets or financial liabilities classified in this category are designated by management on initial recognition when the following criteria are met:

• Thedesignationeliminatesorsignificantlyreducestheinconsistenttreatmentthatwouldotherwisearisefrom measuring the assets or liabilities or recognizing gains or losses on them on a different basis; or• Theassetsandliabilitiesarepartofagroupoffinancialassets,financialliabilitiesorbothwhicharemanagedand their performance evaluated on a fair value basis, in accordance with a documented risk management or investment strategy; or• Thefinancialinstrumentcontainsanembeddedderivative,unlesstheembeddedderivativedoesnotsignificantly modify the cash flows or it is clear, with little or no analysis, that it would not be separately recorded.

Designated financial assets and financial liabilities at FVPL are recorded in the statement of financial position at fair value. Changes in fair value are recorded in ‘Trading gains(losses) - net’ on financial assets and liabilities designated at FVPL. Interest earned or incurred is recorded in interest income or expense, respectively, while dividend income is recorded in ‘Other operating income’ according to the terms of the contract, or when the right of the payment has been established. As of December 31, 2009 and 2008, the Group has no existing financial assets or financial liabilities designated at FVPL.

HTM financial assetsHTM financial assets are quoted, non-derivative financial assets with fixed or determinable payments and fixed maturities for which the Group’s management has the positive intention and ability to hold to maturity. Where the Group would sell other than an insignificant amount of HTM financial assets, the entire category would be tainted and reclassified as AFS financial assets. After initial measurement, these investments are subsequently measured at amortized cost using the

Veterans Bank 2009 Annual Report

21

effective interest rate (EIR) method, less any impairment in value. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees that are an integral part of the EIR. The amortization is included in ‘Interest income’ in the statement of income. Gains and losses are recognized in the statement of income when the HTM financial assets are derecognized and impaired, as well as through the amortization process. The losses arising from impairment of such investments are recognized in the statement of income under ‘Provision for impairment and credit losses.’

The effects of restatement on foreign currency denominated HTM financial assets are recognized in the statement of income.

Loans and receivables, amounts due from BSP and other banks, and interbank loans receivables and SPURAThis accounting policy relates to the statement of financial position captions ‘Due from BSP’, ‘Due from other banks’, ‘Interbank loans receivables and SPURA’, ‘Securities purchased under resale agreement’ and ‘Loans and receivables’. These are non derivative financial assets with fixed or determinable payments and fixed maturities that are not quoted in an active market. They are not entered into with the intention of immediate or short-term resale and are not classified as ‘Financial assets held for trading’, designated as ‘AFS financial assets’ or ‘financial assets designated at FVPL.’

After initial measurement, ‘Loans and receivables’, ‘Due from BSP’, ‘Due from other banks’ and ‘Interbank loans receivables’ and ‘SPURA’ are subsequently measured at amortized cost using the EIR method, less allowance for impairment. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees and costs that are an integral part of the EIR. The amortization is included in the ‘Interest income’ in the statement of income. The losses arising from impairment are recognized in ‘Provision for impairment and credit losses’ in the statement of income.

AFS financial assetsAFS financial assets are those which are designated as such or do not qualify to be classified as designated as financial assets at FVPL, HTM financial assets or loans and receivables. They are purchased and held indefinitely, and may be sold in response to liquidity requirements or changes in market conditions. They include equity investments and other debt instruments.

After initial measurement, AFS financial assets are subsequently measured at fair value. The effective yield component of AFS debt securities, as well as the impact of restatement on foreign currency-denominated AFS debt securities, is reported in statement of income. The unrealized gains and losses arising from the fair valuation of AFS financial assets are excluded, net of tax, from reported income and are reported as ‘Net unrealized gains (losses) on AFS financial assets’ under other comprehensive income in the statement of comprehensive income.

When the security is disposed of, the cumulative gain (losses) or loss previously recognized in equity is recognized as ‘Trading gains (losses) - net’ in the statement of income. Where the Group holds more than one investment in the same security, these are deemed to be disposed of on a specific identification. Interests earned on holding AFS financial assets are reported as interest income using the EIR. Dividends earned on holding AFS financial assets are recognized in the statement of income as ‘Other operating income’ when the right to receive payment has been established. The losses arising from impairment of such investments are recognized as ‘Provisions for impairment and credit losses’ in the statement of income.

Bills payable and other borrowed fundsIssued financial instruments or their components, which are not designated as financial liabilities at FVPL, are classified as liabilities under ‘Bills payable” or other appropriate financial liability accounts, where the substance of the contractual arrangement results in the Group having an obligation either to deliver cash or another financial asset to the holder, or to satisfy the obligation other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of own equity shares. The components of issued financial instruments that contain both liability and equity elements are accounted for separately, with the equity component being assigned the residual amount after deducting from the instrument as a whole the amount separately determined as the fair value of the liability component on the date of issue.

After initial measurement, bills payable and similar financial liabilities not qualified as and not designated as FVPL, are subsequently measured at amortized cost using the EIR method. Amortized cost is calculated by taking into account any discount or premium on the issue and fees that are an integral part of the EIR.

22

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

Derecognition of Financial Assets and LiabilitiesFinancial assetsA financial asset (or, where applicable, a part of a financial asset or part of a group of financial assets) is derecognized where:

• therightstoreceivecashflowsfromtheassethaveexpired;or• theGroupretainstherighttoreceivecashflowsfromtheasset,buthasassumedanobligationtopaytheminfull without material delay to a third party under a “pass-through” arrangement; or• theGrouphastransferreditsrightstoreceivecashflowsfromtheassetandeither(a)hastransferredsubstantiallyall the risks and rewards of the asset, or (b) has neither transferred nor retained the risk and rewards of the asset but has transferred the control of the asset.

Where the Group has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the asset is recognized to the extent of the Group’s continuing involvement in the asset. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of original carrying amount of the asset and the maximum amount of consideration that the Group could be required to repay.

Financial liabilitiesA financial liability is derecognized when the obligation under the liability is discharged or cancelled or has expired. Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in statement of income.

Repurchase and reverse repurchase agreementsSecurities sold under agreements to repurchase at a specified future date (‘repos’) are not derecognized from the statement of financial position. The corresponding cash received, including accrued interest, is recognized in the statement of financial position as a loan to the Group, reflecting the economic substance of such transaction.

‘Securities purchased under resale agreements’ (SPURA) are recorded as loans and advances to banks or counterparty. The difference between the purchase price and resale price is treated as interest income and is accrued over the life of the agreement using EIR.

Impairment of Financial AssetsThe Group assesses at each statement of financial position date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the borrower or a group of borrowers is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganization and where observable data indicate that there is measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults.

Financial assets at amortized cost For financial assets at amortized cost which includes HTM financial assets, Loans and receivables, Due from BSP, Interbank loans receivables SPURA and due from other banks, the Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of the estimated future cash flows (excluding future credit losses that have not been incurred). If the Group determines that no objective evidence of impairment exists for individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses for impairment. Those characteristics are relevant to the estimation of future cash flows for groups of such assets by being indicative of the debtors’ ability to pay all amounts due according to the contractual terms of the assets being evaluated. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are not included in a collective assessment for impairment.

Veterans Bank 2009 Annual Report

23

The carrying amount of the asset is reduced through use of an allowance account and the amount of loss is charged to the statement of income. Interest income continues to be recognized based on the original effective interest rate of the asset. Loans, together with the associated allowance accounts, are written off when there is no realistic prospect of future recovery and all collateral has been realized. If, in a subsequent year, the amount of the estimated impairment loss decreases because of an event occurring after the impairment was recognized, the previously recognized impairment loss is credited to ‘Provision for credit and impairment losses’ in the statement of income and the allowance account is reduced. If a future write-off is later recovered, any amounts formerly charged are credited to the ‘Provision for credit and impairment losses’ in the statement of income.

The estimated future cash flows are discounted at the financial asset’s original effective interest rate. If a loan has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate, adjusted for the original credit risk premium. The calculation of the present value of the estimated future cash flows of a collateralized financial asset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable.

For the purpose of a collective evaluation of impairment, financial assets are grouped on the basis of such credit risk characteristics as industry, collateral type, past-due status and term. Future cash flows in a group of financial assets that are collectively evaluated for impairment are estimated on the basis of historical loss experience for assets with credit risk characteristics similar to those in the Parent Company. Historical loss experience is adjusted on the basis of current observable data to reflect the effects of current conditions that did not affect the period on which the historical loss experience is based and to remove the effects of conditions in the historical period that do not exist currently. Estimates of changes in future cash flows reflect, and are directionally consistent with changes in related observable data from period to period (such changes in property prices, payment status, or other factors that are indicative of incurred losses in the Bank and their magnitude). The methodology and assumptions used for estimating future cash flows are reviewed regularly by the Parent Company to reduce any differences between loss estimates and actual loss experience.

AFS Financial AssetsFor AFS financial assets, the Group assesses at each statement of financial position date whether there is objective evidence that a financial asset or group of financial assets is impaired.

In case of equity investments classified as AFS financial assets, this would include a significant or prolonged decline in the fair value of the investments below its cost. Where there is evidence of impairment, the cumulative loss measured as the difference between the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognized in the statement of income is removed from statement of comprehensive income and recognized in the statement of income. Impairment losses on equity investments are not reversed through the statement of income. Increases in fair value after impairment are recognized as other comprehensive income in the statement of comprehensive income.

In the case of debt instruments classified as AFS financial assets, impairment is assessed based on the same criteria as financial assets carried at amortized cost. Future interest income is based on the reduced amount an is accrued on the rate of interest used to discount future cash flows for the purpose of measuring impairment loss. Such accrual is recorded as part of ‘interest income’ in the statement of income. If, in subsequent year, the fair value of a debt instrument increased and the increase can be objectively related to an event occurring after the impairment loss was recognized in the statement of income, the impairment loss is reversed through the statement of income.

Restructured loansWhere possible, the Group seeks to restructure loans rather than to take possession of collateral. This may involve extending the payment arrangements and the agreement of new loan conditions. Once the terms have been renegotiated, the loan is no longer considered past due. Management continuously reviews restructured loans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subject to an individual or collective impairment assessment, calculated using the loan’s original EIR. The difference between the recorded value of the original loan and the present value of the restructured cash flows, discounted at the original EIR, is recognized in ‘Provisions for impairment and credit losses’ in the statement of income.

Loss on sale of non-performing asset (NPA) to a special purpose vehicle (SPV) companyLoss on sale of NPA to an SPV company on a without recourse basis is deferred over a ten-year period in accordance with

24

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

regulatory accounting policies prescribed by the Bangko Sentral ng Pilipinas for banks and financial institutions availing of the provisions of RA No. 9182, the Special Purpose Vehicle Act of 2002.

Offsetting Financial InstrumentsFinancial assets and financial liabilities are offset and the net amount reported in the statement of financial position if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. This is not generally the case with master netting agreements, and therefore, the related assets and liabilities are presented gross in the statement of financial position.

Revenue RecognitionRevenue is recognized to the extent that it is probable that economic benefits will flow to the Group and the revenue can be reliably measured. The following specific recognition criteria must also be met before revenue is recognized:

Interest incomeFor all financial instruments measured at amortized cost and interest bearing financial instruments classified as AFS and financial assets, interest income is recorded at the EIR, which is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or a shorter period, where appropriate, to the net carrying amount of the financial asset or financial liability. The calculation takes into account all contractual terms of the financial instrument, includes any fees or incremental costs that are directly attributable to the instrument and are an integral part of the EIR, but not future credit losses. The adjusted carrying amount is calculated based on the original EIR. The change in carrying amount is recorded as ‘Interest income’.

Once the recorded value of a financial asset or group of similar financial assets has been reduced due to an impairment loss, interest income continues to be recognized using the original EIR applied to the new carrying amount.

Service fees and commission incomeLoan commitment fees are recognized as earned over the terms of the credit lines granted to each borrower. Loan syndication fees are recognized upon completion of all syndication activities and where the Group does not have further obligations to perform under the syndication agreement.

Service charges and penalties are recognized only upon collection or accrued where there is a reasonable degree of certainty as to their collectibility.

Rental incomeRental income arising on investment properties is accounted for on a straight-line basis over the lease terms on ongoing leases.

Dividend incomeDividend income is recognized when the Group’s right to receive payment is established.

Trading gains (losses) - netResults arising from trading activities including all gains and losses from changes in fair value for financial assets and financial liabilities held for trading and gains and losses from disposal of financial assets held for trading and AFS financial assets.

Other incomeIncome from sale of services is recognized upon rendition of the service. Income from sale of properties is recognized upon completion of the earning process and the collectibility of the sales price is reasonably assured.

Cash and Cash EquivalentsFor purposes of reporting cash flows, cash and cash equivalents include cash and other cash items, amounts due from BSP and other banks, and interbank loans receivable with original maturities of three months or less from dates of placements and that are subject to insignificant risk of changes in value.

Investments in Subsidiaries and AssociateInvestment in subsidiariesSubsidiaries are all entities over which the Group has the power to govern the financial and operating policies, which generally accompanies a shareholding of more than one half of the voting rights. The existence and effect of potential

Veterans Bank 2009 Annual Report

25

voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity.

Investments in subsidiaries are carried at cost, less impairment in value, in the separate or parent company financial statements (see accounting policy on Basis of Consolidation).

Investment in an AssociateAssociates are entities which the Group has significant influence but not control, generally accompanying a shareholding of between 20% and 50% of the voting rights. In the consolidated financial statements, investment in associates is accounted for under the equity method of accounting. Under the equity method, the investment in the associate is carried in the statement of financial position at cost plus post acquisition changes in the Group’s share of net assets of the associate. The consolidated statement of income reflects the share of the results of operations of the associate.

The investment in an associate is in the Parent Company’s financial statement is carried at cost less accumulated impairment, if any.

Bank Premises, Furniture, Fixtures and EquipmentLand is stated at cost less any impairment in value and depreciable properties including buildings, leasehold improvements, and furniture, fixtures and equipment are stated at cost less accumulated depreciation and amortization, and any impairment in value. Such cost includes the cost of replacing part of the plant and equipment when that cost is incurred, if the recognition criteria are met but excludes repairs and maintenance costs.

Depreciation is calculated on the straight-line method over the estimated useful life of the depreciable assets.

The estimated useful lives of the property and equipment follow:

Buildings 20 yearsFurniture, fixtures and equipment 5 yearsLeasehold improvements 5 years or lease term, whichever is shorter

The depreciation and amortization method and useful life are reviewed at least at each reporting date to ensure that the method and period of depreciation and amortization are consistent with the expected pattern of economic benefits from items of property and equipment.

An item of property and equipment is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of income in the year the asset is derecognized.

Investment PropertiesInvestment properties are measured initially at cost, including transaction costs. An investment property acquired through an exchange transaction is measured at fair value of the asset acquired unless the fair value of such an asset cannot be measured in which case the investment property acquired is measured at the carrying amount of asset given up. Foreclosed properties are classified under ‘Investment properties’ upon; (a) entry of judgment in case of juridical foreclosure; (b) execution of the Sheriff’s Certificate of sale in case of extra-judicial foreclosure; or (c) notarization of the Deed of Dacion in case of dation in payment (dacion en pago).

Subsequent to initial recognition, depreciable investment properties are carried at cost less accumulated depreciation and any impairment in value.

Investment properties are derecognized when they have either been disposed of or when the investment property is permanently withdrawn from use and no future benefit is expected from its disposal. Any gains or losses on the retirement or disposal of an investment property are recognized in the statement of income in ‘Gain (Loss) on sale of acquired assets’ in the year of retirement or disposal.

Expenditures incurred after the investment properties have been put into operations, such as repairs and maintenance costs, are normally charged against current operations in the period in which the costs are incurred.

26

Philippine Veterans Bank And SubsidiariesNotes to Financial Statements

Depreciation is calculated for buildings and improvement on a straight-line basis over the estimated useful life of 10 years from the time of acquisition.

Transfers are made to investment properties when, and only when, there is a change in use evidenced by ending of owner occupation, commencement of an operating lease to another party or ending of construction or development. Transfers are made from investment properties when, and only when, there is a change in use evidenced by commencement of owner occupation or commencement of development with a view to sale.

Computer Software CostsSoftware costs are capitalized on the basis of the cost incurred to acquire and bring to use the specific software. These costs, included in ‘Other assets’, are amortized over five years on a straight-line basis.

Costs associated with maintaining the computer software programs are recognized as expense when incurred.